China: Metals & Mining: Base Metals -...

34

May 14, 2013 China: Metals & Mining: Base Metals Equity Research Weak supply growth to improve zinc/lead outlook; resume on 2 cos Supply-demand for zinc/lead to be balanced over medium/long term We expect supply growth from zinc and lead mines to slow down over the medium-to-long term. We note that several zinc and lead miners have announced either closure of mines or cutting production during 2013-2015 due to resource depletion. Furthermore, supply from potential projects coming onstream and small mines in China will be limited before 2015. Our GS commodities research team estimates that global zinc mine production CAGR will slow to 2.4% over 2013E-2015E, and demand will increase to 4.3% on the back of urbanization in China and consumption upgrades, thereby restoring the supply-demand balance for zinc. We expect zinc/lead prices to rise in 2014-2015 as fundamentals improve. Our GS commodities research team’s 2013E/2014E/2015E price forecasts per ton for zinc are US$2,013 / US$2,175/US$2,200 and lead are US$2,163/US$2,338/US$2,365. Industry consolidation and environmental protection should help alleviate excess capacity in China’s zinc and lead industry, in our view. We note tougher environmental norms and emissions targets are likely to reduce zinc and lead refining capacity by 2 mn tons (government’s plan of 1.3mt lead and 0.65mt zinc) during the 12 th Five-Year Plan, which we believe will help support zinc and lead prices in China. Resume coverage on Lingnan and Chihong, both with Neutral Lingnan: We believe overseas expansion (Perilya/GlobeStar) and subsequent improvement in mining operations indicate strong execution skills. Further, the company is now back to normal operations, post the environmental accidents over 2010-2012. We resume coverage with Neutral as its valuation is not attractive, and our 12-month Director’s Cut-based TP of Rmb8.6. Chihong: Resource allocation is complete and earnings growth is now awaited. Rapid resource expansion generated a large increase in capex over the past 3 years, and we see its CROCI improving at a slow pace (2013/2014 CROCI of 9.3%/9.1% down from 10.5% in 2012). We resume coverage with Neutral and our 12-m Director’s Cut-based TP of Rmb10.41. Key risks Downside: Environmental accidents impacting operations; weak zinc/ lead prices; Upside: Potential government stimulus package boosting demand. RATINGS/TP SUMMARY Note: (1) Target prices are in Rmb. (2) Share prices as of May 10, 2013. (3) 12-m TPs are based on EV/GCI vs. CROCI/WACC (Director’s Cut). Source: Datastream, Gao Hua Securities Research estimates. KEY 2013E ZINC AND LEAD A-SHARE ESTIMATES Source: Gao Hua Securities Research estimates. RELATED RESEARCH Metal Detector: Zinc finding its floor, April 23, 2013 Global Commodities Research: GS Mining Commodity Forecasts for 2013, and Beyond, January 16, 2013 Global Commodities Research: The Old Economy Renaissance: 2013-2014 Issues and Outlook, December 5, 2012 Jefferson Zhang +86(21)2401-8945 [email protected] Beijing Gao Hua Securities Company Limited Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non- US affiliates are not registered/qualified as research analysts with FINRA in the U.S. Yong Han, CFA +86(21)2401-8948 [email protected] Beijing Gao Hua Securities Company Limited The Goldman Sachs Group, Inc. Global Investment Research Company Ticker Current POT UP/DOWN Jiangxi Copper (A) 600362.SS Buy 23.32 21.2 10.3% Zhongjin Gold 600489.SS Neutral 13.86 12.4 12.2% Zhongjin Lingnan 000060.SZ Neutral 8.60 9.0 -4.1% Zijin (A) 601899.SS Neutral 3.09 3.1 -0.9% Shandong Gold 600547.SS Neutral 30.96 32.1 -3.6% Tongling 000630.SZ Neutral 14.30 15.4 -7.0% Chihong 600497.SS Neutral 10.41 11.9 -12.5% Chalco (A) 601600.SS Sell 3.30 4.1 -19.3% Yunnan Copper 000878.SZ Sell 6.85 12.6 -45.5% Rating 12M TP Price Net profit growth Production growth PE PB ROE Lingnan 23% 16% 34.9 3.1 9.1% Chihong -8% 8% 48.9 4.0 8.2%

Transcript of China: Metals & Mining: Base Metals -...

May 14, 2013

China: Metals & Mining: Base Metals

Equity Research

Weak supply growth to improve zinc/lead outlook; resume on 2 cos

Supply-demand for zinc/lead to be balanced over medium/long term

We expect supply growth from zinc and lead mines to slow down over

the medium-to-long term. We note that several zinc and lead miners have

announced either closure of mines or cutting production during 2013-2015

due to resource depletion. Furthermore, supply from potential projects

coming onstream and small mines in China will be limited before 2015. Our

GS commodities research team estimates that global zinc mine production

CAGR will slow to 2.4% over 2013E-2015E, and demand will increase to 4.3%

on the back of urbanization in China and consumption upgrades, thereby

restoring the supply-demand balance for zinc.

We expect zinc/lead prices to rise in 2014-2015 as fundamentals improve.

Our GS commodities research team’s 2013E/2014E/2015E price forecasts per

ton for zinc are US$2,013 / US$2,175/US$2,200 and lead are

US$2,163/US$2,338/US$2,365.

Industry consolidation and environmental protection should help

alleviate excess capacity in China’s zinc and lead industry, in our view. We

note tougher environmental norms and emissions targets are likely to

reduce zinc and lead refining capacity by 2 mn tons (government’s plan of

1.3mt lead and 0.65mt zinc) during the 12th Five-Year Plan, which we

believe will help support zinc and lead prices in China.

Resume coverage on Lingnan and Chihong, both with Neutral

Lingnan: We believe overseas expansion (Perilya/GlobeStar) and subsequent

improvement in mining operations indicate strong execution skills. Further,

the company is now back to normal operations, post the environmental

accidents over 2010-2012. We resume coverage with Neutral as its valuation

is not attractive, and our 12-month Director’s Cut-based TP of Rmb8.6.

Chihong: Resource allocation is complete and earnings growth is now

awaited. Rapid resource expansion generated a large increase in capex

over the past 3 years, and we see its CROCI improving at a slow pace

(2013/2014 CROCI of 9.3%/9.1% down from 10.5% in 2012). We resume

coverage with Neutral and our 12-m Director’s Cut-based TP of Rmb10.41.

Key risks

Downside: Environmental accidents impacting operations; weak zinc/ lead

prices; Upside: Potential government stimulus package boosting demand.

RATINGS/TP SUMMARY

Note: (1) Target prices are in Rmb. (2) Share prices as of

May 10, 2013. (3) 12-m TPs are based on EV/GCI vs.

CROCI/WACC (Director’s Cut).

Source: Datastream, Gao Hua Securities Research

estimates.

KEY 2013E ZINC AND LEAD A-SHARE ESTIMATES

Source: Gao Hua Securities Research estimates.

RELATED RESEARCH

Metal Detector: Zinc finding its floor, April 23, 2013

Global Commodities Research: GS Mining Commodity

Forecasts for 2013, and Beyond, January 16, 2013

Global Commodities Research: The Old Economy Renaissance:

2013-2014 Issues and Outlook, December 5, 2012

Jefferson Zhang +86(21)2401-8945 [email protected] Beijing Gao Hua Securities Company Limited Goldman Sachs does and seeks to do business with

companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

Yong Han, CFA +86(21)2401-8948 [email protected] Beijing Gao Hua Securities Company Limited

The Goldman Sachs Group, Inc. Global Investment Research

Company TickerCurrent POT UP/DOWN

Jiangxi Copper (A) 600362.SS Buy 23.32 21.2 10.3%Zhongjin Gold 600489.SS Neutral 13.86 12.4 12.2%Zhongjin Lingnan 000060.SZ Neutral 8.60 9.0 -4.1%Zijin (A) 601899.SS Neutral 3.09 3.1 -0.9%Shandong Gold 600547.SS Neutral 30.96 32.1 -3.6%Tongling 000630.SZ Neutral 14.30 15.4 -7.0%Chihong 600497.SS Neutral 10.41 11.9 -12.5%Chalco (A) 601600.SS Sell 3.30 4.1 -19.3%Yunnan Copper 000878.SZ Sell 6.85 12.6 -45.5%

Rating 12M TP Price

Net profitgrowth

Productiongrowth

PE PB ROE

Lingnan 23% 16% 34.9 3.1 9.1%

Chihong -8% 8% 48.9 4.0 8.2%

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 2

Table of Contents

Slowdown in supply growth for zinc and lead, resume on 2 stocks 3

Zinc and lead supply-demand to be balanced over the next 3 years 4

China zinc/lead industry: Consolidation likely to cut excess capacity 8

Operations comparison for A-share zinc and lead firms 13

Using Director’s Cut to value zinc and lead firms 15

Chihong (600497.SS, Neutral): Resources acquired, awaiting profits 18

Zhongjin Lingnan (000060.SZ, Neutral): Back to normal operations 24

Disclosure Appendix 31

The prices in this report are as of the market close of May 10, 2013.

Exhibit 1: Valuation table for selected global non-ferrous metal companies under GS/GH coverage

*This stock is on our regional Conviction List Note: US stocks are assigned 6-month target prices

Source: DataStream, Goldman Sachs research estimates, Gao Hua Securities Research estimates.

GS/GH 10-May-13

Ticker Rating Price Ccy 12M TP 2013E 2014E 2013E 2014E 2013E 2014E 2013E 2014E 2013E 2014E

China-A share

Jiangxi Copper (A) 600362.SS Buy 21.15 CNY 23.32 1.46 1.36 14.5 15.6 1.6 1.5 9.4 9.6 11% 10%

Zhongjin Gold 600489.SS Neutral 12.35 CNY 13.86 0.55 0.46 22.4 27.0 3.1 2.8 9.4 10.4 15% 11%

Zhongjin Lingnan 000060.SZ Neutral 8.97 CNY 8.60 0.26 0.28 34.9 31.6 3.1 2.8 11.7 10.9 9% 9%

Zijin Mining (A) 601899.SS Neutral 3.12 CNY 3.09 0.24 0.19 13.3 16.1 2.2 2.0 7.5 8.4 17% 13%

Shandong Gold 600547.SS Neutral 32.13 CNY 30.96 1.36 1.18 23.6 27.3 4.9 4.2 12.2 13.2 23% 17%

Tongling Non-ferrous 000630.SZ Neutral 15.38 CNY 14.30 0.77 0.82 20.0 18.8 1.9 1.7 12.7 11.4 10% 10%

Chihong Zinc & Germanium 600497.SS Neutral 11.89 CNY 10.41 0.24 0.32 48.9 37.7 4.0 3.7 14.9 13.5 8% 10%

Chalco (A) 601600.SS Sell 4.09 CNY 3.30 (0.16) (0.12) 1.3 1.3 17.8 20.6 -5% -4%

Yunnan Copper 000878.SZ Sell 12.58 CNY 6.85 0.04 0.04 2.6 2.5 17.5 18.1 1% 1%

Median-A share metals companies 22.4 27.0 2.6 2.4 12.0 11.2 11% 10%

HK-H share

Jiangxi Copper (H) 0358.HK Buy 16.42 HKD 18.30 1.46 1.36 8.9 9.6 1.0 0.9 5.8 5.9 11% 10%

