CHAPTER TWO ANALYZING TRANSACTIONS: The Accounting Equation.

116

CHAPTER TWO ANALYZING TRANSACTIONS: The Accounting Equation

-

Upload

juniper-warner -

Category

Documents

-

view

231 -

download

1

Transcript of CHAPTER TWO ANALYZING TRANSACTIONS: The Accounting Equation.

CHAPTER TWO

ANALYZING TRANSACTIONS: The

Accounting Equation

BUSINESS ENTITY

An individual, association, or organization

That engages in economic activities And controls specific economic resourcesBusiness entity’s finances kept separate

from those of owner (Business Entity Concept)

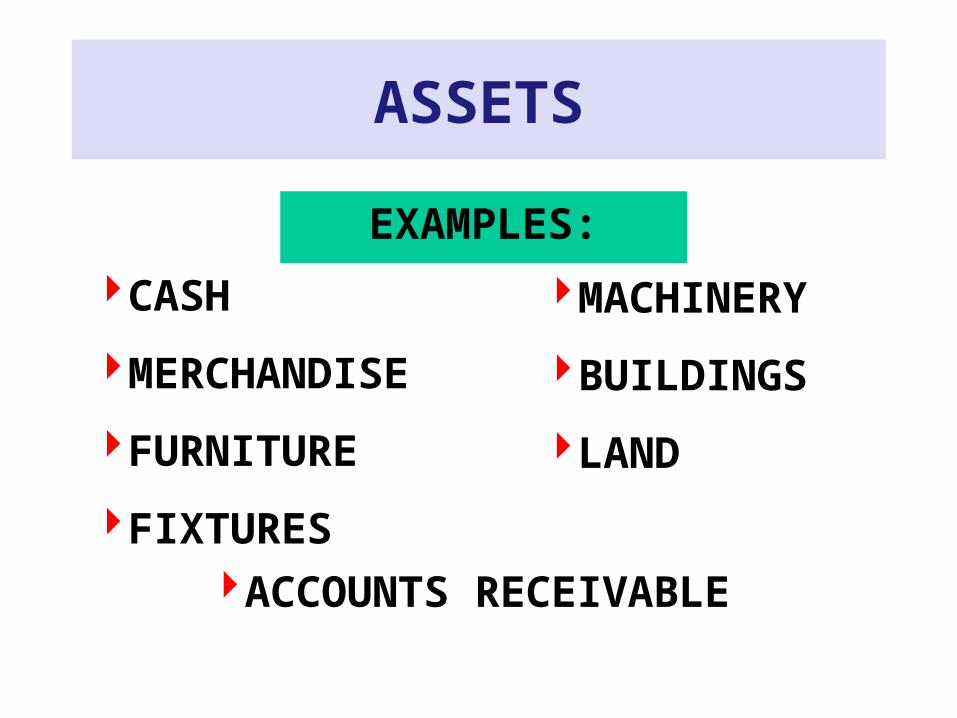

ASSETS

ITEMS OWNED BY A BUSINESS THAT WILL PROVIDE FUTURE BENEFITS

MUST BE “OWNED”NOT RENTED

ASSETS

ITEMS OWNED BY A BUSINESS THAT WILL PROVIDE FUTURE BENEFITS

BUT DOESN’T HAVE TO BE PAID OFF,

COULD STILL BE MAKING PAYMENTS ON IT

ASSETS

EXAMPLES:

CASH

MERCHANDISE

FURNITURE

FIXTURES

MACHINERY

BUILDINGS

LAND

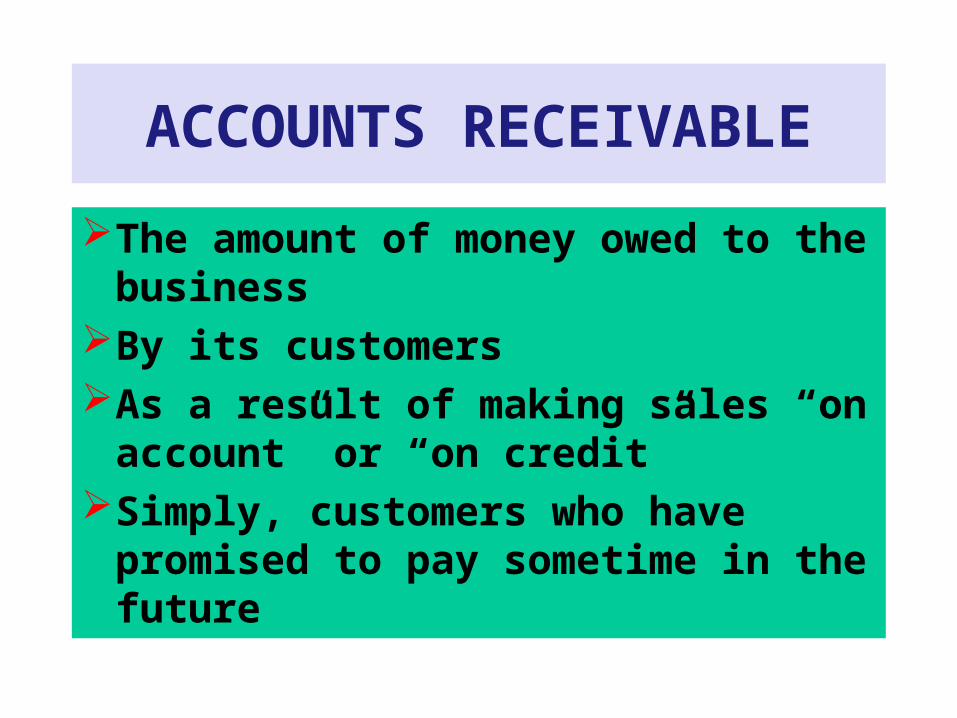

ACCOUNTS RECEIVABLE

ACCOUNTS RECEIVABLE

The amount of money owed to the business

By its customersAs a result of making sales “on account”

or “on credit”Simply, customers who have promised to

pay sometime in the future

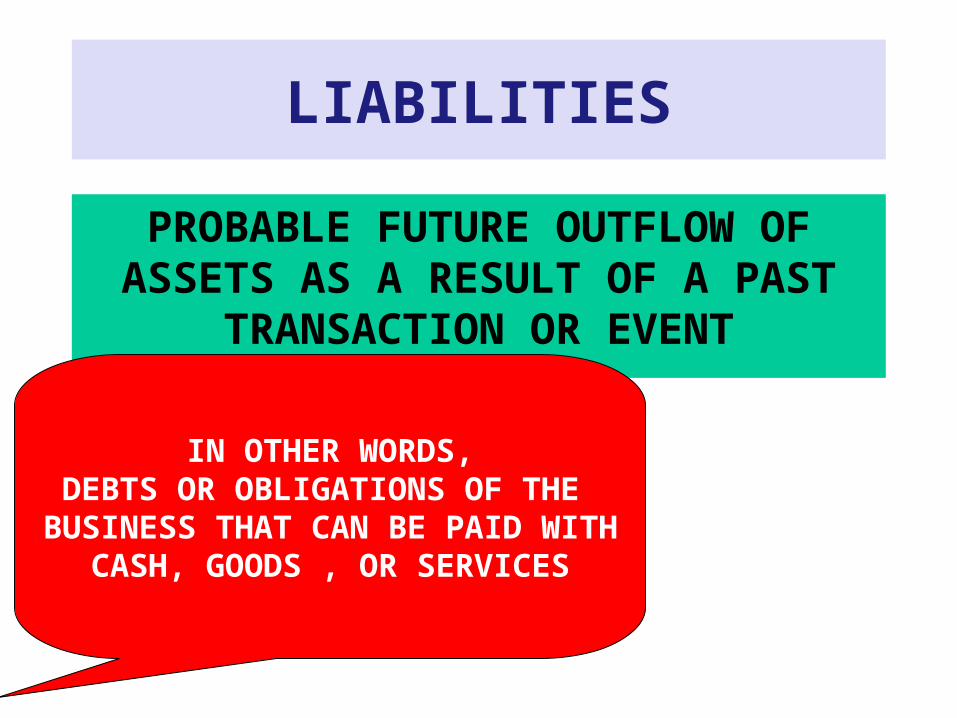

LIABILITIES

PROBABLE FUTURE OUTFLOW OF ASSETS AS A RESULT OF A PAST

TRANSACTION OR EVENT

IN OTHER WORDS,DEBTS OR OBLIGATIONS OF THE

BUSINESS THAT CAN BE PAID WITHCASH, GOODS , OR SERVICES

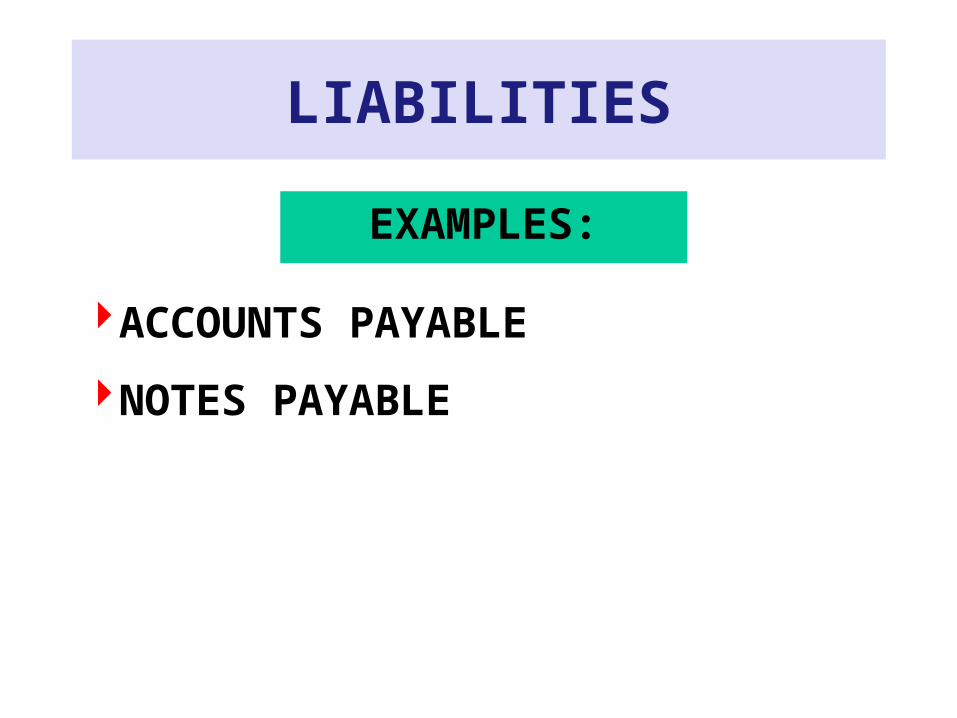

LIABILITIES

EXAMPLES:

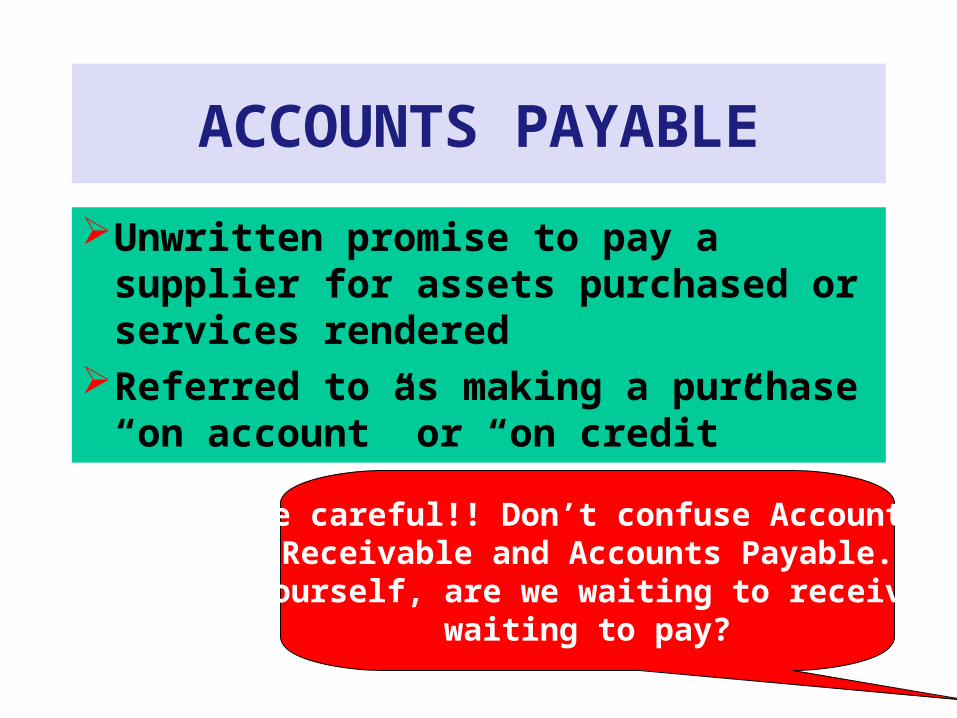

ACCOUNTS PAYABLE

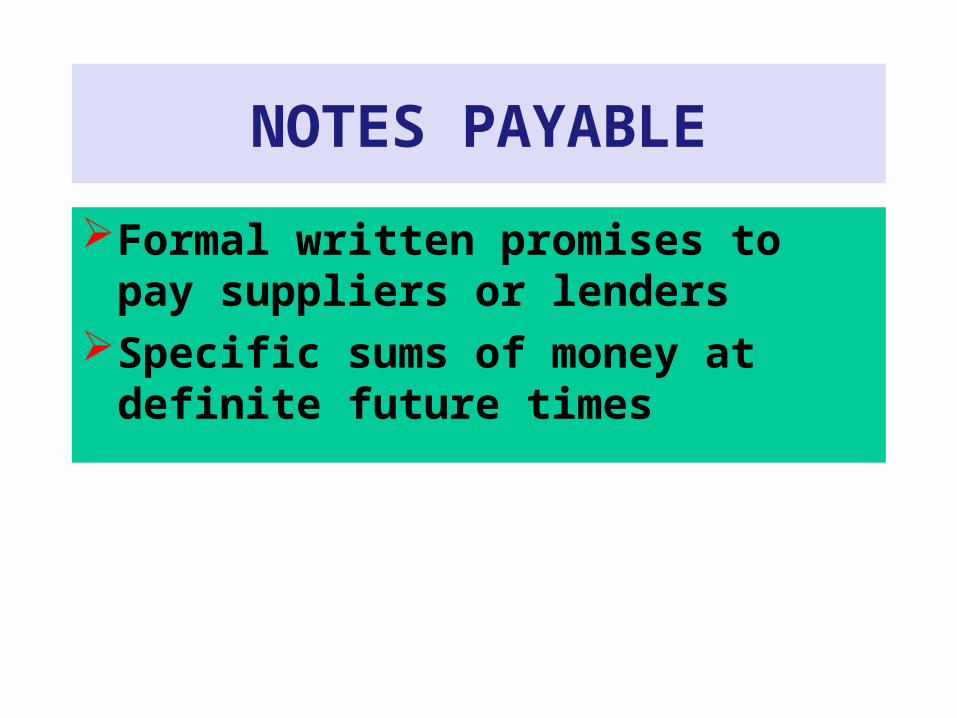

NOTES PAYABLE

ACCOUNTS PAYABLE

Unwritten promise to pay a supplier for assets purchased or services rendered

Referred to as making a purchase “on account” or “on credit”

Be careful!! Don’t confuse AccountsReceivable and Accounts Payable.

Ask yourself, are we waiting to receive? Or waiting to pay?

NOTES PAYABLE

Formal written promises to pay suppliers or lenders

Specific sums of money at definite future times

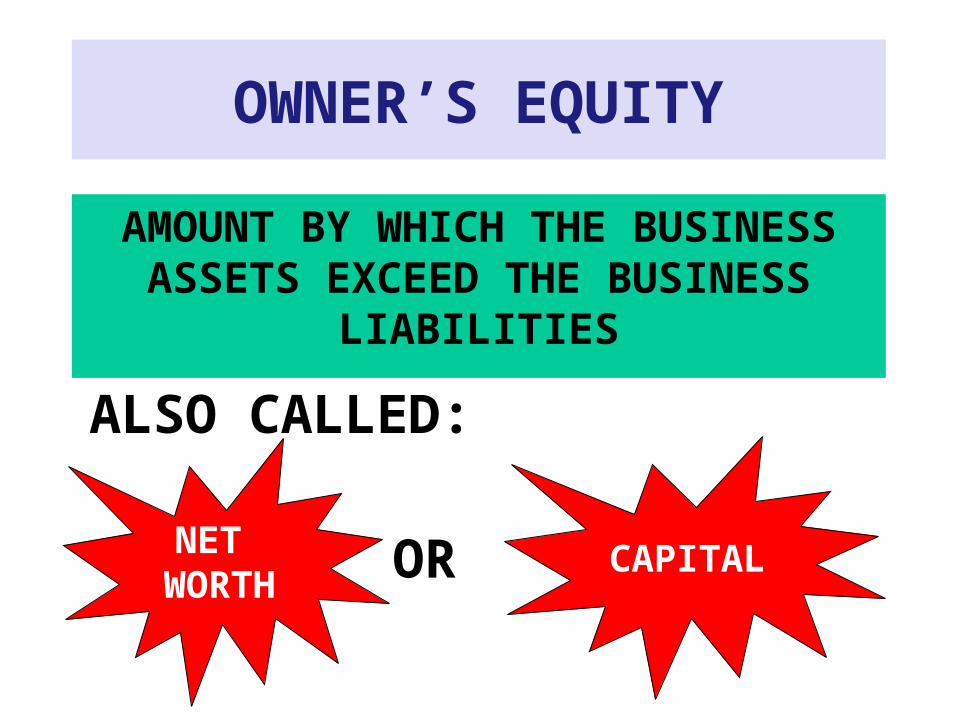

OWNER’S EQUITY

AMOUNT BY WHICH THE BUSINESS ASSETS EXCEED THE BUSINESS

LIABILITIES

NET WORTH

CAPITAL

ALSO CALLED:

OR

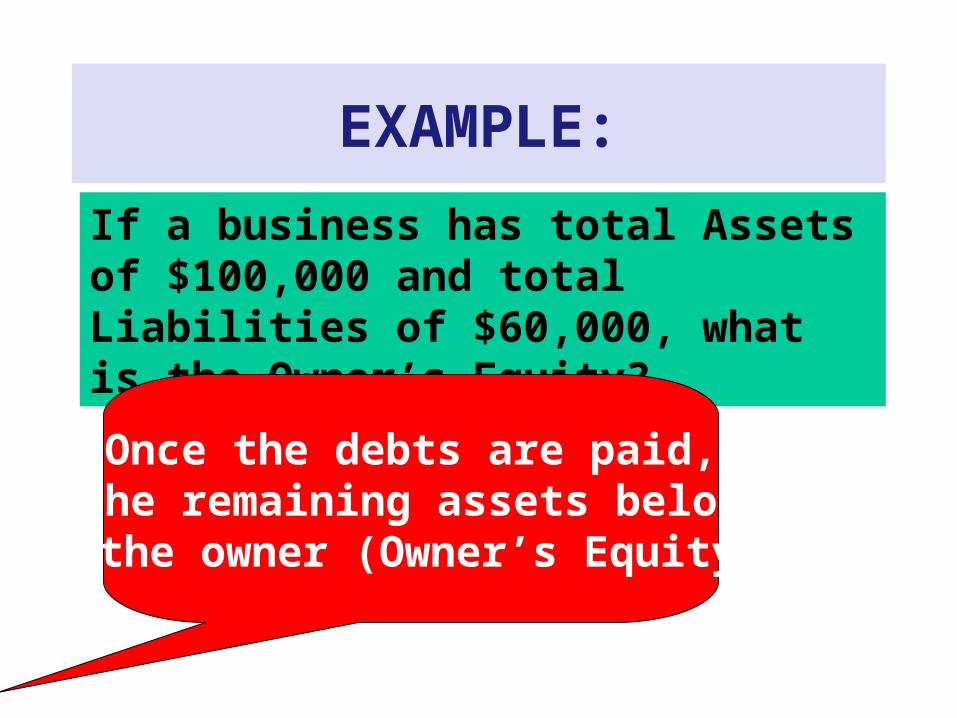

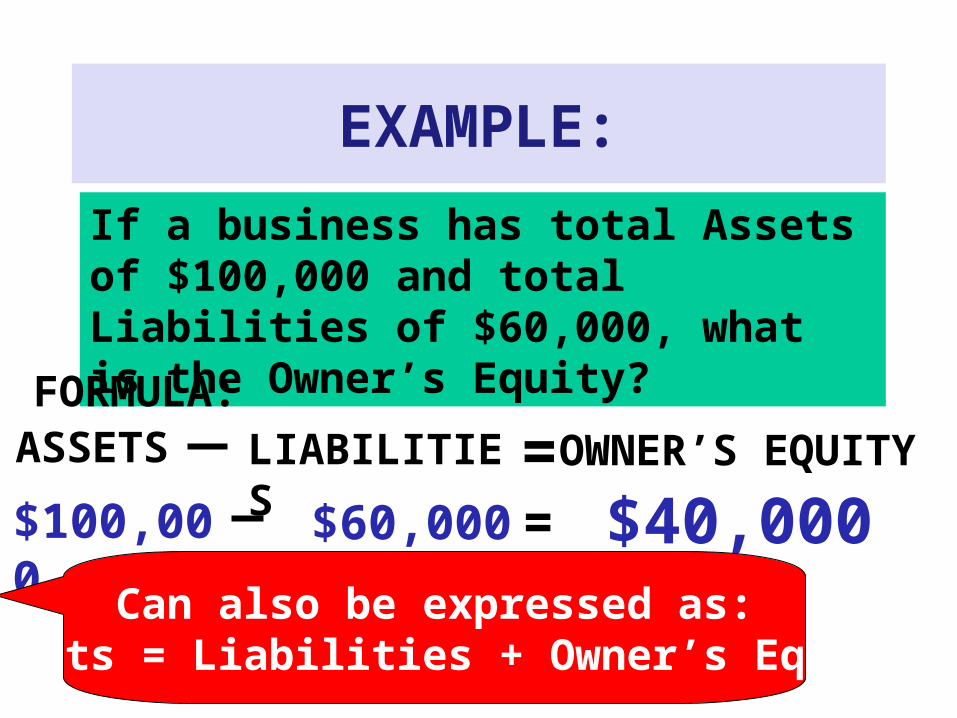

EXAMPLE:

If a business has total Assets of $100,000 and total Liabilities of $60,000, what is the Owner’s Equity?

Once the debts are paid, the remaining assets belong

to the owner (Owner’s Equity).

EXAMPLE:

If a business has total Assets of $100,000 and total Liabilities of $60,000, what is the Owner’s Equity?

FORMULA:

$100,000 $60,000 = $40,000ASSETS LIABILITIES =OWNER’S EQUITY

Can also be expressed as:Assets = Liabilities + Owner’s Equity

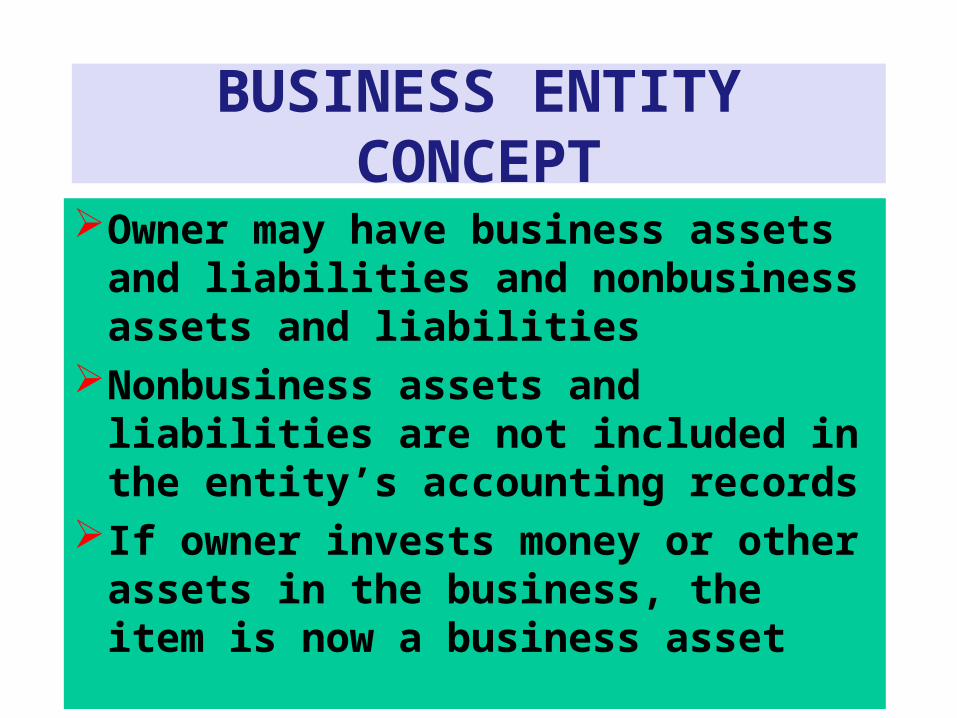

BUSINESS ENTITY CONCEPT

Owner may have business assets and liabilities and nonbusiness assets and liabilities

Nonbusiness assets and liabilities are not included in the entity’s accounting records

If owner invests money or other assets in the business, the item is now a business asset

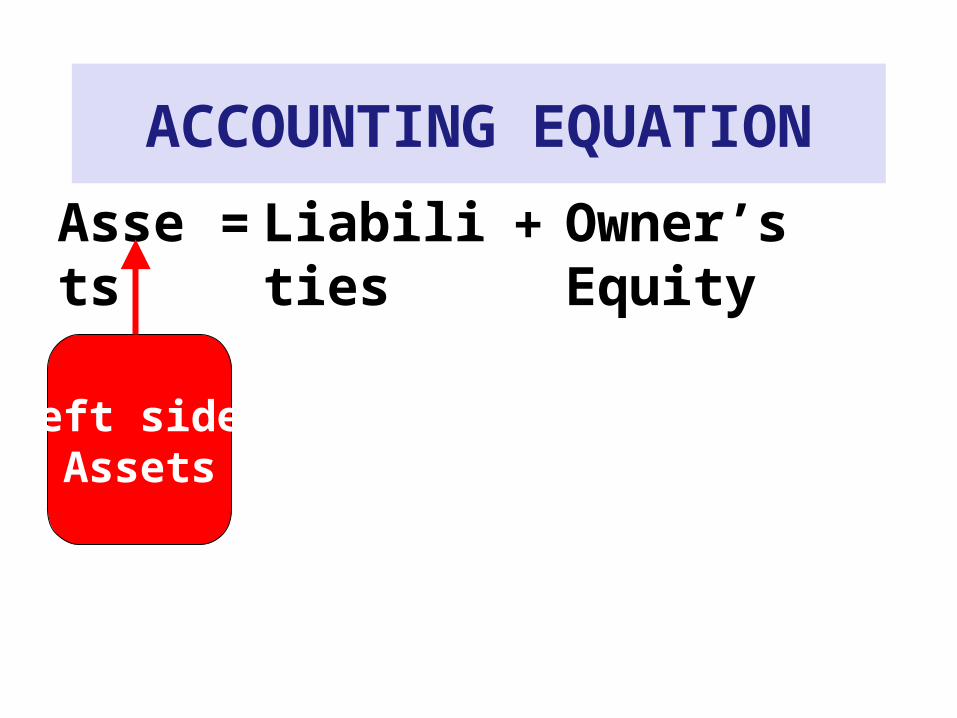

ACCOUNTING EQUATION

Assets Liabilities = Owner’s Equity+

Left side:Assets

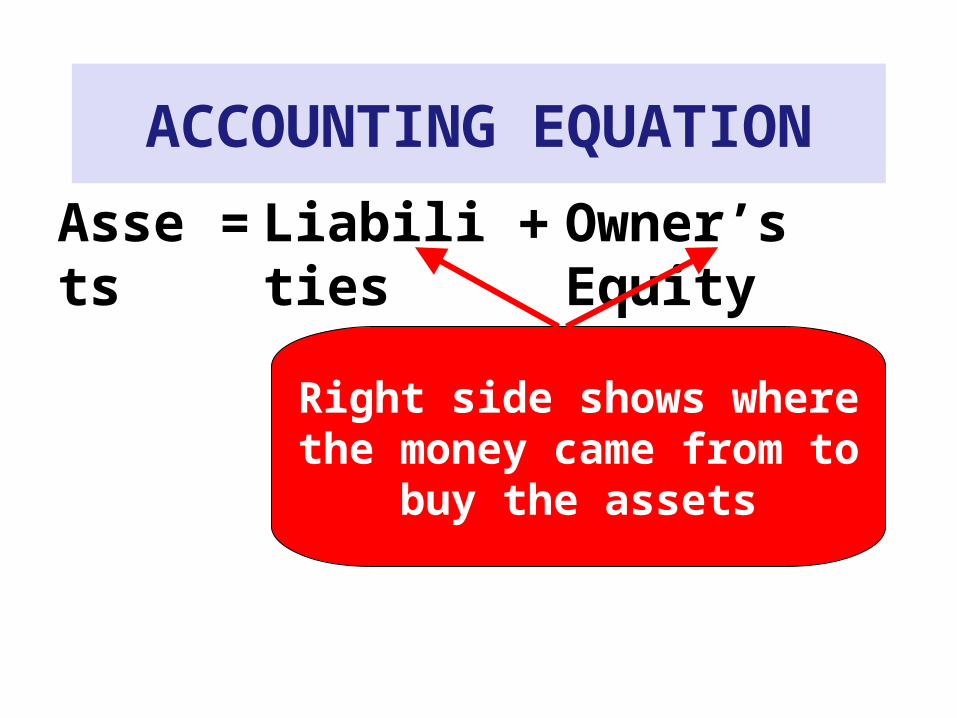

ACCOUNTING EQUATION

Assets Liabilities = Owner’s Equity+

Right side shows wherethe money came from to

buy the assets

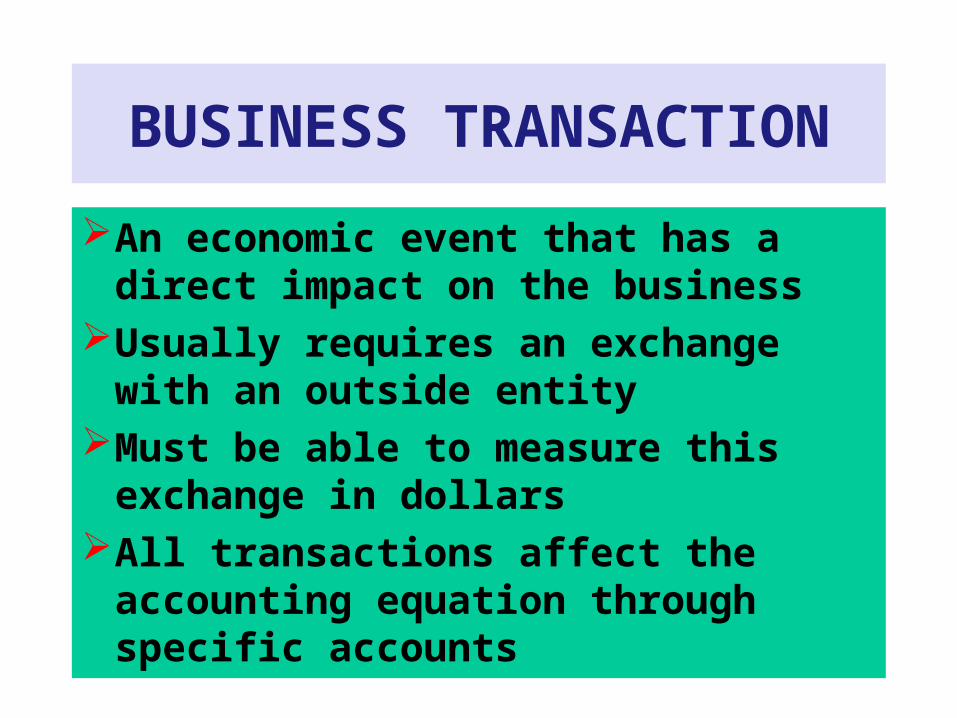

BUSINESS TRANSACTION

An economic event that has a direct impact on the business

Usually requires an exchange with an outside entity

Must be able to measure this exchange in dollars

All transactions affect the accounting equation through specific accounts

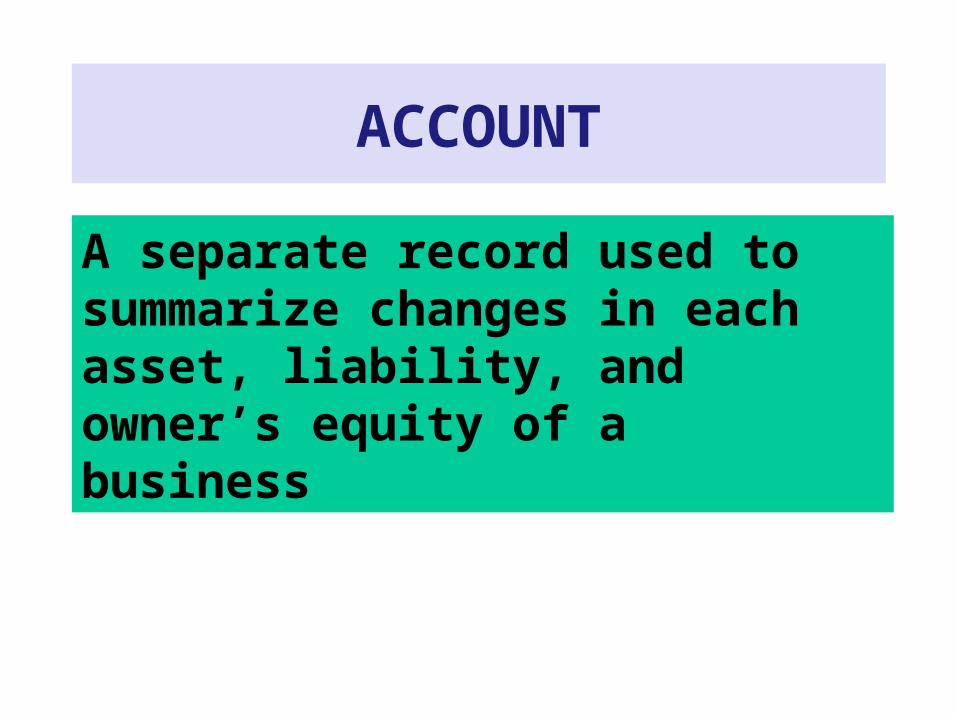

ACCOUNT

A separate record used to summarize changes in each asset, liability, and owner’s equity of a business

