China and Long-range Asia Energy Security: An Analysis of ... · China and Long-range Asia Energy...

19

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives China and Long-range Asia Energy Security: An Analysis of the Political, Economic and Technological Factors Shaping Asian Energy Markets Prepared in conjunction with an energy study sponsored by the Center for International Political Economy and the James A. Baker III Institute for Public Policy. China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives By Ronald Soligo Professor of Economics Rice University and Amy Jaffe Senior Energy Analyst James A. Baker III Institute for Public Policy Rice University "We would like to thank the Center for International Political Economy for financial support, and Alan Troner, Martin Herman, Robert Manning and Joe Barnes for their advice and editorial comments. We would also like to thank Tiffany Cochran, Nadia Naz Janjua, Todd Makse, Steve Lewis, Evan Feigenbaum, Larry Cohen, Steve Gallogly, Peter Bass, David Jhirad, Blake Eskew and Simon Frame for their contribution and support." -The Authors Introduction The Outlook For Oil Demand In China Forecasts for Future Chinese Oil Demand China’s Refining Sector: The Challenge of Meeting Regional Oil Imbalances Table 2:China Refinery Capacity by Crude Tolerance (Thousands b/d) China’s Supply Options China’s Domestic Upstream Oil Sector Table 3: China's Major Fields Table 4: Foreign Investors in Chinese Oilfields The Outlook for Future Chinese Oil Production Pipelines Versus Tankers: The Trade off Between Economic Efficiency And Security Table 5: Cost Estimates of Alternative Routes Table 6: Oil Transport Costs The Future Economics of Current Chinese Production Table 7: Crude Oil Transportation Costs in China (US $/b) The Future Influence On Chinese Oil Demand Growth On Oil Markets Table 8: Forecast Comparisons. (million b/d) Table 9: Demand Scenarios for 2010 (Millions b/d) http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (1 of 19)2/11/2004 7:06:29 AM

Transcript of China and Long-range Asia Energy Security: An Analysis of ... · China and Long-range Asia Energy...

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

China and Long-range Asia Energy Security: An Analysis of the Political, Economic and Technological Factors Shaping Asian Energy Markets

Prepared in conjunction with an energy study sponsored by the Center for International Political Economy and the James A. Baker III Institute for Public Policy.

China's Growing Energy Dependence:The Costs and Policy Implications of Supply Alternatives

By Ronald SoligoProfessor of Economics

Rice University

and

Amy JaffeSenior Energy Analyst

James A. Baker III Institute for Public PolicyRice University

"We would like to thank the Center for International Political Economy for financial support, and Alan Troner, Martin Herman, Robert Manning and Joe Barnes for their advice and editorial comments. We would also like to thank Tiffany Cochran, Nadia Naz Janjua, Todd Makse, Steve Lewis, Evan Feigenbaum, Larry Cohen, Steve Gallogly, Peter Bass, David Jhirad, Blake Eskew and Simon Frame for their contribution and support." -The Authors

Introduction

The Outlook For Oil Demand In ChinaForecasts for Future Chinese Oil Demand

China’s Refining Sector: The Challenge of Meeting Regional Oil Imbalances Table 2:China Refinery Capacity by Crude Tolerance (Thousands b/d)

China’s Supply OptionsChina’s Domestic Upstream Oil SectorTable 3: China's Major FieldsTable 4: Foreign Investors in Chinese Oilfields

The Outlook for Future Chinese Oil Production

Pipelines Versus Tankers: The Trade off Between Economic Efficiency And SecurityTable 5: Cost Estimates of Alternative RoutesTable 6: Oil Transport Costs

The Future Economics of Current Chinese ProductionTable 7: Crude Oil Transportation Costs in China (US $/b)

The Future Influence On Chinese Oil Demand Growth On Oil MarketsTable 8: Forecast Comparisons. (million b/d)Table 9: Demand Scenarios for 2010 (Millions b/d)

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (1 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

The Geopolitical Consequences Of China’s Oil Supply Alternatives

Bibliography

Introduction

The oil sector in China has been the focus of major structural reforms and high-level attention from the Central government in recent years. Despite broad policy moves towards a more market-oriented oil sector, government ownership, limited foreign investment, and inefficient strategies for expansion still largely characterize the industry.

In an effort to make its oil industry internationally competitive, China began to reorganize its oil sector in the late 1980s into large transnational socialist corporations, each with responsibility for a particular operational segment of the oil business. Utilizing planned economy strategies, China had several giant state oil companies that handled different operational functions:

*All onshore oil exploration and production was handled by China National Petroleum Corp. (CNPC).

*All offshore exploration and production was organized by Chinese National Offshore Oil Corp. (CNOOC) though CNOOC opened quickly to foreign partnerships.

*Most refining and marketing was overseen by China National Petrochemical Corp. (Sinopec) though some provinces, municipalities, and even local villages operated refineries and other related facilities.

*All international trade in crude oil and petroleum products was handled by China National Chemicals Import and Export Corporation (Sinochem).

This organizational structure by operational activity created many market distortions as political struggles ensued over division of input costs and profits. For example, CNPC was forced under this system to sell the majority of its crude to Sinopec refineries and other powerful domestic industrial consumers at prices substantially below international levels, reducing CNPC profitability and limiting capital for investment in exploration and production activities. As a result, growth in China’s overall oil production levels began to slow, raising new internal questions about petroleum security and market reform.

A decision was made in 1998 to reorganize the industry once again, this time to create two vertically integrated oil companies with geographic rather than operational function-oriented focus. The transformation was achieved through asset swaps between CNPC and Sinopec, leaving CNPC with about 70% of onshore domestic production and 30% of refining and Sinopec with 25% participation in the upstream sector and about 65% of refining.The majority of CNPC’s assets are in the northern half of the country, while Sinopec’s activities focus on the middle to southern part of China. The current system still suffers from some non-commercial oil movements, inefficient accumulations of inventory and lack of completely transparent pricing.

In the spring of 1998, China announced a major price reform initiative to replace a two-tiered system that had applied state-controlled pricing to about 80% of onshore domestic production controlled by CNPC and market-related pricing to the remaining output. Under the new reforms, the State Council approved a plan to set domestic oil prices at levels linked to international markets. Crude oil prices are set under a market-related monthly price linked to the price of foreign crude in the Singapore market. Recommended marker prices are also set at market-related levels for petroleum product prices and adjusted every 2 months. Oil giants CNPC and SINOPEC are permitted to alter petroleum product prices by 5 percent from this base price as necessary. Despite these attempts at price reform, China’s domestic crude oil and products prices are still not completely decontrolled. The use of market averages means that domestic prices can vary significantly from world oil prices when world prices make large movements. In addition, transportation and port costs are not handled in a systematic, transparent fashion, thwarting free market signals. As a result, short run distortions and inefficiencies are still prevalent, clouding investment decision making.

The reorganization of China’s oil sector came too late to prevent the country from becoming a net importer of crude oil in the 1990s. Since 1979, China’s oil demand has grown faster than domestic oil production. Oil consumption rose from 2.1 million b/d in 1990 to 3.5 million b/d in 1997

and is about 3.95 million b/d currently. Last year, net crude oil imports were over 554, 000 b/d, down slightly from 1997. Net refined product imports stood at an estimated 417,000 b/d, not including an additional 70,000 b/d to 100,000 b/d of illegally smuggled gasoil, fuel oil and other products.The total level of these imports is expected to grow substantially in the coming years as China’s domestic oil requirements continue to increase while its domestic oil production fails to keep pace. Should China’s oil production levels remain relatively stagnant as has been the case

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (2 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

for several years, China’s oil import levels will grow to between 2.0 and 4.0 million b/d over the next ten years.

The implications of China’s shift to a world energy importer are significant. China’s oil demand could represent as much as 17 percent to 23 percent of total Asian oil demand and 5 percent to 7 percent of total world demand for oil by 2010, making China’s influence on and vulnerability to international oil markets significant. China’s energy insecurity will also influence its foreign policy agenda and the geopolitics of oil into the 21st century.

The growing discrepancy between demand and domestic supply will leave China with tough choices. Solutions to this increasing energy "insecurity" include the following: i) a big push to develop oil and natural gas resources in Western China despite the huge requirement of capital investment, high production costs and geological risks ii) increased reliance on Persian Gulf and other crude oil suppliers that are distant from China despite the geopolitical risk that accompany this option iii) construction of a major oil (and possibly natural gas) overland pipeline from Kazakhstan and iv) construction of facilities and pipelines to allow the importation of natural gas from east Siberia or liquefied natural gas (LNG) from Southeast Asia and the Middle East. Overland pipeline options develop routes that avoid the risks associated with long supply lines by tanker. But since tankers offer lower transport costs than pipelines for oil,

the issue becomes one of how much diversification of supply routes is worth.

