Chapter 9 - Elsevierbooksite.elsevier.com/9780080982403/content/10_Redington... · CONTENTS PAGE...

13

CONTENTS PAGE MATERIAL SUMMARY Essential Topic: Redington Immunization Chapter 9 Mathematics of Finance: A Deterministic Approach by S. J. Garrett

Transcript of Chapter 9 - Elsevierbooksite.elsevier.com/9780080982403/content/10_Redington... · CONTENTS PAGE...

CONTENTS PAGE MATERIAL SUMMARY

Essential Topic: Redington ImmunizationChapter 9

Mathematics of Finance: A Deterministic Approachby S. J. Garrett

CONTENTS PAGE MATERIAL SUMMARY

CONTENTS PAGE

MATERIAL

MotivationSurplusImmunizationRedington immunizationVolatilityConvexityExample

SUMMARY

CONTENTS PAGE MATERIAL SUMMARY

MOTIVATION

I Actuaries are typically concerned with assets held to coverfuture liabilities.

I For example, a pension scheme holds assets to cover thefuture pension payments when they become due.

I It is therefore useful to consider the surplus which issimply defined as

value of assets− value of liabilities

CONTENTS PAGE MATERIAL SUMMARY

SURPLUS

I The surplus at a particular time can be defined in terms ofthe net present values of future cash flows arising from theassets and liabilities, NPVA and NPVL.

I In the simple case that the NPVs depend on the constituentcash flows discounted at a constant force of interest δ, wecan define the surplus to be

S(δ) = NPVA(δ)−NPVL(δ)

I We could equally have defined this in terms of a constantinterest rate, i, but using δ will make the mathematics morestraightforward to illustrate.

I Recall that for fixed interest rate quantities i = eδ − 1.I Of course the surplus is a function of more than just δ, but

here we focus on changes in the prevailing interest rateonly.

CONTENTS PAGE MATERIAL SUMMARY

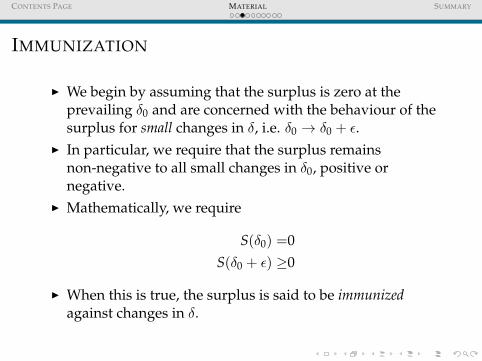

IMMUNIZATION

I We begin by assuming that the surplus is zero at theprevailing δ0 and are concerned with the behaviour of thesurplus for small changes in δ, i.e. δ0 → δ0 + ε.

I In particular, we require that the surplus remainsnon-negative to all small changes in δ0, positive ornegative.

I Mathematically, we require

S(δ0) =0S(δ0 + ε) ≥0

I When this is true, the surplus is said to be immunizedagainst changes in δ.

CONTENTS PAGE MATERIAL SUMMARY

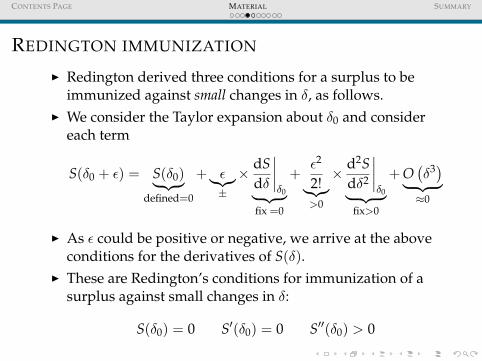

REDINGTON IMMUNIZATION

I Redington derived three conditions for a surplus to beimmunized against small changes in δ, as follows.

