CIP Template

12

Version 1.0 18 March 2009 Structure for a Comprehensive CIP

-

Upload

jon-barsanti-jr -

Category

Documents

-

view

4.417 -

download

2

description

A bare-bones approach to creating a CIP if your organization does not already have one.

Transcript of CIP Template

Version 1.0 18 March 2009

Structure for a Comprehensive CIP

1

CIP Good Practices Version 1.0 18 March 2009

Triangle J Council of Governments Development & Infrastructure Partnership

Capital Improvement Budgets are long-term fi-

nancial plans. The purpose of these plans is to fore-

cast capital improvement expenditures and meas-

ure their impacts on future budgets. These expendi-

tures are designed to enable counties and commu-

nities to provide equal or better service over an ex-

tended period of time. Capital Improvements tend

to be large ticket items that are multi-year invest-

ments. GASB34 defines capital assets “as tangible

and intangible assets used in operations with useful

lives longer than one reporting period and a mini-

mum cost based on approved capitalization levels.”

Capital Budgets may be based upon existing annual

budgets, or they may be used as templates to create

the Annual Budget, as well as the Comprehensive

Annual Financial Reports. The intent of this report

is to provide a basic template for organizations that

either do not currently produce a capital improve-

ments budget or would like to improve their budg-

eting process.

Organizations that do not currently have a CIP

need to evaluate producing the three financial re-

ports,(the comprehensive annual financial report,

the annual budget, and the CIP, ) in a standard

process. Data classifications from one report need

to be consistent with the data classifications in the

other two reports. The Development and Infrastruc-

ture Partnership has identified fourteen classifica-

tions for capital improvement programs. The ma-

jority of the CIPs reviewed have similar classifica-

tions.

The fourteen classifications identified by the Tri-

angle J Development and Infrastructure Partner-

ship are:

1. Schools

2. Transportation

3. Parks and Open space

4. Arts and Culture

5. Water

6. Wastewater

7. Stormwater

8. Solid Waste

9. Justice & Public Protection

10. IT & Communications

11. General Services

12. Housing

13. Health and Human Services

14. Other

When drafting a new CIP, organizations need to

begin building financial documents based upon

these fourteen classifications based on the depart-

ments* your organization currently has and:

Forecast capital spending for either five or ten

years; and

Predict future revenue streams for these capital

expenditures.

Long-range financial documents may not be able

to precisely reflect the future source of funds or

costs of a project. The purpose of identifying fund-

ing sources is to approximate future tax rates,

bonds, or reserve needed to complete the capital

improvements.

If programs are projected less than five years in

advance funding may be difficult to procure. If pro-

grams are projected out further than ten years costs

and revenues become, at best, educated guesses.

There are precedents for classifying funds for pro-

jects as unauthorized bonds or unfunded projects,

especially projects that are timed towards the far

end of the timetable. If revenue streams cannot be

identified, a separate unfunded CIP section needs to

be established. Projected costs of the capital im-

provements, including inflation, need to be clearly

quantified and qualified.

* Note: ‘Departments’ and ‘classifications’ will be

used interchangeably throughout this document.

(Continued on page 2)

2

CIP Good Practices Version 1.0 18 March 2009

Triangle J Council of Governments Development & Infrastructure Partnership

The reasons to standardize the creation of financial

reports are straightforward. Data from the Capital Im-

provement Program can be migrated into the Annual

Budget and then summarized in the subsequent year‟s

Comprehensive Annual Financial report. When data is

entered in a standardized manner, using standardized

project identifiers, reports may be updated without re-

inventing the process. Finally, a standardized product

is beneficial to the reader, especially those who may

read the same financial documents year in and year

out. There are instances where the name of a project, a

school or a park, may change during the period from

concept and design to finished project. Where names

of projects change a translation tables is necessary. The

unique project code should not change( e.g. PR2008-

12 for a Parks and Recreation Project added to the CIP

during the 2008 CIP Budget, one of 12 Parks and Rec-

reation Projects identified that year.)

Successful CIPs will reflect the mission and vision of

the organization. The mission is why the organization

exists. The vision is where the organization is heading.

Capital Improvement Programs can be seen as Goals

statements for the organization. Goals have time lines

and costs associated with them. The process of creat-

ing a vision or a mission statement is outside the scope

of this report.

The process of creating the CIP document can be as

simple as using Excel or one of a number of programs

designed for creating CIPs such as CIPAccess/CIPAce,

PlanIt!, CIPS, CIPvizion, orTeamBudget Capital.

