CHAPTER V CHANGES IN MANAGERlAL...

58

CHAPTER V CHANGES IN MANAGERlAL PERFORMANCE Recent years have witnessed an unprecedented emphasis k i n g placed on profitability of' the Public Sector Enterprises while the Government is still committed to its long standing policy of allowing the Public Sector to achieve commanding heights in the economy. It has made it abundantly clear that the Public Sector Enterprises must generate surpluses so that the society could get a reasonable return on the investment made in these enterprises. Pressure is likely to mount further on the Public Sector Enterprises to increase their efficiency and capacity utilisation, reduce costs exercise better control over project expenditure and take other steps to ensure improvement in Management ~erformance'. Further, the criteria for measurement of Public Sector Performance has remained the bone of contention for a long time, mainly due to the fact that the diversity of forms and functions has come in the way of any common solution generally applicable to all cases2. Public Sector Enterprises survey has indicated some criteria of efficiency measurement in Public Sector Enterprises to that of efficiency in Resource Generation and Resource ~tilisations'. The Nun Sen Gupta Committee also ageed to '~huja, N.L., "Working Capital Holding the Promise to Public Sector Enterprises", lndian Management, March 1990,p.9. 'sumit K.Majumdar, "Public, Joint and Private Sector in Indian Industry- Evaluating Relative Performance Differences", Economic and Political Weekly, February 18-25, 1995. p.29. '~overnmentof India, Public Enternrises Survey, 1993-94, Vol.1, p. I0 I.

Transcript of CHAPTER V CHANGES IN MANAGERlAL...

CHAPTER V

CHANGES IN MANAGERlAL PERFORMANCE

Recent years have witnessed an unprecedented emphasis k ing placed

on profitability of' the Public Sector Enterprises while the Government is still

committed to its long standing policy of allowing the Public Sector to achieve

commanding heights in the economy. It has made it abundantly clear that the Public

Sector Enterprises must generate surpluses so that the society could get a

reasonable return on the investment made in these enterprises. Pressure is likely

to mount further on the Public Sector Enterprises to increase their efficiency and

capacity utilisation, reduce costs exercise better control over project expenditure and

take other steps to ensure improvement in Management ~erformance'. Further, the

criteria for measurement of Public Sector Performance has remained the bone of

contention for a long time, mainly due to the fact that the diversity of forms and

functions has come in the way of any common solution generally applicable to all

cases2. Public Sector Enterprises survey has indicated some criteria of efficiency

measurement in Public Sector Enterprises to that of efficiency in Resource

Generation and Resource ~tilisations'. The Nun Sen Gupta Committee also ageed to

'~huja , N.L., "Working Capital Holding the Promise to Public Sector Enterprises", lndian Management, March 1990,p.9.

'sumit K.Majumdar, "Public, Joint and Private Sector in Indian Industry- Evaluating Relative Performance Differences", Economic and Political Weekly, February 18-25, 1995. p.29.

'~overnment of India, Public Enternrises Survey, 1993-94, Vol.1, p. I0 I .

advocate the managerial performance criteria for management efficiency by making use

of working capltal management4.

Therefore, in this current Chapter an attempt is made to analyse in select

Public Sector Enterprises belonging to Heavy and Medium Engineering during 1975-76

and 1995-96. The Managerial Performance of selected Public Sector Enterprises

belonging to Heavy and Medium Engineering is evaluated on ratios based approach

as suggested by the International Labour Organisation (ILO). These ratios are

examined in this section.

Many studies have come out with certain results like profit

requirements, financial resources utilization, physical resources utilization, market

share innovat~on, productivity and quality, human resources, social responsibility

which could be the basis that the Public Sector Enterprises have to undertake to

deliver a specified level of performance (output, profit, growth and so on) in return to

the capital resources mobilised from the Government. It is generally believed that

the effectiveness of Public Sector Enterprises could be in terms of continuing long-term

g~owth of the corporation, contribution to national income and value added.

Further, a general corporate effectiveness is often measured by the surplus generated

and its relati~nsh~p ,U ihz net cap~tal employed in the corporation.

An International Labour Organisation's (ILO's) publication on

improving the Public Sector Enterprises performance has suggested certain broad

indices which can be worked out by constructing certain ratios from the financial

statements are as follows:

' b u n Sen Gupta, committee Remrt, p.75.

(1) General performance indices.

(2) Management performance.

(3) Financial performance.

(4) Investment performance.

(5) Cost break-down (input coefficient and physical performance).

Different ratios suggested for the measurement of the performance under

different categories wuld be examined as follows:

The above said indices have considered for measuring the managerial

performance of selected public sector enterprises belonging to Heavy and Medium

Engineering engaged in the present study. However, due to limitations on different

aspects of the data the study has considered only three aspects, namely, the General

performance, Management performance and Financial performance. The ratios

considered under each category are also limited to the extent of data available in various

financial statements published by Bureau of public Sector Enterprises in their Annual

Surveys. Broadly the indicators considered are as follows:

V.l GENERAL PERFORMANCE

In order to evaluate the General Performance of the selected Public

Sector Enterprises, the study has calculated three ratios as follows:

Operating Profit

Capital Employed

This ratio demonstrates number of times the capital has rooted in the

process of doing business. Also it shows a management's ability to use tirm assets

239

to generate earnings on its invested capital. Further, it measures productivity as well

as profitability. The profit being the result of all operation, the return on capital

expresses all efficiencies or inefficiencies of business collectively and thus is a

dependable measure for judging its overall efficiency or inefficiency. For this

purpose, the amount of operating profit is considered before making deduction on

interest and tax and the capital is the aggregate of all the capital at disposal of the

company.

The second ratio is calculated as

Sales

Capital Employed

This ratlo is likely to throw light on theeffective utilisation of

capital resources employed in generating the annual turnover. Again it indicates the

number of times an asset flows through a firm's operations and into sales

The third ratio is calculated as

Operating Profit

Sales

This ratio helps In determining the eficiency with which affairs of the

business are being managed. An increase in the ratio over the previous period

indicates improvement in the operational efficiency of the business provided the gross

profit ratio is constant. The d o is thus an effective measure to check the profitability

of a business. A constant increase in this ratio year after year is a definite indication of

improving conditions of the business. These ratios are presented in Tables V. 1.1 to

240

V.1.5 for Heavy Engineering enterprises and Tables V.2.1 to V.2.5 for Medium

Engineering enterprises for further analysis.

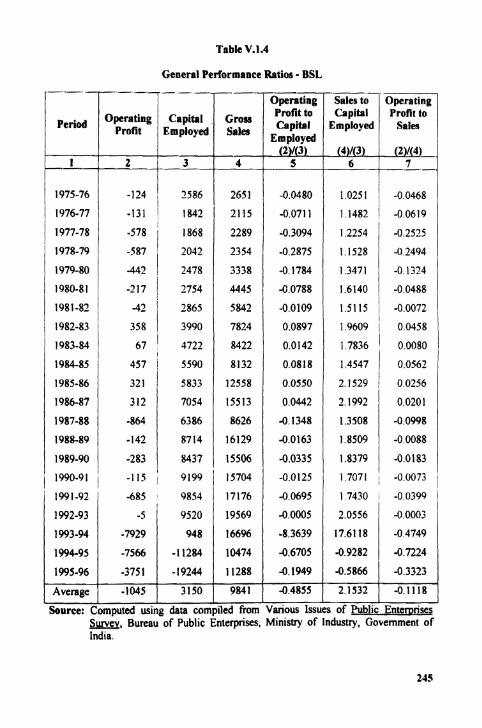

It can be seen from the Tables V. 1.1 to V. 1.5 that the ratio of operating

profit to capital employed of select Public Sector Enterprises belonging to Heavy

Engineering was not uniform during the study period. This ratio fluctuates behveen

0.12 times in the year 1979-80 and 0.33 times in the 1995-96. In HEC, this was

negative in 14 out of 21 years of the study period. This has happened due to

inadequate operating profit in HEC during the reference period. Similar trend was

registered in BSL and JCL during the study period. However, these units have

improved their operating profit during the fourth phase of the study. Next to BHEL, the

Operating Profit to Capital Employed ratio was positive in all the years except in 1978-

79 in case of BHPV during the period of study. It fluctuates between 0.05 times in

the year 1975-76 and 0.37 times in the year 1984-85. Under the unit-wise analysis, the

ratio was nearly consistent in BHEL and BHPV and inconsistent in HEC, BSL and

JCL during the reference period.

