Chapter 4. Understanding Interest Rates Present Value Yield to Maturity Other Yields Other...

40

Chapter 4. Understanding Chapter 4. Understanding Interest Rates Interest Rates • Present Value • Yield to Maturity • Other Yields • Other Measurement Issues

-

date post

21-Dec-2015 -

Category

Documents

-

view

225 -

download

3

Transcript of Chapter 4. Understanding Interest Rates Present Value Yield to Maturity Other Yields Other...

Chapter 4. Understanding Interest Chapter 4. Understanding Interest RatesRatesChapter 4. Understanding Interest Chapter 4. Understanding Interest RatesRates

• Present Value

• Yield to Maturity

• Other Yields

• Other Measurement Issues

• Present Value

• Yield to Maturity

• Other Yields

• Other Measurement Issues

I. Measuring Interest RatesI. Measuring Interest RatesI. Measuring Interest RatesI. Measuring Interest Rates

A. Credit Market Instruments

• simple loan borrower pays back loan and

interest in one lump sum

A. Credit Market Instruments

• simple loan borrower pays back loan and

interest in one lump sum

• fixed-payment loan loan is repaid with equal (monthly)

payments each payment is combination of

principal and interest

• fixed-payment loan loan is repaid with equal (monthly)

payments each payment is combination of

principal and interest

• coupon bond purchase price (P) interest payments (6 months) face value at maturity (F) size of interest payments

-- coupon rate

-- face value

• coupon bond purchase price (P) interest payments (6 months) face value at maturity (F) size of interest payments

-- coupon rate

-- face value

• discount bond zero coupon bond purchased price less than face

value

-- F > P face value at maturity no interest payments

• discount bond zero coupon bond purchased price less than face

value

-- F > P face value at maturity no interest payments

B. Present & Future ValueB. Present & Future ValueB. Present & Future ValueB. Present & Future Value

• time value of money

• $100 today vs. $100 in 1 year not indifferent! money earns interest over time, and we prefer consuming today

• time value of money

• $100 today vs. $100 in 1 year not indifferent! money earns interest over time, and we prefer consuming today

example: future valueexample: future valueexample: future valueexample: future value

• $100 today

• interest rate 5% annually

• at end of 1 year:

100 + (100 x .05)

= 100(1.05) = $105

• at end of 2 years:

100 + (1.05)2 = $110.25

• $100 today

• interest rate 5% annually

• at end of 1 year:

100 + (100 x .05)

= 100(1.05) = $105

• at end of 2 years:

100 + (1.05)2 = $110.25

future valuefuture valuefuture valuefuture value

• of $100 in n years if interest rate is i:

= $100(1 + i)n • of $100 in n years if interest rate is i:

= $100(1 + i)n

present valuepresent valuepresent valuepresent value

• work backwards

• if get $100 in n years,

what is that worth today?

• work backwards

• if get $100 in n years,

what is that worth today?