Zijin Mining (H) 2899.HK Buy 2.33 HKD 2.70 0.24 0.19 7.8 9.5 1.3 1.2 5.0 5.6 17% 13%

China Molybdenum 3993.HK Neutral 3.17 HKD 3.91 0.23 0.22 10.7 11.5 1.0 0.9 5.8 5.2 9% 8%

Zhaojin Mining (H) 1818.HK Sell 8.50 HKD 7.00 0.57 0.45 11.7 14.9 2.1 1.9 8.2 9.5 19% 13%

Chalco (H) 2600.HK Sell 3.24 HKD 2.40 (0.16) (0.12) 0.8 0.8 15.3 17.7 -5% -4%

Median-H share metals companies 9.8 10.6 1.0 0.9 5.8 5.9 11% 10%

US

Vale VALE Buy 16.96 USD 25.60 2.09 2.32 8.1 7.3 1.2 1.1 4.6 4.4 15% 15%

Freeport-McMoRan Copper & GoFCX Buy 32.55 USD 38.00 3.35 3.00 9.7 10.8 1.5 1.4 4.4 4.7 17% 13%

Alcoa AA Neutral 8.70 USD 8.00 0.42 0.65 20.8 13.4 0.7 0.6 7.1 6.3 4% 5%

Southern Copper Corp. SCCO Neutral 33.31 USD 42.00 2.61 2.22 12.7 15.0 4.6 3.9 8.0 8.6 41% 28%

Median-US metals companies 11.2 12.1 1.4 1.2 5.9 5.5 16% 14%

Australia

OceanaGold OGC.AX Buy* 2.07 AUD 2.60 0.16 0.21 13.0 9.8 0.9 0.8 3.9 3.4 7% 9%

Lynas LYC.AX Buy 0.66 AUD 0.81 (0.06) 0.04 15.0 1.9 1.8 9.5 -20% 12%

Teranga Gold TGZ.AX Sell 0.93 AUD 0.50 0.10 (0.03) 9.4 0.6 0.6 3.7 7.6 6% -2%

Alumina AWC.AX Sell 1.09 AUD 0.90 (0.01) 0.00 0.9 0.9 15.4 13.6 -1% 0%

Alacer Gold AQG.AX Sell 2.93 AUD 2.33 0.15 0.10 20.0 30.2 0.8 0.8 2.8 3.2 4% 3%

Iluka Resources ILU.AX Neutral 10.80 AUD 8.85 0.34 1.23 32.1 8.8 2.7 2.4 11.7 4.4 5% 29%

Median-Australian metals companies 20.0 15.0 0.9 0.9 7.7 7.6 4% 3%

EPS PE (X) P/B (X) EV/EBITDA (X) ROE

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 3

Slowdown in supply growth for zinc and lead, resume on 2 stocks

Supply growth from zinc and lead mines likely to slow over the medium-to-long term. The Dairi (Indonesia) and Mount Isa (Australia) zinc and lead mines under construction are

scheduled to come onstream during 2013-2015. However, key mines such as Century and

Brunswick are likely to close down or cut production due to resource depletion. We believe

this would severely limit potential capacity release at zinc and lead facilities before 2015. Our

GS commodities research team estimates that during 2013E-2015E, global zinc mine

production will see a CAGR slowdown to 2.4%, a notch below 4% CAGR over the past decade.

In terms of demand, we expect Chinese urbanization and consumption upgrades to drive

continued growth in the real estate and automobile industries over the medium term. At the

same time, the US real estate and car markets are experiencing a revival. Our GS commodity

research team believes global demand for refined zinc will increase 4.3% CAGR over 2013E-

2015E, outpacing supply growth and restoring the supply-demand balance.

Industry consolidation and stricter environmental norms should help alleviate excess

capacity in China’s zinc and lead industry. Small mines currently account for 90% or

more of China’s zinc and lead industry. The Chinese government has strengthened its push

for M&A among metal mines in recent years to further increase industry consolidation.

Restrictions on refining capacity have also intensified, including tougher environmental

norms and emissions targets that will reduce lead refining capacity (including recycled

lead) by 1.3 mn tons and zinc refining capacity by 650k tons (government’s plan) during the

12th Five-Year Plan (2011-2015). We believe excess capacity in China’s zinc and lead

industry will be alleviated somewhat, reducing headwinds on zinc and lead prices.

We expect zinc and lead prices to rise in 2014E-2015E. Even though we believe high zinc and

lead inventories will depress prices in the short term, as peak consumption season destocking

concludes, supply and demand will become balanced, and zinc and lead prices will rise further

in 2014E-2015E. Our GS commodity research team’s 2013E/2014E/2015E price forecasts per ton

for zinc are US$2,013 / US$2,175/US$2,200 and lead are US$2,163/US$2,338/ US$2,365.

In this report, we resume coverage on two A-share zinc and lead companies.

Chihong’s net profit has higher sensitivity to zinc and lead prices, and we believe

greater organic growth over the next three years will result in the company

benefitting further from rising zinc and lead prices. Zhongjin Lingnan has a stable

asset and liability structure, and more effective overseas assets.

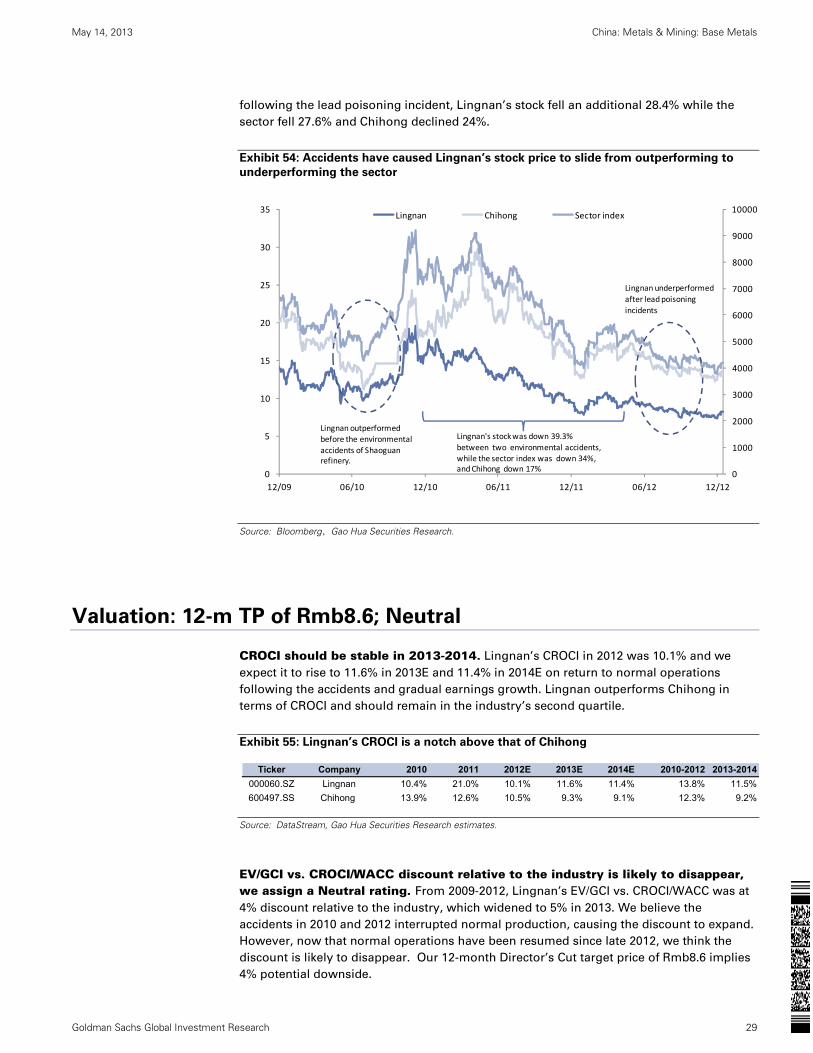

Zhongjin Lingnan: Overseas expansion and mining operations reflect the firm’s

strong execution skills. Lingnan successfully acquired Perliya and GlobeStar overseas in

2009 and 2010 and subsequently their earnings improved significantly, reflecting Lingnan’s

strong execution skills, in our view. Over the past two years, however, it has been affected

by environmental incidents, such as the Shaoguan and Renhua accidents, from which it

has recently recovered to normal production. We resume coverage of Zhongjin Lingnan

with a Neutral rating and a 12-month Director’s Cut–based target price of Rmb8.6.

Chihong: Resource layout complete, awaiting earnings updates. Resource allocation is

complete and earnings growth is awaited. Rapid resource expansion generated a large

increase in capex over past 3 years, and we see its CROCI improving at a slow pace

(2013/2014 CROCI of 9.3%/9.1% down from 10.5% in 2012). Our 12-month Director’s Cut–

based target price is Rmb10.41, and resume coverage with a Neutral rating.

Exhibit 2: Comparison of our earnings estimates and market consensus for A share zinc and lead coverage universe

Source: Wind, Gao Hua Securities Research estimates

Companies 2013E 2014E 2013E 2014E 2013E 2014E 2013E 2014E 2013E 2014E Current TPRmb Rmb

Chihong 318 413 365 414 0.24 0.32 0.28 0.32 -13% 0% 11.9 10.41 -12.5%Lingnan 530 586 536 681 0.26 0.28 0.26 0.33 -1% -14% 9.0 8.60 -4.1%

GH estimated earning GH estimated EPSConsensus Consensus Diff. from Cons. Potential Upside/ Downside

Potentialup/ downsideMn Rmb Mn Rmb Rmb Rmb %

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 4

Zinc and lead supply-demand to be balanced over the next 3 years

Supply: Resource exhaustion and industry consolidation will slow zinc and lead supply growth over the medium-to-long term

We divide sources of global zinc and lead supply into three types: mines in production or

under construction, potential zinc and lead projects, and growth from China. Based on this

analytic framework, we estimate 2013-2015 zinc and lead supply growth of 1.1%/2.6%/3.6%,

with a 2.4% CAGR, slower than the 4% rate over the past 10 years.

Zinc and lead mines under construction coming onstream unable to replace lost capacity

from closing mines. We estimate that mine closings and lost capacity from resource

exhaustion in 2013/2014/2015 will lower zinc concentrate supply by approximately

361k/494k/397k t. The major source of decline in 2013 will be Xstrata as the firm will close its

Brunswick and Perseverance mines due to declining ore quality and resource exhaustion, and

lower production at its Antamina mine, lowering global zinc production by 361k t. The

estimated loss in 2014 is from reduced production at Minmetals’ Century zinc and lead mine,

and the closing of Vedanta’s Lisheen mine, decreasing zinc mine production by 494k t. In

addition, while zinc and lead mines under construction—like Dairi and Mount Isa—will come

onstream over 2013-2015, we estimate that they will only increase zinc mine production in

those years by 510k/236k/132k t, not enough to offset the declines caused by mine closings.

