Citigroup Australia and New Zealand Investment Conference · Citigroup Australia and New Zealand...

16

Citigroup Australia and New Zealand Investment Conference March 2004 David Clarke Chief Executive Officer BT Financial Group

-

Upload

hoangthien -

Category

Documents

-

view

217 -

download

1

Transcript of Citigroup Australia and New Zealand Investment Conference · Citigroup Australia and New Zealand...

Citigroup Australia and New Zealand Investment Conference

March 2004

David Clarke Chief Executive Officer BT Financial Group

Citigroup Aust & NZ Investment Conference – Mar 20042

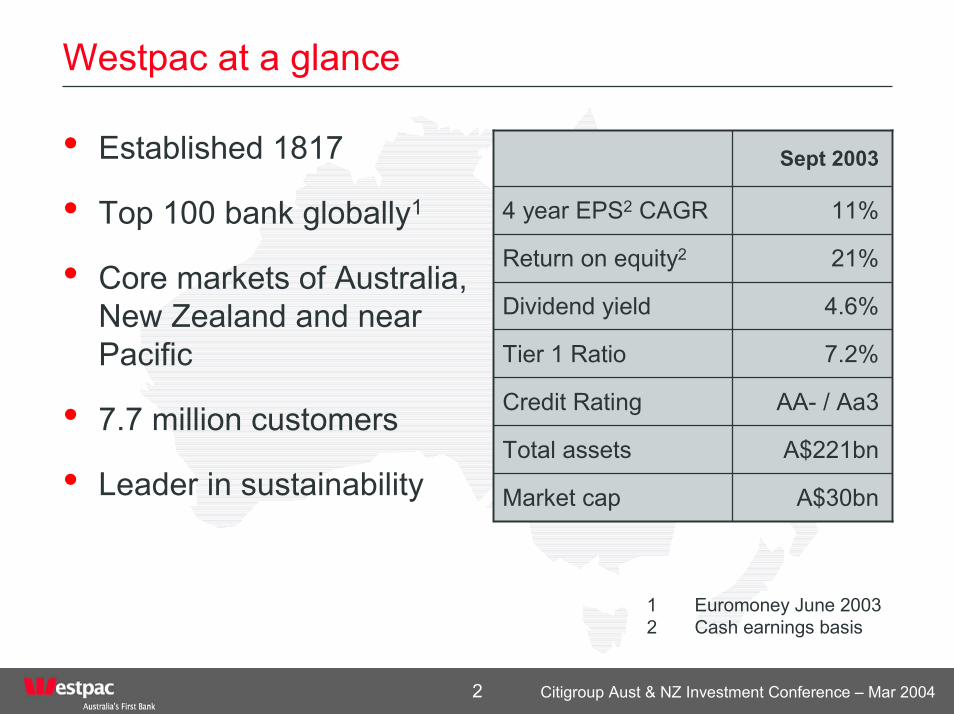

Westpac at a glance

• Established 1817

• Top 100 bank globally1

• Core markets of Australia, New Zealand and near Pacific

• 7.7 million customers

• Leader in sustainabilityA$221bnTotal assets

AA- / Aa3Credit Rating

7.2%Tier 1 Ratio

A$30bnMarket cap

4.6%Dividend yield

21%Return on equity2

11%4 year EPS2 CAGR

Sept 2003

1 Euromoney June 20032 Cash earnings basis

Citigroup Aust & NZ Investment Conference – Mar 20043

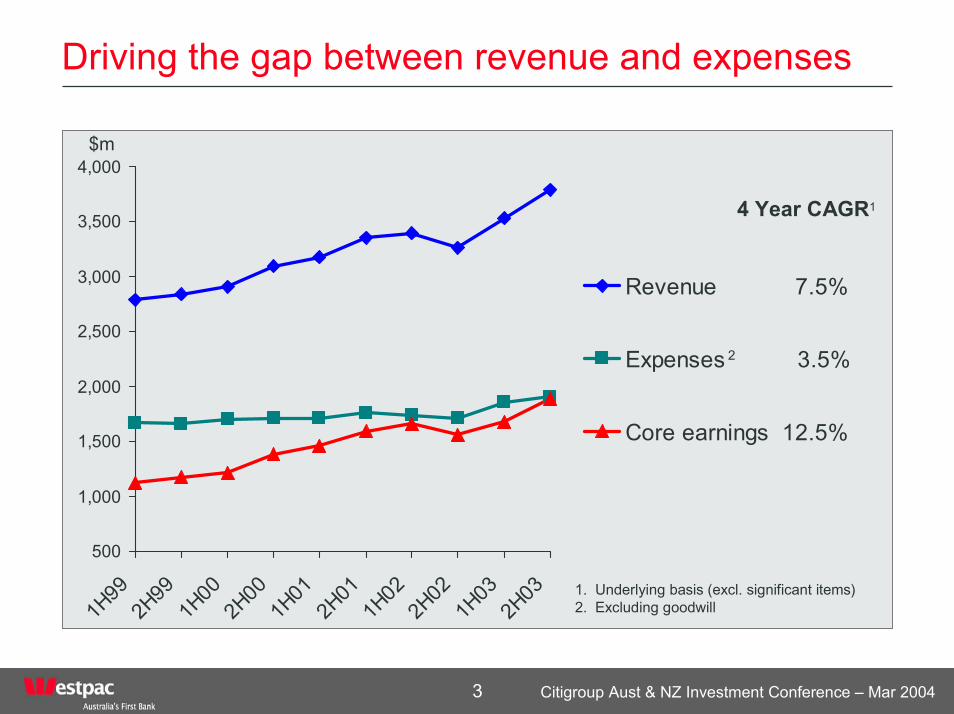

Driving the gap between revenue and expenses

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1H99

2H99

1H00

2H00

1H01

2H01

1H02

2H02

1H03

2H03

Revenue 7.5%

Expenses 3.5%

Core earnings 12.5%

$m

1. Underlying basis (excl. significant items)2. Excluding goodwill

4 Year CAGR1

2

Citigroup Aust & NZ Investment Conference – Mar 20044

Points of differentiation

• Strategy- Focused on core markets of Australia, New Zealand and near Pacific

- Customer centric organisational structure

- Balanced wealth management position

• Customer franchise- Large customer base skewed towards higher value segments

• Low risk- Continued improvement in asset quality, sound provisioning coverage

