Performance Analysis of Gas Burner Using Producer Gas For ...

China’s leading

independent gas

producer

Oil Council – Beijing

September 15, 2015

“18 Years of CBM in China”

www.greendragongas.com

LSE: GDG.LN

This presentation does not constitute an invitation to underwrite, subscribe for, or otherwise acquire or dispose of any shares of Green Dragon Gas Ltd. (the

“Company”) in any jurisdiction. The Company’s shares have not been and will not be registered under the US Securities Act of 1933 (the “Securities Act”) and

may not be offered or sold within the United States absent registration under the Securities Act or an exemption from registration.

The information contained in this presentation is given in good faith but no representation or warranty is made in relation to the accuracy or completeness of the

information, or any oral information provided in connection therewith, or the data it generates and no responsibility, obligation or liability is or will be accepted by

the Company or its affiliates or advisors or by any of their respective officers, employees or agents in relation to it.

This presentation contains certain forward looking statements with respect to the financial condition, results, operations and businesses of the Company. The

statements and forecasts involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. There are a

number of factors that could cause actual results or developments to differ materially from those expressed or implied by these forward looking statements and

forecasts.

Past performance is no guide to future performance and persons needing advice should consult an independent financial advisor.

This presentation and the information contained in it are confidential and should not be distributed, published or reproduced, in whole or in part, or disclosed by

recipients directly or indirectly to any other person.

