Chapter -5 Role of Research and Development in Indian...

55

105 Chapter -5 Role of Research and Development in Indian Industry An essential component of competitive strategy or behaviour is recognizing the role that Research and Development (R&D) which plays a crucial role in the success of a firm, and acting to ensure that technology decisions and policies contribute to the firm's competitive advantage. This unit provides a framework, which can be used to analyze and understand the linkages between R&D and competitive strategy and / or competitive advantage of a firm. Generally, R&D is of two types viz; product innovation and process innovation. R&D plays a crucial role in the Indian industry. R&D has two roles viz; performance promoting and cost reducing. Performance can be measured by profit and sales of the firm. Theoretically, the objective of the firm is to either maximize profit or sales. In this study, profit margin and sales has been considered as a proxy of performance. R&D can increase sales or profit of the firm in the long run. R&D can decrease also the cost of production of the firm, so that firm can compete with his rivals. This chapter highlights whether firm’s R&D is used as performance promoting expenditure or cost reducing expenditure. Role of R&D in the case of automobile and drugs and pharmaceuticals industry are discussed in the following two sections. 5.1: Role of R&D in Indian Automobile Industry In the automobile industry, innovation of a firm is one of the most important factors to maintain its strong competitive position in the industry. Innovation is also a key to resolving most of the global challenges that the industry faces. Without innovations, the entire concept of individual mobility is put at risk. Innovation may be done in the form of fuel efficiency, emissions, safety and security, seamless connectivity and infotainment,

Transcript of Chapter -5 Role of Research and Development in Indian...

105

Chapter -5

Role of Research and Development in Indian Industry

An essential component of competitive strategy or behaviour is recognizing the

role that Research and Development (R&D) which plays a crucial role in the success of a

firm, and acting to ensure that technology decisions and policies contribute to the firm's

competitive advantage. This unit provides a framework, which can be used to analyze and

understand the linkages between R&D and competitive strategy and / or competitive

advantage of a firm. Generally, R&D is of two types viz; product innovation and process

innovation. R&D plays a crucial role in the Indian industry. R&D has two roles viz;

performance promoting and cost reducing. Performance can be measured by profit and

sales of the firm. Theoretically, the objective of the firm is to either maximize profit or

sales. In this study, profit margin and sales has been considered as a proxy of performance.

R&D can increase sales or profit of the firm in the long run. R&D can decrease also the

cost of production of the firm, so that firm can compete with his rivals. This chapter

highlights whether firm’s R&D is used as performance promoting expenditure or cost

reducing expenditure. Role of R&D in the case of automobile and drugs and

pharmaceuticals industry are discussed in the following two sections.

5.1: Role of R&D in Indian Automobile Industry

In the automobile industry, innovation of a firm is one of the most important

factors to maintain its strong competitive position in the industry. Innovation is also a key

to resolving most of the global challenges that the industry faces. Without innovations, the

entire concept of individual mobility is put at risk. Innovation may be done in the form of

fuel efficiency, emissions, safety and security, seamless connectivity and infotainment,

106

hassle free performance, comfort, flexibility and space within the vehicles – and with more

value for the money. The total cost of ownership will remain the most important buying

factor – a fact that limits the number of successful innovations in the automobile industry.

The continuous cost pressure in the automobile industry created by legislation,

competition, increasing risk and stagnating customer demands has a strong impact on

innovation management. The automobile suppliers will have to significantly improve

efficiency in all R&D processes to keep costs under control and keep the performance to

improve. Furthermore, the effectiveness of each innovation must be investigated. This will

be accompanied by structural changes in the industry’s R&D departments. The

concentration process in the supplier industry will improve innovative strength by the way

of cutting costs while increasing the quality of innovations. After a good year 2009-10

during which economies across the world showed signs of recovery, the economic

conditions globally continued to be strong and positive in 2010-11, resulting in a strong

growth for the automotive sector. The Indian economy continued to do glowing, driven by

a good performance from the agricultural and the industrial sector with a GDP growth of

8.6 per cent. The automobile sector recorded a high growth of over 26 per cent in India on

the back of a robust economy3. As the study is on the firm level, it is important to know

about the R&D expenditure and pattern in case of some of the leading firms as these are

mainly concerned with different types of R&D viz; product innovation, process innovation

or both product and process innovation are discussed in the following.

Ashok Leyland Ltd. Company has developed new Engine (N-Series) platform and

applied on vehicles, existing engine platform (H-series) upgraded to BS IV emission

norms. In the case of vehicles, new vehicle platform (‘U Truck’) launched, with initial

3 Annual report of Tata motors 2010 -11

107

offerings in tippers and tractors. Migration of current vehicle is a platform to BS3 / BS4

norms. Benefits derived as a result of R&D are compliance with emission standards slated

for implementation from April 2010. Potential for extension of the engine is a platform to

cover compressed natural gas (CNG), marine & industrial applications. Introduction of

New Lean Development Process with resultant benefit of reduced time to market. Total

R&D Expenditure as a per cent of total turnover is 2.97 per cent.4

During 2009, Eicher Motors Ltd. has emphasized on product innovation. Apart

from these four wheeler vehicles, Eicher Motors Ltd. launched “Classic bike” in the two

categories of 350 cc and 500 cc. The “Classic bikes” are powered by a single cylinder 500

cc Unit Construction Engine (UCE) supported by Electronic Fuel Injection (EFI). The

UCE has an integrated assembly for the engine, gear box, clutch and this reduces the

friction between movable parts, resulting in lower transmission losses. The company have

taken a policy to change the engine from the year 2010. UCE engine will replace the

present “Cast Iron” engines in Electra and standard bikes as well to meet the Indian

emission norms of BS-II (Euro III) effective from the month April 2010. The company

have focussed on R&D activities with the development of new products and variants

thereof apart from improving the existing products and value engineering projects. An

amount of Rs. 6.4 million was occurred on capital account and Rs. 77.7 million on

revenue account in R&D.5

In the case of Force Motors Ltd., the expenditure on research and development for

new products, including the expenditure on Projects and Tool Engineering was 2.92 per

4 Annual Report of Ashok Leyland 2010 -11.

5 Annual Report of Eicher Motors 2010 -11.

108

cent of the operational turnover of the company. The company has put more emphasis on

research and development and tool engineering activities.6

In the case of Hero Cycles Ltd., increasing competition in the market has brought

into sharp focus importance of differentiation. Their Research & Development Centre

recognised by Govt. of India as an in house R&D Centre is instrumental in providing

company a competitive edge by bringing out new products / models and improved

components to meet consumers' aspirations and thus helping the company to achieve its

targeted growth. The state of art R&D Software like three dimensional modelling and

software are extensively used. During the year 2006, company has launched 16 new

models and set of new product for export market. This brought the concept of high quality

with low cost bicycles through internal R&D. The market for fancy cycles has shown a

significant growth since last few years. Total R&D expenditure as a percentage of sales

was 0.03 per cent in 2006. The company is upgrading technology absorption and

innovation to enhance its market share both in domestic and export. The company has not

imported any technology in the last five years. However, it has entered into a technical

assistance agreement with National Bicycle Industrial Co. Ltd. of Osaka, Japan in 2002 for

upgrading its technology7.

Hero Honda Motors Ltd. (HHML), established in 1984, is a joint venture between

Hero Group, the world’s largest bicycle manufacturers and the Honda Motor Company of

Japan. It is the world’s largest two-wheeler manufacturer. During the year 2004, HHML

renewed its technical collaboration with Honda Motor Corporation of Japan for another

ten years up to year 2014. This will give HHML access to Honda’s technology for another

6 Annual Report of Force Motors 2009-10.

7 Annual Report of Hero Cycles Ltd. 2009-10

109

ten years for developing new products. HHML plans to launch two motorcycles in FY05

and a scooter with the technology provided by Honda. Increasing competition, price

undercutting, rising steel prices and other input costs continue to pose a threat. Reduction

in import duties for imports could also pose a threat for the higher end bikes. The company

is planning to further increase its capacity to meet the growing demand for motorcycles. It

is considering setting up a third plant for its products8. Though unfortunately in 2011,

these two companies are separated and produced their product separately.

Mahindra & Mahindra Ltd. has a market share of 10.01 per cent for Commercial

Vehicles, 6.5 per cent for Passenger Vehicles and 1.31 per cent three wheelers. Mahindra

& Mahindra is mainly engaged with the production of Multi Utility Vehicle and Three

Wheeler segments directly. The company competes in the Light Commercial Vehicle

(LCV) segment through its joint venture subsidiary Mahindra Navistar Automotives

Limited and in the passenger car segment through another joint venture subsidiary

Mahindra Renault. In the year 2009, on the domestic sales front, the company along with

its subsidiaries sold a total of 2,20,213 vehicles (including 44,533 three wheelers, 8,603

Light Commercial Vehicles through Mahindra Navistar Automotives and 13,423 cars

through Mahindra Renault), recording a growth of 0.6 per cent over the previous year. The

company’s domestic Multi Utility Vehicle sales volumes increased by 3.3 per cent, as

against a decline of 7.4 per cent for industry Multi Utility Vehicle sales. Hence, Mahindra

& Mahindra has further strengthened its domination of the domestic Multi Utility Vehicle

sub-segment during the year, increasing its market share to 57.2 per cent over the previous

year’s market share of 51.3 per cent. Mahindra & Mahindra has expanded its business in

the overseas market also. In 2009, another model Xylo was launched in South Africa. The

8 Annual Report Hero Honda Motors Ltd. 2004.

110

company formed a new joint venture with Mahindra Automotive Australia Pvt. Ltd., to

meet the demand in the Australian Market9.

Maruti Suzuki will be coming up with the country’s first dual-fuel engine,

running on petrol and CNG, which will make the fuel cost very less drastically. Maruti

Suzuki are developing an engine that will use multi-point fuel injection (MPFI)

technology in CNG model – just as it does in petrol mode by which it will be eliminating

loss of power and efficiency associated with current retro-fitted CNG engines. With this

new engine Maruti Suzuki will bring a marked change in the way CNG-fuelled cars run on

MPFI technology that revolutionised petrol car driving at the beginning of this century.

For the customers, it provides very less burden on their wallet for fuel. And with this

technology taking shape, may be even other car manufacturers also following the same

route10.

In the case of TVS Motor Co. Ltd., the company's strong R&D team is supported

by modern computer aided laboratory, capable of developing new and innovative

products. It has state-of-art facilities for engine testing, noise, vibration and harshness

(NVH) measurements and life testing. At present, more than six hundred engineers are

working for the development of new products and in other advanced areas of technology.