When the initial template is designed in Excel or a

similar product:

1. Determine if the capital improvements are single-

year or multi-year projects.

2. Create a Template for the Fourteen Classifications,

with Funding Sources and Maintenance /

Development Costs (Steps 1 and 2, Page 3)

3. Create 14 pages, representing the 14 categories

(Step 3, page 4)

4.Detail the upfront capital costs

5. Project the maintenance and development costs

6. Allocate the staff costs, where appropriate.

7. Using the following template, identify the source(s)

of funds needed for each project/program item – not

all communities will have all options available:

General Funds

Reserve Funds

Approved Bonds (Bonds, 2/3 bonds, revenue

bonds, utility bonds.)

Certificates of Participation

Impact Fees

Special Funds (Powell Funds, Lottery Proceeds,

Grants)

Bonds – Unapproved

Funds – Unapproved

7. Create a summary page for each department,

totaling the revenue and expenses of the individual

projects. (Page 5, Step 4)

8. Link each cell from the project level to the next

level up in the document - the Department Level.

(e.g. Schools B2 ='School Project #1'!B2) Total Cost

for Lake Church Elementary 2009-09.

9. Link each Department Level to the Summary by

Category Page (eg. 14 Categories Schools B2 =

Schools!B16 ) Total for all school projects for 2008-

09.

10. Link each of the Funding Source Cells and the

Maintenance/Development Cost cells using the same

process.

11. Compile a summary page for the organization,

totaling the expenditures and the funding sources for

all departments, including those that operate outside

of the General Fund, an example being Utilities.

12. Enter the current tax base and projected tax bases

for subsequent years. Use your current tax rate to

(Continued on page 4)

3

CIP Good Practices Version 1.0 18 March 2009

Triangle J Council of Governments Development & Infrastructure Partnership

Step 1: Rename “Sheet1” to “14 Categories” by right-clicking on the “sheet1” tab at the bottom of the worksheet, selecting „rename‟ and

changing the text when the cursor goes to a bar on that tab.

Step 2: Recreate the table below with whichever items you require or will require in your CIPs:

4

CIP Good Practices Version 1.0 18 March 2009

Triangle J Council of Governments Development & Infrastructure Partnership

calculate projected revenue.

13. Calculate the amount of tax one penny would pro-

duce and calculate the tax rate impact for the individ-

ual projects.

14. Using the same process as used for the funding

sources, and project costs, reference the individual

penny rates and tax rate impacts forward to the cate-

gory/department summary page, and move that total

forward to the overall summary page.

Step 3: For each of the 14 items under “Category” in Step 2, create another worksheet/tab.

(Continued on page 7)

5

CIP Good Practices Version 1.0 18 March 2009

Triangle J Council of Governments Development & Infrastructure Partnership

Step 4: In each of these category worksheets, create the following table:

6

CIP Good Practices Version 1.0 18 March 2009

Triangle J Council of Governments Development & Infrastructure Partnership

Step 5: For each project you list in each category sheet, create a separate sheet with the following table:

7

CIP Good Practices Version 1.0 18 March 2009

Triangle J Council of Governments Development & Infrastructure Partnership

Data from each project is best if it flows through the

spreadsheets such that lines and columns on

successive pages are in complete alignment.

Special care must be taken when classifying

projects that may receive bond funds to ensure that

the expenditures do not commingle different

approved bond categories.

If the project(s) identified are long-term or

recurring investments other items must be identified

at the :

Reserve Balances

Reserve Contributions

Revenue Sources (Special Funds, Grants,

Fees, Special Sales tax, or Impact Fees, Bonds)

Capital Budgets or Capital Improvement plans need

to identify:

Property Values (and the date of the last

revaluation)

The current tax rate

The Penny Rate (one cent of property tax on

property values)

The collection rate

The image below (Figure 1) was found in the

Chatham County Budget for 2007-08. It provides a

quick snapshot of the Budget. A similar image could

be produced for a CIP.

Referencing the need for future funds or bonds as

unapproved, as previously noted, is potentially

problematic, unless a discussion of future bonds or

future revenue streams is broached.