Disclaimer

2

The Long Unconventional March

contributing to energy independence

3

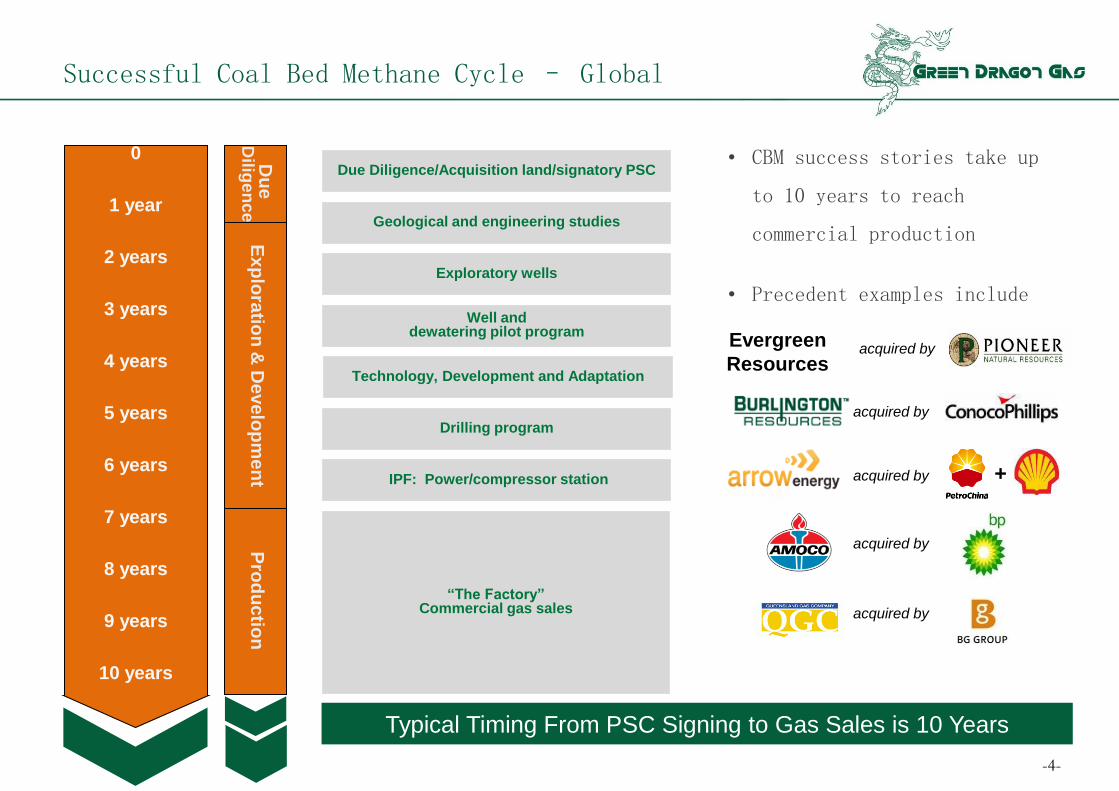

0

1 year

2 years

3 years

4 years

5 years

6 years

7 years

8 years

9 years

10 years

“The Factory” Commercial gas sales

Pro

du

ctio

n

Ex

plo

ratio

n &

De

ve

lop

me

nt

Exploratory wells

Drilling program

IPF: Power/compressor station

Well and dewatering pilot program

Due Diligence/Acquisition land/signatory PSC

Geological and engineering studies

Successful Coal Bed Methane Cycle – Global

-4-

Technology, Development and Adaptation

Typical Timing From PSC Signing to Gas Sales is 10 Years

• CBM success stories take up

to 10 years to reach

commercial production

• Precedent examples include

acquired by

acquired by

acquired by +

acquired by

Evergreen

Resources

acquired by

Du

e

Dilig

en

ce

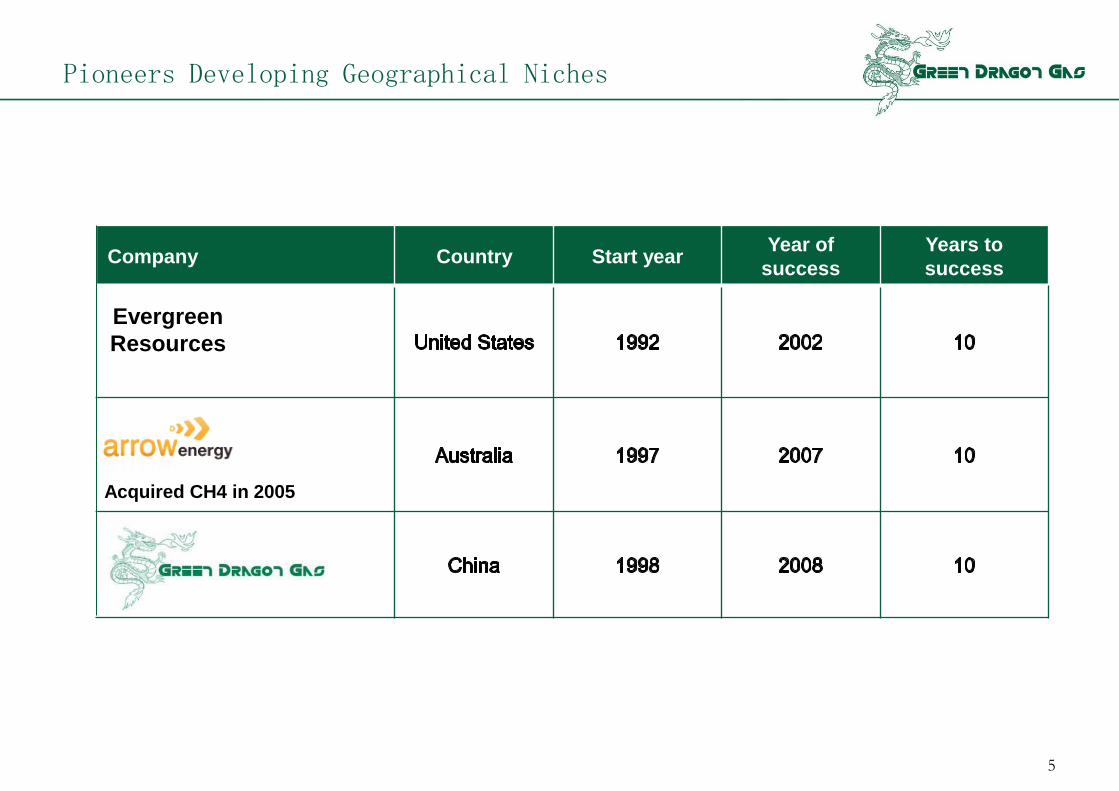

Pioneers Developing Geographical Niches

5

Company Country Start year Year of

success

Years to

success

Evergreen

Resources

Acquired CH4 in 2005

6

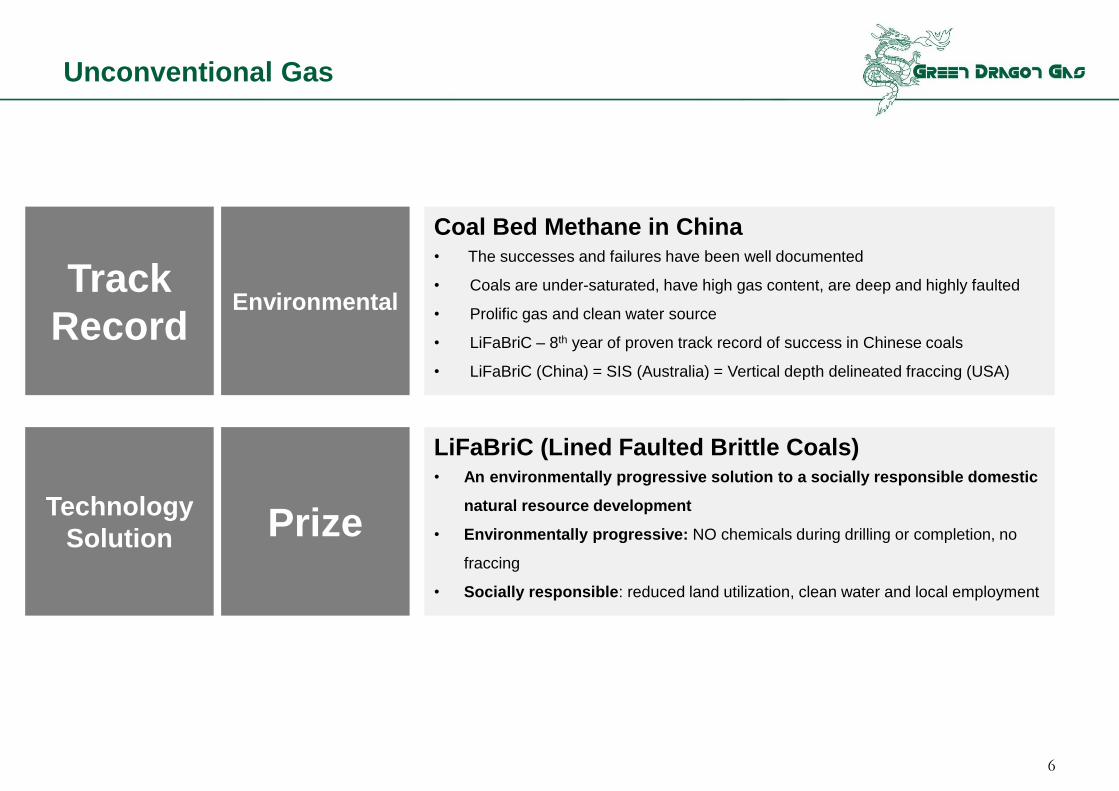

Unconventional Gas

Coal Bed Methane in China • The successes and failures have been well documented

• Coals are under-saturated, have high gas content, are deep and highly faulted

• Prolific gas and clean water source

• LiFaBriC – 8th year of proven track record of success in Chinese coals

• LiFaBriC (China) = SIS (Australia) = Vertical depth delineated fraccing (USA)

LiFaBriC (Lined Faulted Brittle Coals) • An environmentally progressive solution to a socially responsible domestic

natural resource development

• Environmentally progressive: NO chemicals during drilling or completion, no

fraccing

• Socially responsible: reduced land utilization, clean water and local employment

Track

Record Environmental

Prize Technology

Solution

Leading China CBM Independent

Large reserves base • Largest publicly listed CBM reserves base in China: 1P:148Bcf; 2P: 427Bcf; 3P: 2,290Bcf

• Reserves independently verified by 8 consecutive CPRs

• Six Inland Production Sharing Contracts covering 1,869,599 acres (7,566 km² )

• Ongoing migration to 1P reserves: 17% increase at Yearend 2014

Integrated operations and strong partners • Strong, highly capitalised Chinese partners : CUCBM (CNOOC), CNPC and PetroChina

• Proven PSC titles: Protected by Netherlands-PRC Bilateral Investment Treaty

• Equity participation in over 1,800 wells

Centrally located among China’s gas consumers

• Multiple routes to monetise gas: GDG-owned refuelling stations, industrial customers, multiple

gas pipelines, sales via electricity

Experienced leadership and strong corporate profile

• Highly experienced operational management team with a track record in Coal Bed Methane

• High quality shareholder base: includes GIC, Aberdeen, Fidelity, Platinum Asset

Management, Chandler Corp

8 Blocks

$4.3bn 2P Reserves

30 Funded LiFaBriC

commenced

1.9mn acres

Market cap as of Sept 14, 2015 7

History and Corporate Milestones

1997 -1999

2000-2002

Technological

Breakthrough

• MWD (Measurement While Drilling) and LWD (Logging While Drilling) facilitate LiFaBriC development

Public

Floating on AIM

2003

First License

• GDG commences Chinese operations

• First PSC signed on the GFC block

Acquisition of four

additional licenses

• Commenced operations on the ground

• Signing of four other licenses including Shizhuang South

2006

2008

LiFaBriC

2009

Greka Engineering

and Technology

Dividend

2010

Greka Drilling

Dividend

• 8th March demerger of Greka Drilling

• Addition of 2 CNG stations in Pindingshan

• Upgrade of Infrastructure Production Facilities to support 28 new wells of gas production

