Chapter 8 - ITSP | Warringtonbear.warrington.ufl.edu/kraft/MLI26C653/docs/Chapter8.pdf · Chapter 8...

26

Chapter 8 Strategy in the Global Environment

Transcript of Chapter 8 - ITSP | Warringtonbear.warrington.ufl.edu/kraft/MLI26C653/docs/Chapter8.pdf · Chapter 8...

Chapter 8

Strategy in the Global Environment

(

STRATEGIC MANAGEMENT

lecture 8

Dr. John Kraft

CopyrlghlC Houghton MlIIlln ComPIIfIY.AlI rlghbmoMld.

National and Competitive Advantage

CopyrlghIQHoughtonMll!linCompany,Allrighb~.

The Global and National Environments

International expansion represents a way of earning greater returns by transferring the skills and product offerings derived from distinctive competencies to

3 1

3 3

markets where indigenous competitors lack these skills.

The trend toward globalization has many implications:

1. Industries are becoming global in scope Industry boundaries no longer stop at national borders.

2. Shift from national to global markets This has intensified competition in industry after industry.

3. Steady decline in barriers to cross-border trade and investment This has opened up many once protected markets to companies based outside of them.

CopyrighiO Houghton Mimin Company.A11 rlghb I'tI$OMd. 3 5

Opening Case

·:·Evolution of Strategy at Coca Cola

CcpyrlghlO HoughtonMimin Company.AlI rlght$ rcn.orvod. 3 2

Strategy in Action

·:·Finland's Nokia

NOKIA Connecting People

CopytIghtC Hcughlon MiII'Iin Company.AI! rl"hls ,~rvod. 3 4

Increasing Profitability Through Global Expansion

·:·Location economies • Economic benefits from performing a

value creation activity in the optimal location

• Effects - Can lower costs - Can enable differentiation

• Caveats - Transportation costs and trade barriers - Political and economic risks

Co;;;=Ho~~~:~~I;=;:~~ ;;;=~. 316

1

Increasing profitabil1i% Through Global Expansion cont'd)

.:. The experience curve • Serving a global market from one or a few plants is

consistent with moving down the experience curve and establishing a low-cost position

.:. Transferring distinctive competencies . Companies with distinctive competencies can realize large returns by expanding to global markets where competitors lack similar competencies and products

"'.U' tee. u IS'lIIf& awer 01O ..... 'K>""" ... 0

CopyrillhtC Houghton Mllllin Company.AlI rightstllS(lrvod. 3 7

Running Case

·:·Wal-mart in Global Expansion

WAL-MART' "ijiiiFi"f'"

CopyrightCl Houghton Mimln Company.All rights fG$Orvod. 3 9

Four Basic Strategies

LO~ <411F%'J£&Ti*l?t%t#&iI#i U Prtl#.uUIlIforIOC/llrnSDon'!YOnlltlll

o reo. II or& cwo on Ie CopytightC Houghlon MilI'Iln Company.AlI rights fC$Crvod. 3 11

Increasing profitabil~% Through Global Expansion cont'd)

.:. Leveraging the skills of global subsidiaries

· Competencies can be created anywhere within a multinational's global network of operations

· Managers must establish an incentive system to encourage local employees to acquire new competencies

· Managers must have processes in place to identify valuable new competencies and help transfer them within the company

OUICO, 0 <lWer am Ie

CopyrlghlC Houghton MiflUn Company,AI! rillhbmorvod.

Pressures for Cost Reductions and Local Responsiveness

"", ',,'. '.

".~

<(:j

rce. U ".' ...... r s owe rUIn I e CopyrightC Houghton Mlmln Company. All rights rcsorvcd.

Choosing a Global Strategy

Q) Standard Globalization Strategy

3 9

3 10

• Reaping the cost reductions that come from economies of scale and location economies

• Business model based on pursuing a low-cost strategy on a global scale Makes the most sense when there are strong pressures for cost reduction and the demand for local responsiveness is minimal

@ Localization Strategy · Customizing the company's goods or services so that

thy provide a good match to tastes and preferences in different national markets Most appropriate when there are substantial differences across nations with regard to consumer tastes and preferences and where cost pressures are not too intense

CopyrlllhtOHoUi/htonMimln CompDny.AU rlllhbTC$Orvod. 3 12

2

Strategy in Action

·!·Localization of IKEA

CopyrlghlC Houghton MlIfIln Comp4ny.AlI right:$rtI5OlVod. 3 13

Choosing a Global Strategy

® Transnational Strategy • Difficult to pursuedueto its conflicting demands • Business model that simultaneously:

» Achieves low costs » Differentiates across markets

( » Fosters a flow of skills between subsidiaries Building an organization capable of supporting a transnational strategy is a complex and challenging task.

® International Strategy • Multinational companies that sell products that serve

universal needs (minimal need to differentiate) and do not face significant competitors (low cost pressure). In most international companies the head office retains tight control over marketing and product strategy.

CopyrightC Hough!DnMimln Company.AIl rlghbNlSllrvod. 3 15

Film

.:. India

--CopyrightCHoughlDll Mimin Compllny,AI! rights ro:.olVOd. 3117

Closing Case

.!. MTV Networks

[f8"

CopyrighlC Houghton M!l!Iln Company.AIl rlghts~rvod.

Advantages/Disadvantages of Strategies for Competing Globally

SI".~" .. Intemftliol1ll

AdvIInbllllOS

.. TIfI1:1'trllfdiftil'lttTreCumpettnciuto !()Ie i!jl1tMnQtI

DiM .... lIIII!!"

"llItkcflce~\lu?~nsmnn! ·1n.bllrtyt:lf .. Iir.llIO~liQntttlt.cmlt:I

3,,4

.. Abl!r\'j til eU~11lm'.te Il'odlm ell.MtIi 1In.~ m.rbtiflglniectll~'ntev>·ithllltlli ~spOll~nnl

• ~lun:toelPlc/1o:ptrict.ell·ellfT~elleet:s ·lnIbnnyltllulltlloUl\I;meeOllomln .. h:l!ISfeIBCl.ql:aICli!"C'lknClI'cl,lrretllel:tS .. FellutC!ttltTan.s!"tfcliSlin:liYe{om~ehm'

ciutclurc1illfNlkel. - Al:ilir{lotJ!'lDitIlI!otlil!nta-e;II\-eelfetu - ud:rtIIlC!!'e3:j)l)n~n!u .AhilrtylnUf!luillrn:a!innl;lt~'J;

• Ahml'(lo #'Q"~tIit Cl.~IJcflU·t~t\1IIInlltUr • Dijficultitt:llll lwplcmunwtion b~ellu,~ cl • AhlIityUlh'r:lllillutAlinn.:~gll Ilro.,1lzftlio:alpmMIII', • O\l:i~:Y1!;1eustlll!l:l4ptaduct,,"anngsIiM

mll);tti~IIInOtt=rtllne~\I\olelIClt~1 ft'~~n~~n

.nuplnghneflUd\i!DballcJrnll\9

.;;.ource. uDlIsncr 5 OWDr om~. '-'00-.;;.11013 CopyrighiC Houghton Mimln COmpany.AI! rlghb losorvod.

Strategy in Action

·!·McDonald's Is Here, There, and Everywhere

CClpyrlghtC HOllghIDnMifIIln COmpany.Al! right:! rosorvod.

3,,6

3 16

3

Real World

.:. "The Jollibee Phenomenon- A Philippine Multinational"

CopyrlghtC Houghton MllIIJn Company. All righbRl$OtvOd.

Strategy in Action

·:·Evolution of Strategy at P&G

CopyrighlC HCIIlghlon Mlmln ComPllny.AlI rlghb rosarvod.

Basic Entry Decisions

·:·Which overseas markets to enter • Assessment of long-run profit potential

3 19

3121

» A function of the size of the market, purchasing power of consumers, the likely future purchasing power of consumers

• Balancing the benefits, costs, and risks associate with doing business in a country

» A function of economic development and political stability

OUfCCl. U I ers ower om " Copyright C Houghton MlI!lln Comp:InY. All rlghb fc:l(lrvod, 3123

Strategy in Action

·:·"Hewlett Packard in Singapore"

n v e n t

CopyrlghlC Houghton M!l!Iln Company. All rights rosoJVOd, 3 20

Basic Entry Decisions

1. Which overseas markets to enter · Assessment of long-run profit potential

» A function of the size of the market, purchasing power of consumers, the likely future purchasing power of consumers

· Balancing the benefits, costs, and risks associate with doing business in a country

» A function of economic development and political stability

2. Timing of entry · First-mover advantages: preempt and build share

· First-mover disadvantages: pioneering costs 3. Scale of Entry and Strategic Commitments

· Entering on a large scale is a major strategic commitment

» With long tenn impacts that may be difficult to reverse

· Benefits and drawbacks of small-scale entry CopyrightC Houghton Ml!!lln Compu;ny.AlI righb rosolVOd. 3122

Basic Entry Decisions (cont'd)

·:·Timing of entry • First-mover advantages • First-mover disadvantages

·:·Scale of entry and strategic commitments • Entering on a large scale is a strategic

commitment, both positive and negative • Benefits and drawbacks of small-scale entry

, . . n " CopyrightO HoUUhton MlI!1In Company. All righb fO$Gtvvd. 312.

