Chapter 3 Growth of Ayurvedic Industry in...

31

52 Chapter 3 Growth of Ayurvedic Industry in Kerala The events that occurred at the national level regarding the evolution and revival of Ayurveda had its traces in Kerala also. The revitalisation of Ayurveda in Kerala is the story of the establishment of a legend in health care. The revitalization process began in a small town Kottackkal, near Calicut in the Northern Kerala. Panniyinpalli Sankunni Warrier was born into an orthodox but talented family of temple service caste. The family had the reputation of good Ayurvedic physicians. He was given formal training in Ayurveda, at the time when western medicine was gaining acceptance in Kottackkal. He was eager to learn western medicine but the chief handicap was the language which he learned from a native doctor who had mastered English. He was liberal and catholic in his outlook. His house was open to people of all caste and creed. Soon Warrier became well accepted. This visionary realised the poor state of Ayurveda and formed the Arya Vaidya Samajam (meaning association) in 1902. It was a formal gathering of Ayurvedic physicians. Samajam helped to exchange views and experiences and soon became a platform for the revitalisation movement and was perhaps the first public body for this cause in Kerala (Panikkar, 2002). It aimed at a creative introspection of Ayurveda both its past and present. The Samajam meetings had two dimensions which included general speeches and secondly reading papers that led to more professional discussions on illness, treatment and medicine. Samajam was thus successful in bringing together uncodified experiences and innovations in Ayurveda. The deliberations in the Arya Vaidya Samajam took efforts to preserve the stagnation of knowledge and for this

Transcript of Chapter 3 Growth of Ayurvedic Industry in...

52

Chapter 3

Growth of Ayurvedic Industry in Kerala

The events that occurred at the national level regarding the

evolution and revival of Ayurveda had its traces in Kerala also. The revitalisation of

Ayurveda in Kerala is the story of the establishment of a legend in health care. The

revitalization process began in a small town Kottackkal, near Calicut in the Northern

Kerala. Panniyinpalli Sankunni Warrier was born into an orthodox but talented

family of temple service caste. The family had the reputation of good Ayurvedic

physicians. He was given formal training in Ayurveda, at the time when western

medicine was gaining acceptance in Kottackkal. He was eager to learn western

medicine but the chief handicap was the language which he learned from a native

doctor who had mastered English. He was liberal and catholic in his outlook. His

house was open to people of all caste and creed. Soon Warrier became well

accepted. This visionary realised the poor state of Ayurveda and formed the Arya

Vaidya Samajam (meaning association) in 1902. It was a formal gathering of

Ayurvedic physicians. Samajam helped to exchange views and experiences and soon

became a platform for the revitalisation movement and was perhaps the first public

body for this cause in Kerala (Panikkar, 2002).

It aimed at a creative introspection of Ayurveda both its past and

present. The Samajam meetings had two dimensions which included general

speeches and secondly reading papers that led to more professional discussions on

illness, treatment and medicine. Samajam was thus successful in bringing together

uncodified experiences and innovations in Ayurveda. The deliberations in the Arya

Vaidya Samajam took efforts to preserve the stagnation of knowledge and for this

53

they began to publish the classified texts in regional languages. This was of great use

to the people in this profession. By the end of nineteenth century there were as many

as fifty medical journals in Indian languages. Sankunni Warrier himself wrote books

in Malayalam about various dimensions of Ayurveda. The mouthpiece of the

revitalisation process in Kerala began in 1903 with the publication of a fortnightly

journal called Dhanwantari in 1903. This process of retrieval became more

successful with the establishment of some institutional infrastructure for the teaching

of Ayurveda. Keeping this in mind, Pathasala (meaning school) was started with an

aim to bring about timely changes, to train physicians and to acquaint the British

government the about the merits of indigenous system (Varier, 2002). The education

was free was open to all without any caste or a gender barriers.

The establishment of Pathasala stimulated the revitalisation

process. It became an important event in the intellectual-cultural life of Kerala and

emerged as a pioneering institutional effort to reach out to western knowledge from

a strong rooted tradition (Panikkar, 2002). Warrier realised that Ayurveda could be

effective and popular only if its medicines were standardised and prepared in

accordance with textual prescription. This was possible only if practitioners took

initiative to form companies and took steps for marketing. The popularity and

effectiveness of western medicine was largely dependent on its easy availability in

accordance with the prescription of doctors. Warrier emulated this practice. With

this view he established the Arya Vaidya Sala (hereafter AVS) in Kottackkal in the

Malappuram District of Kerala in 1902. This was the landmark in the Ayurvedic

medicine manufacturing sector of Kerala. AVS prepared medicines on modern and

scientific lines and marketed them on a commercial basis. The sale of medicine in

54

AVS was moderate in the beginning. The history of the Ayurvedic industry in the

state changes its direction here.

In Kerala, the efforts for small scale production actually began in

1900 at Trichur District of Kerala by Immatty who belonged to a well reputed

Catholic family. They had physicians in their family. All medicines except

Kashayam was prepared and bottled in their shop. Immatty catered the needs of

people in this areas and South Kerala. The land mark in the Ayurvedic Medicine

manufacturing was already set with the establishment of the AVS, Kottakkal. The

Pathasala that the AVS formed was a workshop for many enthusiastic

manufacturers to begin the process of bulk production.

The manufacturing process till the middle of the 20th

century was

undertaken by the practicing Ayurvedic physicians who had there own personal

pharmacies in their clinics preparing necessary medicines exclusively for their

patients (not for open sale). As they had to show results of these medicines to their

patients, they produced good quality medicines. The growing acceptability of these

physicians earned patients from far away places. It was difficult for the patients to

travel too long to consult their vaidhyars and collect medicines. This growing

demand for the medicines forced the companies to establish agencies as retail outlets

throughout the State. This was the beginning of the agency sale in Kerala. In Kerala

sale of Ayurvedic medicines through agencies was initiated by AVS. This channel of

distribution is still followed in Kerala.

As agency sales got widely accepted the clinic pharmacies declined.

Unlike allopathic medicines Ayurvedic medicines were not popularly sold through

private dispensaries in early days. When the demand for the medicines increased it

became impossible for the manufacturing units to meet the growing demand. This

55

forced the firms to think of large scale production by means of capital intensive

techniques. AVS initiated the mechanisation era with the initiation of AC generator

in 1949 and a counter line grinding system with 12 grinders in 1952 (Varier, 2002).

However the pace of mechanisation was not rapid. It is also essential to understand

the catalysing factors that contributed to the growth of the industry. This is dealt

with in the succeeding section.

3.1 Factors Contributing to the Growth of Ayurvedic Industry in the State

The preceding section of the chapter dealt with the evolution and

transition of Ayurvedic drug manufacturing process. One of the major factors that

contributed to the fast growth of the industry is the spontaneous growth of the health

care infrastructure. Hence a discussion of the health care infrastructure in the state

appears to be essential. The following section attempts to pinpoint this aspect.

3.1.1 Health Care Infrastructure and its Dimensions.

The sustainability and success of any health care system depends

upon the efficiency and quality of infrastructure provided to support it. However

efficient the health care system is, it cannot be useful in the absence of a support

system to hold and foster it. According to the Indian Constitution the expenditure

responsibility relating to the social sector and economic infrastructure are largely

assigned to the state Governments. Enhancing human development levels requires

state to set up their expenditure on key services like health education along with

improving delivery mechanism of public services to obtain desired outcomes. And

the imperfect nature of the health services is often regarded as a reason to justify

government intervention. Government intervention is justified because health

service market is the closest approximation of perfectly competitive equilibrium

(Arrow,1963). The decisions taken by the government is the outcome of a

56

bargaining process which reflects the collective public choices and private interest

of a few (James et al., 1990). In this process those who have stronger role in

decision making succeeds in negotiating a greater share to their side (Sadanandan,

2001). This is true in the case of Ayurvedic heath care system. The government

allocations of budget funds have always gone in favour of allopathic system

(Aravindan and Kunhikannan, 2000). Thus while government intervention in health

care is advocated to prevent discrimination it is the same government involvement

that accentuated the discrimination.

Kerala‟s achievements in health care in the backdrop of low

economic development have been widely discussed among academicians and

researchers. Kerala model as it was called in the early past was extensively put in

research at national and international levels. One of the factors that are considered

responsible for this glory is the achievements the state has made in the field of

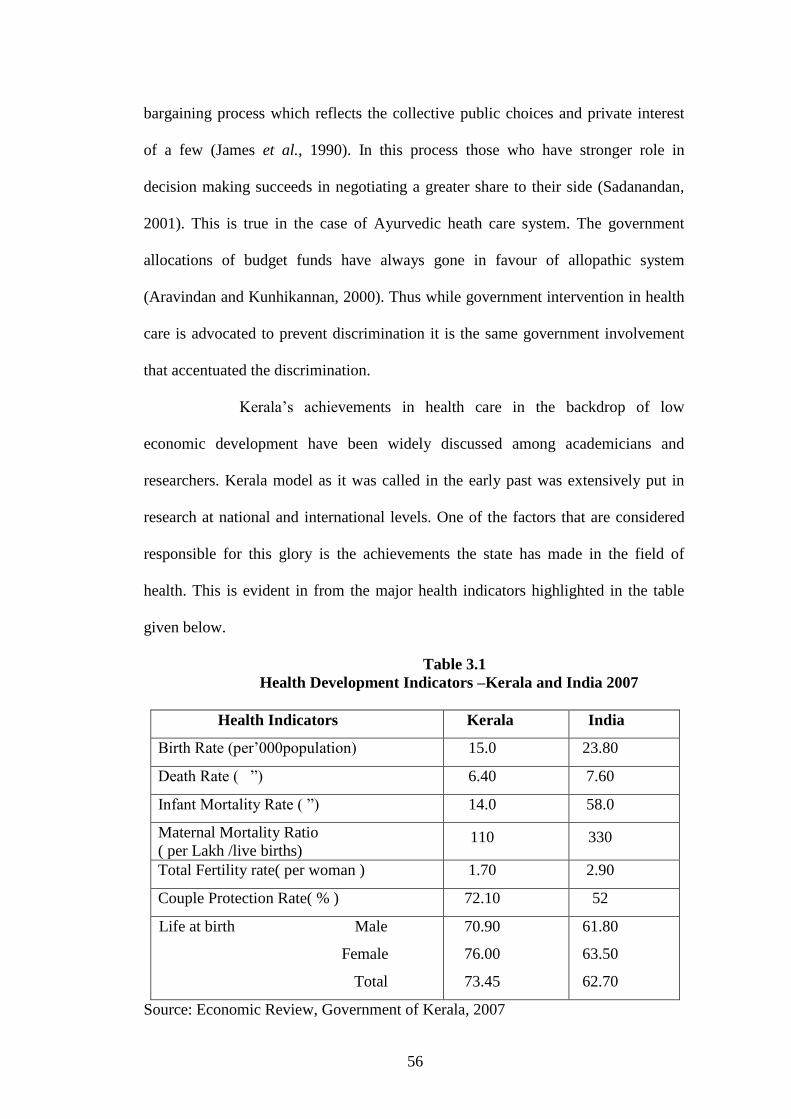

health. This is evident in from the major health indicators highlighted in the table

given below.

