CISDM/UMASS-Amherst 1 THE PRESENTATION IS BASED ON ...

36

THE PRESENTATION IS BASED ON INFORMATION OBTAINED FROM SOURCES THAT CISDM CONSIDERS TO BE RELIABLE; HOWEVER, CISDM MAKES NO REPRESENTATION AS TO, AND ACCEPTS NO RESPONSIBILITY OR LIABILITY FOR, THE ACCURACY OR COMPLETENESS OF THE INFORMATION. Derivative Use In a Global Market: w We Got Here and Where Are We Goin Thomas Schneeweis Director/CISDM t Seoul International Derivatives Securities Confer August 27, 2003

-

Upload

khanyasmin -

Category

Documents

-

view

640 -

download

1

description

Transcript of CISDM/UMASS-Amherst 1 THE PRESENTATION IS BASED ON ...

CISDM/UMASS-Amherst 1

THE PRESENTATION IS BASED ON INFORMATION OBTAINED FROM SOURCES THAT CISDM CONSIDERS TO BE RELIABLE; HOWEVER, CISDM MAKES NO REPRESENTATION AS TO, AND ACCEPTS NO RESPONSIBILITY OR LIABILITY FOR, THE ACCURACY OR COMPLETENESS OF THE INFORMATION.

Derivative Use In a Global Market:How We Got Here and Where Are We Going?

Thomas SchneeweisDirector/CISDM

First Seoul International Derivatives Securities Conference

August 27, 2003

CISDM/UMASS-Amherst 2

Professor Thomas Schneeweis is Michael and Cheryl Philipp Professor of Finance at the School of Management at the University of Massachusetts in Amherst, Massachusetts, Founding Director of the Center for International Securities and Derivatives Markets at the School of Management (CISDM) and President of Schneeweis Partners, LLC, which specializes in the areas of multi-advisor fund creation, asset allocation, and risk management services especially in the area of alternative investments. He is the Founding Editor of the quarterly Institutional Investor publication, The Journal of Alternative Investments, is on the Board of the Managed Funds and is US Council representative for the Alternative Investment Management Association (AIMA). He is also a Founding Director of the Chartered Alternative Investment Analyst Association (CAIA), the global nonprofit educational venture sponsored by CISDM and AIMA that offers the CAIA designation. He has published widely in academic and practitioner journals in the areas of traditional and alternative investments, has been quoted in most major financial publications, and has provided commentary on various US, Europe, and Asian financial news programs.

Speaker Background

CISDM/UMASS-Amherst 3

What is a Derivative? Main Entry: 1de·riv·a·tive

Pronunciation: di-'ri-v&-tivFunction: nounDate: 15th century1 : a word formed by derivation2 : something derived3 : the limit of the ratio of the change in a function to the corresponding change in its independent variable as the latter change approaches zero4 a : a chemical substance related structurally to another substance and theoretically derivable from it b : a substance that can be made from another substance

Source: Merriam Webster On-line

CISDM/UMASS-Amherst 4

What is a Derivative?

Main Entry: derivativeFunction: adjectiveDate: circa 15301 : formed by derivation2 : made up of or marked by derived elements3 : lacking originality : BANAL- de·riv·a·tive·ly adverb- de·riv·a·tive·ness noun

Source: Merriam Webster On-line

CISDM/UMASS-Amherst 5

What is a Derivative?

The term derivative instrument came into commercial use only recently. First legal use of the term is found in 1982 New York Federal Court Case of Am. Stock Exch. Versus Commodity Futures Trading Commission:

“When exercised, options on physicals lead to the delivery of the physical commodity itself; that they are ‘first derivative’ instruments but one step removed from the underlying commodity. Options on futures are ‘second derivative’ instruments which give rise only to delivery of a futures contract, a contractual undertaking which can be transferred to third parties to buy and sell a fixed account and grade of a certain commodity on some specified date...”

CISDM/UMASS-Amherst 6

Academic Research Existence of exchange traded and over the counter

financial and non-financial products have enabled corporations to reduce risk, increase production and raise shareholder value

Derivatives have enabled financial firms to provide a wider array of products at lower costs and at less risk to themselves.

Exchange traded and OTC derivatives markets have offered countries the ability to:

Modernize their financial markets thereby improving the risk management capacity of all of its domestic partners

Compete on a broader scale with competing financial and corporate enterprises.

CISDM/UMASS-Amherst 7

Academic Research

Research on the use of derivative products in asset management as well as in corporate and financial risk management is an evolving area.

