CHART SAMPLE

26

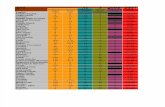

© Synovate 2010 1 Opinion of overall appearance of the tea Opinion of overall color of the tea Opinion of clarity of the tea Q21a. Which of these phrases best describes your opinion of the overall appearance of the drink made of the green tea we sent you to try? Q22. And which of these phrases best describes your opinion of the overall color of the drink? Q24a. Which of the following phrases best describes your opinion of the clarity of the green tea you just tried? A/B/C/D/E - Significantly higher than indicated group with 95% (upper case) and 90% (lower case) confidence level. 25% 26% 24% 24% 26% 24% 19% 25% 21% 22% 29% 28% 27% 38% 34% 34% 38% 27% 23% 25% 22% 27% 37% 33% 33% 33% 35% 31% 35% 32% Excellent Very good 60% 55% 55% 62% 59% T2B BC Appearance related measures – Unbranded 60% 55% 55% 62% 53% 60% 55% 55% 62% 55% Lipton (N=219) [A] Bigelow (N=219) [B] Stash (N=219) [C] Salada (N=219) [D] Green (N=236) [E] Comment b e

-

Upload

nitesh-mishra -

Category

Documents

-

view

131 -

download

1

Transcript of CHART SAMPLE

© Synovate 2010 1

Opinion of overall appearance of the tea

Opinion of overall color of the tea

Opinion of clarity of the tea

Q21a. Which of these phrases best describes your opinion of the overall appearance of the drink made of the green tea we sent you to try?Q22. And which of these phrases best describes your opinion of the overall color of the drink?Q24a. Which of the following phrases best describes your opinion of the clarity of the green tea you just tried?A/B/C/D/E - Significantly higher than indicated group with 95% (upper case) and 90% (lower case) confidence level.

25%26%

24%

24%26%

24%

19%

25%21%

22%

29%

28%27%

38%

34%34%

38%

27%

23%

25%

22%

27%

37%

33%

33%

33%

35%

31%35%

32%

Excellent Very good

60%55%55%62%59%

T2B

BC

Appearance related measures – Unbranded

60%55%55%62%53%

60%55%55%62%55%

Lipton (N=219) [A] Bigelow (N=219) [B] Stash (N=219) [C] Salada (N=219) [D] Green (N=236) [E]

Comment

b

e

© Synovate 2010 2Draft Report

Overall Flavor

Too Strong Too WeakJust Right

Egg Flavor

10%10%

7%

6%6%

4%

8%8%

5%

82%76%

75%

81%84%

83%

70%78%

70%

8%14%

18%

12%11%

13%

22%15%

25%

6%

5%

3%

9%7%

5%7%

8%9%

83%78%

87%75%

75%64%

80%

78%

74%

17%

14%

23%

13%10%

8%18%

17%27%

Lemon Flavor

Too Strong Too WeakJust Right

Too Strong Too WeakJust Right

_____________Q18. What is your opinion of the strength of overall flavor of the mayonnaise? Q22. How would you the rate the strength of the egg flavor in the mayonnaise? Q23. How would you rate the strength of lemon flavor in the mayonnaise? A/B/C/D/E/F - Significantly higher than indicated group with 95% (upper case) and 90% (lower case) confidence level.

d

d

aD

BC

A

A

c

C

c

c

B

b

B

AE

e

e

aE

n Hellmann's (A) (n=159) Best Foods (B) (n=102) n Kraft (C) (n=160)n Safeway (D) (n=154) Kroger (E) (n=155) Wal-Mart (F) (n=155)

Just Right: Strength of Flavor Characteristics

Hellmann's has an advantage over Best Foods and Kraft for strength of egg flavor.Best Foods is considered too weak in lemon flavor and lags Hellmann's and Kroger on optimal ratings.

© Synovate 2010 3

Report writer text Finding B (Arial, 28pt)

Q2a.Q2b.