4

The Choice of Entry Mode When and how to enter a new national market raise the question of how to determine the best mode or vehicle for entry. The optimal one depends on the company's strategy: 1. Exporting

':~~rt,"!!~~aJt~:!~~;'Yt~Cr~i~~:~PI~:~'i~e~'~oaJ::.pansion as 2. Licensing

A foreign licensee buys the rights to produce a company's product for a negotiated fee; hcensee puts up most of the overseas capital.

3. Franchising Franchising is a s~eCialized fann of licensing. The franchiser not on~ sells intangib e property, but also insists that franchisee agrees to allow strict rules as to how it does business.

4. Joint Ventures Typically a 50150 venture - a favored mode for entering a new market

5. Wholly-Owned Subsidiaries Parent company owns 100% of subsidiary's stock - setup or acquire

CopyrightC Houghton Mif!Un Company.AlI rights rC$Orvod, 325

Choosing Among Entry Modes .:. Distinctive Competencies and Entry Mode

To earn greater returns from differentiated products or where competitors lack comparable products, the optImal mode of entry depends on the nature of the company's dlstlnct1ve competency:

Technological know-how » Wholly-owned subsidiary is preferred over licensing and joint

ventures to minimize risk of losing control. Management know·how

» Franchising, joint ventures, or subsidiaries are preferred as risk is low of losing management know..J1ow.

.:. Pressures for Cost Reduction and Entry Mode The greater the cost pressure, the more likely a company wl/l want to pursue some combination of exporting and wholly~owned subsidiary:

Export finished goods from wholly-owned subsidiary Marketing subsidiaries for overseeing distribution

» Tight control over local operations allows company to use profits generated in one market to improve position in other markets.

CopyrighlO Houghton MtI!IIn Compu.ny.A11 rights I1I:SOMXl. 37:1

Making Strategic Alliances Work The failure rate for international strategic alliances is quite high. Success seems to be a function of three main factors:

1. Partner selection - A good partner: Helps the company achieve strategic goals Shares the finn's vision for the purpose of the alliance

• Is unlikely to try to exploit the alliance to its own ends t<:> Conduct research on potential partners

2. Alliance structure Risk of giving too much away is at an acceptable level Guard against opportunism by partner in alliance agreement

3. Manner in which alliance is managed Sensitivity to cultural differences Build relationship capital through Interpersonal relationships

I Successful partners view the alliance as an opportunity to I learn rather than purely as a cost- or risk-sharing device.

CopyrighlO Houghlon Mlftlin Compu.ny.AII rlghbfnl:ll'lOd. 3 29

Advantages and Disadvantages of Different Entry Modes

TableB.1

'--

\'IhDlliO\YMd ,uhsidl,rlocrf

,un .. " •• • Ab~to Inial:' be~lIoll In:! eK~cri~ntO' turrel!t~

• Al:t~U b b!ol FD!Ulun 1.ntrt .. ltIlIao • Sh~I~'(/dilVlllojmlunttcm~m1lbu 'Fnll:lt#!dopUldcn~

~ PICl!ltIIOneflet.h!'l:llol/'l • Abi1ityloenD'~l!rnll!U!::l!~!n'll!llt

t~in~1!tIIl • Abilitylolnlu~ bt'~lIn In~ u~erlentD'

tIfNillltIl<lI'U''lm

CopyrightQ Houghton Mlmln Compu.ny.A11 righbf~lVod.

·H,ghtltntl.'DrteClU • TI.d~b~"~1I • Pn:Ib!eIJlS....mIo~~'nuBt\ing"~= • In:lbl!ltvUllealll~ 1=:~11on tnd !:'ljlud~n~~·

CI1fVultt0f1Ulllia1 'IM~iIityUltn\l~~oingrDb:l1ttrDlt;;ic t~nlon

·lat1eleOfllmlr;rt~Ie"..h~~

• lIIabilityU)tn~u~ltin\l!obals1rlllo.ic. cD!lrtbl.lion

• uti:1 to!\lI'!lIO'(~fll~~t't( • hu\li1ilyto-=ng~gltingloba!stfat~;i:

~a~tl",.lIon • Il'IIIb~H}'lIIle~llle 1=:al!on'n!I ex;::eri~nta·

CI/MI':CI1IHl1ie. ~ uti: fll ~tL'lr.11n~e: I~:hnob;n' • Il,~h en~tumjlUu

Real World

.:. "Diebold"

~P,'II

CopytlghlO Houghton Mlmln Company. All righbl1l:SOlVod.

Strategy in Action

·:·Cisco and Fujitsu

CopyrlghlQ HoughlonMimln ComPllITY.AII righb rnsolVod.

-3126

3 2B

3 30

5

Real World Real World

.:. "Fuj i-Xerox" ·:·"It's a Grand-Latte World"

~@

CopyrlghlC Houghton Mlmin ComJljlfl)'.A1J tlllhtslO$Orvod. 3 31 CopyrlghlC Houghloo MilII!n Company.AIl rillhb rcl$Clrvod. 332

End of Lecture 8

UFIFW~ w~ CoJb,geollloaima

CopyrightCHoughton MiII'Iin Company.AIl rJlihl:l /lt$01Vod. 333

6

markets was the lower level in the latter, where consump-

'Vt:ll<O "~ ".> ~>. capita of colas was only 10-15%

United States figure. Goizueta pushed iOCa-\ .... VJ.c. to become a global company, cen

a great deal of management and maractivities at the corporate headquarters .

TUJL<:,.,.~,focusing on core brands, and taking stakes in foreign bottlers so that the com. exert more strategic control over

one-size-fits~al1strategy was built standardization and the realization of

of scale by, for example, using the messageworldwide ..

global strategy was' adopted by ::iSUI~C~:SSc)r, Douglas Ivester, but by the lat~ . '. the drive toward a one~size~fitscallstrat

running out of steam,assinallet, more ···.local competitors marketing local· bevbegan to halt the Coke groWth engine ..

. 'Coca-Cola failing tqhit its financial tar-: .' the first time in a generation, Ivester ,

in 2000 and was replaced by DougDaft instituted a 180~degree shift

Daft's belie(was that· Coca-Cola to put more power back, in the hands'

country nian~gers;.·.Ije thought ,that product development, and;h1arket"

be tailored.to local needs. He laid employees, many of th~m in Atlanta,

j.l'.".C11"',"U country managers tnuch greater Moreover" in a striking move for

"<\,L,,,-,,,.U15 company, he, announced that the ' would stop making global advertise

he placed advertising budgets and . ; over creative content back in the hands

managers. move was in part influenced by the of Coca-Cola in Japan, the com-

ij,ijt~COJ[la-most profitable market, where the Coke product is not a carbonated

beverage but a canned cold coffee dr~Georgia Coffee-sold in vending rrutchines. The Japanese experience seemed to signal that produCts should be customized to. local tastes and preferences; and Coca-Cola woulddoweU' to decentralize more deciSion-making authori1ttolocal managers,: .....

However, the shift toward 'localizatron. ,did not produce the groyvth . that had ,'been expected; by 2002 the pendulum was swinging back toward more central cooidination, with Atlanta exercising, oversight, over, iriar-

'ketlng andproductdevelopnient i~differep.t .nationsO<Butthis tilne;~t was Iiqtthe Qri~-~i~e.fits~all"eth6softhe Goizueta .• ed.·UnCletil:ie . ,

. le~cleiship ofNeviU~ Isde;ll;·\vhObecaIIle'CEO. in. March20Q4, '. G()ca~C()la hegaIlre~iewing!'::' .and~~4irig .. local marketi~ganct:pr~clu#';~

;, development but ad6pted thdb~lief~l:t~t.:s~t~~~ .). ;' egy,'incl~dingpricing;,productpfferirigs:and":~' . riiarl<et~gh1essage{sh()ul~Q~ va+,ie~f··ftor:r\); .. ', ',markettomatkett6 fuatchJ6cal conditions. 11)del1's .pdsItion; .ir(otheiwords1represerit~it midpoint 'betWeeij.Jhe.strat~gy;.of···Goii~eta);;'· and paft. MoreQver, .J1;den.stressed.tp,e,ihIpor~ ',' ~ fance·of leveraging good ideas acrossnatiq~s;·L ' , A ,casdn pointis Geoigi;lCoffee;Having:$~eIl·i· the suc~essOfthis,b~ver~g'e;inJ~pan,inOcto~.~:,: ber 2007;, COQa~Cola':t~ht~red~iIitoa:si:i:ategic;: .. ,.'. alliance with Illycaffe; bne of Italy'spreinier coffee makers, to build a globaLfranchise for canned or bottled cold cbffeebeverages; Similarly, in 2003, the Coke subsidiary in China developed alow~cost, noncarbonated orangebaseddrinkthat has rapidly become one of the best-sellirig drinks iIi that nation. Seeing the potential of the drink, Coca"Cola is how rolling it out in other Asian countries. It has been a huge hit in Thailand, where itwas in 2005, and seems to be gaining traction India, where it was launched in 2007.1

CHAPTER 8 Strategy in the Global Environment

Strategy in Action 8.1

.. .' .' ....... , ·;·;pl;ionerriarket is one of the great growth . Nokia, a long-time telecommunications equipment ". ". :stories ()ftH~last 'decade .. Starting from a very low base in . supplier, was well positioned to take advantage of this de-

199();ari:llual global sales .ofwirelessphones surged to v~lopment from the start, but there were also other forces .. ' reaclr44()fuillibnunits in2003.Bythe end df2003,thereat work that helped Nokia develop its competitive edge.

