CHAPTER 2 – ASSETS

27

Transcript of CHAPTER 2 – ASSETS

CHAPTER 2 – ASSETS

103

FRS 36 IMPAIRMENT OF ASSETS

Objective The objective of this Standard is to prescribe the procedures that an entity applies to ensure that its assets are carried at no more than their recoverable amount.

An asset is carried at more than its recoverable amount if its carrying amount exceeds the amount to be recovered through use or sale of the asset. If this is the case, the asset is described as impaired and the Standard requires the entity to

recognise an impairment loss. The Standard also specifies when an entity should reverse an impairment loss and prescribes disclosures.

Scope

This Standard shall be applied in accounting for the impairment of all assets, other than:

(a) inventories (see FRS 2 Inventories);

(b) superceded

(c) deferred tax assets (see FRS 12 Income Taxes);

(d) assets arising from employee benefits (see FRS 19 Employee Benefits);

(e) financial assets that are within the scope of FRS 109 Financial Instruments;

(f) investment property that is measured at fair value (see FRS 40 Investment Property);

(g) biological assets related to agricultural activity that are measured at fair

value less costs to sell (see FRS 41 Agriculture);

(h) deferred acquisition costs, and intangible assets, arising from an insurer’s contractual rights under insurance contracts within the scope of FRS 104 Insurance Contracts; and

(i) non-current assets (or disposal groups) classified as held for sale in accordance with FRS 105 Non-current Assets Held for Sale and Discontinued Operations.

CHAPTER 2 – ASSETS

104

1. Individual Asset Impairment An asset is impaired when its carrying amount exceeds its recoverable amount.

Carrying amount is the amount at which an asset is recognised after deducting any accumulated depreciation (amortisation) and accumulated impairment losses thereon

The recoverable amount of an asset or a cash-generating unit is the higher of its fair value less costs to sell and its value in use.

Fair value less costs to sell (also, Net Selling Price (NSP)) is the amount obtainable from the sale of an asset or cash-generating unit in an arm’s length transaction between knowledgeable, willing parties, less the costs of disposal.

Value in use (VIU) is the present value of the future cash flows (PVFCF) expected to be derived from an asset or cash-generating unit.

An entity shall assess at each reporting date whether there is any indication that an asset (including intangible asset with an indefinite useful life and goodwill acquired in a business combination) may be impaired. If any such indication exists, the entity shall estimate the recoverable amount of the asset.

In assessing whether there is any indication that an asset may be impaired, an entity shall consider, as a minimum, the following indications:

External sources of information (a) during the period, an asset’s market value has declined significantly more

than would be expected as a result of the passage of time or normal use. (b) significant changes with an adverse effect on the entity have taken place

during the period, or will take place in the near future, in the technological,

market, economic or legal environment in which the entity operates or in the market to which an asset is dedicated.

(c) market interest rates or other market rates of return on investments have increased during the period, and those increases are likely to affect the discount rate used in calculating an asset’s value in use and decrease the asset’s recoverable amount materially.

(d) the carrying amount of the net assets of the entity is more than its market

capitalisation.

CHAPTER 2 – ASSETS

105

Internal sources of information

(e) evidence is available of obsolescence or physical damage of an asset. (f) significant changes with an adverse effect on the entity have taken place

during the period, or are expected to take place in the near future, in the extent to which, or manner in which, an asset is used or is expected to be used. These changes include the asset becoming idle, plans to discontinue

or restructure the operation to which an asset belongs, plans to dispose of an asset before the previously expected date, and reassessing the useful life of an asset as finite rather than indefinite.∗

(g) evidence is available from internal reporting that indicates that the economic

performance of an asset is, or will be, worse than expected.

Frequency of Impairment Testing FRS 36 required the recoverable amount of an asset to be measured whenever there is an indication that the asset may be impaired. The Standard also requires:

(a) the recoverable amount of an intangible asset with an indefinite useful life to

be measured annually, irrespective of whether there is any indication that it

may be impaired. (b) the recoverable amount of an intangible asset not yet available for use to be

measured annually, irrespective of whether there is any indication that it

may be impaired. (c) goodwill acquired in a business combination to be tested for impairment

annually.

Recognising and Measuring an Impairment Loss An impairment loss shall be recognised immediately in profit or loss, unless the asset is carried at revalued amount in accordance with another Standard (for example, in accordance with the revaluation model in FRS 16 Property, Plant and

Equipment). Any impairment loss of a revalued asset shall be treated as a revaluation decrease in accordance with that other Standard. An impairment loss on a non-revalued asset is recognised in profit or loss.

However, an impairment loss on a revalued asset is recognised directly against any revaluation surplus for the asset to the extent that the impairment loss does not exceed the amount in the revaluation surplus for that same asset.

CHAPTER 2 – ASSETS

106

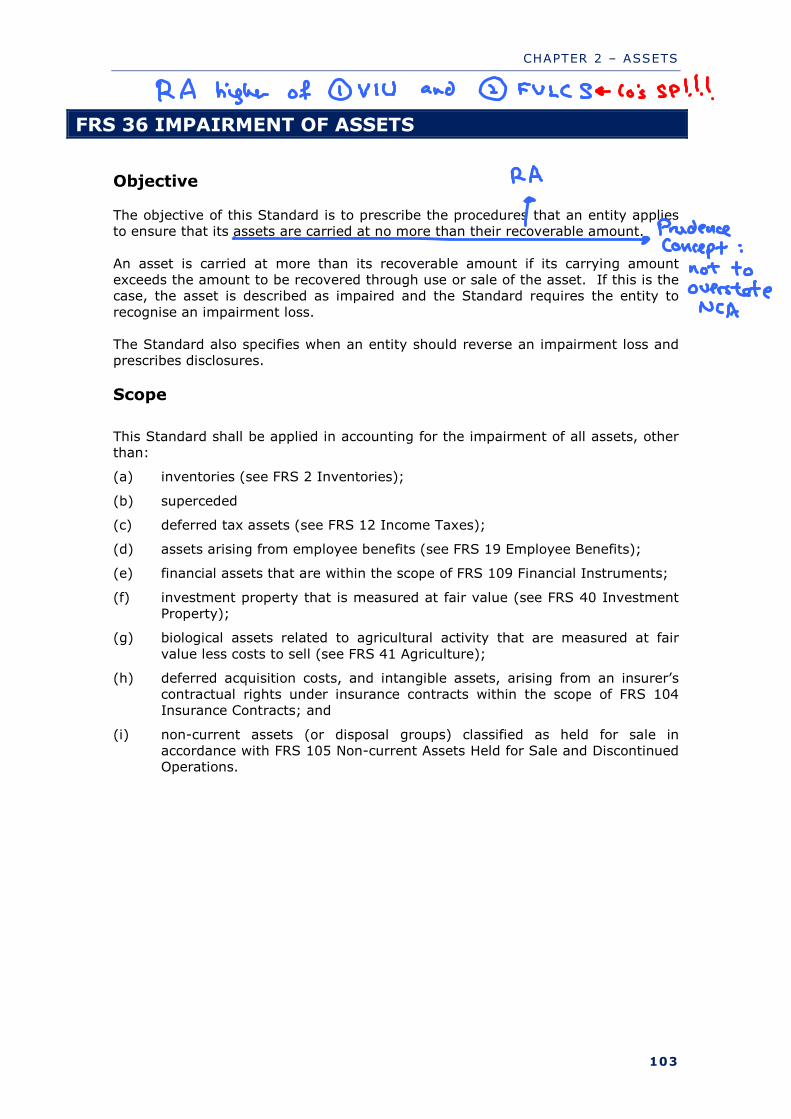

2. Cash-Generating Unit (CGU or Group of Assets) Impairment If there is any indication that an asset may be impaired, recoverable amount shall be estimated for the individual asset. If it is not possible to estimate the

recoverable amount of the individual asset, an entity shall determine the recoverable amount of the cash-generating unit to which the asset belongs (the asset’s cash-generating unit).

Impairment Loss for a Cash-Generating Unit

An impairment loss shall be recognised for a cash-generating unit if, and only if, the recoverable amount of the unit is less than the carrying amount. The impairment loss shall be allocated to reduce the carrying amount of the assets of the unit in the following order:

(a) first, to reduce the carrying amount of the specifically impaired asset;

(b) next, reduce any goodwill allocated to the cash-generating unit; and

(c) then, to the other non-current assets of the unit pro rata on the basis of the

carrying amount of each asset in the unit. In allocating an impairment loss, an entity shall not reduce the carrying amount of an asset below the highest of:

(a) its fair value less costs to sell (if determinable);

(b) its value in use (if determinable); and

(c) zero.

