Chinasoft International (354.HK) 2017... · Convertible loan notes 248,592 244,296 ... Spyglass,...

28

Chinasoft International (354.HK) Interim Presentation 2017 H1

Transcript of Chinasoft International (354.HK) 2017... · Convertible loan notes 248,592 244,296 ... Spyglass,...

Chinasoft International (354.HK)

Interim Presentation

2017 H1

Disclaimer

These presentations and/or other documents have been written and presented by Chinasoft International

Limited (“Chinasoft International” or “the Company”).

The information presented or contained in these materials is subject to change without notice and its

accuracy is not guaranteed.

Neither the presentation nor any of the information contained therein constitutes an offer to sell or issue

or the solicitation of an offer to buy or acquire or invitation to purchases or subscribe for any securities of

the Company in any jurisdiction or an inducement to enter into investment activity, nor may it or any part of

it form the basis of or be relied upon in connection with any contract, commitment or investment decision

whatsoever.

2

目录

1. Financial Results

2. Business Developments and Strategic Outlooks

3. Investment Highlights

4. Company Overview

3

Financial Highlights

4

RMB ‘000 2017H1 2016H1 Growth

Revenue 4,145,060 2,884,951 43.7%

Service Revenue 4,047,248 2,832,120 42.9%

Gross Profit 1,142,673 802,635 42.4%

Profit for the Period 240,445 218,619 10.0%

Profit Attributable to Shareholders 245,470 236,237 3.9%

Basic EPS (RMB Cents) 10.26 11.04 (7.0%)

Operating Profit Excluding Share Option Expenses 311,982 226,292 37.9%

Profit Attributable to Shareholders Excluding Share Option

Expenses317,007 243,910 30.0%

Basic EPS Excluding Share Option Expenses (RMB Cents) 13.25 11.40 16.2%

Segment Results

5

TPG84.7%

IIG15.3%

Revenue Proportion

10.9%

9.6%

10.5%10.1%

TPG IIG

Profit Margin Before Tax

2016H1 2017H1

2,287,883

597,068

3,511,450

633,610

TPG IIG

Revenue

(RMB‘000)

2016H1 2017H1

* Excluding the market investment from associates, IIG’s profit

before tax increased.

Income Statement

6

RMB ‘000 2017H1Of

Revenue

Of Service

Revenue2016H1 Of revenue

Of Service

RevenueGrowth

Revenue 4,145,060 2,884,951 43.7%

Service revenue 4,047,248 2,832,120 42.9%

Cost of sales and services (3,002,387) (72.4%) (2,082,316) (72.2%) 44.2%

Gross profit 1,142,673 27.6% 28.2% 802,635 27.8% 28.3% 42.4%

Other income 33,879 0.8% 0.8% 48,113 1.7% 1.7% (29.6%)

Selling and distribution expenses (146,944) (3.5%) (3.6%) (112,217) (3.9%) (4.0%) 30.9%

Administrative expenses (including share

option expenses)(659,774) (15.9%) (16.3%) (390,651) (13.5%) (13.8%) 68.9%

Allowance for doubtful debts (1,401) (0.03%) (0.03%) (11,382) (0.4%) (0.4%) (87.7%)

Amortization of intangible assets (41,759) (1.0%) (1.0%) (41,479) (1.4%) (1.5%) 0.7%

Interests in associates (15,509) (0.37%) (0.38%) 10,148 0.35% 0.36% (252.8%)

Financial costs (43,064) (1.0%) (1.1%) (39,039) (1.4%) (1.4%) 10.3%

Profit before taxation 268,101 6.5% 6.6% 266,128 9.2% 9.4% 0.7%

Income tax expense (27,656) (0.7%) (0.7%) (47,509) (1.6%) (1.7%) (41.8%)

