CHAPTER 5 MUTUAL FUND INVESTORS’...

45

83 CHAPTER 5 MUTUAL FUND INVESTORS’ BEHAVIOUR 5.1 Introduction 5.2 Fund Selection Behaviour of Mutual Fund Investors 5.2.1 Mutual Fund Product Attributes 5.2.2 Fund Preferences of Mutual Fund Investors 5.2.2.1 Selection of Mutual Fund Schemes 5.2.2.2 Association between Fund Preferences of Mutual Fund Investors and their Objectives of Investment 5.2.2.3 Association between Fund Preferences of Mutual Fund Investors and their Time Horizon 5.2.2.4 Association between Fund Preferences of Mutual Fund Investors and their Risk Perception 5.3 Post-buying Behaviour of Mutual Fund Investors 5.3.1 Association between Post-buying Behavioural Factors of Mutual Fund Investors and their Time Horizon 5.3.2 Association between Post-buying Behavioural Factors of Mutual Fund Investors and their Risk Perception 5.3.3 Association between Post-buying Behavioural Factors of Mutual Fund Investors and their Demography 5.3.4 Product Performance Satisfaction Level

Transcript of CHAPTER 5 MUTUAL FUND INVESTORS’...

83

CHAPTER 5

MUTUAL FUND INVESTORS’ BEHAVIOUR

5.1 Introduction

5.2 Fund Selection Behaviour of Mutual Fund Investors

5.2.1 Mutual Fund Product Attributes

5.2.2 Fund Preferences of Mutual Fund Investors

5.2.2.1 Selection of Mutual Fund Schemes

5.2.2.2 Association between Fund Preferences of Mutual Fund

Investors and their Objectives of Investment

5.2.2.3 Association between Fund Preferences of Mutual Fund

Investors and their Time Horizon

5.2.2.4 Association between Fund Preferences of Mutual Fund

Investors and their Risk Perception

5.3 Post-buying Behaviour of Mutual Fund Investors

5.3.1 Association between Post-buying Behavioural Factors of

Mutual Fund Investors and their Time Horizon

5.3.2 Association between Post-buying Behavioural Factors of

Mutual Fund Investors and their Risk Perception

5.3.3 Association between Post-buying Behavioural Factors of

Mutual Fund Investors and their Demography

5.3.4 Product Performance Satisfaction Level

84

5.1 Introduction

Mutual fund is the most suitable investment for the common man as it

offers an opportunity to invest in a diversified, professionally managed basket of

securities at a relatively low cost. Currently there are large numbers of mutual

fund schemes available in the market, and asset management companies

compete against one another by launching new products and repositioning old

ones. The mutual fund schemes are to be tailored to the changing needs of the

investors. In order to maintain the mutual fund products to the requirements of

the investors the AMC should understand the behaviour of mutual fund investors.

So, mutual fund investors’ behavioural studies occupy a significant role in the

designing of mutual fund products. Mutual fund investors’ behaviour refers to the

attitude and preferences of the investors while, searching, using, evaluating and

disposing mutual fund products and services that they expect, will satisfy their

needs. Therefore, the present study examine the behaviour of mutual fund

investors at two levels such as behaviour exhibited at the time of selecting mutual

fund products, and behaviour of the investors after buying the mutual fund

products. The pre-buying behaviour of the mutual fund investors is known as fund

selection behaviour of mutual fund investors, and buying behaviour exhibited

after the investment is known as post-buying behaviour of mutual fund investors.

5.2 Fund Selection Behaviour of Mutual Fund Investors

Fund selection behaviour refers to the behaviour exhibited by the

individual investors at the time of searching, evaluating and selecting mutual fund

schemes for the investment. It includes the factors influencing mutual fund

investors while selecting mutual fund products, and their fund preferences. These

two aspects are analysed in two parts, first part of this section discuss with key

features of mutual fund products (product attributes) and latter part deals with

fund preferences of the investors.

85

5.2.1 Mutual Fund Product Attributes

To ascertain the key product attributes of mutual fund products influencing

the fund selection behaviour of mutual fund investors, 38 variables were identified

from the evidence of the earlier research studies and discussions with experts in the

mutual fund industry. The 38 identified variables were coded as given below:-

A1. Past Fund performance Record

A2. Funds reputation or brand name

A3. Schemes expense ratio

A4. Schemes portfolio/constituents

A5. Withdrawal facilities/redemption features

A6. Favourable rating by a rating agency

A7. Innovativeness of the scheme

A8. Loan facility

A9. Option to switch scheme

A10. Annual return/Dividend

A11. Capital Appreciation

A12. Tax Benefit

A13. Liquidity

A14. Performance guarantee

A15. Insurance facility

A16. Safety

B1. Ownership of the company (Private/ Public)

B2. Reputation of the Sponsoring firm/Brand name/Track record

B3. Net worth of the sponsor

B4. Sponsor has a well-developed Agency/Network

B5. Sponsors expertise in managing Money

B6. Sponsor has a well-developed Research & Infrastructure

C1. Disclosure of Investment objective in the advertisement

C2. Disclosure of periodicity of Valuation in the advertisement

C3. Disclosure of the method and the Periodicity of the schemes sales

and repurchases in the offer documents

86

C4. Disclosure of NAV in every Trading day

C5. Disclosure of deviation of Investments from the original pattern

D1. Service centre

D2. Professional financial advisor

D3. Service standard

D4. Investor’s grievance redressal machinery

D5. Listing on stock exchange

D6. Technology Enabled Services

E1. Advertisement

E2. Brokers/Agents

E3. Reference Group

E4. Early bird incentives

E5. Awareness of Mutual fund products

The product attributes were measured through a five point Likert-type

scale ranging from ‘most considered’ to ‘least considered’. The identified 38

factors influencing selection of mutual fund schemes are analysed using Principal

Component Analysis, with the objective to identify the factor which is significant

in mutual fund product buying decision. Kaiser-Meyer-Olkin test and Bartlett’s

Test of Shericity measure of sampling adequacy are used to examine the

appropriateness of factor analysis. The approximate chi-square statistic is

13649.451 with 703 degrees of freedom, which is significant at 0.05 levels (table

5.1). The KMO statistic (0.940) is also large (>0.5). Hence, factor analysis is

considered as an appropriate technique of further analysis of data.

Table 5.1 KMO and Bartlett's Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy. .940