ANALYZING BUSINESS TRANSACTIONS

THREE QUESTIONS:

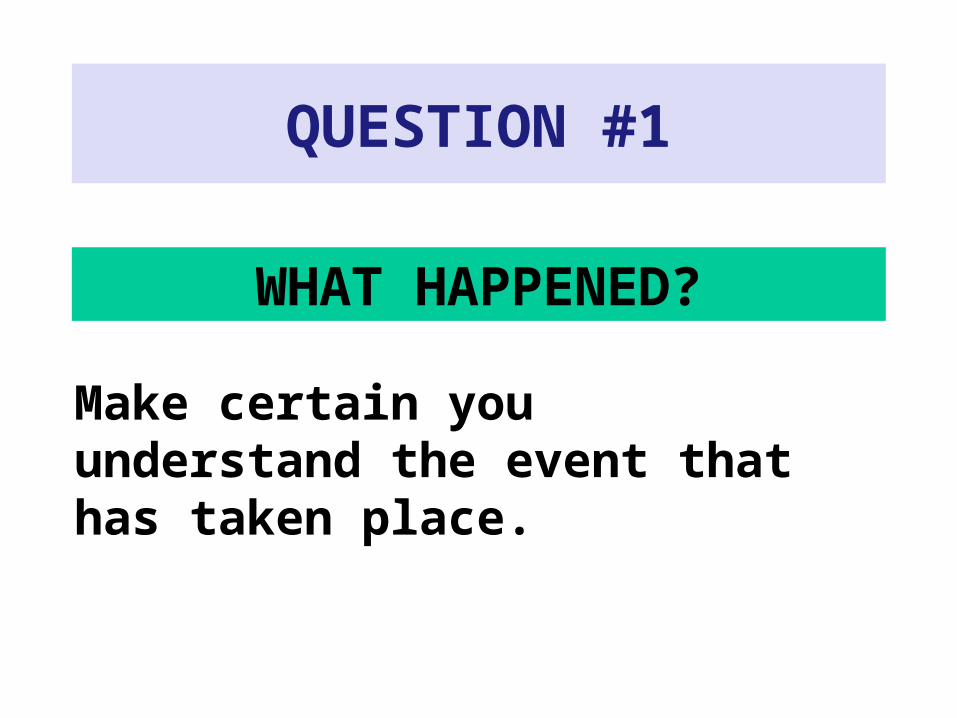

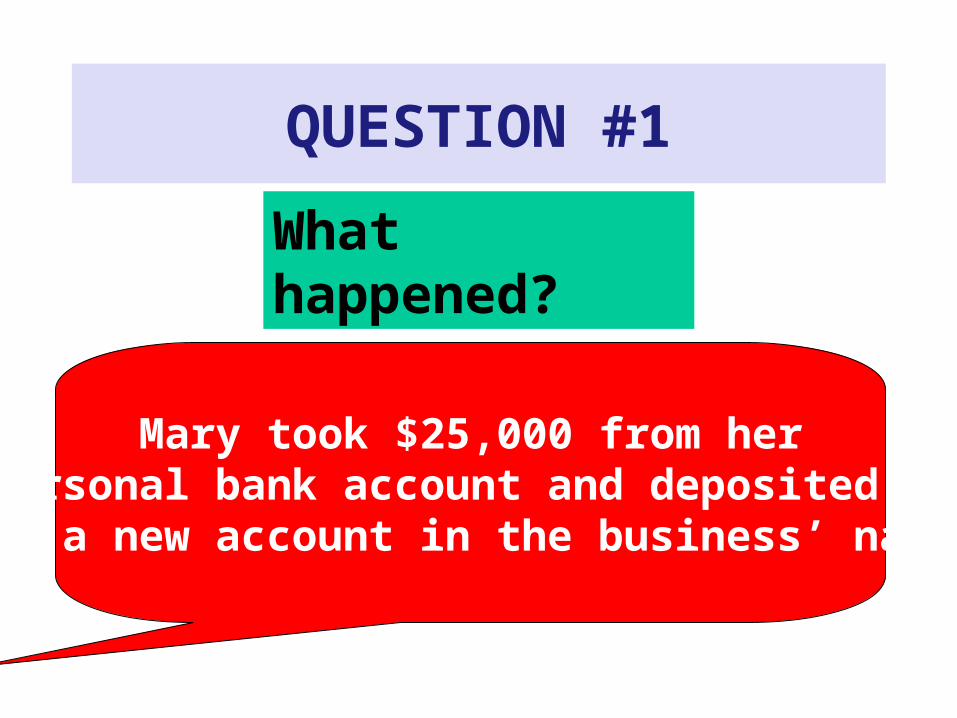

QUESTION #1

WHAT HAPPENED?

Make certain you understand the event that has taken place.

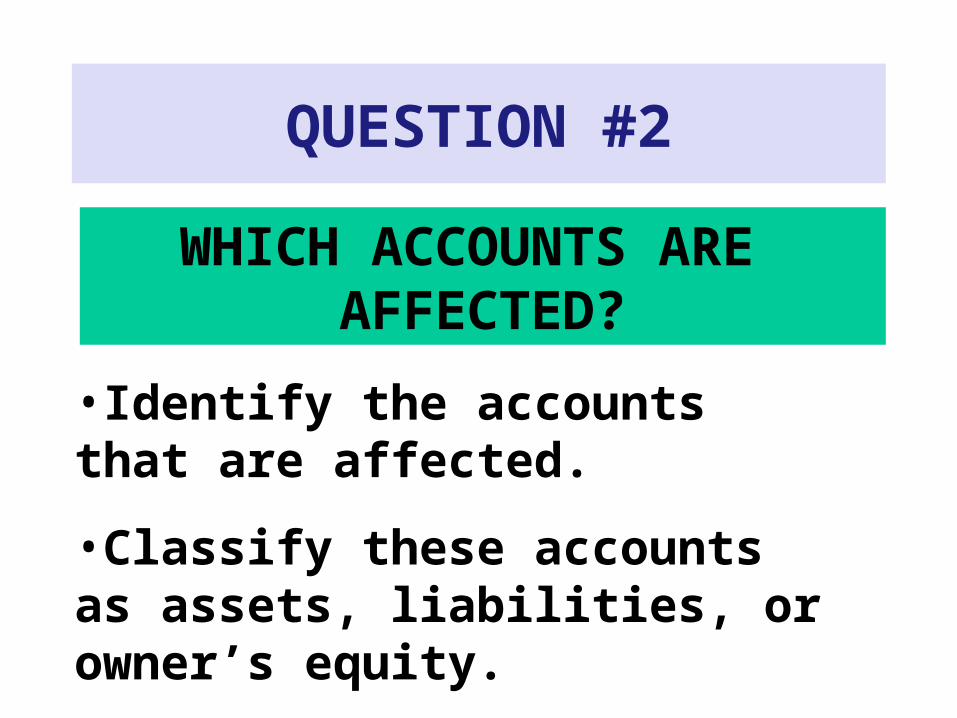

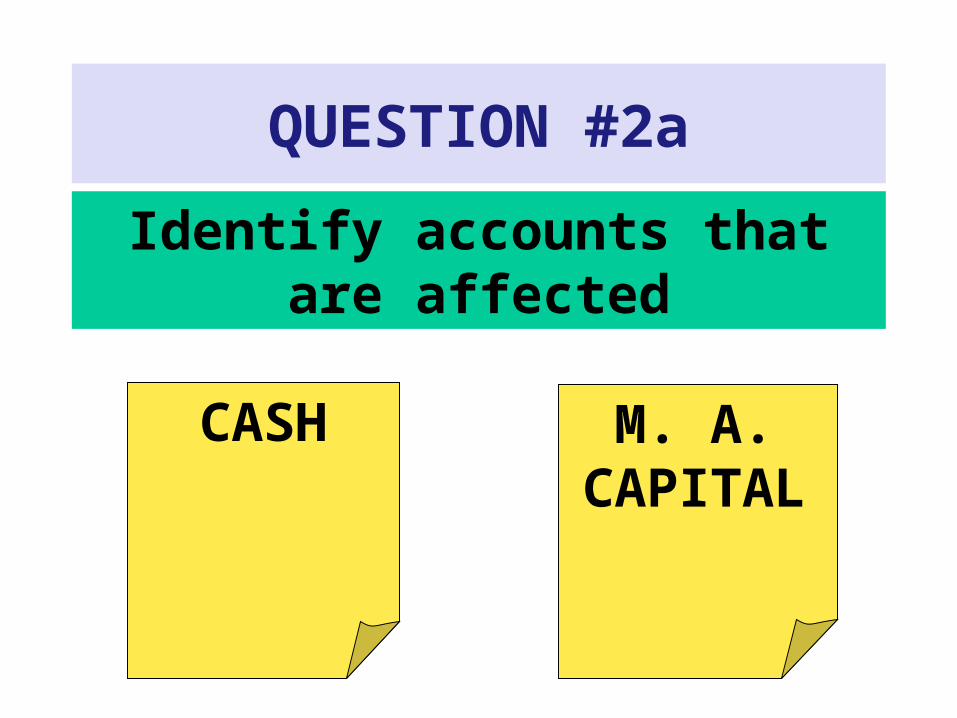

QUESTION #2

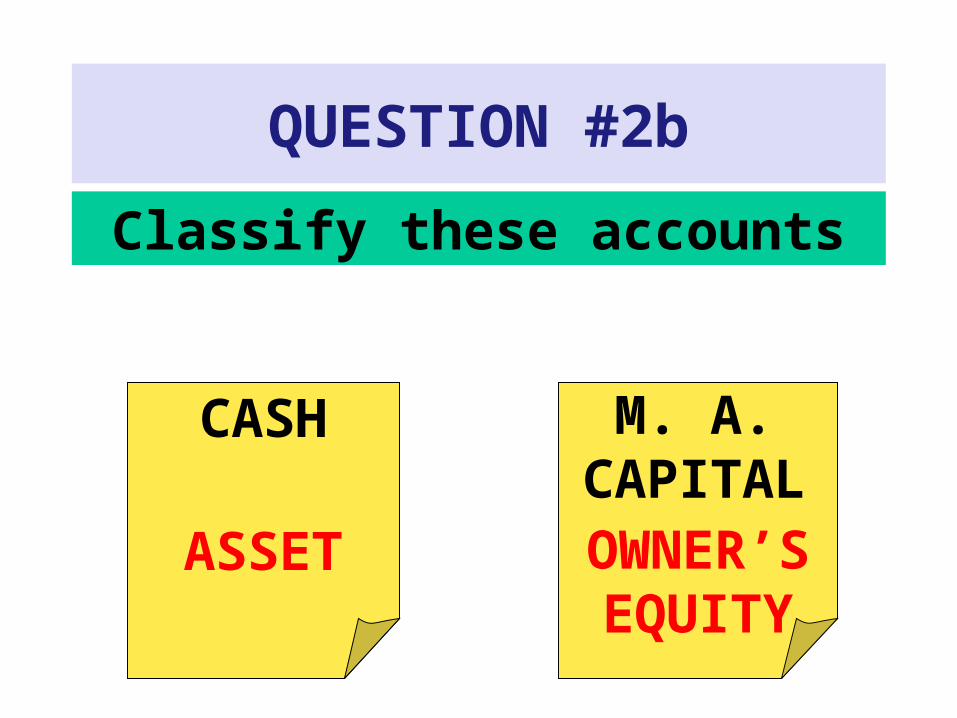

WHICH ACCOUNTS ARE AFFECTED?

•Identify the accounts that are affected.

•Classify these accounts as assets, liabilities, or owner’s equity.

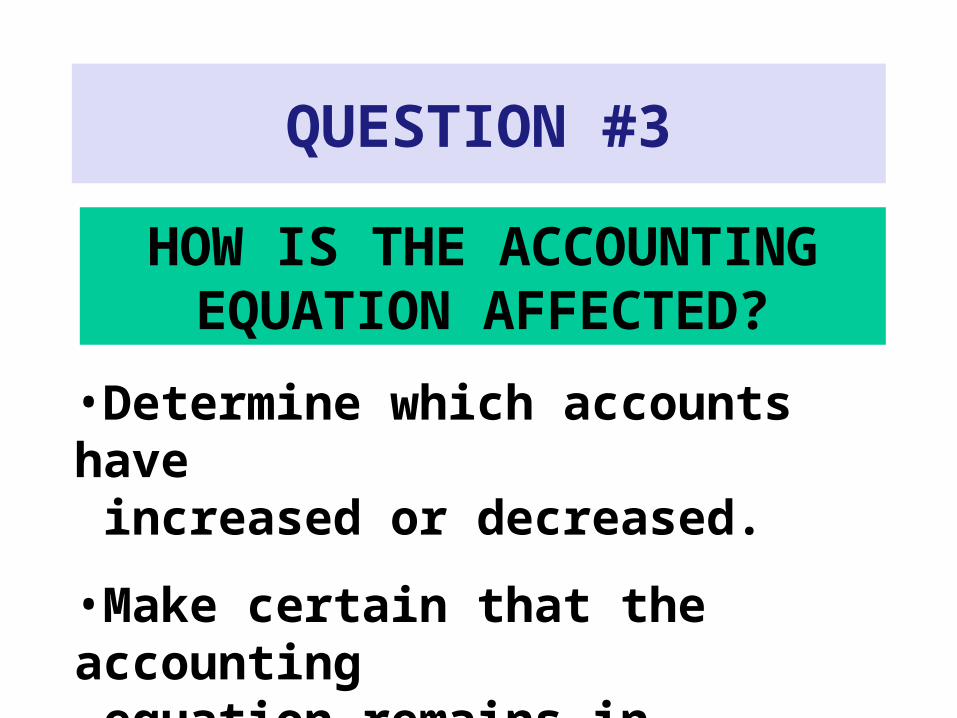

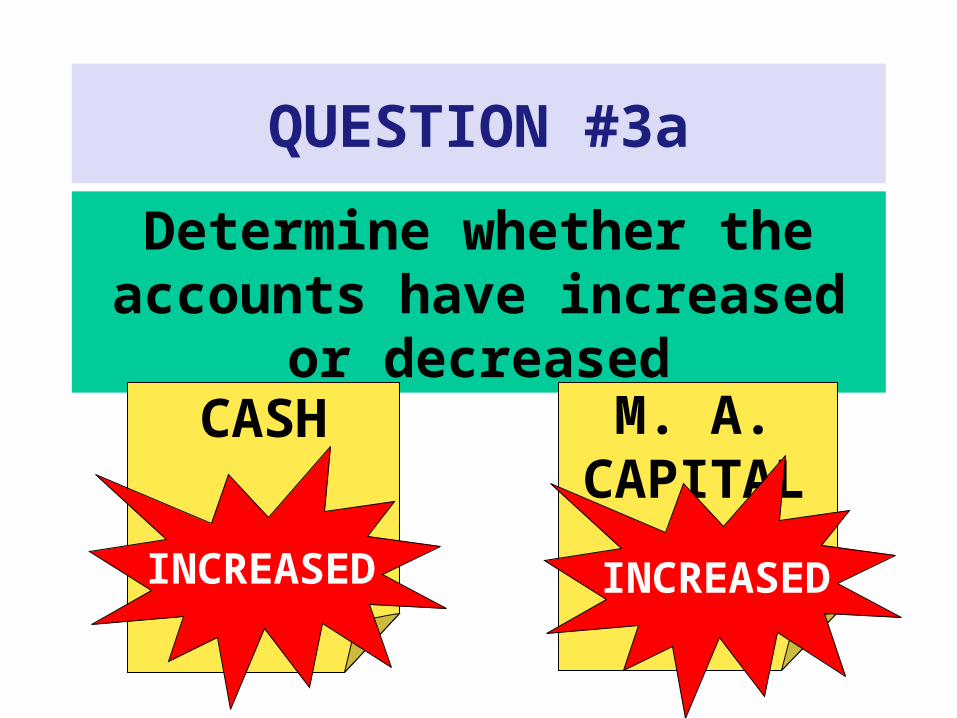

QUESTION #3

HOW IS THE ACCOUNTING EQUATION AFFECTED?

•Determine which accounts have increased or decreased.

•Make certain that the accounting equation remains in balance after the transaction has been entered.

Let’s analyze the effect of transactions on the accounting

equation for Mary Adams Consulting

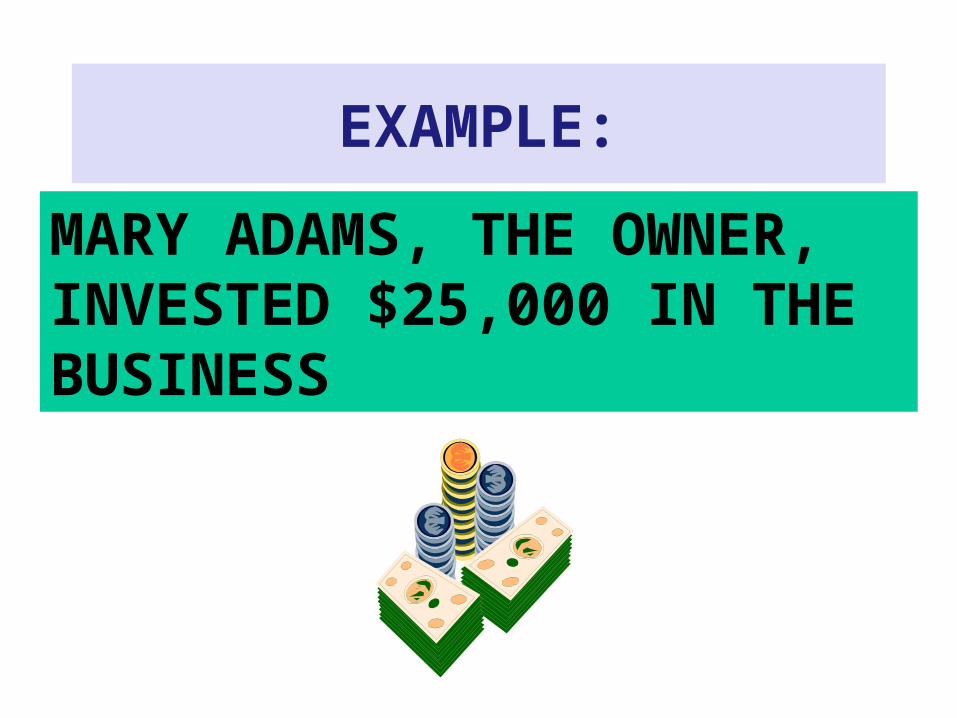

EXAMPLE:

MARY ADAMS, THE OWNER, INVESTED $25,000 IN THE BUSINESS

QUESTION #1

What happened?

Mary took $25,000 from herpersonal bank account and deposited itin a new account in the business’ name

QUESTION #2a

Identify accounts that are affected

CASH M. A. CAPITAL

QUESTION #2b

Classify these accounts

CASH M. A. CAPITAL

ASSET OWNER’S EQUITY

QUESTION #3a

Determine whether the accounts have increased or decreased

CASH M. A. CAPITAL

INCREASED INCREASED

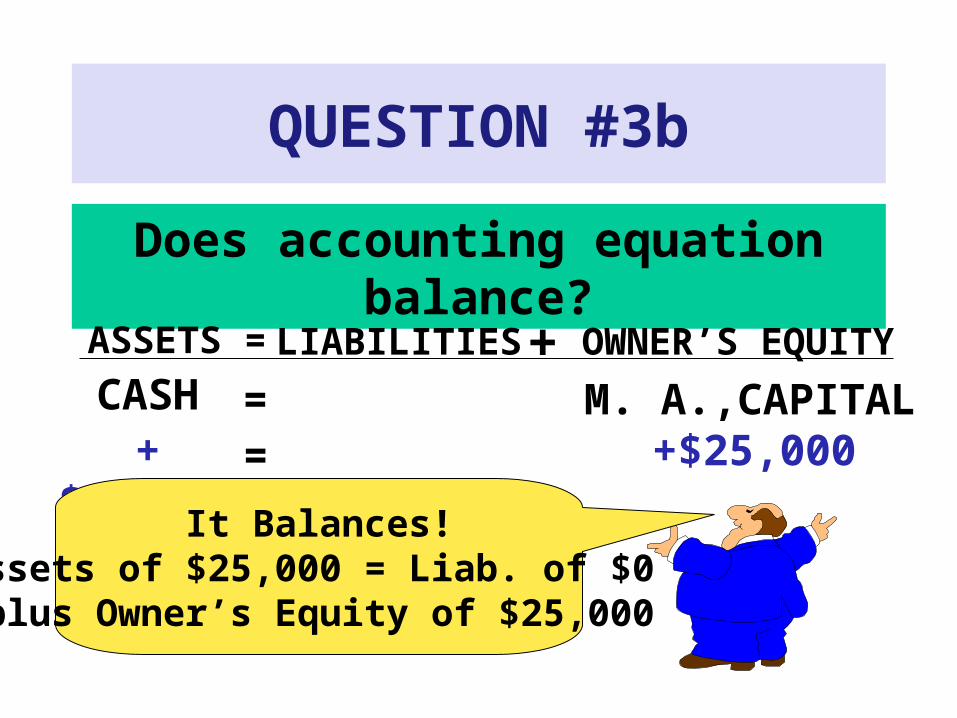

QUESTION #3b

Does accounting equation balance?

ASSETS = LIABILITIES + OWNER’S EQUITY

+$25,000CASH M. A.,CAPITAL=

+$25,000=

It Balances!Assets of $25,000 = Liab. of $0 plus Owner’s Equity of $25,000

EXAMPLE:

PURCHASED OFFICE SUPPLIES FOR $800 CASH

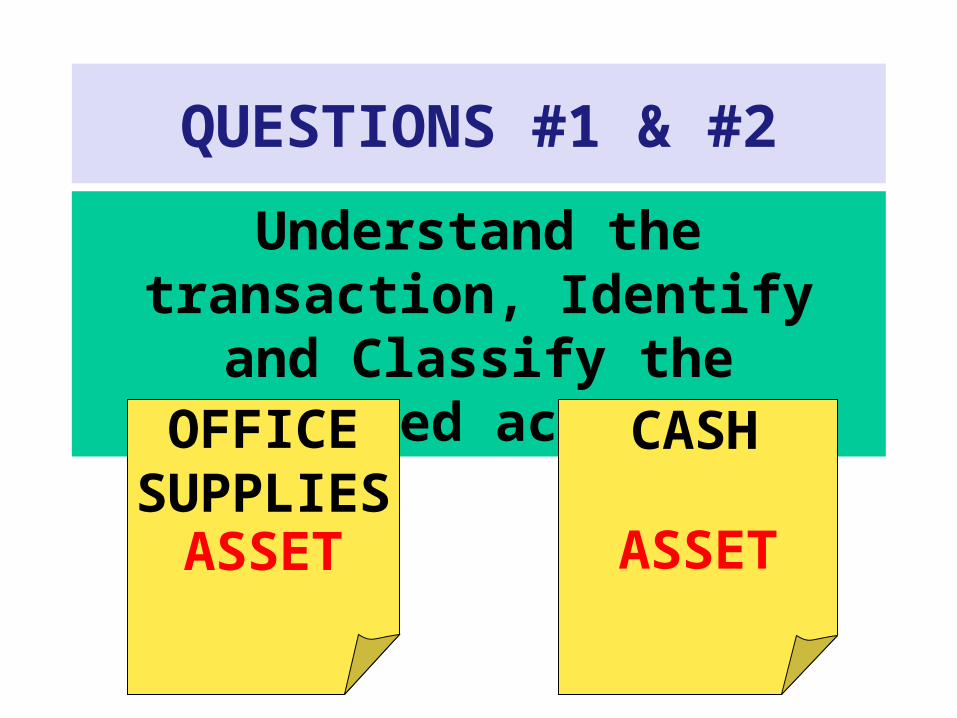

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected

accountsOFFICE

SUPPLIESCASH

ASSET ASSET

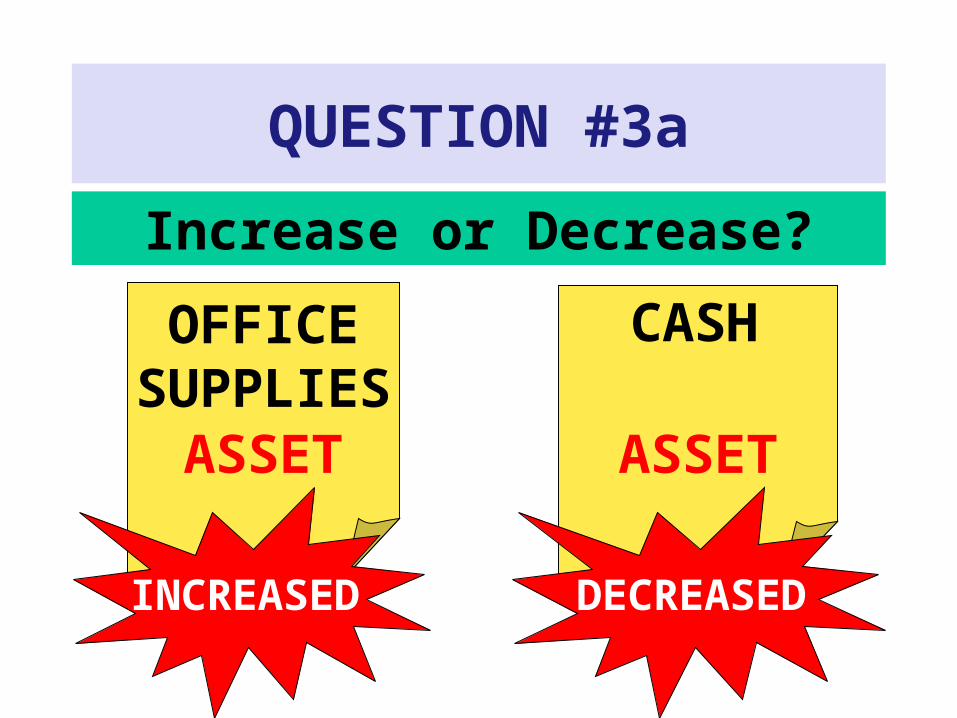

QUESTION #3a

Increase or Decrease?

OFFICE SUPPLIES

CASH

ASSET ASSET

INCREASED DECREASED

QUESTION #3b

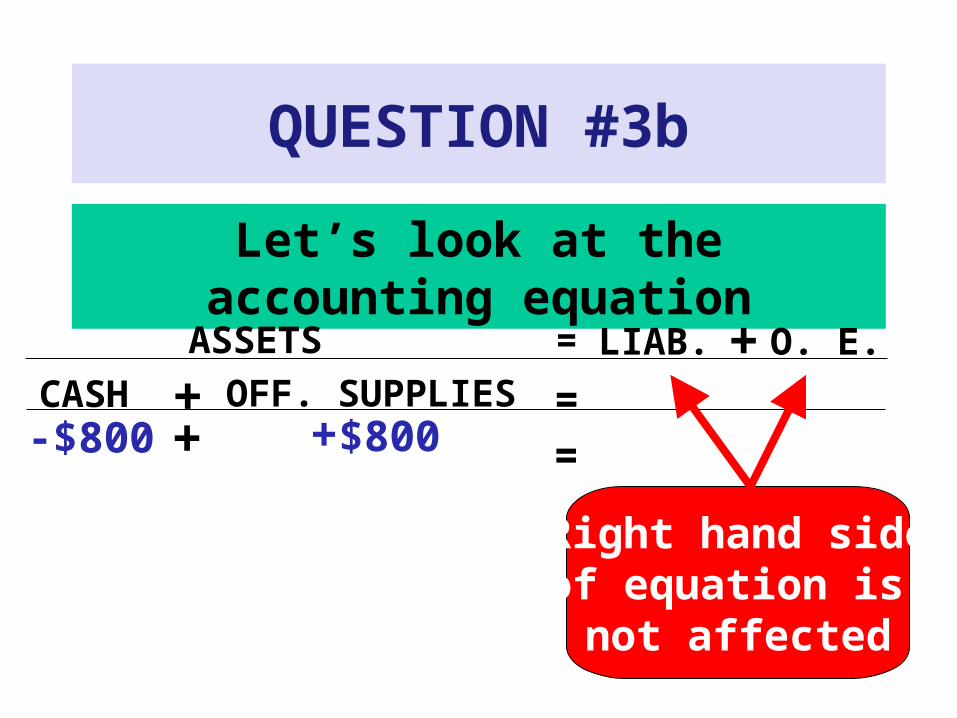

Let’s look at the accounting equation

ASSETS = LIAB. O. E.

