Chapter V PERFORMANCE OF DEPOSITORIES AND DEPOSITORY...

29

128 Chapter V PERFORMANCE OF DEPOSITORIES AND DEPOSITORY PARTICIPANTS Introduction Ratio analysis is the universally used technique for the analysis of financial performance of an organization. A ratio is a statistical yardstick that provides a measure of relationship between the variables or figures. The ratio analysis helps the management to analyze the past performance of the firm and to make further projections. In this study ratio analysis is done to understand the performance of depositories and DPs. Through this, the weaknesses and strengths are identified and appropriate suggestions are given. Financial Performance of Depositories in India Depository is an institution or a kind of organization which holds securities with it, in which trading is done among shares, debentures, mutual funds, derivatives, F&O and commodities. The intermediaries perform their actions in variety of securities at Depository on the behalf of their clients. These intermediaries are known as Depositories Participants. Fundamentally, there are two sorts of depositories in India. One is the National Securities Depository Limited (NSDL) and the other is the Central Depository Service (India) Limited (CDSL). The investor who is known as beneficial owner (BO) has to open a demat account through any DP for dematerialization of his holdings and transferring securities. Depositories were setup with the objective of providing convenient, dependable and secure depository services at affordable cost to all market participants. All leading stock exchanges like the National Stock Exchange, Bombay Stock Exchange, Calcutta Stock Exchange, Delhi Stock Exchange, The Stock Exchange of Ahmadabad, etc have established connectivity with CDSL or NSDL. This Chapter focuses on financial performance of both the depositories i.e. CDSL and NSDL of India. This study is purely based on secondary data and the period of the study is April – 2007 to March – 2012 i.e. five consecutive financial years.

Transcript of Chapter V PERFORMANCE OF DEPOSITORIES AND DEPOSITORY...

128

Chapter V

PERFORMANCE OF DEPOSITORIES AND DEPOSITORY

PARTICIPANTS

Introduction

Ratio analysis is the universally used technique for the analysis of

financial performance of an organization. A ratio is a statistical yardstick that

provides a measure of relationship between the variables or figures. The ratio

analysis helps the management to analyze the past performance of the firm and to

make further projections. In this study ratio analysis is done to understand the

performance of depositories and DPs. Through this, the weaknesses and strengths

are identified and appropriate suggestions are given.

Financial Performance of Depositories in India

Depository is an institution or a kind of organization which holds

securities with it, in which trading is done among shares, debentures, mutual

funds, derivatives, F&O and commodities. The intermediaries perform their

actions in variety of securities at Depository on the behalf of their clients. These

intermediaries are known as Depositories Participants. Fundamentally, there are

two sorts of depositories in India. One is the National Securities Depository

Limited (NSDL) and the other is the Central Depository Service (India) Limited

(CDSL). The investor who is known as beneficial owner (BO) has to open a

demat account through any DP for dematerialization of his holdings and

transferring securities. Depositories were setup with the objective of providing

convenient, dependable and secure depository services at affordable cost to all

market participants. All leading stock exchanges like the National Stock

Exchange, Bombay Stock Exchange, Calcutta Stock Exchange, Delhi Stock

Exchange, The Stock Exchange of Ahmadabad, etc have established connectivity

with CDSL or NSDL. This Chapter focuses on financial performance of both the

depositories i.e. CDSL and NSDL of India. This study is purely based on

secondary data and the period of the study is April – 2007 to March – 2012 i.e.

five consecutive financial years.

129

National Securities Depository Limited (NSDL)

It is an organization promoted by lOBI, UTI and National Stock Exchange

of India Ltd. The aim is to provide facilities for holding and handling securities in

electronic form. Subsequently; SBI (acquired a 4.76 per cent in NSDL). HDFC

bank, Deusche bank, Dena Bank, Canara Bank, Global Trust Bank, Standard

Chartered bank, Citibank NA and HSBC have acquired stake in NSDL. It

commenced its operations in November 1996. Its headquarter is situated at

Mumbai. It is holding and handling securities in electronic form. It facilitates

faster settlement cycles. It provides services related to transactions in securities. It

interfaces with the investors through its agents called depository participant

(DPs). As a depository, NSDL (i) acts as a custodian as well as legally transfer

beneficial ownership, (ii) reduces settlement risk by minimizing the paper work

involved in trading, and settling and transferring securities. NSDL offers the

following benefits: (a) dematerialization, (b) rematerialization, (c) electronic

settlement trades in stock exchanges connected to NSDL, (d) pledging/

hypothecation of dematerialized securities against bank loan, (e) electronic credit

of securities, (f) receipt of non-cash corporate benefits such as bonus in electronic

form, (g) other services viz., holding debt instruments in the same account,

availing stock lending/ borrowing facility etc.

Central Depository Services (India) Limited (CDSL)

Bombay Stock Exchange Limited (BSE) promoted CDSL jointly with

leading banks such as State Bank of India, Bank of India, Bank of Baroda, HDFC

Bank, Standard Chartered Bank, and Union Bank of India and Centurion Bank

CDSL was set up with the objective of providing convenient, dependable and

secure depository services at affordable cost to all market participants. CDSL

received the certificate of commencement of business from SEBI in February

1999. All leading stock exchanges like the National Stock Exchange, Calcutta

Stock Exchange, Delhi Stock Exchange, The Stock Exchange, Ahmadabad, etc

have established connectivity with CDSL. As at the end of Dec 2005, over 5000

issuers have admitted their securities (equities, bonds, debentures, and

commercial papers), units of mutual funds, certificate of deposits etc. into the

CDSL system. CDSL has over 296 DPs spread around 119 cities/towns across the

country, offering convenience for an investor to select a DP based on his location.

Table 5.1 Investor and DP Services

NSDL

Investor Accounts

DP Services Centers

Demat Custody Value

DPs

Companies

Source: www.nsdl.com, www.cdsl.com

Table 5.1 indicates

Custody Value and number of DPs and DP companies

Securities Depository

Limited (CDSL) as on

Table 5.2 Equity Shares in NSDL and CDSL traded in NSE and BSE

Depository

NSDL

CDSL Source: www.nsdl.com,www.cdsl.com

Table 5.2 indicates the both NSDL and CDSL

7,145and1, 51,810 respectively. The

companies are 1,184,586 and 97, 39,080 respectively.

Fig

0

20

40

60

80

100

120

Quantity (in Millions)

130

CDSL system. CDSL has over 296 DPs spread around 119 cities/towns across the

country, offering convenience for an investor to select a DP based on his location.

Investor and DP Services Centers of NSDL and CDSL as on

31-3-2013

NSDL CDSL

s 1,26,88,865 Investor Account

DP Services Centers 14,641 DP Location

Demat Custody Value 76,79,027 Demat Custody Value

567 DPs

10,843 Companies

, www.cdsl.com

5.1 indicates Investor accounts, DP Services Centers and Demat

Custody Value and number of DPs and DP companies of both

itory Limited (NSDL) and Central Depository Service (India)

as on 31st

March, 2013.

Equity Shares in NSDL and CDSL traded in NSE and BSE

Quantity (in

Millions)

Value ( in Millions)

7,145 1,184,586

151,810 9,7www.nsdl.com,www.cdsl.com

Table 5.2 indicates the both NSDL and CDSL have equity

51,810 respectively. The Value of the equity quantity held by both the

1,184,586 and 97, 39,080 respectively.

