Choosing a Prepaid Processor in an Evolving Market - … a Prepaid Processor in an Evolving Market:...

22

© 2008 Javelin Strategy & Research– All Rights Reserved Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs Conducted by Javelin Strategy & Research November 2008

Transcript of Choosing a Prepaid Processor in an Evolving Market - … a Prepaid Processor in an Evolving Market:...

© 2008 Javelin Strategy & Research– All Rights Reserved

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs

Conducted by Javelin Strategy & Research November 2008

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 2

Overview ................................................................................................................................................ 3

Executive Summary ................................................................................................................................ 4

What Will Characterize the Evolution of Prepaid? ................................................................................. 6

The Components of a Prepaid Processing Program ............................................................................... 9

Dispelling Myths About Prepaid Processors ........................................................................................ 14

Summary and Wrap up – Key Considerations for a Prepaid Processing Relationship .......................... 22

Table of Contents

As a leading independent provider of quantitative and qualitative research focused exclusively on financial services topics, Javelin uses rigorous statistical methodologies to conduct in‐depth primary research studies that pinpoint dynamic risks and opportunities.

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 3

Overview

Prepaid card issuance has undergone an explosion in recent years, and all indications are that this trend

will continue. Prepaid issuers—whether new to the marketplace or experiencing growth beyond the

capacity of their current processor—must carefully consider the role and the capabilities of that

processor to realize the full potential of their prepaid program.

The processor decision is integral to the success of the prepaid program. Currently many of the

questions that issuers should proactively pose go unasked, leaving the issuer in an untenable situation

within months of implementation. Prepaid issuers need to clarify all the questions that they should ask

prior to choosing a processor, and must perform a complete, proactive needs analysis for prepaid

processing services.

Many issuers have made mistakes in their early iterations of prepaid programs, selecting processors that

woefully neglect one aspect or another of the overall prepaid arena. This can include, but is not limited

to the following:

• Processors whose focus on one product leaves issuers unable expand.

• Processors who under‐deliver on promises of scalability and reliability, leaving issuers unable to

grow the program to the fullest potential, or

• Processors who cannot assist program managers on a consultative level, leaving all of the

innovation and development to the program manager themselves, and thus proving unable to

fully capitalize on trends in the prepaid marketplace.

Each of the above issues can leave a prepaid program in limbo, with the pain of migrating off a

processing platform worse than the status quo, regardless of how unacceptable the processing provider

and platform may be. The intent of this paper is to help

issuers avoid that pain and assist prepaid program managers

in gaining a deeper level of understanding of what they must

seek from their prepaid processor.

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 4

Executive Summary

Companies making important business decisions to enter and/or expand their prepaid card presence

must be prepared to make critical processing and operational decisions. This paper will help you ask the

tough questions to get the most out of relationships you have with processors and ensure full

optimization from any prepaid program you launch, manage and grow. Whether you have an

established prepaid issuance program, are looking to expand or potentially migrate to a new platform,

or are in the beginning stages of decision‐making regarding a prepaid platform, this information can

serve as further guidance.

Companies looking to enter the prepaid arena need to look at the holistic capabilities of processing

solutions, understanding the various components of an effective prepaid program operation and how

each component is implemented and managed. The first section of this paper is intended to provide an

overview of each component, and an understanding of how components fit into the larger picture for

prepaid processing platform choices.

Establishing a relationship with a processor and determining whether to outsource all or some program

operations components is a decision with multiple criteria. Issuers and program managers – those who

issue cards directly or indirectly through a 3rd party – should consider the following items as paramount

for the viability of a solid operation:

• Product breadth and evolution capabilities: Can the prepaid processor help expand beyond a

single product offering, providing the support and functionality needed for a wider array of

prepaid products?

• Components or client‐defined attributes of the program: Is the processor providing a point

solution or a holistic processing platform?

• Processing engine reliability: Will the system work when needed?

• Scalability of the processing system – can the processor grow as transaction volume and

corresponding support services needs grow?

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 5

Executive Summary

The experience of the processor is a key factor in this equation. Prepaid issuers and program managers

must determine the level of experience that the processor may have not only in transaction processing

itself, but also in managing everything from technology to exception management, to compliance, risk

and fraud management. What are the factors that make the processor superior, or inferior in these

facets?

And finally, the relationship management components of the prepaid processing choice cannot be

overlooked or de‐emphasized. The prepaid processor is the conduit for the issuer or program manager

to the trends and evolution of the prepaid arena. Success – or at the very least the degree of success

realized by an issuer – can be largely dependent on the prepaid processor’s ability to recognize trends

and work with the issuer to expand and manage the program.