-$800CASH =

=+ OFF. SUPPLIES

+$800

Right hand sideof equation is not affected

+

+

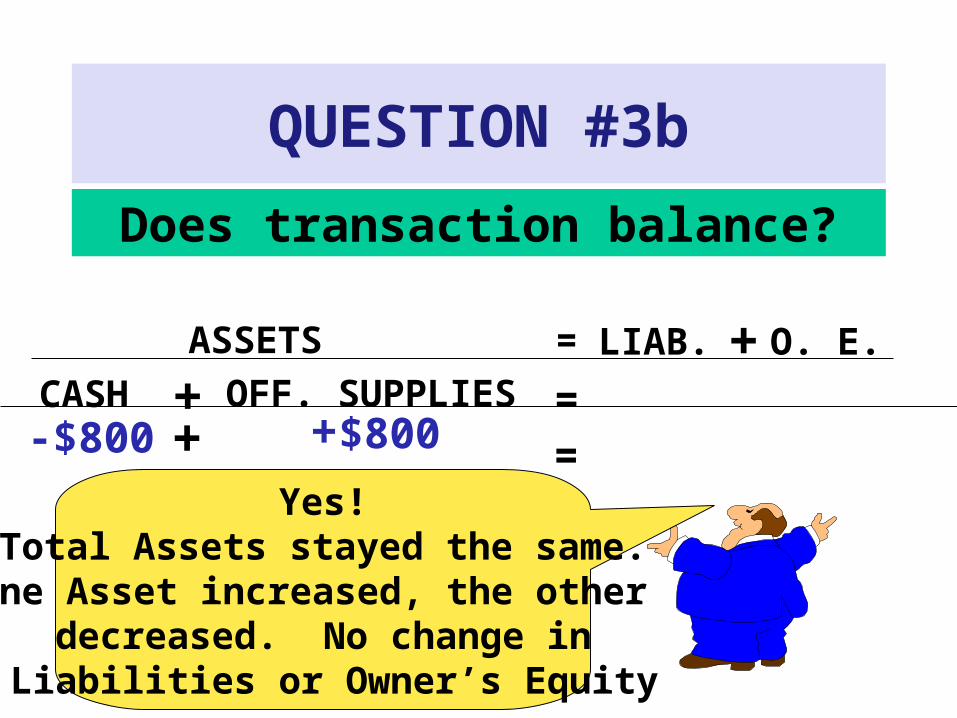

QUESTION #3b

Does transaction balance?

ASSETS = LIAB. O. E.

-$800CASH =

=Yes!

Total Assets stayed the same.One Asset increased, the other

decreased. No change in Liabilities or Owner’s Equity

OFF. SUPPLIES+$800

+++

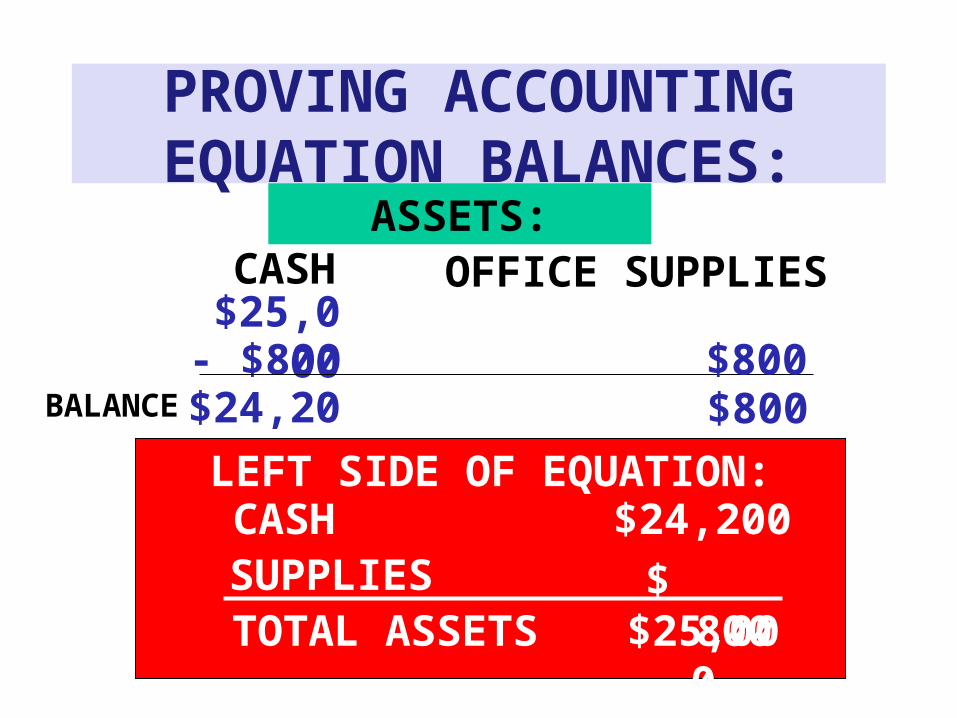

PROVING ACCOUNTING EQUATION BALANCES:

ASSETS:CASH

$25,000- $800

$24,200

OFFICE SUPPLIES

$800$800BALANCE

LEFT SIDE OF EQUATION:CASH $24,200SUPPLIES $ 800TOTAL ASSETS $25,000

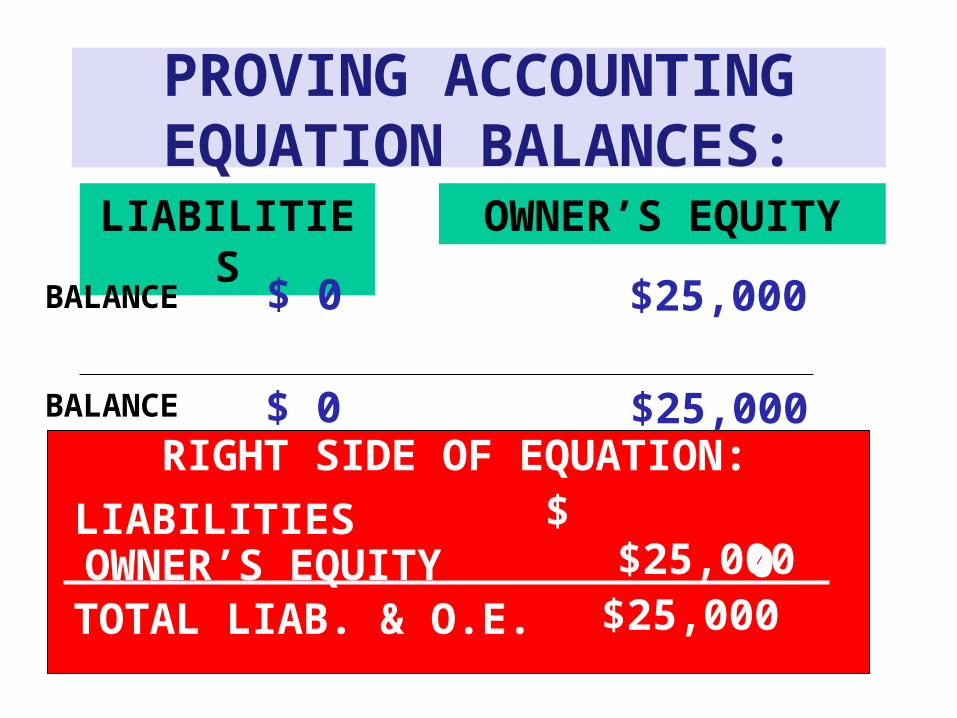

PROVING ACCOUNTING EQUATION BALANCES:

LIABILITIES

$25,000

$25,000BALANCE

OWNER’S EQUITY

RIGHT SIDE OF EQUATION:

LIABILITIES $ 0OWNER’S EQUITY $25,000

TOTAL LIAB. & O.E. $25,000

$ 0

BALANCE $ 0

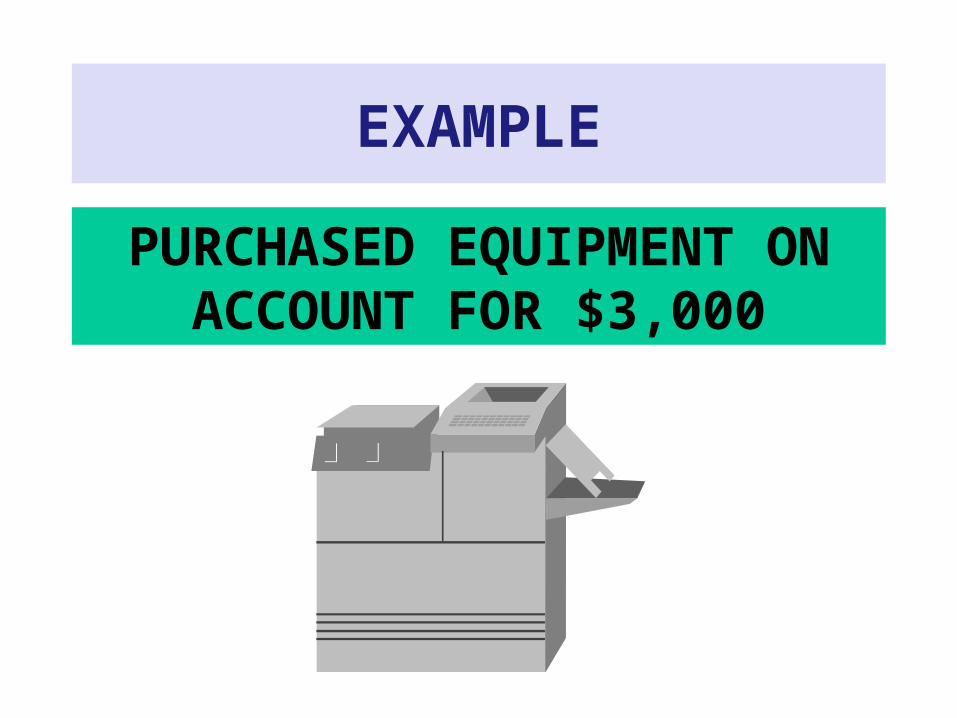

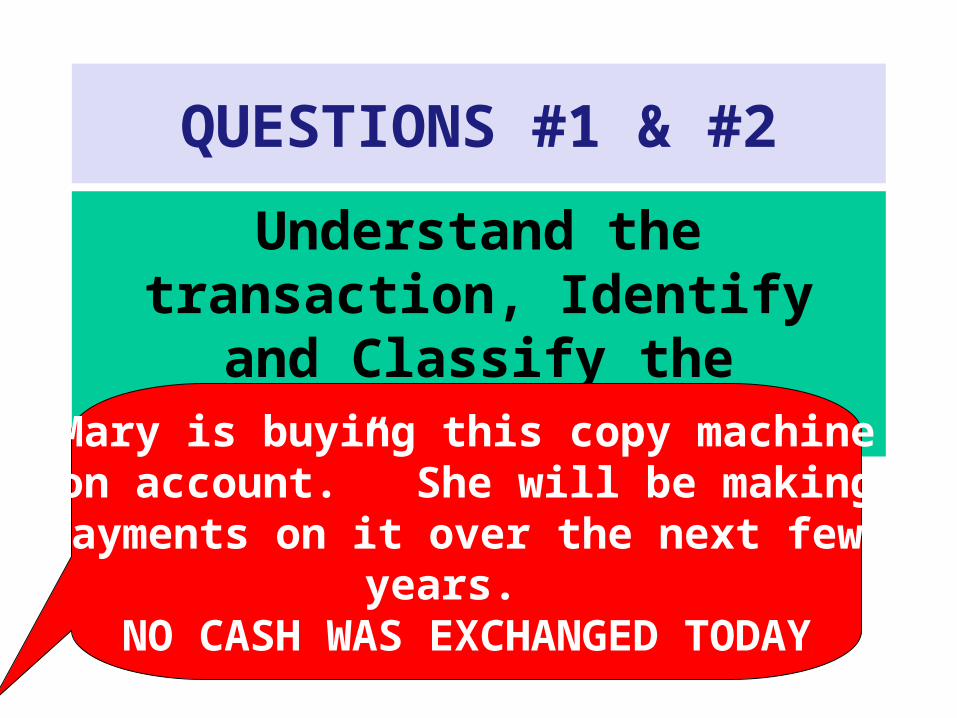

EXAMPLE

PURCHASED EQUIPMENT ON ACCOUNT FOR $3,000

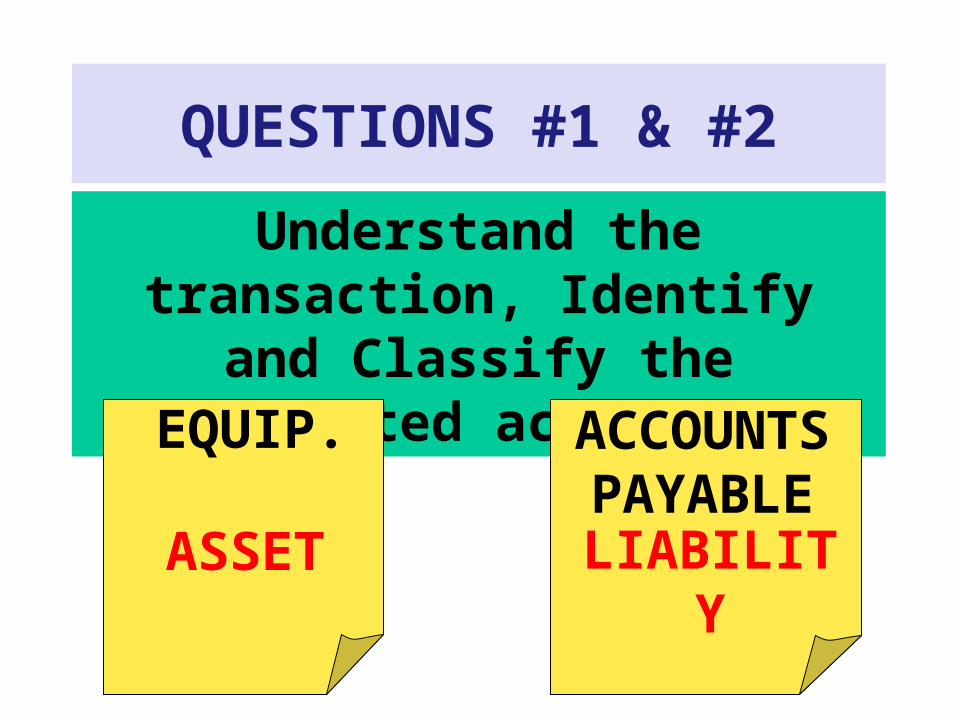

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected

accountsMary is buying this copy machine“on account.” She will be making payments on it over the next few

years. NO CASH WAS EXCHANGED TODAY

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected

accountsEQUIP. ACCOUNTS

PAYABLEASSET LIABILITY

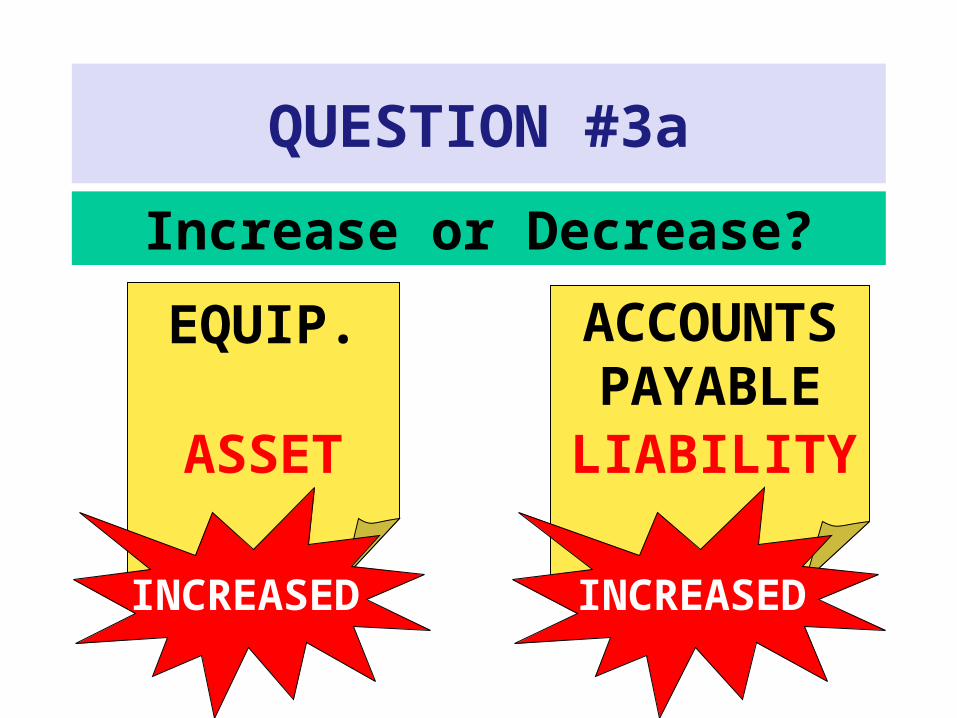

QUESTION #3a

Increase or Decrease?

EQUIP. ACCOUNTS PAYABLE

ASSET LIABILITY

INCREASED INCREASED

QUESTION #3b

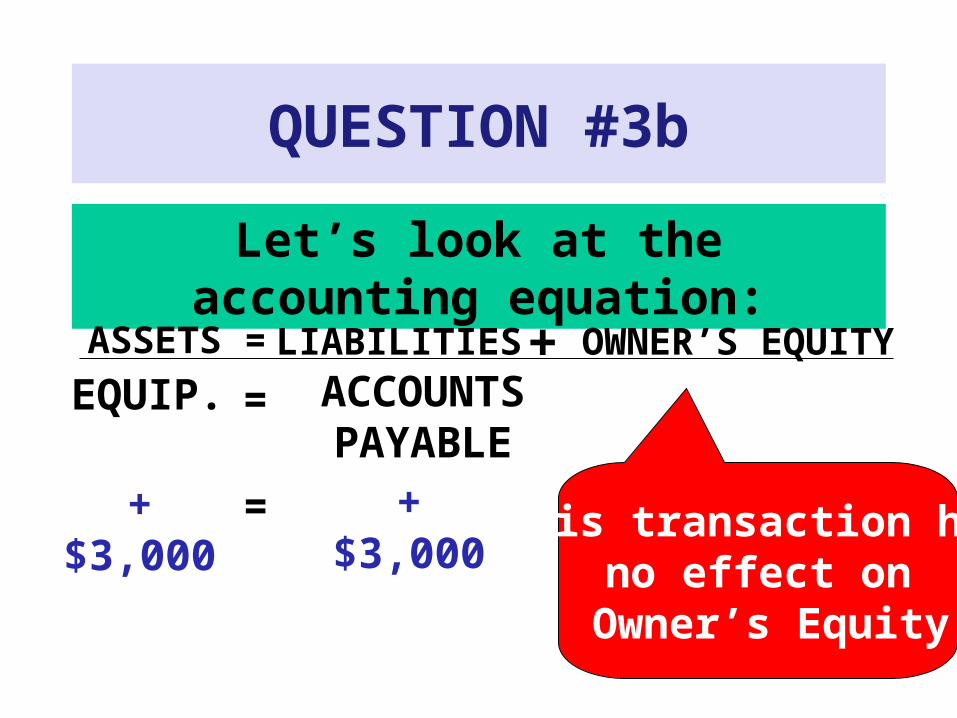

Let’s look at the accounting equation:

ASSETS = LIABILITIES OWNER’S EQUITY

+ $3,000

EQUIP. =

=

ACCOUNTS PAYABLE

+ $3,000 This transaction hadno effect on

Owner’s Equity

+

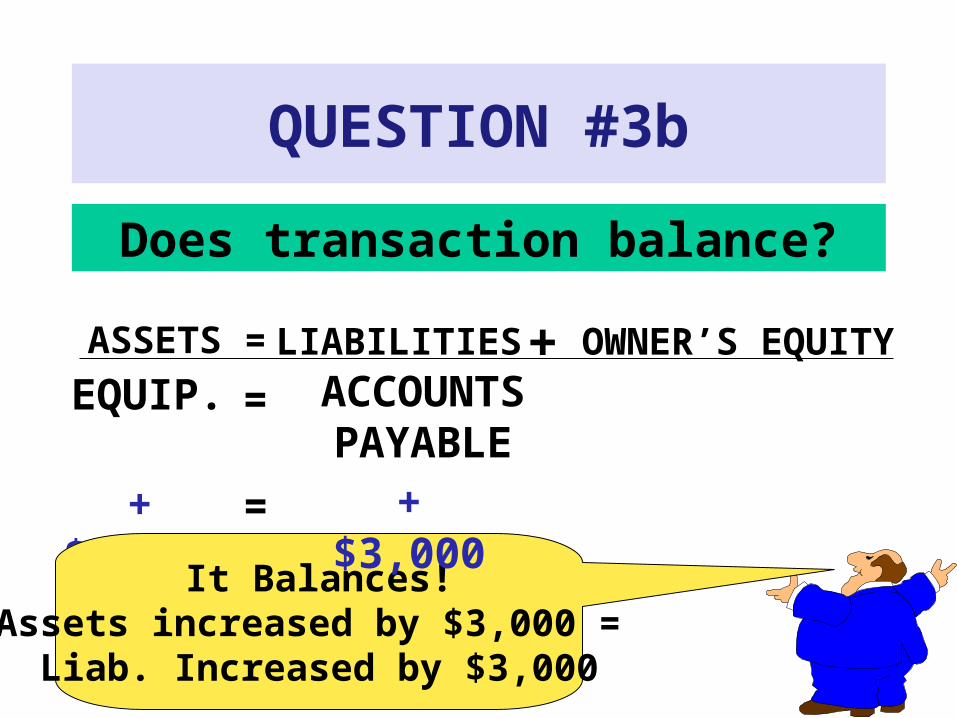

QUESTION #3b

Does transaction balance?

ASSETS = LIABILITIES OWNER’S EQUITY

+ $3,000

EQUIP. =

=

It Balances!Assets increased by $3,000 =

Liab. Increased by $3,000

ACCOUNTS PAYABLE

+ $3,000

+

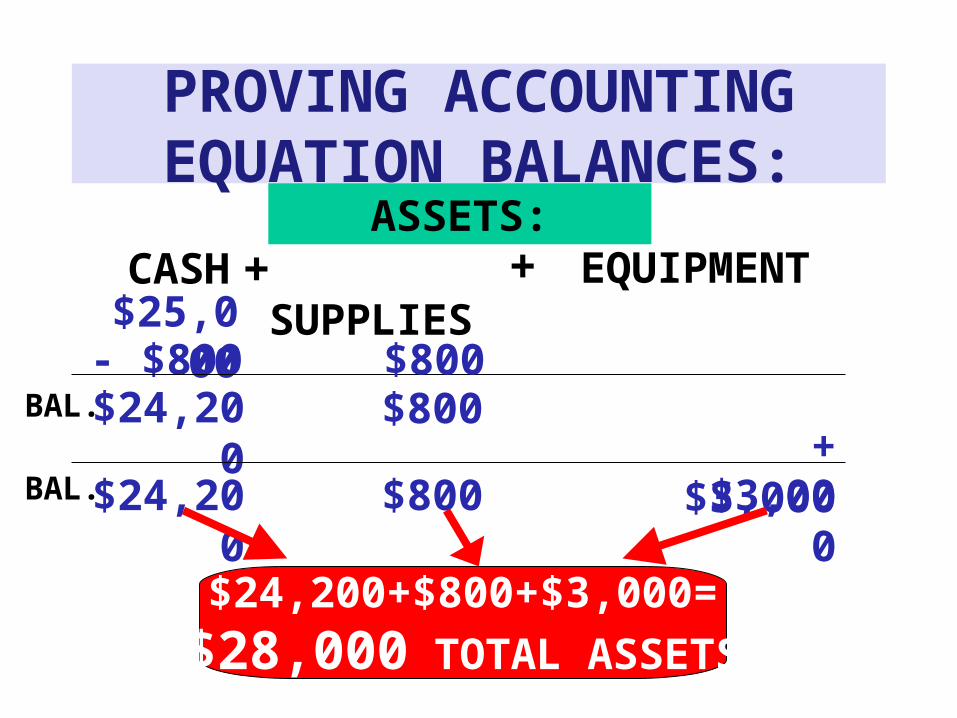

PROVING ACCOUNTING EQUATION BALANCES:

ASSETS:CASH

$25,000- $800

$24,200

SUPPLIES

$800$800BAL.

SUPPLIES $ 800$25,000

EQUIPMENT

+$3,000$24,200 $800 $3,000

$24,200+$800+$3,000=

$28,000 TOTAL ASSETS

BAL.

+ +

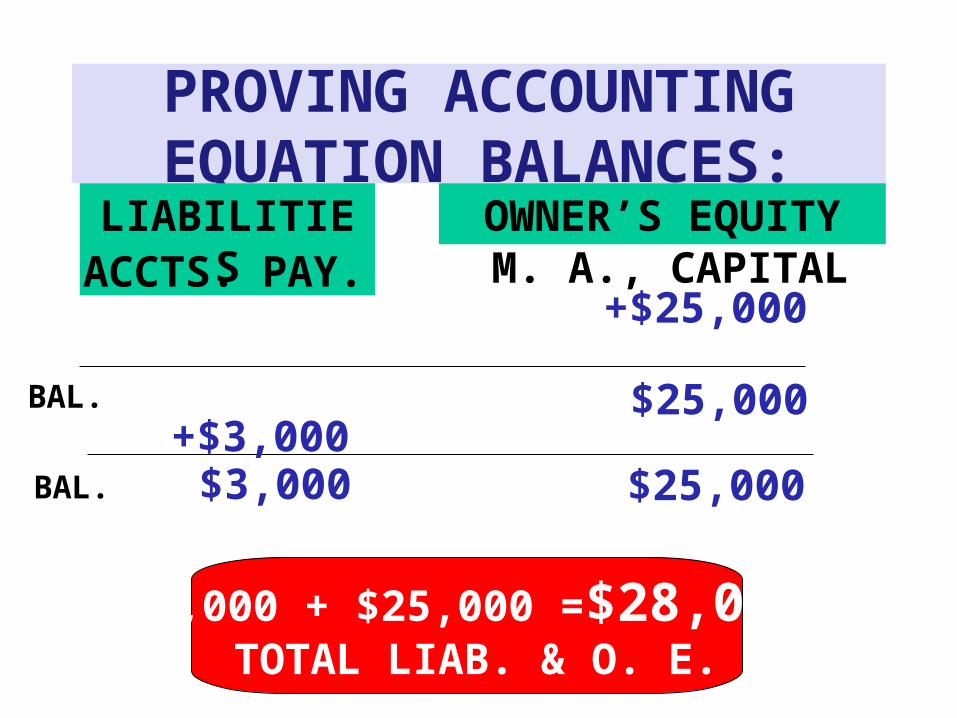

PROVING ACCOUNTING EQUATION BALANCES:

LIABILITIES

+$25,000

$25,000BAL.

OWNER’S EQUITYACCTS. PAY. M. A., CAPITAL

+$3,000$3,000 $25,000BAL.

$3,000 + $25,000 =$28,000 TOTAL LIAB. & O. E.

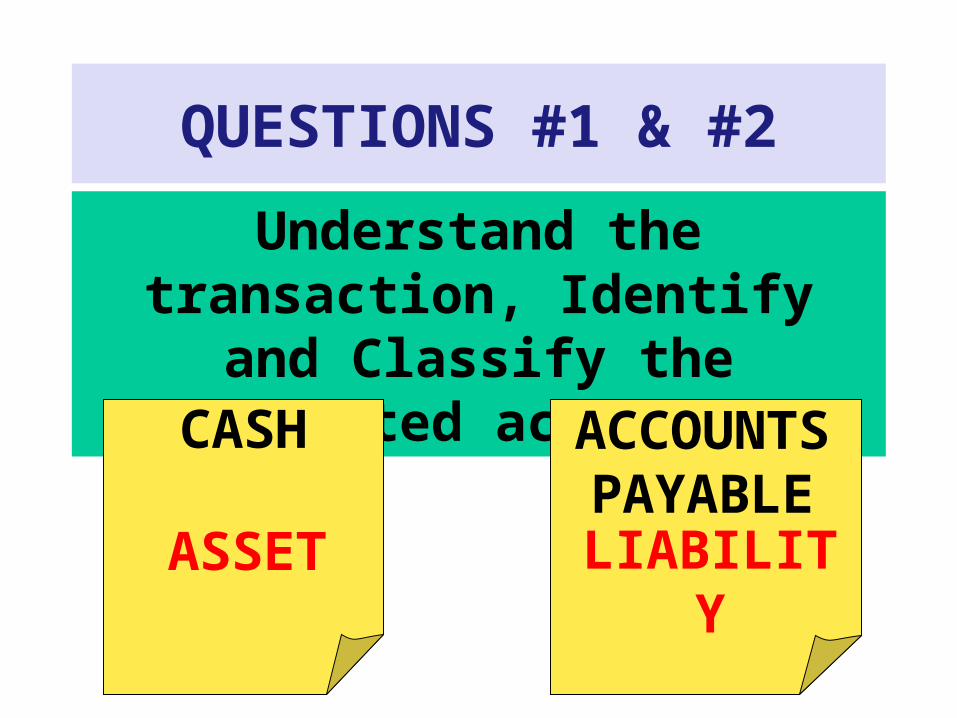

EXAMPLE

MADE $400 PAYMENT ON EQUIPMENT

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected

accountsCASH ACCOUNTS

PAYABLEASSET LIABILITY

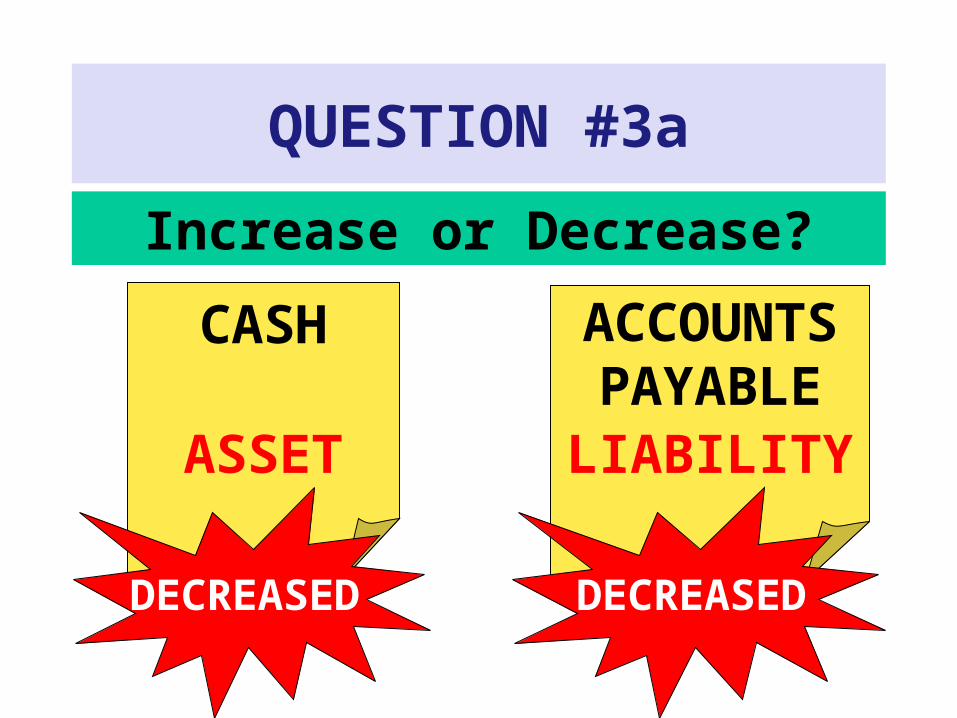

QUESTION #3a

Increase or Decrease?

