Chapter 4 Maxims of Income Tax Planning McGraw-Hill Education Copyright © 2015 by McGraw-Hill...

24

Chapter 4 Chapter 4 Maxims of Income Maxims of Income Tax Planning Tax Planning McGraw-Hill Education Copyright © 2015 by McGraw-Hill Education. All rights reserved.

-

Upload

catherine-cunningham -

Category

Documents

-

view

249 -

download

1

Transcript of Chapter 4 Maxims of Income Tax Planning McGraw-Hill Education Copyright © 2015 by McGraw-Hill...

Chapter 4Chapter 4

Maxims of Income Maxims of Income Tax PlanningTax Planning

McGraw-Hill Education Copyright © 2015 by McGraw-Hill Education. All rights reserved.

4-2

ObjectivesObjectives

• Differentiate between tax avoidance and tax evasion• List the four variables that determine the tax consequences

of a transaction• Explain why an income shift or a deduction shift can improve

NPV • Explain how the assignment of income doctrine constrains

income-shifting strategies• Distinguish between an explicit tax and an implicit tax

4-3

Objectives (continued)Objectives (continued)

• Contrast the tax character of ordinary income and capital gain

• Distinguish between an explicit and implicit tax• Summarize the four tax planning maxims• Describe the legal doctrines that the IRS uses to challenge

tax planning strategies

4-4

Tax AvoidanceTax Avoidance

• Tax avoidance consists of legitimate means of reducing taxes

• Tax evasion consists of illegal means of reducing taxes• Felony offense punishable by severe monetary fines

and imprisonment

4-5

Tax Planning VariablesTax Planning Variables

• Tax consequences of a transaction depend on the interaction of four variables

• Entity variable: Which entity undertakes the transaction?

• Time period variable: In which tax year does the transaction occur?

• Jurisdiction variable: In which taxing jurisdiction does the transaction occur?

• Character variable: What is the tax character of the income, gain, loss, or deduction from the transaction?

4-6

Income Tax Planning - EntityIncome Tax Planning - Entity

• Generally, taxable income is computed under the same rules across business entities• However, the tax on business income depends on the

difference in tax rates across entities • The two taxpaying business entities are individuals

and corporations

4-7

Income Tax Planning - EntityIncome Tax Planning - Entity

• Individual taxpayers • Progressive tax rate structure

ranging from 10% to 39.6%

• Corporate taxpayers• Progressive tax rate structure

ranging from 15% to 39%

• Both sets of rate schedules are included in Appendix C

4-8

Tax RatesTax Rates

• Compute 2014 tax, marginal rate, and average rate on $250,000 income if:

• Taxpayer is a single individual• Taxpayer is a corporation

• Answer:• $66,358 ($45,354 + .33 [$250,000 – $186,350])

33% marginal rate; 26.54% average rate

• $80,750 ($22,250 + .39 [$250,000 – $100,000]) 39% marginal rate; 32.3% average rate

4-9

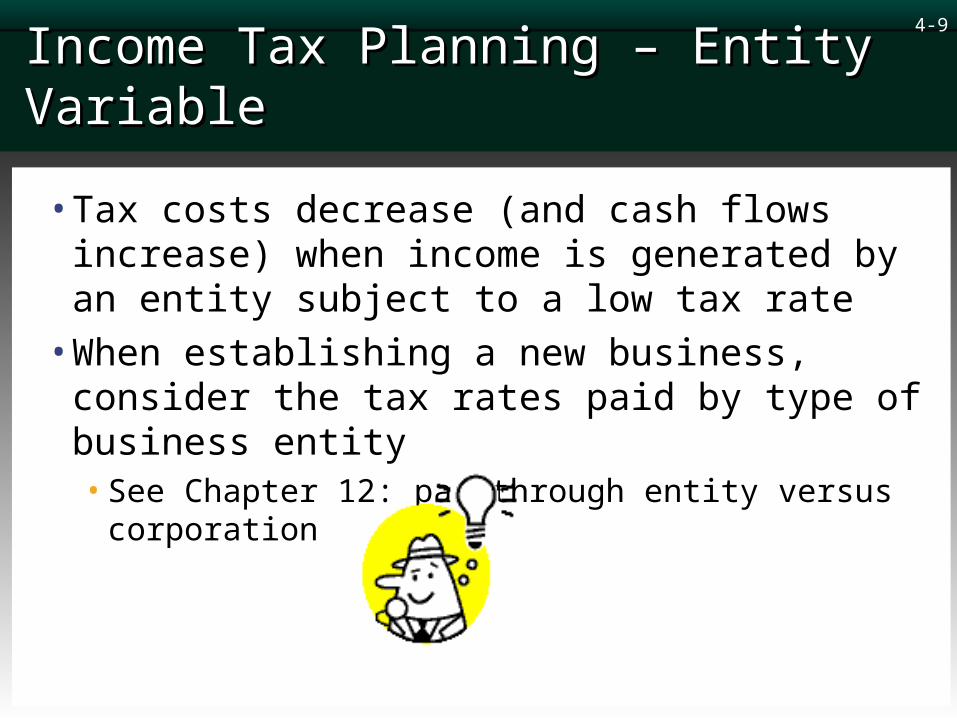

Income Tax Planning – Entity VariableIncome Tax Planning – Entity Variable

• Tax costs decrease (and cash flows increase) when income is generated by an entity subject to a low tax rate