Exhibit 3: Zinc mines in production which will close/decrease production in 2013-2015, and

their effects on zinc concentrate supply Units: 1,000 t

Source: Wood Mackenzie, Goldman Sachs Global ECS Research estimates

Exhibit 4: Key zinc mines under construction set to come online/expand production, 2013-

2015 Units: 1,000 t

Source: Wood Mackenzie, Goldman Sachs Global ECS Research estimates

Capacity Capacity ChangeCompany Zinc mines 2012E 2013E 2014E 2015E 2015E 2015E-2012EMinmetals Century 510 0 -221 -289 0 -510Xstrata Brunswick 203 -183 -20 0 0 -203Vedanta Lisheen 168 0 -168 0 0 -168Xstrata Perseverance 136 -106 -30 0 0 -136Agnico Eagle La Ronde 50 -35 -9 0 6 -44Kazzinc Zyryanovsk 113 12 -16 -63 46 -67Minmetals Golden Grove 68 -13 -30 3 28 -40Kagara Mt Garnet 44 4 0 -48 0 -44Teck Red Dog 540 -10 0 0 530 -10Xstrata Antamina 250 -30 0 0 220 -30

Total 2,082 -361 -494 -397 830 -1,252

Capacity changes in 2013-2015

Capacity Capacity ChangeCompany Zinc mines 2012E 2013E 2014E 2015E 2015E 2015E-2012EXstrata Mount Isa Pb/Zn 375 25 75 35 510 135Herald Diari 0 110 12 0 122 122Various China 4,179 88 35 -49 4,252 73Glencore Perkoa 35 45 10 0 90 55Zijin Kyzyl Tashtygskoe 50 30 10 0 90 40Penoles Velardena 0 40 35 10 85 85Xstrata Bracemac McLeod 0 60 22 0 82 82HudBay Lalor Lake 8 12 20 40 80 72Compania Cerro Lindo 115 35 0 0 150 35Xstrata McArthur River 200 15 4 4 223 23Minmetals Bisha 0 30 60 90 90Hindustan Rampura-Agucha 750 30 -30 10 760 10Tajikistan Altintopkan 10 20 13 22 65 55

Total 5,722 510 236 132 6,599 877

Capacity changes in 2013-2015

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 5

Potential zinc mine capacity release will be relatively slow. We believe another key

factor in determining zinc concentrate supply growth is potential capacity release of zinc

and lead mines. Potential zinc and lead mines have verified resources, but have not yet

begun construction. These projects can be divided based on the amount of progress made,

i.e., projects which are still at the feasibility study stage, projects which have been closed

but may resume production, projects in the financing stage, and projects which have

received construction approval. Our GS commodities research team estimates global

potential zinc mine production of 1.9mt by 2015E. However, based on the current progress

in potential mines, we believe they will come on line relatively slowly.

Exhibit 5: Contribution to ‘probable’ supply, 2011-2015,

by project type/stage Tonnage is in Kt

Exhibit 6: Key potential zinc and lead mines, and

estimated progress Units: 1,000 t

Source: Wood Mackenzie, Goldman Sachs Global ECS Research estimates

Source: ILZSG, Gao Hua Securities Research.

Integration of China’s zinc and lead industry could ease production growth concerns. The integration of China’s zinc and lead industry mainly involves consolidation of small-

scale mines and limiting zinc and lead smelting. We estimate that the Chinese government

will continue to attempt to rectify the zinc and lead industry’s “small-scale and

fragmented” nature and increase industry consolidation. Furthermore, we note that

environmental requirements will limit zinc and lead smelter capacity—energy-saving and

emissions targets will lead to decrease in lead smelting capacity of 1.3 mt by the end of

2015E (including recycled lead capacity), and a decrease in zinc smelting capacity of 650k t;

recycled lead production will increase to 40% (all these targets are set by the government)

of total production. Our base case assumes refined zinc production growth of 6% in 2013E

and 7% in 2014E.

In addition, we believe global refined lead supply growth will slow. With zinc and lead

being generally found in the same mines, most zinc mine closures will equally affect lead

concentrate production, and we estimate that refined lead production growth will slow in

2013-2015. Our GS commodities research team estimates refined lead production growth

at 7% for 2013E, slightly below the average 8.3% growth in 2010-2012.

Demand: Global industrial recovery will spur zinc and lead demand growth

The Goldman Sachs ECS Research team estimates that global GDP will increase to 3.2% in

2013E, from 3.0% in 2012. They estimate 2013E GDP growth in emerging markets (e.g.,

China, India, Brazil, Russia) at 5.8%, up from 2012’s 5.4% (Exhibit 7). The momentum of the

Goldman Sachs Global Leading Indicator has turned positive since August 2012, and

remained so for the past several months, indicating that global manufacturing activity will

continue to recover.

Type/ StageNo. Probable

MinesTotal

tonnage%probable

growthFeasibility 18 1285 68%Potential Restart 12 337 18%Financing/ Refin. 6 207 11%Permitting 2 50 3%Total 39 1878 100%

Zinc mines Country CapacityEstimate year to

come onlineDugald River Australia 200 2015Selwyn Canada 100 2015/16Ozernoye Russia 350 2015/16Gamsberg South Africa 200 2015/16Oued-Amizour (Tala Hamza) Algeria 164 2017/18Mehdiabad Iran 400 2018/19

Total 1414

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 6

Exhibit 7: Our ECS Research team estimates global GDP

recovery in 2013/2014…

Exhibit 8: …and the Goldman Sachs GLI indicates

recovery in global manufacturing

Source: Goldman Sachs Global ECS Research estimates. Source: Bloomberg, Goldman Sachs Global ECS Research estimates.

Zinc: Urbanization in China and upgraded consumption are key drivers of demand

Zinc has good anti-corrosion, thermal conductivity and electrical conductivity properties. Its

main uses in primary consumption are in galvanization and zinc alloys, applications which

account for over 50% of total zinc use. Key downstream industries include property, home

appliances and automotives. On a country level, zinc consumption in China currently

accounts for over 40% of the world total (Exhibit 10), making it one of the world’s major

zinc consumers. Our China real estate team expects total GFA sold to rise 20% yoy in 2013E,

which we believe will drive recovery in industries like home appliances, spurring higher

zinc demand. Urbanization and upgraded consumption are also likely to increase

automotive consumption. Furthermore, moderate recovery in demand in regions outside of

China (the property and automotive industries in the US, other developing economies) will

support global zinc consumption in 2013 and 2014, in our view (Exhibits 11 and 12). Our GS

commodities research team estimates global zinc consumption growth of 3.9% in 2013E

and 4.4% in 2014E.

Exhibit 9: Structure of global primary zinc consumption Galvanization and zinc alloys make up over 50% of zinc

consumption, as of 2011

Exhibit 10: Global zinc consumption by country China consumes over 40% of the world’s zinc, as of 2011

Source: ILZSG, Gao Hua Securities Research

Source: ILZSG, Gao Hua Securities Research

Q1 Q2 Q3 Q4USA 2.1 2.9 2.4 2.7 3.1 3.4Japan 1.4 1.7 3.9 1.7 0.8 0.2Euro area -0.7 0.8 0.3 0.7 0.9 1.1 France -0.7 0.4 -0.2 0.3 0.6 0.8 Germany 0.4 1.8 1.4 1.8 2 2.1 Italy -1.5 0.4 -0.1 0.3 0.6 0.9UK 1.3 2 2 2.1 2 2.1China 7.8 8.4 8.3 8.4 8.4 8.5India 5.8 7.2 7.1 7.1 7.3 7.4Brazil 3.3 4.4 4.6 4.6 4.3 4Russia 3.1 4.3 3.4 4.7 4.5 4.5Advanced Economies 1.2 2.2 2.1 2.1 2.2 2.2Emerging Markets 5.8 6.5 6.5 6.6 6.5 6.6World 3.2 4.1 4 4.1 4.1 4.2

2014Real GDP, % change2014

2013

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

2.0

25

30

35

40

45

50

55

60

65

70

10/08 04/09 10/09 04/10 10/10 04/11 10/11 04/12 10/12 04/13

US PMI China PMI

Europe PMI GS GLI Momentum (Rhs)

50%

17%

17%

6%

6%4%

Zincification

Zinc alloy

Brass

Zinc products

Chemical

Others

40.6%

8.1%16.1%

4.8%

4.0%

26.5%China

USA

Western Europe

India

Japan

Others

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 7

Exhibit 11: US property consumption has improved

significantly since 2012 Units: 1,000 units; %

Exhibit 12: US automotive consumption growth

continues Units: mn cars; %

Source: Wind, Gao Hua Securities Research.

Source: Wind, Gao Hua Securities Research.

Lead: Lead-acid batteries to remain the most stable form of energy storage in 2013-15

Over 70% of lead demand comes from lead-acid batteries, which are mainly used in electric

scooters and cars. We estimate China will remain the largest consumer of lead-acid

batteries in 2013-2015, and continue to consume over 40% of the world’s lead. However,

the continued increase in American car ownership should compensate for weaker demand

for lead-acid batteries as a result of slowing production growth, thereby supporting lead

demand. Our GS commodities research team estimates global lead consumption growth of

8% in 2013E.

Exhibit 13: Over 70% of lead is used in lead-acid batteries as of 2011

Exhibit 14: China consumes over 40% of the world’s lead as of 2011

Source: ILZSG, Gao Hua Securities Research.

Source: ILZSG, Gao Hua Securities Research.

Zinc and lead supply and demand will balance out in the medium-to-long term

Over the next six months, smelters including South Korea’s Onsan and Peru’s La Oroya will

resume production, and the current high levels of world zinc and lead inventories will exert

pressure on prices. However, as destocking concludes, and zinc and lead mines halt/reduce

production, supply and demand will come into balance, in our view. We estimate zinc and

lead prices will rise further in 2013E-2015E. Our 2013E/2014E/2015E price forecasts per ton

for zinc are US$2,013 / US$2,175/US$2,200 and lead are US$2,163/US$2,338/US$2,365, in

line with our ECS Research team.

‐50.0%

‐40.0%

‐30.0%

‐20.0%

‐10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

0

10

20

30

40

50

60

03/09 09/09 03/10 09/10 03/11 09/11 03/12 09/12 03/13

US new house sales (Lhs) yoy

‐50%

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

03/09 09/09 03/10 09/10 03/11 09/11 03/12 09/12 03/13

US auto sales (Lhs) yoy

77%

3%

6%

2%3% 8%

3%

Batteries

Cable Sheathing

Rolled & Extruded

Shot/Ammunition

Alloys

Pigments & Compounds

Miscellaneous

44.50%

1.30%3.90%

15.40%

15.70%

19.20%China

Japan

Korea Rep

USA

Europe

Others

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 8

Exhibit 15: Global zinc supply and demand model

Source: Wood Mackenzie, CRU, Goldman Sachs ECS Research estimates.

Exhibit 16: Global lead supply and demand model

Source: Wood Mackenzie, CRU, Goldman Sachs ECS Research estimates.

For more detailed analysis on global zinc and lead supply and demand, please see our

commodities research team’s January 16, 2013, report titled Global Commodities Research:

GS Mining Commodity Forecasts for 2013, and Beyond, and April 23, 2013, report Metal

Detector: Zinc finding its floor.