Weie:over·L2Pillion wireless, subscribers worldwide, up Unlike virtually every other developed nation, Finland fromi~~s,.thCln JOrriillioIi iri 1990. NokiaiSadominqnthasileverhada nati0I1altelephone monopoly. Instead, ..

' ..•...... plaYetllithemarket for ;mobile telephone, sales~ Nokia's ..the<;01lI1try's telephone ~eryices. haVe long be~n providecl . ...... !,ro()tsa:~e .. iIl·Firil~nd,notno!rriallya c()llntrythat come.s. .' byabol1t,flfty"orso clUtOJ10mous.l(jcal teleph~mecolllpa:' ·t(j~dw.~~ii . one .taJks about ·leading~edge teclulology'" :niesw40se .. electe4. p()ards .. set. price~ .. by referenduIIl . '.' cOinpapies.Jn the C1980s, Nokia was a I(iiTlbling 'Finnish : '.( whichl1atl1rallymeans low prices) i This army ofinde- ..

.. congi9lii~ratewjthaCtirties that embraced tire rnanu~ ." .. pendent :.~4cost-·conscioustelepho~e service . providers ". f~c,tqring;!I#p~tpr~dllcti6#;~onsllmer~1¢2tronks,andpr¢Vei1teg ;Nokia fronltaki~g anythirig for granted in its '. :tel¢co#tinliIiidttibl1S equipfllent. )3jr 2004itha.dtrans-· ··h6me:~oiInfrY~ yVithtypicalFmnish pragnjatisgl, its tus~ fOl:ll1¢d:it$el( 4Itoa Jocilsed telecoIllmlll1icatiorisequip," .•. .)orneiswereWilllilg to buyfrOl1lthe l()west -c6s(suppli~r,.. .

•. : .11i~~thlarlufa:dl1rer\vith·.a .g16bal.· reach,:sale~:6f.·over •...•.. ' .. ·.Wh~ther .•.• th,lt>~asN()lcia;Ericsson, ··1v1otorola;or •• some.·.·.··. $3()biliiori'::i:~<irnirigs:'ofrrioiethin:$5biliioi1"'fuida;':other'company.J'flls sitllationcontrasted sharply with ..

. ,'::3 ~:;~etfd~t.ih(lre9ftlH~gl6p~~#ketfor~ir~les$ ~hol1es~ ." :th~tprey<IilirtginIriost . developed nations untiL the late .•. . . . '. ': H~iih~~. tpIs . .fOJfu~r.c~l1gl()IllerateelTIerg¢4to ~akea', ". ". j~80s. aIld e<}riy 199()s; w,her~ domestktelephone m6nop~; .. · .. \gloli~:[email protected]()~itiwi~iriieless.telec()Ihh.)unic~-:.,?li~stypicallYPllJchctsedequipmentfr6fu ad9mincinf': . .: '#9~~;~qllWII1,~nt?Much; of the (tn,swerlies . iIl~he' his~ .,]Q2alsllPpli~r ,or made it themselves: Nokia resp~nded to' ..h?ry,geogr~phy,andpoliti¢qLecbnolllyofFil1lan4 and . ···t11is.coinp~titivepressurel:>y,doirlg everything possible to ,.'

itsN~r~ic:heighbors.. .... ...... . . .... ,....... ....... ..drivedqwnitsmanufacturing ¢ostswhilestaying at the ............ Ip,1·98J·th.~Nordicnatiohsc06peratedt()cr~ate the.' ··l~aclingedgeofY\Tirelesstechnol()gy,.· ... ' ...... . '.' .. ' ....•.. ' ..... . '.world'sifirst: international,.:wireless telephonenetwcirk.' . . .... ·.·.·the conseqlieI1cesof these forces are dear. Nokia is., ...•.• ···:theY4¥.g()pdreasont~) becoin~pioneers: it cost fal" toq· '.' ·n9~th.electderin(iigitalwirelesstechnology,Which iHhe.· 'nitii:4!ohiyi4owpa traditional Wire line telepllOne serv~ " 'wav(of the future. Manynow regard Ilinland as the. lead ,.·iceiD.·W()~e,sparselY .poptYated and. inhospitaply .coldmcirl«~tforwireless teIepl1brie serviCes. If you. wa.ntto see ....... . . ·.·countrles;Thesame featur~s made telecbmmuniCations:"t4efufureof wireiess, you don't g6 to :New YorkofS~n .• " .

...~~~~J~;.t~it~{;~~::L'~j!~,~te~~~ ..• J:s1"~~r~~:ci:j;;j~~~e~~::;btl:t:~~· ... '. ··telephoI1~t()sUrnmonhelpifthingsWentWrong:As 'a re- 'browse'theWeb, exe~ute e~Commerce transactlons,con:'

sU1t.,;S~~,ddn,N()rw:ay,arid.FinlaI1gbecan1e .. the first .~a- "'troi hous~hola h~ating and lightiIig systeII1s~'~r Pllr~h~se" tionsinthe world' to' takewirelesstelecoIriintinitations····· '.toke· frqrria wireless~enabled .yendin.g ll1~c~e.<N()kia, .:

.seii~u~ly.Theyfound, for'e~iupple,that although it cost • ..' h~sgairied this lead' because Scandinayia startedswitch~, . ·~Pt() ,$80Q persubs.criber to ?ringatraditiohal Wire lin.e/'il1gto4igit~ teclnlg10gyfive years pefore the r.es} of the .. s~rvice to.remote locati()ns;·thesame locations.,couldbe·, .:Wbild.Spiiirecl'qnbyjtstost~conscious . Finnish cus- . .iillk~4by~eless c~lltilaiforonly.$506per·pbrsdIl.:AI;:a, '\,f6ffiers, Nolcia 'n()w.has the.iqwest cost ~trllctureo(aI1Y.· ' .. .C011s·~~Uetfce,12 per~~l1t()fp¢9pieiI1sca;Idinayia9~ed ' .. ' ·.ceUtYarphoI1e" equipJ.llentmanufactuh~rin the·. world, .. ' ¢~llu1a):,phon~s by 1994, <;0Illpai"e4With less than 6 percent •.•. ':'anqtfUlS i~am()re .profitable enterprise than ¥otorola,.

'.' • iIi thellnitecl States, the wciHd's second. riiost . developed .. ' .. ' :it~leadiTIg glQbal.tiyal. It cosiN okia an aVt!rage()f~ 114 to . .. ·irt~rk~t,''J:'hisjead~6ntin4ed~verthe l1eXt' dec~cl~~By t1W .{ 'irIake<tnclseU¢achphol1e ill 2002,comparedWithabcmt' .' .

·· ..•. enq()f2Q03 ,85 percent <?f.thepoplJlatioIi, in>finlaIid ··$l?la.year iearlier; Its '. cl()s~st .• rival,'Iv1ot9rolajn~ ..••. of, b~eg~ :Wh:~#ssph6ne, colllpared with 55per.centinthe.· -. Schamnburg, ;Illinois, spent an average 0($P9 ·.tomake:,

. United States;' '. . .. '.. .... ··ahdselleachphohe.~· . . ". '. ". -.' . . :. , :;:~,'. ~.: .' , ,,' .

PART 3 Strategies

Running Case

Wal-Mart's Global Expansion

. early 1990s managers at Wal-Mart realized that the company's opportunities for growth in the United States were becoming more limited. By 1995 the company would be active in all fifty states, and management calculated that by the early 2000s domestic growth opportunities would be constrained because of market saturation. So the company decided to expand globally. Initially, the critics scoffed. Wal-Mart, they said, was too American a company. While its business model was well suited to America, it would not work in other countries where infrastructure was different, where consumer tastes and preferences varied, and where established retailers already dominated.

