Chapter no. 6 Final accounts with adjustment. meaning Financial statements which are prepared...

32

Chapter no. 6 Chapter no. 6 Final accounts with Final accounts with adjustment adjustment

-

Upload

crystal-davidson -

Category

Documents

-

view

217 -

download

0

Transcript of Chapter no. 6 Final accounts with adjustment. meaning Financial statements which are prepared...

Chapter no. 6Chapter no. 6

Final accounts with Final accounts with adjustmentadjustment

meaningmeaning

Financial statements which are Financial statements which are preparedprepared

at the end of the year to know about at the end of the year to know about the the

financial position of the business are financial position of the business are called called

final accounts. final accounts.

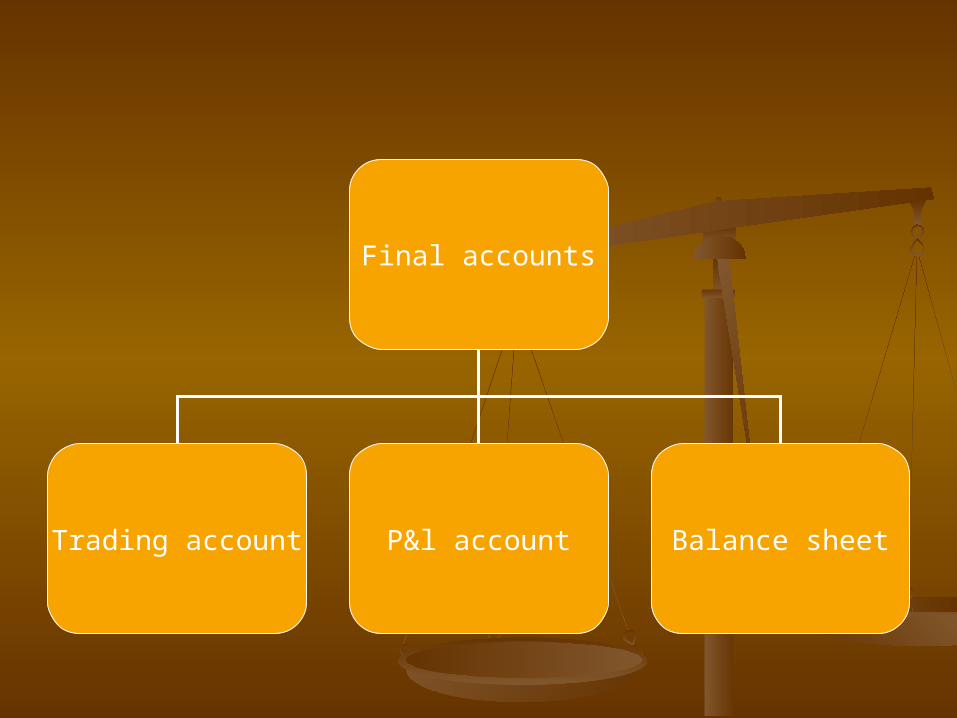

Parts of final acountsParts of final acounts

Trading accountTrading account

Profit and loss accountProfit and loss account

Balance sheetBalance sheet

Final accounts

Trading account P&l account Balance sheet

Need and importance of final Need and importance of final accountsaccounts

To know the result of a businessTo know the result of a business To know the financial position of a To know the financial position of a

businessbusiness To get loans from financial To get loans from financial

institutionsinstitutions To assess income taxTo assess income tax To conduct comparative studyTo conduct comparative study To assist management of businessTo assist management of business