Bartlett's Test of Sphericity

Approx. Chi-square 13649.451

df 703

Sig. .000

Source: Survey data

87

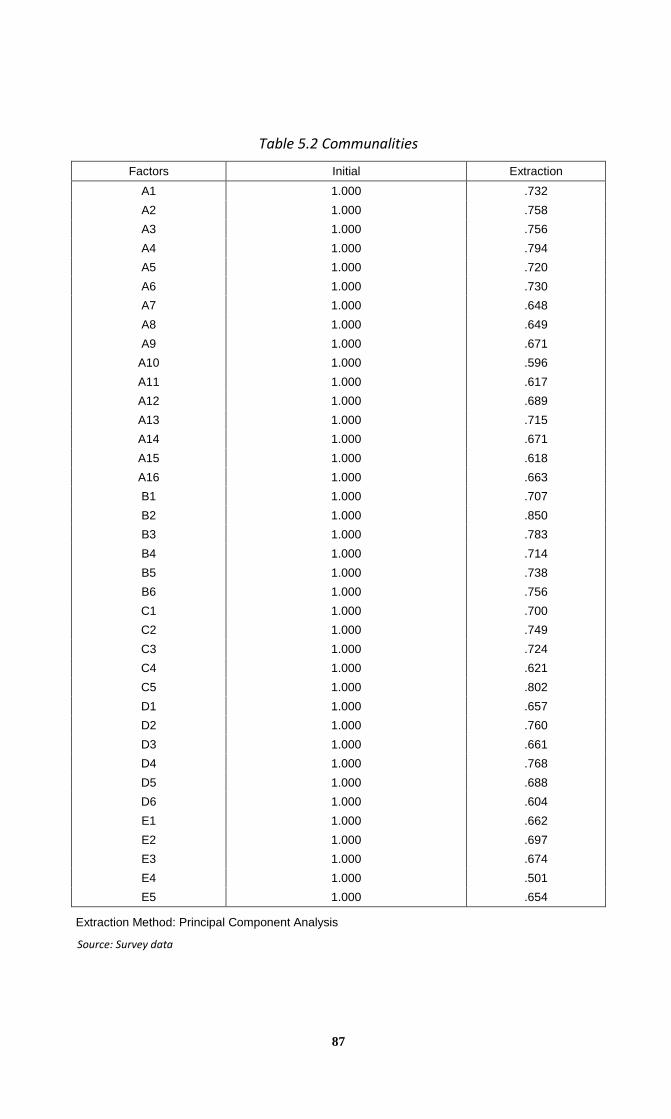

Table 5.2 Communalities

Factors Initial Extraction

A1 1.000 .732

A2 1.000 .758

A3 1.000 .756

A4 1.000 .794

A5 1.000 .720

A6 1.000 .730

A7 1.000 .648

A8 1.000 .649

A9 1.000 .671

A10 1.000 .596

A11 1.000 .617

A12 1.000 .689

A13 1.000 .715

A14 1.000 .671

A15 1.000 .618

A16 1.000 .663

B1 1.000 .707

B2 1.000 .850

B3 1.000 .783

B4 1.000 .714

B5 1.000 .738

B6 1.000 .756

C1 1.000 .700

C2 1.000 .749

C3 1.000 .724

C4 1.000 .621

C5 1.000 .802

D1 1.000 .657

D2 1.000 .760

D3 1.000 .661

D4 1.000 .768

D5 1.000 .688

D6 1.000 .604

E1 1.000 .662

E2 1.000 .697

E3 1.000 .674

E4 1.000 .501

E5 1.000 .654

Extraction Method: Principal Component Analysis

Source: Survey data

88

Table 5.3 Total Variance Explained

Component Initial Eigen values Extraction Sums of Squared

Loadings Rotation Sums of Squared

Loadings

Total % of Variance

Cumulative %

Total % of Variance

Cumulative %

Total % of Variance

Cumulative %

1 19.117 50.308 50.308 19.117 50.308 50.308 5.956 15.674 15.674

2 1.969 5.183 55.490 1.969 5.183 55.490 5.446 14.332 30.006

3 1.648 4.336 59.827 1.648 4.336 59.827 4.506 11.858 41.864

4 1.417 3.729 63.556 1.417 3.729 63.556 3.843 10.114 51.978

5 1.272 3.347 66.902 1.272 3.347 66.902 3.718 9.784 61.761

6 1.075 2.830 69.732 1.075 2.830 69.732 3.029 7.971 69.732

7 .984 2.589 72.321

8 .808 2.126 74.448

9 .764 2.009 76.457

10 .751 1.976 78.433

11 .680 1.790 80.224

12 .599 1.576 81.799

13 .581 1.529 83.329

14 .563 1.483 84.811

15 .506 1.332 86.143

16 .458 1.206 87.349

17 .420 1.104 88.453

18 .394 1.036 89.489

19 .366 .964 90.453

20 .331 .872 91.325

21 .323 .849 92.174

22 .303 .798 92.972

23 .269 .707 93.679

24 .259 .682 94.361

25 .237 .623 94.984

26 .222 .584 95.569

27 .207 .546 96.114

28 .195 .514 96.629

29 .176 .463 97.092

30 .170 .447 97.539

31 .155 .409 97.948

32 .142 .373 98.322

33 .138 .363 98.685

34 .122 .321 99.005

35 .107 .283 99.288

36 .102 .269 99.557

37 .095 .249 99.805

38 .074 .195 100.000

Extraction Method: Principal Component Analysis

Source: Survey data

89

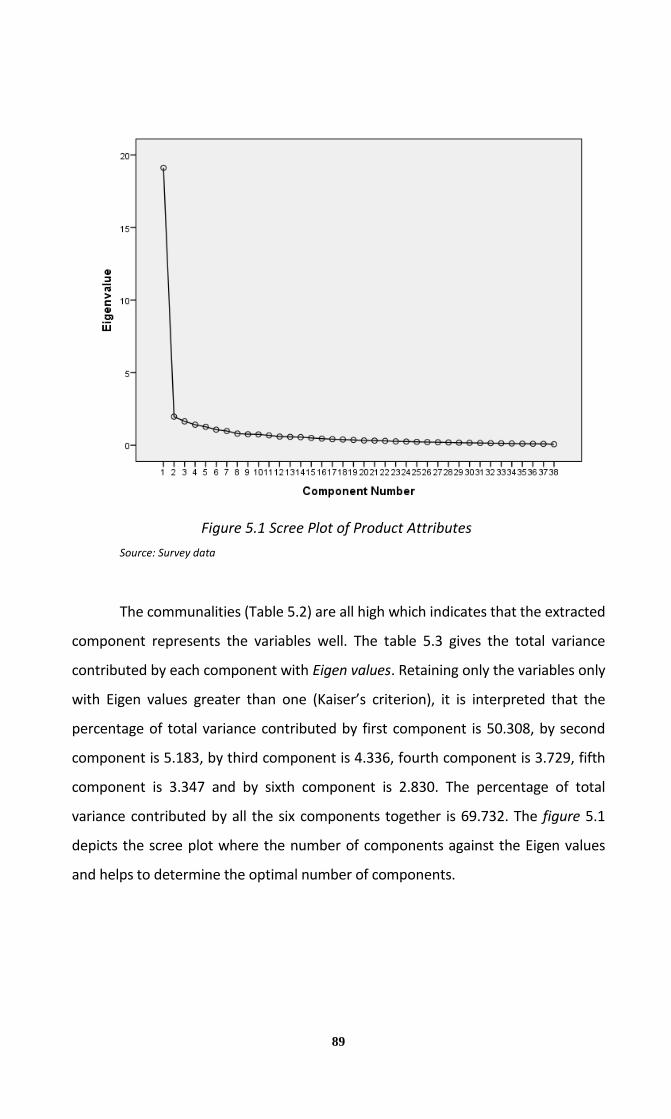

Figure 5.1 Scree Plot of Product Attributes

Source: Survey data

The communalities (Table 5.2) are all high which indicates that the extracted

component represents the variables well. The table 5.3 gives the total variance

contributed by each component with Eigen values. Retaining only the variables only

with Eigen values greater than one (Kaiser’s criterion), it is interpreted that the

percentage of total variance contributed by first component is 50.308, by second

component is 5.183, by third component is 4.336, fourth component is 3.729, fifth

component is 3.347 and by sixth component is 2.830. The percentage of total

variance contributed by all the six components together is 69.732. The figure 5.1

depicts the scree plot where the number of components against the Eigen values

and helps to determine the optimal number of components.

90

Table 5.4 Component Matrixa

Factors Component

1 2 3 4 5 6

A1 .667 -.373 -.007 .367 -.002 .116

A2 .621 -.414 .116 .408 .142 -.039

A3 .732 -.261 -.358 .045 -.059 -.133

A4 .722 -.301 -.386 .079 -.151 -.066

A5 .719 -.217 -.149 .281 -.007 .234

A6 .749 -.135 -.373 -.050 -.061 .070

A7 .723 -.201 -.284 .007 -.015 .057

A8 .667 .307 -.142 -.101 .283 .007

A9 .677 .232 -.075 -.001 .365 .141

A10 .651 .237 .078 .193 .270 .028

A11 .679 .189 -.276 .139 .066 -.143

A12 .599 .256 -.185 .208 .377 -.211

A13 .760 .132 -.335 .033 -.029 .077

A14 .740 .163 -.280 .004 .044 -.125

A15 .640 .389 -.149 -.055 .141 -.115

A16 .705 .092 -.011 -.076 .370 .119

B1 .718 -.169 .324 .184 .153 -.027

B2 .764 -.222 .389 .075 .127 -.211

B3 .799 -.118 .218 .031 -.036 -.283

B4 .781 -.023 .208 .020 -.078 -.232

B5 .781 -.087 .022 -.012 -.175 -.298

B6 .760 -.022 .054 .040 -.260 -.325

C1 .771 -.166 .107 -.225 .122 .017

C2 .786 -.116 .095 -.308 .073 -.096

C3 .761 -.181 .177 -.267 .075 .054

C4 .696 -.144 .262 -.121 .081 .161

C5 .800 -.146 .027 -.370 -.054 .022

D1 .689 -.176 .093 .113 -.011 .361

D2 .762 .124 .104 .074 -.250 .292

D3 .735 -.096 -.060 -.132 -.235 .189

D4 .757 .045 -.222 -.252 -.216 .182

D5 .722 .128 .232 -.253 .011 .181

D6 .680 .019 .120 -.330 .115 .078

E1 .612 .391 .300 .186 -.092 .034

E2 .497 .346 .187 .432 -.202 .261

E3 .624 .436 .022 .042 -.303 -.013

E4 .586 .295 .071 -.016 -.252 -.046

E5 .700 .213 .131 -.015 -.257 -.185

Extraction Method: Principal Component Analysis( a. 6 components extracted)

Source: Survey data

91

Table 5.5: Rotated Component Matrixa

Factors Component

1 2 3 4 5 6

A1 .174 .430 .102 .166 .681 .121

A2 .152 .264 .153 .044 .766 .232

A3 .202 .696 .252 .020 .279 .298

A4 .175 .761 .167 .065 .296 .255

A5 .212 .531 .213 .254 .533 -.002

A6 .306 .700 .286 .134 .180 .120

A7 .301 .623 .255 .097 .279 .133

A8 .345 .233 .651 .206 .033 .091

A9 .367 .192 .642 .213 .202 -.029

A10 .232 .080 .564 .316 .323 .116

A11 .082 .428 .535 .241 .140 .251

A12 .042 .187 .738 .110 .219 .218

A13 .231 .584 .446 .312 .118 .103

A14 .210 .481 .517 .226 .082 .266

A15 .229 .237 .613 .290 -.044 .219

A16 .476 .197 .563 .126 .253 .021

B1 .400 .083 .243 .210 .592 .293

B2 .477 .065 .217 .135 .553 .497

B3 .400 .229 .231 .213 .379 .572

B4 .388 .219 .237 .295 .308 .526

B5 .318 .406 .198 .229 .231 .571

B6 .253 .378 .167 .318 .208 .613

C1 .635 .296 .258 .086 .275 .243

C2 .649 .306 .270 .083 .167 .356

C3 .692 .264 .185 .117 .266 .238

C4 .614 .163 .156 .210 .362 .134

C5 .693 .429 .169 .139 .112 .279

D1 .432 .340 .114 .325 .481 -.062

D2 .398 .353 .142 .621 .258 .075

D3 .475 .519 .069 .340 .169 .131

D4 .486 .606 .198 .340 -.022 .098

D5 .658 .145 .252 .375 .118 .129

D6 .651 .199 .288 .157 .087 .159

E1 .226 -.027 .321 .640 .202 .239

E2 .009 .071 .198 .744 .315 .001

E3 .176 .246 .278 .651 -.056 .278

E4 .237 .215 .210 .514 -.010 .301

E5 .291 .236 .216 .482 .071 .479

Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization.

a. Rotation converged in 14 iterations. Source: Survey data

92

Table 5.6: Component Transformation Matrix

Component 1 2 3 4 5 6

1 .505 .468 .412 .360 .348 .325

2 -.164 -.300 .516 .581 -.526 -.047

3 .376 -.751 -.279 .262 .306 .231

4 -.692 -.028 .101 .288 .653 -.030

5 .142 -.342 .672 -.526 .252 -.267

6 .277 .097 -.158 .322 .139 -.875

Extraction Method: Principal Component Analysis.

Rotation Method: Varimax with Kaiser Normalization.