Project pages are improved through the addition of

geographic locations of the project. If your

organization uses GIS, creating a shapefile or a

geodatabase of projects to track potential projects ,

data tables can be generated from the “dbf” files

associated with the layers. Fields that should be

Figure 1: Budget snapshot from Chatham County Budget

(Continued on page 8)

8

CIP Good Practices Version 1.0 18 March 2009

Triangle J Council of Governments Development & Infrastructure Partnership

included in the shapefiles or database layers are:

Project Identifier

Department

Name

Alias

Phase

Physical Location/Address

Type of Project

Date added to CIP

Year for Project to Occur/start

Year Completed

Funding Source(s)

Bond Package/Classification

Cost (Projected)

Cost (Actual)

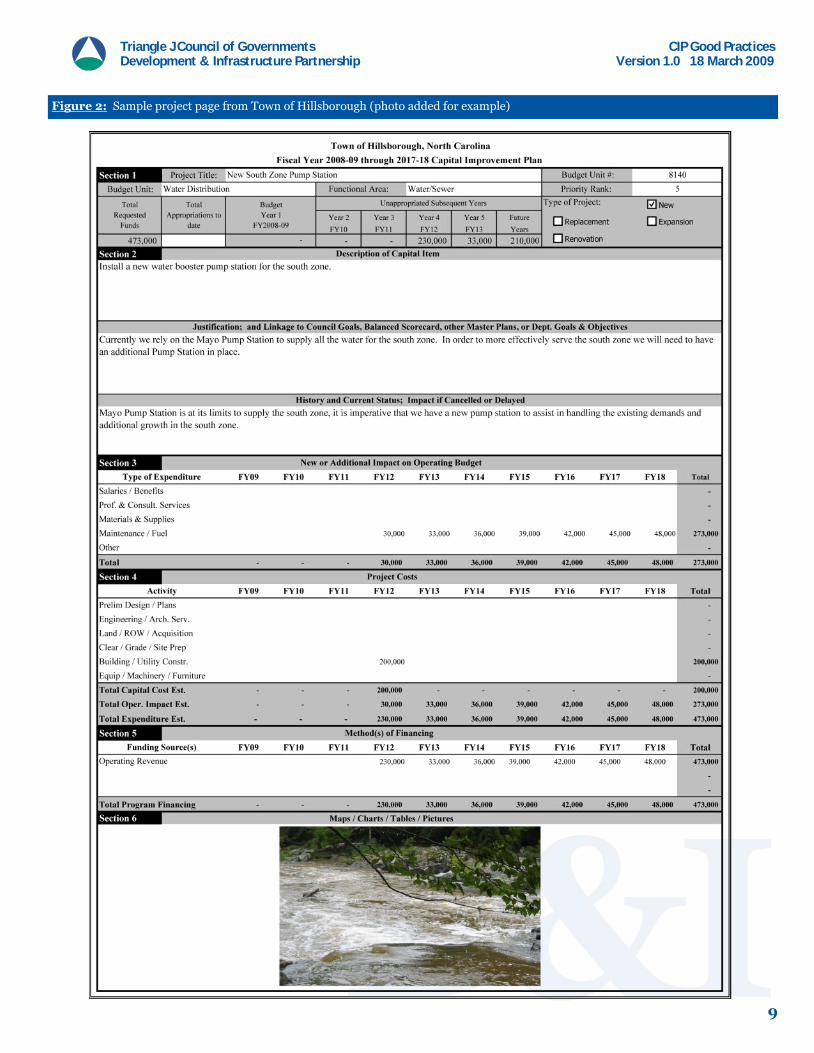

See the project page provided by the Town of Hills-

borough (Page 9, Figure 2).

SUMMARY

Capital Improvement Programs are long-range fiscal

planning documents that are connected to prolonged

physical improvements or capital intensive in nature.

The multi-year, multi-project nature of the CIP offers

flexibility in funding. CIPs, when standardized, can aid

in the development of Annual Budgets and Compre-

hensive Annual Financial Reports. CIPs can also aid in

the planning of future bond needs or project changes

in either future tax rates or service levels. Standardiza-

tion of the CIP process will be beneficial to the fiscal

and physical planning of an organization. The stan-

dardization of the CIP process can be done using finan-

cial workbook software such as Excel, or through any

number of CIP software programs. Classifying the data

according to the fourteen categories delineated by the

Development and Infrastructure partnership will aid

organizations that wish to make peer-to-peer compari-

sons or organizations that wish to streamline the finan-

cial planning process.

If your organization does not currently provide

wastewater, sewer, or water services at this time, for

example, it may not seem to be necessary to itemize

these classifications or departments. If your organiza-

tion is looking to add these services, or any of the other

eleven services, during the next five to ten years, then

it will be beneficial to consider these items within the

context of the current CIP and future CIPs.

9

CIP Good Practices Version 1.0 18 March 2009

Triangle J Council of Governments Development & Infrastructure Partnership

Figure 2: Sample project page from Town of Hillsborough (photo added for example)