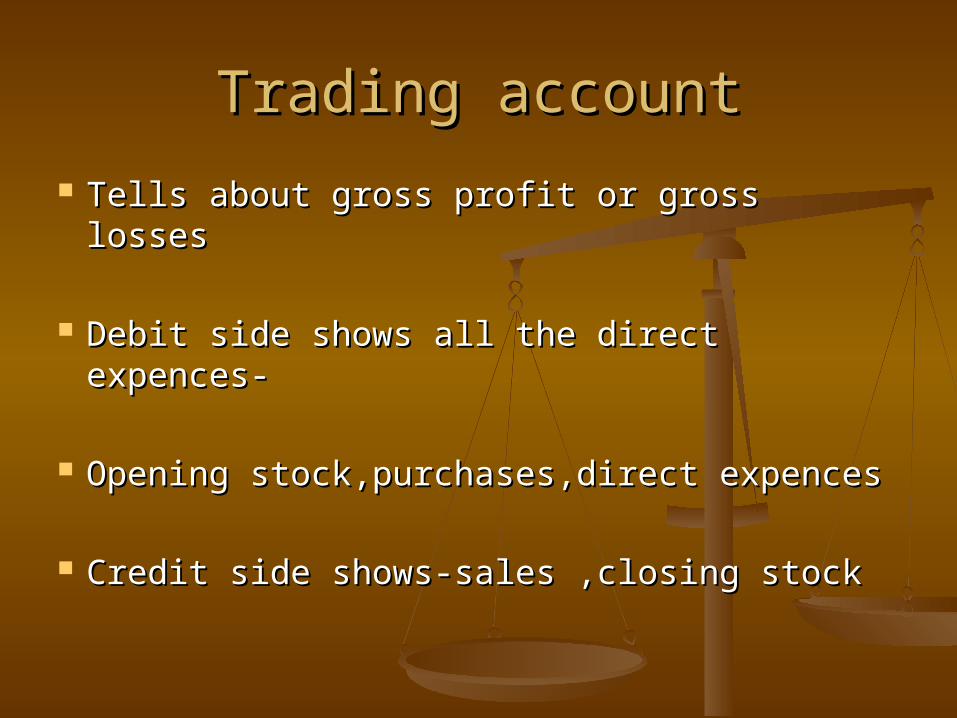

Trading accountTrading account

Tells about gross profit or gross lossesTells about gross profit or gross losses

Debit side shows all the direct expences-Debit side shows all the direct expences-

Opening stock,purchases,direct expencesOpening stock,purchases,direct expences

Credit side shows-sales ,closing stockCredit side shows-sales ,closing stock

Profit and loss accountProfit and loss account

Tells about net profit and net losses.Tells about net profit and net losses.

Debit side shows all indirect Debit side shows all indirect expences and losses.expences and losses.

Credit side shows all indirect incomes Credit side shows all indirect incomes and gains.and gains.

Importance of p&l acountImportance of p&l acount

Tells net profitibilityTells net profitibility

Comparative study of profit and lossComparative study of profit and loss

Control on unnecessary expencesControl on unnecessary expences

Helpful in preparing balance sheetHelpful in preparing balance sheet

Balance sheetBalance sheet

It is a statement to know about It is a statement to know about financial financial

position of a business on a certain position of a business on a certain fixedfixed

date .date .

Need and Importance of balance Need and Importance of balance sheetsheet

Tells about financial position of a firmTells about financial position of a firm Tells about liquidity position of a firm Tells about liquidity position of a firm Tells about the balance of debtors Tells about the balance of debtors

and creditorsand creditors Tells about the liabilities and assets Tells about the liabilities and assets

of the firmof the firm Tells economically capability of a firmTells economically capability of a firm Opening entry on the basis of Opening entry on the basis of

balance sheetbalance sheet

Marshalling of balance sheetMarshalling of balance sheet

In order of liquidityIn order of liquidity

In order of permanenceIn order of permanence

Classification of assets and Classification of assets and liabilitiesliabilities

LiabilitiesLiabilities

long term liabilitieslong term liabilities

Current liabilitiesCurrent liabilities

Contingent Contingent liabilitiesliabilities

AssetsAssets

Fixed assetsFixed assets

Current assetsCurrent assets

Fictitious assetsFictitious assets

Wasting assetsWasting assets

Similarities between trial balance Similarities between trial balance and balance sheetand balance sheet

Both are statementBoth are statement To and by not usedTo and by not used Prepared from the balances of ledgerPrepared from the balances of ledger Prepared on a specific datePrepared on a specific date Balance of cash book written in bothBalance of cash book written in both