CASH ACCOUNTS PAYABLE

ASSET LIABILITY

DECREASED DECREASED

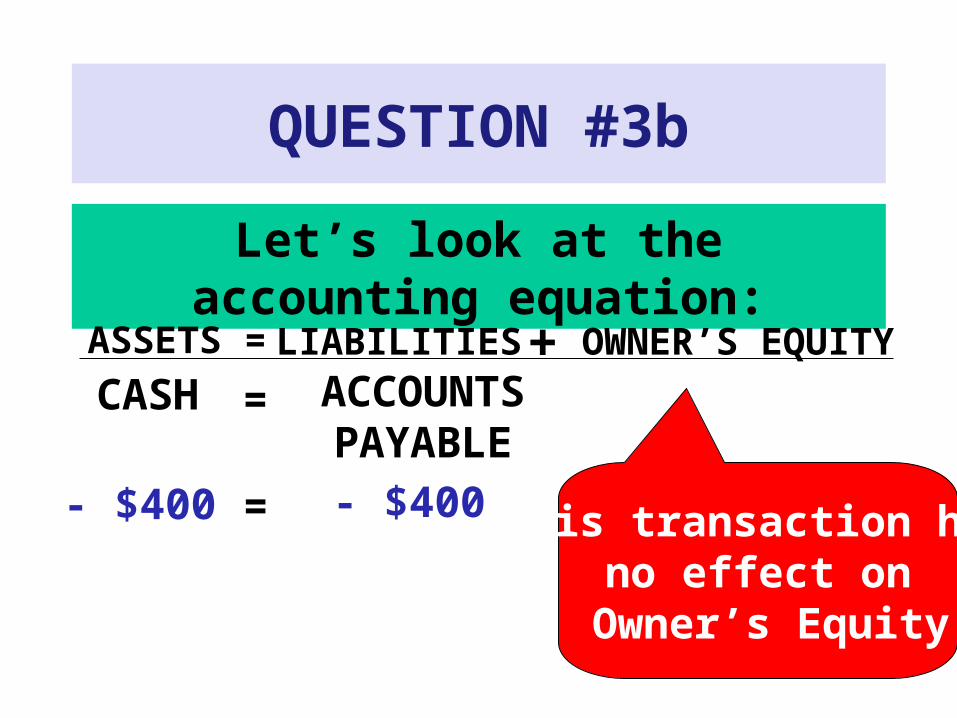

QUESTION #3b

Let’s look at the accounting equation:

ASSETS = LIABILITIES OWNER’S EQUITY

- $400

CASH =

=

ACCOUNTS PAYABLE

- $400 This transaction hadno effect on

Owner’s Equity

+

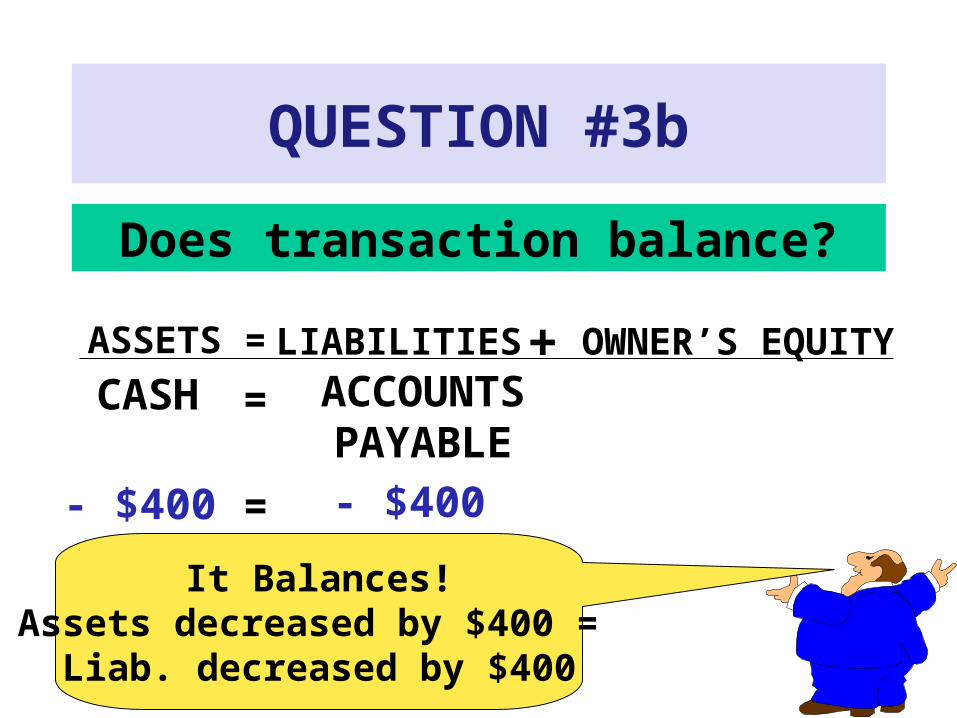

QUESTION #3b

Does transaction balance?

ASSETS = LIABILITIES OWNER’S EQUITY

- $400

CASH =

=

It Balances!Assets decreased by $400 =

Liab. decreased by $400

ACCOUNTS PAYABLE

- $400

+

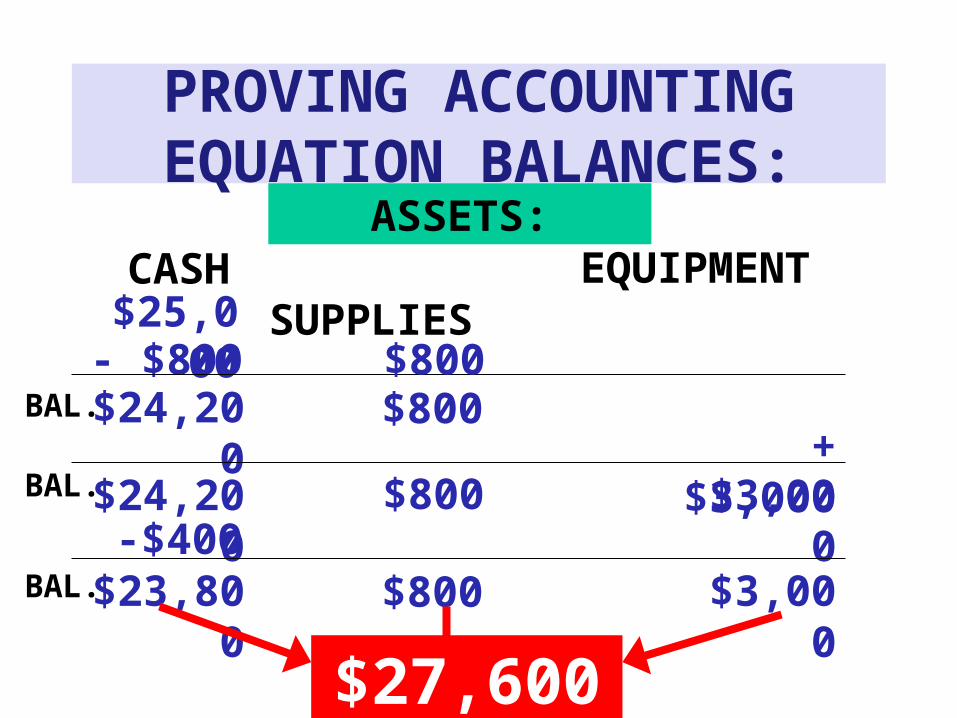

PROVING ACCOUNTING EQUATION BALANCES:

ASSETS:CASH

$25,000- $800

$24,200

SUPPLIES

$800$800BAL.

SUPPLIES

EQUIPMENT

+$3,000$24,200 $800 $3,000

-$400$23,800 $800 $3,000

$27,600

BAL.

BAL.

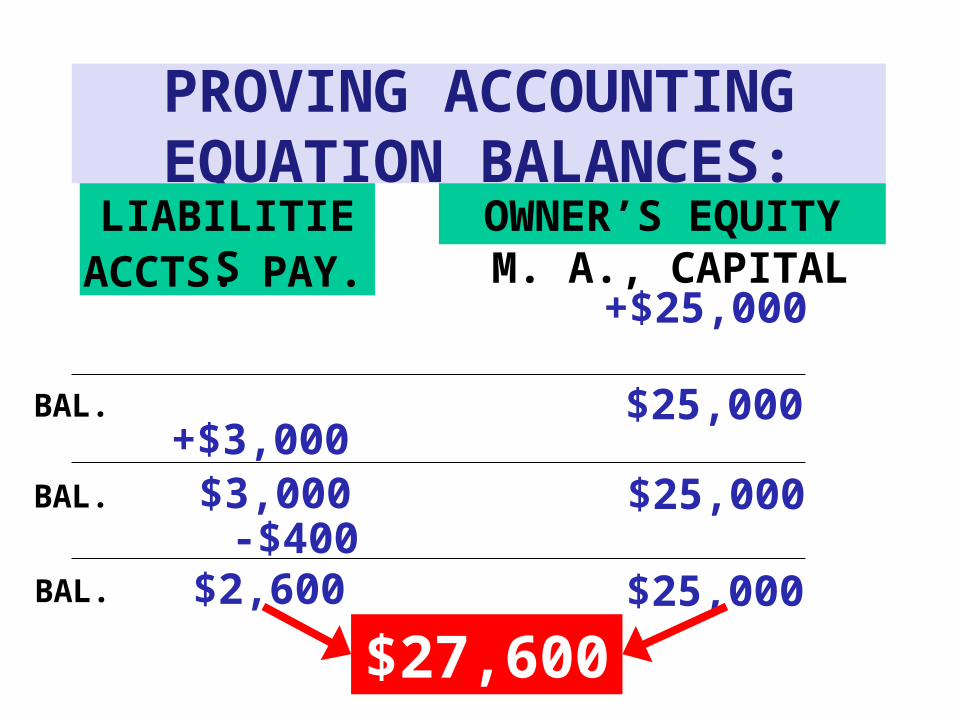

PROVING ACCOUNTING EQUATION BALANCES:

LIABILITIES

+$25,000

$25,000BAL.

OWNER’S EQUITYACCTS. PAY. M. A., CAPITAL

+$3,000$3,000 $25,000BAL.

$25,000BAL.

-$400$2,600

$27,600

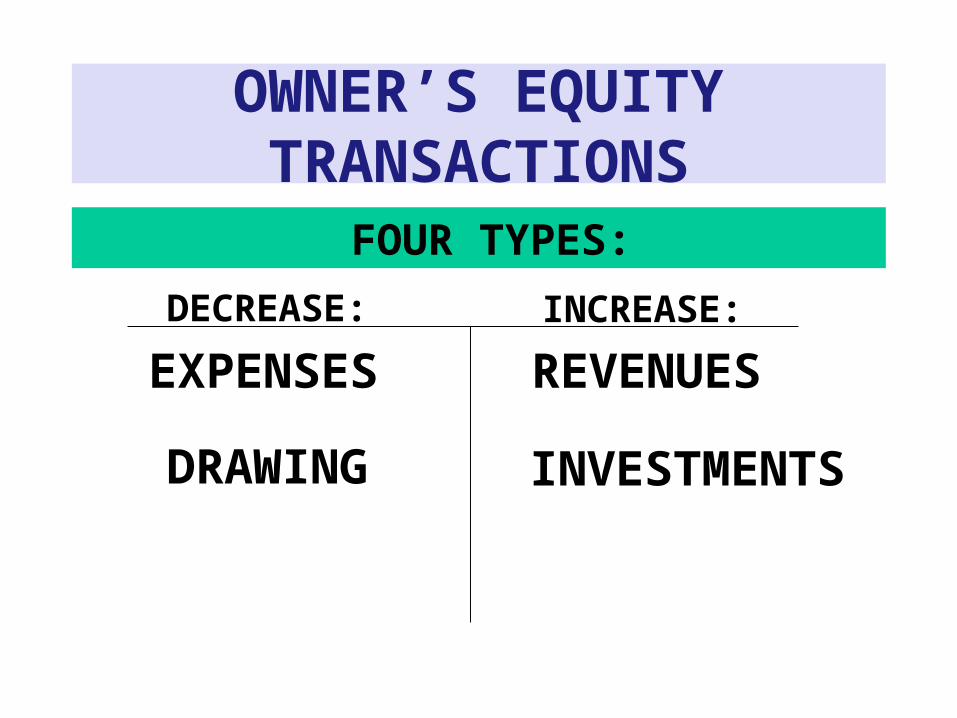

OWNER’S EQUITY TRANSACTIONS

FOUR TYPES:

DECREASE:

EXPENSES

DRAWING

INCREASE:

REVENUES

INVESTMENTS

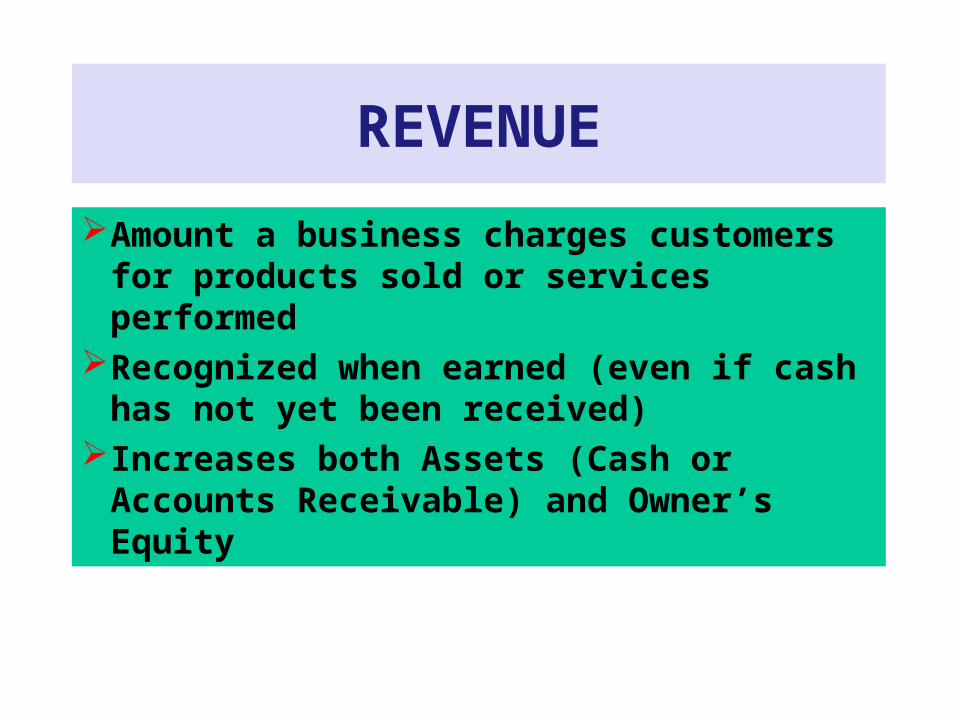

REVENUE

Amount a business charges customers for products sold or services performed

Recognized when earned (even if cash has not yet been received)

Increases both Assets (Cash or Accounts Receivable) and Owner’s Equity

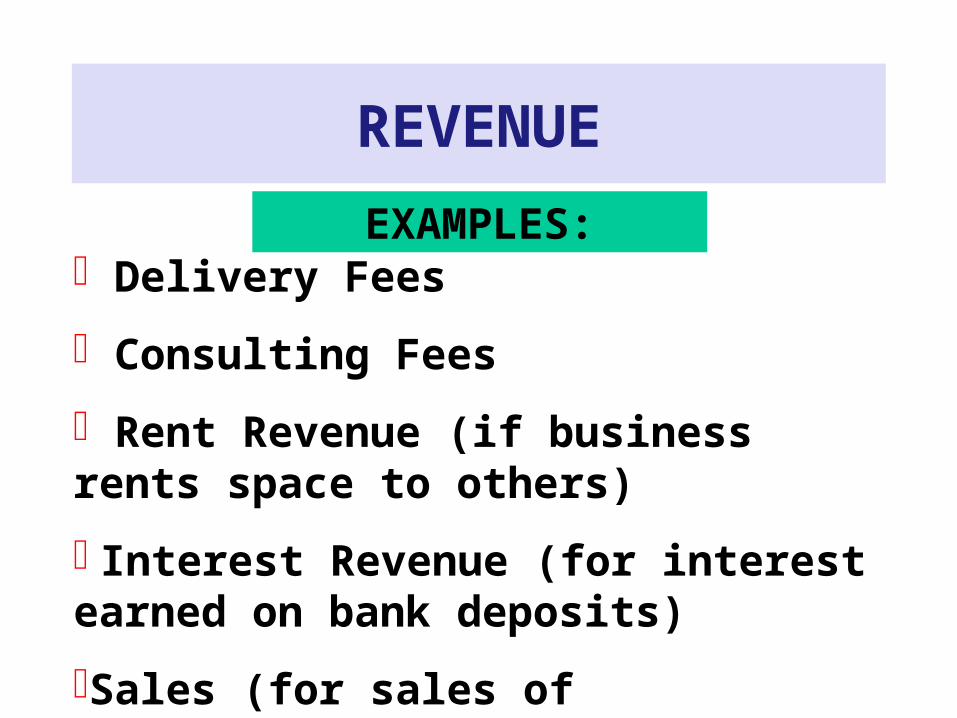

REVENUE

EXAMPLES: Delivery Fees

Consulting Fees

Rent Revenue (if business rents space to others)

Interest Revenue (for interest earned on bank deposits)

Sales (for sales of merchandise)

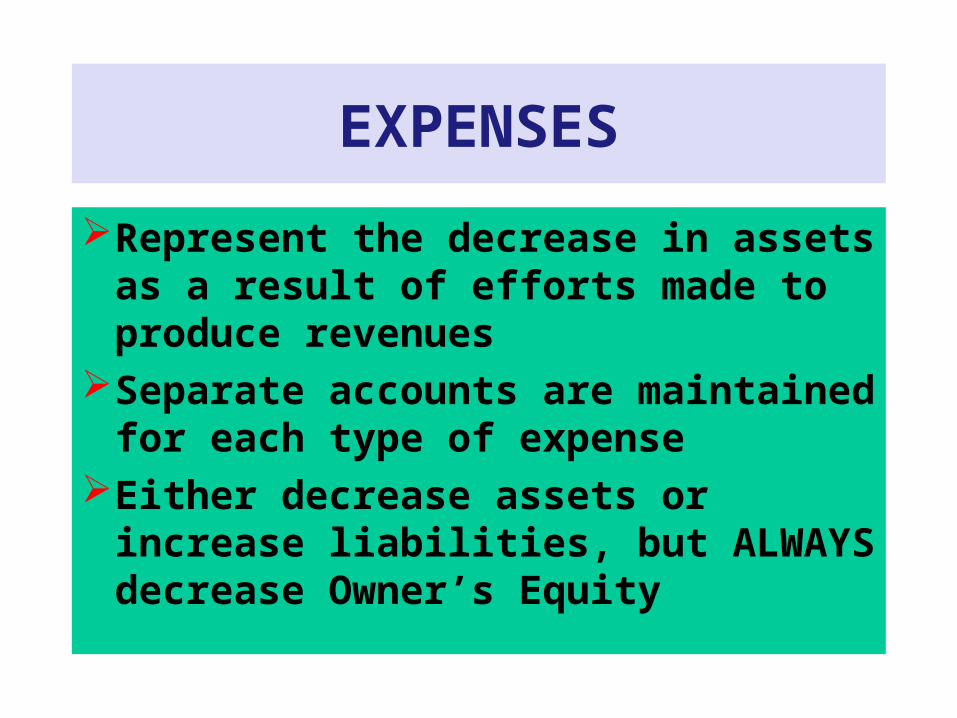

EXPENSES

Represent the decrease in assets as a result of efforts made to produce revenues

Separate accounts are maintained for each type of expense

Either decrease assets or increase liabilities, but ALWAYS decrease Owner’s Equity

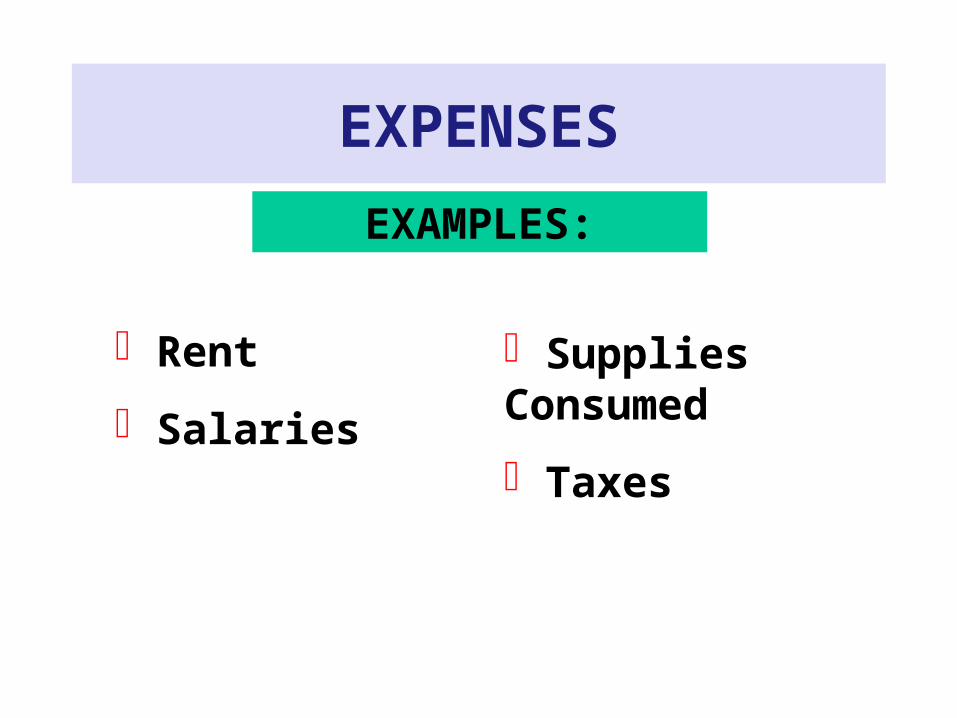

EXPENSES

EXAMPLES:

Rent

Salaries

Supplies Consumed

Taxes

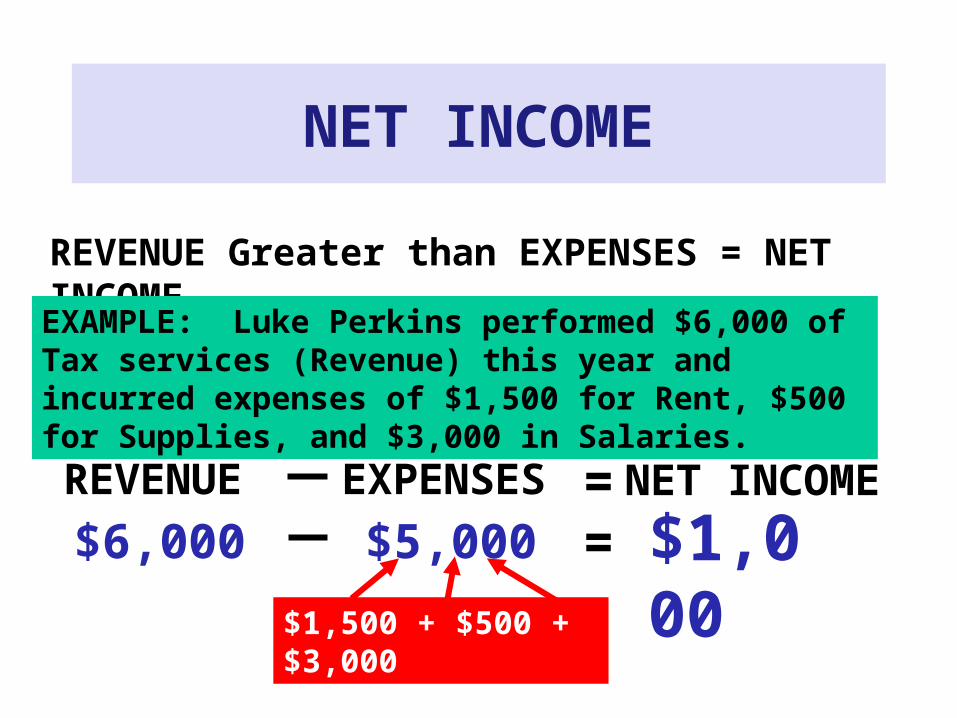

NET INCOME

REVENUE Greater than EXPENSES = NET INCOME

EXAMPLE: Luke Perkins performed $6,000 of Tax services (Revenue) this year and incurred expenses of $1,500 for Rent, $500 for Supplies, and $3,000 in Salaries.

REVENUE EXPENSES = NET INCOME

$6,000 $5,000 = $1,000$1,500 + $500 + $3,000

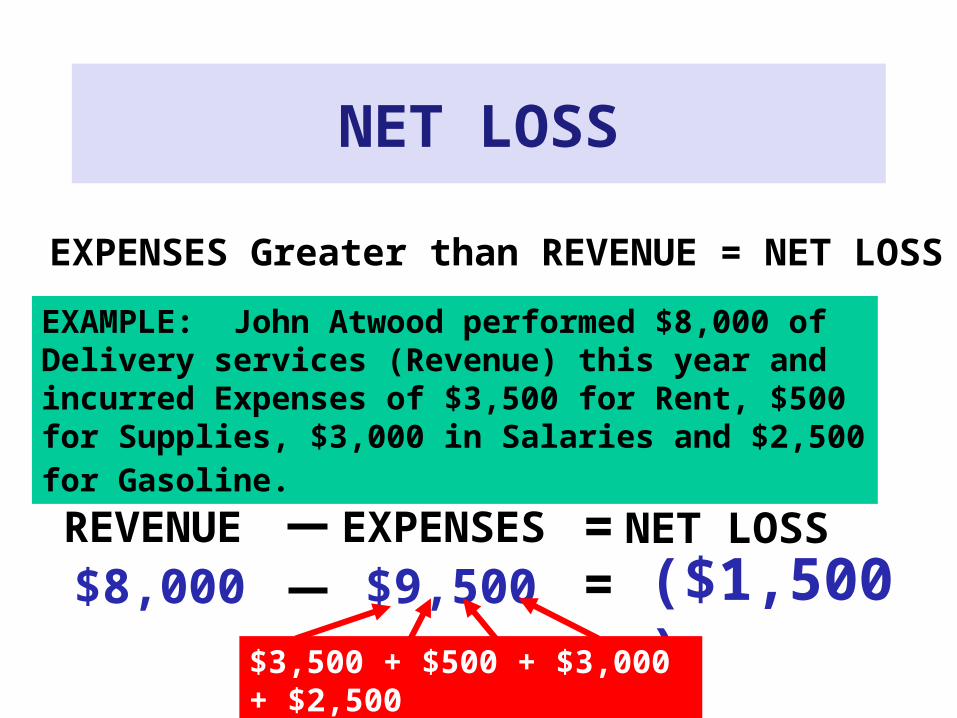

NET LOSS

EXPENSES Greater than REVENUE = NET LOSS

EXAMPLE: John Atwood performed $8,000 of Delivery services (Revenue) this year and incurred Expenses of $3,500 for Rent, $500 for Supplies, $3,000 in Salaries and $2,500 for Gasoline.

REVENUE EXPENSES = NET LOSS

$8,000 $9,500 = ($1,500)$3,500 + $500 + $3,000 + $2,500

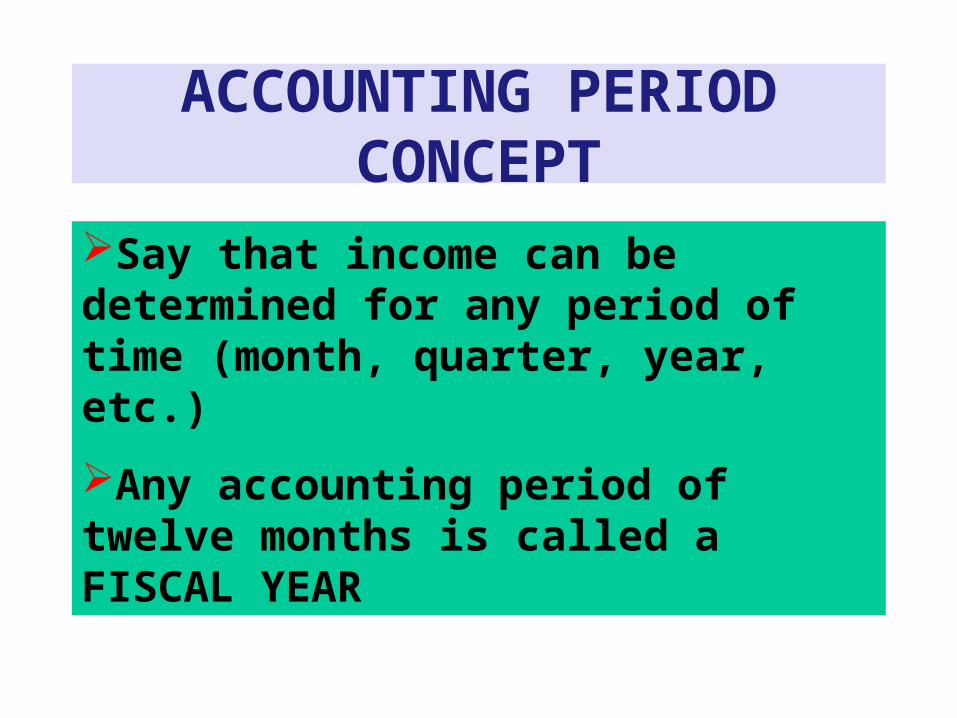

ACCOUNTING PERIOD CONCEPT

Say that income can be determined for any period of time (month, quarter, year, etc.)