Unperturbed, in 1991 Wal-Mart started to expand internationally with the opening of its first stores in Mexico. The Mexican operation was established as a joint venture with Cifera, the largest local retailer. Initially, Wal-Mart made a number of missteps that seemed to prove the critics right. It had problems replicating its efficient distribution system in Mexico. Poor infrastructure, crowded roads, and a lack of leverage with local suppliers, many of whom could not or would not deliver directly to Wal-Mart's stores or distribution centers, resulted in stocking problems and raised costs and prices. Initially, prices at Wal-Mart in Mexico were some 20 percent above prices for comparable products in the company's U.S. stores, which limited Wal-Mart's ability to gain market share. There were also problems with merchandise selection. Many of the stores in Mexico carried items that were popular in the United States. These included ice skates, riding lawn mowers, leaf blowers, and fishing tackle. Not surprisingly, these items did not sell well in Mexico, so managers would slash prices to move inventory, only to find that the company's automated information systems would immediately order more inventory to replenish the depleted stock.

By the mid 1990s, however, Wal-Mart had learned from its early mistakes and had adapted its operations in Mexico to match the local environment. A partnership with a Mexican trucking company dramatically improved the distribution system, while more careful stocking practices meant that the Mexican stores sold merchandise that appealed more to local tastes and preferences. As Wal-Mart's presence grew, many ofWal-Mart's suppliers built factories close by its Mexican distribution centers so that they could better serve the company, which helped to

further drive down inventory and logistics costs. Today, Mexico is a leading light in Wal-Mart's international operations. In 1998, Wal-Mart acquired a controlling interest in Cifera. By 2003, Wal-Mart was more than twice the size of its nearest rival in Mexico, with 623 stores and revenues of over $11 billion.

The Mexican experience proved to Wal-Mart that it could compete outside of the United States. It has subsequently expanded into nine other countries. In Canada, Britain, Germany, Japan, and South Korea, Wal-Mart entered by acquiring existing retailers and then transferring its information systems, logistics, and management expertise. In Puerto Rico, Brazil, Argentina, and China, WalMart established its own stores. As a result of these moves, by 2003 the company had over 1,350 stores outside the United States, employed 330,000 associates, and generated international revenues of more than $46 billion.

In addition to greater growth, expanding internationally brought Wal-Mart two other major benefits. First, Wal-Mart has also been able to reap significant economies of scale from its global buying power. Many ofWal-Mart's key suppliers have long been international companies; for example, GE (appliances), Unilever (food products), and Procter & Gamble (personal care products) are all major Wal-Mart suppliers that have long had their own global operations. By building international reach, Wal-Mart has been able to use its enhanced size to demand deeper discounts from the local operations of its global suppliers, increasing the company's ability to lower prices to consumers, gain market share, and ultimately earn greater profits. Second, Wal-Mart has found that it is benefiting from the flow of ideas across the eleven countries in which it now competes. For example, a two-level store in New York State came about because of the success of multilevel stores in South Korea. Other ideas, such as wine departments in its stores in Argentina, have now been integrated into layouts worldwide.

Wal-Mart realized that if it didn't expand internationally, other global retailers would beat it to the punch. In fact, Wal-Mart does face significant global competition from Carrefour of France, Ahold of Holland, and Tesco from the United Kingdom. Carrefour, the world's second largest retailer, is perhaps the most global of

the lot. This pioneer of the hypermarket concept now operates in twenty-six countries and generates more than 50 percent of its sales outside France. Compared to Carrefour, Wal-Mart is a laggard, with just 18.5 percent of its sales in 2003 generated from international operations. However, there is still room for significant global

CHAPTER 8 Strategy in the Global Environment

expansion because the global retailing market is still very fragmented. In 2003 the top twenty-five retailers controlled less than 20 percent of worldwide retail sales, although forecasts suggest the figure could reach 40 percent by 2009, with Latin America, Southeast Asia, and eastern Europe being the main battlegrounds.b

308 PART 3 Strategies

CHAPTER 8 Strategy in the Global Environment

Strategy in Action 8.2 . MTV Goes Global, with a Local Accent

'MTV Networks has become a symbol of globalization. for India, separate Mandarin feeds for China and Taiwan, a E~tablishe4 ill 1981; the U.S.-based music TV network has Korean feed for South Korea, a Bahasa-language feed for beene:icpanding .outside its North American base since Indonesia, a Japanese feed for Japan, and so on. Digital and

... 1987;whenitopened MTV Europe. Now owned by media satellite technology have made the localization of program-conglorrwrate Viacom," MTV. Networks, which includes miug cheaper and easier. MTV Networks can now beam half .siblingsNi<:~elode9I1 and y.Hi, .the music station for thea dozen feeds off one satellite transponder. 'agi.J:ig~~bY1?9()mers, gelleratesmore than $1 billion in While MTV Networks exercises creative control over'

. revenues ,outside the United States. Since 1987, MTV has . 'thesediff~fentfeeds, and while all the channels have the . 'b~cpi:I;teThep1qstubjqu,itouscablepr9grammer ,in the . . same familiar frenetic look andfeel of MTV in theUnited

wbrld".~y~q04th~n~1:WorkhaAseventy~two channels, or S1:ates,a significant share of the programming and content distillct feeds, that reached a. combined total of321 million . '. isno:w local. When MTV opens a local station now, it first

" .'ho~s~~?ld~:ill110countri~~.' .'. "., . ...•... .,.. '.,", .•. ' ,.', .' '., asksexp~triates fnmlelsewhere ill the world to do a "gene '.' ... ,iWlillefueUmte4 States still leads in number of house- . transfer"'ofcompcinyculture and operatillgprinciples-in

.' ···h(M~;With7qh#Wol1;theIl1o~t Fapid gr9wthis elsevvhere, . ' ,'other words, its busmess model. But mice thes~. are estab~, Pc#cYIa,r!Y:0~i~,vl/here,neflTly.two-thirds of the region's lished, thel1etworkswitches to local eI11ployeesarid .the ,

·• .. >3bi11j.oIlpe(}pIe'are,ili14er,tlUrhr-five, ,the middle class is 'expatriatys m9veon.The idea is to ')~et msidethe heads" of,'. ...eXpanclll;1gqlllckly,ClIld'TV,O~ership isspreadmg rapidly. '" tilelocalpoImlatiml and produceprograrnpling that>. '

,. '" . IvrrV'NetW&r].<Sfigures,'th~t ,every' s~cond' of everyday' ... InCltcl1es tileiJ; tastes~AIthough a~muchas 60pers~nt()f#1e . a1¥~~t':trhiUibllp~OpleaJ:e,-watchillg MTV ru:oundthepfograllunirig still originates in theUriitedStates,With sfa.-woddi the hlajority'6litside the United States. ..... . > pIes sllchasThe Real World having equivalents in, different' .

. . 'Despit¢itsiIlternationaI success, MTV'sglobal e:icpan- countries; anincreasiIlg share ofprogrammingis.lqcalill . '. siongot.off;~()'a weak, stcu1:,In1987, it piped a single . feed .:. c::onc~pti(m; I11 Italy;1v1TV Kitchen .combines .cooking with. .

':. ,acf?s.sEUiope:aIrtios{entirelycomposed otAillerkan prb~. a mlisiccolintdown. Erotica airsin Biazilarid features a ;graillinillgWi~' EAglish.~speal<ing veejays. Nai~eIy,the net - . . panel of youngsters discussing'.sex .. TheII1di\li1. ch<UlIlel :W6rI?sU.S.illanag~rsth~ughfEuropearisw6uld flock toth~ producestwei1ty~orteh6megroWI1 ~l10Ws, b.()ste(I .,by:Jocal. ~erkan¥r6gr~ifBl.lt while ·.vIewerS in Europe .' '. "veejayswhospeak "HIDglish:' a dtY~bied mix6f Hindi al1d .. shiir~dac(jinII1onin~eiest in ahan.dful of global superstars, . . :English; Hit shows include MDlCricketin Control, aJ?pro~ '. 'Who~tth~:i;jIl1e'inchid~d Madotniaand Michael· Jackson, 'J?riate for a land where cricket is a nati()n~ obsession;MTV .. . :. thefr·ta~tesfurned()ut t(),be' sUrprisinglYlocal. What was Housefull, . which. hones in on fIin.difi1m stars (India has . , pOptilariIiGermallymigb.t not bepopular in Great Britant : t}ie biggest filini:ndu~try outside of Hollywood), and MTV.

::;Mai:ty;s~ples. 6ttheA,rrierican'm)lsicscene lefrEutopeans/Bakra,which is m()deled after Candid Camera. . .. '.. .. 'i. "'col<;liand,,:tviT\Tsuffereda$ ,a resUlt.. Soon local copycat .. '. ·.Thislocalizationpushha~f(~aped .... bigbeI1efits for , . : ....• st~ti6i1s,wefesprmglngupiIiEurop~that focused on the . ·MTV,capWring .. viewers b~ckfroiri)()cal·· imita~(m.ln

Inusic '. sceneiniIidividualcouritries; These stations took .... . . India; ratillgsiiicreas~d bymor~thrui 700 per<:ent between.·.· ....• . :. ·-viewersag~~dveffiseE¥aWa.yfrom MTY.ABeWlained by '1996, when thelocalizationpusIibegan" and ~OOO.lriturI1,,· .