From the analysis, it may be inferred that BHEL and BHPV have had

normal operating profit to meet their business obligations during the study period. At

the same time, the ratio was negative in study units, namely, HEC, RSL and JCI.

which reflected poor operational performance of these units during the reference period.

Besides, it can be noticed from the table that operating profit to sales

turnover ratio in BHEL has ranged between 0.24 times in 1975-76 and 0.09 times in

1991-92 during the reference period This may be accounted from Ten rupees as profit

margin for every hundred rupees of sales made in BHEL in the said period. It is quite

surprising to note that similar trend was registered in case of BHPV during the

241

Table V.l.1

General Performance Ratios - BHEL

India

. - .- - - . . - . - -

1975-76

1976-77

1977-78

1978-79

1 1980-81 1 1981-82

1 1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90 1 1990-91 I

1991-92 ,

1 7 3 7 3 ' 86961

17965 1 89962

21398 ) 90867

20948 91772 I

89740

108252

30865 / 120224

31748 ' 171204

132472

153992

177044

199394

231830

270682

300740

323716

1992-93 47961 : 195454 1 1993-94 1 47091 201241

1994-95 46899 181687

1995-96 69525 210676

Average 24418 106521

Source: Computed using data compiled from Various lssues of Public Entemrises m, Bureau of Public Enterprises, Ministry of Industry. Government of

-31600 170065 1 333083

0.2454

0.2340

0.2581

0.3300

0.2142

352528

355368

409418

483346

204006

0.1998

0.1997

0.2355

0.2283

0.2775

0.2506

0.2567

0.2619

0.1858 I

1.9586 ! 00949 '

1.5233 0.1311 !

1.7117 I 1 0,1167 ,

1.8036

1.7659

2.2534

2.2943

1.7604

1.9484

2.1727

2.5834

2.5005

2.5015

0.1360 / 0.1325

0.1146

0.1438

0.1284

0.1209 i

0.1051 / 0.1074

0.1002

2.6708 . 0.0981 ,

Table V.1.2

General Performance Ratios - BEC

I - - -

Operating Profit

Capital Employed

Gross Sales Employed

IWI-92 1 - I Ins2 18222 1 24634 I -0.6065 1 1 3519 ! -0 4486.- ' 1992-93

1993-94

1994-95

1995-96

Average

Source: Computed using data compiled from Various Issues of Public Enternrises Survey, Bureau of Public Enterprises, Ministry of Industry, Government of India.

3.5709

4.3931

-1.6545

-0.8474

1.3750

0.0642

0.0183 1

-0.7352

-0.3567

-0.1990

-2861 ! 12487 I

44590 ' -0.2291

602

-18637

-8895

-269 1

32891

25348

24939

19030

7487

-15321

-29430

13103

0.0804

1.2164

0.3022

0.0039

Table V.1.3

General Performance Ratios - BHPV

Operating Capital Gross I I Profit / Employed ( Bles / --A

Profit to

- 2 3 L

- - .-

Employed

:: 1 I I831 1 28238 I 0.0687 1 2.3868 1 0.0288 1 1995-96 I Average 5775 10911 0.1294 1.6953 0.0764

I 1 .--1 I I I Source: Computed using data comp~led from Various Issues of Public Enternrises

m, Bureau of Public Enterprises, Ministry of Industry, Government of

Table V.1.4

General Performance Ratios - BSL -~=t in~

Profit to capital

Employed (2)/(3)

5

1975-76

1976-77

1977-78

1978-79

1979-80

1980-8 1

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

Sales t o Capital

~mp~oyetj

(4)/(3) 6

---

Profit to S ~ I H

7

I 2586 i -131 1 1842 I

1868

2042

-442 -s87 1 2478

-217 1 2754

4 2 1 2865

358 I 3990

67 ' 4722

457 5590

I 5833

312 3 2 1 j 7054

1990-91 1

2651

2115

2289

2354

3338

4445

5842

7824

8422

8132

12558

15113

8626

16129

15506

-864

-142

-283

m, Bureau of Public Enterprises, Ministry of Industry, Government of India.

-115 1 9199 / 15704

17176

19569

166%

10474

11288

9841

compiled from

6386

8714

8437

6.0480

-0.0711

-0.3094

-0.2875

4.1784

4.0788

-0.0109

0.0897

0.0142

0.0818

0.0550

0.0442

-0.1348

-0.0163

-0.0335

-0.0125

-0.0695

-0.0005

-8.3639

-0.6705

-0.1949

-0.4855

Various Issues

1991-92

1992-93

1993-94

1994-95

1995-96

Average

1.0251 / -0.0168

1 .14821 -0.0619

12254 / -0.2525

I 1528 -0 2494

1.3471 , -0.1324

1 . 6 1 4 0 -00488

1.51 15 -0.0072 I

1.9609 ( 0.0458 ; 1.7836

1.4547 / O.OS62

2.1529 1 0.0256

21992

1.3508

1.8509

1.8379

Surce: Computed using data

/ 1.7071 i -0.0073 1

1 7430 : -0.0399 1 -685 , 9854

-5 1 9520

00201

-0.0998

-0.0088

-0.0183

2.0556

17.61 18

-0.9282

-0.5866

2.1532

-7929

-7566

-3751

-1 045

4.0003

-0.4749

-0.7224

-0.3323

-0.1 118

948

-1 1284

-19244

3150

of Public Enternrises

Table V.1.S

General Performance Ratios - JCL

/ Period Operating Profit

Capital Employed

Gross Salw

- - .- Operating Profit to Capital

Employed (2)/(3)

5

- -. - -

India.

Sales to

1 1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

Operating Capital Profit to

Employed Sales

21 / 5557

187 1 5615

1990-91 1 616 I 8040 00766 I 5437 00496 1 1 I ' 1991-92 ' 123 I 00495 I I I764 , 0 0421

1992-93

5728

6075

6085

6392

7869

9261

12626

202

326

340

555

654

5785

6339

6491

7009

8013

1993-94

1994-95

1995-96

Average

00038

00333

0 0349

00514

0 0524

0 0792

00816

Source: Computed using data comp~led from Vanous Issues of Publ~c Entemnses m, Bureau of Publrc Enterprises, M~n~stry of Industry. Government of

6316

5068

8130

6497

-9796

-2055

-2936

-571

1 0308

10819

1 05 19

1 0084

l 2123

1 3213

15757

3 2939

02475

02067

0 1953

-2974

-8303

-14205

3972

00037 1

0 0332 , 00510 1 0 0432 I 0 0599

00518

-2 1237

-06104 1

-0 5723

0 7301

-1 5510

-04055

-0 3611

4 I005

period of study. A further examination of the Table reveals the operating profit to sales

turnover ratio showed negative trend in the case of HEC, BSL and JCL during the

reference period. It may be noticed from the foregoing analysis that these units have

no sufficient sales in resultant which affected profitability of these sample units during

the study period. Hence, BHEL and BHPV are progressing in the right direction

while comparing to other sample units during the reference period.

As such, a further investigation about the trend of say& should be

carried for the better operating profit margin position of these sample units. For this

purpose operating profit to sales turnover ratio is employed. This ratio varied from 0.24

times in 1975-76 to 0.094 times in 1991-92 in case of BHEL. However, this ratio was

negative in 17 years out of 21 years of the study in case of HEC. Similar trend was

registered in BSL and JCL. It indicates that the sales was inadequate in these units

during the period of the study. But, at the same time, the ratio was positive in all the

years except in 1993-94 and 1994-95 during the study period.

It can be concluded from the foregoing analysis that General

performance was not satisfactory in all sample units belonging to Heavy Engineering

Enterprises during the study period. However, among the sample units, BHEL and

RHPV have had satisfactory performance as compared to other study un~ts during the

reference period.

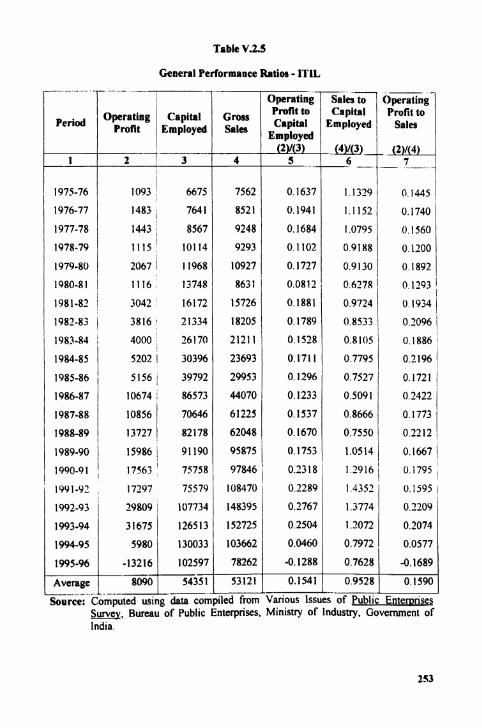

The General performance ratios of select sample units belonging to

Medium Engineering Enterprises have been presented in Tables from V.2.1 to V.2.5. It

can be seen from the tables that The operating profit to Capital employed ratio was less

than one time in BEL during the study period. But, this ratio turned as negative for 4

years in BDL, 2 years in HMT, and one year each in HCL and ITIL respectively over

247

the 21 years of the study period. It shows that BEL has earned profit continuously as

compared to other sample units during the reference period.