The amount of the impairment loss that would otherwise have been allocated to the asset shall be allocated pro rata to the other assets of the unit.

CHAPTER 2 – ASSETS

107

3. Reversing an Impairment Loss for an Individual Asset The increased carrying amount of an asset other than goodwill attributable to a reversal of an impairment loss shall not exceed the carrying amount that would

have been determined (net of amortisation or depreciation) had no impairment loss been recognised for the asset in prior years.

A reversal of an impairment loss for an asset other than goodwill shall be recognised immediately in profit or loss, unless the asset is carried at revalued amount in accordance with another Standard (for example, the revaluation model in FRS 16 Property, Plant and Equipment). Any reversal of an impairment loss of a

revalued asset shall be treated as a revaluation increase in accordance with that other Standard. After a reversal of an impairment loss is recognised, the depreciation (amortisation)

charge for the asset shall be adjusted in future periods to allocate the asset’s revised carrying amount, less its residual value (if any), on a systematic basis over its remaining useful life.

4. Reversing an Impairment Loss for a Cash-Generating Unit

A reversal of an impairment loss for a cash-generating unit shall be allocated to the assets of the unit, except for goodwill, pro rata with the carrying amounts of those assets. These increases in carrying amounts shall be treated as reversals of

impairment losses for individual assets. In allocating a reversal of an impairment loss for a cash-generating unit, the carrying amount of an asset shall not be increased above the lower of:

(a) its recoverable amount (if determinable); and

(b) the carrying amount that would have been determined (net of amortisation or depreciation) had no impairment loss been recognised for the asset in prior periods.

The amount of the reversal of the impairment loss that would otherwise have been allocated to the asset shall be allocated pro rata to the other assets of the unit,

except for goodwill.

5. Reversing an Impairment Loss for Goodwill & Unwinding An impairment loss recognised for goodwill or the unwinding of discount from the same cash flows shall not be reversed in a subsequent period.

CHAPTER 2 – ASSETS

108

6. Recoverable amount disclosures When FRS 113 Fair Value Measurement was issued, FRS 36 was amended to require the disclosure of information about the recoverable amount of impaired

assets if that amount is based on fair value less costs of disposal. An entity shall disclose the following for an individual asset (including goodwill) or a

cash-generating unit, for which an impairment loss has been recognised or reversed during the period: 1. the recoverable amount of the asset (cash-generating unit) and whether the

recoverable amount of the asset (cash-generating unit) is its fair value less

costs of disposal or its value in use.

2. if the recoverable amount is fair value less costs of disposal, the entity shall

disclose the following information:

(i) the level of the fair value hierarchy (see FRS 113) within which the fair value measurement of the asset (cash-generating unit) is categorised in its entirety (without taking into account whether the ‘costs of disposal’ are observable);

(ii) for fair value measurements categorised within Level 2 and Level 3 of the

fair value hierarchy, a description of the valuation technique(s) used to

measure fair value less costs of disposal. If there has been a change in valuation technique, the entity shall disclose that change and the reason(s) for making it; and

(iii) for fair value measurements categorised within Level 2 and Level 3 of the fair value hierarchy, each key assumption on which management has based its determination of fair value less costs of disposal. Key assumptions are

those to which the asset’s (cash-generating unit’s) recoverable amount is most sensitive. The entity shall also disclose the discount rate(s) used in the current measurement and previous measurement if fair value less costs of disposal is measured using a present value technique.

Estimates used to measure recoverable amounts of cash-generating units containing goodwill or intangible assets with indefinite useful lives

CHAPTER 2 – ASSETS

109

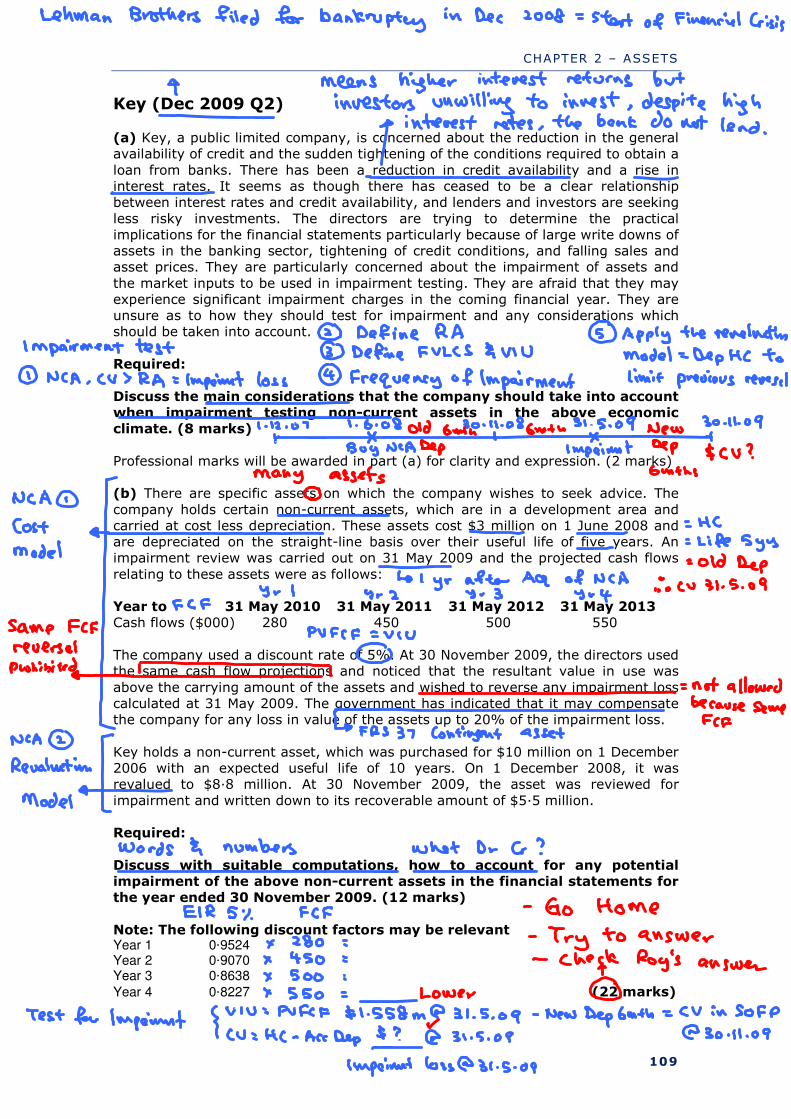

Key (Dec 2009 Q2) (a) Key, a public limited company, is concerned about the reduction in the general availability of credit and the sudden tightening of the conditions required to obtain a

loan from banks. There has been a reduction in credit availability and a rise in interest rates. It seems as though there has ceased to be a clear relationship between interest rates and credit availability, and lenders and investors are seeking

less risky investments. The directors are trying to determine the practical implications for the financial statements particularly because of large write downs of assets in the banking sector, tightening of credit conditions, and falling sales and asset prices. They are particularly concerned about the impairment of assets and

the market inputs to be used in impairment testing. They are afraid that they may experience significant impairment charges in the coming financial year. They are unsure as to how they should test for impairment and any considerations which should be taken into account.

Required:

Discuss the main considerations that the company should take into account when impairment testing non-current assets in the above economic climate. (8 marks)

Professional marks will be awarded in part (a) for clarity and expression. (2 marks) (b) There are specific assets on which the company wishes to seek advice. The

company holds certain non-current assets, which are in a development area and carried at cost less depreciation. These assets cost $3 million on 1 June 2008 and are depreciated on the straight-line basis over their useful life of five years. An impairment review was carried out on 31 May 2009 and the projected cash flows

relating to these assets were as follows: Year to 31 May 2010 31 May 2011 31 May 2012 31 May 2013 Cash flows ($000) 280 450 500 550

The company used a discount rate of 5%. At 30 November 2009, the directors used the same cash flow projections and noticed that the resultant value in use was

above the carrying amount of the assets and wished to reverse any impairment loss calculated at 31 May 2009. The government has indicated that it may compensate the company for any loss in value of the assets up to 20% of the impairment loss.