Fig 5.1 Equity Shares in NSDL and CDSL

Quantity (in Millions) Value ( in Millions)

CDSL system. CDSL has over 296 DPs spread around 119 cities/towns across the

country, offering convenience for an investor to select a DP based on his location.

nters of NSDL and CDSL as on

83,27,482

12,864

97,39.080

579

12,801

Investor accounts, DP Services Centers and Demat

the National

and Central Depository Service (India)

Equity Shares in NSDL and CDSL traded in NSE and BSE

Value ( in Millions)

1,184,586

9,739,080

have equity quantity of

held by both the

NSDL

CDSL

131

Financial Performance of Depositories

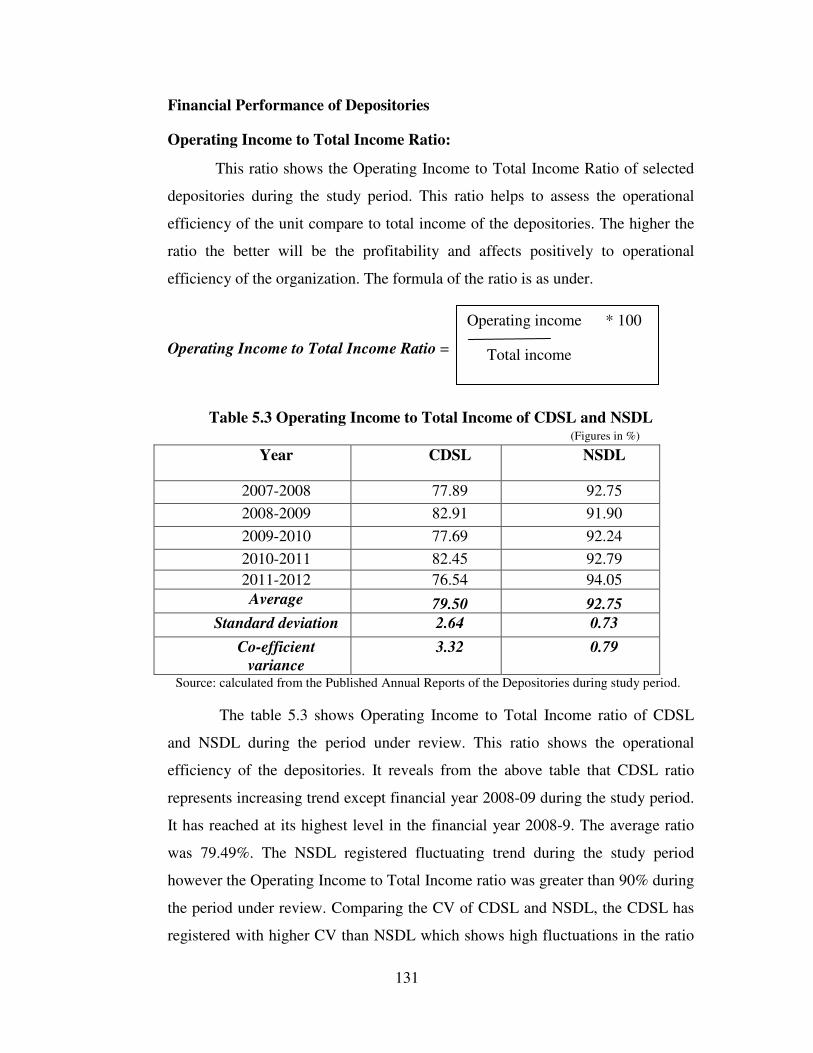

Operating Income to Total Income Ratio:

This ratio shows the Operating Income to Total Income Ratio of selected

depositories during the study period. This ratio helps to assess the operational

efficiency of the unit compare to total income of the depositories. The higher the

ratio the better will be the profitability and affects positively to operational

efficiency of the organization. The formula of the ratio is as under.

Operating Income to Total Income Ratio =

Table 5.3 Operating Income to Total Income of CDSL and NSDL (Figures in %)

Year CDSL NSDL

2007-2008 77.89 92.75

2008-2009 82.91 91.90

2009-2010 77.69 92.24

2010-2011 82.45 92.79

2011-2012 76.54 94.05

Average 79.50 92.75

Standard deviation 2.64 0.73

Co-efficient

variance

3.32 0.79

Source: calculated from the Published Annual Reports of the Depositories during study period.

The table 5.3 shows Operating Income to Total Income ratio of CDSL

and NSDL during the period under review. This ratio shows the operational

efficiency of the depositories. It reveals from the above table that CDSL ratio

represents increasing trend except financial year 2008-09 during the study period.

It has reached at its highest level in the financial year 2008-9. The average ratio

was 79.49%. The NSDL registered fluctuating trend during the study period

however the Operating Income to Total Income ratio was greater than 90% during

the period under review. Comparing the CV of CDSL and NSDL, the CDSL has

registered with higher CV than NSDL which shows high fluctuations in the ratio

Operating income * 100

Total income

whereas NSDL has low ratio which affects positively to its stability.

that NSDL is performing

TI is high and also CV is low.

and enhance its operating efficiency so that it can achieve maximum Operating

Income to Total Income

Fig: 5.2 Operating Income to Total Income

H0: There is no significance difference between CDSL and NSDL with regard to

operating Income to Total Income Ratio.

H1: There is significance difference between CDSL and NSDL with regard to

operating Income to Total Income Ratio

Table 5.3.1 Operating Income to Total Income (One Way ANOVA)

Sum of

Squares

Between

Groups

Within

Groups

Total

438.906

37.634

476.541

Source: SPSS and * significant at 0.01 level of significance

0

2040

6080

100

132

whereas NSDL has low ratio which affects positively to its stability.

that NSDL is performing well when compared with CDSL as mean ratio

high and also CV is low. It is suggested to CDSL to reduce its business risk

operating efficiency so that it can achieve maximum Operating

Income ratio.

Operating Income to Total Income of CDSL and N

: There is no significance difference between CDSL and NSDL with regard to

operating Income to Total Income Ratio.

There is significance difference between CDSL and NSDL with regard to

operating Income to Total Income Ratio.

Operating Income to Total Income (One Way ANOVA)

Sum of

Squares

Df Mean

Square

F-Cal Sig. F-table

@0.01

L.O.S

438.906

37.634

476.541

1

8

9

438.906

4.704

93.299 .000* 11.26

Source: SPSS and * significant at 0.01 level of significance.

Operating Income from Total Income

whereas NSDL has low ratio which affects positively to its stability. It is found

mean ratio of OI to

It is suggested to CDSL to reduce its business risk

operating efficiency so that it can achieve maximum Operating

SL and NSDL

: There is no significance difference between CDSL and NSDL with regard to

There is significance difference between CDSL and NSDL with regard to

Operating Income to Total Income (One Way ANOVA)

table

@0.01

L.O.S

Decision

11.26

H0 is

Rejected

and H1 is

Accepted

CDSL

NSDL

133

The ratio of Operating Income to Total Income is an important measure

for analyzing the operating efficiency of the depository. To test whether there

exists significance difference between CDSL and NSDL with regard to operating

efficiency (OI/TI).The table-5.3.1 indicates that F-cal (93.29) is more than F-table

(11.26) at 0.01 level of significance for degrees of freedom ʋ1= 1 and ʋ2 = 8.

Null hypothesis (H0) is rejected and hence, H1 is accepted .Therefore it is

concluded that there is significance difference between CDSL and NSDL with

regard to operating Income to Total Income Ratio (operating efficiency).

It is suggested to CDSL and NSDL to enhance their operating efficiency so that

their operating Income to Total Income will reach to maximum level.

Other Income to Total Income Ratio

This ratio shows the Other Income to Total Income Ratio of selected

depositories during the study period. This ratio helps to assess depositories’ way

of working. The higher the ratio the better will be the profitability but it can be

said that the depository is unable to work operationally well. The Other Income

here includes Misc. Income, Interest or Dividend Income, profit on sale of assets,

etc. The formula of the ratio is as under.

Other Income to Total Income Ratio =

Table 5.4 Other Income to Total Income Ratio of CDSL and NSDL

(Figures in %)

Year CDSL NSDL

2007-2008 16.96 8.09

2008-2009 22.18 7.76

2009-2010 19.84 8.35

2010-2011 17.55 7.21

2011-2012 23.46 5.95

Average 19.99 7.47

Standard deviation 2.53 0.85

Co-efficient

variation

12.64 11.38

Source: Calculated from the Published Annual Reports of the Depositories during study period.

Other Income * 100

Total Income

134

The table 5.4 shows that Other Income to Total Income ratio of CDSL and

NSDL during the period under review. This ratio shows income earned by

depositories other than Operational one. Other Income includes Misc. Income,

Interest or Dividend Income, profit on sale of assets, etc. It revels from the above

table that CDSL ratio represents decreasing trend except financial year 2008-09

during the study period. It has reached at its highest level in the financial year

2008-09. The average ratio was 22.17%. The NSDL registered fluctuating trend

during the study period however the Other Income to Total Income ratio was

lower than 9% during the period under review which affects positively to

company’s operational efficiency. Comparing the CV of CDSL and NSDL, the

CDSL has registered with higher CV than NSDL which shows high fluctuations

in the ratio whereas NSDL has low ratio which shows stability in company’s

earning. It is observed that CDSL is not performing its operations well even

though it has high mean of OI /TI when compared with NSDL and more over

NSDL has lesser business risk than CDSL. Therefore, it is suggested that to the

CDSL to concentrate on earning consistent income by performing operations well

and that should lead to decrease in business risk.

Chart 5.3 Other Income to Total Income of CDSL and NSDL

H0: There is no significance difference between CDSL and NSDL with regard to

Other Income to Total Income Ratio.

H1: There is significance difference between CDSL and NSDL with regard to

Other Income to Total Income Ratio.