The company works with leading technological research laboratories and institutions. The

company is also working on fuel-efficient technologies and carbon-di-oxide (CO2)

reduction technologies to remain ahead of needs of consumers and environment

regulations. R&D has developed and launched a new 110cc 4 stroke non-geared scooter

9 Annual Report of Mahindra and Mahindrra 2010.

10 By Mridula Maity, Product Development Manager, Rugel 10 01 2009

111

with disc brake system for export market. R&D has developed and launched a new 150cc

4 stroke liquid cooled engine for Indonesian Market. R&D has also developed and

launched another 180cc 4 stroke motorcycle with Anti-Lock Brake System (ABS)

technology. R&D team has so far published 72 technical papers in national and

international conferences11 .

In the case of Tata Motors Ltd., the company strives to be at the forefront of

innovation and works to launch so many new products aimed at the emerging needs of its

customers. It continues to develop and build on its in-house capabilities and works with

the right partners to ensure that it has competitive product offerings. Some of the

company’s key products and initiatives for the year include: showcased the Tata Pixel - a

concept for a future city car at the Geneva Motor Show; launched the Aria - a premium

crossover with high-end features such as 4x4, Torque on Demand, ESP, six air bags;

launched the BS-IV compliant variants of the Indica, Indigo CS, Indica eV2 and Indigo

eCS with segment leading fuel efficiencies. These vehicles are powered by the company’s

1.4L CRAIL engine; launched Elan - a high end variant of the Indigo Manza sedan. Ace

Zip and Magic Iris were test marketed in various parts of the country and are expected to

be formally launched across the country in May this year. This completes the Ace family

offerings now spanning from the Ace Zip and Magic Iris at the lower end and the Super

Ace and Venture on the higher end and launched the Venture - a Multi Purpose Vehicle

(MPV) on the Ace platform. The Prima range launched in the previous year was

expanded with the introduction of the Prima Cons truck range of tippers in the market.

Some Prima trucks launched in Korea and some of the tippers are soon expected to be

launched in the international markets. Jaguar Land Rover launched the all new Jaguar XJ, 11

Annual report 2010-11 of TVS motors ltd.

112

the new 4.4 V8 diesel Range Rover and the new 2.2 diesel Land Rover –Freelander.

Jaguar's Advanced Design Team and the Jaguar Land Rover Technical Innovation Team

created a concept car for the Paris Motor Show to celebrate 75 years of Jaguar Design and

Innovation. The resultant - a stunning Jaguar C-X75, is a radical combination of hyper-

car, eco-friendliness and 21st century’s technology, which won 'Car of the Show'

capturing the imagination of millions. Jaguar Land Rover recently announced their

partnership with Williams F1 to bring a version of this concept to the market in 2013. Tata

Hispano Motors Caracara, South Africa, Spain introduced 4 new brand models of its

buses, viz. Area - an urban bus, 2 hybrid urban buses and Naya - a new deluxe coach.

This along with the Xerus and Intea models launched last year would expand its product

range in high end buses / coaches. As a responsible automotive manufacturer, the Tata

Motors Group continues to develop vehicles and technologies to reduce its carbon

footprint. Some of the significant initiatives / achievements are: Showcased its CNG

parallel Hybrid low-floor city buses in the Commonwealth Games in Delhi. Tata Indica

Vista EVX developed by engineers at our European subsidiary - Tata Motors European

Technical Centre, Plc, bagged ‘the Most Economic Small Passenger EV’ and ‘the Most

Economical and Environment Friendly Small Passenger EV’ under the Small Passenger

EV category at the inaugural Royal Automobile Club, Brighton to London Future Car

Challenge. Tata motor migrated for meeting the BS-IV emission norms by developing BS-

IV compliant range of vehicles, in particular, Indica eV2 and Indigo eCS with 1.4L

CRAIL engines with segment leading fuel efficiencies. Jaguar and Land Rover continue to

invest heavily in environmental innovation to support delivery of the 2012 European

Union requirement for reduction in CO2. In 2010-11 Tata Motors launches new model

including the all new Jaguar XJ, the new 4.4 V8 Diesel Range Rover and the new 2.2

113

Diesel Land Rover - Freelander realised improvements in CO2 performance in excess of

ten per cent. The Jaguar XF and Range Rover Evoque has been launched in the second

quarter of 2011. The Jaguar XF 2.2 Diesel 817 speed automatic transmission variant with

Stop / Start technology reduces the entry model while the Evoque features a number of

lightweight, vehicle efficiency and Power train technologies that make this the most fuel

efficient Range Rover ever. Jaguar Land Rover is working on introducing a new Premium

Light weight Architecture for its products. This has seen a host of environment friendly

technologies including new aluminium alloys, down-sized power trains, Eco HMI,

sustainable materials, best-CO2 navigation routes, electronic power steering, aerodynamic

features and many more technologies. These technologies enable the delivery of class

leading 'Luxury' and 'Performance' combined with low CO2 and lay the foundation for

efficient hybridization of the platform. Jaguar Land Rover's initial Full-Hybrid programme

is also in advanced stages. In 2010-11, some of the Plug-In Hybrid projects of Jaguar Land

Rover were completed and have provided the technical foundation for a production

development programme for Parallel Plug-in Hybrids. In addition, Jaguar Land Rover has

made significant progress on a number of ongoing collaborative research and development

programmes investigating a wide range of CO2 reduction technologies. These include

radical combustion engine downsizing/pressure charging, alternative power sources for

Series Hybrids, Flywheel KERS and waste energy recovery systems. Tata Hispano Motors

Carrocera SA, Spain, won a prestigious order for supplying ten CNG Series Hybrid low-

floor city buses, to be built on the company’s chassis, to EMT Madrid, a Madrid city

public transportation company12.

12

Annual report of Tata Motors 2010-11

114

Therefore it is observed that both product and process innovation continues in the

automobile industry. The role of R&D is whether cost reducing or performance promoting

in the case of automobile industry can be discussed according to the scale wise in the

following sections. Role of R&D in case of cost margin and in the case of performance

promoting role is discussed sequentially in the case of large scale, medium scale and small

scale firms respectively in the following sub-sections 5.1.1, 5.1.2 and 5.1.3.

5.1.1: Role of R&D of Large Scale firms in the Indian Automobile Industry

As the large scale firms are the leading firms, so it is important to know the role of

R&D in case of cost margin as well as profit margin. These two roles of research and

development of the large scale automobile firms are analysed in the following.

Cost reducing role of R&D of large scale firms in Automobile Industry

To analyse the cost reducing role a specification of cost margin (CM) have been

considered which is already mentioned for all types and all scale of firms in equation (4)

under the methodology section of Chapter 3. The result for this specification is given in

the following Table 5.1. Table 5.1 consists with a set of five sub tables (Table 5.1a, Table

5.1b, Table 5.1c, Table 5.1d and Table 5.1e).

115

Table 5.1: Role of R&D on Cost Margin for Large Scale Automobile Firms

Table 5.1a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression on

Cost Margin for Large Scale Automobile Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .379568D-02

Var[u] = .396648D-02 Corr[v(it),v(is)] = .511002

Lagrange Multiplier Test vs. Model (3) = 325.21 ( 1 df, prob value = .000000) (High values of LM favor FEM/REM over CR model.)

Fixed vs. Random Effects (Hausman) = 5.00 ( 2 df, prob value = .081979) (High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .380027D-02

Var[u] = .611608D-02 Sum of Squares .152344D+01

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

Table 5.1a reveals that high value (325.21) of Lagrange Multiplier (LM) indicates

the model specification satisfies either fixed effect model or random effect model. The

decision of fixed effect model or random effect model depends on the value of Hausman

test statistic. It is observed that Hausman statistic is significant at eight percent level of

significance which implies finally the model specification supports the fixed effect model

with group dummy variable (LSDV). The measurement of goodness of fit ie; R-squared is

high (.65) and Adjusted R-squared is (.63) and from the F test it is observed that the entire

regression is meaningful (Table 5.1b).

116

Table 5.1b: ANOVA of the Regression on Cost Margin for Large Scale Automobile Firms

Least Squares with Group Dummy Variables

Ordinary least squares regression Weighting variable = none

Dep. var. = CMit Mean= .8056556931 , S.D.= .1019085690

Model size: Observations = 187, Parameters = 13, Deg.Fr.= 174

Residuals: Sum of squares= .6604483363 , Std.Dev.= .06161

Fit: R-squared= .658096, Adjusted R-squared = .63452

Model test: F[ 12, 174] = 27.91, Prob value = .00000

Diagnostic: Log-L = 262.5543, Restricted(b=0) Log-L = 162.2079

LogAmemiyaPrCrt.= -5.507, Akaike Info. Crt.= -2.669

Estd. Autocorrelation of e(i,t) .332858

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

Table 5.1c: Estimated coefficients of the Regression on Cost Margin for Large Scale

Automobile Firms

Variable Coefficient Standard Error t-ratio P[|T|>t]

RDSi t-1 2.923073763 .35566762 8.219 .0000

GFASit-1 .7329248893E-01 .40468457E-01 1.811 .0717

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

117

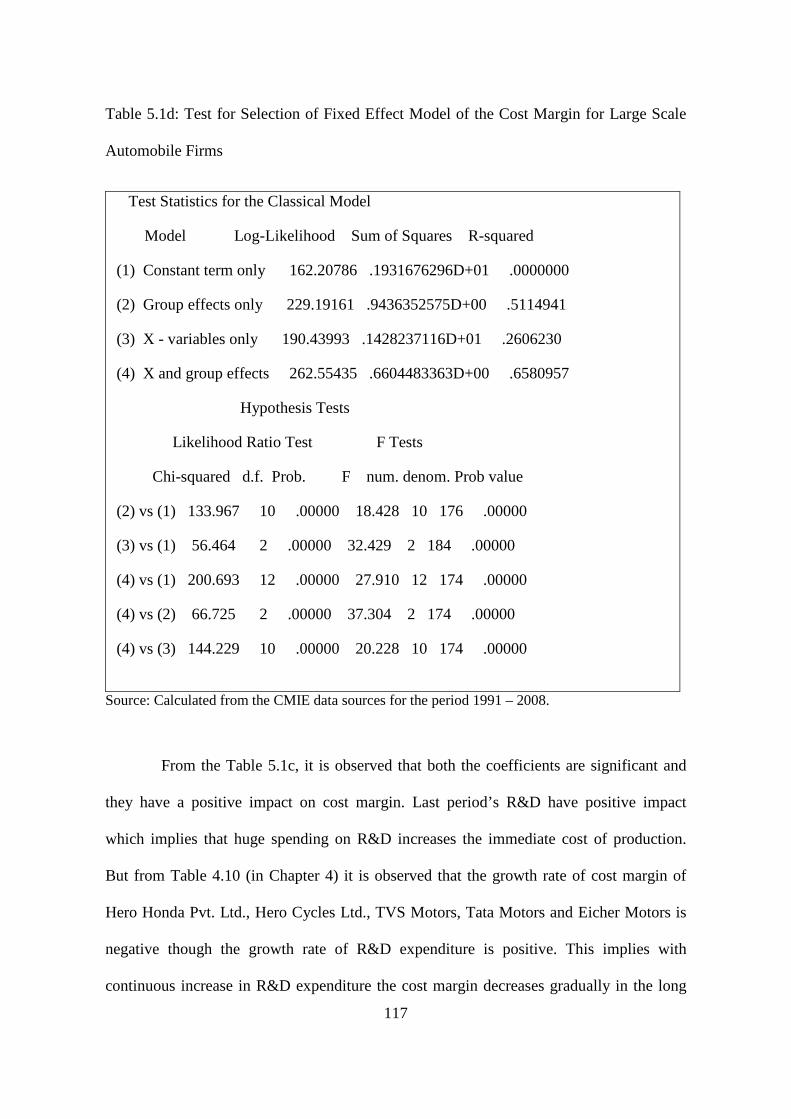

Table 5.1d: Test for Selection of Fixed Effect Model of the Cost Margin for Large Scale

