China Dairy Market Update April 30, 2013 - Orrani Consulting Consulting - ADPI Slides for...

31

China Dairy Market Update April 30, 2013

Transcript of China Dairy Market Update April 30, 2013 - Orrani Consulting Consulting - ADPI Slides for...

China Dairy

Market Update

April 30, 2013

Introduction –

Orrani Consulting

International Dairy Industry Projects

Cheese route to market study - Russia

Dairy market entry – Thailand

Dairy partner search – SEA

Dairy supply & demand study – India

Dairy market

entry study – Iraq

Whey ingredient

opportunity study -

China

Dairy foodservice brand

development – China

Artisanal /

speciality

cheese

market

entry study

– US

Dairy trade

policy

analysis for

whey JV –

Brazil

Dairy ingredient

study – Vietnam

Infant formula market

entry – Philippines

Dairy export

strategy –

Scotland

Organic milk study – China

Dairy market

assessment –

West Africa

Cheese export strategy

– Greece Yoghurt/dessert

study – Japan

Yoghurt/dessert

study – Latin

America

Baby foods

market

assessment –

Mexico

Dairy export study

– Caribbean

Dairy market entry

study – South

Africa

Dairy ingredient assessment - Russia

Dairy export study

– Mauritius

Dairy sector

review – Sub-

Saharan Africa

Dairy trade visit hosting -

Indonesia

Cheese & butter marketing program – Asia

Global dairy buyer survey – Asia, Latin America, MENA,

Europe

Global dairy commodity trade/policy/economics analysis

Strategic review, dairy

industry – Australasia

Whey market

assessment –

Canada

Due diligence

assessment

– US

China ‒ Major Ongoing Change

Continuing Period of National Change

President

Hu Jintao

Li Keqiang Wen Jiabao

Xi Jinping

(& Peng Liyuan!)

Premier

In Out

China is the world factory for food re-exporting

after processing

Now a key market for imported food

with increased domestic consumption

China Food Market – Changes • Gap between import & export has

increased from almost zero in 2006

• H1 2012 ‒ food imports were $54.72

billion, 2 x the export value

• Forecast to become the world’s

largest consumer of imported foods

Limited market for high-value food items due to

low purchasing power

Market entries for diverse range of

premium food products

• Ever-increasing disposable income

makes imported goods affordable

• Diverse premium imported foods are

now widely available in China

market and are selling well

China Food Market – Changes

Immature sales networks

and underdeveloped facilities

Strong advances in different channels

• Retail ‒ Set to be the 3rd largest

retail market by 2025 ($2 trillion)

• Foodservice ‒ 30,000+ western

style restaurants

• Logistics ‒ 20,000+ cold stores

Chinese consumers very price sensitive

Growing consumer awareness of

quality and safety of food due to:

- Increasing number of food safety scandals - More exposure to foreign cultures/lifestyles - One-child policy, young generation, white

collars

• Consumer shift from price- to

quality-orientation

• Willing to spend up to 20% more

for premium food products with

quality and safety guaranteed

Per Capita Disposable Income in China

– Urban Residents

RMB24,565 = Close to $4,000

10,493

11,760

13,786

15,781

17,175

19,109

21,810

24,565

-

5,000

10,000

15,000

20,000

25,000

30,000

2006 2007 2008 2009 2010 2011 2012 2013

RM

B

Recent Openings Outside Tier 1 Cities

• Starbucks in Datong (Tier 3), Apple in Chengdu (Tier 2)

• 2013 opening of the world’s largest freestanding shopping mall in

Tianjin, 30 minutes from Beijing by high-speed train: 530,000 m2 −

larger than 74 soccer fields!

