Chapter 91 Business-Type Activities. Chapter 92 Learning Objectives Why governments and NFPs engage...

36

Chapter 9 1 Chapter 9 Business-Type Activities

-

Upload

coral-fields -

Category

Documents

-

view

230 -

download

4

Transcript of Chapter 91 Business-Type Activities. Chapter 92 Learning Objectives Why governments and NFPs engage...

Chapter 9 1

Chapter 9

Business-Type Activities

Chapter 9 2

Learning Objectives Why governments and NFPs engage in business-

type activities Distinguish between Proprietary and

Governmental activities Fundamental principles of Proprietary Fund

Accounting Enterprise Funds Internal Service Funds Accounting for Insurance Activities GASB 34, special problems of reporting

proprietary funds in government-wide statements

Chapter 9 3

Reasons for use-To compare benefits and costs of the

business-type activities of a government.

-Enhances management of activities

in which goods or services are

provided on a cost-reimbursement basis

to departments of the same government

or to the general public on a user charge basis. Example: the city of Houston maintains two

different types of proprietary funds. -Enterprise funds and Internal Service funds

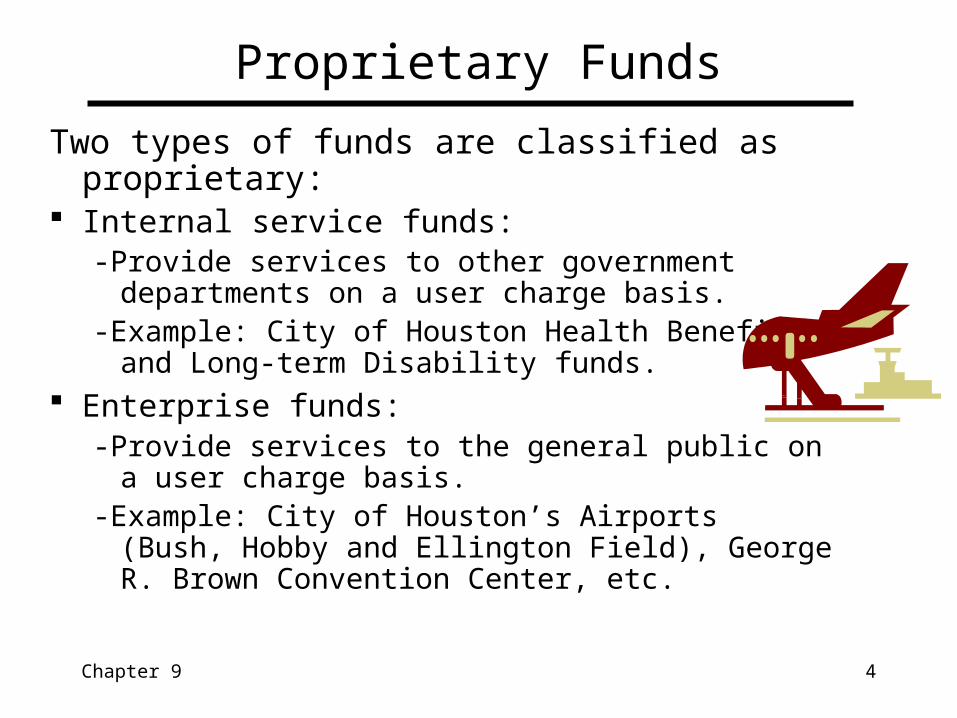

Proprietary Funds

Chapter 9 4

Proprietary Funds

Two types of funds are classified as proprietary: Internal service funds:

-Provide services to other government departments on a user charge basis.

-Example: City of Houston Health Benefit and Long-term Disability funds.

Enterprise funds: -Provide services to the general public on a user charge

basis. -Example: City of Houston’s Airports (Bush, Hobby and

Ellington Field), George R. Brown Convention Center, etc.