Table 3.1

Health Development Indicators –Kerala and India 2007

Health Indicators Kerala India

Birth Rate (per‟000population) 15.0 23.80

Death Rate ( ”) 6.40 7.60

Infant Mortality Rate ( ”) 14.0 58.0

Maternal Mortality Ratio

( per Lakh /live births) 110 330

Total Fertility rate( per woman ) 1.70 2.90

Couple Protection Rate( % ) 72.10 52

Life at birth Male

Female

Total

70.90

76.00

73.45

61.80

63.50

62.70

Source: Economic Review, Government of Kerala, 2007

57

It is evident from the table 3.1 that the accomplishment made by

Kerala are much ahead the rest of the state‟s and all India figures. Key factors

contributing to this success are high accessibility of health system at low cost, non

health contributions such as spread of education land reforms, public distribution

system of food and housing (Varatharajan et al., 2002) committed efforts of the

government etc. Among the factors the most striking would the state investment

decisions. An attempt to analyse the budget allocations of the state towards health

and the split of total health expenditure on various categories and institutions is

done in the succeeding section. The impact of these investments on the private

sector is also dealt with.

3.1.2 Budget allocations and Health Care Sector

In the pre independence period, Kerala consisted of princely kingdoms

of Travancore, Cochin and Malabar. In Travancore the provision of health care

services was considered as the duty of the state. Although the present state of Kerala

was formed in 1956, the good health status of the people existed prior to its existence.

The chief cause for this may be attributed to the existence of Ayurveda system of

health care which is native to Kerala. It was so prevalent in Kerala that people

approached the practitioners instead of going for self treatment. Even during those

days health care received due consideration in State‟s fiscal allocations. And the

increase in the supply of health care led to the increase in demand for the same. As the

state budget expanded there was a legitimate rise in the share of health.During1905-10

health care received 4.31 percent of the total share. Since 1960-65 there was a

phenomenal growth in budget allocations. During this period the all India allocation

for health was 8.30 percent of total budget allocation whereas it was 10.45 percent in

Kerala. These differences in investments allocations continued but with declining

58

trend. During 1991-95 while Kerala allocated 8.60 percent of its total expenditure for

health all India allotment was 8.12 percent (RBI Bulletin, 1995). It may be seen that

this falling share and resultant narrowing of gap between the state and all India is a

clear reflection of the mounting fiscal crisis of the state.

Education received the top priority in the state fiscal allocations

followed by health among social sectors. But the rate of growth pattern of

investments in education was not followed in the case of health. It may be

concluded that while education sector witnessed a phenomenal growth, the

investments in health showed only marginal increase. The trends show that there is

gradual withdrawal of government from health which resulted in the entry and

overall domination of the private sector in health care. Kerala has a long history of

organized health care and by the time of its formation a strong foundation for an

efficient health care system was well laid. Some medical colleges in the state are

about 150 years old (Varatharajan et al., 2002). Health has been a major item of

spending in the budget from early years. The annual growth rate of government

health care expenditure during the last three decades was 13.04 percent which was

more than the growth of Gross State Domestic Product , 9.81percent (Ramankutty,

1999). The budgetary share of health declined since 1980-81 from 6.95 percent to

around 5 percent in 2000-01. As a percentage of the GSDP the figures are more

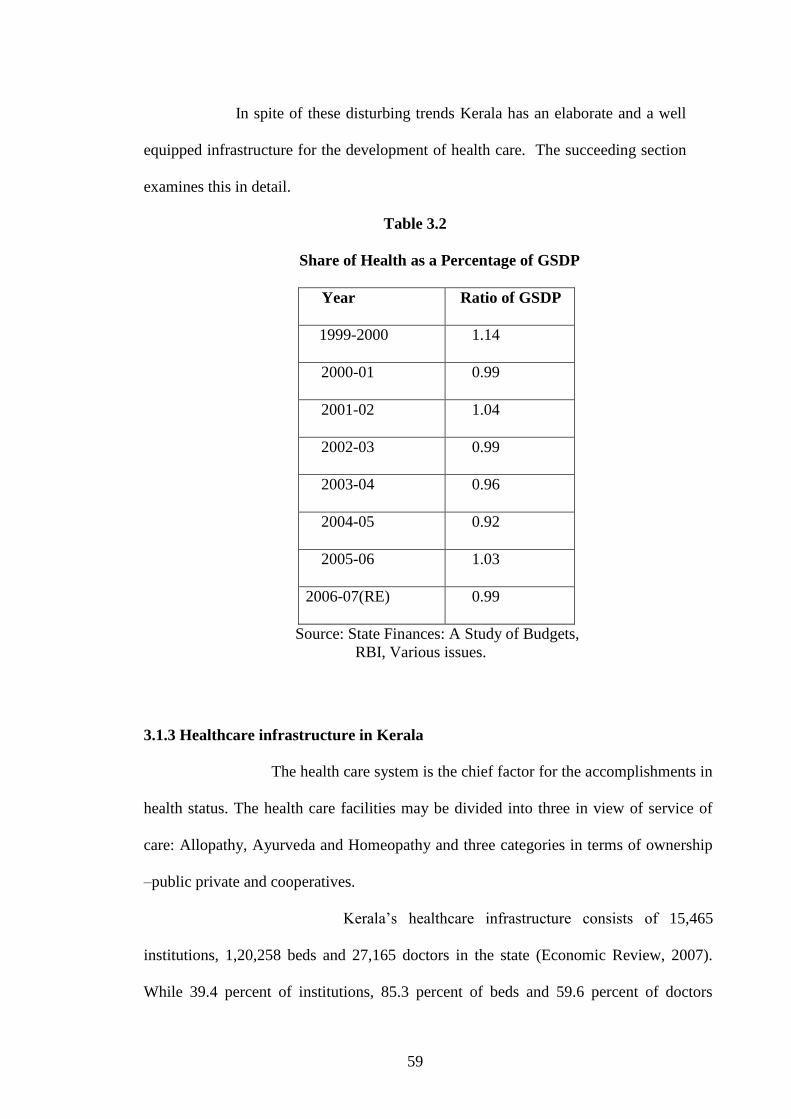

damaging as evident from table 3.2.

It is evident from the table that the health expenditure as a percent of

GSDP experienced a major contraction since 1999. However the share of education,

water supply and sanitation and social services (components other than health in

development expenditure) showed the tendency to revert the trend in spending in the

budget estimates of 2006-07, no such trend was witnessed in the case of health.

59

In spite of these disturbing trends Kerala has an elaborate and a well

equipped infrastructure for the development of health care. The succeeding section

examines this in detail.

Table 3.2

Share of Health as a Percentage of GSDP

Year Ratio of GSDP

1999-2000 1.14

2000-01 0.99

2001-02 1.04

2002-03 0.99

2003-04 0.96

2004-05 0.92

2005-06 1.03

2006-07(RE) 0.99

Source: State Finances: A Study of Budgets,

RBI, Various issues.

3.1.3 Healthcare infrastructure in Kerala

The health care system is the chief factor for the accomplishments in

health status. The health care facilities may be divided into three in view of service of

care: Allopathy, Ayurveda and Homeopathy and three categories in terms of ownership

–public private and cooperatives.

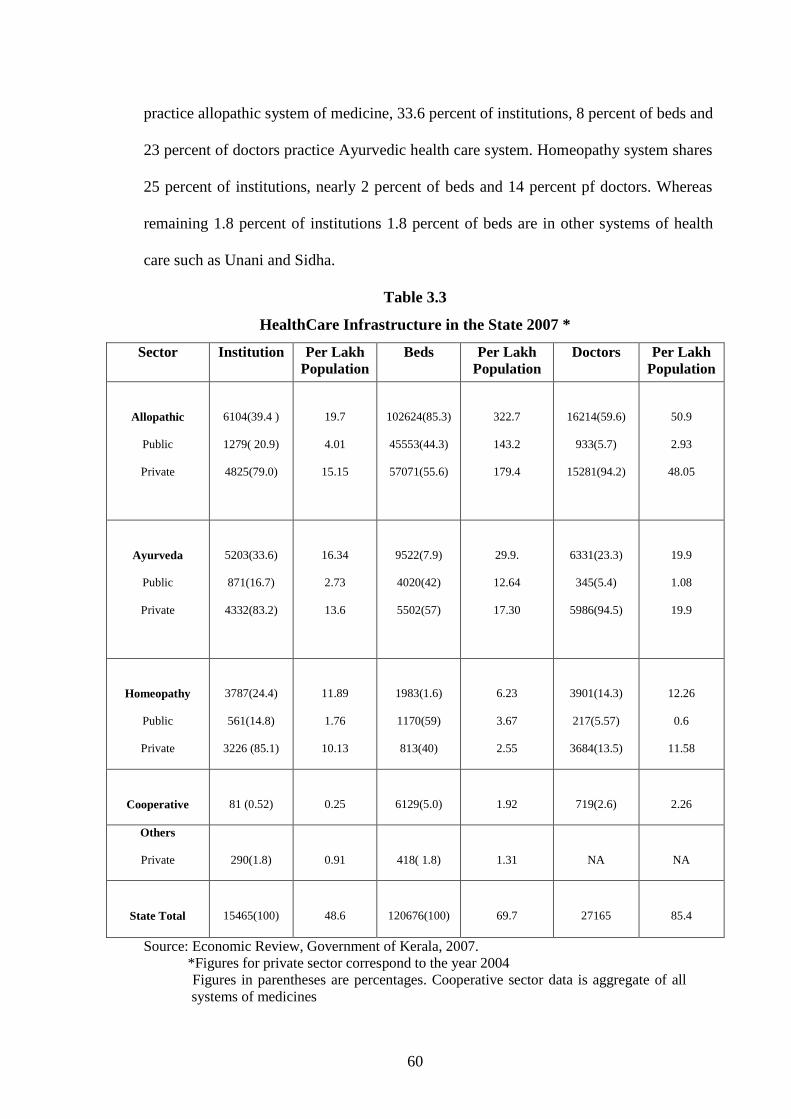

Kerala‟s healthcare infrastructure consists of 15,465

institutions, 1,20,258 beds and 27,165 doctors in the state (Economic Review, 2007).