PV = $100

(1+ i)n

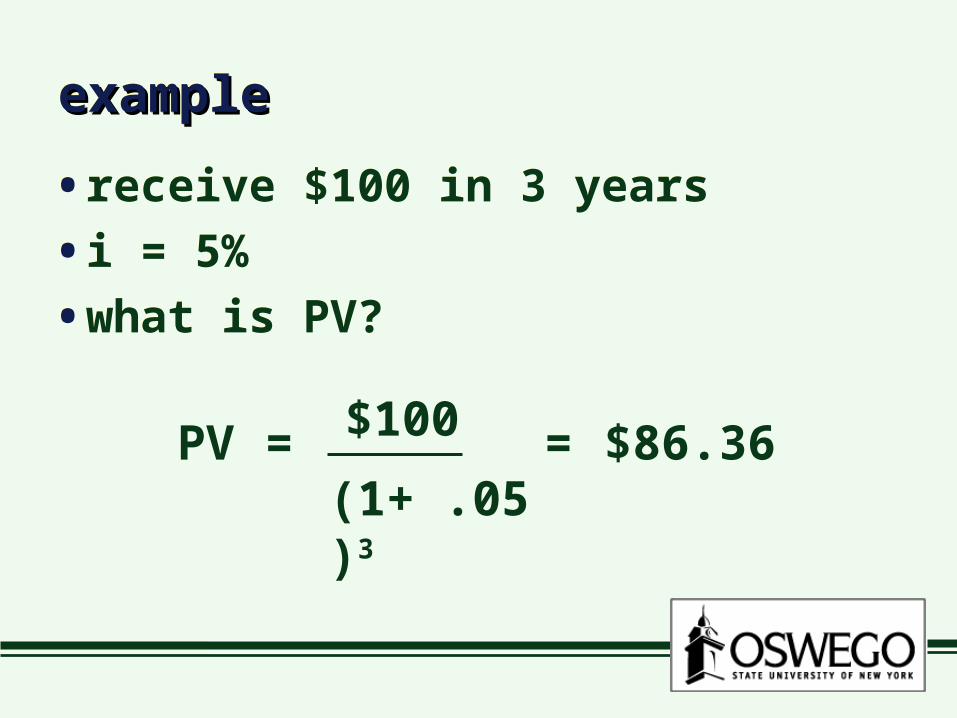

exampleexampleexampleexample

• receive $100 in 3 years

• i = 5%

• what is PV?

• receive $100 in 3 years

• i = 5%

• what is PV?

PV = $100

(1+ .05)3

= $86.36

n

i

PV

PV

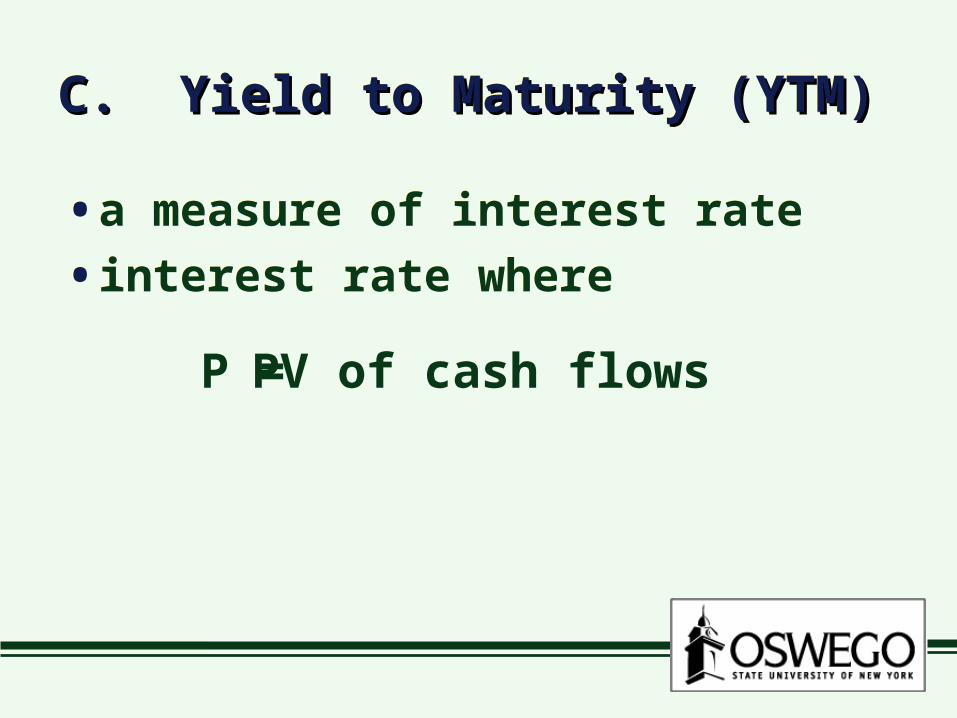

C. Yield to Maturity (YTM)C. Yield to Maturity (YTM)C. Yield to Maturity (YTM)C. Yield to Maturity (YTM)

• a measure of interest rate

• interest rate where• a measure of interest rate

• interest rate where

P = PV of cash flows

example 1: simple loanexample 1: simple loanexample 1: simple loanexample 1: simple loan