I We consider the Taylor expansion about δ0 and considereach term

S(δ0 + ε) = S(δ0)︸ ︷︷ ︸defined=0

+ ε︸︷︷︸±

× dSdδ

∣∣∣∣δ0︸ ︷︷ ︸

fix =0

+ε2

2!︸︷︷︸>0

× d2Sdδ2

∣∣∣∣δ0︸ ︷︷ ︸

fix>0

+O(δ3)︸ ︷︷ ︸≈0

I As ε could be positive or negative, we arrive at the aboveconditions for the derivatives of S(δ).

I These are Redington’s conditions for immunization of asurplus against small changes in δ:

S(δ0) = 0 S′(δ0) = 0 S′′(δ0) > 0

CONTENTS PAGE MATERIAL SUMMARY

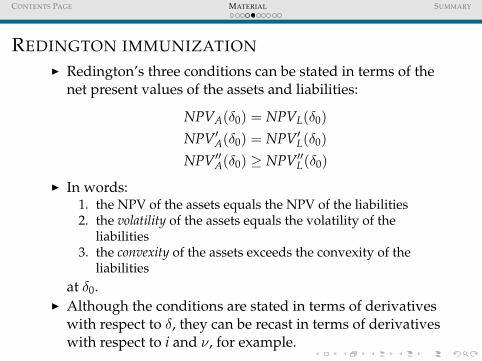

REDINGTON IMMUNIZATIONI Redington’s three conditions can be stated in terms of the

net present values of the assets and liabilities:

NPVA(δ0) = NPVL(δ0)

NPV′A(δ0) = NPV′L(δ0)

NPV′′A(δ0) ≥ NPV′′L(δ0)

I In words:1. the NPV of the assets equals the NPV of the liabilities2. the volatility of the assets equals the volatility of the

liabilities3. the convexity of the assets exceeds the convexity of the

liabilitiesat δ0.

I Although the conditions are stated in terms of derivativeswith respect to δ, they can be recast in terms of derivativeswith respect to i and ν, for example.

CONTENTS PAGE MATERIAL SUMMARY

VOLATILITY

I The volatility of a cash flow gives the proportionate changein the net present value to changes in δ.

I It is defined mathematically as

T(δ0) = −NPV′(δ0)

NPV(δ0)=

∑tcte−δt +

∫∞0 tρ(t)e−δtdt∑

cte−δt +∫∞

0 ρ(t)e−δtdt

∣∣∣∣δ0

I The right-hand expression shows that the volatility is alsothe weighted average term of the cash flow.

I The volatility is therefore also known as the discountedmean term, Macauley duration or simply duration.

I T is a measure of the sensitivity of the NPV to changes in δ.The sensitivity to changes in i can be derived as

− 1NPV

dNPVdi

∣∣∣∣i0=

(− 1

NPVdNPV

dδ× dδ

di

) ∣∣∣∣i0=

T(i0)1 + i0

CONTENTS PAGE MATERIAL SUMMARY

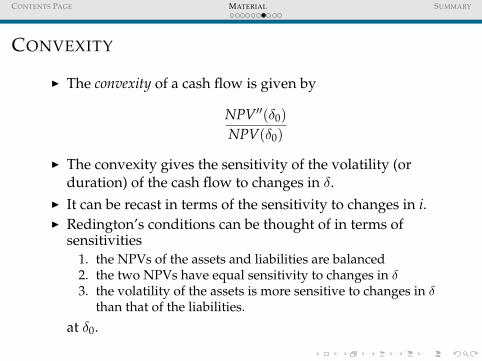

CONVEXITY

I The convexity of a cash flow is given by

NPV′′(δ0)

NPV(δ0)

I The convexity gives the sensitivity of the volatility (orduration) of the cash flow to changes in δ.

I It can be recast in terms of the sensitivity to changes in i.I Redington’s conditions can be thought of in terms of

sensitivities1. the NPVs of the assets and liabilities are balanced2. the two NPVs have equal sensitivity to changes in δ3. the volatility of the assets is more sensitive to changes in δ

than that of the liabilities.

at δ0.