Profit of the period 240,445 5.8% 5.9% 218,619 7.6% 7.7% 10.0%

Profit of the period excluding share

option expenses311,982 7.5% 7.7% 226,292 7.8% 8.0% 37.9%

Balance Sheet

7

RMB ‘000 2017H1 2016

Current assets

Inventory 54,500 20,893

Trade and other receivables 2,749,266 2,092,700

Bill receivable 6,299 23,186

Prepaid lease payments 860 860

Amounts due from cust. for contract work 1,547,993 1,430,206

Amounts due from related companies 50,334 59,939

Pledge deposits 1,008 670

Bank balances and cash 1,054,511 1,298,972

5,464,771 4,927,426

Non-current assets

PPE 852,634 819,799

Intangible assets 201,848 231,075

Goodwill 1,008,479 1,008,479

Interests in associates 93,946 104,190

Available-for-sale investment 61,970 61,965

Prepaid lease payments 38,290 38,723

Other receivable 30,000 30,000

Deferred tax assets 7,589 7,646

2,294,756 2,301,877

Total assets 7,759,527 7,229,303

RMB ‘000 2017H1 2016

Current liabilities

Amounts due to customers for contract work 44,442 122,271

Trade and other payables 1,208,866 1,203,843

Bills payable 24,516 812

Amounts due to related companies 20,089 37,983

Dividend payable 81 83

Tax payable 132,945 130,450

Borrowings 1,160,682 922,452

Consideration payable on acq. of a subsidiary 21,035

2,591,621 2,438,929

Non-current liabilities

Differed tax liabilities 17,746 18,943

Convertible loan notes 248,592 244,296

Borrowings 127,300 194,496

393,638 457,735

Total liabilities 2,985,259 2,896,664

Capital and reserves

Share capital 110,283 106,387

Share premium 2,809,330 2,652,697

Reserves 1,791,255 1,505,130

Equity attributable to owners of the Company 4,710,868 4,264,214

Non-controlling interests 63,400 68,425

Total equity 4,774,268 4,332,639

Operating Cash Flow & DSO

8

-300,290

239,252

-426,864

501,660

-471,596

731,157

-560,976

852,710

-618,007

(In RMB‘000)

13H1 13H2 14H1 14H2 15H1 15H2 16H1 16H2 17H1

DSO(Days)

183174 177

155 154

2013 2014 2015 2016 2017H1

Operating Cash Flow

目录

1. Financial Results

2. Business Developments and Strategic Outlooks

3. Investment Highlights

4. Company Overview

9

I. Large Customers Continue to Grow

10

HSBC

• Share of HSBC’s CMB outsourcing

increased from 5% to 50%,

becoming the largest IT service

provider of CMB

• Launched Mobil-Z, HSBC’s new

generation mobile banking system

integrating facial recognition, AI

and cloud technology

Microsoft

• Provided tech support for Microsoft

in AI voice recognition area

• Catapult continued to be

Microsoft’s best cooperating

partner, Fuse and Launch gained

favorable comment continuously

and achieved 100% renewal rate

Tencent

• Revenue maintained high speed

growth

• Cooperation with Tencent goes

deeper, rated level A supplier in

Tencent’s supplier rating

Huawei

• Revenue maintained high speed

growth

• Software service successfully

transferred from traditional ADM

to global cooperation, great

progress was made in AO, IO

and ADM

II. Cloud 2.0: A New Era with Huawei

11

In July, Chinasoft became the first and highest ranked Huawei Public

Cloud Partner, as well as the only comprehensive strategic partner

in Huawei dev. cloud. The two parties will work closely in Huawei

dev. cloud, cloud solution, and other cloud services.

1. Chinasoft becomes a leader in the Huawei ecosystem

2. Realize cloud revenue faster than anticipated

3. A new business model towards SaaS direction

Implications:

II. Cloud Businesses Growths

12

Qingdao Government

Affairs Cloud

Yuxi Government

Affairs CloudWuhan City Cloud

Luzhou Government

Affairs Cloud

Ziyang City Cloud

Zhangzhou Government

Affairs Cloud

Langfang Public Cloud

Dalian Software Dev. CloudYan’an Government

Affairs Cloud

Henan Government

Affairs Cloud

Hangzhou Unicom

Public Cloud

Wulanchabu

Cloud Platform

Xinjiang Cloud Migration Project

CSI won the bid of establishing

Vanke document cloud platform,

and became the core supplier of

Vanke.

CSI won the exclusive bid for

Henan Development and Reform

Commission's private cloud

migration.

CSI’s enterprise cloud disk

solution for education industry

helped informatization of China

University of Geosciences

CSI delivered enterprise cloud

disk project for ICBC Asia.

II. Cloud – Based Solutions Accelerates

13

Rail TransitACC

Solutions on CloudE-Commerce

Cloud

Business AuditCloud

Process & ITCloud

Retail Cloud

Corporate Customer

Label Cloud

Entity-Relationship Cloud Logistics Cloud

City OperationBig Data

CollectionCloud

Financial Supervision Cloud

Financial Big-DataReal time Anti-Fraud

API Integration Management

Cloud Platform

Enterprise Cloud Disk

Data AssetsManagement

Platform

Establishment

Data Anal./

Application

Data Mgmt.