Automobile Firms

Test Statistics for the Classical Model

Model Log-Likelihood Sum of Squares R-squared

(1) Constant term only 162.20786 .1931676296D+01 .0000000

(2) Group effects only 229.19161 .9436352575D+00 .5114941

(3) X - variables only 190.43993 .1428237116D+01 .2606230

(4) X and group effects 262.55435 .6604483363D+00 .6580957

Hypothesis Tests

Likelihood Ratio Test F Tests

Chi-squared d.f. Prob. F num. denom. Prob value

(2) vs (1) 133.967 10 .00000 18.428 10 176 .00000

(3) vs (1) 56.464 2 .00000 32.429 2 184 .00000

(4) vs (1) 200.693 12 .00000 27.910 12 174 .00000

(4) vs (2) 66.725 2 .00000 37.304 2 174 .00000

(4) vs (3) 144.229 10 .00000 20.228 10 174 .00000

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

From the Table 5.1c, it is observed that both the coefficients are significant and

they have a positive impact on cost margin. Last period’s R&D have positive impact

which implies that huge spending on R&D increases the immediate cost of production.

But from Table 4.10 (in Chapter 4) it is observed that the growth rate of cost margin of

Hero Honda Pvt. Ltd., Hero Cycles Ltd., TVS Motors, Tata Motors and Eicher Motors is

negative though the growth rate of R&D expenditure is positive. This implies with

continuous increase in R&D expenditure the cost margin decreases gradually in the long

118

run that indicates R&D has a cost reducing role in the industry. From the Table 5.1d, it is

observed that the fixed effect model satisfies either group effects or both explanatory

variables with group effects (as the R-square and F test is very high). These fixed effects

are given below in following Table 5.1e.

Table 5.1e: Estimated Fixed Effects of cost margin of large scale automobile firms

Company name Coefficient Standard Error t-ratio

Ashok Leyland Ltd. .73438 .02613 28.10044

Eicher Motors Ltd. .79451 .01826 43.50074

Force Motors Ltd. .65438 .03013 21.71790

Hero Cycles Ltd. .84337 .01831 46.05878

Hero Honda Motors Ltd. .82276 .01786 46.05929

Hindustan Aeronautics Ltd. .81233 .03469 23.41494

Hindustan Motors Ltd. .65688 .02890 22.72724

Mahindra & Mahindra Ltd. .70277 .02188 32.11972

Maruti Suzuki India Ltd. .65664 .02033 32.29308

TVS Motor Co. Ltd. .80091 .02066 38.76782

Tata Motors Ltd. .71237 .02573 27.68788

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

From the fixed effect results of large scale firms only Force Motors, Maruti

Suzuki and Hindustan Motors are showing lower cost margin compared to other

automobile firms. Fixed effect of all large scale firms are positive and highly significant

(Table 5.1e).

119

Performance promoting role of R&D of Large scale firms in Automobile Industry

To analyse the performance promoting role a specification of profit margin (PM)

have been considered which is already mentioned for all types and all scale of firms in

equation (5) under the methodology section of Chapter 3. Profit margin (PM) is

considered as a performance indicator. The result for this specification is given in the

following Table 5.2. Table 5.2 consists with a set of two sub tables (Table 5.2a and Table

5.2b).

Table 5.2: Role of R&D on Profit Margin for Large Scale Automobile Firms

Table 5.2a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression on

Profit Margin for Large Scale Automobile Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .760162D-03

Var[u] = .732226D-03

Corr[v(it),v(is)] = .490641

Lagrange Multiplier Test vs. Model (3) = 305.74 (1 df, prob value = .000000) (High values of LM favor FEM/REM over CR model.)

Fixed vs. Random Effects (Hausman) = 3.73 (2 df, prob value = .154660) (High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .761350D-03

Var[u] = .113435D-02 Sum of Squares .292837D+00

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

120

Table 5.2a reveals that high value (305.74) of Lagrange Multiplier (LM) indicates

the model specification satisfies either fixed effect model or random effect model. The

decision of fixed effect model or random effect model depends on the value of Hausman

test statistic. It is observed that Hausman statistic is not significant which implies the

model satisfies random effect model.

Table 5.2b: Estimated coefficients of the Regression on profit Margin for Large Scale

Automobile Firms

Variable Coefficient Standard Error b/St.Er. P[|Z|>z]

RDSit-1 .7743865555 .15802541 4.900 .0000

GFASTit-1 -.1095354775 .17093333E-01 -6.408 .0000

Constant .8289858E-01 .11318783E-01 7.324 .0000

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

From the Table 5.2b it is observed that all coefficients are significant at less than

one percent level of significance. Last period’s R&D has a positive impact on current

period’s profit margin that is R&D has a positive role on firm’s performance whereas

GFAS has a negative impact on profit margin. From the growth rate of gross fixed asset, it

is observed that all the large scale firms are maintaining very high growth rate (Table 4.10

in Chapter 4). Theoretically, large scale firms are interested to maintain long run

performance and for that they are going not only for purchasing machinery but also

increasing plant size or purchasing land or buildings. So immediate impact of gross fixed

asset on profit are negative for large scale firms as per their motive of capturing more

market share in the long run. So the impact of GFA on profit is theoretically justified.

121

Both growth rate of R&D and profit are high for large scale firms (Table 4.10 in

Chapter 4). High growth rate of the two variables indicate that R&D increases over time

and side by side firms are maintaining a positive profit margin over time. The rate of

growth of R&D is higher that growth rate of profit margin. From the regression analysis it

is also observed that if R&D of the last period increases by Rs.100 then profit margin

increases by Rs. 77.

5.1.2: Role of R&D of the Medium Scale Indian Automobile Industry

In the case of medium scale automobile firms, the cost reducing role of R&D and

performance promoting role of R&D is discussed sequentially in the following.

Cost reducing role of Medium scale firms in the Automobile Industry

To examine cost reducing role, same specification of cost margin (CM) have been

considered like large scale firms and analysed on the basis of findings in the given Table

5.3. Table 5.3 consists with a set of three sub tables (Table 5.3a, Table 5.3b, and Table

5.3c).

122

Table 5.3: Role of R&D on Cost Margin for Medium Scale Automobile Firms

Table 5.3a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression on

Cost Margin for Medium Scale Automobile Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .303745D-01

Var[u] = .243631D-02

Corr[v(it),v(is)] = .074253

Lagrange Multiplier Test vs. Model (3) = 1.77 ( 1 df, prob value = .183360) (High values of LM favor FEM/REM over CR model.)

Fixed vs. Random Effects (Hausman) = 4.07 ( 2 df, prob value = .130606) (High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .306157D-01

Var[u] = .508130D-02 Sum of Squares .380012D+01

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

From the above Table 5.3a, it is found statistically (as LM test is insignificant)

that this model specification supports the pooling regression analysis.

123

Table 5.3b: ANOVA of the Regression on Cost Margin for Medium Scale Automobile Firms

OLS Without Group Dummy Variables

Ordinary least squares regression Weighting variable = none

Dep. var. = CMit Mean= .8910113703 , S.D.= .1800842537

Model size: Observations = 118, Parameters = 3, Deg.Fr.= 115

Residuals: Sum of squares= 3.773240314 , Std.Dev.= .18114

Fit: R-squared= .005563, Adjusted R-squared = .01173

Model test: F[ 2, 115] = .32, Prob value = .72558

Diagnostic: Log-L = 35.6875, Restricted(b=0) Log-L = 35.3584

LogAmemiyaPrCrt. = -3.392, Akaike Info. Crt.= -.554

Panel Data Analysis of CM [ONE way]

Unconditional ANOVA (No regressors)

Source Variation Deg. Free. Mean Square

Between .332229 6. .553715E-01

Residual 3.46212 111. .311903E-01

Total 3.79435 117. .324303E-01

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

Table 5.3c: Estimated coefficients of the Regression on Cost Margin for Medium Scale

Automobile Firms

Variable Coefficient Standard Error t-ratio P[|T|>t]

RDSi t-1 .7378536222 1.7429993 .423 .6728

GFASit-1 .2381885228E-01 .35488130E-01 .671 .5035

Constant .8737292716 .27552333E-01 31.712 .0000

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

124

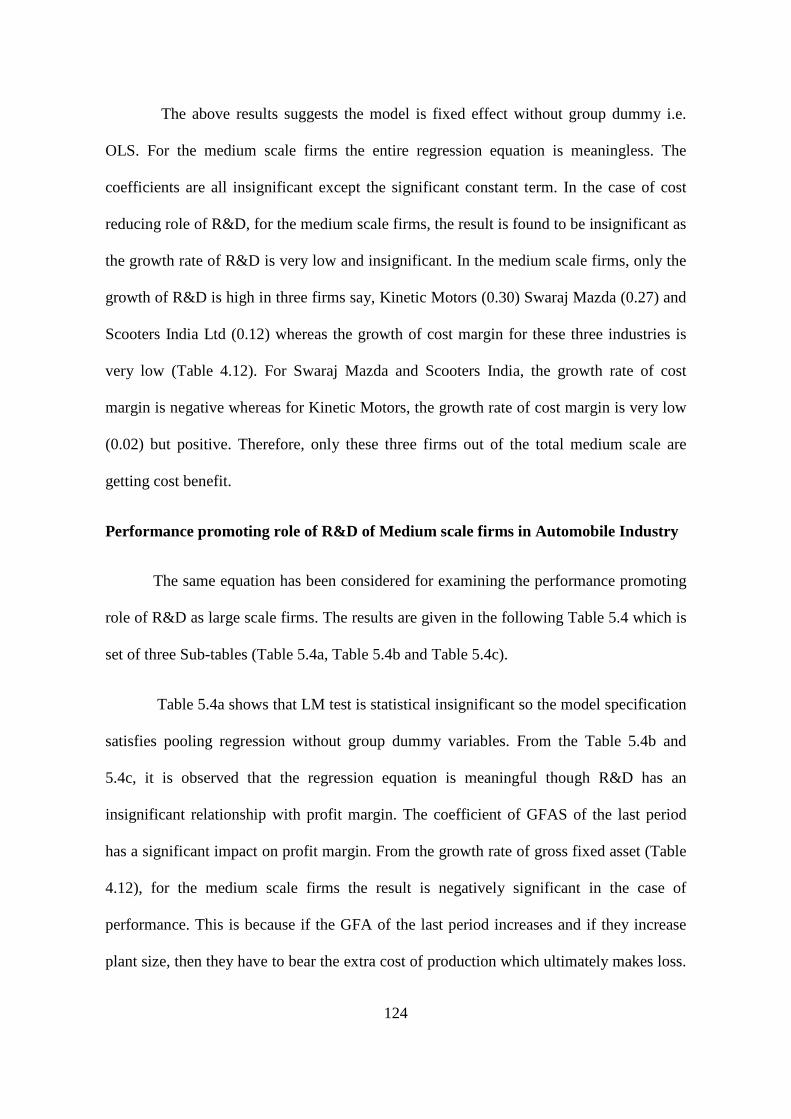

The above results suggests the model is fixed effect without group dummy i.e.