Source: Survey data

On the basis of varimax rotation with Kaiser Normalisation six factors have

been emerged (table 5.3 and 5.4). Each factor is constituted by all those variables

that have factor loading greater than or equal to 0.5. After rotation factor one

account for 15.67 percent of the variance: factor two accounts for 14.332 percent

of variance; factor three accounts for 11.818 percent; factor four accounts for

10.114 percent of variance; factor five accounts for 9.784; factor six accounts for

7.971 percent of variance; and all the six factors together explained for 69.732

percent of variance. The identified factors with the associated variables and factor

loadings are given in the table 5.7

It is evident from the analysis that the changing preferences of the mutual

fund investors create many new needs, which may be controlled by key

determinants. The table 5.7 depicts that the first factor identified with key

attributes of mutual fund products are disclosure of deviation of Investments

from the original pattern; disclosure of the method and the periodicity of the

schemes sales and repurchases in the offer documents; disclosure of periodicity

of valuation in the advertisement disclosure of investment objective in the

advertisement; disclosure of NAV in every trading day; listing on stock exchange;

93

and technology enabled services. These attributes can be grouped under Factor- 1

and termed as Service Quality.

Table 5.7 Key factors influencing selection of mutual fund products

Component Factor Variables Factor

Loadings

F1 Service quality

Disclosure of deviation of Investments 0.693

Disclosure of the method and the

Periodicity of the schemes 0.692

Disclosure of periodicity of Valuation in

the advertisement 0.649

Disclosure of Investment objective in

the advertisement 0.635

Disclosure of NAV in every Trading day 0.614

Listing on stock exchange 0.658

Technology Enabled Services 0.651

F2 Fund quality

Schemes portfolio/constituent 0.761

Favourable rating by a rating agency 0.700

Schemes expense ratio 0.696

Innovativeness of the scheme 0.623

Liquidity 0.584

MF’s investors grievance redressal

machinery 0.606

Service standard 0.519

F3 Core of the

product

Tax Benefit 0.738

Loan facility 0.651

Option to Switch scheme 0.642

Insurance facility 0.613

Annual return/Dividend 0.564

Safety 0.563

Capital Appreciation 0.535

Performance guarantee 0.517

F4 Promotional mix

Brokers/Agent 0.744

Reference Group 0.651

Advertisement 0.640

Early bird incentives 0.514

Professional financial advisor 0.621

94

F5 Investor’s

confidence

Funds reputation or brand name 0.766

Past Fund performance Record 0.681

Withdrawal facilities/redemption

features 0.533

Ownership of the company (Private/

public) 0.592

Reputation of the Sponsoring

firm/Brand name/Track record 0.553

F6 Fund sponsor

quality

Sponsor has a well developed Research

& Infrastructure 0.613

Net worth of the sponsor 0.572

Sponsors expertise in managing Money 0.571

Sponsor has a well developed

Agency/network 0.526

Source: Survey data

The second factor is designated Fund Quality on the basis of the loaded

variables. The data set of the Factor-2 loading indicates that among various

product attributes, schemes portfolio/constituents; favourable rating by a rating

agency; schemes expense ratio; innovativeness of the scheme; liquidity; mutual

fund investors grievance redressal machinery; and service standard are found to

be important by customers for making a brand choice.

Factor- 3 shows significance for tax benefit; loan facility; option to switch

scheme; insurance facility; annual return/dividend; safety; capital Appreciation;

and performance guarantee. These attributes can be grouped under Factor-3 and

termed as core of the product. These are the core parts of a mutual fund product

which are common expectation of any customer While, making a purchase

decision.

Factor-4 includes attributes such as brokers/agents; reference group;

advertisement; early bird incentives; and professional financial advisor. This

element is more important in a competitive market where most of the product

offerings are similar and the customer finds it difficult to take a decision. In an

advanced and matured market like that of urban India what needs to be done for

95

the success of a mutual fund is a high degree of promotional mix than the current

practice. Present communication and promotions about various mutual fund

products in India are informative only. As the market has advanced to a higher

level what needs to be done is to promote own brands than promoting the

category only for attracting investors of mutual fund.

Factor-5 clearly indicates the combination of five attributes such as funds

reputation/brand name; past fund performance record; withdrawal facilities/

redemption features; ownership of the company (Private/ public); and reputation

of the sponsoring firm/brand name/track record. This factor is termed as

Investor’s Confidence, which is built over a period of time due to consistency in

performance and transparency in market behaviour.

The last and sixth factor is designated as Fund Sponsor Quality on the

basis of the factor loadings. The set of the Factor-6 loading indicates that the

variables such as sponsor has a well developed research & infrastructure; net

worth of the sponsor; sponsors expertise in managing money; and sponsor has a

well developed agency/network are found to be important by customers for

deciding their buying decision.

The six factors explained above are the proposed product combinations of

a mutual fund offering to the investors. If the product designers will be careful

about these key issues while, designing a brand of mutual fund then only the

brand will see a higher customer response and enjoy market success.

5.2.2 Fund Preferences of Mutual Fund Investors

The second factor considered under fund selection behaviour is the fund

preferences of mutual fund investors. In order to assess the fund preferences of

the mutual fund investors, various schemes of mutual funds are classified under

two groups namely schemes of mutual funds on the basis of maturity period, and

schemes of mutual funds on the basis of investment objectives. Here, the

researcher made an attempt to study the fund preference of mutual fund

96

investors by analysing the pattern of selecting different schemes of mutual funds;

and associating their pattern of selection with their investment objectives, time

horizon and risk perception.

5.2.2.1 Selection of Mutual Fund Schemes

The table 5.8 and 5.9 shows the number of respondents who have opted

different schemes of mutual funds on the basis of maturity period, and

investment objectives respectively.

Table 5.8 Number of respondents opted different schemes of Mutual funds on the

basis of maturity period

Sl

No Schemes

Opted Not opted

Total

Frequency Percentage Frequency Percentage

1 Open-ended

schemes 305 76.25 95 23.75 400

2 Close-ended

schemes 45 11.25 355 88.75 400

3 Interval schemes 25 6.25 375 93.75 400

Source: Survey data

The table 5.8 reveals that out of 400 sample respondents

305(76.25percent) respondents opted open-ended scheme. But in the case of

close-ended scheme, the percentage share in this respect is only 11.25. Similarly,

only 6.25 percent of respondents have opted interval schemes.

97

Table 5.9 Number of respondents opted different schemes of Mutual funds on the

basis of investment objectives

Sl.

No Schemes

Opted Not opted Total

Frequency Percentage Frequency Percentage

1 Growth-fund 296 74 104 26 400

2 Income-fund 42 10.50 358 89.5 400

3 Balanced-fund 40 10 360 90 400

4 Tax saving schemes 91 22.75 309 77.25 400

5 Money market funds 27 6.75 373 93.25 400

6 Sectoral based

funding 25 6.25 375 93.75 400

7 Index-Funds 23 5.75 377 94.25 400

8 Exchange Traded

funds 65 16.25 335 83.75 400

9 Capital protection

scheme 24 6 376 94 400

10 Fund of funds 11 2.75 389 97.25 400

Source: Survey data

The study on the pattern of fund preference of mutual fund investors on

the basis of investment objectives (table 5.9) indicates that 74 percent of the

respondents opted for growth-fund where as the percentage share of other types

of funds in this respect is comparatively very low. The percentage of respondents

opted income-fund is only 10.5 and the percentage share of balanced-fund is only

10. However, the percentage of respondents opted for tax saving schemes is

22.75 and exchange traded fund is 16.25. But, the percentage share of

respondents opted money market fund, sectoral fund, index fund, capital

protection scheme, and fund of funds is below 10 percent, and it indicates that

majority of the investors have not shown interest in opting such schemes.

98

5.2.2.2 Association between Fund Preferences of Mutual Fund Investors and

their Objectives of Investment

In order to study the influence of investment objectives of mutual fund

investors on their fund preferences, Friedman’s test has been conducted. The

association test has been done in accordance with the fund preferences on the

basis of maturity period and investment objectives. The table 5.10 and 5.11

presents the Friedman’s test to associate the investment objectives with fund

preferences on the basis of maturity period.

Ha: There is a significant difference in the ranking of investment objectives

of the mutual fund investors across their fund preferences.

Table 5.10 Investment objectives Vs Funds preference on the basis of Maturity

period

Objectives Open-ended Close-ended Interval schemes

Mean Rank Mean Rank Mean Rank

Rank Return 5.18 1 5.02 1 4.56 2

Rank Liquidity 3.07 4 3.31 3 3.29 3

Rank Safety 4.41 2 4.96 2 5.40 1

Rank Tax benefits 2.15 6 3.09 4 2.87 6

Rank Capital app 3.65 3 2.33 5 2.88 5

Rank Meet

Contingencies 2.59 5 2.22 6 2.99 4

Source: Survey data

Table 5.11 Equal Variance Test: Fund preference on the basis of Maturity period

Group N Missing Median 25% 75%

Col 1 6 0 3.2 2.333 4.956

Col 2 6 0 3.14 2.882 4.559

Col 3 6 0 3.294 2.655 4.419

‘F’ value Table Value d.f. P value Sig. 5 % level Inference

0.333 5.991 2 0.956 Not significant Ha rejected

Source: Survey data

99

The calculated value of ‘F’ (0.333) with 2 degrees of freedom is less than

the tabulated value of chi-square (5.991) at 5 percent level of significance and

therefore, no significant difference in the ranking of investment objectives across

fund preferences on the basis of maturity period. Thus, the null hypothesis is

accepted and alternative hypothesis is rejected.