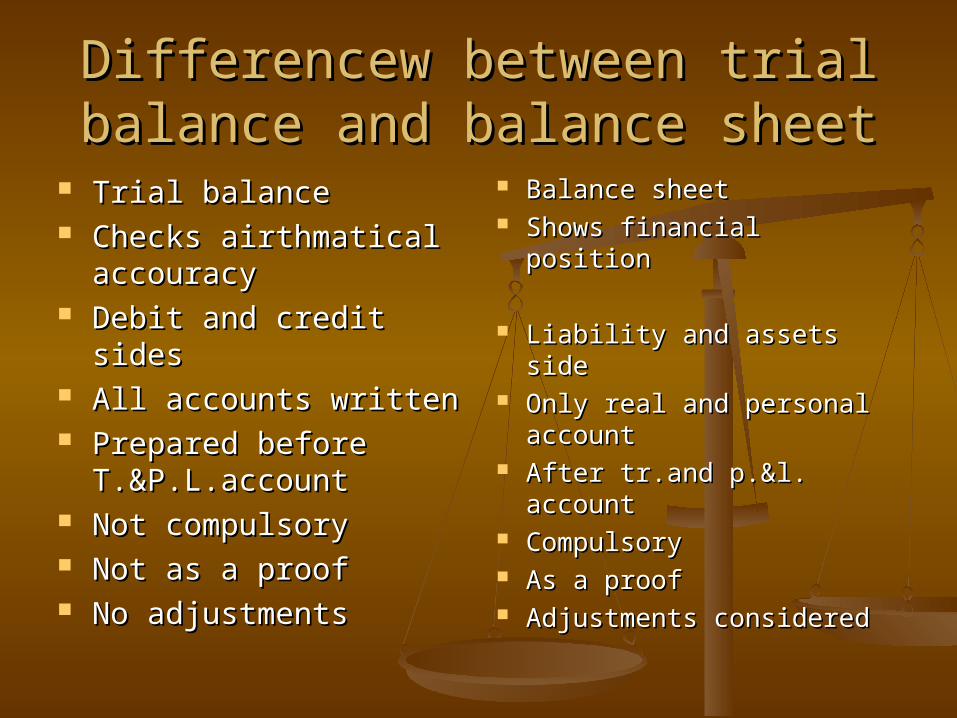

Differencew between trial balance Differencew between trial balance and balance sheetand balance sheet

Trial balanceTrial balance Checks airthmatical Checks airthmatical

accouracyaccouracy Debit and credit sidesDebit and credit sides All accounts writtenAll accounts written Prepared before Prepared before

T.&P.L.accountT.&P.L.account Not compulsoryNot compulsory Not as a proofNot as a proof No adjustmentsNo adjustments

Balance sheetBalance sheet Shows financial positionShows financial position

Liability and assets sideLiability and assets side Only real and personal Only real and personal

accountaccount After tr.and p.&l. After tr.and p.&l.

accountaccount CompulsoryCompulsory As a proofAs a proof Adjustments consideredAdjustments considered

adjustmentsadjustments

If any transaction omitsIf any transaction omits If wrongly entered in other accountIf wrongly entered in other account If amount is wrongly enteredIf amount is wrongly entered If any transation wrongly entered in If any transation wrongly entered in

wro ng side accoutwro ng side accout

Need and importance of Need and importance of adjustments adjustments

To find out correct profit and loss To find out correct profit and loss and financial positionand financial position

To rectify the errorTo rectify the error To complete the incomlete To complete the incomlete

transactiontransaction To record the transcactionsTo record the transcactions To record the current incomes and To record the current incomes and

expencesexpences

Closing stockClosing stock

Trading account (given in adj.):Trading account (given in adj.):

credit sidecredit side

Balance sheet :Balance sheet :

current assetscurrent assets

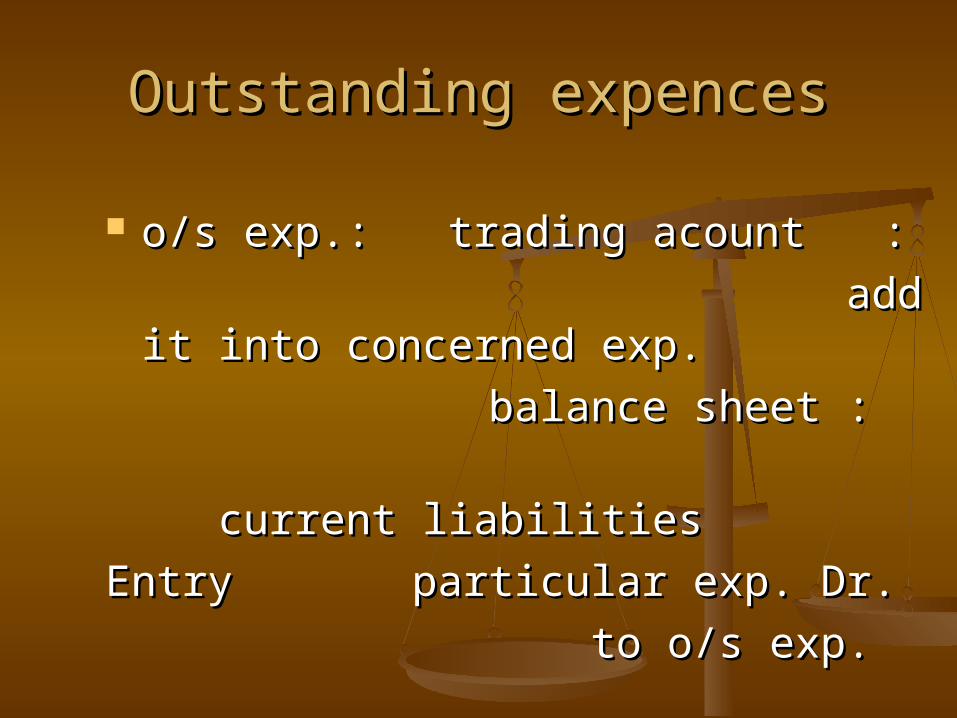

Outstanding expencesOutstanding expences

o/s exp.: trading acount :o/s exp.: trading acount :

add it into add it into concerned exp.concerned exp.

