China’s Opening-up Part II. Challenges for China's and ...

24

1 China’s Opening-up and Reform Yan ZHANG (张晏) China Center for Economic Studies School of Economics Fudan University • Local Debts, Land Finance, and Central- Local Relationship • Urbanization, Industrialization, and Investment Driving Force • Regional Partition, Urban-rural Partition, and Inequality in China Part II. Challenges for China's Economic Reform and Opening-up: Special Issues Part II. Challenges for China's Economic Reform and Opening-up: Special Issues Lecture 5. Challenge 3-Private Enterprises, Financial Constraints, and Marketization (Privatization)

Transcript of China’s Opening-up Part II. Challenges for China's and ...

1

China’s Opening-up and Reform

Yan ZHANG (张晏)

China Center for Economic Studies School of Economics Fudan University

• Local Debts, Land Finance, and Central-Local Relationship

• Urbanization, Industrialization, and Investment Driving Force

• Regional Partition, Urban-rural Partition, and Inequality in China

Part II. Challenges for China's Economic Reform and Opening-up: Special Issues

Part II. Challenges for China's Economic Reform and Opening-up: Special Issues

Lecture 5. Challenge 3-Private Enterprises, Financial Constraints, and

Marketization (Privatization)

2

Chinese Corporation: CHERY (奇瑞)

v the state-owned Chery Automobile � The company with the fifth-biggest brand in the local

market – ahead of Nissan, Ford and Hyundai. It held a 60% stake of China’s export market.

� It was one of the first made-in-china export bound for the United States.

• US auto giant Chrysler Group signed a deal with China‘s biggest automaker, Chery, to launch a low-cost production venture that could export the first Chinese-made cars to the United States and other markets. (in 2007)

• Chery’s attempts to export to the U.S. ended in failure. In fact, Chery lost its leadership position among the country’s local car companies when its vehicle sales declined by over 12 percent in 2012. Despite 10 percent overall industry growth this year, Chery is still struggling. The company’s sales have declined by 9 percent so far in 2014.

CHERY Automobile

v Chery Automobile Co., Ltd. was founded in 1997 by five of Anhui’s local state owned investment companies with an initial capitalization of RMB 3.2 billion.

v The first car came off the production line on December 18, 1999. And on August 22, 2007 (Mar. 26, 2010), the one-millionth (two-million) car of Chery rolled out the assembly line successfully.

v In 2007 (2010), the annual sales volume of Chery reached 381,000 (682058) units, increasing by 24.8% (36.3%) compared with 2006(2009). In 2007 also, Chery achieved an annual export volume of 119,800 units. The overseas sales of Chery had increased sharply, ranking 1st for 8 consecutive years in car export in China since 2002.

Chinese Homegrown Private Automobile: Geely (吉利)

v Geely Signs Definitive Stock Purchase Agreement with Ford to Acquire Volvo Car Corporation � Zhejiang Geely Holding Group, China's No 10 automaker, sealed a

binding deal last March to buy ailing Swedish luxury car brand Volvo from US giant Ford for $1.8 billion.

v The deal is China's biggest overseas auto purchase and represents the most ambitious move by a homegrown auto brand. � Li Shufu has a very strategic target that can be boosted by Volvo's

green technologies." � The takeover may help Geely take a step forward in competing with

other homegrown brands

Chinese Homegrown Private Automobile: Geely (吉利)

v Geely is one of China’s top ten auto manufacturers and also among the country’s top 500 firms. Over the past ten years, Geely has grown faster than any other company in the Chinese automotive industry.

v Established as an independent firm in 1986, Geely launched its auto manufacturing business in 1997 and is today a fully integrated independent auto firm with a complete auto eco-system from design and research and development to production, distribution and servicing.

v In 2005 Geely Automobile Holdings Limited was listed on the Hong Kong Stock Exchange and is responsible for the majority of Geely’s manufacturing operations.

v Li, shufu(李书福):a crazy man/General Motors(02)

