Chapter Six Process Costing COPYRIGHT © 2012 Nelson Education Ltd.

70

Chapter Six Process Costing COPYRIGHT © 2012 Nelson Education Ltd.

-

Upload

franklin-preston -

Category

Documents

-

view

214 -

download

0

Transcript of Chapter Six Process Costing COPYRIGHT © 2012 Nelson Education Ltd.

Chapter SixProcess Costing

Chapter SixProcess Costing

COPYRIGHT © 2012 Nelson Education Ltd.

COPYRIGHT © 2012 Nelson Education Ltd.

Learning ObjectivesLearning Objectives

1. Describe the basic characteristics and cost flows associated with process manufacturing

2. Define equivalent units and explain their role in process costing. Explain the differences between the weighted average method and the FIFO method of accounting for process costs

3. Prepare a departmental production report using the weighted average method

4. Explain how non-uniform inputs and multiple processing departments affect process costing

5. (Appendix) Prepare a departmental production report using the FIFO method

6-2

OBJECTIVE OBJECTIVE 11

Describe the basic characteristics and cost

flows associated with process manufacturing

COPYRIGHT © 2012 Nelson Education Ltd.

Characteristics of Process ManufacturingCharacteristics of Process Manufacturing

Large manufacturing plants

Tire manufacturers

Food

Process costing works well whenever relatively homogeneous products pass through a series of

processes and they receive similar amount of manufacturing costs

Example Industries:

Chemicals

6-4

COPYRIGHT © 2012 Nelson Education Ltd.

Types of ProcessesTypes of Processes

Sequential processingRequires that units pass through one process before they

can be worked on in later processes

Parallel processingPartially completed units can be worked on simultaneously in

different processes and then brought together in a final process for completion

6-5

COPYRIGHT © 2012 Nelson Education Ltd.

Raw Materials Cost FlowRaw Materials Cost Flow

Manufacturing cost flows are same as those for a job-order system

Raw Materials

Materials purchases

As raw materials are purchased, cost of these materials flow into a raw

materials account

6-6

COPYRIGHT © 2012 Nelson Education Ltd.

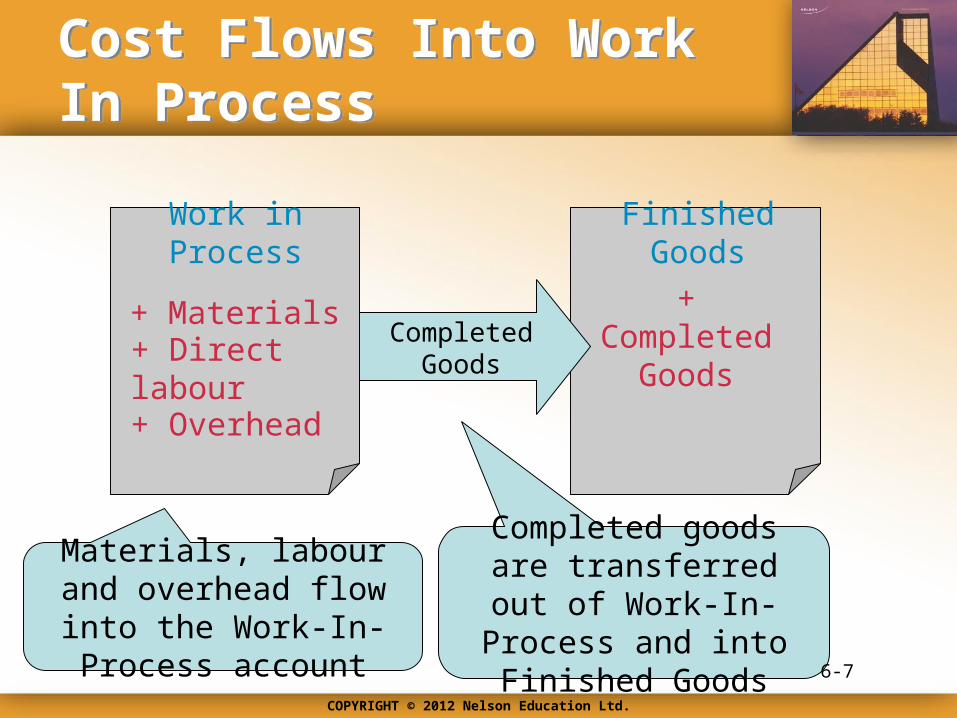

Cost Flows Into Work In ProcessCost Flows Into Work In Process

Work in Process

+ Materials

+ Direct labour

+ Overhead

Finished Goods

+ Completed Goods

CompletedGoods

Completed goods are transferred out of Work-

In-Process and into Finished Goods 6-7

Materials, labour and overhead flow into the

Work-In-Process account

COPYRIGHT © 2012 Nelson Education Ltd.

Cost Flows Into Work In ProcessCost Flows Into Work In Process

Finished Goods

+ Completed Goods

Cost of Goods Sold

+ Sold GoodsSoldGoods

Goods that are sold are transferred out of Finished Goods

and into Cost of Goods Sold

6-8

COPYRIGHT © 2012 Nelson Education Ltd.

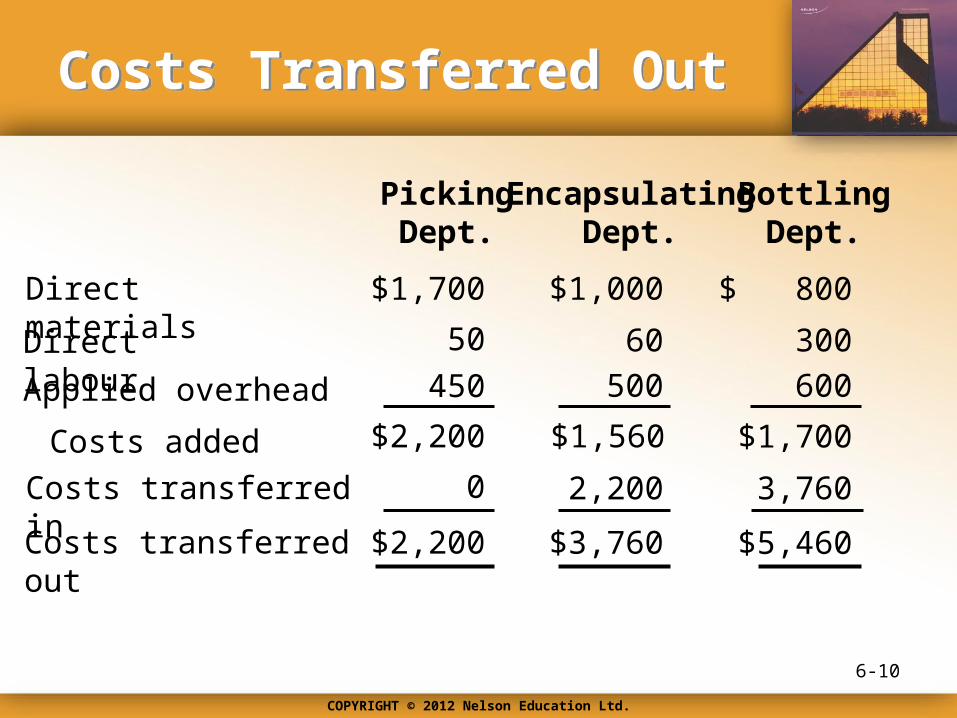

Example: Cornerstone 6-1Example: Cornerstone 6-1

6-9

Information:

Picking Dept.

Healthblend produces 2,000 bottles of multivitamins with the following costs:

Encapsulating Dept.

Direct materialsDirect labour

$1,700

Applied overhead

Bottling Dept.

$1,000 $80050 60 300

450 500 600

How to Calculate Cost Flows Without Work-In-Process (WIP)

• Calculate the costs transferred out of each department• Prepare journal entries that reflect these cost transfers

Required:

COPYRIGHT © 2012 Nelson Education Ltd.

Costs Transferred OutCosts Transferred Out

6-10

Picking Dept.

Encapsulating Dept.

Direct materials

Direct labour

$1,700

Applied overhead

Bottling Dept.