Table 5.12 Investment objectives Vs Fund preference on the basis of Investment

Objectives

FUNDS

INVESTMENT OBJECTIVES

Return Liquidity Safety Tax

benefit

Capital

appreciation

Provision for

Contingencies

Growth-

fund

Mean 5.28 2.99 4.42 2.18 3.59 2.66

Rank 1 4 2 6 3 5

Income-

fund

Mean 5.29 2.93 4.43 2.10 4.19 2.26

Rank 1 4 2 6 3 5

Balanced-

fund

Mean 4.73 3.88 4.43 2.25 3.10 2.55

Rank 1 3 2 6 4 5

Tax

schemes

Mean 4.89 2.91 3.92 3.11 3.49 2.93

Rank 1 6 2 4 3 5

Money

market

Mean 4.48 3.85 4.67 1.94 3.33 2.82

Rank 2 3 1 6 4 5

Sectoral

based

Mean 4.81 3.19 4.31 2.06 3.56 3.06

Rank 1 4 2 6 3 5

Index

funds

Mean 5.47 3.47 4.12 2.12 3.76 2.06

Rank 1 4 2 5 3 6

Exchange

traded

Mean 5.11 2.88 5.17 2.49 3.77 2.63

Rank 2 4 1 6 3 5

Capital

Protection

scheme

Mean 4.98 3.11 4.64 2.56 3.07 2.73

Rank 1 3 2 6 4 5

Fund of

funds

Mean 5.71 1.71 5.00 3.43 3.86 1.29

Rank 1 5 2 4 3 6

Source: Survey data

100

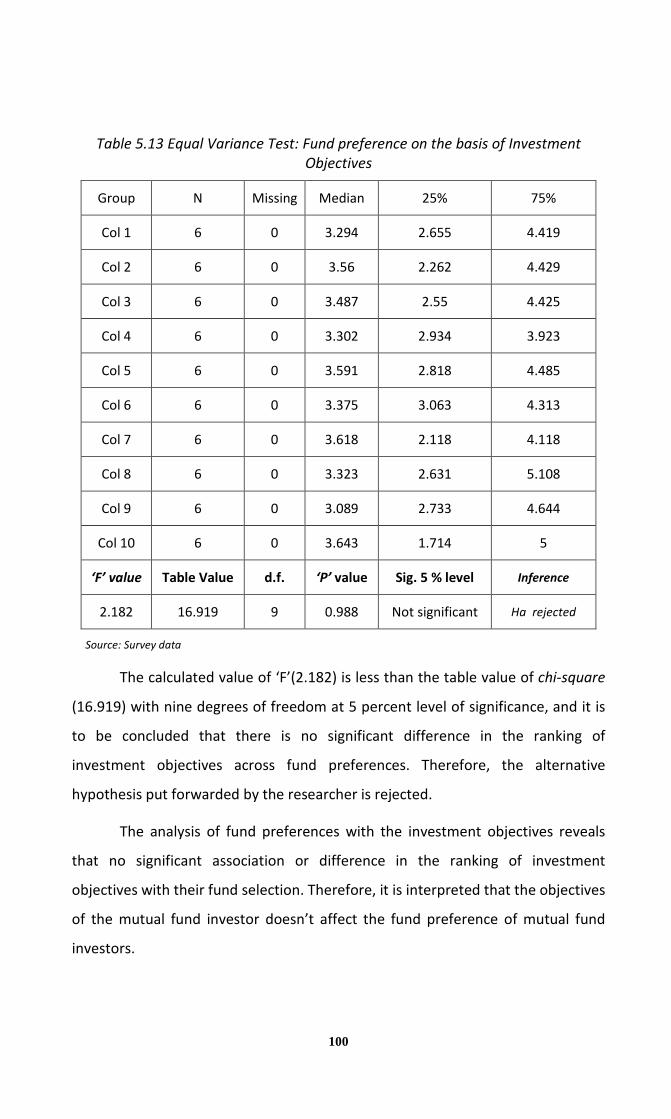

Table 5.13 Equal Variance Test: Fund preference on the basis of Investment

Objectives

Group N Missing Median 25% 75%

Col 1 6 0 3.294 2.655 4.419

Col 2 6 0 3.56 2.262 4.429

Col 3 6 0 3.487 2.55 4.425

Col 4 6 0 3.302 2.934 3.923

Col 5 6 0 3.591 2.818 4.485

Col 6 6 0 3.375 3.063 4.313

Col 7 6 0 3.618 2.118 4.118

Col 8 6 0 3.323 2.631 5.108

Col 9 6 0 3.089 2.733 4.644

Col 10 6 0 3.643 1.714 5

‘F’ value Table Value d.f. ‘P’ value Sig. 5 % level Inference

2.182 16.919 9 0.988 Not significant Ha rejected

Source: Survey data

The calculated value of ‘F’(2.182) is less than the table value of chi-square

(16.919) with nine degrees of freedom at 5 percent level of significance, and it is

to be concluded that there is no significant difference in the ranking of

investment objectives across fund preferences. Therefore, the alternative

hypothesis put forwarded by the researcher is rejected.

The analysis of fund preferences with the investment objectives reveals

that no significant association or difference in the ranking of investment

objectives with their fund selection. Therefore, it is interpreted that the objectives

of the mutual fund investor doesn’t affect the fund preference of mutual fund

investors.

101

5.2.2.3 Association between Fund Preferences of Mutual Fund Investors and

their Time Horizon

Here, the basic objective is to assess the fund preferences of mutual fund

investors in relation to their time horizon of investments. It is assumed that the

fund preferences of mutual fund investors depend on their level of time horizon

of investments. So, the researcher made an attempt to associate the fund

preferences of mutual fund investors with their time horizon of investments

(Table 5.14 & 5.15). Due to the lack of availability of sufficient number of

respondents opted for all the schemes, the analysis has been confined to selected

funds viz., Open-end, Close-end, Growth-fund, Income-fund, balanced-fund, Tax

saving fund and Exchange traded fund.

Ha: The fund preference of mutual fund investors depends on their time

horizon

Table 5.14 Fund preferences Vs Time horizon of Mutual Fund investors

Fund Time Period Opted / not

Total Yes No

Open-end

Below 1 year Count 31 11 42

% within Time Horizon 73.8% 26.2% 100.%

1 to 3 years Count 158 34 192

% within Time Horizon 82.3% 17.7% 100%

3 to 6 years Count 68 28 96

% within Time Horizon 70.8% 29.2% 100%

6 to 9 years Count 20 5 25

% within Time Horizon 80.0% 20.0% 100%

9 years & Above Count 28 17 45

% within Time Horizon 62.2% 37.8% 100%

Total Count 305 95 400

% within Time Horizon 76.2% 23.8% 100.%

Close-end

Below 1 year Count 6 36 42

% within Time Horizon 14.2% 85.7% 100%

1 to 3 years Count 10 182 192

% within Time Horizon 5.2% 94.7% 100.%

3 to 6 years Count 18 78 96

% within Time Horizon 18.7% 81.2% 100.%

6 to 9 years Count 5 20 25

% within Time Horizon 20% 80% 100.%

9 years & Above Count 6 39 45

% within Time Horizon 13.3% 86.7% 100.%

Total Count 45 355 400

% within Time Horizon 11.2% 88.8% 100%

102

Growth-fund

Below 1 year Count 32 10 42

% within Time Horizon 76.2% 23.8% 100.0%

1 to 3 years Count 151 41 192

% within Time Horizon 78.6% 21.4% 100.0%

3 to 6 years Count 62 34 96

% within Time Horizon 64.6% 35.4% 100.0%

6 to 9 years Count 15 10 25

% within Time Horizon 60.0% 40.0% 100.0%

9 years & Above Count 36 9 45

% within Time Horizon 80.0% 20.0% 100.0%

Total Count 296 104 400

% within Time Horizon 74.0% 26.0% 100.0%

Income-fund

Below 1 year Count 7 35 42

% within Time Horizon 16.7% 83.3% 100.%

1 to 3 years Count 19 173 192

% within Time Horizon 9.89% 90.1% 100.%

3 to 6 years Count 5 91 96

% within Time Horizon 5.2% 94.8% 100.%

6 to 9 years Count 6 19 25

% within Time Horizon 24% 76% 100.%

9 years & Above Count 5 40 45

% within Time Horizon 11.1% 88.8% 100.%

Total Count 42 358 400

% within Time Horizon 10.5% 89.5% 100.%

Balanced-

fund

Below 1 year Count 6 36 42

% within Time Horizon 2.38% 85.7% 100.%

1 to 3 years Count 11 181 192

% within Time Horizon 5.72% 94.2% 100.%

3 to 6 years Count 13 83 96

% within Time Horizon 13.5% 86.4% 100.%

6 to 9 years Count 5 20 25

% within Time Horizon 20% 80% 100.%

9 years & Above Count 5 40 45

% within Time Horizon 11.1% 88.9% 100.%

Total Count 40 360 400

% within Time Horizon 10.0% 90.0% 100.%

Tax Saving

Below 1 year Count 6 33 42

% within Time Horizon 14.2% 78.5% 100.%

1 to 3 years Count 39 153 192

% within Time Horizon 20.3% 79.6% 100.%

3 to 6 years Count 30 66 96

% within Time Horizon 31.2% 68.8% 100.%

6 to 9 years Count 6 19 25

% within Time Horizon 24.0% 76.0% 100.%

9 years & Above Count 10 35 45

% within Time Horizon 22.2% 77.8% 100.%

Total Count 91 309 400

% within Time Horizon 22.8% 77.2% 100.%

103

ETF

Below 1 year Count 6 36 42

% within Time Horizon 14.28% 86.05% 100.0%

1 to 3 years Count 33 159 192

% within Time Horizon 17.18% 82.81% 100.0%

3 to 6 years Count 15 81 96

% within Time Horizon 15.6% 84.4% 100.0%

6 to 9 years Count 6 19 25

% within Time Horizon 24% 76% 100.0%

9 years & Above Count 5 40 45

% within Time Horizon 11.11% 88.89% 100.0%

Total Count 65 335 400

% within Time Horizon 16.2% 83.8% 100.0%

Source: Survey data

Table: 5.15 Chi- square test for dependence of Fund preferences Vs Time horizon

of Mutual Fund investors

Funds Calculated value

of chi- square

Table

Value

Degrees

of

freedom

P value significance

at 5 % level Inference

Open-end 10.647 5.991 2 0.031 *Significant Ha is accepted

Close-end 20.594 5.991 2 0.001 *Significant Ha is accepted

Growth 10.072 5.991 2 0.039 *Significant Ha is accepted

Income 7.798 5.991 2 0.020 *Significant Ha is accepted

Balanced 6.686 5.991 2 0.035 *Significant Ha is accepted

Tax schemes 9.881 5.991 2 0.042 *Significant Ha is accepted

ETF 1.719 5.991 2 0.423 NS Ha is rejected

Source: Survey data

The table 5.14 depicts that out of 305 mutual fund investors who have

opted open-ended schemes, 158 investors opted for a period of one to three

years. But, in the case of investors who have not opted open-ended scheme, out

of 95 investors 34 investors prefer a time period of one to three years. The chi-

square test reveals that the calculated value (10.647) is more than the tabulated

value (5.991) at two degrees of freedom with five percent level of significance,

and it falls in the critical region, the alternative hypothesis is to be accepted.