CONTENTS PAGE MATERIAL SUMMARY

EXAMPLE

An investor has liabilities of £1m and £2m due at times t = 4and 5, respectively. He currently holds assets X and Y. If eachunit of X produces an income of £1m at t = 4 and each unit of Yproduces £1m at t = 8, construct a portfolio consisting of theliabilities and amounts of X and Y that is immune to smallchanges in interest rate at i = 5% per annum.

Answer

We require holdings x and y such that Redington’s conditionshold at i = 5%. We choose to work in terms of δ and theconditions are stated as

1. 1e−4δ + 2e−5δ = xe−4δ + ye−8δ

2. −4e−4δ − 10e−5δ = −4xe−4δ − 8ye−8δ

3. 16e−4δ + 50e−5δ < 16xe−4δ + 64ye−8δ

CONTENTS PAGE MATERIAL SUMMARY

EXAMPLE

Conditions 1. and 2. form simultaneous equations thatdetermine x and y. This are stated as

1. 2.3898 = 0.8227x + 0.6768y2. 11.1261 = 3.2908x + 5.4147y

and are solved with x = 2.4287 and y = 0.5787. We can easilycheck that these values satisfy condition 3.

3. 52.3395 < 58.0388

A portfolio consisting of the liabilities and £2.4287m of asset Xand £0.5787m of asset Y has zero NPV at i = 5% and isimmunized against small changes in i and δ.

CONTENTS PAGE MATERIAL SUMMARY

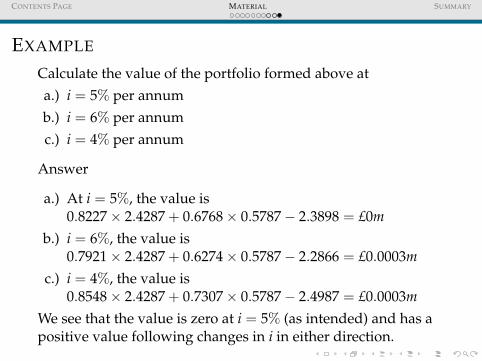

EXAMPLE

Calculate the value of the portfolio formed above ata.) i = 5% per annumb.) i = 6% per annumc.) i = 4% per annum

Answer

a.) At i = 5%, the value is0.8227× 2.4287 + 0.6768× 0.5787− 2.3898 = £0m

b.) i = 6%, the value is0.7921× 2.4287 + 0.6274× 0.5787− 2.2866 = £0.0003m

c.) i = 4%, the value is0.8548× 2.4287 + 0.7307× 0.5787− 2.4987 = £0.0003m

We see that the value is zero at i = 5% (as intended) and has apositive value following changes in i in either direction.

CONTENTS PAGE MATERIAL SUMMARY

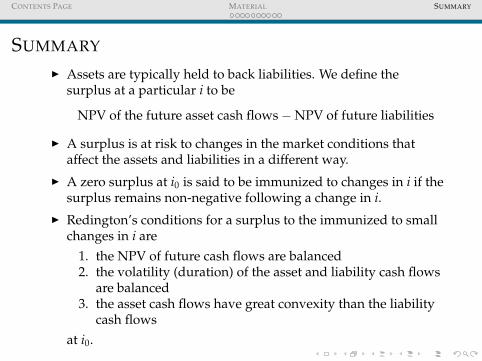

SUMMARY

I Assets are typically held to back liabilities. We define thesurplus at a particular i to be

NPV of the future asset cash flows−NPV of future liabilities

I A surplus is at risk to changes in the market conditions thataffect the assets and liabilities in a different way.

I A zero surplus at i0 is said to be immunized to changes in i if thesurplus remains non-negative following a change in i.

I Redington’s conditions for a surplus to the immunized to smallchanges in i are

1. the NPV of future cash flows are balanced2. the volatility (duration) of the asset and liability cash flows

are balanced3. the asset cash flows have great convexity than the liability

cash flowsat i0.