Issuers and program managers must therefore analyze the client service and consultative capabilities of

the prepaid processor. How well does the processor understand the market? The trends? Client needs?

How well can the prepaid processor enable its clients to capitalize on these trends and truly drive growth

through the prepaid platform and product set?

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 6

What Will Characterize the Evolution of Prepaid?

As consumer needs evolve and technology drives innovation in the prepaid segment, processors must be

flexible and innovative enough to fully respond, but preferably drive product design, implementation

and performance for their prepaid issuer clients. In the future Prepaid will continue to require product

diversity and flexibility, but the rapid change also requires a business partner with know‐how, proven

experience, understanding of the marketplace, and a flexible platform with common value‐added tools,

such as fraud protection and information management solutions. This will allow for efficient

management of programs that grow as client needs grow. Providers of point solutions that focus on one

particular product or market are not well‐positioned to evolve as prepaid evolves. Issuers must remain

vigilant as to the capabilities of their processors to consistently and continuously meet their needs. They

must continue to question, inform and in some cases drive their processing partner to new levels in

processing and innovation that leads to flexibility and operational efficiency.

In addition to the product capabilities and breadth, there is a second level of complexity that processors

must take into account. The processors truly capable of capitalizing on the evolution of prepaid will

provide their issuing clients with flexible authorization parameters, fee options and decisions, fraud

parameters, load options, purchase options (web, retail, in‐branch), activation approaches, etc., all

responding to the unique needs of a myriad of opportunities.

The Prepaid Card and the Individual Relationship Prepaid products moving forward could well form the basis for deeper relationships with individual

cardholders—more closely mirroring the debit card or credit card relationship of the present. The

evolution will be centered on individual relationships between issuers and cardholders, with greater

longevity for the relationship derived from the product and program. As more consumers utilize one of

various prepaid products as their primary payment mechanism, they will place a greater importance on

the relationship with the issuer of that prepaid product. The market will become less fragmented and

separated by type of prepaid product. Conversely, the relationship with the individual cardholder maybe

less focused on the product as semi‐disposable—payroll cards linked to one employer, or gift cards

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 7

linked to one merchant, for example—and more focused on the longer‐term possibilities of a

relationship between issuer and customer, turning the prepaid relationship into a stronger and more

lucrative bond between individual and issuer.

Historically, prepaid card products have been institutionally‐driven, with the focus on the issuing

entity—a store‐branded gift card, or a company payroll card, for example. As more consumers become

reliant on the prepaid product as their primary payment vehicle, however, the opportunity for financial

institutions and other prepaid card issuers to establish more deep‐seated, individual relationships with

prepaid cardholders will expand considerably, for both retail transactions and bill payment activity.

Issuers can therefore take advantage of this behavior evolution and opportunity, which will result in a

tremendous increase in the average lifetime value of the relationship with a prepaid account holder,

regardless of product type.

The payroll card deepens both commercial and consumer relationships, and is at the heart of the

evolution strategy for many financial institutions and other players. This mindset—presently most

readily apparent in the payroll card product—could also pervade to general purpose reloadable cards,

particularly among certain subsections of the consumer population that show a higher propensity to use

prepaid products, including younger consumers, as well as under‐banked and unbanked consumers.

Several large institutions and other players in the prepaid space, for example, are focusing on the payroll

card as a primary vehicle for this evolution.

The combination of bolstering commercial relationships through this offering, as well as the extended

outreach to individual cardholders—for some potentially the only “branded” payment card they

possess—maybe thought of as an evolutionary stage in prepaid card evolution.

What Will Characterize the Evolution of Prepaid?

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 8

What Will Characterize the Evolution of Prepaid?

Companies looking to enter the prepaid arena need to look at the holistic capabilities of processing solutions, understanding the various components of an effective

prepaid program operation and how each component is implemented and managed.