Any accounting period of twelve months is called a FISCAL YEAR

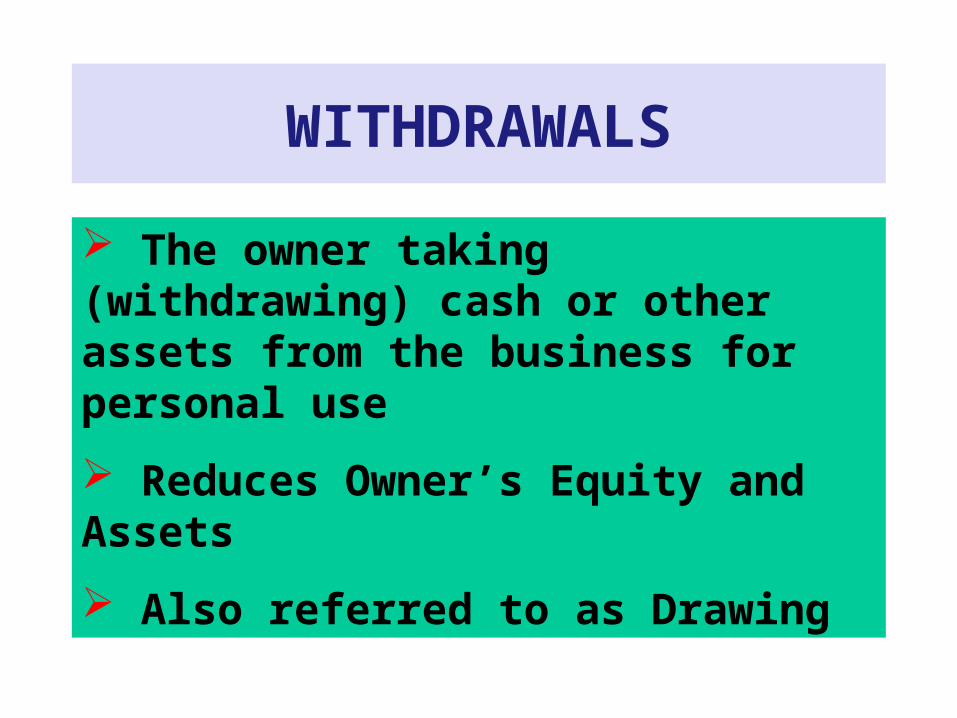

WITHDRAWALS

The owner taking (withdrawing) cash or other assets from the business for personal use

Reduces Owner’s Equity and Assets

Also referred to as Drawing

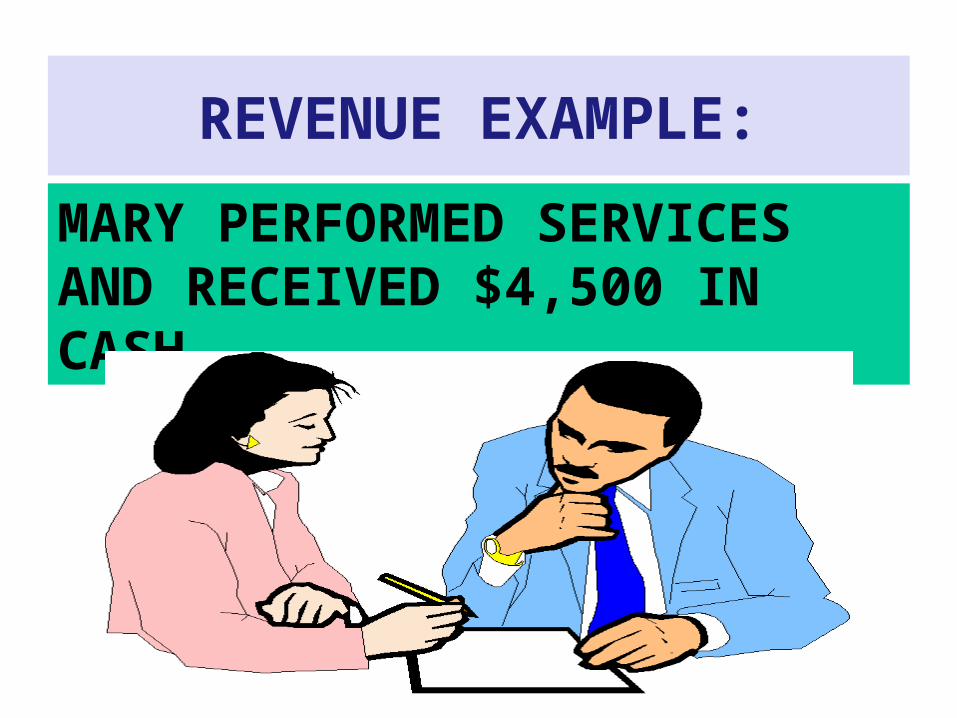

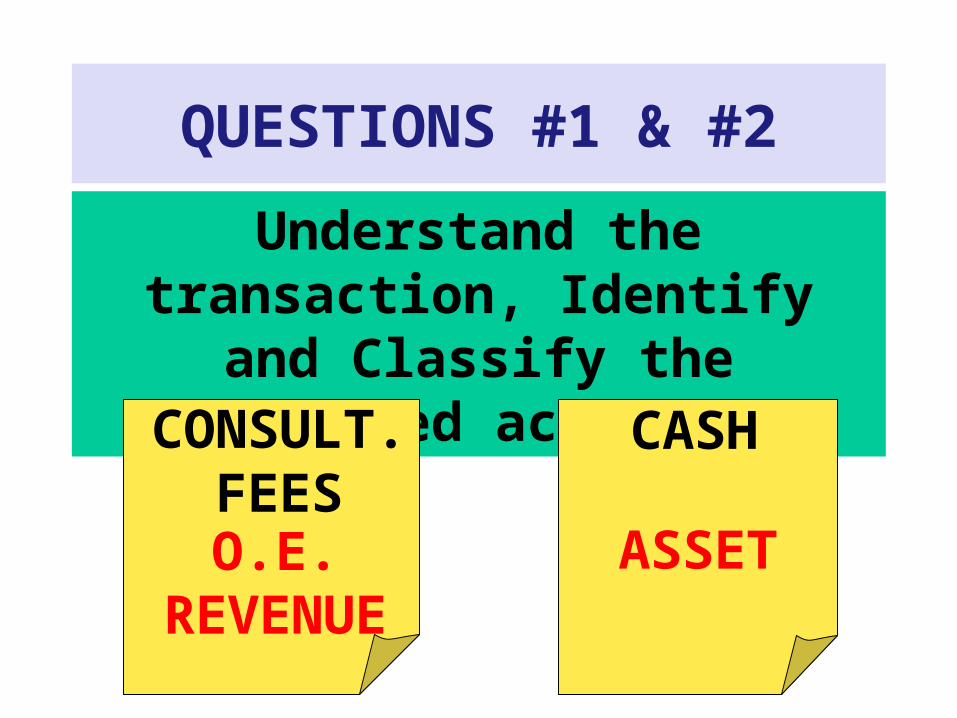

REVENUE EXAMPLE:

MARY PERFORMED SERVICES AND RECEIVED $4,500 IN CASH

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected

accountsCONSULT.

FEESCASH

O.E. REVENUE

ASSET

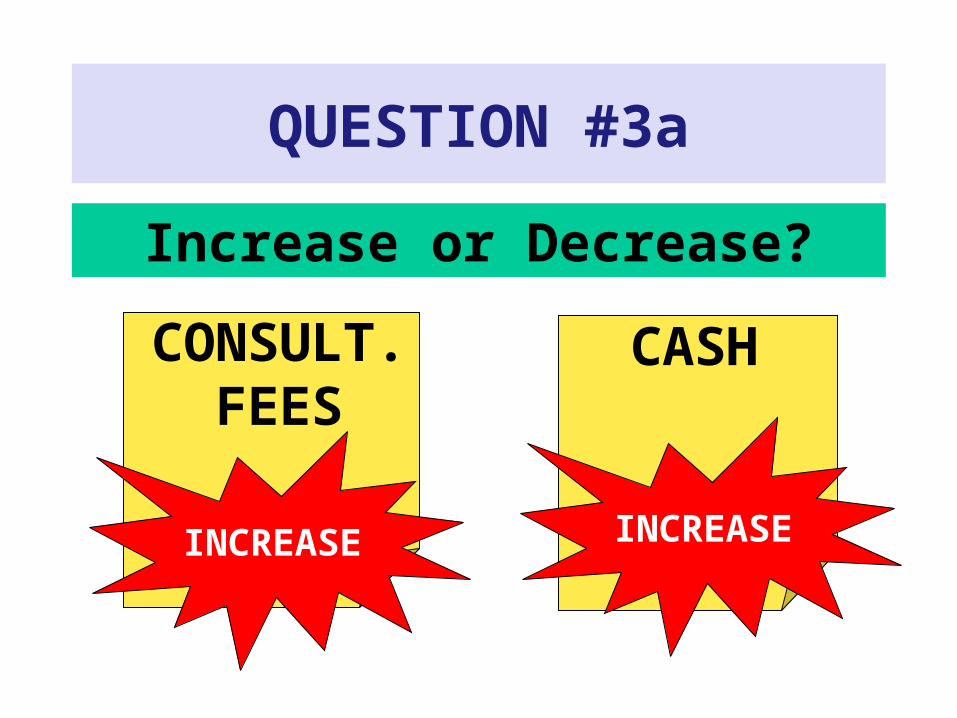

QUESTION #3a

Increase or Decrease?

CONSULT. FEES

CASH

INCREASE INCREASE

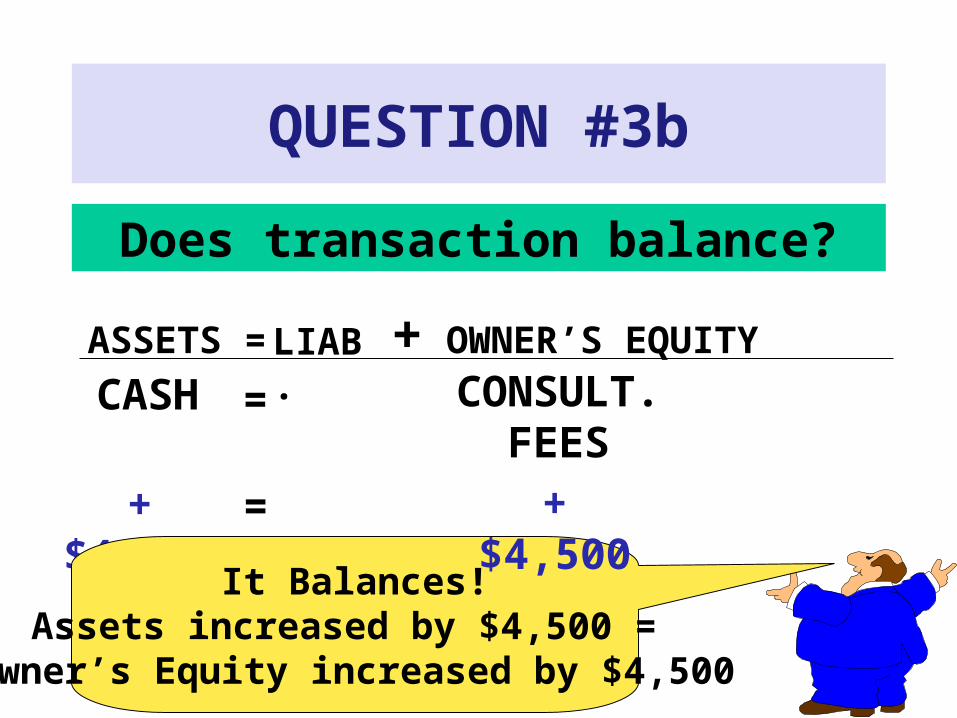

QUESTION #3b

Does transaction balance?

ASSETS = LIAB. OWNER’S EQUITY

+$4,500

CASH =

=

It Balances!Assets increased by $4,500 =

Owner’s Equity increased by $4,500

CONSULT. FEES

+$4,500

+

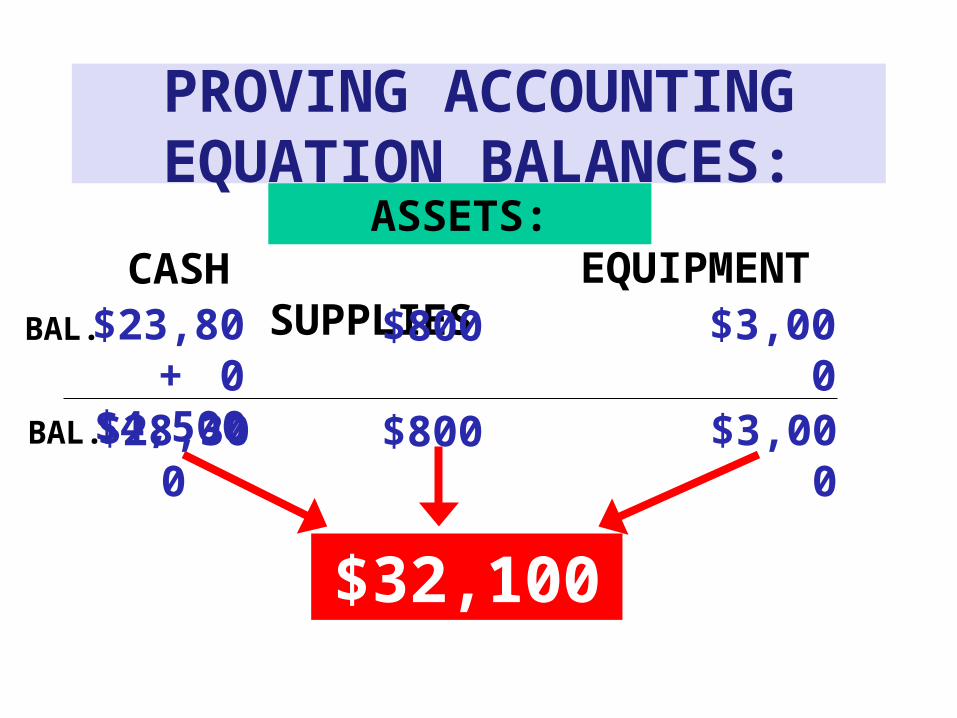

PROVING ACCOUNTING EQUATION BALANCES:

ASSETS:CASH SUPPLIES EQUIPMENT

$23,800 $800 $3,000

$32,100

BAL.

+ $4,500BAL.$28,300 $800 $3,000

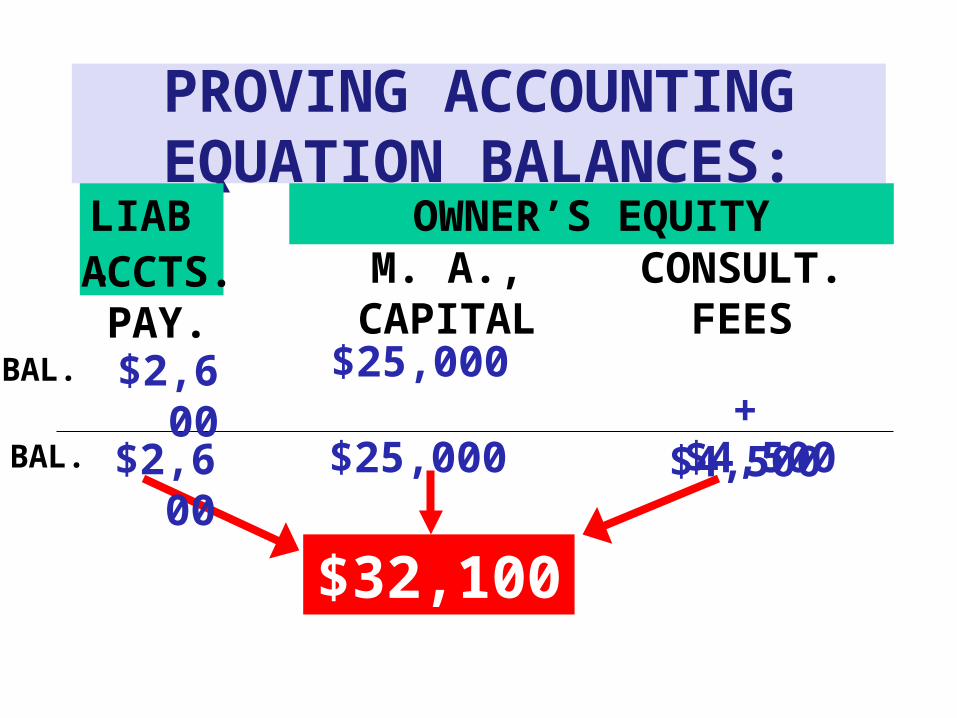

PROVING ACCOUNTING EQUATION BALANCES:

LIAB. OWNER’S EQUITYACCTS.

PAY.M. A.,

CAPITAL$25,000BAL. $2,600

$32,100

CONSULT. FEES

+ $4,500BAL. $2,600 $25,000 $4,500

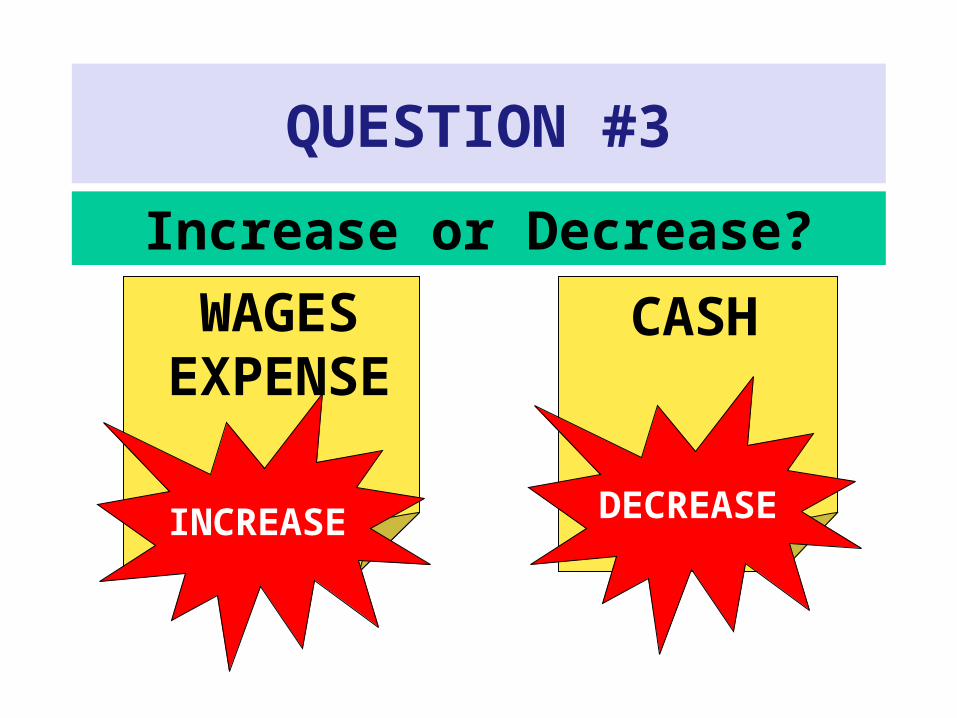

EXPENSE EXAMPLE

MARY ADAMS PAID HER ASSISTANT $750 IN WAGES

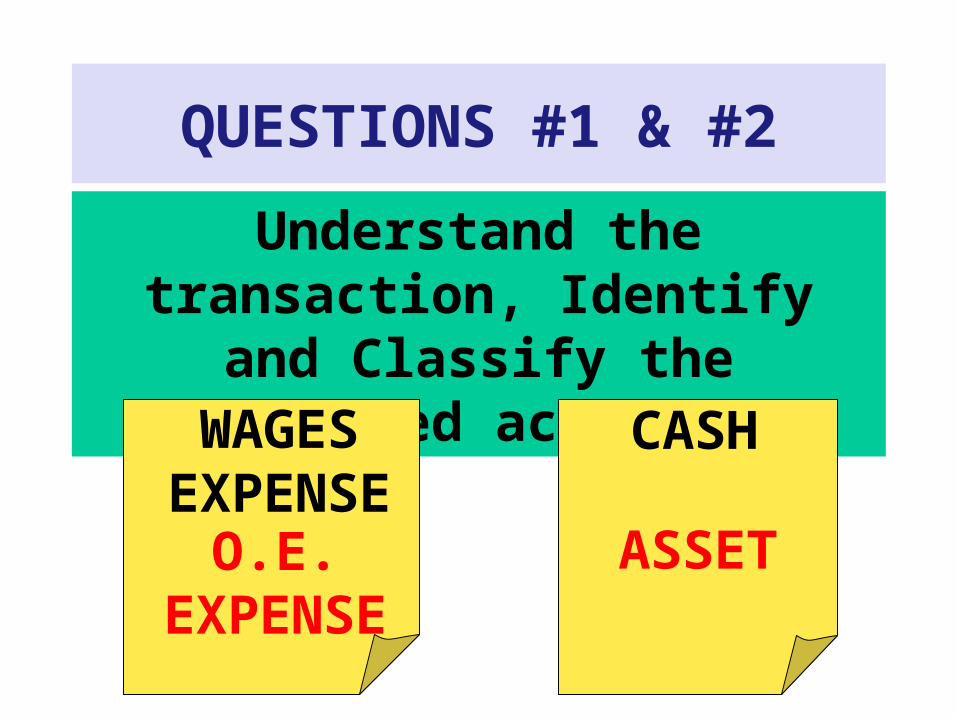

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected

accountsWAGES

EXPENSECASH

O.E. EXPENSE

ASSET

QUESTION #3

Increase or Decrease?

WAGES EXPENSE

CASH

INCREASE DECREASE

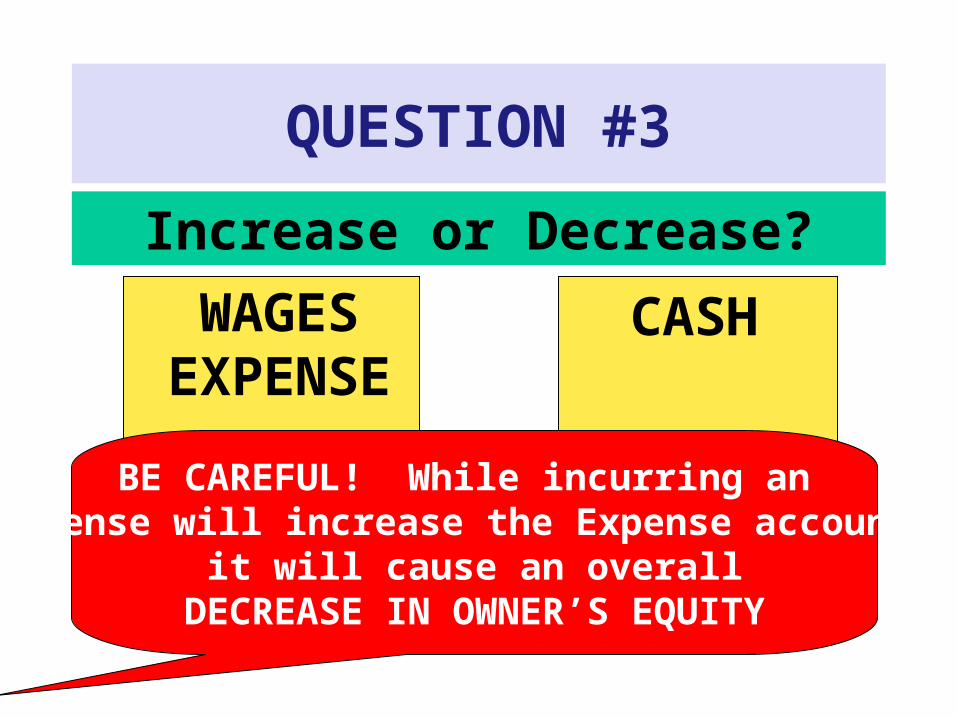

QUESTION #3

Increase or Decrease?

WAGES EXPENSE

CASH

BE CAREFUL! While incurring an expense will increase the Expense account,

it will cause an overallDECREASE IN OWNER’S EQUITY

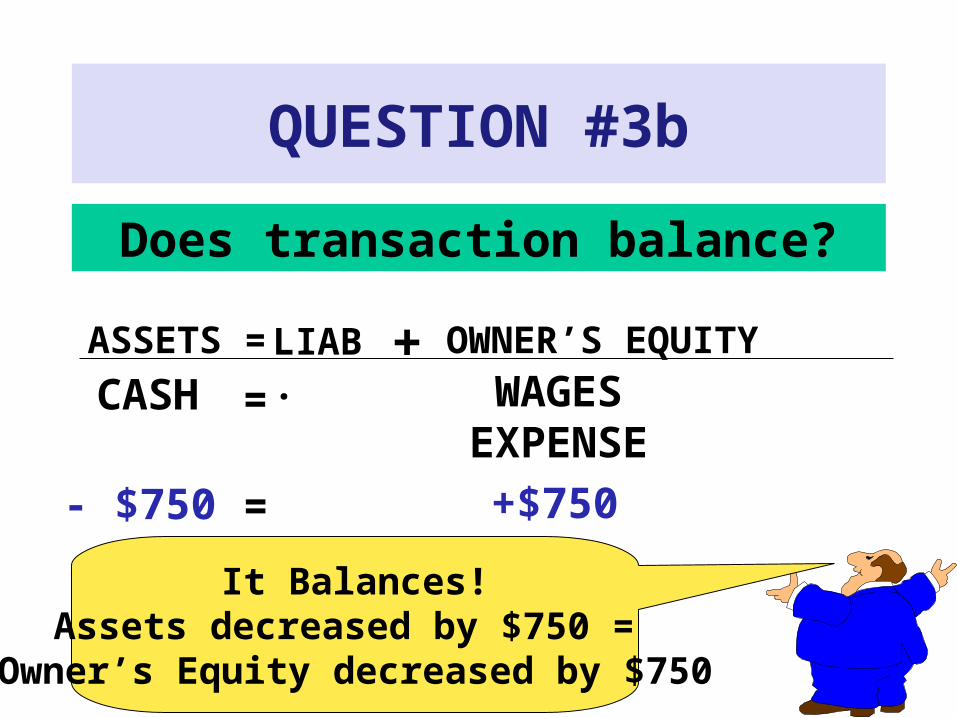

QUESTION #3b

Does transaction balance?

ASSETS = LIAB. OWNER’S EQUITY

- $750

CASH =

=

It Balances!Assets decreased by $750 =

Owner’s Equity decreased by $750

WAGES EXPENSE

+$750

+

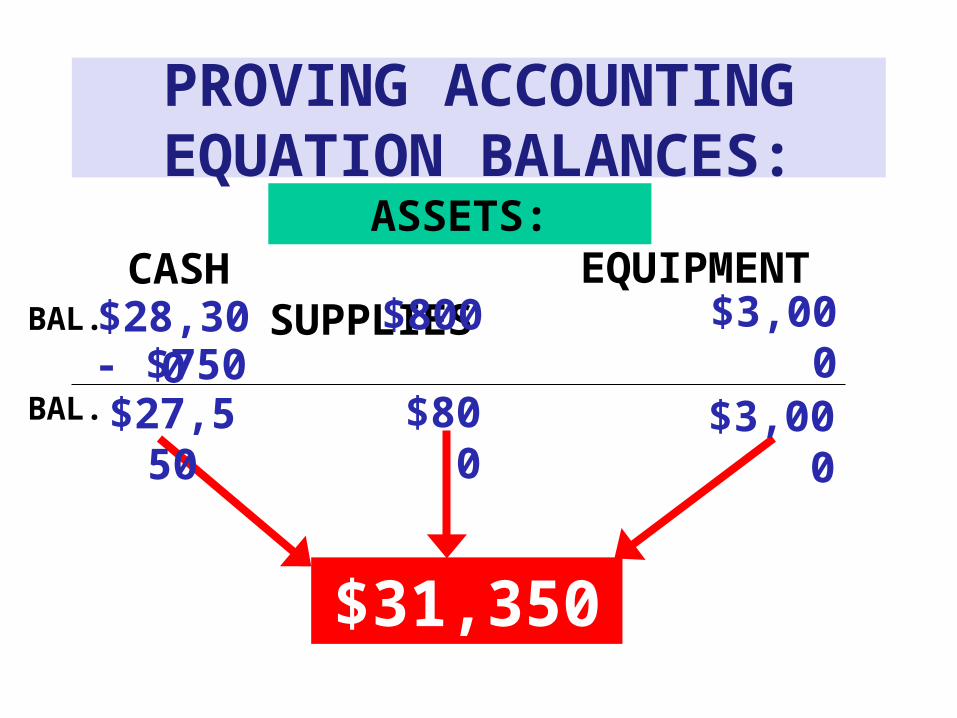

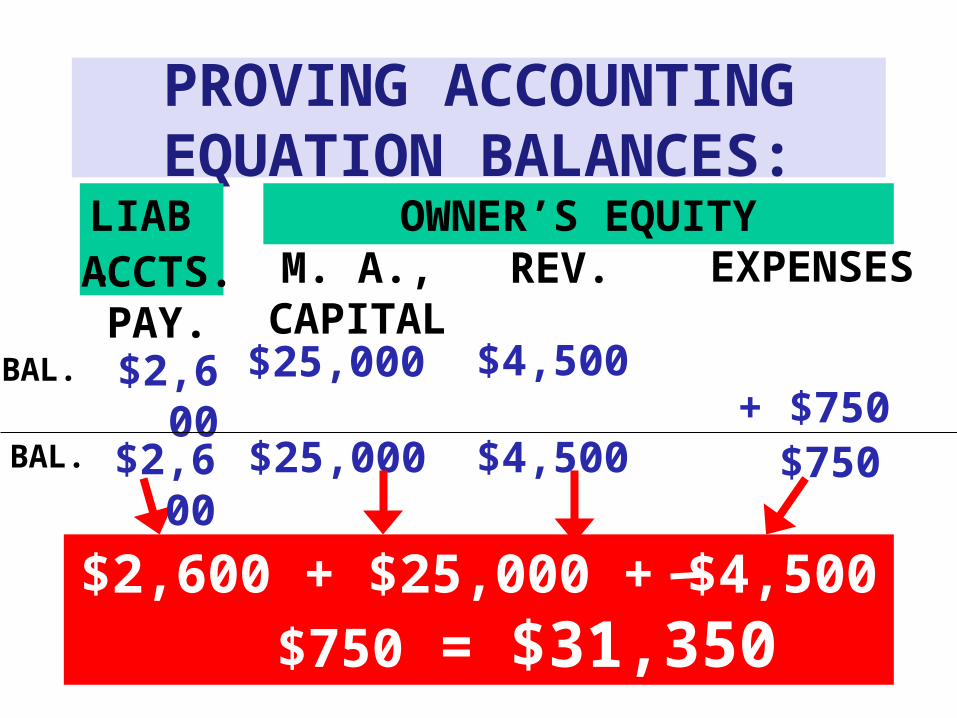

PROVING ACCOUNTING EQUATION BALANCES:

ASSETS:CASH SUPPLIES EQUIPMENT

$31,350

BAL.$28,300 $800 $3,000- $750

$27,550 $800 $3,000BAL.

PROVING ACCOUNTING EQUATION BALANCES:

LIAB. OWNER’S EQUITYACCTS.

PAY.M. A.,

CAPITAL$25,000BAL. $2,600

$2,600 + $25,000 + $4,500 $750 = $31,350

REV.