104

But, in the case of close-ended fund, out of 355 investors (majority) who

have not opted the scheme 182 investors prefer a time period of one to three

years while, out of 45 investors who have opted close-ended scheme, 18

investors prefer a time period of three to six years. The statistical test shows that

the calculated value of chi- square (20.594) is more than the tabled value (5.991)

and thus, the alternative hypothesis is accepted.

The analysis of growth-fund reveals that out of 296 investors who have

opted growth-fund schemes, 151 investors prefer a time period of one to three

years. In the case of investors who have not opted growth-fund, out of 104

investors, 41 investors prefer a time period of one to three years. The chi-square

test shows that the calculated value (10.072) is greater than the tabulated value

(5.991) at two degrees of freedom with five percent level of significance, and it

falls in the critical region, the alternative hypothesis is to be accepted.

Out of 358 investors who have not opted income-fund schemes, 173

investors prefer a time period of one to three years. But, out of 42 investors who

have opted income-fund scheme, 19 investors prefer a time period of one to

three years. The calculated value of the chi- square (7.798) is greater than the

tabled value (5.991) at two degrees of freedom with five percent level of

significance, and it falls in the critical region, the alternative hypothesis is to be

accepted.

In the case of balanced-fund out of 360 investors who have not opted

balanced-funds, 181 investors prefer a time period of one to three years.

Similarly, out of 40 investors who have opted balanced-fund, 13 investors prefer a

time period of three to six years. The statistical test shows that the chi-square

value (6.686) is greater than the tabled value at two degrees of freedom with five

percent level of significance, and it falls in the critical region, the alternative

hypothesis is to be accepted.

In the case of tax saving fund, out of 309 investors who have not opted the

scheme, 153 investors prefer a time period of one to three years. Similarly, out of

105

91 investors who have opted the tax saving scheme, 39 investors prefer a time

period of one to three years. Here, the chi-square value (9.881) is more than the

tabled value (5.991) and thus, the alternative hypothesis is accepted.

Out of 335 investors who have not opted ETF, 159 investors prefer a time

period of one to three years. Similarly, out of 65 investors who have not opted

ETF, 33 investors prefer a time period of one to three years. The statistical test

shows that that the calculated value of chi- square (1.719) is less than the tabled

value (5.991) and thus, the alternative hypothesis is rejected.

The foregoing analysis of association between fund preferences and time

horizon of mutual fund investors reveals that out of seven funds, significant

association has been observed in six funds. No significant association has been

found in the case of ETF. Therefore, the researcher has accepted the alternative

hypothesis and concluded that fund preferences of mutual fund investors depend

on their time horizon of investments.

5.2.2.4 Association between Fund Preferences of Mutual Fund Investors and

their Risk Perception

It is assumed that the fund selection of mutual fund investors depend on

their level of risk perception. So the researcher made an attempt to associate the

fund preferences of mutual fund investors with their risk perception (table 5.16).

Due to the lack of availability of sufficient number of respondents opted for

certain schemes, the analysis has been restricted to selected funds such as Open-

end, Close-end, Growth-fund, Income-fund, Balanced-fund, Tax saving fund and

Exchange traded fund.

Ha: The fund preference of mutual fund investors depends on their risk

perception.

106

Table: 5.16 Association between Fund Preferences of Mutual Fund Investors and

their Risk Perception

Fund Level of risk Opted / Not

Total Yes No

Open-end

Low Count 13 17 30

% within Risk MF group 43.3% 56.7% 100.0%

Medium Count 163 51 214

% within Risk MF group 76.2% 23.8% 100.0%

High Count 129 27 156

% within Risk MF group 82.7% 17.3% 100.0%

Total Count 305 95 400

% within Risk MF group 76.2% 23.8% 100%

Close-end

Low Count 6 24 30

% within Risk MF group 20.0% 80.0% 100.0%

Medium Count 21 193 214

% within Risk MF group 9.8% 90.2% 100.0%

High Count 18 138 156

% within Risk MF group 11.5% 88.5% 100.0%

Total Count 45 355 400

% within Risk MF group 11.2% 88.8% 100%

Growth-

fund

Low Count 16 14 30

% within Risk MF group 53.3% 46.7% 100.0%

Medium Count 148 66 214

% within Risk MF group 69.2% 30.8% 100.0%

High Count 132 24 156

% within Risk MF group 84.6% 15.4% 100.0%

Total Count 296 104 400

% within Risk MF group 74.0% 26.0% 100%

Income-

fund

Low Count 6 24 30

% within Risk MF group 20% 80% 100.0%

Medium Count 27 187 214

% within Risk MF group 13.5% 85.9% 100.0%

High Count 9 147 156

% within Risk MF group 5.8% 94.2% 100.0%

Total Count 42 358 400

% within Risk MF group 10.5% 89.5% 100%

107

Balanced-

fund

Low Count 6 24 30

% within Risk MF group 20.0% 80.0% 100.0%

Medium Count 23 191 214

% within Risk MF group 10.7% 89.3% 100.0%

High Count 11 145 156

% within Risk MF group 7.1% 92.9% 100.0%

Total Count 40 360 400

% within Risk MF group 10.0% 90.0% 100%

Tax Saving

Low Count 6 24 30

% within Risk MF group 20.0% 80.0% 100.0%

Medium Count 51 163 214

% within Risk MF group 23.8% 76.2% 100.0%

High Count 34 122 156

% within Risk MF group 21.8% 78.2% 100.0%

Total Count 91 309 400

% within Risk MF group 22.8% 77.2% 100%

ETF

Low Count 7 23 30

% within Risk MF group 23.3% 76.7% 100.0%

Medium Count 31 183 214

% within Risk MF group 14.5% 85.5% 100.0%

High Count 27 129 156

% within Risk MF group 17.3% 82.7% 100.0%

Total Count 65 335 400

% within Risk MF group 16.2% 83.8% 100%

Source: Survey data

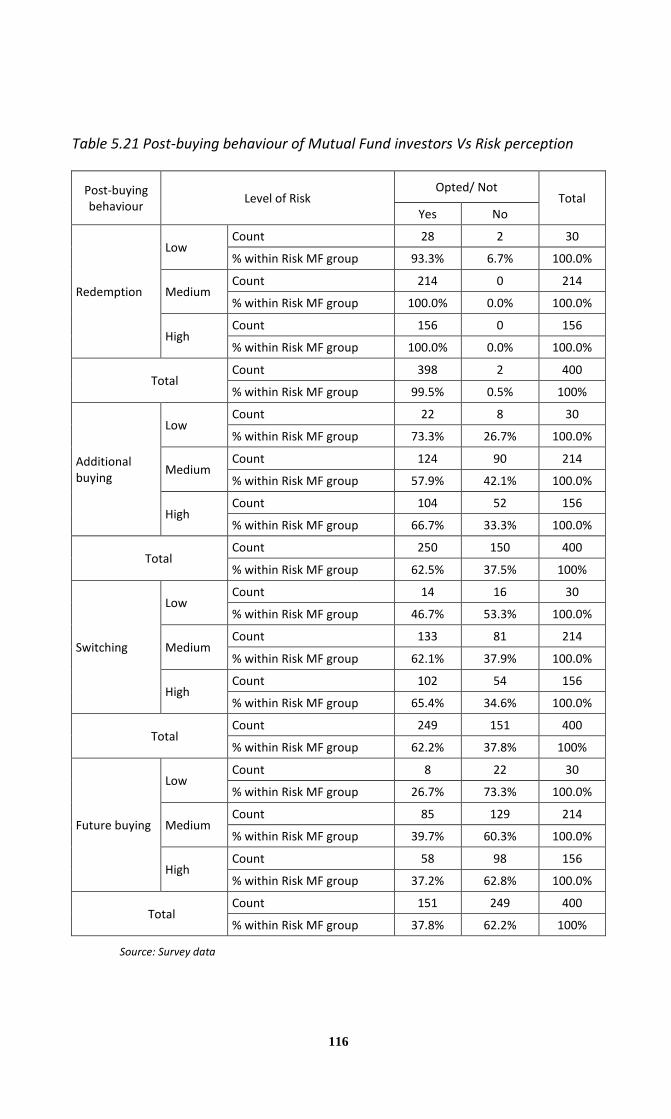

The table 5.16 depicts that out of 305 mutual fund investors who have

opted open-ended schemes, 163 investors fall under medium level of risk group.

But, in the case of investors who have not opted open-ended scheme, out of 95

investors 51 investors fall under the medium level of risk group. The chi-square

test reveals that the calculated value (19.621) is more than the tabulated value

(5.991) at two degrees of freedom with five percent level of significance, and it

falls in the critical region, the alternative hypothesis is to be accepted.

108

Table 5.17 Chi-square tests for dependence of Fund preferences Vs

Risk perception of MF investors

Funds Calculated value

of chi- square

Table

Value

Degrees of

freedom ‘P’ value

Significance

at 5 % level Inference

Open-end 19.621 5.991 2 0.000 *Significant Ha is accepted

Close-end 1.405 5.991 2 0.843 NS Ha is rejected

Growth 24.512 5.991 2 0.000 *Significant Ha is accepted

Income 7.344 5.991 2 0.025 *Significant Ha is accepted

Balanced 7.528 5.991 2 0.023 *Significant Ha is accepted

Tax schemes 0.263 5.991 2 0.877 NS Ha is rejected

ETF 3.499 5.991 2 0.174 NS Ha is rejected

Source: Survey data

But, in the case of close-ended fund, out of 355 investors (majority)

who have not opted the scheme, 193 investors belong to medium level of risk

group; While, out of 45 investors who have opted close-ended schemes, 21

investors falls under medium level of risk group. The statistical test shows that

the calculated value of chi- square (1.405) is less than the tabled value (5.991)

and thus the alternative hypothesis is rejected.