- Strong capital position

• Leader in sustainability- Corporate governance and sustainability ethic embedded in the organisation

- Leading bank globally in the Dow Jones Sustainability index, two years running

Citigroup Aust & NZ Investment Conference – Mar 20045

BT Financial Group

• Investment consistent with the size of the wealth management opportunity

• Modern wealth management operation- Funds management- Life insurance and risk- Wrap and corporate

superannuation- Margin lending- Broking

• Only large bank with a major Wrap capability

$190mCash earnings

$251mIn force premiums

$13bnAssets under admin

$43bnFunds under mgt

Sept 2003

Funds Mgt61%

Life Insurance &

Risk35%

Other4%

Composition of cash earnings 2003

Citigroup Aust & NZ Investment Conference – Mar 20046

BT – our competitive position

7

-7.2122.6Institutional310.6310.7Broking

7.759.2Retail

N/a9.3214.4Margin lending310.676.7Life and risk3*15.1*311.1Wrap and master trust311.456.0Corporate super

RankMarket

share (%)RankMarket

share (%)Product

Share of new business

Current market share

* Impact on market share and rank due to large transfer of administration of AMP Investment Solutions to ASGARD in Dec 2003

Sources: Retail& Wrap & M’trust - ASSIRT February 2004 (as at Dec 2003)

- New Business – September 2003 – ASSIRT Market share report September 2003Corporate super - Dexx&r Employer Super League Table September 2003Life and risk - Dexx&r Life analysis, Quarterly Statistics ending 30 September 2003Margin lending - BT loan book verses RBA industry total – 31 December 2003Broking - ASX market analysis (January) 9 Feb 2004Institutional - Institutional Rainmaker Mandate Analysis 2003 – 04 (does not include externally managed FUM)

