CHAPTER 5 RESEARCH METHODOLOGY -...

39

CHAPTER 5 RESEARCH METHODOLOGY The sample for the study, research instruments, data collection and analysis, are discussed in detail in this chapter. The researcher accessed the internet and searched for these terms: Accounting Standards, International Accounting Standards, International Financial Reporting Standards and Generally Accepted Accounting Principles. Based upon the hits each relevant item was read and reviewed for its contribution to the research subject. 5.1. Research Design Research design indicates a plan of action to be carried out in connection with a proposed research work. The process of research design includes the selection of the research problem, the presentation of the problem, the formulation of hypothesis, conceptual clarity, methodology, and data collection, testing of the hypothesis, interpretation, presentation and the like. The study carried out with four different segregate based on the objectives of study and for each segregate different hypothesis has been designed and on that bases data was collected and analysed. 57

Transcript of CHAPTER 5 RESEARCH METHODOLOGY -...

CHAPTER 5

RESEARCH METHODOLOGY

The sample for the study, research instruments, data collection and analysis, are

discussed in detail in this chapter.

The researcher accessed the internet and searched for these terms: Accounting

Standards, International Accounting Standards, International Financial Reporting

Standards and Generally Accepted Accounting Principles. Based upon the hits each

relevant item was read and reviewed for its contribution to the research subject.

5.1. Research Design

Research design indicates a plan of action to be carried out in connection with a

proposed research work. The process of research design includes the selection of the

research problem, the presentation of the problem, the formulation of hypothesis,

conceptual clarity, methodology, and data collection, testing of the hypothesis,

interpretation, presentation and the like.

The study carried out with four different segregate based on the objectives of study

and for each segregate different hypothesis has been designed and on that bases data

was collected and analysed.

57

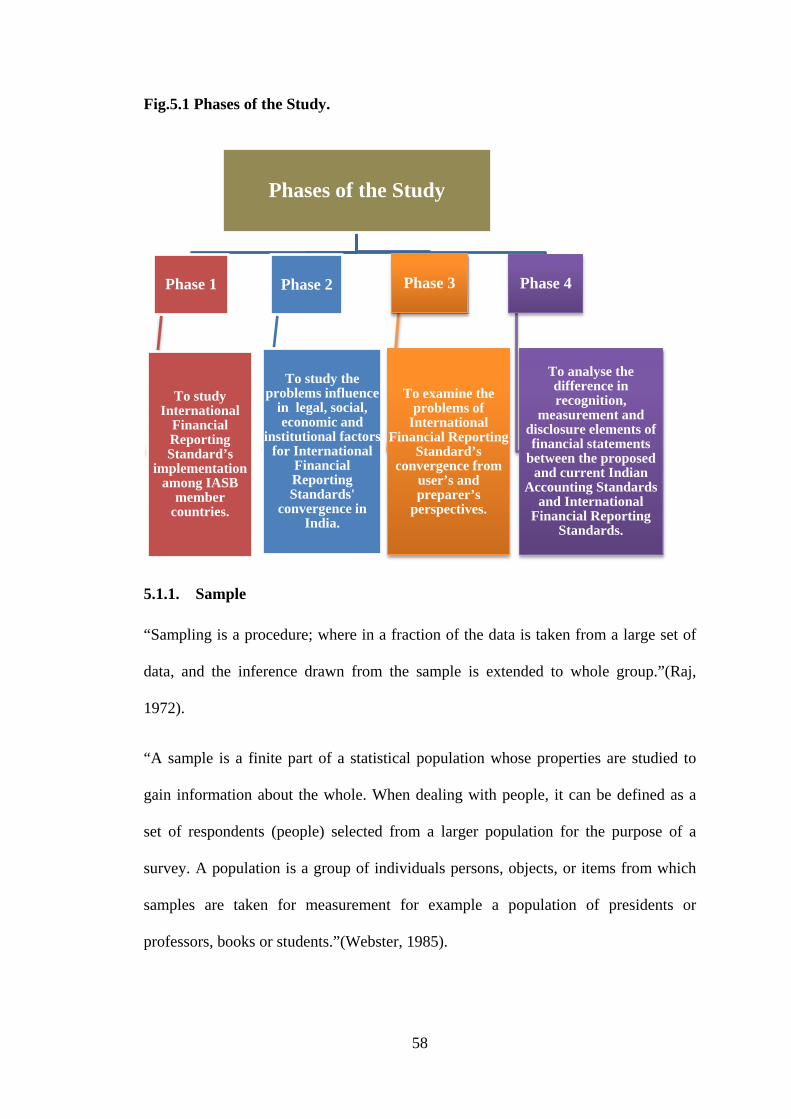

Fig.5.1 Phases of the Study.

5.1.1. Sample

“Sampling is a procedure; where in a fraction of the data is taken from a large set of

data, and the inference drawn from the sample is extended to whole group.”(Raj,

1972).

“A sample is a finite part of a statistical population whose properties are studied to

gain information about the whole. When dealing with people, it can be defined as a

set of respondents (people) selected from a larger population for the purpose of a

survey. A population is a group of individuals persons, objects, or items from which

samples are taken for measurement for example a population of presidents or

professors, books or students.”(Webster, 1985).

Phases of the Study

Phase 1

To study International

Financial Reporting Standard’s

implementation among IASB

member countries.

Phase 2

To study the problems influence

in legal, social, economic and

institutional factors for International

Financial Reporting Standards'

convergence in India.

Phase 3

To examine the problems of

International Financial Reporting

Standard’s convergence from

user’s and preparer’s

perspectives.

Phase 4

To analyse the difference in recognition,

measurement and disclosure elements of financial statements

between the proposed and current Indian

Accounting Standards and International

Financial Reporting Standards.

58

“A sample design is a definite plan for obtaining a sample from a given population. It

refers to the technique or the procedure the researcher would adopt in selecting items

for the sample. Sample design may as well lay down the number of items to be

included in the sample i.e., the size of the sample. Sample design is determined before

data are collected.”(Kothari, 2004).

The sample for this study was segregated into four phases according to previous

figure (Fig.5.1), first phase was IASB member countries, second phase deals with

problems influence in legal, social, economic and institutional factors for International

Financial Reporting Standards’ convergence in India third phase involved with

problems of International Financial Reporting Standards’ convergence from user’s

and preparer’s prospective and finally fourth phase refers to difference in recognition,

measurement and disclosure elements of financial statements between the proposed

and current Indian Accounting Standards and International Financial Reporting

Standards. Both primary and secondary data has been used in this study.

59

Fig.5.2 Phases of the Data Collections.

• Phase 1

5.2. Population of IASB Member Countries:

The Population of 123 IASB member countries are universe and it’s divided this in to

three parts converging countries, adopting countries and non adopting countries .It is a

qualitative data which is given directly in IASB web site and they are defined by

using of the designed questionnaire content of four factors of IFRS implementation.

The first factor was, commitment to global financial reporting standards which

consists of four questions, the second factor is jurisdiction for domestic companies

with debt or equity in public market which consists of six questions the third factor

refers to IFRS endorsement which consists of six questions and fourth factor is

translation of IFRS which consists of five questions. Thus twenty one questions are

formed in four parts.

SAMPLES

Phase 1 IASB Member

Countries N=100

Adpting Countries N=49

Converging Countries

N=41

Not-Adopting Countries

N=10

Phase 2 Respondents

N=384

Stakeholders N=384

Phase 3 Preparers & Users

N=385

Preparers N=200

Users N=185

Phase 4

IFRS/IND AS

IFRS/Indian GAAP

60

5.2.1. Sample of IASB Member Countries:

The frame consists of three categories; countries are in convergence process and

countries in adoption process and non-adopted countries. The sample 100 countries

has been selected for the study in three categories, sample of 49 countries in adoption

sample of 41 countries in convergence process and sample of 10 non-adopted

countries was select according to Morgan Sampling table based on judgment

sampling method.

Fig 5.3 Classification of IASB Member Countries:

IASB Member Countries

Adopting Countries

Converging Countries

Non-Adopting Countries

61

Table 5.1 The Sample of IASB Member Countries.

