Chapter 9

24

Chapter 9 Journalizing Purchases and Cash Payments

-

Upload

charissa-harmon -

Category

Documents

-

view

29 -

download

0

description

Chapter 9. Journalizing Purchases and Cash Payments. Merchandising Business. Retail and Wholesale Merchandising Businesses. Special Journal. Because things are more confusing to a corporation we have to spread things out to make it easier to understand. - PowerPoint PPT Presentation

Transcript of Chapter 9

Chapter 9

Journalizing Purchases and Cash Payments

Merchandising Business

• Retail and Wholesale Merchandising Businesses

Special Journal

• Because things are more confusing to a corporation we have to spread things out to make it easier to understand.

• We use 5 separate journals to help record– Purchases– Cash Payments– Sales – Cash Receipts

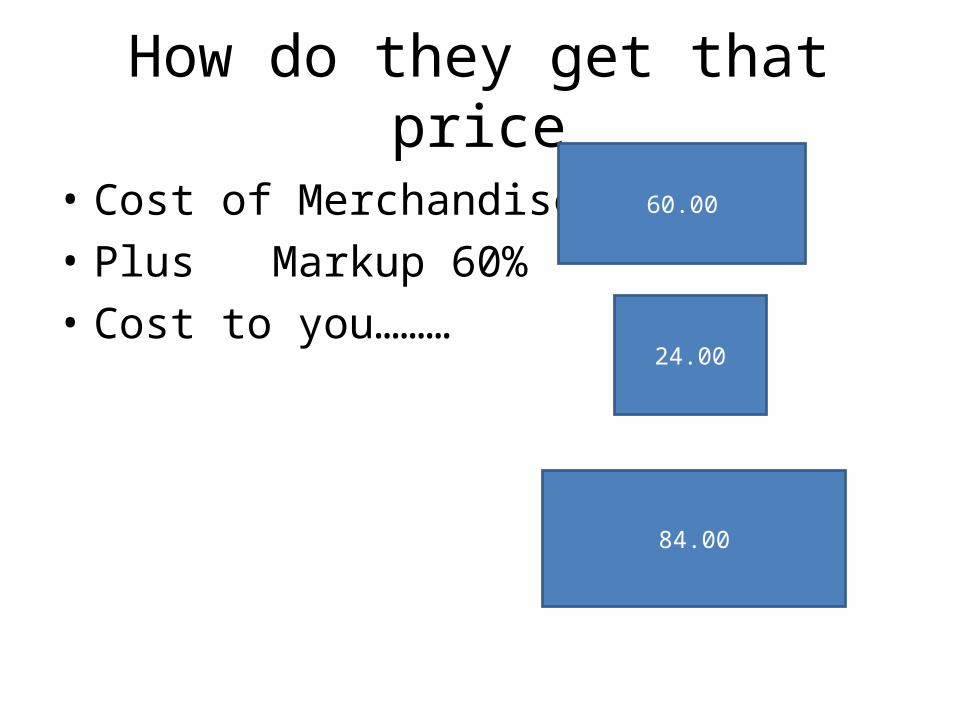

How do they get that price

• Cost of Merchandise• Plus Markup 60%• Cost to you………

60.00

24.00

84.00

Purchases Journal

Date Account Credited Purch No. Post Ref

Purch Dr. Accts

Pay Cr

Special amount columns

Purchased merchandise on account from Pro golf company $7254.00. Purchase Invoice No.

179Purchases Journal

Date Account Credited Purch No. Post Ref

Purch Dr. Accts

Pay Cr

2-Mar Pro Golf Company 179 7254

Please work on Aplia “On your Own”

Journalizing Cash Payments Using Cash Payments Journal

Section 9-2

Terms you need to know

• Cash Payment Journal– Whenever cash is paid

• Cash Discount – A deduction from the original amount when cash

is paid also called Purchase Discount

Paid Cash for Advertising $150.00 Check 292

Cash Payments Journal

Date Account Title

General

Accounts Payable

DebitPurchase Discount

Cash CreditCk No. Post Ref Debit Credit

Nov 2 Advertising Expense 292 15.00 15.00

Paid Cash for office supplies $94.00 Check No. 293

Cash Payments Journal

Date Account Title

General

Accounts Payable

DebitPurchase Discount

Cash CreditCk No. Post Ref Debit Credit

Nov 2 Advertising Expense 292 15.00 15.00

Nov 5 Supplies – Office 293 94.00 94.00

Purchasing Merchandise

• WHENEVER YOU SEE THE WORD MERCHANDISE!!!!!! You will use the Purchase account in some fashion.