balance sheet : balance sheet :

current current liabilitiesliabilities

Entry particular exp. Dr.Entry particular exp. Dr.

to o/s exp.to o/s exp.

prepaid expencesprepaid expences

trading acount :trading acount :

deduct it into deduct it into concerned exp.concerned exp.

balance sheet : balance sheet :

current assetscurrent assets

Entry prepaid exp. Dr.Entry prepaid exp. Dr.

to particular exp.to particular exp.

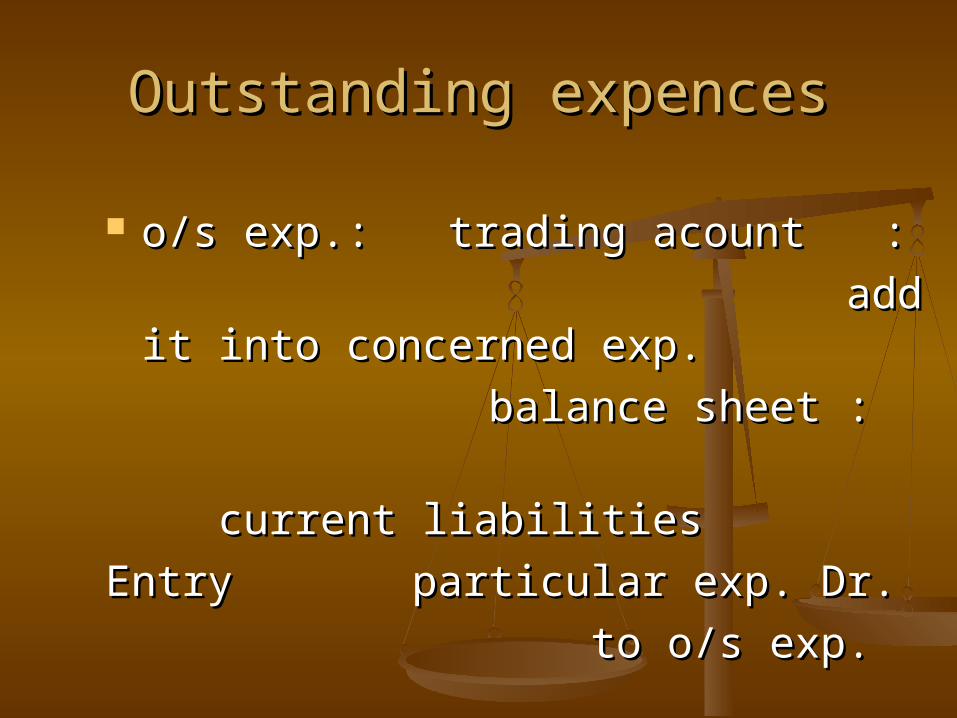

Outstanding expencesOutstanding expences

o/s exp.: trading acount :o/s exp.: trading acount :

add it into add it into concerned exp.concerned exp.

balance sheet : balance sheet :

current current liabilitiesliabilities

Entry particular exp. Dr.Entry particular exp. Dr.

to o/s exp.to o/s exp.

Outstanding incomeOutstanding income

o/s income: trading acount :o/s income: trading acount :

add it into add it into concerned incomeconcerned income

balance sheet : balance sheet :

current assetscurrent assets

Entry: accrued income. Dr.Entry: accrued income. Dr.

to particular incometo particular income

Prereceived or unearned incomePrereceived or unearned income

Trading and p/l accout :Trading and p/l accout : deduct from particular deduct from particular

incomeincome balance sheet :balance sheet : current liabilitycurrent liability

Entry : particular income dr;Entry : particular income dr; to unearned incometo unearned income