Countries

Sl.No Adopting Converging Non-Adopting

1. Chile Albania Bhutan

2. Costa-Rica Austria Brunei

Darussalam

3. Croatia China Cayman

4. Cyprus Colombia Egypt

5. Czech Republic Denmark Guinea

6. Dominican-Republic Ecuador Indonesia

7. El-Salvador Fiji Macao

8. Estonia Hungary Madagascar

9. Finland Iceland Thailand

10. France India Niger

11. Georgia Israel

12. Germany Japan

13. Ghana Liechtenstein

14. Greece Lithuania

15. Grenada Malaysia

16. Guatemala Malta

17. Honduras Mauritius

18. Hong Kong Mexico

19. Iraq Moldova

20. Ireland Mongolia

21. Italy Montserrat

22. Jamaica Myanmar

23. Kenya Netherlands

24. Korea New Zealand

25. Kosovo Norway

26. Latvia Pakistan

27. Lesotho Portugal

62

28. Luxembourg Romania

29. Macedonia Russia

30. Maldives Saudi Arabia

31. Oman Singapore

32. Paraguay Slovakia

33. Poland Switzerland

34. Rwanda Taiwan

35. Serbia Turkey

36. South Africa Uganda

37. Slovenia Ukraine

38. Spain United-Arab-Emirates

39. Sri Lanka United States of

America

40. St-Kitts-and-Nevis Uzbekistan

41. St-Lucia Venezuela

42. St-Vincent & the

Grenadi

43. Swaziland

44. Sweden

45. Tanzania

46. United Kingdom

47. Uruguay

48. Zambia

49. Zimbabwe

N 49 41 10

Total 100

(Source: Survey Data)

63

5.2.2. Adopting Countries:

IFRS began as an attempt to harmonize accounting across the European Union. But

the value of harmonization quickly made the concept attractive around the world,

IFRS adopted countries consist of 49 countries.

5.2.3. Converging Countries:

In general terms, ‘convergence’ means to achieve harmony with IFRSs; in precise

terms convergence can be considered “to design and maintain national accounting

standards in a way that financial statements prepared in accordance with national

accounting standards draw unreserved statement of compliance with IFRSs”. IFRS

converging countries consist of 41 countries.

5.2.4. Non- Adopting Countries:

Non-Adopting countries refers to those countries which are neither in convergence

nor in adoption countries and did not apply for global harmonization of their

accounting standards yet in formal way IFRS adopted countries consist of 10

countries.

Table 5.2 Sample of IASB Member Countries.

IASB member countries N %

Converging Countries 41 41%

Adoption Countries 49 49%

Non Adoption Countries 10 10%

Total 100 100%

(Source: Survey Data)

64

Fig.5.4 Sample of IASB Member Countries.

5.3. Sample of Individual Respondents

The sample of individual respondents was segregated into two phases. First phase is

the sample of individual respondents (stakeholders) and the second phase involved

with problems of International Financial Reporting Standards’ convergence from

user’s and preparer’s prospective.

Fig 5.5 Sample of Individual Respondents.

Converging 41%

Adoption 49%

Non Adoption 10%

Sample of Individual Respondents

Stakeholders N=384

Users & Preparers

Preparers N=200

Users N=185

65

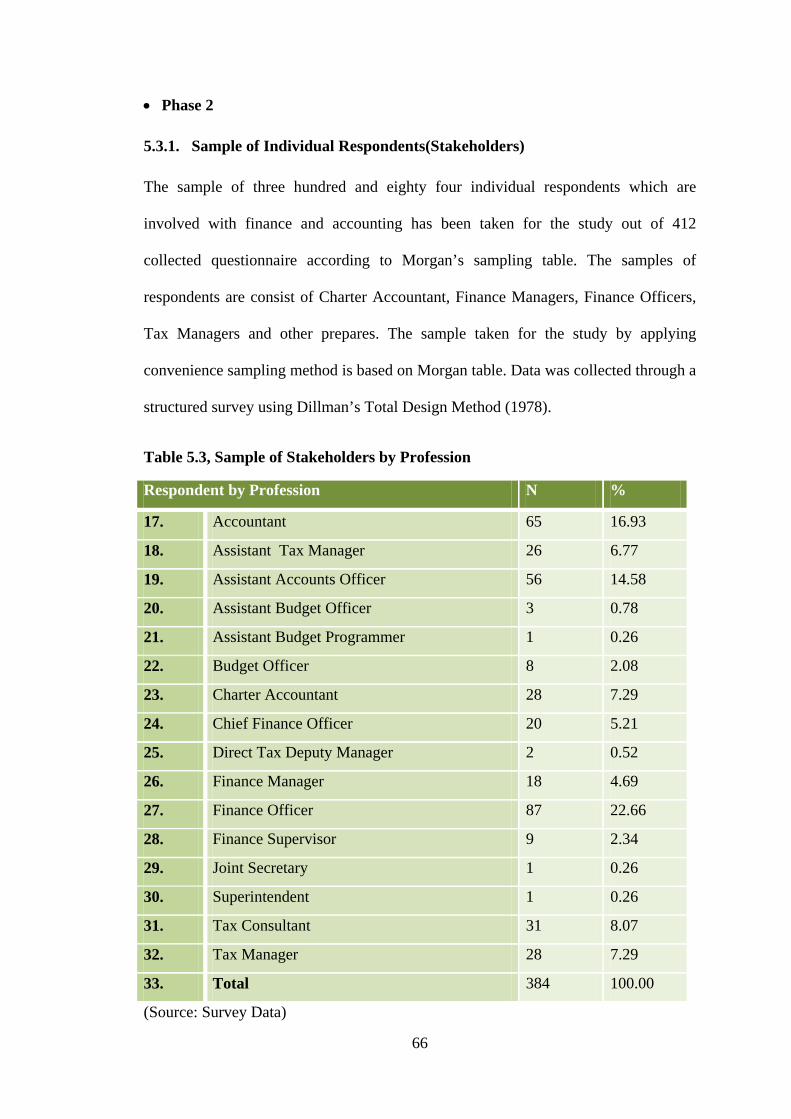

• Phase 2

5.3.1. Sample of Individual Respondents(Stakeholders)

The sample of three hundred and eighty four individual respondents which are

involved with finance and accounting has been taken for the study out of 412

collected questionnaire according to Morgan’s sampling table. The samples of

respondents are consist of Charter Accountant, Finance Managers, Finance Officers,

Tax Managers and other prepares. The sample taken for the study by applying

convenience sampling method is based on Morgan table. Data was collected through a

structured survey using Dillman’s Total Design Method (1978).

Table 5.3, Sample of Stakeholders by Profession

Respondent by Profession N %

17. Accountant 65 16.93

18. Assistant Tax Manager 26 6.77

19. Assistant Accounts Officer 56 14.58

20. Assistant Budget Officer 3 0.78

21. Assistant Budget Programmer 1 0.26

22. Budget Officer 8 2.08

23. Charter Accountant 28 7.29

24. Chief Finance Officer 20 5.21

25. Direct Tax Deputy Manager 2 0.52

26. Finance Manager 18 4.69

27. Finance Officer 87 22.66

28. Finance Supervisor 9 2.34

29. Joint Secretary 1 0.26

30. Superintendent 1 0.26

31. Tax Consultant 31 8.07

32. Tax Manager 28 7.29

33. Total 384 100.00

(Source: Survey Data)

66

As seen in the table 5.6, 16 group of professional respondents, respond to the

questionnaire and they has been selected according to Morgan table based on

convenience sampling method.

Fig 5.6 Sample of Stakeholders by Profession

From the above table 5.6, it has been seen that the sample consisted of 384

respondents from 16 professional financial jobs.

17%

7%

15%

1% 0%

2%

7% 5%

1%

5%

23%

2%

0% 0% 8% 7%

Accountant

Assistant Tax Manager

Assistant Accounts Officer

Assistant Budget Officer

Assistant Budget Programmer

Budget Officer

CA

Chief Finance Officer

Direct Tax Deputy Manager

Finance Manager

Finance Officer

Finance Supervisor

Joint Secretary

Superintendent

Tax Consultant

Tax Manager

67

• Sample of Stakeholders by Region

Sample of 384 Stakeholders has been selected and it covers most of Indians’ region.

Table 5.4 Sample of Respondent by Region.

Respondent by Region N %

1. Ahmedabad 10 2.60 2. Assam 5 1.30 3. Bangalore 17 4.43 4. Baroda 1 0.26 5. Chandigarh 10 2.60 6. Chennai 13 3.39 7. Chhattisgarh 1 0.26 8. Coimbatore 3 0.78 9. Cuttack 6 1.56 10. Delhi 85 22.14 11. Ernakulam 20 5.21 12. Goa 1 0.26 13. Gujarat 2 0.52 14. Gwalior 8 2.08 15. Himachal Pradesh 3 0.78 16. Hyderabad 34 8.85 17. Jaipur 18 4.69 18. Jharkhand 7 1.82 19. Kanpur 22 5.73 20. Kolkata 25 6.51 21. Mumbai 59 15.36 22. Patna 15 3.91 23. Pune 16 4.17 24. Shillong 3 0.78 Total 384 100.00 (Source: Survey Data)

As per table 5.4, 24 regions were selected by researcher for coverage of study. Hence

Morgan sampling table was used to select samples.

68

Fig 5.7 Sample of Stakeholders by Region.

From the above table 5.6 it has been seen that the sample consists of 24 regions from

different parts and states of India. Among all regions, Delhi with 22.14 % was the

highest respondent rank.

• Sample of Individual Respondents (Stakeholders) by Sex

The following table 5.5 gives the classifications of Sample of Respondents by Sex

Table 5.5 Sample of Stakeholders by Sex.

