CHARTING THE FINANCIAL CRISIS · Antecedents of the Crisis ... As panic spread, the nationÕs...

85

at BROOKINGS CHARTING THE FINANCIAL CRISIS U.S. Strategy and Outcomes January 2020

Transcript of CHARTING THE FINANCIAL CRISIS · Antecedents of the Crisis ... As panic spread, the nationÕs...

at BROOKINGS

CHARTING THE FINANCIAL CRISIS

U.S. Strategy and Outcomes

January 2020

Introduction

The global !nancial crisis and great recession of 2007–2009 constituted the worst shocks to the United States economy in

generations. Books have been and will be written about the housing bubble and bust, the !nancial panic that followed, the

economic devastation that resulted, and the steps that various arms of the U.S. and foreign governments took to prevent the

Great Depression 2.0. But the story can also be told graphically, as these charts aim to do.

What comes quickly into focus is that as the crisis intensi!ed, so did the government’s response. Although the seeds of the

harrowing events of 2007–2009 were sown over decades, and the U.S. government was initially slow to act, the combined e"orts

of the Federal Reserve, Treasury Department, and other agencies were ultimately forceful, #exible, and e"ective. Federal

regulators greatly expanded their crisis management tool kit as the damage unfolded, moving from traditional and domestic

measures to actions that were innovative and sometimes even international in reach. As panic spread, so too did their e"orts

broaden to quell it. In the end, the government was able to stabilize the system, re-start key !nancial markets, and limit the

extent of the harm to the economy.

No collection of charts, even as extensive as this, can convey all the complexities and details of the crisis and the government’s

interventions. But these !gures capture the essential features of one of the worst episodes in American economic history and the

ultimately successful, even if politically unpopular, government response.

Copyright © 2020 Hutchins Center at the Brookings Institution and Yale Program on Financial Stability

www.som.yale.edu/!nancialcrisischarts

1

Antecedents of the Crisis

In the years leading up to the crisis, the underlying performance of the U.S. economy had eroded in important ways.

2

%

0

1

2

4

3

5

200820052000199519901985198019751970

Sources: Congressional Budget O!ce, “An Update to the Economic Outlook: 2018 to 2028”; authors’ calculations

ANTECEDENTS

Because the growth of productivity and the labor force had slowed in the decade before the crisis, the potential economic growth rate was falling.Growth in real potential GDP

Productivity growthContribution to real potential GDP from:

Labor force growth

3

94

96

98

100

102

104

106

’08’07’06’05’04’03’02’01’00’99’98’97’96’95’94’93’92’91’90

ANTECEDENTS

Overall prime-age participation in the labor force had been falling, as the participation of women slowed and men’s continued a decades-long decline.Civilian labor force participation rates for people ages 25–54, indexed to January 1990=100

Women, ages 25–54

All people, ages 25–54

Men, ages 25–54

Source: Bureau of Labor Statistics via Haver Analytics

4

– 50

0

+ 50

+100

+150

+200

+250

+300%

200820052000199519901985198019751970

ANTECEDENTS

Income growth for the top 1 percent had risen sharply, driving income inequality to levels not seen since the 1920s.Cumulative growth in average income since 1979, before transfers and taxes, by income group

Bottom 20 percentof households

81st to 99thpercentiles of

households

Top 1 percentof households

Middle 60 percentof households

Source: Congressional Budget O!ce, “The Distribution of Household Income, 2014”

5

ANTECEDENTS

Meanwhile, the !nancial system was becoming increasingly fragile.

6

0

8

6

4

2

10%

2008200019901980197019601950194019301920

ANTECEDENTS

A “quiet period” of relatively low bank losses had extended for nearly 70 years and created a false sense of strength.Two-year historical loan-loss rates for commercial banks

Sources: Federal Deposit Insurance Corp.; Federal Reserve Board; International Monetary Fund

7

–15

–10

– 5

0

+ 5

+10

+15

+20%

200820052000199519901985198019751970

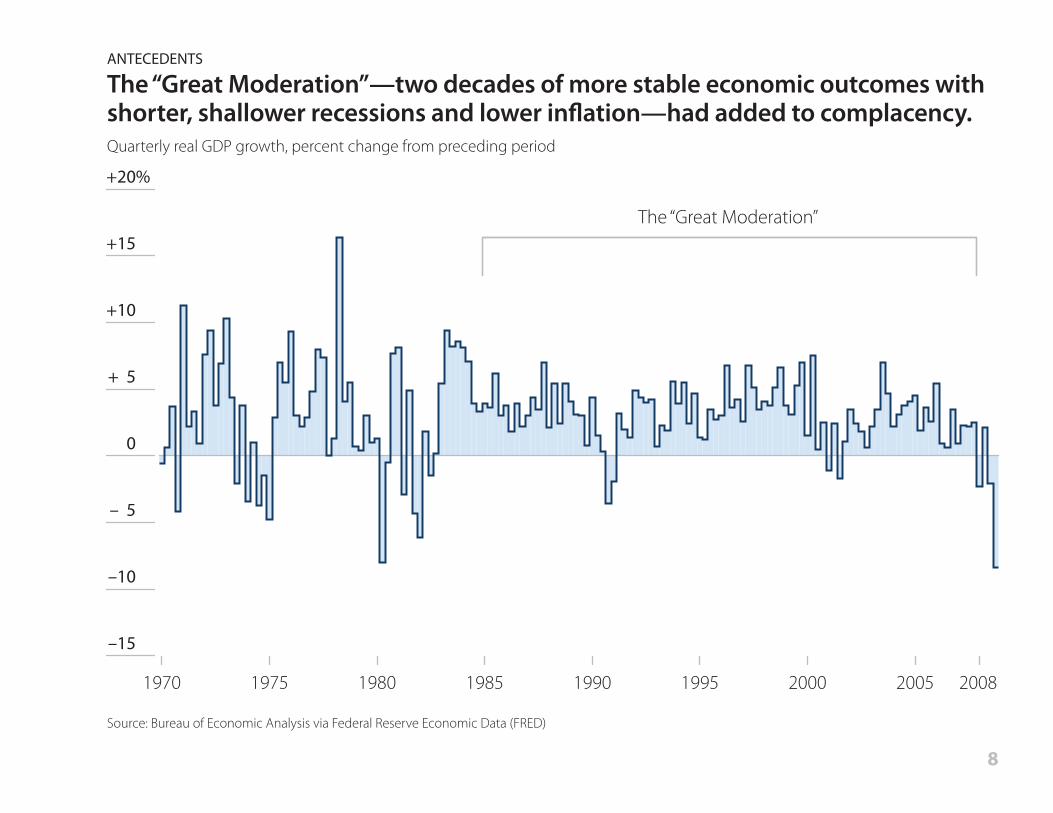

ANTECEDENTS

The “Great Moderation”—two decades of more stable economic outcomes with shorter, shallower recessions and lower in!ation—had added to complacency. Quarterly real GDP growth, percent change from preceding period

Source: Bureau of Economic Analysis via Federal Reserve Economic Data (FRED)

The “Great Moderation”

8

0

5

10

15

20%

200820052000199519901985198019751970

ANTECEDENTS

Long-term interest rates had been falling for decades, re!ecting decreasing in!ation, an aging workforce, and a rise in global savings.Benchmark interest rates, monthly

30-year !xedmortgage rate

10-yearTreasury 2-year

Treasury

Sources: Federal Reserve Board and Freddie Mac Primary Mortgage Market Survey® via Federal Reserve Economic Data (FRED)

9

1970 1975 1980 1985 1990 1995 2000 2005 2008

0

+ 40

+ 60

+ 80

+100%

+ 20

Home prices had increased modestly through several boom-and-bust cycles since the 1970s, but started a much more dramatic rise in the late 1990s.

ANTECEDENTS

Home prices across the country had been rising rapidly for nearly a decade.

Real home price index, percentage change from 1890

Source: U.S. Home Price and Related Data, Robert J. Shiller, Irrational Exuberance

10

0

20

40

60

80

100

120

140%

200820052000199519901985198019751970

ANTECEDENTS

Household debt as a share of income had risen to alarming heights.

Aggregate household debt as a share of disposable personal income

Source: Federal Reserve Board Financial Accounts of the United States, based on Ahn et al. (2018)

Mortgage debt

Consumer debt

11

0

50

100

150

200

250

200820052000199519901985198019751970

%

ANTECEDENTS

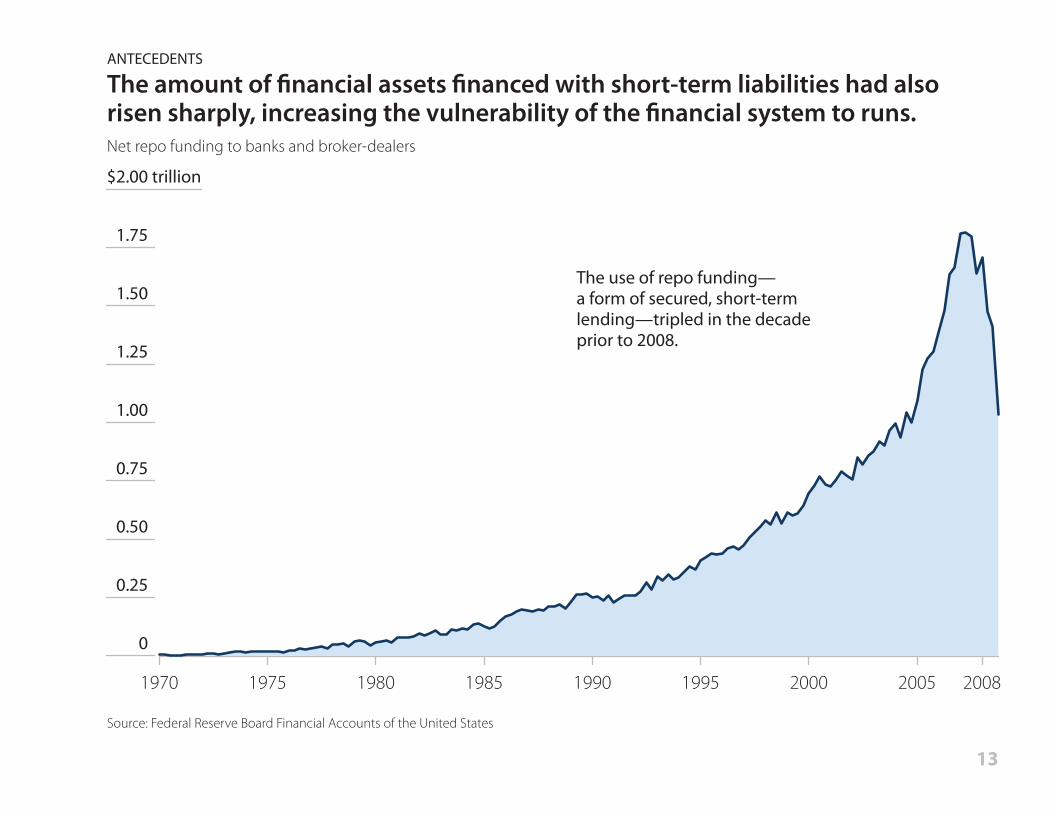

Credit and risk had migrated outside the regulated banking system.

Credit market debt outstanding, by holder, as a share of nominal GDP

Insurers

GSEs

ABS

MMFs

Notes: GSE: government-sponsored enterprise (including Fannie Mae and Freddie Mac); ABS: asset-backed securities issuers; MMFs: money market fundsSource: Federal Reserve Board Financial Accounts of the United States

Q1 198031%

69%

Q1 200864%

36%

Nonbank FinancialsBroker-Dealers

Banks

12

0

0.25

0.50

0.75

1.00

1.25

1.50

1.75

$2.00 trillion

200820052000199519901985198019751970

The use of repo funding—a form of secured, short-term lending—tripled in the decade prior to 2008.

ANTECEDENTS

The amount of !nancial assets !nanced with short-term liabilities had also risen sharply, increasing the vulnerability of the !nancial system to runs.Net repo funding to banks and broker-dealers

Source: Federal Reserve Board Financial Accounts of the United States

13

The Arc of the Crisis

14

0

100

200

300

400

500 basis points

200920082007

Two widely accepted indicators of !nancial sector stress are credit default swap (CDS) spreads, which measure the cost of insuring a !rm’s debt, and the Libor-OIS spread, which is a common measure of banks’ counterparty credit risk.

Bank CDSspreads

Notes: Credit default swap spreads are equal-weighted averages of JPMorgan Chase, Citigroup, Wells Fargo, Bank of America, Morgan Stanley, and Goldman Sachs. Libor-OIS spread used throughout is the spread between the 3-month London Interbank O"ered Rate and the 3-month USD overnight indexed swap rate.Sources: Libor-OIS: Bloomberg Finance L.P.; bank CDS spreads: Bloomberg Finance L.P., IHS Markit

ARC OF THE CRISIS

The !nancial crisis unfolded in several phases.