The analysis of growth-fund reveals that out of 296 investors who have

opted growth-fund schemes, 148 investors have medium level of risk

perception and 132 investors has high level of risk perception. In the case of

investors who have not opted growth-fund, out of 104 investors, 66 investors

belongs to medium level of risk group. The chi-square test shows that the

calculated value (24.512) is greater than the tabulated value (5.991) at two

degrees of freedom with five percent level of significance, and it falls in the

critical region, the alternative hypothesis is to be accepted.

Out of 358 investors who have not opted income-fund schemes, 187

investors belong to medium level risk group and 147 investors belong to high

109

level risk group. But, out of 42 investors who have opted income-fund scheme,

27 investors belong to medium level of risk group. The calculated value of the

chi- square (7.344) is greater than the tabled value (5.991) at two degrees of

freedom with five percent level of significance, and it falls in the critical region,

the alternative hypothesis is to be accepted.

In the case of balanced-fund, out of 360 investors who have not opted

balanced-funds, 191 investors belong to medium level of risk group and 145

investors coming under high level risk group. Similarly, out of 40 investors

who have opted balanced-fund, 23 investors fall under medium level of risk

group and 11 investors belong to high level risk group. The statistical test

shows that the chi-square value (7.528) is greater than the tabled value at two

degrees of freedom with five percent level of significance, and it falls in the

critical region, the alternative hypothesis is to be accepted.

In the case of tax saving fund out of 309 investors who have not opted

the scheme, 163 investors coming under medium level of risk group and 122

investors belongs to high-level risk group. Similarly, out of 91 investors who

have opted the tax saving scheme, 51 investors belongs to medium level risk

group and 34 investors represented by high-level risk group. Here the chi-

square value (0.263) is less than the tabled value (5.991) and thus, the

alternative hypothesis is rejected.

Out of 335 investors who have not opted ETF, 183 investors belong to

medium level risk group and 129 investors fall under high level risk group.

Similarly, out of 65 investors who have not opted ETF, 31 investors have

medium level of risk perception and 27 investors have high level of risk

perception. The statistical test shows that that the calculated value of chi-

square (3.499) is less than the tabled value (5.991) and thus, the alternative

hypothesis is rejected.

110

The foregoing analysis of association between fund preference and

investment objectives reveals that there is no significant association between

the fund preference of mutual fund investors and their investment objectives.

In the case of time horizon there is a significant association between fund

preferences and time horizon of mutual fund investors in respect of open-end,

close-end, growth, income, balanced and tax saving fund. The analysis of risk

perception and fund preferences indicates that risk perception of investors

depends on fund preferences in respect of open-end, growth-fund, income-

fund and balanced-fund; whereas, no statistical significance has been

observed in the case of close-end, tax saving and ETF.

5.3 Post-buying Behaviour of Mutual Fund Investors

Since, the former part of this chapter has been dealt with the fund

selection behaviour of mutual fund investors, the latter part of the discussion

emphasised on post-buying behavioural aspects. The post-buying behaviour of

investors is referred to as a collective sum of all the behavioural factors

exhibited by the mutual fund investors after investing in mutual funds such as

product performance satisfaction level, redemption factors, switching reasons,

additional buying and future buying intention. In this section the researcher

has made an attempt to study the post-buying behaviour of mutual fund

investors across their time horizon, risk perception and demographic features.

The table 5.18 depicts the post-buying profile of mutual fund investors.

The table 5.18 reveals that out of 400 sample mutual fund investors, 99.5

percent of the respondents has redeemed mutual fund units; and 62.2 percent of

the investors has performed switching of funds.

111

Table 5.18 Number of mutual fund investors opted for Redemption, Additional

buying, Switching of funds and Future buying intention

Post-buying

behavioural factors

Whether

Opted /Not

No of

respondents Percentage

Cumulative

percentage

Redemption of units

Yes 398 99.5 99.5

No 2 0.5 100

Total 400

Switching of funds

Yes 249 62.2 62.2

No 151 37.8 100

Total 400

Additional buying

Yes 250 62.5 62.5

No 150 37.5 100

Total 400

Future buying

intention

Yes 151 37.8 37.8

No 249 62.2 100

Total 400

Source: Survey data

In the case of additional units buying, majority (62.5 percent) of the

investors has bought additional units of mutual fund. However, the study reveals

that majority (62.2 percent) of the respondents had not shown future intention to

buy the mutual fund products.

5.3.1 Association between Post-buying Behavioural Factors of Mutual Fund

Investors and their Time Horizon

In order to analyse whether the time horizon of investments influence

post-buying behavioural factors of mutual fund investors, the association test

between the variables have been performed (Table 5.19 & 5.20).

Ha: The post-buying behaviour of mutual fund investors depends on time

horizon of the investment.

112

Table 5.19 Post-buying behaviour of mutual fund investors Vs Time horizon

Post-buying

behaviour Time Period

Opted/Not Total

Yes No

Redemption

Below 1 year Count 42 0 42

% within Time Horizon 100.0% 0.0% 100.0%

1 to 3 years Count 190 2 192

% within Time Horizon 99.0% 1.0% 100.0%

3 to 6 years Count 96 0 96

% within Time Horizon 100.0% 0.0% 100.0%

6 to 9 years Count 25 0 25

% within Time Horizon 100.0% 0.0% 100.0%

9 years & Above Count 45 0 45

% within Time Horizon 100.0% 0.0% 100.0%

Total Count 398 2 400

% within Time Horizon 99.5% .5% 100%

Additional

buying

Below 1 year Count 20 22 42

% within Time Horizon 47.6% 52.4% 100.0%

1 to 3 years Count 116 76 192

% within Time Horizon 60.4% 39.6% 100.0%

3 to 6 years Count 62 34 96

% within Time Horizon 64.6% 35.4% 100.0%

6 to 9 years Count 16 9 25

% within Time Horizon 64.0% 36.0% 100.0%

9 years & Above Count 36 9 45

% within Time Horizon 80.0% 20.0% 100.0%

Total Count 250 150 400

% within Time Horizon 62.5% 37.5% 100%

Switching

Below 1 year Count 20 22 42

% within Time Horizon 47.6% 52.4% 100.0%

1 to 3 years Count 129 63 192

% within Time Horizon 67.2% 32.8% 100.0%

3 to 6 years Count 55 41 96

% within Time Horizon 57.3% 42.7% 100.0%

6 to 9 years Count 18 7 25

% within Time Horizon 72.0% 28.0% 100.0%

9 years & Above Count 27 18 45

% within Time Horizon 60.0% 40.0% 100.0%

Total Count 249 151 400

% within Time Horizon 62.2% 37.8% 100%

113

Future buying

Below 1 year Count 13 29 42

% within Time Horizon 31.0% 69.0% 100.0%

1 to 3 years Count 63 129 192

% within Time Horizon 32.8% 67.2% 100.0%

3 to 6 years Count 39 57 96

% within Time Horizon 40.6% 59.4% 100.0%

6 to 9 years Count 11 14 25

% within Time Horizon 44.0% 56.0% 100.0%

9 years & Above Count 25 20 45

% within Time Horizon 55.6% 44.4% 100.0%

Total Count 151 249 400

% within Time Horizon 37.8% 62.3% 100%

Source: Survey data

Table 5.20 Chi- square test for dependence of Post-buying behaviour of Mutual

Fund investors Vs Time horizon

Variables

Calculated

value of

chi- square

Table

Value

Degrees

of

freedom

‘P’ value significance

at 5 % level Inference

Additional buying 10.406 9.488 4 0.034 NS Ha is rejected

Switching 7.93 9.488 4 0.094 NS Ha is rejected

Future

preferences 9.642 9.488 4 0.047* *Significant Ha is accepted

Source: Survey data

The table 5.19 reveals that out of 398 mutual fund investors who have

redeemed their mutual fund units, 190 (47.5percent) investors belong to one to

three years time horizon of investments. The investors who have redeemed

mutual fund units belong to three to six years of investment were 24.12 percent.

Out of 250 mutual fund investors who have bought additional units of

mutual funds, 116 (29 percent) investors have reported time horizon of one to

three years. The investors belong to three to six years of time horizon of

investment were 62 (24.8 percent). But, out of 150 mutual fund investors who

have not bought any additional units of mutual fund, 76 (50.67 percent) of

investors belong to time horizon of one to three years. The statistical test shows

114

no significant association between time horizon of investment and additional

units bought by the mutual fund investors (Table 5.20).

In the case of 151 mutual fund investors who have expressed future

intention to invest in mutual funds, 63 (41.72 percent) investors came under the

time horizon of one to three years. The investors with time horizon of three to six

years who have expressed future intention to buy the mutual fund were 39 (258)

percent. But, out of 249 investors who had not expressed future intention to buy,

129 (51.8) of investors represented by the time horizon of one to three years. The

statistical test shows that calculated value of chi-square (9.642) is greater than

the tabulated value (9.488) and falls in the rejection region with four degrees of

freedom at five percent level of significance. Thus, the null hypothesis is rejected

and it is concluded that there exist a significant association between time horizon

and future buying intention of mutual fund investors.

Out of 249 mutual fund investors who had switched their funds 129 (51.8

percent) investors account for time horizon of one to three years. But out of 151

investors who had not switched their funds, 63 (41.72 percent) investors belongs

to time horizon of one to three years. No significant association has been

observed between switching of funds and their time horizon.

The foregoing analysis reveals that out of four variables of post-buying

behaviour of mutual fund investors, statistically significant association has been

found in the future buying intention only. In the case of redemption, majority of

the investors who have redeemed the mutual fund units belong to the time

horizon of one to six years. However, no significant association has been observed

in the case of additional units buying and switching of funds. Therefore, it can be

concluded that time horizon influences redemption behaviour and future buying

preferences of mutual fund investors.