Back to top

The Outlook For Oil Demand In China

Forecasts for Future Chinese Oil Demand

Chinese demand for oil (and oil products) can be expected to increase sharply over the next two decades. Using very conservative estimates, including the assumption that the energy mix in industry, the residential and commercial sector and in transportation will remain constant at their 1995 levels, Medlock and Soligo have estimated energy and oil demand for 2010-2020. These estimates are shown in Table 1. For 2010, oil demand is estimated to be between 5.4 and 7.0 million b/d, corresponding to GDP growth rates of 3.2% and 7.9% respectively. For 2020, demand is estimated at 6.8 - 10.9 million b/d, again for growth rates 3.2% and 7.9%. These estimates compare with DOE reference case projections of 7.0 mill b/d in 2010 and 11.2 mill b/d in 2020. The DOE "reference case" assumes a real GDP growth rate of 7.9% and are very similar to those shown for a 7.2% per capita GDP growth scenario.

On the other hand, if the sectoral energy mix changes, as it most likely will, oil demand will exceed these estimates. For example, assume that the oil component in the energy mix in transportation rises from 62% to 80% by 2010 and then gradually to 90% by 2010 - a reasonable assumption given that transportation growth will be dominated by growth in private transport in owner-owned vehicles. In this case, oil demand in 2010 will be between 5.8 and 7.6 million b/d, depending on GDP growth rates, and between 7.6 and 12.3 mill b/d in 2020.

Regardless of what GDP growth rate one assumes, oil imports will rise, both absolutely and as a share of total oil and energy use. By 2010, our estimates for imports lie between 2.0 and 4.0 million b/d. For 2020, our estimates are 3.3-7.4 b/d. Including projected increases in LNG imports will further indicate a growing dependence of foreign energy supplies, raising the issue of energy security for China.

Back to top

China’s Refining Sector: The Challenge of Meeting Regional Oil Imbalances

The refining industry in China includes over 100 refineries and petrochemical plants with a total capacity of around 4.75 million b/d (not including a large, uncounted number of very small, locally operated refineries) making China one of the largest refiners in the Asia pacific region. Worldwide, only the U.S., Russia and Japan have larger refining capacity than China. Sinopec still controls about 3.36 million b/d of the country’s total refining capacity. CNPC holds another 505,000 b/d with the rest controlled by local independents.

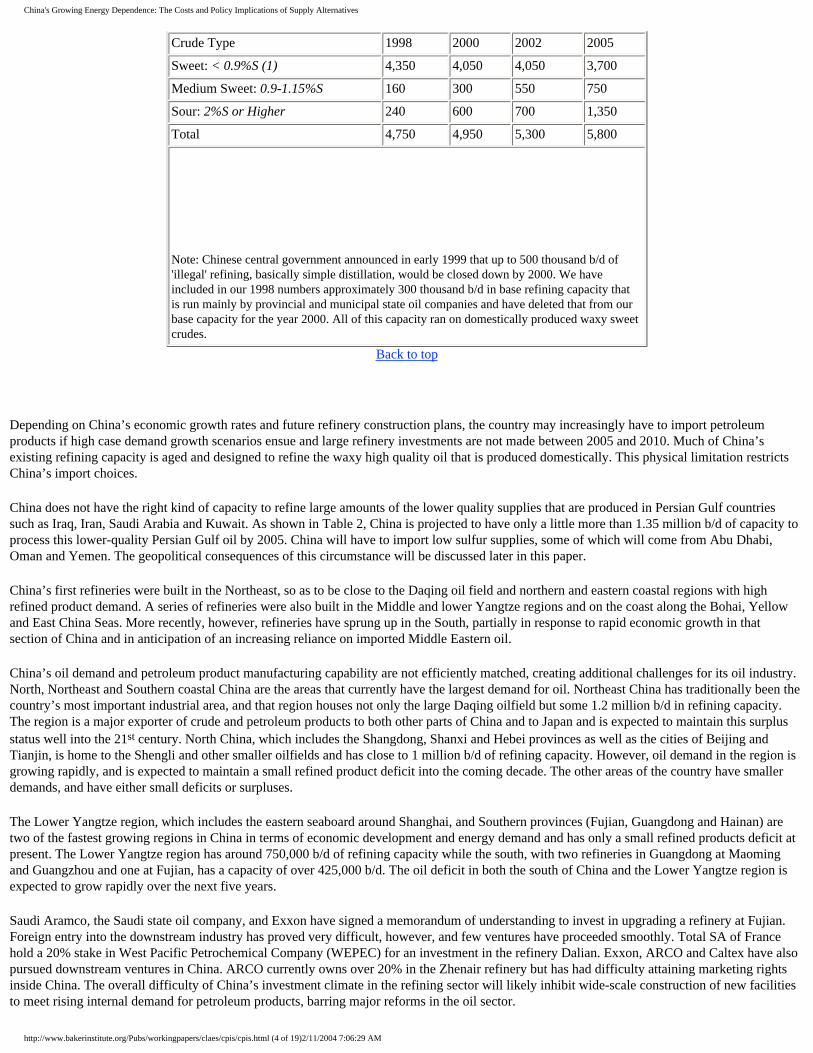

Table 2 gives projected refinery capacities by type of crude that can be refined to the year 2005 as compiled by Asia Pacific Energy Consulting (APEC). Assessing projects already announced and planned, APEC anticipates that China’s refining capacity will rise to about 5.8 million b/d by 2005.

Table 2:China Refinery Capacity by Crude Tolerance (Thousands b/d)

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (3 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

Crude Type 1998 2000 2002 2005

Sweet: < 0.9%S (1) 4,350 4,050 4,050 3,700

Medium Sweet: 0.9-1.15%S 160 300 550 750

Sour: 2%S or Higher 240 600 700 1,350

Total 4,750 4,950 5,300 5,800

Note: Chinese central government announced in early 1999 that up to 500 thousand b/d of 'illegal' refining, basically simple distillation, would be closed down by 2000. We have included in our 1998 numbers approximately 300 thousand b/d in base refining capacity that is run mainly by provincial and municipal state oil companies and have deleted that from our base capacity for the year 2000. All of this capacity ran on domestically produced waxy sweet crudes.

Back to top

Depending on China’s economic growth rates and future refinery construction plans, the country may increasingly have to import petroleum products if high case demand growth scenarios ensue and large refinery investments are not made between 2005 and 2010. Much of China’s existing refining capacity is aged and designed to refine the waxy high quality oil that is produced domestically. This physical limitation restricts China’s import choices.

China does not have the right kind of capacity to refine large amounts of the lower quality supplies that are produced in Persian Gulf countries such as Iraq, Iran, Saudi Arabia and Kuwait. As shown in Table 2, China is projected to have only a little more than 1.35 million b/d of capacity to process this lower-quality Persian Gulf oil by 2005. China will have to import low sulfur supplies, some of which will come from Abu Dhabi, Oman and Yemen. The geopolitical consequences of this circumstance will be discussed later in this paper.

China’s first refineries were built in the Northeast, so as to be close to the Daqing oil field and northern and eastern coastal regions with high refined product demand. A series of refineries were also built in the Middle and lower Yangtze regions and on the coast along the Bohai, Yellow and East China Seas. More recently, however, refineries have sprung up in the South, partially in response to rapid economic growth in that section of China and in anticipation of an increasing reliance on imported Middle Eastern oil.

China’s oil demand and petroleum product manufacturing capability are not efficiently matched, creating additional challenges for its oil industry. North, Northeast and Southern coastal China are the areas that currently have the largest demand for oil. Northeast China has traditionally been the country’s most important industrial area, and that region houses not only the large Daqing oilfield but some 1.2 million b/d in refining capacity. The region is a major exporter of crude and petroleum products to both other parts of China and to Japan and is expected to maintain this surplus status well into the 21st century. North China, which includes the Shangdong, Shanxi and Hebei provinces as well as the cities of Beijing and Tianjin, is home to the Shengli and other smaller oilfields and has close to 1 million b/d of refining capacity. However, oil demand in the region is growing rapidly, and is expected to maintain a small refined product deficit into the coming decade. The other areas of the country have smaller demands, and have either small deficits or surpluses.