Sex N %

Female 41 10.68

Male 343 89.32

TOTAL 384 100

(Source: Survey Data)

3% 1%

4% 0% 3% 3%

0% 1%

2%

22%

5%

0% 1%

2% 1%

9% 5%

2%

6%

7%

15%

4% 4%

1%

Ahmedabad

Assam

Bangalore

Baroda

Chandigarh

Chennai

Chhattisgarh

Coimbatore

Cuttack

Delhi

Ernakulam

Goa

Gujarat

Gwalior

Himachal Pradesh

69

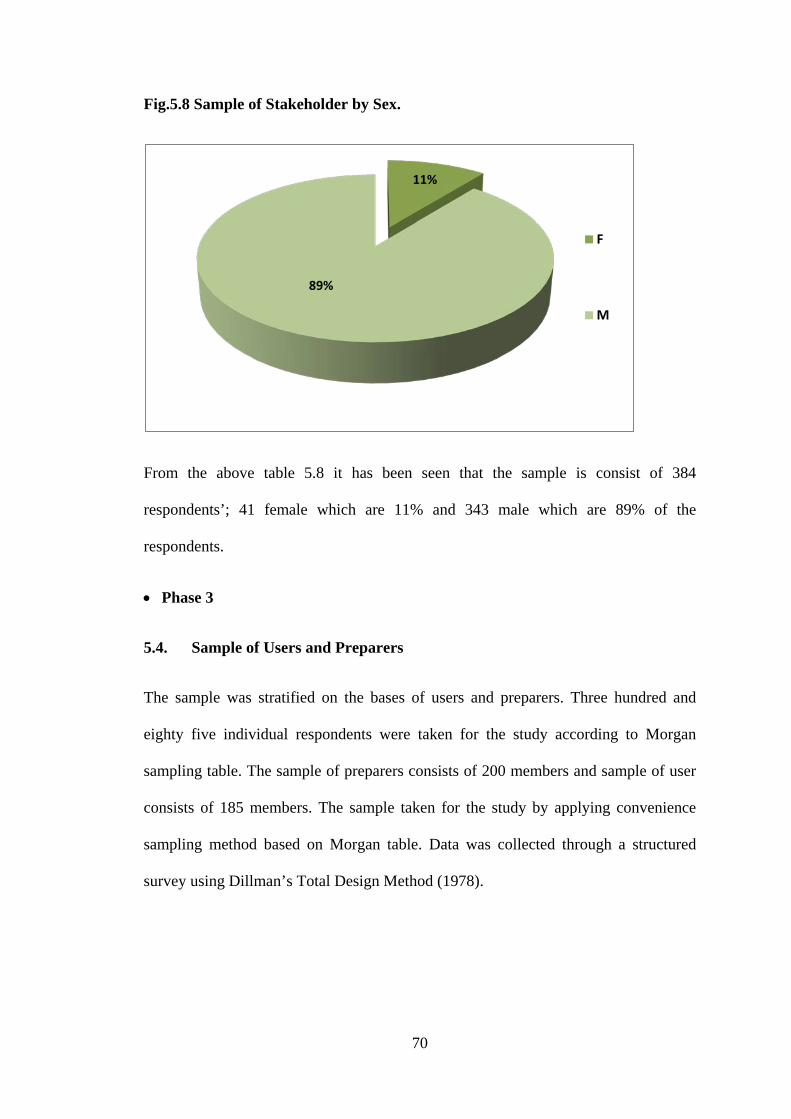

Fig.5.8 Sample of Stakeholder by Sex.

From the above table 5.8 it has been seen that the sample is consist of 384

respondents’; 41 female which are 11% and 343 male which are 89% of the

respondents.

• Phase 3

5.4. Sample of Users and Preparers

The sample was stratified on the bases of users and preparers. Three hundred and

eighty five individual respondents were taken for the study according to Morgan

sampling table. The sample of preparers consists of 200 members and sample of user

consists of 185 members. The sample taken for the study by applying convenience

sampling method based on Morgan table. Data was collected through a structured

survey using Dillman’s Total Design Method (1978).

11%

89%

F

M

70

• Preparers

Table 5.6 Sample of Preparers by Profession.

Sample of Preparers by Profession N %

1. Accountant 21 10.5

2. Assistant Accounts Officer 2 1

3. Assistant Budget Officer 2 1

4. Assistant Tax Manager 23 11.5

5. Accounts Officer 46 23

6. Budget Officer 10 5

7. Charter Accountant 18 9

8. Chief finance officer 1 0.5

9. Direct Tax Deputy Manager 2 1

10. Finance Manager 4 2

11. Finance Officer 22 11

12. Tax Consultant 25 12.5

13. Tax Manager 24 12

Total 200 100

(Source: Survey Data)

As seen in the above table sample of respondent by profession, it could be seen that

the total number of 13 groups of professional respondent. They responded to the

questionnaire and they have been selected according to Morgan table based on

convenience sapling method.

71

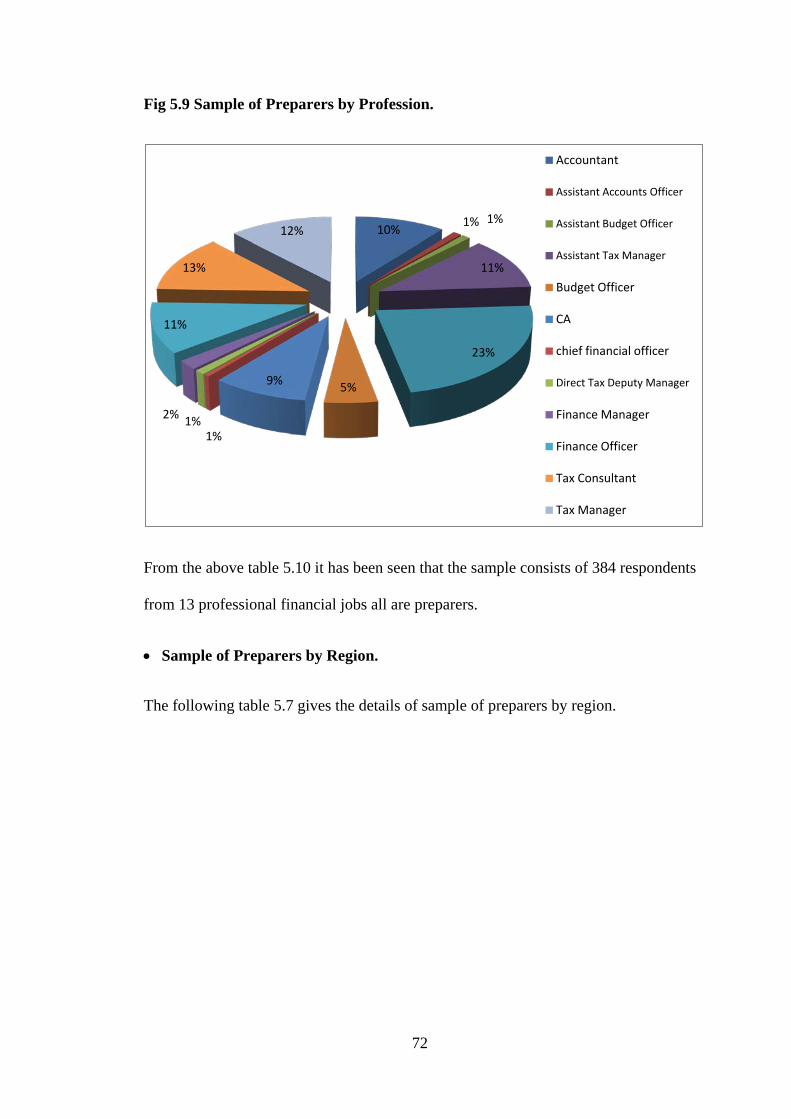

Fig 5.9 Sample of Preparers by Profession.

From the above table 5.10 it has been seen that the sample consists of 384 respondents

from 13 professional financial jobs all are preparers.

• Sample of Preparers by Region.

The following table 5.7 gives the details of sample of preparers by region.

10% 1% 1%

11%

23%

5% 9%

1% 1% 2%

11%

13%

12%

Accountant

Assistant Accounts Officer

Assistant Budget Officer

Assistant Tax Manager

Budget Officer

CA

chief financial officer

Direct Tax Deputy Manager

Finance Manager

Finance Officer

Tax Consultant

Tax Manager

72

Table 5.7 Sample of Preparers by Region.

Respondent by Region N %

1. Andhra Pradesh 19 9.5

2. Assam 4 2

3. Bihar 16 8

4. Chhattisgarh 8 4

5. Delhi 10 5

6. Gujarat 21 10.5

7. Haryana 2 1

8. Jharkhand 6 3

9. Karnataka 10 5

10. Kerala 17 8.5

11. Maharashtra 32 16

12. Mizoram 2 1

13. Nagaland 2 1

14. Odisha 2 1

15. Orissa 1 0.5

16. Puducherry 1 0.5

17. Punjab 9 4.5

18. Rajasthan 4 2

19. Tamil Nadu 7 3.5

20. Tripura 2 1

21. Uttar Pradesh 11 5.5

22. Uttarakhand 2 1

23. West Bengal 12 6

Total 200 100

(Source: Survey Data)

As presented in table 5.7, the samples of respondents are from 23 regions. The regions

cover most part of India. Here also Morgan table was the bases of selection of region

to represent in total sample.

