Chapter 8. Managerial accounting

39

Chapter 8. Managerial accounting MSc. Nguyen T Thuc Hien

Transcript of Chapter 8. Managerial accounting

Chapter 8. Managerial accounting

MSc. Nguyen T Thuc Hien

TABLE OF CONTENTS

DEFINITION OF MANAGERIAL ACCOUNTING

WHAT DO MANAGEMENT ACCOUNTANTS DO?

TALKING ABOUT MANAGERIAL ACCOUNTING

01

03

02

1. DEFINITION OF MANAGERIAL ACCOUNTING

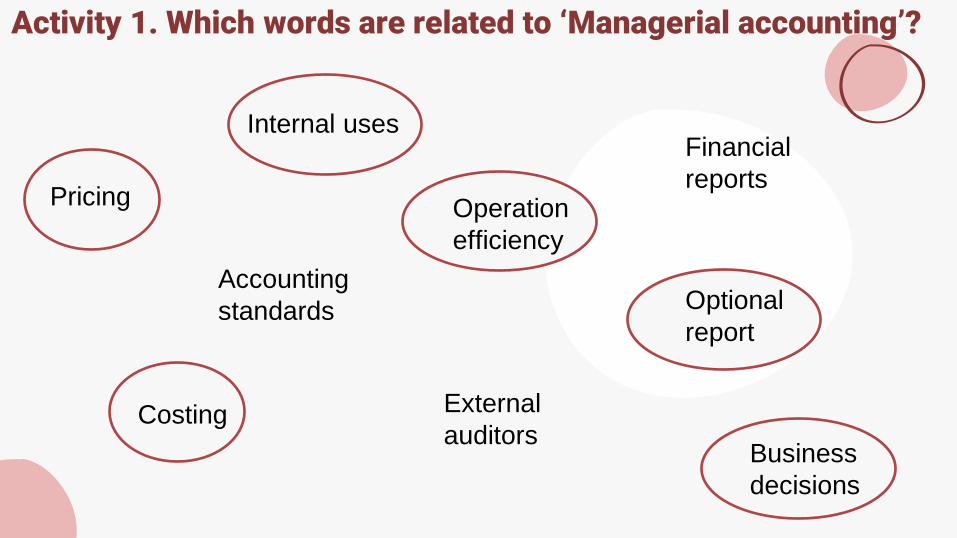

Activity 1. Which words are related to ‘Managerial accounting’?

Internal uses

Accounting

standards

Operation

efficiency

Optional

report

External

auditors

Financial

reports

Costing

Business

decisions

Pricing

Internal uses

Accounting

standards

Operation

efficiency

Optional

report

External

auditors

Financial

reports

Costing

Business

decisions

Pricing

Activity 1. Which words are related to ‘Managerial accounting’?