Bank credit default swap spreads and Libor-OIS spread

Libor-OISspread

Increasing Stress EarlyEscalation

Panic and Resolution

15

200820072006

–50

–40

–30

–20

–10

0

+10%

DetroitSan Francisco

MiamiTampa

Los AngelesSan Diego

PhoenixLas Vegas

Change, July 2006–March 2008–22.5%–22.6–23.1–23.4–24.4–25.6–26.6–27.7

ARC OF THE CRISIS

Home prices peaked nationally in the summer of 2006, then fell rapidly—eight major cities had declines of more than 20 percent by March 2008.Change in S&P CoreLogic Case-Shiller Home Price Indexes for 20 cities and U.S., from U.S. peak in July 2006, not seasonally adjusted

U.S. peak:July 2006

U.S. change by March 2008: –9.0%

Sources: S&P CoreLogic Case-Shiller Home Price Indexes for 20 individual cities and National Home Price Index via Federal Reserve Economic Data (FRED)

16

basis points

0

50

100

150

200

250

300

350

400

200920082007

Note: GSE: government-sponsored enterpriseSource: Bloomberg Finance L.P.

ARC OF THE CRISIS

Stress in the !nancial system built up gradually over late 2007 and early 2008, as mortgage troubles and recession fears increased.Libor-OIS spread

Bank of England provides emergency credit to Northern

Rock, a troubled mortgage lender, Sept. 14, 2007

Banks and GSEs start reporting billions in losses in Nov. 2007, and

warn of dividend cuts and a need for more capital; stocks fall

BNP Paribas freezes three funds on

Aug. 9, 2007, amid fragile ABS markets

JPMorgan Chase rescues Bear Stearns with emergency support from Federal Reserve, March 14, 2008

Stock markets plunge Jan. 21, 2008, amid recession fears

Bank of America announces intent to buy Countrywide Financial,

a troubled mortgage lender, Jan. 11, 2008

17

Libor-OISspread

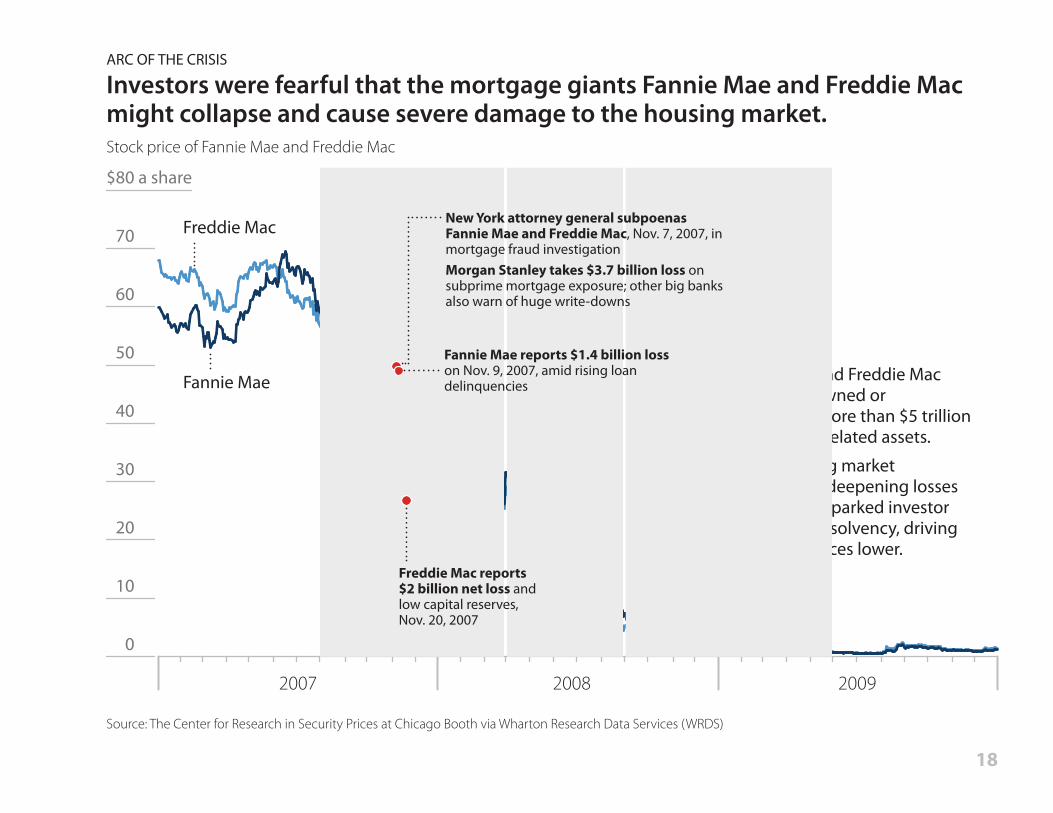

Fannie Mae and Freddie Mac collectively owned or guaranteed more than $5 trillion in mortgage-related assets.As the housing market deteriorated, deepening losses at both GSEs sparked investor concerns of insolvency, driving their share prices lower.

200920082007

0

10

20

30

40

50

60

70

$80 a share

Source: The Center for Research in Security Prices at Chicago Booth via Wharton Research Data Services (WRDS)

ARC OF THE CRISIS

Investors were fearful that the mortgage giants Fannie Mae and Freddie Mac might collapse and cause severe damage to the housing market.Stock price of Fannie Mae and Freddie Mac

Freddie Mac

Fannie Mae

New York attorney general subpoenas Fannie Mae and Freddie Mac, Nov. 7, 2007, in mortgage fraud investigationMorgan Stanley takes $3.7 billion loss on subprime mortgage exposure; other big banks also warn of huge write-downs

Fannie Mae reports $1.4 billion loss on Nov. 9, 2007, amid rising loan delinquencies

Freddie Mac reports$2 billion net loss andlow capital reserves,Nov. 20, 2007

18

200920082007

0

100

200

300

400

500

600

Note: Credit default swap spread is an equal-weighted average of JPMorgan Chase, Citigroup, Wells Fargo, Bank of America, Morgan Stanley, and Goldman Sachs.Sources: S&P 500 Financials: Bloomberg Finance L.P., S&P Dow Jones Indices LLC; bank CDS spreads: Bloomberg Finance L.P., IHS Markit

ARC OF THE CRISIS

As panic spread, the nation’s largest banks and investment banks looked increasingly vulnerable to failure.S&P 500 Financials index level, and average of six big banks’ CDS spreads in basis points

S&P 500 Financials

Averagebank CDSspread

Lehman Brothers !les for bankruptcy; Bank of America announces plans to acquire Merrill Lynch, Sept. 15, 2008Reserve Primary Fund “breaks the buck”;Fed rescues AIG with $85 billion credit facility, Sept. 16Fed authorizes Goldman Sachs and Morgan Stanley to become bank holding companies, Sept. 21Washington Mutual fails and is acquired in part by JPMorgan Chase, Sept. 25

S&P downgrades credit ratings of11 major global banks, Dec. 20, 2008

19

A self-reinforcing cycle of fear

ARC OF THE CRISIS

The rise in losses, the fear of further losses, and the liquidity pressures on the system pushed the price of !nancial assets down and added to concerns about the solvency of the !nancial system.

Economic or assetprice growth slows

People run from weak!nancial institutions

Financial institutionsunload assets in !re sale

Asset pricesdecline further

Banks lend less andpeople spend less

Economicgrowth slows

More !nancialinstitutions

look weak

20

–6

–3

0

+3

+6%

–9

2010200920082007Q4Q3Q2Q1 Q4Q3Q2Q1 Q4Q3Q2Q1 Q4Q3Q2Q1

ARC OF THE CRISIS

Yet the economic forecasts suggested a modest and manageable slowdown in economic growth. The forecasters were wrong. Real GDP, percent change from preceding quarter, SAAR, and Philadelphia Fed surveys of professional forecasters

Sources: Bureau of Economic Analysis via Federal Reserve Economic Data (FRED) (data update of Aug. 29, 2018); Philadelphia Federal Reserve Survey of Professional Forecasters, Q3 2007 and Q1 and Q3 2008

Professional Forecasters’GDP forecast, Aug. 2007

Actual GDP

Professional Forecasters’GDP forecast, Feb. 2008

Professional Forecasters’GDP forecast, Aug. 2008

21

The U.S. Strategy

22

U.S. STRATEGY

Among the key elements of the U.S. policy response were:

Use of the Fed’s lender-of-last-resort authorities beyond the banking system, for investment banks and funding markets.

An expansive use of guarantees to prevent runs on money market funds and a broad array of !nancial institutions.

An aggressive recapitalization of the !nancial system,in two stages, backed by expanded FDIC guarantees.

A powerful use of monetary and !scal policyto limit the severity of the recession and restore economic growth.

A broad mix of housing policies to prevent the failure of the GSEs, slow the fall of home values, lower mortgage rates, and aid in re!nancings.

An extension of dollar liquidity to the global !nancial system, combined with international cooperation and Keynesian stimulus.

23

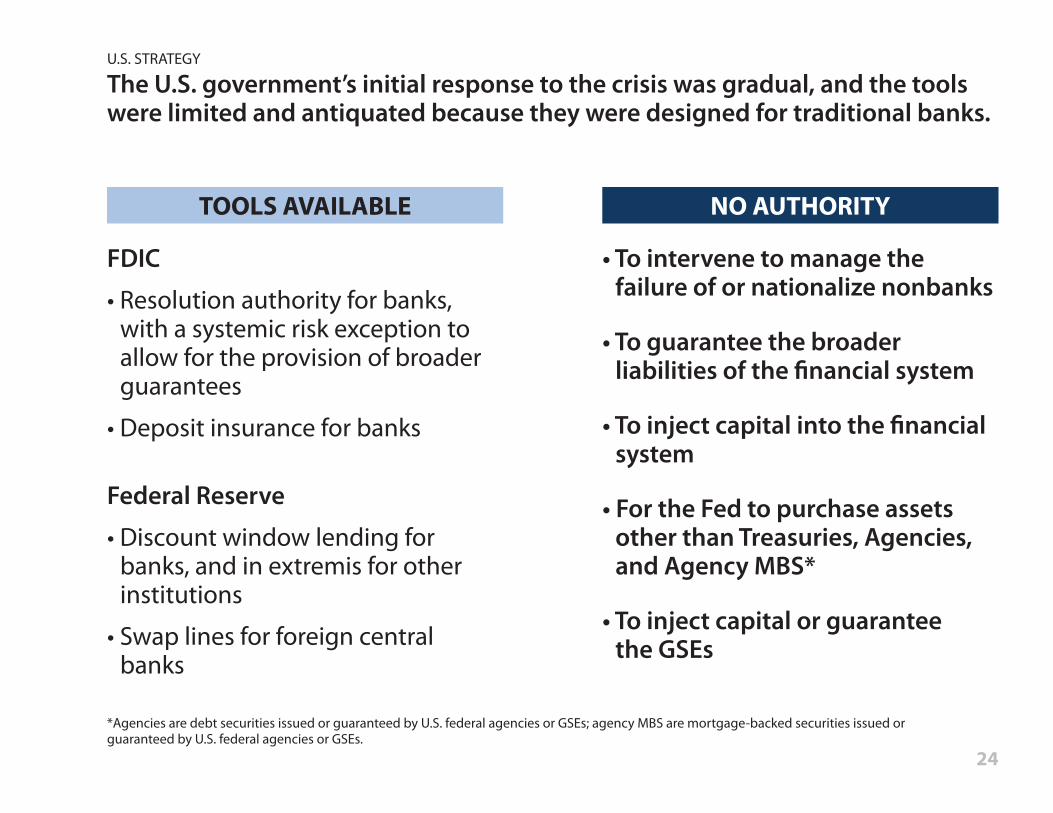

U.S. STRATEGY

The U.S. government’s initial response to the crisis was gradual, and the tools were limited and antiquated because they were designed for traditional banks.

FDIC• Resolution authority for banks,

with a systemic risk exception to allow for the provision of broader guarantees

• Deposit insurance for banks

Federal Reserve• Discount window lending for

banks, and in extremis for other institutions

• Swap lines for foreign central banks

TOOLS AVAILABLE

• To intervene to manage the failure of or nationalize nonbanks

• To guarantee the broader liabilities of the !nancial system

• To inject capital into the !nancial system

• For the Fed to purchase assets other than Treasuries, Agencies, and Agency MBS*

• To inject capital or guaranteethe GSEs

NO AUTHORITY

*Agencies are debt securities issued or guaranteed by U.S. federal agencies or GSEs; agency MBS are mortgage-backed securities issued or guaranteed by U.S. federal agencies or GSEs.

24

basis points

0

50

100

150

200

250

300

350

400

200920082007

Libor-OIS

Source: Libor-OIS: Bloomberg Finance L.P. Note: Start dates for programs re!ect the date of their announcement. The Federal Reserve administered the bank stress tests under the SCAP while the Treasury established a capital backstop under the CAP.

Increasing Stress EarlyEscalation

Panic and Resolution

U.S. STRATEGY

But the response became more forceful and comprehensive as the crisis intensi!ed and Congress provided new emergency authority.Libor-OIS spread

25

Systemic!nancialpolicies

Monetary and!scal policies

Housing andautos

International

Fannie, Freddie conservatorship (FHFA)

PPIP (Treasury)

Agency MBS Purchase Program (Treasury)

HAMP (Treasury)HARP (FHFA)

TALF (Fed, Treasury)

Recovery Act (Obama)Stimulus Act (Bush)

Central bank swap lines Swap line extension (Fed)

Quantitative easing (Fed)Fed funds interest rate cuts (Fed)

CPP (Treasury)

AIG stabilization (Fed, Treasury)

TLGP, deposit insurance (FDIC) CPFF (Fed)

MMF guarantees (Treasury)AMLF (Fed)

TSLF (Fed)Bear Stearns rescue (Fed)

Auto industry support (Treasury)

PDCF (Fed)

TAF TAF extension (Fed)

Stress tests (Fed, Treasury)

U.S. STRATEGY

The U.S. government deployed a mix of systemic policies to stabilize !nancial institutions and markets:

Liquidity programs to keep !nancial institutions operating and credit "owing to consumers and businesses.