3

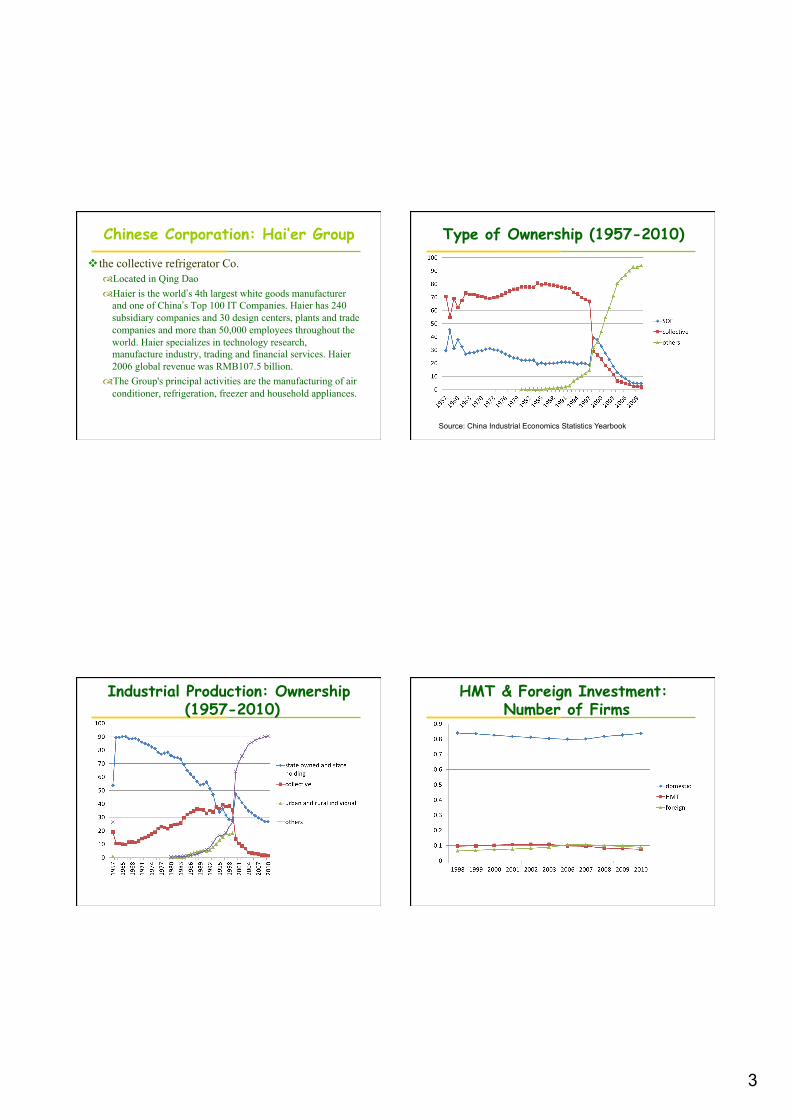

Chinese Corporation: Hai’er Group

v the collective refrigerator Co. � Located in Qing Dao � Haier is the world’s 4th largest white goods manufacturer

and one of China’s Top 100 IT Companies. Haier has 240 subsidiary companies and 30 design centers, plants and trade companies and more than 50,000 employees throughout the world. Haier specializes in technology research, manufacture industry, trading and financial services. Haier 2006 global revenue was RMB107.5 billion.

� The Group's principal activities are the manufacturing of air conditioner, refrigeration, freezer and household appliances.

Type of Ownership (1957-2010)

Source: China Industrial Economics Statistics Yearbook

Industrial Production: Ownership (1957-2010)

HMT & Foreign Investment: Number of Firms

4

HMT & Foreign Investment: Industrial Production 5. Enterprises reforms and privatization

v Enterprises reforms � Price Reform or Enterprise Reform: Debates in

1980s � 1996 SOE Reform and Privatization � Monopoly, Corruption, and Present Large-scale

SOEs v Performance of Industrial Reform v Issues ahead

v Starting point: centralized economy before 1978 � Managements of state owned factories in

command economy of 1950s; � Red guards and “revolutionists” taking over the

management of factories during Cultural Revolutions: 1966-1976;

v Debates in 1980s: Price Reform or Enterprise Reform? � Price reform first, enterprise reform later, both

gradually

5.1.1 Price Reform or Enterprise Reform: Debates in 1980s

Price Reform or Enterprise Reform: Debates in 1980s

v Consensus on Socialism Market Economy? � Goods—commodity economy-socialist market

economy

5

SOEs before 1978: Li (1997)

Decisions on output, price were both controlled by the central govt. during the planned economy. Workers in SOES are taken as holding a iron bowl.

v Incentives and remuneration reforms in 1980s v Delegation of decision making powers v Change of Ownerships v Accounting Practices v Employment v Partial and slow privatization since 1990s v Corporatization of Medium and Large Sized

SOEs

Enterprises reforms after 1978

Li (1997) Incentives and remuneration reforms in 1980s

6

Delegation of decision making powers Development of other enterprises

v Rapid entry and expansion of TVEs in 1980s v Slow development of private enterprises in