Example – World’s Largest Shopping Mall

Dairy in China ‒

Trends and Opportunities

Dairy Farming Development Ongoing

• Supply/demand gap remains

• Production 37.44 million MT in 2012, up only 5%

• Demand 40-41 million MT

• Fonterra predicts national demand of 70 billion L by 2020

• 5YP of September 2011 targets

• 38% of cows on large-scale dairy farms (100+ cows) by 2015 (vs 28%)

• Many regional governments had earlier pushed in similar direction

• Examples of key investments in large-scale farms in 2012

• January: Nestlé − $395 million, 5 yr program, Heilongjiang

• June: New Hope − $158 million, 3-5 years, East China, Sichuan, Yunnan

• August: Yili − $190 million in 2012 alone (after $1.2 billion 2007-2011)

• September: Mengniu − $553 million, next 5 years

Dairy Industry Output Recovering

• Output up from 23.8 to 25.5 million MT

1,658 1,534

1,784 1,839 1,854

2,095 2,231 2,116 2,143 2,086

2,148 2,341

1,763 1,711

1,964 1,909

1,989

2,152 2,095 2,129

2,474

2,256

2,458 2,551

100

600

1,100

1,600

2,100

2,600

3,100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

'000 MT

2011 2012 Linear (2012)

Source: Dairy Association of China

Regional Perspectives – 2012 Output

3,257 3,207

2,726

1,858

1,677

-15%

2.9%

1.3%

4.2%

5.7%

-20%

-15%

-10%

-5%

0%

5%

10%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

IMAR Shandong Hebei Heilongjiang Henan

'000 MT

Output Growth rate

• IMAR output down 15% in 2012, but other key regions grew

Source: Dairy Association of China

Import Demand Still Trending Upwards

405,557

167,553

378,380

91,282

48,326 38,806

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

WMP SMP Whey Infant Formula Butter Cheese

MT

2008

2009

2010

2011

2012

WMP

imports -

124,775 MT

in Jan-Feb

2013, up

50% vs. Jan-

Feb 2012

23% NL

18% NZ

17%FR

What impact

could a

China-US

FTA have on

trade?

Source: China Customs

96% NZ 63% NZ

11% US

46% US

15% FR

89% NZ 44% NZ

24% US

20% AUS

Rising Farmgate Prices

• The raw milk price in China increased constantly in 2012-2013 due to

• Rising prices of corn (+4% y-o-y in March) and soy meal (+23%)

• Increasing demand

• Trend likely to continue in 2013 ‒ 8% rise?

• Shanghai: current base price of RMB4/kg ‒ $0.65

0.54 0.54

0.54 0.55

0.50

0.52

0.54

0.56

0.58

0.60

December January February March

$/k

g

Source: Dairy Association of China

Retail Prices Following Suit

1.42

1.48

1.86

1.99

1.30

1.40

1.50

1.60

1.70

1.80

1.90

2.00

US

D/k

g

Milk Products

Yoghurt

30.59

32.10

22.80

24.57

20

22

24

26

28

30

32

34

US

D/k

g

Multinational IF

Domestic IF

Source: Ministry of Commerce

Food Safety Remains Work in Progress

• March 10 − new “superministry” − General Food

& Drug Administration to take over tasks from

• Ministry of Agriculture ‒ focused on milk

production/collection/distribution

• General Administration of Quality Supervision,

Inspection & Quarantine (AQSIQ) ‒ dealing with

imported and local foods

• State Administration of Industry and Commerce (SAIC)

– products from factory door to point of sale

• Ministry of Health/MOH – approves foods/substances

with no local standard

• Bureau of Public Security/BPS – enforces Criminal Law

• Regulations are being continually overhauled

• Mainstream foreign brands = “reassuringly expensive”

Key requirement − more prevention and less reaction

Y-o-Y Growth ‒ How’s the Local Industry Doing?

8.12 8.53

9.44 9.86

10.25 10.22 10.26

11.70

0.39 0.52 0.49 0.51 0.58 0.77 0.49

0.86

19.3% 21.4% 22.3% 18.5%

22%

16.6% 11.3% 18.5%

8.2%

76.2%

16.7%

9.2%

42.0%

43.4%

-1.9%

25.2%

-20%

0%

20%

40%

60%

80%

100%

0

2

4

6

8

10

12

14

Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012

(Billion $)

Sales Total profit Growth rate of sales Growth rate of total profit

• ~18% of the country’s 649 processors made losses in 2012 (2011: 16%)

• But profitability growth outpacing sales growth – premium products

Source: CEMAC/NBS

NPD Focus on Premium & Foreign

Flower Cow Milk – Yichun UHT Milk – 200ml –

$0.79 (RMB5)