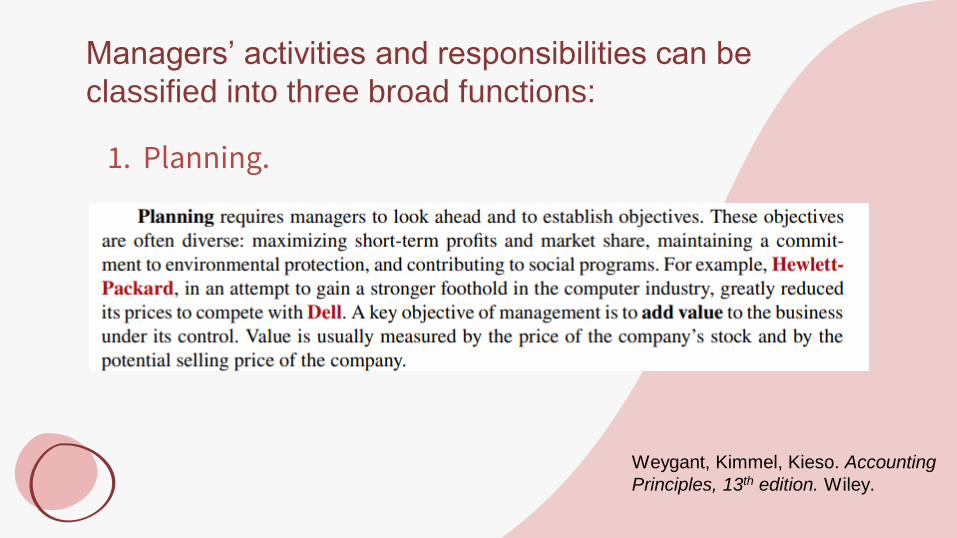

1. Planning.

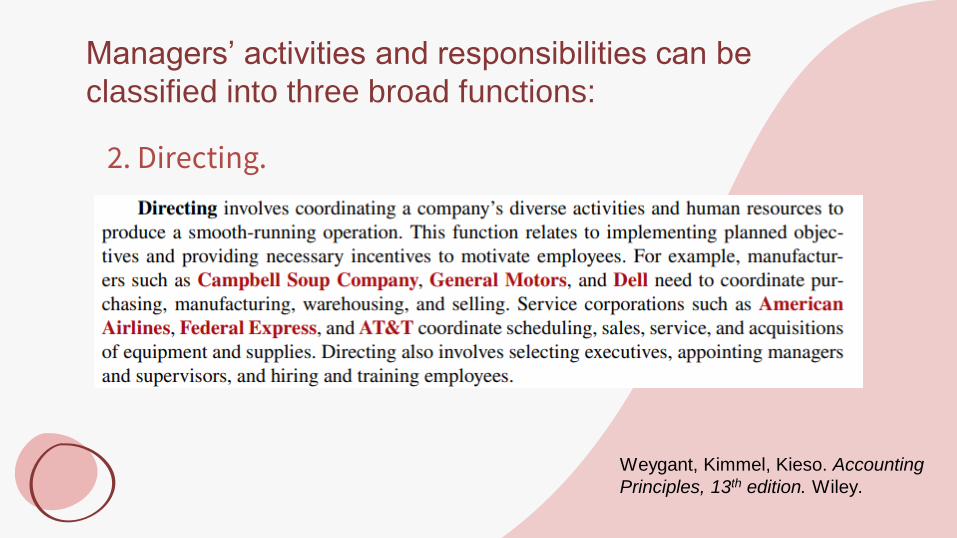

1. Directing.

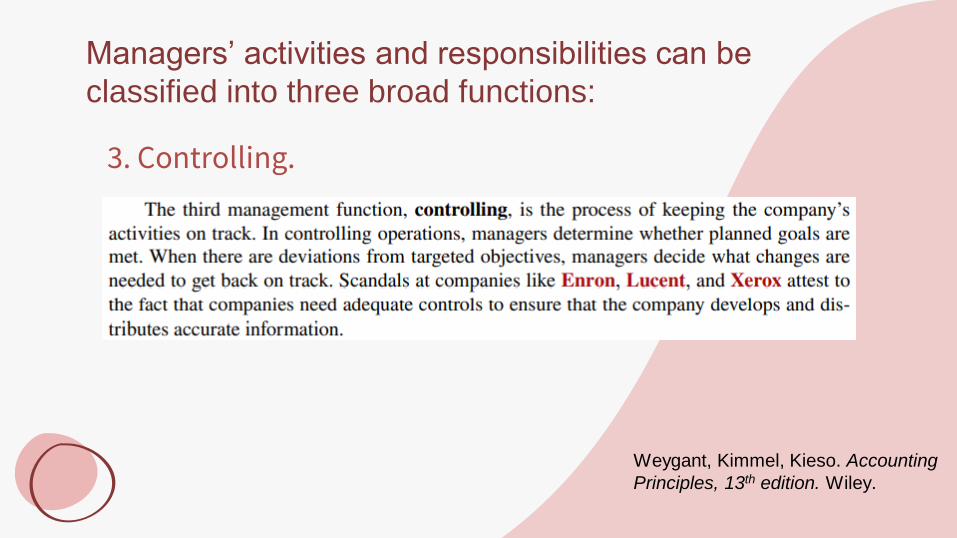

2. Controlling.

Managers’ activities and responsibilities can be

classified into three broad functions:

Weygant, Kimmel, Kieso. Accounting

Principles, 13th edition. Wiley.

2. Directing.

Managers’ activities and responsibilities can be

classified into three broad functions:

Weygant, Kimmel, Kieso. Accounting

Principles, 13th edition. Wiley.

3. Controlling.

Managers’ activities and responsibilities can be

classified into three broad functions:

Weygant, Kimmel, Kieso. Accounting

Principles, 13th edition. Wiley.

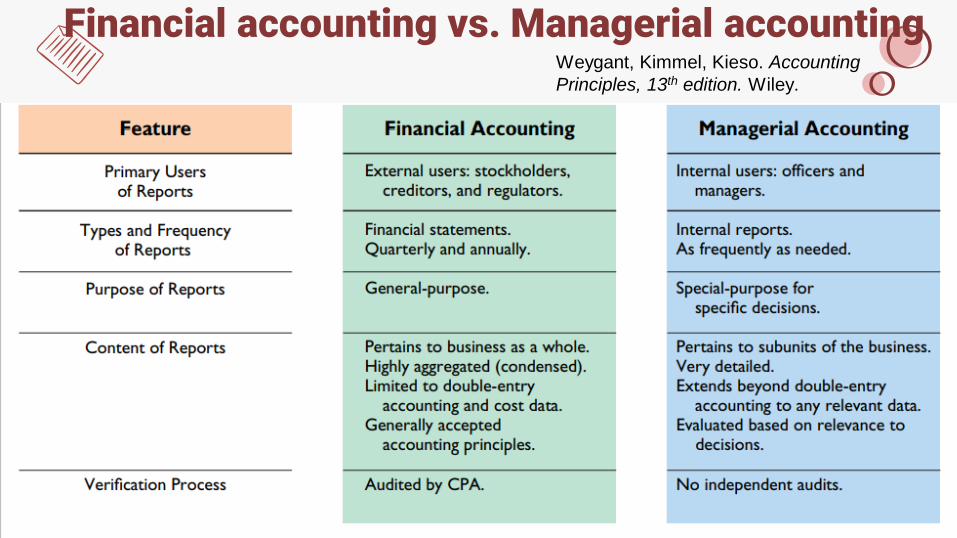

Financial accounting vs. Managerial accountingWeygant, Kimmel, Kieso. Accounting

Principles, 13th edition. Wiley.