Guarantee programs to support critical funding markets for !nancial institutions.

Capitalization strategies with private and government capital to prevent the failure of systemic institutions and resolve uncertainty about the !nancial system.

26

U.S. STRATEGY

As the crisis intensi!ed, the U.S. government’s liquidity programs expanded along several dimensions:

•"Domestic International

• Traditional Novel

• Institutions Markets

27

billion

0

100

200

300

400

500

$600 billion

0

100

200

300

400

500

$600

2010200920082007 2010200920082007

Source: Federal Reserve Board, based on English and Mosser (2020). Transaction-level data on discount window lending during the crisis were released under Freedom of Information Act court decisions (see: https://www.federalreserve.gov/foia/servicecenter.htm)

U.S. STRATEGY

The Federal Reserve initially deployed its traditional lender-of-last-resort tools to provide liquidity to the banking system.Federal Reserve discount window usage Term Auction Facility (TAF) usage

Use of theFed’s discountwindow

Term AuctionFacility

Banks were reluctant to borrow from the Fed’s discount window over fear it would signal they were in !nancial trouble . . .

. . . so the Fed initiated TAF in a similar role, and opened it to both domestic and foreign banks.

Foreign banksU.S. banks

28

billion

0

100

200

300

400

500

$600 billion

0

100

200

300

400

500

$600

20102009200820072010200920082007

Note: PDCF includes loans extended to select other broker-dealers.Source: Federal Reserve Board via Federal Reserve Economic Data (FRED)

U.S. STRATEGY

And then the Fed expanded its tools to support dealers and funding markets. Securities lent to dealers: Term Securities Lending Facility Primary Dealer Credit Facility (PDCF) loans

Term SecuritiesLending Facility

Primary DealerCredit Facility

. . . and then created the PDCF to provide emergency liquidity to investment banks, which did not have access to the discount window.

The Fed established the TSLF to promote liquidity in U.S. Treasury bonds and other important collateral markets . . .

29

0

3

6

9

12

15%

200920082007

Asset-backedcommercial paper

Commercial paper

Source: Federal Reserve Bank of New York based on data from the Federal Reserve Board of Governors, “Commercial Paper Rates and Outstanding Summary,” derived from data supplied by the Depository Trust & Clearing Corporation

U.S. STRATEGY

The Fed and Treasury introduced programs to address fragility in the commercial paper market, a key source of funding to !nancial institutions and businesses.Overnight issuance as a share of outstanding commercial paper

Commercial Paper Funding Facility (CPFF)announced by Fed, Oct. 7, 2008

Master Liquidity Enhancement Conduit (MLEC)On Oct. 15, 2007, Treasury facilitates plan for private banks to support the ABCP market; it is never implemented

BNP Paribas freezes three funds on Aug. 9, 2007,

amid fragile ABS markets

After the bankruptcy of Lehman Brothers, anxious investors demanded ultra-short terms for commercial paper, exposing issuers to signi!cant rollover risk amid the continued retreat of market liquidity.

AMLF and money market guarantees Sept. 19, 2008

Fed establishes ABCP Money Market Mutual Fund Liquidity

Facility; Treasury announces temporary guarantee program

for money market mutual funds, a major buyer of

commercial paper

Lehman bankruptcySept. 15, 2008

30

0

10

20

30

40

50

60

$70

20112010200920082007

billion

Sources: Federal Reserve Bank of New York based on data from JP Morgan, Bloomberg Finance L.P., and the Federal Reserve Board of Governors

U.S. STRATEGY

The Fed and Treasury also helped restart the asset-backed securitization market, a vital source of funding for credit cards, auto loans, and mortgage lending.Asset-backed securities issuance (eligible classes) and amount pledged to TALF

TALF, which becomes operational in March 2009, has an immediate e!ect on restoring market functionPPIP, introduced in February 2009, also supports the market

Lehman bankruptcyAfter the "rm’s collapse in September 2008, the ABS

market is nearly frozen

Early crisis average

Post-TALF and PPIP average

ABS market nearly frozen

Total issuance (eligible classes)Amount pledged to TALF

31

U.S. STRATEGY

The U.S. government put in place a mix of guarantees to backstop critical parts of the !nancial system.

32

DecemberNovemberOctober SeptemberAugust 2008

– 150

– 120

– 90

– 60

– 30

0

+ 30

+ 60

+$ 90 billion

Sources: iMoneyNet; authors’ calculations based on Schmidt et al. (2016)

U.S. STRATEGY

Treasury agreed to guarantee about $3.2 trillion of money market fund assets to stop the run on prime money market funds.Daily U.S. money market fund !ows

Prime institutionalmoney market fund !ows

Lehman bankruptcySept. 15, 2008before market

opened

Reserve Primary Fund “breaks the buck”Sept. 16, 2008; the fund held Lehman commercialpaper that was valued at zero after the bankruptcy

Treasury announces Temporary GuaranteeProgram for Money Market FundsSept. 19, 2008

Treasury opens guarantee programSept. 29, 2008

33

Increased coverage gave consumers and businesses more con!dence that their money was safe.

48

50

52

54

56

58

60

62%

Temporary increase to $250,000as authorized by the EmergencyEconomic Stabilization Act

$250,000 made permanentby Dodd-Frank

20112010200920082007

$100,000FDIC insurancecoverage

U.S. STRATEGY

The FDIC expanded its deposit insurance coverage limits on consumer and business accounts in an e!ort to prevent bank runs.Share of total deposits FDIC insured

Note: Does not include non-interest-bearing transaction account amounts insured by Dodd-Frank through the end of 2012.Source: U.S. Treasury, “Reforming Wall Street, Protecting Main Street”

FDIC-insureddeposits

53% 59%

34

0

50

100

150

200

250

300

350

$400 billion

20122011201020092008 200920082007

Nonbanks

Bank holdingcompanies

Commercialbanks 0

100

200

300

400

500 basis points

Bank CDSspreads

FDIC debtguarantees

*Debt Guarantee Program covered debt issued by both the parent company and its a!liates.Sources: Debt issuance: Federal Deposit Insurance Corp., authors’ calculations; CDS spreads: Bloomberg Finance L.P., IHS Markit

U.S. STRATEGY

By agreeing to guarantee new !nancial debt, the FDIC helped institutions obtain more stable funding.Debt outstanding under the TLGP (DGP)* Average-weighted CDS spread for six big banks

TLGP Debt Guarantee Program introduced

Oct. 14, 2008

35

U.S. STRATEGY

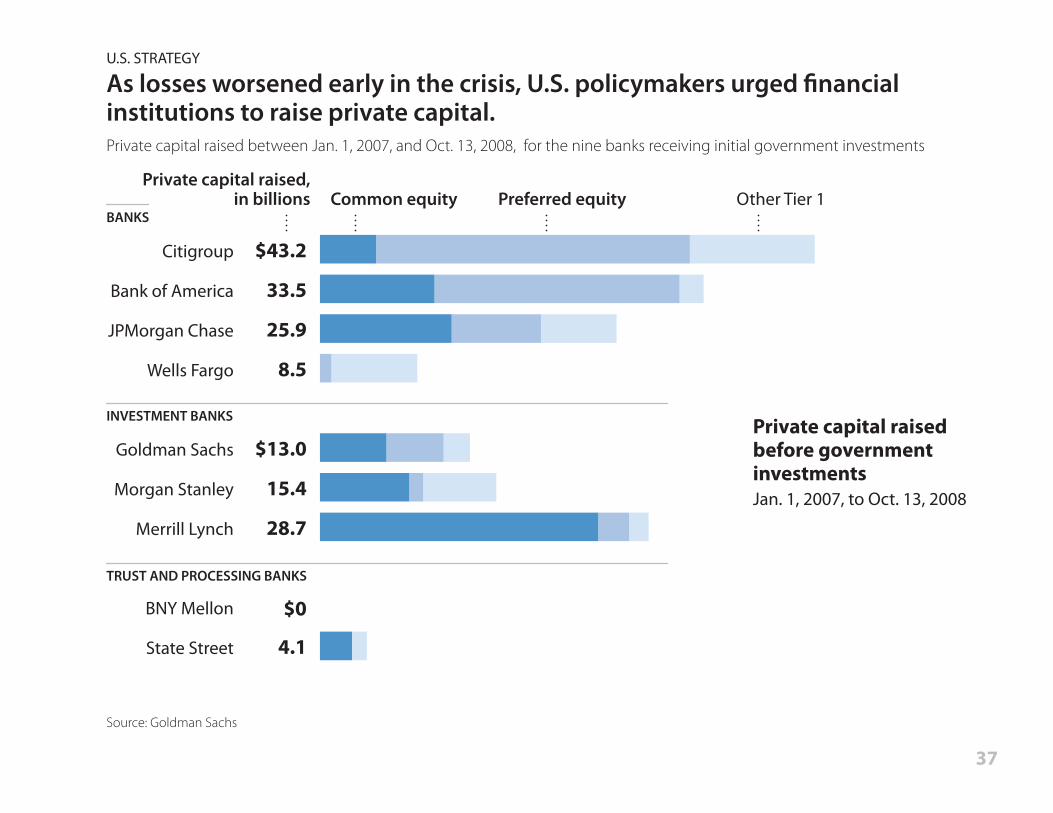

The U.S. government moved to strengthen the capital in the !nancial systemas the crisis intensi!ed by:

Encouraging the biggest institutions to raise private capital early in the crisis.

Injecting substantial government capital into the banking system when the crisis worsened and Congress providedemergency authority.

Stabilizing the most troubled banks with additional capitaland ring-fence guarantees.

Conducting stress tests to complete the recapitalization ofthe !nancial system.

36

Private capital raised,in billions

Private capital raisedbefore governmentinvestmentsJan. 1, 2007, to Oct. 13, 2008

33.5

25.9

$13.0

15.4

28.7

$0

4.1

8.5

State Street

BNY Mellon

Merrill Lynch

Morgan Stanley

Goldman Sachs

Wells Fargo

$43.2Citigroup

JPMorgan Chase

Bank of America

Common equity Preferred equity Other Tier 1

U.S. STRATEGY

As losses worsened early in the crisis, U.S. policymakers urged !nancial institutions to raise private capital.Private capital raised between Jan. 1, 2007, and Oct. 13, 2008, for the nine banks receiving initial government investments

Source: Goldman Sachs

BANKS

INVESTMENT BANKS

TRUST AND PROCESSING BANKS

37

Capital raised,in billions

35.0

25.0

$15.8

10.0

10.0

$3.0

2.0

37.7

$59.1

State Street

BNY Mellon

Merrill Lynch

Morgan Stanley

Goldman Sachs

Wells Fargo

JPMorgan Chase

Bank of America

Citigroup**

Governmentpreferred equity*

Government TargetedInvestment Program capital

Governmentand othercapital raisedOct. 14, 2008, toMay 6, 2009$10 billion goes to Bank of America

after acquisition of Merrill Lynch

Private common equity

Otherpreferred equity

OtherTier 1

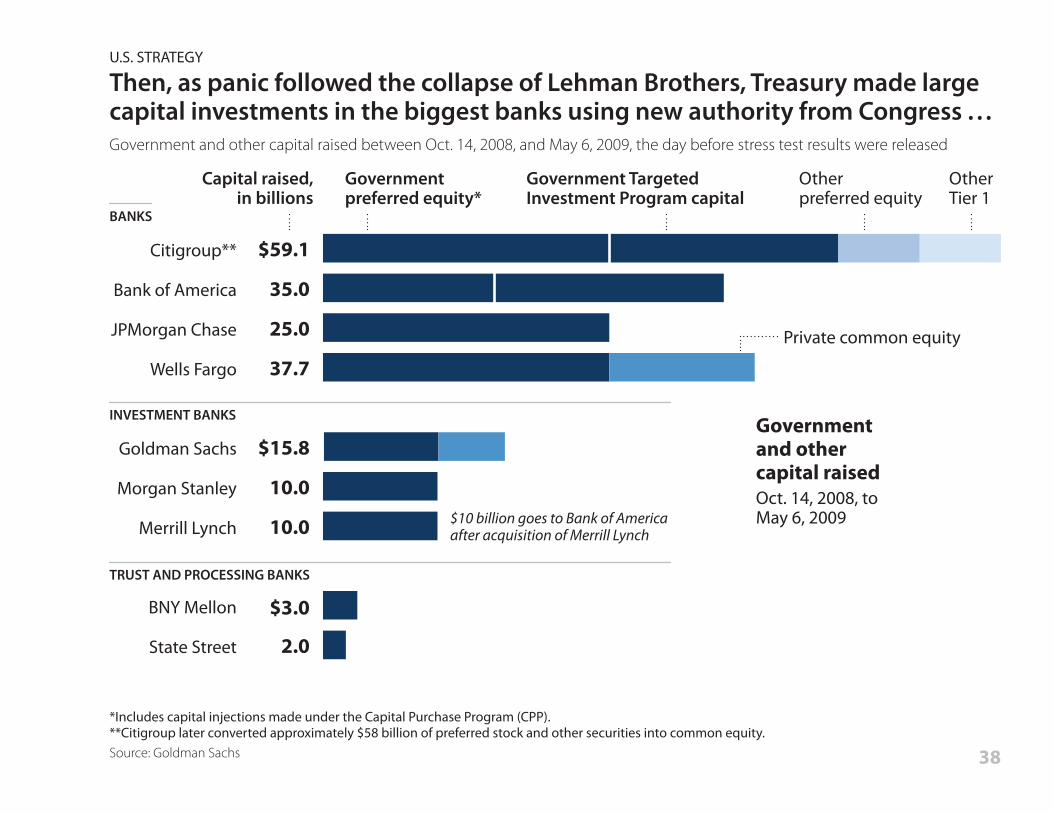

U.S. STRATEGY

Then, as panic followed the collapse of Lehman Brothers, Treasury made large capital investments in the biggest banks using new authority from Congress . . .Government and other capital raised between Oct. 14, 2008, and May 6, 2009, the day before stress test results were released

*Includes capital injections made under the Capital Purchase Program (CPP). **Citigroup later converted approximately $58 billion of preferred stock and other securities into common equity.Source: Goldman Sachs

BANKS

INVESTMENT BANKS

TRUST AND PROCESSING BANKS

38

0

50

100

150

200

250

$300 billion

2014201320122011201020092008

By the end of 2008, more than 200 banks had received funds under the Capital Purchase Program. Overall, $205 billion would be distributed to 707 banks.An additional $40 billion was split between Citigroup and Bank of America under the Targeted Investment Program.