The Lower Yangtze region, which includes the eastern seaboard around Shanghai, and Southern provinces (Fujian, Guangdong and Hainan) are two of the fastest growing regions in China in terms of economic development and energy demand and has only a small refined products deficit at present. The Lower Yangtze region has around 750,000 b/d of refining capacity while the south, with two refineries in Guangdong at Maoming and Guangzhou and one at Fujian, has a capacity of over 425,000 b/d. The oil deficit in both the south of China and the Lower Yangtze region is expected to grow rapidly over the next five years.

Saudi Aramco, the Saudi state oil company, and Exxon have signed a memorandum of understanding to invest in upgrading a refinery at Fujian. Foreign entry into the downstream industry has proved very difficult, however, and few ventures have proceeded smoothly. Total SA of France hold a 20% stake in West Pacific Petrochemical Company (WEPEC) for an investment in the refinery Dalian. Exxon, ARCO and Caltex have also pursued downstream ventures in China. ARCO currently owns over 20% in the Zhenair refinery but has had difficulty attaining marketing rights inside China. The overall difficulty of China’s investment climate in the refining sector will likely inhibit wide-scale construction of new facilities to meet rising internal demand for petroleum products, barring major reforms in the oil sector.

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (4 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

Back to top

China’s Supply Options

China’s Domestic Upstream Oil Sector

Table 3 shows China's major oil fields and the level of production of each. Total crude oil production in China now currently averages about 3.1 million barrels a day, most of which is concentrated in a small number of highly productive fields. At present, over 50% of China’s oil output comes from just two mature and declining fields –Daqing, located in Northeast China, and Shengli, located in the Northern Shangdong province. Daqing, China’s largest oil field, produces about 1.1 million barrels a day (b/d). A small portion of this crude is exported to Japan but most of it is transported by pipeline or railcar to refineries in North and Northeast China. Some Daqing oil is shipped to the Lower Yangtze region and the southern provinces by small coastal vessels and refined there. Shengli production averages about 600,000 b/d. About 220,000 b/d of Shengli production remains in the Shangdong province for refining. The remainder is shipped by pipeline to the coast or to refineries along the Yangtze river. Both fields are considered as over-drilled and are poor candidates for additional tertiary recovery schemes. Some decline in output rates is expected from both fields over the next five to ten years.

Table 3: China's Major Fields

Field

Province

Region

1996 Output (thousands b/day)

Daqing Heilongjiang Northeast 1120

Shengli Shandong North 600

Liaohe Liaoning Northeast 300

Nanhai East N/A Offshore 235

Huabei Hebei North 93

Xinjiang Xinjiang West 166

Dagang Shandong North 87

Zhongyuan Henan North 80

Jilin Jilin Northeast 74

Tarim Xinjiang West 62

Tu-Ha Xinjiang West 58

Changqing Gansu Northwest 55

Bohai N/A Offshore 42

Henan Henan North 37

Qinghai Qinghai West 28

Nanhai West N/A Offshore 23

Jiangsu Jiangsu Lower Yangtze 21

Yanchang Shaanxi Northwest 18

Jianghan Hubei Middle Yangtze 17

Jidong Hebei North 11

Back to top

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (5 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

The next tier of smaller fields includes Liaohe and Xinjiang. Liaohe production averages around 300,000 b/d and is shipped mainly by pipeline to refineries in the Lower Yangtze region. The Xinjiang Uigur autonomous region in Western China has three giant crude oil basins: Tarim, Junggar and Tu-Ha. Although current output from the region is small, China believes this region could see a large boost in output from exploration and development activities, possibly to as high as one million b/d by 2010. However, such development would require massive investment, including construction of a major 4,000 kilometer pipeline to more populous East and Southeast regions. Construction of a pipeline from the Tarim area to Shanshan was completed in 1997 and plans exist to extend the line to Lanzhou and points east, with a spur to energy-short Sichuan province. Eventually the system could be extended to Shanghai and its environs..

Certain onshore exploration blocks have been targeted for foreign investment. China began its move to open up its industry in the 1970s, originally permitting joint ventures in the southern provinces, and later expanding to other parts of the country. Ventures with foreign companies have been handled by the China National Oil Development Corporation. Western oil company activities in the onshore has been limited mainly to smaller oilfields and to wildcat exploration. Table 4 shows the areas in which foreign energy companies are involved. Among the companies with upstream investment in China are Exxon, Texaco, Agip, BP, Amoco, Shell, and a number of Indonesian and Japanese companies. China has placed some hopes on developing the Western oilfields of the Tarim Basin but to date low oil prices and an uncertain environment for foreign investors has slowed the development of the region.

Offshore oil production represents less than 7% of total oil production at around 300,000 b/d, in part because of sparse exploration success in the limited areas awarded by China to foreign oil company investors. About a third of the offshore production is sold abroad, mainly to refiners in Singapore, with the rest sent to China’s southern provinces.

In the last two decades, the Chinese government has made overtures to reform the oil industry through diversification and foreign investment. It loosened restrictions on the offshore component first, in 1979, in order to attract foreign companies. Through the work of the China National Offshore Oil Corporation, this strategy has been somewhat successful, as a majority of production increase from offshore fields now comes from

Back to top

Table 4: Foreign Investors in Chinese Oilfields

Field

●

Foreign Partners

Anhui Fuyang Basin Amoco Orient Petroleum

Chengdao West Block Amoco Orient Petroleum, Energy Development

Dafenshan-Eboliang Esso China

Daqing-Zhaozhou-13 Sunwing

Hainan Fushan Sag CSR Orient Petroleum, BHP Petroleum, Basin Oil NL, Base Resources

Hunan Dongting Basin Fletcher Challenge Exploratio, Santa Fe Energy Resources, Nomeco China Oil

Jiangsu Subei Basin Shell Exploration, Pecten Orient

Jidong Getuo Block Kerr-McGee China Petroleum, Energy Development

Jidong Laopu Block Kerr-McGee China Petroleum, Energy Development

Jilin Min-114 Block JKR International

Jilin Qian-130 Block JKR International

Leshan Block Texaco China

Liaohe LVR International

Liaohe Qingshui Block Shell Exploration

NW Songliao Basin Esso China

NW Tarim Block 12 Esso China Upstream

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (6 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

NW Tarim Block 13 Esso China Upstream

SE Tarim Block 3 Esso China, Sumitomo, Indonesia Petroleum

Shengli Canadian Fracmaster

Southern Tarim Block 14 Agip, EACO, Elf Hydrocarbures Chine, Japan Energy, Texaco China B.V.

Southern Tarim Block 6 Agip, Texaco China

Southern Tarim Block 7 Agip, Texaco China

Tarim Block 1 Agip, Elf Hydrocarbures Chine, Japan Energy, Texaco China B.V.

Tarim Block 4 BP Exploration, Nippon Exploration, Itochu Oil, Mitsubishi, Mitsui

Ya'an Block Texaco China

Zhaodong Block Apache China, Exploration Co. of Louisiana

Source: East-West Center and Industry Sources

Back to top

areas developed by foreign oil companies such as Agip, Chevron, Texaco, Shell, and Phillips. However, only small to medium-sized oil and gas fields have been discovered to date and many dry holes were drilled in the region. So far, Chinese central planners and some officials in the oil conglomerates have opposed a wide scale opening to foreign investors on national development and security grounds.

Back to top

The Outlook for Future Chinese Oil Production

Despite an opening to foreign investment, China’s domestic oil production is not expected to increase substantially in the coming years. Low oil prices, ineffective price reform, massive flooding at the Daqing oil field and insufficient domestic oil transportation infrastructure combined to produce a small drop in Chinese oil output which totaled 3.2 million b/d in 1998. While some analysts continue to predict Chinese oil production could rebound over the next ten years, there are many factors that might work against this result. They include: capital constraints within China’s major industries, general ineffectiveness of oil sector corporate reforms, lack of interest among foreign investors in acreage offered for exploration, and the prospects that oil prices could remain low.

For these and other reasons, we expect that domestic output will stagnate for the next 10 years and remain close to 3.1 million b/d through 2010. Other forecasts are as follows:

● * Edinburgh, UK-based Wood Mackenzie Consultants forecasts oil production at 3.0 million b/d for 2010.

* Hawaii based East-West Center has a more optimistic forecast for 2010 output as between 3.4 and 4.1 million b/d.

* Asia Pacific Energy Consulting forecasts a more pessimistic assessment of flat to down to 2.8-2.9 million b/d for 2010.

* Petroleum Industry Research Associates (PIRA) forecasts 3.7 million b/d.

* The DOE reference case forecasts production at 3.6 million b/d.