73

Fig. 5.10 Sample of Preparers by Region.

From the above table 5.10, it has been seen that the sample consisted of 23 regions

from different parts and states of India. Among all regions Maharashtra with 16% was

the highest respondent in the list.

• Sample of Preparers by Sex

The following table 5.8 gives the details of Sample of Respondents by sex.

Table 5.8 Sample of Preparers by Sex.

Sex N %

Female 13 6.50

Male 187 93.50

TOTAL 200 100

(Source: Survey Data)

10%

2%

8%

4% 5% 11%

1% 3%

5%

9%

16%

1% 1%

1% 1%

1%

5% 2%

4% 1%

6% 1%

6%

Andhra Pradesh Assam

Bihar

Chhattisgarh

Delhi

Gujarat

Haryana

Jharkhand

Karnataka

Kerala

Maharashtra

Mizoram

Nagaland

Odisha

Orissa

74

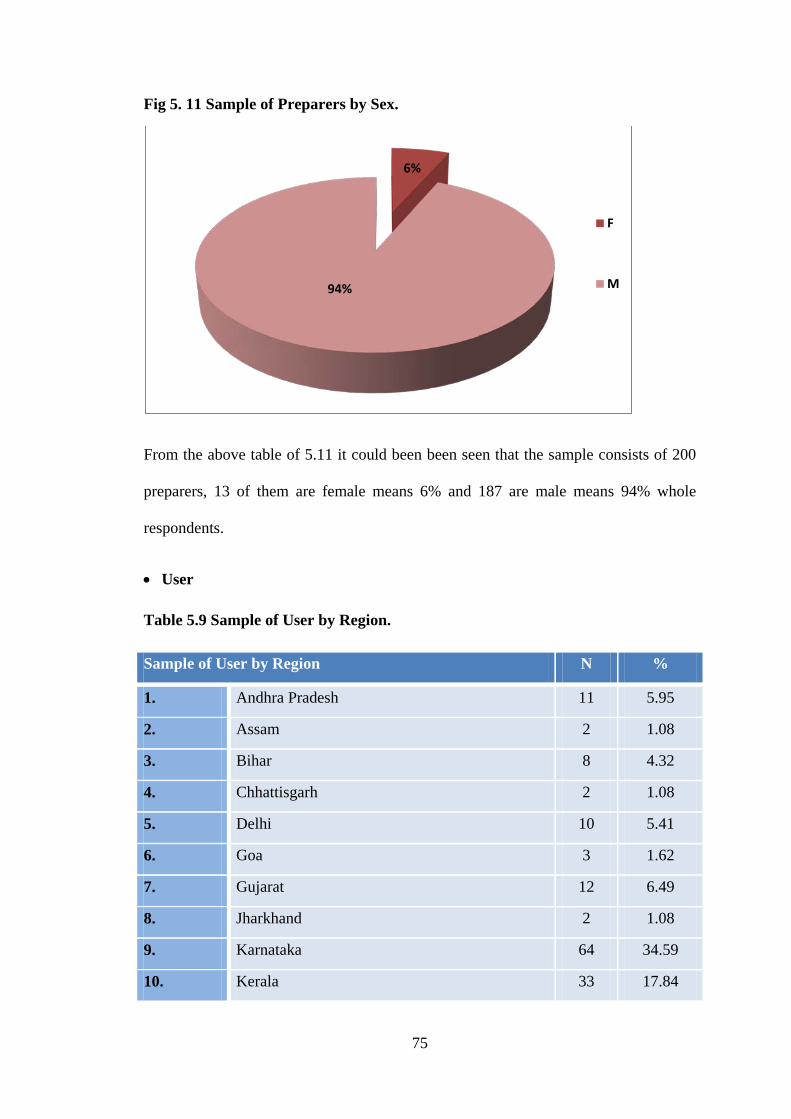

Fig 5. 11 Sample of Preparers by Sex.

From the above table of 5.11 it could been been seen that the sample consists of 200

preparers, 13 of them are female means 6% and 187 are male means 94% whole

respondents.

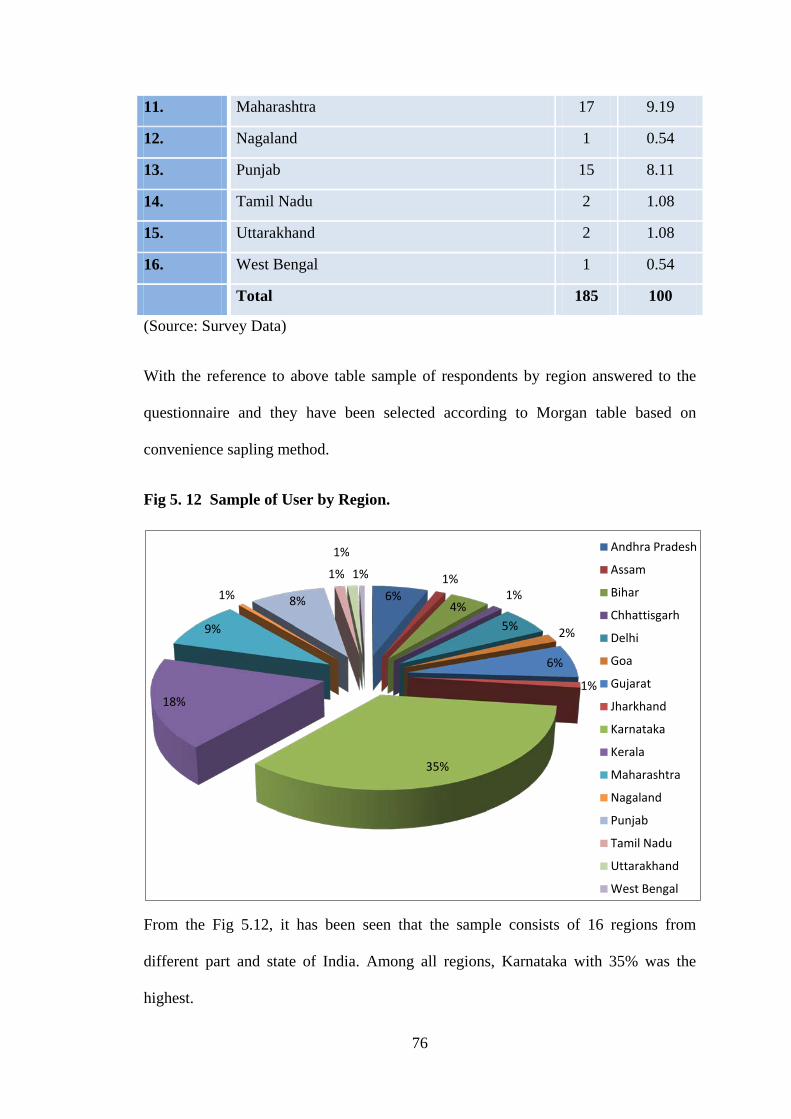

• User

Table 5.9 Sample of User by Region.

Sample of User by Region N %

1. Andhra Pradesh 11 5.95

2. Assam 2 1.08

3. Bihar 8 4.32

4. Chhattisgarh 2 1.08

5. Delhi 10 5.41

6. Goa 3 1.62

7. Gujarat 12 6.49

8. Jharkhand 2 1.08

9. Karnataka 64 34.59

10. Kerala 33 17.84

6%

94%

F

M

75

11. Maharashtra 17 9.19

12. Nagaland 1 0.54

13. Punjab 15 8.11

14. Tamil Nadu 2 1.08

15. Uttarakhand 2 1.08

16. West Bengal 1 0.54

Total 185 100

(Source: Survey Data)

With the reference to above table sample of respondents by region answered to the

questionnaire and they have been selected according to Morgan table based on

convenience sapling method.

Fig 5. 12 Sample of User by Region.

From the Fig 5.12, it has been seen that the sample consists of 16 regions from

different part and state of India. Among all regions, Karnataka with 35% was the

highest.

6% 1%

4% 1%

5% 2%

6%

1%

35%

18%

9%

1% 8%

1%

1%

1%

Andhra Pradesh

Assam

Bihar

Chhattisgarh

Delhi

Goa

Gujarat

Jharkhand

Karnataka

Kerala

Maharashtra

Nagaland

Punjab

Tamil Nadu

Uttarakhand

West Bengal

76

Sample of User by Sex

The following table 5.10 gives the details of Sample of Users by Sex.

Table 5.10 Sample of User by Sex.

Sex N %

Female 49 26.49

Male 136 73.51

TOTAL 200 100

(Source: Survey Data)

Fig 5. 13 Sample of User by Sex

From the above table 5.13 it has been seen that the sample consisted of 185 users’, 49

are female, means (26%) and 136 are male means (74%).