BAL. $2,600 $25,000

$4,500

$4,500

EXPENSES

+ $750$750

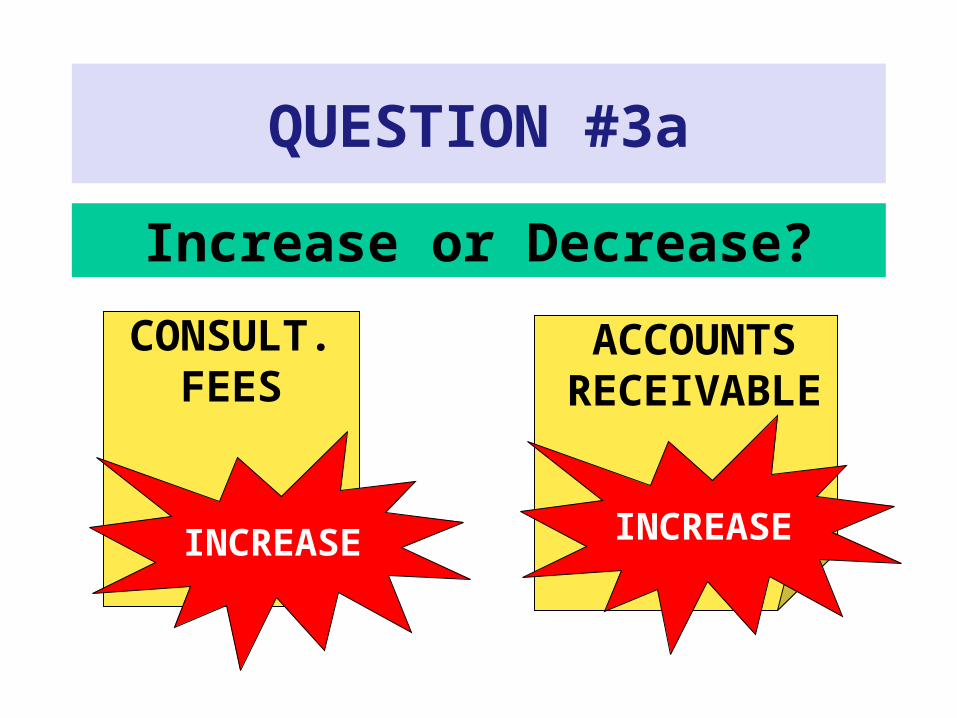

REVENUE ON ACCOUNT EXAMPLE:

MARY PERFORMED $6,000 OF SERVICES ON ACCOUNT

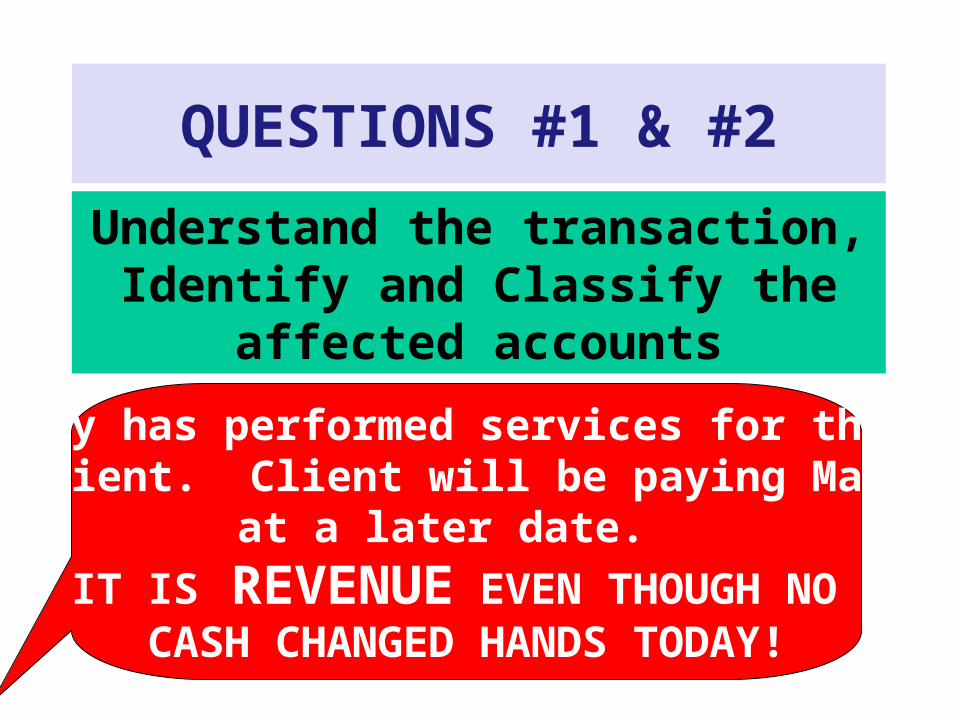

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected accounts

Mary has performed services for this client. Client will be paying Mary

at a later date.

IT IS REVENUE EVEN THOUGH NO CASH CHANGED HANDS TODAY!

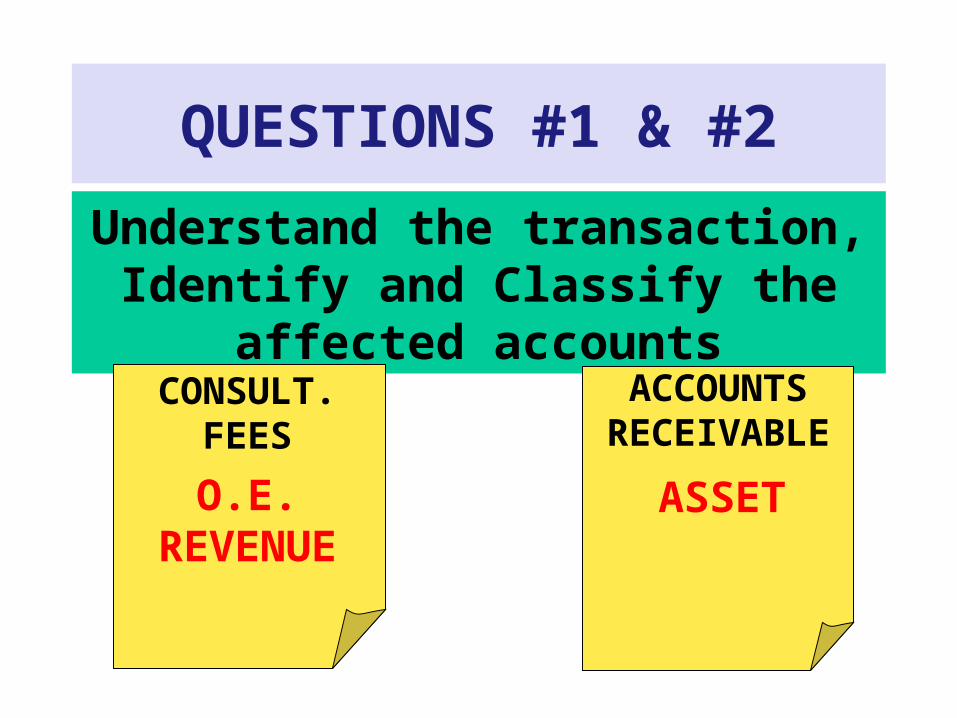

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected accounts

CONSULT. FEES

ACCOUNTS RECEIVABLE

O.E. REVENUE

ASSET

QUESTION #3a

Increase or Decrease?

CONSULT. FEES

ACCOUNTS RECEIVABLE

INCREASE INCREASE

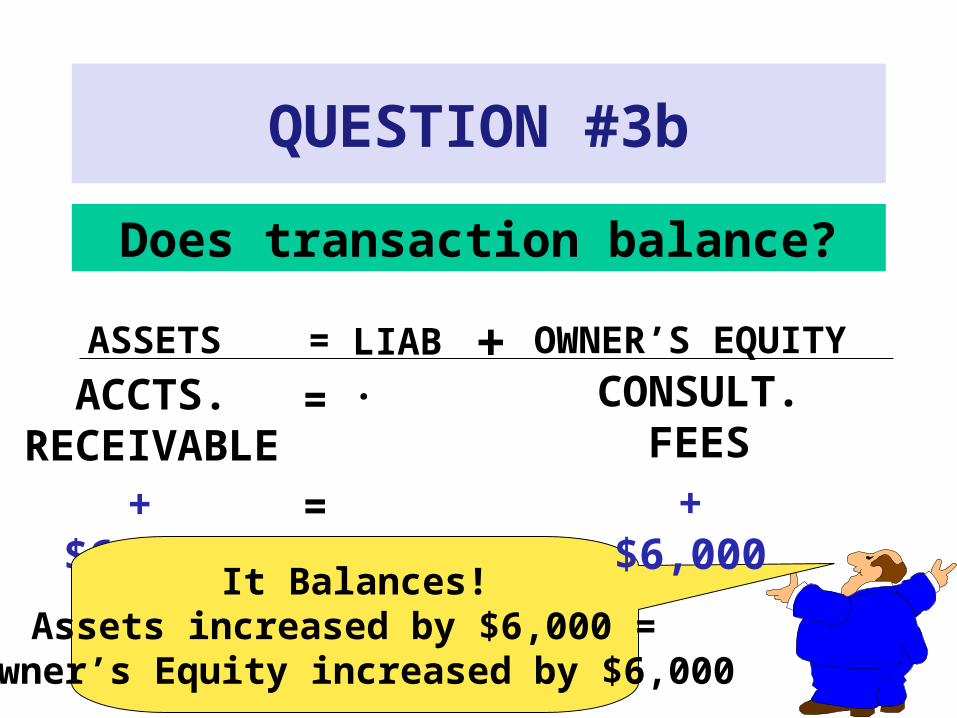

QUESTION #3b

Does transaction balance?

ASSETS = LIAB. OWNER’S EQUITY

+$6,000

ACCTS. RECEIVABLE

=

=

It Balances!Assets increased by $6,000 =

Owner’s Equity increased by $6,000

CONSULT. FEES

+$6,000

+

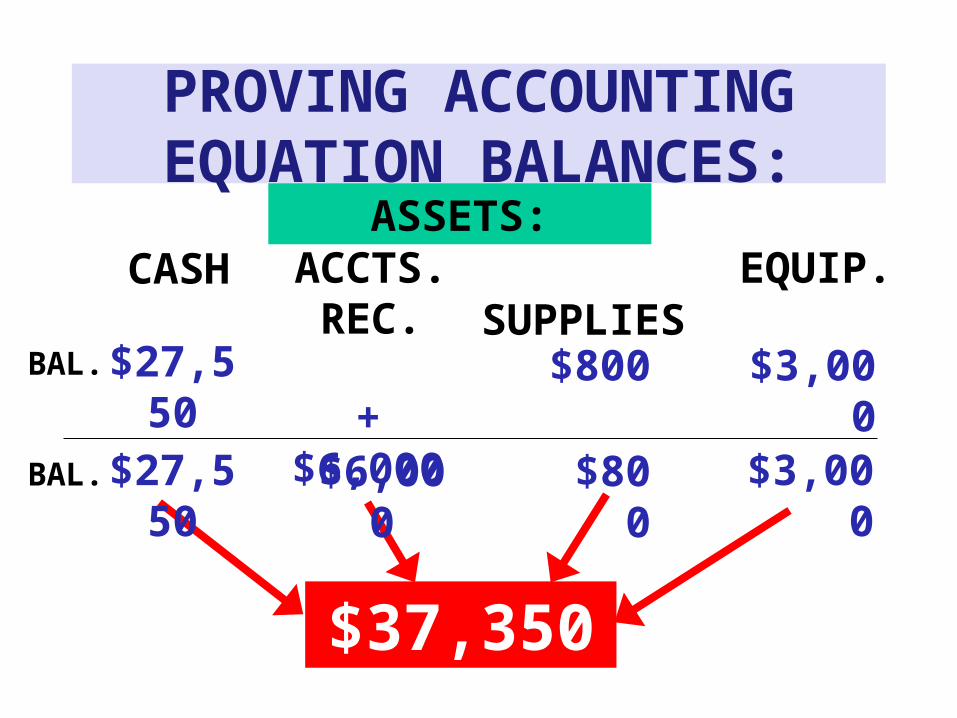

PROVING ACCOUNTING EQUATION BALANCES:

ASSETS:CASH SUPPLIES EQUIP.

$37,350

BAL. $800 $3,000

$27,550 $800 $3,000BAL.

$27,550

ACCTS. REC.

+ $6,000$6,000

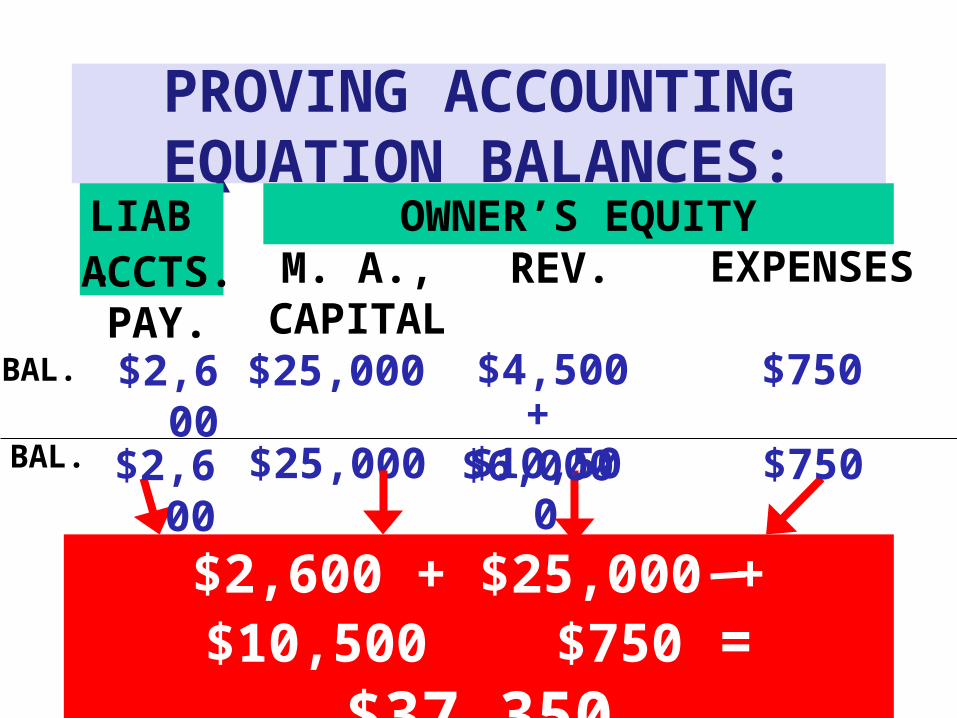

PROVING ACCOUNTING EQUATION BALANCES:

LIAB. OWNER’S EQUITYACCTS.

PAY.M. A.,

CAPITAL$25,000BAL. $2,600

$2,600 + $25,000 + $10,500 $750 = $37,350

REV.

BAL. $2,600 $25,000

$4,500

$10,500

EXPENSES

$750+ $6,000

$750

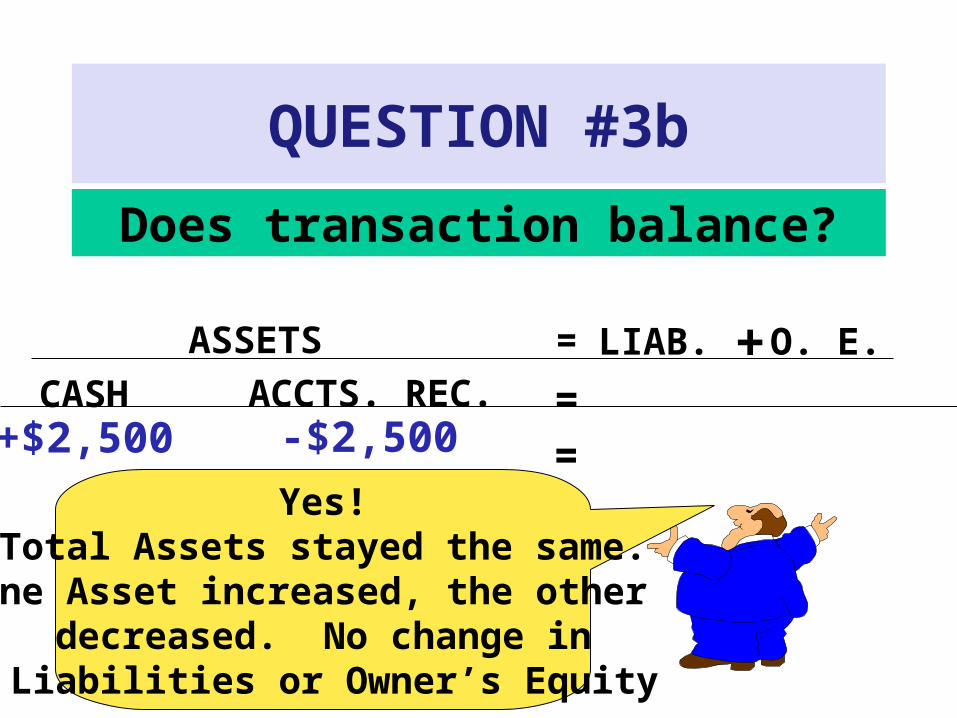

CUSTOMER PAYMENT EXAMPLE

RECEIVED $2,500 IN CASH FOR SERVICES PERFORMED IN PREVIOUS TRANSACTION

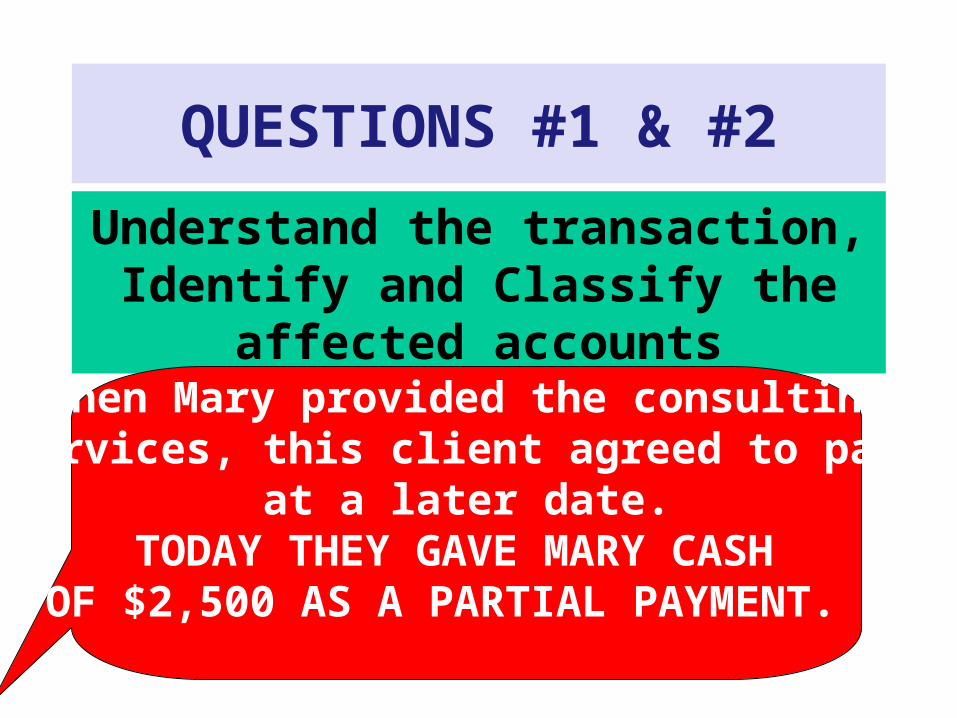

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected accounts

When Mary provided the consultingservices, this client agreed to pay

at a later date.TODAY THEY GAVE MARY CASH

OF $2,500 AS A PARTIAL PAYMENT.

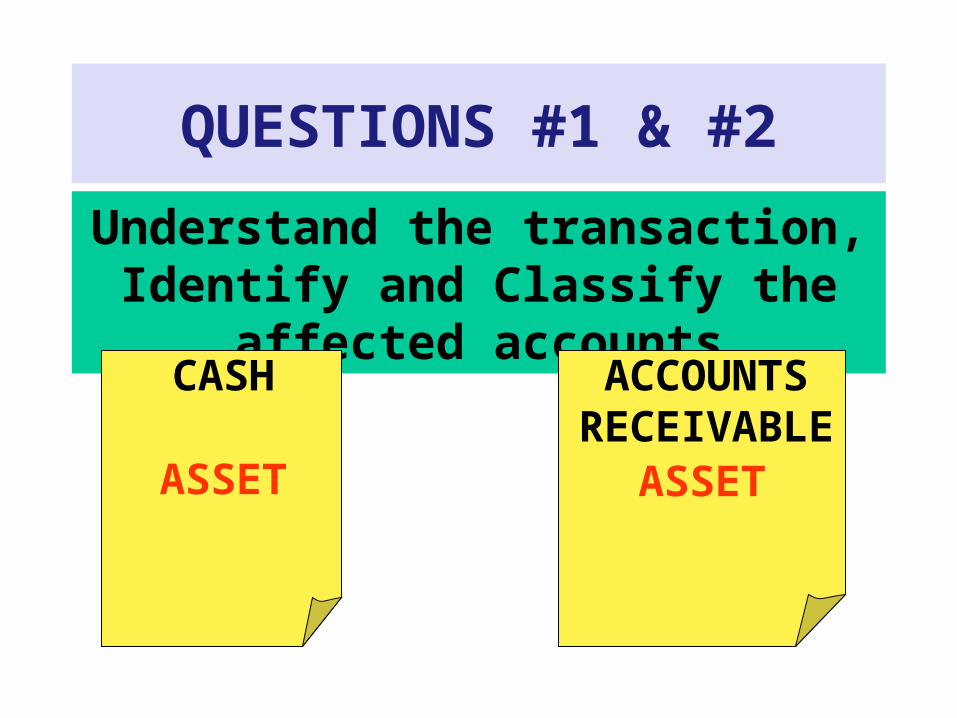

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected accounts

CASH ACCOUNTS RECEIVABLE

ASSET ASSET

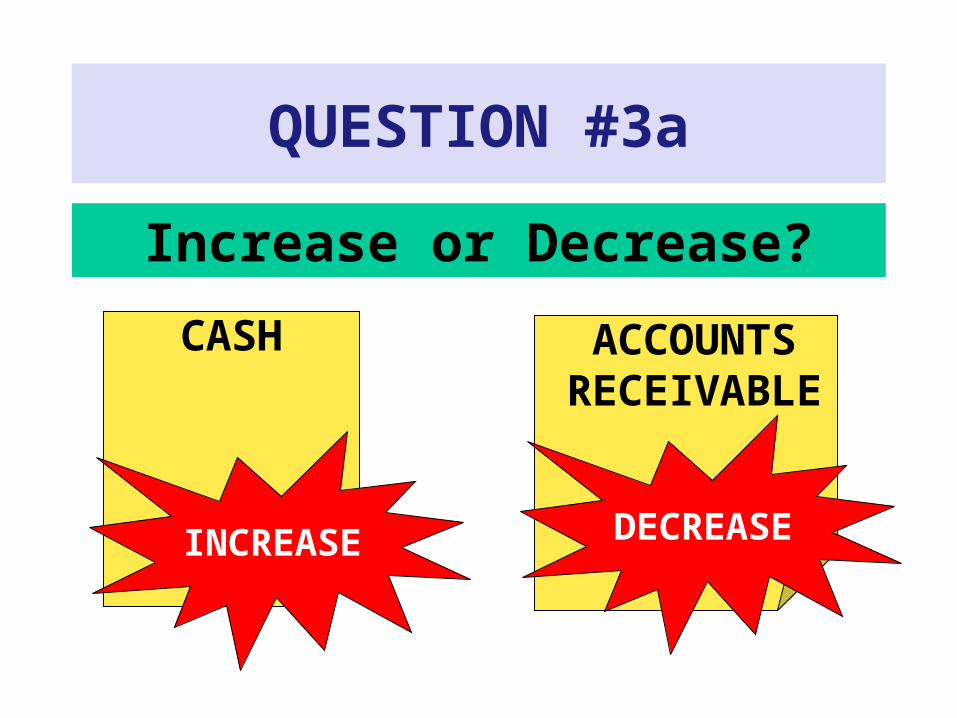

QUESTION #3a

Increase or Decrease?

CASH ACCOUNTS RECEIVABLE

INCREASE DECREASE

QUESTION #3b

Does transaction balance?

ASSETS = LIAB. O. E.

+$2,500CASH =

=Yes!

Total Assets stayed the same.One Asset increased, the other

decreased. No change in Liabilities or Owner’s Equity

ACCTS. REC.-$2,500

+

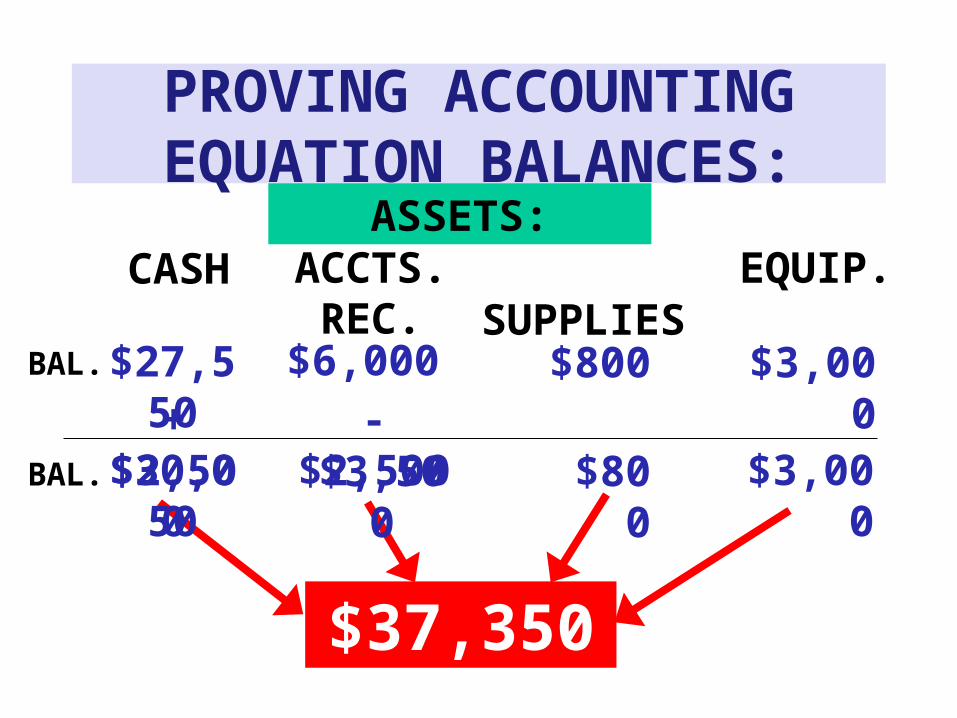

PROVING ACCOUNTING EQUATION BALANCES:

ASSETS:CASH SUPPLIES EQUIP.

$37,350

BAL. $800 $3,000

$30,050 $800 $3,000BAL.

$27,550

ACCTS. REC.$6,000

$3,500+$2,500 -$2,500

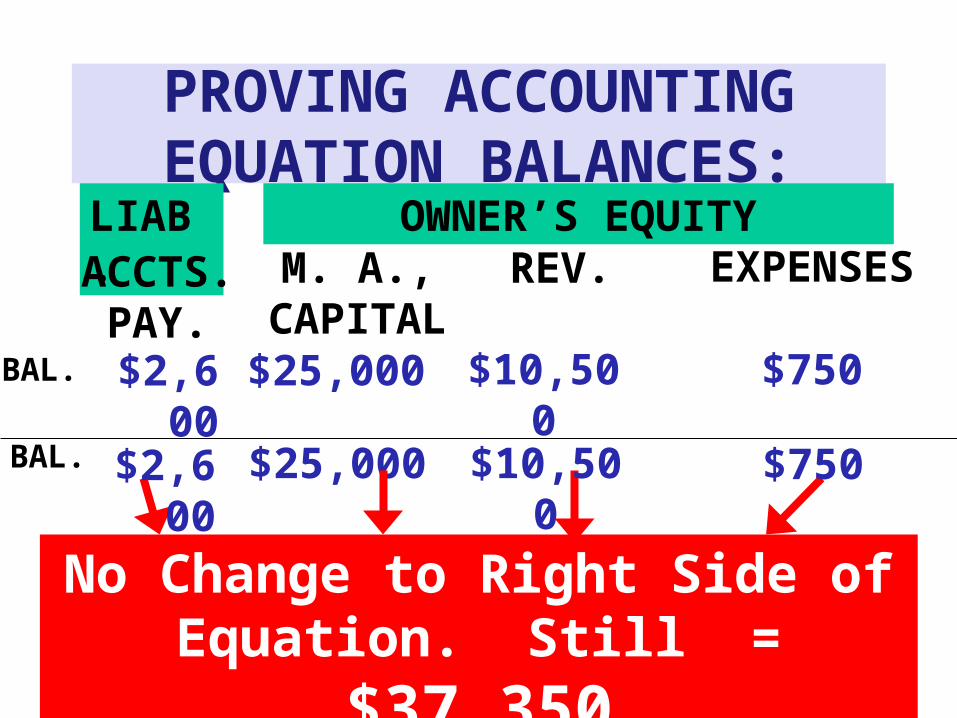

PROVING ACCOUNTING EQUATION BALANCES:

LIAB. OWNER’S EQUITYACCTS.

PAY.M. A.,

CAPITAL$25,000BAL. $2,600

No Change to Right Side of Equation.

Still = $37,350

REV.

BAL. $2,600 $25,000

$10,500

$10,500

EXPENSES

$750

$750

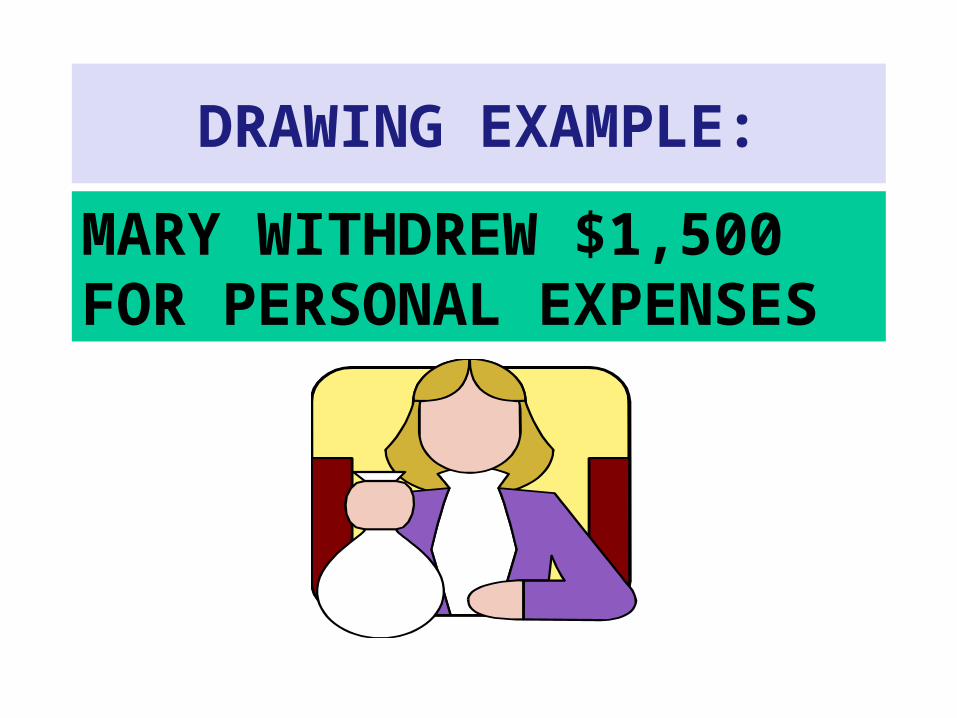

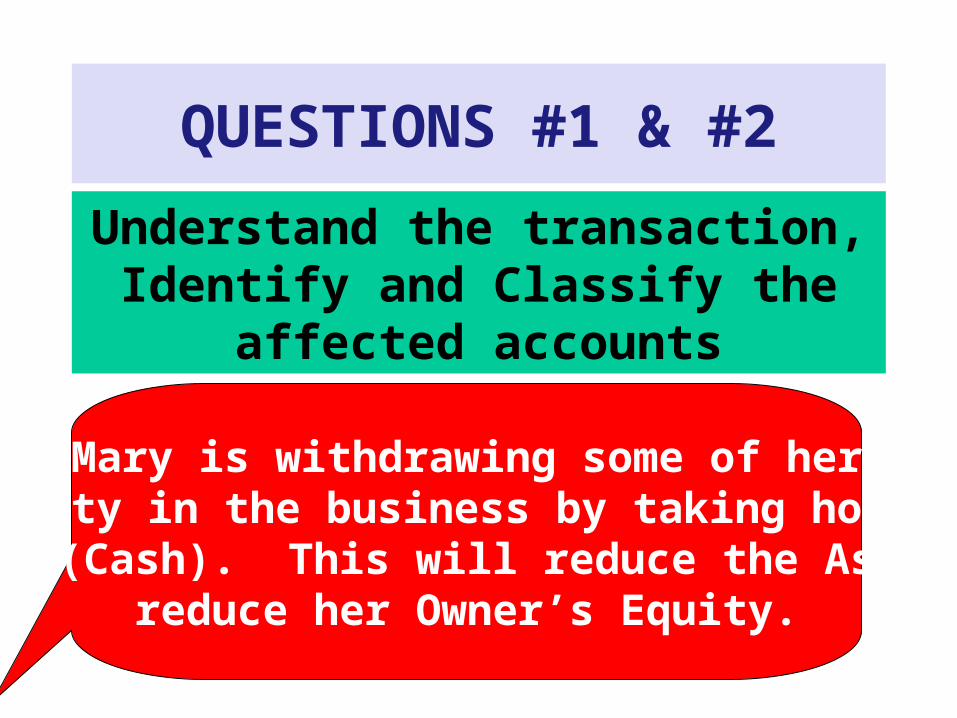

DRAWING EXAMPLE:

MARY WITHDREW $1,500 FOR PERSONAL EXPENSES

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected accounts

Mary is withdrawing some of her equity in the business by taking home an

asset (Cash). This will reduce the Assets &reduce her Owner’s Equity.