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 9

The Components of a Prepaid Processing Program

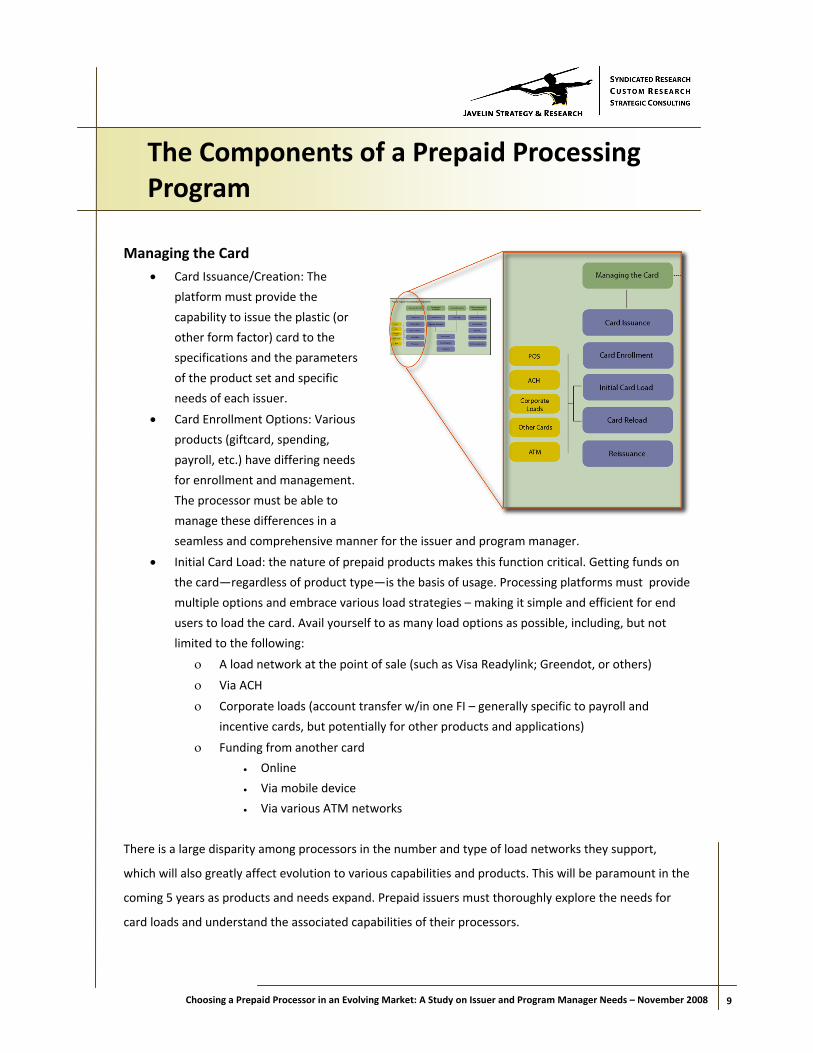

Managing the Card • Card Issuance/Creation: The

platform must provide the

capability to issue the plastic (or

other form factor) card to the

specifications and the parameters

of the product set and specific

needs of each issuer.

• Card Enrollment Options: Various

products (giftcard, spending,

payroll, etc.) have differing needs

for enrollment and management.

The processor must be able to

manage these differences in a

seamless and comprehensive manner for the issuer and program manager.

• Initial Card Load: the nature of prepaid products makes this function critical. Getting funds on

the card—regardless of product type—is the basis of usage. Processing platforms must provide

multiple options and embrace various load strategies – making it simple and efficient for end

users to load the card. Avail yourself to as many load options as possible, including, but not

limited to the following:

ο A load network at the point of sale (such as Visa Readylink; Greendot, or others)

ο Via ACH

ο Corporate loads (account transfer w/in one FI – generally specific to payroll and

incentive cards, but potentially for other products and applications)

ο Funding from another card

• Online

• Via mobile device

• Via various ATM networks

There is a large disparity among processors in the number and type of load networks they support,

which will also greatly affect evolution to various capabilities and products. This will be paramount in the

coming 5 years as products and needs expand. Prepaid issuers must thoroughly explore the needs for

card loads and understand the associated capabilities of their processors.

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 10

The Components of a Prepaid Processing Program

• Card Reload

ο POS

ο ATM

ο Evolving

ο Other

• Card Reissuance: What are the processes in place to immediately deliver reissued cards,

and how does the processor handle inventory management of replacement cards?

Whether this is an in‐house activity that the processor performs, or done through

established partnerships, the prepaid issuer must ensure that the card replacement

process is seamless and without problem to the end user. This will be of rising importance

should the prepaid card become the primary—and in many cases the only—payment

mechanism that end users carry. Replacement is a high profile segment of a prepaid

program that can readily expose faults in the issuer program and be the catalyst for lost

customers if there are hiccups in the process.