• loan = $1500, 1 year, 6%

• future payment

= $1500(1+.06) = $1590

• yield to maturity, i

• loan = $1500, 1 year, 6%

• future payment

= $1500(1+.06) = $1590

• yield to maturity, i

$1500 = $1590

(1+ i)i = 6%

example 2: fixed pmt. loanexample 2: fixed pmt. loanexample 2: fixed pmt. loanexample 2: fixed pmt. loan

• $15,000 car loan, 5 years

• monthly pmt. = $300

• so $15,000 is price today

• cash flow is 60 pmts. of $300

• $15,000 car loan, 5 years

• monthly pmt. = $300

• so $15,000 is price today

• cash flow is 60 pmts. of $300

• YTM solves• YTM solves

• i/12 is monthly discount rate

• i is yield to maturity• i/12 is monthly discount rate

• i is yield to maturity

• how to solve for i? trial-and-error bond table* financial calculator spreadsheet

• how to solve for i? trial-and-error bond table* financial calculator spreadsheet

• payment between $297.02 & $300.57

• YTM is between 7% and 7.5%

(7.42%)

• payment between $297.02 & $300.57

• YTM is between 7% and 7.5%

(7.42%)

example 3: coupon bondexample 3: coupon bondexample 3: coupon bondexample 3: coupon bond

• 2 year Tnote, F = $10,000

• coupon rate 6%

• price of $9750

• what are interest payments?

(.06)($10,000)(.5) = $300 every 6 mos.

• 2 year Tnote, F = $10,000

• coupon rate 6%

• price of $9750

• what are interest payments?

(.06)($10,000)(.5) = $300 every 6 mos.

• YTM solves the equation• YTM solves the equation

• i/2 is 6-month discount rate

• i is yield to maturity• i/2 is 6-month discount rate

• i is yield to maturity

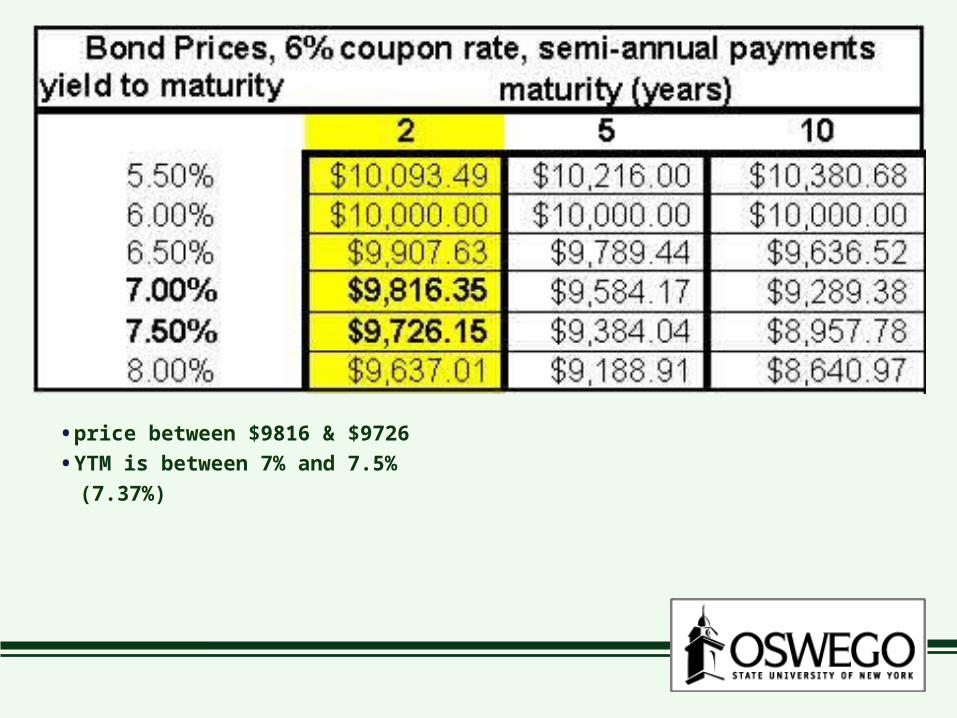

• price between $9816 & $9726

• YTM is between 7% and 7.5%

(7.37%)

