Hybrid Financing: Preferred Stock, Leasing, Warrants, and Convertibles

Upload

rosalyn-mccormickCategory

view

269download

7

Chapter 19

Convertibles, Warrants,and Derivatives

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

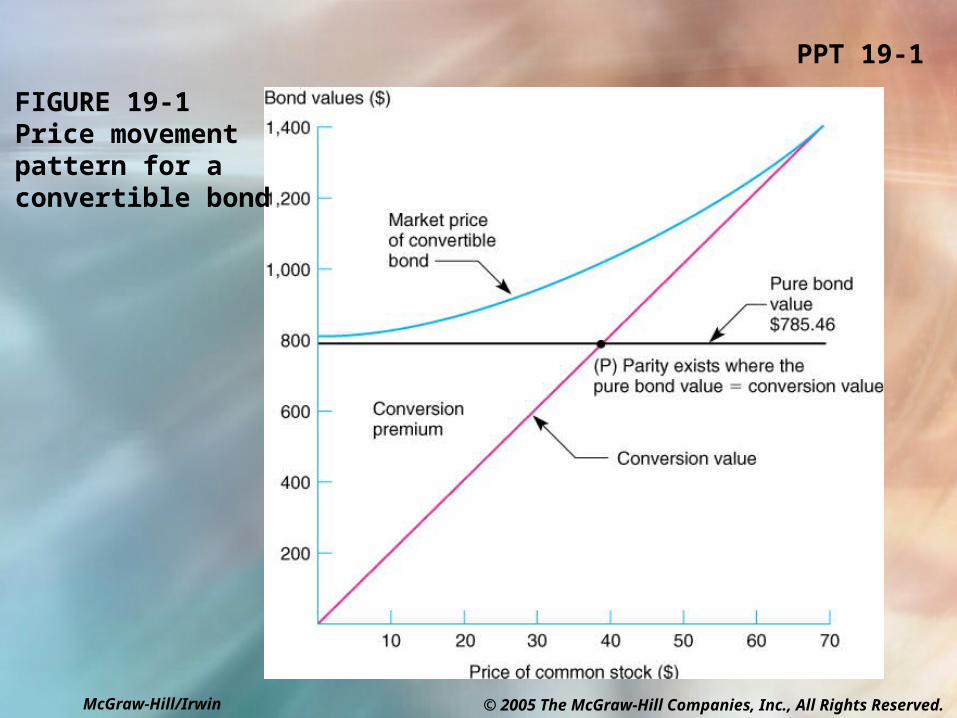

PPT 19-1

FIGURE 19-1Price movementpattern for a convertible bond

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

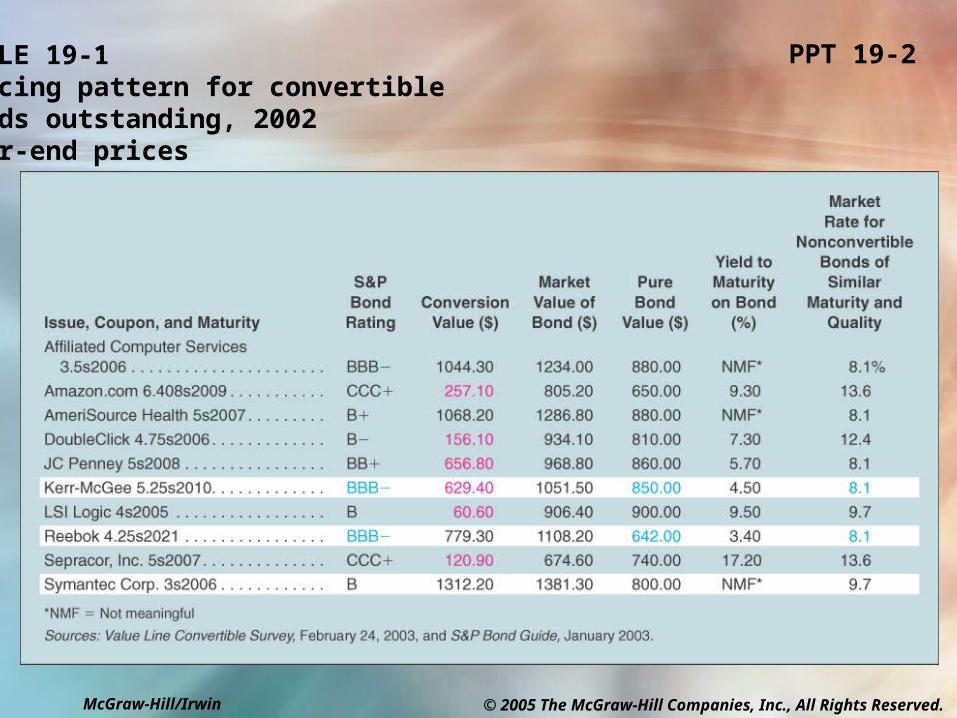

PPT 19-2TABLE 19-1Pricing pattern for convertiblebonds outstanding, 2002year-end prices