Government capital investmentsin banks

Sources: Timeline of funds outstanding: TARP Tracker; banks receiving funds, by asset size: U.S. Treasury, “Troubled Asset Relief Program: Two Year Retrospective,” SNL Financial; banks receiving funds, by state: authors’ calculations based on TARP Investment Program transaction reports, Aug. 8, 2018

U.S. STRATEGY

. . . and used additional funds to make direct government investments inhundreds of smaller banks.Principal outstanding for government bank capital investments Distribution of banks participating in the Capital Purchase Program

0 1 to 10

Less than$1 billion

$1 to $10billion

Over $10billion

Banks receiving funds: by asset size

Banks receiving funds: by state11 to 20 21 to 30 31 to 71

473 banks 177 57

39

CitigroupCDSspreads

0

100

200

300

400

500

600

700 basis points

2010200920082007

*The Federal Reserve Bank of New York’s loss position was structured in the form of a nonrecourse loan.Sources: Asset Guarantee Program terms: Special Inspector General for TARP, “Extraordinary Financial Assistance Provided to Citigroup, Inc.”; CDS spreads: Bloomberg Finance L.P., IHS Markit

U.S. STRATEGY

In addition to capital injections, the government expanded its tools with asset guarantees for the most troubled banks, Citigroup and Bank of America.Asset Guarantee Program (AGP), Citigroup assets, and “ring-fence” loss responsibility structure(Asset guarantees for Bank of America were drawn up but never implemented.)

Pool of Citigroupassets:$301 billion

Homemortgageloans$175.1 billion

MBS,commercialreal estate $76.3 billion

1st Loss 2nd Loss 3rd Loss Tail Loss

CitigroupAGP announcedNov. 23, 2008

Citigroup AGP asset pool !nalizedNov. 17, 2009

Citigroupexits AGP and repaysTARP fundsDec. 23, 2009

Other

Treasury$5.0 bil.

FDIC$10.0 bil.

Citigroup$39.5 bil.

Citigroup$0.6 bil.

Citigroup$1.1 bil.

Citigroup$24.5 bil.FRBNY*$220.4 bil.

40

0

$50

$100

$150

$200 billion

2012201120102009

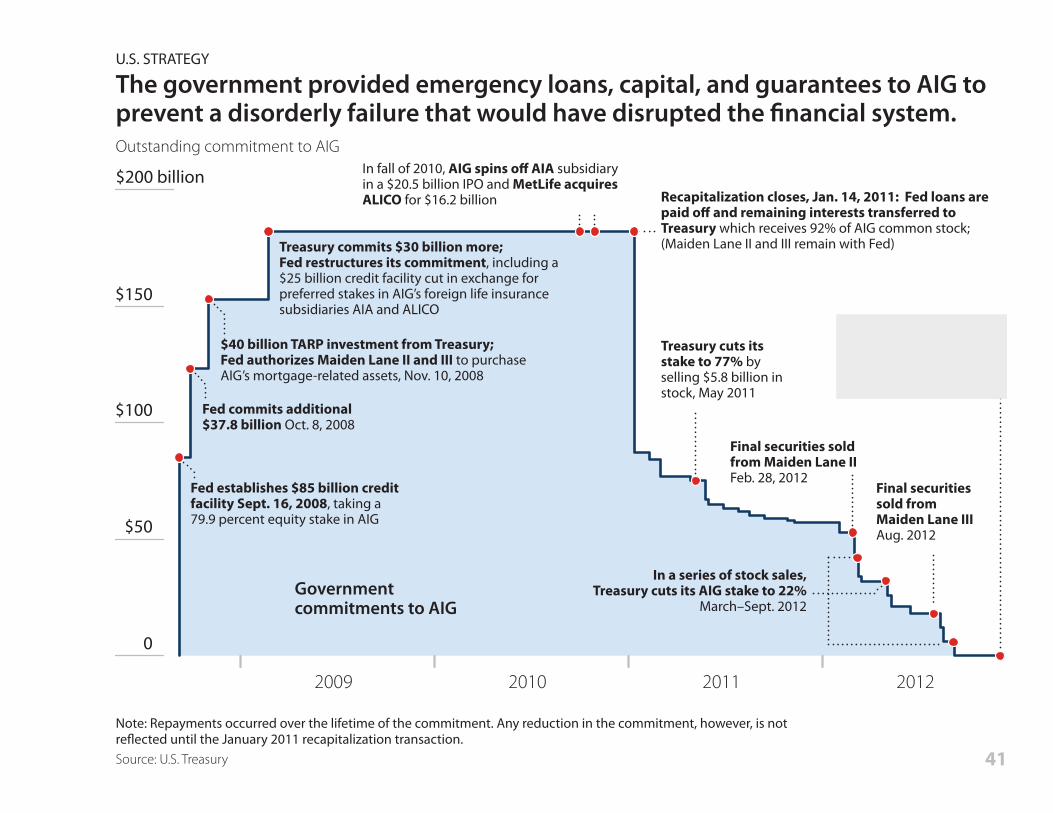

Note: Repayments occurred over the lifetime of the commitment. Any reduction in the commitment, however, is not re!ected until the January 2011 recapitalization transaction.Source: U.S. Treasury

U.S. STRATEGY

The government provided emergency loans, capital, and guarantees to AIG to prevent a disorderly failure that would have disrupted the !nancial system.Outstanding commitment to AIG

Fed establishes $85 billion credit facility Sept. 16, 2008, taking a 79.9 percent equity stake in AIG

In fall of 2010, AIG spins o! AIA subsidiary in a $20.5 billion IPO and MetLife acquires ALICO for $16.2 billion

Fed commits additional$37.8 billion Oct. 8, 2008

$40 billion TARP investment from Treasury;Fed authorizes Maiden Lane II and III to purchase AIG’s mortgage-related assets, Nov. 10, 2008

Treasury commits $30 billion more;Fed restructures its commitment, including a $25 billion credit facility cut in exchange for preferred stakes in AIG’s foreign life insurance subsidiaries AIA and ALICO

Treasury cuts its stake to 77% by selling $5.8 billion in stock, May 2011

In a series of stock sales,Treasury cuts its AIG stake to 22%

March–Sept. 2012

Final securities sold from Maiden Lane II Feb. 28, 2012

Final securities sold from Maiden Lane III Aug. 2012

Government makes $23 billion pro"tafter Treasury sells "nal

shares in AIG, Dec. 2012

Recapitalization closes, Jan. 14, 2011: Fed loans are paid o! and remaining interests transferred to Treasury which receives 92% of AIG common stock; (Maiden Lane II and III remain with Fed)

Governmentcommitments to AIG

41

0

2

4

6

8

10%

’10’00’90’80’70’60’50’40’30’20

U.S. STRATEGY

As con!dence in banks further eroded, government “stress tests” increased transparency, helping regulators and investors make credible loss projections . . . Two-year historical loan-loss rates for commercial banks SCAP capital shortfall, May 7, 2009

9.1%At 9.1% of outstanding loans,the Fed’s loss estimates for thestress test were higher than peaklosses during the Great Depression.

Note: The $74.6 billion in required capital is after earnings and capital measures in the !rst quarter of 2009. Citigroup’s requirement, for example, fell from $92.6 billion to $5.5 billion after adjusting for capital actions and earnings in the !rst quarter of 2009 and its plan to convert approximately $58 billion of preferred stock into common equity.Sources: Federal Deposit Insurance Corp.; Federal Reserve Board; International Monetary Fund

Two-year historical loan-loss ratesfor commercial banks

$0.6 PNC Financial

$1.1 Fifth Third Bank

$1.8 KeyCorp

$1.8 Morgan Stanley

$2.2 SunTrust Banks

$2.5 Regions Financial

$11.5 GMAC

$13.7 Wells Fargo

Bank ofAmerica$33.9

CAPITAL RAISES NEEDED, IN BILLIONS

$5.5 Citigroup

Of 19 institutions participating inthe Supervisory Capital Assessment Program (SCAP), ten were requiredto raise $74.6 billion in capital; nine others did not need additional capital.

42

Private capital raised,in billions

Private capital raisedafter stress testresults releasedMay 7, 2009, throughDec. 31, 2010

9.8

$22.7

32.8

$0

6.9

—

$2.8

2.3

20.9

State Street

BNY Mellon

Merrill Lynch Acquired by Bank of America

Morgan Stanley

Goldman Sachs

Wells Fargo

JPMorgan Chase

Bank of America

Citigroup

Common equity Preferred equityOther Tier 1

U.S. STRATEGY

. . . and accelerated the return of private capital.

Private capital raised, May 7, 2009, through Dec. 31, 2010

Note: In April 2009, before the release of stress test results, Goldman Sachs raised $5.8 billion in capital for the repayment of TARP funds.Source: Goldman Sachs

BANKS

INVESTMENT BANKS

TRUST AND PROCESSING BANKS

43

0

20

40

60

80

100

$120 billion

201620152014201320122011201020092008

U.S. STRATEGY

Indeed, the U.S. recapitalized its banking system more quickly and aggressively than Europe.Capital raised each year

Note: Authors’ estimates based on !gures from Goldman Sachs.Source: Goldman Sachs

U.S. banks~90% of 2008–2016 capital was raised 2008–2010

European banks~50% of 2008–2016 capital was raised 2008–2010

44

U.S. STRATEGY

Alongside programs designed to address the systemic problems in the !nancial system, the Fed and Treasury put in place a forceful mix of monetary policy and !scal stimulus.

45

0

’12’11’10’09’08’07

0

50

100

150

$200 billion

1

2

3

4

5

6%

’12’11’10’09’08’07

Fed funds target rateUpper bound

Fed assetpurchases

10-year Treasury rate

Sources: Target rate: Federal Reserve Board; 10-year Treasury: Federal Reserve Board via Federal Reserve Economic Data (FRED); monthly asset purchases: Federal Reserve Bank of New York, Haver Analytics

U.S. STRATEGY

As the Fed funds rate neared zero, the Fed made large-scale asset purchases to drive down long-term interest rates—a policy known as quantitative easing. Fed funds target rate or range and 10-year Treasury rate Gross asset purchases, monthly

Target range

QE 1 QE 2 QE 3

QE 1 QE 2 QE 3

TreasuriesAgency debtMBS

46

0

+0.5

+1.0

+1.5

+2.0

+2.5

+3.0

+3.5

+4.0%

201220112010200920082007

Note: $168 billion represents the combined stimulus from pre–Recovery Act measures through 2012.Sources: Council of Economic Advisers; Congressional Budget O!ce; Bureau of Economic Analysis; calculations by Jason Furman

U.S. STRATEGY

The U.S. passed the !rst !scal stimulus very early in the crisis. But at$168 billion, it was relatively small and needed time to take e"ect. Quarterly e"ect of #scal stimulus measures on GDP

Estimated impact on GDPfrom !scal legislation

Post–Recovery ActRecovery ActPre–Recovery Act

Economic StimulusAct of 2008Feb. 13, 2008

Supplemental Appropriations ActJune 30, 2008

Housing and Economic Recovery Act (HERA) July 31, 2008

Unemployment Compensation Extension Act Nov. 21, 2008

47

0

+0.5

+1.0

+1.5

+2.0

+2.5

+3.0

+3.5

+4.0%

201220112010200920082007

Note: $712 billion represents the stimulus from the Recovery Act through 2012.Sources: Council of Economic Advisers; Congressional Budget O!ce; Bureau of Economic Analysis; calculations by Jason Furman

U.S. STRATEGY

The Recovery Act of 2009 provided a larger mix—$712 billion—of temporary tax cuts and spending increases, o!setting some but not all of the fall in GDP.Quarterly e"ect of #scal stimulus measures on GDP

American Recovery and Reinvestment Act of 2009Feb. 17, 2009

Estimated impact on GDPfrom "scal legislation

Post–Recovery ActRecovery ActPre–Recovery Act

48

0

+0.5

+1.0

+1.5

+2.0

+2.5

+3.0

+3.5

+4.0%

201220112010200920082007

Note: $657 billion represents the combined stimulus from post–Recovery Act measures through 2012.Sources: Council of Economic Advisers; Congressional Budget O!ce; Bureau of Economic Analysis; calculations by Jason Furman

