China’s Iron and Steel Industry Faces Harsh Winter: A Look at the Current Situation and Future

13

0 Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda SPEEDA Research Institute provides insights and independent analysis given by our in-house analysts. This report will focus on the Chinese iron and steel industry and its perspective. China the Global Leader in Crude Steel Production According to the World Steel Association, the global output of crude steel was 1.662 billion tonnes in 2014, up 1.2% YoY. By region, China ranked top amongst all nations, growing 0.9% YoY to 820 million tonnes that year. It was followed by Japan at 110 million tonnes, and the USA, India, and South Korea in descending order. Crude Steel Output Rank (FY2014) Rank Country/Region Continent Crude Steel Output (100 million tonnes) 1 China Asia 8.2 2 Japan Asia 1.1 3 USA The Americas 0.9 4 India Asia 0.9 5 South Korea Asia 0.7 6 Russia Europe 0.7 7 Germany Europe 0.4 8 Turkey Europe 0.3 9 Brazil The Americas 0.3 10 Ukraine Europe 0.3 Source: World Steel Association

-

Upload

kyna-tsai -

Category

Economy & Finance

-

view

173 -

download

0

Transcript of China’s Iron and Steel Industry Faces Harsh Winter: A Look at the Current Situation and Future

0

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

SPEEDA Research Institute provides insights and independent analysis given by

our in-house analysts. This report will focus on the Chinese iron and steel

industry and its perspective.

China the Global Leader in Crude Steel

Production

According to the World Steel Association, the global output of crude steel was

1.662 billion tonnes in 2014, up 1.2% YoY. By region, China ranked top amongst

all nations, growing 0.9% YoY to 820 million tonnes that year. It was followed by

Japan at 110 million tonnes, and the USA, India, and South Korea in descending

order.

Crude Steel Output Rank (FY2014)

Rank Country/Region Continent Crude Steel Output (100 million tonnes)

1 China Asia 8.2

2 Japan Asia 1.1

3 USA The Americas 0.9

4 India Asia 0.9

5 South Korea Asia 0.7

6 Russia Europe 0.7

7 Germany Europe 0.4

8 Turkey Europe 0.3

9 Brazil The Americas 0.3

10 Ukraine Europe 0.3 Source: World Steel Association

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

1

Crude Steel Output by Region (1.7 billion tonnes; FY2014)

Percentage

China 50%

Others 20%

Japan 7%

USA 5%

India 5%

South Korea 4%

Russia 4%

Germany 3%

Brazil 2%

Source: World Steel Association

China’s per Capita Consumption Equal to Japan’s

Looking at the regional crude steel apparent consumption (production + import -

export) per capita, China stood at 510 kg per person in 2014, recording a CAGR

of approximately 7% over the period of 2007–2014. This figure surpassed that of

the USA and Germany, which are major industrial countries. South Korea was

the champion, with the apparent consumption per capita standing at 1,118 kg.

This is mainly attributable to the fact that South Korea has the highest per capita

automobile production volume in the world, which is reported to be 0.09 units

as per various disclosed materials, outperforming China (0.02 units) and the USA

(0.03 units) significantly.