$1,000 $ 800

50 60 300

450 500 600

Costs added $2,200 $1,560 $1,700

Costs transferred in 0 3,7602,200

Costs transferred out $2,200 $3,760 $5,460

COPYRIGHT © 2012 Nelson Education Ltd.

Journal EntriesJournal Entries

Work in Process (Encapsulating)

Work in Process (Picking)

$2,200

$2,200

Work in Process (Bottling)

Work in Process (Encapsulating)

$3,760

$3,760

Finished Goods $5,460

Work in Process (Bottling) $5,460

6-11

COPYRIGHT © 2012 Nelson Education Ltd.

Transferred-In CostsTransferred-In Costs

Transferred-In Costs are costs transferred from a prior process to a subsequent process

From the viewpoint of the subsequent process, transferred-in costs are a type of raw material cost

6-12

COPYRIGHT © 2012 Nelson Education Ltd.

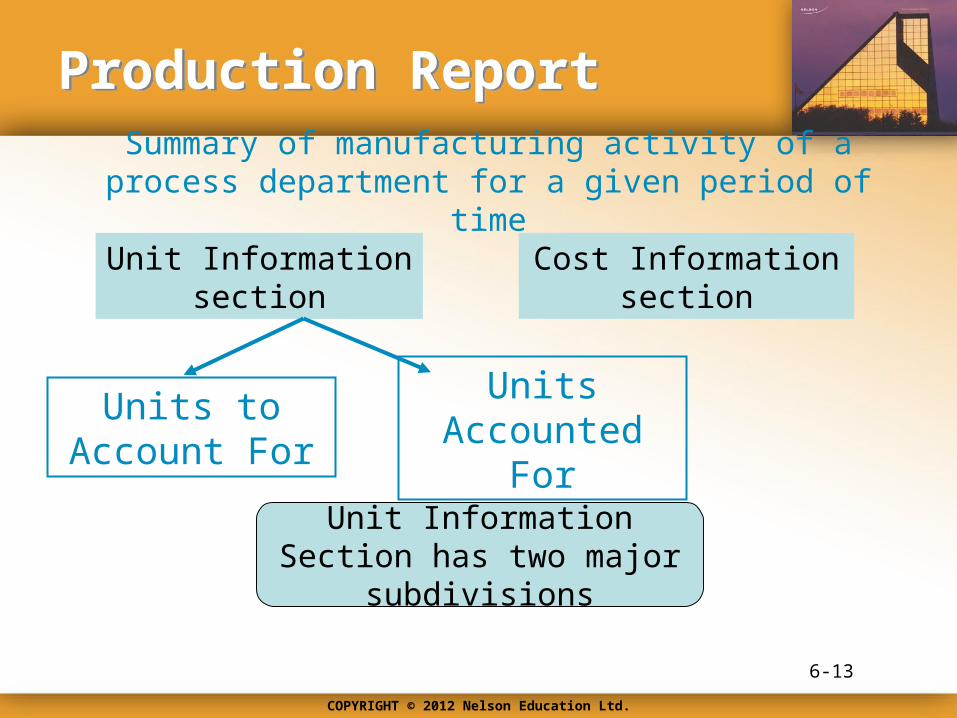

Production ReportProduction Report

Summary of manufacturing activity of a process department for a given period of time

Unit Information section

Cost Information section

Units to Account For

Units Accounted For

Unit Information Section has two major subdivisions

6-13

COPYRIGHT © 2012 Nelson Education Ltd.

Production ReportProduction Report

Unit Information section

Cost Information section

Costs to Account For

Costs Accounted For

Cost Information Section has two major subdivisions

6-14

OBJECTIVE OBJECTIVE 22

Define equivalent units and explain their role in process

costing. Explain the differences between the weighted average

method and the FIFO method of accounting for process costs

COPYRIGHT © 2012 Nelson Education Ltd.

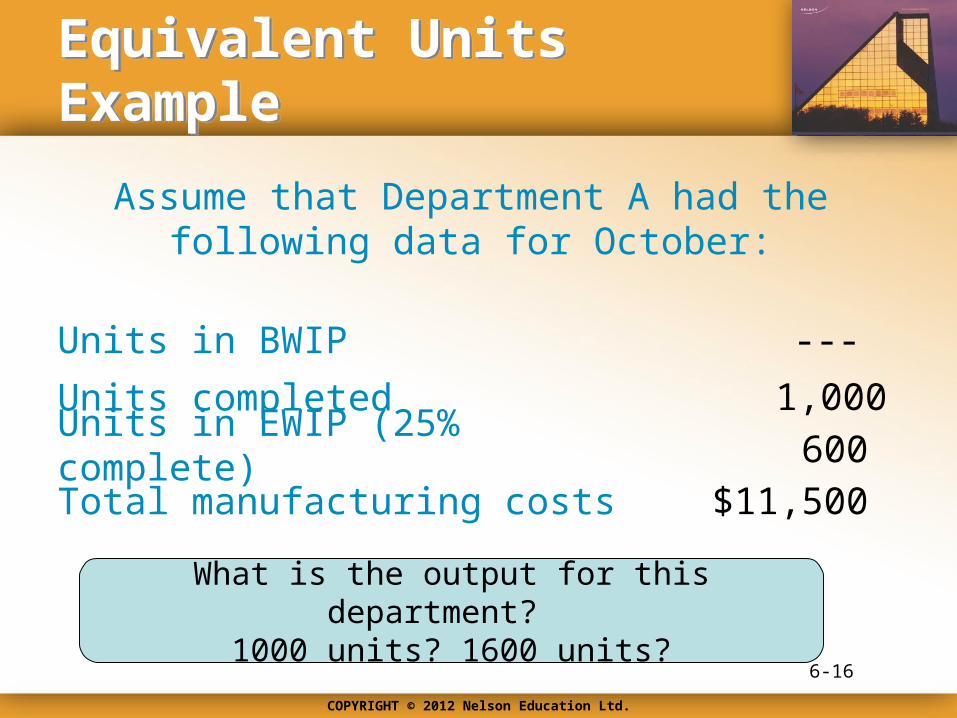

Equivalent Units ExampleEquivalent Units Example

Assume that Department A had the following data for October:

Units in BWIP ---

Units completed 1,000Units in EWIP (25% complete) 600

Total manufacturing costs $11,500

What is the output for this department? 1000 units? 1600 units?

6-16

COPYRIGHT © 2012 Nelson Education Ltd.

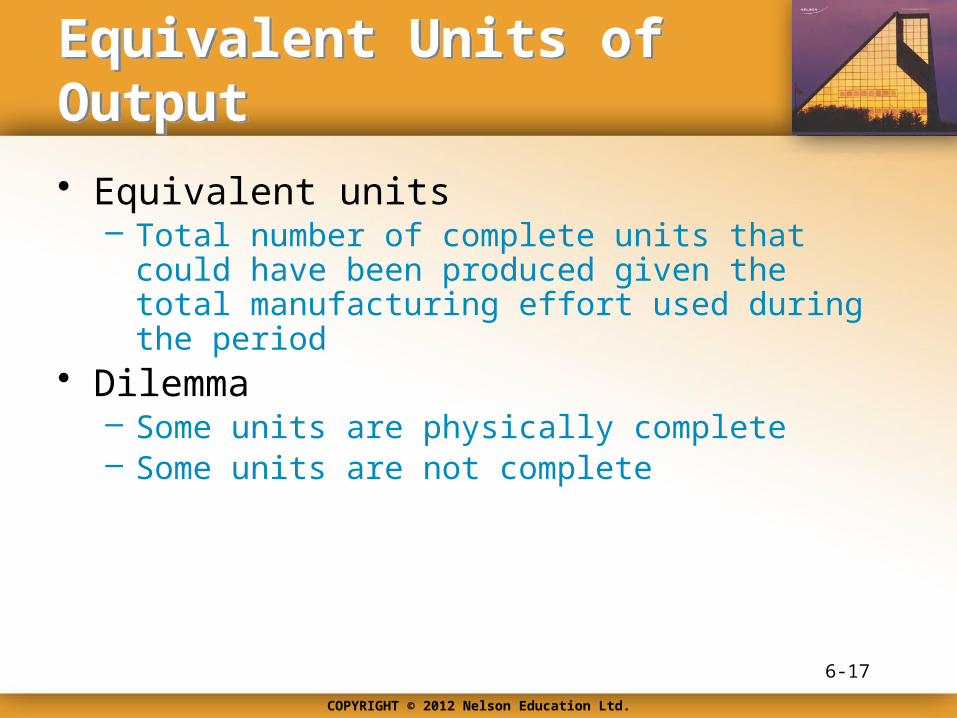

Equivalent Units of OutputEquivalent Units of Output

• Equivalent units– Total number of complete units that could have been

produced given the total manufacturing effort used during the period

• Dilemma– Some units are physically complete– Some units are not complete

6-17

COPYRIGHT © 2012 Nelson Education Ltd.