U.S. STRATEGY

A further $657 billion from a series of smaller post–Recovery Act measures added to the level of economic support . . . Quarterly e"ect of #scal stimulus measures on GDP

Estimated impact on GDPfrom !scal legislation

Post–Recovery ActRecovery ActPre–Recovery Act

Supplemental Appropriations ActJune 2009

Worker, Homeowner andBusiness Assistance Act;Defense Appropriations ActNov.–Dec. 2009

Temporary Extension Act; Hiring Incentives to Restore Employment Act March 2010

ContinuingExtension Act April 2010

Unemployment Compensation Extension Act;FAA Air Transportation Act; Small Business Jobs ActJuly–Sept. 2010

VOW Act; Temporary Payroll Tax Cut Continuation ActNov.–Dec. 2011

Tax Relief Act Dec. 2010

Middle-Class Tax Relief and Job Creation ActFeb. 2012

49

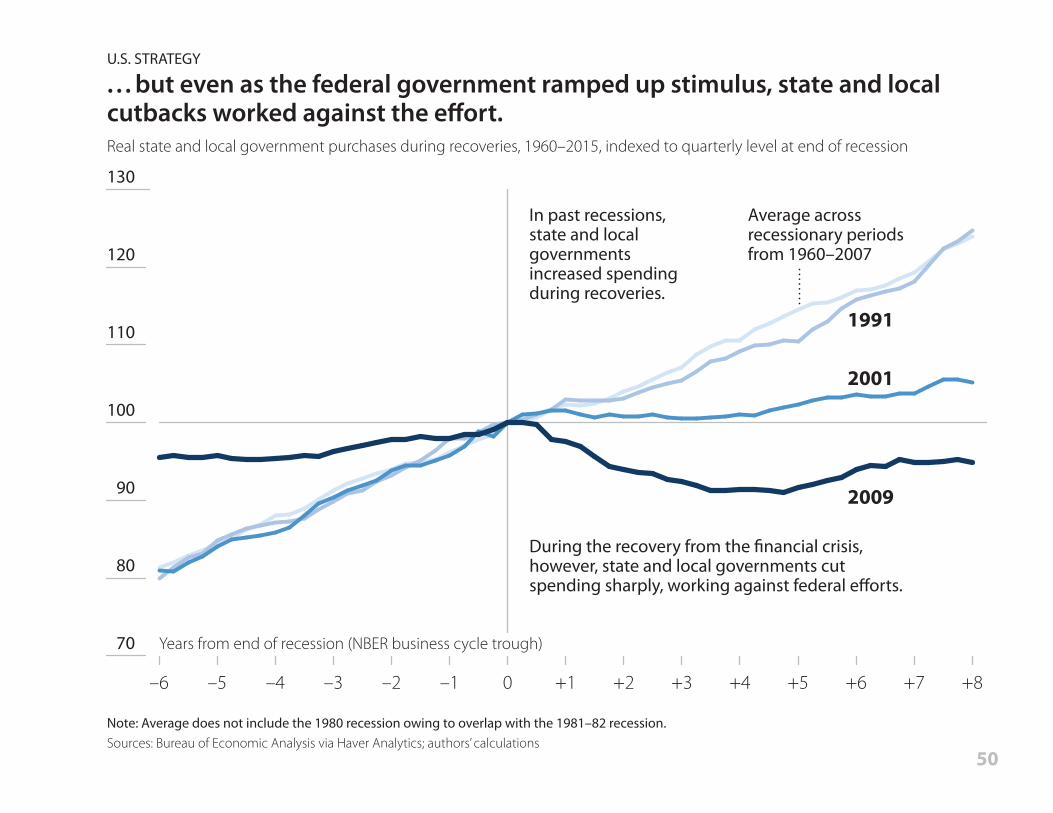

2009

2001

1991

Average acrossrecessionary periodsfrom 1960–2007

During the recovery from the !nancial crisis, however, state and local governments cut spending sharply, working against federal e"orts.

In past recessions, state and local governments increased spending during recoveries.

Years from end of recession (NBER business cycle trough)

U.S. STRATEGY

. . . but even as the federal government ramped up stimulus, state and localcutbacks worked against the e!ort. Real state and local government purchases during recoveries, 1960–2015, indexed to quarterly level at end of recession

Note: Average does not include the 1980 recession owing to overlap with the 1981–82 recession.Sources: Bureau of Economic Analysis via Haver Analytics; authors’ calculations

70

80

90

100

110

120

130

+8+7+6+5+4+3+2+10–1–2–3–4–5–6

50

U.S. STRATEGY

The government put in place a series of housing programs to:

•!Lower mortgage rates and ensure the availability of credit

• Reduce mortgage foreclosures

• Help struggling borrowers re"nance mortgages to take advantage of lower rates

51

0

1

2

3

4

5

6

7%

0

100

200

300

400

500

600

700,000

201620152014201320122011201020092008200720062005

Sources: Mortgage rates: Freddie Mac Primary Mortgage Market Survey® via Federal Reserve Economic Data (FRED); foreclosure completions: CoreLogic

U.S. STRATEGY

The government’s housing programs brought down mortgage rates and reduced foreclosures but were not powerful enough to contain the damage.30-year !xed mortgage rate Foreclosure completions, annual rate distributed evenly across four quarters

Hope NowOct. 10, 2007 Treasury and HUD facilitate creationof private loan modi!cation program

Home prices peakJuly 2006

HAMP and HARP Treasury releases details on Home A"ordable Modi!cation Program and Home A"ordable Re!nance Program, March 4, 2009

Fannie Mae, Freddie Mac conservatorship Sept. 7, 2008FHFA takes control of GSEsAgency MBS Purchase Program Treasury announces plan to purchase securities, also on Sept. 7

Quantitative easing Fed announces it will buy GSE debt and GSE-backed MBS, Nov. 25, 2008

FDIC-IndyMac modi!cationsProgram implementedAug. 20, 2008, for failed IndyMac Bank

ForeclosurecompletionsRight scale

30-year !xedmortgage rateLeft scale

52

0

50

100

150

200

250

$300 billion

0

50

100

150

200

250

300 basis points

201120102009200820072006

Agency MBS Left scale

Agency MBS spread Right scalePrivate-market MBS Left scale

Sources: MBS issuance: Securities Industry and Financial Markets Association; agency MBS spread: Bloomberg Finance L.P., authors’ calculations

U.S. STRATEGY

Government support of Fannie Mae and Freddie Mac kept mortgage credit !owing and stabilized the housing market after private issuers pulled back.Mortgage-backed securities issuance Agency MBS-to-Treasury spread

Fannie Mae, Freddie Macconservatorship Sept. 7, 2008

Senior Preferred Stock Purchase Agreements (SPSPAs)GSEs receive capital backstop of up to $100 billion, Sept. 26

Fed QE 1 Fed announces it will buyGSE debt and GSE-backed MBS, Nov. 25, 2008

First SPSPA Amendment increases commitmentto $200 billion per GSE, May 6, 2009

Second SPSPA Amendmentincreases commitmentagain, Dec. 24, 2009

53

0

100

200

300

400

500

600

700,000

201620152014201320122011201020092008200720062005

FHA lossmitigation

HAMP permanentmodi!cations

Private sectormodi!cations

Foreclosurecompletions

Note: Modi!cations through Nov. 2016; other program results through 2016. Foreclosure completions are plotted using an annual rate distributed evenly across four quarters.Sources: FHA loss mitigation: Dept. of Housing and Urban Development; HAMP modi!cations: U.S. Treasury; private sector modi!cations: HOPE NOW; foreclosure completions: CoreLogic

U.S. STRATEGY

Loan modi!cation programs, including HAMP, helped millions of struggling home owners with their mortgages.Mortgages modi!ed or receiving loss mitigation aid, April 1, 2009, through Nov. 30, 2016

Streamlined administrative processes,Aug. and Oct. 2009

Revised HAMP rules, March 2010, to encourage some principal write-downs to combat negative equity and to o"er some unemployed borrowers principal forbearance for up to three months

HAMP Tier 2 becomes e!ective,June 2012, facilitating modi!cations for non-GSE borrowers

Streamline HAMP announced, July 2015, allowing modi!cations for seriously delinquent borrowers with documentation limitations

54

0

100

200

300

400

500

600

700,000

201620152014201320122011201020092008200720062005

HARPre!nances

Note: Foreclosure completions are plotted using an annual rate distributed evenly across four quarters.Sources: Re!nances: Federal Housing Finance Agency; foreclosure completions: CoreLogic

U.S. STRATEGY

The Home A"ordable Re!nance Program lowered mortgage rates, encouraged re!nancings, and helped “underwater” home owners avoid foreclosure.Loans re!nanced through the Home A"ordable Re!nance Program

Foreclosurecompletions

Raised loan-to-value ceiling,July 2009, to allow somewhat deeper underwater borrowers to re!nance

Streamlined administrative processes, Aug. and Oct. 2009

HARP 2.0, Oct. 2011, eased representation and warranty requirements to increase pool of eligible borrowers and increase servicer participation

55

Other borrower assistanceLoan modi!cations5.3 million8.2 million

0

2

4

6

8

10

12 million

PROGRAMS

HAMP All trial and permanent loan modi!cations

HOPE NOW Proprietary modi!cations

GSE Standard and streamlined modi!cations

FHA MODIFICATIONS Additional loss mitigation

PROGRAMS

FHFA HomeSaver advance; repayment plans; forbearance plans; and foreclosure alternatives

FHA Loss mitigation interventions

STATE AND LOCAL HOUSING FINANCE AGENCY INITIATIVES Mortgages and !nanced units

HARDEST HIT FUND Local foreclosure prevention

Through2012

Through2017

Special re!nancings9.5 million

PROGRAMS

HARP Completed re!nances

FHFA Streamline re!nances

FHA Streamline re!nances Through

2012

Through2017

Through2012

Through2017

U.S. STRATEGY

The government’s programs helped millions of home owners, but were slow to take e"ect and reached a limited number of people threatened by foreclosure.Home owners assisted through crisis-era loan modi!cation programs and other foreclosure prevention actions

Source: Barr et al. (2020)

56

U.S. STRATEGY

Even though the crisis started in the United States, its impact reverberated around the world—and the response required U.S. policymakers to work closely with their global counterparts to:

Establish central bank swap linesto address dollar funding shortages

Coordinate monetary policyto send a powerful message to the markets

Arrange for IMF supportfor emerging markets countries a!ected by the crisis

57

By Oct. 14, 2008, the Fed had expanded currency swap lines to essentially unlimited amounts with four central banks: ECB, Switzerland, and the Banks of England and Japan.Limited swap lines were arranged with 10 other central banks:

billion

0

100

200

300

400

500

$600

Sources: Amounts outstanding: Federal Reserve Board, authors’ calculations; maximum commitments: Goldberg et al. (2010)

U.S. STRATEGY

The Federal Reserve established swap lines with more than a dozen foreign central banks to ease funding pressures arising from a shortage of dollars.Central bank liquidity swaps

Othercountries

JapanECB

Canada

Australia

Sweden

Brazil

Mexico

South Korea

Singapore

Denmark

Norway

New Zealand

Swap line limitsSwap line amounts outstanding

201020092008

Australia, Denmark, Norway, Sweden added Sept. 24, 2008

Japan, Bank of England, Canada added Sept. 18, 2008

Brazil, Mexico, New Zealand,South Korea, Singapore added Oct. 28–29, 2008

Fed establishes swap lines with the ECB and SwitzerlandDec. 12, 2007

$30

$30

$30

$30

$30

$30

$30

billions

$15

$15

$15

58

20122011201020092008 200720062005

0

1

2

3

4

5

6% target rate

United States

United Kingdom

Switzerland

Canada

EuropeanCentralBank

Japan

Source: Bloomberg Finance L.P.

U.S. STRATEGY

The Federal Reserve and the world’s major central banks orchestrated a coordinated interest rate cut.Central bank target interest rates for each country (month-end)

On Oct. 8, 2008, the Fed joins the European Central Bank, the Bank of England, and the central banks of Canada, Sweden, and Switzerland in cutting interest rates.