• price between $9816 & $9726

• YTM is between 7% and 7.5%

(7.37%)

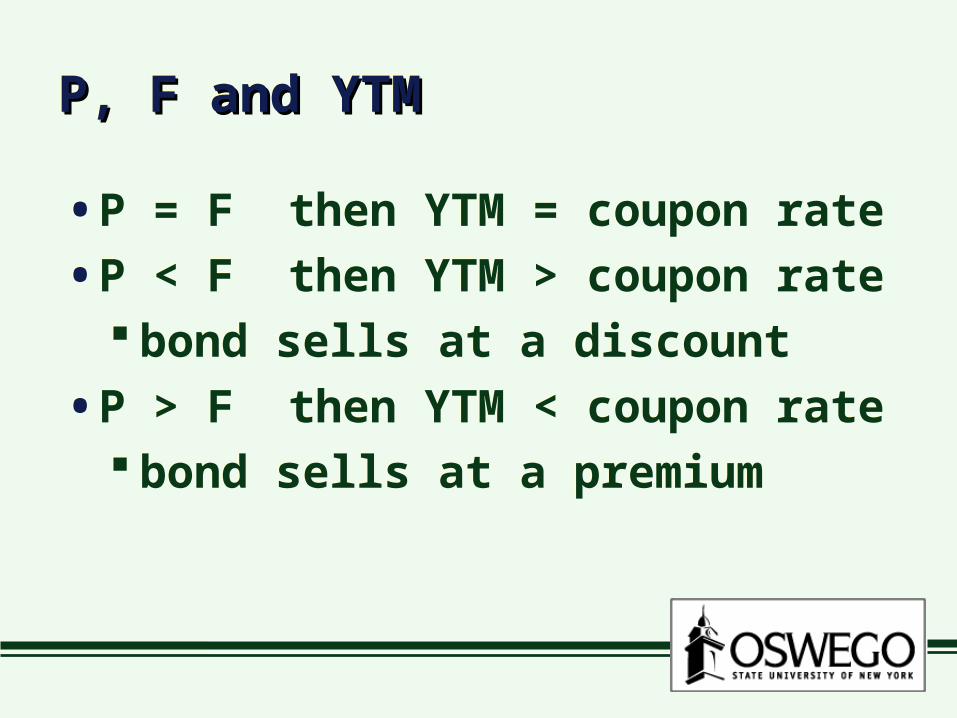

P, F and YTMP, F and YTMP, F and YTMP, F and YTM

• P = F then YTM = coupon rate

• P < F then YTM > coupon rate bond sells at a discount

• P > F then YTM < coupon rate bond sells at a premium

• P = F then YTM = coupon rate

• P < F then YTM > coupon rate bond sells at a discount

• P > F then YTM < coupon rate bond sells at a premium

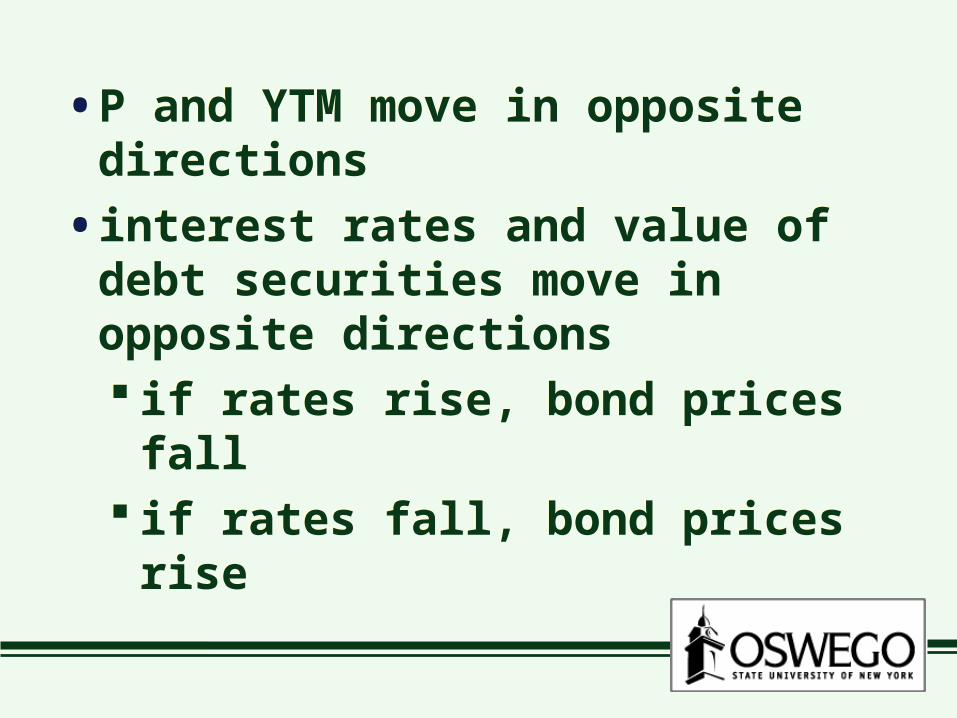