Example: Cornerstone 6-2Example: Cornerstone 6-2

6-18

Information:

October Data:

Calculate the equivalent units for October

1,000 units completed

600 units25 percent complete

Required:

How to Calculate Equivalent Units of Production:No Beginning Work-In-Process

COPYRIGHT © 2012 Nelson Education Ltd.

Equivalent UnitsEquivalent Units

6-19

Equivalent Units

1,150

Units Completed 1,000

Units in Ending WIP × 25% complete 150

COPYRIGHT © 2012 Nelson Education Ltd.

Example: Cornerstone 6-3Example: Cornerstone 6-3

6-20

Information:

Manufacturing Costs for the period

Units Transferred Out11,500

Units in Ending Work In Process(25% Complete) 600

1,000

How To Measure Output and Assign Costs: No Beginning Work-In-Process

• Calculate the unit cost• Calculate the cost of goods transferred out and

the cost of ending work-in-process (EWIP)

Required:

COPYRIGHT © 2012 Nelson Education Ltd.

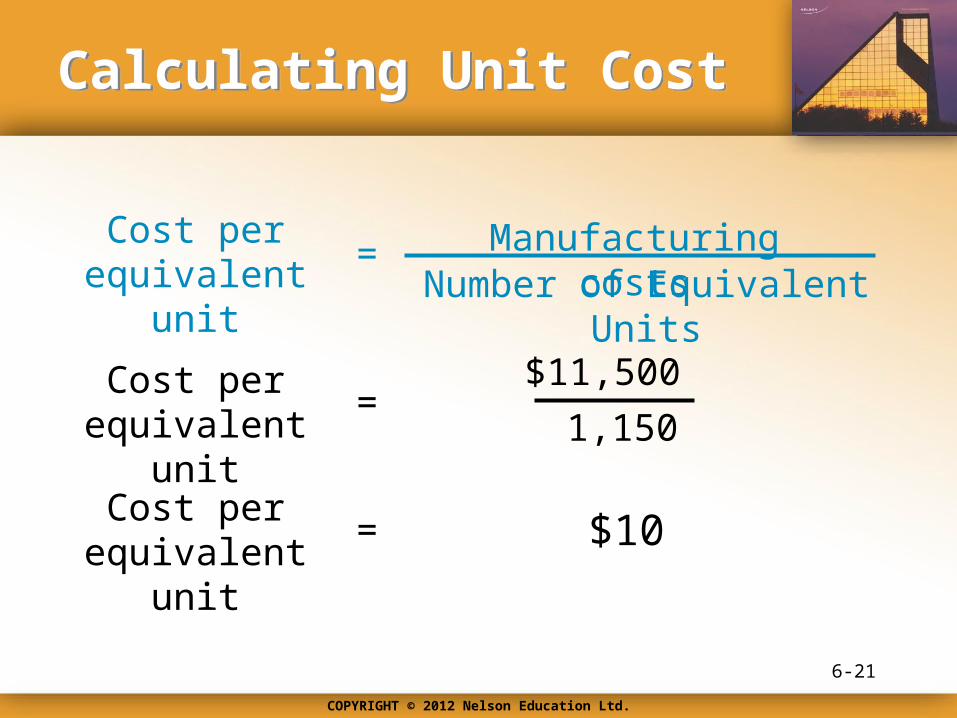

Calculating Unit CostCalculating Unit Cost

Cost per equivalent unit = Manufacturing costs

Number of Equivalent Units

$11,500

1,150=

$10

Cost per equivalent unit

Cost per equivalent unit

=

6-21

COPYRIGHT © 2012 Nelson Education Ltd.

Cost of Goods Transferred OutCost of Goods Transferred Out

Cost of goods transferred out

=

$10

= $10,000

× 1,000 units

Cost of goods transferred out

Unit Cost

× Units

Transferred Out

6-22

COPYRIGHT © 2012 Nelson Education Ltd.

Cost of Ending Work-In-Process (EWIP)Cost of Ending Work-In-Process (EWIP)

Cost of ending work in process =

$10

= $1,500

× 150

Cost of ending work in process

Unit Cost

× Units in EWIP

Things get more complicated if there are units in work-in-process at the

beginning of the period

6-23

COPYRIGHT © 2012 Nelson Education Ltd.

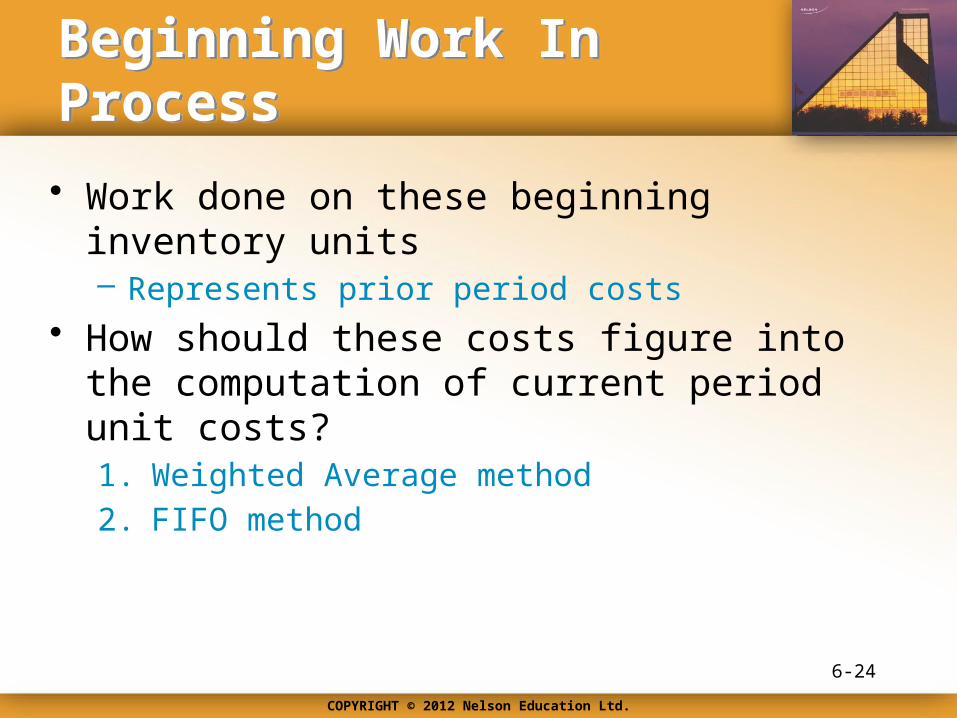

Beginning Work In ProcessBeginning Work In Process

• Work done on these beginning inventory units– Represents prior period costs

• How should these costs figure into the computation of current period unit costs?1. Weighted Average method

2. FIFO method

6-24

COPYRIGHT © 2012 Nelson Education Ltd.

Weighted Average MethodWeighted Average Method

• Combines– Beginning inventory costs– Current period costs

• Calculates Unit Cost for the period– By averaging

• Unit cost is used to compute costs for:– Goods transferred out– Goods remaining in work-in-process

6-25

COPYRIGHT © 2012 Nelson Education Ltd.