In the unitwise analysis, HCL and ITlL have had operating surplus in all

years except in 1995-96 during the reference pericd. In case of BDL, the operating

profit was meagre during the first phase and it incurred loss during the second phase of

the study period. However, BDL has been improved its operating profit in the

subsequent phases of the study. This might have occurred due to the influence and

attitudes of the Government towards Public Sector Enterprises since the

introduction of liberalisation policies. Further, it can be found out from the Table that

Operating profit was positive in HMT except in the years 1993-94 and 1994-95 during

the study period.

While the examination of the tables that provided sales to capital

employed ratlo was more than one time in case of BEL, HMT and HCL during the

reference period. It indicates that capital has been utilised prudently for generating

adequate sales in the respective sample units during the study period. The analysis

further substantiates that there was fluctuation on ratio in BDL and ITIL over the period

of the study.

It emphasises that sales was inconsistent in BDL and ITIL during swdy

period which m~ght have happened on account of poor management and changing

policies of the government.

On careful examination of the data available in the tables, the operating

surplus to sales ratio was similar as operating profit to capital employed ratio during

the study period. The ratio indcates that profit margin was meagre in all sample units

Table V.2.1

General Performance Ratios - BEL,

I"- Operating Sales to Operating Profit to Capital Profit to Operating Clpibl Employed &Ies Sales Eeployd (2)/(3) (4)/(3)- , - -(2)/(4)

5 -.G - 7

I

I

Average 1 5081 1 24032 / 38886 i 0.2214 1 1 . 4 5 1 6 1 0 1 6 2 0 I I I I I I

Source: Computed using data compiled from Various Issues of Public Enternrises m, Bureau of Public Enterprises, Ministry of Industry, Government of India.

Table V.2.2

General Performance Ratios - BDI,

India

1975-76 10 I 330 I I3

405

471

692

550

228

483

324

355

146

684

3362

3445

4264

5240

8930

110258

392

464

502

1976-77 1

0 2572

0 0836

01590 \ 0 1414 / 01469 I

-00176

Enterunses

I 00303 / 1 2273 I 00247 ,

1977-78

1978-79

m, Bureau of Publlc Enterprises, Ministry of Industry, Government of

146

93

1979-80

I

00276

02110

0 1691 1

0 2193

-0 1781

-0 3364

-0 8169

-1 8288

0 2222

0 2403

01974

0 1522 I

0 0950

0 2885

( 01543

538

00332 / 12015

Source: Computed usmy data compiled from Vanous lssues of Publ~c

0 1300

00440

00985

0 1698

01910

-00536 1 2

1991-92 I 3234

03147

0 1853

0 0929

-0 1972

0 5054

0 5271

06194

12011

13001

10056

24885

21296

20124

14982

15627

7366

1992-93

1993-94

1994-95

1995-96

Average

14914

10956

0 4238

1 1078 1980-81 ' -86 I 436 I

1981-82 1 -109 j 617

1982-83 1 -290 ' 626

12576

11226

12465

17995

20317

5448

938

1982

2544

2984

866

1983-84

1984-85

1985-86

1986-87

1987-88

I -0 1767 I 0 5251

-04633

-3 1412

0 2349

0 5747

03164

0 1316

00576

-267 85

647

808 I S 2 1406

0 5671

17176

1 0572

2 3912

16031

0 8644

0 6060

680

649 I 1988-89

0 1727 1 0 5986

1 00751 1 04868

2149

4933

8647

1989-90 / 2 1 14918 I

1990-91 / 1583 1 21074

Table V.23

General Performance Ratios - AMTL

Period Operating Capital 1 r o t 1 Employ4

1995-96 46143

Average 34080 - Source: Computed using data con m. Bureau of Public

India.

. Operating Sales . . . to Operating

Grosls Profit to Capital Profit to Capital Employed Sales

Elnoloved

-J d a r i o u s lssues of Publii Enternrises nterprises, Ministry of Industry, Government of

General Performance Ratios - HCL

- 3 1 3 2 0 0 5 9 0.5010 -0.01171 1 5 - 9 6

Average 2375 21335 24669 0.1348 1.2066 0.1072 -2-

Source: Computed using data compiled from Various Issues of Public Enternrises m, Bureau of Public Enterprises, Ministry of Industry, Government of India.

Table V.2.5

General Performance Ratios - lTIL

Period Operating Capital 1 1 ..rn Employed 1 Gross Sales

o p e r a t i n g r - i i l (lag- 1 Profit to Capital Profit to Capital Employed Sales

Emoloved

1992-93 29809 107734 148395 0 2767 13774 0 2209

1993-94 31675 1 126513 152725 0 2504 l 7072 0 2074

1994-95 130033 103662 00460 0.7972 0 0577

1995-96 -0.1288 0 7628 -0 1689

54351 53121 Average 0.1541 09528 01590 - --

Source: Computed using data complled from Vanous Issues of Publlc Entemnses m, Bureau of Publ~c Enterprises, Mln1stl-y of Industry, Government of lnd~a

during the initial years of the study but it found negative during the second phase in

BDL, fourth phase in HMT, HCL and ITIL respectively over the period of study.

However, it is worth mentioning that the ratio of BEL was positive and

consistent in all the years and on an average was 22 per cent during the period of study.

Hence, BEL is placed in a better position than other units like BDL, HCL, HMT and

ITIL during the reference period.

From the foregoing exposition, it can therefore be concluded that the

analysis of general performance of ratios was setisfactory in BEL during the study

period among the selected units of Medium Engineering Enterprises.

V.2 MANAGEMENT PERFORMANCE RATIOS

Management performance of select Public Sector Enterprises

belongng to Heavy and Med~um Engineering has been evaluated through ratios as

identified by International Labour Organisation (ILO). The computation of

Management ratios and their significance are given in the following paragraphs.

hdcx Index Measures

Operating Surplus -------*--------.

Total Assets

Cost of Sales

Stock

Gross Value Added ....................... Fixed Assets

Gross Value Added

Total Assets

Gross Value Added ------------*----------

Labour Cost

Sales -----*---------

Labour Cost

Fixed Assets

Labour Cost

Pre Tax Surplus ------------------- Labour Cost

Sales Less Material ---- Total Wages and Salaries

It is calculated to know the productivity of the total assets that are available to management.

This ratio is deemed to reflect the efficiency of lnventory Management. It further explains whether investment in inventories is within proper limit or not. Usually inventory should not exceed 2 4 months consumption of the year.

This ratio is calculated to measure the productivity of capital in terms of gross value added. Also it indicates nature of capital intensive in an organisation.

It is computed to measure the productivity of total assets in generating value added.

It is a measure of productivity of labour in generating d u e added.

This ratio is calculated to measure the labour productivity per employee in terms in sales.

This ratio indicates the relationship between Fixed Assets and Labour Cost. It also explains whether capital is intensive or not.

This ratio is computed to know the proportion between profit and Labour Cost. Further, it explains profit per employee dunng operating of an organisation.

This ratio is computed to know the value added per every hundred ruptes wages and salaries paid

The Management Perfonname ratios of select Public Sector Enterprises

belonging to Heavy Engineering are presented in Tables V.3.l to V.3.5.

It can be seen from the tables that the Operating Surplus to Total Assets

ratio of BHEL has shown fluctuating trend between 24 per cent in 1975-76 and 7 per

cent in 1994-95. This ratio was negative in many years in HEC, BSL and JCL during

the study period. However, this ratio was positive in all the years except in the year

1978-79 in case of BHPV and on an average of this ratio was 5 per cent during the

study period. The analysis shows that Operating profit to Total Asset ratio of BHEL is

better than that of HEC, BSL, BHPV and JCL.