Key holds a non-current asset, which was purchased for $10 million on 1 December 2006 with an expected useful life of 10 years. On 1 December 2008, it was revalued to $8·8 million. At 30 November 2009, the asset was reviewed for

impairment and written down to its recoverable amount of $5·5 million. Required:

Discuss with suitable computations, how to account for any potential impairment of the above non-current assets in the financial statements for the year ended 30 November 2009. (12 marks)

Note: The following discount factors may be relevant Year 1 0·9524

Year 2 0·9070

Year 3 0·8638

Year 4 0·8227 (22 marks)

CHAPTER 2 – ASSETS

110

Ghorse (Dec 2007 Q3) Ghorse, a public limited company, operates in the fashion sector and had undertaken a group re-organisation during the current financial year to 31 October

2007. As a result the following events occurred: (c) A subsidiary company had purchased computerised equipment for $4 million on

31 October 2006 to improve the manufacturing process. Whilst re-organising the group, Ghorse had discovered that the manufacturer of the computerised equipment was now selling the same system for $2·5 million. The projected cash flows from the equipment are:

Year ended 31 October Cash flows $m 2008 1.3

2009 2.2 2010 2.3

The residual value of the equipment is assumed to be zero. The company uses a discount rate of 10%. The directors think that the fair value less costs to sell of the equipment is $2 million. The directors of Ghorse propose to write down the non-current asset to the new selling price of $2·5 million. The company’s policy is to

depreciate its computer equipment by 25% per annum on the straight line basis. Required:

Discuss the accounting treatment of the above transactions.

(5 marks)

Note: your answer should include appropriate calculations where necessary and a discussion of the accounting principles involved.

CHAPTER 2 – ASSETS

116

FRS 17 LEASES

Scope This Standard shall be applied in accounting for all leases other than: (a) leases to explore for or use minerals, oil, natural gas and similar non-

regenerative resources; and

(b) licensing agreements for such items as motion picture films, video recordings, plays, manuscripts, patents and copyrights.

However, this Standard shall not be applied as the basis of measurement for: (a) property held by lessees that is accounted for as investment property (see

FRS 40 Investment Property);

(b) investment property provided by lessors under operating leases (see FRS 40);

(c) biological assets held by lessees under finance leases (see FRS 41 Agriculture); or

(d) biological assets provided by lessors under operating leases (see FRS 41).

A lease is classified as a finance lease if it transfers substantially all the risks and rewards incidental to ownership. A lease is classified as an operating lease if it

does not transfer substantially all the risks and rewards incidental to ownership. Whether a lease is a finance lease or an operating lease depends on the substance of the transaction rather than the form of the contract. Examples of situations that

individually or in combination would normally lead to a lease being classified as a finance lease are:

(a) the lease transfers ownership of the asset to the lessee by the end of the lease term;

(b) the lessee has the option to purchase the asset at a price that is expected to be sufficiently lower than the fair value at the date the option becomes

exercisable for it to be reasonably certain, at the inception of the lease, that the option will be exercised;

(c) the lease term is for the major part of the economic life of the asset even if title is not transferred;

(d) at the inception of the lease the present value of the minimum lease payments amounts to at least substantially all (> 90%) of the fair value of the leased asset ; and

(e) the leased assets are of such a specialised nature that only the lessee can use them without major modifications.

When a lease includes both land and buildings elements, an entity assesses the

classification of each element as a finance or an operating lease separately as above. In determining whether the land element is an operating or a finance lease, an important consideration is that land normally has an indefinite

economic life.

CHAPTER 2 – ASSETS

117

Leases in the Financial Statements of Lessee 1. Finance Lease in Lessee

A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an asset. Title may or may not eventually be transferred.

Initial Recognition At the commencement of the lease term, lessees shall recognise finance leases as assets and liabilities in their statement of financial positions at amounts equal to

the fair value of the leased property or, if lower, the present value of the minimum lease payments (PVMLP), each determined at the inception of the lease. The discount rate to be used in calculating the present value of the minimum lease

payments is the interest rate implicit in the lease, if this is practicable to determine; if not, the lessee’s incremental borrowing rate shall be used. Any initial direct costs

of the lessee are added to the amount recognised as an asset. Minimum lease payments shall be apportioned between the finance charge and the reduction of the outstanding liability.

A finance lease gives rise to depreciation expense for depreciable assets as well as finance expense for each accounting period. The depreciation shall be calculated in

accordance with FRS 16 Property, Plant and Equipment and FRS 38 Intangible Assets. If the lessee will DO NOT obtain ownership by the end of the lease term, the asset shall be fully depreciated over the shorter of the lease term and its useful life.

2. Operating Lease in Lessee

An operating lease is a lease other than a finance lease. Lease payments under an operating lease shall be recognised as an expense on a

straight-line basis over the lease term unless another systematic basis is more representative of the time pattern of the user’s benefit.

Finance Lease in Lessee

Operating Lease in Lessee

1. Capitalise PPE at lower of FV and PVMLP

2. Depreciate shorter of useful life and lease term if no ownership. If user obtains ownership, depreciate over the

useful life. 3. Calculate lease interest and split lease obligation into NCL and CL.

Charge as rental expenses

CHAPTER 2 – ASSETS

118

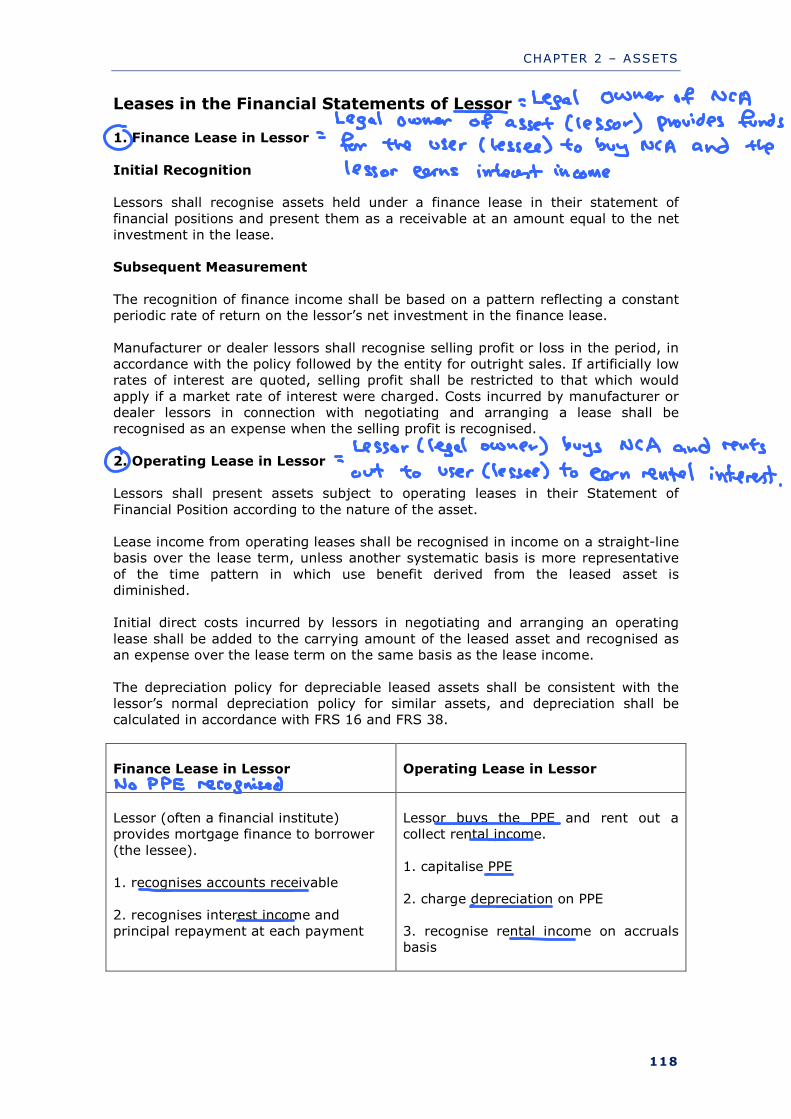

Leases in the Financial Statements of Lessor 1. Finance Lease in Lessor

Initial Recognition Lessors shall recognise assets held under a finance lease in their statement of

financial positions and present them as a receivable at an amount equal to the net investment in the lease. Subsequent Measurement

The recognition of finance income shall be based on a pattern reflecting a constant periodic rate of return on the lessor’s net investment in the finance lease.

Manufacturer or dealer lessors shall recognise selling profit or loss in the period, in accordance with the policy followed by the entity for outright sales. If artificially low rates of interest are quoted, selling profit shall be restricted to that which would

apply if a market rate of interest were charged. Costs incurred by manufacturer or dealer lessors in connection with negotiating and arranging a lease shall be recognised as an expense when the selling profit is recognised.

2. Operating Lease in Lessor Lessors shall present assets subject to operating leases in their Statement of

Financial Position according to the nature of the asset. Lease income from operating leases shall be recognised in income on a straight-line basis over the lease term, unless another systematic basis is more representative

of the time pattern in which use benefit derived from the leased asset is diminished. Initial direct costs incurred by lessors in negotiating and arranging an operating

lease shall be added to the carrying amount of the leased asset and recognised as an expense over the lease term on the same basis as the lease income.

The depreciation policy for depreciable leased assets shall be consistent with the lessor’s normal depreciation policy for similar assets, and depreciation shall be calculated in accordance with FRS 16 and FRS 38.