1990s v MBOs and ownership transformation of

TVEs in later 1990s v FDIs in 1990s and onwards

Development of other enterprises

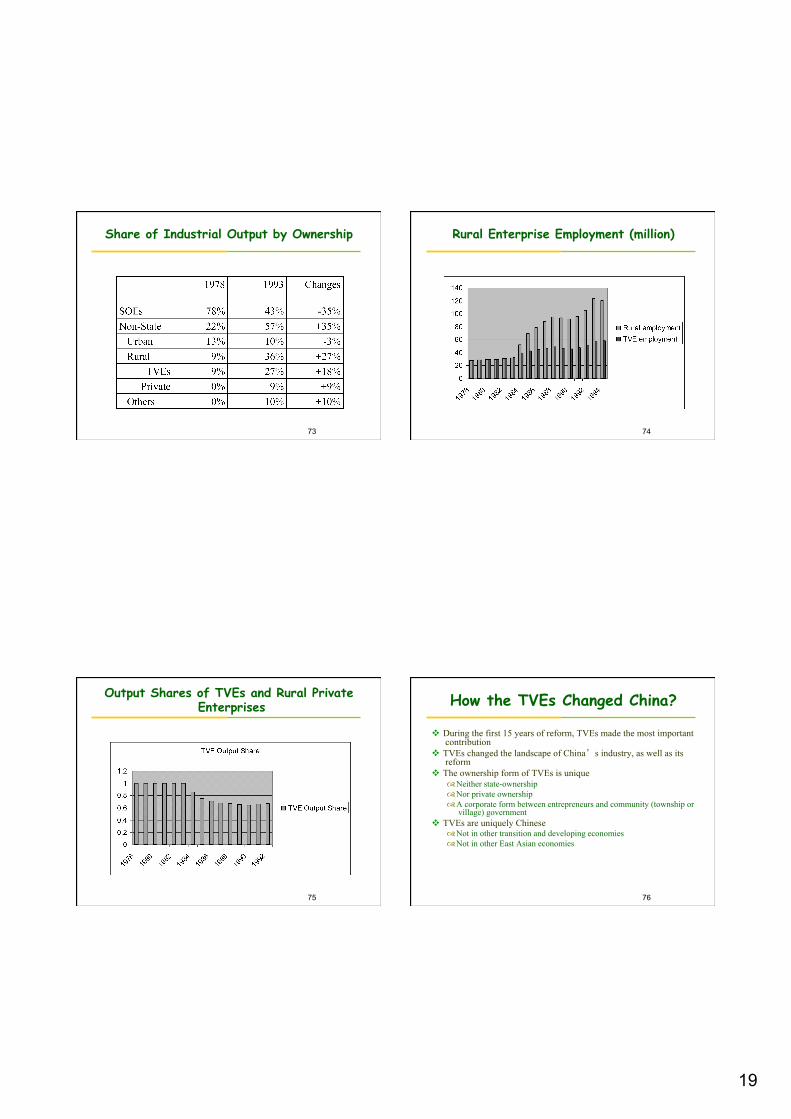

v Until the mid-1990s, the most dramatic method of ownership reform in Chinese industry was the entry of new non-state firms through three avenues. The first is the proliferation of collectives, principally, township and village enterprises (TVEs) during the 1980s.2

v Second, the number of individually owned enterprises (getihu) having eight or fewer employees increased rapidly into the millions by 1994.

v The third source of new entry is foreign investment, from investors in Hong Kong, Taiwan, and Macao (HMT) and from foreign sources (FOR), primarily OECD and Southeast Asian countries.

5.1.2 1996 SOE reform

v “Holding on the Big, Freeing the small” v The Party domination v Diversification of ownership structure and

participation of foreign/private investors

7

1996 SOE reform: Jefferson & Su (2006)

v Under the slogan “retain the large, release the small” (juada fangxiao), China’s leadership mandated the conversion of all but the largest 300 or so of the nation’s industrial SOEs, in principle.

v As part of this initiative, former Premier Zhu Rongji placed China’s loss-making SOEs on a strict three-year schedule during which they were supposed to implement a modern enterprise system and convert losses to surpluses. The principal response to these mandates was a rapid acceleration in the number of conversions across both China’s state and collective sectors.

SOEs & SASAC v China’s state-owned enterprises (SOEs) overseen by the central

government’s State-Owned Assets Supervision and Administration Commission (SASAC) made net profits of RMB 1131.5 billion in 2010 and RMB 400 billion in 2004. All non-financial SOEs, including those administered by provincial and municipal authorities, earned total profits of RMB 759 billion in 2003, representing 6.5 percent of GDP and equivalent to 35 percent of fiscal revenue.

v Some large publicly-listed SOEs pay out 20-60 percent of their earnings in dividends. Yet, for historical reasons, no government entity – neither the Ministry of Finance (MOF) nor SASAC – receives any dividends from large centrally-administered SOEs, a pattern that mostly applies as well to local governments and locally-administered SOEs. This is in contrast to arrangements in other countries, where the state, as key shareholder, normally receives dividends, like other shareholder.

SOEs & SASAC

v Following the establishment of SASACs at the central, provincial, and municipal levels during 2003-04, SOE dividend policy was brought to the government’s reform agenda when the annual working conference of SASACs discussed the issue of a “state assets management budget” in January 2005. Central SASAC Chairman Li Rongrong indicated that his Commission would “work closely with the Ministry of Finance to try to start this reform this year following the strategy set by the State Council”

SOEs & SASAC

v 121 central SOEs (governed by the SASAC) v Financial sectors: banking institutions such as the China Bank are

governed by the CBRC(China Banking Regulatory Commission), insurance institutions are administrated by the CIRC (China Insurance Regulatory Commission)

v Other firms administrated by other govt. departments: � China Post (中国邮政) governed by the Ministry of Finance

• China Post has been a loss-generating enterprise since its independence from telecommunication in 1996

� China Tobacco

8

Privatization: Jefferson & Su (2006)

v Although the shareholding experiment was introduced in 1993, shareholding conversion became a broadbased initiative involving large numbers of both SOEs and COEs only after the restructuring initiatives of 1997 to 1998. In 1997, the Chinese Communist Party’s 15th Party Congress made the shareholding system a centerpiece of China’s enterprise restructuring. While formal privatization was ruled out for ideological reasons, the shareholding experiment was viewed widely as a covert mandate for privatization, as Li et al. (2000) claim.

Ownership distribution

Privatization: Jefferson & Su (2006) v From 1997 to 2001, the number of registered state-owned

enterprises declined by nearly one half. According to Fan (2002), more than 70 percent of small SOEs have been privatized or restructured in some regions during this period. However, conversion of SOEs enterprises was not limited to small-size enterprises. During the period from 1997 to 2001, the number of large and medium-size SOEs declined from 14,811 to 8675, while the number of large and mediumsize shareholding enterprises increased from 1801 to 5659.

v Furthermore, the conversion process extended to collective-owned enterprises, including the township and village enterprise sector that had been celebrated for its competitive performance, e.g., Weitzman and Xu (1994). Li and Rozelle (2000) report that the privatization of rural industry was deep and fundamental and that more than 50 percent of local government-owned firms transferred shares, either partially or completely, to the private sector. This process of conversion has been extensive even among the largest, most successful collective-owned enterprises (COEs). The number of large and mediumsize COEs declined by 35 percent—from 3613 in 1998 to 2465 in 2001.

v Sectoral Change of Industrial Output; v Productivity Improved; v Decline of Profitability; v Collapse of Employment and Social Welfare