115

5.3.2 Association between Post-buying Behaviour of Mutual Fund Investors

and their Risk Perception

Risk perception of mutual fund investors is one of the important factors

that affect post-buying behaviour of mutual fund investors. The post-buying

behavioural factors such as redemption, switching, additional units buying and

future preferences may have an association with risk perception of the investors.

Therefore, the researcher has made an attempt to test the dependence of the risk

perception of mutual fund investors with their post-buying behavioural factors

(Table 5.21 & 5.22).

Ha: The post-buying behaviour of mutual fund investors depends on their

risk perception.

The table 5.21 reveals that out of 250 investors who have bought

additional units of mutual fund, 49.6 percent of them represented by medium

level of risk perception, and 41.6 percent of them belongs to high-level risk group.

But, out of 150 investors who haven’t bought additional units, 90 investors belong

to medium level risk group and 52 investors represented by high level risk groups.

The statistical test shows no significant association between risk group and

additional units buying (Table 5.22).

In the case of future intention to buy, out of 151 investors having interest

in future buying of mutual fund, 85 investors belong to medium level risk

perception and 58 investors having high-level risk perception. Similarly, out of 249

investors who didn’t have any future buying intention, 51.8 percent of them

represented by medium level risk group and 39.35 percent accounted by high

level risk group. However, chi-square test shows no significant association

between future buying intention of mutual fund investors and their risk

perception (Table 5.22).

116

Table 5.21 Post-buying behaviour of Mutual Fund investors Vs Risk perception

Post-buying

behaviour Level of Risk

Opted/ Not Total

Yes No

Redemption

Low Count 28 2 30

% within Risk MF group 93.3% 6.7% 100.0%

Medium Count 214 0 214

% within Risk MF group 100.0% 0.0% 100.0%

High Count 156 0 156

% within Risk MF group 100.0% 0.0% 100.0%

Total Count 398 2 400

% within Risk MF group 99.5% 0.5% 100%

Additional

buying

Low Count 22 8 30

% within Risk MF group 73.3% 26.7% 100.0%

Medium Count 124 90 214

% within Risk MF group 57.9% 42.1% 100.0%

High Count 104 52 156

% within Risk MF group 66.7% 33.3% 100.0%

Total Count 250 150 400

% within Risk MF group 62.5% 37.5% 100%

Switching

Low Count 14 16 30

% within Risk MF group 46.7% 53.3% 100.0%

Medium Count 133 81 214

% within Risk MF group 62.1% 37.9% 100.0%

High Count 102 54 156

% within Risk MF group 65.4% 34.6% 100.0%

Total Count 249 151 400

% within Risk MF group 62.2% 37.8% 100%

Future buying

Low Count 8 22 30

% within Risk MF group 26.7% 73.3% 100.0%

Medium Count 85 129 214

% within Risk MF group 39.7% 60.3% 100.0%

High Count 58 98 156

% within Risk MF group 37.2% 62.8% 100.0%

Total Count 151 249 400

% within Risk MF group 37.8% 62.2% 100%

Source: Survey data

117

Table 5.22 Chi-square test for dependence of Post-buying behaviour of Mutual

Fund investors Vs Risk perception

Variables

Calculated

value of

chi- square

Table

Value

Degrees

of

freedom

‘P’ value Significance

at 5 % level Inference

Additional buying 5.901 5.991 2 0.052 NS Ha is rejected

Switching 2.163 5.991 2 0.339 NS Ha is rejected

Future

preferences 1.106 5.991 2 0.575 NS Ha is rejected

Source: Survey data

Out of 249 mutual fund investors who have switched their funds, 53.41

percent belongs to medium level risk group and 40.96 percent constituted by

high-level risk group. Similarly, out of 151 mutual fund investors who didn’t

switch their funds, 53.64 percent accounted by medium level of risk perception

and 35.76 percent constituted by high level risk group. However, no significant

association has been observed between risk perception and switching of fund

(Table 5.22).

In the case of redemption of mutual fund units out of 398 mutual fund

investors who have redeemed their mutual fund units, 53.76 percentage of them

belongs to medium level of risk group and 39.19 percent represented by high

level risk group.

The foregoing analysis indicates that the investors with medium and high

level of risk perception have shown both features (Yes/No) of post-buying

behavioural factors such as additional units buying, future buying intention and

switching of fund. But in the case of redemption factors majority of the investors

who have redeemed their units belong to medium and high level risk groups.

However, the statistical test shows that risk perception of mutual fund investors

and their post-buying behavioural factors are independent of each other.

118

5.3.3 Association between Post-buying Behavioural Factors of Mutual Fund

Investors and their Demographic Features

In order to study the influence of demographic factors on post-buying

behaviour of the mutual fund investors, the researcher has made an attempt to

associate the post-buying behavioural factors such as additional buying factors,

future buying intention and switching of funds with selected demographic

features of mutual fund investors. The chi-square test has been done for each of

the post-buying behavioural factors to test the association between the variables.

The detailed cross tab of the association between the variables is presented in

Appendix B.

a) Additional buying Vs Demographic Features

The additional buying of mutual fund investors with their demographic

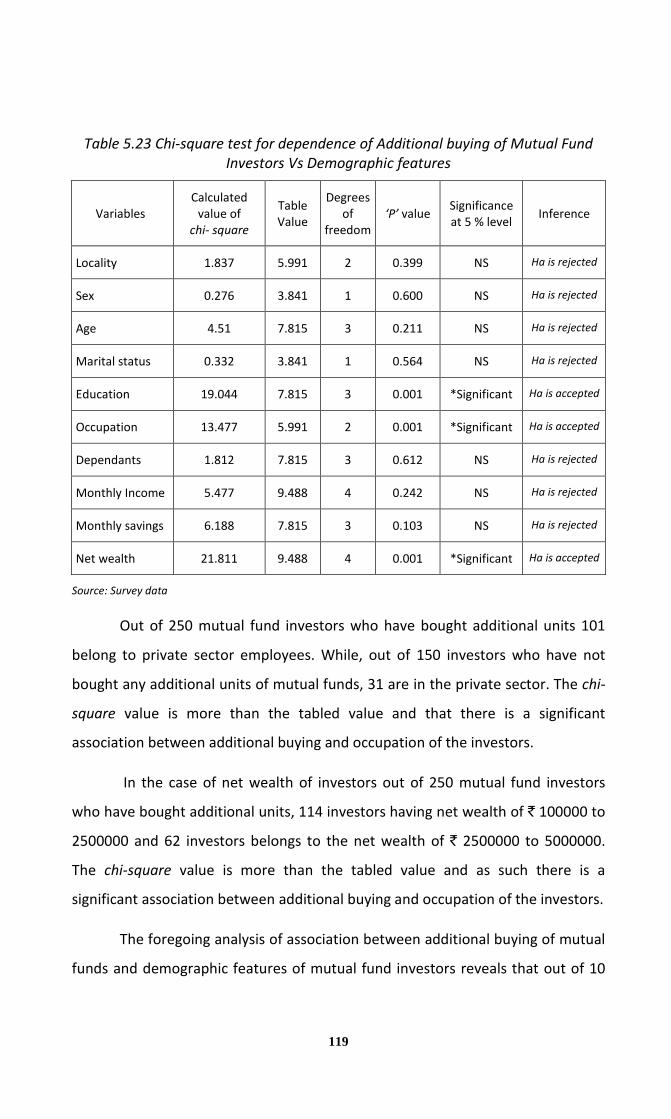

features have been tested with chi-square and its results are shown in table 5.23.

Ha: The additional buying of mutual fund investors and their demographic

features are dependent of each other.

The chi-square test shows no significant association between additional

buying with locality of the investors, sex, age and marital status, number of

dependants, monthly income and savings of the investors. While education,

occupation and net wealth of the investors have got significance with additional

buying of mutual fund units.

In the case of education, out of 250 investors who have bought additional

units of mutual fund, 124 investors belong to postgraduates and 79 investors

have postgraduate professional qualification. Since the chi-square value is more

than the tabled value, there is a significant association between additional buying

and educational status of the investors.

119

Table 5.23 Chi-square test for dependence of Additional buying of Mutual Fund

Investors Vs Demographic features

Variables

Calculated

value of

chi- square

Table

Value

Degrees

of

freedom

‘P’ value Significance

at 5 % level Inference

Locality 1.837 5.991 2 0.399 NS Ha is rejected

Sex 0.276 3.841 1 0.600 NS Ha is rejected

Age 4.51 7.815 3 0.211 NS Ha is rejected

Marital status 0.332 3.841 1 0.564 NS Ha is rejected

Education 19.044 7.815 3 0.001 *Significant Ha is accepted

Occupation 13.477 5.991 2 0.001 *Significant Ha is accepted

Dependants 1.812 7.815 3 0.612 NS Ha is rejected

Monthly Income 5.477 9.488 4 0.242 NS Ha is rejected

Monthly savings 6.188 7.815 3 0.103 NS Ha is rejected

Net wealth 21.811 9.488 4 0.001 *Significant Ha is accepted

Source: Survey data

Out of 250 mutual fund investors who have bought additional units 101

belong to private sector employees. While, out of 150 investors who have not

bought any additional units of mutual funds, 31 are in the private sector. The chi-

square value is more than the tabled value and that there is a significant

association between additional buying and occupation of the investors.

In the case of net wealth of investors out of 250 mutual fund investors

who have bought additional units, 114 investors having net wealth of ` 100000 to

2500000 and 62 investors belongs to the net wealth of ` 2500000 to 5000000.

The chi-square value is more than the tabled value and as such there is a

significant association between additional buying and occupation of the investors.

The foregoing analysis of association between additional buying of mutual

funds and demographic features of mutual fund investors reveals that out of 10

120

selected demographic variables significant association has been observed in the

case of three variables such as education, occupation and net wealth of mutual

fund investors. Therefore, it is concluded that the education, occupation and net

wealth of mutual fund investors have significant association with additional

buying of mutual fund units.

b) Future Buying Intention Vs Demographic features

Future buying intention of mutual fund investors may have an association

with demographic features of the investor. Therefore, the researcher made an

attempt to associate demographic features with future buying intention of

mutual fund investors (table 5.24).