Managing the Cardholder • Cardholder Care (Call Center

Services): Many issuers rely on

their processor to provide

various levels of cardholder care,

operating not only call centers,

but also providing the capability

for online end user account

management. This is particularly

important for issuers of prepaid

payroll cards, but extends to

other products, particularly

reloadable spending cards, but

also with standard gift cards.

Issuers must fully analyze these

capabilities with each processor, matching them to their perceived needs and to those of

end users.

• Statement Generation, Balance Inquiry Capabilities, (online, via ATM, IVR, and potentially

via SMS): With the evolution of reloadable prepaid products, it is increasingly important

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 11

The Components of a Prepaid Processing Program

that end users have constant account management access, and that this is congruent with

technology evolution for other payment products. Is the processor providing for account

access via the mobile channel, for example, or

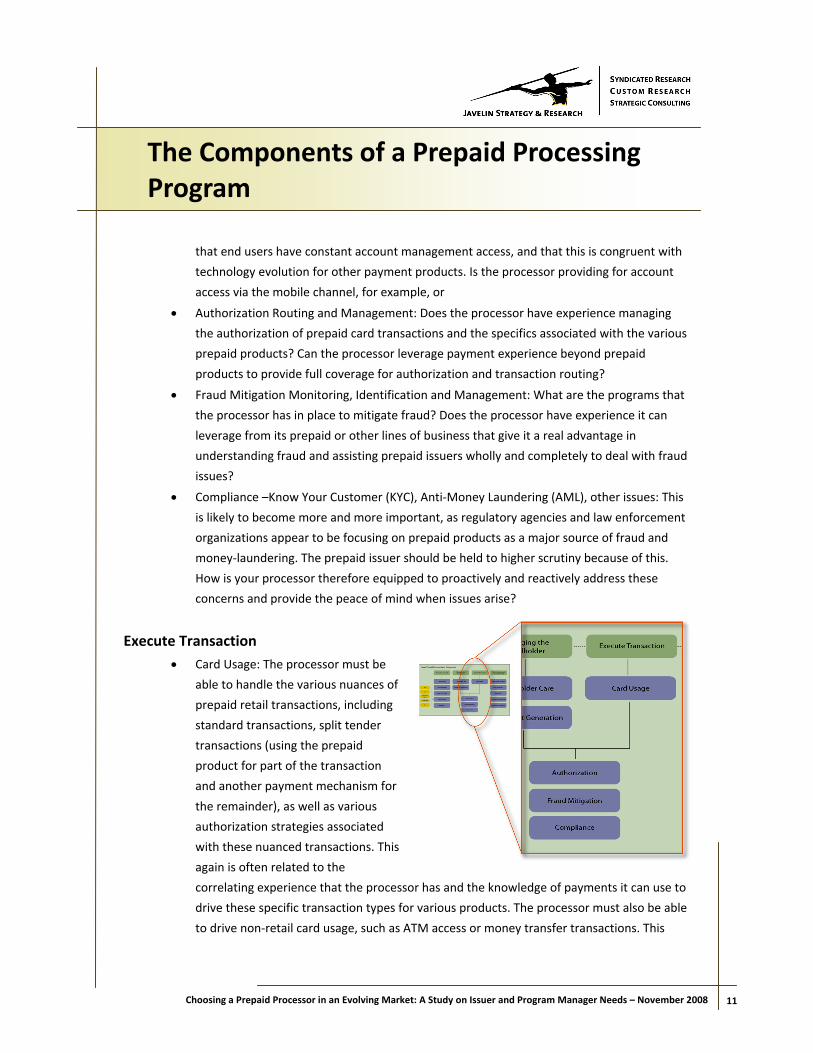

• Authorization Routing and Management: Does the processor have experience managing

the authorization of prepaid card transactions and the specifics associated with the various

prepaid products? Can the processor leverage payment experience beyond prepaid

products to provide full coverage for authorization and transaction routing?

• Fraud Mitigation Monitoring, Identification and Management: What are the programs that

the processor has in place to mitigate fraud? Does the processor have experience it can

leverage from its prepaid or other lines of business that give it a real advantage in

understanding fraud and assisting prepaid issuers wholly and completely to deal with fraud

issues?

• Compliance –Know Your Customer (KYC), Anti‐Money Laundering (AML), other issues: This

is likely to become more and more important, as regulatory agencies and law enforcement

organizations appear to be focusing on prepaid products as a major source of fraud and

money‐laundering. The prepaid issuer should be held to higher scrutiny because of this.

How is your processor therefore equipped to proactively and reactively address these

concerns and provide the peace of mind when issues arise?