• P and YTM move in opposite directions

• interest rates and value of debt securities move in opposite directions if rates rise, bond prices fall if rates fall, bond prices rise

• P and YTM move in opposite directions

• interest rates and value of debt securities move in opposite directions if rates rise, bond prices fall if rates fall, bond prices rise

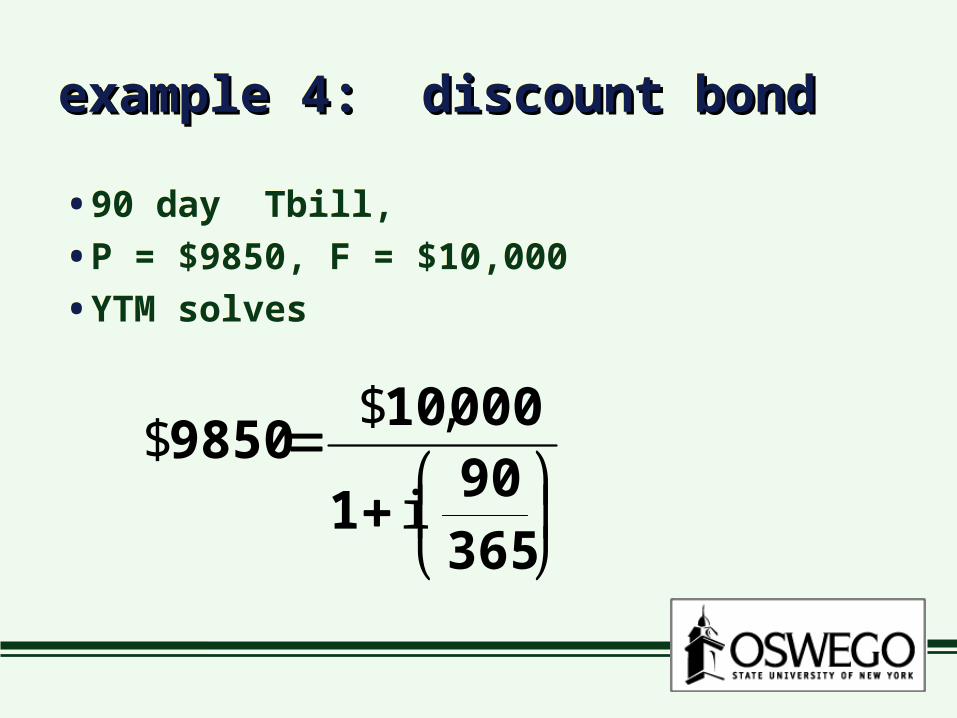

example 4: discount bondexample 4: discount bondexample 4: discount bondexample 4: discount bond