China zinc/lead industry: Consolidation likely to cut excess capacity

Zinc and lead supply in China: A two-pronged approach by mines and refineries

should hold back blind expansion

The General Office of the State Council released “Comments on Properly Consolidating

Metal and non-Metal Mines in Accordance with the Law” from the State Administration of

Work Safety on November 4, 2012. The document proposes the government to control

unlicensed mining and other illegal activities. Small mines that do not conform to industry

policy and unable to ensure safety will be either consolidated or closed in accordance with

the law. The restructuring of small mines will help alleviate fragmentation and

uncoordinated behavior because 90% or more of China’s zinc and lead mines are small-

scale operations, in our view.

Further, we think the recent fallback in zinc prices could limit zinc ore supply growth in

China. In our 4-year global supply growth model, which pre-dates the recent market

weakness, more than 70% of supply growth came from China. As the majority of small

Chinese zinc and lead mines have costs at the upper range of the global zinc and lead cost

curve, we think the recent downturn in zinc prices will limit Chinese supply growth.

000 tonnes 2009 2010 2011 2012 2013E 2014E 2015E

Global mine supply 11,021 11,817 12,194 13,013 13,159 13,495 13,977% change -4.0 7.2 3.2 6.7 1.1 2.6 3.6

Including disruption allow. (%) -- -- -- 0% 3% 4% 4%Global refined supply 11,174 12,288 12,920 13,020 13,300 13,750 14,300

% change -3.2 10.0 5.1 0.8 2.2 3.4 4.0

Global refined consumption 10,136 11,754 12,517 12,672 13,119 13,699 14,316 % change (9.5) 16.0 6.5 0.9 3.9 4.4 4.5

Balance 1,038 534 403 393 181 51 (16) Year end inventory (weeks) 4.8 6.2 6.7 8.3 8.7 8.5 8.1 LME Price ($/ t) 1,655 2,162 2,194 1,950 2,013 2,175 2,200 LME Price (c/lb) 75 98 100 88 91 99 100

000 tonnes 2009 2010 2011 2012 2013E

Refined supply 9,042 9,916 10,600 11,496 12,353% growth -2% 10% 7% 8% 7%Refined consumption 8,872 10,032 10,547 11,373 12,230 % growth (3.0) 13.0 5.0 8.0 8.0 Global balance 170 (116) 52 123 122 LME Price (US$/ t) 1,719 2,149 2,402 2,063 2,163

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 9

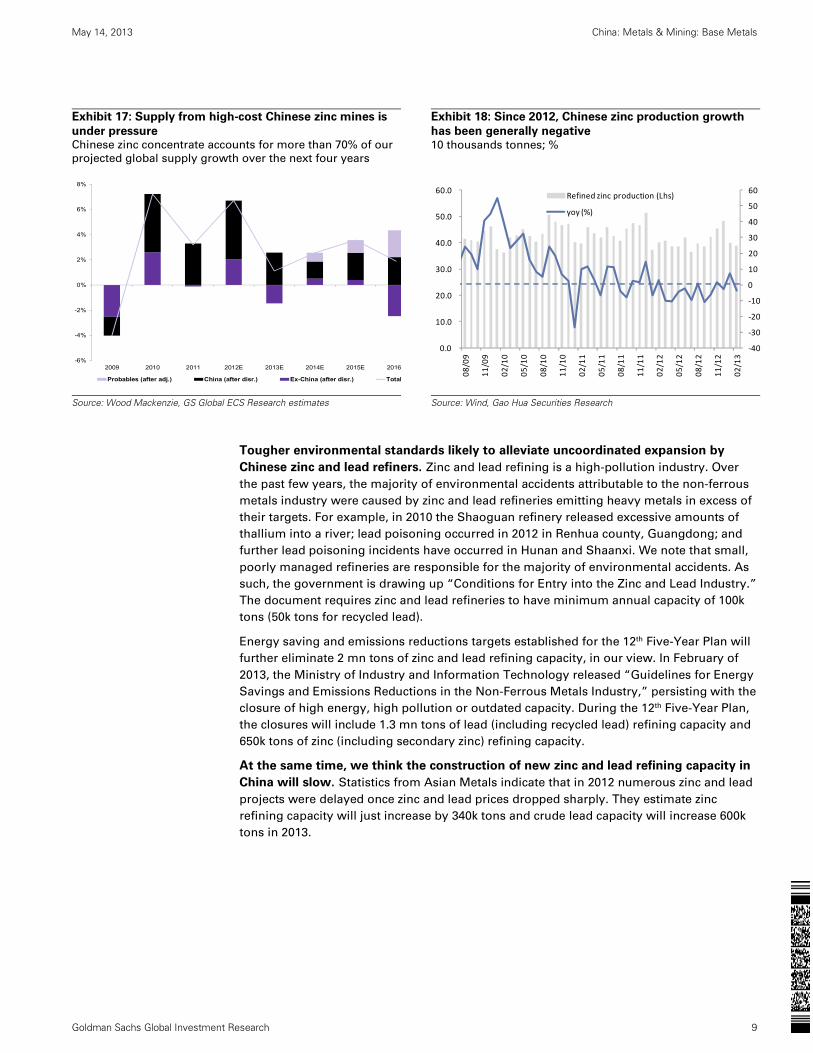

Exhibit 17: Supply from high-cost Chinese zinc mines is

under pressure Chinese zinc concentrate accounts for more than 70% of our

projected global supply growth over the next four years

Exhibit 18: Since 2012, Chinese zinc production growth

has been generally negative 10 thousands tonnes; %

Source: Wood Mackenzie, GS Global ECS Research estimates

Source: Wind, Gao Hua Securities Research

Tougher environmental standards likely to alleviate uncoordinated expansion by

Chinese zinc and lead refiners. Zinc and lead refining is a high-pollution industry. Over

the past few years, the majority of environmental accidents attributable to the non-ferrous

metals industry were caused by zinc and lead refineries emitting heavy metals in excess of

their targets. For example, in 2010 the Shaoguan refinery released excessive amounts of

thallium into a river; lead poisoning occurred in 2012 in Renhua county, Guangdong; and

further lead poisoning incidents have occurred in Hunan and Shaanxi. We note that small,

poorly managed refineries are responsible for the majority of environmental accidents. As

such, the government is drawing up “Conditions for Entry into the Zinc and Lead Industry.”

The document requires zinc and lead refineries to have minimum annual capacity of 100k

tons (50k tons for recycled lead).

Energy saving and emissions reductions targets established for the 12th Five-Year Plan will

further eliminate 2 mn tons of zinc and lead refining capacity, in our view. In February of

2013, the Ministry of Industry and Information Technology released “Guidelines for Energy

Savings and Emissions Reductions in the Non-Ferrous Metals Industry,” persisting with the

closure of high energy, high pollution or outdated capacity. During the 12th Five-Year Plan,

the closures will include 1.3 mn tons of lead (including recycled lead) refining capacity and

650k tons of zinc (including secondary zinc) refining capacity.

At the same time, we think the construction of new zinc and lead refining capacity in

China will slow. Statistics from Asian Metals indicate that in 2012 numerous zinc and lead

projects were delayed once zinc and lead prices dropped sharply. They estimate zinc

refining capacity will just increase by 340k tons and crude lead capacity will increase 600k

tons in 2013.

-6%

-4%

-2%

0%

2%

4%

6%

8%

2009 2010 2011 2012E 2013E 2014E 2015E 2016

Probables (after adj.) China (after disr.) Ex-China (after disr.) Total

‐40

‐30

‐20

‐10

0

10

20

30

40

50

60

0.0

10.0

20.0

30.0

40.0

50.0

60.0

08/09

11/09

02/10

05/10

08/10

11/10

02/11

05/11

08/11

11/11

02/12

05/12

08/12

11/12

02/13

Refined zinc production (Lhs)

yoy (%)

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 10

Exhibit 19: Zinc projects to come online in 2013E

Exhibit 20: Lead projects to come online in 2013E

Source: Asian Metals, Gao Hua Securities Research estimates

Source: Asian Metals, Gao Hua Securities Research estimates

China zinc/lead demand: Urbanization/consumption upgrades likely to be key drivers

Zinc: The completed de-stocking of galvanized sheets may directly drive zinc demand. Since 2009, Chinese production of coated sheets (primarily galvanized sheets) enjoyed

sustained growth, increasing from 19.43 mn tons in 2009 to 37.63 mn tons in 2012 (growth

of 94%). In terms of inventories, galvanized sheet stocks fell to the average level since 2009,

in 2H12. We believe that as the de-stocking process winds down, continued urbanization in

China will increase demand from galvanized sheets.

Exhibit 21: Chinese production of coated sheets has risen

since 2009 Coated sheets are the key demand driver for zinc

Exhibit 22: Galvanized sheet inventories have fallen to

the average level since 2009 The end of de-stocking should drive increased zinc demand

Source: Wind, Gao Hua Securities Research.

Source: Wind, Gao Hua Securities Research.

Real estate sales and car production growth continue to support consumption. Data

from the National Bureau of Statistics indicates that yoy sales growth for commercial

housing in China turned negative for almost a year starting October 2011 but then

rebounded strongly to positive growth in October 2012. The rebound was especially

pronounced in 1Q13, when yoy growth reached 37%. At the same time, housing sales have

driven a clear increase in demand for appliances. In addition, we believe that the auto

industry will further support demand. Our China auto analyst expects 2013E/2014E/2015E

car sales to grow 8.5%/8.5%8%, maintaining a strong growth rate. In 2H12, dealerships’

inventories declined; restocking has been driving a rebound in car production.

CompanyCapacity

expansionCurrentcapacity

Year tocome online

Huize of Chihong 100 380 2013Hulunbeier Chihong 140 380 2013Western Mining 100 160 2013Total in 2013 340Jinding zinc Co. 100 220 2014Yunxi zinc Co. 100 120 2014Xinganmen Boyuan 100 100 2014Huili zinc & lead 100 100 2014Total in 2014 400

Company ProvinceCapacity

expansionYear to

come online

Zhuzhou Smelter Group Hunan 100 Jan-13

Zhantai non-ferrous metals Hunan 100 Mar-13

Hongling zinc & lead mine Inner Mongolia 100 2013

Hulunbeier Chihong Inner Mongolia 60 2013

Huize of Chihong Yunnan 60 2013

Luanchuan Shibao mining Henan 80 2013

Hengbang Smelting Co. Shandong 100 2013

Total in 2013 600

(40)

(20)

0

20

40

60

80

100

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

02/09 08/09 02/10 08/10 02/11 08/11 02/12 08/12 02/13

Coated sheets production yoyKt %

0

5

10

15

20

25

30

35

40

45

50

02/09 08/09 02/10 08/10 02/11 08/11 02/12 08/12 02/13

Galvanized sheets Average from 2009

Kt

Average from 2009

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 11

Exhibit 23: China property sales maintain strong growth

10 thousands sqm; %

Exhibit 24: As per our China auto analyst, China car sales

likely to maintain strong growth

Source: Wind, Gao Hua Securities Research

Source: Wind, Gao Hua Securities Research estimates

Lead: Benefiting from consumption upgrades. Broken down by lead’s end users (2011),

in China, 28% of lead is used in the manufacture of electric scooters, 22% in the automotive

industry, 22% in lead-acid batteries for export and the rest in UPS, motorcycles and other

fields.