The outlook for 2020 is not much better. The DOE forecasts 2020 production at 3.5 million b/d. We find this a reasonable projection given the possibility that technological improvements and market efficiency gains will be made in China’s energy sector over the next twenty years and could eventually arrest decline in production rates.

Should domestic output increase only modestly over the next two decades, Chinese imports of crude oil and petroleum products will increase steadily. In an effort to diversify from the troubled domestic oil sector, state-concern CNPC has responded to China’s expected growth in oil demand by making large investments in foreign oil fields in Kazakhstan, Peru, Venezuela and Sudan. It has announced plans to invest in Iraq’s oil industry after United Nations sanctions against Baghdad are lifted. China has also proposed projects to transport Caspian oil and gas production by

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (7 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

pipeline to China directly or through Iran to the Persian Gulf and to form an exploration venture in Iran in return for a higher allocation of crude oil.

Despite the preference for diverse sources of foreign imports CNPC’s sudden burst of investment activity seems to imply, analysis of the economics of China’s various supply options demonstrate that optimum strategies should be determined not only by China’s available cash flow and geopolitical and security considerations, but also by the overall level of international oil prices which will determine which of China’s various oil supply options make the most economic sense. The following section of this paper analyzes the trade-offs between various options under different oil market price scenarios.

Back to top

Pipelines Versus Tankers:

The Trade off Between Economic Efficiency And Security

China’s expected energy dependence leaves it with tough choices. One of the solutions to increasing energy "insecurity" is to develop oil resources in Western China and to build a costly pipeline to transport this oil to east and/or southeast markets within China. Another option that has been discussed is to import oil from Kazakhstan via an all land route which could also link up with fields in the Tarim basin on its way to the major markets. The main alternative to these proposals is to import crude by tanker. The two pipeline options develop routes that avoid the security risks associated with long supply lines by tanker that must pass through relatively narrow and congested sea lanes of the South China. But since tankers offer lower transport costs than pipelines for oil, the issue becomes one of how much China is willing to pay for diversification of supply.

Table 5: Cost Estimates of Alternative Routes

ROUTE Length Diameter Capacity Total Cost Cost/b

Kilometers Inches Mb/d US$bill US$

Uzen/Arkbinsk -Xinjiang 3,000 40 1,000 $3.35 2.03

Korla-Guangdong 4,200 40 1,000 $4.69 2.84

Korla-Guangdong 4,200 40 500 $4.69 5.67

Korla-Guangdong 4,200 30 500 $3.70 4.48

Kazak border - Guangdong 5,000 40 1,000 $5.58 3.38

Azerb/Turkmen/Kharg 2,150 40 1,500 $3.00 1.21

CAOPP 1,673 42 1,000 $5.00 3.03

CAOPP/Pakistan 1,667 42 1,000 $2.70 1.63

CAOPP 1,667 42 1,000 $2.70 1.63

CNPC to China 3,000 40 1,000 $3.50 2.12

CNPC to Iran 1,200 28 250 $1.10 2.66

CNPC to China to Shanghai/Canton (2.12+3.38) $5.50/b

Kharg Island to China via tanker $1.00/b

Azeri/Kazak via pipeline through Iran

$2.21/b

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (8 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

Tarim Basin to Guangdong

$2.84/b

Assumptions:

Cost of capital 20%

Length of life 30 years

Operating costs 2% of capital cost

Back to top

Given the current and prospective relatively low oil prices on international markets, it may not make economic sense to develop Tarim. Table 5 shows the transport costs for oil for various routes including Tarim to Guangdong. Under conservative assumptions, the cost of transporting Tarim Basin oil to Guangdong will be around $2.84/b, excluding right of way costs. This estimate assumes that there would be sufficient production at Tarim to support a large capacity pipeline of 1 million b/d. A smaller pipeline would produce higher per barrel costs. For example a 30 inch, 500,000 b/d pipeline would increase transport costs to $4.48 per barrel. If a 40 inch pipeline were built in anticipation of large volumes later, the per barrel cost for 500,000 b/d would be $5.67.

Given that production costs are roughly $10/b at the field, the total cost of Tarim oil in the Southern Chinese market will be at least $13/b. Right of way costs could easily push that to $15. Given tanker costs of approximately $1.00/b from the Middle East and excluding any right of way costs or transit tariffs, Tarim basin oil would be competitive with imports of lighter Middle Eastern crudes at prices of $12 - equivalent to $13-$15 for West Texas Intermediate (WTI). Assuming a $1/b premium for quality differences between Tarim and the sour crudes from Iran, Iraq and Saudi Arabia, Tarim oil would be competitive at prices of $10-$11 for Middle East sour crudes.

While world oil prices have recently posted a substantial increase, they remain at a level where Tarim basin oil is marginal at best. Furthermore, it would not make economic sense to develop these fields and build the pipeline infrastructure until there is some reasonable expectation that prices will remain above these levels long enough for investors to recover their costs.

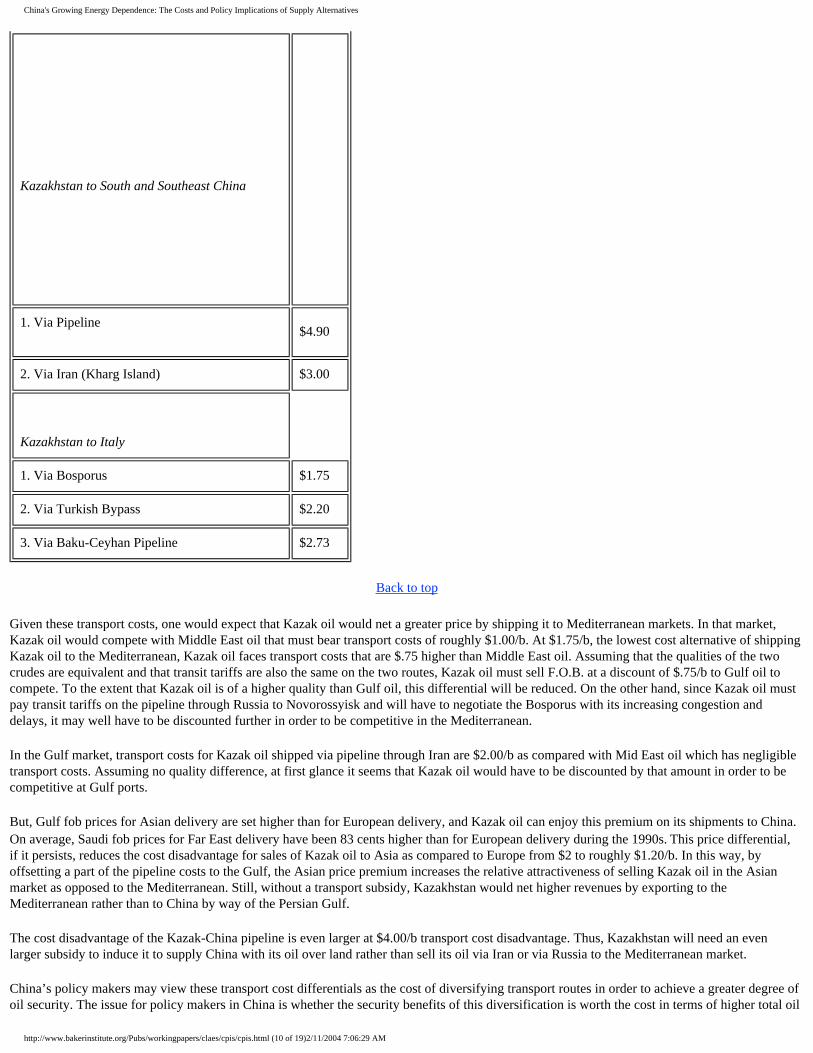

Even if Tarim were developed, it is unlikely that production could be increased sufficiently over the next two decades to obviate the need for growing imports. An alternative to Tarim oil is to import oil from Kazakhstan via a 7,200 kilometer pipeline crossing both Kazakhstan and China. This pipeline (assuming a 40 inch 1 million b/d and excluding right of way costs) would imply a per barrel transport cost of $4.90.

To justify the Kazak-China pipeline, the F.O.B. price of Kazak oil must be set so that, net of transport costs, it allows Kazak oil to compete, on a quality adjusted basis, either in the Mediterranean or the Gulf markets. Table 6, shows the cost, excluding right-of-way and/or transit tariffs, of shipping Kazak oil to Italy and China by different routes. The alternative routes to China are an all land pipeline from Kazak fields to South/Southeast China and a pipeline from Kazak fields through Iran where it would then be loaded on a tanker for shipment to China. For the Mediterranean market, the alternatives are to transport the oil to Novorossyisk by pipeline and then by tanker to Italy, from Novorossyisk to Italy using a short pipeline to bypass the Bosporus and finally, by pipeline to Ceyhan in southern Turkey and then by tanker to Italy.