II. Big Data Business Soars

14

Over 1,000 big data engineers; longest employed and most

experienced team in China

End-to-end enterprise, cross platform level services (including big

data tools, application, and services)

Big data tools, Financial, Banks, Insurances, Securities,

Government, Media, Energy, etc.

Cross Platform Capabilities

DB2(DPF)

Team

Capabilities

Experiences

New Clients in 2017 H1

Chinasoft’s Tools and Products

II. Artificial Intelligence Breakthroughs

15

Using AI + Cloud to improve

accuracy of speech recognition

for a global IT company.

Using AI + big data to create a

brand new smart AI

recommendation system for

Jointforce.

mVTM is a new generation of

video teller machine with facial

recognition and other risk

controls.

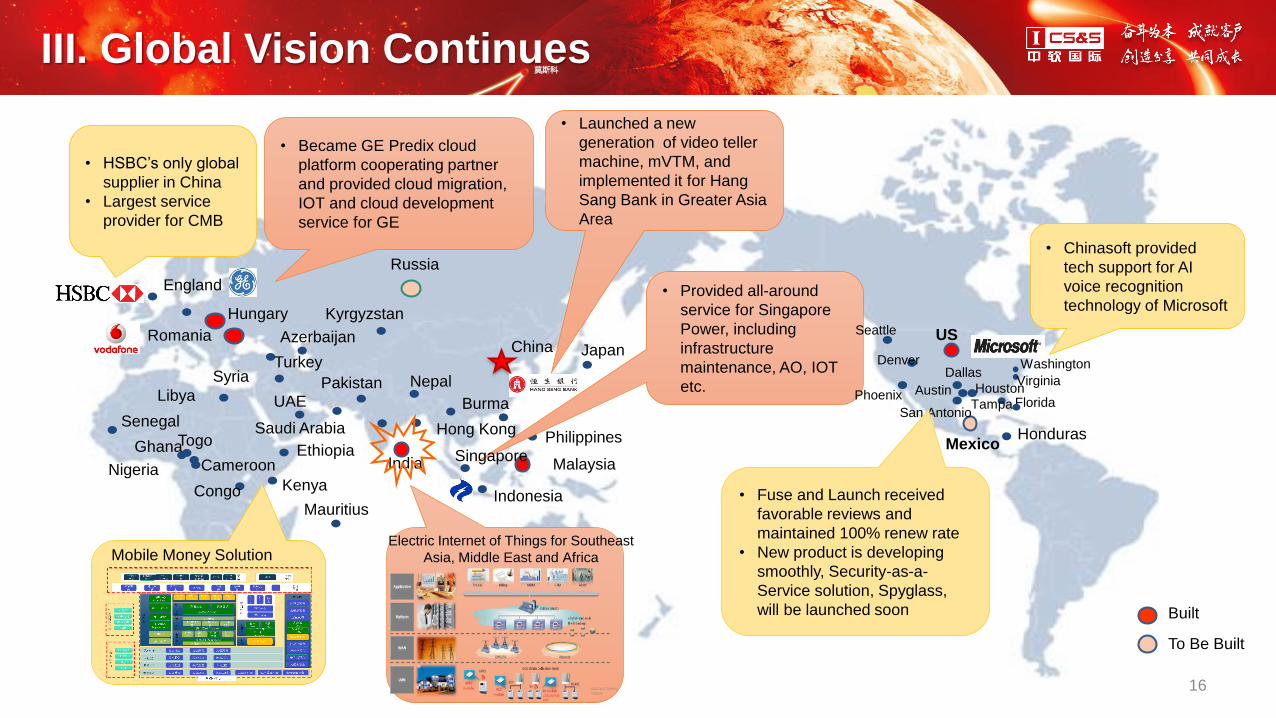

III. Global Vision Continues

16

LibyaNepal

India

Hong Kong

Malaysia

Indonesia

Philippines

Burma

Turkey

Russia

Kyrgyzstan

Azerbaijan

England

Hungary

UAEPakistan

Saudi Arabia

Ethiopia

Syria

Senegal

Ghana

Nigeria

Togo

Cameroon

Congo Kenya

Mauritius

China Japan

Mexico

US

Honduras

Romania

• HSBC’s only global

supplier in China

• Largest service

provider for CMB

• Became GE Predix cloud

platform cooperating partner

and provided cloud migration,

IOT and cloud development

service for GE

• Chinasoft provided

tech support for AI

voice recognition

technology of Microsoft• Provided all-around

service for Singapore

Power, including

infrastructure

maintenance, AO, IOT

etc.