OLS. For the medium scale firms the entire regression equation is meaningless. The

coefficients are all insignificant except the significant constant term. In the case of cost

reducing role of R&D, for the medium scale firms, the result is found to be insignificant as

the growth rate of R&D is very low and insignificant. In the medium scale firms, only the

growth of R&D is high in three firms say, Kinetic Motors (0.30) Swaraj Mazda (0.27) and

Scooters India Ltd (0.12) whereas the growth of cost margin for these three industries is

very low (Table 4.12). For Swaraj Mazda and Scooters India, the growth rate of cost

margin is negative whereas for Kinetic Motors, the growth rate of cost margin is very low

(0.02) but positive. Therefore, only these three firms out of the total medium scale are

getting cost benefit.

Performance promoting role of R&D of Medium scale firms in Automobile Industry

The same equation has been considered for examining the performance promoting

role of R&D as large scale firms. The results are given in the following Table 5.4 which is

set of three Sub-tables (Table 5.4a, Table 5.4b and Table 5.4c).

Table 5.4a shows that LM test is statistical insignificant so the model specification

satisfies pooling regression without group dummy variables. From the Table 5.4b and

5.4c, it is observed that the regression equation is meaningful though R&D has an

insignificant relationship with profit margin. The coefficient of GFAS of the last period

has a significant impact on profit margin. From the growth rate of gross fixed asset (Table

4.12), for the medium scale firms the result is negatively significant in the case of

performance. This is because if the GFA of the last period increases and if they increase

plant size, then they have to bear the extra cost of production which ultimately makes loss.

125

As a result their performance decreases which is also empirically supported by the past

literature. Strickland and Weiss (1976) have observed the negative impact.

Table 5.4: Role of R&D on Profit Margin for Medium Scale Automobile Firms

Table 5.4a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression on

Profit Margin for Medium Scale Automobile Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .435777D+00

Var[u] = .220178D-01 Corr [v(it),v(is)] = .048095

Lagrange Multiplier Test vs. Model (3) = .03 (1 df, prob value = .863941) (High values of LM favor FEM/REM over CR model.)

Fixed vs. Random Effects (Hausman) = 4.93 (2 df, prob value = .084958) (High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .445046D+00

Var[u] = .390018D-01 Sum of Squares .529149D+02

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

126

Table 5.4b: ANOVA of the Regression of Profit Margin for Medium Scale Automobile Firms

OLS Without Group Dummy Variables

Ordinary least squares regression Weighting variable = none

Dep. var. = PM it Mean= -.8112575389E-01, S.D.= .6922310975

Model size: Observations = 118, Parameters = 3, Deg.Fr.= 115

Residuals: Sum of squares= 52.64637328 , Std.Dev.= .67661, R-squared= .060968, Adjusted R-squared = .04464 Model test: F[ 2, 115] = 3.73, Prob value = .02686

Diagnostic: Log-L = -119.8166, Restricted(b=0) Log-L = -123.5280

LogAmemiyaPrCrt.= -.756, Akaike Info. Crt.= 2.082

Panel Data Analysis of PM [ONE way]

Unconditional ANOVA (No regressors)

Source Variation Deg. Free. Mean Square

Between 2.58507 6. .430845

Residual 53.4794 111. .481797

Total 56.0645 117. .479184

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

Table 5.4c: Estimated coefficients of the Regression on Profit Margin for Medium Scale

Automobile Firms

Variable Coefficient Standard Error t-ratio P[|T|>t]

RDSi t-1 -1.830701248 6.5106477 -.281 .7791

GFASit-1 -.3593216693 .13255927 -2.711 .0077

Constant .1349466672 .10291659 1.311 .1924

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

5.1.3: Role of R&D of the Small Scale Indian Automobile Industry

In the case of small scale automobile firms, the cost reducing role of R&D and

performance promoting role of R&D is discussed sequentially in the following.

127

Cost reducing role of Small scale firms in the Automobile Industry

To examine the cost reducing role, a same type of specification of cost margin

(CM) have been considered like large scale and medium scale firms and analysed on the

basis of findings in the given Table 5.5. Table 5.5 consists with a set of three sub tables

(Table 5.5a, Table 5.5b, and Table 5.5c).

Table 5.5a shows that LM test is statistical insignificant so the model specification

satisfies pooling regression without group dummy variables.

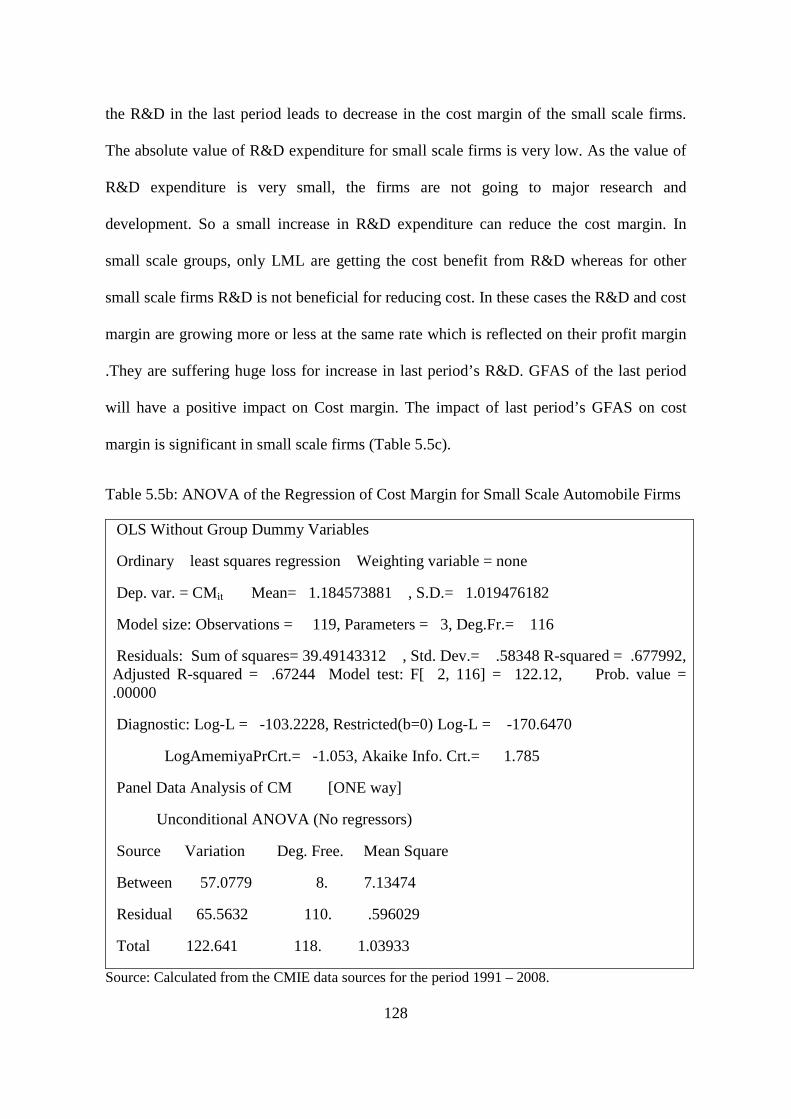

Table 5.5: Role of R&D on Cost Margin for Small Scale Automobile Firms

Table 5.5a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression on

Cost Margin for Small Scale Automobile Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .311421D+00

Var[u] = .204399D-01 Corr[v(it),v(is)] = .061592

Lagrange Multiplier Test vs. Model (3) = 1.29 ( 1 df, prob value = .255960) (High values of LM favor FEM/REM over CR model.)

( Fixed vs. Random Effects (Hausman) = 3.77 ( 2 df, prob value = .152070) (High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .349806D+00

Var[u] = -.277434D-01 Sum of Squares .397513D+02

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

It is observed from the Table 5.5b that the regression specification is meaningful as

the high value of F statistic and high degree of measurement of goodness of fit. Table 5.5c

explores the findings. In case of cost reducing role of R&D, it is found that an increase in

128

the R&D in the last period leads to decrease in the cost margin of the small scale firms.

The absolute value of R&D expenditure for small scale firms is very low. As the value of

R&D expenditure is very small, the firms are not going to major research and

development. So a small increase in R&D expenditure can reduce the cost margin. In

small scale groups, only LML are getting the cost benefit from R&D whereas for other

small scale firms R&D is not beneficial for reducing cost. In these cases the R&D and cost

margin are growing more or less at the same rate which is reflected on their profit margin

.They are suffering huge loss for increase in last period’s R&D. GFAS of the last period

will have a positive impact on Cost margin. The impact of last period’s GFAS on cost

margin is significant in small scale firms (Table 5.5c).