Finance Lease in Lessor

Operating Lease in Lessor

Lessor (often a financial institute) provides mortgage finance to borrower

(the lessee). 1. recognises accounts receivable

2. recognises interest income and principal repayment at each payment

Lessor buys the PPE and rent out a collect rental income.

1. capitalise PPE

2. charge depreciation on PPE 3. recognise rental income on accruals basis

CHAPTER 2 – ASSETS

119

Sale and Leaseback Transactions A sale and leaseback transaction involves the sale of an asset and the leasing back of the same asset. The lease payment and the sale price are usually interdependent

because they are negotiated as a package. The accounting treatment of a sale and leaseback transaction depends upon the type of lease involved.

1. If a sale and leaseback transaction results in a finance lease, any excess of sales proceeds over the carrying amount shall not be immediately recognised as income by a seller-lessee. Instead, it shall be deferred and amortised over the lease term.

SP > CV, gain on disposal deferred as NCL and amortised to SOPL If the leaseback is a finance lease, the transaction is a means whereby the lessor

provides finance to the lessee, with the asset as security. For this reason it is not appropriate to regard an excess of sales proceeds over the carrying amount as income. Such excess is deferred and amortised over the lease term.

2. If a sale and leaseback transaction results in an operating lease, and it is clear that the transaction is established at fair value, any profit or loss shall be recognised immediately. If the sale price is below fair value, any profit or loss shall

be recognised immediately except that, if the loss is compensated for by future lease payments at below market price, it shall be deferred and amortised in proportion to the lease payments over the period for which the asset is expected to

be used. If the sale price is above fair value, the excess over fair value shall be deferred and amortised over the period for which the asset is expected to be used. If the leaseback is an operating lease, and the lease payments and the sale price

are at fair value, there has in effect been a normal sale transaction and any profit or loss is recognised immediately. For operating leases, if the fair value at the time of a sale and leaseback transaction

is less than the carrying amount of the asset, a loss equal to the amount of the difference between the carrying amount and fair value shall be recognised immediately.

For finance leases, no such adjustment is necessary unless there has been an impairment in value, in which case the carrying amount is reduced to recoverable amount in accordance with FRS 36.

Summary for Sale and Leaseback into Operating Lease

1. SP = FV, gain or loss to SOPL immediately 2. SP < FV, gain or loss to SOPL immediately

But if the loss is compensated for by future reduced lease payments at below market price, then it shall be deferred and amortised in proportion to the lease payments over the period for which the asset is expected to be used.

3. SP > FV, excess of SP deferred and amortised over the period for which the asset is expected to be used

4. FV < CV, difference between the CV and FV (i.e. a loss) shall be recognised immediately. This adjusts the CV to FV which is similar to an impairment loss.

CHAPTER 2 – ASSETS

120

Havanna (Dec 2013 Q2)

(c) Havanna has decided to sell its main office building to a third party and lease

it back on a 10-year lease. The lease has been classified as an operating lease. The current fair value of the property is $5 million and the carrying value of the asset is $4·2 million. The market for property is very difficult in the jurisdiction and

Havanna therefore requires guidance on the consequences of selling the office building at a range of prices. The following prices have been achieved in the market during the last few months for similar office buildings:

(i) $5 million (ii) $6 million (iii) $4·8 million (iv) $4 million

Havanna would like advice on how to account for the sale and leaseback, with an explanation of the effect which the different selling prices would have on the

financial statements, assuming that the fair value of the property is $5 million.

(8 marks)

Required: Advise Havanna on how the above transactions should be dealt with in its

financial statements with reference to Financial Reporting Standards where appropriate.

CHAPTER 2 – ASSETS

130

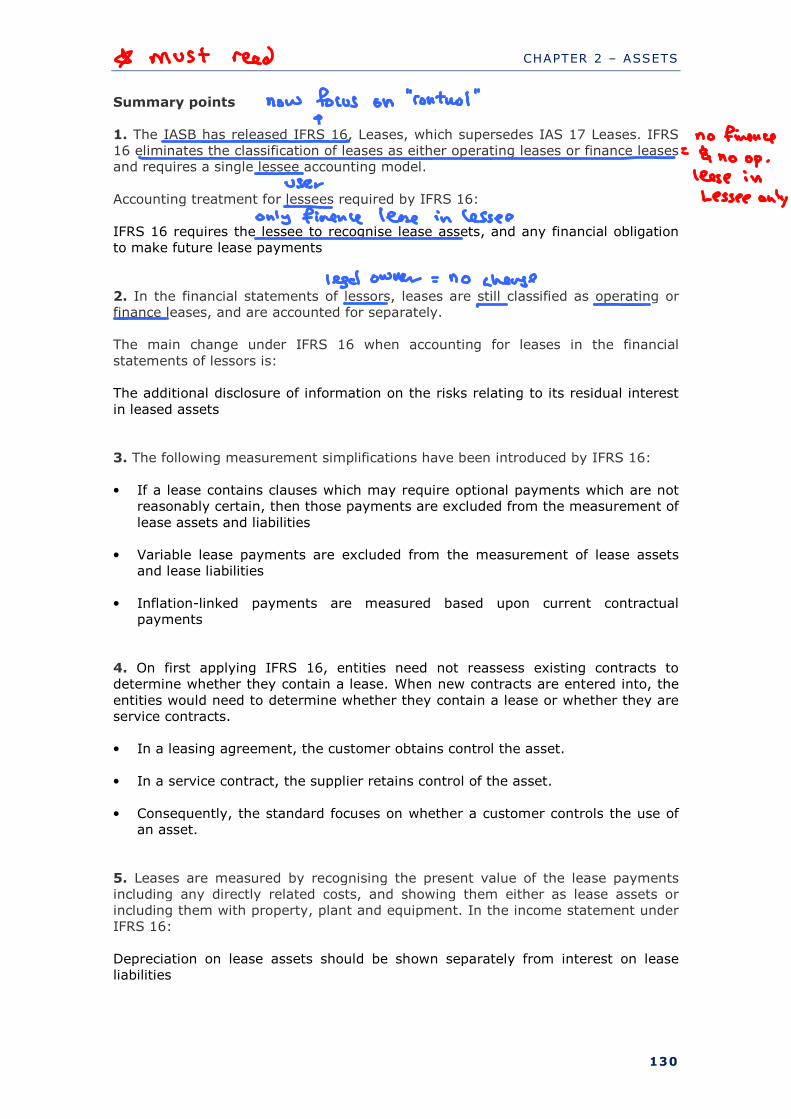

Summary points

1. The IASB has released IFRS 16, Leases, which supersedes IAS 17 Leases. IFRS 16 eliminates the classification of leases as either operating leases or finance leases and requires a single lessee accounting model.

Accounting treatment for lessees required by IFRS 16:

IFRS 16 requires the lessee to recognise lease assets, and any financial obligation to make future lease payments

2. In the financial statements of lessors, leases are still classified as operating or finance leases, and are accounted for separately. The main change under IFRS 16 when accounting for leases in the financial

statements of lessors is: The additional disclosure of information on the risks relating to its residual interest

in leased assets 3. The following measurement simplifications have been introduced by IFRS 16:

• If a lease contains clauses which may require optional payments which are not

reasonably certain, then those payments are excluded from the measurement of

lease assets and liabilities

• Variable lease payments are excluded from the measurement of lease assets and lease liabilities

• Inflation-linked payments are measured based upon current contractual

payments

4. On first applying IFRS 16, entities need not reassess existing contracts to determine whether they contain a lease. When new contracts are entered into, the

entities would need to determine whether they contain a lease or whether they are service contracts. • In a leasing agreement, the customer obtains control the asset.

• In a service contract, the supplier retains control of the asset.

• Consequently, the standard focuses on whether a customer controls the use of an asset.