Built

To Be Built

• Launched a new

generation of video teller

machine, mVTM, and

implemented it for Hang

Sang Bank in Greater Asia

Area

Electric Internet of Things for Southeast

Asia, Middle East and AfricaMobile Money Solution

Austin

DallasDenver

Virginia

FloridaHouston

Phoenix

San Antonio

Seattle

Tampa

Washington

Singapore

• Fuse and Launch received

favorable reviews and

maintained 100% renew rate

• New product is developing

smoothly, Security-as-a-

Service solution, Spyglass,

will be launched soon

16

IV. Jointforce 2.0

180,000+ 3000+ 20,000+ RMB 800 mn

17

As of June 30, 2017:

Jointforce 1.0:

jointforce.com

Jointforce 2.0:

jfh.com

For David and the “little guys”

out there

IV: A Full Product Upgrade

18

Provide

Service

Buy

Service

Platform

Community

Developer

Service

providerClients

Company

Team

Engineer

Service

Through

Platform

Delivery Guarantee

One-stop development service

Private

Project

Delivery

Manage

ment

Ord

er

Huawei Software

Development CloudJointForce

3Steps

Quick Start

20%More Efficient

30%Cost Saving

Customized Application DevelopmentAPP Dev. Wechat Dev. Front-End Dev.

Website Building UI Design Industry APP Dev.

AI Big Data AR/VR

Application Integration Information Security

Business Management Software

Tools Software Games Dev. Desktop Software

Development Platform Software Internationalization

Industry SolutionsEducation Finance E-Commerce

Health Care Travel Catering

Industrial Design & Smart ManufacturingHardware Dev. Mold Design Embedded Dev.

Industrial Design Circuit Design 3D Printing

Technical ServicesShort Term On-Site Testing Service

IT Operation and Maintenance

System Adjustment IT HR

Branding and MediaBrand Design Animation

Advertisement Marketing

New One-Stop shop;