Compared with other metals, lead’s downstream uses skew towards consumption. As such,

we expect that consumption upgrades, increased car sales and the replacement of bicycles

with electric scooters in rural areas will drive lead demand growth. We believe production

of cars and electric scooters should enjoy sustained growth during 2013-2015.

Exhibit 25: Chinese lead-acid battery production has

continued to enjoy strong growth over the past 5 years

Exhibit 26: Electric scooter production has increased

rapidly in China

Source: Wind, Gao Hua Securities Research.

Source: Wind, Gao Hua Securities Research.

Car starting batteries are the main application for lead-acid batteries, accounting for about

48% of the market as of 2011, and are a type of consumable that require regular

replacement. As car ownership increases in China, so will the consumption of batteries.

Accordingly, we see China’s increasing car ownership rate as a support for Chinese lead

demand.

‐100%

‐50%

0%

50%

100%

150%

200%

0

100

200

300

400

500

600

700

800

03/09 09/09 03/10 09/10 03/11 09/11 03/12 09/12 03/13

Real estate sales area by daily

yoy (Rhs)

0.8 0.8 1.4 2.3 2.6 3.3

4.3 5.3 5.7

8.6

11.7 12.7

13.9 15.0 16.3

17.6 16.5%

1.7%

80.3%65.7%

13.8%

24.1%32.5%

22.4%

7.4%

51.1%35.4%

8.7% 9.2%8.5% 8.5%

8.0%

-150%

-100%

-50%

0%

50%

100%

0

5

10

15

20

25

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

E

2013

E

2014

E

2015

E

Passenger Car Sales Volume Passenger Car growth rate (YoY) (RHS)

115,735 116,391

142,297 140,695

175,955

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2008 2009 2010 2011 2012

Production of Lead‐acid batteriesKvAh

1,530

30,960

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

China E‐bike productionThousands

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 12

Exhibit 27: Car ownership in China continues to increase rapidly Units: 1 mn cars, %

Source: Wind, Gao Hua Securities Research.

Our supply/demand models for zinc and lead in China

Exhibit 28: China’s zinc supply/demand should trend towards balance in 2013/2014

Source: China Nonferrous Metals Industry Association, Wind, Gao Hua Securities Research estimates.

Exhibit 29: China’s refined lead supply/demand model

Source: China Nonferrous Metals Industry Association, Wind, Gao Hua Securities Research estimates.

7.71

73.27

0%

5%

10%

15%

20%

25%

30%

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Private car ownership in China

yoy (Rhs)

000t 2009 2010 2011 2012 2013E 2014E

China refined zinc capacity 4,425 5,115 5,720 5,800 6,140 6,540Capacity utilization (%) 97% 102% 93% 84% 84% 84%

China refined zinc production 4,286 5,209 5,308 4,847 5,131 5,466yoy (%) 6% 22% 2% -9% 6% 7%

Net import of refined zinc 641 280 301 509 540 512Import 670 323 348 515 550 520Export 29 43 46 6 10 8

China refined zinc supply 4,927 5,489 5,610 5,356 5,671 5,978

China refined zinc demand 4,350 4,850 5081 5285 5,621 5,987Demand growth (%) 5% 11% 5% 4% 6% 7%

Balance 577 639 528 71 50 (9)

000t 2009 2010 2011 2012 2013E 2014E

China refined lead capacity 4,450 4,980 5,382 5,632 5,932 6,232Capacity utilization (%) 85% 83% 79% 82% 82% 82%

China refined lead production 3,773 4,158 4,262 4,646 4,893 5,141 Mined lead production 2,626 2,794 2,836 3,284 3,328 3,290 Recyced lead 1,147 1,364 1,426 1,362 1,566 1,851

Refined lead production yoy (%) 10% 3% 9% 5% 5%Net import of refined lead 134 -2 0 5 0 3

Import 157 22 7 7 5 7Export 23 23 6 2 5 4

China refined lead supply 3,907 4,156 4,262 4,651 4,893 5,144

China refined lead demand 3,650 3,950 4005 4510 4,815 5,179Demand growth (%) 6% 8% 1% 13% 7% 8%

Balance 257 206 257 141 78 (35)

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 13

Operations comparison for A-share zinc and lead firms

We compared China’s two main zinc and lead firms—Zhongjin Lingnan and Chihong—

across multiple dimensions. We looked at the firms’ 2013-2015 zinc and lead concentrate

production growth rate, net profits and sensitivity to zinc and lead prices, production costs

and other operational indicators. We further checked firms’ ratio of interest-bearing bonds

to total invested capital, among other factors, to examine financial pressure. We evaluated

gross margins on zinc and lead operations, ROE and CROCI as indicators of profitability.

Our comparisons lead us to conclude: Chihong’s net profits are more sensitive to zinc

and lead prices and the firm’s production growth also outpaces Zhongjin Lingnan.

Lingnan’s overseas mines have higher operational effectiveness and are more stable.

1. Zinc and lead concentrate production growth: We estimate Chihong‘s zinc and lead

concentrate production growth will reach 10.4% CAGR in 2013E-2015E. If Chihong were to

successfully complete the rights issue and purchase Rongda Mining, the CAGR would

climb to 12% (our base case does not include Rongda). Lingnan is expanding Panlong mine

and entering Potosi and Silver Peak mines into service, pushing its 2013-2015 production

growth to 6.8% CAGR. That , however, remains below Chihong’s rate.

2. Net profit sensitivity to zinc and lead prices. We measured the sensitivity of firms’ net

profits to zinc and lead prices. If zinc and lead prices were to rise by 1%, net profit at

Chihong should rise 4%, whereas the figure for Lingnan is about 2.1%. We think Chihong is

likely to benefit more, as we expect zinc and lead prices to rise in 2014 and 2015.

Exhibit 30: Chihong has greater organic growth

Exhibit 31: Chihong will benefit more from higher prices

Sensitivity of net profit to 1% rise in zinc and lead prices

Source: Company data, Gao Hua Securities Research estimates.

Source: Company data, Gao Hua Securities Research estimates.

3. Production costs for zinc and lead concentrate: Lingnan’s primary mine, Fankou, has

lead grade 5% and zinc grade 9%. We estimate the firm’s 2013 costs to be Rmb4,966 per

ton. In comparison, Huize, Chihong’s primary mine, is of higher quality with lead grade

8.5% and zinc grade 20%. Costs per ton are Rmb4,600, a step below Lingnan’s costs.

4. Gross margins for mining and refining: Lingnan had mining and refining gross margin

of 28.5% in 2012 due to slightly higher production costs. That figure is clearly below

Chihong’s gross margin, which was 39.2% in 2012.

10.4%

6.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Chihong Lingnan

Zinc & Lead concentrate production

growth in 2013-20154%

2%

0%

1%

1%

2%

2%

3%

3%

4%

4%

5%

Chihong Lingnan

Zinc & Lead prices sensitivity to 2013 net profit

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 14

Exhibit 32: We estimate Chihong has lower production

cost as of 2013E…

Exhibit 33: …and better gross mining and refining

margins in 2012

Source: Company data, Gao Hua Securities Research estimates.

Source: Company data, Gao Hua Securities Research.

5. Interest-bearing bonds to total invested capital: We use the ratio of interest-bearing

bonds to total invested capital to measure financial cost pressure (total invested capital is

the sum of interest-bearing bonds and shareholder equity attributable to their parent firm).

As of late 2012, the ratio for Lingnan was 38.6%, where as Chihong’s ratio was76.5%,

indicating a significant amount of financial pressure. Chihong’s high gearing ratio is

primarily due to recent rapid resource expansion. However, the firm’s plan to raise capital

through a rights offering has been approved by CSRC on March 15. If the rights issue were

to be successfully completed, it could help lower Chihong’s interest-bearing bond to total

invested capital ratio to about 45%, alleviating financial pressure once bank loans are

returned.

6. Assets acquired overseas and operations: Lingnan and Chihong, aside from developing

domestic resources, have in recent years continued to look for growth abroad. Lingnan in 2009

acquired Perliya during the financial crisis and that year moved from losses to profit; in 2010 it

again leveraged the Perliya platform to acquire GlobeStar mine and began to develop a variety

of metals. Profitability also became more stable. Chihong in 2010 became involved with one of

the world’s biggest zinc and lead mines—Canada’s Selwyn zinc and lead mine, which is

scheduled to enter service in 2015/2016. Further, Chihong announced in 2012 that it had

acquired a zinc and lead mine in Bolivia. Overall, Lingnan’s overseas operations already

account for 25% (2012) of the company’s net earnings and operational effectiveness is higher

while Chihong’s overseas assets are still under construction.

Exhibit 34: Lingnan is under less financial pressure Lingnan has a more stable asset and debt structure as of

2012

Exhibit 35: Comparison of overseas acquisitions and

operational status Lingnan’s overseas operational efficiency is higher

Source: Company data, Gao Hua Securities Research estimates.

Source: Company data, Gao Hua Securities Research.

4,600

4,966

3,000

3,500

4,000

4,500

5,000

5,500

Huize mine of Chihong Fankou mine of Lingnan

Zinc & Lead concentrate production cost

39.2%

28.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

Chihong Lingnan

Gross margin of mining/smelting

business in 2012

76.5%

38.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Chihong Lingnan

Interest-bearing debt/total invested capitalCompany Overseas resources Operation

Selywn in CanadaScheduled to come online in2015/2016

Zinc & Lead projects in BoliviaAnnounced in Dec 2012 while notcomplete yet

Perilya in Australia

Globestar

Chihong

Lingnan

Made profit in the purchasingyear of Perilya; Profit alsoimproved for Globestar; both ofthem contribute Rmb90 mn(25%) of net profit in 2012

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 15

7. ROE: We expect Lingnan’s ROE to rise to 9.1% in 2013E as zinc and lead prices increase

and the negative influence of environmental accidents fades. That figure outpaces

Chihong’s ROE, which we estimate to be 8.2% in 2013E.

8. CROCI: We estimate Lingnang’s 2013E CROCI will edge up to 11.6% and remain in the

sector’s second quartile for the next three years. For Chihong, which continues to invest

significant sums into new mines, we expect CROCI to slip to 9.3%, placing it in the sector’s

third quartile.

Exhibit 36: Lingnan’s ROE should outpace Chihong in

2013E

Exhibit 37: Lingnan’s CROCI is also outpacing Chihong in

2013E

Source: Company data, Gao Hua Securities Research estimates.

Source: Company data, Gao Hua Securities Research estimates.