Chapter 9 5

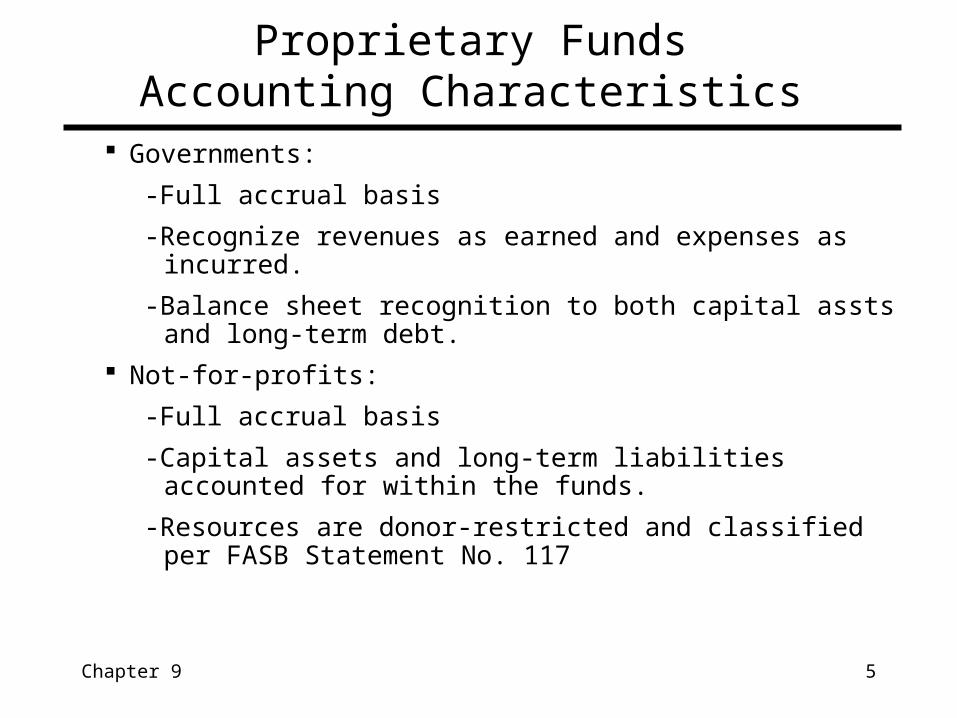

Governments:

-Full accrual basis

-Recognize revenues as earned and expenses as incurred.

-Balance sheet recognition to both capital assts and long-term debt.

Not-for-profits:

-Full accrual basis

-Capital assets and long-term liabilities accounted for within the funds.

-Resources are donor-restricted and classified per FASB Statement No. 117

Proprietary FundsAccounting Characteristics

Chapter 9 6

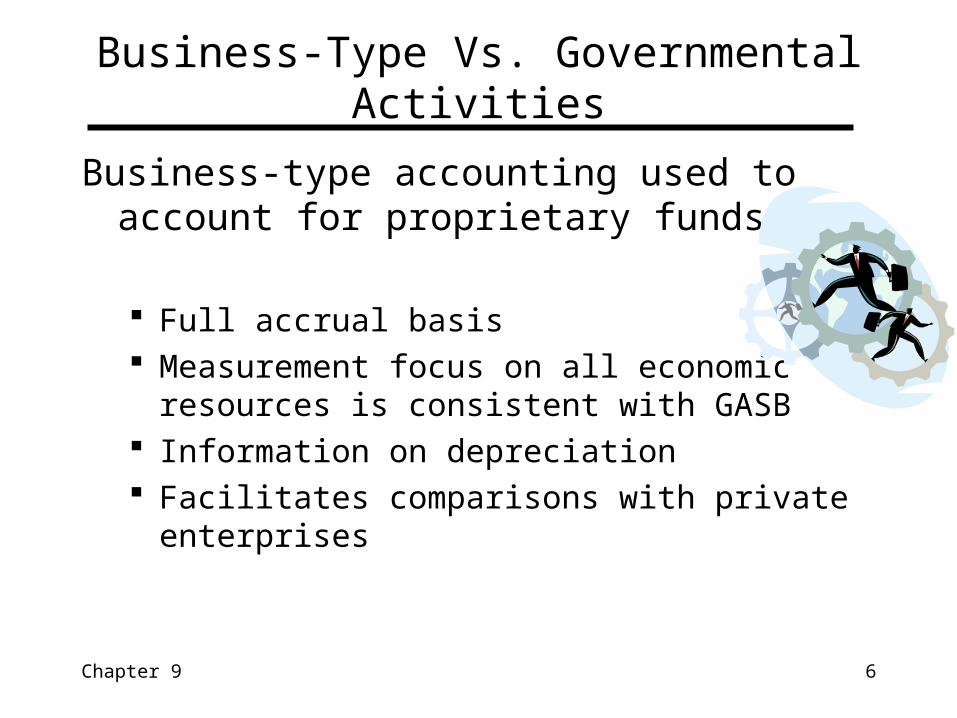

Business-Type Vs. Governmental Activities

Business-type accounting used to account for proprietary funds:

Full accrual basis Measurement focus on all economic resources is

consistent with GASB Information on depreciation Facilitates comparisons with private enterprises

Chapter 9 7

Similar to those for a for-profit entity: Statement of Net Assets (or Balance Sheet):

-Invested in capital assets, net of related debt-Restricted Net assets-Unrestricted Net Assets