What happens when we get a discount?

• A discount is a reduction in price because of a agreement in contract.– Trade discount

• Used when we purchase different amounts– 10 for $20– 20 for $10

– Trade discounts – $1500 x 60% = $900.00– 1500 – 900 = $600

Nov. 7. Purchased merchandise for cash, $600.00. Check No. 301

Cash Payments Journal

Date Account Title

General

Accounts Payable

DebitPurchase Discount

Cash CreditCk No. Post Ref Debit Credit

Nov 2 Advertising Expense 292 15.00 15.00

Nov 5 Supplies – Office 293 94.00 94.00

Nov 7 Purchases 301 600.00 600.00

Purchase Discount

• Purchase discount is a contra- account– An account that reduces a related account on a

financial statement.– Can you name any others

Nov 8. Paid cash on account to Gulf Craft Supply $488.04, covering Purchase invoice No. 82 for

$498.00, less 2% discount, $9.96 Check No. 302Cash Payments Journal

Date Account Title

GeneralAccounts Payable

DebitPurchase Discount

Cash CreditCk No.

Post Ref Debit Credit

Nov 2 Advertising Expense 292 15.00 15.00

Nov 5 Supplies – Office 293 94.00 94.00

Nov 7 Purchases 301 600.00 600.00

Nov 8 Gulf Craft Supply 302 498.00 9.96 488.04

Paid cash on account NO DISCOUNTPaid cash on account to American Paint $2,650

covering Purchase No. 77 Check No. 303Cash Payments Journal

Date Account Title

GeneralAccounts Payable

DebitPurchase Discount

Cash CreditCk No.

Post Ref Debit Credit

Nov 2 Advertising Expense 292 15.00 15.00

Nov 5 Supplies – Office 293 94.00 94.00

Nov 7 Purchases 301 600.00 600.00

Nov 8 Gulf Craft Supply 302 498.00 9.96 488.04

Nov 13 American Paint 303 2650.00 2650.00

Performing Additional Cash Payments Journal Operations

9-3

PETTY CASH FUND REPORTPETTY CASH REPORT

DATE:______________________ CUSTODIAN_____________

EXPLANATION RECONCILIATIONREPLENISH

AMOUNT

FUND TOTAL 250

PAYMENTS

SUPPLIES 45.34

ADVERTISING 25

MISCELLANEOUS 144.22

LESS: TOTAL PAYMENTS 214.56 214.56

EQUALSRECORDED AMOUNT ON HAND 35.44

LESS: ACTUAL AMOUNT ON HAND 33.85 EQUALS CASH SHORT OR OVER 1.59 1.59

216.15

JOURNALIZING THE PETTY CASH REPORT

SUPPLIES 45.34

ADVERTISING 25

MISCELLANEOUS 144.22

LESS: TOTAL PAYMENTS 214.56EQUALS RECORDED AMOUNT ON HAND 35.44LESS: ACTUAL AMOUNT ON HAND 33.85EQUALS CASH SHORT OR OVER 1.59

Cash Payments Journal

Date Account Title General Accounts

Payable Debit

PURCHASE DISCOUNT

CREDITCash CreditCk No.

Post Ref Debit Credit

NOV 18 SUPPLIES OFFICE 45.34 216.15

Advertising expense 25.00

Miscellaneous expense 144.22

cash short and over 1.59

November 18 Paid cash to replenish the petty cash fund$208: office supplies #32.33, advertising , $50.00; miscellaneous, $128.50, cash short 1.59 check no 310

Section 4Journalizing other transaction s using a general journal

• When a transaction does not fit – i.e. When we buy supplies on account or when

we buy something don’t like it and return it. It doesn’t fit the criteria of the last two journals

– Purchases and cash payments so it must go into the General Journal.

November 6. Bought supplies on account from Gulf Craft Supply, $210.00. Memorandum No. 52.

General Journal

Date Account Title Doc. NoPost Ref. Debit Credit

Nov 6 Supplies – Store M52 210

Accts Pay/Gulf Craft Supply

• Purchase Return and Allowance – Contra Account to Purchases

Purchase Return and allowanceNovember 28. Returned merchandise to Crown Distributing, $252.0, covering Purchase Invoice

No. 80General Journal

Date Account TitleDoc. No

Post Ref. Debit Credit

Nov 28 Accounts Pay/Crown Distributors DM78 252.00

Purchase Return and Allowance 252.00