Ha: The future buying intention of mutual fund investors and their

demographic features are dependent of each other.

The chi-square test shows no significant association between future

buying intention with locality, sex, age, marital status, occupation, and monthly

income of the investors. While, education, number of dependants, monthly

savings and net wealth of the investors have got significance with future buying

intention of Mutual Fund Investors.

In the case of education, out of 151 investors who opted for future buying

intention, 74 investors belong to postgraduates and 54 investors have

postgraduate professional qualification. The chi-square value is more than the

tabled value which shows that there is a significant association between future

buying intention and education of the investors.

121

Table 5.24 Chi-square test for dependence of Future buying intention of Mutual

Fund Investors Vs Demographic features

Variables

Calculated

value of

chi- square

Table

Value

Degrees

of

freedom

‘P’ value Significance

at 5 % level Inference

Locality 0.213 5.991 2 0.899 NS Ha is rejected

Sex 0.111 3.841 1 0.985 NS Ha is rejected

Age 5.303 7.815 3 0.151 NS Ha is rejected

Marital status 0.268 3.841 1 0.604 NS Ha is rejected

Education 14.372 7.815 3 0.002 *Significant Ha is accepted

Occupation 8.029 9.488 4 0.091 NS Ha is rejected

Dependants 10.277 7.815 3 0.016 *Significant Ha is accepted

Monthly Income 7.518 9.488 4 0.111 NS Ha is rejected

Monthly savings 12.913 7.815 3 0.005 *Significant Ha is accepted

Net wealth 15.629 7.815 3 0.001 *Significant Ha is accepted

Source: Survey data

Out of 151 mutual fund investors who have opted future buying intention,

53 investors are having three or more dependants. As the chi-square value is

more than the tabled value there is a significant association between future

buying intention and number of dependants of the investors.

The investors having average monthly savings up to ` 25000 have shown

more interest in future buying of mutual fund products.

In the case of net wealth of investors, out of 151 mutual fund investors who

have opted for future buying intention, 80 investors having net wealth of ` 100000

to 2500000 and 28 investors belong to the net wealth of ` 2500000 to 5000000.

The chi-square value is more than the tabled value, and thus there is a significant

association between future buying intention and occupation of the investors.

122

It can be summarized from the analysis that the variables such as

education, dependents, average savings and net assets have got significant

relationship in the future preferences of mutual fund investors. Thus, it can be

generalized that the earning capacity, educational profile, net wealth and family

size influences the future buying intention of the investors while making mutual

fund investments.

b) Switching of fund Vs Demographic Features

After considering additional buying and future buying intention, switching

of funds is the next important variable to be tested for association with

demography. Table 5.25 elaborates the test of dependence of switching of funds

Vs demographic features of mutual fund investors.

Ha: The Switching of funds and the demographic features of mutual fund

investors are dependent of each other.

The chi-square test shows no significant association between switching of

Mutual Fund Investors with locality sex, age, marital status, and occupation,

number of dependants, monthly savings, income and net wealth of the investors.

But, locality and educational level of investors have got significant association

with switching of fund.

123

Table 5.25 Chi-square test for dependence of Switching of Funds Vs Demographic

features

Variables

Calculated

value of

chi- square

Table

Value

Degrees

of

freedom

‘P’ value Significance

at 5 % level Inference

Locality 4.817 5.991 2 0.09 *Significant Ha is accepted

Sex 0.736 3.841 1 0.391 NS Ha is rejected

Age 4.152 7.815 3 0.246 NS Ha is rejected

Marital status 0.076 3.841 1 0.783 NS Ha is rejected

Education 9.45 7.815 3 0.024 *Significant Ha is accepted

Occupation 9.02 9.488 4 0.061 NS Ha is rejected

Dependants 6.888 7.815 3 0.076 NS Ha is rejected

Monthly Income 0.767 9.488 4 0.943 NS Ha is rejected

Monthly savings 0.319 7.815 3 0.956 NS Ha is rejected

Net wealth 1.209 7.815 3 0.751 NS Ha is rejected

Source: Survey data

Out of 249 mutual fund investors who have opted for switching of funds, 104

(43.2 percent) belongs to urban areas and 72 (28.8 percent) of investors represented

by rural areas. While, out of 151 investors who have not switched the funds, 76 (48

percent) of investors constituted from urban areas and 45 (30 percent) comes from

rural areas. As the chi-square value is more than the tabled value there is a significant

association between Switching of Funds and their locality.

In the case of education, out of 249 investors who opted for switching of

funds, 107 investors belong to postgraduates (non professional) and 86 investors

have postgraduate professional qualification. The chi-square value is more than

the tabled value, which shows that there is a significant association between

switching of funds and educational level of the investors.

The foregoing analysis of association between post-buying behaviour and

demographic features of mutual fund investors indicates that educational status

124

and economic status of mutual fund investors have an association with post-

buying behavioural aspects of mutual fund investors in respect of additional

buying, switching of funds and future buying preferences.

5.3.4 Product Performance Satisfaction Level of Mutual Fund Investors

Product performance satisfaction level can be referred to as the

satisfaction level of mutual fund investors with regards to return, transparency,

safety, liquidity, service quality, fund management and the overall performance of

the mutual fund products. Here, the researcher made an attempt to analyse the

satisfaction level of mutual fund investors in respect of different funds/schemes

opted by the investors. For these purpose seven parameters of satisfaction of

mutual fund investors in respect of the investment including overall performance

of the fund has been taken in to consideration. The respondents are asked to rate

the performance parameters on five point Likert-type scale ranging from excellent

to extremely poor. The standardised regression weight obtained for the seven

parameters is presented in table 5.26.

Table 5.26 Standardized Regression Weights of parameters of Product

Performance Satisfaction

Sl No. Parameters Estimate Rank

1 Return 0.676 6

2 Transparency 0.677 5

3 Safety 0.673 7

4 Service 0.792 3

5 Professional management 0.853 2

6 Liquidity 0.764 4

7 Overall performance 0.867 1

Source: Survey data

The standardised regression weight of product performance satisfaction

level of mutual fund investors reveals that overall performance is one of the

major indicators of satisfaction level of mutual fund investors. The second rank

125

belongs to professional management of AMCs with regression weight of 0.853.

Service quality, liquidity, transparency, return and safety are the third, fourth,

fifth, sixth and seventh rank respectively.

Later on, the researcher has classified the overall satisfaction level of

mutual fund investors in to three groups such as low level of satisfaction, medium

level of satisfaction and high level of satisfaction. The Table 5.27 shows the

detailed result of overall product performance satisfaction level of the

respondents in respect of the schemes/funds opted by them .

Ho: Mutual fund product performance satisfaction level of the investors is

uniform across different types of funds.

Table 5.27 Overall Product performance satisfaction level of the mutual fund

investors in respect of different funds

Sl

No Funds

Level of satisfaction

Total Chi-

square ‘P’ value

High % Medium % Low %

1 Open-ended 34 11.14 104 34.09 167 54.75 305 85.91 0.000*

2 Closed ended 7 15.55 11 24.44 27 60 45 14.93 0.0007*

3 Growth-fund 26 8.78 98 33.10 172 58.10 296 106.74 0.000*

4 Income Fund 6 14.28 15 35.71 21 50 42 8.14 0.0170*

5 Balanced Fund 7 17.5 13 32.5 20 50 40 5.34 0.0692

6 Tax Saving 5 5.49 32 35.16 54 59.34 91 38.03 0.000*

7 Exchange

Traded 5 7.69 19 29.23 41 63.07 65 29.01 0.000*

*Significant at 5 % level (d.f.2)

Source: Survey data

The table 5.26 reveals that out of 305 mutual fund investors who have

opted open-ended scheme, 54.74 percent of the investors have only low level of

satisfaction about their fund performance, and 34.09 percent of the investors

126

have medium level of satisfaction. The Chi-square test reveals that the

satisfaction level of the respondents among the sample groups is not uniform.

Out of 45 mutual fund investors who have opted close-ended scheme, 60

percent of them have only low level of satisfaction about their fund performance,

while 24.44 percent of the investors have medium level of satisfaction. The

statistical test shows that there is a significant difference in the satisfaction level

of mutual fund investors.

Out of 296 mutual fund investors who have opted growth-funds, 58.1

percent investors have only low level of satisfaction about their fund

performance, whereas 33.1 percent of the investors have medium level of

satisfaction. The Chi-square test reveals that the satisfaction level of the

respondents among the sample groups is not uniform.

Out of 42 mutual fund investors who have opted income-funds, 50

percent of the investors have only low level of satisfaction about their fund

performance, and 35.71 percent of the investors have medium level of

satisfaction. The Chi-square test reveals that the satisfaction level of the

respondents among the sample groups is not uniform.

In the case of balanced-funds, out of 40 investors who have opted the

scheme, 50 percent of the investors have only low level of satisfaction about their

fund performance, and 13 percent of the investors have medium level of

satisfaction. However, the statistical test shows no significant difference in the

satisfaction level of the mutual fund investors in respect of balanced-funds.

Out of 91 mutual fund investors who have opted tax saving funds, 59.34

percent of the investors have only low level of satisfaction about their fund

performance, and 32 percent of the investors have medium level of satisfaction.

The Chi-square test reveals that the satisfaction level of the respondents among

the sample groups is not uniform.

127

Out of 65 mutual fund investors who have opted ETF, 63.07 percent of

them have shown only low level of satisfaction about their fund performance, and

19 percent of the investors have medium level of satisfaction. The Chi-square test

reveals that the satisfaction level of the respondents among the sample groups is

not uniform.

The foregoing analysis of product performance satisfaction level of mutual

fund investors in respect of different funds opted by them shows that most of the

investors have only low level of satisfaction about the performance of mutual

fund. It also reveals that the satisfaction level of the mutual fund investors in

respect of the funds opted by them is not uniform among the sample groups.

Therefore, the null hypothesis put forth by the researcher is rejected and

concluded that there is a significant difference in the product performance

satisfaction level of mutual fund investors in respect of the funds opted by them

(except in case of balanced-fund).