Types Purchased Past 3 Months

5

1

2

5

4

5

5

9

6

17

18

17

3

13

23

23

25

28

31

33

34

37

38

43

44

54

4

3

Donuts

Cereal Bars

Snack Cakes

Cupcakes

Muffins

Snack Bars

Cakes (Full Size)

Brownies

Pastries/Specialty

Danish

Snack Pies

Pies (Full Size)

Some other type

None of the above

%West

(n=285)Midwest/Southeast

(n=321)Northeast

(n=307) % %

3

1

4

3

3

1

13

5

5

25

20

16

2

10

19

22

22

27

30

23

44

36

30

53

51

55

2

1

3

2

5

3

5

2

17

6

3

13

22

15

1

10

18

21

24

30

28

18

48

30

32

43

48

50

1

3

Purchase Most Often Purchase P3M

© Synovate 2010 4

Report writer text Finding C (Arial, 28pt)

**Very Small Base*Small BaseQ3.

Primary Eater

44%

50%

52%

62%

60%

63%

50%

50%

56%

45%

45%

61%

44%

46%

43%

31%

35%

34%

31%

24%

27%

29%

31%

34%

26%

40%

10%

7%

18%

3%

6%

7%

26%

24%

15%

24%

21%

13%

17%Donuts (n=167,175,143)

Cereal Bars (n=135,163,137)

Snack Cakes (n=132,170,122)

Snack Bars (n=105,140,136)

Muffins (n=112,116,85)

Cupcakes (n=116,96,92)

Brownies (n=97,96,80)

Pastries/Specialty (n=87,85,85)

Cakes (Full Size) (n=102,74,52)

Danish (n=77,71,67)

Snack Pies (n=70,70,59)

Pies (Full Size) (n=69,61,51)

Some other type (n=39*,33*,29**)

Northeast

45%

58%

52%

64%

49%

65%

46%

35%

55%

44%

45%

63%

49%

26%

38%

31%

27%

34%

27%

29%

31%

24%

33%

29%

21%

26%

29%

4%

17%

9%

17%

8%

25%

34%

21%

23%

27%

16%

25%

46%

56%

40%

67%

44%

67%

46%

47%

57%

46%

41%

57%

44%

39%

31%

37%

25%

36%

26%

20%

14%

26%

29%

24%

28%

24%

15%

13%

23%

9%

20%

7%

34%

39%

17%

25%

35%

15%

32%

Midwest/Southeast West

Myself Other Adult Child

© Synovate 2010 5

Report writer text Finding C (Arial, 28pt)

**Very Small Base*Small BaseQ3.

Primary Eater

44%

50%

52%

62%

60%

63%

50%

50%

56%

45%

45%

61%

44%

46%

43%

31%

35%

34%

31%

24%

27%

29%

31%

34%

26%

40%

10%

7%

18%

3%

6%

7%

26%

24%

15%

24%

21%

13%

17%Donuts (n=167,175,143)

Cereal Bars (n=135,163,137)

Snack Cakes (n=132,170,122)

Snack Bars (n=105,140,136)

Muffins (n=112,116,85)

Cupcakes (n=116,96,92)

Brownies (n=97,96,80)

Pastries/Specialty (n=87,85,85)

Cakes (Full Size) (n=102,74,52)

Danish (n=77,71,67)

Snack Pies (n=70,70,59)

Pies (Full Size) (n=69,61,51)

Some other type (n=39*,33*,29**)

Northeast

45%

58%

52%

64%

49%

65%

46%

35%

55%

44%

45%

63%

49%

26%

38%

31%

27%

34%

27%

29%

31%

24%

33%

29%

21%

26%

29%

4%

17%

9%

17%

8%

25%

34%

21%

23%

27%

16%

25%

46%

56%

40%

67%

44%

67%

46%

47%

57%

46%

41%

57%

44%

39%

31%

37%

25%

36%

26%

20%

14%

26%

29%

24%

28%

24%

15%

13%

23%

9%

20%

7%

34%

39%

17%

25%

35%

15%

32%

Midwest/Southeast West

Myself Other Adult Child

© Synovate 2010 6

Report writer text Finding C (Arial, 28pt)

**Very Small Base*Small BaseQ3.

Primary Eater

44%

50%

52%

62%

60%

63%

50%

50%

56%

45%

45%

61%

44%

46%

43%

31%

35%

34%

31%

24%

27%

29%

31%

34%

26%

40%

10%

7%

18%

3%

6%

7%

26%

24%

15%

24%

21%

13%

17%Donuts (n=167,175,143)