Execute Transaction • Card Usage: The processor must be

able to handle the various nuances of

prepaid retail transactions, including

standard transactions, split tender

transactions (using the prepaid

product for part of the transaction

and another payment mechanism for

the remainder), as well as various

authorization strategies associated

with these nuanced transactions. This

again is often related to the

correlating experience that the processor has and the knowledge of payments it can use to

drive these specific transaction types for various products. The processor must also be able

to drive non‐retail card usage, such as ATM access or money transfer transactions. This

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 12

The Components of a Prepaid Processing Program

includes, but is not limited to the expansion of these transactions through new emerging

non‐card mechanisms such as mobile handsets.

• Exception Transactions: Does the processor have deep‐seated knowledge and

understanding of the intricacies involved in recognizing, processing and servicing exception

transactions? Can the processor effectively manage chargeback transactions, deal with

negative balances on the card, and make these capabilities as invisible and smooth as

possible for the issuer?

Platform Management and Growth Potential

• Value Added Services: it is important to

know to what extent the processor

supports additional transaction types

and services offered to end users,

including bill pay, money transfer,

among other mechanisms that will gain

prominence as prepaid usage becomes

more primary among a greater number

of consumers.

• Card Marketing: How capable is the

processor in working with issuers to market the card products? How innovative and

consultative can the processor be in promoting the prepaid products and their usage? Can

the processor deliver the marketing support commensurate with each issuer’s needs?

• Reporting: Processors must have the integrated capability to deliver effective program and

individual account reporting to meet the needs of issuers with regards to portfolio analysis,

as well as individual account analysis. With many issuers seeking to leverage the prepaid

product as a catalyst to deeper product relationships with end users, reporting becomes an

effective tool in analyzing individual cardholder readiness for those additional products.

Issuers must fully analyze the reporting capabilities offered by their processor as it relates

to their needs.

• Consultative Relationship: Is the processor reactively providing what issuer clients request,

or knowledgeable enough about the evolution of the prepaid market to proactively assist

the issuer in defining those needs? Can the processor move from the needs definition to

implementation, and then the evolving needs definition stage once the platform is up and

running. The prepaid processors that stand head and shoulders above the myriad are those

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 13

The Components of a Prepaid Processing Program

that provide more than just the nuts and bolts processing solution. Those that can work

with clients and actually help grow clients’ prepaid programs through a consultative

relationship are processors that demonstrate the most value over the life of a processing

relationship.

• Technology Expansion (contactless, mobile, etc.): Is the processor poised to provide inroads

to evolutionary technology in the prepaid space? Hand in hand with the consultative

relationship is the ability of the processor to seamlessly and consistently provide issuers

with the latest technology advancements, such as account access through mobile devices,

the potential for contactless technology in standard card form factor, within the mobile

device, or elsewhere. The processor is the primary conduit for the issuer in the awareness

and implementation of the latest technology in prepaid. Issuers need to have the implicit

trust in their processor to be on the cutting edge with technology advances and to assist

them in applying technology to meet the evolving needs of their end user customers.

• Product Breadth: The processor must be able to meet the product needs of the issuer,

servicing the unique characteristics of the base of prepaid products, which may include:

ο Consumer self (travel card)

ο Consumer other (gift card)

ο Employer (payroll, incentive, spending, fleet, petty cash)

ο Employee Benefits

ο Government

ο Teen spending card

ο Reloadable spending (general purpose reloadable)

ο Merchant‐specific Incentive/Rebate

ο Healthcare

No Processor can meet every need, but it is important to find a relationship that most

closely matches your product evolution strategy, and addresses all functionality. Issuers

with a healthcare focus may need to seek out a relationship specific to that product set,

potentially separate from the primary processing relationship.

• Support for Established Relationships: Can the processor leverage and support pre‐existing

acquirer relationships? If the issuer needs to build gateways to various acquirers, can the

processor accomplish this? Are those gateways established or would they be “special

order” and potentially delayed by the certification process? Should this prove to be an

imperative for the issuer, these questions must be posed to determine the viability and

compatibility of the processor with the issuer needs.

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 14

Prepaid Evolution: Scalability in Transaction Volume and Product Breadth Myth: Transaction Volume Scalability is Easy as 1‐2‐3

Prepaid issuers certainly look at transaction

volume growth as one primary measure of

success. But with growth comes the reality

that processors may have to struggle to scale

to meet the ongoing needs of their issuer

clients, particularly at peak volume periods.