System

5.2 Performance of Industrial Reform

9

Growth

Source: World Bank

China’s Real GDP (1960-2010)

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

-通用格式

Real GDP

Billions of 2000 Dollars

Sectoral Composition of GDP Components of GDP in 2010

10

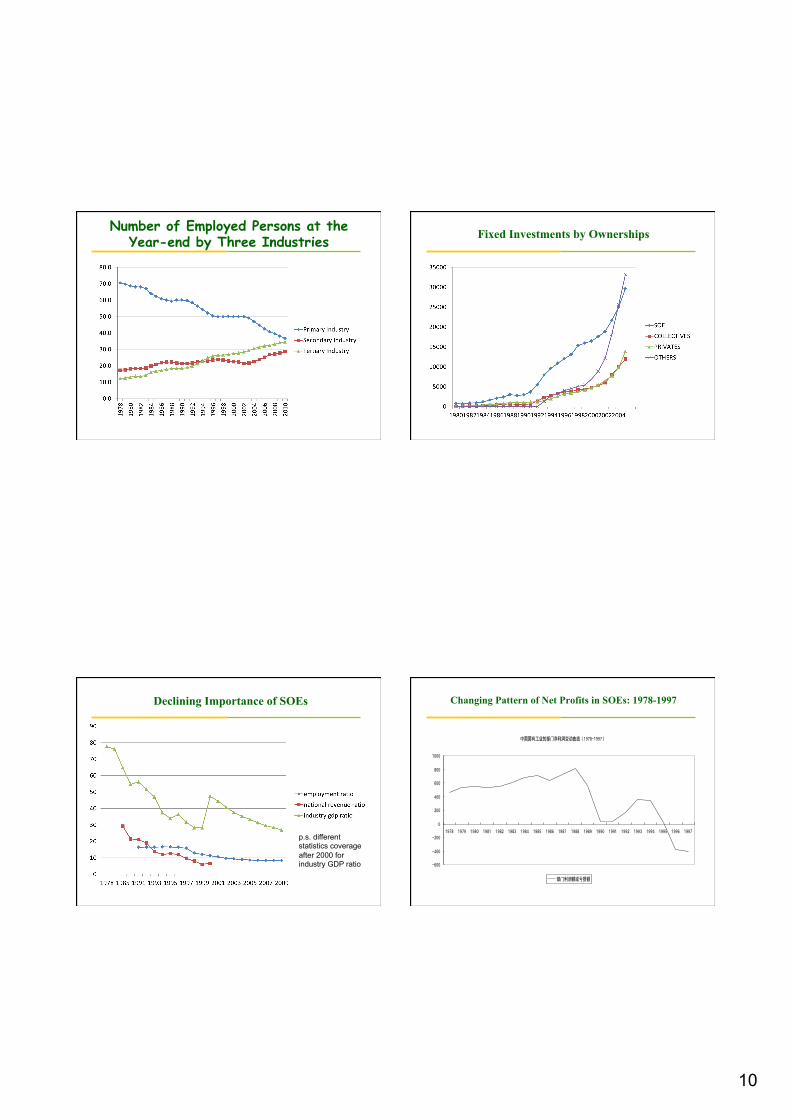

Number of Employed Persons at the Year-end by Three Industries Fixed Investments by Ownerships

Declining Importance of SOEs

p.s. different statistics coverage after 2000 for industry GDP ratio

Changing Pattern of Net Profits in SOEs: 1978-1997

中国国有工业的部门净利润变动曲线(1978-1997)

-600

-400

-200

0

200

400

600

800

1000

1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

部门利润额减亏损额

11

Non-State Industrial Sector in China

v SOEs under reform and restructuring, but slowly.

v Non-state businesses emerge and expand rapidly, taking over the industrial output.

v SOEs lose money and remain afloat under “too big to fail”system.

v Private business was finally encouraged.

Rising Share of Non-State Industrial Sector

0"10"20"30"40"50"60"70"80"

1978

"19

80"

1985

"19

90"

1991

"19

92"

1993

"19

94"

1995

"19

96"

1997

"19

98"

1999

"20

00"

2001

"20

02"

2003

"20

04"

2005

"20

06"

2007

"20

08"

2009

"

collec0ve"and"private"enterprises"employment"ra0o"

Non=SOE"industry"gdp"ra0o"

p.s. different statistics coverage after 2000 for industry GDP ratio

43

Evaluation of SOE reforms: 1978-1993

v Limited success � From improved incentives and autonomy � From increased competition

v Problems � Autonomy is limited – Government intervention continues � Contracts are short term – Incentives are biased toward short run

profits � Contracts are tailor made to each enterprises – negotiation on

contractual terms more important than performance � Firms gain when they make money, but do not lose when they lose

money � Limited ways to punish failure

44

The Problem of the “Soft Budget Constraint” (Janos Kornai)

v The Phenomenon � The government (or banks or other organizations) keeps bailing out

financially troubled firms � A general problem, but especially wide spread in countries like China

v Consequences � Anticipating the relaxed financial discipline, firms behave

opportunistically and irresponsibly � Examples: choose unprofitable projects, take unnecessary risks, divert

funds for own benefits, hire more labor than needed, conduct related party transactions (friends and relatives)

� Why? Because someone else will eventually pay

12

45

The Problem of the “Soft Budget Constraint” (Janos Kornai)

v The reasons for the Soft Budget Constraint � The government’s threat to punish financial failures

(such as let firm go bankrupt) is not “credible” � It means by the time the firm is already in trouble, the

government feels it is in its interests not to let it fail v Why?