Citigroup Aust & NZ Investment Conference – Mar 20047

Meeting the challenges

• Integration

• Investment management performance

• Retail outflows

• Leveraging distribution

• Maintain momentum in core businesses

Citigroup Aust & NZ Investment Conference – Mar 20048

Integration – nearing completion

• Insulated core business from integration task

• Dedicated project management resource

• Resolved key people, roles and location issues quickly

• Synergies ahead of plan – over 85% of 2004 synergies locked-in

Integration progress

Jul-0

2

Oct

-02

Jan-

03

May

-03

Aug-

03

Nov

-03

Mar

-04

Jun-

04

Sep-

04

Dec

-04

People & Location

Systems

Customer Contact

Investment Management

Registry consolidation & selected back office insourcing

Customer MIS

Complete

In progress

Citigroup Aust & NZ Investment Conference – Mar 20049

Fund performance and outflows

• New team in place quickly

• Strict adherence to investment management disciplines with a focus on risk

• Built transparency and accountability into process

• Active communication with research houses

Citigroup Aust & NZ Investment Conference – Mar 200410

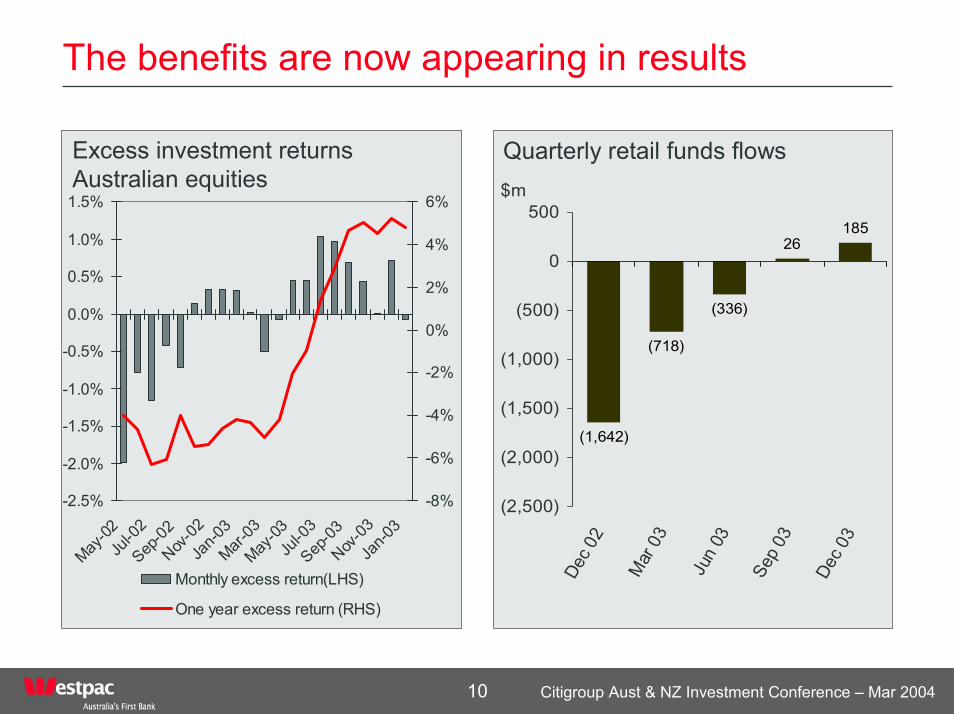

The benefits are now appearing in results

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

May-02

Jul-0

2Sep

-02Nov

-02Ja

n-03

Mar-03

May-03

Jul-0

3Sep

-03Nov

-03Ja

n-03

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Monthly excess return(LHS)

One year excess return (RHS)

Excess investment returns Australian equities

(1,642)

(718)

(336)

26185

(2,500)

(2,000)

(1,500)

(1,000)

(500)

0

500

Dec 0

2

Mar

03

Jun

03

Sep 0

3

Dec 0

3

$m

Quarterly retail funds flows

Citigroup Aust & NZ Investment Conference – Mar 200411

Leveraging the Westpac customer base

• Sub-optimal cross sell

• Under resourced internal financial planner and advice (FP&A) network

- Internal review underway

• Corporate super already achieving significant wins

Citigroup Aust & NZ Investment Conference – Mar 200412

Maintained focus on core businesses

• Integration has not distracted broader Westpac group

• Momentum in funds under administration continues

• Life and risk business growing well above existing share

0

1

2

3

4

5

6

7

8

9

10

11

Mar-98

Dec-98

Sep-99

Jun-0

0Mar-

01Dec-0

1Sep

-02 A

pr -03

Dec-03

Wrap funds under administration$bn

Citigroup Aust & NZ Investment Conference – Mar 200413

The strategy going forward

• Complete integration

• Maintain investment management disciplines

• Increase focus on customer responsiveness

• Fully leverage the Westpac group planners

Citigroup Aust & NZ Investment Conference – Mar 200414

Credit growth

-8

-4

0

4

8

12

16

20

24

Jan-90 Jan-92 Jan-94 Jan-96 Jan-98 Jan-00 Jan-02 Jan-04

%

-8

-4

0

4

8

12

16

20

24

Housing Business Total Total period average

Forecasts

Australian Credit Growth

Source: RBA

Citigroup Aust & NZ Investment Conference – Mar 200415

Westpac’s on track

• BT Financial Group- Business in excellent shape - Integration on track, with higher synergies - Tapping power of the Westpac customer base

• Economic environment remains favourable

• Housing market beginning to soften

• Outlook for Westpac remains positive

Citigroup Aust & NZ Investment Conference – Mar 200416

Disclaimer

The material contained in this presentation is intended to be general background information on Westpac Banking Corporation and its activities as at 9 March 2004.

The information is supplied in summary form and is therefore not necessarily complete. Also, it is not intended that it be relied upon as advice to investors or potential investors, who should consider seeking independent professional advice depending upon their specific investment objectives, financial situation or particular needs.