While 39.4 percent of institutions, 85.3 percent of beds and 59.6 percent of doctors

60

practice allopathic system of medicine, 33.6 percent of institutions, 8 percent of beds and

23 percent of doctors practice Ayurvedic health care system. Homeopathy system shares

25 percent of institutions, nearly 2 percent of beds and 14 percent pf doctors. Whereas

remaining 1.8 percent of institutions 1.8 percent of beds are in other systems of health

care such as Unani and Sidha.

Table 3.3

HealthCare Infrastructure in the State 2007 *

Sector

Institution Per Lakh

Population

Beds Per Lakh

Population

Doctors Per Lakh

Population

Allopathic

Public

Private

6104(39.4 )

1279( 20.9)

4825(79.0)

19.7

4.01

15.15

102624(85.3)

45553(44.3)

57071(55.6)

322.7

143.2

179.4

16214(59.6)

933(5.7)

15281(94.2)

50.9

2.93

48.05

Ayurveda

Public

Private

5203(33.6)

871(16.7)

4332(83.2)

16.34

2.73

13.6

9522(7.9)

4020(42)

5502(57)

29.9.

12.64

17.30

6331(23.3)

345(5.4)

5986(94.5)

19.9

1.08

19.9

Homeopathy

Public

Private

3787(24.4)

561(14.8)

3226 (85.1)

11.89

1.76

10.13

1983(1.6)

1170(59)

813(40)

6.23

3.67

2.55

3901(14.3)

217(5.57)

3684(13.5)

12.26

0.6

11.58

Cooperative

81 (0.52)

0.25

6129(5.0)

1.92

719(2.6)

2.26

Others

Private

290(1.8)

0.91

418( 1.8)

1.31

NA

NA

State Total

15465(100)

48.6

120676(100)

69.7

27165

85.4

Source: Economic Review, Government of Kerala, 2007.

*Figures for private sector correspond to the year 2004

Figures in parentheses are percentages. Cooperative sector data is aggregate of all

systems of medicines

61

Public sector commands control over 17 percent of institutions 44 percent

of beds and 5.6 percent of the doctors, while 82 percent of institutions 55 percent of beds

and 94 percent of doctors are in private sector. The remaining 0.52 percent of institutions

5 percent of beds and 2.6 percent of doctors is in the cooperative sector. The private

sector completely outstrips the public sector in terms of the number of institutions, beds

and practicing doctors. The public sector now has 2711 institutions, 50743 beds and

1495 doctors. Although 32 percent (16.7 percent Ayurveda and 14.8 percent

homeopathic) of public institutions practice Indian system of medicine, Allopathic

system controls over 79 percent of institutions, 44 percent of beds and over 92.7 percent

of doctors. Historically, the involvement of private sector in health care of Kerala was

provided by institutions such as mission hospitals which existed for a non – profit causes

(Kawasimha, 1998). But the present state of the mushrooming private sector, reveals that

it exist for a pure profit cause. The advancement in technology, the aging of the society

and the over health consciousness of the people have raised the cost of health care. At

the same time the fiscal crisis of the state had reached dangerous point leading to falling

share of health in the state budgets. This gave a space for the private sector to grow and

dominate the health care sector in Kerala.

Needless to say the fiscal crisis of the state has affected the quality of

health care provided in the public sector. Most of the people prefer private sector

because of the care provided by the public sector did not satisfy them. The shortage of

medicines, less availability of facilities, curt attitude of the health personnel, and lack of

cleanliness in the government owned medical institutions led to the growing demand for

private sector. It is believed that in Kerala demand for health is governed by the factors

more than ability to pay (Sankar, 2001). Further, more the underutilisation of the health

care infrastructure in the public sector, due to financial and managerial reasons has led

62

to the creation of idle capacity in the public sector which is estimated to be 12.3 percent

for doctors, 25.7 percent for nurses, 25.7 percent for beds, 53.2 percent for building

spaces and 59.3 percent for land. (Varatharajan et al., 2002). Thus it is clear from the

forgoing analysis that the trend and prospects in the health expenditure has laid down a

clear platform for the growth of Ayurvedic industry in the state. The gradual withdrawal

of the government from health care led to the upcoming of the private sector and this

augmented the emergence of large number of Ayurvedic medicine manufacturing units

in Kerala.

3.2 Structure of Ayurvedic Industry in Kerala

Normally Ayurvedic drug manufacturers in Kerala are classified into

two categories - organised and unorganised manufacturers. The organised sector can

be further classified into large scale manufacturers and small scale manufacturers.

Large scale manufacturers: are well established manufactures who

operate at national and international levels. They are the leaders in the industry who

bring dynamic changes into the industry. Large firms have the advantage of being

the torch bearers of the royal families who possessed mastery of Ayurveda. These

firms enjoy the goodwill and acceptance in the minds of the present day consumers.

They invest largely in R & D and are largely responsible for the revival and growth

of the Ayurvedic industry in the country. In terms of source of knowledge, nature

and process of drug discovery, product innovation, marketing, scientific

applications, fragmentation of markets, consumer categories and pricing they

resemble the allopathic pharmaceutical sector.

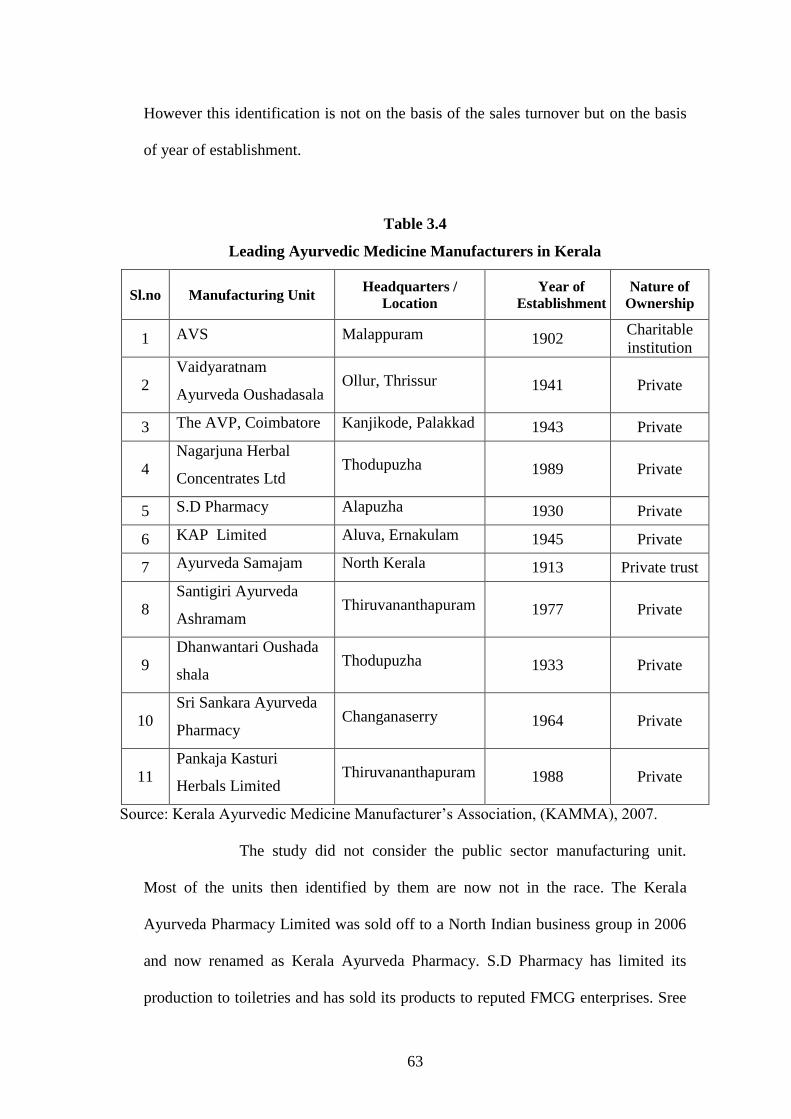

A study of the Ayurvedic industry conducted by EXIM Bank (2002)

and Kerala State Industrial Development Corporation (2004) identified 11 major

players in the State. The major players identified by the KSIDC are as follows.

63

However this identification is not on the basis of the sales turnover but on the basis

of year of establishment.

Table 3.4

Leading Ayurvedic Medicine Manufacturers in Kerala

Sl.no Manufacturing Unit Headquarters /

Location

Year of

Establishment

Nature of

Ownership

1 AVS Malappuram 1902 Charitable

institution

2

Vaidyaratnam

Ayurveda Oushadasala Ollur, Thrissur 1941 Private

3 The AVP, Coimbatore Kanjikode, Palakkad 1943 Private

4

Nagarjuna Herbal

Concentrates Ltd Thodupuzha 1989 Private

5 S.D Pharmacy Alapuzha 1930 Private

6 KAP Limited Aluva, Ernakulam 1945 Private

7 Ayurveda Samajam North Kerala 1913 Private trust

8

Santigiri Ayurveda

Ashramam Thiruvananthapuram 1977 Private

9

Dhanwantari Oushada

shala Thodupuzha 1933 Private

10

Sri Sankara Ayurveda

Pharmacy Changanaserry 1964 Private

11

Pankaja Kasturi

Herbals Limited Thiruvananthapuram 1988 Private

Source: Kerala Ayurvedic Medicine Manufacturer‟s Association, (KAMMA), 2007.

