Chapter 31

20

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-1 Chapter 31 Further consolidation issues IV: Accounting for changes in the degree of ownership of a subsidiary

-

Upload

uriah-hale -

Category

Documents

-

view

20 -

download

10

description

Chapter 31. Further consolidation issues IV: Accounting for changes in the degree of ownership of a subsidiary. Objectives of this lecture. Know how to account for an increase in ownership of a subsidiary Know how to account for a subsidiary that is acquired in stages - PowerPoint PPT Presentation

Transcript of Chapter 31

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-1

Chapter 31Further consolidation

issues IV: Accounting for changes in the degree of

ownership of a subsidiary

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-2

Objectives of this lecture

• Know how to account for an increase in ownership of a subsidiary

• Know how to account for a subsidiary that is acquired in stages

• Know how to account for a decrease in ownership of a subsidiary

• Know how to account for a loss of control in a subsidiary

• Know how to account for the gain or loss on the sale of a subsidiary in both the consolidated financial statements and the parent entity’s financial statements

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-3

Increase in the ownership interest held in a subsidiary

• It is common for a parent entity to acquire additional shares in a subsidiary over time

• There are two general approaches that potentially could be used when accounting for increases in the ownership of a subsidiary. These two approaches have been referred to as the:

1. step-by-step method

2. single-date method

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-4

The step-by-step method

Pursuant to the step-by-step method, which was the method required by AASB 3 until recently:

– Each individual investment in the subsidiary is accounted for separately

– Once control of the subsidiary is established, the consolidation worksheet entries will eliminate the various investments in the subsidiary

– Restate the subsidiary’s assets to fair value as at each exchange date

– For each investment elimination we will calculate a separate amount of goodwill

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-5

The single-date method• By contrast, under the single-date method, goodwill would

be recognised by a single consolidation journal entry at that point in time when the parent entity ultimately gains control of the subsidiary

• That is, the aggregate costs of the investments would be eliminated against the parent’s share of capital and reserves at the date control is ultimately established and only one amount of goodwill (or bargain gain on purchase) is calculated

• While the step-by-step method was the method required by AASB 3 until 2008, in 2008 AASB 3 was revised and now the requirement is that the single-date method be applied

• This was a major change in the accounting standard

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-6

Single-date method• As noted above, when additional shares in a subsidiary are

acquired we are not to account for each acquisition separately. Rather, AASB 10, paragraph 23, requires that:

Changes in a parent’s ownership interest in a subsidiary that do not result in the parent losing control of the subsidiary are equity transactions (i.e. transactions with owners in their capacity as owners).

• Some of the general requirements of the single-date method can be summarised as follows:

– No gain or loss from these changes in ownership is recognised in the statement of comprehensive income once control has been achieved.

– No change in the carrying amounts of the subsidiary’s assets (including goodwill) or liabilities is recognised as a result of such transactions.

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-7

Applying the single-date method

• The non-controlling interest in share capital and reserves at the date the additional equity in a subsidiary is acquired needs to be determined

• No goodwill or bargain purchase on acquisition of the additional interest is recognised

• The second share purchase is seen as a transfer of equity between owners

• The basis of this argument is that if the parent entity already had established control of the subsidiary (and therefore control of its assets) then it already controlled all of the assets of the subsidiary, and therefore the second transaction provided the entity with no further assets

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-8

Applying the single-date method (cont.)

• In accordance with the above perspective, AASB 10 requires the purchase of an additional ownership interest in a subsidiary, after control to be gained, to be treated as an equity transaction

• Specifically, there is an equity transfer between the parent entity and the non-controlling interests. Par 23 AASB 10

• Need to determine the non-controlling interest in the subsidiary just prior to the subsequent acquisition

• No goodwill or bargain purchase on acquisition of the additional equity interest is recognised as this is not considered a significant economic event