The increased importance of a wider variety

of prepaid products leads to more in depth

needs from the operating platform and

processor. Speed to market (i.e. “get me up

and running yesterday!”), while important,

cannot be the driving factor in selecting a

prepaid processing provider. Reliability,

scalability, hardened security & compliance

standards, product evolution capabilities, and

increased portability for end users are

primary factors that prepaid issuers must

consider.

Surprisingly, these capabilities are not readily apparent among all platform providers. Due diligence

surrounding the processing capabilities and platform uptime, for example, is a must for all companies

considering a major investment in a prepaid platform. Fundamentals count ‐ Those lured by the bells

and whistles of a point solution or a quick installation will likely fall short in the ability to foster long‐

term growth. Additionally, longevity and experience count. Processors with large scale transaction

processing experience (debit and credit) have learned through doing how to effectively and efficiently

provide prepaid processing services. Many issuers and program managers have reached levels of success

with their business that is making them take a second look at their processor’s capabilities. Success and

growth in prepaid requires many of these new questions to be addressed.

Dispelling Myths About Prepaid Processors

Baseline functionality may include, but is not limited to the following: Card management, cardholder care, robust

transaction processing, and tactical consulting. Additional features expand as program needs expand. These generally include a more strategic consultative relationship, and a deeper understanding of the complexities facing each

individual prepaid program.

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 15

Reliability and Scalability in Transaction Volume Myth: All Processors Experience Little to no Downtime For many prepaid card issuers, the point of sale (or purchase) is often the primary and certainly recurring

opportunity they have to prove the integrity of their product and value of their brand to form and

maintain a trusted relationship with cardholders. This is true for both purchase transactions and further

emphasized for reload capabilities. Customers need purchase and load capability at all times. For

reloadable spending cards, and even for gift cards, the reputation of the issuing institution is at stake

with each transaction. If it doesn’t work, customers walk. And the reality is that not all prepaid processor

or platforms can provide the level of reliability that issuers need. At the most basic level, the prepaid

processing platform must have a proven track record of reliability. Can the platform be up and running

at all times when needed – whether that be pre‐, during, or post‐purchase?

Hand in hand with reliability is scalability. Prepaid card issuers must also assess the capabilities of the

platform to grow as their needs grow, first and foremost in terms of transaction volume. Is the platform

robust enough to handle expanding transaction volume? Point solutions may serve well in the present,

but as the prepaid issuance program expands, can the processing platform expand to meet volume

needs? Included in this are also the various functions, such as inventory control, fraud mitigation,

reporting, and transaction settlement—are they all contained within the one platform, or does the

issuer need to cobble together pieces of this from various players?

These issues extend further to the specific program elements that affect the issuer‐customer

relationship most predominantly, including authorization performance, call center and VRU capabilities,

fraud mitigation, online account access and usage, among other capabilities. How are those capabilities

measured, and what is the performance record over time? More importantly, how does the processor

track performance and work toward its continual improvement? Prepaid issuers must have these

questions answered and not assume they are inherent to all prepaid processing platforms and service

providers.

Dispelling Myths About Prepaid Processors

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 16

Customization and Product Evolution Capabilities Myth: One Size Fits All‐ Issuers Seek Static Processing Solutions. Prepaid means different things to different players—and issuer needs are ever‐evolving. The reality is all

processors face the challenge of meeting the diverse and expanding needs of prepaid marketplace. The

line of questions includes the following:

• Does processor have a demonstrated record of continual investment?

• Do they have long‐term product roadmap and what is their track record in delivering on‐time

against it?

• Have they demonstrated they meet their commitments?

• Do they consult with their customers?

• Does this consultation happen in a one‐on‐one environment or by facilitating joint customer

working groups?

Many prepaid processors are ill‐equipped to handle the dynamic nature of those needs. As indicated

previously, the prepaid market moving forward will encompass a wider variety of products. Different

issuers will see value in different products, and opportunities will arise for individual issuers to expand to

additional products. In fact, prepaid card issuers are already taking advantage of expertise they have

gained with one product to seamlessly extend their lines of business. The processor must serve as a

conduit to that product expansion, and must have expertise in the various success factors and needs

associated with disparate product sets. For example, gift card programs, reloadable spending cards, and

payroll card programs have different end users, reporting needs, payment network access needs, among

other differences. Does the prepaid processor have expertise with each of these products to provide for

this seamless expansion? Can the processor work with the issuer to strategically and effectively develop

these product lines?