FIFO MethodFIFO Method

Only current work and costs are used to calculate this

period’s unit cost

Separates work and costs for the equivalent units in beginning inventory from work and costs of the

equivalent units produced during the current period

6-26

OBJECTIVE OBJECTIVE 33

Prepare a departmental production report using the weighted average method

COPYRIGHT © 2012 Nelson Education Ltd.

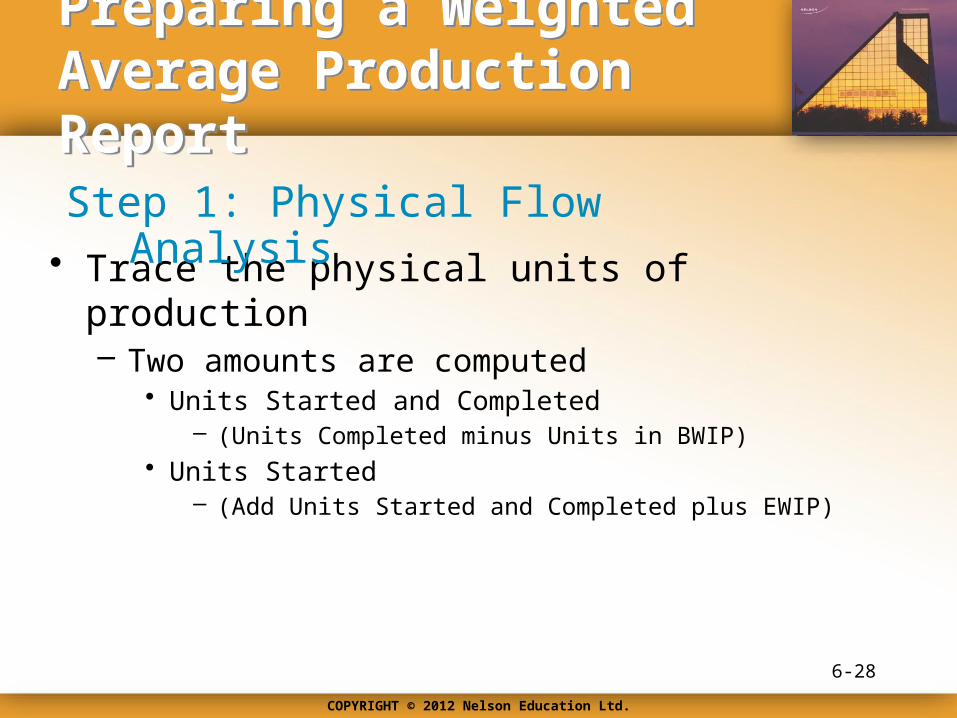

Preparing a Weighted Average Production ReportPreparing a Weighted Average Production Report

• Trace the physical units of production– Two amounts are computed

• Units Started and Completed – (Units Completed minus Units in BWIP)

• Units Started– (Add Units Started and Completed plus EWIP)

Step 1: Physical Flow Analysis

6-28

COPYRIGHT © 2012 Nelson Education Ltd.

Preparing a Weighted Average Production ReportPreparing a Weighted Average Production Report

• Adding together– Units Completed– Units in Ending Work In Process × Fraction Complete

• Beginning Inventory– Included in the units completed– Treats beginning inventory as if it was started and

completed the current period

Step 2: Calculation of Equivalent Units

6-29

COPYRIGHT © 2012 Nelson Education Ltd.

Preparing a Weighted Average Production ReportPreparing a Weighted Average Production Report

• Manufacturing Costs ÷ Equivalent Unit– Costs include:

• Prior period costs associated with beginning work-in-process• Current period manufacturing costs

Step 3: Computation of Unit Cost

6-30

COPYRIGHT © 2012 Nelson Education Ltd.

Preparing a Weighted Average Production ReportPreparing a Weighted Average Production Report

• Computing cost of goods transferred out– Multiplying

• Unit cost (computed in step #3)• Units completed (computed in step #1)

• Computing cost of ending work in process – Multiplying

• Unit cost (computed in step #3)• Equivalent units (computed in step #2)

Step 4: Valuation of Inventories

6-31

COPYRIGHT © 2012 Nelson Education Ltd.

• Checks to see if:– Costs to account for

• Beginning Work In Process + Costs incurred during the period

– Equal• Costs assigned to inventory

– Transferred out + Ending Work-In-Process

Step 5: Cost Reconciliation

Cornerstones 6-4, 6-5, and 6-6 will walk us through an example

6-32

Preparing a Weighted Average Production ReportPreparing a Weighted Average Production Report

COPYRIGHT © 2012 Nelson Education Ltd.

Example: Cornerstone 6-4Example: Cornerstone 6-4

Units in process, July 1, 75% completeProduction:

20,000 litres

Units completed and transferred out 50,000 litres

Units in process, July 31, 25% complete 10,000 litres

Information:

6-33

How to Measure Output and Assign Costs: Weighted Average

Work in process, July 1Costs:

$3,525Costs added during July $10,125

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

• Calculate an output measure for July

• Assign costs to units transferred out and ending work in process using the weighted average method

Required:

6-34

COPYRIGHT © 2012 Nelson Education Ltd.

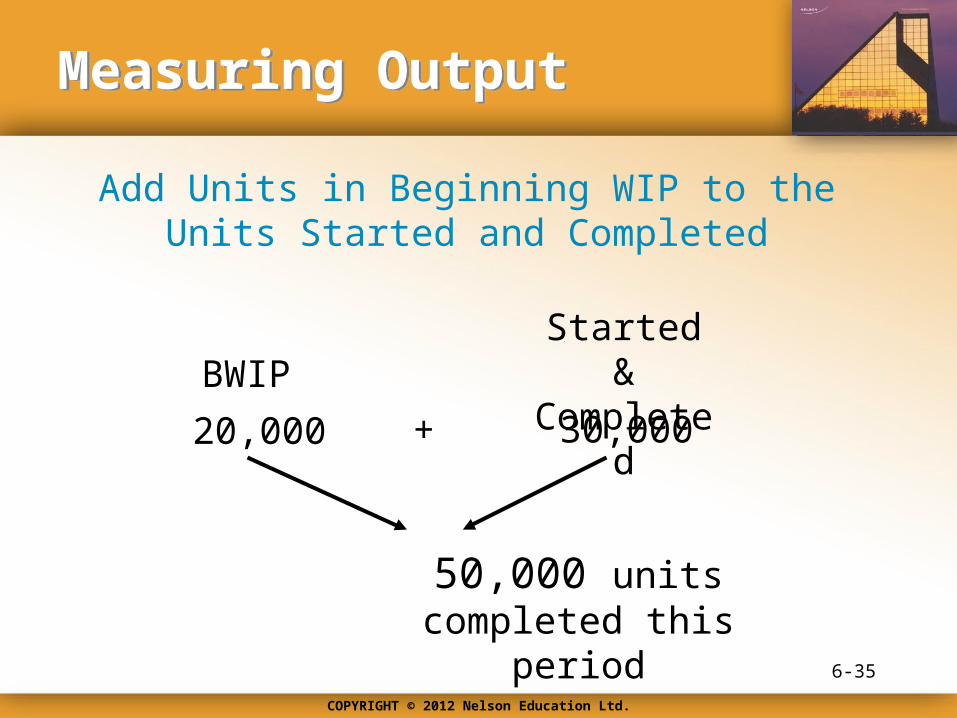

Measuring OutputMeasuring Output

20,000 + 30,000

Add Units in Beginning WIP to the Units Started and Completed

50,000 units completed this period

BWIPStarted &

Completed

6-35

COPYRIGHT © 2012 Nelson Education Ltd.