New theories come into existence which better explain risk and return relationships

Research is dynamic to address changes in regulation.

Trading technology changes in the underlying markets in which assets trade and in which corporate and financial firms operate. New technologies such as off exchange and computer traded markets contrast to traditional floor traded markets.

CISDM/UMASS-Amherst 8

Types of Derivatives

Credit DerivativesCredit spread forwardsCredit spread optionsCredit swaps (credit event swaps; default swaps)

Price DerivativesCommodity derivatives (e.g., futures or options in gold or silver)Financial derivatives

CISDM/UMASS-Amherst 9

Types of Financial DerivativesForwards – Foreign exchange forwards

Forward rate agreements (FRAs)

Futures – Currency futures (est. 1972)Interest rate futures (est. 1975)Stock index futures (est. 1982)Single stock futures (est. 2002)

Options – Options on physicals (stock, currency, interest, etc.)

Options on futures (currency or interest futures) Options on swaps (swaptions)

Swaps – Currency or interest rate swapsAssets or commodity swaps

CISDM/UMASS-Amherst 10

Types of Interest Rate Swaps Fixed to floating rate swap (coupon swap) Floating to floating rate swap (basis swap) Yield curve swap Zero-coupon swap Amortizing vs. non-amortizing (bullet) swap Accreting swap Forward swap Non-LIBOR swap Par value swap Off-market (non-par) swap Extendable swap

CISDM/UMASS-Amherst 11

Size of the Global Derivatives Market(Notional Principal Amount in $ billions)

(as of end-2002)OTC Exchanges Total

Currency 18,075 74 18,149 Interest rate 89,995 21,719 111,714Equity 2,214 2,089 4,303Others 17,280 NA 17,280

Total 127,564 23,882 151,446

Source: Bank for International Settlements

CISDM/UMASS-Amherst 12

Global Exchange-Traded Derivatives(Notional Principal Amount in $ billions)

(as of December 2002)

Currency Interest Equity Total

Futures 47.3 9,958.5 334.5 10,340.4Options 26.6 11,759.8 1,753.8 13,540.1

Total 73.9 21,718.3 2,088.3 23,880.5

Source: Bank for International Settlements

CISDM/UMASS-Amherst 13

Why the Concern Over Derivatives?Delayed Understanding:

The delay in both the investor’s understanding and the market’s awareness of new research and market relationships often results in a delay in the appreciation of these changes by investors, corporate officials, and government regulators.

Existence of Myths:Myths develop around how new financial products operate, as well as the their impact on financial markets, both domestically and globally.

In short, as markets change so do myths, with some myths changing more slowly than others.

CISDM/UMASS-Amherst 14

Why the Concern Over Derivatives and Changes in Financial Markets? Causes of Financial Change:

economic need technological change regulatory or governmental direction or lack thereof

It is our ability to work within this dynamic that allows us to constantly offer competitive products.

This constant tradeoff between the comfort of constancy and the necessity for change lies at the heart of this dynamic, which drives the creation of new financial products.

CISDM/UMASS-Amherst 15

Myths in the Use of Derivatives Derivatives are Complex New Instruments

Derivatives are Purely Speculative

Derivatives are Not Part of the Productive Process

The Risks Associated with Derivatives are New and Unknown

Derivatives Link Participants Thereby Increasing Systemic Risks

Derivatives Help Form Risky New Forms of Investment, Such as Hedge Funds

CISDM/UMASS-Amherst 16

Use of Derivatives through History

Mesopotamia (3000 BC)

Greece (600 BC)

Japan (1600’s)

US (Commodity - 1850’s)

US (Financial - 1970’s)

World (1990’s)

CISDM/UMASS-Amherst 17

Modern Growth in Derivatives

Supply and demand issues lead to the rise and fall of many similar derivatives products during the past 100 years.

Currency derivatives came into existence out of the failure of the U.S. to monitor its own currency.

Individual options grew in the early 1970’s as risk management tools, partly in response to the collapse of the stock markets of the late 1960’s and the linkage of simple models of derivatives pricing and the advent of held computers.

Interest rate futures and equities indices took off after the ERISA laws created the pension fund asset base, necessitating the management of the risks involved in managing those assets. US government also helped by creating a pool of government securities with ‘billion dollars a year deficits’.