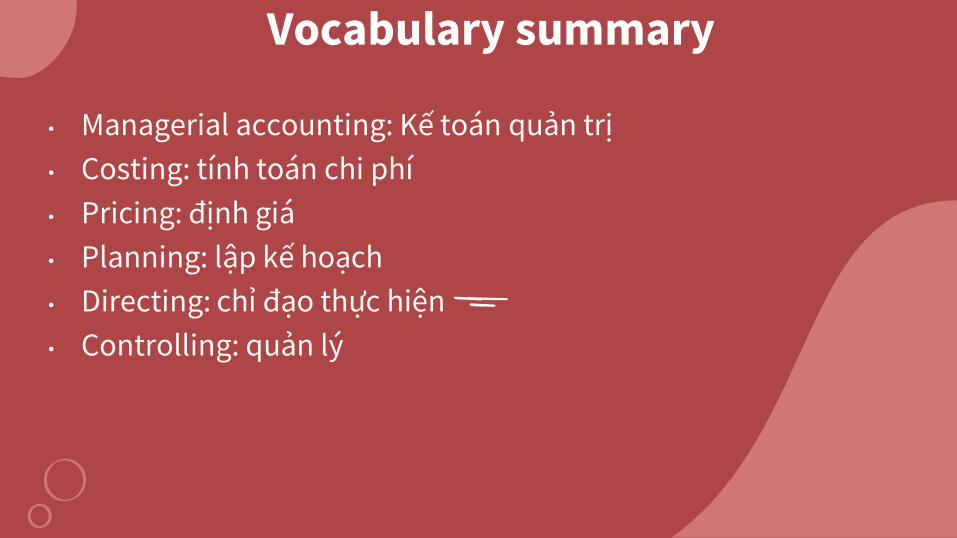

Vocabulary summary

• Managerial accounting: Kế toán quản trị

• Costing: tính toán chi phí

• Pricing: định giá

• Planning: lập kế hoạch

• Directing: chỉ đạo thực hiện

• Controlling: quản lý

2. WHAT DO MANAGEMENT ACCOUNTANTS DO?

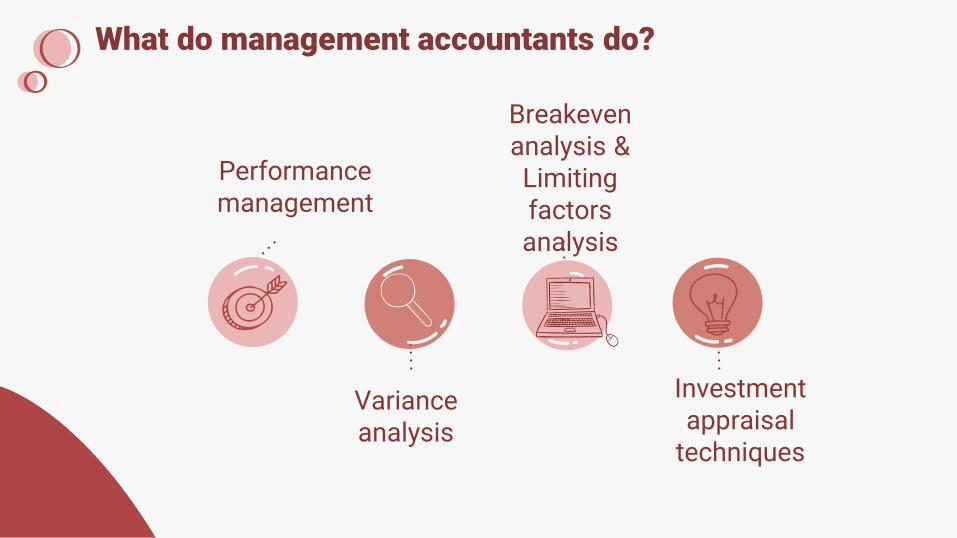

What do management accountants do?

Calculating unit costs

Budgeting

Pricing calculations

Working capital

What do management accountants do?

Performance management

Breakeven analysis & Limiting factors analysis

Variance analysis

Investment appraisal

techniques

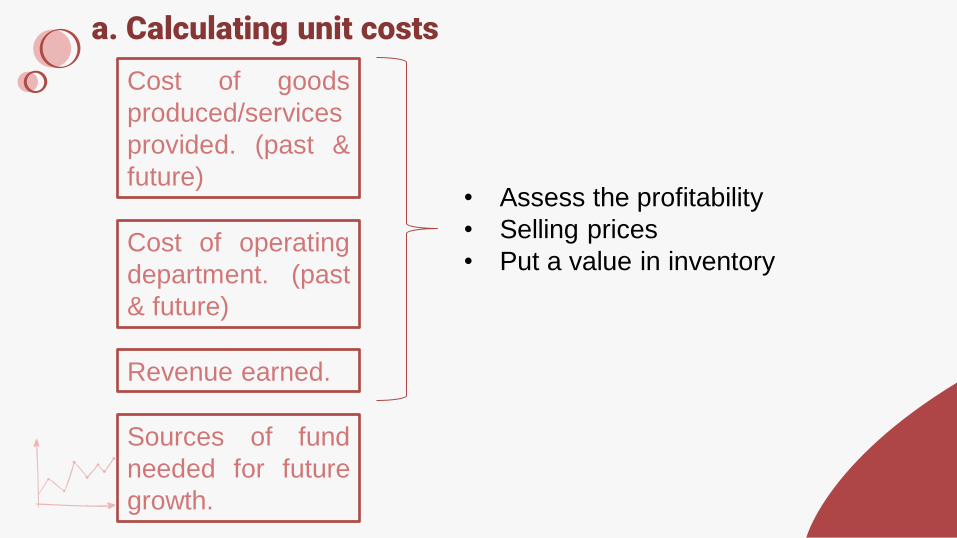

a. Calculating unit costs

Cost of goods

produced/services

provided. (past &

future)

Cost of operating

department. (past

& future)

Revenue earned.

• Assess the profitability

• Selling prices

• Put a value in inventory

Sources of fund

needed for future

growth.