26%

74%

F

M

77

• Phase 4

5.5. Difference in recognition, measurement and disclosure elements of financial

statements between the proposed Indian Accounting Standards, current

accounting standards and International Financial Reporting Standards

Today, in India, process of convergence with International Financial Reporting

Standards is going on. Hence new accounting standards proposed with the name of

Ind-AS, which is slightly different from International Financial Reporting Standards

as well as Indian GAAP are currently used as accounting standards which is

according to the study has more differences with International Financial Reporting

Standards in compare to Ind-AS.

To analyse the difference in recognition, measurement and disclosure elements of

financial statements between the proposed and current Indian Accounting Standards

and International Financial Reporting Standards’ secondary data has been used and

accounting standards was directly given in ICAI and IFRS web site.

78

Table 5.11 Differences between Proposed Indian Accounting Standards, Current Accounting Standards and International Financial

Reporting Standards.

IFRS Indian GAAP Ind AS

1.Framework for the Preparation and Presentation of Financial Statements

Framework for the Preparation and Presentation of Financial Statements Disclosure of Accounting Policies

Framework for the Preparation and Presentation of Financial Statements

IAS 1 provides all are requirements for the presentation of financial statements.

Based on Indian GAAP Companies Act requires preparation of: 1. Balance Sheet, 2. Profit and Loss Account, 3. Notes to Accounts.

Similar to IFRS with some exception.

1.1.Presentation of Financial Statements based on historical cost or fair valuation

IFRS worked based on fair valuation

Indian GAAP work based on historical cost.

Similar to IFRS

1.2. Presentation of Financial Statements - formats

Books of account should be prepared only on introduced formats given by IASB.

Based on Indian GAAP but there is chance to use IFRS as well.

Such thing does not exist in Ind-AS 1.

1.3.Presentation of Financial Statements – classification of financial liabilities under refinancing arrangements

Refinance arrangements or reschedule payments on a long-term basis is completed after the end of the reporting period.

Refinance arrangements does not exist in Indian GAAP.

Similar to IFRS.

79

1.4.Presentation of Financial Statements - classification of financial liabilities upon breach of covenants

Non-current if the loaner has united before the tip of the coverage amount to supply a grace amount of minimum 12 months once the coverage amount inside that the breach may be corrected and therefore the loaner cannot demand immediate reimbursement.

Based on Indian GAAP it does not exist.

Similar to IFRS.

1.5.Presentation of Financial Statements - statement of comprehensive income

All income items as well as expense items are included.

Profit and loss is based on Indian GAAP and also equivalent of separate income statement under IFRS.

All companies and industries required to show all items of income and expense in a one set of statement of profit and loss.

1.6.Presentation of Financial Statements - statement of changes in equity

A statement of changes in equity is given showing (a) the overall comprehensive financial gain for the amount (b) effects of retrospective application or statement on every element of equity (c) for every element of equity, a reconciliation between opening and closing balances.

Based on Indian GAAP it does not exist.

Similar to IFRS. .

1.7.Presentation of Financial Statements - reclassification

While comparative figures are Reclassified then, nature, amount and reason of changes should be disclosed.

A revelation is created in monetary statements that comparative amounts are reclassified to adapt to the presentation within the current amount while not extra disclosures for the character, quantity and reason for assortment.

Similar to IFRS.

1.8.Presentation of Financial Statements - critical judgment

While management in applying accounting policies then disclosure of critical judgments made by Requires.

Based on Indian GAAP it does not exist.

Similar to IFRS

80

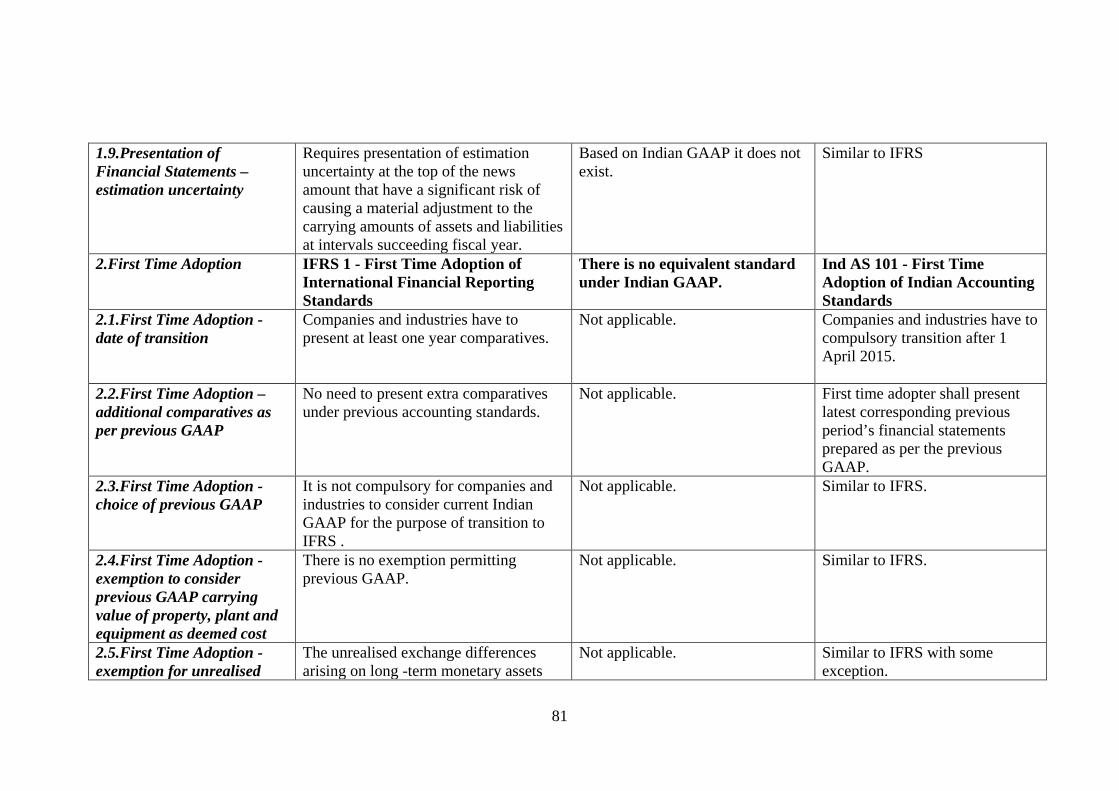

1.9.Presentation of Financial Statements – estimation uncertainty

Requires presentation of estimation uncertainty at the top of the news amount that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities at intervals succeeding fiscal year.

Based on Indian GAAP it does not exist.

Similar to IFRS

2.First Time Adoption IFRS 1 - First Time Adoption of International Financial Reporting Standards

There is no equivalent standard under Indian GAAP.

Ind AS 101 - First Time Adoption of Indian Accounting Standards

2.1.First Time Adoption - date of transition

Companies and industries have to present at least one year comparatives.

Not applicable. Companies and industries have to compulsory transition after 1 April 2015.

2.2.First Time Adoption – additional comparatives as per previous GAAP

No need to present extra comparatives under previous accounting standards.

Not applicable. First time adopter shall present latest corresponding previous period’s financial statements prepared as per the previous GAAP.

2.3.First Time Adoption - choice of previous GAAP

It is not compulsory for companies and industries to consider current Indian GAAP for the purpose of transition to IFRS .

Not applicable. Similar to IFRS.

2.4.First Time Adoption - exemption to consider previous GAAP carrying value of property, plant and equipment as deemed cost

There is no exemption permitting previous GAAP.

Not applicable. Similar to IFRS.

2.5.First Time Adoption - exemption for unrealised

The unrealised exchange differences arising on long -term monetary assets

Not applicable. Similar to IFRS with some exception.

81

foreign currency exchange differences on long-term monetary assets and liabilities

and liabilities are recognised immediately in profit or loss.

2.6.First Time Adoption - exemption from retrospective application of effective interest method and impairment requirements

There is no exemption from retrospective application of effective interest technique or the impairment needs for money instruments.

Not applicable. Similar to IFRS with some exception.

2.7.First Time Adoption - non-current assets held for sale and discontinued operations

No exemption in respect of non-current assets held for sale and discontinued operations.

Not applicable. Similar to IFRS with some exception.

2.8.First Time Adoption - reconciliations

IFRS needs reconciliations for gap equity, total comprehensive financial gain, income statement and shutting equity for the comparative amount to clarify the transition to IFRS from previous accumulation

Not applicable. similar to IFRS

3. Share-based Payment

IFRS 2 - Share-based Payment There is no equivalent standard. Ind AS 102 - Share-based Payment

3.1.Share-based Payment - recognition

Recognise as the expense over the vesting amount. Product and services in a very share based mostly payment group action area unit recognised once product area unit received or as services area unit rendered.

Similar to IFRS. Similar to IFRS.