Statement of Revenues, Expenses, and changes in Fund Net Assets:-comparable to income statement of a business-Reconciles beginning and ending net assets

Statement of Cash Flows:

-Required for proprietary funds but not

governmental funds

-Summarizes the entity’s cash account

Proprietary FundsRequired Financial Statements

Chapter 9 8

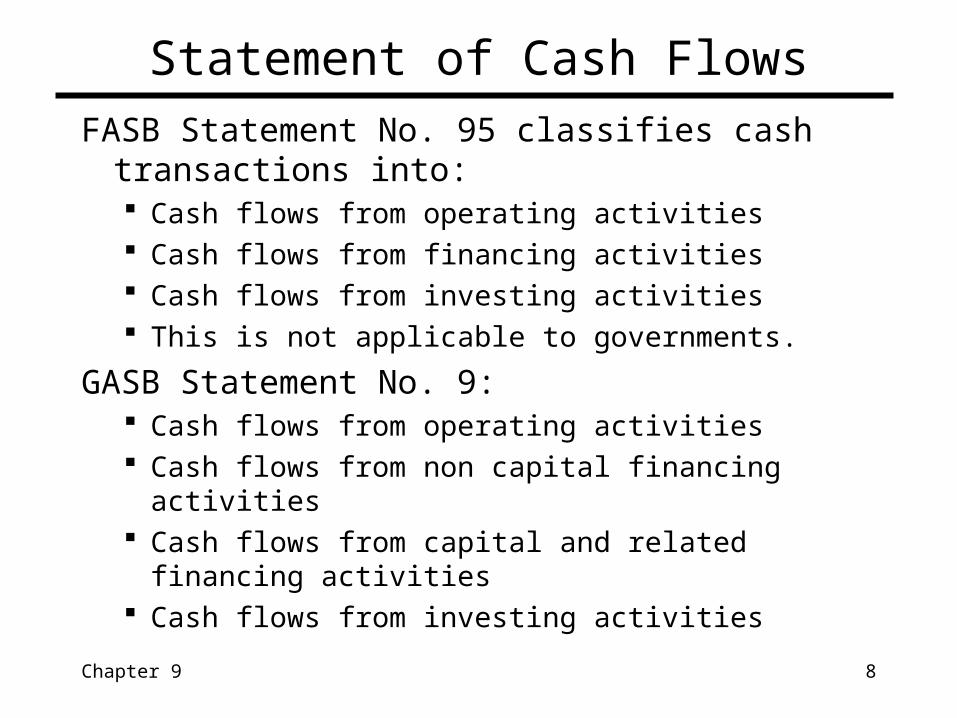

Statement of Cash Flows

FASB Statement No. 95 classifies cash transactions into: Cash flows from operating activities Cash flows from financing activities Cash flows from investing activities This is not applicable to governments.

GASB Statement No. 9: Cash flows from operating activities Cash flows from non capital financing activities Cash flows from capital and related financing activities Cash flows from investing activities