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

PPT 19-3

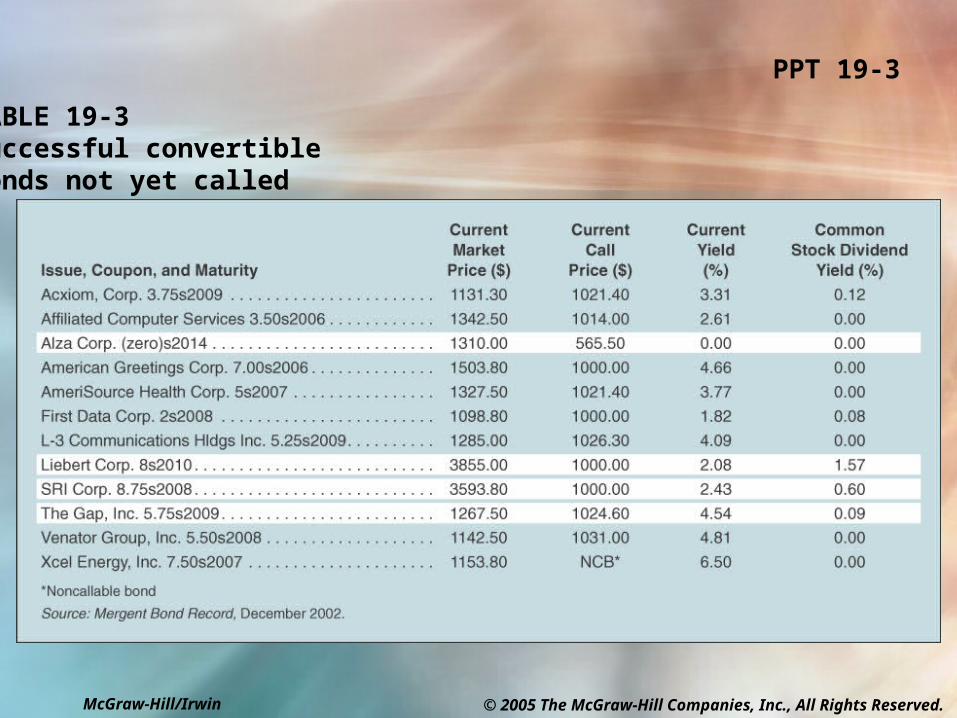

TABLE 19-3Successful convertiblebonds not yet called

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

PPT 19-4

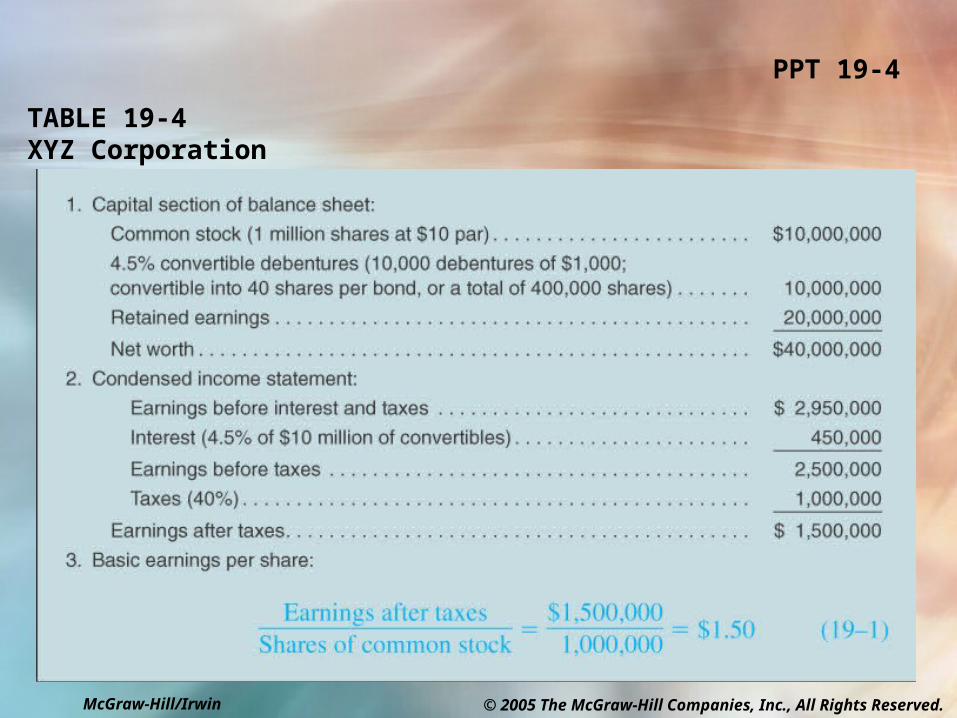

TABLE 19-4XYZ Corporation

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

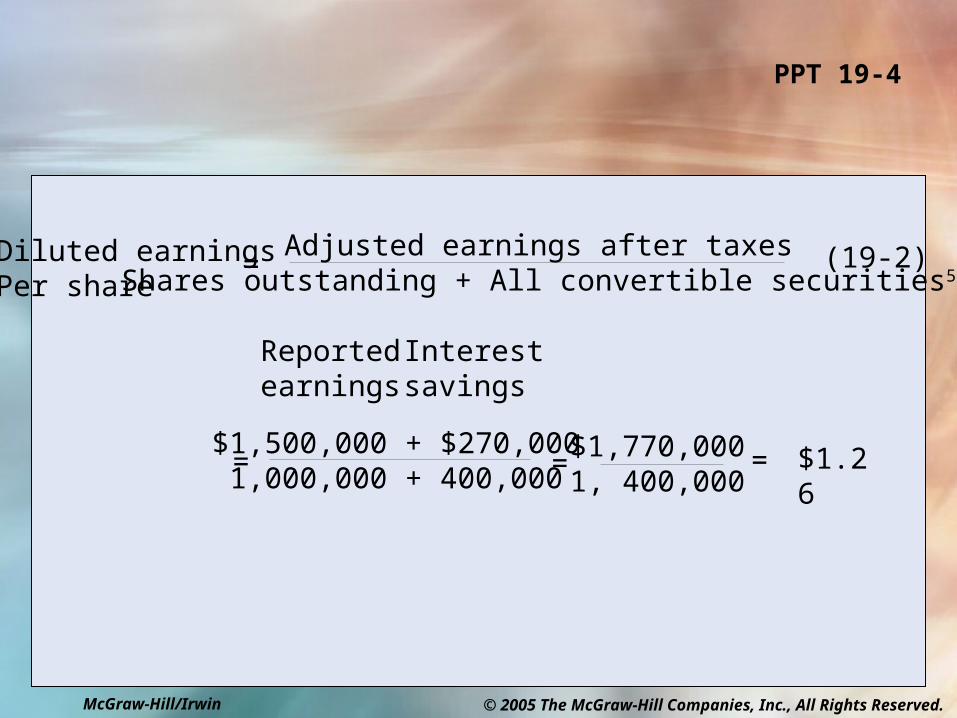

Diluted earningsPer share