Prepaid issuers must have an understanding of whether the processor can meet all of these needs

moving forward. This can be quite difficult, of course, as those forward needs may not be clearly defined

from the outset of entering the prepaid space. It is for this reason that issuers must be more

comprehensive in their analysis and vetting of processor capabilities—thinking more holistically about

what they may need and whether the processor can provide it.

Dispelling Myths About Prepaid Processors

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 17

Security, Risk Management and Compliance are not Givens, and Issuers are More Highly Scrutinized Myth: All Processors Provide Effective Risk Mitigation and Compliance Security and risk management are paramount in prepaid card issuance—both with respect to fraud

mitigation and also in the scrutiny that issuers face to comply with money‐laundering and homeland

security standards. Prepaid card issuers may be increasingly held accountable for the actions of not only

their immediate constituents and customers, but also the indirect usage of their products down the line.

Secure processing is therefore only one aspect of prepaid card security overall. Issuers must thoroughly

analyze the prepaid processor’s capability to also provide AML and KYC capabilities, as well as other

homeland security initiatives. These issues are standard for processors familiar with the financial

institution regulatory arena, but in reality sometimes fall outside the set of core competencies for

prepaid point solution providers and processors. Can the following processes be handled efficiently –

fraud, risk mitigation, compliance tools, flexibility in rule sets, parameters, reporting, ‘on behalf of’

services. Security and peace of mind in the prepaid platform can be viewed in various ways. The

following angles are paramount when analyzing the security capabilities of the prepaid processor:

• The security of a stable system; • The security (i.e., confidence and peace‐of‐mind) from working with an experienced partner; • The security (i.e., protection) from fraud risks and scams; and • The security in knowing that one is complying with company and regulatory policies.

When all these above security questions are adequately and proactively addressed in the platform

decision process, prepaid issuers can move forward and grow their programs more effectively and more

securely.

Dispelling Myths About Prepaid Processors

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 18

Transaction Processing and Associated Services Make a Complete Circle: Can Your Processor Help you Drive Strategy? Myth: Processors Need Only Provide Processing Capabilities The prepaid processing platform is only as good as the processor behind it. The bottom line for prepaid

issuers is the formation of a consultative relationship with the prepaid processor, something that—in

reality—not all processors can effectively provide. The processor must provide knowledge, expertise,

and strategic direction as well as professional services, integration and transaction processing. Part of

the evaluation that all prospective prepaid card issuers must make is whether the processor has the

market knowledge to truly drive the business—anticipating future needs, fleshing out and managing

expectations— whichever direction the issuer may take. The path to revenue and profitability is not the

same for a financial institution, a merchant, and other third party issuers. Successful prepaid processors

will proactively evaluate the market opportunity with their clients, not reactively build solutions to meet

the pre‐defined needs of those clients. Often, those needs are not pre‐defined or even known. The

expertise that the processor brings to the relationship may prove to be strategically invaluable. Issuers

must ask: Is this value inherent in the platform, or are the “builds” (extensions) reactive to customer

needs? The value of the consultative prepaid processing relationship reaches beyond technical

integration. Strategically, the platform provider must be able to proactively create need scenarios and

drive the client to the understanding of how to best develop products that drive profitability and fully

leverage prepaid capabilities, leading to greater customization capabilities and in turn, greater

customization in implementations.

Dispelling Myths About Prepaid Processors

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 19

Can Credit and Debit Experience be Leveraged in the Prepaid Space? Myth: Credit and Debit Card Processing Experience and Architecture is Ill‐Suited for Prepaid There has been an abundance of technology approaches to prepaid processing systems, and in turn a

variety of models have emerged which promise both an open system and open architecture. Promises of

“newer, cheaper, better, and faster” abound in the prepaid processing space. The reality is that

experience is necessary to fully build availability, security, and flexibility into a prepaid

platform that meet the needs of today's markets with the capability to easily address subsequent years’

continued growth. Leveraging that experience effectively delivers value for issuers and program

managers, as well as for prepaid card users.

The proven flexibility and availability of credit and debit card platforms have been utilized as the core

processing engine for prepaid platforms, with open systems integration to seamlessly extend those

services into other platforms via web services, including the following functionality:

• Inventory management

• Fraud and risk management

• Non‐financial transaction processing

• Web and IVR

Fundamentally, the differentiator of the credit or debit card platform at its foundation is the availability

of the processing engine and the flexibility that can be provided through the addition of distributed

architecture principles and technologies, a balance that point solutions and platforms may not fully

address.