From Table V.3.1, it is evident that the cost of sales to stock tumover

ratio in BHEL was significant which had been fluctuating between 8.37 times in 1975-

76 and 1.05 times In 1987-88. Over the period, it also evidences decreasing trend.

On an average, the ratio has turned over 2.44 times during the period. This shows that

sufficient and satisfactory business activities in BHEL during the study period.

In HEC also the cost of sales to stock turnover ratio is fluctuating

between 0.51 time in 1976-77 and 2.56 times in 1995-96. On an average this ratio has a

turnover of 1.10 times duriitg this period of study. This ratio is less than that of BHEL.

Evidently, similar trend was registered in case of BHPV, BSL and JCL

and on an average this ratio was 1.89 times, 3.09 times and 1.78 times of the

res-ve units during the study period. From this analysis, it may be inferred that

the movement of inventories was fast in BHEL while comparing to other study units

during the study period.

The data available from the tables, it is evident that the Gross Value

Added to Fixed Assets ratio was consistent in B m L but it was inconsistent in other

256

sample units during the study period On an average, this was 2.15 times in BHEL,

0.34 times in HEC, 0.97 times in BHPV, 0.95 times in BSL and 0.71 times in JCL

respectively during the study period. This indicates that the Fixed Assets have been

utilised satisfactorily for building up Gross Value Added in BHEL while comparing to

other sample units belonging to Heavy Engineering group. Next to BHEL, BHPV's

position was good during reference pmod.

Further, as exhibited in tables, Gross Value Added to Total Fixed Assets

ratios of sample units were fluctuating during the study period. On an average the

ratio was 0.51 times in BHEL, 0.18 times in HEC, 0.28 times in BHPV, 0.32 times in

BSL and 0.24 times in JCL during the reference period. This indicates that the Gross

Value Added has been showing real growth by proper utilisation of Total Assets only

upto 199 1-92 in all study units except in BHPV. As it is apparent that even when there

occurred positive real growth in 1990s, it was much lower than in 1980s, thus revealing

an investment slowdown in study units during liberalisation. However, 1994-95 and

1995-96 witnessed a positive real growth of Value Added as during 1980s in case of

BHPV during the reference period. This study results is coincided with the result of

Romeshan's study on Public Sector Enterprises through reforms?

Tables reveal the ratio of Gross Value Added to Labour Cost to its

utilisation as assuming one of the indicators to measure the performance of the study

units. It can be found out from the tables that the ratio was more consistent and more

than 2 times over the study period in case of BHEL and BHPV. At the same time, the

ratio was more than one from 1975-76 t~ 1993-94 but it declined to less than during

1994-95 and 1995-96 in the study units, namely, HEC,BSL and JCL during the reference

hmeshan, P., "Public ~nterprises Through Reforms - A Financial Ratios Analysis", Pmductivity, Vo1.38, No.2, July-September 1997, pp.264-275.

period This reflects that the Labour productivity is good in terms of Value Added in

the sample units like BHEL and BHPV. However, Labour productivity is satisfactory

in relation to Value Added in case of HEC, BSL and JCL.

As regards to Sales to Labour Cost ratio, it is found to be fluctuated in

all study units during the reference period. On an average of the ratio is 6.94 times in

BHEL, 3.1 1 times in HEC, 6.94 times in BHPV, 2.76 times in BSL and 2.99 times in

JCL during the study period. It states that the Labour Productivity is highly intensive in

terms of Sales in BHEL and BHPV as compared to other units over the period of the

study.

It is evident from the Table V.3.1, which depicts that Fixed Assets to

Labour Cost ratio has ranged between 0.85 times in 1982-83 and 1.79 times 1995-96 in

BHEL. This ratio has been varied in year after year in the sample units and on an

average of this ratio was 5.23 times in HEC (Table V.3.2), 3.82 times in BHPV (Table

V.3.3). 1.86 times in BSL (Table V.3.4) and 1.83 times in JCL (Table V.3.5) during the

study period. It indicates that the fixed assets to Labour Cost ratio is similar as to the

Total Asset to Labour Cost ratio, while the rste of Productivity was relatively small.

Interpreting this ratio, the Productivity of the invested Fixed Asset of the sample units

has come down year after year even during 1990 and some symptoms of

improvements appeared during the fourth phase in BHEL and HEC during the period

under study.

It can also be observed from the tables that Pretax Surplus to Labour

Cost ratio is not quite satisfactory in all study units. However, this ratio was

positive and consistent in case of BHEL but it was negative for many years in HEC,

BSL and JCL during the study period. In BHPV, this ratio was positive in all the years

of the study except 1978-79. It represents that the growth rate of the Pre-tax Profit in

258

terms of Labour Cost of the BHEL and BHPV is successively higher since 1991-92. It

reached a magnificent level in 1994-95 and 1995-96. But this ratio can be found an

uninspiring one since '991-92 in case of WC, BSL and JCL during the study period.

This might had happened on account of economic liberalisation and Public Sector

Enterprises reforms.

Finally, Sales Less Material Cost to Labour Cost ratio indicates that

the ratio 'nas been widely fluctuating in BHEL and BHPV but it mildly varied year

after year in case of HEC, BSL and JCL over the period of the study. On an average,

this ratio was 2.18 times in BHEL, 1.34 times in HEC, 1.22 times in BHPV, 1.64 times

in BSL and 1.30 times in JCL during the study period Looking at the analysis, it may

be inferred that the Labour Productivity in terns of Sales i s highly intensive in BHEL

and BHPV as compared to other study units during the period under study. However,

Sales in proportion to Employees shows higher ratio in the initial years of the study

and did not rise even under the liberalised conditions of the 1990s. Rather, it declined

noticeably during this period. As a matter of fact, the raw-material was also

proportionately stable during this period This stagnation has occurred in the study

units during 1990s due to the influence of Public Sector refonns and economic

liberalisation pursued by the Government.

From the foregoing analysis, the management performance of select

Public Sector Enterpnises belonging to Heavy Engineering was measured through

different ratios. The analysis revealed that the positive changes and noticeable in

sample uaib like BHEL and BHPV in this study. Hence, it can be concluded that

management performance of BHEL and &V wa.. comparatively good among the

sample units over the period of the study.

Tab

le V

.3.2

Man

agem

ent P

erfo

rman

ce R

atio

s -

HE

C

Per

iod

opm

fjw

Su

rplu

s to

T

otal

h

se

h

0.0426

0.0490

-0.0578

-0.03 10

-0.0480

' -0.0889

-0.1049

4.0914

-0 0798

-0.0492

-0 0068

0.1011

0.0575

1

-0.0131

i -0.0817

-0.1657

-0.051 5

OOlll

1 -0

.406

7

Co

st o

f S

ale

to

Sto

ck

-0.1973

1- 2.5641

-0.0598

i 1.1017

Sou

rce:

Bureau of Public E

nter

pris

es,

Fix

ed

To

tal

-E+w

lic

Ent

eror

ises S

urve

y, M

ini

Gro

ss

Add

ed t

o L

abo

ur

Labour

Cost

2.6356

2.4%8

0.8470

1 2.5341

1 3.1057

1.5885

1 3.1178

1 5.2330

ry of

Indu

stry

, Gov

ernm

ent o

f Ind

ia, New

Pre

Tax

S

urp

lm to

L

ab

ou

r C

ost

Del

hi Vol. I

.

Tab

le V

.33

Man

agem

ent P

erfo

rman

ce R

atio

s - BH

PV

1995-96

1 0.0209

j .- 3.3720

Ave

rage

1

0.M63

1 1.8948

So

um

: Bureau of Public E

nter

pris

es, P

Gro

ss

Val

ue

Flrc

d V

alue

Sa

les

to

to

, A

dded

to

; L

abou

r , L

abou

r ~

ixe

d

TOW

I i

Lab

our

i c

os

t !

- .

--

~

..

-

1.7045

1 0.3072 1

2.8059

1 6.4140

1 1.

6461

0.9708

1 0.2799

1 3.1635

1 6.9402 i

3.8257

lic

Ent

aori

ses S

UIV y, M

inis

try

of Indusuy, G

over

nmen

t of

Indi

a, N

ew

Prr

Tax

S

urp

lus

to

Lab

our

Cost

0.0434

The Management Performance ratios of select Public Sector Enterpriws

belonging to Medium Engineering are given in Tables V.4.1 to V.4.5 for further

examination.

The data presented in the tables provide that Operating Surplus to Total

Asset ratio is varied between 0.25 times in 1981-82 and 0.05 times in 1995-96.