ToIll,FF~ston:;,~l1ai,rman. ofMTVNetworks, "We were going '.' .. ,19saljz~tipnhelpsMTY t9 ',' captUrelTIoFe: Qf,1i].ose '~-.' ..••..... Jqi,1i].el119~t sh3IIo:w layer of what . United viewers and .. ' .. i1rlportaIitadv~rtising revenues,evenfroln pther,in]l1tIDa~ ' .. i)rOllgh~.theIritQgether .. It4idn'tgo' ()vyr to0'WeU:' '.' . ..' .. ·tignals$uch,as 'Coca~Cola, whose o0i,adver~si,ng budgets .. '.

,'"IP,)9g?;'MIV chllPged it~strategy~~ brdke Europe:· '#eoften locanYdet~rrrlllle(:L In.E~Qpe; 1v1Ty's aclvertisjng .•....... ,,)lJiQr~giof1~ fe~d$, of which there are now ~ight:. one fo~ the •..• . .', r~venlles liIcreased by 50· percy(lt,betyveen .19,95 ,and .' 2000, .'.

'.. •.••. Vll1ted~gcl()in @dI:i;el~d; anotherf9~,CielTI1aI1y,i\~stri~, ,:"Y11ilethe tbtaImcvket forpaJi lEll1'0peart advertising ii; . . '#d.Swi1:Z~t,lcW4;6fleJoiSccincijrtav1a;. one for Italy; ()ne fo~. .."alued at just $'400ll,lillion; th~. total market f()r1ocal adver~ . '. rrc1A~e; B#~Jo{~pcAA;oIie for 1{ollanq;fu1d a feed for oth.er. ' '.~ tising .~cr()ss . Europe . is .' a much bigger pie, .v:cillledat,$12 ... , ..

, .......... Eui()p~cui'p~ti91is, iI1~hl(lirig B.el~umand Gr~ece.1penet~ .,. ' .. billion .. IviTVnow gets 70 perc~nt of its. EuropeaIl adver~ ". WQrkacloptedthesariielo.calizationstrategy elsewhere in the ' ...•... tising reVenue .• from .1o~aIsp()ts,upfrom 15' i?~rcehtirl' ·.,~world.Nr~ple; iIi,Aslait has mlEnglish-Hindi channel.. ·.1995.Siriillar trendsareevidenfelsewhere inthewodd.c ,

";', ".',;::;,' ,., ~ ,i":'\': '. ",' . '. ' " " . :. ..

(

(

Strategy in Action 8.1 McDonald's Is Here, There, and Everywhere

Established in 1955, by the early 1980s McDonald's faced a problem: after three decades of rapid growth, the U.S. fast food market was beginning to show signs of market saturation. McDonald's response to the slowdown was to expand rapidly abroad. In 1980, 28 percent of the chain's new restaurant openings were abroad; in 1986, the figure was 40 percent, in 1990, it was close to 60 percent; and in 2000, it was almost 90 percent. Since the early 1980s, the company's overseas revenues and profits have grown at 22 percent annually. By the end of 2000, McDonald's had 28,707 restaurants in 120 countries outside the United States, which generated $21 billion, or 53 percent of the company's $40 billion in revenues.

McDonald's shows no signs of slowing down. Management notes that there is still only one McDonald's restaurant for every 500,000 people in the ~)\'erseas countries that it currently does business in, which compares to one McDonald's restaurant for every 25,000 people in the United States. Moreover, the company currently serves less than 1 percent of the world's population. Thus, the (;ompany's strategy is for this overseas expansion to continue at a rapid rate. In Europe, it opened more than 500 new restaurants in 1999 and in 2000, while the figure for Asia was around 600. A major expansion plan is for Latin America, where the company plans to invest $2 billion over the next few years.

McDonald's enters an overseas country only after careful preparation. In what is a fairly typical pattern, before McDonald's opened its first Polish restaurant in 1992, it spent eighteen months establishing essential contacts and getting to know the local culture. Locations, real estate, construction, supply, personnel, legal, and government relations were all worked out in advance. In June

1992, a team of fifty employees from the United States, Russia, Germany, and Britain went to Poland to help with the opening of the first four restaurants there. By mid-1994, all of these employees except one had returned to their home countries. They were no longer needed because Polish nationals had been trained to run an efficient McDonald's operation.

Indeed, another key to the company's global expansion strategy is the export of the business model that spurred its growth in the United States. McDonald's success was built on a formula of close relations with suppliers, nationwide marketing might, tight control over store-level operating procedures, and a franchising system that encourages entrepreneurial individual franchisees. Although this system has worked well in the United States, some modifications must be made in other countries. One of the company's biggest challenges had been to infuse each store with the same culture and standardized operating procedures that have been the hallmark of its success in the United States. To aid in this task, in many countries McDonald's has enlisted the help of large partners through joint venture arrangements. The partners playa key role in learning and transplanting the -organization's values to local employees. Overseas partners have also played a key role in helping McDonald's adapt its marketing methods and menu to local conditions. Although U.S.-style fast food remains the staple fare on the menu, local products have been added. In Brazil, for example, McDonald's sells a soft drink Jllade ~ from the guarana, an Amazonian berry. Patrons of}i McDonald's in Malaysia, Singapore, and Thailand savor r milkshakes flavored with durian, a fruit considered an/ aphrodisiac by the locals. In Arab countries, McDonald.:§'

(

restaurants maintain halal menus, which signify compli'anee with Islamic laws on food preparation, especially b1:ef. In 1995, McDonald's opened the first kosher restau-

hr'kt in suburban Jerusalem which does not serve dairy l~products. And in India, the big Mac is made with lamb 'and called the Maharaja Mac. ':\' McDonald's biggest problem has been to replicate its 'U.S. supply chain in other countries. U.S. suppliers are flacely loyal to McDonald's; they must be, because their fortunes are closely linked to those of McDonald's. McDonald's maintains rigorous specifications for all the raw ingredients it uses-the key to its consistency and quality control. Outside the United States, however, McDonald's has found suppliers far less willing to make the investments required to meet its specifications. In Great Britain, for example, McDonald's experienced quality problems with two local bakeries supplying hamburger buns, so it built its own bakery to supply its stores there. In a more elireme case, when McDonald's decided to open a store in Russia, it found that local suppliers lacked the capability to produce goods of the quality it required. The company was forced to integrate vertically through the

CHAPTER 8 Strategy in the Global Environment 265

local food industry on a heroic scale, importing potato seeds and bull semen and indirectly managing dairy farms, cattle ranches, and vegetable plots. It also had to construct the world's largest food-processing plant, at a cost of $40 million. The restaurant itself cost only $4.5 million.

Now that it has a successful overseas operation, McDonald's is experiencing benefits that go beyond the immediate financial ones. Increasingly, it is finding that its overseas franchisees are a source of valuable new ideas. The Dutch operation created a prefabricated modular store that can be moved over a wet:kend and is now widely used to set up temporary restaurants at big outdoor events. The Swedes came up with an enhanced meat freezer that is now used companywide. And the small satellite stores and low-overhead mini-McDonald's that are now appearing in hospitals and sports arenas in the United States originated in Singapore.

Sources: Kathleen Deveny, et aI., "McWorld?" Business Weck, October 13, 1986, pp. 78-86. "Slow Food," Economist, February 3, 1990, p. 64. Harlan S, Byrne. "VveJcomc to McWorld," Barron's, August 29, 1994, pp. 25-28. Andrew E. Serwer, "McDonald's Conquers the World," Fortulle, October 17, 1994, pp. 103-116.

( J

The Jollibee Phenomenon-A PhL_rJt.Jlne Multinational

,.:.; I'

Jollibee is one of the Philippines' phenomenal business success stories. Jollibee, which stands for "Jolly Bee," began operations in 1975 as a two-branch ice cream parlor. It later expanded its menu to include hot sandwiches and other meals. Encouraged by early success, Jollibee Foods Corporation was incorporated in 1978, with a network that had grown to seven outlets. In 1981, when Jollibee had 11 stores, McDonald's began to open stores in Manila, the capital city. Many observers

thought Jollibee would have difficulty competing against McDonald's. However, Jollibee saw this as an opportunity to learn from a very successful global competitor. Jollibee benchmarked its performance against that of McDonald's and started to adopt operational systems similar to those used at McDonald's to control its quality, cost, and service at the store level. This helped Jollibee to improve its performance.

. As it came to better understand McDonald's business model, Jollibee began to look for a weakness in McDonald's global strategy. ·Jollibee executives concluded that McDonald's fare was too standardized for many locals, and that the local firm could gain share by tailoring its menu to local tastes. Jollibee's hamburgers were set apart by a secret mix of spices blended into the ground beef to make the burgers sweeter than those produced by McDonald's, appealing more to Philippine tastes. It also offered local fare including various rice dishes, pineapple burgers, banana langka and peach mango pies for desserts. By pursuing this strategy, Jollibee maintained a leadership position over the global giant. By late 2002, Jollibee had 465 stores in

the Philippines, a market share of more than 50 percent, and revenues of about $500 million. McDonald's, in contrast, had 237 stores.