Table 6: Oil Transport Costs

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (9 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

Kazakhstan to South and Southeast China

1. Via Pipeline$4.90

2. Via Iran (Kharg Island) $3.00

Kazakhstan to Italy

1. Via Bosporus $1.75

2. Via Turkish Bypass $2.20

3. Via Baku-Ceyhan Pipeline $2.73

Back to top

Given these transport costs, one would expect that Kazak oil would net a greater price by shipping it to Mediterranean markets. In that market, Kazak oil would compete with Middle East oil that must bear transport costs of roughly $1.00/b. At $1.75/b, the lowest cost alternative of shipping Kazak oil to the Mediterranean, Kazak oil faces transport costs that are $.75 higher than Middle East oil. Assuming that the qualities of the two crudes are equivalent and that transit tariffs are also the same on the two routes, Kazak oil must sell F.O.B. at a discount of $.75/b to Gulf oil to compete. To the extent that Kazak oil is of a higher quality than Gulf oil, this differential will be reduced. On the other hand, since Kazak oil must pay transit tariffs on the pipeline through Russia to Novorossyisk and will have to negotiate the Bosporus with its increasing congestion and delays, it may well have to be discounted further in order to be competitive in the Mediterranean.

In the Gulf market, transport costs for Kazak oil shipped via pipeline through Iran are $2.00/b as compared with Mid East oil which has negligible transport costs. Assuming no quality difference, at first glance it seems that Kazak oil would have to be discounted by that amount in order to be competitive at Gulf ports.

But, Gulf fob prices for Asian delivery are set higher than for European delivery, and Kazak oil can enjoy this premium on its shipments to China. On average, Saudi fob prices for Far East delivery have been 83 cents higher than for European delivery during the 1990s. This price differential, if it persists, reduces the cost disadvantage for sales of Kazak oil to Asia as compared to Europe from $2 to roughly $1.20/b. In this way, by offsetting a part of the pipeline costs to the Gulf, the Asian price premium increases the relative attractiveness of selling Kazak oil in the Asian market as opposed to the Mediterranean. Still, without a transport subsidy, Kazakhstan would net higher revenues by exporting to the Mediterranean rather than to China by way of the Persian Gulf.

The cost disadvantage of the Kazak-China pipeline is even larger at $4.00/b transport cost disadvantage. Thus, Kazakhstan will need an even larger subsidy to induce it to supply China with its oil over land rather than sell its oil via Iran or via Russia to the Mediterranean market.

China’s policy makers may view these transport cost differentials as the cost of diversifying transport routes in order to achieve a greater degree of oil security. The issue for policy makers in China is whether the security benefits of this diversification is worth the cost in terms of higher total oil

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (10 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

import costs.

Other benefits of the all land, such as the ability to also use the pipeline to carry Chinese domestic western production to its eastern markets (and thus eliminating the need to construct a separate pipeline to carry domestic production), and the externalities generated by the infrastructure that must be constructed in order to build the pipeline, the marginal cost of "security" may make this route more acceptable to Chinese planners.

Back to top

The Future Economics of Current Chinese Production

The preceding discussion was concerned about the viability of developing the Tarim basin and an all land pipeline from Kazakhstan as solutions to the prediction that China will increasingly become dependent on imports of oil from the Middle East and Africa creating a long supply line serviced by tankers, which must funnel through the "chokepoints" of South Asia sea lanes.

This section considers another implication of the liberalization of the domestic energy industry. In particular, we focus on what is likely to happen to production of existing fields when the Chinese market is open to relatively unfettered competition from imports.

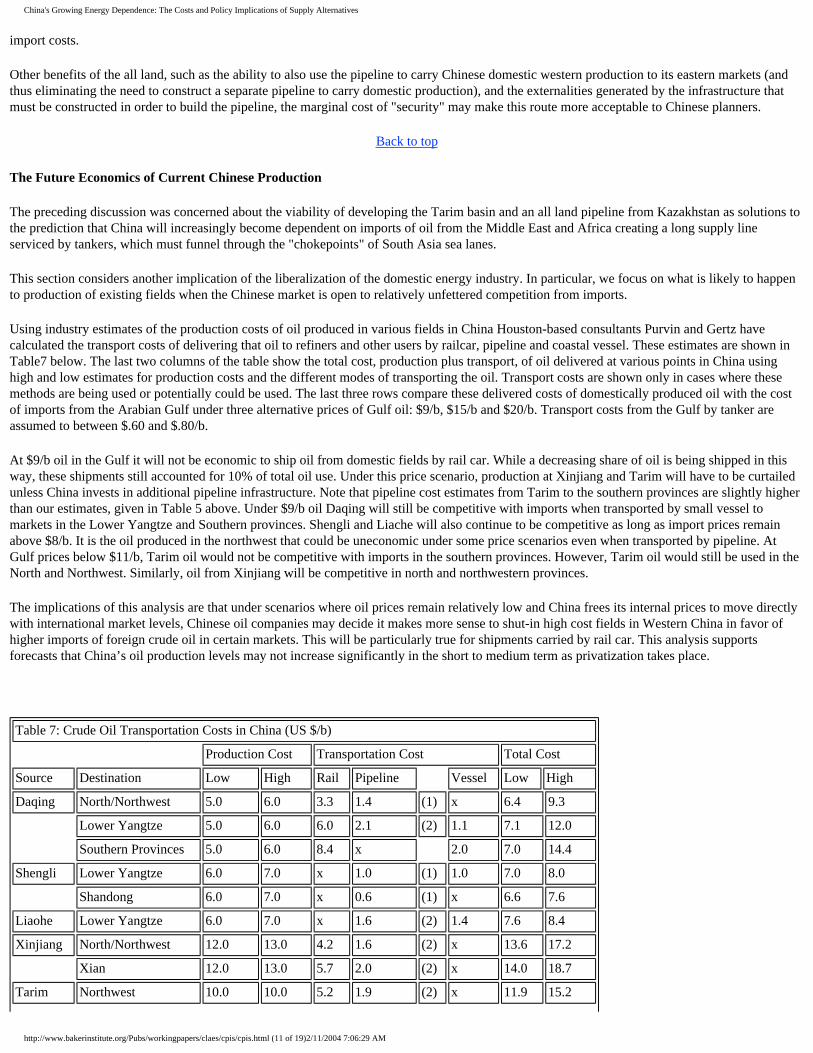

Using industry estimates of the production costs of oil produced in various fields in China Houston-based consultants Purvin and Gertz have calculated the transport costs of delivering that oil to refiners and other users by railcar, pipeline and coastal vessel. These estimates are shown in Table7 below. The last two columns of the table show the total cost, production plus transport, of oil delivered at various points in China using high and low estimates for production costs and the different modes of transporting the oil. Transport costs are shown only in cases where these methods are being used or potentially could be used. The last three rows compare these delivered costs of domestically produced oil with the cost of imports from the Arabian Gulf under three alternative prices of Gulf oil: $9/b, $15/b and $20/b. Transport costs from the Gulf by tanker are assumed to between $.60 and $.80/b.

At $9/b oil in the Gulf it will not be economic to ship oil from domestic fields by rail car. While a decreasing share of oil is being shipped in this way, these shipments still accounted for 10% of total oil use. Under this price scenario, production at Xinjiang and Tarim will have to be curtailed unless China invests in additional pipeline infrastructure. Note that pipeline cost estimates from Tarim to the southern provinces are slightly higher than our estimates, given in Table 5 above. Under $9/b oil Daqing will still be competitive with imports when transported by small vessel to markets in the Lower Yangtze and Southern provinces. Shengli and Liache will also continue to be competitive as long as import prices remain above $8/b. It is the oil produced in the northwest that could be uneconomic under some price scenarios even when transported by pipeline. At Gulf prices below $11/b, Tarim oil would not be competitive with imports in the southern provinces. However, Tarim oil would still be used in the North and Northwest. Similarly, oil from Xinjiang will be competitive in north and northwestern provinces.

The implications of this analysis are that under scenarios where oil prices remain relatively low and China frees its internal prices to move directly with international market levels, Chinese oil companies may decide it makes more sense to shut-in high cost fields in Western China in favor of higher imports of foreign crude oil in certain markets. This will be particularly true for shipments carried by rail car. This analysis supports forecasts that China’s oil production levels may not increase significantly in the short to medium term as privatization takes place.