The study did not consider the public sector manufacturing unit.

Most of the units then identified by them are now not in the race. The Kerala

Ayurveda Pharmacy Limited was sold off to a North Indian business group in 2006

and now renamed as Kerala Ayurveda Pharmacy. S.D Pharmacy has limited its

production to toiletries and has sold its products to reputed FMCG enterprises. Sree

64

Sankara Pharmacy is now concentrating on the treatment side alone. Pankaja Kasturi

has focused its attention in the promotion of its branded product which has made

remarkable impact in the Ayurvedic sector of Kerala. The Pharmaceutical

Corporation (Indian Medicines) Kerala Limited (popularly known as Oushadi and

hereafter Oushadi) commenced in 1941 and registered as company in 1975 is the

largest producer of Ayurvedic medicines in the public sector in India.

Small scale manufactures: these firms operate in a particular

geographical area and produce a few specialised drugs. They are large in number but

contribute very marginally to the total production. Their production is mainly

household oriented1. They do not carry production on all days. Nonetheless they are

very strong in their area of operation.

The unorganised sector consists of small units owned and operated by

vaidhyars who are locally well accepted. They have rich clients and are always

approachable. They produce as per the need and do not face problems like

infrastructural constraints, procurement of medicines, mechanisation and other fiscal

formalities and regulations. The production process followed by them is very simple.

Most of the medicinal herbs needed for the preparation are grown in their own

premises or are locally bought. Their consumers have greater confidence in them

and they are not registered manufacturers their sales turnover is not officially known

but the total sales of the entire unorganised manufactures taken together will be

much larger than the sales of the large firms taken individually.

65

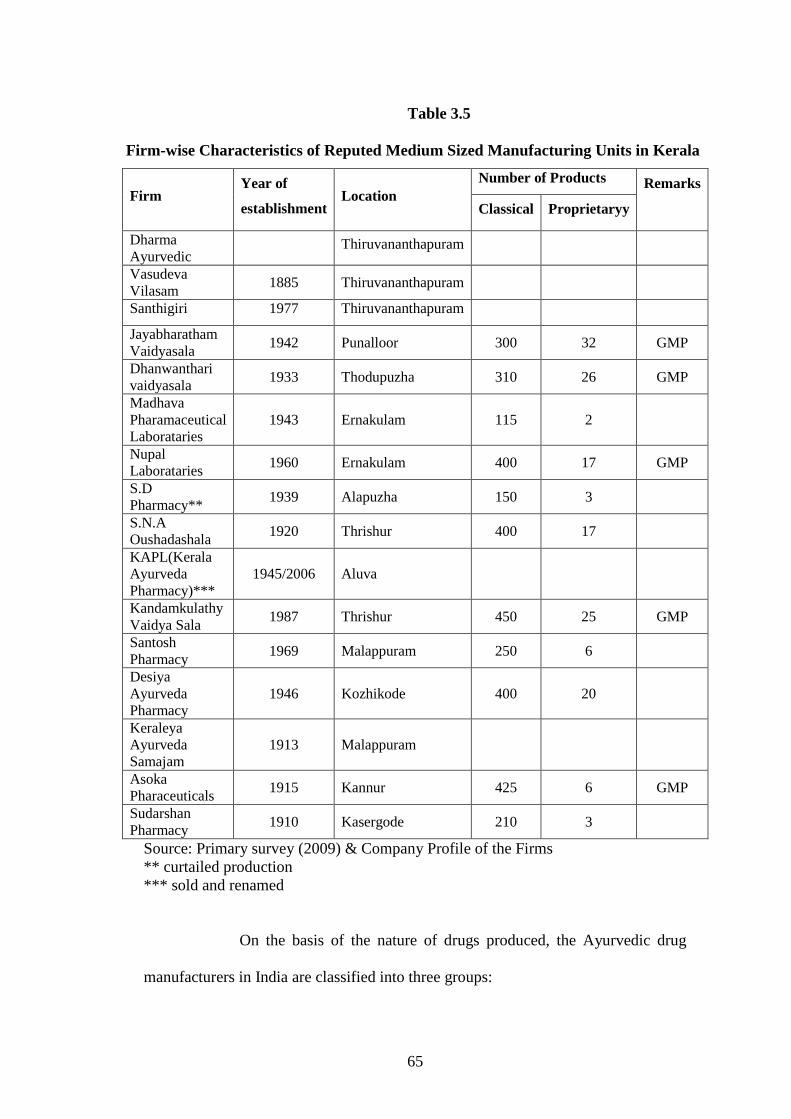

Table 3.5

Firm-wise Characteristics of Reputed Medium Sized Manufacturing Units in Kerala

Firm Year of

establishment Location

Number of Products Remarks

Classical Proprietaryy

Dharma

Ayurvedic Thiruvananthapuram

Vasudeva

Vilasam 1885 Thiruvananthapuram

Santhigiri 1977 Thiruvananthapuram

Jayabharatham

Vaidyasala 1942 Punalloor 300 32 GMP

Dhanwanthari

vaidyasala 1933 Thodupuzha 310 26 GMP

Madhava

Pharamaceutical

Laborataries

1943 Ernakulam 115 2

Nupal

Laborataries 1960 Ernakulam 400 17 GMP

S.D

Pharmacy** 1939 Alapuzha 150 3

S.N.A

Oushadashala 1920 Thrishur 400 17

KAPL(Kerala

Ayurveda

Pharmacy)***

1945/2006 Aluva

Kandamkulathy

Vaidya Sala 1987 Thrishur 450 25 GMP

Santosh

Pharmacy 1969 Malappuram 250 6

Desiya

Ayurveda

Pharmacy

1946 Kozhikode 400 20

Keraleya

Ayurveda

Samajam

1913 Malappuram

Asoka

Pharaceuticals 1915 Kannur 425 6 GMP

Sudarshan

Pharmacy 1910 Kasergode 210 3

Source: Primary survey (2009) & Company Profile of the Firms

** curtailed production

*** sold and renamed

On the basis of the nature of drugs produced, the Ayurvedic drug

manufacturers in India are classified into three groups:

66

1. Truly traditional manufacturers who produce proper Ayurvedic

medicines based on classic texts2. They are largely self-regulated, grown on the

basis of their merit and good will. They still consider production of Ayurvedic

medicines as ethical or holistic.

2. Firms that produce cosmetic and personnel care products3 they draw upon

the traditional knowledge without fully following them.

3. New entrants into the scene are firms producing patent products. They use

the textual sources and formulate medicines according to their R& D.

Majority of the firms operating in the state come under the first

category but there seem to be a fast rise in the number of firms indulged in the

making of cosmetic and patented products. The well established companies of

Ayurvedic medicines are strengthening this part of their operations (Banerjee, 2002).

3.3 Characteristics of Ayurvedic Industry in Kerala

The Ayurvedic Industry in the state possesses certain

characteristic features. These features are unique to Kerala.

1. Monopolistic in nature. The Ayurvedic industry in the state is a classic example for

monopolistic market structure. It implies that there are large number of producers

and large number of consumers for the Ayurvedic medicines. It follows product

differentiation to the extent that each producer produces textual medicines by

making minor modifications in the classical formulations. These differentiated

products are known as patented products or proprietary medicines. The patented

products are new formulations made on the basis of established Ayurvedic

knowledge.

2. High concentration. There is heavy geographical concentration of units in

Kerala. Majority of the units are located in north Kerala. 58 percent of the units in

67

1998, 45 percent in 2001 and 48 percent of the units in 2007 are located in north

Kerala. This concentration of industry may be ascribed to the availability of

medicinal plants, existence of qualified vaidhyars, recognition for Ayurvedic system

etc.

3. Traditional legacy. Majority of the units have a strong traditional knowledge of

Ayurveda which was richly inherited from their forefathers. This is evident from the

close observation of the units in Kerala. Even the new generation Ayurvedic firms

possess sound hereditary traits. This hereditary legacy has helped tremendously in

earning reputation and good will for the units. The respect for the traditional families

who practiced Ayurveda with a holistic approach was transmitted to their present

day torchbearers which are evident from their growing sales figures.

4. Medicinal plant market nexus. Like any other industry the Ayurvedic

manufacturing units in Kerala are closely knitted to those areas where there is easy

availability of medicinal herbs. The concentration of the units in north Kerala is

mainly credited to the supply of herbs from the Attapady, Badagara, Nilambur and

Wayanad forest regions, the focus of units lying in the central Kerala depend upon

the medicinal plant market in the high ranges of Idukki district and the units in the

south Kerala depend upon the tribal belt of the southern parts of Western Ghats

particularly from area such as Palode and Kottur market. This proximity to

medicinal plant market helps them to reduce the cost of transportation and easy and

timely availability of raw materials.

5. Private sector domination. The Ayurvedic industry in the State is dominated by

the private sector. There are only two public sector firms in the state, The

Pharmaceutical Corporation of Kerala Limited (Oushadi) and Ayurdhara4

established in 2000 operated by the Kerala State SC/ST Federation. These two units

68

supply Ayurvedic medicines to the government Ayurvedic hospitals, dispensaries

and clinics. Besides they have agencies within the state and outside. Among these

two units Oushadi is key public sector firm and that part of the demand unmet by

Oushadi is fulfilled by Ayurdhara.

6. Existence of a few large firms and too many small firms. Another unique

characteristic of the industry is the coexistence of a few large firms who produce

nearly 80 percent of the total Ayurvedic medicines and large number of small firms

who contribute marginally to the total output. This coexistence has created negative

effect on the very existence of the small firms.