Source: World Steel Association

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

2

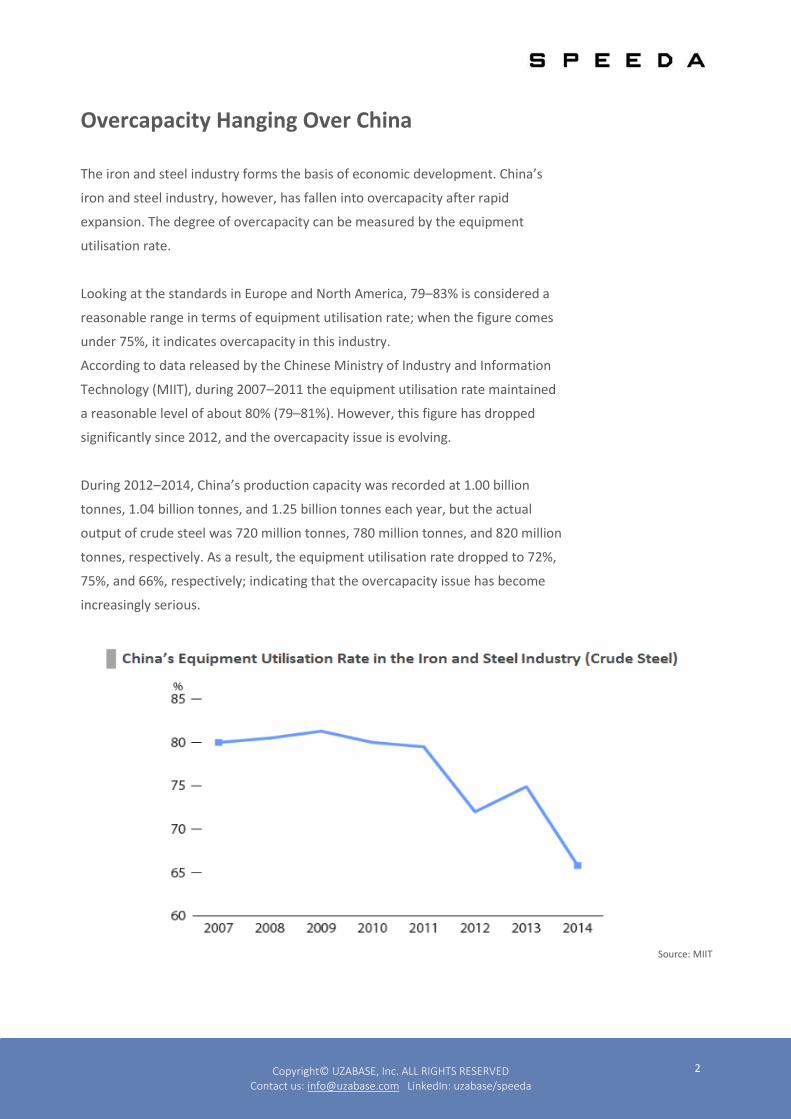

Overcapacity Hanging Over China

The iron and steel industry forms the basis of economic development. China’s

iron and steel industry, however, has fallen into overcapacity after rapid

expansion. The degree of overcapacity can be measured by the equipment

utilisation rate.

Looking at the standards in Europe and North America, 79–83% is considered a

reasonable range in terms of equipment utilisation rate; when the figure comes

under 75%, it indicates overcapacity in this industry.

According to data released by the Chinese Ministry of Industry and Information

Technology (MIIT), during 2007–2011 the equipment utilisation rate maintained

a reasonable level of about 80% (79–81%). However, this figure has dropped

significantly since 2012, and the overcapacity issue is evolving.

During 2012–2014, China’s production capacity was recorded at 1.00 billion

tonnes, 1.04 billion tonnes, and 1.25 billion tonnes each year, but the actual

output of crude steel was 720 million tonnes, 780 million tonnes, and 820 million

tonnes, respectively. As a result, the equipment utilisation rate dropped to 72%,

75%, and 66%, respectively; indicating that the overcapacity issue has become

increasingly serious.