� Political objectives (believe in socialist ideology, avoid workers’ riot, need for political support of SOEs)

� Social objectives (avoid unemployment problem) � Economic reasons (bad investment is sunk, by gone is by

gone, good money chases bad money) v All the above are related to public ownership and government

control of firms and financing sources

46

Corporate Governance

v A universal problem in corporations, especially in publicly held corporations � Conflict of interests between managers (corporate

insiders) and investors (outsiders) � Conflict interests among different types of investors: large

shareholders vs. small shareholders, shareholders vs. creditors, private investors vs. institutional investors

v Three sets of laws applied to corporate governance � Company laws governing all firms (state corporate laws

in the U.S.) � Securities laws governing publicly traded firms and

securities firms (federal laws in the U.S.) � Bankruptcy laws governing creditors and debtors

v The central issue: how to make sure managers serve the interests of investors so that investors are willing to invest

47

Special Issues in China

v Governance structure: Co-existence of the new system with the old

v Introducing new institutions for corporate control � The Shareholders’ Meeting � The Board of Directors (Chairman of the Board is CEO) � The Supervisory Board (a la the German system)

v But without dismantling old representative bodies � The Party Committee (the Party Secretary) � The Employee Representative Committee � The Workers’ Union

v The central issue � The principle of “Party controlling personnel” � Managers still have a cadre rank (e.g., vice minister or

minister level manager) 48

Special Issues in China

v The double problem of corporate governance in China � The political interference problem � The agency problem

v The fundamental dilemma � Delegating more control rights to managers provides

them with incentives, but also enables them to plunder state assets

� Maintaining Party control over the selection and dismissal of managers serves to check managerial asset stripping but also lead to political interference

v Some reform measures � Independent directors (up to 1/3 of all board directors) � Regulatory authority of China Securities Regulatory

Commission

13

49

Special Issues in China

v Ownership issues � In traditional SOEs: Government is the sole owner � In most publicly traded firms: Government is the largest

investor

v Reform directions � Diversifying ownership structure by introducing multiple

investors, domestic and foreign � Reducing the proportion of state shares in publicly traded

firms

50

China’s Largest Firms (2006, in sales)

v 1. Sinopec 中石化 v 2. State Grid 国家电网 v 3. CNPC/PetroChina 中石油 v 4. ICBC 工商行 v 5. China Mobile中国移动 v 6. China Life中国人寿 v 7. China Southern Power Grid 中国南方电网 v 8. CCB建行 v 9. China Telecom 中国电信 v 10. Bank of China 中国银行

51

China’s Largest Firms (2006, in sales)

v 1. Sinopec 中石化 v 2. State Grid 国家电网 v 3. CNPC/PetroChina 中石油 v 4. ICBC 工商行 v 5. China Mobile中国移动 v 6. China Life中国人寿 v 7. China Southern Power Grid 中国南方电网 v 8. CCB建行 v 9. China Telecom 中国电信 v 10. Bank of China 中国银行

52

China’s Largest Firms(2006, in sales)

v 11. BaoSteel宝钢 v 12. Sinochem中化 v 13. ABC中国农业银行 v 14. Shanghai Brilliance上海百联集团 v 15. FAW一汽 v 16. China Railway Project, 中国铁路工程 v 17. COFCO 中国粮油食品 v 18. SAIC 上海汽车工业公司 v 19. China Minmetals中国五矿 v 20. China Railway Construction 中国铁路建筑总公司