Bundled with Huawei Dev. Cloud

IV. Business Models Shifts

19

New membership and storefront business model

IV. Cloud Software Park Ignites New Ecosystem

20

JinanQingdao

西安Xuzhou

NanjingShanghai

Guangzhou

Hangzhou

Wuhan

Changsha

Dalian

Hefei

Tianjin

Suzhou

Shenzhen

Chongqing

Chengdu

Xiamen

Beijing

4 Signed

15 To be Signed

提供本地化需

求市场、服务

市场、服务商

及解决方案

提供园区招商服

务、园区推广、

活动组织、企业

孵化培育

提供O2O的园

区企业教育和

训服务

目录

1. Financial Results

2. Business Developments and Strategic Outlooks

3. Investment Highlights

4. Company Overview

21

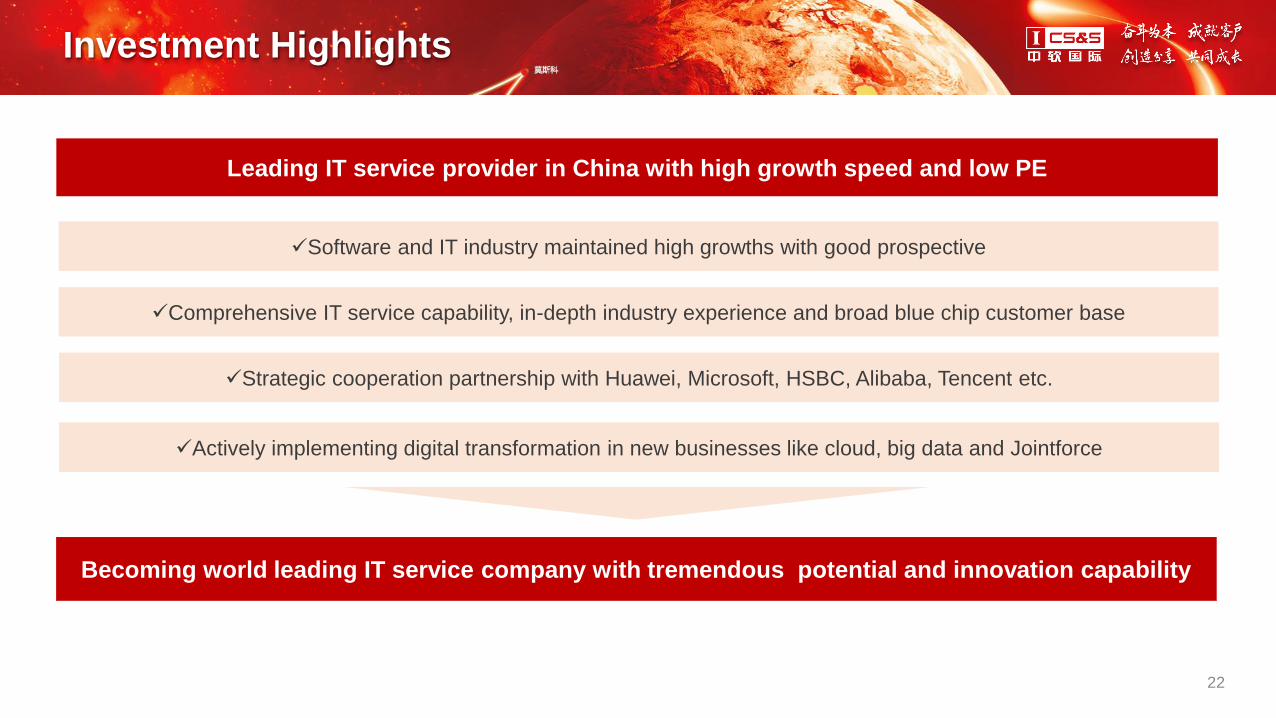

Investment Highlights

Leading IT service provider in China with high growth speed and low PE

✓Software and IT industry maintained high growths with good prospective

✓Strategic cooperation partnership with Huawei, Microsoft, HSBC, Alibaba, Tencent etc.

Becoming world leading IT service company with tremendous potential and innovation capability

✓Comprehensive IT service capability, in-depth industry experience and broad blue chip customer base

✓Actively implementing digital transformation in new businesses like cloud, big data and Jointforce

22

目录

1. Financial Results

2. Business Developments and Strategic Outlooks

3. Investment Highlights

4. Company Overview

23

Company Overview

24

TPG Technology and Professional

Services Group

IIGInternet IT Services

Group

Chinasoft is a large comprehensive “end-to-end” Chinese

IT service provider headquartered in Beijing and services

global clients.

Long-tail market

Jointforce

SaaS

Big client+ Industry

Outsourcing

Solutions

SMAC

Dr. Chen

11.01%Shenzhen-

Hong Kong

Connect

10.00%

Microsoft

4.05%

Huawei

3.54%Others71.40%

Shareholders

Established 2000

HK GEM Listing 2003

HK Main Board Listing 2008

Code 354.HK

Revenue in 2016 6.78 Billion RMB

Employees 50,356

Broad Blue Chip Customer Base

25

- 20 Chinese government ministries level

institutions

- 6 "Twelve“ Gold Project

- 100% Chinese banks

- 26 foreign banks

- 13 finance institutes

- Nearly 100 hi-tech and Internet

companies- 100% coverage of the top 3 Chinese

telecom operators

- 2 top three global

telecommunications equipment

supplier

Government

Hi-Tech, Internet

BFSI

Manufacturing

Telecom

Public

Services

- 100% coverage of the top 100 Chinese

cigarette brands

- 2 top 3 Chinese car brands

- 4 top 5 strong Chinese machinery

manufacturers

- 5 top 10 Chinese steel companies

• Shanghai

• Beijing

• Shenzhen

• Tianjin

• Chongqing

• Hanzhou

• Qingdao

-----

- Over 30 cities

- Issued over 100 million

system cards, Covered

more than 30 cities

“金审”

“金质”

“金保”

“金农”

“金宏”

“金卡”