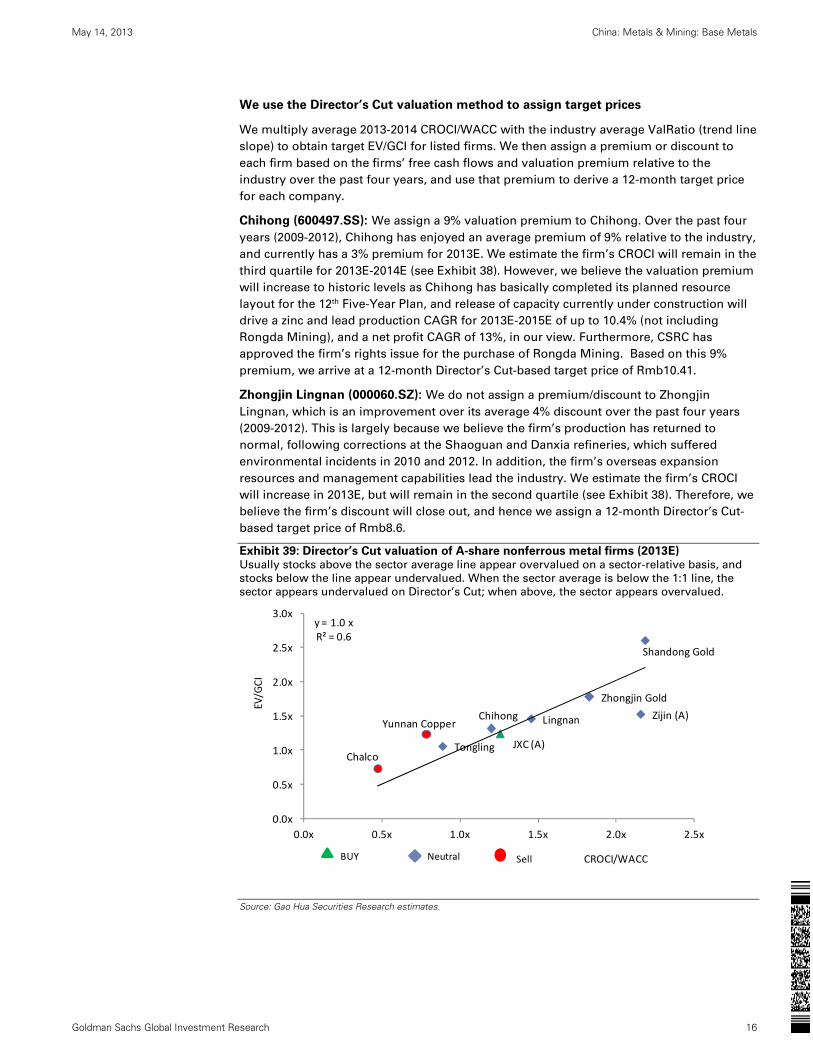

Using Director’s Cut to value zinc and lead firms

We use Director’s Cut methodology for valuing A-share zinc and lead firms, in line

with our other covered commodity stocks. Based on current valuations, the non-

ferrous metals’ industry average EV/GCI vs. CROCI/WACC is 1.0X.

Cash returns on cash invested (CROCI) is a key measure of a firm’s ability to create value.

By comparing firm’s past-three-years and 2013E-2014E CROCI, we divide non-ferrous

metals A-shares into quartiles, with the highest-CROCI firms in the first quartile, and the

lowest-CROCI firms in the fourth quartile.

Exhibit 38: A-share metal firms’ CROCI

Gold firms have higher CROCI while aluminum firms have lower CROCI

Source: Gao Hua Securities Research estimates.

8.2%

9.1%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

Chihong Lingnan

2013E ROE

9.3%

11.6%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

11.0%

11.5%

12.0%

Chihong Lingnan

2013E CROCI

Ticker Company 2010 2011 2012 2013E 2014E 2015E

600362.SS Jiangxi Copper 2 2 2 2 2 2000630.SZ Tongling 3 3 4 3 3 3000878.SZ Yunnan Copper 2 4 2 4 4 4000060.SZ Zhongjin Lingnan 4 2 3 2 2 2600497.SS Chihong 3 3 3 3 3 3601600.SS Chalco 4 4 4 4 4 4600489.SS Zhongjin Gold 1 1 1 1 1 1600547.SS Shandong Gold 1 1 1 1 1 1601899.SS Zijin Mining 1 1 1 1 1 1

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 16

We use the Director’s Cut valuation method to assign target prices

We multiply average 2013-2014 CROCI/WACC with the industry average ValRatio (trend line

slope) to obtain target EV/GCI for listed firms. We then assign a premium or discount to

each firm based on the firms’ free cash flows and valuation premium relative to the

industry over the past four years, and use that premium to derive a 12-month target price

for each company.

Chihong (600497.SS): We assign a 9% valuation premium to Chihong. Over the past four

years (2009-2012), Chihong has enjoyed an average premium of 9% relative to the industry,

and currently has a 3% premium for 2013E. We estimate the firm’s CROCI will remain in the

third quartile for 2013E-2014E (see Exhibit 38). However, we believe the valuation premium

will increase to historic levels as Chihong has basically completed its planned resource

layout for the 12th Five-Year Plan, and release of capacity currently under construction will

drive a zinc and lead production CAGR for 2013E-2015E of up to 10.4% (not including

Rongda Mining), and a net profit CAGR of 13%, in our view. Furthermore, CSRC has

approved the firm’s rights issue for the purchase of Rongda Mining. Based on this 9%

premium, we arrive at a 12-month Director’s Cut-based target price of Rmb10.41.

Zhongjin Lingnan (000060.SZ): We do not assign a premium/discount to Zhongjin

Lingnan, which is an improvement over its average 4% discount over the past four years

(2009-2012). This is largely because we believe the firm’s production has returned to

normal, following corrections at the Shaoguan and Danxia refineries, which suffered

environmental incidents in 2010 and 2012. In addition, the firm’s overseas expansion

resources and management capabilities lead the industry. We estimate the firm’s CROCI

will increase in 2013E, but will remain in the second quartile (see Exhibit 38). Therefore, we

believe the firm’s discount will close out, and hence we assign a 12-month Director’s Cut-

based target price of Rmb8.6.

Exhibit 39: Director’s Cut valuation of A-share nonferrous metal firms (2013E) Usually stocks above the sector average line appear overvalued on a sector-relative basis, and

stocks below the line appear undervalued. When the sector average is below the 1:1 line, the

sector appears undervalued on Director’s Cut; when above, the sector appears overvalued.

Source: Gao Hua Securities Research estimates.

JXC (A)Tongling

Yunnan Copper LingnanChihong

Chalco

Zhongjin Gold

Shandong Gold

Zijin (A)

y = 1.0 xR² = 0.6

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

0.0x 0.5x 1.0x 1.5x 2.0x 2.5x

EV/GCI

CROCI/WACCNeutralBUY Sell

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 17

Exhibit 40: Director’s Cut derivation of 12-month target prices; we rate both Chihong and

Zhongjin Lingnan Neutral

Source: Company data, Datastream, Gao Hua Securities Research estimates.

Zhongjin Lingnan Chihong Ave CROCI (2013E-2014E) 11.5% 9.2%Sector Valratio (EV/GCI vs. CROCI/WACC) 1.0x 1.0xValuation prem./disc.Adjustment 0% 9%Historical premium/discount -4% 9%Adjusted Valratio 1.0x 1.1xCROCI/WACC (2013E-2014E) 1.4x 1.2xTarget EV/GCI 1.5x 1.3xGCI (mn) 14,613 22,102Minority interests 1,611 2,529Net debt 2,099 12,231MV (pricing currency mn) 17,743 13,635Share outstanding (mn) 2,063 1,31012M Target price 8.60 10.41 Rating Neutral NeutralPotential upside (%) -4.1% -12.5%Current price (2013/5/10) 9.0 11.9

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 18

Chihong (600497.SS, Neutral): Resources acquired, awaiting profits

Investment view

We resume coverage on Chihong with a Neutral rating and a 12-m

Director’s Cut-based target price of Rmb10.41, implying 12.5% downside

potential. We believe the firm’s core growth driver will be the release of

capacity from acquired mines beginning production. In addition, we

believe the potential acquisition and consolidation of Rongda Mining

through a rights issue, if successfully completed, could be accretive to

earnings, and help lower the firm’s financial cost. However, with the

firm’s 2013E/2014E CROCI in the third quartile, and a 2013E P/E ratio of

48.9X—above the industry median—we assign a Neutral rating.

Key growth drivers

The firm may meet its 12th Five-Year Plan resource target early.At the end of 2009, Chihong set strategic targets for the 12th Five-Year

Plan: zinc and lead resources reaching 10mt by 2015, and refining

capacity of 1mt. Over the past three years, the firm has expanded its

resources through domestic consolidation and overseas purchases. In

terms of smelting production, the Huize 160k t smelting project is

scheduled to begin production in 2H13, and the 200k t Hulunbuir facility

is slated to start operations in late 2013.

Potential acquisition and consolidation of Rongda Mining could be earnings accretive. Chihong’s application for a rights issue has

been approved by the CSRC on March 15, and it plans to use Rmb2.1 bn

for acquiring a 51% stake in Rongda Mining held by the parent company

Yunnan Metallurgical Group (our base case does not include assets from

Rongda Mining). Rongda had net profits attributable to the parent

company of Rmb363 mn in 2012, 51% of which would imply Rmb185

mn. If Chihong’s rights issue and Rongda acquisition were to be

successfully completed, we estimate Rongda could potentially

contribute Rmb0.11 to Chihong’s 2013E EPS. Furthermore, the company

announced that the rights issue will raise not more than Rmb5 bn, of

which Rmb2.1 bn will be used to acquire the 51% stake in Rongda, and

the rest will be deposited in the bank, potentially lowering the firm’s

asset-liability ratio to around 53%.

Valuation

From 2009-2012, Chihong saw a 9% valuation premium on average. It is

currently at 3%; but we think if the rights issue were to be successfully

completed, earnings updates post the potential purchase of Rongda may

help raise the premium closer to the historical average. We apply a 9%

valuation premium and arrive at our 12-month Director’s Cut-based

target price of Rmb10.41.

Risks

Downside: An “environmental tax” levied on the firm’s products;

Upside: Faster-than-expected progress on projects under construction.

Growth

Returns *

Multiple

Volatility Volatility

Multiple

Returns *

Growth

Investment Profile

Low High

Percentile 20th 40th 60th 80th 100th

* Returns = Return on Capital For a complete description of the investment

profile measures please refer to the

disclosure section of this document.

Yunnan Chihong Zinc & Germanium (600497.SS)

Asia Pacific Metals & Mining Peer Group Average

Key data Current

Price (Rmb) 11.89

12 month price target (Rmb) 10.41

Market cap (Rmb mn / US$ mn) 15,577.0 / 2,536.3

Foreign ownership (%) --

12/12 12/13E 12/14E 12/15E

EPS (Rmb) 0.27 0.24 0.32 0.39

EPS growth (%) 1.6 (8.5) 29.8 22.5

EPS (diluted) (Rmb) 0.27 0.24 0.32 0.39

EPS (basic pre-ex) (Rmb) 0.27 0.24 0.32 0.39

P/E (X) 52.6 48.9 37.7 30.8

P/B (X) 4.8 4.0 3.7 3.5

EV/EBITDA (X) 24.2 14.9 13.5 13.0

Dividend yield (%) 1.4 1.0 1.3 1.6

ROE (%) 9.3 8.2 10.3 11.7

CROCI (%) 10.5 9.3 9.1 8.9

2,000

2,100

2,200

2,300

2,400

2,500

2,600

2,700

10

11

12

13

14

15

16

17

May-12 Aug-12 Nov-12 Feb-13

Price performance chart

Yunnan Chihong Zinc & Germanium (L) Shanghai SE A Share Index (R)

Share price performance (%) 3 month 6 month 12 month

Absolute (24.1) (1.9) (24.5)

Rel. to Shanghai SE A Share Index (17.8) (9.6) (19.0)

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 5/10/2013 close.