05

101520253035

NSDL

CDSL

135

Table 5.4.1 Other Income to Total Income (One Way ANOVA)

Source Sum of

Squares

D

f

Mean

Square

F-Cal Sig. F-table

@0.01

L.O.S

Decision

Between

Groups

Within Groups

Total

392.252

35.615

427.866

1

8

9

392.252

4.452

88.110 .000* 11.26 H0 is

Rejected

and H1 is

Accepted

Source: SPSS and * significant at 0.01 level of significance

The ratio of other Income to Total Income is an important measure for

analyzing whether depository is performing its operations well or not? The anova

test is conducted between CDSL and NSDL to know the significance difference

between CDSL and NSDL with regard to other income to total income ratio. The

table 5.4.1 indicates that F-cal (88.11) is more than F-table (11.26) at 0.01 level of

significance for degrees of freedom ʋ1= 1 and ʋ2 = 8. Null hypothesis (Ho) is

rejected and hence, H1 is accepted .Therefore it is concluded that there is

significance difference between CDSL and NSDL with regard to other Income to

Total Income Ratio. It is suggested that of CDSL and NSDL have to enhance their

other income by performing their operations well or effectively.

Total Expenses to Total Income Ratio

This ratio shows the Total Expenses to Total Income Ratio of selected

depositories during the study period. This ratio helps to assess depositories’

Profitability from the view point of expenses. Higher ratio affects negatively to

the profitability of depositories’ income earning capacity. Total expenses include

administration, and other expenses of the organization. The formula of the ratio is

as under.

Total Expenses to Total Income Ratio =

TotalExpenses *100

Total Income

136

Table 5.5 Total Expenses to Total Income Ratio of CDSL and NSDL

(

F

i

g

u

r

e

s

i

n

Source: calculated from the Published Annual Reports of the Depositories during study period.

The table 5.5 shows Total Expenses to Total Income ratio of CDSL and

NSDL during the period under review. This ratio shows expenses accrued by

depositories during study period. Total expenses include administration, and other

expenses of the organization. It reveals from the above table that CDSL ratio

represents decreasing trend during 2008-12. CDSL was controlling its total

expenses effectively. Its ratio reached to highest level of 38.11 in the financial

year 2008-9.

The NSDL registered fluctuating from 2007 to2011 and then increased

marginally in 2011-12. The lower Total expenses to Total Income ratio affects

positively to company’s operational efficiency and profitability. Comparing the

CV of CDSL and NSDL, the CDSL has registered with lower CV than NSDL

which shows that NSDL has less stability in term of Total Expenses to Total

Income ratio during the study period. Therefore, it is found that CDSL is

controlling its total expenses to total income consistently and its trend is in

decreasing from2008-12. The NSDL has high level of Total expenses to Total

income as its mean ratio is 70.14 and CV of 9.23. In this regard, it is suggested to

the NSDL to control its total expenses effectively so that it can improve its

consistency in total expenses to total income.

Year CDSL NSDL

2007-2008 33.80 60.97

2008-2009 38.11 80.51

2009-2010 33.46 66.35

2010-2011 32.84 71.07

2011-2012 32.46 71.80

Average 34.14 70.14

Standard deviation 2.04 6.48

Co-efficient variance 5.98 9.23

Fig 5.4 Total Expenses to Total Income

H0: There is no significance difference between CDSL an

Total Expenses to Total Income Ratio.

H1: There is significance difference between CDSL and NSDL with regard to

Total Expenses to Total Income Ratio.

Table 5.5.1Total Expenses

Source Sum

Squares

Between

Groups

Within

Groups

Total

3241.080

230.462

3471.542Source: SPSS and * significant at 0.01 level

The table 5.5.1 indicates that F

0.01 level of significance for degrees of freedom

hypothesis (H0) is rejected and hence,

that there is no uniformity in Total expenses to

CDSL and NSDL and it is significant statistically.

020406080

100

`in

Laksh

s i

n %

137

Total Expenses to Total Income of CDSL and NSDL

: There is no significance difference between CDSL and NSDL with regard to

to Total Income Ratio.

There is significance difference between CDSL and NSDL with regard to

to Total Income Ratio.

Total Expenses to Total Income (One Way ANOVA)

Sum of

Squares

Df Mean

Square

F-Cal Sig. F-

table

@0.01

L.O.S

3241.080

230.462

3471.542

1

8

9

3241.080

28.808

112.51 .000* 11.26

Source: SPSS and * significant at 0.01 level of significance

.1 indicates that F-cal (112.11) is more than F-table (11.26

0.01 level of significance for degrees of freedom ʋ1= 1 and ʋ2 = 8.

) is rejected and hence, H1 is accepted .Therefore it is conclude

uniformity in Total expenses to Total Income Ratio

CDSL and NSDL and it is significant statistically. It is suggested to

Years

of CDSL and NSDL

d NSDL with regard to

There is significance difference between CDSL and NSDL with regard to

to Total Income (One Way ANOVA)

table

@0.01

L.O.S

Decision

11.26 H0 is

Rejected

and H1 is

Accepted

table (11.26) at

2 = 8. Null

s accepted .Therefore it is concluded

Total Income Ratio between

It is suggested to that CDSL

CDSL

NSDL

138

and NSDL have to enhance their efforts in controlling expenses to improve its

efficiency.

Return on Investment Ratio of CDSL and NSDL

This ratio shows the percentage return received by depositories on their

total share holder’s fund during the study period. This ratio helps to assess

depositories’ Profitability from the view point of share holder’s fund. Higher ratio

affects positively to the profitability of depositories’ income earning capacity.

Total share holder fund includes share capital and reserve and surplus during one

financial year. The formula of the ratio is as under.

ROI =

Table 5.6 Return on Investment Ratio of CDSL and NSDL

(Figures in %)

Year CDSL NSDL

2007-2008 20.83 20.36

2008-2009 17.17 9.54

2009-2010 20.58 22.01

2010=2011 18.16 19.51

2011-2012 16.16 20.52

Average 18.58 18.39

Standard

deviation

1.85 4.49

Co-efficient

variance

9.94 24.45

Source: calculated from the Published Annual Reports of the Depositories

Return on Investment is an important measure of performance of any

organization. ROI is important for the owners of the organization. The table 5.6

shows that Return on Investment ratio of CDSL and NSDL during the period

under review. This ratio reveals that returns earned by depositories on their

investment during study period. The profit which is taken as post tax. It reveals

from the above table that CDSL ratio represents fluctuating trend during the study

Profit after Tax * 100

Total Share Holders Fund

139

period of 2007-12 except in 2008-09 which shows that its profitability was not

stable. CDSL has achieved its highest level of 20.83 % in the financial year 2007-

08. The average ROI of CDSL obtained during the study is 18.58%. The NSDL

also registered fluctuating trend during the study period which also affects

negatively to its profitability. The Return on Investment ratio recorded 9.54%

which was the lowest during the period 2007-12 which affects negatively to

company’s operational efficiency. NSDL achieved highest ROI of 22.01 % in the

year 2009-10 .Comparing the CV of CDSL and NSDL; the CDSL has registered

with lower CV than NSDL which shows that NSDL has less stability in term of

Return on Investment ratio during the study period. It is found that both the

depositories have almost earned equally to the extent of 18 % of ROI during the

study from 2007-12 and more over CDSL has more consistency in ROI when

compared with NSDL. NSDL has high business risk due to fluctuating trend in

ROI and but its ROI is increased to 20.52 % in 2011-12 from 19.51 in 2010-11. In

this regard, it is suggested to the depositories to improve their operating and other

incomes and simultaneously control the total expenses and thus enhances the

consistency in ROI.

Fig 5.5 Return on Investment Ratio of CDSL and NSDL

H0: There is no significance difference in the return on investment (ROI) of

CDSL and NSDL.

H1: There is no significance difference in the return on investment (ROI) of CDSL

and NSDL.

0

5

10

15

20

25

30

0 5 10

`in

Laksh

s i

n %

Years

CDSL

NSDL

Linear (CDSL)

Linear (NSDL)

140

Table 5.6.1 Return on Investment (One Way ANOVA)

Sum of

Squares

Df Mean

Square

F-Cal Sig. F-

table

@0.01

L.O.S

Decision

Between

Groups

Within

Groups

Total

.092

118.182

118.275

1

8

9

.92

14.773

.006 .939ns

11.26 H0 is

Accepted

and H1 is

Rejected

Source: SPSS and ns- not significant at 0.01 level of significance.