Chapter 9 9

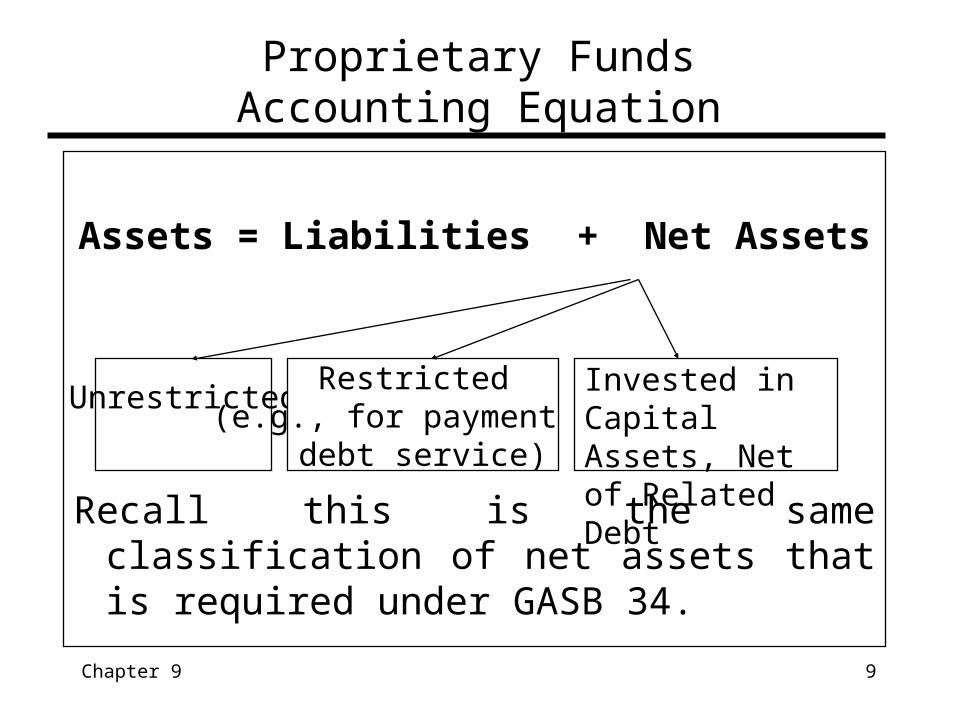

Assets = Liabilities + Net Assets

Recall this is the same classification of net assets that is required under GASB 34.

Proprietary Funds Accounting Equation

UnrestrictedRestricted

(e.g., for payment of debt service)

Invested in Capital Assets, Net of Related Debt

Chapter 9 10

Enterprise funds are used to report the same functionspresented as business-type activities in the government-wide financial statements.Reasons for use Used to -Account for services provided to the general public on a user charge basis

or where the governing body has determined that periodic determination of revenues earned, expenses incurred, and/or net income is appropriate

-For capital maintenance, public policy, management control, accountability, or other purposes

The City of Houston uses enterprise funds to account for its aviation system, combined utility system (formerly called the water and sewer system), and the convention and entertainment facilities.

Enterprise Funds

Chapter 9 11

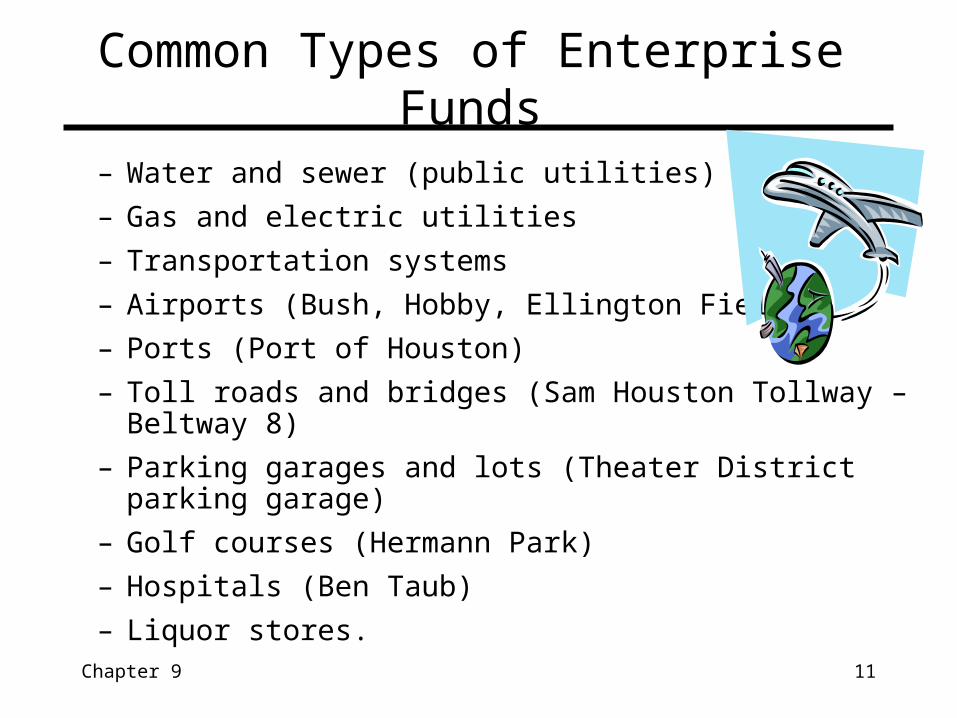

Common Types of Enterprise Funds

– Water and sewer (public utilities)

– Gas and electric utilities

– Transportation systems

– Airports (Bush, Hobby, Ellington Field)

– Ports (Port of Houston)

– Toll roads and bridges (Sam Houston Tollway – Beltway 8)

– Parking garages and lots (Theater District parking garage)

– Golf courses (Hermann Park)

– Hospitals (Ben Taub)

– Liquor stores.