Cereal Bars (n=135,163,137)

Snack Cakes (n=132,170,122)

Snack Bars (n=105,140,136)

Muffins (n=112,116,85)

Cupcakes (n=116,96,92)

Brownies (n=97,96,80)

Pastries/Specialty (n=87,85,85)

Cakes (Full Size) (n=102,74,52)

Danish (n=77,71,67)

Snack Pies (n=70,70,59)

Pies (Full Size) (n=69,61,51)

Some other type (n=39*,33*,29**)

Northeast

45%

58%

52%

64%

49%

65%

46%

35%

55%

44%

45%

63%

49%

26%

38%

31%

27%

34%

27%

29%

31%

24%

33%

29%

21%

26%

29%

4%

17%

9%

17%

8%

25%

34%

21%

23%

27%

16%

25%

46%

56%

40%

67%

44%

67%

46%

47%

57%

46%

41%

57%

44%

39%

31%

37%

25%

36%

26%

20%

14%

26%

29%

24%

28%

24%

15%

13%

23%

9%

20%

7%

34%

39%

17%

25%

35%

15%

32%

Midwest/Southeast West

Myself Other Adult Child

© Synovate 2010 7

54%

1% 4%10%

7%

1%22%

* Small BaseQ.7: How often do you experience the following?

Frequency Experience Condition – Among Total Users

Total Poison Ivy Users

(135)

Mean: 3.0

Once a week or more often

Every 2-3 weeks

Once a month

Every 2-3 months

Every 4-6 months

Once or twice a year

Less than once a year

50%

3% 6%8%

11%

22%

Total Poison Oak Users

(36)*

3.7

25%

9%

12%

22%

11%

16%

4%

Total Temporary RashOr Itch Caused By Insect Bites,

Allergic Reaction, Etc. Users(358)

11.6

8%

47%

9%

16%

8%

10%

3%

Total Eczema Users(79)

Mean: 28.7

5%

57%9%

10%

4%

12%

4%

Total Psoriasis Or SomeOther Chronic Condition Users

(105)

34.0

© Synovate 2010 8

54%

1% 4%10%

7%

1%22%

* Small BaseQ.7: How often do you experience the following?

Frequency Experience Condition – Among Total Users

Total Poison Ivy Users

(135)

Mean: 3.0

Once a week or more often

Every 2-3 weeks

Once a month

Every 2-3 months

Every 4-6 months

Once or twice a year

Less than once a year

50%

3% 6%8%

11%

22%

Total Poison Oak Users

(36)*

3.7

25%

9%

12%

22%

11%

16%

4%

Total Temporary RashOr Itch Caused By Insect Bites,

Allergic Reaction, Etc. Users(358)

11.6

8%

47%

9%

16%

8%

10%

3%

Total Eczema Users(79)

Mean: 28.7

5%

57%9%

10%

4%

12%

4%

Total Psoriasis Or SomeOther Chronic Condition Users

(105)

34.0

22

26

29

36

1

5

10

11

54

56

43

46

22

13

18

7

17

19

18

20

2

3

4

3

44

54

52

55

37

24

26

22

21

29

19

15

3

4

4

42

36

45

53

34

30

32

32

11

10

10

15

1

1

44

56

55

56

44

35

34

29

21

24

23

27

4

5

2

3

32

47

52

47

43

24

23

23

13

13

13

10

4

3

5

1

43

67

60

69

40

17

23

20

Perception of HPV Vaccination (1/2)

Connection creates value 9

Q23: With regards to the vaccine against Human Papillomavirus/cervical cancer, to what extent would you say that you agree with each of the following statements ?

Totally disagree Disagree somewhatAgree somewhat Totally agree

Spain YMNorway YM(623)

Denmark YM Portugal YM(76) (136)(109) (159)

YOUNG MEN

…is as important as

other recommended

vaccination

…is a vaccine I trust

…is supported by my doctor

…is a safe vaccine

TOTAL COUNTRIES

ST Agree

BASE : Aware of HPV vaccine /Cervical cancer vaccine

France YM(139)

81 %

78 %

78 %

77 %

76 %

70 %

61 %

53 %

83 %

84 %

83 %

89 %

75 %

71 %

75 %

70 %

88 %

91 %

89 %

85 %

76 %

68 %

78 %

85%

…is as important as other recommended vaccination

…is a vaccine I trust

…is supported by my doctor

…is a safe vaccine

…has demonstrated its efficacy

…is for girls only

…can also be administered to boys to prevent diseases in boys

1.0 2.0 3.0 4.0

Total countries NOR (GP) DEN (All) SP (Ped)POR (Ped) FRC

Perception of HPV Vaccination

Connection creates value 10

Q23: With regards to the vaccine against Human Papillomavirus/cervical cancer, to what extent would you say that you agree with each of the following statements ?