The table 5.6.1 indicates that F-cal (0.006) is less than F-table (11.26) at

0.01 level of significance for degrees of freedom ʋ1= 1 and ʋ2 = 8. Alternative

hypothesis (H1) is rejected and hence, Ho is accepted .Therefore it is concluded

that there is uniformity in Return on Investment (ROI) earning of CDSL and

NSDL and it is not significant statistically. Both the depositories have earned

equally to the extent of 18 % only. It is suggested to depositories of CDSL and

NSDL to enhance their efforts in improving the operating incomes and other

incomes and by simultaneously the controlling expenses and that improves the

consistency in Return on Investment ratio.

Performance of Select Depository Participants

Financial statements are formal records of the financial activities of a

business, person, or other entity and provide an overview of a business or person's

financial condition in both short and long term. In this study give an accurate

picture of a select DPs condition and operating results in a condensed form.

Analysis and interpretation of financial statements help in determining the

liquidity position, long term solvency, financial viability and profitability of a

firm. Ratio analysis shows whether the depository participants are improving or

deteriorating in past years. Moreover, Comparison of different aspects of all the

firms can be done effectively with this. It helps the investors to decide in which

firm the risk is less or in which one they should invest so that maximum benefit

can be earned. So before have taking decision one have to carefully study its

financial condition and worthiness of DPs. Unfortunately very limited work has

141

been done on analysis and interpretation of financial statements of Indian for DPs.

An attempt has been carried out in this research to analyze and interpret the

financial statements of four select depository participants.

Performance of Karvy Stock Broking Ltd.

Current Ratio of Karvy Stock Broking Ltd:

Current ratio matches current assets with current liabilities and tells us

about Karvy Stock Broking Ltd whether the current assets are enough to settle

current liabilities. General rule is that higher the current ratio better it is but a ratio

of 2:1 is considered as ideal.

Table 5.7 Current Ratio of Karvy Stock Broking Limited

Years Current Ratio

2009 - 2010 0.13

2010 – 2011 0.93

2011 - 2012 3.64

Average 1.57

Source: Compiled from the annual reports of Karvy Stock Broking Co.Ltd.

The table 5.7 indicates that average current ratio of KSBCL is 1.57 which

is below the standard norm of 2:1, so KSBCL cannot meet its short term

obligations effectively. The trend of current ratio of KSBCL is in increasing trend.

Therefore, it is found that liquidity position of the KSBCL is not satisfactory as

its average current ratio during the study is 1.57 and its ratio in years 2009-10 to

2010-11 were lower than standard norm of 2:1 which means for every one rupee

worth of current liability KSBCL has 1.57 rupees worth of current assets. In this

regard, it is suggested to the KSBCL to take appropriate measures to enhance the

current assets over current liabilities so that it has sufficient liquidity to discharge

short term obligations effectively.

142

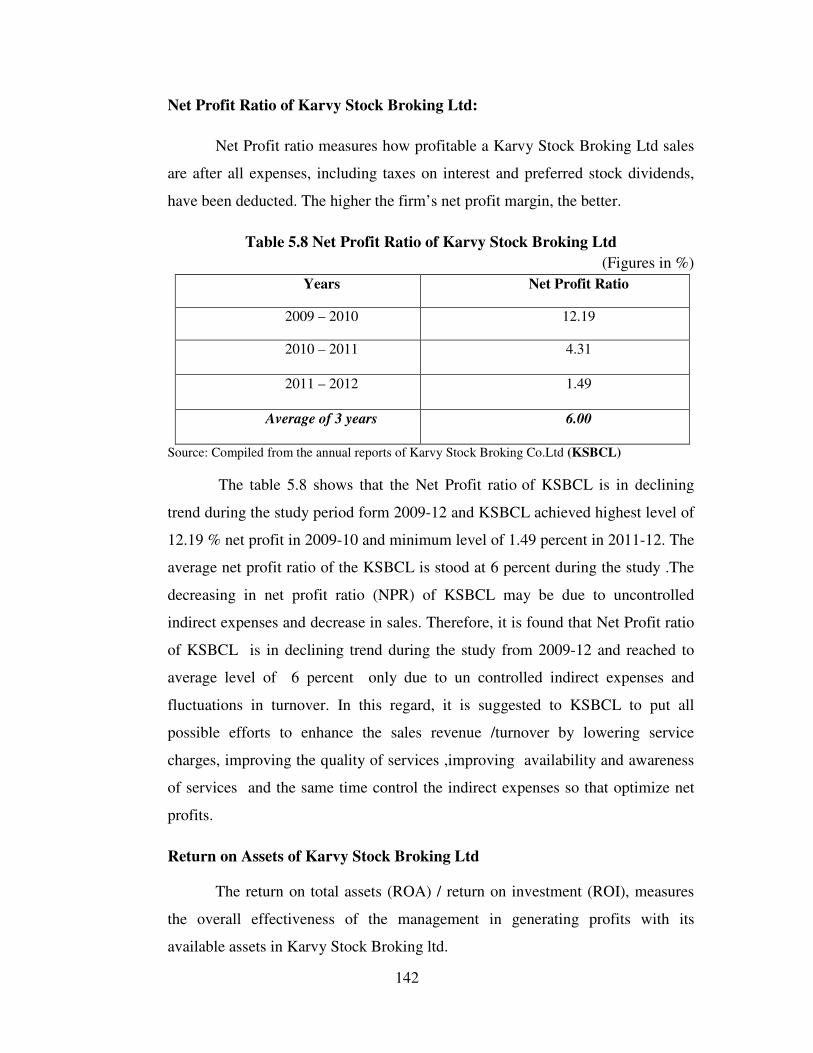

Net Profit Ratio of Karvy Stock Broking Ltd:

Net Profit ratio measures how profitable a Karvy Stock Broking Ltd sales

are after all expenses, including taxes on interest and preferred stock dividends,

have been deducted. The higher the firm’s net profit margin, the better.

Table 5.8 Net Profit Ratio of Karvy Stock Broking Ltd

(Figures in %)

Years Net Profit Ratio

2009 – 2010 12.19

2010 – 2011 4.31

2011 – 2012 1.49

Average of 3 years 6.00

Source: Compiled from the annual reports of Karvy Stock Broking Co.Ltd (KSBCL)

The table 5.8 shows that the Net Profit ratio of KSBCL is in declining

trend during the study period form 2009-12 and KSBCL achieved highest level of

12.19 % net profit in 2009-10 and minimum level of 1.49 percent in 2011-12. The

average net profit ratio of the KSBCL is stood at 6 percent during the study .The

decreasing in net profit ratio (NPR) of KSBCL may be due to uncontrolled

indirect expenses and decrease in sales. Therefore, it is found that Net Profit ratio

of KSBCL is in declining trend during the study from 2009-12 and reached to

average level of 6 percent only due to un controlled indirect expenses and

fluctuations in turnover. In this regard, it is suggested to KSBCL to put all

possible efforts to enhance the sales revenue /turnover by lowering service

charges, improving the quality of services ,improving availability and awareness

of services and the same time control the indirect expenses so that optimize net

profits.

Return on Assets of Karvy Stock Broking Ltd

The return on total assets (ROA) / return on investment (ROI), measures

the overall effectiveness of the management in generating profits with its

available assets in Karvy Stock Broking ltd.

143

Table 5.9 Return on Assets of Karvy Stock Broking Ltd

(Figures in %)

S

o

u

r

c

e

:

C

o

m

piled from the annual reports of Karvy Stock Broking.Ltd

The table 5.9 shows that ROA of KSBCL is in declining trend during the

study from 2009-12. The average return on Assets (ROA) of KSBCL during the

study was 3.59 percent only which indicates the in efficiency of the management

in utilizing the assets for generating adequate returns. Therefore, it is found that

the average return on assets (ROA) of KSBCL during the study from 2009-12 is

3.59 percent only which indicates that management is not utilized the assets to the

optimum extent in generating sufficient returns. It is suggested to the KSBCL to

utilize the all the assets to the optimum extent and improve operational efficiency

so that Return on assets (ROA) is maximized.

India Info Line Limited (IIFL)

Current Ratio of IIFL

Current ratio matches current assets with current liabilities and tells us

about IIFL whether the current assets are enough to settle current liabilities.

Current ratio below 1 shows critical liquidity problems because it means that total

current liabilities exceed total current assets. General rule is that higher the

current ratio better it is but a ratio of 2:1 is considered as ideal.

Years ROA

2009 - 2010 8.60

2010 – 2011 1.78

2011 - 2012 0.41

Average ROA 3.59

144

Table 5.10 Current Ratio of IIFL

(Figure in %)

Years Current Ratio

2009 – 2010 1.52

2010 – 2011 1.42

2011 – 2012 1.39

Average CR 1.44

Source: Compiled from the annual reports of the IIFL.