I n the mid-1980s, Jollibee had gained enough confidence to start expanding internationally. Its initial ventures were into neighboring Asian countries such as Indonesia, where it pursued the strategy of localizing the menu to better match local tastes, thereby differentiating itself from McDonald's. In 1987, Jollibee entered the Middle East, where a large contingent of expatriate Filipino workers provided a ready-made market for the company. The strategy of focusing on expatriates worked so well that in the late 1990s Jollibee decided to enter another foreign market where there was a large Filipino population-the United States. Between 1999 and 2002, Jollibee opened eight stores in the United States, all in California. Even though many believe the U.S. fast-food market is saturated, the stores have performed well. While the initial clientele was strongly biased toward the expatriate Filipino community, where Jollibee's brand awareness is high, non-Filipinos increasingly are coming to the restaurant. In the San Francisco store, which has been open the longest, more than half the customers are now non-Filipino. Today Jollibee has 28 international stores and a potentially bright future as a niche player in a market that has historically been dominated by U.S. multinationals.

Sources: Christopher Bartlett and Sumantra Ghoshal, "Going Global: Lessons from Late Movers," . Harvard Business Review, March-April 2000, pp. 132-45; "Jollibee Battles Burger Giants in US Market," Philippine Daily Inquirer, July 13, 2000; www. jollibee.com.ph; and M. Bailon, "Jollibee Struggling to Expand in U.S.," Los Angeles Times, September 16, 2002, p. Cl.

.~;~ ;~~ ·:~l

{r ",i.1

." .,.t.~~

(

Strategy in Action 8.2 Hewlett Packard in Singapore

In the late 1960s, Hewlett Packard was looking around Asia for a low-cost location to produce electronic components that were to be manufactured using labor-intensive processes. It eventually settled on Singapore, opening its first factory there in 1970. Although Singapore did not have the lowest labor costs in the region, costs were low relative to North America, plus the Singapore location had several important benefits that could not be found at many other locations in Asia. The education level of the local work force was high; English was widely spoken; the government seemed stable and committed to economic development; and the city-state had one of the betterdeveloped infrastructures in the region, including good communications and transportation networks and a rapidly developing industrial and commercial base. HP also extracted favorable terms from the Singapore government with regard to taxes, tariffs, and subsidies.

Initially, the plant manufactured only basic components. The combination of low labor costs and a favorable tax regime helped to malce this plant profitable early. In 1973, HP transferred the manufacture of one of its basic hand-held calculators from the United States to Singapore in order to reduce manufacturing costs, which the Singapore factory was quickly able to do. Increasingly confident in the capability of the Singapore factory to handle entire products as opposed to just components, HP's management transferred other products to Singapore over the next few years, including keyboards, solidstate displays, and integrated circuits. However, all of these products were still designed, developed, and initially produced in the United States.

The plant's status shifted in the early 1980s when HP embarked on a worldwide campaign to boost product quality and reduce costs. HP transferred the production of its HP41C hand-held calculator to Singapore. The managers at the Singapore plant were given the goal of substantially reducing manufacturing costs. They argued that this could be achieved only if they were allowed to redesign the product so it could be manufactured at a lower overall cost. HP's central management agreed, and

twenty engineers from the Singapore facility were transferred to the United States for one year to learn how to design application-specific integrated circuits. They took this expertise back to Singapore and set about redesigning the HP41C.

The results were a huge success. By redesigning the product, the Singapore engineers reduced manufacturing costs for the HP41C by 50 percent. Using this newly acquired capability for product design, the Singapore facility then set about redesigning other products it produced. HP's corporate managers were so impressed with the progress made at the factory that they transferred production of the entire calculator line to Singapore in 1983. This was followed by the partial transfer of ink jet production to Singapore in 1984 and keyboard production in 1986. In all cases, the facility redesigned the products and often reduced unit manufacturing costs by more than 30 percent. The initial development and design of all these products, however, still occurred in the United States.

In the late 1980s and early 1990s, the Singapore plant started to take on added responsibilities, particularly in the inl< jet printer business. In 1990, it was given the job of redesigning an HP ink jet printer for the Japanese market. Although the initial product redesign was a market failure, the managers at Singapore pushed to be allowed to try again, and in 1991 they were given the job of redesigning HP's DeskJet 505 printer for the Japanese market. This time the redesigned product was a success, garnering significant sales in Japan. Emboldened by this success, the plant has continued to take on additional design responsibilities. Today, it is viewed as a lead plant within HP's global network, with primary responsibility not just for manufacturing but also for the development and design of a family of small ink jet printers targeted at the Asian market.

Sources: K. Ferdows, "Making the Most of Foreign Factories," Harvard Business Review (March-April1997): 73-88. "HewlettPackard: Singapore;' Harvard Business School Case #694-035 (1996).

The Evolution of Global Strategy at Procter & Gamble

Founded in 1837, Cincinnati-based Procter & Gamble has long been one of the world's most international of companies. Today P&G is a global colossus in the consumer products business with annual sales in excess of $50 billion, some 54 percent of which are generated outside of the United States. P&G sells over three hundred brands-including Ivory Soap, Tide, Pampers, lAM pet food, Crisco, and Folgers-to consumers in 160 countries. It has operations in 80 countries and employs close to 100,000 people globally. P&G established its first foreign factory in 1915 when it opened a plant in Canada to produce Ivory Soap and Crisco. This was followed in 1930 by the establishment of the company's first foreign subsidiary in Britain. The pace of international expansion quickened in the 1950s and 1960s as P&G expanded rapidly in Western Europe, and then again in the 1970s when the company entered Japan and other Asian nations. Sometimes P&G entered a nation by acquiring an established competitor and its brands, as occurred in Britain and Japan, but more typically the company set up operations from the ground floor.

By the late 1970s the business model at P&G was well established. The company developed new products in Cincinnati and then relied on semiaut.onomous foreign subsidiaries to manufacture, market, and distribute those products in different nations. In many cases, foreign subsidiaries had their own production facilities and tailored the packaging, brand name, and marketing message to local tastes and preferences. For years this business model delivered a steady stream of new products and reliable growth in sales and profits. By the 1990s, however, profit growth at P&G was slowing down.

The essence of the problem was simple: P&G's costs were too high primarily because of extensive duplication of manufacturing, marketing, and administrative facilities in different national subsidiaries. The duplication of assets made sense in the world of the 1960s, when national markets were segmented from each other by barriers to cross-border trade. Products produced in Britain, for example, could not be sold economically in Germany because of the high tariff duties levied on imports into Germany. By the 1980s, however, barriers to crossborder trade were falling rapidly worldwide and fragmented national markets were merging into larger regional or global markets. Moreover, the retailers through which P&G distributed its products were themselves growing larger and more global, such as Wal-Mart from the United States, Tesco from the United Kingdom, and Carrefour from France. These emerging global retailers were demanding price discounts from P&G.

In 1993 P&G embarked on a major reorganization in an attempt to control its cost structure and recognize the new reality of emerging global markets. The company shut down some thirty manufacturing plants around the globe, laid off 13,000 employees, and

(

PART 3 Strategies

concentrated production in fewer plants that could better realize economies of scale and serve regional markets. These actions cut some $600 million a year out of P&G's cost structure. It wasn't enough: profit growth remained sluggish.

In 1998 P&G launched its second reorganization of the decade. Named "Organization 2005;' the goal was to transform P&G into a truly global company. The company tore up its old organization, which was based on countries and regions, and replaced it with one based on seven self-contained global business units, ranging from baby care to food products. Each business unit was given complete responsibility for generating profits from its products, as well as for manufacturing, marketing, and developing the products. Each business unit was also told to concentrate production in fewer larger facilities to try to build global brands wherever possible, thereby eliminating marketing differences between countries,

and to accelerate the development and launching of new products. In 1999 P&G announced that, as a result of this initiative, it would close down another ten factories and layoff 15,000 employees, mostly in Europe, where there was still extensive duplication of assets. The annual cost savings were estimated to be about $800 million. P&G planned to use the savings to cut prices and increase marketing spending in an effort to gain market share and thus further lower costs through the attainment of scale economies.