Table 7: Crude Oil Transportation Costs in China (US $/b)

Production Cost Transportation Cost Total Cost

Source Destination Low High Rail Pipeline Vessel Low High

Daqing North/Northwest 5.0 6.0 3.3 1.4 (1) x 6.4 9.3

Lower Yangtze 5.0 6.0 6.0 2.1 (2) 1.1 7.1 12.0

Southern Provinces 5.0 6.0 8.4 x 2.0 7.0 14.4

Shengli Lower Yangtze 6.0 7.0 x 1.0 (1) 1.0 7.0 8.0

Shandong 6.0 7.0 x 0.6 (1) x 6.6 7.6

Liaohe Lower Yangtze 6.0 7.0 x 1.6 (2) 1.4 7.6 8.4

Xinjiang North/Northwest 12.0 13.0 4.2 1.6 (2) x 13.6 17.2

Xian 12.0 13.0 5.7 2.0 (2) x 14.0 18.7

Tarim Northwest 10.0 10.0 5.2 1.9 (2) x 11.9 15.2

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (11 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

Basin Southern Provinces 10.0 10.0 9.8 3.2 (2) x 13.2 19.8

Arabian

Gulf

Lower Yangtze 9.0 9.0 x x 0.7 9.7 9.7

Southern Provinces 9.0 9.0 x x 0.6 9.6 9.6

Arabian

Gulf

Lower Yangtze 15.0 15.0 x x 0.7 15.7 15.7

Southern Provinces 15.0 15.0 x x 0.7 15.7 15.7

Arabian

Gulf

Lower Yangtze 20.0 20.0 x x 0.8 20.8 20.8

Southern Provinces 20.0 20.0 x x 0.7 20.7 20.7

Notes:

1. Existing pipeline route 2. (2) Not an existing pipeline route 3. Estimates include only freight charges (do not include duties, losses, insurance, terminal costs etc.) 4. Rail and vessel costs are Purvin and Gertz estimates based on Chinese costs obtained from industry sources. 5. Pipeline costs are Purvin and Gertz estimayes based on typical tariff and distance relationships for crude oil pipelines.

Source: Purvin & Gertz

Back to top

The Future Influence On Chinese Oil Demand Growth On Oil Markets

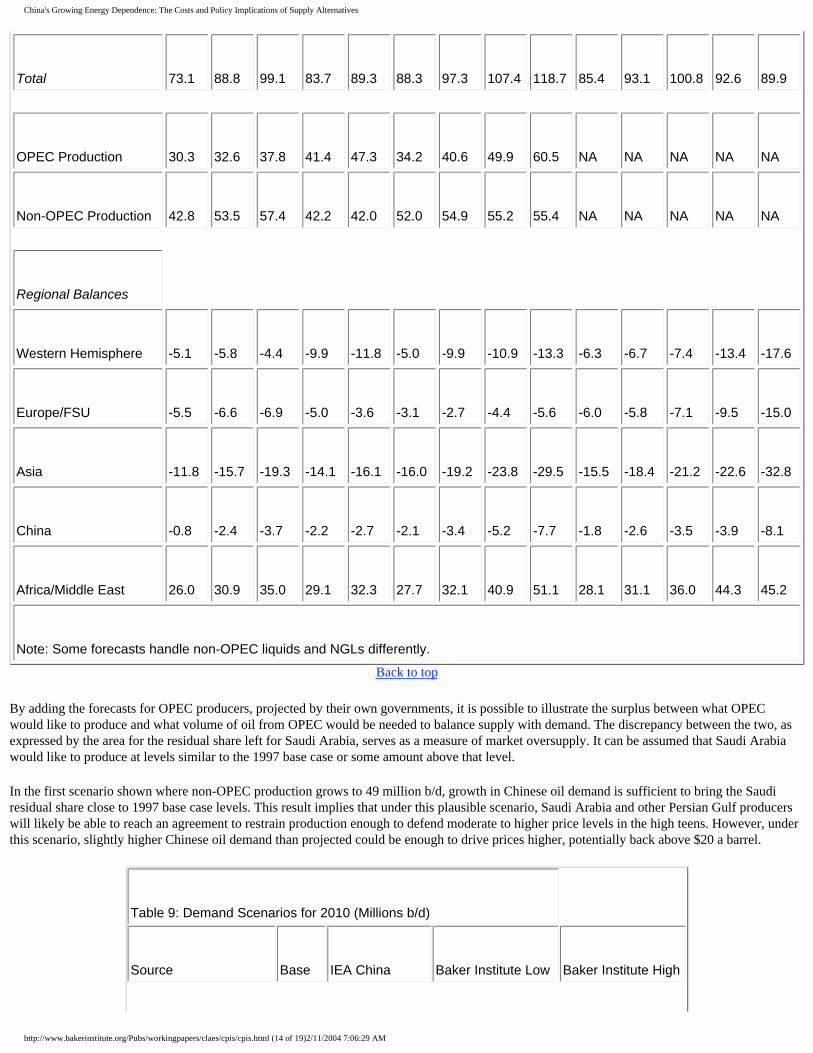

Forecasts discussed above for growth in Chinese oil demand indicate that China’s oil use will rise from around 4 percent to 5 percent of world oil use in 1997 to about 5 percent to 6 percent by 2010. There has been speculation that China’s rising oil use would be a major factor driving international oil prices to new higher levels in the coming decade. However, analysis of various scenarios for the international oil market for 2010 do not support this thesis.

Under two scenarios, falling within the range of consensus projections by most analysts for non-OPEC production of between 49 and 54 million b/d, rising Chinese oil demand could either produce a market with a slight oversupply that could be relatively easily managed by OPEC or a larger surplus similar to that which drove prices down substantially in 1998. Only in the case of stagnant growth in non-OPEC production would rising Chinese oil demand likely create a significant shortage on international oil markets.

Table 8 shows projections of world demand for oil by various sources. The International Energy Agency’s "business as usual" or median estimate for total world demand for 2010 of 93.8 million b/d serves as a reasonable starting point to analyze oil supply and demand trends for 2010. This estimate is within the middle of the range for high and low projections of world demand for that year among various private oil industry consultancy groups.(including Petroleum Industry Research Associates, Petroleum Finance Co., Purvin & Gertz) and the U.S. Department of Energy.

The IEA demand forecast includes an estimate for Chinese demand of 7.1 million b/d. In table (chart-scenarios Baker high/ low), we illustrate the influence that three scenarios for rising Chinese demand could have on the outlook for international oil markets in 2010. We start from the IEA global demand estimates and alter it by three China demand scenarios. The first projects Chinese oil demand to average 7.1 million b/d in line with IEA estimates. The second projects Chinese oil demand to average 5.39 million b/d in line with the Baker Institute’s low-case scenario. The third projects Chinese oil demand to average 6.99 million b/d in line with the Baker Institute high scenario.

Non-OPEC production has expanded by 1 to 1.5 percent per annum between 1988 and 1997 despite prolonged periods of oil price weakness. This was accomplished through a combination of technological advances in discovery and drilling systems and unearthing of new basins in South America, in deep water and elsewhere. Non-OPEC production fell by 0.7 percent in 1998 due to falling world oil prices. However, a recovery in oil prices in the spring of 1999, oil company mergers and cost-cutting as well as continued technological advances are likely to mean that this drop in non-OPEC output may not be sustained. Assuming that non-OPEC average growth slows to one percent per annum, given the potential for expanding future investment opportunities in Persian Gulf countries as well as a possible return of price weakness, non-OPEC production would reach 49 million b/d by 2010, slightly lower than the midpoint for forecasts shown in table 8

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (12 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

Table 8: Forecast Comparisons. (million b/d)