7. Capital intensive. One of the major defects of the Ayurvedic industry in the past

was the traditional method of producing medicines. Mostly the medicines were

produced by the Vaidhyars using their hands and this was a reason for lesser

acceptance for Ayurvedic medicines especially in the West. This was replaced by

mechanised units. All the leading producers have well equipped machines and the

process of manufacture is well coordinated through skilled and trained labour.

However the contribution of capital to total product is not seen to be significant. The

traces of traditional methods of production are still seen among small scale

manufacturers.

8. Production in anticipation of demand. The production in this industry is in

anticipation of demand and not according to demand. The demand requirements

cannot be suddenly met because the preparation of medicines is a lengthy process

which involves preserving. It also depends upon the availability of raw materials.

Hence the total quantity to be produced is done on the basis of past demand and

future expectations.

69

9. Price differentials. Although the ingredients of the textual medicines are the

same for all manufactures the price of the product varies from firm to firm. These

price variations are mainly due to the differences in the size of the firm, the

economies in production enjoyed by the large firms. But the interesting aspect about

the industry is that these differences in price do not influence the consumer‟s

preference for a particular firm. Hence it may be inferred that it is the brand name

rather than the price that influences the consumer demand.

10. Family–owned business Ayurvedic medicine manufacturing companies

whether in organised or unorganised sector are mostly family owned business. The

origin of these units may be traced back to a vaidya who used to prepare medicines

for dispensing and gradual acceptance led to the growth of such units. Most of these

units are run by third generation members. This ownership pattern has led to transfer

knowledge from one generation to other thereby enriching the knowledge base of

the units.

3.4 Growth of Ayurvedic Industry in Kerala

The evolution and transition of Ayurvedic industry in the

state its structure and characteristics has been described in the earlier section. The

discussion on the Industry helps to get an overview of the industry. Needless to say

the Ayurvedic industry in the state has attained phenomenal growth over the years

both in terms of the real output employment, volume of sales etc. The succeeding

section attempts to portray the overall growth of the Ayurvedic industry in the state.

70

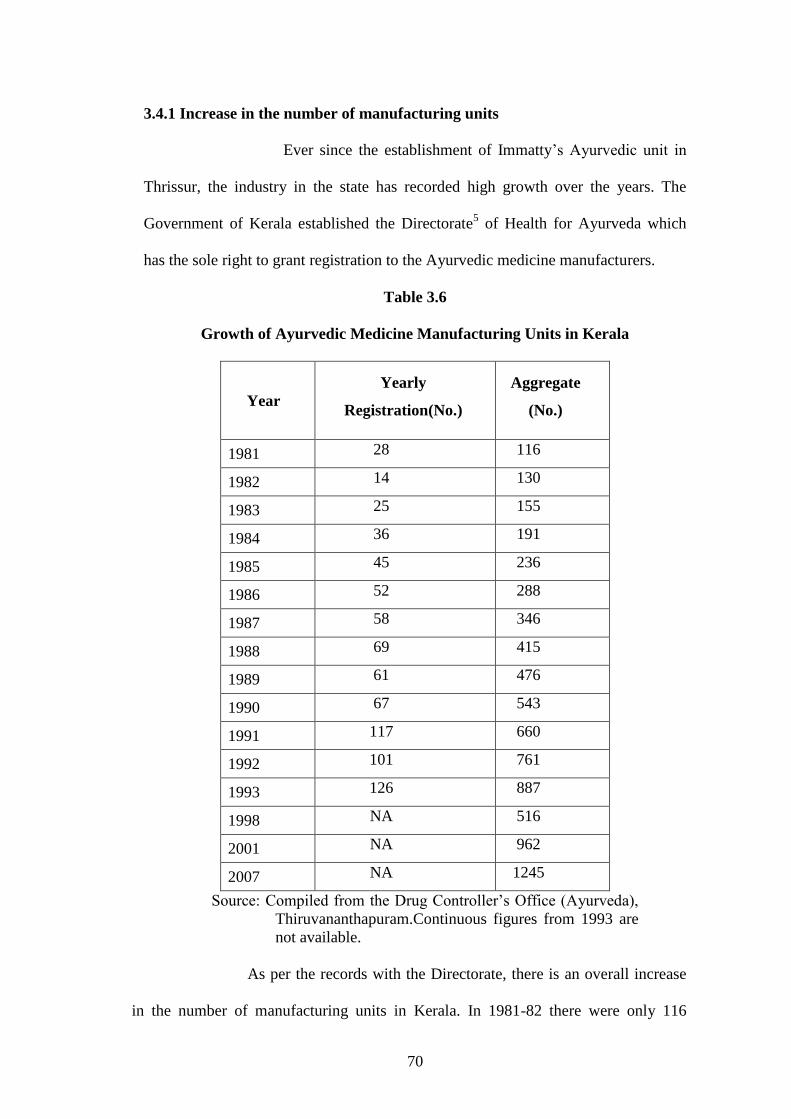

3.4.1 Increase in the number of manufacturing units

Ever since the establishment of Immatty‟s Ayurvedic unit in

Thrissur, the industry in the state has recorded high growth over the years. The

Government of Kerala established the Directorate5 of Health for Ayurveda which

has the sole right to grant registration to the Ayurvedic medicine manufacturers.

Table 3.6

Growth of Ayurvedic Medicine Manufacturing Units in Kerala

Year

Yearly

Registration(No.)

Aggregate

(No.)

1981 28 116

1982 14 130

1983 25 155

1984 36 191

1985 45 236

1986 52 288

1987 58 346

1988 69 415

1989 61 476

1990 67 543

1991 117 660

1992 101 761

1993 126 887

1998 NA 516

2001 NA 962

2007 NA 1245

Source: Compiled from the Drug Controller‟s Office (Ayurveda),

Thiruvananthapuram.Continuous figures from 1993 are

not available.

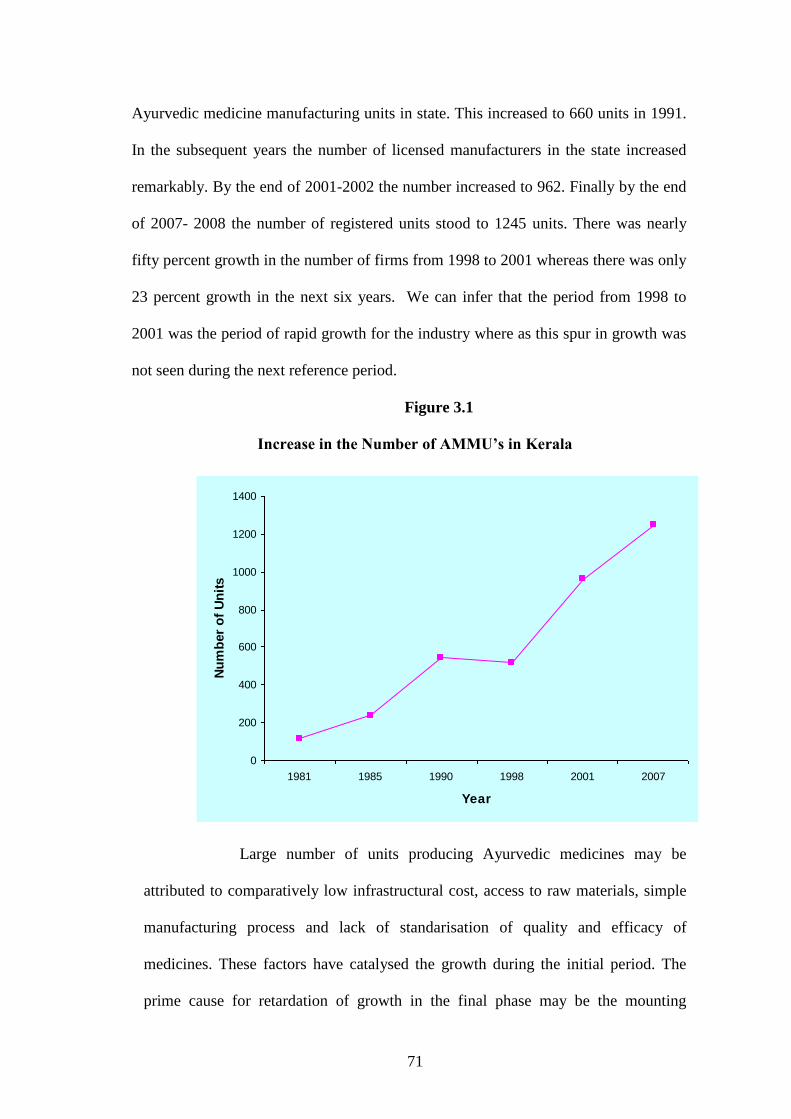

As per the records with the Directorate, there is an overall increase

in the number of manufacturing units in Kerala. In 1981-82 there were only 116

71

Ayurvedic medicine manufacturing units in state. This increased to 660 units in 1991.

In the subsequent years the number of licensed manufacturers in the state increased

remarkably. By the end of 2001-2002 the number increased to 962. Finally by the end

of 2007- 2008 the number of registered units stood to 1245 units. There was nearly

fifty percent growth in the number of firms from 1998 to 2001 whereas there was only

23 percent growth in the next six years. We can infer that the period from 1998 to

2001 was the period of rapid growth for the industry where as this spur in growth was

not seen during the next reference period.

Figure 3.1

Increase in the Number of AMMU’s in Kerala

0

200

400

600

800

1000

1200

1400

1981 1985 1990 1998 2001 2007

Year

Nu

mb

er

of

Un

its

Large number of units producing Ayurvedic medicines may be

attributed to comparatively low infrastructural cost, access to raw materials, simple

manufacturing process and lack of standarisation of quality and efficacy of

medicines. These factors have catalysed the growth during the initial period. The

prime cause for retardation of growth in the final phase may be the mounting

72

resource depletion, increased cost of production, governmental regulations etc. If we

go through the year of establishment of the leading firms in Kerala we find that all

the large and leading firms were established during the early phase. Further the

increasing demand for herbal cosmetics have paved the way for the upcoming of too

many small and medium firms in the final phase. The nature of the industry shows

heavy concentration as discussed in the characteristics of the Ayurvedic industry.