The table 5.10 indicates that a current ratio of 1.44 is below the standard

norm of 2:1, so IIFL cannot meet its short term obligations effectively. The trend

of current ratio of IIFL is in decreasing trend. Therefore, it is found that liquidity

position of the IIFL is not satisfactory as its average current ratio during the study

is 1.44 only which means every one rupee current liability IIFL has 1.44 rupees of

current assets. In this regard, it is suggested to the IIFL to take appropriate

measures to enhance the current assets over current liabilities so that its liquidity

can discharge short term obligations effectively.

Net Profit Ratio of IIFL

Net profit margin = Earnings after Taxes (EAT) / Sales. It measures how

profitable a IIFL sales are after all expenses, including taxes on interest and

preferred stock dividends, have been deducted. The higher the firm’s net profit

margin, the better.

Table 5.11 Net Profit Ratio of IIFL

(Figure in %)

Years Net Profit Ratio

2009 - 2010 22.02

2010 - 2011 15.29

2011 - 2012 10.13

Average 15.81

Source: Compiled from the annual reports of the IIFL.

145

The table 5.11 shows that the Net Profit ratio is in decreasing trend during

the study period form 2009-12 and IIFL achieved highest level of 22.02 % net

profit in 2009-10 and minimum level of 10.13 % in 2011-12. The average net

profit ratio of the IIFL is stood at 15.81 % during the study .The decreasing in net

profit ratio (NPR) of IIFL may be due to uncontrolled indirect expenses even

though sales are increasing. Therefore, it is found that Net Profit ratio of IIFL is in

decreasing trend during the study from 2009-12 and reached to average level of

15.81 % only due to un controlled indirect expenses even though the turnover is

in increasing trend. In this regard, it is suggested to IIFL to put all possible efforts

to control the indirect expenses and at same the time continues the increasing

trend in sales in future also.

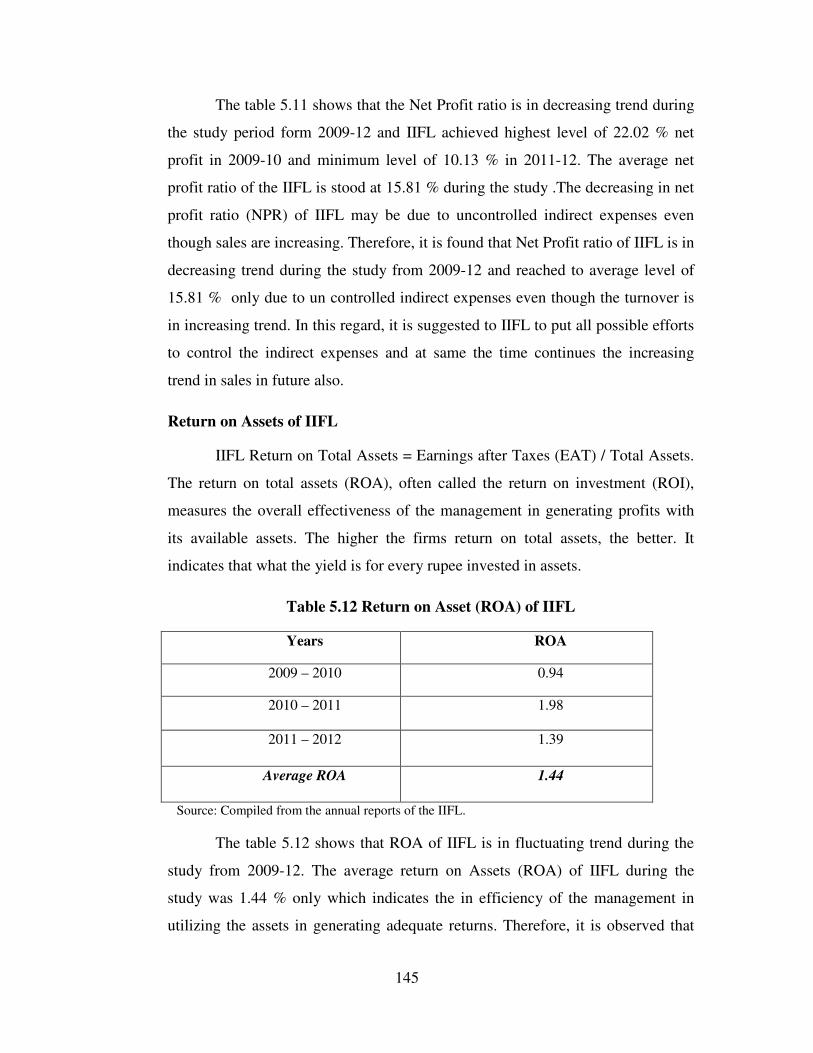

Return on Assets of IIFL

IIFL Return on Total Assets = Earnings after Taxes (EAT) / Total Assets.

The return on total assets (ROA), often called the return on investment (ROI),

measures the overall effectiveness of the management in generating profits with

its available assets. The higher the firms return on total assets, the better. It

indicates that what the yield is for every rupee invested in assets.

Table 5.12 Return on Asset (ROA) of IIFL

Years ROA

2009 – 2010 0.94

2010 – 2011 1.98

2011 – 2012 1.39

Average ROA 1.44

Source: Compiled from the annual reports of the IIFL.

The table 5.12 shows that ROA of IIFL is in fluctuating trend during the

study from 2009-12. The average return on Assets (ROA) of IIFL during the

study was 1.44 % only which indicates the in efficiency of the management in

utilizing the assets in generating adequate returns. Therefore, it is observed that

146

the average return on assets (ROA) of IIFL during the study is 1.44 % only which

indicates that management is not utilized the assets to the optimum extent in

generating sufficient returns. It is suggested to the IIFL to utilize the all the assets

to the optimum extent so that Return on assets (ROA) is maximized.

PCS Securities Ltd.

Current Ratio of PCS Securities Ltd:

Current ratio matches current assets with current liabilities and tells us

PCS Securities whether the current assets are enough to settle current liabilities.

Current ratio below 1 shows critical liquidity problems because it means that total

current liabilities exceed total current assets. General rule is that higher the

current ratio better it is but a ratio of 2:1 is considered as ideal.

Table 5.13 Current Ratio of PCS Securities

(Figure in %)

Years Current Ratio

2009 – 2010 2.62

2010 – 2011 1.38

2011 – 2012 2.71

Average CR 2.24

Source: Compiled from the annual reports of PCS Securities Limited

The table 5.13 indicates that a current ratio of 2.24 is more than the

standard norm of 2:1, so PCS can meet its short term obligations effectively. The

trend of current ratio of PCS is in fluctuating trend. Therefore, it is found that

liquidity position of the PCS is satisfactory as its average current ratio during the

study is 2.24 only which means every one rupee current liability PCS has 2.24

rupees of current assets. In this regard, it is suggested to the PCS management to

invest idle funds in money market instruments so that to achieve trade-off

between liquidity and profitability.

147

Net Profit Ratio:

Net profit margin = Earnings after Taxes (EAT) / Sales. It measures how

profitable a PCS Securities sales are after all expenses, including taxes on interest

and preferred stock dividends, have been deducted. The higher the firm’s net

profit margin, the better.

Table 5.14 Net Profit Ratio of PCS Securities

(Figures in %)

Years Net Profit Ratio

2009 - 2010 9.40

2010 - 2011 13.50

2011 - 2012 7.38

Average 25.36

Source: Compiled from the annual reports of PCS Securities Limited

The table 5.14 shows that the Net Profit ratio is in decreasing trend during

the study period form 2011-12 and PCS achieved highest level of 13.50 % cash

profit in 2010-11 and minimum level of 9.40 % in 2009-10. The average net profit

ratio of the PCS is stood at 25.36 % during the study .The decreasing in net profit

ratio (NPR) of PCS may be due to uncontrolled indirect expenses even though

sales are increasing. Therefore, it is found that Net Profit ratio of PCS is in

decreasing trend during the study from 2011-12 and reached to average level of

25.36% only due to un controlled indirect expenses even though the turnover is

in increasing trend. In this regard, it is suggested to PCS to put all possible efforts

to control the indirect expenses and at same the time continues the increasing

trend in sales in future also.