14

53

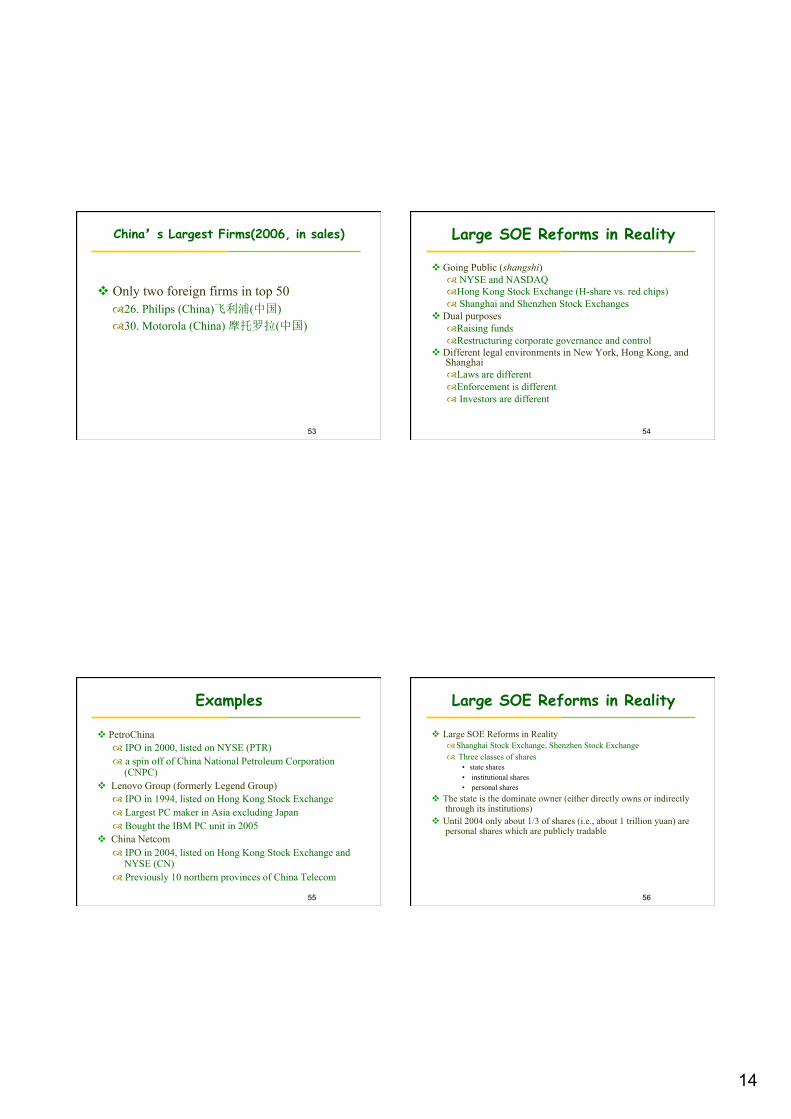

China’s Largest Firms(2006, in sales)

v Only two foreign firms in top 50 � 26. Philips (China)飞利浦(中国) � 30. Motorola (China) 摩托罗拉(中国)

54

Large SOE Reforms in Reality

v Going Public (shangshi) � NYSE and NASDAQ � Hong Kong Stock Exchange (H-share vs. red chips) � Shanghai and Shenzhen Stock Exchanges

v Dual purposes � Raising funds � Restructuring corporate governance and control

v Different legal environments in New York, Hong Kong, and Shanghai � Laws are different � Enforcement is different � Investors are different

55

Examples

v PetroChina � IPO in 2000, listed on NYSE (PTR) � a spin off of China National Petroleum Corporation

(CNPC) v Lenovo Group (formerly Legend Group)

� IPO in 1994, listed on Hong Kong Stock Exchange � Largest PC maker in Asia excluding Japan � Bought the IBM PC unit in 2005

v China Netcom � IPO in 2004, listed on Hong Kong Stock Exchange and

NYSE (CN) � Previously 10 northern provinces of China Telecom

56

Large SOE Reforms in Reality

v Large SOE Reforms in Reality � Shanghai Stock Exchange, Shenzhen Stock Exchange � Three classes of shares

• state shares • institutional shares • personal shares

v The state is the dominate owner (either directly owns or indirectly through its institutions)

v Until 2004 only about 1/3 of shares (i.e., about 1 trillion yuan) are personal shares which are publicly tradable

15

57

Large SOE Reforms in Reality

v Does public listing improve firm performance? � To examine the relationship between ownership structure of publicly

listed companies and their performance v One study found

� Neither state shares nor personal shares help firm performance � But institutional shares help firm performance

v Another study found � Public listing is associated with sharp deterioration of financial

performance of companies � Ownership concentration does not help � A more balanced ownership structure among top shareholders helps

firm performance

5.3 Issues Ahead

v Political rights: � 2 sessions members of 2012 from Chinese A stock

markets represented 22.6% market value of the two markets, about RMB 6400 billion.

� Most of these 2 sessions members (111 NPC members, 55 CPPCC members) are from large central SOEs and local leading corporations.

v SASAC and state ownerships in corporatization of SOEs;

v IPOs (Initial Public Offering) and non-tradable shares;--------Financial markets

v The Party, the director of board, and CEOs; � Share incentive for public listed SOEs ineffective in

China? ----------Xia and Zhang (2008) v Unions and workers’ association of share holding;

Issues Ahead

v Who Benefits? � the recent boom of Chinese outstanding SOEs

has affected the economy in other ways, by delivering most of the benefits of economic growth to state-owned companies in the form of higher profits, with relatively little going into the pockets of ordinary wage-earners. The massive reorganization of the state sector in the late 1990s pushed responsibility for a lot of health and education spending on to families.

SOE Divdidends

v Central State-owned enterprises (SOEs) will hand over 15 percent of their total profits to the State this year - 5 percent more than last year - in a bid to share the benefits provided by the rapid growth of the SOEs with the public. "For those central SOEs with strong competitiveness, the profits turned over to the public finance should be at the same level as that of domestically listed companies, although the proportion will increase to 15 percent this year," said Shao Ning, vice-chairman of the State-owned Assets Supervision and Administration Commission (SASAC), the supervisory body for central SOEs.

v

16

2011 SOE dividend payments

v In 1993, the Chinese government established SOE dividend payment regulations, dividing firms into three groups according to industrial sectors. Enterprises in the tobacco, petroleum, telecommunication, coal development and electricity sectors were required to submit 10% of their dividends to the MoF; military enterprises were exempted from payments; and SOEs in all other sectors were required to submit dividends of 5%.

v Central State-owned enterprises (SOEs) will hand over 15 percent of their total profits to the State this year - 5 percent more than 2010 - in a bid to share the benefits provided by the rapid growth of the SOEs with the public.

Issues Ahead

v Regulation of the large SOEs: � Greater independence is good for corporate

performance, but there are also signs that China's more powerful SOEs are outstretching the ability of the country's regulators to control them.

� It would decrease the efficiency of macroeconomic control.

Regulation of the large SOEs

v The most remarkable incident occurred, when the large state-owned oil companies forced the authorities to raise fuel prices by helping to create an artificial shortage. � The Chinese government sets prices for oil sold

domestically, which puts pressure on the large oil companies – PetroChina, Sinopec and CNOOC – when international prices rise. The response from the large oil companies was a high-stakes game of bluff with the authorities: the amount of oil sold in China was reduced and several large refineries were put on “scheduled maintenance”. When many smaller, private refineries also refused to sell oil at the government-set price, creating an even bigger shortage, the authorities had no option but to increase prices.