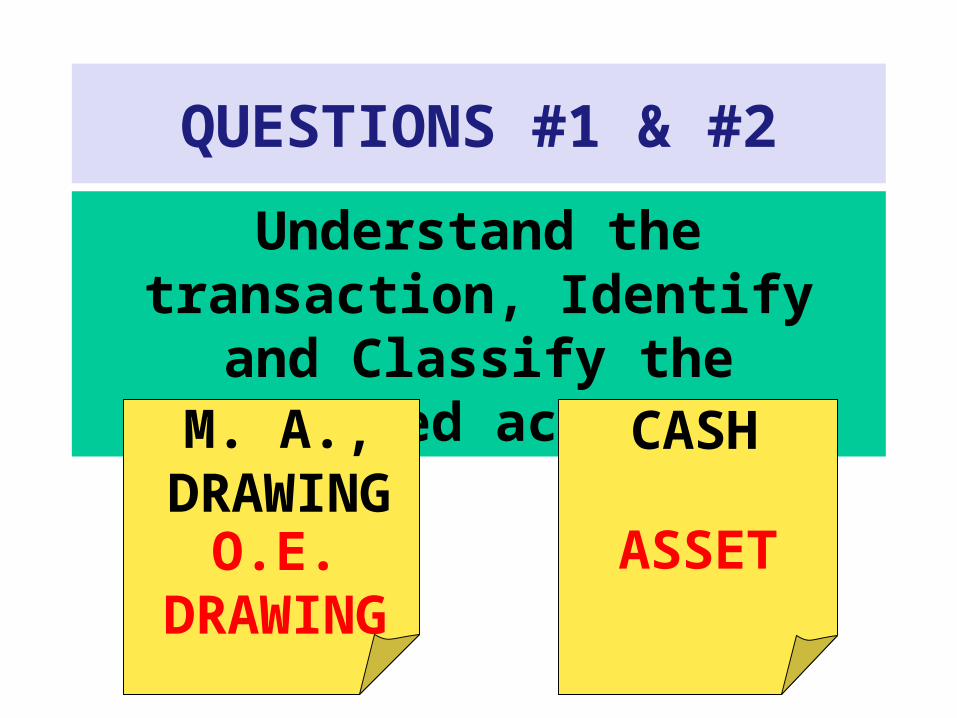

QUESTIONS #1 & #2

Understand the transaction, Identify and Classify the affected

accountsM. A.,

DRAWINGCASH

O.E. DRAWING

ASSET

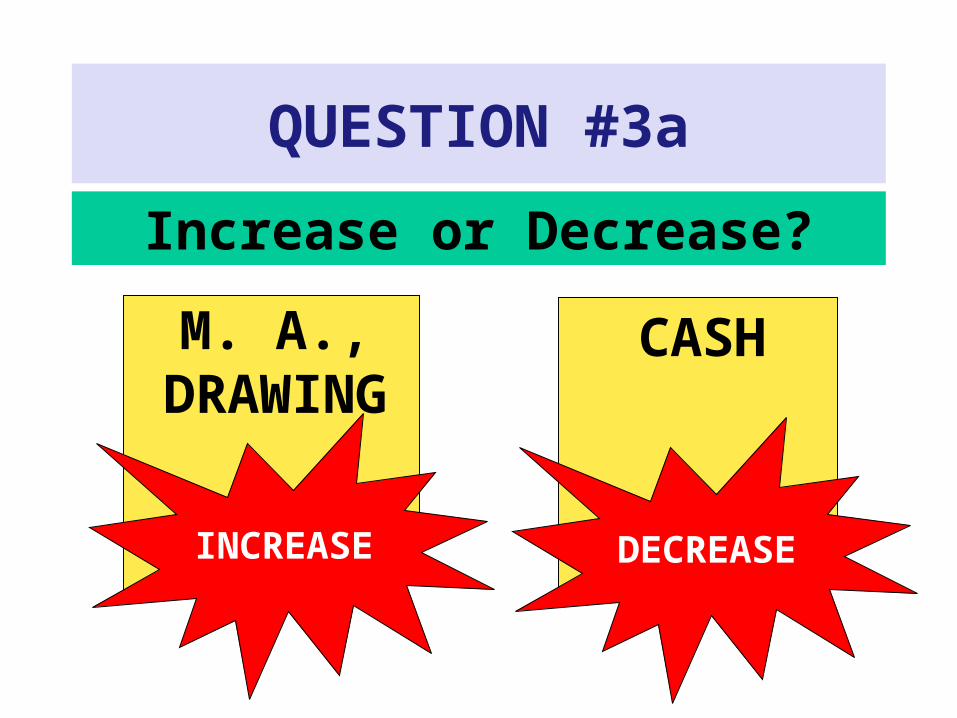

QUESTION #3a

Increase or Decrease?

M. A., DRAWING

CASH

INCREASE DECREASE

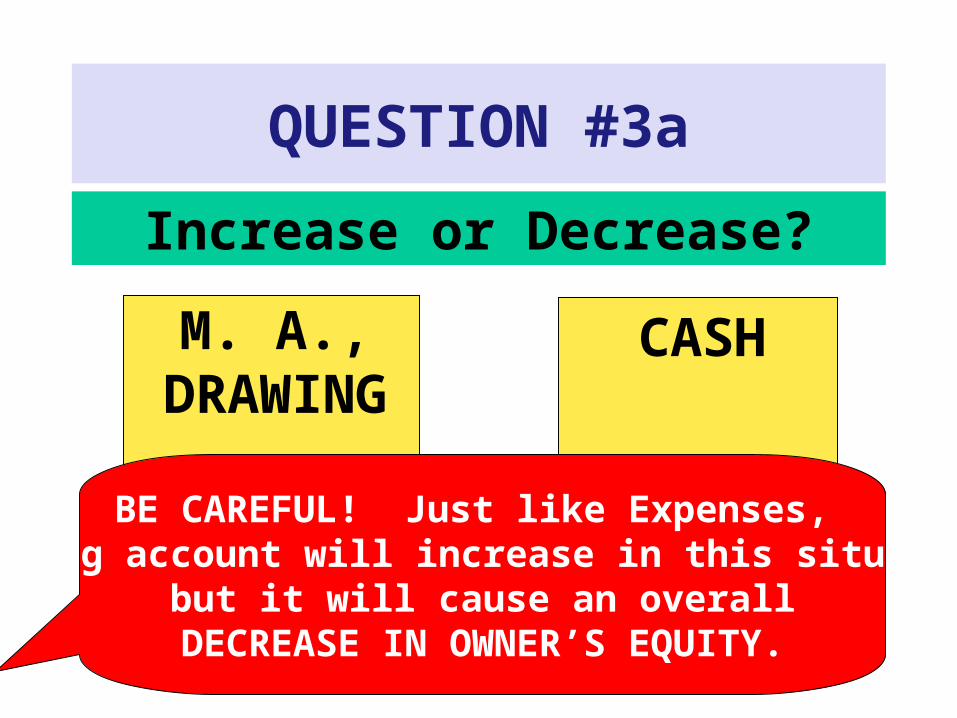

QUESTION #3a

Increase or Decrease?

M. A., DRAWING

CASH

BE CAREFUL! Just like Expenses, Drawing account will increase in this situation,

but it will cause an overallDECREASE IN OWNER’S EQUITY.

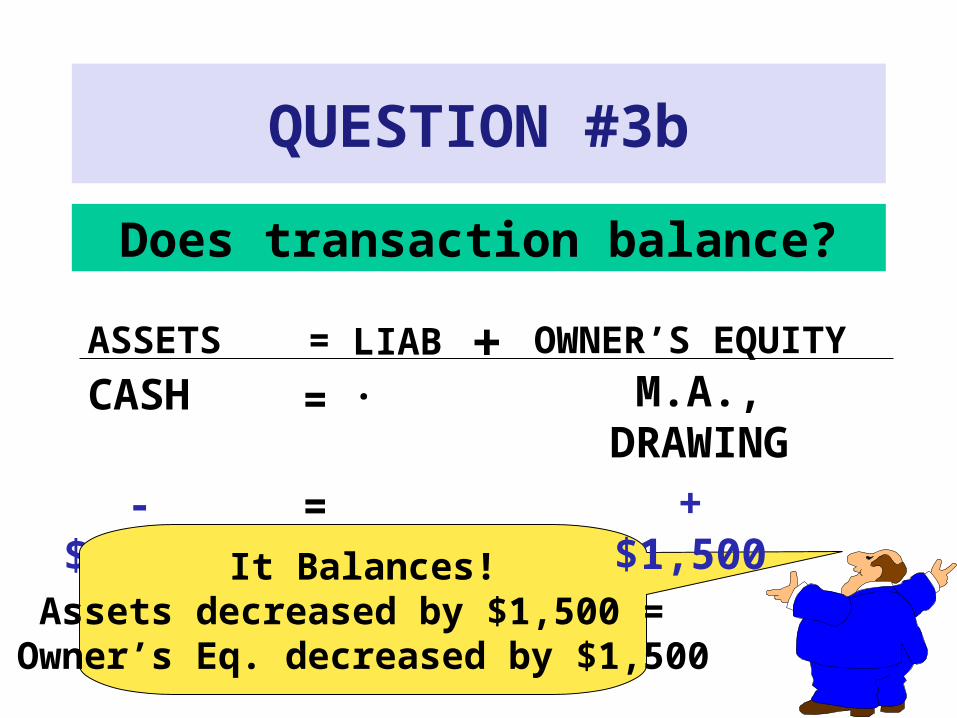

QUESTION #3b

Does transaction balance?

ASSETS = LIAB. OWNER’S EQUITY

-$1,500

CASH =

=It Balances!

Assets decreased by $1,500 = Owner’s Eq. decreased by $1,500

M.A., DRAWING

+$1,500

+

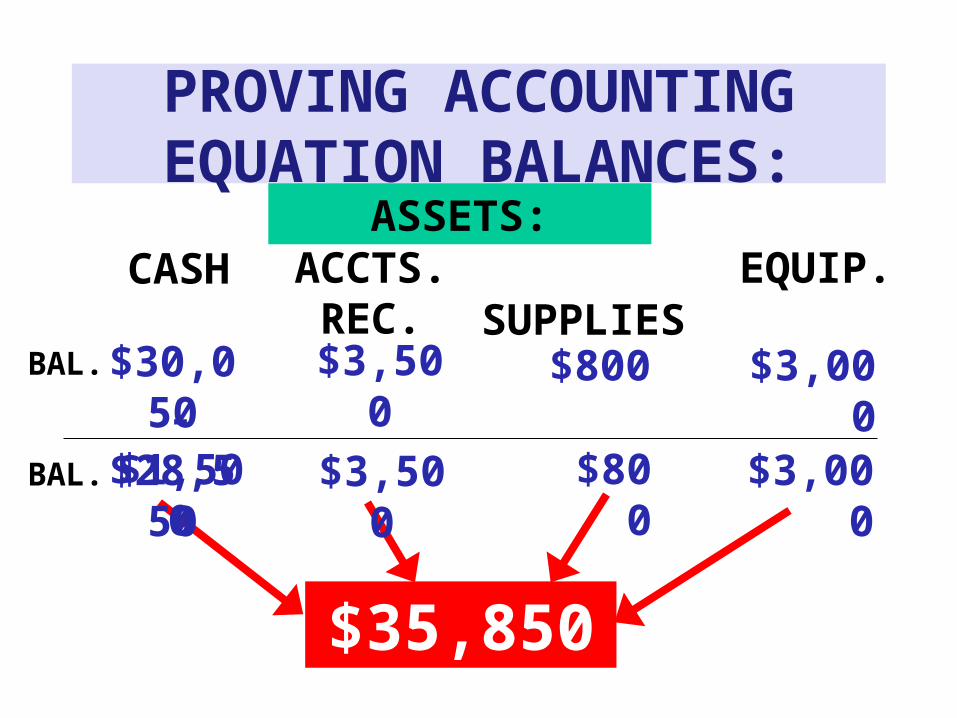

PROVING ACCOUNTING EQUATION BALANCES:

ASSETS:CASH SUPPLIES EQUIP.

$35,850

BAL. $800 $3,000

$28,550 $800 $3,000BAL.

$30,050

ACCTS. REC.

$3,500-$1,500

$3,500

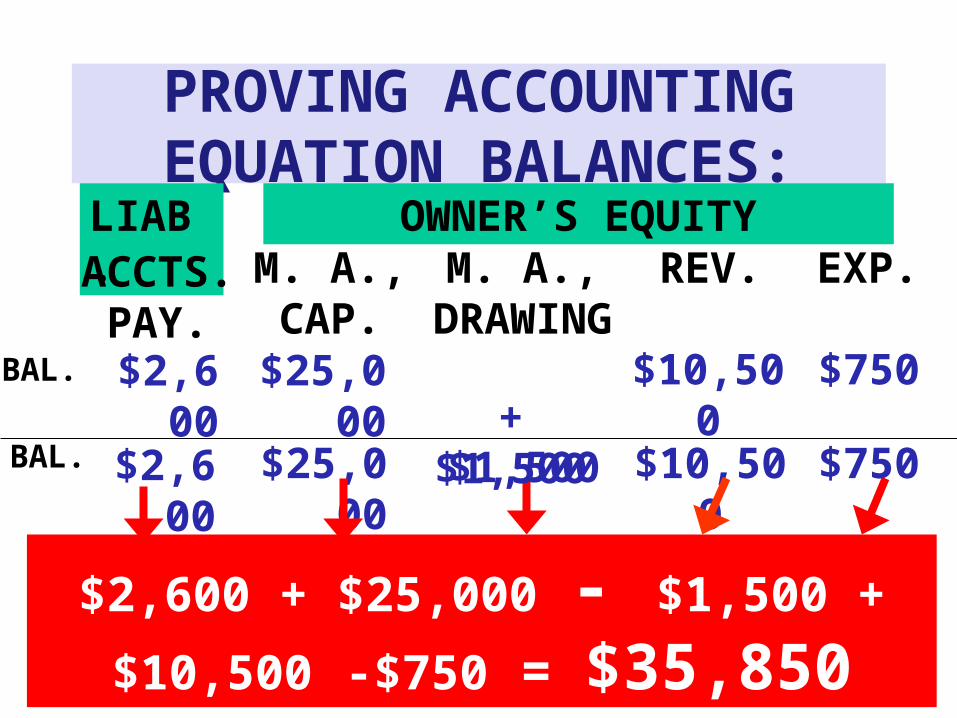

PROVING ACCOUNTING EQUATION BALANCES:

LIAB. OWNER’S EQUITYACCTS.

PAY.M. A., CAP.

$25,000BAL. $2,600

$2,600 + $25,000 - $1,500 + $10,500 -$750

= $35,850

REV.

BAL. $2,600 $25,000

$10,500

$10,500

EXP.

$750

$750

M. A., DRAWING

+$1,500$1,500

FINANCIAL STATEMENTS

THREE COMMONLY PREPARED FINANCIAL STATEMENTS:o INCOME STATEMENTo STATEMENT OF OWNER’S EQUITYo BALANCE SHEET

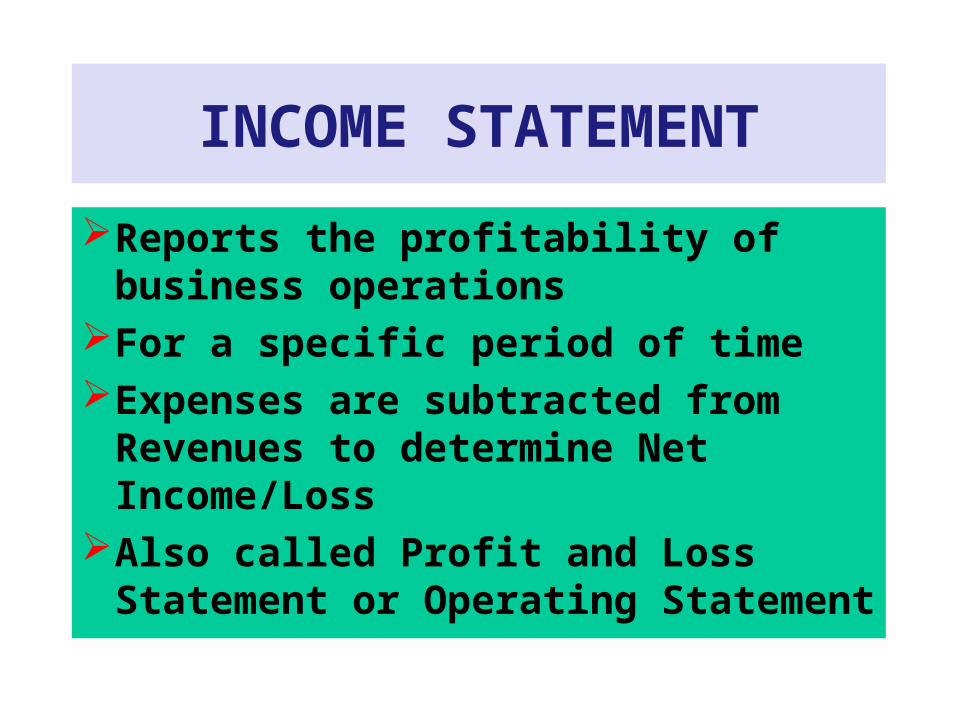

INCOME STATEMENT

Reports the profitability of business operations

For a specific period of timeExpenses are subtracted from Revenues

to determine Net Income/LossAlso called Profit and Loss Statement or

Operating Statement

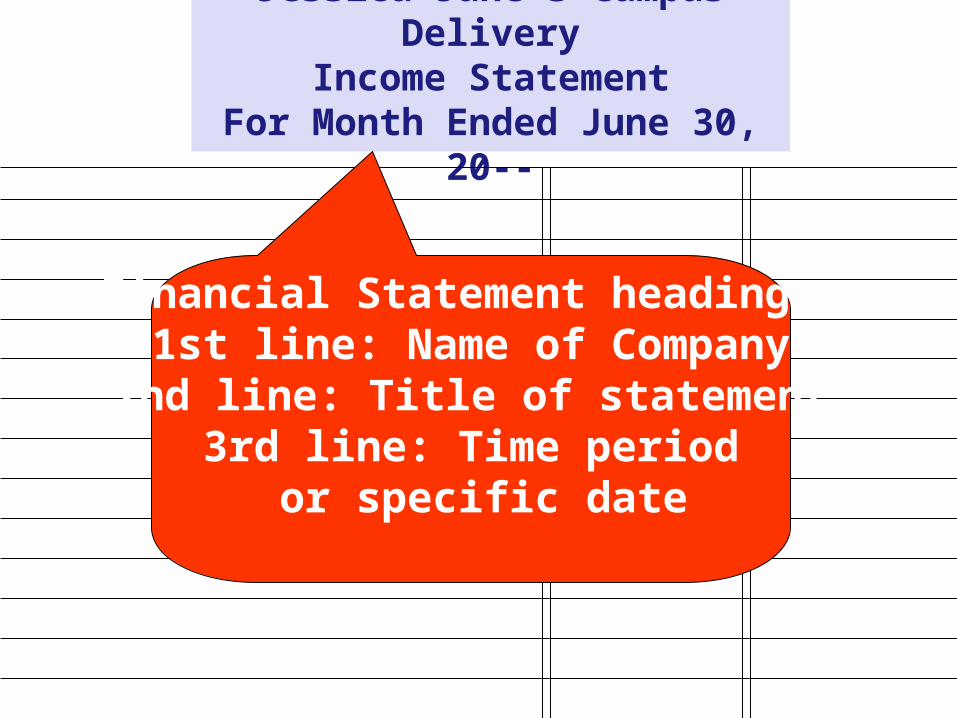

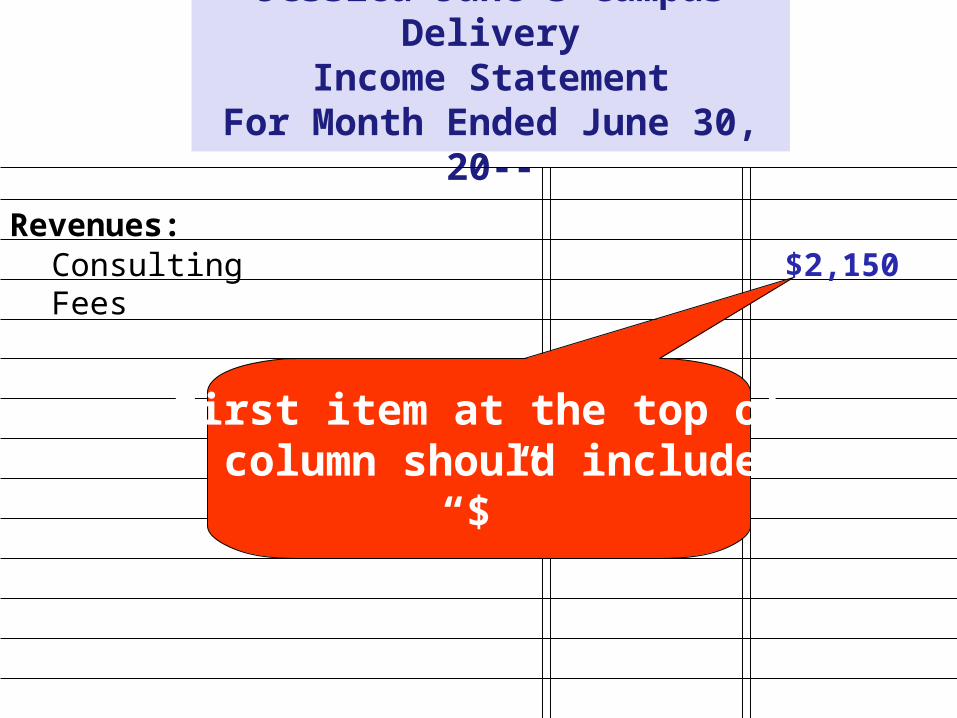

Jessica Jane’s Campus DeliveryIncome Statement

For Month Ended June 30, 20--

Financial Statement headings:1st line: Name of Company2nd line: Title of statement

3rd line: Time period or specific date

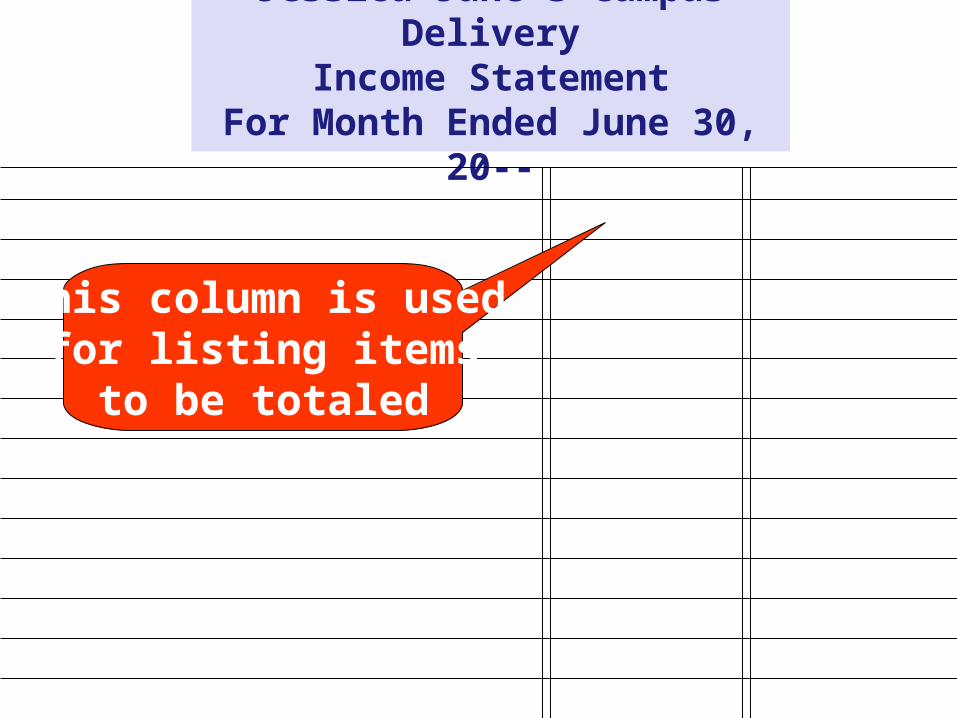

Jessica Jane’s Campus DeliveryIncome Statement

For Month Ended June 30, 20--

This column is usedfor listing items

to be totaled

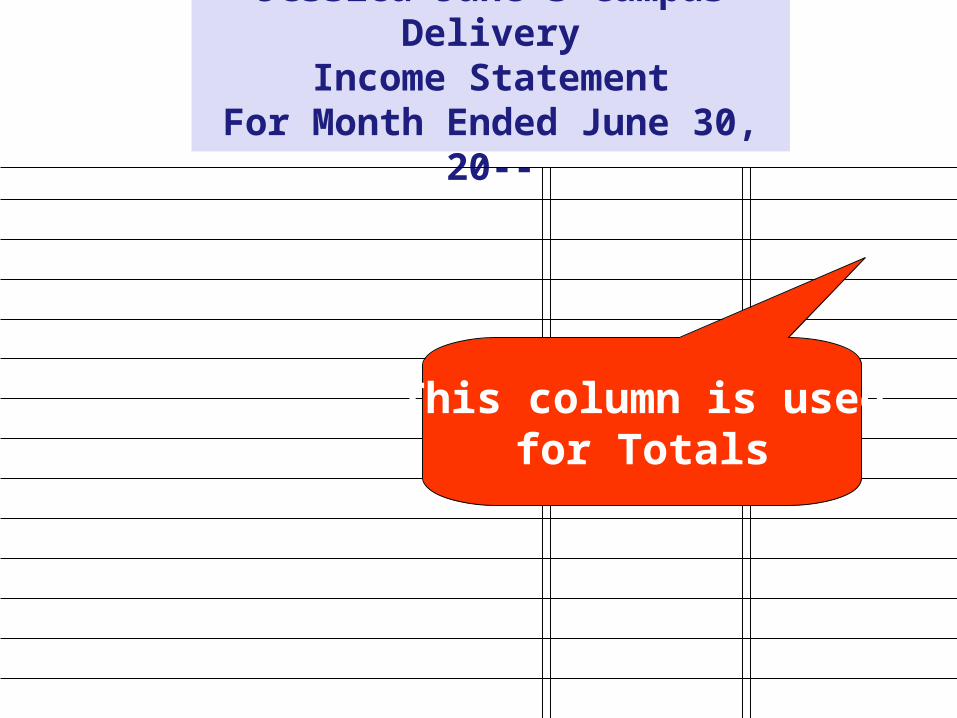

Jessica Jane’s Campus DeliveryIncome Statement

For Month Ended June 30, 20--

This column is usedfor Totals

Jessica Jane’s Campus DeliveryIncome Statement

For Month Ended June 30, 20--

Revenues:Consulting Fees $2,150

First item at the top ofa column should include

“$”