82

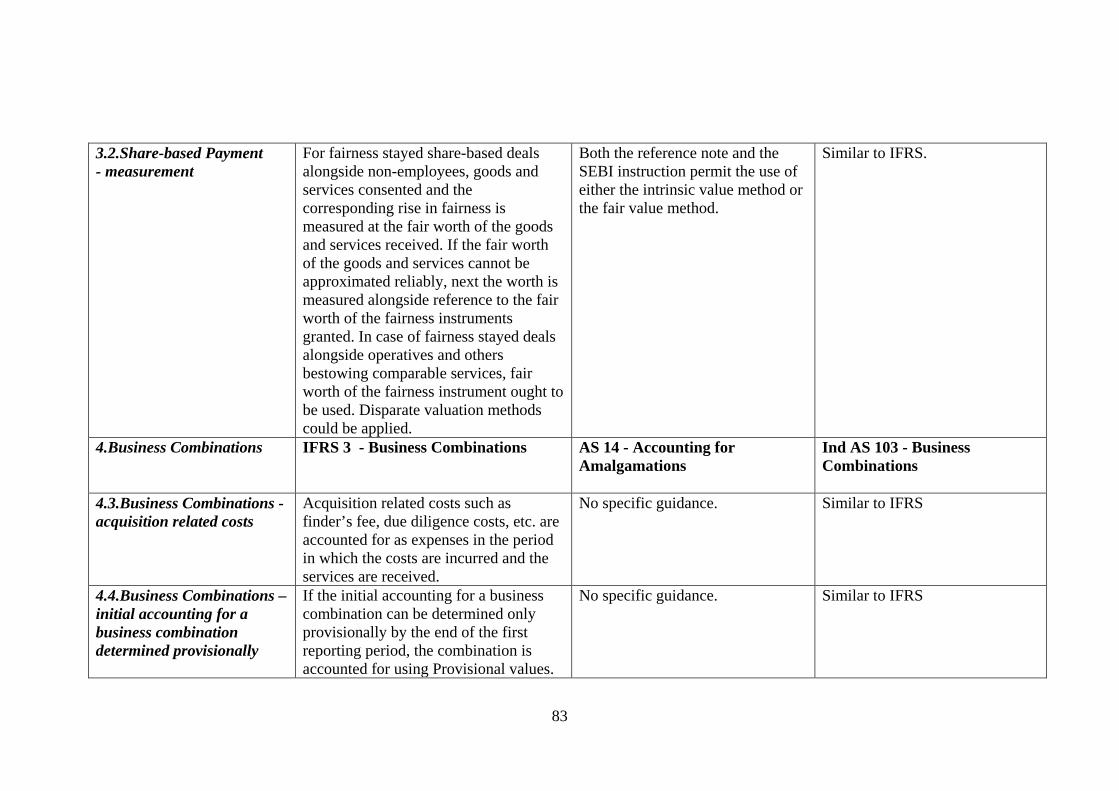

3.2.Share-based Payment - measurement

For fairness stayed share-based deals alongside non-employees, goods and services consented and the corresponding rise in fairness is measured at the fair worth of the goods and services received. If the fair worth of the goods and services cannot be approximated reliably, next the worth is measured alongside reference to the fair worth of the fairness instruments granted. In case of fairness stayed deals alongside operatives and others bestowing comparable services, fair worth of the fairness instrument ought to be used. Disparate valuation methods could be applied.

Both the reference note and the SEBI instruction permit the use of either the intrinsic value method or the fair value method.

Similar to IFRS.

4.Business Combinations

IFRS 3 - Business Combinations AS 14 - Accounting for Amalgamations

Ind AS 103 - Business Combinations

4.3.Business Combinations - acquisition related costs

Acquisition related costs such as finder’s fee, due diligence costs, etc. are accounted for as expenses in the period in which the costs are incurred and the services are received.

No specific guidance. Similar to IFRS

4.4.Business Combinations – initial accounting for a business combination determined provisionally

If the initial accounting for a business combination can be determined only provisionally by the end of the first reporting period, the combination is accounted for using Provisional values.

No specific guidance. Similar to IFRS

83

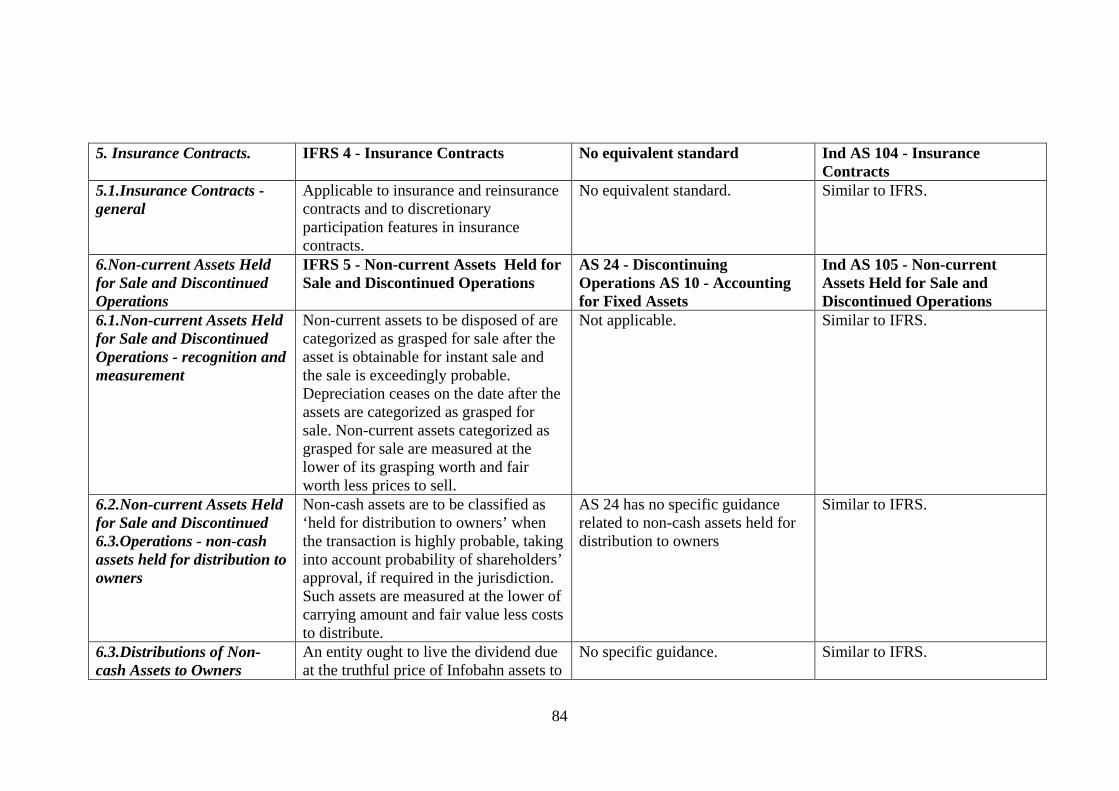

5. Insurance Contracts. IFRS 4 - Insurance Contracts No equivalent standard Ind AS 104 - Insurance Contracts

5.1.Insurance Contracts - general

Applicable to insurance and reinsurance contracts and to discretionary participation features in insurance contracts.

No equivalent standard. Similar to IFRS.

6.Non-current Assets Held for Sale and Discontinued Operations

IFRS 5 - Non-current Assets Held for Sale and Discontinued Operations

AS 24 - Discontinuing Operations AS 10 - Accounting for Fixed Assets

Ind AS 105 - Non-current Assets Held for Sale and Discontinued Operations

6.1.Non-current Assets Held for Sale and Discontinued Operations - recognition and measurement

Non-current assets to be disposed of are categorized as grasped for sale after the asset is obtainable for instant sale and the sale is exceedingly probable. Depreciation ceases on the date after the assets are categorized as grasped for sale. Non-current assets categorized as grasped for sale are measured at the lower of its grasping worth and fair worth less prices to sell.

Not applicable. Similar to IFRS.

6.2.Non-current Assets Held for Sale and Discontinued 6.3.Operations - non-cash assets held for distribution to owners

Non-cash assets are to be classified as ‘held for distribution to owners’ when the transaction is highly probable, taking into account probability of shareholders’ approval, if required in the jurisdiction. Such assets are measured at the lower of carrying amount and fair value less costs to distribute.

AS 24 has no specific guidance related to non-cash assets held for distribution to owners

Similar to IFRS.

6.3.Distributions of Non-cash Assets to Owners

An entity ought to live the dividend due at the truthful price of Infobahn assets to

No specific guidance. Similar to IFRS.

84

be distributed. The liability ought to be remeasured at every news date and at settlement, with changes recognised directly in equity. The distinction between the dividend paid and also the carrying quantity of Infobahn assets distributed ought to be recognised in profit or loss and may be disclosed severally. Further disclosures ought to be created, if Infobahn assets being command for distribution to homeowners meet the definition of a discontinued operation.