This time the strategy seemed to work. In 2003 and then again in 2004, P &G reported strong growth in both sales and profits. Between 2002 and 2004 revenues surged 28 percent, from $40.2 billion to $51.4 billion, while profits increased an impressive 46 percent, from $4.35 billion to $6.34 billion. Significantly, P&G's global competitors, such as Unilever, Kimberley-Clark, and Colgate-Palmolive, were struggling in 2003 and 2004.1

1'i , ... ~

.. ~ 1

Diebold

For much of its 144-year history, Diebold Inc. did not worry much about international business. As a premier name in bank vaults and then automated teller machines (ATMs), the Ohio-based company fO!lnd tbi'lt it had its hands full focusing on U.S. financial institutions. The company first started to sell ATM machines in foreign markets in the 1980s. Wa of going it alone, Diebold forged a distribution a reement with the na-tional e ectronics com an . . er the agree-ment, Ie 0 manufactured ATMs in the United States and exported them to foreign customers after Philips had made the sale.

In 1990, Diebold pulled out of the agreement with Philips and established a joint venture with IBM, Interbold, for the research, development, and distn utlO M m . Ie 0 ,w Ich owned a 70 percent stake in the joint venture, supplied the machines, while IBM supplied the global marketing, sales, and service functions. Diebold established a joint venture rather than setting u its own international distribution s stem because the company thoug t It lacked the resources to establisl i ai i ii 1te1l1B(ional presence. In El'ssence, Diebold was -axporting its machines via IBM's distribution network. } By 1997, foreign sales had grown from the single digits to more than 20 percent of Diebold's total revenues, while sales in the United States were slowing due to a saturated domestic market. Looking forward, Diebold saw rapid growth in demand for ATMs in a wide range of developed and developing markets. Particularly enticing were countries such as China, India and Brazil, where an emerging middle class was starting to use the banking system in large numbers and demand for ATMs was expected to surge. It was at this point that Diebold decided to establish its own foreign distribution network.

As a first step-Diebold purchased IBM's 30 percent stake in the Interbold joint Venture. In a w y lebold's dissatisfaction with IBM' e ,w IC 0 ten e sort 0 quota. Part of the problem was that for IBM's sales force, Diebold's ATMs were just part of their product portfolio, and not necessarily their top priority. Diebold believed it could attain a greater market share if it gained direct control over distribution.

The company also realized that in addition to local distribution, it would need a local manufacturing presence in a number of regions. Among the reasons for this were differences in the way ATMs are used, requiring cus-

tomization of the product. In parts of Asia, for example, many customers pay their utility bills with cash via ATMs. To gain market share, Diebold had to design ATMs that both accept and count stacks of up to 100 currency notes, and weed out counterfeits. In other countries, ATMs perform multiple functions from filing tax returns to distributing theater tickets. Diebold believed that locating manufacturing close to key markets would help facilitate local customization.

To jump-start its international expansion, Diebold went on a foreign acquisition binge. In 1999 it acquired Brazil's Procomp Amazonia Industria Electronica, an electronics company with sales of $400 million and a big presence in ATMs. This was followed in quick succession by the acquisitions of the ATM units of France's Groupe Bull and Holland's Getronics, both major players in Europe for a combined $160 million. In China, where no substantial indigenous competitors were open to acquisition, Diebold established a manufacturing and distribution joint venture in which it took a majority ownership position. The result: by 2002 Diebold had a manufacturing presence in Asia, Europe, and Latin America as well as the United States and distribution operations in some 80 nations, the majority of which were wholly owned by Diebold. International sales accounted for some 37 percent of the company's $1.94 billion in revenues in 2002, and were forecast to grow at double-digit rates.

Interestingly, the acquisition of Brazil's Procomp also took Diebold into a new and potentially lucrative global business. In addition to its ATM business, Procomp had an electronic voting machine business. In 1999, Procomp won a $105 million contract, the largest in Diebold's history, to outfit Brazilian polling stations with electronic voting terminals. Diebold's management realized this might become a large global business. In 2001, Diebold expanded its presence in the electronic voting business by acquiring Global Election Systems Inc., a U.S. company that provides electronic voting technology for states and countries that want to upgrade from traditional voting tecnnology.

Sources: H. S. Byrne, "Money Machine," Barrons, May 27, 2002, p. 24; M. Arndt, "Diebold," Business Week, August 27, 2001, p. 138; W. A. Lee, "After Slump, Diebold Pins Hopes on New ATM Market Features," American Banker. September 15, 2000, p. 1; and C. Keenan, "A Bigger Diebold, Phasing Out IBM Alliance, Will Market ATMs Itself," American Banker, July 3, 1997, p. 8.

1I1ESY lit:

Cisco and fujitsu

In late 2004, Cisco Systems, the world's largest manufacturer of Internet routers entered into an alliance with the Japanese cornputer, electronics, and telecommunications equipment firm, Fujitsu. The stated purpose of the alliance was to jointly develop next generation high-end routers for sales in Japan. Routers are the digital switches that sit at the heart of the Internet and direct traffic; they are, in effect, the traffic cops of the Internet. Although Cisco has long held the leading share in the market for routersindeed, it pioneered the original router technology-it faces increasing competition from other firms, such as Juniper Technologies and China's fast growing Huawei Technologies.At the same time, demand in the market is shifting as more and more telecommunications companies' adopt Internet-based telecommunications services. While Cisco has long had a strong global presence, management also felt that the company needed to have better presence in Japan, which is shifting rapidly to second generation highspeed Internet-based telecomrnunications networks.

By entering into an alliance with Fujitsu, Cisco feels it can achieve a number of goals. First, both firms can pool their R&D efforts, which will enable them to share complementary technology and develop products quicker, thereby gaining an advantage over competitors. Second, by combining Cisco's proprietary leading edge router technology with Fujitsu's production expertise,

the companies believe that they can produce products' that are more reliable than those currently offered. Third, Fujitsu will give Cisco a stronger sales presence in Japan. Fujitsu has good links with Japan's telecommunications companies and a well-earned reputation for reliability. It ' will leverage these assets to sell the routers produced by the alliance, which will be co-branded as Fujitsu~

Cisco products. Fourth, sales may be further enhanced,. by bundling the co-branded routers together with telecommunications equipment that Fujitsu sells marketing an entire solution to customers. Fujitsu fTlany telecommunications products but lacks a presence in routers. Cisco is strong in routers but strong offerings elsewhere. The combination of the company's products will enable Fujitsu to offer telecommunications companies "end-to-end" cations solutions. Since many companies prefer to chase their equipment from a single provider, this sll() drive sales.

The alliance introduced its first products in May If it is successful, both firms should benefit. ment costs will be lower than if they did not Cisco will grow its sales in Japan; and Fujitsu ca ' the co-branded routers to fill out its product line more bundles of products to Japan's telecommun companies.

Sources: "Fujitsu, Cisco Systems to Develop High-!=nd Routers for Web Traffic;' Knight Ridder-Tribune Business News, December 6,2004, "Fujitsu and Cisco Introduce New High Performance Routers for IP Next Generation Networks;' JCN Newswire, May 25, 2006.

294 P\RT -' S'ra'~le.l

. 8.4 :' . . . .' /11 . ' . . .. . - ~.. , ... .. ," .-.

: . . .. ., .' ~

rlginally established in 1962, fuJi-Xerox is structured as a 50/50 joint venture between the Xerox Group, the U.S. maker of photocopiers, and Fuji Photo Film, Japan's largest

manufacturer of fiJm products. With 1995 sales of more than $8 billion, FUji-Xerox provides Xerox with more than 20 percent of its worldwide revenues. A prime motivation for the initial establishment of the joint venture was the facl that in the early 1960s the Japanese government did not allow foreign companies to set up wholly owned subsidiaries in Japan. The joint venture was originally conceived as a marketing organization to sell xerographic products that would be manufactured by Fuji Photo under license from Xerox. However, when the Japanese government refused to approve the establishment of a joint venture intended solely as a sales company, the joint venture agreement was re\ised to give Fuji-Xerox manufacturing rights. Day-to-day management of the venture was placed in the hand of a Japanese management tearn, which was given autonomy to develop its 0\\11 operations and strat-

. egy, subject to oversight by a board of directors that contained representatives from both Xerox and Fuji Photo.

Initially. Fuji-Xcrox followed the lead of Xerox in manufactUring and selling the large high-mlume copiers developed by Xerox in the lniled Stales. These machines were sold at a premium price 10 the high end of the mar-

~ ..

ket. However, Fuji-Xerox noticed that in the]apanese market new competitors, such as Canon and Ricoh. were making Significant inroads by building small low-volume copiers and focusing on the mid- and low-priced segments of the market. This led to Fuji-Xerox's development of its first "homegrown" copier, the FX2200, which at the time was billed as the world's smallest copier. Introduced in 1973. the FXZOO hit the market just in time to allow FUji-Xerox to hold its ovm against a blizzard of new competition in Japan, which followed the expiration of many of Xerox's key patents.

Around the same time, Fuji-Xerox also embarked on a total qUality control (TQC) program. The aims of the program were to speed up the development of new products. reduce waste. improve quality. and lower manufac· turing costs. Its first fruit was the FX3500. lJ1lroduced in 197;. by 19'79 the FX3500 had broken the Japanese record for the number of copiers sold in one year. Partly because oflhe FX3500's success. in 1980 the compan~ won Japan's prestigious Demint! Prize. The succes~ of Ihis copier W:L~ all the more notahk hecause at [he same tinlt Xerox wa.~ canceling a senes of programs 10 derelop Ic)\\·

to mid·k'\d copier!> and reaffimling in~\(:;ld il" commilment 10 sening Ihe high end uf the market.