5. Leases are measured by recognising the present value of the lease payments including any directly related costs, and showing them either as lease assets or including them with property, plant and equipment. In the income statement under IFRS 16:

Depreciation on lease assets should be shown separately from interest on lease liabilities

CHAPTER 2 – ASSETS

131

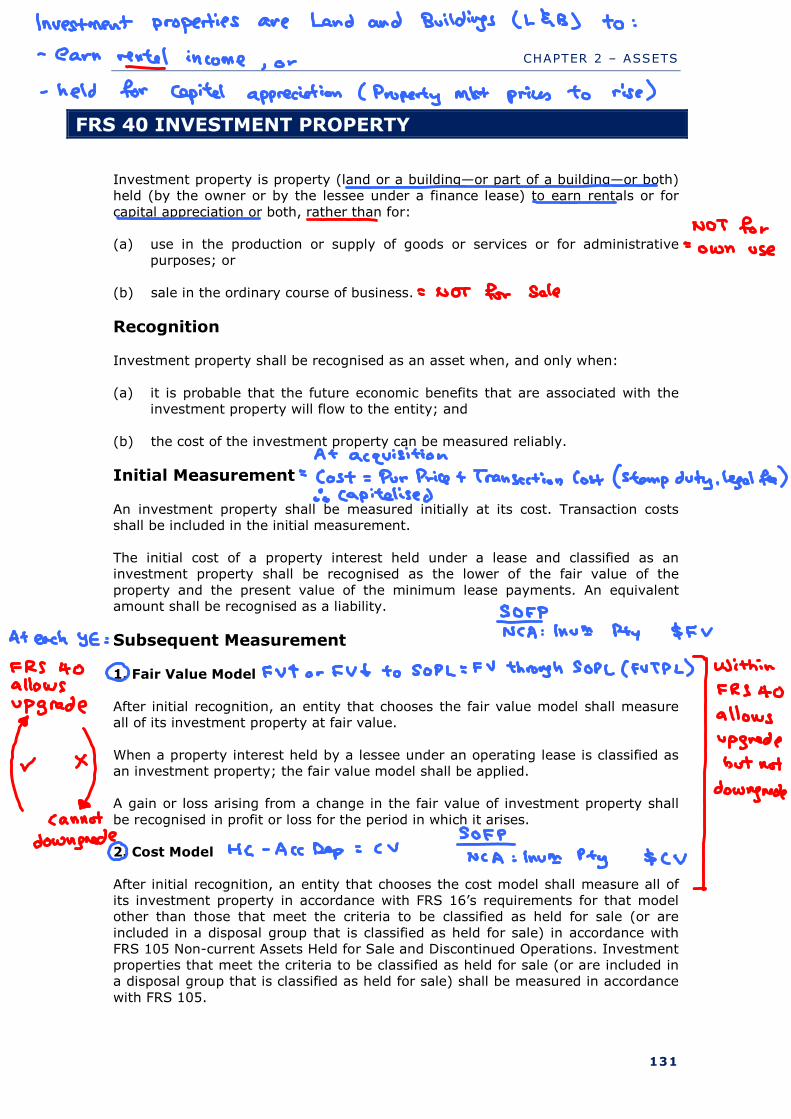

FRS 40 INVESTMENT PROPERTY

Investment property is property (land or a building—or part of a building—or both) held (by the owner or by the lessee under a finance lease) to earn rentals or for

capital appreciation or both, rather than for: (a) use in the production or supply of goods or services or for administrative

purposes; or

(b) sale in the ordinary course of business.

Recognition Investment property shall be recognised as an asset when, and only when:

(a) it is probable that the future economic benefits that are associated with the

investment property will flow to the entity; and

(b) the cost of the investment property can be measured reliably.

Initial Measurement An investment property shall be measured initially at its cost. Transaction costs shall be included in the initial measurement.

The initial cost of a property interest held under a lease and classified as an investment property shall be recognised as the lower of the fair value of the

property and the present value of the minimum lease payments. An equivalent amount shall be recognised as a liability.

Subsequent Measurement 1. Fair Value Model

After initial recognition, an entity that chooses the fair value model shall measure all of its investment property at fair value.

When a property interest held by a lessee under an operating lease is classified as an investment property; the fair value model shall be applied. A gain or loss arising from a change in the fair value of investment property shall

be recognised in profit or loss for the period in which it arises. 2. Cost Model

After initial recognition, an entity that chooses the cost model shall measure all of its investment property in accordance with FRS 16’s requirements for that model other than those that meet the criteria to be classified as held for sale (or are

included in a disposal group that is classified as held for sale) in accordance with FRS 105 Non-current Assets Held for Sale and Discontinued Operations. Investment properties that meet the criteria to be classified as held for sale (or are included in a disposal group that is classified as held for sale) shall be measured in accordance

with FRS 105.

CHAPTER 2 – ASSETS

132

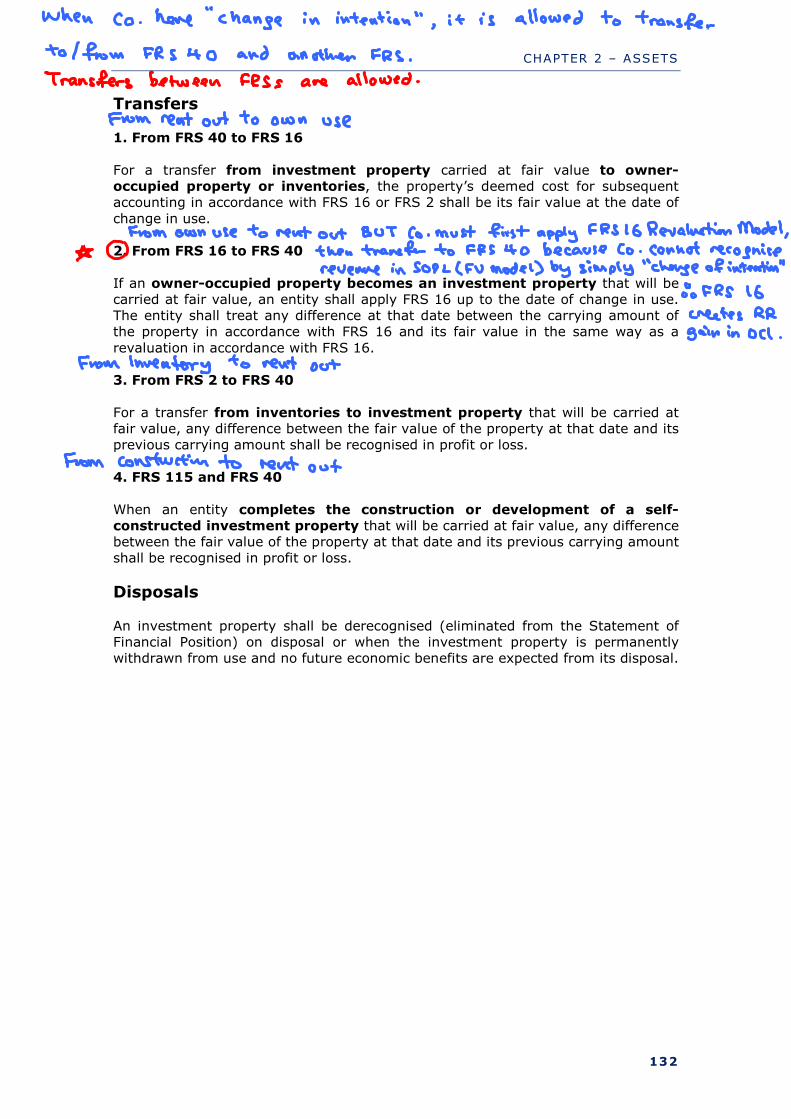

Transfers 1. From FRS 40 to FRS 16

For a transfer from investment property carried at fair value to owner-occupied property or inventories, the property’s deemed cost for subsequent accounting in accordance with FRS 16 or FRS 2 shall be its fair value at the date of

change in use. 2. From FRS 16 to FRS 40

If an owner-occupied property becomes an investment property that will be carried at fair value, an entity shall apply FRS 16 up to the date of change in use. The entity shall treat any difference at that date between the carrying amount of the property in accordance with FRS 16 and its fair value in the same way as a

revaluation in accordance with FRS 16. 3. From FRS 2 to FRS 40

For a transfer from inventories to investment property that will be carried at fair value, any difference between the fair value of the property at that date and its previous carrying amount shall be recognised in profit or loss.

4. FRS 115 and FRS 40

When an entity completes the construction or development of a self-constructed investment property that will be carried at fair value, any difference between the fair value of the property at that date and its previous carrying amount shall be recognised in profit or loss.

Disposals

An investment property shall be derecognised (eliminated from the Statement of Financial Position) on disposal or when the investment property is permanently withdrawn from use and no future economic benefits are expected from its disposal.