59

0

25

50

75

100

125

150

$175 billion

14 1513121110987654321Months after the start of new IMF lending

Asian !nancial crisis (1997–1998)

Global !nancial crisis (2008–2009)

Note: Start date for new IMF lending for the Asian !nancial crisis (AFC) is July 1997 and for the global !nancial crisis (GFC) is Sept. 2008. SDR data were converted to U.S. dollars at $1.355820 per SDR (the rate on July 31, 1997) for the AFC and $1.557220 per SDR (the rate on Sept. 30, 2008) for the GFC.Sources: International Monetary Fund; authors’ calculations based on Lowery et al. (2020)

U.S. STRATEGY

The IMF provided substantial aid to countries a"ected by the crisis, outpacing its response to the Asian !nancial crisis in 1997.Increase in IMF lending commitments from start of Asian and global !nancial crises

Proposal to expand New Arrangements to Borrow

resources of the IMF by up to $500 billion, April 2009

Flexible credit lines

Standby and extendedarrangements

Standby and extendedarrangements

60

Outcomes

61

21Peak 321 1Peak

%

–70

–60

–40

–30

–10

0

–50

–20

Peak

–25

–15

– 5

0%

–20

–10

–20

–15

– 5

0%

–10

Year later Year laterYear later

Notes: Stock declines shown to !nancial crisis trough; house prices 3 years after peak; household wealth !gures are based on the change between the nominal annual average of 1929 and of 1930, and the change in the nominal level from Q1 2008 to Q1 2009. Sources: Stock prices: The Center for Research in Security Prices at Chicago Booth via Wharton Research Data Services (WRDS); housing prices: U.S. home price and related data, Robert J. Shiller, Irrational Exuberance; GD household wealth: Mishkin (1978); GR household wealth: Federal Reserve Board Financial Accounts of the United States

OUTCOMES

The severity of the stress of the 2008 !nancial crisis was, in some respects, worse than in the Great Depression.Stock market prices from peak Nominal house prices from peak Decline in household wealth

Stock market House prices Householdwealth

FinancialCrisis–57.8%

FinancialCrisis–18.3% Financial

Crisis–14.1%

GreatDepression–44.9%

GreatDepression–6.2%

GreatDepression–6.0%

62

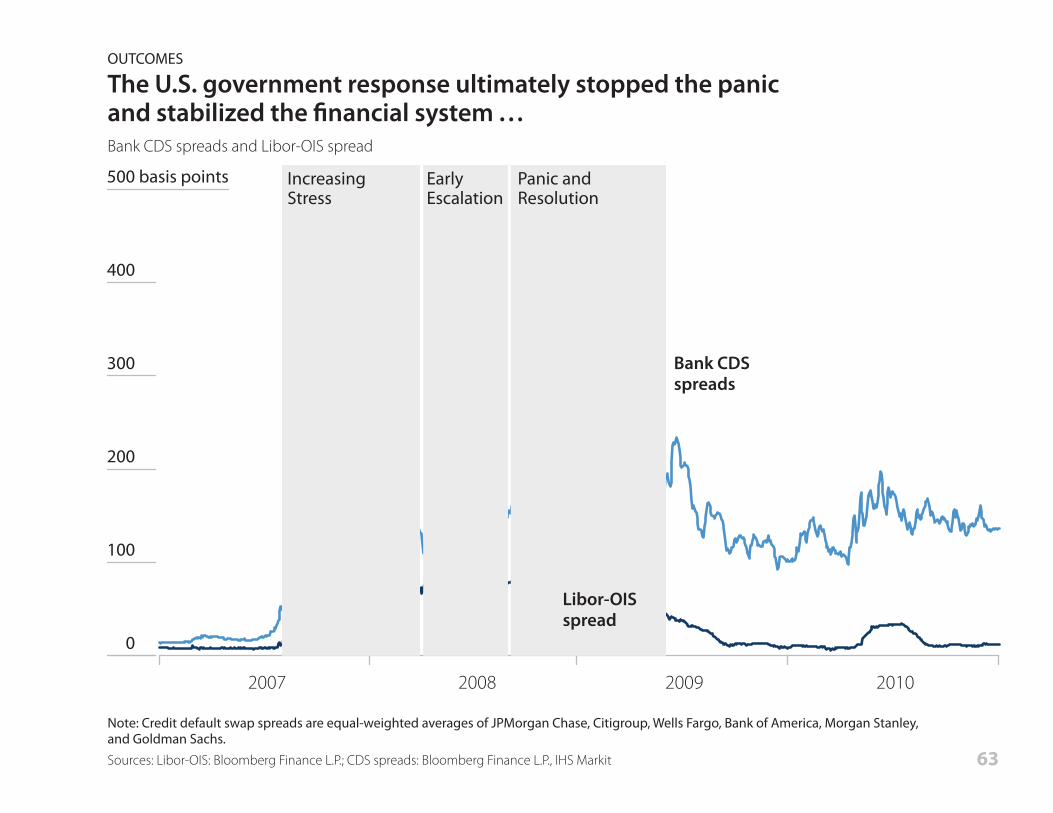

2010200920082007

0

100

200

300

400

500 basis points

Bank CDSspreads

Note: Credit default swap spreads are equal-weighted averages of JPMorgan Chase, Citigroup, Wells Fargo, Bank of America, Morgan Stanley, and Goldman Sachs.Sources: Libor-OIS: Bloomberg Finance L.P.; CDS spreads: Bloomberg Finance L.P., IHS Markit

OUTCOMES

The U.S. government response ultimately stopped the panicand stabilized the !nancial system . . .Bank CDS spreads and Libor-OIS spread

Libor-OISspread

IncreasingStress

EarlyEscalation

Panic andResolution

63

0

1

2

3

4

5

6

$7 trillion

201020092008

–6

–4

–2

0

+2

+4

+6%

OUTCOMES

. . . and allowed the economy to slowly begin digging out of adeep recession.Treasury, Federal Reserve, and FDIC exposures Real GDP and employment growth, year-over-year percent change (monthly)

Sources: Liang et al. (2020), based on U.S. government exposures: Congressional Oversight Panel, “Guarantees and Contingent Payments in TARP and Related Programs” via Federal Reserve Bank of St. Louis, Federal Deposit Insurance Corp., Federal Reserve Board, Federal Housing Finance Agency, U.S. Treasury; employment: Bureau of Labor Statistics; real GDP: Macroeconomic Advisers via Haver Analytics

GovernmentcommitmentsLeft scale

GuaranteesOther programsTARPFed liquidity

Real GDPYear-over-yearchange Right scale

EmploymentYear-over-yearchange Right scale

64

0

100

200

300

400

500

600

700 basis points

2010200920082007

+80

+60

+40

+20

0

–20%

2007 2008 2009 2010

Sources: ABS spreads: Federal Reserve Bank of New York based on data from JP Morgan and Bloomberg Finance L.P.; lending standards: Federal Reserve Board

OUTCOMES

The response helped restart the credit markets and bank lending so that !nancing was once again cheaper and easier to obtain.Consumer asset-backed security (ABS) spreads Net percentage of banks tightening loan standards

Credit lessavailable

Primemortgage

credit moreavailable

Triple-A-ratedcredit cardABS spread

Triple-A-ratedauto ABS spread

65!

0

1

2

3

4

5%

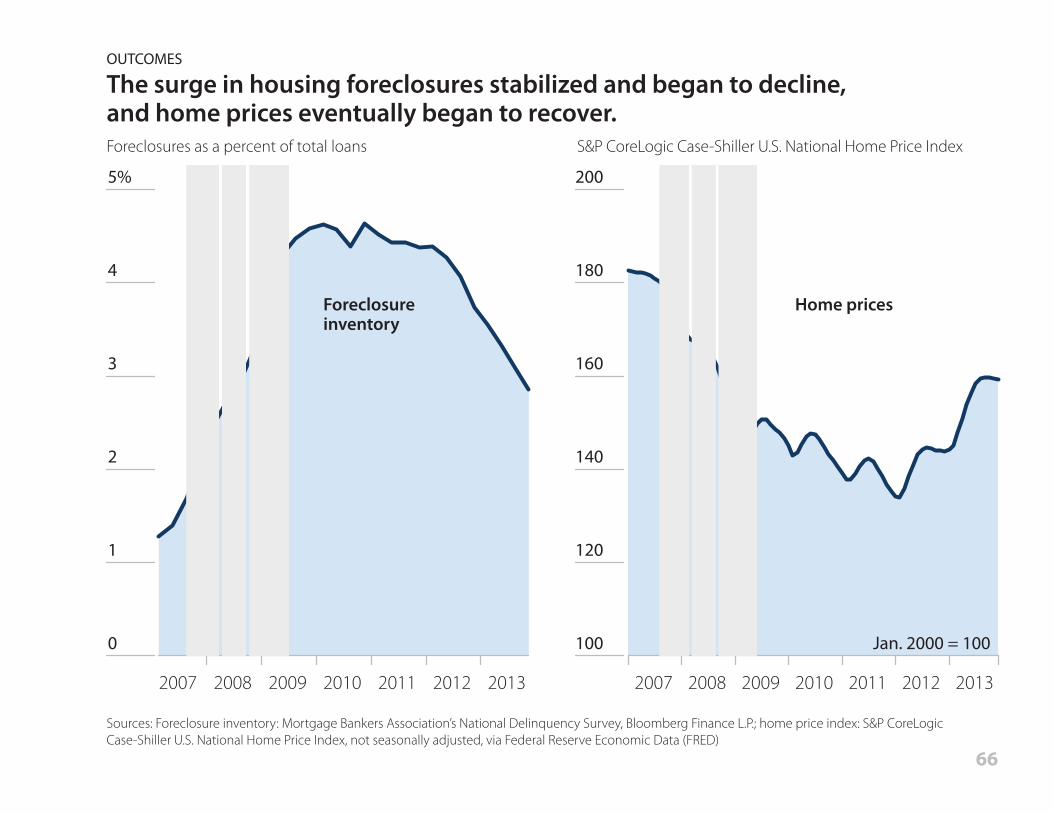

2013201220112010200920082007 2013201220112010200920082007

100

120

140

160

180

200

OUTCOMES

The surge in housing foreclosures stabilized and began to decline,and home prices eventually began to recover.Foreclosures as a percent of total loans S&P CoreLogic Case-Shiller U.S. National Home Price Index

Sources: Foreclosure inventory: Mortgage Bankers Association’s National Delinquency Survey, Bloomberg Finance L.P.; home price index: S&P CoreLogic Case-Shiller U.S. National Home Price Index, not seasonally adjusted, via Federal Reserve Economic Data (FRED)

Foreclosureinventory

Home prices

Jan. 2000 = 100

66

– 10

0

+10

20

+30

+40

+50%

109876543210

Q4 2007

2001

1990

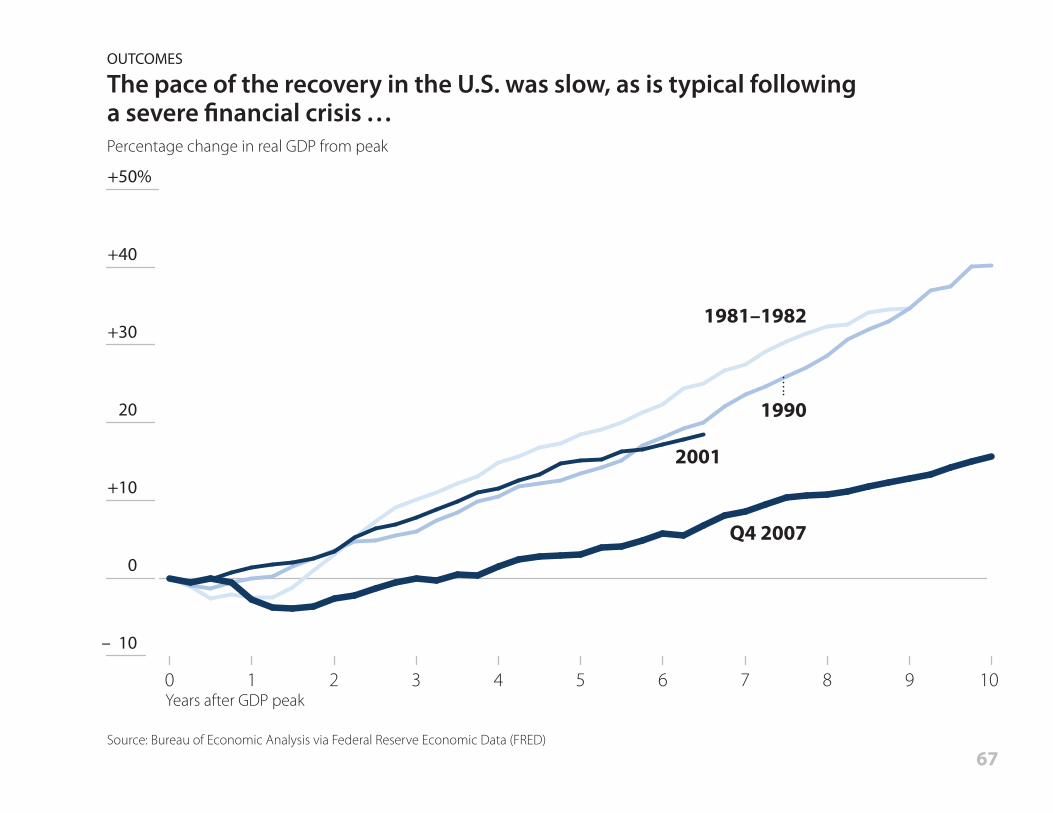

1981–1982

Years after GDP peak

OUTCOMES

The pace of the recovery in the U.S. was slow, as is typical followinga severe !nancial crisis . . . Percentage change in real GDP from peak

Source: Bureau of Economic Analysis via Federal Reserve Economic Data (FRED)67

–10

– 8

– 6

– 4

– 2

0

+ 2

+ 4

+ 6%

201320122011201020092008

Germany

United Kingdom

Italy

Spain

France

OUTCOMES

. . . although growth has been stronger than in many European countries. Real GDP, percentage change from 4th quarter 2007

Source: Organisation for Economic Co-operation and Development

United States

68

OUTCOMES

Financial crises are typically costly to economic output, but the U.S. strategy was able to limit the damage compared to other crises.

Sources: Reinhart and Rogo! (2009); Bureau of Economic Analysis via Federal Reserve Economic Data (FRED); based on comparisons from Liang et al. (2020)

Decline in output peak to trough(real GDP per capita)

How bad was the drop in GDP?

63 !nancial crises inadvanced economies,1857 to 2013

–9.6%

U.S. !nancial crisis

Duration of recessionHow long was the recession?

2.9years

1.5years

Recovery of output toprevious peak

How fast was the recovery?