Table 5.5b: ANOVA of the Regression of Cost Margin for Small Scale Automobile Firms

OLS Without Group Dummy Variables

Ordinary least squares regression Weighting variable = none

Dep. var. = CMit Mean= 1.184573881 , S.D.= 1.019476182

Model size: Observations = 119, Parameters = 3, Deg.Fr.= 116

Residuals: Sum of squares= 39.49143312 , Std. Dev.= .58348 R-squared = .677992, Adjusted R-squared = .67244 Model test: F[ 2, 116] = 122.12, Prob. value = .00000

Diagnostic: Log-L = -103.2228, Restricted(b=0) Log-L = -170.6470

LogAmemiyaPrCrt.= -1.053, Akaike Info. Crt.= 1.785

Panel Data Analysis of CM [ONE way]

Unconditional ANOVA (No regressors)

Source Variation Deg. Free. Mean Square

Between 57.0779 8. 7.13474

Residual 65.5632 110. .596029

Total 122.641 118. 1.03933

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

129

Table 5.5c: Estimated coefficients of the Regression on Cost Margin for Small Scale

Automobile Firms

Variable Coefficient Standard Error t-ratio P[|T|>t] |

RDSit-1 -34.59117992 4.5874701 -7.540 .0000

GFASit-1 .2377323827 .30264229E-01 7.855 .0000

Constant .9909995787 .57176970E-01 17.332 .0000

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

Performance promoting role of R&D of Small Scale firms in Automobile Industry

To analyse the performance promoting role same specification of profit margin

(PM) have been considered which is already mentioned for large and medium scale of

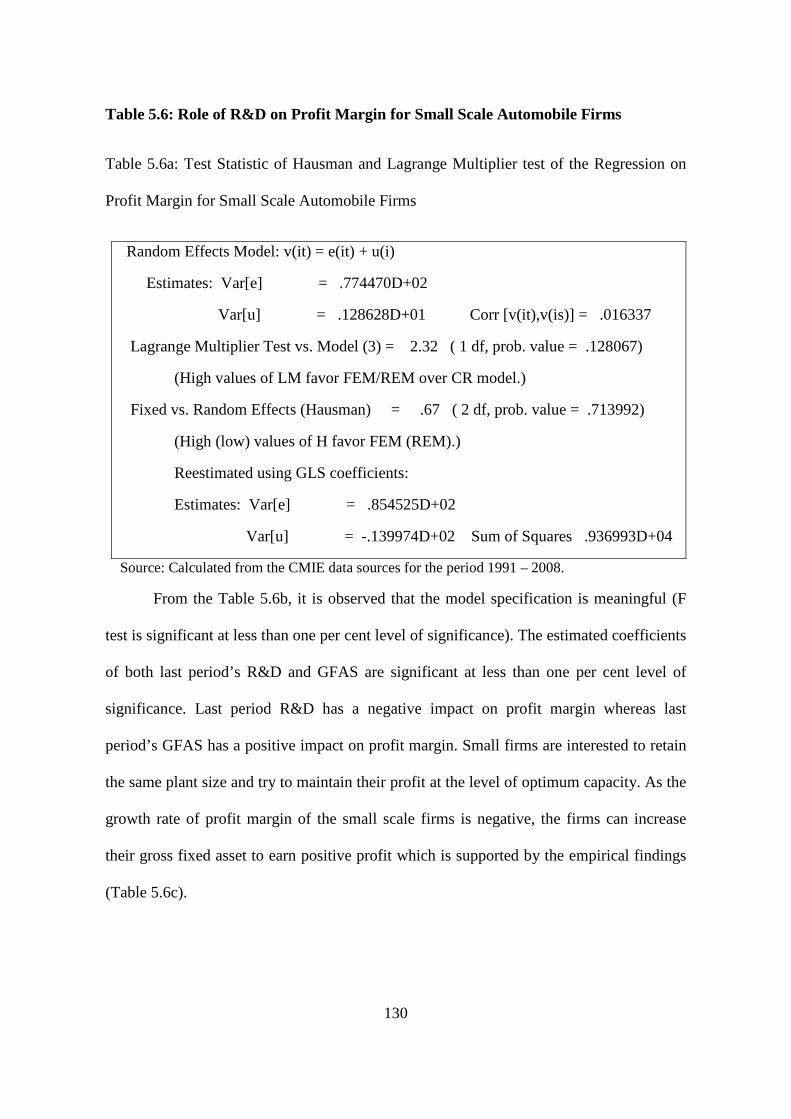

firms. The result for this specification is given in the following Table 5.6. Table 5.6

consists with a set of three sub tables (Table 5.6a, Table 5.6b and Table 5.6c).

Table 5.6a shows that LM test is statistical insignificant (as the value of LM

statistic is low) so the model specification satisfies pooling regression without group

dummy variables.

130

Table 5.6: Role of R&D on Profit Margin for Small Scale Automobile Firms

Table 5.6a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression on

Profit Margin for Small Scale Automobile Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .774470D+02

Var[u] = .128628D+01 Corr [v(it),v(is)] = .016337

Lagrange Multiplier Test vs. Model (3) = 2.32 ( 1 df, prob. value = .128067)

(High values of LM favor FEM/REM over CR model.)

Fixed vs. Random Effects (Hausman) = .67 ( 2 df, prob. value = .713992)

(High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .854525D+02

Var[u] = -.139974D+02 Sum of Squares .936993D+04

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

From the Table 5.6b, it is observed that the model specification is meaningful (F

test is significant at less than one per cent level of significance). The estimated coefficients

of both last period’s R&D and GFAS are significant at less than one per cent level of

significance. Last period R&D has a negative impact on profit margin whereas last

period’s GFAS has a positive impact on profit margin. Small firms are interested to retain

the same plant size and try to maintain their profit at the level of optimum capacity. As the

growth rate of profit margin of the small scale firms is negative, the firms can increase

their gross fixed asset to earn positive profit which is supported by the empirical findings

(Table 5.6c).

131

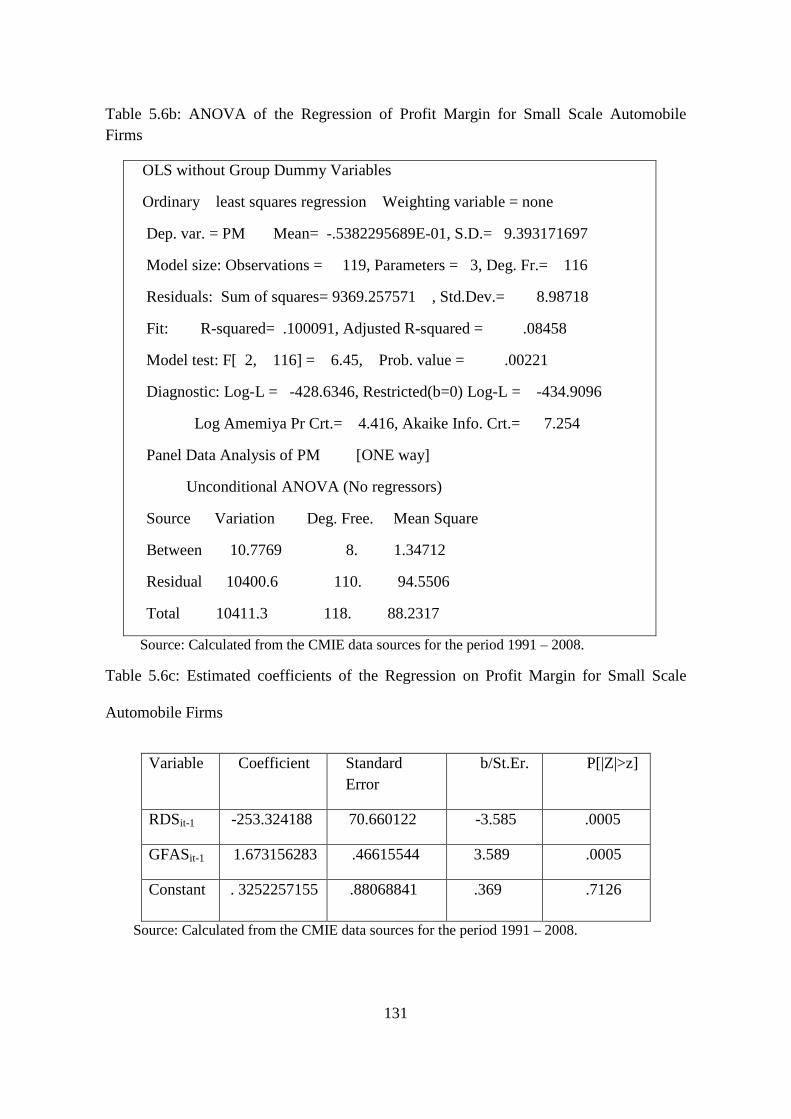

Table 5.6b: ANOVA of the Regression of Profit Margin for Small Scale Automobile Firms

OLS without Group Dummy Variables

Ordinary least squares regression Weighting variable = none

Dep. var. = PM Mean= -.5382295689E-01, S.D.= 9.393171697

Model size: Observations = 119, Parameters = 3, Deg. Fr.= 116

Residuals: Sum of squares= 9369.257571 , Std.Dev.= 8.98718

Fit: R-squared= .100091, Adjusted R-squared = .08458

Model test: F[ 2, 116] = 6.45, Prob. value = .00221

Diagnostic: Log-L = -428.6346, Restricted(b=0) Log-L = -434.9096

Log Amemiya Pr Crt.= 4.416, Akaike Info. Crt.= 7.254

Panel Data Analysis of PM [ONE way]

Unconditional ANOVA (No regressors)

Source Variation Deg. Free. Mean Square

Between 10.7769 8. 1.34712

Residual 10400.6 110. 94.5506

Total 10411.3 118. 88.2317

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

Table 5.6c: Estimated coefficients of the Regression on Profit Margin for Small Scale

Automobile Firms

Variable Coefficient Standard Error

b/St.Er. P[|Z|>z]

RDSit-1 -253.324188 70.660122 -3.585 .0005

GFASit-1 1.673156283 .46615544 3.589 .0005

Constant . 3252257155 .88068841 .369 .7126

Source: Calculated from the CMIE data sources for the period 1991 – 2008.

132

An Aggregative and Comparative Analysis of the Role of R&D on different scale of

firms in Automobile Industry

From the comparison Tables 5.7, it is found that R&D of the last period in the

industry as a whole has a significant negative impact on cost margin of the current period.

It implies that increase in R&D of the last period will decrease the cost for the entire

industry. But, for large scale firms the impact is positive because, firms’ behaviours are

different in the industry and that may due to heterogeneous nature and different size. Large

scale firms are going for major innovation and medium and small scale firms are going for

minor innovation ie; the pattern of R&D are different due to different financial strength.

GFAS of the last period will have a positive impact on Cost margin. Increase in GFA

implies that the company will go for purchasing more intangible assets, land, building,

plant and machinery which will ultimately increase the cost structure which is

theoretically justified. The impact of last period’s GFAS on cost margin is significant and

higher in large scale firms (Table 5.7).