However, it is positive throughout the study period. But, at the same time, the ratio

was negative for three years in BDL, for two years in HMT' and one year in HCL and

ITI1, respectively during the study period. It indicates that the sample units have not

generated adequate Operating Profit by using their Total Assets available during the

study pericd. Further, it reflects that the Productivity is not commendable in the study

units during the reference period. On the other hand, the ratio was positive and showed

improvement during 1990s in BEL while comparing to other study units during the

reference period.

It is evident from the Table V.4.1 that the Cost of Sales to Stock

Turnover ratio in BEL has shown raising trend from 0.60 times in 1975-76 to 2.37

times in 1995-96. It implies good inventory management and sufficient business

activities d:!ring thc study period.

It is sign~ficant to note that this has been fluctuating widely in other

study units, namely, BDL (Table V.4.2), HMT (Table V.4.3), HCL (Table V.4.4) and

ITIL (Table V.4.5) during the reference period. On an average of the ratio was 1.40

times in BDL, 1.88 times in HMT, 2.69 times in HCL and 1.65 times in ITIL during

the period of study. This explains that the inventory management was sat~sfactory

in all study units. At the same time, higher ratio in HCL reflects effic~ent business

activities during the study period. A low ratio is noticed in BDL which is an Indicator

265

of excessive inventory and over investment in inventory during the reference period.

Hence, the inventory management was good in BEL and HCL as compared to other

units during the period under study.

The tables also show the Gross Value Added to Fixed Asset ratio for

select sample units belonging to Medium Engineering enterprises. Considering

the relationship between Gross Value Added and Fixed Assets in each year, as a

specific lcvel of operation of the study units, reveals that thc ratici was positi\,e and

consistent in HEL and HMT during the study period. In BDL, this ratio was negative

during 1984-85 but there was an improvement during 1990s. It implies that Gross

Value Added has not been built adequately by employing Fixed Assets in the study

units. Further. it can be seen from the data presented in the Table that an average of the

ratio was 0.44 times in HCL and 0.96 times ITlL during the study period. From the

analysis, it is noticed that the ratio was less than one in most of the years of the

sample unlts. It ~nd~cates the excessive investment on Fixed Assets in the study units

and they do not build up Gross Value Added proportionately during the study period.

Evidently, similar trend was found on Gross Value Added to Total Asset

Ratio of all sample units during the study period. It is necessary to note that this ratio

i s less than one in all select units during the reference pcriod This indicates that

Total Assets were excessive in all samplc units and they did not build adequate Value

Added in sample units over the period of the study. Hence, the Productivity is low in

study units. However, performance was satisfactory dunng 1980s in all sample units

while comparing their performance during 1990s. Moreover, economic

liberalisat~on and Public Sector refoms do not influence on performance to these

units during the study period.

It can be observed from the tables that Gross Value Added to Labour Cost

ratio has been fluctuated in all study units. This ratio is calculated to measure the

Labour Productivity of the sample units. On an average the ratio was 2.25 times in

BEL, 1.83 times in BDL, 2.21 times in HMT, 4.75 times in HCL and 2.29 times in ITIL

during the study period. It implies that the Labour Productivity is high in HCL among

the study units during the study period.

I t is seen from the tables that the Sales to Labour Cost ratlo is found to

be fluctuating substantially over the various phases of the study in all sample units.

This ratio establishes the relationship between Sales and Labour Cost. Also, it measures

the Labour Productivity of a firm in terms of Sales hence it is useful to judge the

performance of Management. On an average the ratio was 4.20, 4.59,4.44, 12.56, 3.16

ilmes In BEL. (Table V.4.11, RDL (Table V.4.2). HMT (Table V.4.3). HCI, (Table

V.4.4) and ITII. (Table V.4.5) respectively during the study period. This indicates

that the Labour Product~vity is very intensive in terms of Sales in HCL among the study

units during the reference period. However, it is noticed that the Labour Productivity

IS at the appreciable level in other study units over the period of the stud!

The tables also present the Fixed Assets to 1.abour Cost ratio of the

sample units during the study period. It may be noted that this ratio found to be

fluctuated in sample units like BEL, BDL and HCL over the period of the study. At

the same time, the ratio declined from 5.75 times in 1975-76 to 1.59 times In 1995-96

in case of HMT. It is quite contrast to other sample units, the ratio of ITIL has raised

from 1.13 times in 1975-76 to 2.63 times in 199: -96 during tlie reference period.

However, the average of this ratio for the sample units over their period of 21 years of

the study was 3.23 times in BEL 5.84 times in BDL, 3.19 times in HMT, 8.33 times

in HCL and 5.52 times in ITJL respectively during the study period It indicates that

the Labour Productivity was high in HCL which reflected heavy investment made on

Fixed Assets during the reference period. Over the period of the study, the Labour

Productivity in terms of Fixed Assets was relatively good in the sample units,

namely, BEL, BDL and HMT. Further, the low ratio of ITIL indicates that higher

Labow Cost involved in operation due to surplus employees in the study unit. From

the foregoing analysis, it can be concluded that the Labour Productivity in terms of

Fixed Assets was good in BEL, BDL and HMT during the study period.

It can be seen from the tables that the ratio of Operating Profit to

Employees has shown improvement fiom 0.05 times in 1975-76 to 0.72 times in 1993-

94 in BEL but it declined during the years 1994-95 and 1995-96. Looking at the data

available in the Table, it may be noted that in BDL the ratio was insignificant during the

late 1970s but it turned as negative in early 1980s. Subsequently, the ratio has shown

in raising trend during 1990s in the study unit.

In HMT, the ratio varied between 0.06 times in 1975-76 and 0.25

times in 1992-93. AAenvards it tumednegative during the years 1993-94 and 1994-

95 over the period of the study. It is necessary to note that t h~s ratio was positive in

HCL during the entire period of study except in the year 1995-96. The same trend was

in case of ITlL during the study period. From the above given exposition, it may

be i n f t r d that the Operating Profit to Employees ratio was positive only in BEL for

the entire period of the study. Hence, BEL has earned profit adequately over the

period of the study as compared to other sample units.

From the data available in Tables V.4.1 to V.4.5, it demonstmtes

that Sales minus Material Cost to Labour Cost ratio has been fluctuating in all sample

units during the period of the study. However, the ratio was sigaificant snd positive

during 1990s in all sample units except in BDL. It explains the Labour Productivity in

terms of Sales is good in all sample units except BDL during 1990s of this study.

On an average, the ratio was 2.20 times in BEL, 1.71 times in BDL,

2.05 times in HMT, 5.23 times in HCL and 2.35 times in TTIL during the period the

study. This indicate that the Labour Productivity in terms of Net Sales is more

intensive in HCL and ITIL among the study units over the period of the study. At the

same time, BDL has no adequate Sales during 1979-80 and 1984-8s hence this unit is

not having consistent Sales during the reference period.

From the foregoing analysis, the Management Performance of select

Public Sector Enterprises belonging to Medium Engineering was evaluated through

various ratios as suggested by the International Labour Organisation (LO). The

results of various ratios pertaining to sample units, disclose that all the ratios are

mostly favourable to the only sample unit namely BEL during the study. Next to the

BEL, the results are good to HCL during the reference period Therefore, it can be

concluded that the Management Performance of BEL and HEC was comparatively good

among the sample units during the reference period.

Further, the Management Performance of select Heavy Engineering

units compared against the performance of select Medium Engineering units during the

study period. The results of the study reveals that the performance of Medium

Engineering units was better than that of Heavy Engineering units over the period of

2 1 years of the study.

Tab

le V

.4.1

Mrn

agem

ent

Per

form

ance

Rat

ios - B

EL

Per

iod

1975

-76

1976

-77

1977

-78

1978

-79

1979

-80

1980

-81

3981

-82

1982

-83

1983

-84

1984

-85

1985

-86

1986

-87

1987

-88

1988

-89

1989

-90

1990

-91

1991

-92

1992

-93

1993

-94

Ope

mtln

g 1

Surp

ler

to

/ T

otal

I

Asa

ets

0.08

42

0.09

75

0.07

13

0.06

91

' 0.

2570

0.

1287

0.

1092

.

0.09

60

0.06

39

0.07

63

I

0.06

41

0.08

50

0.11

13

0.09

44

0.09

68

Add

ed to

0.73

06

0.71

65

0.72

38

0.65

34

0.50

46

0.96

%

1.04

84

1.01

85

0.89

78

0.71

83

0.67

40

0.65

6 1

0.62

73

0.68

92

0.64

78

0.62

52

0.66

84

0.64

43

Gro

ss

Val

ue

Add

ed t

o T

otal

A

sset

a 0.