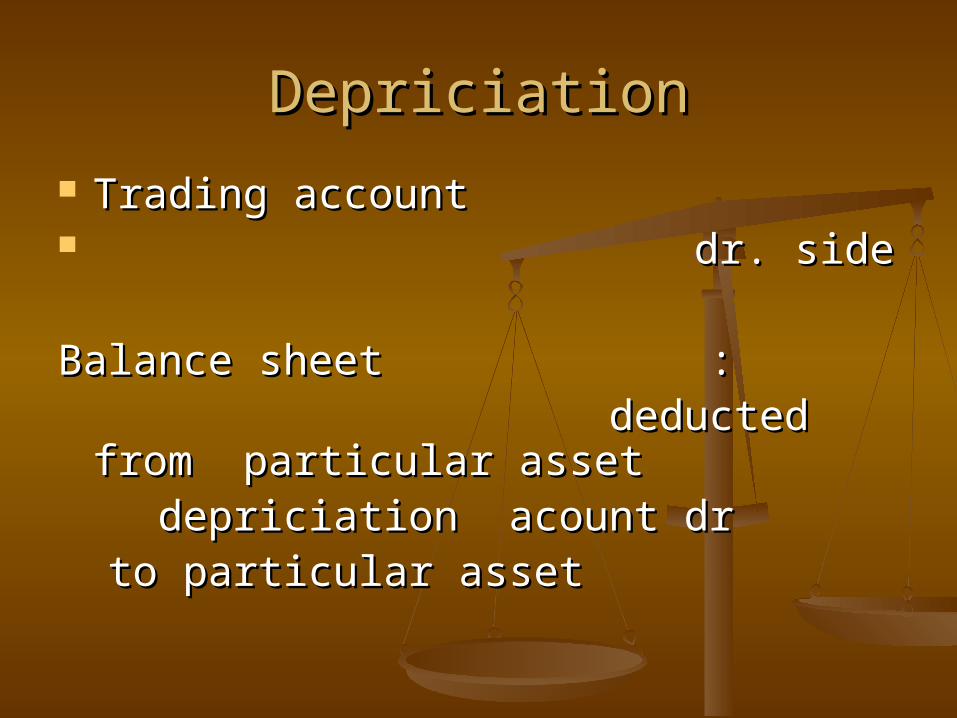

DepriciationDepriciation

Trading account Trading account dr. sidedr. side Balance sheet :Balance sheet : deducted from deducted from

particular assetparticular asset depriciation acount dr depriciation acount dr to particular assetto particular asset

Interest on capitalInterest on capital

Profit and loss account:Profit and loss account:

debit sidedebit side

balance sheet:balance sheet:

liability side add in liability side add in capitalcapital

entry interest on capital dr.entry interest on capital dr.

to capitalto capital

Interest on drawingInterest on drawing

Profit and loss account:Profit and loss account:

cedit sidecedit side

Balance sheet: Balance sheet:

liability side deducted in liability side deducted in capitalcapital

Entry drawing account dr.Entry drawing account dr.

to interest on drawing to interest on drawing

Interest on loanInterest on loan

Profit and loss account:Profit and loss account:

debit sidedebit side

Balance sheet: Balance sheet:

liability side added in liability side added in loanloan

Entry :Entry :

interest on loan account dr. interest on loan account dr.

To loan account To loan account

Bad debtsBad debts

Profit and loss account:Profit and loss account: debit sidedebit sideBalance sheet: Balance sheet: assets side deducted assets side deducted

from debtorfrom debtor Entry :Entry : bad debts account dr. bad debts account dr. To debtors account To debtors account

Provision for doubtful debtsProvision for doubtful debts

Profit and loss account:Profit and loss account: debit sidedebit sideBalance sheet: Balance sheet: assets side deducted assets side deducted

from debtorfrom debtor Entry :Entry : provision for debts account dr. provision for debts account dr. To debtors account To debtors account

Discount on debtorsDiscount on debtors

Profit and loss account:Profit and loss account: debit sidedebit sideBalance sheet: Balance sheet: assets side deducted assets side deducted

from debtorfrom debtor EntryEntry profit and loss account dr. profit and loss account dr. To discount on debtors To discount on debtors

account account

Provision for discount on creditorsProvision for discount on creditors

Profit and loss account:Profit and loss account: credit sidecredit sideBalance sheet: Balance sheet: liability side deducted liability side deducted

from creditorsfrom creditors EntryEntry discount on creditors account dr. discount on creditors account dr. To profit and loss account To profit and loss account

Implied interestImplied interest

Profit and loss account-Profit and loss account-

debit sidedebit side

Balance sheet- Balance sheet-

liability side added in liability side added in loanloan

Entry Entry

interest on loan account dr. interest on loan account dr.

to loan accountto loan account

Loss of goodsLoss of goods

Trading account- deducted from Trading account- deducted from purchasespurchases

Profit and loss account-debit sideProfit and loss account-debit side

Entry-loss account dr.Entry-loss account dr. To purchasesTo purchases p/l account dr.p/l account dr. to loss by accidentto loss by accident