133

Table 5.7: Comparison of the Role of R&D on Cost Margin of different scale of firms

in Automobile Industry

Firm’s size Constant RDSit-1 GFASit-1 Modela

Total .884*

(44.58)

-6.74*

(-4.62)

.0542*

(5.69)

OLS

Large scale 2.92*

(8.21)

.073**

(1.81)

Fixed effect model

Medium scale

.873*

(31.71)

.738

(.423)

.0238

(.671)

OLS

Small scale .991*

(17.33)

-34.59*

(-7.54)

.238*

(7.85)

OLS

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

Note: Parentheses shows the t-values for the coefficient

* denotes the level of significance at 1% or less than 1% level of significance

a Fixed effect and Random effect model depends on the value of Hausman test statistics and Least Square Dummy variable (LSDV) and Least Square without Dummy variable (LSWDV) model depends on the value of LM test statistic.

Table 5.8 reveals the comparative analysis of the role of research and development in

the automobile industry. For the performance promoting role of R&D, it is observed that

last period’s R&D has a negative impact on profit margin for the industry as a whole

though only for large scale of firms this impact is positive. From the micro level study, it

is observed that only large scale firms are consistently emphasised on innovation and

spend huge amount of money on research and development; whereas medium scale firms

and small scale firm are not consistent on that part and that reflects on their impact.

134

Table 5.8: Comparison of the Role of R&D on Performance of the different scale of

firms in Automobile Industry

Firm’s size Constant RDSit-1 GFASit-1 Modela

Total -79.15*

(-3.57)

.528*

(3.61)

Fixed effect model

Large scale .828*

(7.32)

.774*

(4.90)

-.109*

(-6.40)

Random effect model

Medium scale

.134

(1.31)

-1.83

(-.281)

-.359*

(-2.71)

OLS

Small scale .325

(.369)

-253.32*

(-3.58)

1.67*

(3.58.)

OLS

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

Note: Parentheses shows the t-values for the coefficient

*denotes the level of significance at 1% or less than 1% level of significance

**denotes the level of significance at 5% or less than 5% level of significance

The impact of last period’s GFAS on profit margin for the industry as a whole is

positive and significant though it is negatively significant for large and medium scale

firms. Domowitz et al. (1986) have observed also the positive impact for all industries by

considering cross-section and time series data. The patterns of investment on their gross

fixed assets are different for different scale of firms. So, immediate impact of gross fixed

assets on profit is negative for some firms as per their motive of capturing more market

share in the long run. Strickland and Weiss (1976) have observed the negative relation. So,

both the positive and negative impact of GFAS on profit margin is theoretically justified.

135

5.2: Role of R&D in Indian Drugs and Pharmaceuticals Industry

The pharmaceutical industry is one of the most R&D intensive sectors and the

R&D activities involve scientific research in emerging or unexplored fields. Earlier, the

Indian pharmaceutical industry spent very little on R&D. In the early 1990s, its R&D

expenditures amounted to only about 1.5 per cent of sales (Grace 2004, p. 37). Even larger

companies such as Ranbaxy and Dr. Reddy’s Laboratories spent only 2-3 per cent of their

sales on R&D in 1992-93. Since then, however, and particularly since the early 2000s,

there has been a substantial increase in spending on research in a segment of the industry.

Ranbaxy is the largest R&D spender in the Indian pharmaceutical industry. In 1994-95,

when TRIPS came into effect, it spent Rs. 365.8 million on R&D (4.61 per cent of its

sales). Dr. Reddy’s, the second largest R&D spender, expenditure increased steadily and

sharply from Rs 39.8 million (2.01 per cent of sales) in 1994-95 to Rs 2977.9 (17. 12 per

cent) in 2004-05. The larger Indian pharmaceutical companies are among the largest

investors in R&D among all industries combined in India. Each of the top five R&D

spenders in corporate India are pharmaceutical companies - Ranbaxy, Dr. Reddy’s

Laboratories, and Cipla Ltd. (Choudhuri 2007). It comes along with a lot of risk as the

research may or may not ultimately lead to a commercial product. The pharmaceutical

industry is mainly driven by the growing expectations of the consumer and the rising cost

of developing new products. All pharmaceutical companies want to reduce their R&D

costs and are under extreme pressure to develop new drugs. To economize R&D and to

reduce the lead-time for development of new drug, many companies have sought alliance

partners with breading-edge technologies and expertise in particular fields as a way to

outsource R&D activities. The R&D function among the Indian pharmaceuticals

companies is at a very promising stage. Even well established companies spend as low as

136

2.5 per cent of their total turnover towards R&D expenses. Signing of the recent WTO

agreement by India facilitates the recognition of product patents. To counter this regime,

domestic players have initiated investment on research. But, it is important to know the

research which is the most important part of drugs and pharmaceuticals industry that

whether it is cost reducing or performance promoting. To have a brief idea about the role

of R&D in the drugs and pharmaceuticals industry, it is important know about the role of

R&D expenditure in the case of some pharmaceuticals companies.

When the first Cipla products were ready for the market in September 1937, The

Sunday Standard predicted that “with intelligent direction and skilful production, (Cipla)

bids fair to establish a great reputation in the East”. Indeed, the company’s reputation has

gone beyond the East. From a quiet beginning, today Cipla Ltd. is well known

internationally by doctors and patients alike, in most countries across the globe. Cipla Ltd.

has achieved an overall growth of about eight per cent in turnover during the year 2009-

10. Domestic growth was steady at ten per cent. According to ORG-IMS Statistics of

drugs, Cipla remained the leader in the domestic market, as on 31st March 2010 with a

market share of 5.38 per cent. However, growth in formulation exports was affected due to

various factors including non-availability of important raw materials, lower tender

business in anti-retroviral and unfavourable movements in foreign exchange rate. The

Company introduced many new drugs and formulations during that year. The Company

will continue its R&D efforts in the various areas indicated in above. The major thrust

would be on developing new products and drug delivery systems. The total R&D

expenditure as a percentage of total turnover is around five per cent13.

13

Annual Report 2009-10 of Cipla Ltd.

137

Dr. Reddy's Laboratories Ltd. founded in 1984 with $160,000. Dr. Reddy’s was

the first Asia-Pacific pharmaceutical outside of Japan and the sixth Indian company to be

listed on the New York Stock Exchange. It earned $446 million in fiscal year 2005,

deriving 66 per cent of this income from the foreign market. In order to strengthen its

global position Dr. Reddy acquired UK-based BMS Laboratories and subsidiary Meridian

Healthcare. Although 58 per cent of Dr. Reddy’s revenues come from generic drugs, the

company was committed to WTO-compliance long before the 2005 bill took effect, and

most of these products were already off patent. Dr. Reddy has long been a research-

oriented firm, preceding many of its peers in setting up a New Drug Development

Research (NDDR) in 1993 and out-licensing its first compound just four years later. Dr.

Reddy’s has since out licensed two more molecules and currently has three others in

clinical trials.

Glaxo Smith Kline continues to be committed to research and development of

medicines that will improve the quality of life of people around the world and that truly

make a difference to patients. The Clinical Operations group in India, which conducts

clinical studies across a number of disease areas ranging from cancer, iron deficiency

anaemia, coronary heart disease, osteoporosis, malaria, supports this global and local

effort. The company maintained its leadership position in the pharmaceuticals market with

Net Sales (net of Excise Duty), registering a growth of 12.9 per cent. Sales performance in

all of the company’s diversified business units ie; in the mass market and mass specialty

segments, dermatological, oncology, critical care and vaccines helped to support sales

growth. The company is engaged in conducting 22 clinical trials of which seven were

initiated in 2010. A total of 216 patients participated in these studies. Most of the clinical

studies initiated in 2010 were in oncology. The company has trained more than 165

138

investigators at 73 clinical trial sites across India. Quality continues to be the key priority,

and is evidenced by a number of successful internal compliance audits. In order to support

the launch of new drugs that would benefit and improve the quality of life of the patients

suffering from various diseases, the company submitted seven NDAs (New Drug

Applications) for various products including vaccines and two IND (Investigational New

Drug) applications to the CDSCO (Central Drugs Standard Control Organization) under

the Ministry of Health and Family Welfare, Government of India. The company has

received approval for six NDAs and one IND from CDSCO, which paves the way for

speedy introduction of new drugs. Additionally, to support the R&D efforts of Glaxo

Smith Kline, the company submitted six global Clinical Trial applications to the CDSCO

and have been granted approval to conduct three studies on the Indian population through

the Clinical Operations group in India. Some of the novel innovative products for oral use,

approved by the regulatory agency in India during the year under review, include

pazopanib (Votrient) an oncology product for the treatment of advanced renal cell

carcinoma, eltrombopag (Revolade) for the treatment of immune thrombocytopenia (ITP),

and ambrisentan (Volibris) for the treatment of pulmonary arterial hypertension. In

addition, a new indication approved for the existing oncology product lapatinib (Tykerb)

in combination with letrozole will be beneficial for Indian patients with metastatic breast

cancer. Efforts towards ensuring a speedy review and approval by regulatory authorities

for these products will help achieve early access to new and innovative therapeutic options

to patients in the country14.

Piramal Healthcare continues to conduct Research and Development related to

pre-formulation and formulation development and clinical manufacturing of NCE’s for

14 Annual Report of Glaxo Smith Kline Ltd. 2010.

139

external clients; Process optimization, research and scale up, for the early phase projects

from clients. Total R&D expenditure during the year was Rs. 413.2 million.15 Due to this

R&D, there is cost effective development of formulations for global pharmaceutical

companies, thus bringing in more molecules into the global pipeline. Support of the new

“network” paradigm of the global innovator in pharmaceutical industry is thereby putting

India in the crux of this industrial culture change. Total R&D expenditure as a percentage

to sales is 2.60 per cent.16

Ranbaxy Laboratories Ltd is the leader in the Indian pharmaceutical market, taking

in $1.174 billion in revenues for a net profit of $160 million in 2004. It was the first Indian

pharmaceutical to have a proprietary drug (extended-release Ciprofloxacin, marketed by

Bayer) approved by the U.S. FDA (Food and Drug Administration), and the U.S. market

accounts for 36 per cent of its sales. 78 per cent of Ranbaxy’s sales are from overseas

markets; its offices in 44 countries manage manufacturing in seven countries and

distribution in over 100. IMS Health estimated that Ranbaxy is among the top 100

pharmaceuticals in the world and that it is the 15th fastest growing company. By 2012,

Ranbaxy hopes to be one of the top five generics producers in the world, and it

consolidated its position with the purchase of French firm RGP Aventis in 2003. Ranbaxy

also has higher aspirations, however, “to build a proprietary prescription business in the

advanced markets.” To this end, it keeps a dedicated research facility in Gurgaon staffed

with over 1100 scientists. They currently have two molecules in Phase II trials and 3-5 in

pre-clinical testing. It spent $75 million in R&D in 2004, a 43 per cent increase over its

15 Annual Report of Piramal Health Care Ltd. 2010-11.

16 Annual report 2010-11 of Piramal Healthcare Ltd.

140

2003 expenditure. Ranbaxy has achieved a growth of 75 per cent of its turnover (Sales +

Services Rendered), reaching a value of € 3.190.826 (in Rs. 192,2184,434)17.