2011

2012

Landmark

Government Ruling

• Chinese Gov’t rules in favor of Green Dragon on validity of PSC

2013

Binding Agreements

with CNOOC and

PetroChina

2014

Production Ramp-up

• Launch 150 LiFaBriC drilling program

First Gas

• Gas production commences at GSS

• Landmark agreements lead to shareholder participation in over 1,800 wells

• 30th Sept demerger of Greka Engineering

• Zhengzhou Greka Gas Co Ltd entered into a 20-year agreement with PetroChina Huabei Oilfield

• The Company listed on the Alternative Investment Market (“AIM”) in London on August 17, 2006

• “Lined Faulted Brittle Coal”

• improved drainage factor

FTSE 250

8

Upstream Asset Portfolio: 6 PSCs over 8 Blocks

Xinjiang

Tibet

Qinghai

Inner Mongolia

Heilongjiang

Jilin

Liaoning

Beijing

Hebei

ShandongNingxia

Gansu

Shanxi

Shaanxi

Jiangsu

HubeiShanghai

Zhejiang

Fujian

Jiangxi

Guizhou

Sichuan

YunnanGuangxi Guangdong

Hong Kong

Anhui

Hunan

Chongqing

Tianjin

Qinyuan PSC

(GQY PSC)

3,665km2

Baotian-

Qingshan

PSC (GGZ

PSC) 947km2

Fengcheng PSC

(GFC PSC)

1,541km2

Shizhuang South

PSC (GSS PSC)

388km2

Shizhuang

North PSC

(GSN PSC)

375km2

Chengzhuang

Block (GCZ

Block) 67km2

Existing main gas pipelines

CNG mother stations

Group CBM blocks

Capital of province

Henan

Panxie East PSC

(GPX PSC)

584km2

P Production

D Development / Pilot stage

EA Exploration & Appraisal

P

P

D

EA

EA

EA

EA

Both included under ShizhuangSouth PSC

GSS GDG interest: 60%

Partner: CUCBM (CNOOC)

Operator: GDG

1P/2P/3P: 132/372/1,299 bcf

LiFaBriC/vertical wells: 78/183

Total: 1,649 wells*

GCZ GDG interest: 47%

Partner: PetroChina

Operator: PetroChina

1P/2P/3P: 15.6 /28.5/45.3 bcf

LiFaBriC/vertical wells: 0/0

Total: 114 wells*

GSN GDG interest: 50%

Partner: CUCBM (CNOOC)

Operator: CUCBM (CNOOC)

1P/2P/3P: N/A / N/A / 706 Bcf

LiFaBriC/vertical wells: 3/10

Total: 201 wells*

GQY (A) GDG interest: 10%

Partner: CUCBM (CNOOC)

Operator: CUCBM (CNOOC)

1P/2P/3P: N/A

LiFaBriC/vertical wells: N/A / NA

Total: 7 wells*, 18 coal holes

GQY (B) GDG interest: 60%

Partner: CUCBM (CNOOC)

Operator: GDG

2C: 22.8Bcf

LiFaBriC/vertical wells: 14/30

Total: 59 wells*

GFC GDG interest: 49%

Partner: CUCBM (CNOOC)

Operator: GDG

1P/2P/3P: N/A / 27 / 240 Bcf

LiFaBriC/vertical wells: 2/26

Total: 32 wells*

GPX GDG interest: 60%

Partner: CUCBM (CNOOC)

Operator: GDG

1P/2P/3P: N/A

LiFaBriC wells/ vertical wells: 2/10

Total: 14 wells*, 14 coal holes

GGZ GDG interest: 60%

Partner: PetroChina

Operator: GDG

Best Prospective: 443 Bcf

LiFaBriC wells/vertical wells : 5/30

Total: 30 wells*, 30 coal holes

* Total wells is inclusive of non operated wells

Reserves by Netherland, Sewell & Associates, Inc as of December 31, 2014 9

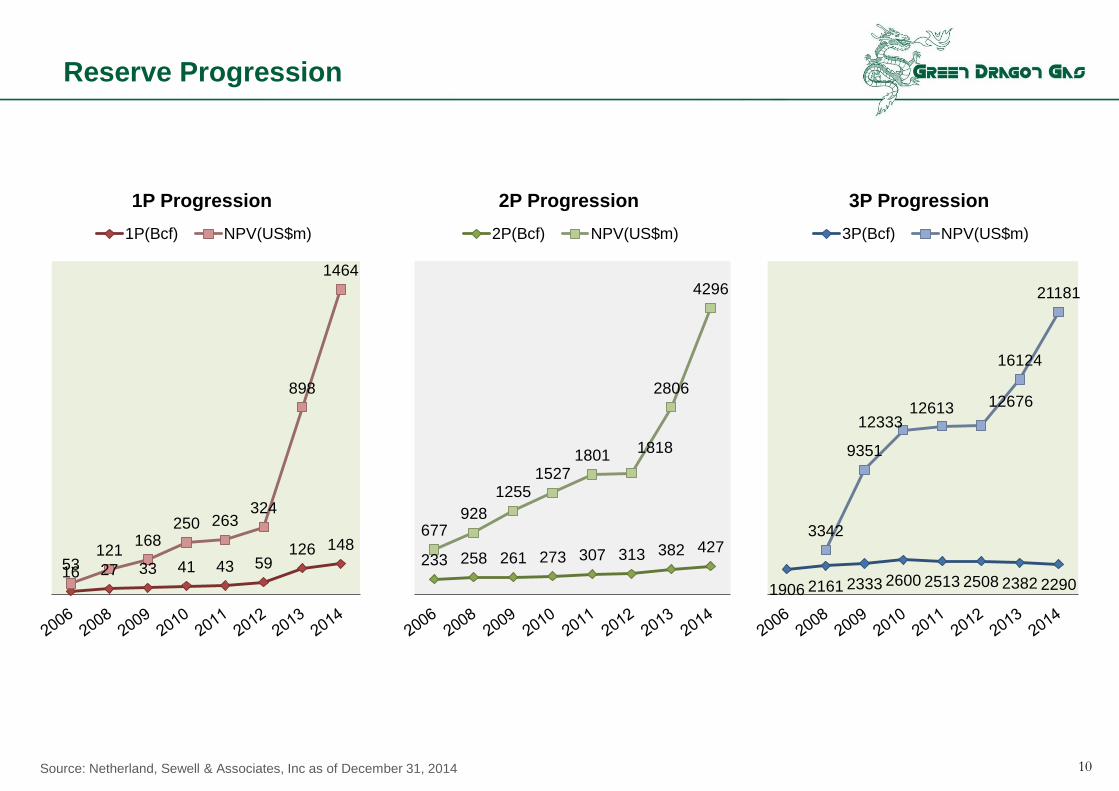

Reserve Progression

16 27 33 41 43 59 126 148

53 121

168 250 263

324

898

1464

1P Progression

1P(Bcf) NPV(US$m)