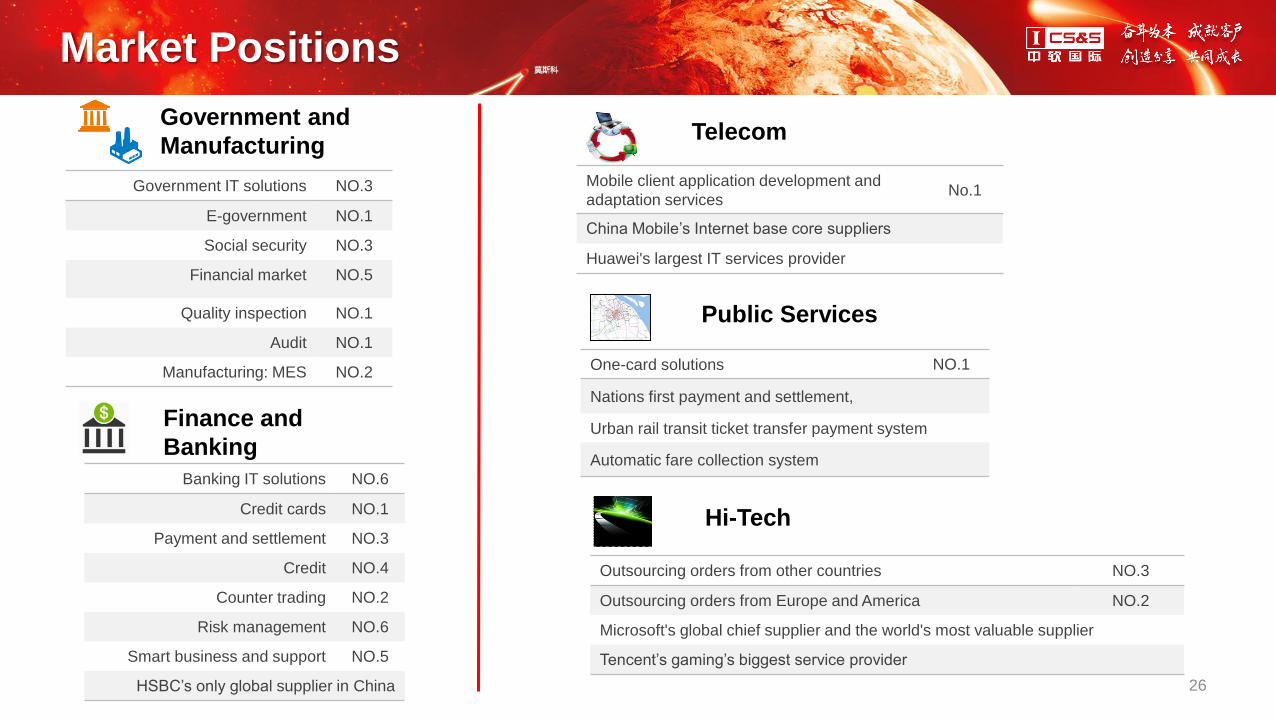

Market Positions

26

Finance and

Banking

Banking IT solutions NO.6

Credit cards NO.1

Payment and settlement NO.3

Credit NO.4

Counter trading NO.2

Risk management NO.6

Smart business and support NO.5

HSBC’s only global supplier in China

Government IT solutions NO.3

E-government NO.1

Social security NO.3

Financial market NO.5

Quality inspection NO.1

Audit NO.1

Manufacturing: MES NO.2

Hi-Tech

Public Services

One-card solutions NO.1

Nations first payment and settlement,

Urban rail transit ticket transfer payment system

Automatic fare collection system

Telecom

Mobile client application development and

adaptation servicesNo.1

China Mobile’s Internet base core suppliers

Huawei's largest IT services provider

Government and

Manufacturing

Outsourcing orders from other countries NO.3

Outsourcing orders from Europe and America NO.2

Microsoft's global chief supplier and the world's most valuable supplier

Tencent’s gaming’s biggest service provider

Solution Capabilities

27

Core

Products

Telecom

BFSI

Manufacture./

Distribution

Government

Audit Management

Social Insurance and Benefits

State Owned Asset Mgmt

Food and Drug Management

Administrative Management

Policy Planning System

Online Audit Application

Public Portal

Cloud Migration & Integration

ERP

MES

LES

Safety Production Management

WMS

EAI

Product Code Tracking

Mobile Payment

Mobile Instant Communication

Mobile Community

Corporate Weibo

Mobile Application Store

One-Click Dial

Embedded Browser

Mobile Advertisement

Platform

Payment System

Receivable System

Credit System

Bank Card System

Credit Card System

Risk Management System

Digital Marketing

Supply Chain Leverage

Insurance System

Digital Insurance System

Insurance Dev. Support

Reimbursement System

.

Pro

fessio

nal S

erv

ice B

usin

ess

Public Services One Card Access

AFC

ACC

Smart Transportation Airport Operating System

CRM

OA

BI

Portal Group

RFID

GIS

Electronic Ticketing

System

TopLink/TSA+ Platform

Used in Union Pay, Government, and Provinces Centers

Support Cross Regional Bank Card Online Transaction

Genera

l S

olu

tions

Electricity Material Management Solution Marketing Management Solutions

Middleware Platform ResourceOne is Based on SOA and Cloud

Popular in Government and Manufacturing Verticals – “trusted cloud”

Named the Best Government Platform by CCID 5 Years In a Row

ARK Middleware

One-stop big data dev. platform