3003

0.

3007

0.

2868

0.

3066

0.

26%

0.

1%2

0.39

90

0.44

62

0.36

35

0.35

74

0.32

98

0.27

72

0.25

08

0.23

43

0.24

17

0.27

45

0.27

64

0.25

90

0.24

84

--

Gm

r

Val

ue

Add

ed t

o L

abou

r C

ost

2.

7386

2.

5662

2.

2Oll

f ,

9357

1.

8058

1.

6770

2.

6019

2.

5889

2.

4988

1.

4942

2.

4704

2.

5950

2.

6586

2.

2845

2.

4833

2.

43 1

4 2.

2237

2.

2503

2.

3850

Sal

es to

L

abou

r C

ost

4.23

98

4.15

23

3.93

65

3.29

29

3.40

37

3.10

83

4.11

01

3.70

04

3.27

78

3.48

75

3.73

08

4.46

76

5.07

41

4.97

52

5.45

83

5.77

80

5.42

68

4.90

90

5.41

51

... . ..

-. -

~

I -~

-

..

-

..

1995

-96

1 0.

0467

1

2.37

18

1 0.

6818

1

0.29

78

1 1.

7165

1

4.09

72

! 2.

5177

1

0.3%

3 1

1.88

73

Avc

m t

0.09

02

1.23

70

0.72

43

0.29

44

2.25

41

4.29

93

3.23

47

0.27

64

2.20

32

Sau

negB

ur!a

u of

Pub

lic E

lit~

rise

s, PU

bL E

ntem

rise

/Sur

rcr,

~

iniJ

Ly

of

tmiu

stry

! ~o

vm

en

t

bfh

dia

, N

ew Li VO

I. I

Tab

le V.4.5

Man

agem

ent

Per

form

ance

Rat

ios - IT

lL

Gro

ss

Cro

ss

i G

ross

V

alue

v

alu

e v

alu

e A

dded

lo

Add

ed t

o I

Add

ed t

o 1

i Tota

l I

Lab

our

Per

iod

opc=

tin

g S

urp

lm to

'O

ut of

T

otnl

S

ales

to

Ass

ets

Stoc

k 1

Ass

ets

1 A

sset

s 1.

5466

!

0.43

66

1.43

%

1 0.

4504

1995

-96

1 -0

.082

9 /

2.19

77

1 0.

3722

[

0.16

29

1 0.

9790

1

2.95

18

1 2.

6303

1

-0.5

979

Ave

rage

1

0.09

28

1 1.

6543

1

0.95

62

j 0.

3215

1

2.29

18

1 4

.20

Wi

2.52

11

( 0.

2611

S

oure

e: Bureau

of P

ublic

Ent

erpr

ises

, Pub

lic E

nter

nris

es S

urve

y, M

inis

try

of I

ndus

try,

Gov

enun

ent o

f In

dia,

New D

elhi

, Vol

. 1.

to

Lab

our

Cos

t 1.

7534

1.

8877

s.kr

Le3

s M

ater

id to

To

w

Wag

es &

S

alar

ies

2.01

53

2.01

12

Fix

ed

Ass

ets

to

Lab

our

Pre

Tax

Su

rplu

s to

L

abo

ur

Cos

t I

Cos

t C

ost

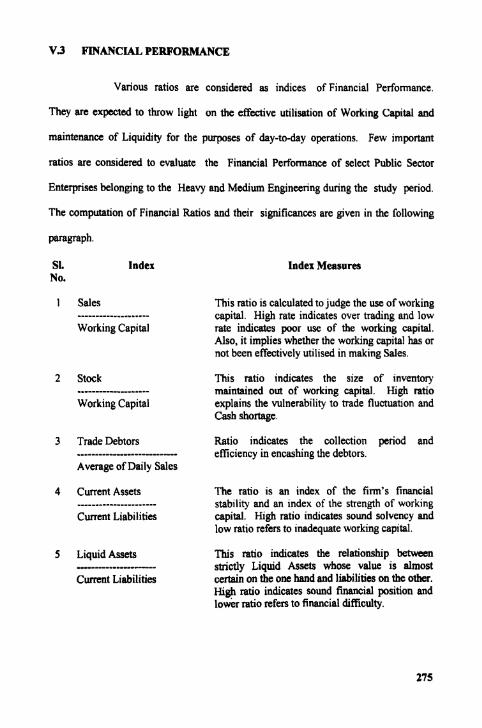

V.3 FINANCIAL PERFORMANCE

Various ratios are considered as indices of Financial Performance.

They are expected to throw light on the effective utilisation of Working Capital and

maintenance of Liquidity for the purposes of day-to-day operations. Few important

ratios are considered to evaluate the Financial Performance of select Public Sector

Enterprises belonging to the Heavy and Medium Engineering during the study period.

The computation of Financial Ratios and their significances are given in the following

SI. Index No.

Lndex Measures

1 Sales This ratio is calculated to judge the use of working capital. High rate indicates over trading and low

Working Capital rate indicates poor use of the working capital. Also, it implies whether the working capital has or not been effectively utilised in making Sales.

2 Stock .................... Working Capital

3 Trade Debtors

Average of Daily Sales

4 Current Assets -------------------*--

Current Liabilities

5 Liquid Assets -------------------- Current Liabilities

This ratio indicates the size of inventory maintained out of working capital. High ratio explains the vulnerability to trade fluctuation and Cash shortage.

Ratio indicates the collection period and efficiency in encashing the debtors.

The ratio is an index of the firm's financial stability and an index of the strength of working capital. High ratio indicates sound solvency and low ratio refers to inadequate working capital.

This ratio indicates the relationship between strictly Liquid Assets whose value is almost certain on the one hand and liabilities on the other. High ratio indicates sound financial position and lo& ratio refers to financial diWculty.

6 Contribution --

Operating Profit

7 Long Term loan ---------------------------**

Paid up Capital, Reserve And Long Term loan

8 Fixed Assets -------------------- Capital Employed

9 Inventory

Average Weekly Sales

10 Sales

Capital Employed

11 Gross Profit

Sales

12 Pre-tax Surplus ----------------- Sales

This ratio implies relationship between contribution and operating profit and also it indirectly refers to the relation between Operating Profit and Sales.

It indicates the level of business finance excessive reliance on borrowing money.

This ratio indicates the proportion of Total Finance available invested in Fixed Assets.

The ratio demonstrates the velocity of Inventory Turnover in an organisation.

This ratio indicates the number of times the Capital has been rotated in the process of doing business.

This is Profitability ratio which indicates the efficiency of the production.

This ratio implies the Operating Profit Margin on Sales.

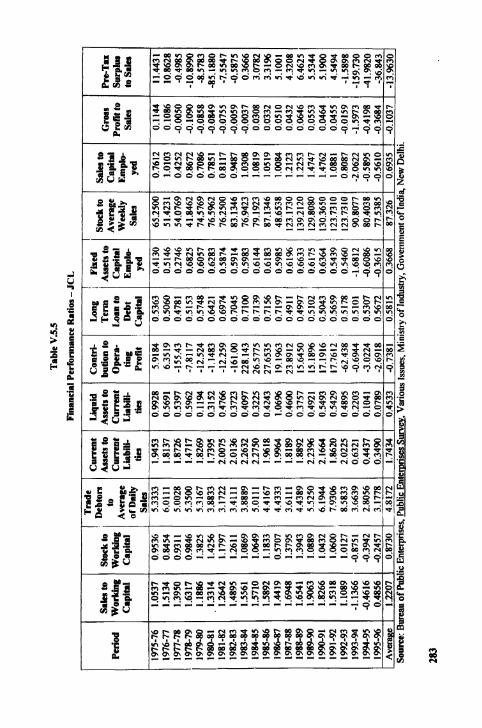

Financial ratios of select sample units belonging to the Heavy

Engineering Enterprises have been presented in Tables from V.5.1 to V.5.5 for

further examination and interpretation.

It can be seen From the tables that the Turnover ratios represented

positive trcnd in sample units, namely, BHEL (Table V.5.1) and BIIPV (Table V.5.3)

but negative trend was found in some of the years in case of HEC (Table V.S.2), BSL

(Table V.5.4) and JCL (Table V.5.5) during the study period. It implies that the sales

t~end was relatively satisfactory in BHEL and BHPV than other sample units during the

276

study period. From the above analysis, it is be infemd that the Working Capital

rquirernents could be met from sale proceeds in the sample units like BHEL and

BHPV while comparing to other sample units during the reference period.