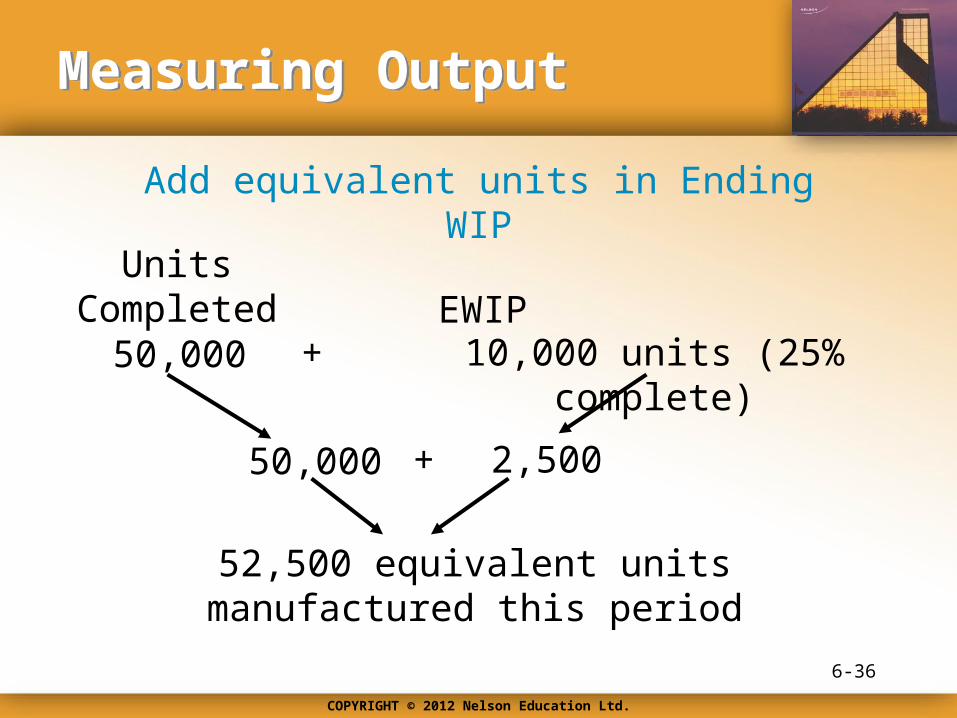

Measuring OutputMeasuring Output

50,000 + 10,000 units (25% complete)

Add equivalent units in Ending WIP

52,500 equivalent units manufactured this period

50,000 2,500+

Units Completed EWIP

6-36

COPYRIGHT © 2012 Nelson Education Ltd.

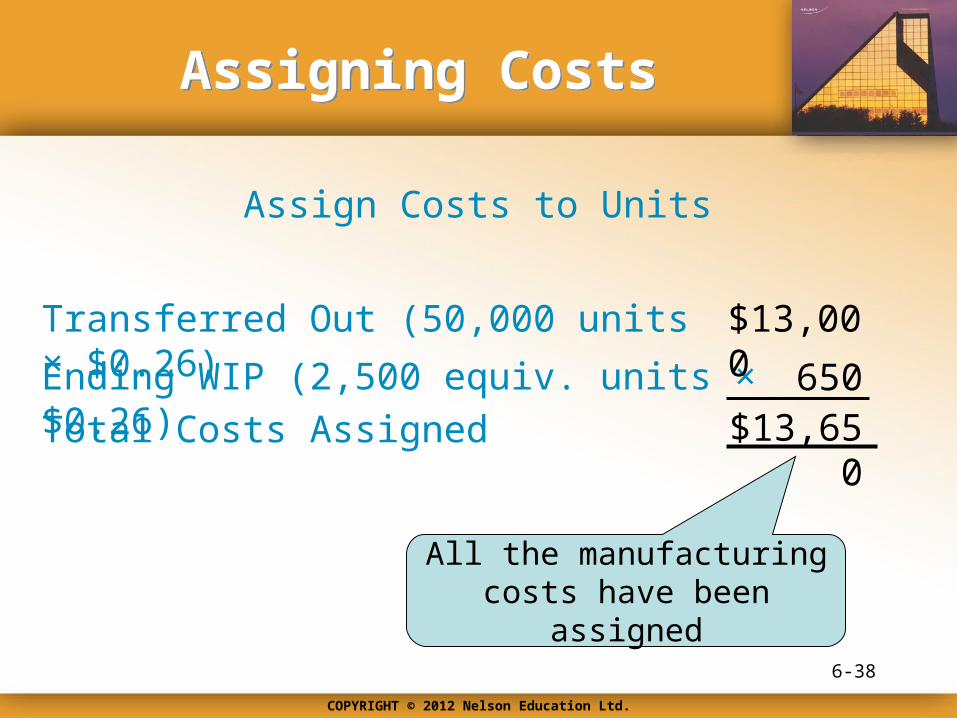

Assigning CostsAssigning Costs

Costs added during July 10,125$13,650

Work in process, July 1

Total costs assigned

$ 3,525

Unit cost = $13,650/52,500 equivalent units

Unit cost = $0.26 per equivalent unit

Compute Unit Cost

6-37

COPYRIGHT © 2012 Nelson Education Ltd.

Assigning CostsAssigning Costs

Ending WIP (2,500 equiv. units × $0.26) 650$13,650

Transferred Out (50,000 units × $0.26)

Total Costs Assigned

$13,000

Assign Costs to Units

All the manufacturing costs have been assigned

6-38

COPYRIGHT © 2012 Nelson Education Ltd.

Example: Cornerstone 6-5Example: Cornerstone 6-5

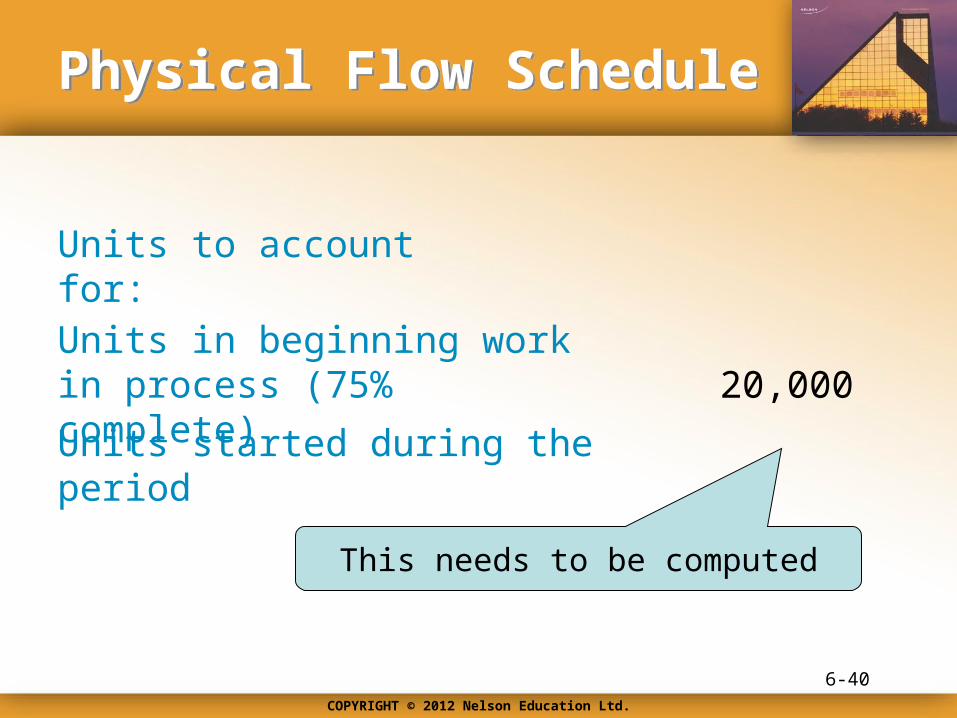

Units in process, July 1, 75% completeProduction:

20,000 litresUnits completed and transferred out 50,000 litresUnits in process, July 31, 25% complete 10,000 litres

Information:

Required:

Prepare a physical flow schedule

6-39

How to Prepare a Physical Flow Schedule

COPYRIGHT © 2012 Nelson Education Ltd.

Physical Flow SchedulePhysical Flow Schedule

Units in beginning work in process (75% complete) 20,000

Units started during the period

Units to account for:

This needs to be computed

6-40

COPYRIGHT © 2012 Nelson Education Ltd.

Units Started and CompletedUnits Started and Completed

Units started and completed =

Units completed

= 50,000

– Units, BWIP

– 20,000Units started and

completed

Units started and completed = 30,000

6-41

COPYRIGHT © 2012 Nelson Education Ltd.