Is price control correct? Is there a better way?

Case: Hai Er development.

v Haier's history begins long before the actual founding of the company, in 1920's Qingdao where a refrigerator factory was built to supply the Chinese market. It was taken over by the Chinese Communist Party after 1949 and went into a long decline. By the 1980s, the factory was in debt for over CNY Ґ1.4 million and suffered from dilapidated infrastructure and poor management and quality controls. Production had slowed to a trickle, rarely surpassing 80 refrigerators a month, and the factory was close to bankruptcy.

v In desperation, the Qingdao government turned to a young assistant city-manager, Zhang Ruimin, responsible for a number of city owned appliance companies. Zhang was appointed the managing director of the factory in 1984.

17

Hai Er development.

v Haier was founded as Qingdao Refrigerator Co. in 1984. With China opening up to world markets, foreign corporations began searching for partnerships in China. One of these, Germany's Liebherr Group, entered into an agreement with Qingdao Refrigerator Co., offering technology and equipment to its Chinese counterpart. Refrigerators were to be manufactured under the name of Qingdao-Liebherr.

v Combined with Zhang's disciplined management techniques, which broke from the tradition of the Iron rice bowl in Chinese state-owned enterprises, the company began to turn around. By 1986, Qingdao Refrigerator had returned to profitability and sales growth averaged 83 percent per year. With sales of just CNY Ґ3.5 million in 1984, sales rocketed to CNY Ґ40.5 billion by 2000; a growth of more than 11,500 percent.

Hai Er development.

v With the success of Qingdao's refrigerator company, the municiple government asked it to take over some of the city's other ailing appliance makers. In 1988, the company assumed control of Qingdao Electroplating Company (making microwaves) and in 1991, also took over Qingdao Air Conditioner Plant and Qingdao Freezer.

v Having diversified its product line beyond refrigerators, the company adopted a new name in 1991. Borrowing from the German name of its partner, "Haier" came from the last two syllables of the Chinese transliteration of Liebherr (pronounced "Li-bu-hai-er"). Qingdao Haier Group was further simplified in 1992 to Haier Group, the company's current name.

Hai Er went into US market

v With this success, Haier looked to make further inroads in the North American market by moving into the full-sized refrigerator category. This would bring it into direct competition with established American giants: GE, Whirlpool, Frigidaire, and Maytag; not to mention foreign competitors like LG and Samsung. As part of its strategy, Haier decided to build a production facilty in the United States at Camden, South Carolina, opened in 2000. By 2002, US revenues reached USD $200 million, small when compared to its overall revenue of $7 billion, but Haier set an ambitious sales goal $1 billion and 10 percent of the US refrigerator market. Also in 2002, Haier moved into the Landmark Building in downtown Manhattan. Formerly the headquarters for the Greenwich Bank, the 52,000 square foot building was built in 1924 in the neo-classical style.

v Hai Er reached more than 35 percent of the US small and medium size refrigerator market in 2000.

Hai Er: Ownership Structure

v Although under partial public ownership, Haier is still technically a "collective" company, meaning that it is supposed to be owned by its employees. However, its actual ownership situation is opaque; the employees receive no dividends and do not know how much they own in reality.

v Interference from officials is also a risk for SOE's like Haier. Various levels of government often try to push their ailing companies upon successful ones, often resulting in failure; Haier was once talked into acquiring a pharmaceutical company, even though it had no prior experience or infrastructure in biotechnology.

18

Hai Er: Ownership Structure

v As a government entity, Haier was also officially barred from entering the stock exchange early on. However, the company needed funds for its expansion and therefore sought loopholes to access private equity. In 1993, it listed a subsidiary Qingdao Haier Refrigerator Co. on the Shanghai Stock Exchange, raising CNY Ґ370 million. In 2005, Haier entered the Hong Kong Stock Exchange through a "backdoor listing" by acquiring a controlling stake in a publicly listed joint venture Haier-CCT Holdings Ltd. (SEHK: 1169). Haier is also an index stock of the Dow Jones China 88 Index.

Discussion

v Topic 1: what are the differences between privatization in China and privatization in your country?

v Topic 2: How to establish a better corporate structure for SOEs?

v Topic 3: What can Chinese firms benefit from globalization?

v Topic 4: How do you think about Chinese family corporations?

v Topic 5: Many workers lost their jobs during Chinese SOE reforms, especially after 1996. Exchange your information and opinions please.

71

Ownership Classification

72

Share of Industrial Output by Ownership

19

73

Share of Industrial Output by Ownership

74

Rural Enterprise Employment (million)

75

Output Shares of TVEs and Rural Private Enterprises

76

How the TVEs Changed China?

v During the first 15 years of reform, TVEs made the most important contribution

v TVEs changed the landscape of China’s industry, as well as its reform

v The ownership form of TVEs is unique � Neither state-ownership � Nor private ownership � A corporate form between entrepreneurs and community (township or

village) government v TVEs are uniquely Chinese

� Not in other transition and developing economies � Not in other East Asian economies

20

77

Why TVEs?

v Why is TVE a puzzle? � We usually think government ownership is bad � Reform is to transform government ownership to private

ownership � But TVEs represent a major anomaly: government ownership is

the key to reform success

v Understanding TVEs � Interlinked contract at early stage � Unravels along the way

78

Prior to 1979

v 1958: Communes set up small scale industrial enterprises such as steel mills but short lived

v 1970s: Re-emergence of “Commune-Brigade Enterprises” (CBEs), the predecessor to TVEs

v Annual growth rate: 26% between 1970 and 1976 v By 1978: 49 billion yuan output, of which 39 billion

yuan from industry (9% of national total industrial output)