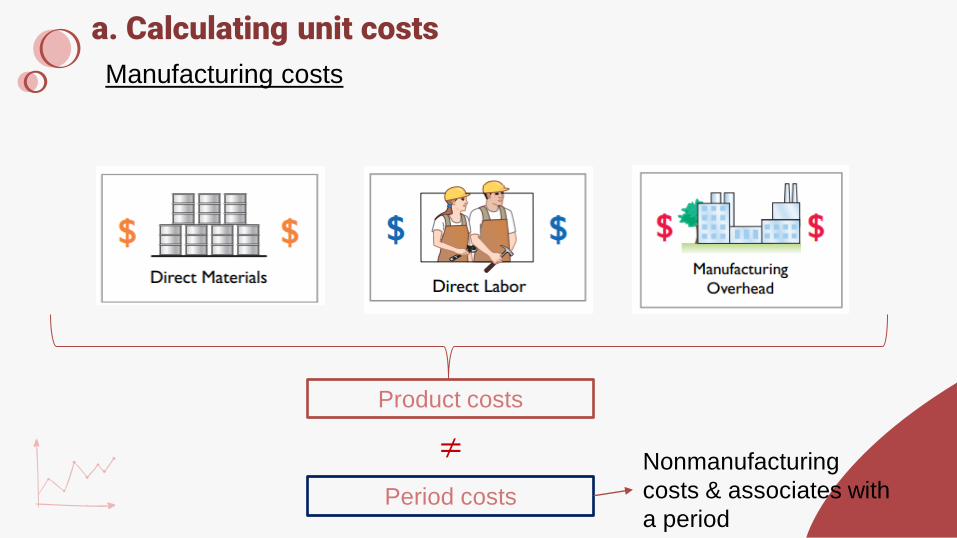

a. Calculating unit costs

Manufacturing costs

Product costs

Period costs

≠Nonmanufacturing

costs & associates with

a period

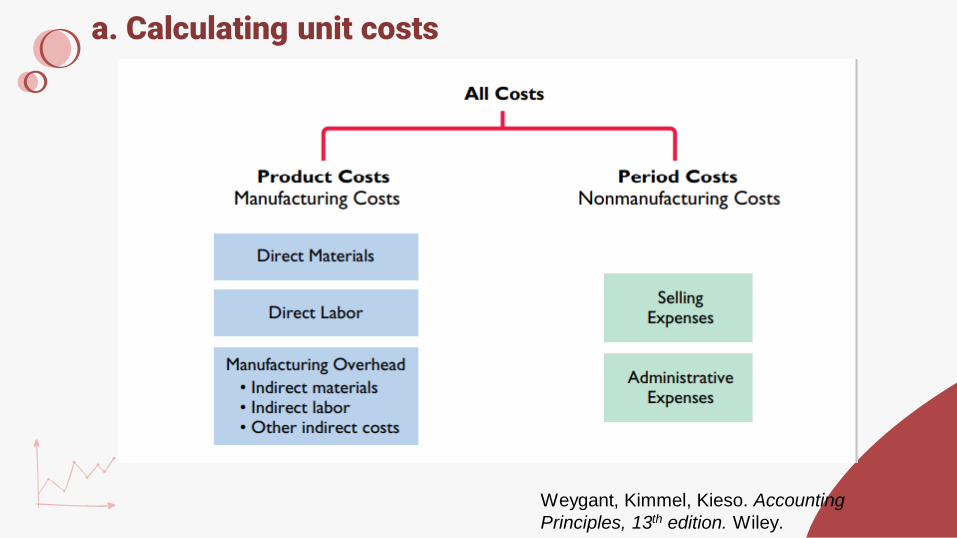

a. Calculating unit costs

Weygant, Kimmel, Kieso. Accounting

Principles, 13th edition. Wiley.

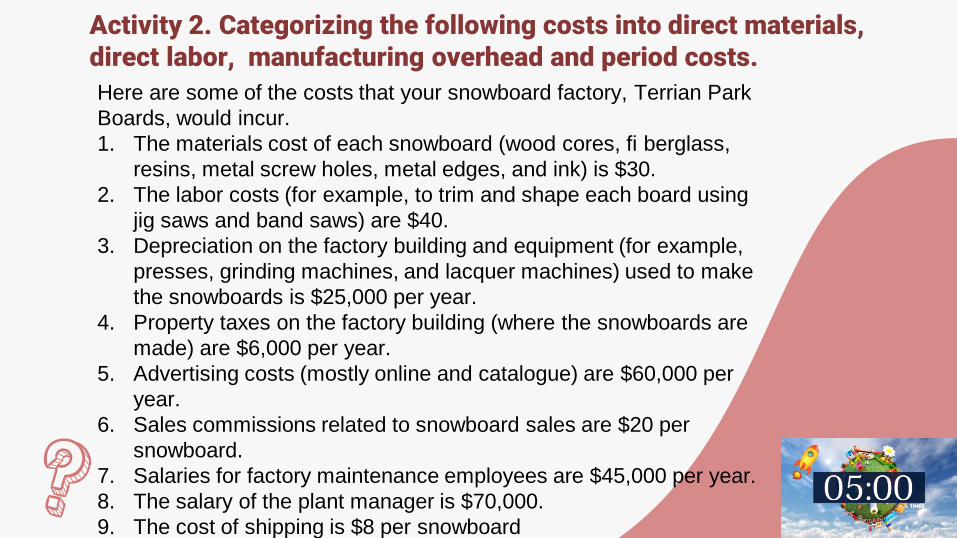

Activity 2. Categorizing the following costs into direct materials, direct labor, manufacturing overhead and period costs.

Here are some of the costs that your snowboard factory, Terrian Park

Boards, would incur.

1. The materials cost of each snowboard (wood cores, fi berglass,

resins, metal screw holes, metal edges, and ink) is $30.

2. The labor costs (for example, to trim and shape each board using

jig saws and band saws) are $40.

3. Depreciation on the factory building and equipment (for example,

presses, grinding machines, and lacquer machines) used to make

the snowboards is $25,000 per year.

4. Property taxes on the factory building (where the snowboards are

made) are $6,000 per year.

5. Advertising costs (mostly online and catalogue) are $60,000 per

year.

6. Sales commissions related to snowboard sales are $20 per

snowboard.

7. Salaries for factory maintenance employees are $45,000 per year.

8. The salary of the plant manager is $70,000.

9. The cost of shipping is $8 per snowboard

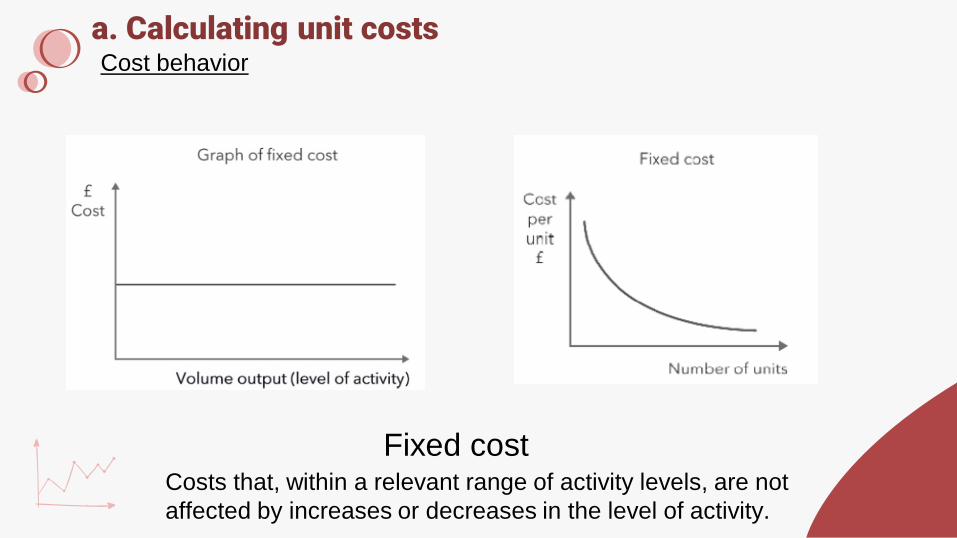

a. Calculating unit costs Cost behavior

Fixed costCosts that, within a relevant range of activity levels, are not

affected by increases or decreases in the level of activity.