By the early 1980s. Fuji-Xerox was numbcr r ..... o in the Japancsc copier market. \\ith a share in the 20 percent to

C!tAPTER R Sire/If',!.,.'" /11 Ihe Glohal tll/'lrrJII!/TI'r:1 295

perce~;~~ ,:fi!~'~::f~i~'f~~;J;!~l~_I~~~~ ';;:i~~"i~~;~~~oori:~"~t::~; , on. In contrast, Xerox was miming into all sorts of ,": ;' Jti'1983 to 300 per million by 1992," , ' , ! :',' roblems in the' U.S. IDarkel As Its"patents had expired, a ',,: In 1985 and 1986, Xerox bei3n focusing on itS new-

ber of compain~, includirig 'Canon, Ricoh, Kodak, , p!OdUct development process. One goal was to design d ffiM, had begun to take 'market share from Xerox. products that, while customized to market conditions in

on and Ricoh were particularly successful by fOCUSing different countries, also contained a large number of glob-n that segment of the market that Xerox had ignored- ally standardized parts. Another goal was to reduce the time , e low end. As a result, Xerox's market share in the it took to design new products and bring them to market. . ericas fell from 35 percent in 1975 to 25 percent in To achieve these goals, Xerox set up joint product develop-980, while its profitability slumped. ment teams with Fuji-Xerox. Each team managed the de-

,;. Seeking to recapture share, Xerox began to sell Fuji- sign, component sources, manufacturing, distribution, and " ox'S 00500 copier in the United States. Not only did follow-up customer service on a worldwide basis. The use

e FX3500 help Xerox halt the rapid decline in its share of of design teams cut as much as one year from the overall e U.S. market, but it also opened Xerox's eyes to the ben- product development cycle and saved millions of dollars, ts of Fuji-Xerox's TQC program. Xerox found thaI the re- The new approach to product deve!opmenlled to the

,'-ect rate for Fuji-Xerox parts was onJy a fraction of that for creation of the 5100 copier-the first product designed .. 5. parts. VISits to Fuji-Xerox revealed another importint jointly by Xerox and Fuji·Xerox for the worldwide market. ,truth: quality in manufacturing does not increase real Manufactured in U.S. planlS, il was launched in Japan in -Costs; it lowers them by decreasing the number of defec- November 1990 and in the Vniled States the folloVring ". e products and reducing sen-ice costs. These develop- February. The global design of the 5100 reportedly re-ments forced Xerox 10 rethink the way it did business. duced overall time to market and saved the company

From being the main prO\ider of products. technol- more than $10 million in deve)opmenl costs. 'ogy. and management know· how 10 Fuji-Xerox, Xerox he· Thanks 10 the ~kill~ and producl" acquired from Fuji-'-came in the 1980s the willing pupil of Fuji-Xerox. In Xerox. Xerox's pOSition improl'ed markedly during Ihe 1983. Xerm. introduced ilS Leadership Through Quality 19805. The company was able to regain market share

it'program. which WJS based on Fuji·Xerox·s TQC program. from ilS competilors and 10 boosl its profits and revenues. ~ As part of this effort. Xerox launched quality training for Xerox's share of the U.S. copier market increased from a E its suppliers and was rewarded when the numher of de- low of 10 percenl in 198510 18 perc en! in 1991.3Z

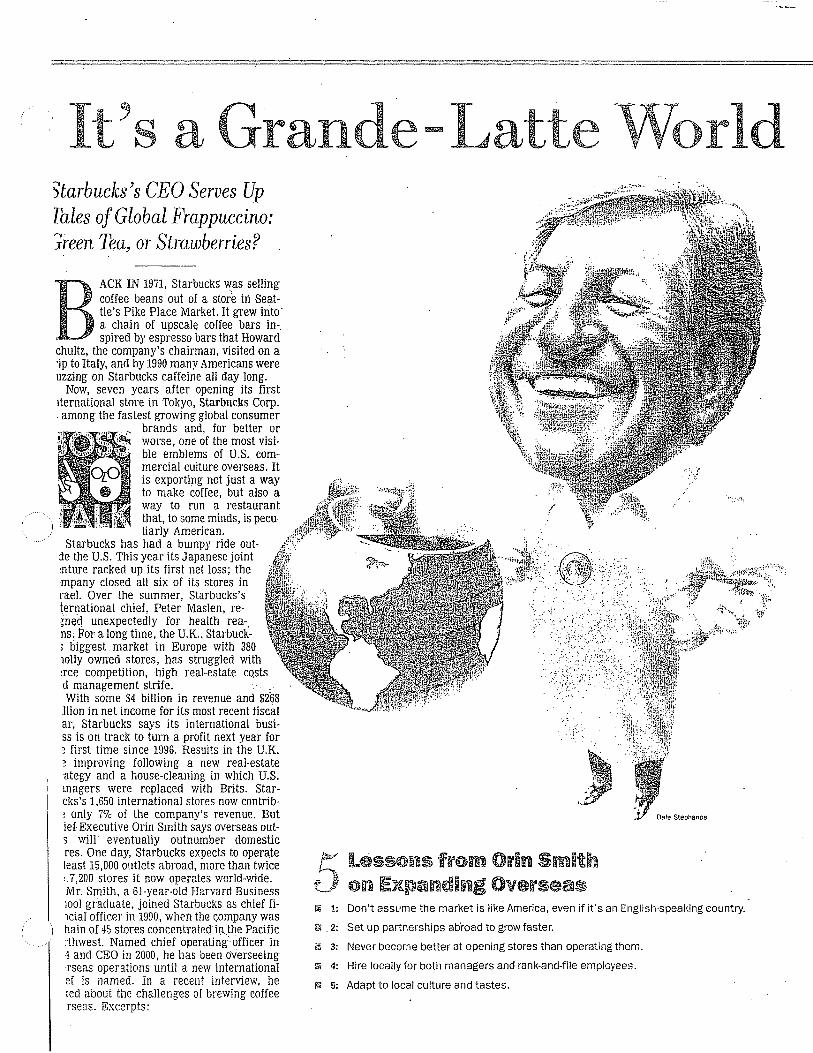

It's a Grande-Latte vorld ~tarbucks) s CEO Serves Up fales of Global Frappuccino: ;reen Tea, or Strawberries?

BACK IN 1971, StarbuckS was selling coffee beans out of a store iii Seattie's Pike Place Market. It grew into· a chain of upscale coffee bars in-" " spired by espresso bars that Howard

chultz, the company's chairman, visited on a 'ip to ItalY, and by 1990 many Americans were uzzing on Starbucks caffeine all day long.

Now, seven years after opening its first lternational store in Tokyo, Starbucks Corp. " among the fastest growing global consumer

brands and, for better or worse, one of the most visible emblems of U.S. commercial culture overseas. It is exporting not just a way to make coffee, but also a way to run a restaurant that, to some minds, is peculiarly American.

Starbucl{s has had a bumpy ride out:le the U.S. This year its Japanese joint ~nture racked up its first net loss; the mpany closed all six of its stores in rae!. Over the summer, Starbucks's ternational chief, Peter Maslen, re~ne"cj unexpectedly for health rea-" ns; For a long time, the U.K .. Starbuck-; biggest market in Europe with 380 lOlly owned stores, has struggled with ~rce competition, high real-estate costs d management strife. With some $4 billion in revenue and $268

"Ilion in net income for its most recent fiscal ar, Starbucks says its international b\lsiss is on track to turn a profit next year for ~ first time since 1996. Results in the U.K. ~ improving following a new real-estate "ategy and a house-cleaning in which U.S. magers were replaced with Brits. Starcks's 1,650 international stores now contrib~ only 7'7c of the company's revenue. But ief Executive Orin Smith says overseas outs will" eventually outnumber domestic res. One day, Starbucks expects to operate least 15,000 outlets abroad, more than twice ,.7,200 stores it now operates world-wide. Mr; Smith, a 61-year-old Harvard Business 100] graduate, joined Starbucks as chief filciar officer in 1990, when the company was hain of 45 stores concentrated i\1.~he Pacific :thwest. Named chief operating"officer in 4 and CEO in 2000, he has been ov"erseeing rseas operations until a new· international ef is named. In a recent interview, he ted about the challenges of brewing coffee rseas. Excerpts:

h Le$SO~lS from Orin Smith f._Ion Expanding Overseas l\j 1: Don't assume the market is like America, even if it's an English-speaking country.

~ "2: Set up partnerships ab"road to grow faster.

iii 3: Never become better at opening stores than operating them.

~ 4: Hire locally for both managers and rank-and-file employees.

Pi1 5: Adapt to local culture and tastes.