Chapter 9 12

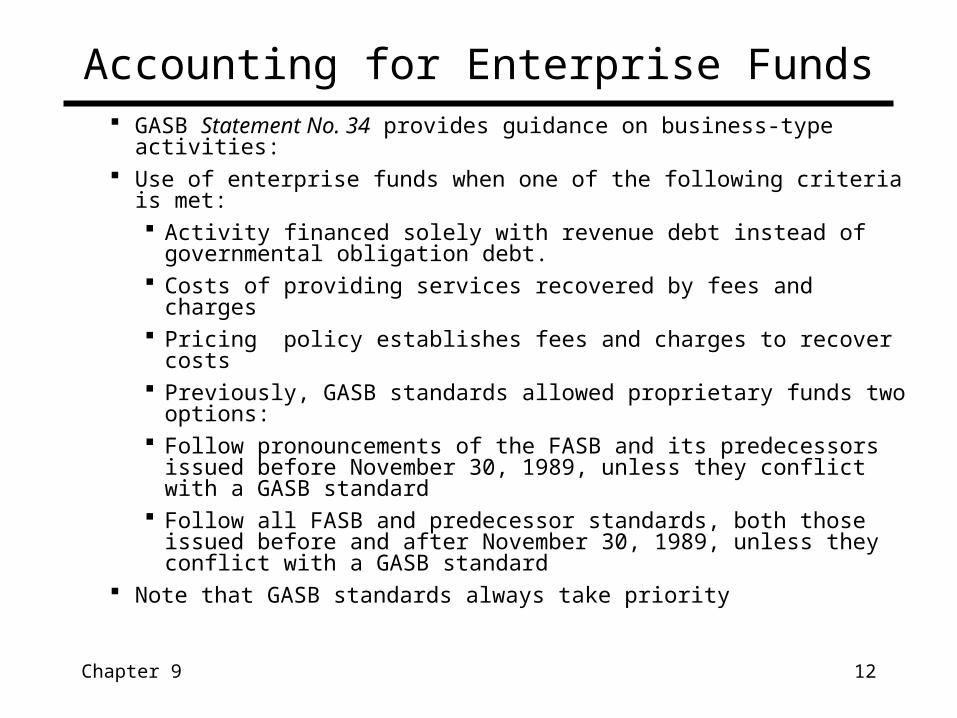

GASB Statement No. 34 provides guidance on business-type activities: Use of enterprise funds when one of the following criteria is met:

Activity financed solely with revenue debt instead of governmental obligation debt.

Costs of providing services recovered by fees and charges Pricing policy establishes fees and charges to recover costs Previously, GASB standards allowed proprietary funds two options: Follow pronouncements of the FASB and its predecessors issued

before November 30, 1989, unless they conflict with a GASB standard

Follow all FASB and predecessor standards, both those issued before and after November 30, 1989, unless they conflict with a GASB standard

Note that GASB standards always take priority

Accounting for Enterprise Funds

Chapter 9 13

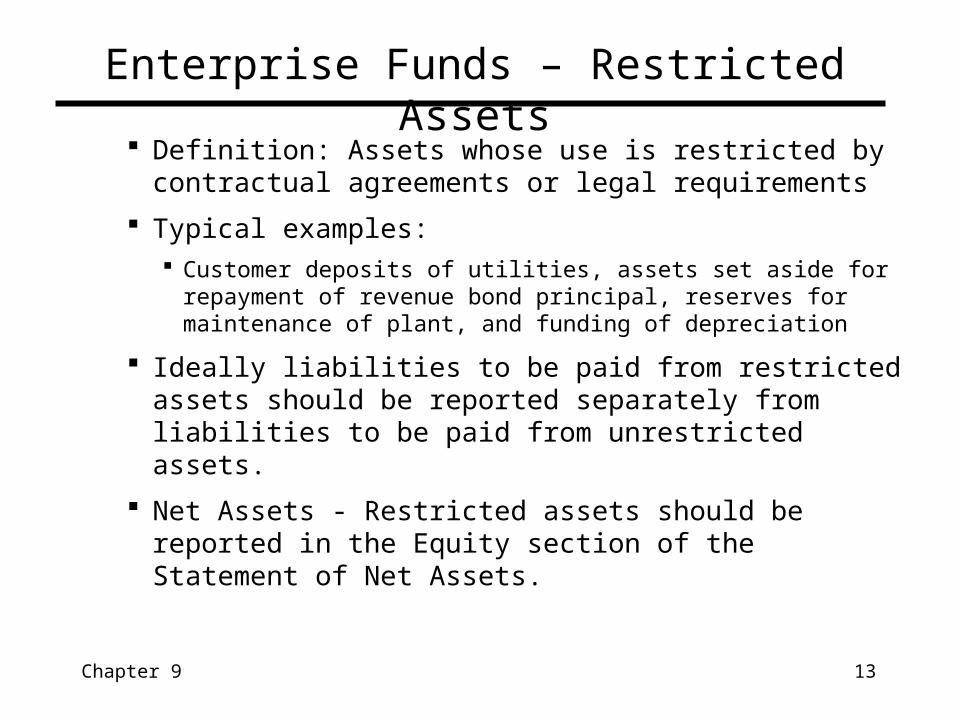

Definition: Assets whose use is restricted by contractual agreements or legal requirements

Typical examples: Customer deposits of utilities, assets set aside for repayment of

revenue bond principal, reserves for maintenance of plant, and funding of depreciation

Ideally liabilities to be paid from restricted assets should be reported separately from liabilities to be paid from unrestricted assets.