The role of R&D is whether cost reducing or performance promoting in the case of

drugs and pharmaceuticals industry is discussed scale wise sequentially in the following.

5.2.1: Role of R&D of Large Scale firms in the Indian Drugs and Pharmaceutical

Industry

As the large scale firms are the leader firms of the drugs and pharmaceuticals

industry, so it is important to know the role of R&D in case of cost margin as well as

profit margin. These two roles of research and development of the large scale drugs and

pharmaceutical firms are analysed in the following.

Cost reducing role of R&D of Large scale firms in Drugs and Pharmaceutical

Industry

To analyse the cost reducing role a specification of cost margin (CM) have been

considered which is already mentioned for all types and all scale of firms in equation (4)

under the methodology section of Chapter 3. The result for this specification is given in

the following Table 5.9. Table 5.9 consists with a set of five sub tables (Table 5.9a and

Table 5.9b).

From the Table 5.9a, it is observed that the model specification follows the random

effect model. The value of LM test is significant at less than five per cent level of

significance but the value of Hausman test is insignificant. Table 5.9b reveals that Last

period’s R&D has a positive and significant impact on current period’s cost margin. Large

17

Annual report 2010 of Ranbaxy Ltd.

141

scale firms are the leading firms and they are more interested in future performance, they

continue to invest on R&D which leads to immediate increase in cost margin of the firms.

In the group of large scale firms, some firms are getting cost margin benefit due to higher

R&D. The growth of R&D is very high whereas the growth of cost margin is negative for

the firms say Cipla Ltd, Glaxo Smith Kline Ltd. (Table 4.17). Whereas for other firms like

Dr. Reddy’s Laboratories Ltd, Piramal Healthcare Ltd. and Ranbaxy Laboratories Ltd., the

growth rate of cost margin is positive though the value is very much lower than growth of

R&D. So, R&D has some positive impact for reducing cost margin in the long run (Table

4.17).

Table 5.9: Role of R&D on Cost Margin for Large Scale Drugs and Pharmaceuticals

Firms

Table 5.9a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression of

Cost Margin for Large Scale Drugs and Pharmaceutical Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .570868D-02

Var[u] = .648047D-03 Corr [v(it),v(is)] = .101947

Lagrange Multiplier Test vs. Model (3) = 4.01 ( 1 df, prob. value = .045220)

(High values of LM favor FEM/REM over CR model.)

Fixed vs. Random Effects (Hausman) = 1.99 ( 2 df, prob. value = .369065)

(High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .573895D-02

Var[u] = .196233D-02 Sum of Squares .558455D+00

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

142

Table 5.9b: Estimated coefficients of the Regression of Cost Margin for Large Scale

Drugs and Pharmaceutical Firms

Variable Coefficient Standard Error b/St.Er. P[|Z|>z]

RDSit-1 1.033619441 .23065725 4.481 .0000

GFASit-1 -.5324820E-01 .50100461E-01 -1.063 .2879

Constant .7561726269 .26049481E-01 29.028 .0000

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

Performance promoting role of R&D of Large scale firms in Drugs and

Pharmaceutical

Industry

To analyse the performance promoting role a specification of profit margin (PM) have

been considered which is already mentioned for all types and all scale of firms in equation

(5) under the methodology section of Chapter 3. The results of this specification for large

scale firms are given in the following Table 5.10 which consist three sub-tables (Table

5.10a, Table 5.10b and Table 5.10c).

143

Table 5.10: Role of R&D on Cost Margin for Large Scale Drugs and

Pharmaceuticals Firms

Table 5.10a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression of

Profit Margin for Large Scale Drugs and Pharmaceutical Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .404990D-02

Var[u] = .161384D-03 Corr [v(it),v(is)] = .038322

Lagrange Multiplier Test vs. Model (3) = .30 ( 1 df, prob. value = .585762)

(High values of LM favor FEM/REM over CR model.)

Fixed vs. Random Effects (Hausman) = .18 ( 2 df, prob. value = .912085)

(High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .439454D-02

Var[u] = .154371D-03 Sum of Squares .379094D+00

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

Table 5.10a shows that LM test is statistical insignificant (as the value of LM

statistic is very low) so the model specification satisfies pooling regression without group

dummy variables. Table 5.10b shows the pooling regression specification is meaningful as

the F test is significance at eight per cent level of significance though the value of R-

squared is very low.

144

Table 5.10b: ANOVA of the Regression of Profit Margin for Large Scale Drugs and

Pharmaceutical Firms

OLS Without Group Dummy Variables

Ordinary least squares regression Weighting variable = none

Dep. var. = PM Mean= .1278401956 , S.D.= .6716104829E-01

Model size: Observations = 90, Parameters = 3, Deg.Fr.= 87

Residuals: Sum of squares= .3790156724 , Std.Dev.= .06600

Fit: R-squared= .055869, Adjusted R-squared = .03416

Model test: F[ 2, 87] = 2.57, Prob. value = .08202

Diagnostic: Log-L = 118.4450, Restricted(b=0) Log-L = 115.8579

Log Amemiya Pr Crt.= -5.403, Akaike Info. Crt.= -2.565

Panel Data Analysis of PM [ONE way]

Unconditional ANOVA (No regressors)

Source Variation Deg. Free. Mean Square

Between .224983E-01 4. .562457E-02

Residual .378946 85. .445818E-02

Total .401444 89. .451061E-02

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

Table 5.10c: Estimated coefficients of the Regression of Profit Margin for Large Scale

Drugs and Pharmaceutical Firms

Variable Coefficient Standard Error b/St.Er. P[|Z|>z]

RDSit-1 .3371842731 .18433319 1.829 .0708

GFASit-1 -.6052695E-01 .356215E-01 -1.699 .0929

Constant .1443555617 .17224129E-01 8.381 .0000

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

145

This is reflected in their profit margin. Profit margin increases if they invest more

money on previous year’s R&D (Table 5.10c). GFAS of the last period will have a

negative impact on profit margin. The impact of last period’s GFAS on profit margin is

significant.

From the growth rate of gross fixed asset, it is observed that all the large scale

firms are maintaining very high growth rate (Table 4.17 in Chapter 4). Theoretically, large

scale firms are interested to maintain long run performance and for that they are going not

only for purchasing machinery but also increasing plant size or purchasing land or

buildings. So immediate impact of gross fixed asset on profit are negative for large scale

firms as per their motive of capturing more market share in the long run. So the impact of

GFA on profit is theoretically justified.

Both growth rate of R&D and profit are high for large scale firms (Table 4.17 in

Chapter 4). High growth rate of the two variables indicate that R&D increases over time

and side by side firms are maintaining a positive profit margin over time. The rate of

growth of R&D is higher that growth rate of profit margin. From the regression analysis it

is also observed that if R&D of the last period increases by Rs.100 then profit margin

increases by Rs. 33.

5.2.2: Role of R&D in the Medium scale Indian Drugs and Pharmaceuticals Industry

In the case of medium scale firms, the cost reducing role of R&D and performance

promoting role of R&D is discussed in the following.

146

Cost reducing role of R&D of Medium scale firms in Drugs and Pharmaceutical

Industry

To examine cost reducing role, same specification of cost margin (CM) have been

considered like large scale firms and analysed on the basis of findings in the given Table

5.11. Table 5.11 consists with a set of two sub tables (Table 5.11a, and Table 5.11b).

Table 5.11: Role of R&D on Cost Margin for Medium Scale Drugs and

Pharmaceutical Firms

Table 5.11a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression on

Cost Margin for Medium Scale Drugs and Pharmaceutical Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .451648D-02

Var[u] = .708305D-03 Corr[v(it),v(is)] = .135566

Lagrange Multiplier Test vs. Model (3) = 31.52 ( 1 df, prob. value = .000000)

(High values of LM favor FEM/REM over CR model.)

Fixed vs. Random Effects (Hausman) = 1.31 ( 2 df, prob. value = .519792)

(High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .452287D-02

Var[u] = .979082D-03 Sum of Squares .121197D+01

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

From the Table 5.11a, it is observed that the model specification follows the

random effect model. The value of LM test is significant at less than five per cent level of

significance but the value of Hausman test is insignificant.

147

Table 5.11b: Estimated coefficients of the Regression of Cost Margin for Medium Scale

Drugs and Pharmaceutical Firms

Variable Coefficient Standard Error b/St.Er. P[|Z|>z]

RDSit-1 -.599296266 .35290176 -1.698 .0895

GFASit-1 .2008713E-01 .42060063E-01 .478 .6329

Constant .7632484830 .16198391E-01 47.119 .0000

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

It is found that an increase in the R&D in the last period leads to increase in the

cost margin of the medium scale firms (Table 5.11b). So, the immediate impact of R&D

increases next period’s cost margin. But, the growth rate of cost margin is negative in most

of the medium scale firms. Though the rate of growth of R&D is very much lower but

negative growth of cost margin implies that R&D has some positive impact for reducing

cost margin (Table 4.19).

Performance promoting role of R&D of Medium scale firms in Drugs and

Pharmaceutical Industry

To examine performance promoting role, same specification of profit margin (PM)

have been considered like large scale firms and analysed on the basis of findings in the

given Table 5.12. Table 5.12 consists with a set of two sub tables (Table 5.12a, and Table

5.12b).

148

Table 5.12: Role of R&D on Profit Margin for Medium Scale Drugs and

Pharmaceutical Firms

Table 5.12a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression on

Profit Margin for Medium Scale Drugs and Pharmaceutical Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .372287D+03

Var[u] = .694712D+01 Corr [v(it),v(is)] = .018319

Lagrange Multiplier Test vs. Model (3) = .07 ( 1 df, prob. value = .793901)

(High values of LM favor FEM/REM over CR model.)