Units StartedUnits Started

Units started =Units

started and completed

= 30,000

+ Units, EWIP

+ 10,000

Units started = 40,000

Units started

6-42

COPYRIGHT © 2012 Nelson Education Ltd.

Physical Flow SchedulePhysical Flow Schedule

Units in beginning work in process (75% complete) 20,000

Units started during the period 40,000Total units to account for 60,000

Units to account for:

6-43

COPYRIGHT © 2012 Nelson Education Ltd.

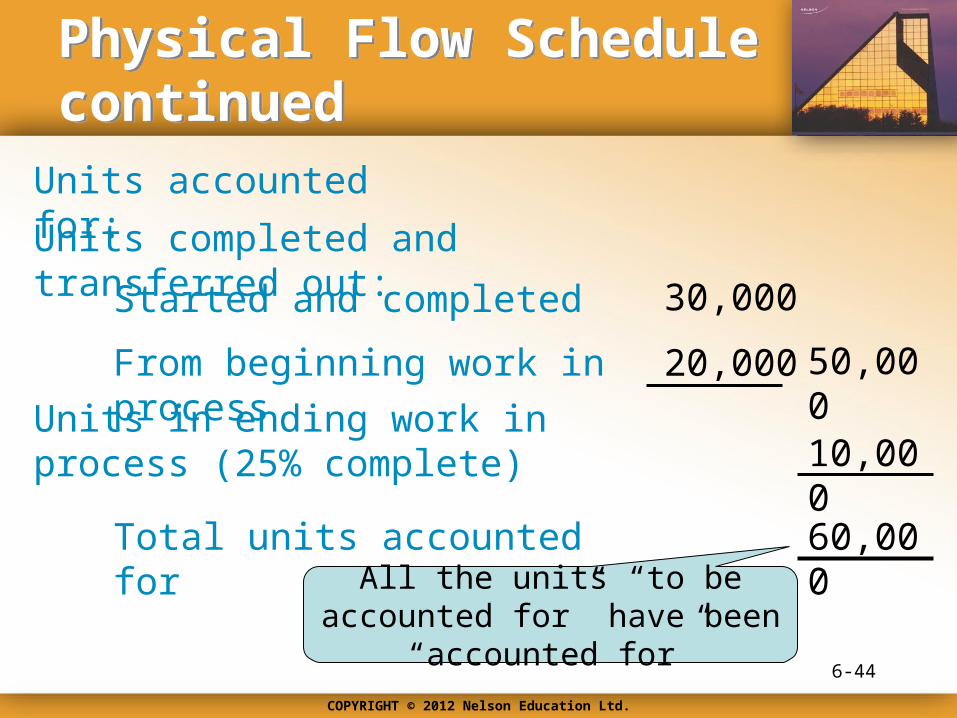

Physical Flow Schedule continuedPhysical Flow Schedule continued

Units completed and transferred out:

30,000Started and completed

20,000

Total units accounted for 60,000

Units accounted for:

From beginning work in process

Units in ending work in process (25% complete)

50,000

10,000

All the units “to be accounted for” have been “accounted for”

6-44

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

Calculation of Equivalent Units

Units completed 50,000

Now we need to calculate the unit cost

Add: Units in ending work in process × fraction complete 2,500

52,500Equivalent units of output

6-45

10,000 × 25%

COPYRIGHT © 2012 Nelson Education Ltd.

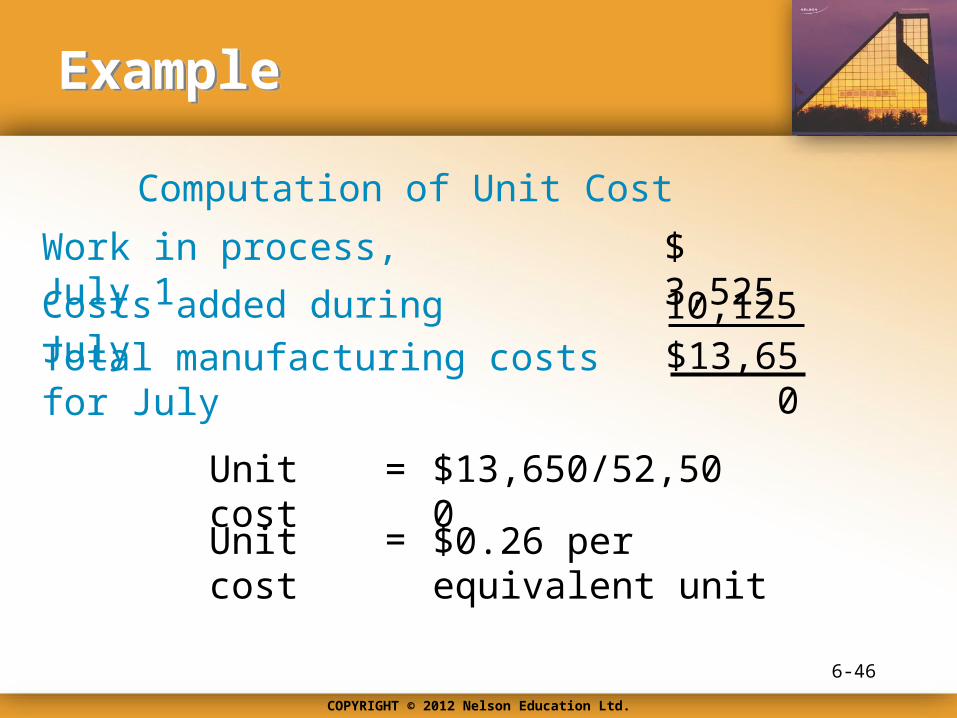

ExampleExample

Computation of Unit Cost

Costs added during July 10,125$13,650

Work in process, July 1

Total manufacturing costs for July

$ 3,525

Unit cost = $13,650/52,500

Unit cost = $0.26 per equivalent unit

6-46

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

Goods in ending work in process 650

Total manufacturing costs assigned to inventories are as follows:

$13,000Goods transferred out

Total costs accounted for $13,650

Cost Reconciliation

6-47

50,000 units × $0.26

2,500 units × $0.26

COPYRIGHT © 2012 Nelson Education Ltd.

Example: Cornerstone 6-6Example: Cornerstone 6-6

Information:Calculations in Cornerstones 6-4 & 6-5

Prepare a production reportRequired:

6-48

How to Prepare a Production Report: Weighted Average Method

COPYRIGHT © 2012 Nelson Education Ltd.

Healthblend CompanyPicking Department

Production Report for July 2011

Unit InformationPhysical FlowUnits To Account For:

20,00040,000

Units in Beg. WIPUnits started

Total units to account for 60,000

Units Accounted For:Units completed 50,000Units in End. WIP 10,000

Total units accounted for 60,000

Equivalent Units

Units completed 50,000Units in EWIP 2,500

52,500Total equivalent units

6-49

COPYRIGHT © 2012 Nelson Education Ltd.

Healthblend CompanyPicking Department

Production Report for July 2011

(Continued)

Cost Information

Costs to account for:

$ 3,525

10,125

Beginning Work In Process

Incurred during the period

Total costs to account for $13,650

Cost per equivalent unit $ 0.26

6-50

COPYRIGHT © 2012 Nelson Education Ltd.

Healthblend CompanyPicking Department

Production Report for July 2011

(Continued)

Costs accounted for:$13,000

$650Goods transferred out

Total costs accounted for $13,650

Transferred Out

Ending WIP Total

Goods in Ending WIP ---

$13,000

--- $13,000

$650

650

6-51

COPYRIGHT © 2012 Nelson Education Ltd.

Evaluation of the Weighted Average MethodEvaluation of the Weighted Average Method

Major benefit of this method is the simplicity

Main disadvantage is reduced accuracy in computing unit costs

If greater accuracy is desired, a company should use the FIFO method to determine unit costs

6-52

OBJECTIVE OBJECTIVE 44

Explain how nonuniform inputs and multiple

processing departments affect process costing

COPYRIGHT © 2012 Nelson Education Ltd.