a. Calculating unit costs Cost behavior

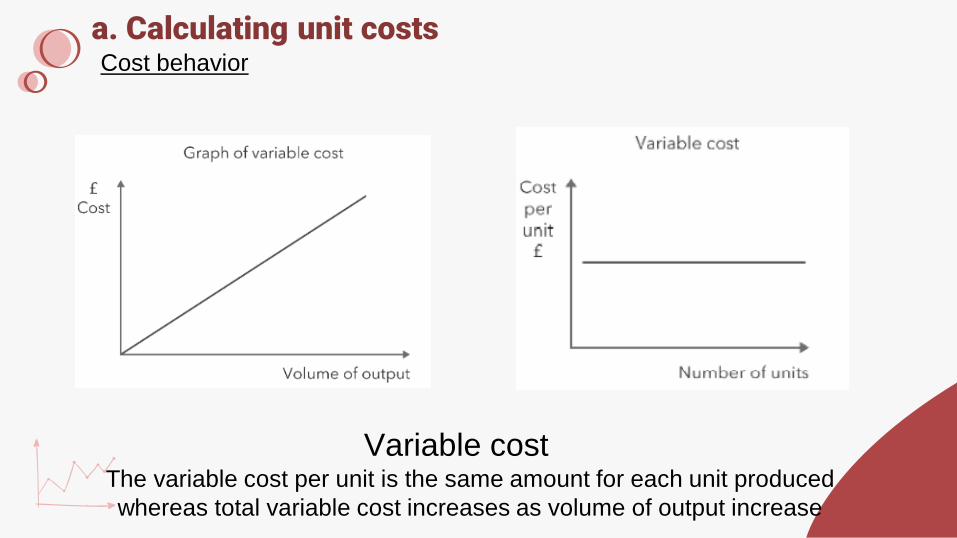

Variable costThe variable cost per unit is the same amount for each unit produced

whereas total variable cost increases as volume of output increase

a. Calculating unit costs Cost behavior

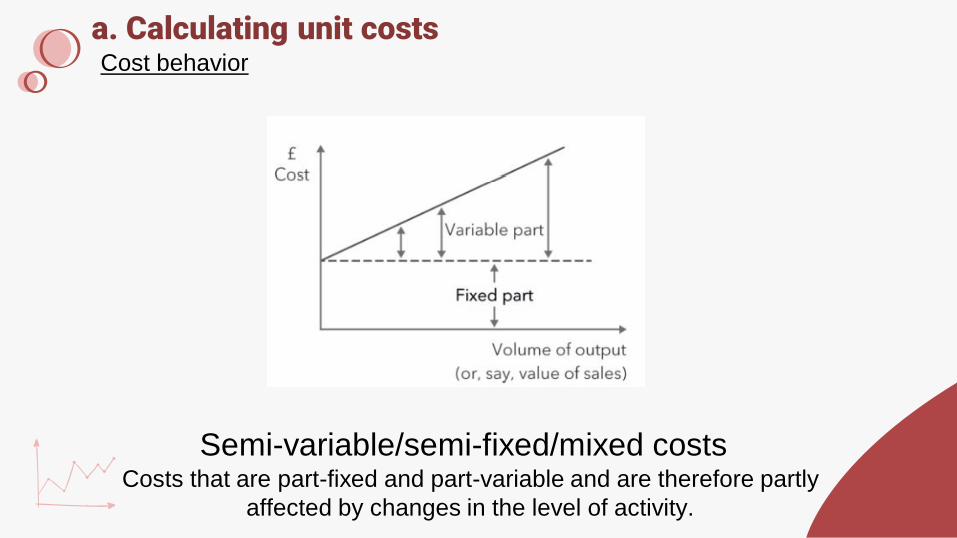

Semi-variable/semi-fixed/mixed costsCosts that are part-fixed and part-variable and are therefore partly

affected by changes in the level of activity.