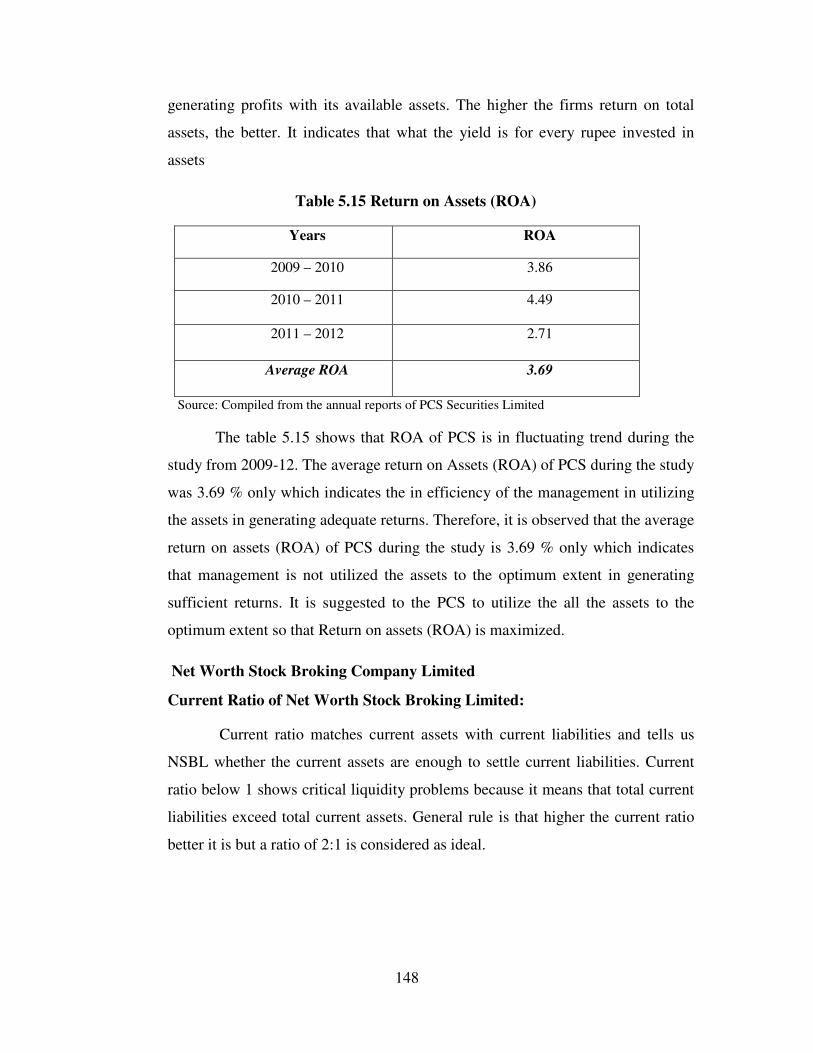

Return on Assets of PCS Securities:

PCS Securities Return on Total Assets = Earnings after Taxes (EAT) /

Total Assets. The return on total assets (ROA), often called the return on

investment (ROI), measures the overall effectiveness of the management in

148

generating profits with its available assets. The higher the firms return on total

assets, the better. It indicates that what the yield is for every rupee invested in

assets

Table 5.15 Return on Assets (ROA)

Years ROA

2009 – 2010 3.86

2010 – 2011 4.49

2011 – 2012 2.71

Average ROA 3.69

Source: Compiled from the annual reports of PCS Securities Limited

The table 5.15 shows that ROA of PCS is in fluctuating trend during the

study from 2009-12. The average return on Assets (ROA) of PCS during the study

was 3.69 % only which indicates the in efficiency of the management in utilizing

the assets in generating adequate returns. Therefore, it is observed that the average

return on assets (ROA) of PCS during the study is 3.69 % only which indicates

that management is not utilized the assets to the optimum extent in generating

sufficient returns. It is suggested to the PCS to utilize the all the assets to the

optimum extent so that Return on assets (ROA) is maximized.

Net Worth Stock Broking Company Limited

Current Ratio of Net Worth Stock Broking Limited:

Current ratio matches current assets with current liabilities and tells us

NSBL whether the current assets are enough to settle current liabilities. Current

ratio below 1 shows critical liquidity problems because it means that total current

liabilities exceed total current assets. General rule is that higher the current ratio

better it is but a ratio of 2:1 is considered as ideal.

149

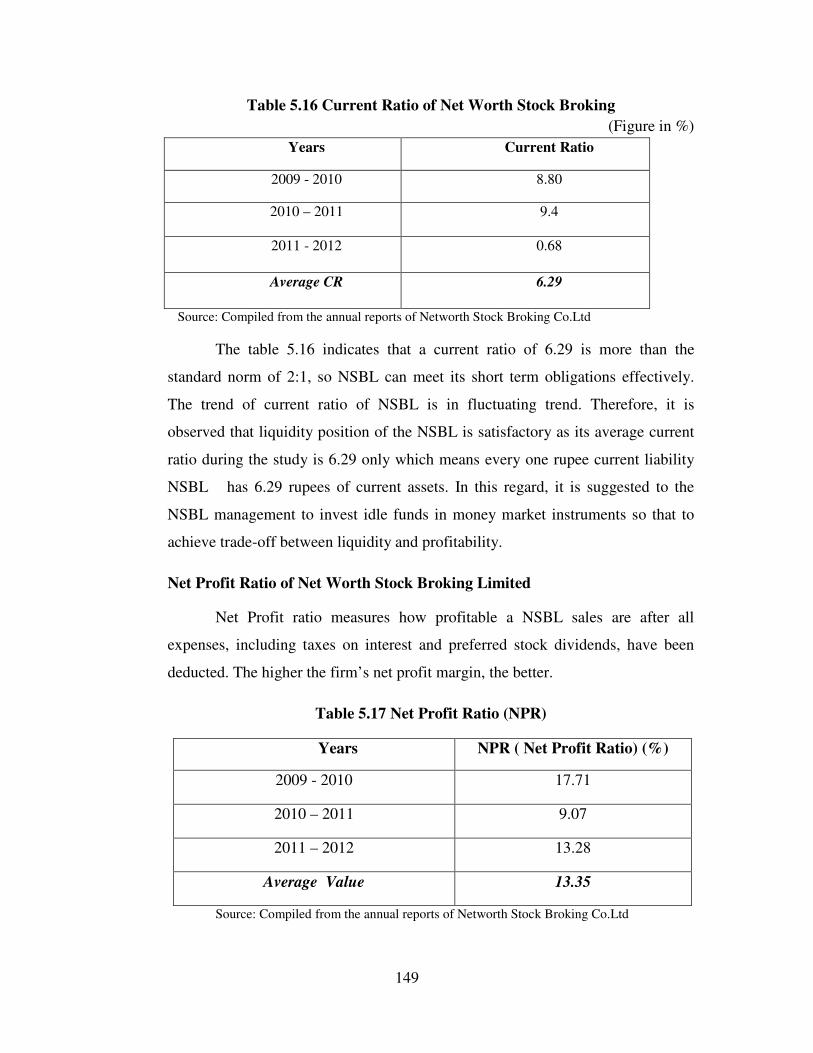

Table 5.16 Current Ratio of Net Worth Stock Broking

(Figure in %)

Years Current Ratio

2009 - 2010 8.80

2010 – 2011 9.4

2011 - 2012 0.68

Average CR 6.29

Source: Compiled from the annual reports of Networth Stock Broking Co.Ltd

The table 5.16 indicates that a current ratio of 6.29 is more than the

standard norm of 2:1, so NSBL can meet its short term obligations effectively.

The trend of current ratio of NSBL is in fluctuating trend. Therefore, it is

observed that liquidity position of the NSBL is satisfactory as its average current

ratio during the study is 6.29 only which means every one rupee current liability

NSBL has 6.29 rupees of current assets. In this regard, it is suggested to the

NSBL management to invest idle funds in money market instruments so that to

achieve trade-off between liquidity and profitability.

Net Profit Ratio of Net Worth Stock Broking Limited

Net Profit ratio measures how profitable a NSBL sales are after all

expenses, including taxes on interest and preferred stock dividends, have been

deducted. The higher the firm’s net profit margin, the better.

Table 5.17 Net Profit Ratio (NPR)

Years NPR ( Net Profit Ratio) (%)

2009 - 2010 17.71

2010 – 2011 9.07

2011 – 2012 13.28

Average Value 13.35

Source: Compiled from the annual reports of Networth Stock Broking Co.Ltd

150

The table 5.17 shows that the Net Profit ratio is in fluctuating trend during

the study period form 2009-12 and Networth company achieved highest level of

17.71 % net profit in 2009-10 and minimum level of 9.07 % in 2010-11. The

average net profit ratio of the Networh is stood at 13.35 % during the study .The

net profit ratio (NPR) of Networh is low due to uncontrolled indirect expenses

and decreasing sales. Therefore, it is found that Net Profit ratio of Networth

Company is in fluctuating trend during the study from 2009-12 and on average,

the firm earned a net profit of 13.35 % only due to uncontrolled indirect expenses

and declining trend in sales. In this regard, it is suggested to Net worth Company

to put all possible efforts to enhance the sales by lowering service charges,

improving the quality of services and other promotional efforts. More over

measures should be taken to control the indirect expenses also for magnifying the

profits of the firm.