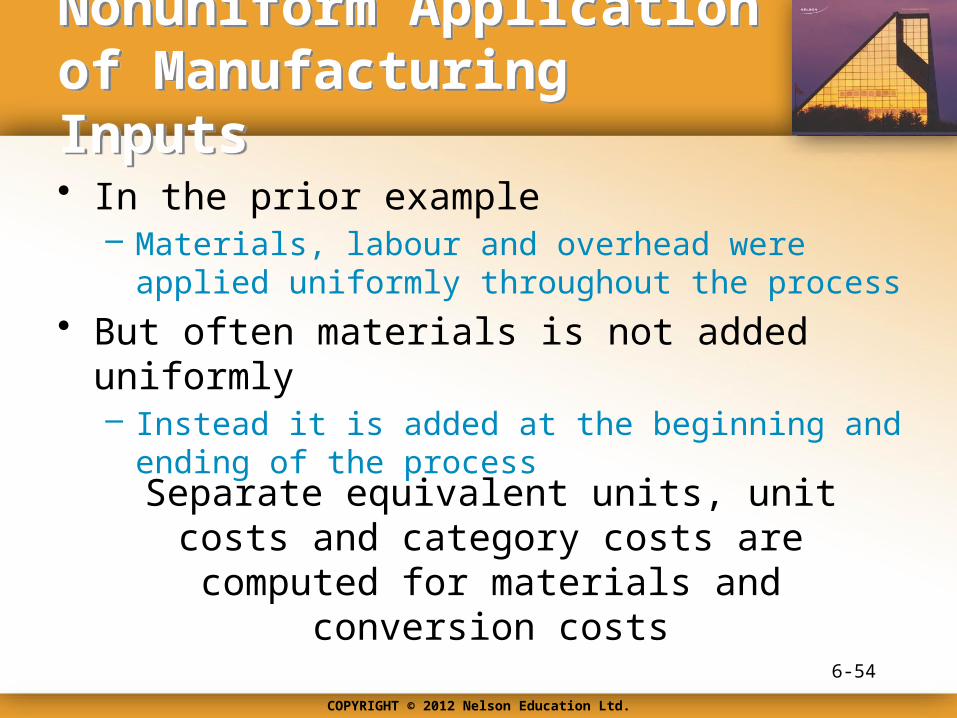

Nonuniform Application of Manufacturing InputsNonuniform Application of Manufacturing Inputs

• In the prior example– Materials, labour and overhead were applied uniformly

throughout the process

• But often materials is not added uniformly– Instead it is added at the beginning and ending of the

process

6-54

Separate equivalent units, unit costs and category costs are computed for materials

and conversion costs

COPYRIGHT © 2012 Nelson Education Ltd.

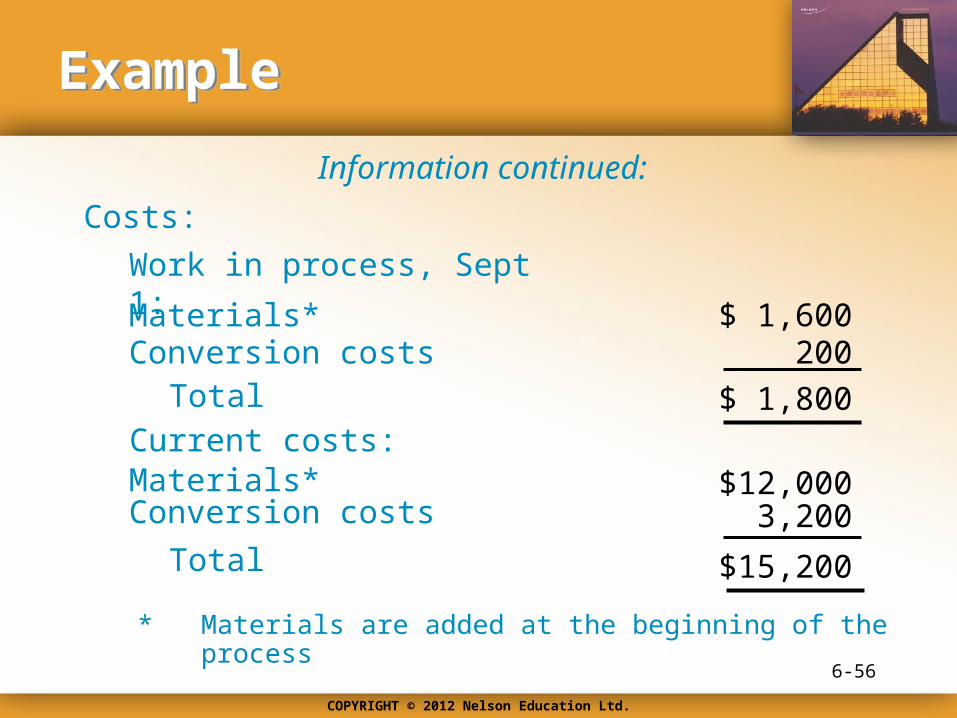

Example: Cornerstone 6-7Example: Cornerstone 6-7

Units in process, Sept 1, 50% complete*Production:

10,000Units completed and transferred out 60,000Units in process, Sept 30, 40% complete* 20,000

Information:

* Percentage complete as to conversion costs

6-55

How to Calculate Equivalent Units, Unit Costs, and Value Inventories with Nonuniform Inputs

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

Work in process, Sept 1:

Costs:

$ 1,600

Current costs:

Information continued:

Materials* Conversion costs 200

$ 1,800Total

$12,000Materials* Conversion costs 3,200

$15,200Total

* Materials are added at the beginning of the process

6-56

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

• Calculate equivalent units

• Calculate unit cost

• Calculate the valuation of the inventories

Required:

6-57

COPYRIGHT © 2012 Nelson Education Ltd.

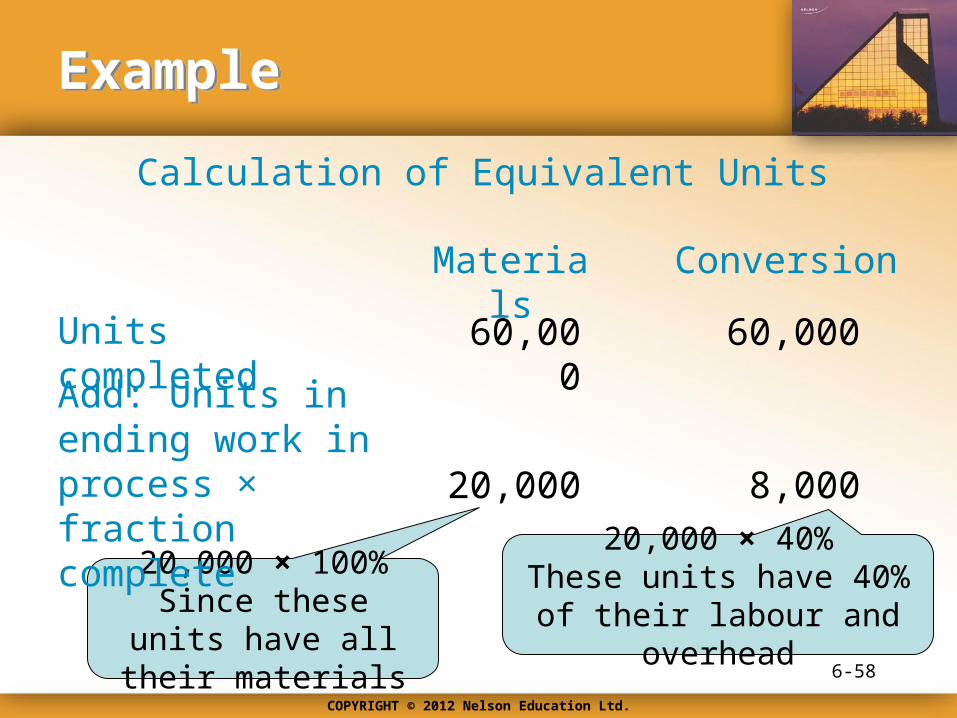

ExampleExample

20,000 × 100%Since these units

have all their materials

Materials

Calculation of Equivalent Units

Conversion

Units completed

Add: Units in ending work in process × fraction complete

60,000 60,000

20,000

6-58

8,000

20,000 × 40%These units have 40% of their labour and overhead

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

Materials

Calculation of Equivalent Units

Conversion

Units completed

Add: Units in ending work in process × fraction complete

60,000 60,000

20,000 8,000

Equivalent units of output 80,000 68,000

6-59

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

Calculation of Unit Cost

Unit materials cost = ($1,600 + $12,000)/80,000

Unit conversion cost

Unit materials cost = $0.17

= ($200 + $3,200)/68,000Unit conversion cost = $0.05

Total unit cost = $0.17 + $0.05Total unit cost = $0.22

6-60

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

Valuation of Ending Work in Process and Goods Transferred Out

Cost of ending work in process:$3,400Materials $0.17 × 20,000

Conversion $0.05 × 8,000 400Total cost $3,800

Valuation of goods transferred out:Cost of goods transferred out $13,200

$0.22 × 60,0006-61

COPYRIGHT © 2012 Nelson Education Ltd.