79

Prior to 1979

v Main motivation: agricultural mechanization drive � Typical business: machine repairing, food

processing � Limits: only to serve agriculture � Grey areas: subcontracting for SOEs in nearby

urban areas (Southern Jiangsu province near Shanghai)

80

The Golden Period: 1979-mid-1990s

v Government Policies: a gradual process from tolerance to encouragement � Lifted restrictions on lines of business (most industrial lines,

not only agricultural supporting industries) � Provided some tax relief (three years tax holidays) � But other supports were limited (e.g., limited credit from state

banks) v The Effects of Agricultural Reform

� Township and Village government focused on rural industry after the household responsibility system

� The success of agriculture reform supplied labor, capital, and market for rural industry growth

21

81

The Golden Period: 1979-mid-1990s

v TVEs at the peak (1992): 52 million employees � Townships

• 48,200 townships • On average 8.2 township enterprises in each township • Total of 400,000 township enterprises with 26 million employees

� Villages • 806,000 villages • On average 1.4 village enterprises in each village • Total of 1.1 million village enterprises with 26 million employees

82

Industrial Subsectoral Composition of TVEs (1985)

83

TVEs vs. Private Firms

v Distinct feature of TVE: Entrepreneurs and Community (Township or Village) Government’s coalition

v What do entrepreneurs contribute? � Ideas � Management skills � Connections (people) � Connections (supplies and marketing)

84

TVEs vs. Private Firms

v What does township and village government contribute? � Political protection � Initial capital investment � Help obtain loans from rural credit cooperatives/banks

• Negotiation • Collateral provision • Loan guarantee

� Selection and rewarding managers • Profit sharing • Leasing

� Connections

22

85

TVEs vs. Private Firms

v What does township and village government benefit? � Use of after tax profits

• Retained profits earmarked for local public expenditure (40%) • Retained profits for reinvestment (60%)

� Private benefits • Cars, banquets, cell phones, offices, hotel rooms, traveling • “corruption”

� Promotion • Not clear

86

Economic Conditions for Rural Industry

v Distortions under central planning created enormous opportunities for rural industry to enter � Very cheap labor in rural areas � High prices for industrial goods due to state monopoly � Persistent shortages, especially in consumer goods � Small scale operation advantage: low overhead, � flexibility

v Early entry is very profitable: average rate of profit on capital was 32%, or 40% if tax revenue also included, in 1978 � Even without state subsidies in input prices and capital

87

Why Privatize TVEs

v Government ownership has costs � Some TVEs were collectives in name (in Wenzhou) � But most TVEs were real collectives

v Changing economic conditions � Markets became more competitive, profit rates declined rapidly � Private firms enter, attracting able entrepreneurs away � When TVEs grew larger, more costly to manage with

government involvement v Changing political conditions

� Private property rights become more secure

88

Patterns of TVE Privatization

v A local government driven process, no national privatization program � Some started in mid-1990s, some started in late 1990s

v Various methods of TVE privatization � Sale (at discount) to managers and employees � Sale to outside domestic investors � Sale to foreign investors � Going public (IPO)

v Various corporate forms after privatization � “stock cooperatives” � Private firms � Joint ventures

23

89

Case 1: Shunde, Guangdong Province

v Fast growing area in Pearl River Delta, 60 miles south of Guangzhou � In late 1980s, account for 1/2 of top 10 TVEs in the country � Big brand names such as Rongsheng refrigerator � Big market shares in consumer electric products (e.g., gas

ranges and electric fans) � Starting 1993, TVEs were privatized

• Some were sold to employees • Some were sold to public • Township governments still maintain some minority shares in

profitable firms

90

Case 2: Wuxi, Jiangsu Province

v Birth place of TVE, in Southern Jiangsu, 80 miles northwest of Shanghai

v All of rural firms are TVEs, no private firms existed v Strong local governments v Late starter of privatization, under pressure from Zhejiang

province competition � 1996: modest privatization, mainly distribution shares to employees � 1999: second round, managers buy shares from employees

v Southern Jiangsu becoming more attractive than Pearl River Delta for Taiwan investment

91

Domestic De Novo Private Firms

v Varieties of private firms: Domestic privatized firms, de novo private firms, and foreign firms

v From rural to urban areas, from local to national or even international

v Takeoff of domestic de novo private firms (start from scratch) in urban areas in mid-1990s

v A class of the new rich: siren laoban (private bosses)

92

Entrepreneurs and Private Firms

v Liu Yonghao, New Hope Group of Sichuan (新希望集团), animal feed

v Hou Weigui, Huawei (华为通讯) of Shenzhen, telecommunication equipment

v Li Shufu, Geely of Zhejiang (吉利汽车), automobile

24

93

Entrepreneurs and Private Firms

v Deng Zhonghan, Vimicro (中星微电子), micro processor

v Li Yanhong, Baidu (百度), search engine v Ma, Yun, Alibaba (阿里巴巴), b2b e

-commerce

94

The Case of Zhejiang Province

v Population 44 million, size of South Korea v The first province where private industry accounts for the majority

of output in late 1990s v Small enterprises employing 82% of workers and producing 79%

of industrial output v Zhejiang is special: the state sector was small to start with for

historical reasons v Lessons from Zhejiang:

� future trend of China � need SOE reform to relax the constraint on private enterprise

development

95

Problems

v Political status v Government regulation

� Registration difficulties � Business line restrictions

v Financing � Hard to get bank loans � Hard to raise funds from the public