Dispelling Myths About Prepaid Processors

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 20

Conversions are Painful—Implementations Should not Be Myth: Implementation and Conversion Capabilities are a Dime‐a‐Dozen What record does the prepaid processor have with new prepaid card program implementations and

conversions of existing programs? These questions must go well beyond the timetable to be up and

running. Quick implementation does not always equate with worry‐free implementation. How does a

processor differentiate between a conversion and a migration? What are the compelling reasons for that

migration?

A large part of the consultative relationship is the core implementation and the migration or conversion

knowledge that the processor brings. Implementations should not be painful. They should be thoughtful,

with heavy planning in the early stages. Here too, experience counts. The ability that the processor has

to make the implementation—or especially the conversion—as painless as possible for the prepaid

issuer, potentially “hand holding” through the process, will prove to be invaluable. Some prepaid issuers

would rather stay with a processor that does not meet their growth needs than go through the

perceived pain of a conversion. Processors with proven conversion capabilities, and of course proven

robust platforms, can enable prepaid issuers to realize the full potential of their prepaid programs. In

reality, this capability is a proven differentiator for select processors, and issuers must dig deep to find

that capability.

Dispelling Myths About Prepaid Processors

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 21

Is the Processor Prepared to Embrace Technology Evolution? Myth: Technology is Irrelevant and Stagnant in Prepaid Further to the proactive and forward thinking that a prepaid processor must provide is the capability to

expand as technology expands. Technology enhancements enable further expansion of prepaid

programs. The standard magnetic stripe, “credit card” form factor for prepaid products may evolve as

other card products and the payments infrastructure evolve. This includes contactless (standard card

form factor, key fobs, others), and virtual prepaid cards embedded in mobile handsets or other mobile

devices. Unique and innovative solutions and the realization of more solid prepaid programs may be

linked directly to technology. Prepaid issuers must therefore ask whether the processor is prepared to

take advantage of capabilities—and correlated potential sources of growth—such as contactless. Is the

processor at the forefront of all payment initiatives, or lacking in breadth and hence missing out on

expansion possibilities? In reality, this matters.

Financial Institution Reaction and Needs are focused More on Brand Financial institutions and those companies that are part of the supply chain who help bring prepaid

cards to market benefit from not only the processing relationship, but also the power of strong, trusted

brands – both their own and those of the payment networks – in extending to various prepaid product

categories. Depending on the size of the institution and the nature of the card program (how robust,

how many cards issued, the types of products, etc.), the

financial institution could rely heavily on the card brand

and the inherent prepaid capabilities of the card network.

Any processor decision must therefore take into account

the relationship and interaction the processor has with

any and all card brands.

Dispelling Myths About Prepaid Processors

Choosing a Prepaid Processor in an Evolving Market: A Study on Issuer and Program Manager Needs – November 2008 22

There are an abundance of factors that prepaid issuers must consider in establishing a relationship with

a processor. The processor decision is not one to be taken lightly. As the above evidence indicates, the

analysis of a processor fit is multi‐faceted. Primarily, issuers must remember to look for the following

key aspects and strengths when choosing a processor:

• A proven record of a stable, reliable platform

• Product breadth and evolution capabilities

• Scalability – the inherent capability of the prepaid processor

• The processor’s ability to serve as a conduit to product expansion

• Experience and link to major card brands

• Proven record in managing all facets of the card program

ο Card creation

ο Card load

ο Retail transaction

ο Transaction authorization management

ο Cardholder care

ο Risk and exception management

• Technology evolution capabilities

• Consultative relationship

The productive relationship between prepaid issuer and processor is one that takes full advantage of all

capabilities the processor has, moving well beyond simple nuts‐and‐bolts transaction processing to an in

depth interaction. The paragon being a situation in which the issuer can rely on the processor for more

complete program management assistance and collaboration. This is not an easy situation to create, and

it requires a deeper level of analysis on the part of the issuer. Once it is attained, however, the

possibilities for expansion of the prepaid program are enhanced many‐fold.

In collaboration with Visa Debit Processing Service , Javelin has written, Choosing a Prepaid Processor in an Evolving Market: A

Study on Issuer and Program Manager Needs. Visa Debit Processing Service partially underwrote Javelin’s cost of data collection,

analysis and reporting in this study. Javelin retains complete independence of data analysis and reporting, and this report has been

created solely by Javelin employees.

Summary and Wrap up – Key Considerations for a Prepaid Processing Relationship