CISDM/UMASS-Amherst 18

Modern Growth in Derivatives Prior to the 1990s, the U.S., the government was central in

the risk management process, as both a regulator and a risk provider, but the banking collapse of the early 1990s led to the realization of the government’s limitations as a risk provider.

With bank risk of increasing concern, new attempts were made to link with others to form a broader risk management form, such as the Basel Accords.

The change in technology, market needs, and regulation led to the privatization of the trading floor and encouraged banks to leave certain risk management to others.

Globalization lead to the multiplication of these opportunities around the world.

Change was driving the creation of new derivative products which were in themselves creating the opportunity for change.

CISDM/UMASS-Amherst 19

Myths of Derivative Based Strategies: The Case of Hedge Funds Hedge Funds Are New Financial Products Based on

Derivatives

Hedge Funds Use Derivatives For Speculation

Hedge Funds Use Derivatives for Leverage and Leverage is Bad

Hedge Funds Offer Little Economic Value and No Benefit to the Investor

Derivatives Have Little Use in Hedge Fund Risk Control

CISDM/UMASS-Amherst 20

Hedge funds have existed since the 1940s, but it was not until the 1990s that they experienced rapid growth.

$38.91

$571.71

$536.06

$456.43

$374.77$367.56

$256.72

$185.75$167.36$167.79

$95.72$58.37

$487.58

$0

$100

$200

$300

$400

$500

$600

$700

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 Q2 2002

Ass

ets

(in

$bill

ions

)

Hedge Funds: An Investment Product Of The 1990s

CISDM/UMASS-Amherst 21

Causes of Hedge Fund Growth:

The increase in the number of new financial vehicles.

The “privatization” of the trading floor or investment

bank

A change in technology, permitting sophisticated investment strategies to be designed and implemented without the infrastructure of a large investment house

Hedge Funds: An Investment Product Of The 1990s

CISDM/UMASS-Amherst 22

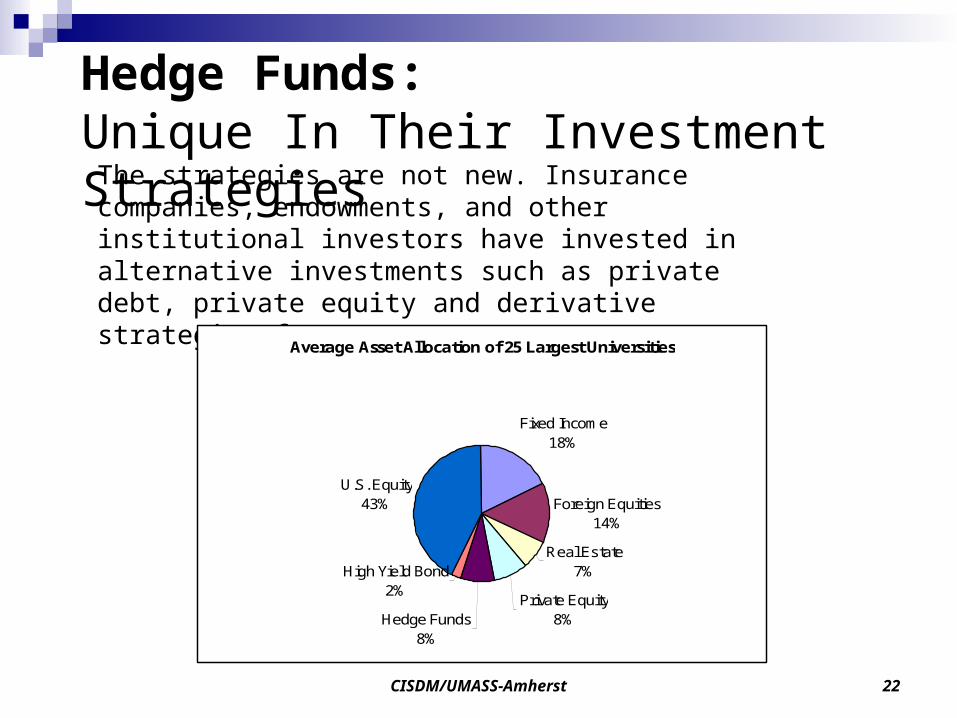

The strategies are not new. Insurance companies, endowments, and other institutional investors have invested in alternative investments such as private debt, private equity and derivative strategies for years.