CHAPTER 2 – ASSETS

133

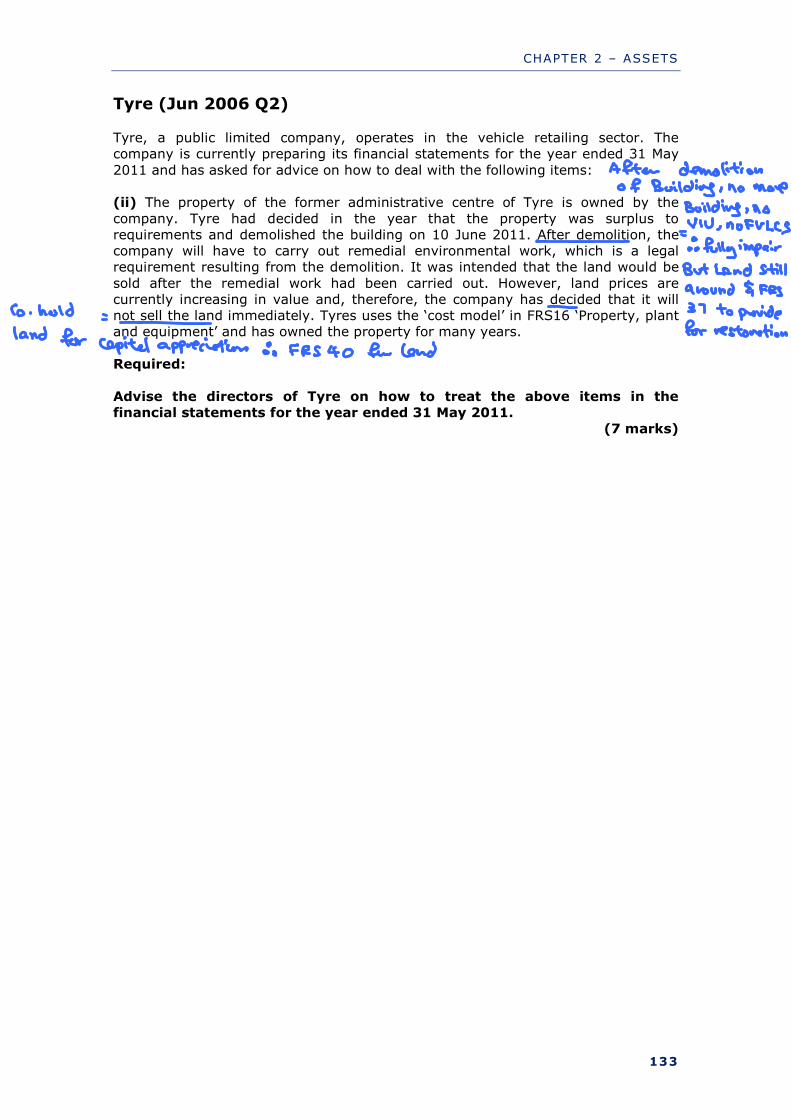

Tyre (Jun 2006 Q2) Tyre, a public limited company, operates in the vehicle retailing sector. The company is currently preparing its financial statements for the year ended 31 May

2011 and has asked for advice on how to deal with the following items: (ii) The property of the former administrative centre of Tyre is owned by the

company. Tyre had decided in the year that the property was surplus to requirements and demolished the building on 10 June 2011. After demolition, the company will have to carry out remedial environmental work, which is a legal requirement resulting from the demolition. It was intended that the land would be

sold after the remedial work had been carried out. However, land prices are currently increasing in value and, therefore, the company has decided that it will not sell the land immediately. Tyres uses the ‘cost model’ in FRS16 ‘Property, plant and equipment’ and has owned the property for many years.

Required:

Advise the directors of Tyre on how to treat the above items in the financial statements for the year ended 31 May 2011.

(7 marks)

CHAPTER 2 – ASSETS

134

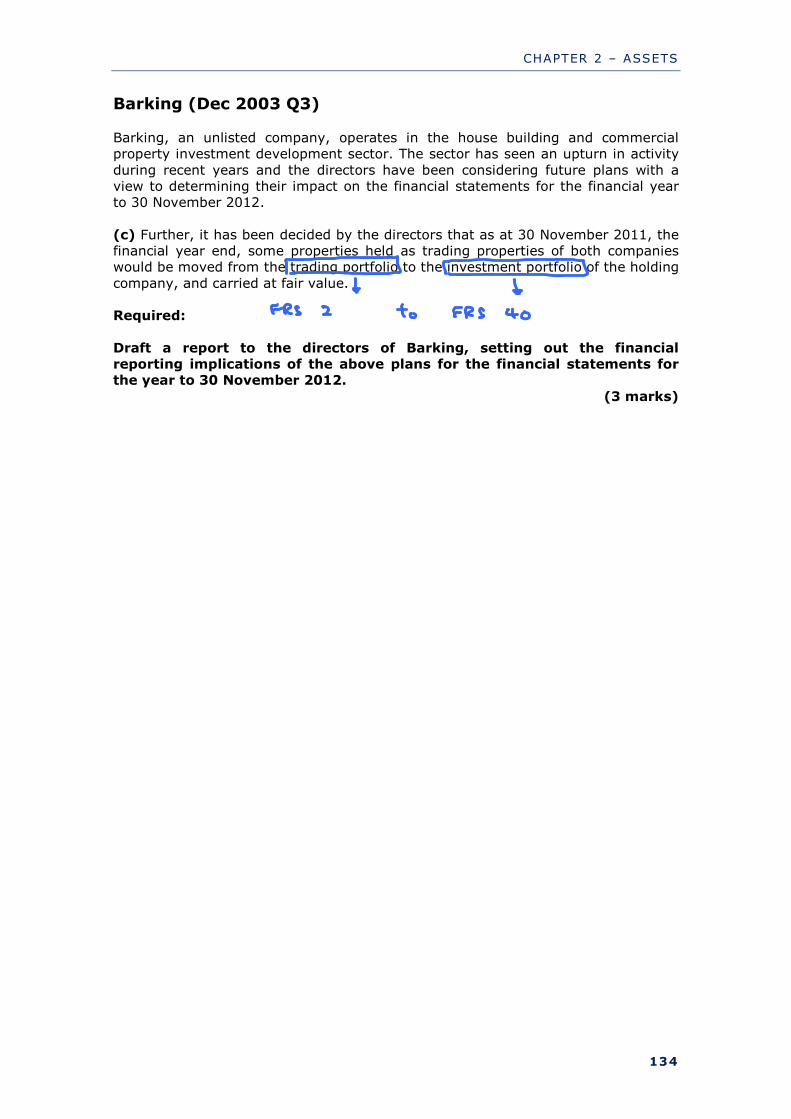

Barking (Dec 2003 Q3) Barking, an unlisted company, operates in the house building and commercial property investment development sector. The sector has seen an upturn in activity

during recent years and the directors have been considering future plans with a view to determining their impact on the financial statements for the financial year to 30 November 2012.

(c) Further, it has been decided by the directors that as at 30 November 2011, the financial year end, some properties held as trading properties of both companies would be moved from the trading portfolio to the investment portfolio of the holding

company, and carried at fair value. Required:

Draft a report to the directors of Barking, setting out the financial reporting implications of the above plans for the financial statements for the year to 30 November 2012.

(3 marks)

CHAPTER 2 – ASSETS

135

FRS 2 INVENTORIES

Inventories should be carried at the lower of cost and net realisable value.

Cost The cost of inventories shall comprise all costs of purchase, costs of conversion and other cost incurred in bringing the inventories to their present location and

condition. Cost of purchase Purchase price, irrecoverable taxes, transport, handling and other costs directly

attributable to the acquisition of finished goods, materials and services. Trade discounts are deducted but cash or settlement discounts are not.

Costs of conversion Costs directly related to the units of production, such as direct labour. exclusions: abnormal costs, storage costs, administration costs and selling expenses.

Net Realisable Value The amount at which the inventories are expected to realise should be based on the most reliable evidence available at the time of the estimate less any costs directly

related to selling the inventories. For consistency purposes, an entity shall apply the FIFO or Weighted Average to all

inventories of the same nature. The standard does not allow LIFO.