This can be established from the table 3.7.

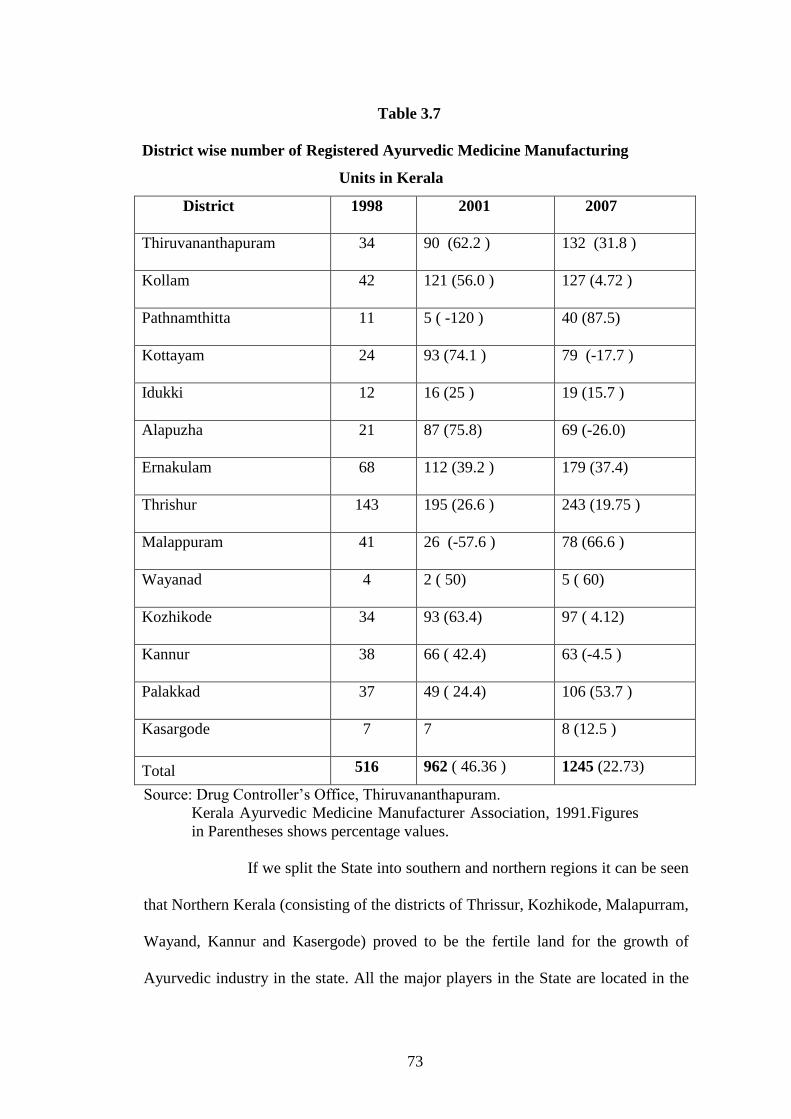

The table clearly shows the growth of the industry in absolute and

relative terms. The number of units increased from 516 to 962 units in 2001 and to

1245 units in 2007. The rate of growth in the number of units in Kollam declined

sharply from 56 percent in 2001 to 4.6 percent in 2007.

The district of Thrissur has the credit of having the maximum

number of units in Kerala and it still continues to hold the record. Various reasons

are attributed to this record. Easy availability of land, existence of many royal

families (Ashtavaidya)6 who inherited the practice of Ayurveda, the easy availability

of medicinal plants,(trade of medicinal plants from Attapady region in Palakkad is

concentrated at Thrissur), the rapid acceptance of the Ayurvedic system, the

patronage given by the King Sakthan Thampuran etc. have attributed to this

sustained success. It was reported by the respondents that people of Thrissur have a

greater passion for medicinal plants and they used to supply the medicinal plants or

their parts to manufacturing units, voluntarily. However a steady rise was seen in the

district of Malappuram which is the headquarters of the leader of Ayurvedic industry

in Kerala, the AVS.

73

Table 3.7

District wise number of Registered Ayurvedic Medicine Manufacturing

Units in Kerala

District 1998 2001 2007

Thiruvananthapuram 34 90 (62.2 ) 132 (31.8 )

Kollam 42 121 (56.0 ) 127 (4.72 )

Pathnamthitta 11 5 ( -120 ) 40 (87.5)

Kottayam 24 93 (74.1 ) 79 (-17.7 )

Idukki 12 16 (25 ) 19 (15.7 )

Alapuzha 21 87 (75.8) 69 (-26.0)

Ernakulam 68 112 (39.2 ) 179 (37.4)

Thrishur 143 195 (26.6 ) 243 (19.75 )

Malappuram 41 26 (-57.6 ) 78 (66.6 )

Wayanad 4 2 ( 50) 5 ( 60)

Kozhikode 34 93 (63.4) 97 ( 4.12)

Kannur 38 66 ( 42.4) 63 (-4.5 )

Palakkad 37 49 ( 24.4) 106 (53.7 )

Kasargode 7 7 8 (12.5 )

Total 516 962 ( 46.36 ) 1245 (22.73)

Source: Drug Controller‟s Office, Thiruvananthapuram.

Kerala Ayurvedic Medicine Manufacturer Association, 1991.Figures

in Parentheses shows percentage values.

If we split the State into southern and northern regions it can be seen

that Northern Kerala (consisting of the districts of Thrissur, Kozhikode, Malapurram,

Wayand, Kannur and Kasergode) proved to be the fertile land for the growth of

Ayurvedic industry in the state. All the major players in the State are located in the

74

northern region. The aggregate figures depict the steady growth of the industry over

the years. It can be seen that if the early growth was marked by the coming of large

units, the growth in the later years is attributed to the establishment of small firms.

Most of these new firms are engaged in the manufacturing of cosmetic herbal

products which have a greater demand in the market. But the field experience

revealed that many of the registered units were not operating. Again there were units

which carried out production in seasonally specific periods like August to January

(Karkidakam7) which is considered to be the month for rejuvenating health using

Ayurveda. Hence it can be concluded that the actual number of operating units may

be much lesser than the published figures.

3.4.2 Consumption of Raw material

The increase in the amount of inputs used in the production of

the output may be treated as the indicator for the growth of the industry. As mentioned

in the forgoing section the number of small and medium firms exceeds the number of

large firms. A serious handicap in this area is that most of the small and tiny units do

not maintain proper records of the raw material consumption. Hence the analysis is

based on the raw material consumption figures of the large firms. Major raw material

used in the Ayurvedic industry is medicinal plants obtained from forest and cultivable

lands. Apart from this the industry used jaggery, ghee, oil, preservatives, permitted

amounts of alcohol etc. Here the data relates to the consumption of medicinal plants

alone, as they constitute 80 percent of the total raw material used in the formulation of

Ayurvedic medicines. The data shows that the consumption of the raw material is on

an increase. From the output figures and the data obtained from the leading firms we

can infer that the consumption in absolute terms has consistently increased during the

period of study.

75

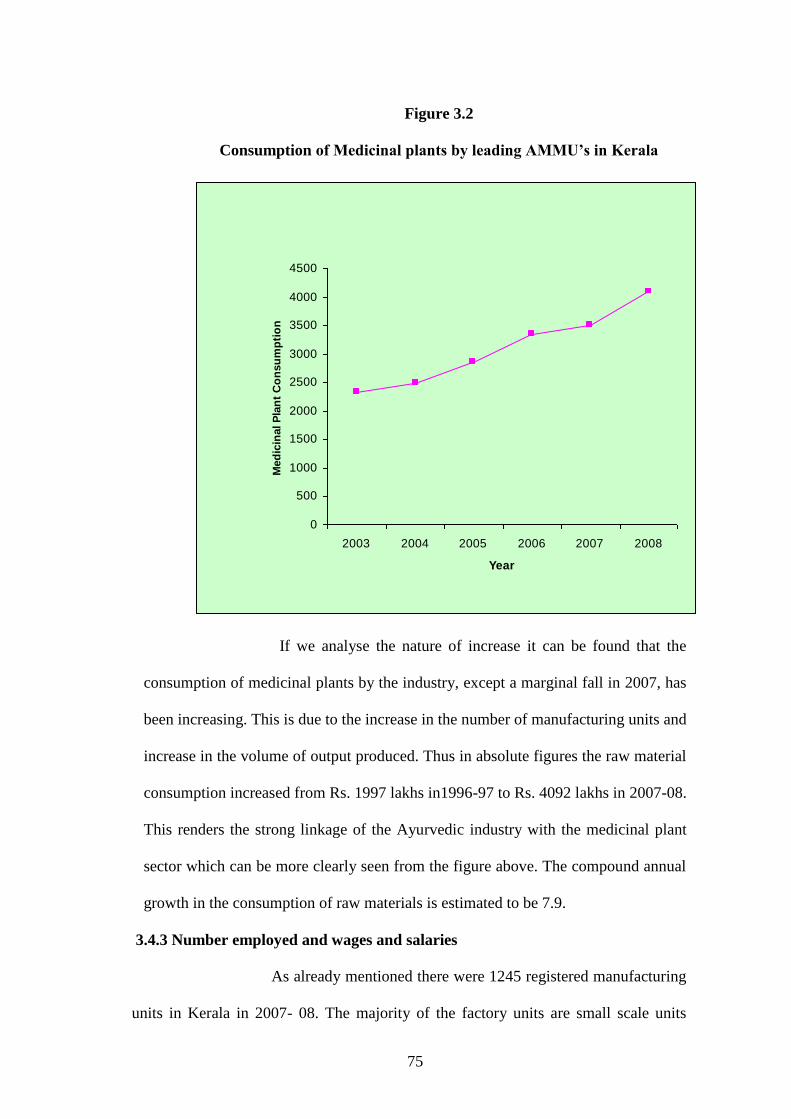

Figure 3.2

Consumption of Medicinal plants by leading AMMU’s in Kerala

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2003 2004 2005 2006 2007 2008

Year

Med

icin

al P

lan

t C

on

su

mp

tio

n

If we analyse the nature of increase it can be found that the

consumption of medicinal plants by the industry, except a marginal fall in 2007, has

been increasing. This is due to the increase in the number of manufacturing units and

increase in the volume of output produced. Thus in absolute figures the raw material

consumption increased from Rs. 1997 lakhs in1996-97 to Rs. 4092 lakhs in 2007-08.