Average Asset Allocation of 25 Largest Universities

Fixed Income18%

Foreign Equities14%

Real Estate7%

Private Equity8%Hedge Funds

8%

High Yield Bond2%

U.S. Equity43%

Hedge Funds: Unique In Their Investment Strategies

CISDM/UMASS-Amherst 23

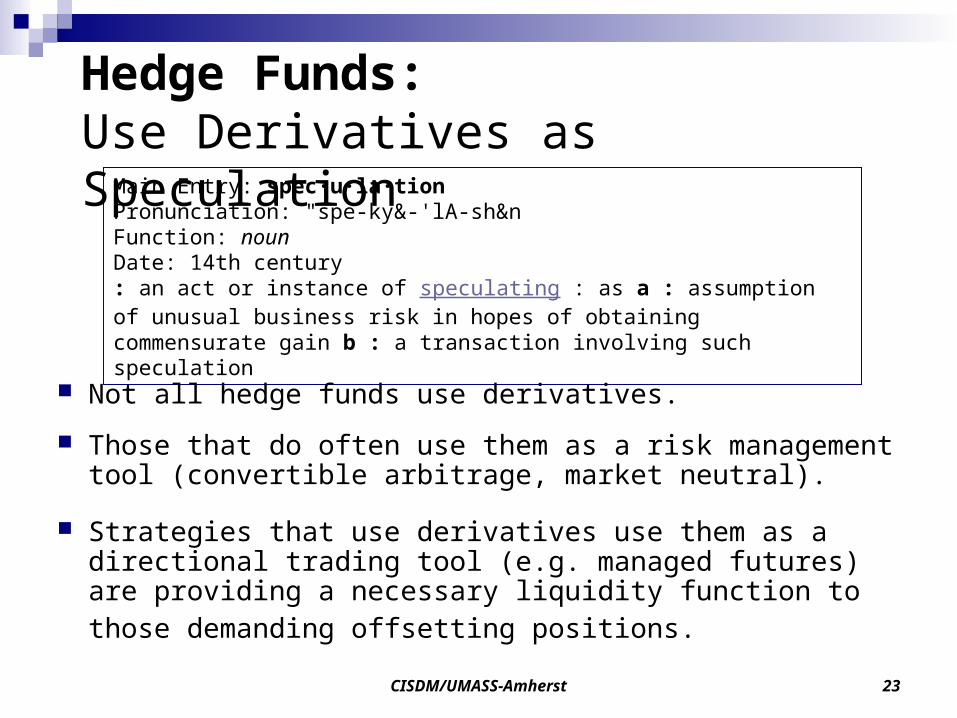

Main Entry: spec·u·la·tion Pronunciation: "spe-ky&-'lA-sh&nFunction: nounDate: 14th century: an act or instance of speculating : as a : assumption of unusual business risk in hopes of obtaining commensurate gain b : a transaction involving such speculation

Hedge Funds: Use Derivatives as Speculation

Not all hedge funds use derivatives.

Those that do often use them as a risk management tool (convertible arbitrage, market neutral).

Strategies that use derivatives use them as a directional trading tool (e.g. managed futures) are providing a necessary liquidity function to those demanding offsetting positions.

CISDM/UMASS-Amherst 24

Leverage itself is not something to be avoided. Banks are levered about 20 to 1 (about 5% of assets are

equity capital, 95% are loans and deposits).

Residential real estate is typically levered 5 to 1 (a 20% down payment is common, with 80% borrowed)

Corporations in risky businesses tend to be financed mostly with equity because of the unpredictability of the returns.

The more highly levered an instrument is, the more care one must take to insure that the payment flow is more predictable or large losses are possible.

Hedge Funds: All Use of Leverage is Bad

CISDM/UMASS-Amherst 25

Hedge Funds: Offer No Economic Value

Hedge funds invest in a wide variety of investment arenas, including private equity, private debt, merger and acquisitions, emerging markets.

Many worthwhile projects could not find the necessary financing without hedge funds.

Hedge funds offer liquidity to other investors in these assets, as the primary use of derivative products is to offer a mechanism for firms to reduce or manage their own risk.