Net Assets - Restricted assets should be reported in the Equity section of the Statement of Net Assets.

Enterprise Funds – Restricted Assets

Chapter 9 14

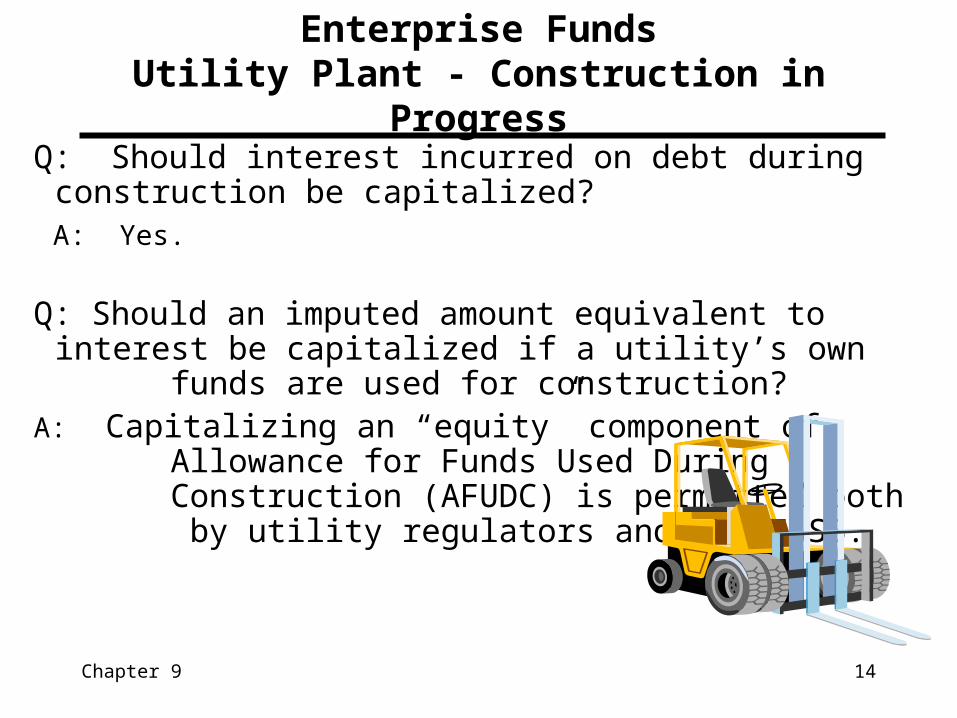

Enterprise FundsUtility Plant - Construction in Progress

Q: Should interest incurred on debt during construction be capitalized?

A: Yes.

Q: Should an imputed amount equivalent tointerest be capitalized if a utility’s own funds are used for construction?

A: Capitalizing an “equity” component of Allowance for Funds Used During Construction (AFUDC) is permitted both by utility regulators and the FASB.

Chapter 9 15

In addition to the usual Accounts Payable and Accrued Expenses, use two special current liability accounts: Customers Advances for Construction

Usually up-front deposits required to be made by builders to provide all or part of the cost of connecting new structures to utility lines. May or may not be refunded in part upon completion

Customer Deposits Usually reported under the caption “Liabilities

Payable from Restricted Assets”