7.Exploration for and Evaluation of Mineral Resources

IFRS 6 - Exploration for and Evaluation of Mineral Resources

No equivalent standard. . Ind AS 106 - Exploration for and Evaluation of Mineral Resources

7.1.Exploration for and Evaluation of Mineral Resources - general

Exploration and analysis assets area unit measured at price or review less accumulated amortisation and impairment loss. AN entity determines the policy specifying that expenditure is recognised as exploration and analysis plus.

As per the steerage note, there area unit 2 various strategies for accounting for acquisition, exploration and development prices, viz. the victorious Efforts technique or the complete price technique. The steerage note recommends the victorious Efforts technique.

Similar to IFRS.

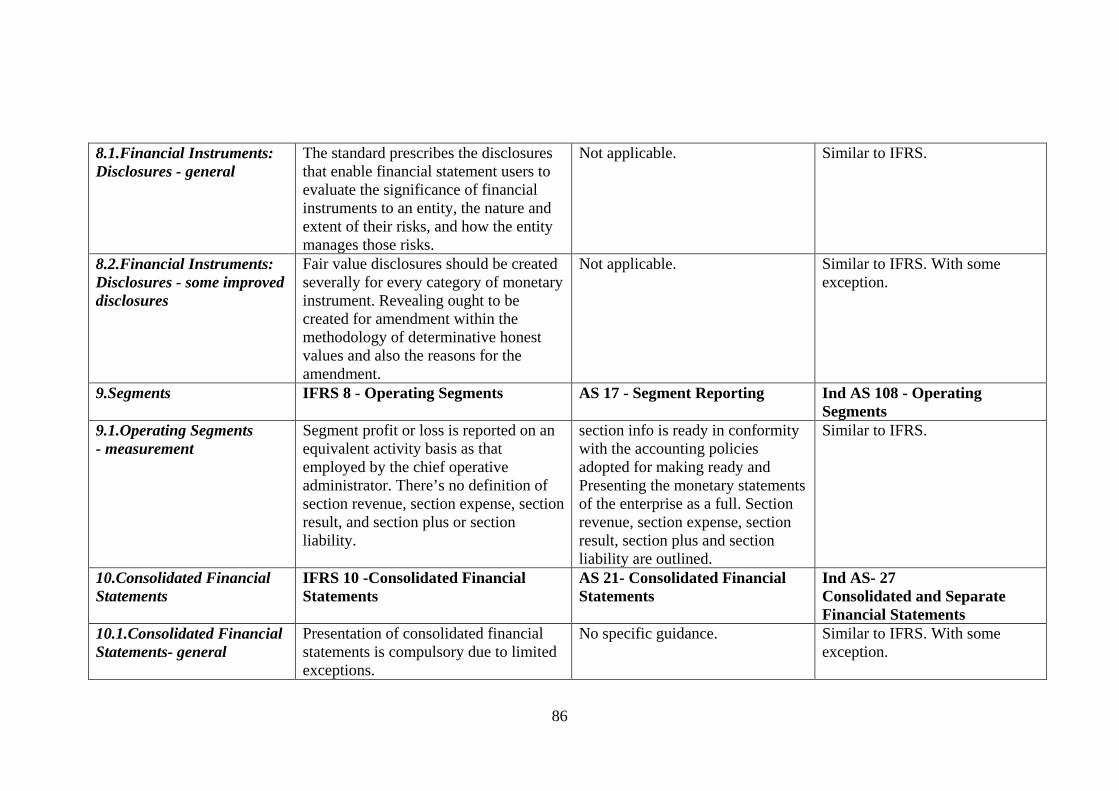

8.Financial Instruments: Disclosures

IFRS 7 &9 Financial Instruments: Disclosures

AS 32 - Financial Instruments: Disclosures

Ind AS 107 & 39 - Financial Instruments: Disclosures

85

8.1.Financial Instruments: Disclosures - general

The standard prescribes the disclosures that enable financial statement users to evaluate the significance of financial instruments to an entity, the nature and extent of their risks, and how the entity manages those risks.

Not applicable. Similar to IFRS.

8.2.Financial Instruments: Disclosures - some improved disclosures

Fair value disclosures should be created severally for every category of monetary instrument. Revealing ought to be created for amendment within the methodology of determinative honest values and also the reasons for the amendment.

Not applicable. Similar to IFRS. With some exception.

9.Segments

IFRS 8 - Operating Segments AS 17 - Segment Reporting Ind AS 108 - Operating Segments

9.1.Operating Segments - measurement

Segment profit or loss is reported on an equivalent activity basis as that employed by the chief operative administrator. There’s no definition of section revenue, section expense, section result, and section plus or section liability.

section info is ready in conformity with the accounting policies adopted for making ready and Presenting the monetary statements of the enterprise as a full. Section revenue, section expense, section result, section plus and section liability are outlined.

Similar to IFRS.

10.Consolidated Financial Statements

IFRS 10 -Consolidated Financial Statements

AS 21- Consolidated Financial Statements

Ind AS- 27 Consolidated and Separate Financial Statements

10.1.Consolidated Financial Statements- general

Presentation of consolidated financial statements is compulsory due to limited exceptions.

No specific guidance. Similar to IFRS. With some exception.

86

10.2.Consolidation of Special purpose entities (SPE)

Consolidated where the substance of the relationship indicates control.

No specific guidance. Similar to IFRS

10.3.Employee share (stock) trusts

Consolidated where substance of relationship indicates control (SIC-12 Model). Entity’s own shares held by an employee share trust are accounted for as treasury shares.

Employee share trusts are not consolidated

Similar to IFRS

11.Joint Ventures IFRS 11 -Joint Arrangements AS 27- Financial Reporting of Interests in Joint Ventures

Ind AS- 31 Interests in Joint Ventures

11.1.Presentation of jointly controlled entities (joint ventures)

Both proportional consolidation and equity method permitted.

In consolidated financials: proportional consolidation is used. In standalone financials: at cost less impairment

Similar to IFRS

87

5.6. RESEARCH INSTRUMENT AND STATISTICAL TOOLS

In this research both primary and secondary data has been used. Four different

questionnaires, designed for the purpose of collecting primary and secondary data

according to research objectives administrated on respondents.

In this research different statistical technique has been used both descriptive and

inferential statistics applied with different technique like one sample t-test, ANOVA

analysis, Binomial test with coverage of Z-proportion test , karlpearson coefficient of

correlation, mean analysis and variance analysis with the help of SPSS package and

Microsoft excel.

5.6.1 IASB Member Countries Questionnaire

IASB member countries questionnaire was designed to obtain differences in

International Financial Reporting Standards’ implementation among IASB countries.

Collected data are given directly in IASB web site. The designed questionnaire

contains four factors of IFRS implementation. The first factor was commitment to

global financial reporting standards which consists of four questions. The second

factor is jurisdiction for domestic companies with debt or equity in public market. It is

consists of six questions. Third factor refers to IFRS endorsement which consists of

six questions and the fourth factor is translation of IFRS which consists of five

questions. Totally twenty one questions in four part were administrated. Three point

scale method has been used. The scale 2 represents “Yes”, the scale 1 represents “Yes

with Explained exception” and the scale zero represent “NO”.

88

5.6.2 Influence of Legal, Social, Economic and Institutional Factor for IFRS

Convergence in India.

Questionnaire has been prepared to examine the Influence of legal, social, economic

and institutional factors for International Financial Reporting Standards’ convergence

in India. This Questionnaire consists of 26 questions divided into 4 parts. First part

consists of seven questions, second part consists of six questions, third part consists of

six questions and fourth part consists of seven. Data has been collected through a

structured survey, using Dillman’s total design method (1978).

Five point “Likert scale”, method have been used the scale 4 represent “Very

Important”, the scale 3 represent “Important” scale 2 represent “Neutral”, scale 1

represent “Slightly Important” and the scale zero represent “Not Important”.

5.6.3 Problem of International Financial Reporting Standards’ Convergence

from User’s and Preparer’s Prospective.

To examine the problems for International Financial Reporting Standards’

convergence among users and preparers two separate questionnaire has been designed

for each group. Preparer’s questionnaire consists of 33 questions fewer than 17 factors

which concentrated on main differences between Indian accounting standards’ and

IFRS. User’s questionnaire consist of 18 questions under 4 factors which concentrated

on main problems of user due to convergence with IFRS in India like; issues

contributing to relevance in India over the convergence with IFRS, issues contribute

to availability, issues contribute to understandability and issues contribute to

comparability. Data have been collected through a structured survey using Dillman’s

total design method (1978). five point “Likert scale”, method has been used. The scale

4 represent “Very Difficult”, the scale 3 represent “Difficult”, scale 2 represent

“Neutral”, scale 1 represent “Slightly Difficult” and the scale zero represent “Not

Difficult”.

89

5.6.4 Difference in Recognition, Measurement and Disclosure Elements of

Financial Statements between the Proposed Indian Accounting

Standards, Current Accounting Standards and International Financial

Reporting Standards.