Source: MIIT

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

3

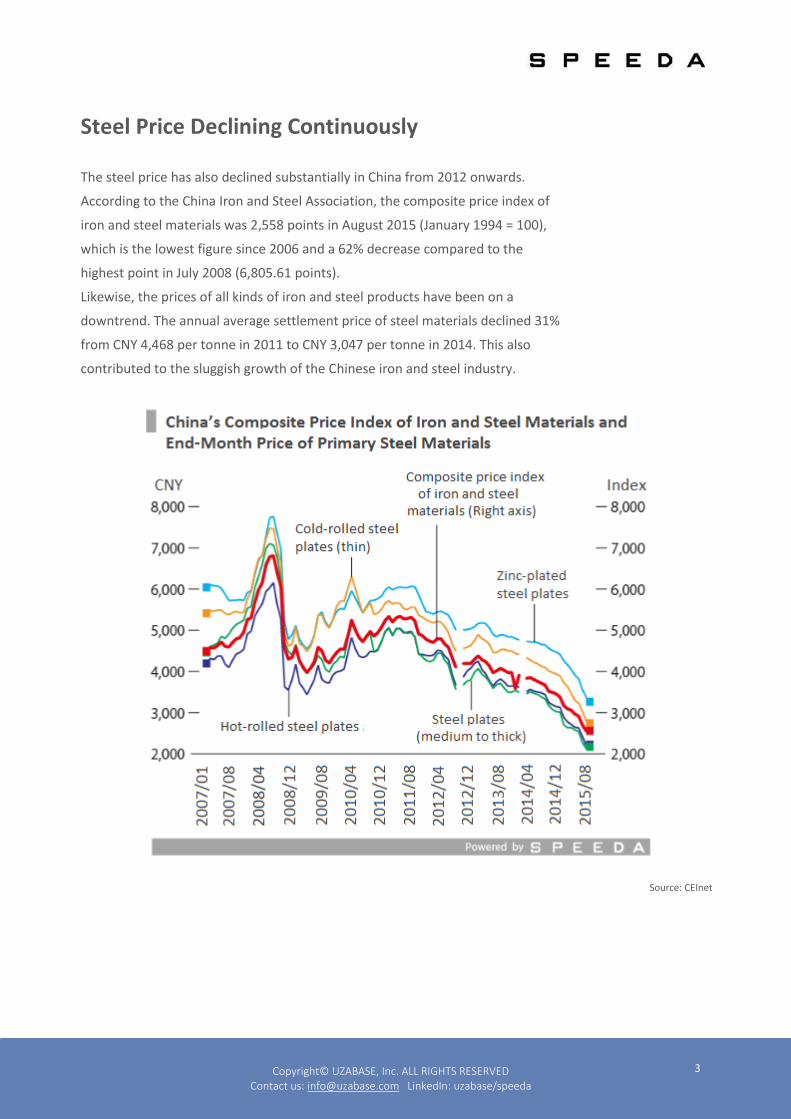

Steel Price Declining Continuously

The steel price has also declined substantially in China from 2012 onwards.

According to the China Iron and Steel Association, the composite price index of

iron and steel materials was 2,558 points in August 2015 (January 1994 = 100),

which is the lowest figure since 2006 and a 62% decrease compared to the

highest point in July 2008 (6,805.61 points).