Enterprise FundsSpecial Current Liabilities

Chapter 9 16

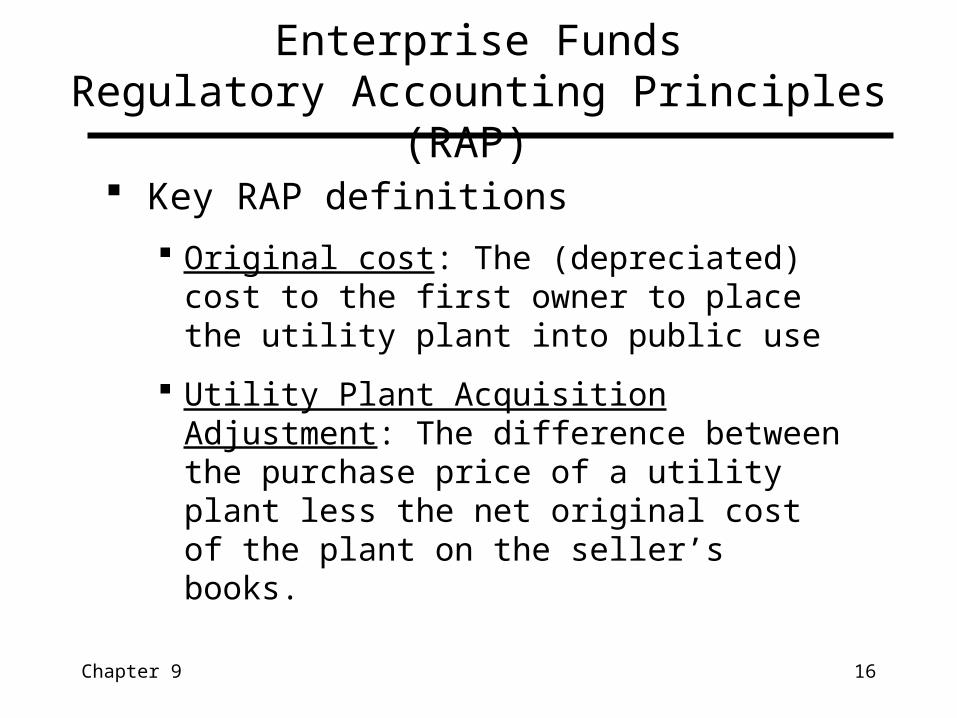

Key RAP definitions

Original cost: The (depreciated) cost to the first owner to place the utility plant into public use

Utility Plant Acquisition Adjustment: The difference between the purchase price of a utility plant less the net original cost of the plant on the seller’s books.

Enterprise FundsRegulatory Accounting Principles (RAP)

Chapter 9 17

Accounted for either in governmental or enterprise funds

If usage fees are charged—accounted for in enterprise funds.

Governments have to report both -- expense and liability.

Liability of post closure costs reported only in government-wide.

“Pay-as-you-go” basis

Municipal Solid Waste Landfills

Chapter 9 18

An EPA rule requires all municipal landfills to meet stringent location, design, and operating requirements to minimize the potential for environmental damage.

Operators must also provide financial assurance they can properly close landfills when full and provide post-closure ground water monitoring for 30 years after closure.

These stringent rules are designed to protect the environment from irresponsible handling of hazardous materials

Estimate the current cost of hiring a qualified third-party to close the MSWLF and care for it for 30 years after closure

Recognize a portion of this cost proportionate to the ratio of estimated capacity utilized during a year over the total capacity of the landfill as an expense of the enterprise fund and as a liability

Annual adjustments are made as estimates change from year to year.

Municipal Solid Waste Landfills (cont’d)

Chapter 9 19

Enterprise Funds Segment Information

When there are multiple enterprise funds

Summary operating data, including extent of intra- governmental subsidies, should be disclosed in the notes for "major non-homogeneous enterprise funds."

Chapter 9 20

Used to account for services provided by governmental units to other governments on a cost reimbursement basis.

These funds are accounting entities.

Promotes efficiency

Usually accounted for in general fund or some governmental fund

Authorized by legislative approval

ISF resources are rarely restricted.

Accounted for in general fund or other governmental fund.

Reasons for use: Improve management of common resources by placing them under centralized management and control

The City of Houston uses internal service funds to account for health and benefits and long-term disability activities.– Because both of these services predominantly benefit governmental rather than

business-type functions, they have been included within governmental activities in the government-wide financial statements.

Internal Service Funds

Chapter 9 21

Revenues recognized when earned.

Expenses recognized on full accrual basis.

Derives revenues mainly from other governmental or proprietary funds.

Accounting for both ISF & enterprise funds: must follow all FASB pronouncements issued prior to Nov. 30th 1989 unless it conflicts with GASB pronouncement.

Generally should use the same accounting procedures that a similar for-profit entity would use. Billings to Departments is the revenue account that is similar to Sales of a for-profit entity

Revenues and expenses are closed at year-end to Excess of Net Billings to Departments over Costs (or Excess of Costs over Net Billings to Departments) rather than to Income Summary

Accounting for Internal Service Funds

Chapter 9 22

Motor pools

Central purchasing

Storage

Issuance of supplies

Self-insurance pools

Central data processing

Printing

Common Types of Internal Service Funds

Chapter 9 23

Other than the slight difference in terminology, the financial statements are essentially the same as those of a comparable for-profit entity.