To consider difference in recognition, measurement and disclosure, elements of

financial statements between the proposed Indian Accounting Standards, current

Accounting Standards and International Financial Reporting Standards, current

Accounting Standards and Ind-AS has taken from ICAI website and IFRS has taken

from IASB website. Three point scales have been used; the scale 3 represent “Similar

to IFRS”, the scale 2 represent “Similar to IFRS with exception” and the scale 1

represent “Not Similar to IFRS”.

5.7. Data Collection and Analysis

The study was based on both primary and secondary data.

I. Secondary data.

Secondary data consist of two phases:

• A part of secondary data is given directly in International Accounting Standards

board (IASB) website. Totally there are one hundred and twenty three countries

listed in IASB website and based on Morgan’s table minimum of ninety three

samples are required. Total number of hundred countries in adopting, converging

and non-adopting has been selected. The data were collected through questionnaire

method. To measure the level of implementation of IFRS in IASB member

countries questionnaire was filled with three point scale method. Reliability of the

questionnaire was tested by using Cronbach’s Alpha in SPSS. Countries have been

selected according to judgment sampling method.

90

• Second part of secondary data is accounting standards given directly in Institute of

Chartered Accountants of India (ICAI) and International Accounting Standards

board (IASB) website , all IFRSs compared with proposed Indian Accounting

Standards’ and current Accounting Standards’.

Table 5.12, Reliability Analysis for Implantation of IFRS among IASB Member

Countries.

Factors Cronbach's

Alpha

1. Commitment to Global Financial Reporting Standards .858

2. Domestic Companies Securities Trade in a Public Market. .850

3. IFRS Endorsement .857

4. Translation of IFRSS .860

Overall .855

According to above table it could be observed that reliability of the questionnaire is

more than 0.85 in all cases for instance in case of commitment to global financial

reporting standards reliability is 0.858, for domestic companies whose debt or equity

securities trade in a public market in the jurisdiction is 0.850, IFRS endorsement is

0.857, translation of IFRS is 0.860 and in Overall reliability is 0.855.

II. Primary Data

The primary data also consist of two phases:

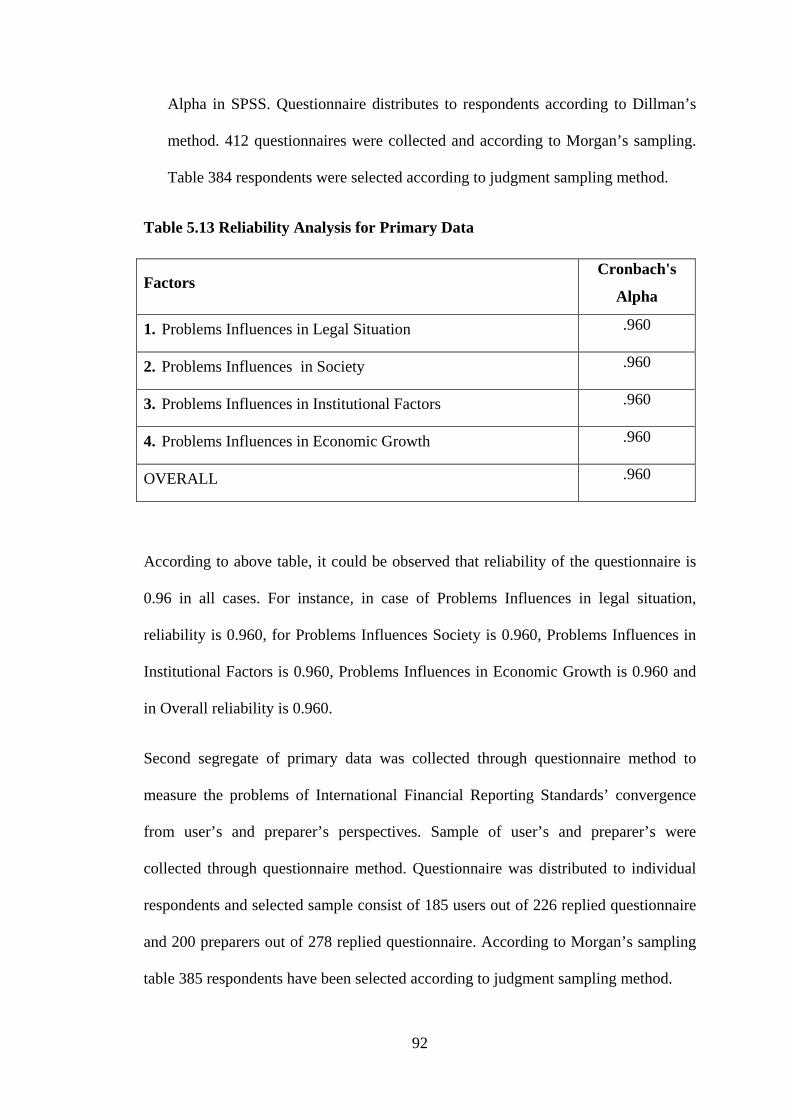

• First segregate of primary data was collected through questionnaire method to

measure the problems influence in legal, social, economic and institutional factors

over convergence with IFRS in India. Questionnaires were distributed to

stakeholders after doing pilot study and analysing reliability by using Cronbach’s

91

Alpha in SPSS. Questionnaire distributes to respondents according to Dillman’s

method. 412 questionnaires were collected and according to Morgan’s sampling.

Table 384 respondents were selected according to judgment sampling method.

Table 5.13 Reliability Analysis for Primary Data

Factors Cronbach's

Alpha

1. Problems Influences in Legal Situation .960

2. Problems Influences in Society .960

3. Problems Influences in Institutional Factors .960

4. Problems Influences in Economic Growth .960

OVERALL .960

According to above table, it could be observed that reliability of the questionnaire is

0.96 in all cases. For instance, in case of Problems Influences in legal situation,

reliability is 0.960, for Problems Influences Society is 0.960, Problems Influences in

Institutional Factors is 0.960, Problems Influences in Economic Growth is 0.960 and

in Overall reliability is 0.960.

Second segregate of primary data was collected through questionnaire method to

measure the problems of International Financial Reporting Standards’ convergence

from user’s and preparer’s perspectives. Sample of user’s and preparer’s were

collected through questionnaire method. Questionnaire was distributed to individual

respondents and selected sample consist of 185 users out of 226 replied questionnaire

and 200 preparers out of 278 replied questionnaire. According to Morgan’s sampling

table 385 respondents have been selected according to judgment sampling method.

92

Table 5.14 Reliability Analysis for Preparers.

Factors Cronbach's

Alpha

1.Disclosure of Accounting Policies .992

2.Valuation of Inventories .992

3.Cash Flow Statements .992

4. Contingencies and Events Occurring after the Balance Sheet Date .992

5.Segment Reporting .992

6.Accounting for Fixed Assets .993

7.Leases .992

8.Employee Benefits .992

9.Related Party Disclosures .992

10.Consolidated Financial Statements .993

11.Financial Reporting of Interests in Joint Ventures .992

12.Earnings Per Share .992

13.Interim Financial Reporting .993

14. Provisions, Contingent Liabilities and Contingent Assets .992

15.Intangible Assets .992

16.Accounting for Investments .993

17.Accounting for Amalgamations .993

Overall .992

According to above table it could be observed that reliability of the questionnaire is

more than 0.992 in all cases of problems of convergence with International Financial

Reporting Standards in India from preparer’s Perspective.

93

Table 5.15 Reliability Analysis for Users.

Factors Cronbach's

Alpha

1. Issues contribute to Relevance in India over the

Convergence with IFRS. .976

2. Issues contribute to Availability in India over the

Convergence with IFRS. .975

3. Issues contribute to Understand ability in India over the

Convergence with IFRS. .971

4. Issues contribute to Comparability in India over the

Convergence with IFRS. .974

Overall .974

According to above table it could be observed that reliability of the questionnaire is

more than 0.971 in all cases. For instance, in case of Issues contribute to relevance in

India over the convergence with IFRS reliability is 0.975, Issues contribute to

availability in India over the convergence with IFRS reliability is 0.975, Issues

contribute to understandability in India over the convergence with IFRS reliability is

0.971, Issues contribute to comparability in India over the convergence with IFRS

reliability is 0.974 and in overall reliability is 0.974.

Summary

This chapter addressed the research methodology that was employed for the present

research study. The methodology covered the detailed description of the sample of

IASB member countries. It consists of converging countries, adopting countries and

non- adopting countries as well as description of the sample of individual respondent

for IFRS convergence in India. It also describes the research instruments used in this

study, data collection process and analysis methods were discussed.

94

References:

1. Kothari, C. (2004). Research methodology: methods and techniques:

New Age International.

2. Raj, D. (1972). The Design Of Sample Surveys: McGraw-Hill Book

Company.

3. Webster, R. (1985). Quantitative spatial analysis of soil in the field

Advances in soil science (pp. 1-70): Springer.

95