• 90 day Tbill,

• P = $9850, F = $10,000

• YTM solves

• 90 day Tbill,

• P = $9850, F = $10,000

• YTM solves

36590

1

000109850

i

,$$

9850

00010

365

901

$

,$i

19850

00010

365

90

$

,$i

9850

985000010

365

90

$

,$i

90

365

9850

985000010

$

,$i = 6.18%

• in general,• in general,

D. Current YieldD. Current YieldD. Current YieldD. Current Yield

• approximation of YTM for coupon bonds• approximation of YTM for coupon

bonds

ic =annual coupon payment

bond price

• better approximation when maturity is longer P is close to F

• better approximation when maturity is longer P is close to F

example 5example 5example 5example 5

• 2 year Tnotes, F = $10,000

• P = $9750, coupon rate = 6%

• current yield

• 2 year Tnotes, F = $10,000

• P = $9750, coupon rate = 6%

• current yield

ic =600

9750= 6.15%

• current yield = 6.15%

• true YTM = 7.37%

• lousy approximation only 2 years to maturity selling 25% below F

• current yield = 6.15%

• true YTM = 7.37%

• lousy approximation only 2 years to maturity selling 25% below F

E. Discount YieldE. Discount YieldE. Discount YieldE. Discount Yield

• yield on a discount basis

• approximation of YTM• yield on a discount basis

• approximation of YTM

idb = F - P

Fx

360d

• compare w/ YTM• compare w/ YTM

idb = F - P

Fx

360d

iytm = F - P

Px

365d

iytm > idb

example 6:example 6:example 6:example 6:

• 90-day Tbill, price $9850• 90-day Tbill, price $9850

idb = 10,000 - 9850

9850x

36090

= 6%

true YTM is 6.18%

II. Other measurement issuesII. Other measurement issuesII. Other measurement issuesII. Other measurement issues

A. Interest rates vs. return

• YTM assumes bond is held until maturity

• if not, resale price is important

A. Interest rates vs. return

• YTM assumes bond is held until maturity

• if not, resale price is important

B. Maturity & bond price volatilityB. Maturity & bond price volatilityB. Maturity & bond price volatilityB. Maturity & bond price volatility

• YTM rises from 6 to 8% bond prices fall but 10-year bond price falls the

most

• Prices are more volatile for longer maturities long-term bonds have greater

interest rate risk

• YTM rises from 6 to 8% bond prices fall but 10-year bond price falls the

most

• Prices are more volatile for longer maturities long-term bonds have greater

interest rate risk

• Why? long-term bonds “lock in” a

coupon rate for a longer time if interest rates rise

-- stuck with a below-market coupon rate

if interest rates fall

-- receiving an above-market coupon rate

• Why? long-term bonds “lock in” a

coupon rate for a longer time if interest rates rise

-- stuck with a below-market coupon rate

if interest rates fall

-- receiving an above-market coupon rate

C. Real vs. Nominal Interest RatesC. Real vs. Nominal Interest RatesC. Real vs. Nominal Interest RatesC. Real vs. Nominal Interest Rates

• thusfar we have calculated nominal interest rates ignores effects of rising inflation

• thusfar we have calculated nominal interest rates ignores effects of rising inflation

real interest rate, ireal interest rate, irrreal interest rate, ireal interest rate, irr

nominal interest rate = i

expected inflation rate = πe

approximately:

i = ir + πe

• The Fisher equation

or ir = i - πe

nominal interest rate = i

expected inflation rate = πe

approximately:

i = ir + πe

• The Fisher equation

or ir = i - πe

• real interest rates measure true cost of borrowing

• why? as inflation rises, real value of loan

payments falls, so real cost of borrowing falls

• real interest rates measure true cost of borrowing

• why? as inflation rises, real value of loan

payments falls, so real cost of borrowing falls