CISDM/UMASS-Amherst 26

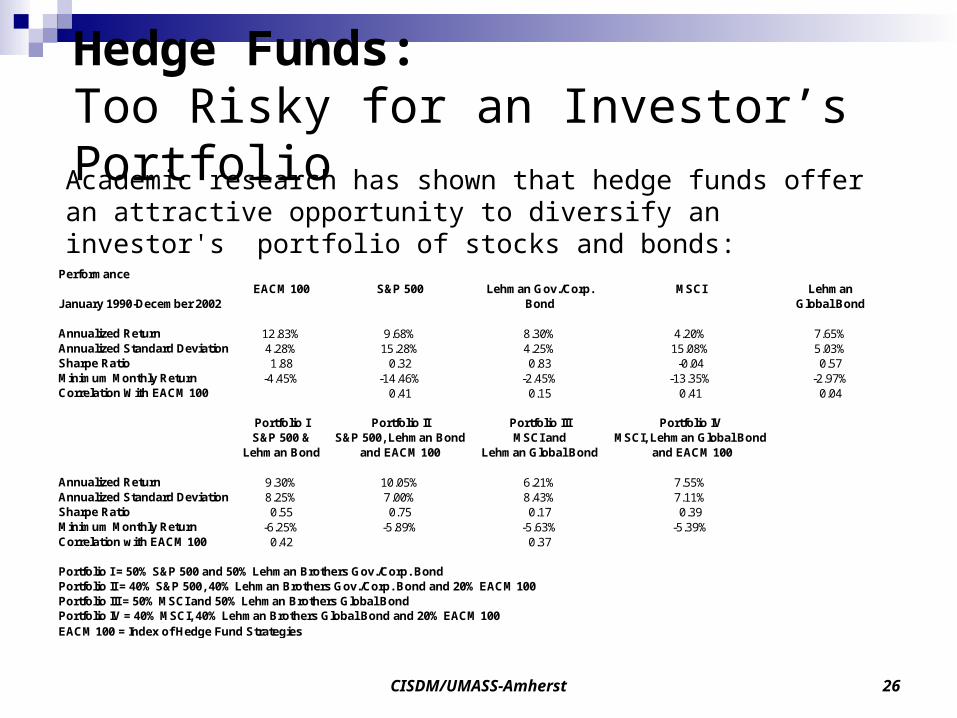

Academic research has shown that hedge funds offer an attractive opportunity to diversify an investor's portfolio of stocks and bonds:

PerformanceEACM 100 S&P 500 Lehman Gov./Corp. MSCI Lehman

January 1990-December 2002 Bond Global Bond

Annualized Return 12.83% 9.68% 8.30% 4.20% 7.65%Annualized Standard Deviation 4.28% 15.28% 4.25% 15.08% 5.03%Sharpe Ratio 1.88 0.32 0.83 -0.04 0.57Minimum Monthly Return -4.45% -14.46% -2.45% -13.35% -2.97%Correlation With EACM 100 0.41 0.15 0.41 0.04

Portfolio I Portfolio II Portfolio III Portfolio IVS&P 500 & S&P 500, Lehman Bond MSCI and MSCI, Lehman Global Bond

Lehman Bond and EACM 100 Lehman Global Bond and EACM 100

Annualized Return 9.30% 10.05% 6.21% 7.55%Annualized Standard Deviation 8.25% 7.00% 8.43% 7.11%Sharpe Ratio 0.55 0.75 0.17 0.39Minimum Monthly Return -6.25% -5.89% -5.63% -5.39%Correlation with EACM 100 0.42 0.37

Portfolio I = 50% S&P 500 and 50% Lehman Brothers Gov./Corp. BondPortfolio II = 40% S&P 500, 40% Lehman Brothers Gov./Corp. Bond and 20% EACM 100Portfolio III = 50% MSCI and 50% Lehman Brothers Global BondPortfolio IV = 40% MSCI, 40% Lehman Brothers Global Bond and 20% EACM 100EACM 100 = Index of Hedge Fund Strategies

Hedge Funds: Too Risky for an Investor’s Portfolio

CISDM/UMASS-Amherst 27

The risk and return attributes of hedge funds are determined solely by their investment strategy.

Some hedge funds invest primarily in long only cash instruments and employ little leverage, as the underlying asset itself has a high return to risk tradeoff.

Other hedge funds invest in low-risk strategies such as security arbitrage. These funds use leverage positions in order to offer a reasonable expectation of return.

The fact is that the typical hedge fund's returns have been less volatility by far than the typical stock or stock mutual fund.

Hedge Funds: Highly Levered, Risky Investments

CISDM/UMASS-Amherst 28

Market Oversight In A Derivatives World

It is hard to imagine but Enron is now over two years old and LTCM is five years in the past. I wonder if all the new seminars being conducted not only in the United States but overseas have taken the time to rethink just how fragile, financial markets and how easily the mighty fall.