Base

PIRA

PFC

USDOE

Purvin & Gertz

IEA

Year

1997

2005

2010

2005

2010

2005

2010

2015

2020

2005

2010

2015

2010

2020

Demand

Western Hemisphere

27.4

31.7

34.0

32.3

34.3

32.9

36.1

37.5

39.9

30.9

32.9

34.6

32.4

35.1

Europe/FSU

20.1

22.2

23.5

21.7

22.1

21.3

22.7

24.2

25.5

22.4

24.2

26.3

24.2

27.2

Asia

19.6

23.9

27.7

22.0

23.6

24.8

28.5

33.0

38.4

26.0

28.9

31.7

29.0

37.5

China

4.0

5.9

7.4

5.4

6.0

5.6

7.0

8.8

11.2

5.9

6.9

8.0

7.1

10.1

Africa/Middle East

6.7

8.2

9.5

7.5

8.5

8.7

9.7

10.9

12.2

7.6

8.3

8.9

8.2

10.3

Total

73.8

86.0

94.7

83.4

88.6

87.7

97.0

105.6

116.0

86.9

94.3

101.5

93.8

110.1

Production

Western Hemisphere

18.9

25.9

29.6

22.4

22.5

24.9

26.2

26.6

26.6

24.5

26.1

27.2

19.0

17.5

Europe/FSU

14.6

15.6

16.6

16.7

18.5

18.2

20.0

19.8

19.9

16.4

18.4

19.1

14.7

12.2

Asia

7.7

8.2

8.4

7.9

7.5

8.8

9.3

9.2

8.9

8.8

9.2

9.5

6.4

4.7

China

3.2

3.5

3.7

3.2

3.3

3.5

3.6

3.6

3.5

4.1

4.3

4.5

3.2

2.0

Africa/Middle East

31.9

39.1

44.5

36.6

40.8

36.4

41.8

51.8

63.3

35.7

39.4

45.0

52.5

55.5

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (13 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

Total

73.1

88.8

99.1

83.7

89.3

88.3

97.3

107.4

118.7

85.4

93.1

100.8

92.6

89.9

OPEC Production

30.3

32.6

37.8

41.4

47.3

34.2

40.6

49.9

60.5

NA

NA

NA

NA

NA

Non-OPEC Production

42.8

53.5

57.4

42.2

42.0

52.0

54.9

55.2

55.4

NA

NA

NA

NA

NA

Regional Balances

Western Hemisphere

-5.1

-5.8

-4.4

-9.9

-11.8

-5.0

-9.9

-10.9

-13.3

-6.3

-6.7

-7.4

-13.4

-17.6

Europe/FSU

-5.5

-6.6

-6.9

-5.0

-3.6

-3.1

-2.7

-4.4

-5.6

-6.0

-5.8

-7.1

-9.5

-15.0

Asia

-11.8

-15.7

-19.3

-14.1

-16.1

-16.0

-19.2

-23.8

-29.5

-15.5

-18.4

-21.2

-22.6

-32.8

China

-0.8

-2.4

-3.7

-2.2

-2.7

-2.1

-3.4

-5.2

-7.7

-1.8

-2.6

-3.5

-3.9

-8.1

Africa/Middle East

26.0

30.9

35.0

29.1

32.3

27.7

32.1

40.9

51.1

28.1

31.1

36.0

44.3

45.2

Note: Some forecasts handle non-OPEC liquids and NGLs differently.

Back to top

By adding the forecasts for OPEC producers, projected by their own governments, it is possible to illustrate the surplus between what OPEC would like to produce and what volume of oil from OPEC would be needed to balance supply with demand. The discrepancy between the two, as expressed by the area for the residual share left for Saudi Arabia, serves as a measure of market oversupply. It can be assumed that Saudi Arabia would like to produce at levels similar to the 1997 base case or some amount above that level.

In the first scenario shown where non-OPEC production grows to 49 million b/d, growth in Chinese oil demand is sufficient to bring the Saudi residual share close to 1997 base case levels. This result implies that under this plausible scenario, Saudi Arabia and other Persian Gulf producers will likely be able to reach an agreement to restrain production enough to defend moderate to higher price levels in the high teens. However, under this scenario, slightly higher Chinese oil demand than projected could be enough to drive prices higher, potentially back above $20 a barrel.

Table 9: Demand Scenarios for 2010 (Millions b/d)

Source

Base

IEA China

Baker Institute Low

Baker Institute High

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (14 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

1997

Scenario

China Demand

China Demand

Global Demand (total)

73.15

93.80

92.09

93.69

China

4.00

7.10

5.39

6.58

Global Supply

73.15

93.80

92.09

93.69

Non-OPEC

42.80

49.00

49.00

49.00

China

3.20

3.20

3.10

3.10

OPEC Total

30.35

44.80

43.09

44.69

OPEC Liquids

2.50

3.50

3.50

3.50

Iran

3.65

5.00

5.00

5.00

Iraq

1.20

6.00

6.00

6.00

Kuwait

2.00

4.00

4.00

4.00

UAE

2.30

3.50

3.50

3.50

Venezuela

3.40

6.00

6.00

6.00

Other OPEC

6.60

8.00

8.00

8.00

Saudi Arabia

8.70

8.80

7.09

8.69Back to top

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (15 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

However, China’s large increase in oil use would make a considerable difference under a scenario where non-OPEC production remained flat over the next decade. Under such a scenario, China’s expected oil demand growth would indeed contribute to a significant rise in international oil price levels. To meet rising Chinese and world demand, were non-OPEC production stagnant, OPEC would have to raise its current oil production capacity significantly beyond current plans for expansion. Otherwise, world oil markets would experience a large shortage of oil supply of several millions of barrels a day. This scenario is considered less likely by many forecast analysts, but could pose serious challenges to energy consuming countries.

By contrast, were non-OPEC production to rise by 54 million b/d, a rough mean of various analyst forecasts for 2010, Saudi Arabia and the Persian Gulf producers would have to shut in a considerable 3 million b/d to 4 million b/d of productive capacity to defend higher prices under either high or low scenarios for Chinese oil demand growth. Under this scenario, oil prices would remain under pressure much as they were in 1998.

Back to top

The Geopolitical Consequences Of China’s Oil Supply Alternatives

Over the past few decades, China has had the luxury of neutrality towards events in oil geopolitics. Oil prices inside China were fixed by the state central planners and had no relation to world price levels. Internal supplies fairly evenly matched domestic requirements. Its economy was sheltered from the volatile international oil scene and therefore, its leaders could be indifferent to conflicts in the Middle East or elsewhere. Oil disruptions neither hurt nor helped China substantially.

By contrast, the U.S. economy, as a major consumer and importer of oil, was vulnerable to sudden swings in international oil prices, dictating foreign policies that would promote stability in international oil markets. The U.S. navy defended Persian Gulf supplies while U.S. policy-makers worked to remove political and economic barriers to oil development outside the volatile region. The Soviet Union was a major oil exporter and its economy benefited directly from rising oil prices. Soviet interests in oil markets so diverged from American’s that policy theorists in the 1980s suggested the U.S. would benefit from events that could drive oil prices lower to hurt the Soviet treasury.

The implications of China’s shift to a world energy importer are significant. Over the next ten to twenty years, China will have to participate in international energy trade on a substantial and sustained basis, form energy supply and transportation alliances, and make security and environmental choices about fulfilling its future burgeoning energy needs. These trade and policy options will be constrained by economic factors, such as the unwieldy organization of China’s oil and gas industry and the aged and inefficient infrastructure that exists in China today as discussed above.

As China’s oil import levels rise to levels above 2 million b/d, it will be increasingly difficult for China to meet its crude oil import requirements without concluding large, long-term contracts for the supply of oil. Over the past year or so, China has indicated intentions to deepen its oil trading relationships with Iraq or Iran, leading to fears that Beijing will form oil-for arms, military-client relationships with these nations. This would mean that a conflict between either of Iraq or Iran and a U.S. ally in the Persian Gulf could draw China into conflict with Western powers.

Ironically, however, Chinese politicians and energy planners may not be thinking and analyzing in unison. One explanation might be the legacy of the historical split in operations between exploration activities by CNPC, refining activities by SINOPEC and supply and trading activities by SINOCHEM. China’s oil sector may not be able to benefit directly from access to very large volumes of oil from Iraq and Iran. As mentioned above, aged and unsophisticated oil refining equipment throughout most of China means that Chinese oil firms are limited in the quality of oil they can process. China cannot refine large amounts of most of the lower quality supplies that are produced in Persian Gulf countries such as Iraq, Iran, Saudi Arabia and Kuwait. By 2005, China is only likely to be able to process little more than 1.35 million b/d of this lower quality Persian Gulf oil, though it will be able to import other high quality supplies from Abu Dhabi, Yemen and Oman. This commercial constraint will reduce at least the economic incentive for China to pursue client-state oil for arms alliances with any of the major Middle East producers unless large-scale investments --not yet planned-- can be made in its domestic refining sector.