YOUNG MEN

BASE : Aware of HPV vaccine /Cervical cancer vaccine (623) (76) (109) (136) (159) (139)

After “burden” both Mothers and Young Men seem quite favorable towards HPV vaccination in boys/ym

Connection creates value 11

Reactions to HPV vaccination of BOYS

BASE : All

SpainNorway Denmark PortugalTOTAL COUNTRIES

151

50 3421 25 73

101

40 49 2 33 66 72

37 54

89% 84% 99% 91% 97%(86) (177)(135) (143)(743)

Mothers BOYS PC

Mothers BOYS CC

YOUNG MEN

122

51 34

(181) (176)(262) (141)(961)

31 26 71

82

41 49 2 35 64 71

41 51

90% 86 % 98 % 92 % 96 %

(152) (226)(120) (206)(910)

132 47 38152 51 32 191 51 29 10 54 36 5

250 42

83% 79% 90% 93% 85%

I am very unfavorable I am somewhat unfavorable I am somewhat favorable

In spite of the fact that the Young men seem to feel little affected personally, their attitude towards HPV vaccination in boys/ym is favorable

ST favorable

France

213 52 24

76 %

(202)

(201)

177 52 24

76 %

(200)

274 55 14

69%

2.2

3.6

2.5

3.7

3.9

4.2

3.8

4.9

2.0

3.5

2.2

3.9

3.7

4.0

3.6

5.8

2.3

4.0

2.3

3.6

3.9

4.5

4.1

4.7

69

67

67

53

49

42

40

23

64

73

73

56

64

48

38

26

Drivers for vaccination

Connection creates value 12

Q37a: What could be the reasons that you want your son to get vaccinated against the Human Papillomavirus ?

Q37b: Could you please rank the reasons you selected in order of their importance for you ?

Mothers BOYS PC

Drivers 1/2Spain Mothers Norway Mothers

(66) (153)Denmark Mothers

(131)Portugal Mothers

(142)TOTAL COUNTRIES

(652)

BASE Driver : Certainly or probably will get vaccinated or is already vaccinated BASE Rank : item quoted in Q37a

France Mothers(160)

I welcome any protection against cancers for my son

myself

Boys should have the same access to protection

as girls

I want to avoid any risk of the virus for my son

I want to avoid any risk of transmission of the virus

to future or current partners

I want to avoid genital warts for my son

Getting my son vaccinated will help to eradicate the

Human PapillomavirusI think that the vaccination

offers the best protection against Human Papillomavirus

I trust the previous success of girl’s vaccination

79

73

66

59

50

52

37

33

65

59

58

44

44

36

37

18

68

65

70

58

36

43

48

21

71

68

68

51

59

35

37

21

PC

PC

CC

RANK2.3

3.4

3.3

3.8

4.5

3.7

4.2

4.6

2.4

3.8

2.4

3.3

3.9

4.1

3.5

4.8

2.0

3.6

2.4

4.1

3.8

4.8

4.2

4.8

CC

CC

PC CC

In a typical month, how many new and restart prescriptions or orders do you write for each of the following agents?