Statement of Net Assets

Statement of Revenues, Expenses, and Changes in Net Assets

Statement of Cash Flows - prepared in conformity with GASB standards rather than FASB standards.

Internal Service Funds Financial Statements

Chapter 9 24

Internal Service Funds Statement of Cash Flows

Similarities between GASB and FASB standards:

Cash Flows Statement shows cash inflows/outflows relating to operating, financing, and investing activities

Both sets of standards define cash flows as cash and cash equivalents (i.e., time deposits, marketable securities, and other items readily convertible to cash)

Chapter 9 25

Internal Service Fund—Illustration

Q: Assume that one of the government’s internal service funds was for data processing services, for which the golf course was billed $30,000, all of which was classified as “contractual services” in the golf course fund. How would that amount be reported in the column for ISF? How would it be reported in the government-wide financial statements?

A: Fund Statements: Billings of ISF would be reported as a revenue of ISF and as an expense of the golf course. The related cost of providing the service would be reported as an expense of the ISF.

Government-wide: Billings would be reported ONLY as an expense of the golf course. The revenues and expenses of the ISF would be eliminated in the consolidation process.

Chapter 9 26

Internal Service FundsCapital Assets and Depreciation

Depreciation of capital assets acquired by contributions or grants.

The issue is: should the ISF be able to recover in its prices or rates a cost it did not incur for such assets?

Chapter 9 27

ISF Illustration

Q: ISF reported $2.7 million in depreciation, an amount that the government takes into account in establishing the rates charged to other funds. How would this charge be reflected in the government-wide statements?

A: The depreciation charges are incorporated into the amounts billed to the funds to which the ISF provide services. Therefore, in the government-wide, they would be incorporated into the expenses of the functions accounted for in those funds.

Chapter 9 28

ISF Example

Q: In which column on the government-wide statement of net assets—that for governmental or business-type activities—is it most likely that the assets and liabilities of the ISF would be included?

A: Unless the ISF provide services mainly to units accounted for in proprietary funds, their assets and liabilities would be reported in the column for governmental-type activities.

Chapter 9 29

Pricing is set by local management or by legislative policy

Pricing objectives vary Can cover full costs (direct and indirect),

direct costs only, or whatever management desires.

Full cost prices do not reflect cost of providing incremental amounts of goods or services.

Legislative bodies are sometimes reluctant to establish ISFs because they are do not wish to let purchasing occur outside the budget.

Pricing Policies for Internal Service Funds

Chapter 9 30

Q: Is this a real concern?

Even if an ISF is created for central purchasing and sales of supplies, the legislative body still maintains budgetary control over the expenditures made by most departments and programs via the General Fund and special revenues funds budgets.

Internal Service Funds (cont’d)

Chapter 9 31

GASB-mandated use of an ISF GASB standards require that an ISF be used for risk

management (self-insurance) pools of a government: The ISF should recognize claims expense and a related liability

when: it is probable that an asset has been impaired or a liability has

been incurred and the amount is reasonably estimable, or if an estimable loss has been incurred and it is probable that a

claim will be asserted Disclose other loss contingencies in the notes.

Internal Service Funds

Chapter 9 32

Critical Implications:

Duplicate reported expenses:

costs and revenues are reported twice within the same set of financial statements.

Transfer of depreciation to governmental funds

Detract from Objectivity of Financial Statements

Obscure Fund Balance Surpluses or Deficits:

surpluses/deficits can be transferred from general fund to the internal service fund.

ISF Accounting Procedures

Chapter 9 33

Terminating an Internal Service Fund

Transfer ISF's assets to another fund which will continue same activity

Terminate activity and distribute assets in-kind to another fund or funds

Convert ISF's assets to cash and distribute cash to another fund or funds

Chapter 9 34

Self-Insurance Governments elect to self-insure their risks Reduces portion of the premium Accounted for in either general fund or ISF. Insurance department acts as an independent insurance

company. Self insurance is no insurance: no transfer of risks to

outsider. It simply sets aside funds to provide for possible losses. Payments for self-insurance premiums:

Only portion of the premium is reported as expenditure—this amount is recognized as revenue in ISF.

Excess is treated as a nonreciprocal transfer.

Chapter 9 35

Proprietary funds (internal service and enterprise) are used to account for the business-type activities of a government

Accrual accounting is used for proprietary funds and the required financial statements are the same as those for a for-profit entity, except that GASB standards must be used where they apply

ISF are reported as governmental activities on the government-wide statements

Regulatory accounting terminology and principles are used by some government owned utilities.

END

Business –Type ActivitiesSummary

Chapter 9 36

Copyright © 2007 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that named in Section 117 of the United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.