Likewise, the prices of all kinds of iron and steel products have been on a

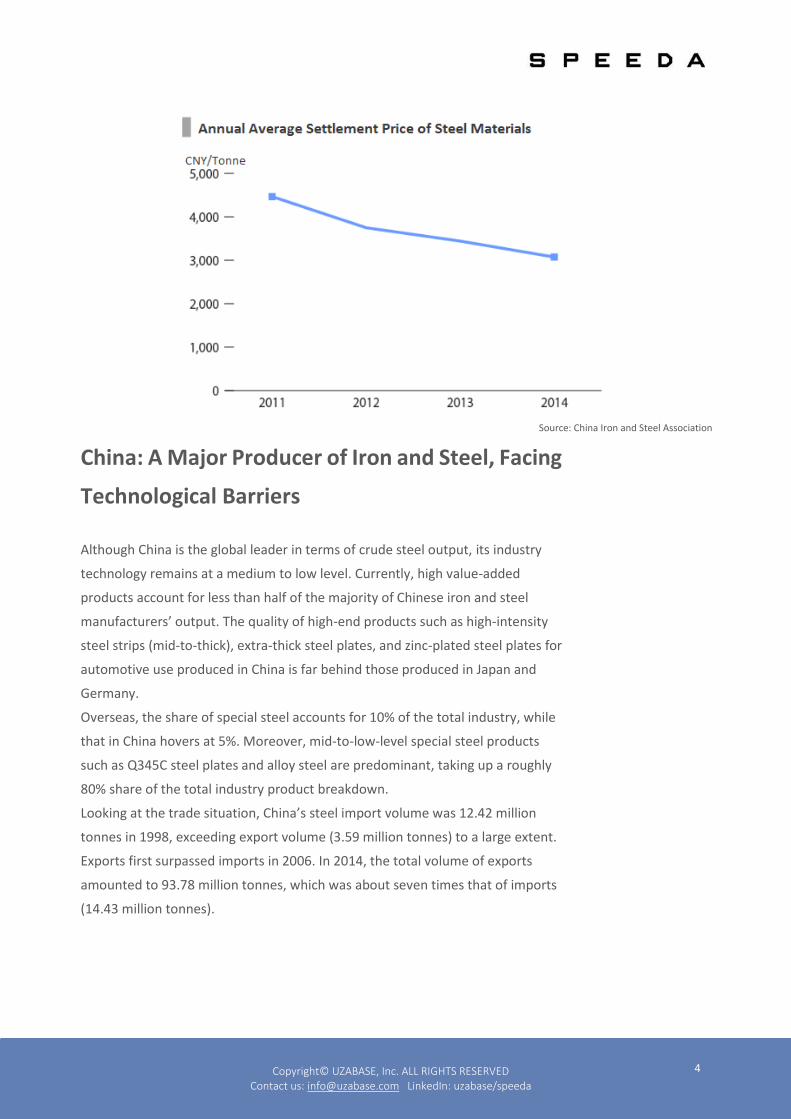

downtrend. The annual average settlement price of steel materials declined 31%

from CNY 4,468 per tonne in 2011 to CNY 3,047 per tonne in 2014. This also

contributed to the sluggish growth of the Chinese iron and steel industry.

Source: CEInet

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

4

Source: China Iron and Steel Association

China: A Major Producer of Iron and Steel, Facing

Technological Barriers

Although China is the global leader in terms of crude steel output, its industry

technology remains at a medium to low level. Currently, high value-added

products account for less than half of the majority of Chinese iron and steel

manufacturers’ output. The quality of high-end products such as high-intensity

steel strips (mid-to-thick), extra-thick steel plates, and zinc-plated steel plates for

automotive use produced in China is far behind those produced in Japan and

Germany.

Overseas, the share of special steel accounts for 10% of the total industry, while

that in China hovers at 5%. Moreover, mid-to-low-level special steel products

such as Q345C steel plates and alloy steel are predominant, taking up a roughly

80% share of the total industry product breakdown.

Looking at the trade situation, China’s steel import volume was 12.42 million

tonnes in 1998, exceeding export volume (3.59 million tonnes) to a large extent.

Exports first surpassed imports in 2006. In 2014, the total volume of exports

amounted to 93.78 million tonnes, which was about seven times that of imports

(14.43 million tonnes).

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

5

On the other hand, the unit price of imports and exports shows that the majority

of the Chinese steel industry is comprised of low value-added products, while

high value-added products are mostly imported. In 1998 the import unit price

was USD 506.23 per tonne, and the export unit price was USD 471.10 per tonne.

In 2014, the import unit price was USD 1,241 per tonne, and the export unit

price was USD 755 per tonne.

South Korea is the largest export destination of Chinese steel products,

accounting for 13.8% of total exports, with 12.97 million tonnes of products

imported from China. Among the top ten importing countries and regions,

Southeast Asian countries take up seven places. This is attributable to the

region’s expanding infrastructure construction, and a subsequent increase in the

need for iron and steel products.

However, faced with increasing imports from China, iron and steel

manufacturers in these countries are now taking active measures to defend their

own shares within the local market.

In December 2014, Hyundai Steel (KOR) and Dongkuk Steel Group (KOR) filed an

anti-dumping lawsuit against Chinese steel exports. It is highly likely that the

steel exports from China to South Korea will be levied with an anti-dumping tax

at a rate of 18–33% in the future. Similar trends can be observed in India, the

USA, and some European countries as well.