CHAPTER 2 – ASSETS

136

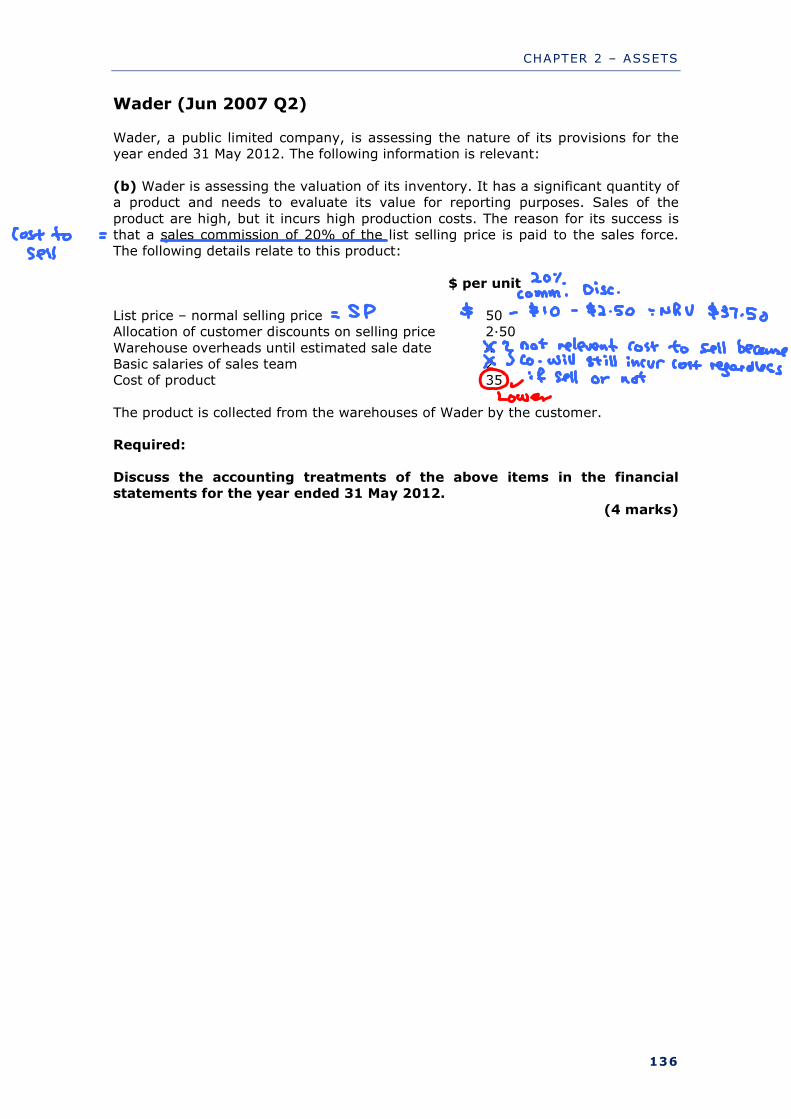

Wader (Jun 2007 Q2) Wader, a public limited company, is assessing the nature of its provisions for the year ended 31 May 2012. The following information is relevant:

(b) Wader is assessing the valuation of its inventory. It has a significant quantity of a product and needs to evaluate its value for reporting purposes. Sales of the

product are high, but it incurs high production costs. The reason for its success is that a sales commission of 20% of the list selling price is paid to the sales force. The following details relate to this product:

$ per unit List price – normal selling price 50 Allocation of customer discounts on selling price 2·50

Warehouse overheads until estimated sale date 4 Basic salaries of sales team 2 Cost of product 35

The product is collected from the warehouses of Wader by the customer. Required:

Discuss the accounting treatments of the above items in the financial statements for the year ended 31 May 2012.

(4 marks)

CHAPTER 2 – ASSETS

137

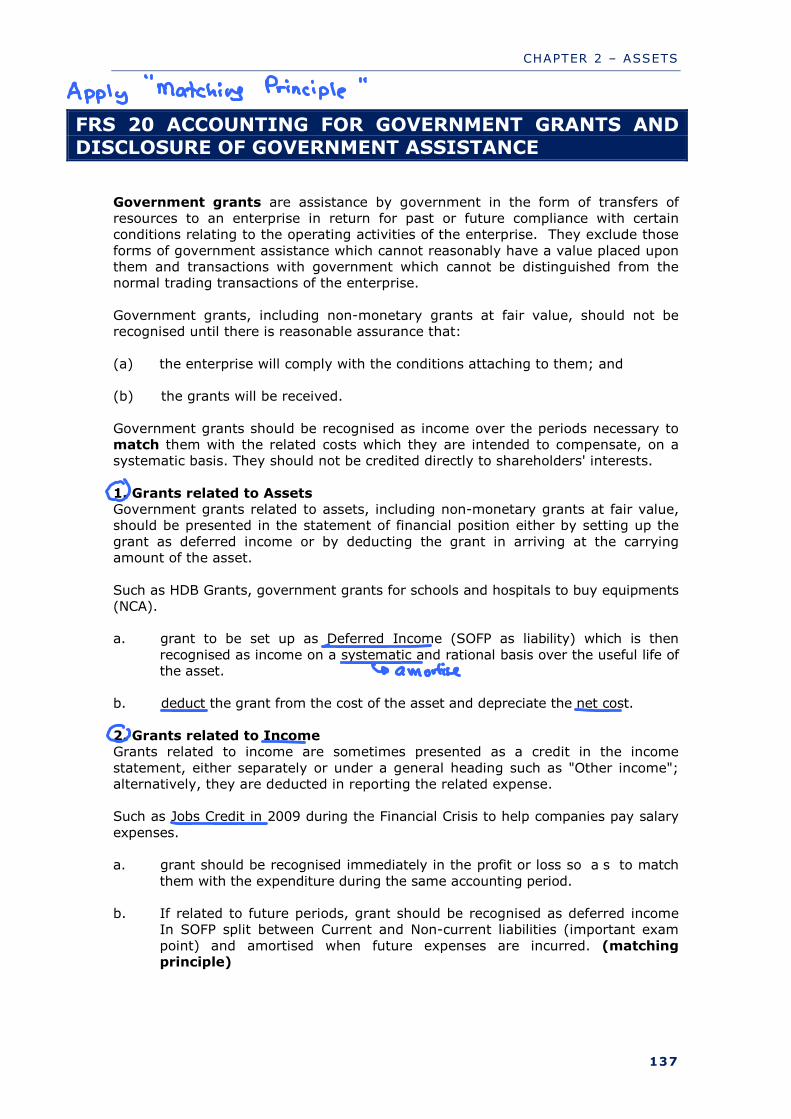

FRS 20 ACCOUNTING FOR GOVERNMENT GRANTS AND

DISCLOSURE OF GOVERNMENT ASSISTANCE

Government grants are assistance by government in the form of transfers of resources to an enterprise in return for past or future compliance with certain conditions relating to the operating activities of the enterprise. They exclude those

forms of government assistance which cannot reasonably have a value placed upon them and transactions with government which cannot be distinguished from the normal trading transactions of the enterprise.

Government grants, including non-monetary grants at fair value, should not be recognised until there is reasonable assurance that:

(a) the enterprise will comply with the conditions attaching to them; and

(b) the grants will be received.

Government grants should be recognised as income over the periods necessary to match them with the related costs which they are intended to compensate, on a systematic basis. They should not be credited directly to shareholders' interests.

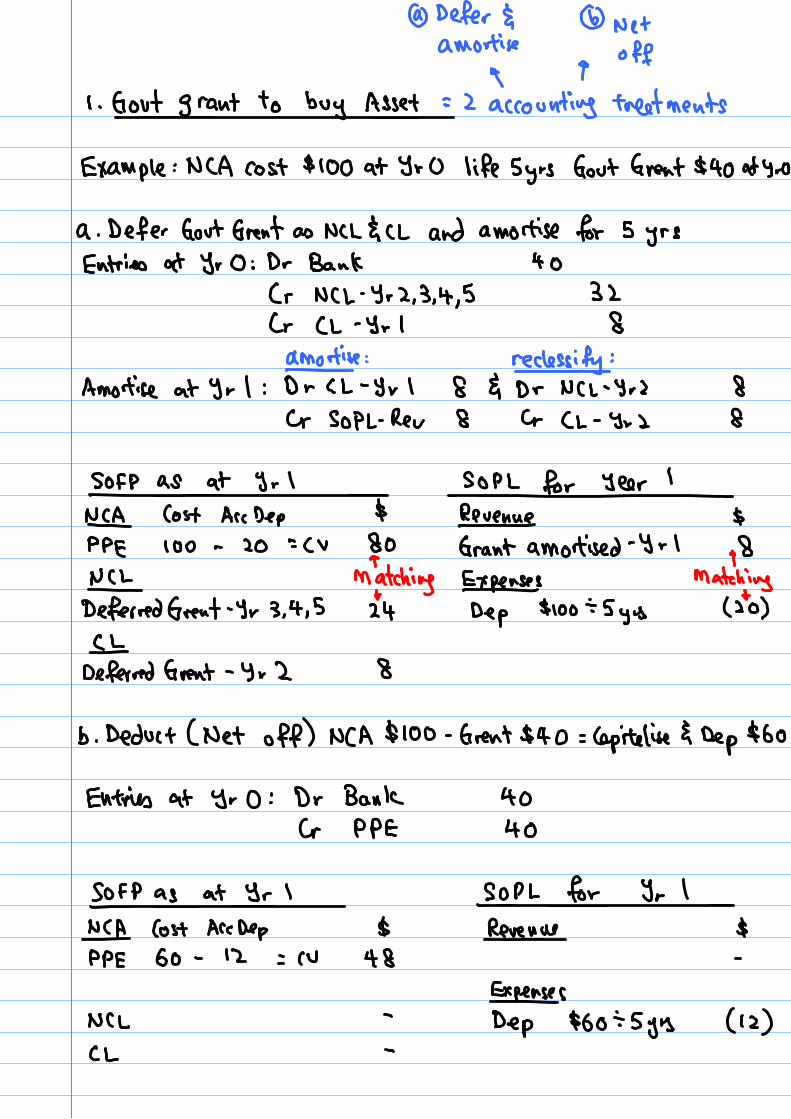

1. Grants related to Assets Government grants related to assets, including non-monetary grants at fair value, should be presented in the statement of financial position either by setting up the

grant as deferred income or by deducting the grant in arriving at the carrying amount of the asset.