140.0

140.0

140.0

140.0

140.0

Total(n=630)

Mean Among Total PhysiciansA/B/C indicates statistically significant difference @ 95% confidence level between countriesD/E indicates statistically significant difference @ 95% confidence level between specialties

US (A)

(n=321)France (B)

(n=155)Germany (C)

(n=154)PCP (D)

(n=280)Specialists (E)

(n=350)

Stub 1

Stub 1

Stub 1

Stub 1

Stub 1

QD

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

140.0

Top-2 Box Summary: Please use the following scale to indicate how much you agree or disagree with the following statements

50%

20%

20%

20%

20%

100%

40%

40%

40%

40%

Total(n=630)

% Among Total PhysiciansA/B/C indicates statistically significant difference @ 95% confidence level between countriesD/E indicates statistically significant difference @ 95% confidence level between specialties

US (A)

(n=321)France (B)

(n=155)Germany (C)

(n=154)PCP (D)

(n=280)Specialists (E)

(n=350)

Stub 1

Stub 1

Stub 1

Stub 1

Stub 1

Q5

50%

20%

20%

20%

20%

100%

40%

40%

40%

40%

50%

20%

20%

20%

20%

100%

40%

40%

40%

40%

50%

20%

20%

20%

20%

100%

40%

40%

40%

40%

50%

20%

20%

20%

20%

100%

40%

40%

40%

40%

50%

20%

20%

20%

20%

100%

40%

40%

40%

40%

Somewhat AgreeAgree Completely

Thinking about the next 100 patients you will see for each of the patient types listed below, how will you treat and/or

99%

37%

14%

20%

17%

20%

14%

99%

37%

17%

5% RRR (A)

(n=630)

Stub 1

Stub 1

Stub 1

Stub 1

Stub 1

Q6-6b

12% RRR (B)

(n=630)20% RRR (C)

(n=630)30% RRR (D)

(n=630)

99%

37%

14%

20%

17%

20%

14%

99%

37%

17%

99%

37%

14%

20%

17%

20%

14%

99%

37%

17%

99%

37%

14%

20%

17%

20%

14%

99%

37%

17%

0.9% Bleeding0.3% Bleeding

Mean % Among Physicians AskedLetter indicates statistically significant difference @ 95% confidence level between sub groups

Segment segments segz size pie

Segment15%

Segment25%

Segment25%

Segment33%

Segment2%

Breakdown of subgroup By Segment (n=366)

1. Size of Segment

Segment26%

Segment39%

Segment21%

Segment12%

Segment2%

Breakdown of subgroup By Segment (n=182)

Provides effective asthma control

Is associated with enhanced compliance

Effective forallergic rhinitis

Exhibits anti-inflammatory properties Prevents lung

remodeling

Reduces reliance on PRN short-acting beta-

agonists

Provides nocturnal control of asthma

Effect is evident on the 1st day of treatment

Provides real world effectiveness

Works in a high percentage of asthma

patients Is appropriate switch therapy for patients uncontrolled on an

inhaled corticosteroid

Has a favorable side effect profile

Is easy to use

Is effective for asthma patients with allergic

triggers Has a convenientdosing regimen

Is cost effective forthe patient

Has favorable managed care status

Is effective in blocking leukotrienes

Is not associated with systemic side effects

Prevents disease progression

Is an appropriate first-line monotherapy

maintenance medication for asthma

Derived vs. Stated Importance Map:

Sta

ted

Impo

rtanc

eLo

wH

igh

Derived Importance HighLow

Key DriversCost of Entry

Underlying DriversLeastInfluential

% Among Total Physicians - Adult Market N=284/288Importance: % of Physicians Who Find Attribute Most Influential When Prescribing for Asthma (Bradley-Terry Paired Comparison Analysis)Imagery: % of Physicians Selecting Brand as Most Strongly Associated with Statement (Maximum Benefit Differentiation) Letters denote statistically significant differences at the 95% confidence level between brands.Number denote statistically significant differences at the 95% confidence level between waves

Provides Effective Asthma Control

Importance Singulair® [A] Advair [B]

89%

80%

79%

76%

71%

70%

69%

82%

74%

75%

56%

74%

62%

55%

Alvesco [D]

Works In A High Percentage Of Asthma

Patients

Provides Real World Effectiveness

ExhibitsAnti-inflammatory

Properties

Reduces Reliance On PRN Short-acting

Beta-agonists

Is Appropriate Switch Therapy For Patients

Uncontrolled On An Inhaled Corticosteroid

Is Not Associated With Systemic Side Effects

8%

8%

16%

15%

8%

23%

86%

4%

6%

19%

8%

6%

25%

79%

90%

87%

81%

51%

88%

68%

5%

91%

87%

78%

56%

90%

70%

5%

1%

2%

2%

5%

1%

7%

3%

2%

2%

1%

10%

1%

5%

5%

Flovent [C]