Source: CEInet

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

6

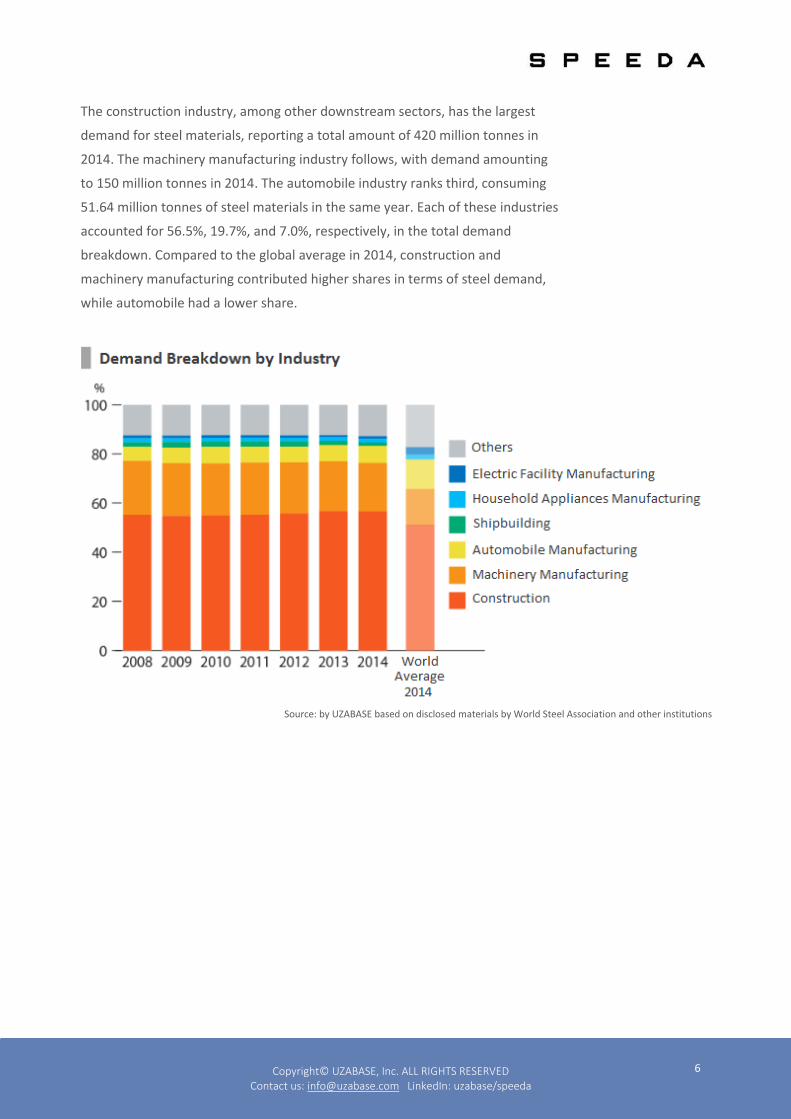

The construction industry, among other downstream sectors, has the largest

demand for steel materials, reporting a total amount of 420 million tonnes in

2014. The machinery manufacturing industry follows, with demand amounting

to 150 million tonnes in 2014. The automobile industry ranks third, consuming

51.64 million tonnes of steel materials in the same year. Each of these industries

accounted for 56.5%, 19.7%, and 7.0%, respectively, in the total demand

breakdown. Compared to the global average in 2014, construction and

machinery manufacturing contributed higher shares in terms of steel demand,

while automobile had a lower share.

Source: by UZABASE based on disclosed materials by World Steel Association and other institutions

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

7

Low Market Concentration in China’s Iron and

Steel Industry

According to data released by China Iron and Steel Association, the number of

companies involved in the industry amounted to 11,031 in 2012; of them,

10,608 were SMEs, accounting for 96% of the total. The CR4 ratio (four-firm

concentration ration) was 22% in 2012, lower than that of Japan (74%) and the

USA (53%) that year.

In addition, the CR10 ratio in 2014 was 36%, while the CR3 ratios of South Korea

and Brazil were 90% and 89% respectively. Other major iron and steel

manufacturing countries such as Japan, Russia, India, and the USA had CR3 ratios

of 83%, 83%, 67%, and 60%, respectively.

So far, growth of overall capacity in the Chinese iron and steel industry has

stemmed from an increase in the number of manufacturers, since the industry

structure— where SMEs form the majority— has hindered it from taking

advantage of a scale economy. Additionally, the slowdown of the Chinese

economy will push the industry into a harder situation.

Source: chinacir.com.cn

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

8

Top Four Firms of Steel Industry in Leading Countries (2014)

China Top Four Steel Manufacturers Crude Steel Output (million tonnes)

1 Hebei Iron & Steel 47

2 BaoSteel Group 43

3 Jiangsu Shagang Group 35

4 Angang Steel 34

Japan Top Four Steel Manufacturers Crude Steel Output (million tonnes)

1 Nippon Steel & Sumitomo Metal 49

2 JFE Steel 31

3 Kobe Steel 8

4 Nisshin Steel 4

USA Top Four Steel Manufacturers Crude Steel Output (million tonnes)

1 United States Steel 20

2 Steel Dynamics 6

3 AK Steel 6

4 Commercial Metals Company *3 Source: World Steel Association

Note: * data from 2013.