• When establishing a new business, consider the tax rates paid by type of business entity• See Chapter 12: passthrough entity versus corporation

4-10

Income Tax Planning – Entity VariableIncome Tax Planning – Entity Variable

• Income shifting • Arranging transactions to transfer income from a high

tax rate entity to a low tax rate entity

• Deduction shifting• Arranging transactions to transfer deductions from a

low tax rate entity to a high tax rate entity

• After an income or deduction shift, the parties in the aggregate are financially better off by the tax savings from the transaction

4-11

Income Tax Planning – Entity VariableIncome Tax Planning – Entity Variable

• Assignment of income doctrine• Constraint on income shifting

• Income must be taxed to the entity that earns it from sale of goods or performance of services

• Income generated by capital must be taxed to the entity that owns the capital

4-12

Income Tax Planning – Time Period VariableIncome Tax Planning – Time Period Variable

• In present value terms, tax costs decrease (and cash flows increase) when a tax cost is deferred until a later taxable year

• Constrained by:• Opportunity costs• Tax rate increase

4-13

Income Tax Planning – Time Period VariableIncome Tax Planning – Time Period Variable

• Opportunity costs• Shifting tax costs to later period may involve postponing

a cash inflow. Thus, the opportunity cost of postponing the cash inflow may exceed the savings from tax deferral

• Opportunity cost is the loss of the immediate use of cash

4-14

Income Tax Planning – Time Period VariableIncome Tax Planning – Time Period Variable

• Tax rate increase

• If taxpayers defer the recognition of income to a future year and Congress increases future tax rates, the cost of the rate increase offsets the benefit of the deferral

• The risk that deferred income will be taxed at a higher rate increases with the length of the deferral period

4-15

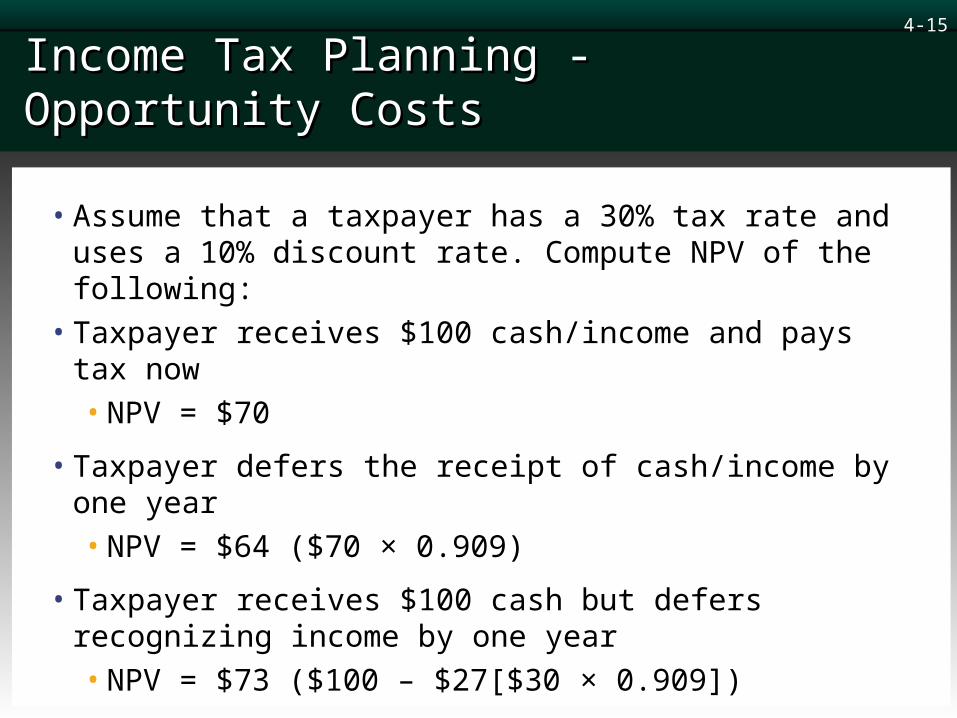

Income Tax Planning - Opportunity CostsIncome Tax Planning - Opportunity Costs

• Assume that a taxpayer has a 30% tax rate and uses a 10% discount rate. Compute NPV of the following:

• Taxpayer receives $100 cash/income and pays tax now• NPV = $70

• Taxpayer defers the receipt of cash/income by one year• NPV = $64 ($70 × 0.909)

• Taxpayer receives $100 cash but defers recognizing income by one year• NPV = $73 ($100 – $27[$30 × 0.909])

4-16

Income Tax Planning - Tax Rate IncreaseIncome Tax Planning - Tax Rate Increase

• Taxpayer receives $100 cash but defers recognizing income by one year. Congress increases the tax rate from 30% to 40% next year• NPV = $64 ($100 – $36 [$40 × 0.909])