Attempts to control current concerns may not be proper under the next market cycle. There are among us those who remember the glory days of managed futures and global macro, to be replaced by fixed income arbitrage and other market neutral strategies, only to fall to the new kid on the block, equity hedge and merger arbitrage, just in time for convertible arbitrage and distressed debt to make a comeback until just this month when increases in swap spreads sent those strategies tumbling.

CISDM/UMASS-Amherst 29

Market Oversight In A Derivatives WorldRecent SEC DiscussionsWhile one can put various spins on the SEC discussions, it was a wonderful back and forth on the relative worth of Government Order, Market Order, and Moral Order.

The government expressed the common concern that somehow, someway, someplace, there was someone doing something to somebody. It was the government’s duty to find those involved in this process and find ways to stop them.

The respondents, a collection of practitioners, academics, and investors, attempted to respond in various ways to the charges. The practitioner’s, as expected, brought up the specter of a Market Order, in which the actual trading strategies and the traders themselves were forced by the very environment that they trade in to provide an honest product, back by honest people, providing an honest services to honest investors.

CISDM/UMASS-Amherst 30

Market Oversight In A Derivatives WorldMultiple Perspectives Market order means different things to different participants in

the process:

Government Order Proponents were concerned that government order was required to ensure market order (e.g., systemic risk).

Market Order Proponents expressed concern that the government regulations that would necessitate a government based system might in fact lessen the probability of market order. Ultimately, increased government regulation might result in hedge funds’ demise and the demise of liquidity in the very markets that this government order is supposed to promote.

If government supervision is a good thing, how much of a good thing can the market withstand? Practitioners pointed out that when individuals are forced into goodness at an extreme cost they tend to run away or find a means to reduce that cost. If the government forces a moral order through government order, many hedge funds will simply move to those areas in which ‘religion’ is less costly or the sun is shining.

CISDM/UMASS-Amherst 31

Market Oversight In A Derivatives WorldMultiple Perspectives Any action by practitioners to waylay ‘government order’ was

seen by the high priests of that religion as a direct attack on their order. Both parties sought refuge in the arms of the investor.

Market Order Proponents pointed out that all investors deserve the right to make their own decisions and that the special privilege to invest in hedge funds should not be the right only of the wealthy.

Government Order Proponents responded that any religion (e.g. government order) has as its primary responsibility the requirement to protect its flock. In short, there is a higher authority than the market. In fact, the religion of government order would not even be necessary if the participants in the market simply had some level of personal ‘moral order’.

CISDM/UMASS-Amherst 32

Market Oversight In A Derivatives WorldA Multi-Pronged Solution

An Alternative Approach: Active board and senior management oversight of trading

activities

Establishment of an internal risk-management audit function that is independent of the trading function

Thorough and timely audits to identify internal control weaknesses

Risk-measurement and risk-management information systems that include stress tests, simulations, and contingency plans for adverse market movements.

As stand alone answers, technology, regulation, and open market solutions are inadequate.

CISDM/UMASS-Amherst 33

Derivatives and Derivative Based Products In The Future

Increasing technology, regulation and globalization has increased the pace of change and the need to manage it

Increasing competition has led to the necessity for individuals, firms, and countries to embrace the new means of asset management

Potential examples include weather, energy, fish futures, and regional futures exchanges

CISDM/UMASS-Amherst 34

There are a good many roads here," observed the shaggy man, turning slowly around, like a human windmill. "Seems to me a person could go 'most anywhere, from this place." --The Road to Oz (1909)

Illustration by John R. Neill from The Road to Oz, © 1909 L. Frank Baum.

CISDM/UMASS-Amherst 35

Conclusions

Derivatives and derivative-based products have become a common part of economic activity

New forms of derivatives are part of a constantly changing landscape, reflecting changes in economic needs, technology, and regulatory oversight

Conflict arises between market participants as they address the tradeoff between the desire by individuals and the market for constancy and the changes caused by markets dynamics

Determining how best to regulate and monitor those potential conflicts is necessary to achieve the benefits of these new financial products and markets

CISDM/UMASS-Amherst 36

Selected References

Schneeweis, Thomas and Joseph Pescatore eds. The Handbook of Alternative Investment Strategies: An Investor’s Guide. Institutional Investor, 1999.

Schneeweis, Thomas, George Martin, and Hossein Kasemi, “Understanding Hedge Fund Performance,” CISDM, 2003.

Schneeweis, Thomas, “Derivates Use in a Global Market,” CISDM, 2003.