Chinese Steel Manufacturers Facing Issues of

Profitability and Scale

According to the World Steel Association, ArcelorMittal (LUX) was the leading

manufacturer in terms of crude steel output in 2014, reaching 98.08 million

tonnes. The company’s output was larger than the combined total of runners-up

Nippon Steel & Sumitomo Metal (JPN; 49.03 million tonnes) and Hebei Iron &

Steel (CHN; 47.09 million tonnes).

Looking at the breakdown of the top ten manufacturers, Chinese firms took up

six places, but only three of them had a positive net profit margin. On the other

hand, three non-Chinese companies made profit, and Nippon Steel & Sumitomo

Metal recorded a net profit margin of 3.8%.

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

9

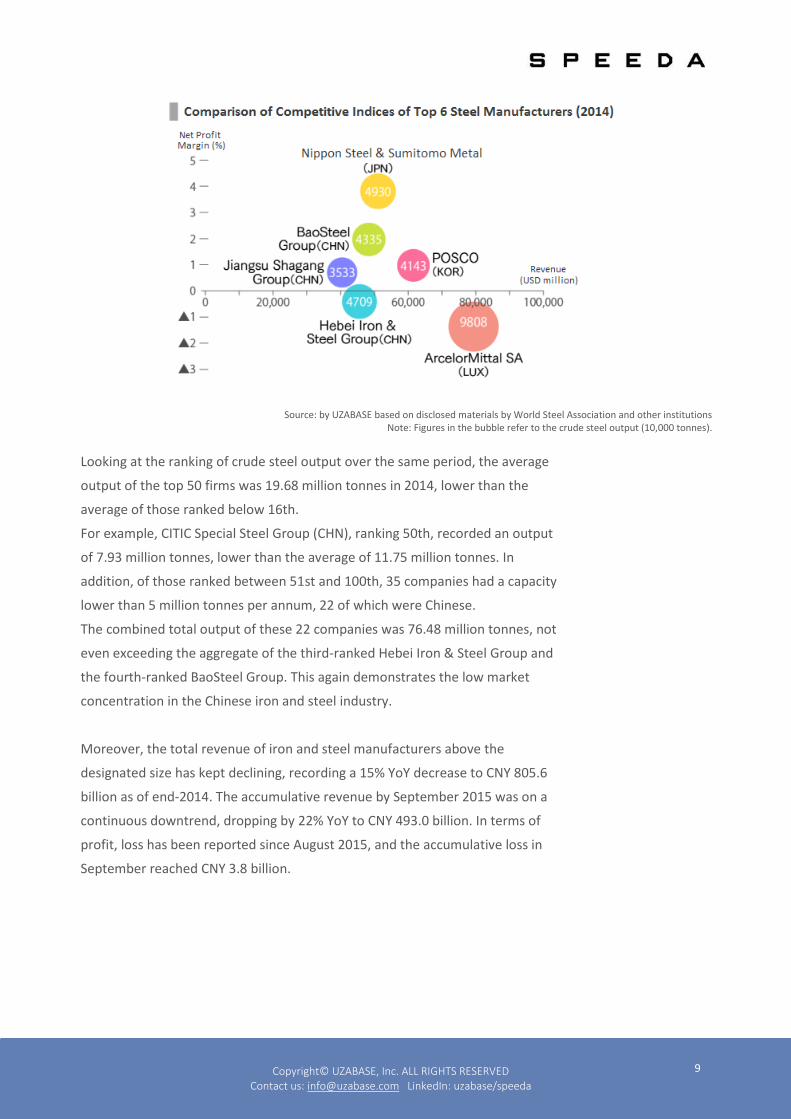

Source: by UZABASE based on disclosed materials by World Steel Association and other institutions Note: Figures in the bubble refer to the crude steel output (10,000 tonnes).

Looking at the ranking of crude steel output over the same period, the average

output of the top 50 firms was 19.68 million tonnes in 2014, lower than the

average of those ranked below 16th.

For example, CITIC Special Steel Group (CHN), ranking 50th, recorded an output

of 7.93 million tonnes, lower than the average of 11.75 million tonnes. In

addition, of those ranked between 51st and 100th, 35 companies had a capacity

lower than 5 million tonnes per annum, 22 of which were Chinese.

The combined total output of these 22 companies was 76.48 million tonnes, not

even exceeding the aggregate of the third-ranked Hebei Iron & Steel Group and

the fourth-ranked BaoSteel Group. This again demonstrates the low market

concentration in the Chinese iron and steel industry.