1%

4%

2%

29%

3%

2%

7%

3%

5%

3%

26%

3%

1%

12%

CD ACD

D ACD AD

CD ACD

CD ACD

CD ACD C

BCD D

ACD

Importance / Imagery Charts

Q3/4

7/0512/05

ACD

D ACD8

CD ACD

ACD 8AD 8

D ACD

CD ACD C

BCD 8BD

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Has a favorable side effect profile Prevents lung remodeling Is an appropriate first-linemonotherapy maintenance

medication for asthma

Exhibits anti-inflammatoryproperties

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Importance Singulair Advair Flovent Alvesco Upper parity Lower Parity

Competitive Performance Diagnostic Charts

Extremely Important

Extremely Unimportant

83%

Competitor Advantage

Parity Zone

Singulair® Advantage

Singulair® Best Brand %

Q3,4

Among Total Adult (PCP/Allr/PUD)Physicians.

12/057% 20% 8%

Competitive Performance Diagnostic Charts

4% 6% 5% 6% 6% 9%

Q5, 6

Among Total PED (GP/FPs/Allr/PED)Physicians.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Provideseffective asthma

control

Preventsdisease

progression

Exhibits anti-inflammatory

properties

Reducesreliance on PRN

short-actingbeta-agonists

Prevents lungremodeling

Providesnocturnalcontrol ofasthma

Is anappropriate first-

linemonotherapymaintenance

medication forasthma

Indicated forpatients asyoung as 12months old

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Importance Singulair Advair Flovent Alvesco Pulmicort Respules Upper parity Lower Parity

Extremely Important

Extremely Unimportant

Competitor Advantage

Parity Zone

Singulair® Advantage

Singulair® Best Brand % 28% 48%

12/05

PwC

Heat map (Q3 FY11)

21September 2011

Scoring methodThe chart above identifies systemic and isolated strengths and weaknesses in the survey results. The survey items used a five-point scale (Strongly Disagree, Disagree, Neutral, and Agree, and Strongly Agree). The last two response options are combined to form one "Agree Score" which is the one reported in the tables and charts. The higher the reported number, the more favorable the result. Unfavorable results are color-coded:

22

48

42

34d

88d

47

83D

73

34

2

1

4

19

4

1

1d

9

1

1

FY’10 (B)

FY’11 (C)

Martini & Rossi Asti (M&R) and Korbel are still the category leaders in Brand awareness, but M&R has lost awareness vs. two years ago. Korbel has also declined in brand awareness over the past 2 years but not significantly. This more gradual decline may be tied to Korbel’s large ad spend.

Brand Awareness Profiles

Q.1U/2U When you think of champagne or sparkling wine, what one brand first comes to mind? What other brands come to mind next? Q.1A You may have mentioned some of these already, but please use the list below to indicate which of these brands of champagne or sparkling wine you are aware of.

#Less than 0.5%NOTE: Competitive brands ranked on Est. Price Point

FY’09 (A)

Add chart to far right for FY12. Data should stay in same order as stubs shown on slide on Left. Reduce chart widths as

needed.Data file: 104712compaa01 (hold off on Martini Net for now)

Unaided First Brand Mentions: Table 1-B6Total Unaided Brand Mentions: Table 2-B6

Total Brand Awareness: Table 5-B6

Please update base sizes for FY12

44

53B

27

82

15AB

19AB

45

74

69

32

2

2

2

23

1

4

1

1

6

1a

FY’12 (D)

Martini/Martini & Rossi Asti

Ballatore

Yellow Tail Sparkling Wine

Freixenet

Korbel

Piper Sonoma

Mumm Napa

Chandon (Domaine Chandon)

Moet & Chandon White Star/Brut

Moet & Chandon Nectar

Veuve Clicquot Yellow Label

53d

48

38D

83

42

85D

70

36

3

2

4

17

2

1

1

1

1

5

48

49b

35d

86

22ABd

27ABd

43

80

68

33

1

2

5d

19

6a

1

7

Base: P12M C/SW Drinkers FY’09(204); FY’10(262); FY11(203); FY12(201) Unaided 1st Brand Mentions Unaided Brand Mentions Total Brand Awareness

23

Saw/Heard/Read Advertising – Top 10 Sources ListConsumers recollection of where they saw M&R advertising is unchanged from the past two years.