Return on Assets of Net Worth Stock Broking Limited:

NBSL The return on investment (ROI), measures the overall effectiveness

of the management in generating profits with its available assets. The higher the

Net worth Stock broking limited return on total assets, the better. It indicates that

what the yield is for every rupee invested in assets.

Table 5.18 Return on Assets of Net Worth Stock Broking

(Figures in %)

Years ROA (%)

2009 - 2010 17.49

2010 – 2011 3.89

2011 - 2012 3.22

Average ROA 8.2

Source: Compiled from the annual reports of Networth Stock Broking Co.Ltd

The table 5.18 shows that ROA of NSBL is in declining trend during the

study from 2009-12. The average return on Assets (ROA) of NSBL during the

study was 8.2 percent only which indicates the in efficiency of the management in

utilizing the assets in generating adequate returns. Therefore, it is found that the

151

average return on assets (ROA) of NSBL during the study is 8.2 percent only

which indicates that management is not utilized the assets to the optimum extent

in generating sufficient returns. It is suggested to the NSBL to utilize the all the

assets to the optimum extent and improve operational efficiency so that Return on

assets (ROA) is maximized.

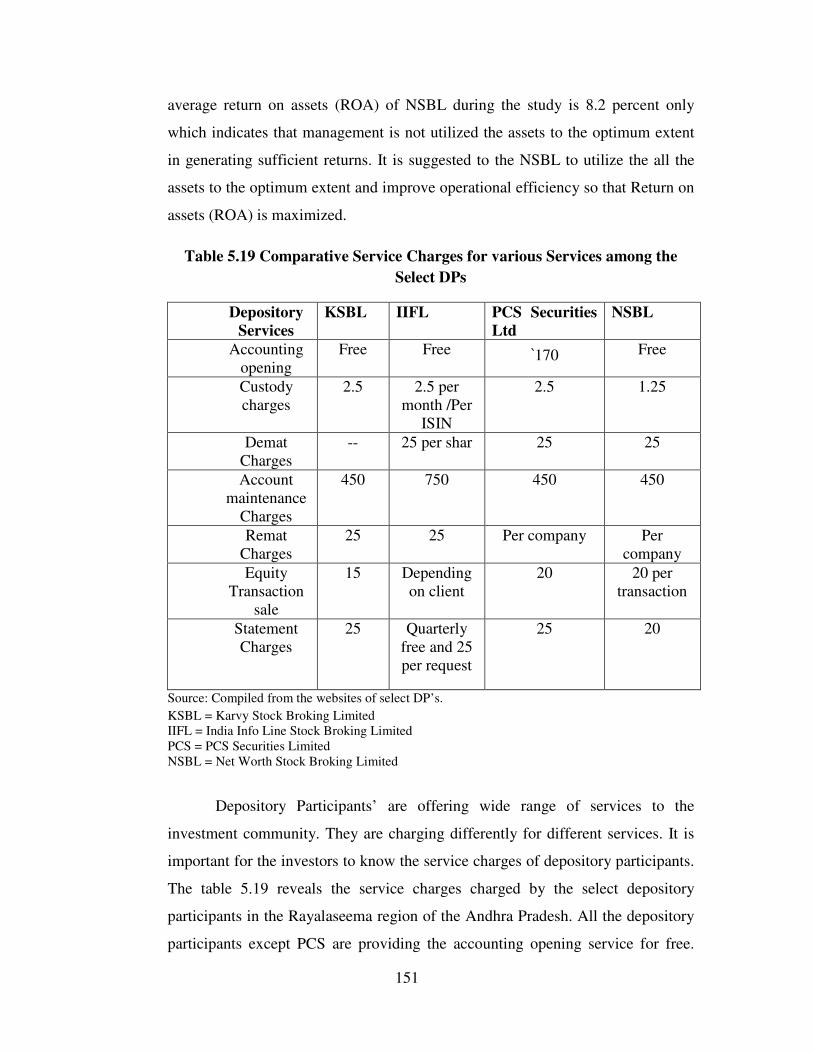

Table 5.19 Comparative Service Charges for various Services among the

Select DPs

Depository

Services

KSBL IIFL PCS Securities

Ltd

NSBL

Accounting

opening

Free Free `170 Free

Custody

charges

2.5 2.5 per

month /Per

ISIN

2.5 1.25

Demat

Charges

-- 25 per shar 25 25

Account

maintenance

Charges

450 750 450 450

Remat

Charges

25 25 Per company Per

company

Equity

Transaction

sale

15 Depending

on client

20 20 per

transaction

Statement

Charges

25 Quarterly

free and 25

per request

25 20

Source: Compiled from the websites of select DP’s.

KSBL = Karvy Stock Broking Limited

IIFL = India Info Line Stock Broking Limited

PCS = PCS Securities Limited

NSBL = Net Worth Stock Broking Limited

Depository Participants’ are offering wide range of services to the

investment community. They are charging differently for different services. It is

important for the investors to know the service charges of depository participants.

The table 5.19 reveals the service charges charged by the select depository

participants in the Rayalaseema region of the Andhra Pradesh. All the depository

participants except PCS are providing the accounting opening service for free.

152

PCS securities Ltd is charging for accounting opening for 170 rupees. All

depository participants except NSBL are almost charging same for the custody of

securities. NSBL is charging 1.25 rupees for security custody charges only .All

the depository participants are charging same except KSBCL for the service of

demat. KSBCL is offering the demat service for free of cost. Among the select

depository participants, IIFL is charging to the extent of 750 rupees for account

maintenance service where as the remaining DP’s are charging 450 rupees only.

Among the select DP’s IIFL and KSBCL are charging 25 rupees for remat service

where as remaining (NSBL and PCS) are charging per company wise. The service

charge charged by the select depository participants for equity transaction sale

and statement charges are competitive.

It is observed that Net worth Stock Broking Ltd and Karvey Stock

Broking Co.Ltd are charging less for various services offered to the investors

when compared with other depository participants. The service charges charged

by select depository participants for the services of security custody, equity

transaction sale and transaction statement are competitive. Among select the

depository participants, only PCS securities is charging to the extent of 170

rupees others are providing the accounting opening service for free of cost. IIFL is

charging to the extent of 750 rupees for account maintenance service where as the

remaining DP’s are charging 450 rupees only. In this regard, it is suggested to the

depository participants to offer services to the investors for reasonable /nominal

charges so that large number of investors are motivated and invest towards capital

market securities.

Table 5.20 Current Ratio (One Way ANOVA)

Source Sum of

Squares

Df Mean

Square

F-Cal Sig. F-table

@0.01

L.O.S

Decision

Between

Groups

Within

Groups

Total

47.560

55.326

102.887

3

8

11

15.853

6.916

2.292 .155ns

7.59 H0 is

Accepted

and H1 is

Rejected

Source : SPSS and ns – not significant at 0.01 level of significance

153

H0: Current Ratio (CR) position of KSBL, IIFL, PCS, and NSBL does not differ

significantly.

H1: Current Ratio (CR) position of KSBL, IIFL, PCS and NSBL differ

Significantly.

Current ratio is an important indicator of liquidity position. A current

ratio of 2:1 is considered as standard norm or ideal .The average current ratios of

IIFL, PCS, NSBL and KSBCL were 1.44, 2.24, 6.29 and 1.57 respectively. IIFL

and KSBCL liquidity position is not satisfactory and PCS and NSBL maintained

satisfactory liquidity position. To test whether there is significance difference in

the liquidity position of IIFL, PCS, NSBL and KSBL or not. The F-test / Anova is

conducted and result is given in the table 5.20. It reveals that F-cal (2.29) is less

than F-table (7.59) at 0.01 level of significance for degrees of freedom ʋ1=3 and

ʋ2 = 8. Alternative hypothesis (H1) is rejected and hence, H0 is accepted

.Therefore it is concluded that there is uniformity in the current ratio (CR) or

liquidity position of IIFL, PCS, NSBL and KSBCL or Current ratio position of

IIFL, PCS, NSBL and KSBCL does not differ significantly. All the depository

participants have to maintain standard norm level of liquidity so that they remain

competitive and can discharge their short term obligations effectively.