Ansy Dairy – AuMina

Milk Powders –

$30.4/kg (RMB190)

Gentech – Carrickmore formula – $47/900g (RMB298)

MiMille Dairy/Arla Foods –

premium and premium

plus+ infant formula

• Premium infant formula ($32-49 per 900g) - up 23%

• Super premium infant formula (>$49 per 900g) ‒ up 134%

• Example: premium lines now ~27-28% of Mengniu sales (2008: 17%)

45%

5% 20%

30% Yili

Bright

Mengniu

Others

Major Domestic Brands in China

Role Reversal at the Top?

• Bright Dairy ($2 billion)

• Reasonable profit performance in 2012: H1 +61.9%, Q3 +16.7%

• More premium products, diversified sales channels

• Conspicuous underperformers?

• Beijing Sanyuan − profitable on liquid/yoghurt, but Sanlu acquisition difficult,

growth elusive

• Wandashan − Heilongjiang’s advantages not realised

Yili ($7 billion)

• Known for

“proper”, less

edgy approach

• Now seeking

innovation and

profitability

• NZ investment

Mengniu ($6 billion)

• Traditionally aggressive

approach

• Now increasingly risk

averse (COFCO & Arla

2 key shareholders)

• Focus on premium

Snapshot 1 ‒ Modern Dairy: Growth & Widening Customer Base

• Beneficiary of state push for

• Large-scale dairy farming

• Production growth 2015 – 50 million MT / 2020 – 64 million MT

• Sales USD173.9 million (RMB1,092 million) – up 48.5%

• Pre-tax profit USD28.3 million (RMB178 million) – up 9.2%

• 22 farms – targets 30+ by 2015

• 176,264 cows – targets 260,000+ by 2015

• Milk sales 260,906 MT – up 33.6% (vs H1 2012)

• Less reliance on Mengniu seems likely (unless its acquired by Mengniu!)

• 86.7% sold to Mengniu – down 11.8%

• Diversification / risk mitigation

• COFCO driving Mengniu to develop own farms

Note: Based on H1 2013

(June–December 2012)

Snapshot 2 ‒ Yakult: Pushing Inland

• Currently building 3rd plant in China, for 2014 completion

• Local production capacity will be ~2.86 million bottles/day,

facilitating further expansion into the cities in inland

• Strategic rollout:

• Focus on coastal

regions after market

entry (2001)

• Developed sales in

Wuhan (2009),

Xi’an and

Changsha (2012)

• Sales office in

Chengdu (January

2013)

Snapshot 3 ‒ Want Want: Pushing Inland

• Sales $3,358 million (+14% vs 2011)

• Net profit $554 million (+32%)

• Dairy products & beverages now 50.9% of sales

• Fastest growing business segment +22.6% vs rice

vs. crackers -6.5%, snack foods +14.8%

• Targeting growth in 3rd / 4th tier cities

34.4% 36.1% 27.4% 28.0% 27.7% 24.2%

29.0% 28.8%

25.4% 23.7% 24.5% 24.7%

35.7% 34.5% 46.6% 47.6% 47.3% 50.9%

0.9% 0.6% 0.6% 0.7% 0.5% 0.2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012