Q.3A In which of these places have you seen, heard or read anything about champagne or sparkling wine recently? Among P12M C&SW Drinkers aware of Advertising

In A Store/In-Store Display

Magazines

TV

In A Bar/Club/Lounge

In A Restaurant

Talking To Someone Else

RadioPosters, Billboards Or Other

Outdoor AdsDuty Free Shop

NewspapersThe Internet Or Email Or Text

MessageSome Other Place

60%

45%B

40%D

33%

27%

29%

13%

15%

15%

13%

13%

16%

60%

32%

33%

31%

25%

30%

17%

20%

15%

13%d

10%

11%

M/M&R FY09 (A)

M/M&R FY10 (B)

M/M&R FY11 (C)

M/M&R FY12 (D)

Base: Aware of Advertising for Brand (119) (126) (89) (90)

60%

40%

34%

34%

24%

22%

20%d

19%

15%

15%d

13%

12%

Add chart to far right for FY12. Data should stay in same order as stubs shown on slide on Left. Add base size for FY12.

Reduce chart widths as needed.Data file: 104712compaa01

Table 7-B6

66%

36%

26%

27%

26%

29%

11%

12%

17%

7%

14%

9%

24

Freixenet2009 2010 2011 2012

A B C D204 262 203 201

4 3 5 2

62 66 65 73

20 16 19 126 8 7 5

5 6 2 51 2 11 1

Chandon (Domaine Chandon)2009 2010 2011 2012

A B C D204 262 203 201

Korbel2009 2010 2011 2012

A B C DBase: Total 204 262 203 201

Martini/Martini & Rossi Asti2009 2010 2011 2012

A B C DBase: Total 204 262 203 201

7 3 3 6

5853 57 55

2327 22 25

9 8 10 63 6 6 61 2 11

0%

20%

40%

60%

80%

100%

6 6 8 58 13

19 23

37 3633 29

18 1413 14

22 23 18 243 4 4 24 5 5 2

Lover

Friend

Acquaintance

Familiar

Aware

Stranger

Rejecter

0%

20%

40%

60%

80%

100%

10 4 8 5

1712

14 18

3636 31 28

1918 16 22

1426 24 20

2 2 4 42 1 2 2Lover

Friend

Acquaintance

Familiar

Aware

Stranger

Rejecter

CommitmentM&R has declined in acquaintances adding to strangers over the past two years. At the same time Korbel has had a decline in Awares with an increase in strangers.

#- Less than .5%Q.27 Consideration, Q.4, Consumption

Add Chart for FY12 to each section (to the right of FY2012).

Data file: 104712compgmaa012009 – Table: 1-B309

2010 – Table: 1-B30122011 – Table: 1-B30152012 – Table: 1-B3018

25

55%

48%

50%

58%

42%

52%

46%

40%

34%

30%

30%

38%

28%

M&R Brand ImageryOver the course of the last two years, M&R has made significant headway on the majority of brand imagery attributes including affinity (brand for me), quality and value.

Base: Aware of Brand and Randomly Selected: FY 2009 (104), FY 2010 (118), FY 2011 (99), FY 2012 (93)Q.29 Using a scale from 5 to 1 where 5 means “Agree Completely” and 1 means “Disagree Completely”, please tell us how much you agree or disagree that each statement

describes the brands shown.

Martini/Martini & Rossi Asti FY09

(A)

Martini/Martini & Rossi Asti FY10

(B)

Is For Really Great Times With Friends

Is A Good Value For The Money

Is Good To Give As A Gift

Is Easy To Drink

Is Great For Home Entertaining

Not Only For Special Occasions

Is A Brand I'd Take To A Party

Smooth Tasting

Is A Brand For MeAn Informal Brand Of Champagne/Sparkling

WineHas A Sweeter Taste Than Other Brands

Is A High Quality Brand

Is For Fun Loving People

Is A Brand That Impresses Others

Truly Different From Other Brands

Shows Your Sense Of Style

Captures The Joy Of Living

Is Getting More Popular

Is For People Who Are Knowledgeable About Sparkling Wine And Champagne

Is An Imported Italian Brand

Top 2 Box (Agree Completely/Somewhat) Martini/Martini & Rossi Asti FY11

(C)