a. Calculating unit costs

• Product costs: chi phí sản xuất sản phẩm

• Direct labor costs: chi phí nhân công trực tiếp

• Direct material costs: chi phí nguyên vật liệu trực tiếp

• Manufacturing overhead costs: chi phí phân bổ

• Period costs: chi phí trong kỳ

• Selling expenses: chi phí bán hàng

• Administrative expenses: chi phí quản lý

a. Calculating unit costs

• Fixed costs: chi phí cố định

• Variable costs: chi phí biến đổi

• Semi-fixed/semi-variable/mixed costs: chi phí hỗn hợp

• Total costs: chi phí tổng

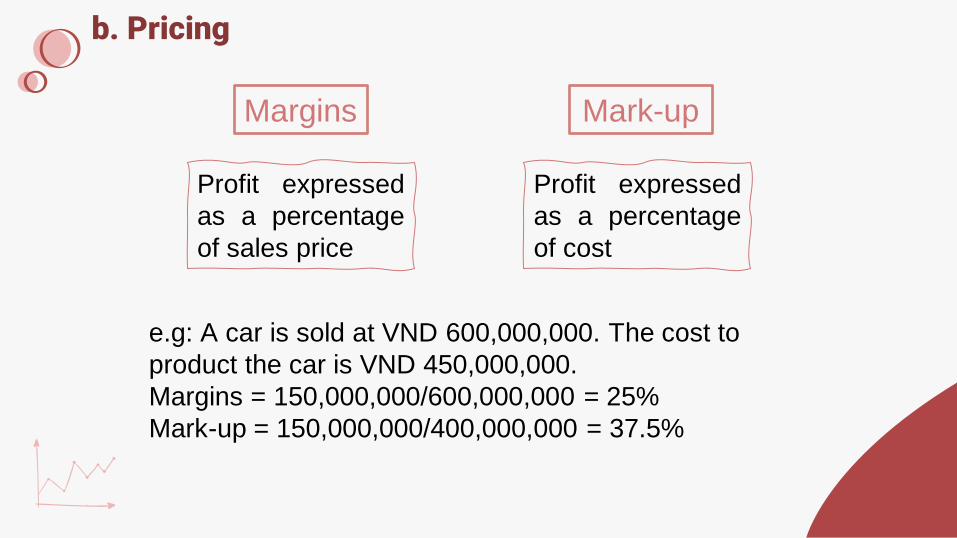

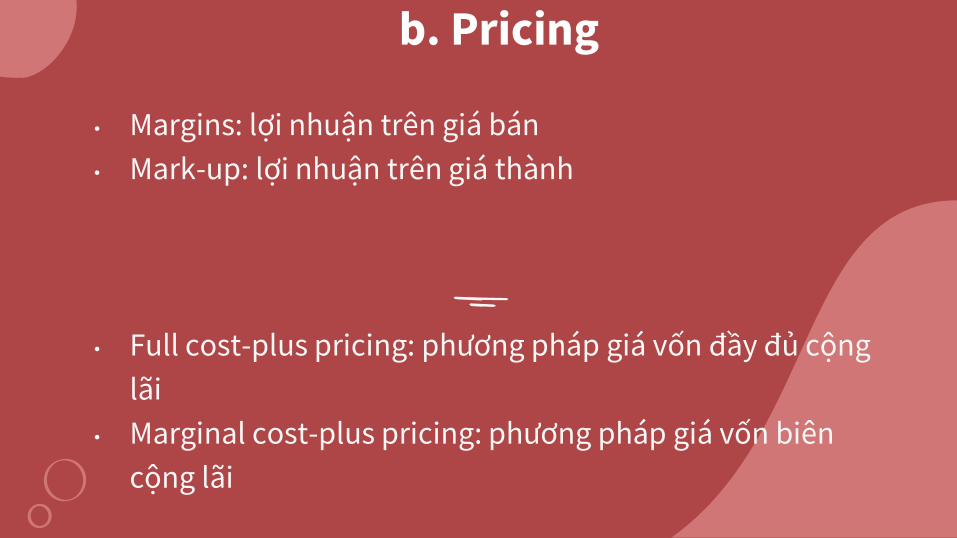

b. Pricing

Margins Mark-up

Profit expressed

as a percentage

of cost

Profit expressed

as a percentage

of sales price

e.g: A car is sold at VND 600,000,000. The cost to

product the car is VND 450,000,000.

Margins = 150,000,000/600,000,000 = 25%

Mark-up = 150,000,000/400,000,000 = 37.5%

b. Pricing

• Margins: lợi nhuận trên giá bán

• Mark-up: lợi nhuận trên giá thành

• Full cost-plus pricing: phương pháp giá vốn đầy đủ cộng

lãi

• Marginal cost-plus pricing: phương pháp giá vốn biên

cộng lãi

We only study the basic terms. Others must take more time and are investigated in management accounting module itself.

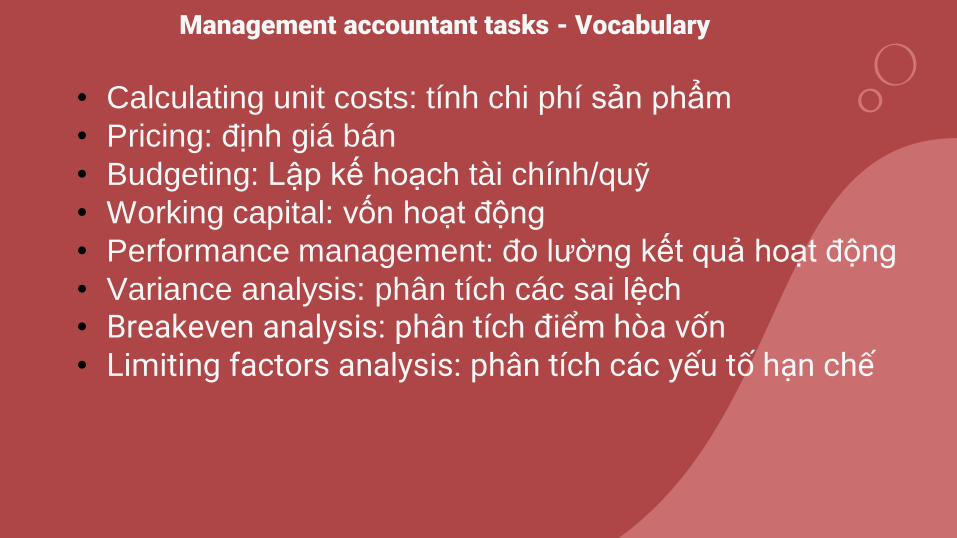

Management accountant tasks - Vocabulary

• Calculating unit costs: tính chi phí sản phẩm

• Pricing: định giá bán

• Budgeting: Lập kế hoạch tài chính/quỹ

• Working capital: vốn hoạt động

• Performance management: đo lường kết quả hoạt động

• Variance analysis: phân tích các sai lệch

• Breakeven analysis: phân tích điểm hòa vốn• Limiting factors analysis: phân tích các yếu tố hạn chế