Table 5.21 Return on Assets (One Way ANOVA)

Source Sum of

Squares

Df Mean

Square

F-Cal Sig. F-table

@0.01

L.O.S

Decision

Between

Groups

Within

Groups

Total

72.780

170.342

243.122

3

8

11

24.260

21.293

1.139 .390ns

7.59 H0 is

Accepted

and H1 is

Rejected

Source : SPSS and ns – not significant at 0.01 level of significance

H0: There is no significant difference in the return on assets (ROA) of KSBL,IIFL,

PCS and NSBL.

H1: There is significant difference in the return on assets (ROA) of KSBL , IIFL,

PCS and NSBL.

154

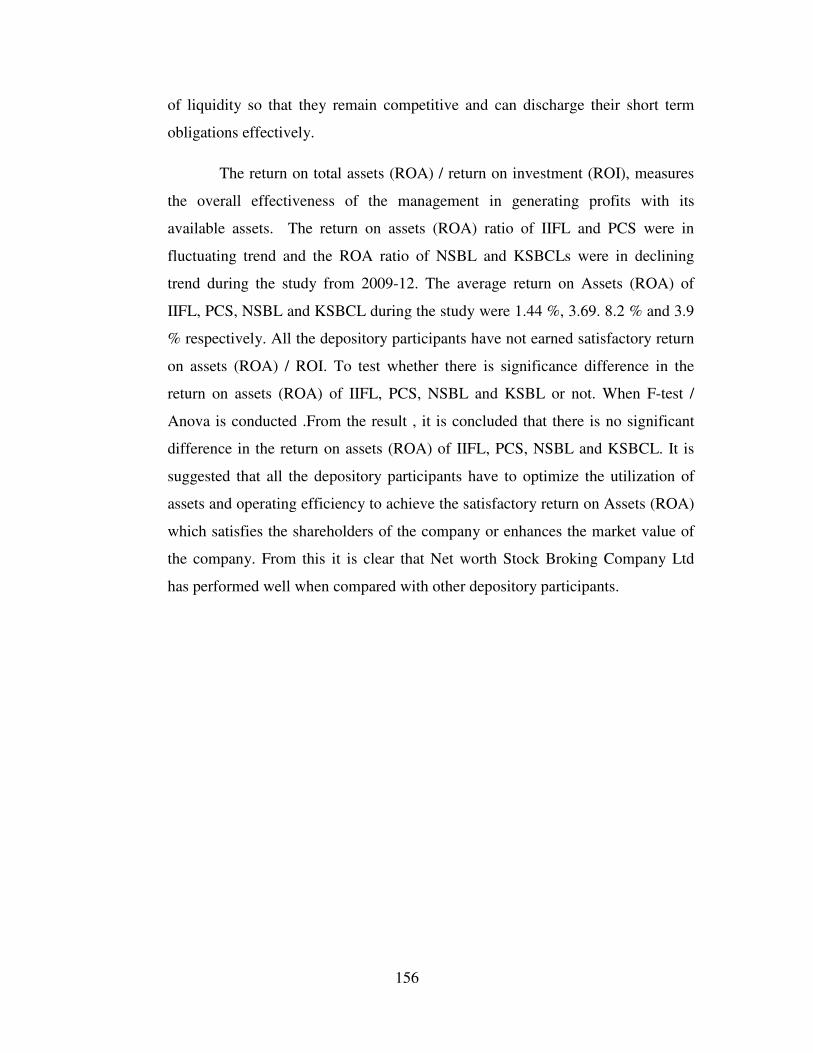

The return on total assets (ROA) / return on investment (ROI), measures

the overall effectiveness of the management in generating profits with its

available assets. The return on assets (ROA) ratio of IIFL and PCS were in

fluctuating trend and the ROA ratio of NSBL and KSBCLs were in declining

trend during the study from 2009-12. The average return on Assets (ROA) of

IIFL, PCS, NSBL and KSBCL during the study were 1.44 %, 3.69. 8.2 % and 3.9

% respectively. All the depository participants have not earned satisfactory return

on assets (ROA) / ROI. To test whether there is significance difference in the

return on assets (ROA) of IIFL, PCS, NSBL and KSBL or not. The F-test / Anova

is conducted and result is given in the table 5.21. It reveals that F-cal (1.139) is

less than F-table (7.59) at 0.01 level of significance for degrees of freedom ʋ1=3

and ʋ2 = 8. Alternative hypothesis (H1) is rejected and hence, Ho is accepted

.Therefore it is concluded that there is no significant difference in the return on

assets (ROA) of IIFL, PCS, NSBL and KSBCL. It is suggested that all the

depository participants have to optimize the utilization of assets and operating

efficiency to achieve the satisfactory return on Assets (ROA) which satisfies the

shareholders of the company or enhances the market value of the company.

It can be concluded from the above that the depositories and select

depository participants (IIFL, NSBL, PCS and KSBCL) are providing wide range

of services. All are interested in knowing the financial performance of

depositories, CDSL and NSDL and depository participants of IIFL, PCS, NSBL

and KSBCL as earning returns from the services rendered is essential for survival

in the market. Operating Income to Total Income ratio helps to assess the

operational efficiency of the unit compare to total income of the depositories. It is

found that NSDL is performing well when compared with CDSL as mean ratio of

Other Income to TI (Total Income) is high and also CV is low. It is suggested to

CDSL to reduce its business risk and enhance its operating efficiency so that it

can achieve maximum Operating Income to Total Income ratio.

From the point of view of ratio of Other Income to Total Income earned,

it is observed that CDSL is not performing its operations well even though it has

155

high mean of OI /TI when compared with NSDL and more over NSDL has lesser

business risk than CDSL. From the point of view of Total expenses to Total

Income, it is found that CDSL is controlling its total expenses to total income

consistently and its trend is in decreasing from2008-12. The NSDL has high level

of Total expenses to Total income as its mean ratio is 70.14 and CV of 9.23. In

this regard, it is suggested to the NSDL to control its total expenses effectively so

that it can improve its consistency in total expenses to total income. It is found

that both the depositories have almost earned equally to the extent of 18 % of ROI

during the study from 2007-12 and more over CDSL has more consistency in ROI

when compared with NSDL. It is also proved statistically that two depositories

have same ROI. NSDL has high business risk due to fluctuating trend in ROI and

but its ROI is increased to 20.52 % in 2011-12 from 19.51 in 2010-11.

Depository Participants are rendering wide range of services to investing

community. It is necessary to understand the service charges charged by select

depository participants as it has impact on the performance of the firms. It is

observed that Networh Stock Broking Ltd and Karvey Stock Broking Co.Ltd are

charging less for various services offered to the investors when compared with

other depository participants. The service charges charged by select depository

participants for the services of security custody, equity transaction sale and

transaction statement are competitive. Among select the depository participants,

only PCS securities is charging to the extent of 170 rupees others are providing

the accounting opening service for free of cost. IIFL is charging to the extent of

750 rupees for account maintenance service where as the remaining DP’s are

charging 450 rupees only..The average current ratios of IIFL, PCS, NSBL and

KSBCL were 1.44, 2.24, 6.29 and 1.57 respectively. IIFL and KSBCL liquidity

position is not satisfactory and PCS and NSBL maintained satisfactory liquidity

position. When Anova / F-test is conducted to know whether there is significance

difference in liquidity position of selected depository participants or not?. From

result, it is concluded that the liquidity position of IIFL, PCS, NSBL and KSBCL

or Current ratio position of IIFL,PCS ,NSBL and KSBCL does not differ

significantly. All the depository participants have to maintain standard norm level

156

of liquidity so that they remain competitive and can discharge their short term

obligations effectively.

The return on total assets (ROA) / return on investment (ROI), measures

the overall effectiveness of the management in generating profits with its

available assets. The return on assets (ROA) ratio of IIFL and PCS were in

fluctuating trend and the ROA ratio of NSBL and KSBCLs were in declining

trend during the study from 2009-12. The average return on Assets (ROA) of

IIFL, PCS, NSBL and KSBCL during the study were 1.44 %, 3.69. 8.2 % and 3.9

% respectively. All the depository participants have not earned satisfactory return

on assets (ROA) / ROI. To test whether there is significance difference in the

return on assets (ROA) of IIFL, PCS, NSBL and KSBL or not. When F-test /

Anova is conducted .From the result , it is concluded that there is no significant

difference in the return on assets (ROA) of IIFL, PCS, NSBL and KSBCL. It is

suggested that all the depository participants have to optimize the utilization of

assets and operating efficiency to achieve the satisfactory return on Assets (ROA)

which satisfies the shareholders of the company or enhances the market value of

the company. From this it is clear that Net worth Stock Broking Company Ltd

has performed well when compared with other depository participants.