It is shown in tables that trade debtors ratio of BHEL has registered

upward trend tremendously from 25.98 times in 1975-76 to 822.82 times in 1995-96.

The similar trend was recorded in BHPV during the reference period. It can be said that

these sample units have taken more time for collecting dues from debtors which results

to meet Working Capital requirements from short-term borrowings. Tables further

show that this ratio was low and fluctuated during the initial years but it improved

steadily in case of HEC. While this ratio was insignificant in BSL and JCL due to

inadequate sales during the period of study. Hence the liquidity of these units were

affected and the Working Capital requirements could be met from external resources.

The data assembled in tables relate to the current ratio of sample units

during the study period. On an average, the ratio was 1.39 times in BHEL, 1.26 times in

HEC, 1.44 times in BHPV, 1.74 times in BSL and 1.74 times in JCL during the reference

period. Looking at the current ratio of sample units, it may be observed that all units

had satisfactory ratio during the study period Comparison of this ratio against the

Turnover ratios of the respective sample units revealed that there was correlation

between Turnover ratios and Current ratios in the case of BHEL and B W V but no

correlation in other sample units. As such, it can be said that sample units such as

HEC. BSL and JCL depended more on short-term borrowings for Working Capital

requirement than on Sales proceeds during the study period.

Further, it can be seen from the tables that the Quick Asset ratio (Acid

Test Ratio) was less than one time in all sample units. It can, therefore, be stated that

no sample urit could be maintained suitable proportion of Liquid Assets against

Current Liabilities as suggested by Tandon committee6.

The tables also present information about various financial ratios of the

sample units. The contribution to Operating Profit ratio was consistent and positive

only in BHEL, however, it was negative in most of the years in other sample units

during the study period. It reflects that BHEL alone had sufficient sales to meet its

financial commitments during the study period.

Again, it can be noticed from the tables that the Fixed Assets to Capital

Employed ratios reported positive trend in all sample units. However, it showed

negative trend dwing the year 1994-95 and 1995-96 in HEC, BSL and JCL. On an

average, the ratio was 0.87 times in BHEL, 1.56 times in HEC, 0.80 times in BHPV,

1.12 times in BSL and 0.36 times in JCL during the study period. It implies that

sample units had generated additional assets by employing capital in business

operation during the study period. As far as unit-wise analysis, it was more

consistent and satisfactory for asset creation in BHEL and BHPV than that of other

sample units during the reference period.

Significantly, it can be seen From the tables that Gross Rofit ratios of

sample units revealed profitability trend during the study period. Under unit-wise

analysis, on an average of this ratio was 13 per cent in case of BHEL during the study

period. Next to BHEL, in BHPV the ratio was positive in all the years except 1978-79

and it was meagre to the extent of 7 per cent during the r e f e m period. Moreover,

-

vandon Committee Reuort, 1975, p. 135.

278

Tab

le V

.S.1

Fin

anci

al P

erfo

rman

ce R

ah

- BH

EL

sale

at0

wor

king

C

apih

l

1.08

32

2.18

49

2.45

58

2.60

%

2.12

65

2.08

1 1

. 2.0

410

2.11

70

2 .m

3.

7481

4.

2678

5.

0791

6.

5086

4.

5004

3.

9724

4.

1634

2.

5335

2.

2346

2.

2968

Liq

uM

Ass

ets

to

Cu

nm

t L

hbit

i-

ties

0.09

1 1

0.11

95

0.19

29

0.23

11

0.27

62

0.27

47

0.12

55

0.11

23

0.12

68

0.23

69

0.28

13

0.33

25

0.34

84

0.33

94

0.31

19

0.25

94

0.29

48

0.20

79

0.27

72

Con

hi-

buti

on to

oper

a-

ting

P

rofi

t

2.48

08

2.79

30

4.08

21

5.51

19

6.28

28

7.31

89

5.94

06

5.40

87

5.12

19

5.92

55

5.64

28

6.44

63

6.30

43

6.89

13

6.56

26

6.97

41

6.78

95

4.88

91

4.87

80

Long

Ter

n

Loa

n to

D

ebt

Cap

ital

-- 0.

3514

0.

3684

0.

3439

0.

2835

0.

2617

0.

2707

0.

2749

0.

2895

0.

2624

0.

2634

0.

253

1 0.

2398

0.

2388

0.

1980

0.

1663

0.

1679

0.

1125

0.

1025

0.

0995

Fid

Assets to

Cap

ital

E

mpl

o-

yed

0.54

79

0.79

12

0.90

77

0.89

02

0.76

08

0.78

16

0.79

11

0.79

51

0.90

38

0.97

33

1.05

81

0.14

36

1.25

86

1.10

55

1.07

77

1.16

20

0.84

22

0.77

61

0.81

42

Sto

ck to

S

alts

to

Ave

rage

C

apil

al

We

tw

Em

plo-

S

ala

ye

d

1994

-95

1995

-96

Ave

rage

S

ourc

e: B

urea

u of

Pub

lic E

nter

prise

s. m

c

Ent

eror

ises

Sur

vey,

Various is

sues

, Min

isby of In

dus@

. G

over

nmen

t of I

ndia

, New D

elhi

.

3.01

01

2.95

57

3.08

95

1.05

54

/ 690

.322

2 1

.07

20

, 82

2.82

50

1.6

30

7'

318.

9573

1.31

83

1.35

47

1.39

75

0.17

31

0.13

09

0.22

59

5.69

92

4.92

57

5.56

52

0.10

56

0.10

09

0.22

64

' 0.

9493

0.

8817

0.

8672

2526

.692

30

81.9

23

1658

.862

2.06

24

2.09

73

1.67

93

0.12

52

0.15

74

0.13

15

12.5

158

15.7

350

19.9

192

Peri

od

i T

rade

Sllc

s to

S

tock

to

i W

ork

ins

Wor

king

1975

-76

1976

-77

Cu

mn

t A

s~

h

to

Cu

rren

t L

iaM

li-

ties

1.75

67

1.91

64

1.67

74

1.61

67

1.38

30

1.11

03

1.03

65

1.35

11

1.21

15

1.21

02

1.00

73

0.94

%

0.96

85

1.55

21

1.95

20

1.59

57

1.17

80

1.07

27

0.97

12

0.60

15

1977

-78

1978

-79

1979

-80

1980

-81

1981

-82

1982

-83

1983

-84

1984

-85

1985

-86

1986

-87

1987

-88

1988

-89

1989

-90

1990

-91

1991

-92

1992

-93

1993

-94

1994

-95

1995

-96

Ave

rage

0.87

06

0.82

28

Sto

ck to

A

vera

ge

We

Y.

s.k

s

234.

596

267.

404

249.

769

249.

788

243.

923

260.

577

308.

519

367.

865

452.

096

438.

096

446.

769

53 1.

058

567.

250

581.

769

690.

904

738.

404

737.

942

486.

019

524.

923

371.

654

Tab

lt V

S.2

Fha

ncia

l Per

form

ance

Rat

ios - H

EC

Co

nh

i-

So

um

: Bu

reau

of P

ublic

Ent

erpr

ises

, Pub

lic EI

0.85

43

1.05

91

1.21

33

- 3.

3027

13

.477

7 1.

6168

1.

9836

2.

8657

85

.545

5 -1

1.83

80

-17.

4930

1.

4775

I.

102

9 0.

9721

2.

6005

13

.402

4 -2

2.55

10

-1.0

100

-0.6

409

3.79

21

0.49

99 1

0.03

25 1

-2.4

171

1 0.

5250

1 -0

.971

1 !

311.

288

1 -0

.792

4 1

-0.3

814

1.26

75 1

0.15

62 1

4.58

88 1

0.54

40 1

1.56

74 /

431.

458

1 1.

2831

1 -0

.179

7 em

rises

Sur

vey,

Various Is

sues

. Min

istry

of I

ndus

hy, G

over

nmen

t of

Indi

a, N

ew D

elhi

.

1.61

45

1.50

85

0.23

08

0.14

92

0.13

29

0.14

83

0.17

69

0.18

49

0.13

55

0.15

26

Pn

-Tn

su

rplu

s to s

* S

ales

8.

4361

10

.752

8 1.

8769

1 7.

7500

1,

8814

; 5.

5833

3.73

34

3.30

66

-2.8

263

-7.3

369

2.50

97'

6.91

68

19.8

552

2.76

95

4.43

06

4.17

39

105.