TALKING ABOUT MANAGERIAL ACCOUNTING

3

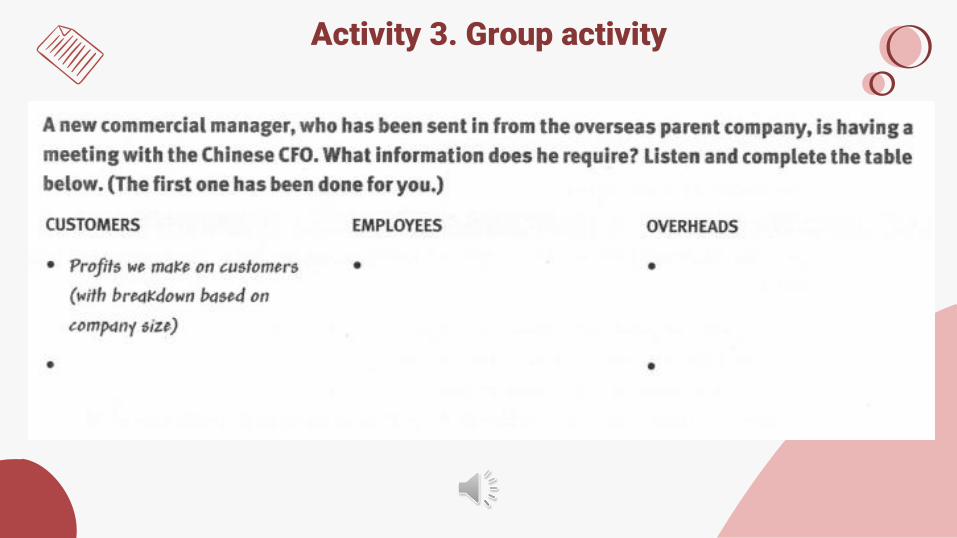

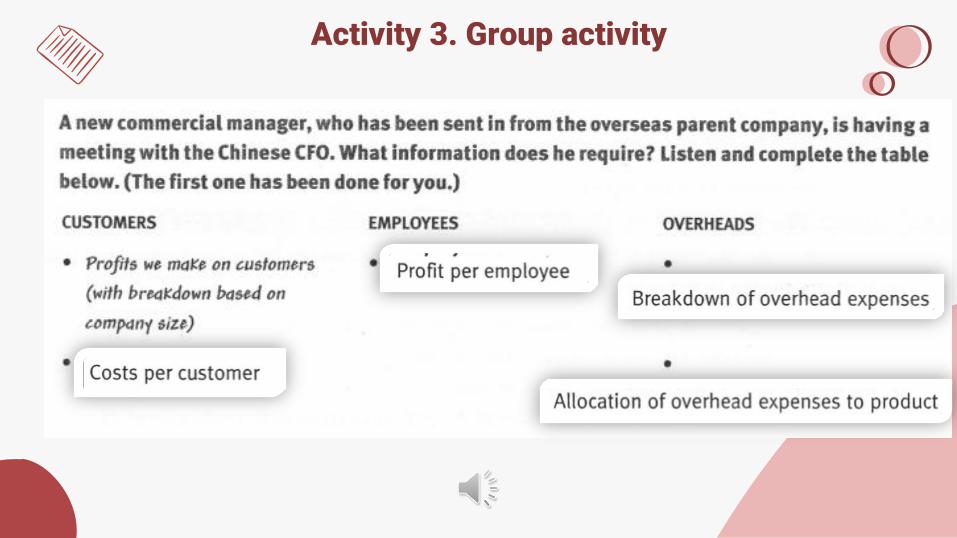

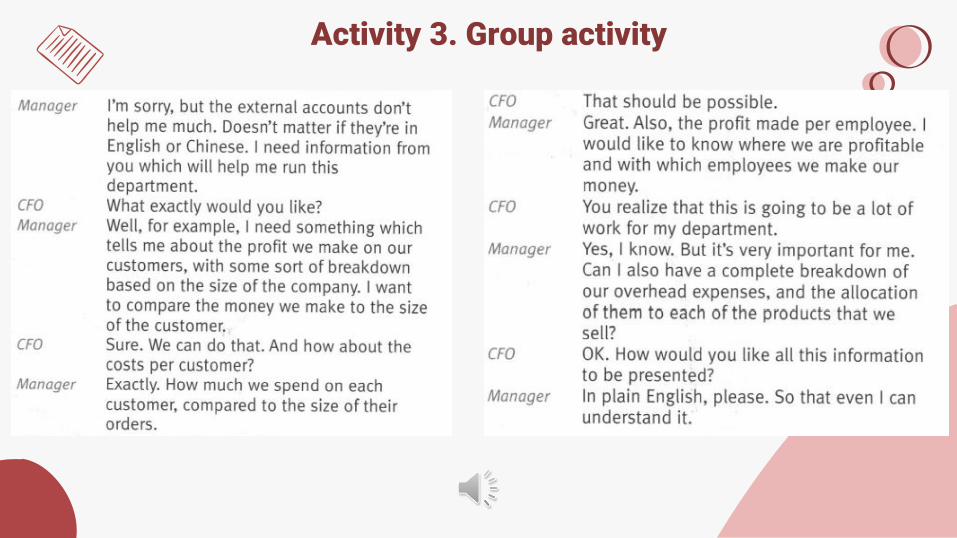

Activity 3. Group activity

Activity 3. Group activity

Activity 3. Group activity

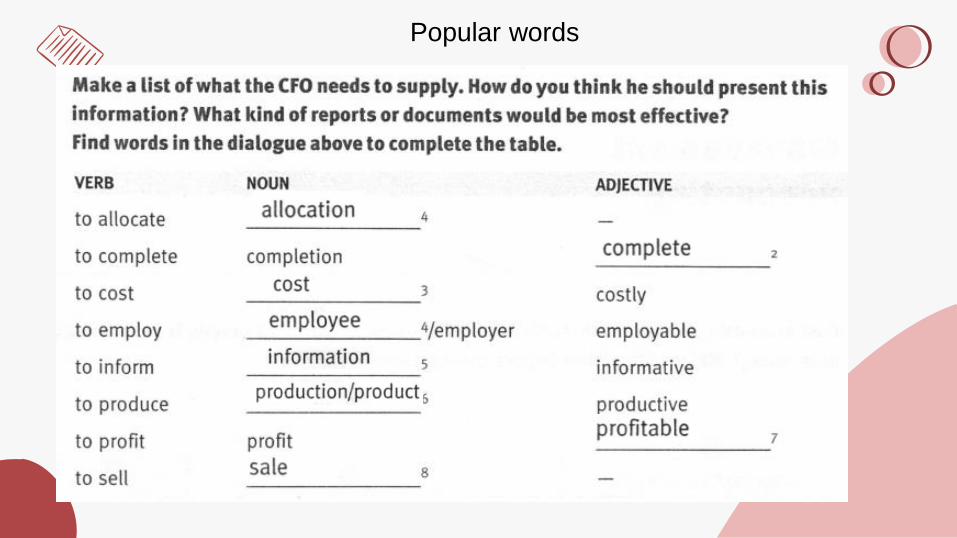

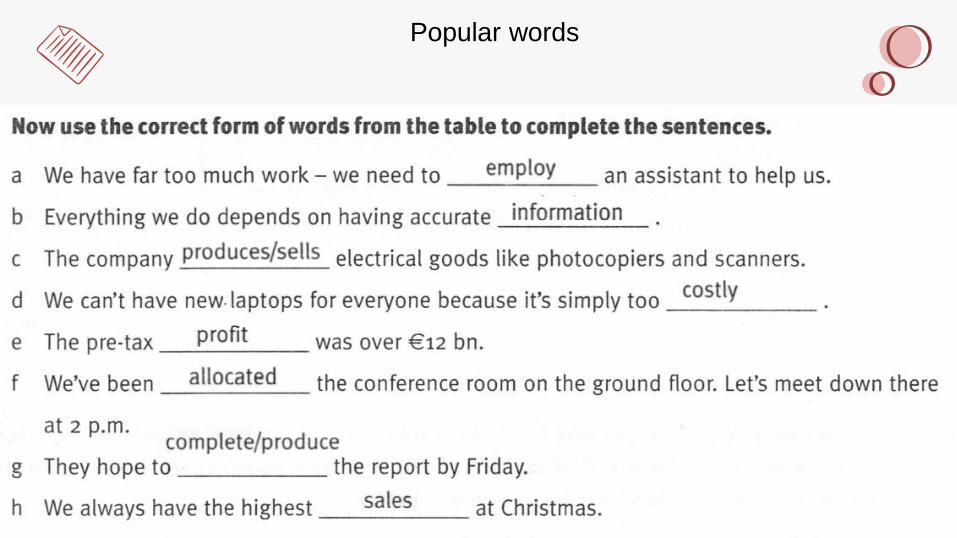

Popular words

Popular words

Activity 4. Group workRead the Statement of Cash Flows

and decide if the statement is true or false.