Fixed vs. Random Effects (Hausman) = 3.39 ( 2 df, prob. value = .183877)

(High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .374739D+03

Var[u] = .100907D+02 Sum of Squares .876316D+05

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

From the Table 5.12a, it is revealed that the value of Lagrange Multiplier (LM) is

insignificant which indicates the results supports pooling regression without dummy

variable. The pooling regression equation is meaningful as the value of F statistic is

significant at one per cent level of significant (Table 5.12b). Table 5.12c reveals that past

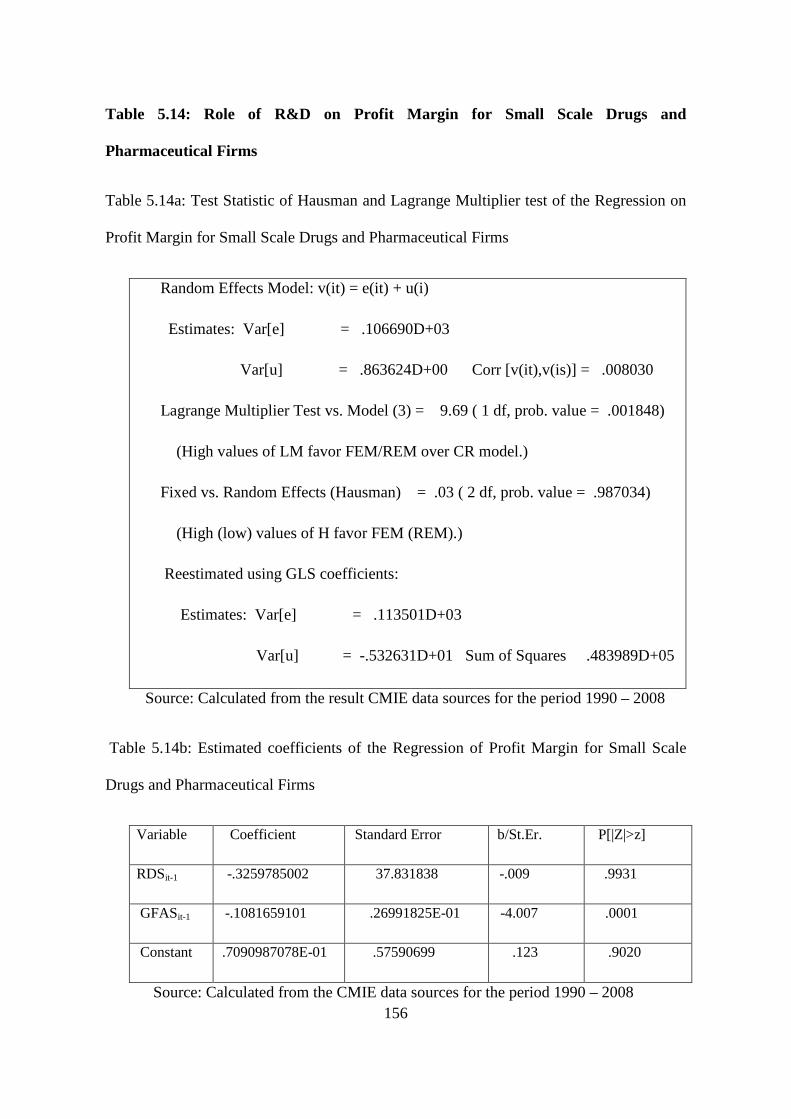

period’s R&D has no significant impact on the firms’ performance though past period’s

GFAS has a negative impact on profit margin for the medium scale drugs and

pharmaceutical firms. Medium scale firms are interested not only for purchasing

machinery but also increasing plant size or purchasing land or buildings. So, immediate

impact of gross fixed asset on profit margin is negative but significant. Strickland and

149

Weiss (1976) have observed the negative relation. So the impact of GFA on profit is

theoretically justified.

Table 5.12b: ANOVA of the Regression of Profit Margin for Medium Scale Drugs and

Pharmaceutical Firms

OLS Without Group Dummy Variables

Ordinary least squares regression Weighting variable = none

Dep. var. = PMit Mean= -1.200266195 , S.D.= 19.76152521

Model size: Observations = 234, Parameters = 3, Deg.Fr.= 231

Residuals: Sum of squares= 87603.08249 , Std. Dev.= 19.47393

Fit: R-squared = .037230, Adjusted R-squared = .02889

Model test: F[ 2, 231] = 4.47, Prob. value = .01250

Diagnostic: Log-L = -1025.2859, Restricted(b=0) Log-L = -1029.7250

Log Amemiya Prrt.= 5.951, Akaike Info. Crt.= 8.789

Panel Data Analysis of PM [ONE way]

Unconditional ANOVA (No regressors)

Source Variation Deg. Free. Mean Square

Between 4722.45 12. 393.538

Residual 86268.2 221. 390.354

Total 90990.7 233. 390.518

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

150

Table 5.12c: Estimated coefficients of the Regression of Profit Margin for Medium Scale

Drugs and Pharmaceutical Firms

Variable Coefficient Standard

Error

t-ratio P[|T|>t]

RDSit-1 6.814797584 87.323653 .078 .9379

GFASit-1 -26.00554912 9.4704184 -2.746 .0065

Constant 8.388960467 3.4582100 2.426 .0160

Source: Calculated from the CMIE data sources for the period 1990 – 2008.

5.2.3: Role of R&D in the Small scale Indian Drugs and Pharmaceuticals Industry

Both cost reducing role and performance promoting role of R&D for small scale

drugs and pharmaceutical firms is discussed sequentially in this sub-sections.

Cost reducing role of R&D of Small scale firms in Drugs and Pharmaceutical

Industry

To examine cost reducing role, same specification of cost margin (CM) have been

considered like large scale firms and medium scale firms. The findings are given in Table

5.13. Table 5.13 consists with a set of five sub tables (Table 5.13a, Table 5.13b, Table

5.13c, Table 5.13d and Table 5.13e).

151

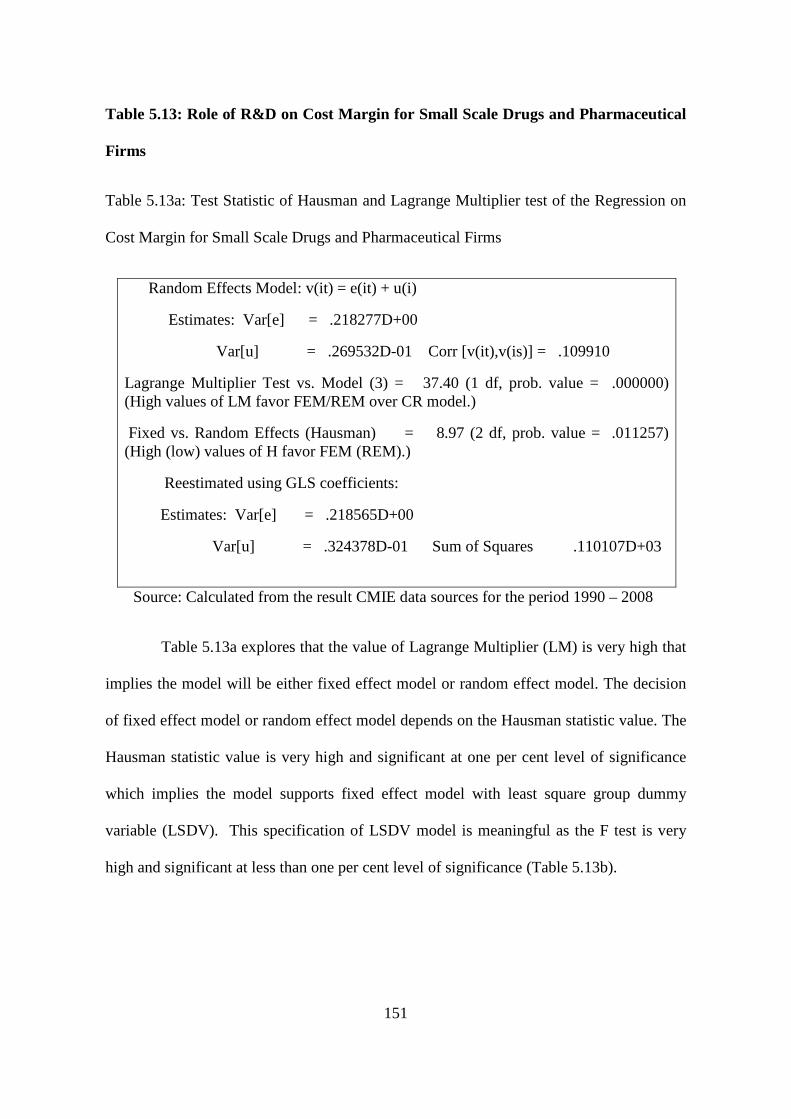

Table 5.13: Role of R&D on Cost Margin for Small Scale Drugs and Pharmaceutical

Firms

Table 5.13a: Test Statistic of Hausman and Lagrange Multiplier test of the Regression on

Cost Margin for Small Scale Drugs and Pharmaceutical Firms

Random Effects Model: v(it) = e(it) + u(i)

Estimates: Var[e] = .218277D+00

Var[u] = .269532D-01 Corr [v(it),v(is)] = .109910

Lagrange Multiplier Test vs. Model (3) = 37.40 (1 df, prob. value = .000000) (High values of LM favor FEM/REM over CR model.)

Fixed vs. Random Effects (Hausman) = 8.97 (2 df, prob. value = .011257) (High (low) values of H favor FEM (REM).)

Reestimated using GLS coefficients:

Estimates: Var[e] = .218565D+00

Var[u] = .324378D-01 Sum of Squares .110107D+03

Source: Calculated from the result CMIE data sources for the period 1990 – 2008

Table 5.13a explores that the value of Lagrange Multiplier (LM) is very high that

implies the model will be either fixed effect model or random effect model. The decision

of fixed effect model or random effect model depends on the Hausman statistic value. The

Hausman statistic value is very high and significant at one per cent level of significance

which implies the model supports fixed effect model with least square group dummy

variable (LSDV). This specification of LSDV model is meaningful as the F test is very

high and significant at less than one per cent level of significance (Table 5.13b).

152

Table 5.13b: ANOVA of the Regression of Cost Margin for Small Scale Drugs and

Pharmaceutical Firms

Least Squares with Group Dummy Variables

Ordinary least squares regression Weighting variable = none

Dep. var. = CMit Mean= .9094580965 , S.D.= .5351138786

Model size: Observations = 450, Parameters = 27, Deg.Fr.= 423

Residuals: Sum of squares= 92.33122649 , Std. Dev.= .46720

Fit: R-squared= .281859, Adjusted R-squared = .23772

Model test: F[ 26, 423] = 6.39, Prob. value = .00000

Diagnostic: Log-L = -282.1527, Restricted(b=0) Log-L = -356.6477

LogAmemiyaPrCrt.= -1.464, Akaike Info. Crt.= 1.374

Estd. Autocorrelation of e(i,t) .315516

Source: Calculated from the result CMIE data sources for the period 1990 – 2008

Table 5.13c: Estimated coefficients of the Regression of Cost Margin for Small Scale

Drugs and Pharmaceutical Firms

Variable Coefficient Standard Error t-ratio P[|T|>t]

RDSit-1 2.292675659 1.9465428 1.178 .2395

GFASit-1 .86301518E-02 .13180932E-02 6.547 .0000

Source: Calculated from the result CMIE data sources for the period 1990 – 2008

Table 5.13c reveals that past period’s R&D has no significant impact on the firms’