64%

60%a

64%A

65%

58%A

55%

59%AD

43%

51%A

44%A

34%

42%

42%A

68%AB

65%

65%A

63%a

62%AB

60%

60%AB

60%A

59%

58%d

55%Abd

54%A

51%AB

47%A

46%Ab

44%

41%AB

40%AB

39%a

37%AB

Add chart to far right for FY12. Add base size for FY12. Reduce chart widths as

needed. Order statements by M&RFY11 – use same statement order throughout rest

of imagery slides.Data file: 104712compaa01

Table: 213-B6

Martini/Martini & Rossi Asti FY12

(D)

67%AB

66%

66%A

69%A

72%AB

66%

69%AB

65%A

65%a

45%

42%

62%Ab

53%AB

56%Ab

49%AB

48%

48%AB

48%AB

39%

34%AB

26

= Rating is significantly higher than Martini & Rossi Asti

= Rating is significantly lower than Martini & Rossi Asti

M&R Brand Imagery

Note: Ballatore & Mumm Napa were not asked at Imagery/PersonalityQ.29 Using a scale from 5 to 1 where 5 means “Agree Completely” and 1 means “Disagree Completely”, please tell us how

much you agree or disagree that each statement describes the brands shown.

M&R is perceived to have a sweeter taste than other brands and is among the highest rated on quality and a brand that impresses others.

Top 2 Box (Agree Completely/Somewhat) Martini/ Martini & Rossi Asti

Yellow Tail Sparkling

Wine Freixenet KorbelPiper

Sonoma

Chandon (Domaine Chandon)

Moet & Chandon

White Star/Brut

Moet & Chandon

NectarVeuve Clicquot

Yellow Label$14.99 $8.99 $11.99 $13.99 $14.99 $19.99 $34.99 $44.99 $44.99

Base: Aware of Brand And Randomly Selected 93 58 41 92 18 53 76 73 33Is For Really Great Times With Friends 67c 66c 49 68C 50 62 66c 70C 70cIs A Good Value For The Money 66fGH 67fGH 54 70cFGH 50 49 50 45 55Is Good To Give As A Gift 66 67 66 65 67 70 79aD 79AD 82aDIs Easy To Drink 69 64 61 72 56 64 64 66 79ceIs Great For Home Entertaining 72C 72c 54 72C 61 66 71c 70c 82CfNot Only For Special Occasions 66e 66 56 61 44 55 57 58 58Is A Brand I'd Take To A Party 69E 64e 56 67E 39 58 75CEf 68E 82bCdEFSmooth Tasting 65f 59 56 66F 56 49 63 68F 79BCeFgIs A Brand For Me 65Cf 53 41 61C 61 49 64Cf 63C 73bCF

An Informal Brand Of Champagne/Sparkling Wine 45 72ACDEFGHI 39 48gh 44 38 34 34 33

Has A Sweeter Taste Than Other Brands 42 45 29 34 33 30 43 44 39Is A High Quality Brand 62Bd 36 59B 49 44 57B 76ABcDEF 82ABCDEF 85ABCDEFIs For Fun Loving People 53c 71ACdEFg 37 58C 39 49 57C 59C 64CeIs A Brand That Impresses Others 56BF 34 46 45 56 38 71ABCDF 77ABCDeF 67BcDFTruly Different From Other Brands 49cd 36 34 37 50 47 54BCD 55BCD 55bcdShows Your Sense Of Style 48 38 51 51 56 45 66ABdF 66ABdF 55Captures The Joy Of Living 48 50 39 47 39 49 57c 56c 45Is Getting More Popular 48 62aCDF 37 46 44 38 61CdF 51 58cfIs For People Who Are Knowledgeable About Sparkling Wine And Champagne 39 36 37 32 44 51D 66ABCDf 59ABCD 67ABCD

Is An Imported Italian Brand 34BD 17 29 16 28 25 25 26 27

Replace with FY12 data only. Order statements same as previous slide. The Pert Group will add

the significance arrows later.Data file: 104712compaa01

Table: 20-B1018