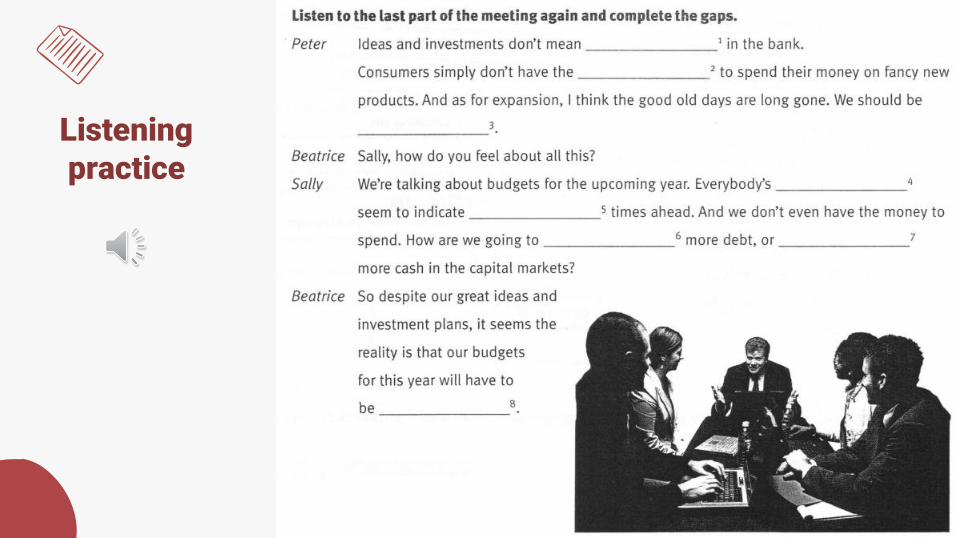

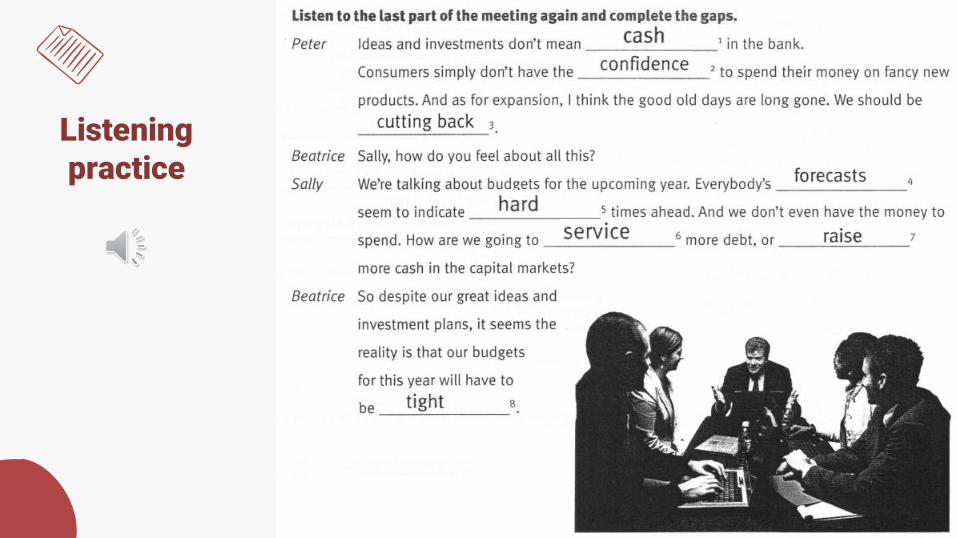

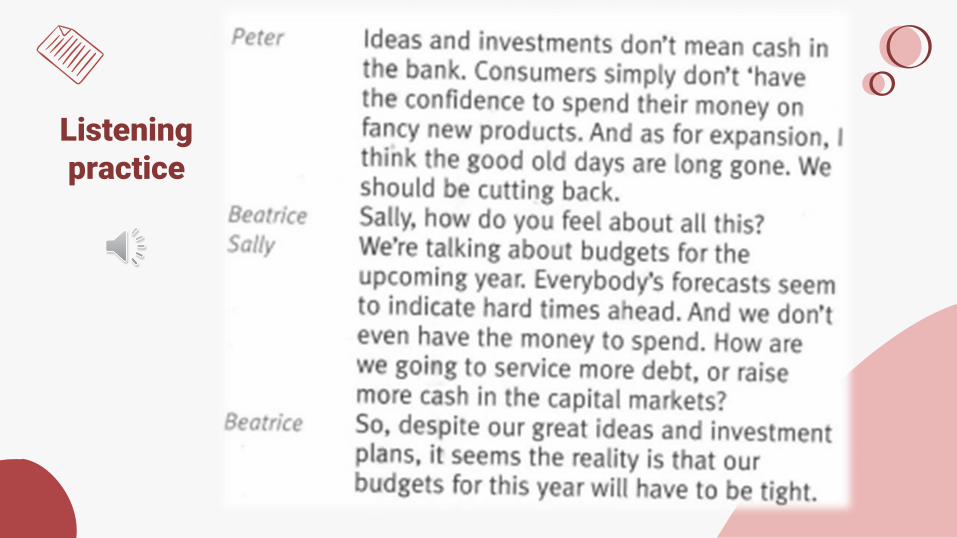

Listening practice

Listening practice

Listening practice

Have a nice day!