7.3years

5.5years

–5.25%

69

OUTCOMES

U.S. taxpayers made a pro!t on the !nancial rescue.Income or cost of !nancial stability programs

Sources: Federal Deposit Insurance Corp.; Federal Housing Finance Agency; Federal Reserve Board; Webel and Labonte (2018); U.S. Treasury

CapitalInvestments

GSEsAIGCPPCitigroupBank of AmericaGMAC/AllyCDCIChrysler Financial

ChryslerGeneral Motors

Liquidity/Credit Markets

GSE Debt PurchasesCPFFTAFPPIPTALFTSLFMaiden LanePDCFAMLFSBA 7(a)

+$17.66.14.13.92.30.80.80.60.50.0

GuaranteePrograms

DGPMMF Guarantee

TAGP

+$10.21.2

–0.3

FDICResolution

In billions In billions

In billionsIn billions

Cumulative Income, 2008–10

DIF Losses, 2008–10

+$88.222.721.9

6.63.12.40.00.0

–1.2–10.5

+$45.4

–60.0

70

Bank holding companieswith more than$500 billion in assets

All institutions

Bank capital levels

0

2

4

6

8

10

12

14%

20172016201520142013201220112010200920082007200620052004200320022001

Long after the !nancial crisis, banks have continued to increase their capital, pushed in large part by more stringent regulatory requirements.

OUTCOMES

Today the !nancial system has signi!cantly more capital and would be better able to withstand losses in the event of a severe economic downturn.CET1 and Tier 1 common equity as percent of risk-weighted assets

Note: Capital ratio is based on tier 1 common equity pre-2014 and common equity tier 1 (CET1) as of 2015, and is a combination of the two during 2014.Source: Federal Reserve Bank of New York’s Research and Statistics Group

71

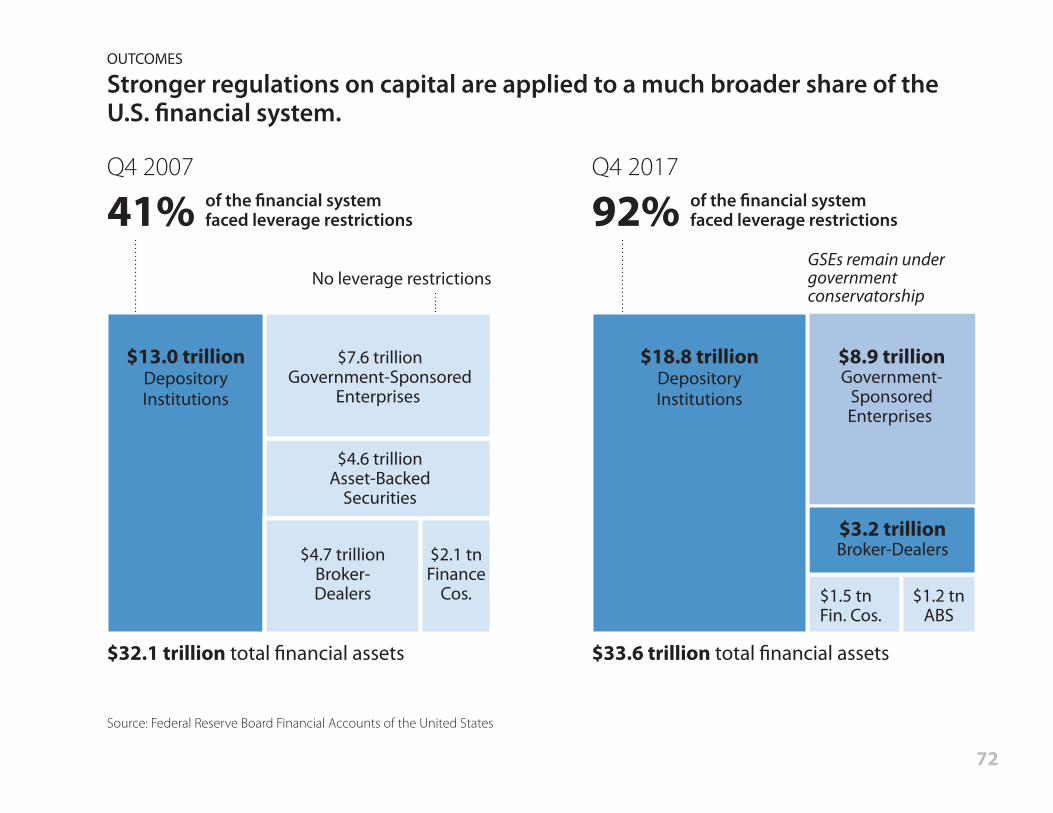

$32.1 trillion total !nancial assets $33.6 trillion total !nancial assets

GSEs remain undergovernmentconservatorship

OUTCOMES

Stronger regulations on capital are applied to a much broader share of the U.S. !nancial system.

Source: Federal Reserve Board Financial Accounts of the United States

$13.0 trillionDepositoryInstitutions

$18.8 trillionDepositoryInstitutions

$7.6 trillionGovernment-Sponsored

Enterprises

$8.9 trillionGovernment-

SponsoredEnterprises

$4.6 trillionAsset-Backed

Securities

$3.2 trillionBroker-Dealers

$1.2 tnABS

$1.5 tnFin. Cos.

$4.7 trillionBroker-Dealers

$2.1 tnFinance

Cos.

No leverage restrictions

Q4 2007

41% of the !nancial systemfaced leverage restrictions

Q4 2017

92% of the !nancial systemfaced leverage restrictions

72

OUTCOMES

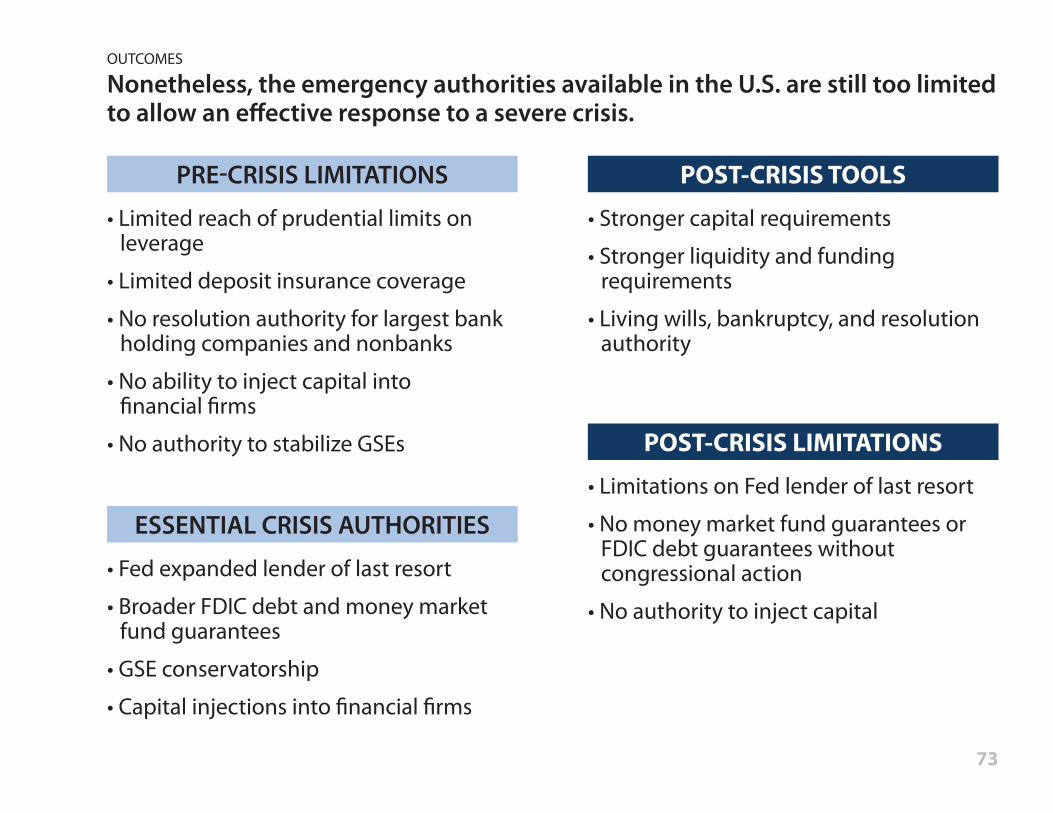

Nonetheless, the emergency authorities available in the U.S. are still too limited to allow an e!ective response to a severe crisis.

• Limited reach of prudential limits on leverage

• Limited deposit insurance coverage

• No resolution authority for largest bank holding companies and nonbanks

• No ability to inject capital into!nancial !rms

• No authority to stabilize GSEs

PRE"CRISIS LIMITATIONS

• Fed expanded lender of last resort

• Broader FDIC debt and money market fund guarantees

• GSE conservatorship

• Capital injections into !nancial !rms

ESSENTIAL CRISIS AUTHORITIES

• Stronger capital requirements

• Stronger liquidity and funding requirements

• Living wills, bankruptcy, and resolution authority

POST-CRISIS TOOLS

• Limitations on Fed lender of last resort

• No money market fund guarantees or FDIC debt guarantees without congressional action

• No authority to inject capital

POST-CRISIS LIMITATIONS

73

OUTCOMES

This was a terribly damaging crisis. It did not need to be so bad.

The damage illustrates the costs of running a !nancial system with weak oversight, and of going into a crisis without the essential tools for aggressive early action to prevent disaster.

The recovery was slow and fragile, made slower by the premature shift to tighter !scal policy.

Even after repairing the immediate damage, the U.S. economy still faces a number of longer-term challenges, with causes that predated the crisis.

74

ABCP asset-backed commercial paper

ABS asset-backed securities

AMLF Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility

CAP Capital Assistance Program

CDCI Community Development Capital Initiative

CDS credit default swaps

CET1 Common Equity Tier 1

CPFF Commercial Paper Funding Facility

CPP Capital Purchase Program

DGP Debt Guarantee Program

DIF Deposit Insurance Fund

EESA Emergency Economic Stabilization Act of 2008

FDIC Federal Deposit Insurance Corporation

FHA Federal Housing Administration

FHFA Federal Housing Finance Agency

GDP gross domestic product

GSEs government-sponsored enterprises

HAMP Home A!ordable Modi"cation Program

HARP Home A!ordable Re"nance Program

HUD U.S. Department of Housing and Urban Development

Libor-OIS London Interbank O!ered Rate–Overnight Indexed Swap rate

Acronyms

MBS mortgage-backed securities

MLEC Master Liquidity Enhancement Conduit

MMFs money market funds

NBER National Bureau of Economic Research

PDCF Primary Dealer Credit Facility

PPIP Public-Private Investment Program

QE Quantitative Easing

SAAR seasonally adjusted annual rate

SBA 7(a) Small Business Association Section 7(a) Securities Purchase Program

SCAP Supervisory Capital Assessment Program

SDR special drawing right

SPSPAs Senior Preferred Stock Purchase Agreements

TAF Term Auction Facility

TAGP Transaction Account Guarantee Program

TALF Term Asset-Backed Securities Loan Facility

TARP Troubled Assets Relief Program

TLGP Temporary Liquidity Guarantee Program

TSLF Term Securities Lending Facility

75

ABCP asset-backed commercial paper

ABS asset-backed securities

AMLF Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility

CAP Capital Assistance Program

CDCI Community Development Capital Initiative

CDS credit default swaps

CET1 Common Equity Tier 1

CPFF Commercial Paper Funding Facility

CPP Capital Purchase Program

DGP Debt Guarantee Program

DIF Deposit Insurance Fund

EESA Emergency Economic Stabilization Act of 2008

FDIC Federal Deposit Insurance Corporation

FHA Federal Housing Administration

FHFA Federal Housing Finance Agency

GDP gross domestic product

GSEs government-sponsored enterprises

HAMP Home A!ordable Modi"cation Program

HARP Home A!ordable Re"nance Program

HUD U.S. Department of Housing and Urban Development

Libor-OIS London Interbank O!ered Rate–Overnight Indexed Swap rate

MBS mortgage-backed securities

MLEC Master Liquidity Enhancement Conduit

MMFs money market funds

NBER National Bureau of Economic Research

PDCF Primary Dealer Credit Facility

PPIP Public-Private Investment Program

QE Quantitative Easing

SAAR seasonally adjusted annual rate

SBA 7(a) Small Business Association Section 7(a) Securities Purchase Program

SCAP Supervisory Capital Assessment Program

SDR special drawing right

SPSPAs Senior Preferred Stock Purchase Agreements

TAF Term Auction Facility

TAGP Transaction Account Guarantee Program

TALF Term Asset-Backed Securities Loan Facility

TARP Troubled Assets Relief Program

TLGP Temporary Liquidity Guarantee Program

TSLF Term Securities Lending Facility

Acronyms

76

This chart book was produced as part of an e!ort led by Ben S. Bernanke, Timothy F. Geithner,

and Henry M. Paulson, Jr., to examine the U.S. government’s interventions in the 2007–2009

"nancial crisis, a joint project of the Yale School of Management, Program on Financial

Stability, and the Brookings Institution, Hutchins Center on Fiscal and Monetary Policy.