Moreover, the total revenue of iron and steel manufacturers above the

designated size has kept declining, recording a 15% YoY decrease to CNY 805.6

billion as of end-2014. The accumulative revenue by September 2015 was on a

continuous downtrend, dropping by 22% YoY to CNY 493.0 billion. In terms of

profit, loss has been reported since August 2015, and the accumulative loss in

September reached CNY 3.8 billion.

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

10

Source: CEInet Note: Companies above designated size refer to those make an annual revenue more than CNY 20 million.

China’s Iron and Steel Industry: What’s to Come

and Where to Go

Mergers and Acquisitions and Industry Reorganisation

As mentioned above, the Chinese iron and steel industry has low market

concentration, which hampers the industry from taking advantage of a scale

economy. In addition, the slowdown of the Chinese economy will also affect the

demand for iron and steel. Therefore, industry players will likely face a harsher

environment in the future.

As per data from China Iron and Steel Association, in 1H 2015 the aggregate

profit of the top ten profit-making companies was CNY 16.5 billion, up by 113%

YoY. In contrast, the aggregate loss of the top ten loss-making companies was

CNY 13.9 billion, up by 152% YoY. This indicates a polarised course of

development in terms of profitability in this industry.

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

11

Against such a background, it can be said that the industry is right at the

threshold of mergers and acquisitions and industry reorganisation. Seven big

M&A deals took place in this industry in 2014. While private players have been

actively carrying out M&As, state-run companies are lingering about.

Additionally, the M&A activities are region-specific.

Entering 2015, the Chinese government made plans regarding industry

reorganisation to support the industry development. In March, the MIIT issued

the Solicitation of Public Opinion on Policies Concerning Steel Industry

Adjustment (Revised in 2015) and demanded the industry to accelerate in

mergers, acquisitions and reorganisation.

The policy also set goals on the CR10 ratio, aiming to boost the figure to 60% by

2025 and encouraging the formation of steel conglomerates that comprise three

to five firms with global competitiveness and influence.

The MIIT is also stipulating the Industry Transforming Plan (2015–2017) for the

iron and steel industry, which will be the guideline for the industry’s future

development. Going forward, it can be expected that state-owned companies

will undergo progressive M&As as well.

Copyright© UZABASE, Inc. ALL RIGHTS RESERVED Contact us: [email protected] LinkedIn: uzabase/speeda

12

Entering Overseas Markets

In 2014, Beijing has been promoting the strategy of “One Belt One Road”, which

aims at expanding the scope of infrastructure companies by pushing them to

overseas markets. It can be anticipated that iron and steel manufacturers will

also leverage this opportunity to counteract domestic overcapacity to a certain

extent.

As per data from the Customs of the PRC, by 1Q 2015, India and Pakistan of

South Asia have increased their steel material imports by 207% and 124% YoY

respectively; Turkey, the UAE, Saudi Arabia, and Iran have also reported a

growth rate of 200%, 137%, 110%, and 97%, respectively. Vietnam, Indonesia,

the Philippines, Thailand, Malaysia, and Myanmar of Southeast Asia have each

recorded a YoY growth in imports of 134%, 114%, 47%, 79%, 78%, and 77%.

Furthermore, with demand overseas increasing, Chinese steel manufacturers are

setting up branches abroad as well. On 27 March 2015, Metallurgical

Corporation of China (MCC Group, CHN) and Magang Group (CHN) joined a

memorandum with Ferrum (CHE) regarding establishing a joint venture for steel

production with an annual capacity of one million tonnes in Kazakhstan. Jiuquan

Iron & Steel Group (CHN) has also expressed its intention of building a

production plant in Kazakhstan.

Summary

The Chinese iron and steel industry, despite ranking top in crude steel output, is

facing serious issues. While exports keep growing, the industry’s low

technological level will gradually diminish its competitiveness. Furthermore, low

market concentration hinders the industry from making use of scale economies

for higher profits. Finally, with the slowdown in the country’s economy, the

industry faces grim prospects ahead.

Among the top ten crude steel manufacturers in 2014, six of them were Chinese

companies, with half of these reporting losses. In the future, reorganisations and

M&As, together with entry into overseas markets, should be put into action in

an effort to lead the industry back to a favourable trend.