Multiple DepartmentsMultiple Departments

Some departments receive partially completed goods from prior departments

Usual approach is to treat transferred-in goods as a separate material category

Cost of this material is the cost of the goods transferred out as computed in

the prior department

6-62

COPYRIGHT © 2012 Nelson Education Ltd.

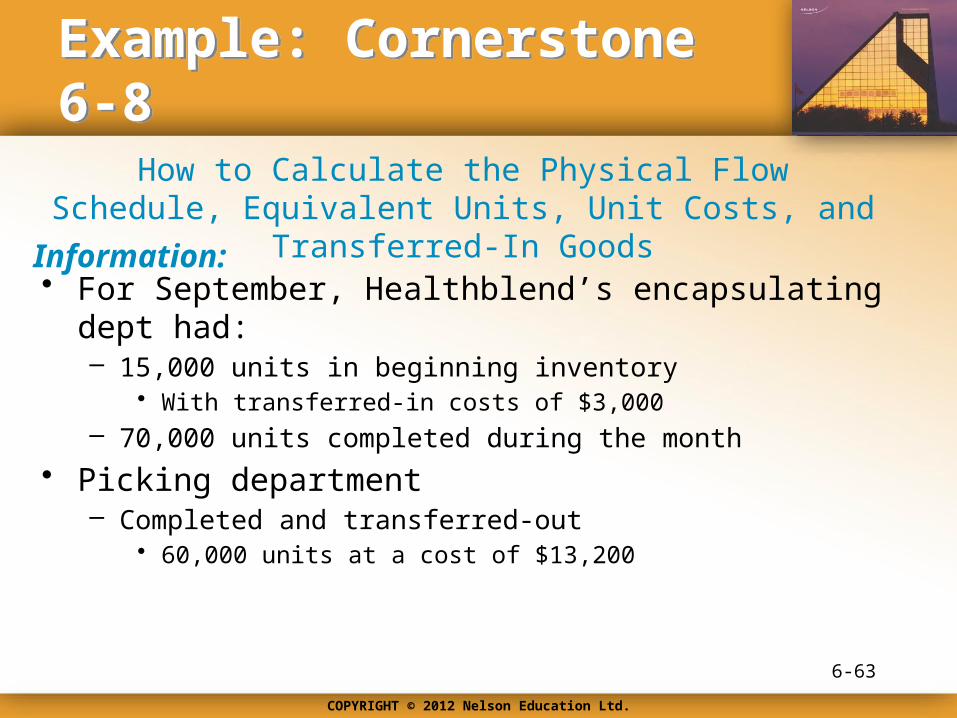

Example: Cornerstone 6-8Example: Cornerstone 6-8

• For September, Healthblend’s encapsulating dept had:– 15,000 units in beginning inventory

• With transferred-in costs of $3,000– 70,000 units completed during the month

• Picking department– Completed and transferred-out

• 60,000 units at a cost of $13,200

Information:

6-63

How to Calculate the Physical Flow Schedule, Equivalent Units, Unit Costs, and Transferred-In Goods

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

• Prepare a physical flow schedule with transferred-in goods• Calculate equivalent units for the transferred-in category• Calculate unit cost for the transferred-in category

Required:

6-64

COPYRIGHT © 2012 Nelson Education Ltd.

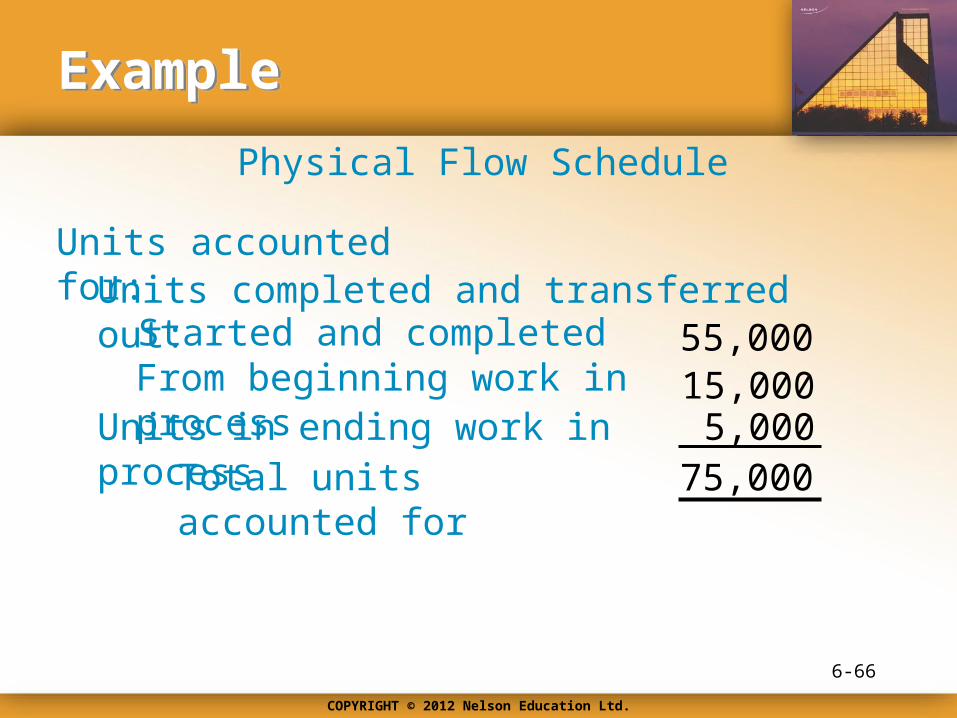

ExampleExample

Physical Flow Schedule

Units to account for:Units in beginning work in process 15,000

60,000Units transferred in during Sept.Total units to account for 75,000

6-65

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

Physical Flow Schedule

Units accounted for:Units completed and transferred out:

55,000Started and completedFrom beginning work in process 15,000

Units in ending work in processTotal units accounted for

5,00075,000

6-66

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

67

Equivalent Units for the transferred-in category

Units completedAdd: Units in ending work in process × fraction complete

70,000Transferred-in:

5,000

Equivalent units of output 70,000

5,000 × 100%since

these units have all

their materials

COPYRIGHT © 2012 Nelson Education Ltd.

ExampleExample

Calculation of Unit Cost for the Transferred-in Category

Unit cost = ($13,200 + $3,000)/75,000

$0.216

Unit cost = $16,200 / 75,000

Unit cost =

6-68

For the transferred-in category

OBJECTIVE OBJECTIVE 55

Appendix:

Prepare a departmental production report using

the FIFO method

COPYRIGHT © 2012 Nelson Education Ltd.

Production ReportFIFO CostingProduction ReportFIFO Costing

• Separates the cost of BWIP from cost of current period

• Review:– Cornerstone 6-9, How to calculate output and cost

assignments: FIFO method, page 264; and– Cornerstone 6-10, How to prepare a production report:

FIFO method, page 267

6-70