INVESTMENT LIST MEMBERSHIP

Neutral

Coverage View: Neutral

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 19

Yunnan Chihong Zinc & Germanium: Summary financials

Profit model (Rmb mn) 12/12 12/13E 12/14E 12/15E Balance sheet (Rmb mn) 12/12 12/13E 12/14E 12/15E

Total revenue 12,130.4 16,558.8 19,759.2 21,342.4 Cash & equivalents 1,171.0 1,205.1 1,466.4 1,221.5

Cost of goods sold (10,287.1) (14,526.3) (17,492.7) (18,903.6) Accounts receivable 1,296.7 1,879.0 1,910.4 2,182.6

SG&A (848.5) (853.6) (951.9) (1,024.3) Inventory 1,277.0 1,906.8 1,927.2 2,216.0

R&D -- -- -- -- Other current assets 0.0 0.0 0.0 0.0

Other operating profit/(expense) (57.4) (47.9) (53.5) (57.5) Total current assets 3,744.7 4,990.9 5,304.0 5,620.2

EBITDA 1,324.9 2,039.8 2,184.6 2,298.4 Net PP&E 12,234.1 13,195.5 13,474.3 13,814.4

Depreciation & amortization (387.5) (908.9) (923.5) (941.4) Net intangibles 5,215.8 5,001.4 4,787.1 4,572.7

EBIT 937.4 1,130.9 1,261.1 1,357.0 Total investments 819.3 819.3 819.3 819.3

Interest income 8.2 14.5 14.9 18.1 Other long-term assets 204.4 279.0 332.9 359.6

Interest expense (600.8) (755.6) (770.2) (755.6) Total assets 22,218.3 24,286.1 24,717.6 25,186.2

Income/(loss) from uncons. subs. 39.4 0.0 0.0 0.0

Others 32.1 0.0 0.0 0.0 Accounts payable 2,794.3 3,573.4 4,094.7 4,191.8

Pretax profits 416.4 389.8 505.8 619.5 Short-term debt 7,587.8 8,087.8 7,587.8 7,587.8

Income tax (74.6) (77.1) (100.0) (122.5) Other current liabilities 0.0 0.0 0.0 0.0

Minorities 6.1 5.5 7.2 8.8 Total current liabilities 10,382.1 11,661.1 11,682.4 11,779.6

Long-term debt 4,848.5 5,348.5 5,348.5 5,348.5

Net income pre-preferred dividends 347.9 318.2 413.0 505.8 Other long-term liabilities 619.8 846.1 1,009.6 1,090.5

Preferred dividends 0.0 0.0 0.0 0.0 Total long-term liabilities 5,468.3 6,194.5 6,358.0 6,438.9

Net income (pre-exceptionals) 347.9 318.2 413.0 505.8 Total liabilities 15,850.3 17,855.6 18,040.5 18,218.5

Post-tax exceptionals 0.0 0.0 0.0 0.0

Net income 347.9 318.2 413.0 505.8 Preferred shares 0.0 0.0 0.0 0.0

Total common equity 3,833.2 3,901.3 4,155.2 4,454.5

EPS (basic, pre-except) (Rmb) 0.27 0.24 0.32 0.39 Minority interest 2,534.7 2,529.2 2,522.0 2,513.2

EPS (basic, post-except) (Rmb) 0.27 0.24 0.32 0.39

EPS (diluted, post-except) (Rmb) 0.27 0.24 0.32 0.39 Total liabilities & equity 22,218.3 24,286.1 24,717.6 25,186.2

DPS (Rmb) 0.19 0.12 0.16 0.19

Dividend payout ratio (%) 71.9 50.0 50.0 50.0 BVPS (Rmb) 2.93 2.98 3.17 3.40

Free cash flow yield (%) (5.6) (4.0) 5.1 (0.2)

Growth & margins (%) 12/12 12/13E 12/14E 12/15E Ratios 12/12 12/13E 12/14E 12/15E

Sales growth 92.1 36.5 19.3 8.0 CROCI (%) 10.5 9.3 9.1 8.9

EBITDA growth 22.6 54.0 7.1 5.2 ROE (%) 9.3 8.2 10.3 11.7

EBIT growth 34.6 20.6 11.5 7.6 ROA (%) 1.9 1.4 1.7 2.0

Net income growth (3.1) (8.5) 29.8 22.5 ROACE (%) 5.6 5.0 5.5 5.9

EPS growth 1.6 (8.5) 29.8 22.5 Inventory days 54.0 40.0 40.0 40.0

Gross margin 15.2 12.3 11.5 11.4 Receivables days 47.1 35.0 35.0 35.0

EBITDA margin 10.9 12.3 11.1 10.8 Payable days 97.7 80.0 80.0 80.0

EBIT margin 7.7 6.8 6.4 6.4 Net debt/equity (%) 176.9 190.2 171.8 168.1

Interest cover - EBIT (X) 1.6 1.5 1.7 1.8

Cash flow statement (Rmb mn) 12/12 12/13E 12/14E 12/15E Valuation 12/12 12/13E 12/14E 12/15E

Net income pre-preferred dividends 347.9 318.2 413.0 505.8

D&A add-back 387.5 908.9 923.5 941.4 P/E (analyst) (X) 52.6 48.9 37.7 30.8

Minorities interests add-back (6.1) (5.5) (7.2) (8.8) P/B (X) 4.8 4.0 3.7 3.5

Net (inc)/dec working capital 84.1 (433.1) 469.5 (463.9) EV/EBITDA (X) 24.2 14.9 13.5 13.0

Other operating cash flow 546.0 151.7 109.6 54.2 EV/GCI (X) 1.6 1.4 1.3 1.2

Cash flow from operations 1,359.4 940.1 1,908.4 1,028.8 Dividend yield (%) 1.4 1.0 1.3 1.6

Capital expenditures (2,534.5) (1,655.9) (988.0) (1,067.1)

Acquisitions (1,433.7) 0.0 0.0 0.0

Divestitures 0.0 0.0 0.0 0.0

Others (138.4) 0.0 0.0 0.0

Cash flow from investments (4,106.6) (1,655.9) (988.0) (1,067.1)

Dividends paid (common & pref) (196.5) (250.1) (159.1) (206.5)

Inc/(dec) in debt 3,815.6 1,000.0 (500.0) 0.0

Common stock issuance (repurchase) 421.8 0.0 0.0 0.0

Other financing cash flows (789.2) 0.0 0.0 0.0

Cash flow from financing 3,251.6 749.9 (659.1) (206.5)

Total cash flow 504.4 34.1 261.3 (244.8) Note: Last actual year may include reported and estimated data.

Source: Company data, Goldman Sachs Research estimates.

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 20

Resource strategy promotes sustained growth

Chihong has the potential to meet its resource goals early. At the end of 2009, Chihong

set strategic targets for the 12th Five-Year Plan: zinc and lead resources reach 10mt by 2015,

and refining capacity of 1mt. Over the past three years, the firm has expanded its

resources: In April 2011, it purchased Yongchang mine, Lancang Lead mine and

Daxing’anling Mining, increasing its zinc and lead holdings by 1.32mt; in 2011, it also

purchased Jinxin Mining, increasing its zinc and lead holdings by 155k t; in December 2012,

it announced the purchase of Bolivian Yangfan mine, D Copper mine, and Amazon Mining;

in March 2013, the firm signed an agreement with Selwyn to purchase the remaining 50%

equity stake in the Selwyn-Chihong joint venture; further, Chihong’s application for a rights

issue has been approved by the CSRC on March 15, and it plans to use the money raised to

acquire 51% stake in Rongda Mining. We believe that, if the above projects all progress

smoothly, the firm has the potential to increase its resource holdings from 3mt in 2009 to

10mt in 2013, meeting its 12th Five-Year Plan resource targets early.

Exhibit 41: Zinc and lead reserves controlled by the firm, as of 2012

Source: Company data, Gao Hua Securities Research

Exhibit 42: Zinc and lead projects with announced purchases in progress, as of March 2013

Source: Company data, Gao Hua Securities Research.

Smelting capacity is likely to be released gradually over the next two years. The firm’s

160k t Huize refinery project (60k t/a crude lead, 100k t/a refined zinc and comprehensive

slag utilization process) is scheduled to begin trial production, and is likely to begin normal

production in 2H13. The 200k t Hulunbuir refinery (140k t/a zinc, 60k t/a lead refining) is

likely to begin production at the end of 2013, according to the company.

OreKt Zinc (%) Lead (%) Silver (g/ t) Zinc (kt) Lead (kt) Silver (t)

Huize mine 100% 3,756 20.2% 8.5% 757 321 0Zhaotong Yiliang mine 100% 1,610 14.0% 3.0% 46.0 225 48 74Yongchang mine 93% 5,318 7.3% 3.0% 159.5 397 173 33Lancang mine 100% 5,619 3.3% 4.6% 156.7 280 272 1,206Daxing'anling Mining 100% 7,240 2.1% 0.7% 149 52Jinxin mining 100% 4,081 3.5% 0.3% 142 13 442Hulunbuir Chihong 50%Selwyn in Canada 50% 16,063 10.3% 4.2% 1,646 679Total 3,598 1,558 1,755

Zinc & Lead mines EquityGrade Resources

OreKt Zinc (kt) Lead (kt) Silver (t) Copper (kt)

Mines announced to acquire

Rongda mine 51% 526 426 2,057 49

D copper mine in Bolivia 835

Yangfan mine in Bolivia 817

Amazon mining in Bolivia 1,007

Zinc & Lead mines EquityResources

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 21

Potential consolidation of Rongda accretive to earnings

The firm’s application for a rights issue was approved by the CSRC on March 15, and

Chihong has announced that it will use the money raised to acquire Yunnan Metallurgical

Group’s 51% stake in Rongda Mining (our base case does not include assets from Rongda).

Rongda and its wholly owned subsidiary Yishengyuan Mining have approval for four

mines with total zinc and lead reserves of 952k t, 2057 t of silver, and 49k t of copper. In

2012, Rongda realized net profits attributable to the parent company of Rmb363 mn, with a

51% stake implying Rmb185 mn. Assuming Chihong’s rights issue and Rongda purchase

were to be successfully completed, on Chihong’s 2012 earnings it would about 15%

accretive.

We believe the potential rights issue could also improve the firm’s asset-liability

structure, lowering financial costs. As of end-2012, Chihong had an asset-liability ratio of

71%, with interest-bearing debt of over Rmb12 bn. Financial costs for the firm in 2012

reached Rmb600 mn, significantly higher than the firm’s 2012 net profit attributable to the

parent company of Rmb350 mn. Based on the company’s announcements, the rights issue

will raise not more than Rmb5 bn, of which Rmb2.1 bn will be used to acquire the 51%

stake in Rongda, and the rest will be deposited in the bank. We calculate that this could

lower the firm’s asset-liability ratio to 53%, saving approximately Rmb180 mn in financial

costs in 2013.

Exhibit 43: Scenario analysis: EPS after potential

consolidation of Rongda (based on share capital after

rights issue)

Exhibit 44: Asset-liability ratio before and after potential

rights issue, as of 2012

Source: Company data, Gao Hua Securities Research estimates.