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-9

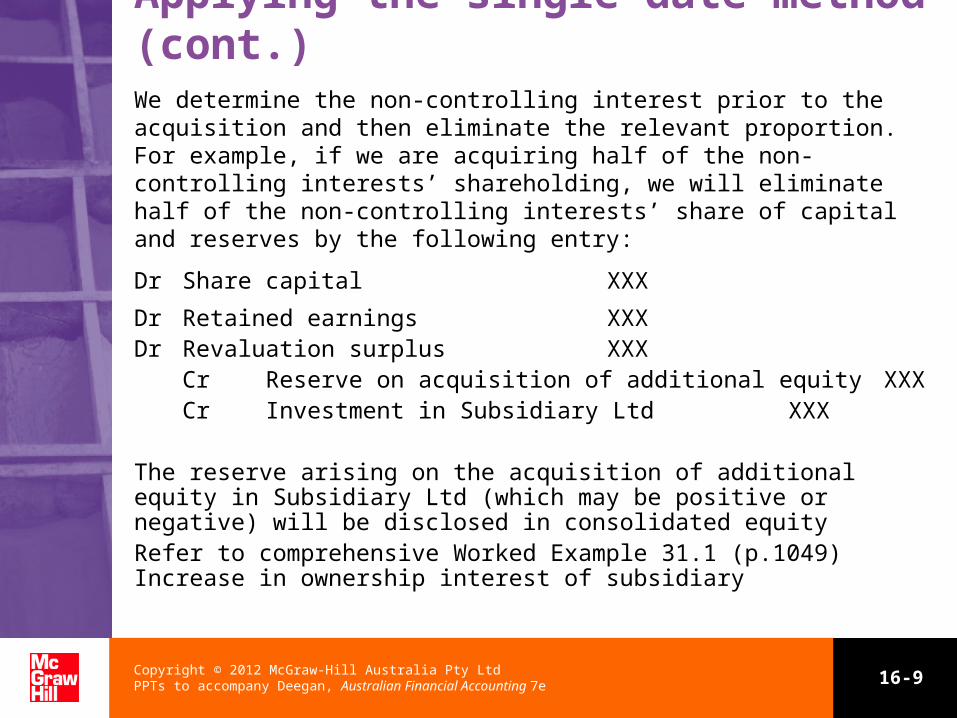

Applying the single-date method (cont.)We determine the non-controlling interest prior to the acquisition and then eliminate the relevant proportion. For example, if we are acquiring half of the non-controlling interests’ shareholding, we will eliminate half of the non-controlling interests’ share of capital and reserves by the following entry:

Dr Share capital XXX

Dr Retained earnings XXXDr Revaluation surplus XXX

Cr Reserve on acquisition of additional equity XXXCr Investment in Subsidiary Ltd XXX

The reserve arising on the acquisition of additional equity in Subsidiary Ltd (which may be positive or negative) will be disclosed in consolidated equityRefer to comprehensive Worked Example 31.1 (p.1049) Increase in ownership interest of subsidiary

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-10

Obtaining control over an entity in which a non-controlling interest is held

• It is possible for an acquirer to obtain control of an acquiree in stages through successive purchases of shares

• If the acquirer holds a non-controlling equity investment in the acquiree immediately prior to obtaining control, this investment must be remeasured to fair value as at the date of subsequently obtaining control and included in the calculation of goodwill

• Any gain or loss on the remeasurement is recognised in consolidated profit or loss

Refer to illustrated example p.1055-1056 and Worked Example 31.2 (p.1057) Two investments culminating in control of a subsidiary

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-11

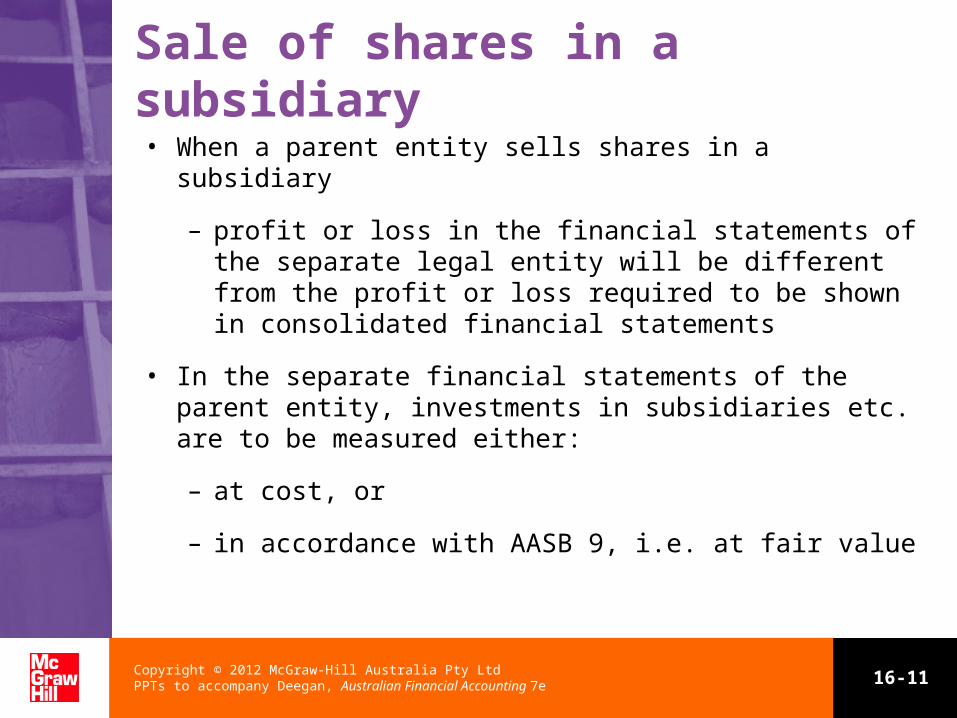

Sale of shares in a subsidiary

• When a parent entity sells shares in a subsidiary

– profit or loss in the financial statements of the separate legal entity will be different from the profit or loss required to be shown in consolidated financial statements

• In the separate financial statements of the parent entity, investments in subsidiaries etc. are to be measured either:

– at cost, or

– in accordance with AASB 9, i.e. at fair value

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-12

Sale of shares in a subsidiary (cont.)