China’s rising oil import requirements and the physical constraints of its refining sector suggests that China will become increasingly dependent on the same energy sources as the U.S., Japan, and other industrialized economies. This could tie its strategic interests more closely with Western interests in the Middle East. A rising reliance on Persian Gulf oil and gas imports imply that China will suffer the same negative consequences as the U.S., Japan and Europe if military equipment it or others pass to regimes such as those in Iraq or Iran is used to impede the free flow of oil from the Middle East or elsewhere. Continued political instability in Afghanistan or Central Asia will have similarly dire consequences for China’s chances of tapping Caspian energy supplies. However, it remains to be seen if China’s energy interests will be enough to alter China’s military’s perceptions of its own more general strategic interests, particularly on the issue of weapons non-proliferation. China may continue to perceive a benefit in diverting U.S. strategic engagement away from Asia. China’s leaders may view larger strategic interests in Asia – beyond the energy sector – as better served by diverting US diplomatic attention and military assets away from the Asian theatre to places like the Middle East. This latter interpretation of Chinese interests will depend greatly on Beijing’s perceptions of US intentions and their potential risk to China.

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (16 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

Some analysts worry that China’s dependence on the same energy supplies as its neighbors and Western industrial nations will prompt heightened competition in the energy arena and drive Asian regional arms races. Kent Calder notes that "Expansionist, confrontationist strategies, not to mention the acquisition of nuclear weapons, offer some attractive prospects of gain to regional powers, such as preferential access to energy resources and sea lanes in the South China Sea. The costs of armament and preparation for war, conversely, become less onerous as East Asia grows increasingly affluent. This combination of wealth and bellicosity is a recipe for disaster." But such predictions have already missed the mark on several counts and are likely to continue to do so.

While it is true that China will increasingly compete for similar energy supplies with Japan, South Korea and India, the possibility that this will lead to increased tensions and conflict is not a foregone conclusion. For one thing, as the above forecasts show, the possibility that the world will have a slight to moderate surplus of oil for the foreseeable future reduces the need for a confrontational posture towards supplies. And, Asia’s recent financial woes have reduced not only the rate of rising energy use but also the budgets for increased military spending . However, the possibility of a major supply disruption will continue to exist and with it, the risk that rivalry could emerge during a time of crisis.

Another reason China’s rising energy requirements might not disrupt balance of power politics in Asia is that China does not yet have the military muscle to challenge successfully the U.S. and its regional allies in the Asian seas. China lacks the military capability and the basing facilities to close Asian sea lanes for any extended period of time –should the U.S. Navy intervene to reopen them.

Chinese capabilities do include short-to-medium range ballistic and cruise missile systems that could threaten commercial energy shipments operating in Asian sea lanes. Still, even this capability would not be sufficient to defend its own incoming shipments of oil and other goods from retaliation by American or regional militaries in response to its own aggressive acts.

Thus, in formulating its future foreign policy in light of changes in its energy supply balance, China’s leadership will have to take a hard look at the possible outcomes from competition and conflict over energy resources and compare them to the potential benefits of cooperation on energy matters.

The flip-side of China’s basic inability to assert itself definitively in Asian sea lanes is that it will enhance Beijing’s interests in the free navigation in these areas in which the U.S. Navy plays a major role as defender.

Ironically, this change for China will coincide with a greater U.S. reliance on energy supplies from its own Western hemisphere, potentially raising burden-sharing issues with Asian nations about the expense of the U.S. military role in the Persian Gulf.

Baker Institute forecasts show that the Western hemisphere will become increasingly self-sufficient in oil supplies by the year 2000 and only slightly more dependent on imports from outside the hemisphere by 2010 (see pie chart table). By contrast, Asia’s reliance on oil imports from outside the Asia-Pacific region will grow steadily between 1998 and 2010, possibly reach as high as 20 to 21 million b/d over the next decade.

It remains to be seen whether China’s leadership can publicly acknowledge and accept the reality of the benefits it might incur from the U.S. naval presence in East Asia and the Middle East. For now, the regime still criticizes Japan for its reliance on "third parties" and calls for the U.S. to remove its military from Asia on the grounds that the Cold War threat has been resolved.

China may respond to its energy vulnerability by investing in on-land routes for the transportation of oil and gas from neighboring Kazakhstan. But as discussed above, this option can only make economic sense in a market where international oil prices top $13 -$15 a barrel (in current dollars) for a prolonged period. This, of course, does not preclude the possibility that China would nonetheless build and subsidize this pipeline to diversify its oil transport routes and further "energy security".

China’s dilemma regarding Asian sea lanes could potentially produce an excellent opportunity for improvement in U.S.-China relations. But it could also create a dangerous trigger for a deterioration of mutual trust. Implicit U.S. strategic guarantees to maintain open access to Asian routes for energy trade could give real meaning for Beijing to a U.S. China "strategic partnership." U.S or allied actions to disrupt China’s access to the same lines of energy transport would almost certainly have a deleterious effect on Pacific security and stability.

Back to top

Bibliography

Bernstein, Richard and Ross H. Munro. 1997. "The Coming Conflict with America."

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (17 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

Foreign Affairs, Vol. 76, No. 2. March/April 1997.

Calder, Kent E. 1997. Asia’s Deadly Triangle: How Arms, Energy and Growth Threaten to Destabilize Asia-Pacific. London: Nicholas Brealey.

Campbell, Colin J. and Jean H. Laherrere. 1998. "The End of Cheap Oil." Scientific American, March 1998.

Christoffersen, Gaye. 1998. "China’s Intentions for Russian and Central Asian Oil and Gas." NBR Analysis. Seattle: National Bureau of Asian Research, Vol. 9, No. 2, March 1998.

Department of Defense. 1998. "The United States Security Strategy for the East Asia-

Pacific Region." Washington, DC: DoD.

East-West Center data.

Energy Intelligence Group database.

Fesharaki, Fereidun 1998. "China Oil Price Reforms a Major Step in Deregulation of its Petroleum Sector" Oil and Gas Journal. Vol. 96 No. 32 August 10, 1998. P. 46

Horsnell, Paul. 1997. Oil in Asia: Markets, Trading, Refining and Deregulation. London: Oxford University Press.

Jaffe, Amy M. and Ronald Soligo. 1998. "Saudi Arabian Price Discrimination," prepared for The Baker Institute for Public Policy, Houston, Texas.

International Energy Agency (IEA). 1998. World Energy Outlook. Paris: OECD.

Lardy, Nicholas R. 1998. "China and the Asian Contagion." Foreign Affairs, Vol. 77, No. 4. July/August 1998.

Lewis, Steven. 1999. "Privatizing China’s State-Owned Oil Companies," prepared for

The Baker Institute for Public Policy. Houston, Texas.

Mahbubani, Kishore. 1997. "An Asia-Pacific Consensus." Foreign Affairs, Vol. 76, No. 5. September/October 1997.

Medlock, Kenneth B., III and Ronald Soligo. 1999. "The Composition and Growth in Energy Supply in China," prepared for The Baker Institute for Public Policy, Houston, Texas.

Pei, Minxin. 1998. "Is China Democratizing?" Foreign Affairs, Vol. 77, No. 1. January/February 1998.

Pillsbury, Michael. 1997. "Dangerous Chinese Misperceptions: The Implications for

DoD." Washington, DC: Office of Net Assessment, Department of Defense.

PIW. 1996. "US Sanctions Give Mideast Oil Play to China and Russia," Petroleum Intelligence Weekly, Vol. 35, No. 3, p. 3. January 1996.

PIW. 1997. "China Brings Ample Funding to CNPC’s Far Flung Oil Search," Petroleum Intelligence Weekly, Vol. 36, No. 33, p. 1. August 1997.

PIW. 1998. "China Picks Good Moment to Start Down Path to LNG."

Rodman, Peter W. 1998. Between Friendship and Rivalry: China and America in the 21st Century. Washington, DC: The Nixon Center.

Ross, Robert S. 1997. "Beijing as a Conservative Power." Foreign Affairs, Vol. 76, No. 2. March/April 1997.

Sankey, Paul and Gavin Thompson. 1999."Asia Pacific Energy Markets Service." Wood Mackenzie Asia Pacific Energy Consulting, January 1999.

Soligo, Ronald and Amy M. Jaffe. 1998. "The Economics of Pipeline Routes: TheConundrum of Oil Exports From the Caspian Basin," prepared

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (18 of 19)2/11/2004 7:06:29 AM

China's Growing Energy Dependence: The Costs and Policy Implications of Supply Alternatives

for The Baker Institute for Public Policy, Houston, Texas.

Back to top

http://www.bakerinstitute.org/Pubs/workingpapers/claes/cpis/cpis.html (19 of 19)2/11/2004 7:06:29 AM