4-17

Income Tax Planning – Jurisdiction VariableIncome Tax Planning – Jurisdiction Variable

• The jurisdiction variable is important because local, state, and foreign tax laws differ

• Tax costs decrease (and cash flows increase) when income is generated in a low tax rate jurisdiction

• The jurisdiction variable is discussed in Chapter 13

4-18

Income Tax Planning – Character VariableIncome Tax Planning – Character Variable

• Tax character of income is determined by law• Every income item is characterized as either

ordinary income or capital gain

• Ordinary income is generated from sale of goods or performance of services in regular course of business

• Income generated by investments (interest, dividends, royalties, and rents) is ordinary

• Capital gains are generated by the sale or exchange of capital assets (defined in Chapter 8)

4-19

Income Tax Planning – Character VariableIncome Tax Planning – Character Variable

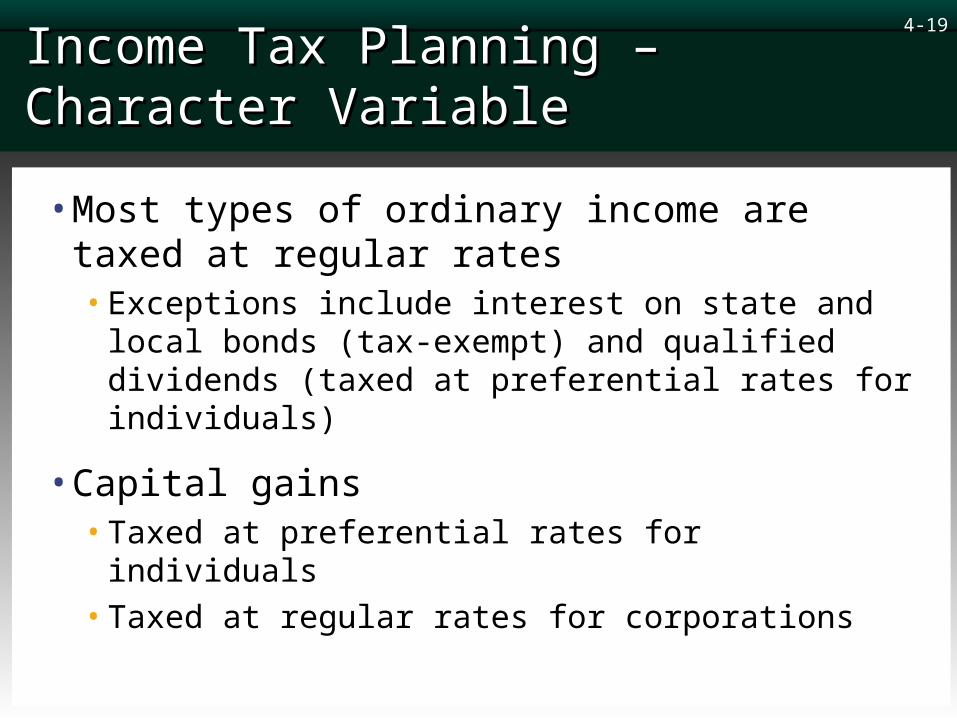

• Most types of ordinary income are taxed at regular rates• Exceptions include interest on state and local bonds (tax-

exempt) and qualified dividends (taxed at preferential rates for individuals)

• Capital gains • Taxed at preferential rates for individuals• Taxed at regular rates for corporations

4-20

Income Tax Planning – Character VariableIncome Tax Planning – Character Variable

• Tax costs decrease (and cash flows increase) when income is taxed at a preferential rate because of its character.• Because capital gains are taxed at preferential rates,

individuals try to arrange transactions to convert ordinary income to capital gain

• The Internal Revenue Code contains dozens of provisions that prevent the conversion of ordinary income to capital income

4-21

Conflicting Tax Planning MaximsConflicting Tax Planning Maxims

• Sometimes, the four tax planning maxims conflict!

• For example, a transaction defers tax may shift income to an entity with a higher tax rate

• Managers should remember that their strategic goal is not tax minimization but NPV maximization

4-22

Implicit TaxesImplicit Taxes

• Reduced before-tax rate of return on a tax-favored investment is called an implicit tax

• Example: A corporate bond pays 9% and a municipal bond pays 6.3% • Investor who purchases the municipal bond incurs a 30% implicit

tax (2.7% reduced rate/9%)

• Investors with marginal rates greater than 30% maximize their after-tax rate of return by purchasing the municipal bond

• Investors with marginal rates less than 30% maximize their after-tax rate of return by purchasing the corporate bond

4-23

Tax Law DoctrinesTax Law Doctrines

• IRS can use legal doctrinesto challenge a tax planning strategy

• Economic substance/business purpose doctrine A transaction must have a business purpose other than tax avoidance• Codified in §7701(o)

• Substance over form doctrine IRS can look through legal formalities to determine economic substance

• Step transaction doctrine IRS can collapse a series of interdependent transactions into one transaction

4-24