233 258 261 273 307 313 382 427 677

928

1255 1527

1801 1818

2806

4296

2P Progression

2P(Bcf) NPV(US$m)

1906 2161 2333 2600 2513 2508 2382 2290

3342

9351

12333 12613 12676

16124

21181

3P Progression

3P(Bcf) NPV(US$m)

Source: Netherland, Sewell & Associates, Inc as of December 31, 2014 10

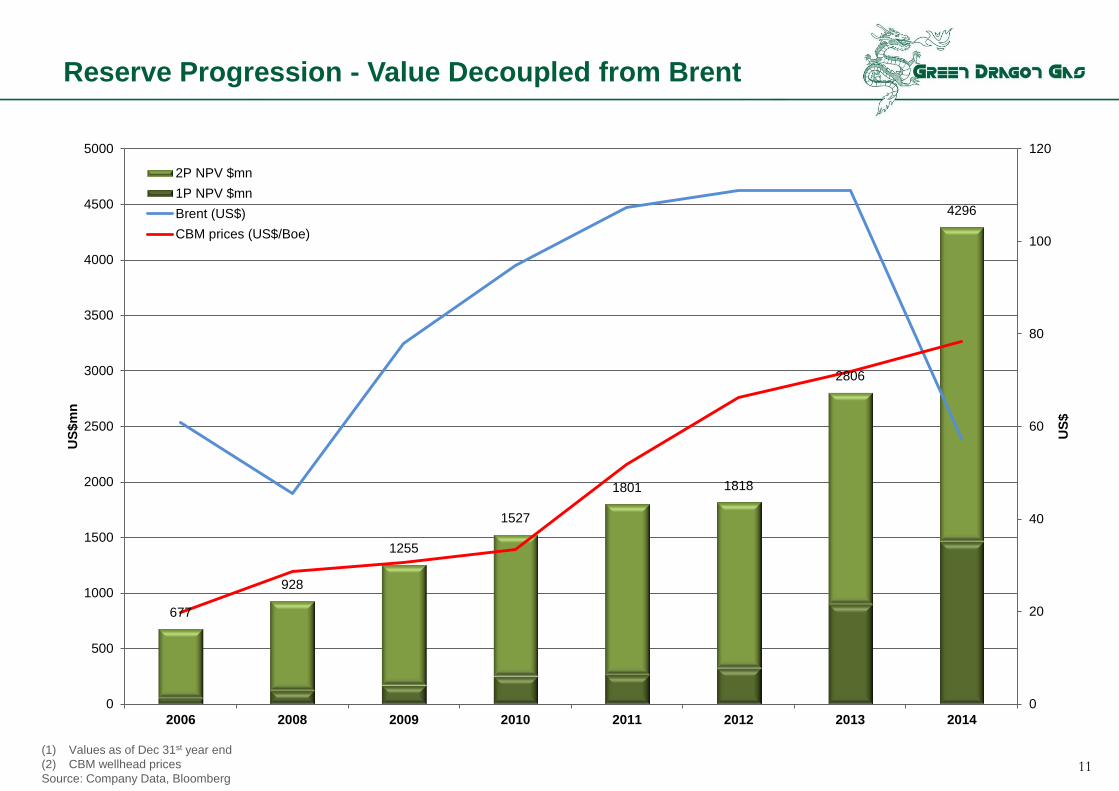

Reserve Progression - Value Decoupled from Brent

11

(1) Values as of Dec 31st year end

(2) CBM wellhead prices

Source: Company Data, Bloomberg

677

928

1255

1527

1801 1818

2806

4296

0

20

40

60

80

100

120

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2006 2008 2009 2010 2011 2012 2013 2014

US

$

US

$m

n

2P NPV $mn

1P NPV $mn

Brent (US$)

CBM prices (US$/Boe)

GSS Evolution to Commerciality

Source: Company data as of June 30, 2015 12

0

100

200

300

400

500

600

700

800

900

0

5,000

10,000

15,000

20,000

25,000Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Gro

ss

Pro

du

cti

on

(M

MC

F)

PV

10

(U

S$

) N

SA

I A

ud

it

GSS Production (MMCF)

3P PV10

2P PV10

Production

Phase

Vertical

Eureka

R&D Phase

LiFaBriC (Lined Faulted Brittle Coals)

SRHD (short radius horizontal drilling)

MLHD (multilateral horizontal drilling)

Cooperation

Phase

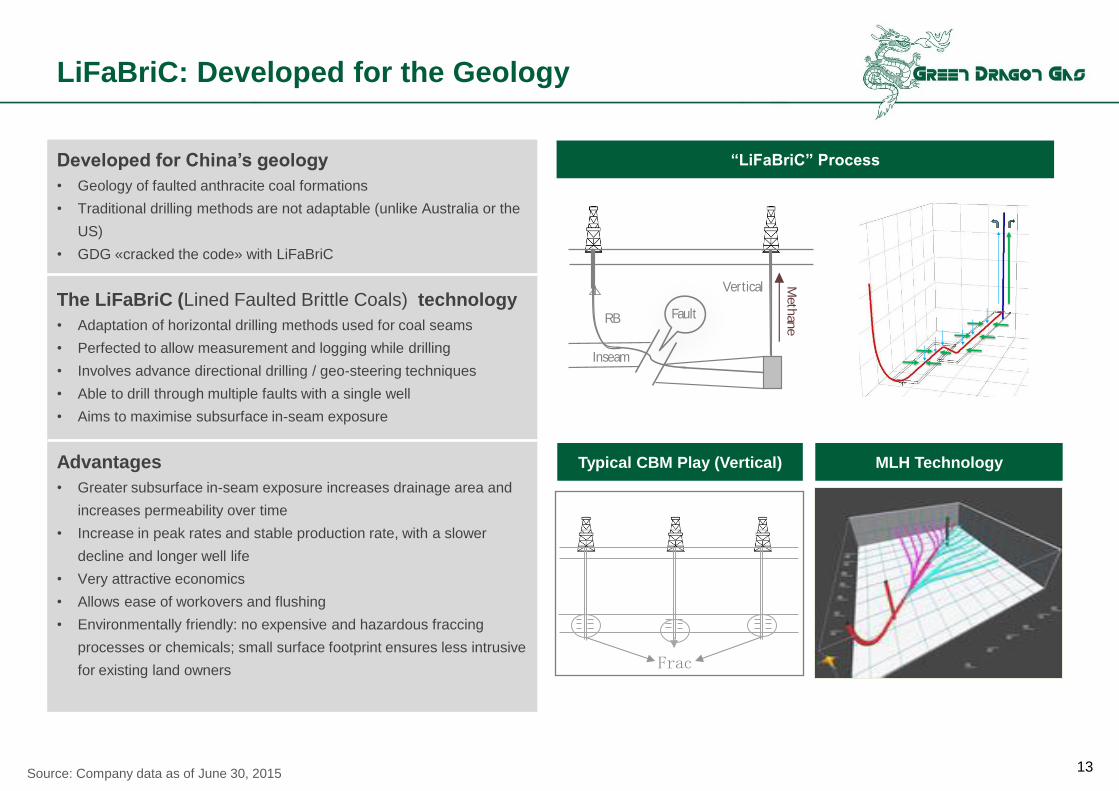

LiFaBriC: Developed for the Geology

Developed for China’s geology

• Geology of faulted anthracite coal formations

• Traditional drilling methods are not adaptable (unlike Australia or the

US)