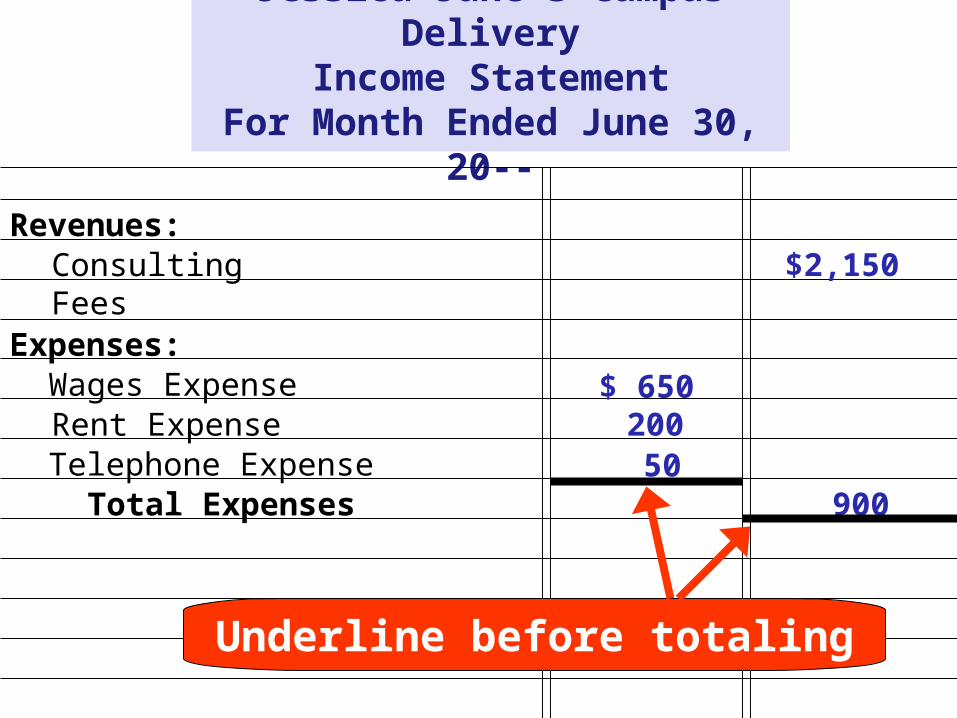

Jessica Jane’s Campus DeliveryIncome Statement

For Month Ended June 30, 20--

Revenues:Consulting Fees

Expenses:Wages ExpenseRent ExpenseTelephone Expense

Total Expenses

$2,150

$ 65020050

900

Underline before totaling

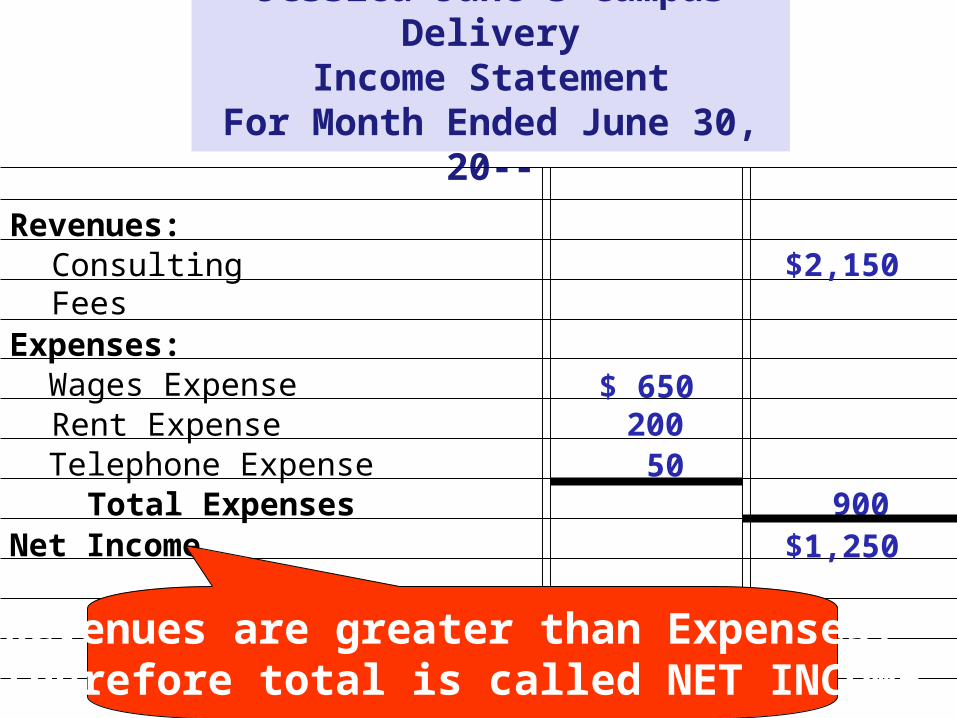

Jessica Jane’s Campus DeliveryIncome Statement

For Month Ended June 30, 20--

Revenues:Consulting Fees

Expenses:Wages ExpenseRent ExpenseTelephone Expense

Total ExpensesNet Income

$2,150

$ 650200

50900

$1,250

Revenues are greater than Expenses, therefore total is called NET INCOME

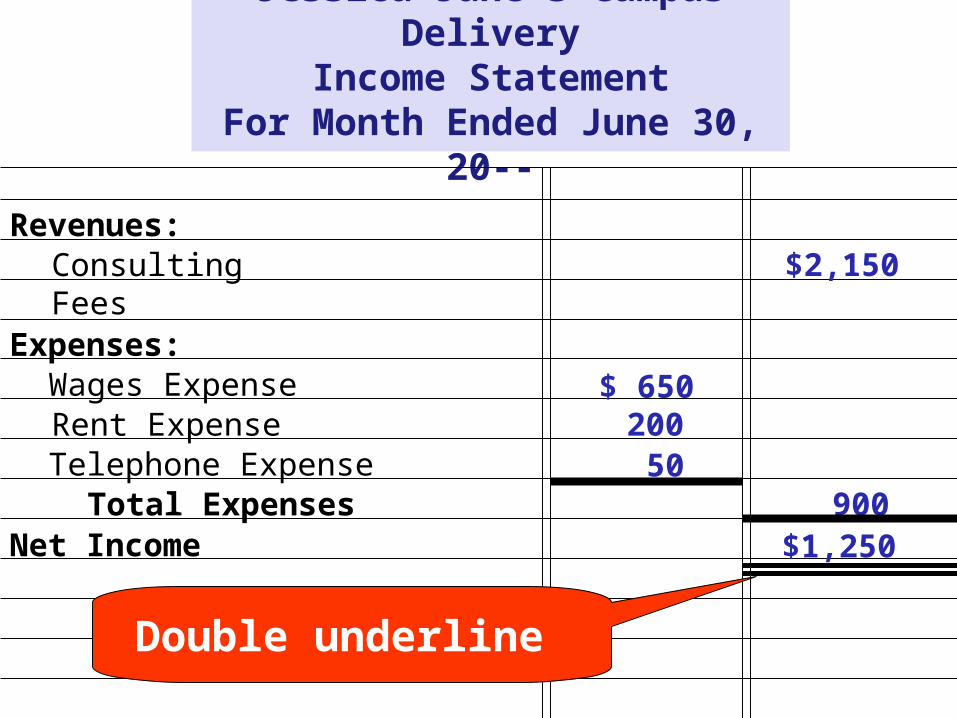

Jessica Jane’s Campus DeliveryIncome Statement

For Month Ended June 30, 20--

Revenues:Consulting Fees

Expenses:Wages ExpenseRent ExpenseTelephone Expense

Total ExpensesNet Income

$2,150

$ 650200

50900

$1,250

Double underline

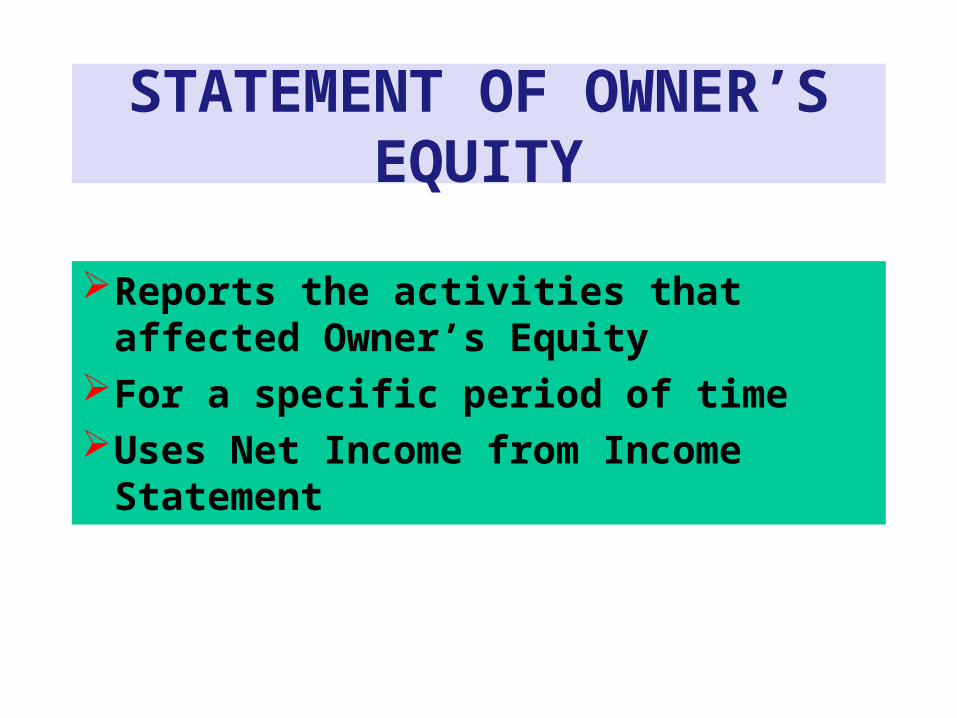

STATEMENT OF OWNER’S EQUITY

Reports the activities that affected Owner’s Equity

For a specific period of timeUses Net Income from Income Statement

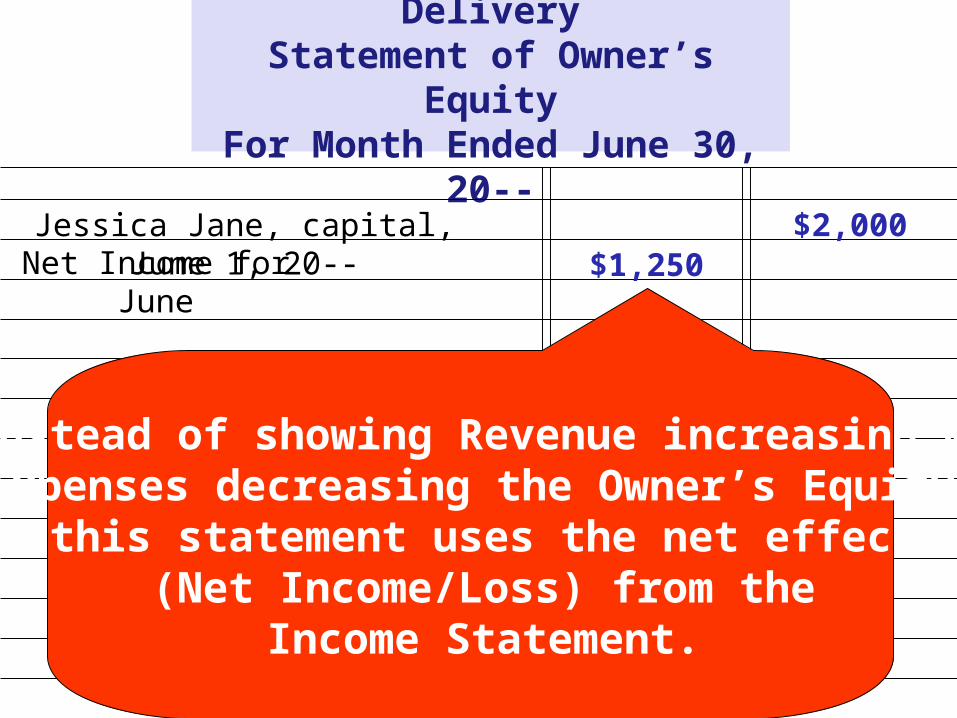

Jessica Jane’s Campus DeliveryStatement of Owner’s Equity

For Month Ended June 30, 20--

Jessica Jane, capital, June 1, 20-- $2,000Net Income for June $1,250

Instead of showing Revenue increasing & Expenses decreasing the Owner’s Equity,

this statement uses the net effect (Net Income/Loss) from the

Income Statement.

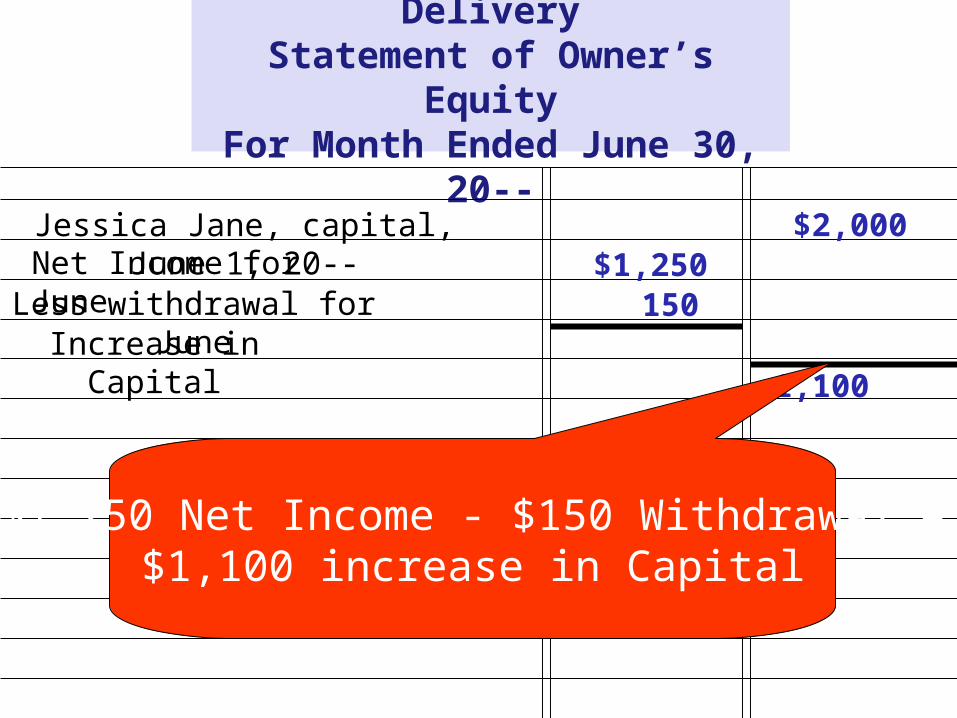

Jessica Jane’s Campus DeliveryStatement of Owner’s Equity

For Month Ended June 30, 20--

Jessica Jane, capital, June 1, 20-- $2,000Net Income for JuneLess withdrawal for JuneIncrease in Capital

$1,250150

1,100

$1,250 Net Income - $150 Withdrawal =$1,100 increase in Capital

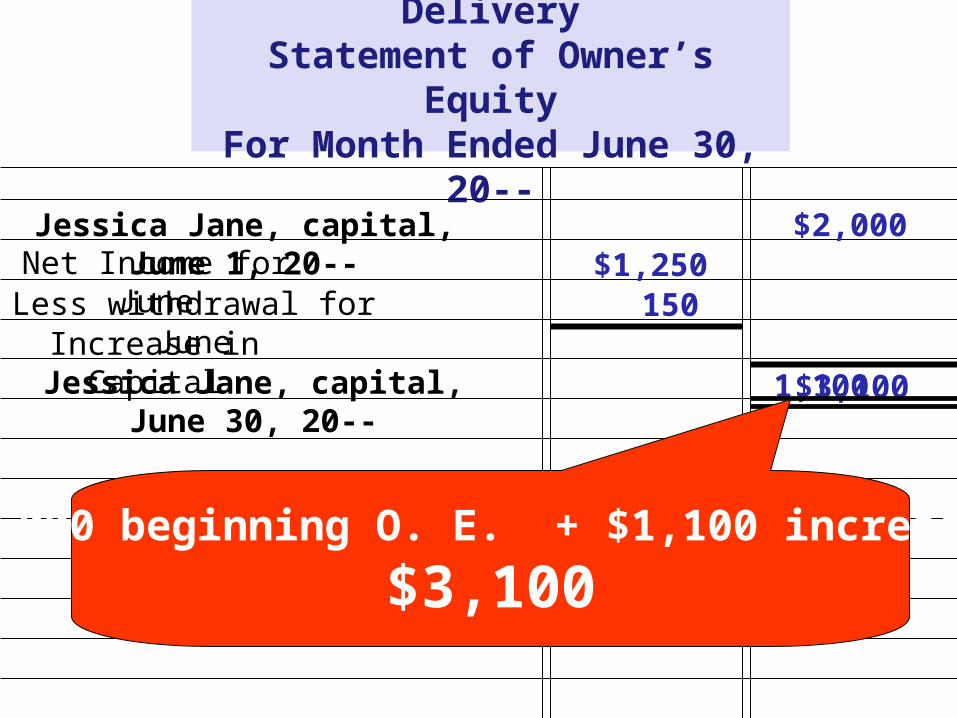

Jessica Jane’s Campus DeliveryStatement of Owner’s Equity

For Month Ended June 30, 20--

Jessica Jane, capital, June 1, 20-- $2,000Net Income for JuneLess withdrawal for JuneIncrease in Capital

$1,250150

1,100Jessica Jane, capital, June 30, 20-- $3,100

$2,000 beginning O. E. + $1,100 increase =

$3,100

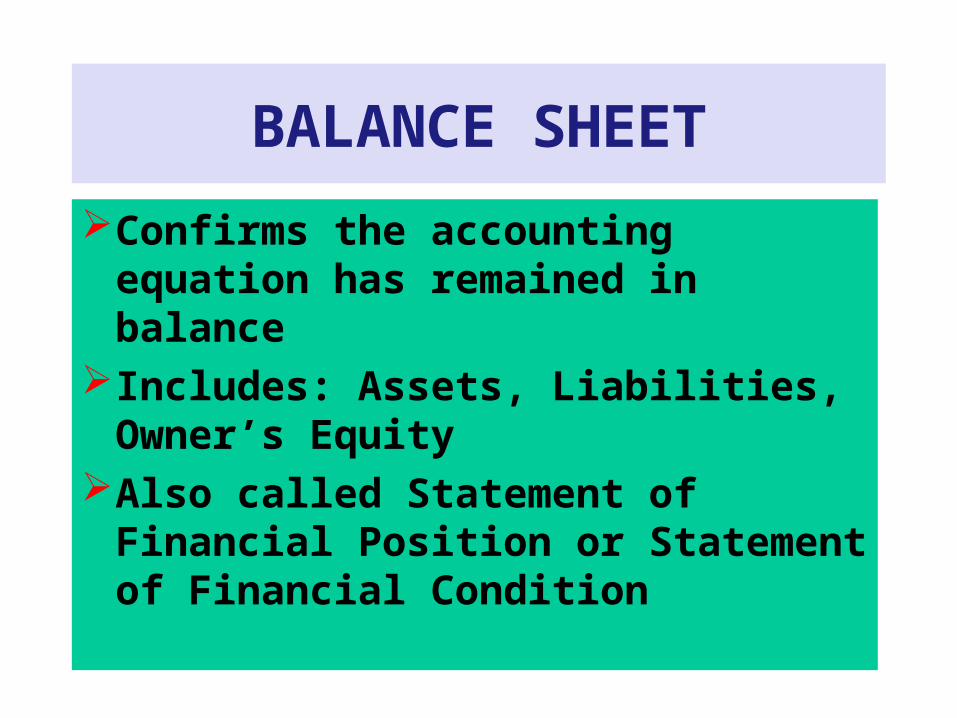

BALANCE SHEET

Confirms the accounting equation has remained in balance

Includes: Assets, Liabilities, Owner’s Equity

Also called Statement of Financial Position or Statement of Financial Condition

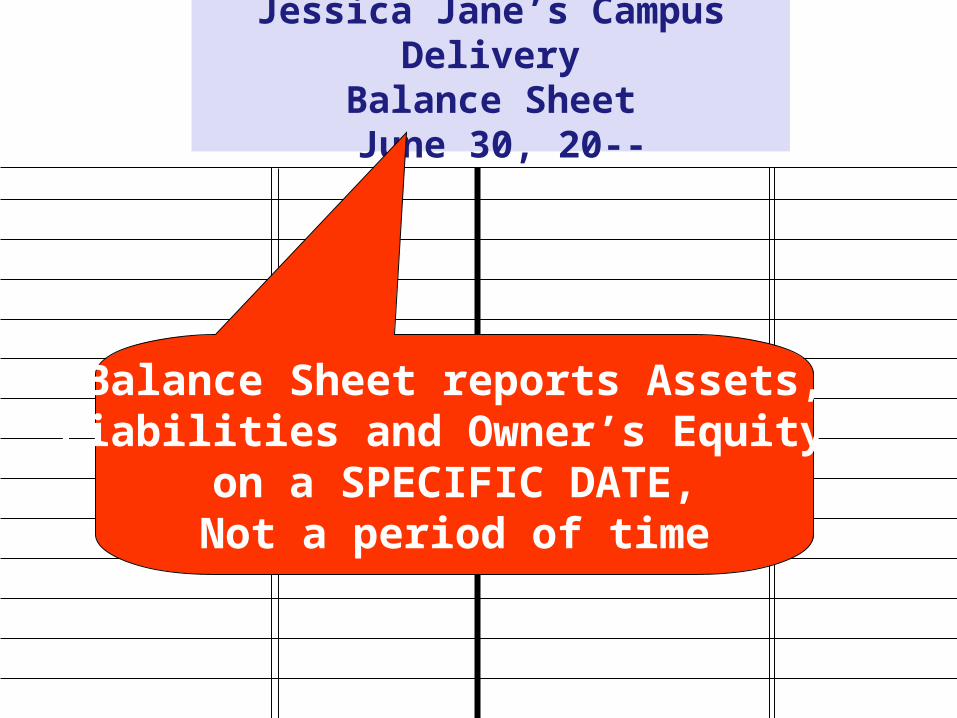

Jessica Jane’s Campus DeliveryBalance Sheet June 30, 20--

Balance Sheet reports Assets,Liabilities and Owner’s Equity

on a SPECIFIC DATE,Not a period of time

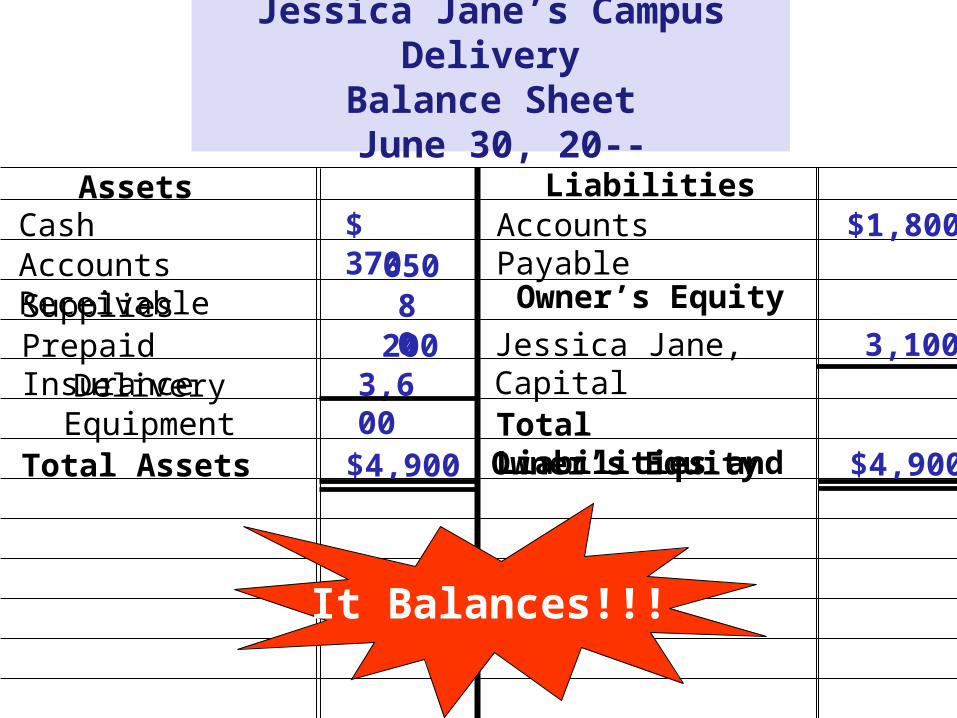

Jessica Jane’s Campus DeliveryBalance Sheet June 30, 20--

Assets LiabilitiesCash $ 370Accounts Receivable 650Supplies 80Prepaid Insurance 200Delivery Equipment 3,600

$4,900Total Assets

Accounts Payable

Owner’s Equity

Jessica Jane, Capital

$1,800

3,100

Total Liabilities andOwner’s Equity $4,900

It Balances!!!

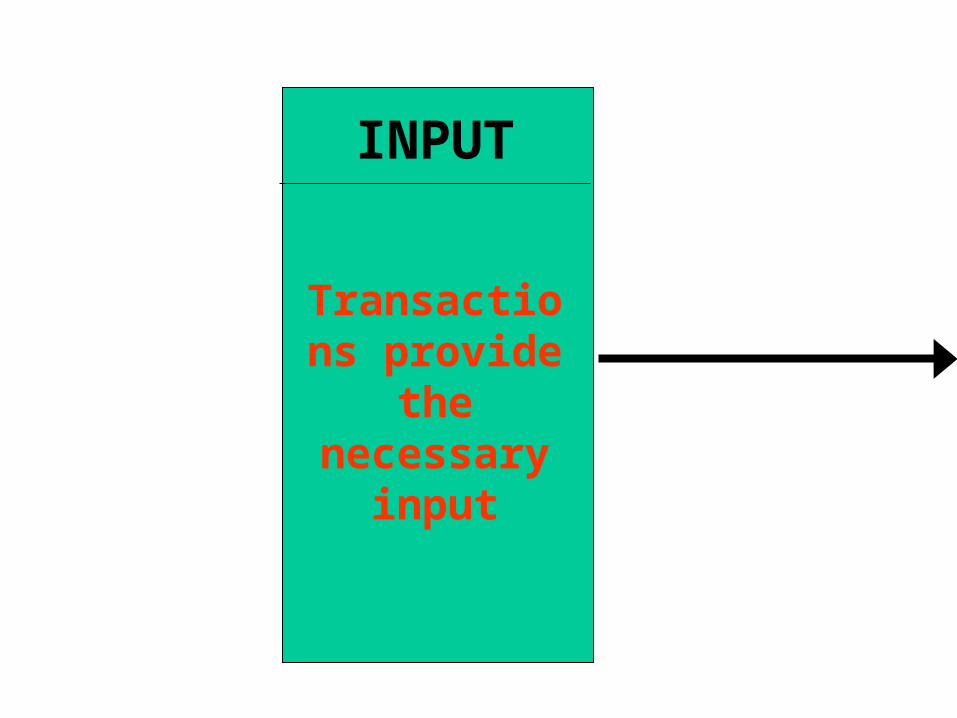

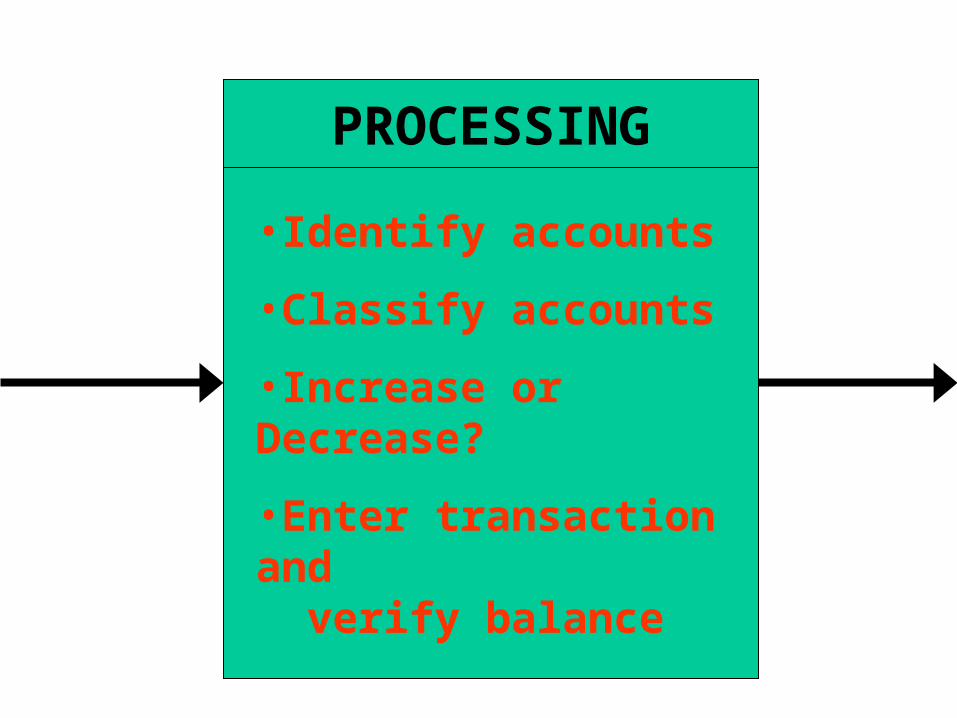

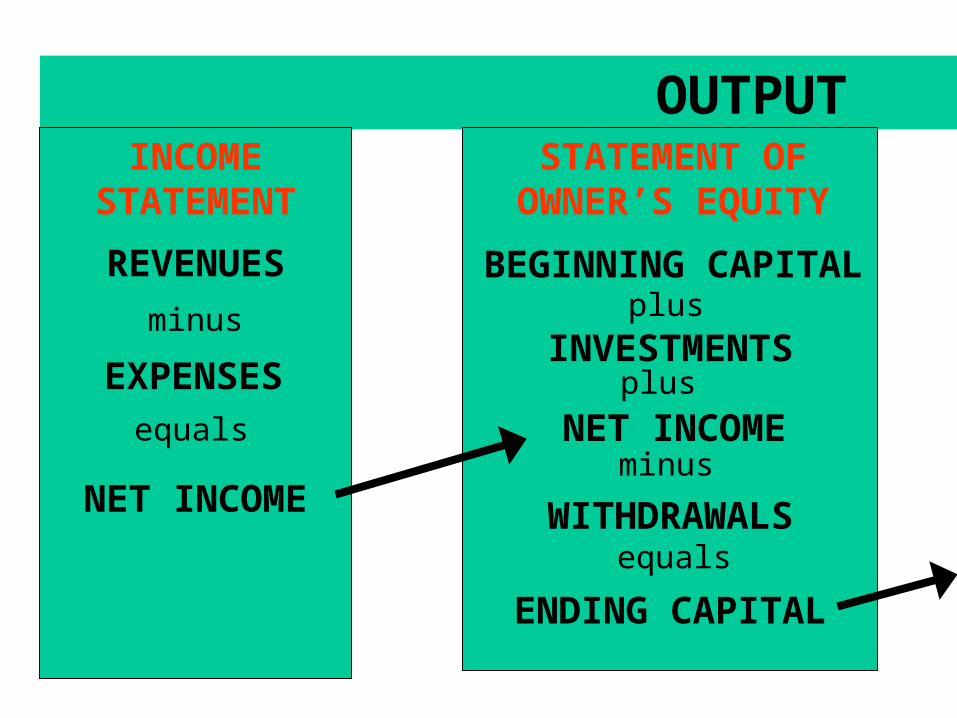

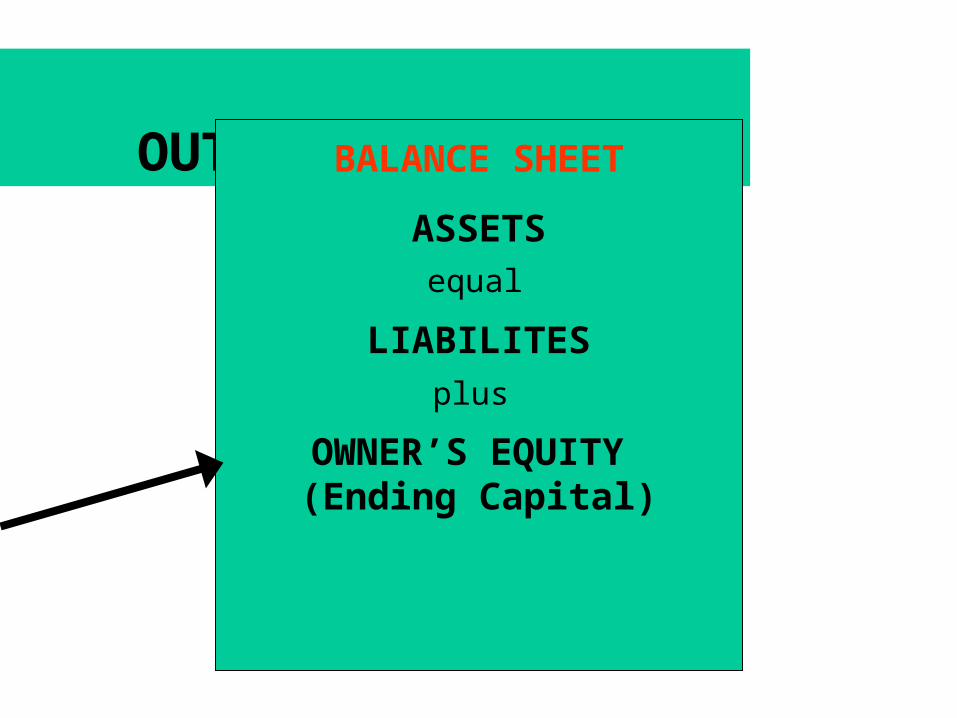

ACCOUNTING PROCESS

THREE BASIC PHASES:

oInput

oProcessing

oOutput

INPUT

Transactions provide the necessary

input

PROCESSING

•Identify accounts

•Classify accounts

•Increase or Decrease?

•Enter transaction and verify balance

OUTPUT INCOME

STATEMENT

REVENUES

minus

EXPENSESequals

NET INCOME

STATEMENT OF OWNER’S EQUITY

BEGINNING CAPITALplus

INVESTMENTSplus

NET INCOMEminus

WITHDRAWALSequals

ENDING CAPITAL

OUTPUTBALANCE SHEET

ASSETSequal

LIABILITESplus

OWNER’S EQUITY (Ending Capital)

![Chapter 02 Analyzing and Recording Transactions...Chapter 02 – Analyzing and Recording Transactions 2-1 Chapter 02 Analyzing and Recording Transactions True / False Questions [Question]](https://static.fdocuments.us/doc/165x107/5ea240e72b04b75f702106a5/chapter-02-analyzing-and-recording-transactions-chapter-02-a-analyzing-and.jpg)