Such as HDB Grants, government grants for schools and hospitals to buy equipments (NCA). a. grant to be set up as Deferred Income (SOFP as liability) which is then

recognised as income on a systematic and rational basis over the useful life of the asset.

b. deduct the grant from the cost of the asset and depreciate the net cost.

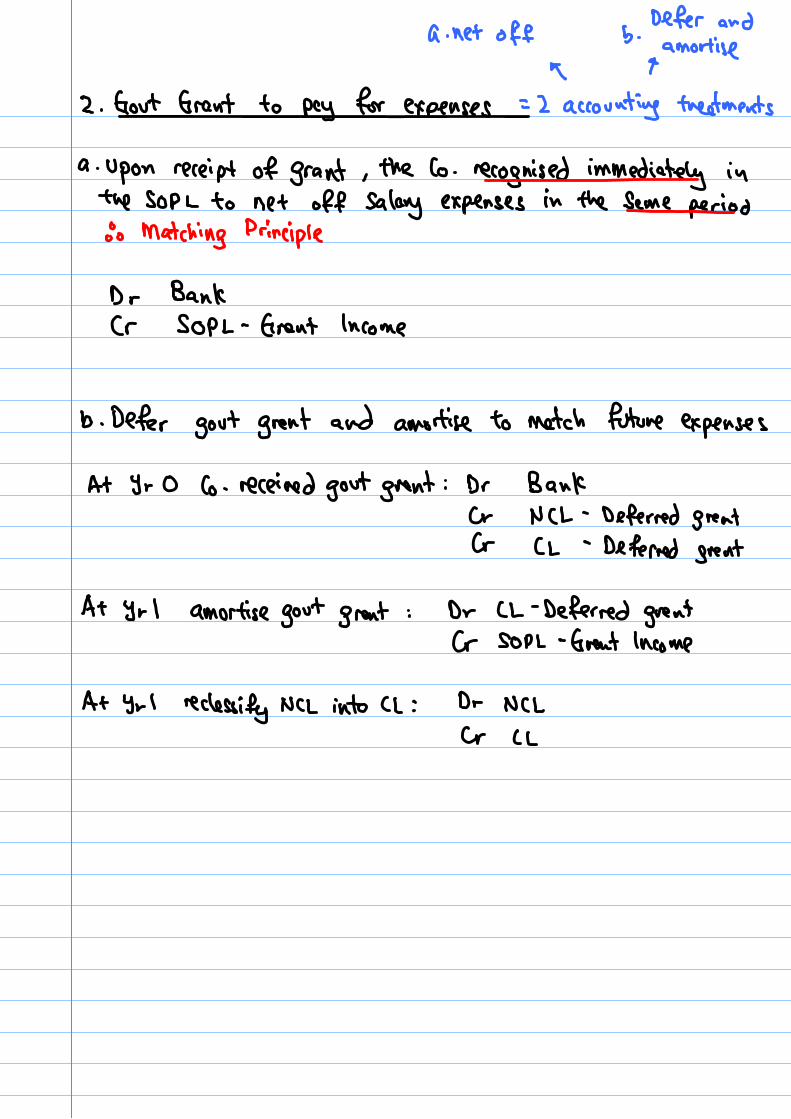

2. Grants related to Income Grants related to income are sometimes presented as a credit in the income

statement, either separately or under a general heading such as "Other income"; alternatively, they are deducted in reporting the related expense. Such as Jobs Credit in 2009 during the Financial Crisis to help companies pay salary

expenses. a. grant should be recognised immediately in the profit or loss so a s to match

them with the expenditure during the same accounting period. b. If related to future periods, grant should be recognised as deferred income

In SOFP split between Current and Non-current liabilities (important exam

point) and amortised when future expenses are incurred. (matching principle)

CHAPTER 2 – ASSETS

138

Repayment of Government Grants

A government grant that becomes repayable should be accounted for as a revision to an accounting estimate – prospective treatment (FRS 8 Accounting Policies, Changes in Accounting Estimates and Errors).

Government assistance is action by government designed to provide an economic benefit specific to an enterprise or range of enterprises qualifying under

certain criteria. Government assistance for the purpose of this Standard does not include benefits provided only indirectly through action affecting general trading conditions, such as the provision of infrastructure in development areas or the imposition of trading constraints on competitors.

CHAPTER 2 – ASSETS

139

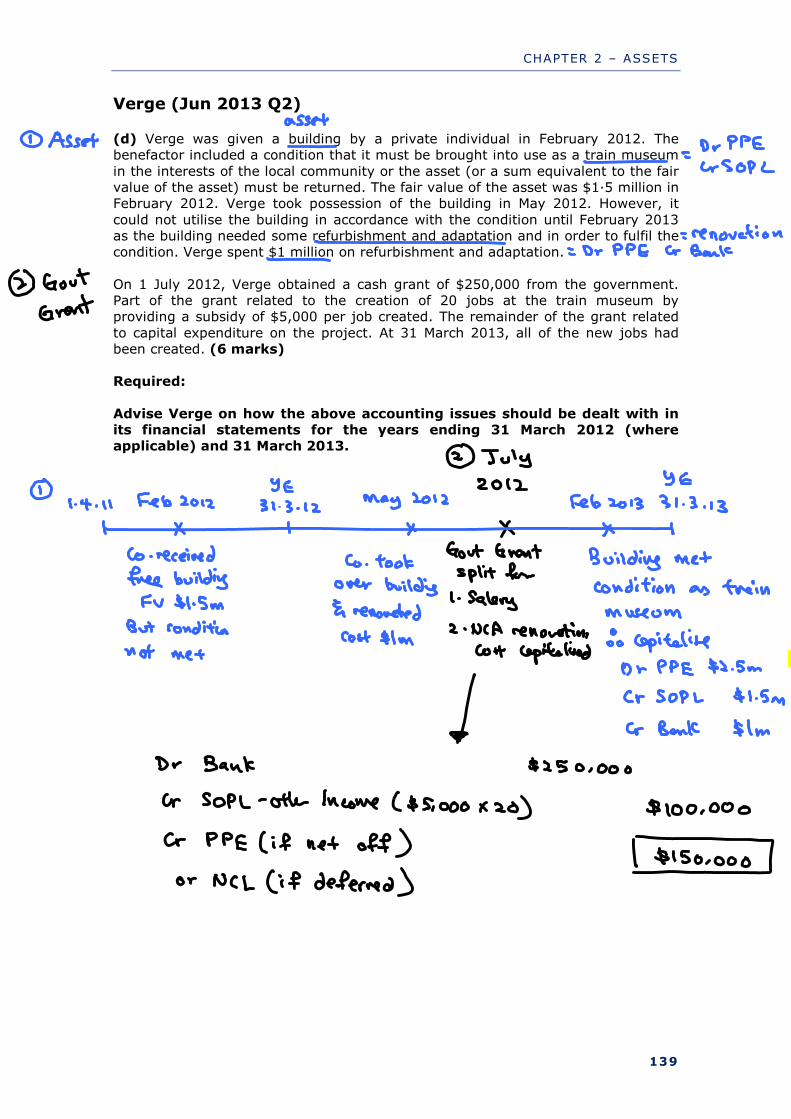

Verge (Jun 2013 Q2)

(d) Verge was given a building by a private individual in February 2012. The benefactor included a condition that it must be brought into use as a train museum

in the interests of the local community or the asset (or a sum equivalent to the fair value of the asset) must be returned. The fair value of the asset was $1·5 million in February 2012. Verge took possession of the building in May 2012. However, it

could not utilise the building in accordance with the condition until February 2013 as the building needed some refurbishment and adaptation and in order to fulfil the condition. Verge spent $1 million on refurbishment and adaptation.

On 1 July 2012, Verge obtained a cash grant of $250,000 from the government. Part of the grant related to the creation of 20 jobs at the train museum by providing a subsidy of $5,000 per job created. The remainder of the grant related

to capital expenditure on the project. At 31 March 2013, all of the new jobs had been created. (6 marks) Required:

Advise Verge on how the above accounting issues should be dealt with in its financial statements for the years ending 31 March 2012 (where applicable) and 31 March 2013.