• GDG «cracked the code» with LiFaBriC

The LiFaBriC (Lined Faulted Brittle Coals) technology

• Adaptation of horizontal drilling methods used for coal seams

• Perfected to allow measurement and logging while drilling

• Involves advance directional drilling / geo-steering techniques

• Able to drill through multiple faults with a single well

• Aims to maximise subsurface in-seam exposure

Advantages

• Greater subsurface in-seam exposure increases drainage area and

increases permeability over time

• Increase in peak rates and stable production rate, with a slower

decline and longer well life

• Very attractive economics

• Allows ease of workovers and flushing

• Environmentally friendly: no expensive and hazardous fraccing

processes or chemicals; small surface footprint ensures less intrusive

for existing land owners

Meth

ane

Inseam

RB

Vertical

Fault

SIS Technology “LiFaBriC” Process

13 Source: Company data as of June 30, 2015

Typical CBM Play

Frac

Typical CBM Play (Vertical) MLH Technology

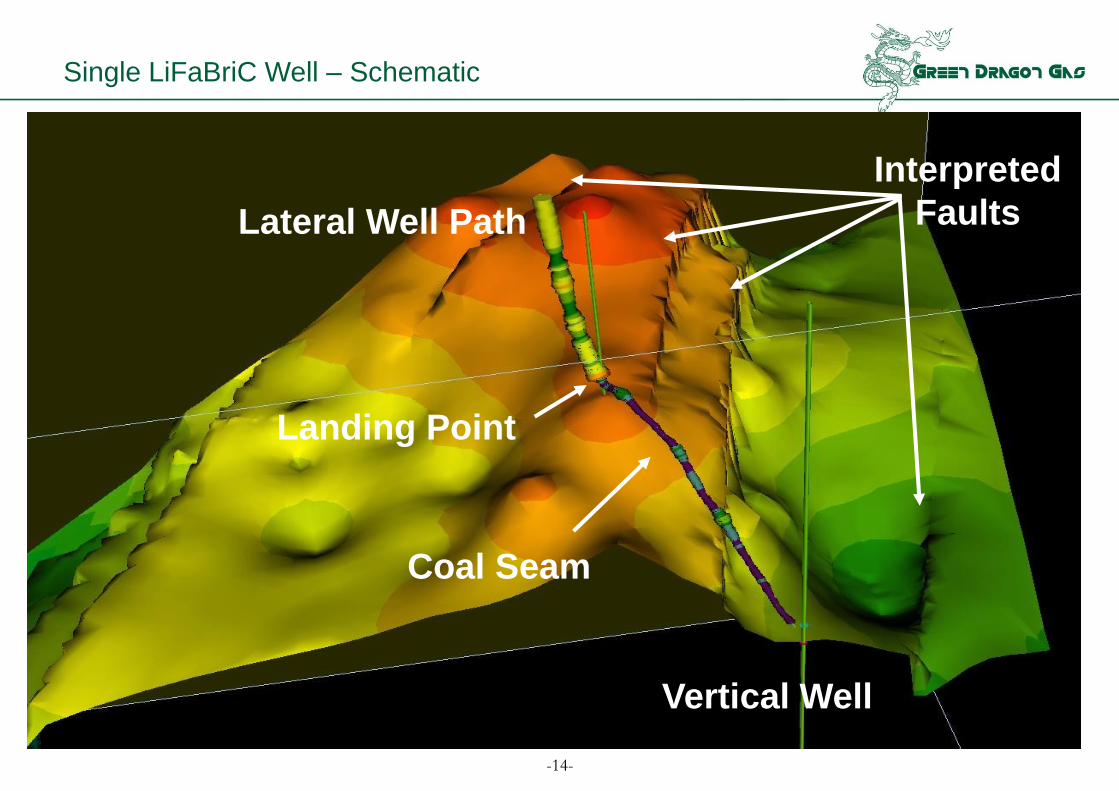

Vertical Well

Lateral Well Path

Landing Point

Coal Seam

Interpreted

Faults

Single LiFaBriC Well – Schematic

-14-

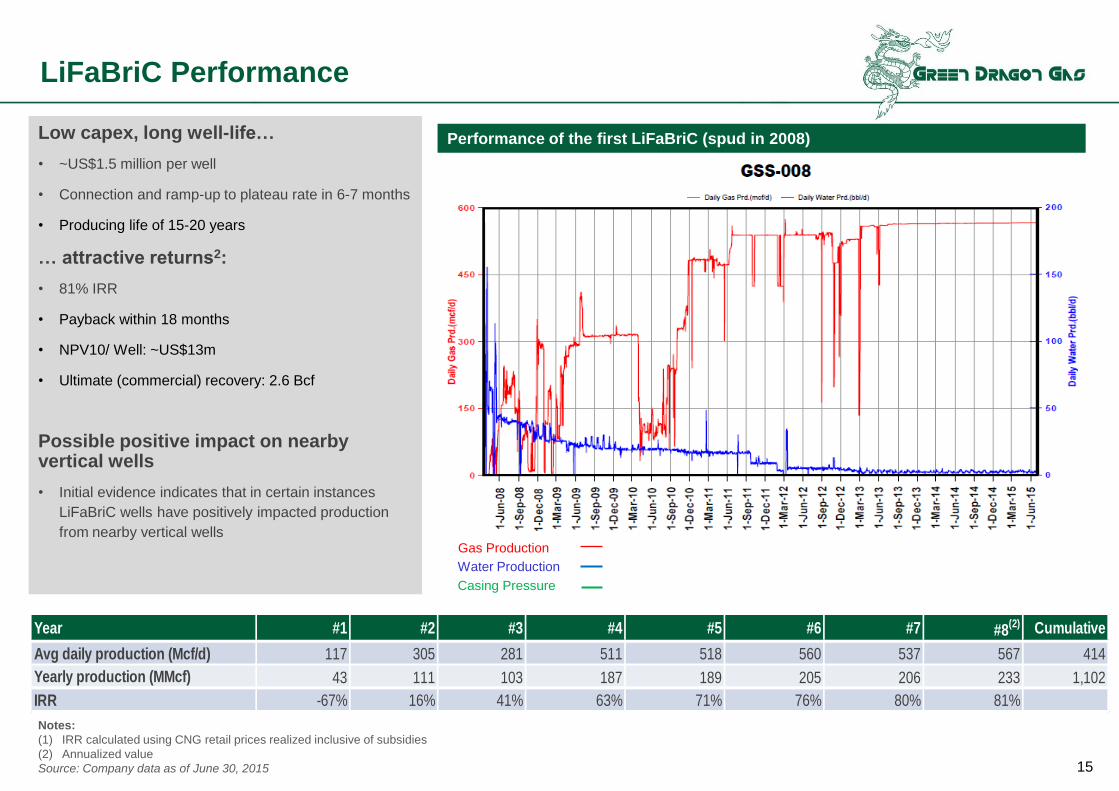

LiFaBriC Performance

Notes:

(1) IRR calculated using CNG retail prices realized inclusive of subsidies

(2) Annualized value

Source: Company data as of June 30, 2015

Low capex, long well-life…

• ~US$1.5 million per well

• Connection and ramp-up to plateau rate in 6-7 months

• Producing life of 15-20 years

… attractive returns2:

• 81% IRR

• Payback within 18 months

• NPV10/ Well: ~US$13m

• Ultimate (commercial) recovery: 2.6 Bcf

Possible positive impact on nearby vertical wells

• Initial evidence indicates that in certain instances

LiFaBriC wells have positively impacted production

from nearby vertical wells

Gas Production

Water Production

Casing Pressure

Performance of the first LiFaBriC (spud in 2008)

15

Year #1 #2 #3 #4 #5 #6 #7 #8(2) Cumulative

Avg daily production (Mcf/d) 117 305 281 511 518 560 537 567 414

Yearly production (MMcf) 43 111 103 187 189 205 206 233 1,102

IRR -67% 16% 41% 63% 71% 76% 80% 81%

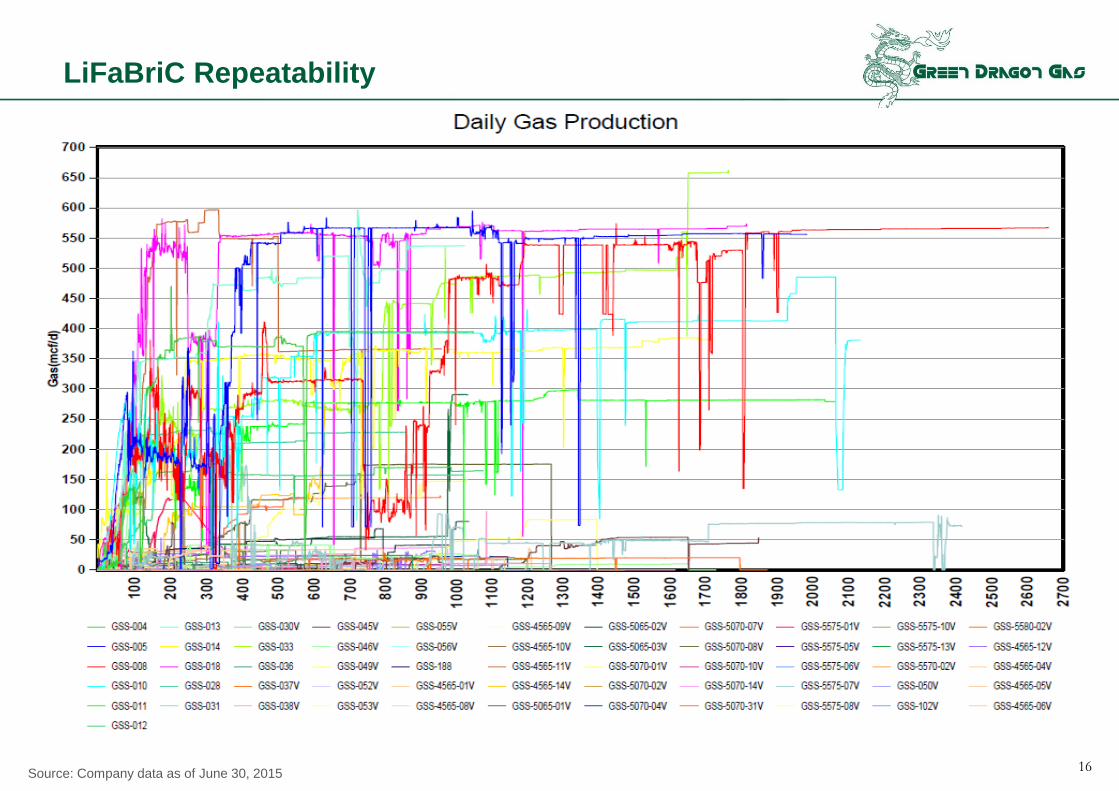

LiFaBriC Repeatability

Source: Company data as of June 30, 2015

Daily Gas Production

16

Corporate Social Responsibility

Commitment to the Environment

• Zero use of harmful chemicals

• Wells powered by clean burning Natural Gas

• Clean water as a by product of production for irrigation

or consumption

• Use of biodegradable mud

• No recorded environmental incidents

Commitment to the communities we operate

• Drilling of water wells for local villages

• Maintenance of local infrastructure

Commitment to our people

• 156,904 OH&S incident free man hours as of Q2 2015

• In depth HSE policy and continuous training

17

Energy consumption per person

(million people) Growth rate (%) (energy consumption per person – toe) (gas consumption per person - toe)

Supportive Chinese market dynamics

• Largest population in the world

• One of the highest GDP growth rates (2014: 7.3%; projected 7% p.a. to 2020)

• Currently very low energy consumption per capita – projected to increase with a rising middle class

• Extremely low proportion of gas in the energy mix – expected to grow to 10% by 2020E with strong support from the government

Population 2014A GDP growth rate

China - Solid Fundamentals for Gas Demand Growth

Source: BP Statistical Review, June 2015; IMF World Economic Outlook Database, April 2015