This renders the strong linkage of the Ayurvedic industry with the medicinal plant

sector which can be more clearly seen from the figure above. The compound annual

growth in the consumption of raw materials is estimated to be 7.9.

3.4.3 Number employed and wages and salaries

As already mentioned there were 1245 registered manufacturing

units in Kerala in 2007- 08. The majority of the factory units are small scale units

76

employing less than 20 labourers. Many of the small and tiny units adhere to seasonal

labourers. Here, record of actual labour, directly employed in the production of

medicines is only considered. Thus the number of labour employed in the production

increased from 2780 in 1999-98 to 4880 labourers in 2007-08.

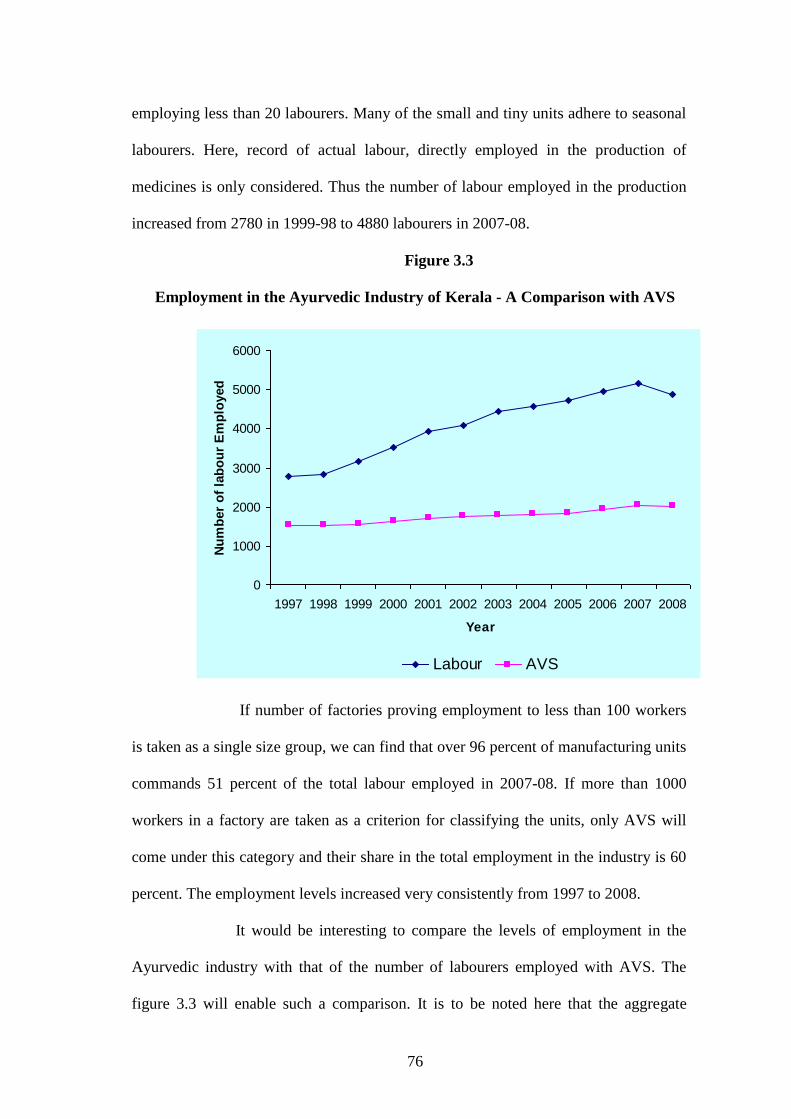

Figure 3.3

Employment in the Ayurvedic Industry of Kerala - A Comparison with AVS

0

1000

2000

3000

4000

5000

6000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Year

Nu

mb

er

of

lab

ou

r E

mp

loyed

Labour AVS

If number of factories proving employment to less than 100 workers

is taken as a single size group, we can find that over 96 percent of manufacturing units

commands 51 percent of the total labour employed in 2007-08. If more than 1000

workers in a factory are taken as a criterion for classifying the units, only AVS will

come under this category and their share in the total employment in the industry is 60

percent. The employment levels increased very consistently from 1997 to 2008.

It would be interesting to compare the levels of employment in the

Ayurvedic industry with that of the number of labourers employed with AVS. The

figure 3.3 will enable such a comparison. It is to be noted here that the aggregate

77

employment trends in the Ayurvedic industry has been similar to the trend of

employment in AVS. The pattern of the employment corresponds to the rise and fall

of the labour employed in the industry. This may help us to confer that the industry

has followed the pattern of its leader. This trend needless to say happens because AVS

employs maximum number of labour. The compound annual growth in the number of

labour employed in the Ayurvedic industry as a whole was estimated to be 6. Wages

and salaries disbursed to the employees have also increased over the years. From

Rs.661 lakhs in 1997- 98, the total emoluments given to the employees in the

Ayurvedic industry have increased to Rs.2374 lakhs in 2007-08. The compound

annual growth in the increase in wages and salaries estimated to be 14.8.

3.4.4 Product Profile

The modernisation and commercialisation that has happened in the

Ayurvedic industry of Kerala is very evident when we observe the dynamic change in

the product profile of the firms. The developments in Ayurvedic pharmacy during the

past half a century focused on the enhancement of effectiveness, changing the form of

medicine (for instance, decoctions into tablets) and improving tastiness. The industry

produces three kinds of medicines such as medicines that are based on classical

formulations or textual medicines; proprietary medicines8 which are patented

9 and

cosmetic and toiletries.

Over the years the number of firms producing the third category of

medicines has increased and the numbers of firms producing pure Ayurvedic

medicines have declined. Most of the firms deal with branded products10

which are of

great demand and are sold as over–the-counter products. These consumer brands are

advertised directly to consumers through public media such as television, newspapers

and magazines. In contrast, the biomedical providers are marketed to physicians,

78

pharmacists and chemists. Most of the medium sized firms produce patented

medicines by altering some composition in the classical formulations. Generally, the

proprietary medicines and beauty products fall into the category of consumer brands

and seem to be fast moving in the world market. However the national trend shows

that there is greater demand and orientation towards the consumer brands.

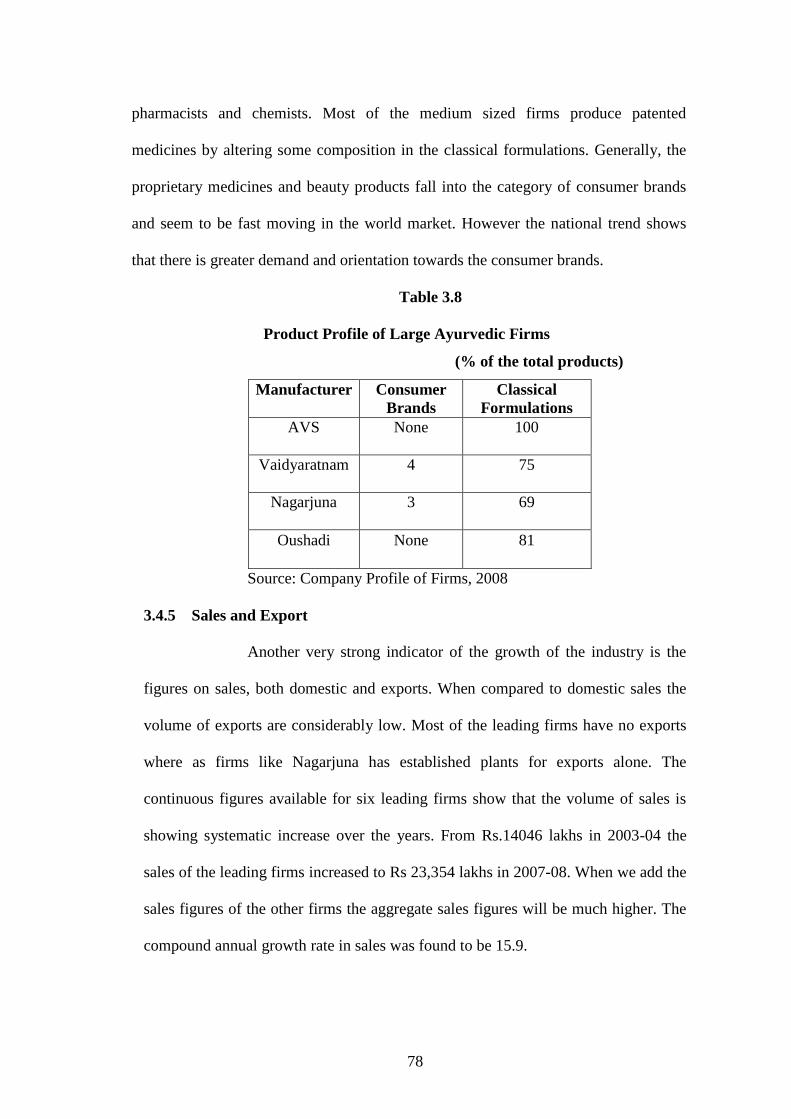

Table 3.8

Product Profile of Large Ayurvedic Firms

(% of the total products)