Source: Company data, Gao Hua Securities Research estimates.

Further profit contributions will have to wait until capacity release from the

purchased overseas resources. Although the firm has increased its resources relatively

rapidly over the past few years, earnings from the Yongchang and Lancang zinc and lead

mines have been relatively weak due to geologic conditions; Jinxin Mining has just

received resource registration; Selwyn-Chihong Mining is scheduled to begin production

at the end of 2015, contributing in 2016. Therefore, we estimate relatively slow 2013E/2014E

zinc and lead concentrate production growth (8.1%/8.0% from7.8% in 2012), while the start

of zinc and lead concentrate production at Selwyn-Chihong would potentially lead to a

15.2% growth in 2015E.

0.27

0.31

0.22

0.24

0.26

0.28

0.3

0.32

No consolidation Consolidated Rongda mine

2012 EPS 71%

53%

0%

10%

20%

30%

40%

50%

60%

70%

80%

No consolidation Consolidated Rongda mine

Asset-liability ratio

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 22

Scattered metals are an important source of profits

The company’s key scattered metals include germanium and cadmium. Presently, Chihong

has 30 tons of annual germanium capacity and is constructing 800 tons of annual cadmium

capacity.

Chihong’s main germanium products are pure germanium and germanium dioxide, and

most of which are used in optical instruments or military applications, with stable orders.

In 2011, Chihong produced 5.56 tons of pure germanium and 11.64 tons of germanium

dioxide, accounting for 6.2% of gross earnings. In 2012, we estimate Chihong sold only 10

tons of germanium products and the contribution to gross earnings declined to 2% as

prices and sales volumes declined. But germanium prices have been among the strongest

performers in metals in 2013, rising 7% since the start of the year. As a result, we expect

the contribution of germanium products to earnings to increase.

Exhibit 45: Price trends for germanium products

Exhibit 46: Price trends for cadmium ingot

Source: Asian Metals, Gao Hua Securities Research.

Source: Asian Metals, Gao Hua Securities Research.

Potential environmental tax on lead may be a headwind for Chihong

The Economic Information newspaper reported on March 12, 2013, that the Ministry of

Finance will accelerate reforms to the environmental protection tax. The move will place an

environmental protection tax on products that contain lead or other highly polluting

materials. In 2012, lead products accounted for 8% of Chihong’s total income (not including

lead product trade income). We perform a scenario analysis on the environmental

protection tax rate as below.

Exhibit 47: Scenario analysis of the impact of an environmental tax on Chihong in 2013 Our base case is no environmental tax

Source: Gao Hua Securities Research estimates.

0

2000

4000

6000

8000

10000

12000

14000

05/09 11/09 05/10 11/10 05/11 11/11 05/12 11/12 05/13

Germanium oxide 99.99% min

Germanium metal 99.99% min

Rmb/t

0

5000

10000

15000

20000

25000

30000

35000

40000

05/09 11/09 05/10 11/10 05/11 11/11 05/12 11/12 05/13

Cadmium ingot Rmb/t

1% 3% 5%Net profit changes (%) 0 -2.0% -6.2% -10.3%

Environmental tax rateBase case - Noenvironmental tax

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 23

Director’s Cut target price of Rmb10.41; Neutral rating

CROCI to remain in the third quartile. We think Chihong’s strong organic growth will

help its net profit growth rate outpace Lingnan, its peer. Despite this, we believe Chihong’s

2013E/2014E/2015E CROCI will edge down to 9.3%/9.1%/8.9%, from 10.5% in 2012, primarily

because the firm will continue to make significant capital expenditures over this period and

the release of capacity from mines under construction will likely be slow.

Chihong’s EV/GCI vs. CROCI/WACC premium relative to the industry is likely to rise to its historical average. Over the past four years (2009-2012), Chihong averaged a

9% premium to the industry, but at present that premium has slipped to 3%. But we think

its premium is likely to climb to its historical average, because the company has completed

its resource layout for the 12th Five-Year plan and capacity from mines under construction

should drive zinc and lead ore concentrate production growth of 10.4% CAGR from 2013E-

2015E (not including Rongda). Further, the CSRC has already approved Chihong’s rights

offering to acquire Rongda, the successful completion of which would also support

Chihong’s premium, in our view.

We derive our 12-m Director’s Cut target price of Rmb10.41 and resume coverage with a Neutral rating. Our 12-month target price of Rmb10.41 is based on a

target premium of 9%. Our target price implies 12.5% potential downside.

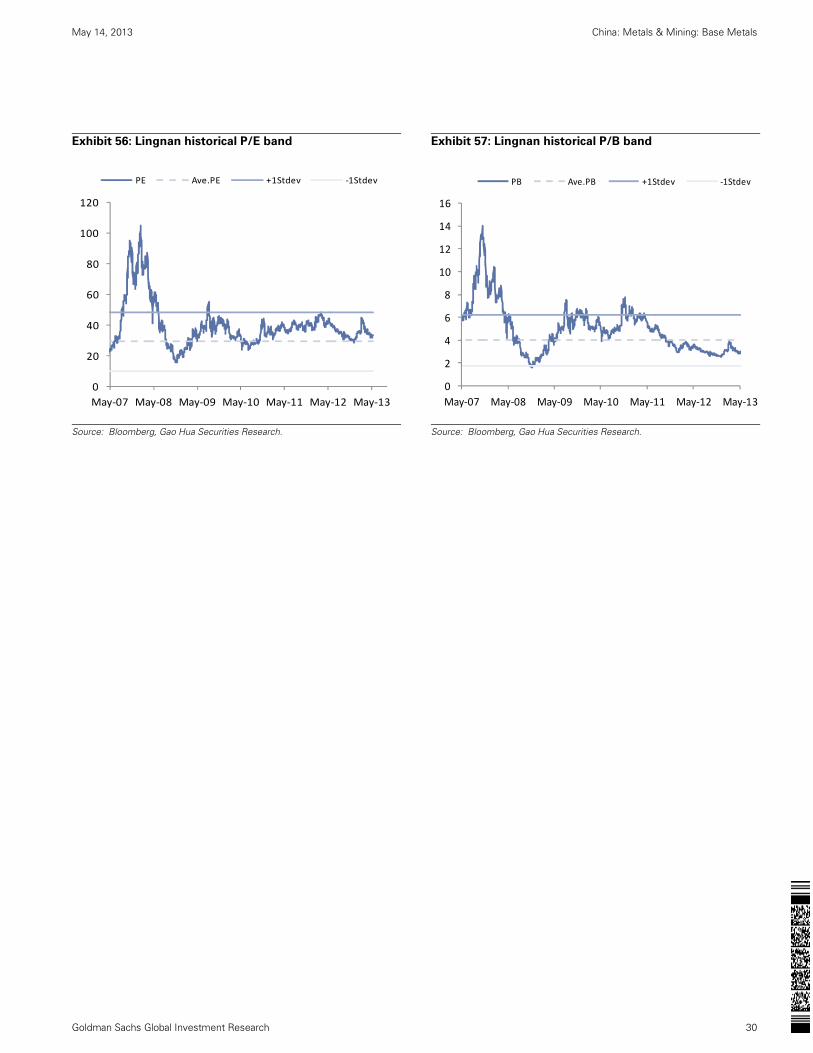

Exhibit 48: Chihong’s historical P/E band

Exhibit 49: Chihong’s historical P/B band

Source: Bloomberg, Gao Hua Securities Research estimates.

Source: Bloomberg, Gao Hua Securities Research estimates.

0

50

100

150

200

250

May‐07 May‐08 May‐09 May‐10 May‐11 May‐12 May‐13

PE Ave.PE +1Stdev ‐1Stdev

0

10

20

30

40

50

60

70

80

90

Ma

y/0

5

No

v/0

5

Ma

y/0

6

No

v/0

6

Ma

y/0

7

No

v/0

7

Ma

y/0

8

No

v/0

8

Ma

y/0

9

No

v/0

9

Ma

y/1

0

No

v/1

0

Ma

y/1

1

No

v/1

1

Ma

y/1

2

No

v/1

2

Ma

y/1

3

Share price 0.50X 1.50X 2.50X

3.50X 4.50X 6.50X

May 14, 2013 China: Metals & Mining: Base Metals

Goldman Sachs Global Investment Research 24

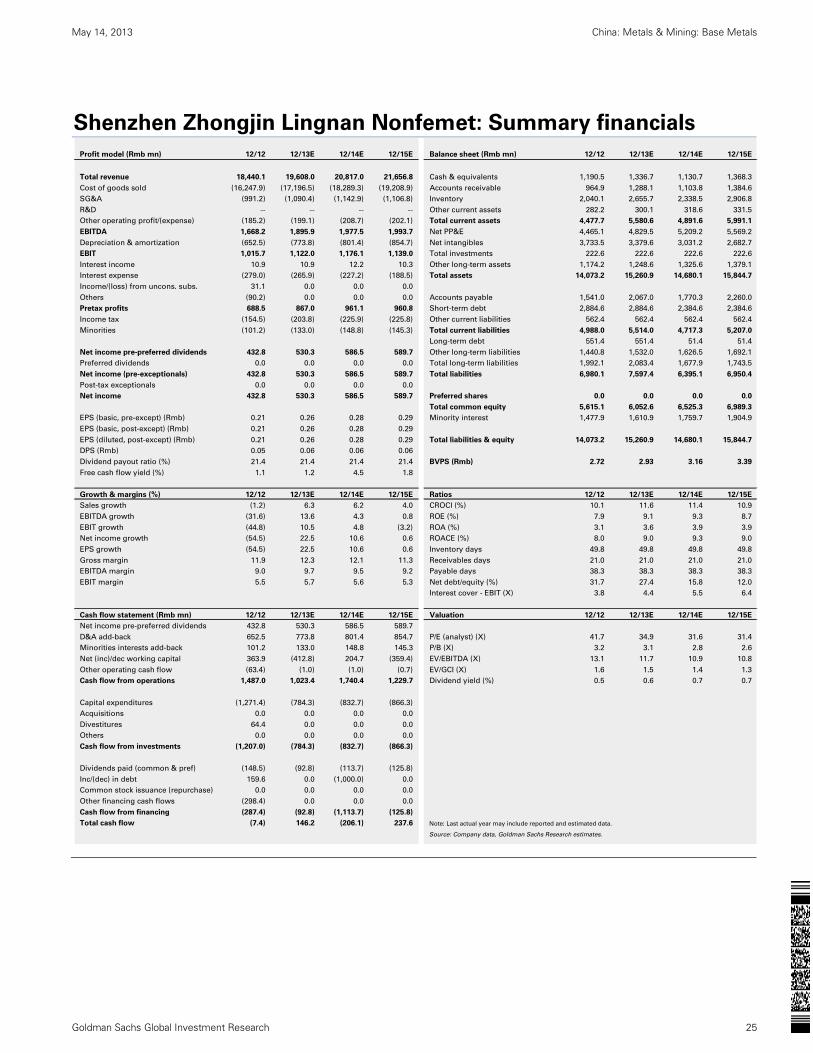

Zhongjin Lingnan (000060.SZ, Neutral): Back to normal operations

Investment view