Gas consumption per person

64

127

143

198

316

1243

1361

0 500 1000 1500

U.K

Japan

Russia

Brazil

U.S.A

India

China

18

0.5

1.5

2.2

2.9

3.6

4.7

7.2

- 2.0 4.0 6.0 8.0

India

Brazil

China

U.K

Japan

Russia

USA

0.04

0.11

0.17

0.80

1.02

2.12

2.59

- 1.00 2.00 3.00

India

China

Brazil

Japan

U.K

U.S.A

Russia

0%

1%

2%

3%

3%

7%

7%

0% 2% 4% 6% 8%

Brazil

Russia

U.S.A

Japan

U.K

India

China

N atural Gas4%

Crude Oil19%

Coal68%

Hydro9%

N atural Gas10%

Crude Oil13%

Coal62%

Hydro & Nuclear

9%

Wind, Solar,

Biomas6%

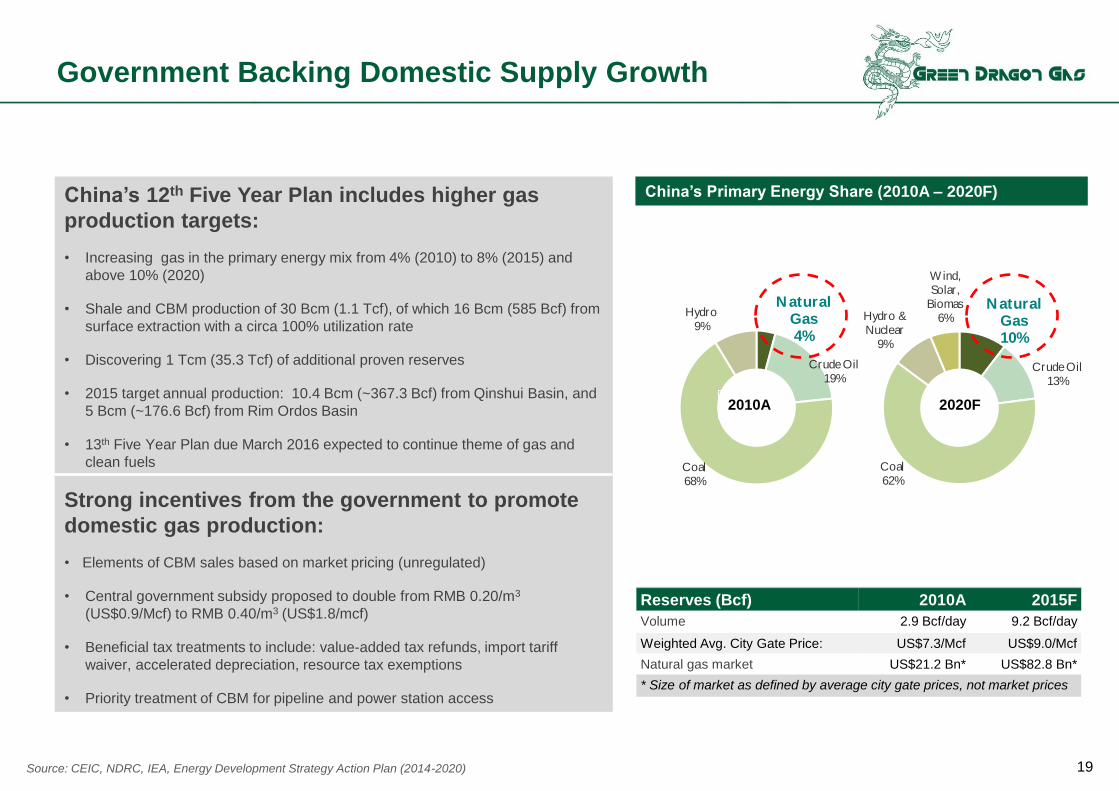

Government Backing Domestic Supply Growth

China’s 12th Five Year Plan includes higher gas

production targets:

• Increasing gas in the primary energy mix from 4% (2010) to 8% (2015) and

above 10% (2020)

• Shale and CBM production of 30 Bcm (1.1 Tcf), of which 16 Bcm (585 Bcf) from

surface extraction with a circa 100% utilization rate

• Discovering 1 Tcm (35.3 Tcf) of additional proven reserves

• 2015 target annual production: 10.4 Bcm (~367.3 Bcf) from Qinshui Basin, and

5 Bcm (~176.6 Bcf) from Rim Ordos Basin

• 13th Five Year Plan due March 2016 expected to continue theme of gas and

clean fuels

Strong incentives from the government to promote

domestic gas production:

• Elements of CBM sales based on market pricing (unregulated)

• Central government subsidy proposed to double from RMB 0.20/m3

(US$0.9/Mcf) to RMB 0.40/m3 (US$1.8/mcf)

• Beneficial tax treatments to include: value-added tax refunds, import tariff

waiver, accelerated depreciation, resource tax exemptions

• Priority treatment of CBM for pipeline and power station access

China’s Primary Energy Share (2010A – 2020F)

2010A 2020F

Source: CEIC, NDRC, IEA, Energy Development Strategy Action Plan (2014-2020)

Reserves (Bcf) 2010A 2015F

Volume 2.9 Bcf/day 9.2 Bcf/day

Weighted Avg. City Gate Price: US$7.3/Mcf US$9.0/Mcf

Natural gas market US$21.2 Bn* US$82.8 Bn*

* Size of market as defined by average city gate prices, not market prices

19

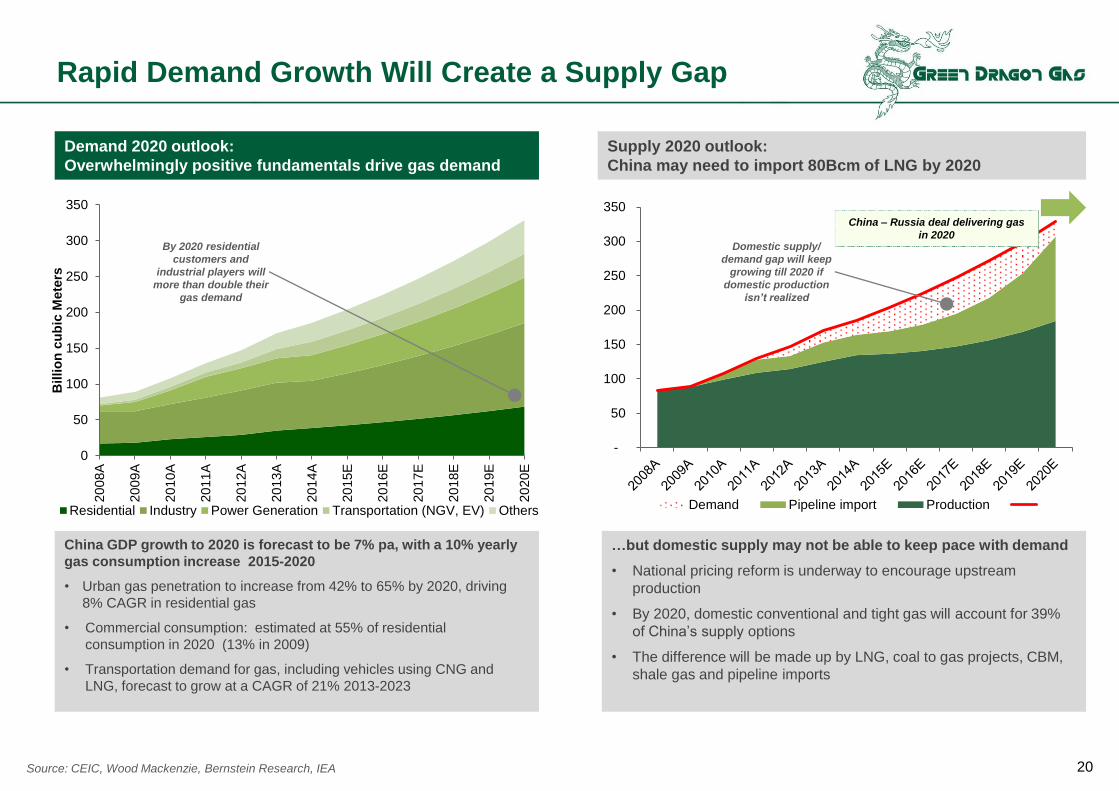

-

50

100

150

200

250

300

350

Demand Pipeline import Production

0

50

100

150

200

250

300

350

20

08A

20

09A

20

10A

20

11A

20

12A

20

13A

20

14A

20

15E

20

16E

20

17E

20

18E

20

19E

20

20E

Billio

n c

ub

ic M

ete

rs

Residential Industry Power Generation Transportation (NGV, EV) Others

Rapid Demand Growth Will Create a Supply Gap

Demand 2020 outlook:

Overwhelmingly positive fundamentals drive gas demand

Supply 2020 outlook:

China may need to import 80Bcm of LNG by 2020

China GDP growth to 2020 is forecast to be 7% pa, with a 10% yearly

gas consumption increase 2015-2020

• Urban gas penetration to increase from 42% to 65% by 2020, driving

8% CAGR in residential gas

• Commercial consumption: estimated at 55% of residential

consumption in 2020 (13% in 2009)

• Transportation demand for gas, including vehicles using CNG and

LNG, forecast to grow at a CAGR of 21% 2013-2023

…but domestic supply may not be able to keep pace with demand

• National pricing reform is underway to encourage upstream

production

• By 2020, domestic conventional and tight gas will account for 39%

of China’s supply options

• The difference will be made up by LNG, coal to gas projects, CBM,

shale gas and pipeline imports

Domestic supply/

demand gap will keep

growing till 2020 if

domestic production

isn’t realized

China – Russia deal delivering gas

in 2020 By 2020 residential

customers and

industrial players will

more than double their

gas demand

Source: CEIC, Wood Mackenzie, Bernstein Research, IEA 20

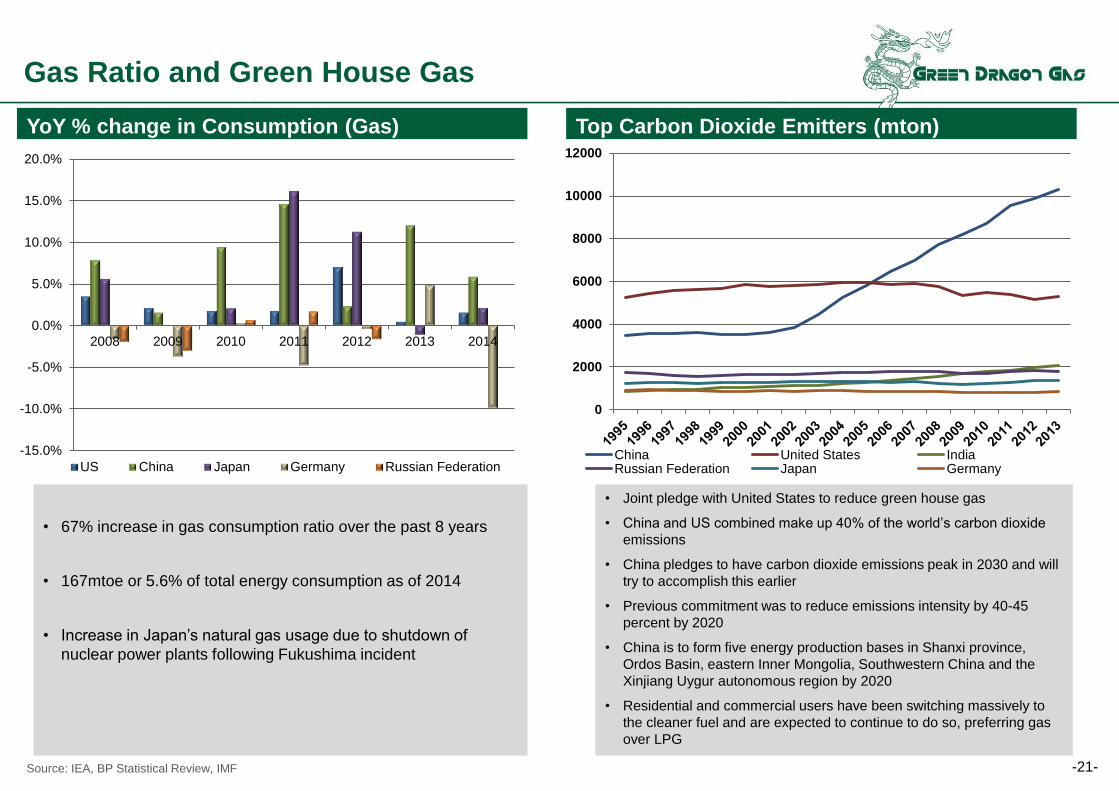

-21-

Top Carbon Dioxide Emitters (mton)

0

2000

4000

6000

8000

10000

12000

China United States IndiaRussian Federation Japan Germany

• Joint pledge with United States to reduce green house gas

• China and US combined make up 40% of the world’s carbon dioxide

emissions

• China pledges to have carbon dioxide emissions peak in 2030 and will

try to accomplish this earlier

• Previous commitment was to reduce emissions intensity by 40-45

percent by 2020

• China is to form five energy production bases in Shanxi province,

Ordos Basin, eastern Inner Mongolia, Southwestern China and the

Xinjiang Uygur autonomous region by 2020

• Residential and commercial users have been switching massively to

the cleaner fuel and are expected to continue to do so, preferring gas

over LPG

Source: IEA, BP Statistical Review, IMF

Gas Ratio and Green House Gas

YoY % change in Consumption (Gas)

• 67% increase in gas consumption ratio over the past 8 years

• 167mtoe or 5.6% of total energy consumption as of 2014

• Increase in Japan’s natural gas usage due to shutdown of

nuclear power plants following Fukushima incident

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

2008 2009 2010 2011 2012 2013 2014

US China Japan Germany Russian Federation

22

What’s Next?

• Monetize the 18 year track record, inclusive of the decade long technology development

• Government policy and pricing has been stable and consistent for the last 18 years and is expected to be

going forward

• The Government provided subsidy is a recognition of the challenges faced in CBM development

• The Government has clearly defined goals for the domestic gas consumption

• Resources must be imported if domestic production lags behind objectives

• While CBM can’t provide all the needed domestic gas demand, it certainly is a vital domestic component of

the solution alongside conventional gas

Energy Independence

Innovate

Transparent

Support

Entrepreneurial

Cooperate

Invest

23

Chinese Independents

Source: Company presentation 24

Global CBM Resources