• From the parent’s perspective, profit or loss on sale of shares is the difference between:

– carrying amount of shares, and

– fair value of sales proceeds

• Carrying amount

– is the amount shown in the financial statements for a particular asset or liability

• From the group’s perspective:

– consideration to be given to economic entity’s share of post-acquisition profits and reserve movements before determining profit or loss on sale of shares

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-13

Sale of shares in a subsidiary (cont.)

• When a parent entity sells shares in a subsidiary the sale may, or may not, lead to a loss of control

• If control is not lost then the subsidiary still forms part of the economic entity and continues to form part of the group financial statements

• Where changes in ownership interest in a subsidiary do not result in a loss of control, AASB 10 requires the transaction to be accounted for as a transfer within equity

• Where a parent entity sells some of its ownership interest but still holds control of the subsidiary, then the assets in the subsidiary that it controls do not change

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-14

Sale of shares in a subsidiary (cont.)

• Where a parent entity loses control of the subsidiary, the parent entity must no longer recognise the individual assets, liabilities and equity (including any non-controlling interest) relating to that subsidiary

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-15

Where a sale of shares results in loss of control of a subsidiaryPursuant to paragraph B98 of AASB 10, if a parent loses control of a subsidiary then it:

(a) derecognises the assets (including any goodwill) and liabilities of the subsidiary at their carrying amounts at the date when control is lost

(b) derecognises the carrying amount of any non-controlling interests in the former subsidiary at the date when control is lost (including any components of other comprehensive income attributable to them)

(c) recognises:

(i) the fair value of the consideration received, if any, from the transaction, event or circumstances that resulted in the loss of control, and

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-16

Where a sale of shares results in loss of control of a subsidiary (cont.)(ii) if the transaction that resulted in the loss of control involves a

distribution of shares of the subsidiary to owners in their capacity as owners, that distribution

(iii) any investment retained in the former subsidiary at its fair value at the date when control is lost.

(c) reclassifies to profit or loss, or transfers directly to retained earnings if required by other Standards, the amounts recognised in other comprehensive income in relation to the subsidiary on the basis described in paragraph B99

(d) recognises any resulting difference as a gain or loss in profit or loss attributable to the parent

Refer to Worked example 31.4 (p.1065) Calculation of profit or loss resulting from loss of control over a subsidiary

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-17

Calculating the profit or loss on disposal of a subsidiary (loss of control)Fair value of the proceeds (if any) from the transaction that resulted in the loss of control XXXadd Fair value of any retained non-controlling equity investment in the former subsidiary, at the date control is lost XXX

add Carrying value of the non-controlling interest in the former subsidiary at the date control is lost XXX

less Carrying value of the former subsidiary’s net assets at the date control is lost (XXX)

add/less any amount included in other components of equity that relate to the subsidiary that would be required to be reclassified to profit or loss or another component of equity if the parent had disposed of the related assets and liabilities (XXX)

Profit or loss on disposal of subsidiary XXX

Refer to Worked example 31.5 (p.1066) Sales of shares in a subsidiary

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-18

Revenues and expenses of sold subsidiary

As indicated in the previous example, where a parent sells its interest in a subsidiary it is a requirement that any profit or loss generated by the subsidiary is to be recorded in the consolidated financial statements for the period of the year during which the parent entity had control of the subsidiary. As paragraph B88 of AASB 10 states:

An entity includes the income and expenses of a subsidiary in the consolidated financial statements from the date it gains control until the date when the entity ceases to control the subsidiary.

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-19

Consolidation adjustments• Consolidated retained earnings will include the parent

entity’s retained earnings plus its share of the subsidiaries’ post-acquisition movements in retained earnings

• In the period following the sale of a subsidiary the opening balance of retained earnings will be required to be equal to the closing balance as shown in the preceding period

• It will be necessary to make a consolidation adjusting journal entry that includes the parent’s share of the post-acquisition movements in retained earnings of the former subsidiary

• Consolidation adjusting journal entries will be needed so that the consolidated financial statements include the parent’s share of the post-acquisition movements in other reserves of the sold subsidiary

Copyright © 2012 McGraw-Hill Australia Pty Ltd PPTs to accompany Deegan, Australian Financial Accounting 7e 16-20

Recognition of non-controlling interests

• The consolidated financial statements are to include all of the revenues and expenses of the subsidiary (subject to adjustments for intragroup transactions) for the period that the parent controlled the subsidiary

• Because we are including all of the revenues and expenses of the sold subsidiary for the period during which the parent entity had control, we will also be required to separately disclose the non-controlling interests in the consolidated profit after tax

• The assets, liabilities and equity accounts of a sold subsidiary will not be shown in the consolidated financial statements

Refer to Worked example 31.6 (p.1068) Sale of all shares held in a subsidiary