Chart Book Project Advisers: Timothy F. Geithner and J. Nellie Liang

Editorial Director: Deborah McClellan

Chart Book Project Director: Eric Dash

Data Visualization: Seth W. Feaster

Lead Data Analyst: Ben HenkenData Analyst: Aidan Lawson

Acknowledgments

77

We wish to thank the following individuals and organizations:

Brookings/Hutchins: David Wessel, Director; Sage Belz, Je!rey Cheng, Vivien Lee, Michael Ng

Yale Program on Financial Stability: Andrew Metrick, Program Director; Alec Buchholtz, Anshu Chen, Greg Feldberg, Christian McNamara, Chase Ross, David Tam, Daniel Thompson, Rosalind Z. Wiggins

Golden Triangle Strategies: Monica Boyer, Emily Cincebeaux, Bill Marsh, Melissa Wohlgemuth

Others: Charlie Anderson, Matthew Anderson, Christie Baer, Michael S. Barr, James Egelhof, Jason Furman,Robert Jackson, Annabel Jouard, Katherine Korsak, Lorie Logan, Francis Mahoney, Vivek Manjunath,Drew McKinley, Patrick Parkinson, Wilson Powell III, Ernie Tedeschi

Data sources: Bloomberg Finance L.P.; the Center for Research in Security Prices at Chicago Booth; CoreLogic®, a property data and analytics company; Freddie Mac; Goldman Sachs; Haver Analytics;IHS Markit; iMoneyNet; Mortgage Bankers Association; Securities Industry and Financial Markets Association; SNL Financial; S&P Dow Jones Indices LLC; Standard & Poor’s; S&P® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC, and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC. © 2017 S&P Dow Jones Indices LLC, its a#liates and/or its licensors. All rights reserved; U.S. Dept. of Housing and Urban Development; Wharton Research Data Services (WRDS).

Acknowledgments

78

Additional data sources: Bureau of Economic Analysis; Bureau of Labor Statistics; Congressional Budget O#ce; Congressional Oversight Panel; Council of Economic Advisers; Federal Deposit Insurance Corp.; Federal Housing Finance Agency; Federal Reserve Bank of New York Financial Crisis Policy Response Timeline; Federal Reserve Bank of New York’s Research and Statistics Group; Federal Reserve Bank of Philadelphia; Federal Reserve Bank of St. Louis; Federal Reserve Bank of St. Louis Financial Crisis Policy Response Timeline; Federal Reserve Board; Federal Reserve Economic Data (FRED); International Monetary Fund; Macroeconomic Advisers®; Mishkin (1978); Organisation for Economic Co-operation and Development; U.S. Dept. of Treasury.

Acknowledgments

79

PAGE 5 Re-created with data underlying Figure 10, “The Distribution of Household Income, 2014,” Congressional Budget O!ce (2018), www.cbo.gov/publication/53597. See link for de"nitions of income and income groups.

PAGE 10 Based on Figure 3.1, U.S. home price and related data, Robert J. Shiller, Irrational Exuberance, 3rd ed. (Princeton, NJ: Princeton University Press, 2015), as updated by the author, www.econ.yale.edu/~shiller/data.htm.

PAGE 11 Based on Figure 1, Panel 1, Michael Ahn, Michael Batty, and Ralf Meisenzahl, “Household Debt-to-Income Ratios in the Enhanced Financial Accounts,” FEDS Notes (Washington, DC: Board of Governors of the Reserve System, January 11, 2018), https://doi.org/10.17016/2380-7172.2138.

PAGE 12 Based on Figure 4.1, Scott G. Alvarez, William Dudley, and J. Nellie Liang, “Nonbank Financial Institutions: New Vulnerabilities and Old Tools,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds., First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

PAGE 13 Based on Exhibit 1, Gary Gorton and Andrew Metrick, “Who Ran on Repo?” (2012), http://faculty.som.yale.edu/garygorton/documents/whorancompleteoctober4.pdf.

Banks’ portion includes net liabilities from federal funds agreements.

PAGE 28 Based on Figures 2.5 and 2.6, William English and Patricia Mosser, “The Use and E#ectiveness of Conventional Liquidity Tools Early in the Financial Crisis,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds. First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

Notes

PAGE 30 Based on Figure 3.7, Lorie Logan, William Nelson, and Patrick Parkinson, “The Fed’s Novel Lender of Last Resort Programs,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds., First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

PAGE 31 Based on Chart 5, Adam Ashcraft, Allan Malz, and Zoltan Pozsar, “The Federal Reserve’s Term Asset-Backed Securities Loan Facility,” Federal Reserve Bank of New York Economic Policy Review 18(3) (November 2012): 29-66, https://www.newyorkfed.org/medialibrary/media/research/epr/2012/EPRvol18n3.pdf.

PAGE 33 Based on Panel A, Lawrence Schmidt, Allan Timmermann, and Russ Wermers, “Runs on Money Market Mutual Funds,” American Economic Review 106(9) (2016): 2625–57, www.aeaweb.org/articles?id=10.1257/aer.20140678.

PAGE 34 Based on Slide 4, “Reforming Wall Street, Protecting Main Street,” U.S. Treasury, July 2012, www.treasury.gov/connect/blog/Documents/20120719_DFA_FINAL5.pdf.

PAGE 35 Commercial banks include depository institutions. Bank holding companies include bank holding companies, savings and loan holding companies, "nancial holding companies, and their funding a!liates. Nonbanks include nonbank entities and their a!liates, as well as bank holding companies with nonbank assets of nonbank subsidiaries comprising more than half of their total assets.

PAGE 41 Based on U.S. Treasury data and AIG infographic and timeline, www.treasury.gov/initiatives/"nancial-stability/TARP-Programs/aig/Pages/default.aspx.

PAGES 47, 48, 49 Based on Figure 16.3, Jason Furman, “The Fiscal Response to the Great Recession: Steps Taken, Paths Rejected, and Lessons for Next Time,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds., First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

PAGE 53 Monthly mortgage-related securities issuance "gures may not match annual "gures reported by the Securities Industry and Financial Markets Association on its website owing to a methodological di#erence in the reporting of each series.

PAGE 54 Based on the "gure “Mortgage Aid Extended More than 9.9 Million Times, Outpacing Foreclosures,” December 2016 Housing Scorecard, www.hud.gov/sites/documents/SCORECARD_2016_12_508C.PDF.

PAGE 56 Some home owners may have participated in more than one program; the sum of home owners helped across all categories does not necessarily re$ect the number of unique borrowers helped.

Based on Table 12.3, Michael Barr, Neel Kashkari, Andreas Lehnert, Phillip Swagel, “Crisis-Era Housing Programs,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds., First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

PAGE 58 Maximum commitments were taken from Table 2, Linda S. Goldberg, Craig Kennedy, and Jason Miu, “Central Bank Dollar Swap Lines and Overseas Dollar Funding Costs,” Federal Reserve Bank of New York Economic Policy Review 17(1) (May 2011): 3–20,www.newyorkfed.org/medialibrary/media/research/epr/11v17n1/1105gold.pdf.

PAGE 60 Based on Figure 17.9, Clay Lowery, Nathan Sheets, and Edwin (Ted) Truman, “International Coordination of Financial and Economic Policies,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds., First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

PAGE 62 The stock market (NYSE/AMEX/NASDAQ/ARCA) is measured by total market value as reported by the Center for Research in Security Prices and is shown to "nancial crisis trough. House prices are shown to three years after peak. Household wealth is a comparison between the change in the annual average (in nominal terms) of household wealth from 1929 to 1930, and the change in the nominal level of household wealth from Q1 2008 to Q1 2009.

Estimates of real household net worth (wealth) during the Great Depression were taken from Table 1, Frederic S. Mishkin, “The Household Balance Sheet and the Great Depression,” The Journal of Economic History 38(4) (December 1978): 918–37, www.jstor.org/stable/2118664.

PAGE 64 Guarantees: Re$ects the U.S. Treasury’s maximum commitments under the Temporary Guarantee Program for Money Market Funds and the FDIC’s maximum commitments under the two components of the Temporary Liquidity Guarantee Program, the Debt Guarantee Program, and the Transaction Account Guarantee Program.

Troubled Assets Relief Program (TARP): Re$ects principal outstanding for TARP programs including bank support programs, credit market programs, auto industry support, assistance to American International Group, and housing programs.

Federal Reserve Liquidity Programs: Re$ects loan amounts outstanding under credit and liquidity programs established the Federal Reserve Board. These include discount window lending (primary credit, secondary credit, and seasonal credit), term auction credit, the Primary Dealer Credit Facility, the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility, the Term Asset-Backed Securities Loan Facility, the Commercial Paper Funding Facility, and central bank liquidity swaps. Also re$ects the value of outstanding securities lent through the Term Securities Lending Facility.

Other Programs: Re$ects the Federal Reserve, FDIC, and Treasury’s commitments under the Asset Guarantee Program; Federal Reserve Board assistance to Maiden Lane companies and support to American International Group; Treasury support for Fannie Mae and Freddie Mac through the senior preferred stock purchase agreements, as well as the face value of Treasury’s total mortgage-backed securities (MBS) portfolio at the end of each month, from October 2008-March 2012.

Exposures via Treasury’s Temporary Guarantee Program for Money Market Funds were taken from “Guarantees and Contingent Payments in TARP and Related Programs: Congressional Oversight Panel

November Oversight Report,” Congressional Oversight Panel (November 2009), https://fraser.stlouisfed.org/title/5018.

Based on Figure 18.5, J. Nellie Liang, Margaret M. McConnell, and Phillip Swagel, “Evidence on Outcomes,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds., First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

PAGE 69 Data for 63 "nancial crises in advanced economies, 1857 to 2013, were taken from Carmen Reinhart and Kenneth Rogo#, “Recovery from Financial Crises: Evidence from 100 Episodes,” American Economic Review: Papers & Proceedings 104(5) (2014): 50–55, https://scholar.harvard.edu/"les/rogo#/"les/aer_104-5_50-55.pdf.

Based on Figure 18.3, J. Nellie Liang, Margaret M. McConnell, and Phillip Swagel, “Evidence on Outcomes,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds., First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

PAGE 70 Based on Table 2 in Baird Webel and Marc Labonte, “Costs of Government Interventions in Response to the Financial Crisis: A Retrospective,” Congressional Research Service (updated September 2018), https://fas.org/sgp/crs/misc/R43413.pdf.

All "gures except otherwise noted are reported on a cash basis and as of Aug. 1, 2018. GSE debt purchases, DIF losses and cumulative income, and TAGP are as of Dec. 31, 2017; Maiden Lane is as of Jan. 31, 2018; and GSEs are as of Q2 2018.

PAGE 72 Depository institutions include U.S.-chartered depository institutions, foreign banking o!ces in the U.S., and credit unions.

80

PAGE 5 Re-created with data underlying Figure 10, “The Distribution of Household Income, 2014,” Congressional Budget O!ce (2018), www.cbo.gov/publication/53597. See link for de"nitions of income and income groups.

PAGE 10 Based on Figure 3.1, U.S. home price and related data, Robert J. Shiller, Irrational Exuberance, 3rd ed. (Princeton, NJ: Princeton University Press, 2015), as updated by the author, www.econ.yale.edu/~shiller/data.htm.

PAGE 11 Based on Figure 1, Panel 1, Michael Ahn, Michael Batty, and Ralf Meisenzahl, “Household Debt-to-Income Ratios in the Enhanced Financial Accounts,” FEDS Notes (Washington, DC: Board of Governors of the Reserve System, January 11, 2018), https://doi.org/10.17016/2380-7172.2138.

PAGE 12 Based on Figure 4.1, Scott G. Alvarez, William Dudley, and J. Nellie Liang, “Nonbank Financial Institutions: New Vulnerabilities and Old Tools,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds., First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

PAGE 13 Based on Exhibit 1, Gary Gorton and Andrew Metrick, “Who Ran on Repo?” (2012), http://faculty.som.yale.edu/garygorton/documents/whorancompleteoctober4.pdf.

Banks’ portion includes net liabilities from federal funds agreements.

PAGE 28 Based on Figures 2.5 and 2.6, William English and Patricia Mosser, “The Use and E#ectiveness of Conventional Liquidity Tools Early in the Financial Crisis,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds. First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

PAGE 30 Based on Figure 3.7, Lorie Logan, William Nelson, and Patrick Parkinson, “The Fed’s Novel Lender of Last Resort Programs,” in Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, eds., First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis (New Haven: Yale University Press, 2020).

PAGE 31 Based on Chart 5, Adam Ashcraft, Allan Malz, and Zoltan Pozsar, “The Federal Reserve’s Term Asset-Backed Securities Loan Facility,” Federal Reserve Bank of New York Economic Policy Review 18(3) (November 2012): 29-66, https://www.newyorkfed.org/medialibrary/media/research/epr/2012/EPRvol18n3.pdf.

PAGE 33 Based on Panel A, Lawrence Schmidt, Allan Timmermann, and Russ Wermers, “Runs on Money Market Mutual Funds,” American Economic Review 106(9) (2016): 2625–57, www.aeaweb.org/articles?id=10.1257/aer.20140678.

PAGE 34 Based on Slide 4, “Reforming Wall Street, Protecting Main Street,” U.S. Treasury, July 2012, www.treasury.gov/connect/blog/Documents/20120719_DFA_FINAL5.pdf.

PAGE 35 Commercial banks include depository institutions. Bank holding companies include bank holding companies, savings and loan holding companies, "nancial holding companies, and their funding a!liates. Nonbanks include nonbank entities and their a!liates, as well as bank holding companies with nonbank assets of nonbank subsidiaries comprising more than half of their total assets.

PAGE 41 Based on U.S. Treasury data and AIG infographic and timeline, www.treasury.gov/initiatives/"nancial-stability/TARP-Programs/aig/Pages/default.aspx.