Rice crackers Snack foods Dairy products and beverages Others

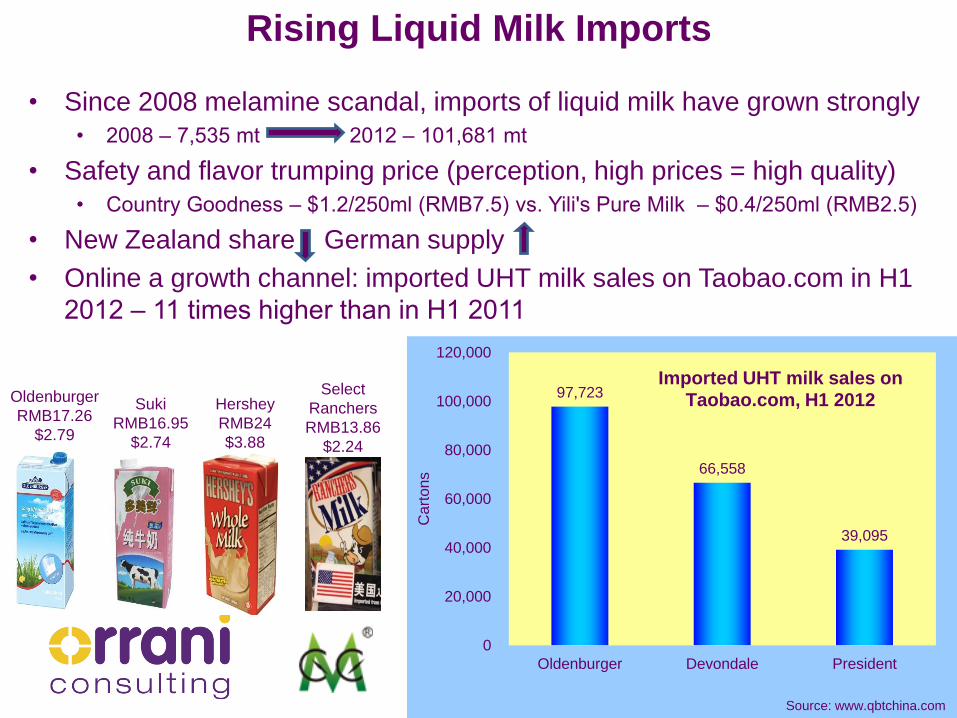

Rising Liquid Milk Imports

• Since 2008 melamine scandal, imports of liquid milk have grown strongly

• 2008 ‒ 7,535 mt 2012 ‒ 101,681 mt

• Safety and flavor trumping price (perception, high prices = high quality)

• Country Goodness ‒ $1.2/250ml (RMB7.5) vs. Yili's Pure Milk ‒ $0.4/250ml (RMB2.5)

• New Zealand share German supply

• Online a growth channel: imported UHT milk sales on Taobao.com in H1

2012 ‒ 11 times higher than in H1 2011

Oldenburger

RMB17.26

$2.79

Suki

RMB16.95

$2.74

Hershey

RMB24

$3.88

Select

Ranchers

RMB13.86

$2.24

97,723

66,558

39,095

0

20,000

40,000

60,000

80,000

100,000

120,000

Oldenburger Devondale President

Cart

ons

Imported UHT milk sales on Taobao.com, H1 2012

Source: www.qbtchina.com

• Annual per capita consumption:

global 2.8kg, China 0.2kg

• Imports over 90% of consumption

• Popular varieties:

Mozzarella

Cheddar

Parmesan

Cream Cheese

Brie

Gouda

• Major foodservice opportunity but

retail still a hard sell

80% 20%

Cheese Challenge Remains

Cheese Challenge Remains

• Positioning for snacking seems attractive

• Dairy’s image as natural / healthy fits into current marketing propositions for snacks

• Yoghurt, ice-cream and milk ‒ popular dairy snacks (children, young white collar workers)

• Efforts by several brands to target the snacking cheese sector, but more

consumer education is critical

• Note ‒ our recent Cheese Technology Landscape report shows China

rising fast as a cheese innovator over last 2 decades, 2nd only to USA in

2011 based on patent applications

Opportunities Comparison –

China, India

Opportunities Comparison – China, India

• Interesting to compare with India (2012: 116 million mt milk)

– Near self sufficiency (only ~13% processed vs. 90-95% in China)

– High import tariffs

– High ‘protein gap’ (~ 1/3 population vegetarian, dairy protein a key

source to fill)

– Rising demand for “Next Generation Food Solutions” (people emerging from poverty, higher income groups)

– Good potential for protein-based solutions for adults, growing children

– Infant foods market constrained by restrictive regulatory environment

– Low cheese production: whey, lactose deficit

– Robust pharma industry: increasing demand for excipients

– Dairy brand Amul rated Most Trusted F&B brand!!

• China’s very high potential shouldn’t obscure other opportunities

UK

Richard Field

+44-7850-594851

USA

Christine Van Asten

+1 (608) 712 9175

www.orrani.com