Manufacturer Consumer

Brands

Classical

Formulations

AVS None 100

Vaidyaratnam 4 75

Nagarjuna 3 69

Oushadi None 81

Source: Company Profile of Firms, 2008

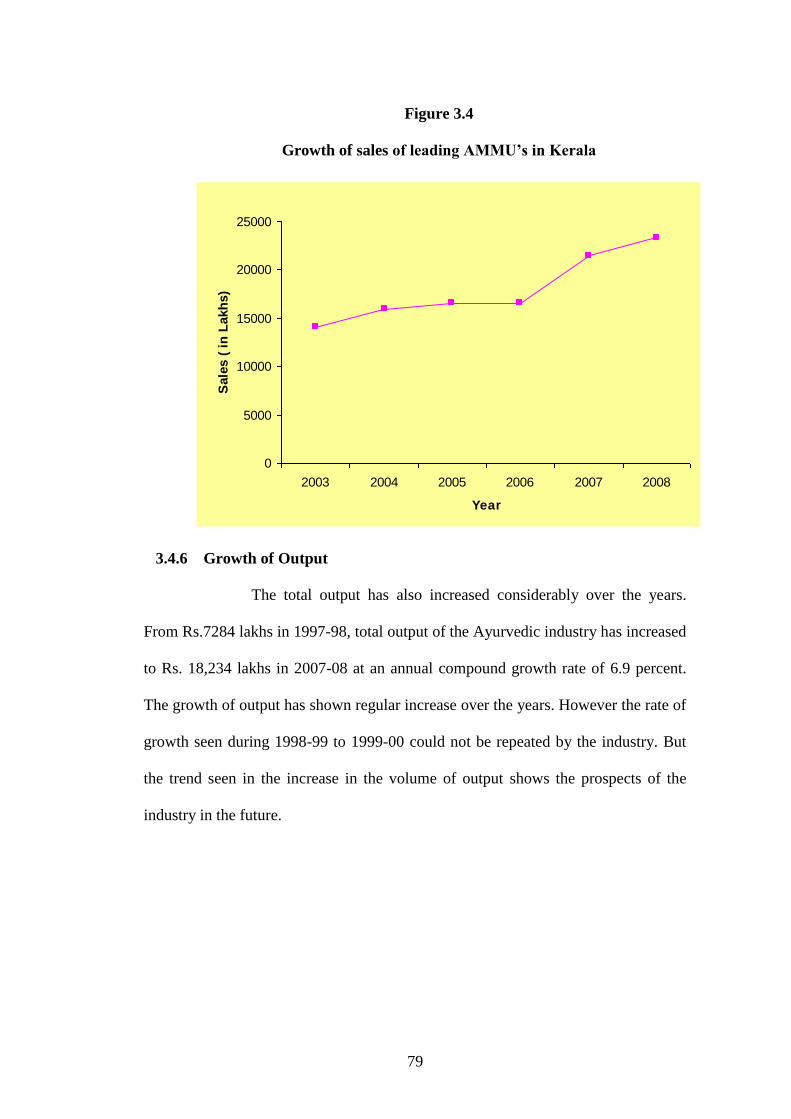

3.4.5 Sales and Export

Another very strong indicator of the growth of the industry is the

figures on sales, both domestic and exports. When compared to domestic sales the

volume of exports are considerably low. Most of the leading firms have no exports

where as firms like Nagarjuna has established plants for exports alone. The

continuous figures available for six leading firms show that the volume of sales is

showing systematic increase over the years. From Rs.14046 lakhs in 2003-04 the

sales of the leading firms increased to Rs 23,354 lakhs in 2007-08. When we add the

sales figures of the other firms the aggregate sales figures will be much higher. The

compound annual growth rate in sales was found to be 15.9.

79

Figure 3.4

Growth of sales of leading AMMU’s in Kerala

0

5000

10000

15000

20000

25000

2003 2004 2005 2006 2007 2008

Year

Sale

s (

in

Lakh

s)

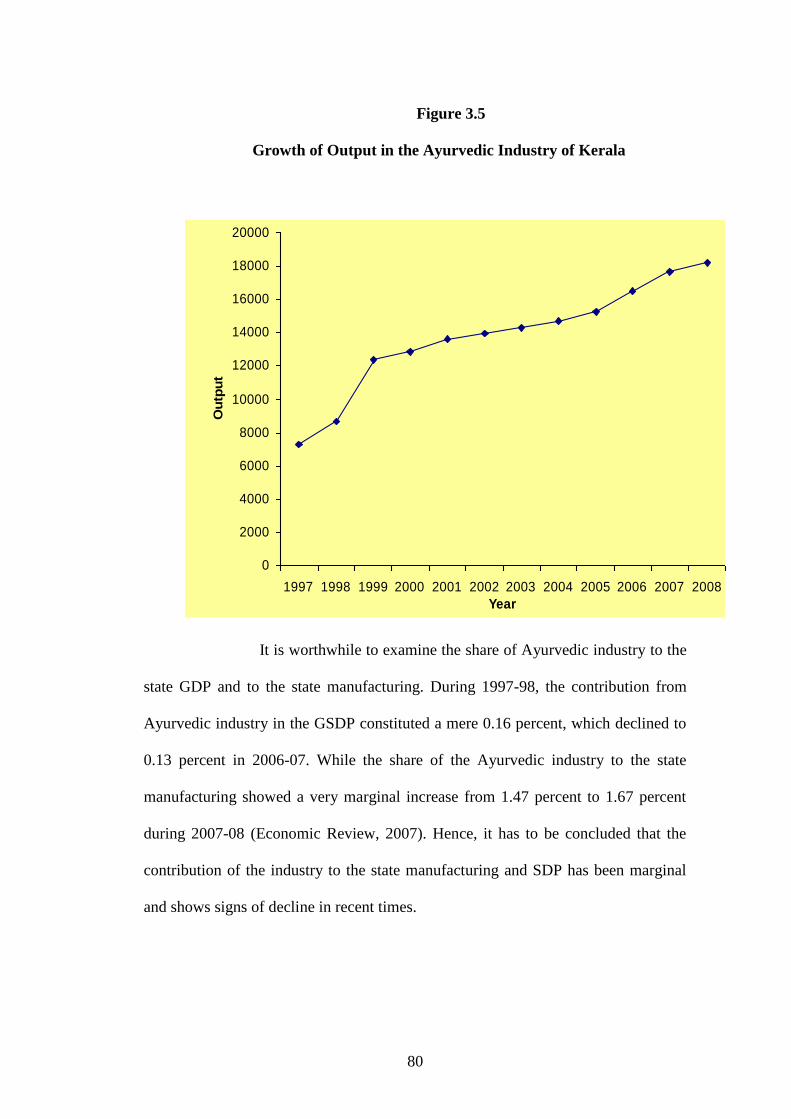

3.4.6 Growth of Output

The total output has also increased considerably over the years.

From Rs.7284 lakhs in 1997-98, total output of the Ayurvedic industry has increased

to Rs. 18,234 lakhs in 2007-08 at an annual compound growth rate of 6.9 percent.

The growth of output has shown regular increase over the years. However the rate of

growth seen during 1998-99 to 1999-00 could not be repeated by the industry. But

the trend seen in the increase in the volume of output shows the prospects of the

industry in the future.

80

Figure 3.5

Growth of Output in the Ayurvedic Industry of Kerala

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Year

Ou

tpu

t

It is worthwhile to examine the share of Ayurvedic industry to the

state GDP and to the state manufacturing. During 1997-98, the contribution from

Ayurvedic industry in the GSDP constituted a mere 0.16 percent, which declined to

0.13 percent in 2006-07. While the share of the Ayurvedic industry to the state

manufacturing showed a very marginal increase from 1.47 percent to 1.67 percent

during 2007-08 (Economic Review, 2007). Hence, it has to be concluded that the

contribution of the industry to the state manufacturing and SDP has been marginal

and shows signs of decline in recent times.

81

The foregoing analysis depicted clearly the evolution and transition

of Ayurvedic industry in the state. From a mere clinical production system the

industry has been transformed into contemporary lines using modern means of

production and novel techniques of marketing. The Ayurvedic industry began as a

petty household production unit; later with the help of mechanisation moved towards

bulk production from there it matured into large scale manufacturing sector. At the

same time dichotomy exists with regards to small manufacturers who still adhere to

the old methods of production. One factor contributing to the growth of the industry

has been the provision of a sound infrastructure facility and that has also been dealt

with in this chapter.

End Notes

1. Petty production was the beginning of the process of industrialisation of Ayurvedic

manufacturing. Here Production was a household activity where all the members of the

family played a part in the production procedure. Apart from them there was some hired

labour who were not paid. Obviously the volume of production was less.

2. Classical formulations are based on Ayurvedic samhitas such as Sahasrayogam and

Astangahrdya which include traditional medicinal formulations such as arishtams, asavams,

ghruthams, lehyams, thailams, and choornams.

3 Personal care products are mostly herbal cosmetic products which are of high demand.

They use the classical formula and innovate it in the user friendly form

4. Ayurdhara was established to save the primary gatherers mostly tribals from the clutches

of exploitation by the private traders. Accordingly tribals sell the medicinal plants collected

from forests directly to the Ayurdhra and the profits earned by the firm is distributed back to

the tribals itself. Thus it is a mechanism to improve the capabilities of the tribals.

5. All medicines produced by the firms have to get prior manufacturing license from the

Drug Controllers Office. The firms will have to inform the composition of medicinal plants

and the reference text on the basis of which the medicines are produced. The license is

issued after the inspection of the composition. The Drug Control Act, 1940 has listed 54

texts which can be used as the reference text for formulation.

6 Ashtavaidya families are Ayurvedic physicians well-versed with knowledge on eight

branches of Ayurveda. The present generation members are well established in the field.

Vaidyaratnam Oushadasala which belongs to Ashtavaidya family is classified as large scale

manufacturer; where as E.T Vaidyaratnam Moos Vaidyasala is a reputed medium sized unit

from the Ashtavaidya family. Both of them come from the Thrishur region.

7. Karkidakom, name of Malayalam month that normally falls between August and

September. In the agricultural dominated society of past Kerala it is believed to be a slack

82

season. Here farmers take rest, repairs their agricultural tools, prepares the seed for sowing

in the next month Chingam. And for undertaking the hectic work in Chingam they refresh

their body using Ayurvedic treatment. Although the agricultural dominated society has

vanished in Kerala, the social custom is still followed in the State. In Tamil Karkidakom is

known by the name Aadi.

8. Proprietary medicines are medicines of known composition

9. Patented medicines are of unknown composition.

10. Branded products are products that bear the trademark of the company like

Chyavanaprash by Dabur India Limited.