6000

-1

3.35

30

8.97

78

8.03

06

10.9

389

12.3

556

12.9

917

16.8

1 11

1 1.7

944

20.4

361

1.54

82

1.62

80

0.45

41

0.4

65

8;

0.46

20

0.47

53

0.08

78 1

-4

.366

4 0.

1000

i -5

.078

3

0.67

19

0.90

93

1.05

52

1.09

99

0.65

28

0.64

36

-18.

9690

1 33

.658

3 1.

6839

; 30

.583

3

1.28

29

1.68

92

2.04

17

1.75

73

-4.6

134

: 0.

4802

-2

.513

5 ;

0.50

15

1.33

01

1.70

53

4.44

75

8.06

41

-20.

2340

-0

.806

1 -0

.444

9 5.

5505

-8.8

990

-3.5

048

0.09

54

0.09

71

0.12

54

0.28

40

0.24

42

0.28

69

0.18

32

0.24

36

0.14

18

0.04

81

34.8

056

30.7

528

27.3

639

29.0

250

32.2

694

28.9

306

38.6

250

20.2

320

' 0.

5205

0.

6069

-8.6

653

-55.

8540

2.

8226

7.

0707

-3

1.22

60 '

-3.9

729

-1.9

216

-9.2

859

40.3

123

-1.1

298

0.64

29 j

2.87

27

0.64

78

4.90

14

0.64

98 1

4.06

25

0.68

32

0.50

28

0.50

14

0.54

01

0.50

82

0.47

36

0.48

70

0.95

66

0.75

49

0.89

17

1.49

10

2.22

20

3.70

94

-1.6

588

Tab

k VJ3

Financial

Per

fom

mce

Rat

ios -

BHP

V

Sale

s to

Pe

riod

W

ork

ing

C

.pih

l

Liq

uid

Ass

ets

to

Cu

rren

t L

iabi

li-

tie

0.0615

0.5867

0.5411

0.3589

0.3579

0.2838

0.2537

0.3721

0.2833

0.2936

0.4269

0.3490

0.4727

0.5363

0.4435

0.5408

0.5775

0.4012

0.3871

0.2542

Fixe

d A

saeh

to

Cap

ital

Emplb

yed

0.6356

0.5927

0.7259

0.7495

0.7609

0.9257

1.0775

1.3222

1.2408

0.9991

0.8794

0.9600

1.3094

0.6155

0.6220

0.5813

0.5571

0.5143

0.6332

0.6770

1995-%

1 2.9678

1 0.91 1

1 i 73 7556

1 1.3404

1 0.3909

1 23.9434

1 03417

/ 0.5927 1

161.17301

2.3073

Ave

rage

1

3.1825

1 2.2467

i 11.5619

1 1.4452

1 0.3892

1 10.3462

1 0.4488 1

0.8082 1

93.462

1 1.6721

Source:

Bur

eau of Public Enterprises, Public

Ente

rnris

es Survey, Various

Issu

es, M

inist

ry o

f Industry, Government

of In

dia,

New

Del

l

Sto

ck to

A

vera

ge

Wee

kly

S.k

s

54.2500

44.3846

37.2885

47.4423

55.3269

49.3846

60.1346

60.8654

118.1730

136.1350

95.3269

106.6920

107.2120

95.9038

120.0960

109.1350

106.8850

158.2310

117.6540

121.0000

Sd

u to

C

apit

al

Emplo-

yed

0.5412

0.7437

0.7650

0.5749

0.9445

1. I576

1.1651

1.9977

1.9485

2.3429

2.1723

2.1474

2.8281

1.7442

1.7658

2.3378

2.0680

1.5878

1.7731

2.2012

it is necessary to mention that the Gmss Profit ratio was negative in most of the years in

HEC, BSL and JCL over the period of the study. It implies that these units did not have

adequate sales which reflected negative trend on Gross Profit during the study period.

At the same time, Cost of Goods sold had mounted year after year due to the firm's

under-utilisation of its capacity, over-investment in Plant and Machinery, purchasing

of Raw Materials at unfavourables prices or it might be represented low Revenue due to

low prices in competitive product market.

Evidently, it can be observed from the Tables that Operating Surplus to

Sales ratios of the sample units reported similar is the Gross Profit ratios of the

sample units during the study period.

An examination of the financial performance of the sample units

belonging to Heavy Engineering in select Public Sector Enterprises is essential as it is

hypothesised that poor returns resulted in poor generation of the Internal resources

during the study period. However, on the basis of various financial ratios and their

results indicated that BHEL's financial performance was more satisfactory among the

sample units during the study period.

Financial rabos of sample units belonging to Medium Engineering

Public Sector Enterprises have been presented in Tables from V.6.1 to V.6.5 for

further analysis.

It can be observed from the tables that the Turnover ratios were

positive and satisfactory in sample units such as BEL (Table V.6.1), HMT (Table

V.6.3) and HCL (Table V.6.4). These ratios were r e p o d negative during the year

1983-84 and 1984-85 in case of BDL (Table V.6.2) and similar trend found during year

1994-95 in ITIL (Table V.6.5) during the study period. On an average, Sales to

Working Capital ratio was 2.21 times in BEL, 2.45 times in BDL, 1.81 times in HMT,

1.86 times in HCL ,and 1.06 times in RIL during the study period. This analysis

indicates that the ratio was relatively satisfactory in all sample units. From the

foregoing analysis, it may be inferred that the working capital requirements could be

met from the sale proceeds in all sample units, however, it was relatively good in case of

BEL during the period under the study.

It is exhibited in tables that Trade Debtor ratio of BEL has shown raising

trend significantly from 3.29 times in 1975-76 to 118.50 times in 1995-96. But tius ratio

has been fluctuated in HMT, HCL and ITIL during the study period At the same

time, this ratio was insignificant in BDL due to inadequate trade debtors. It might have

happened either due to cash sales or poor sales in BDL during the study period.

From the above exposition, it can be said that sample units such as BEL and ITIL have

taken more time for collecting dues from their debtors while comparing to HMT and

HCL during the reference period. As a result, sample units depended on short-term

borrowing for Working Capital requirements. However, it is noticed from the

analysis that the Liquidity position of the sample units, namely, HMT, HCL and ITIL

are good during the period of the study

The data presented in Tables from V.6.1 to V.6.5 pertaining to the

current ratio of sample units during the reference period. Looking at the current ratio

in tables which had been fluctuating in all sample units and an average of this ratio

was 1.49 times in BEL, 1.27 times in BDL, 2.55 times in HMT, 2.43 times in HCL and

2.52 times in JCL during the study period.

It can be observed &om the analysis that all sample units had

comfortable current ratio during the study period. Further, it reveals Cment Assets are

excess over Current Liabilities in all sample units which reflects sound short-term

solvency during the study period.

While comparing this ratio against the Turnover ratios of the respective

sample units, a proper correlation among all sample units except BDL was identified

during the study period. A significant variation was found in respect of current ratio

and turnover ratios of BDL due to wide fluctuation in Sales during the study period.

From the above analysis, it is evident that all sample units except BDL met their

Working Capital requirements from sale proceeds, hence, their short-term solvency

was good during the study period

Again, it can be seen from the tables that the Quick Assets / Acid Test

raOo was less than one time as an average in all sample units during the study

period. Therefore, it can be judged that all units could not be maintained in proper

proportion of Liquid Assets against Current Liabilities.

The tables further explain about different financial ratios of the

study units. The contribution to Operating PrcEt :& c!ez!y sh;.;;s relationsbp

between Operating Profit and Sales of the sample units. In BEL, this ratio was

positive throughout the study period and on an average, this ratio was 5.04 times. It

shows that conaibution was sufficient to meet Fixed wst and left sizeable portion as

Profit in the sample unit. While this ratio has been fluctuated widely in BDL which had

negative values during 1980-81 and 1983-84. This ratio turned as positive from

1984-85 onwards. From this analysis, it can be said that BDL had not earned profit in

all the years of the study period.

In the case of HMT, this ratio was positive and satisfactory from 1975-

76 to 1992-93 but it changed as negative dangerously during the year 1993-94 and

1994-95 due to inadequate Sales and increasing overhead cost, however, it improved

subsequently. On the basis of this ratio, it may be judged that HMT was not having

consistent Financial Performance during the period of the study. In HCL, on an

average, t h ~ s ratio was 3.02 times while it was 3.85 times in ITlL during the study

period. These sample units had sufficient contribution in all the years except in 1995-

96 due to inadequacy of Sales or increasing Cost of Goods sold. Judging from the