Adjusted earnings after taxesShares outstanding + All convertible securities5

(19-2)=

PPT 19-4

Reportedearnings

Interest savings

$1,500,000 + $270,0001,000,000 + 400,000

= = =$1,770,0001, 400,000

$1.26

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

PPT 19-5

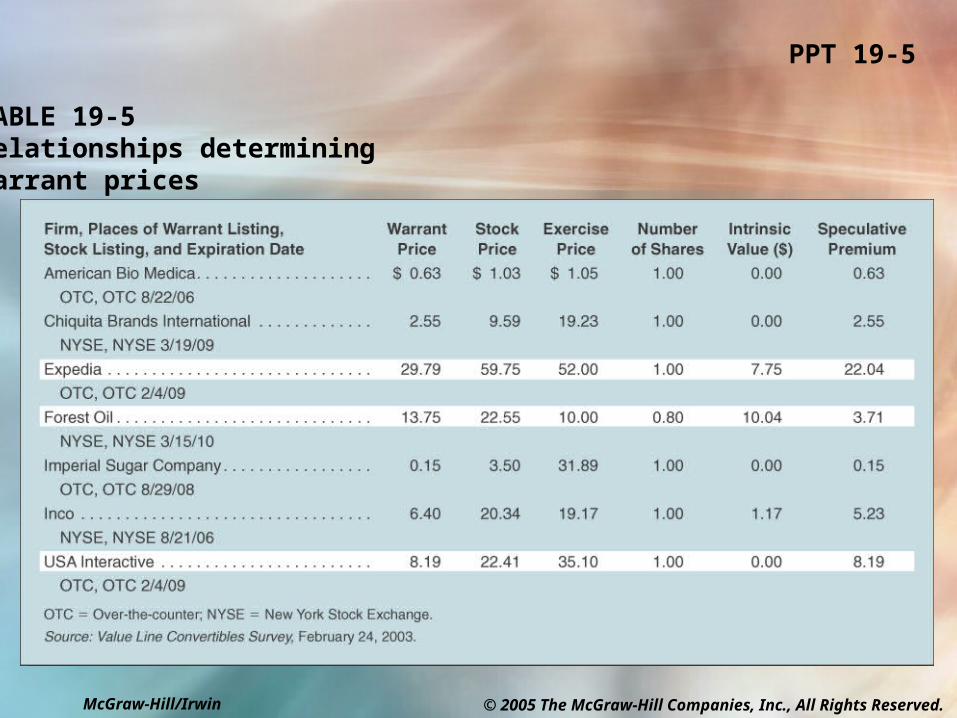

TABLE 19-5Relationships determiningwarrant prices

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

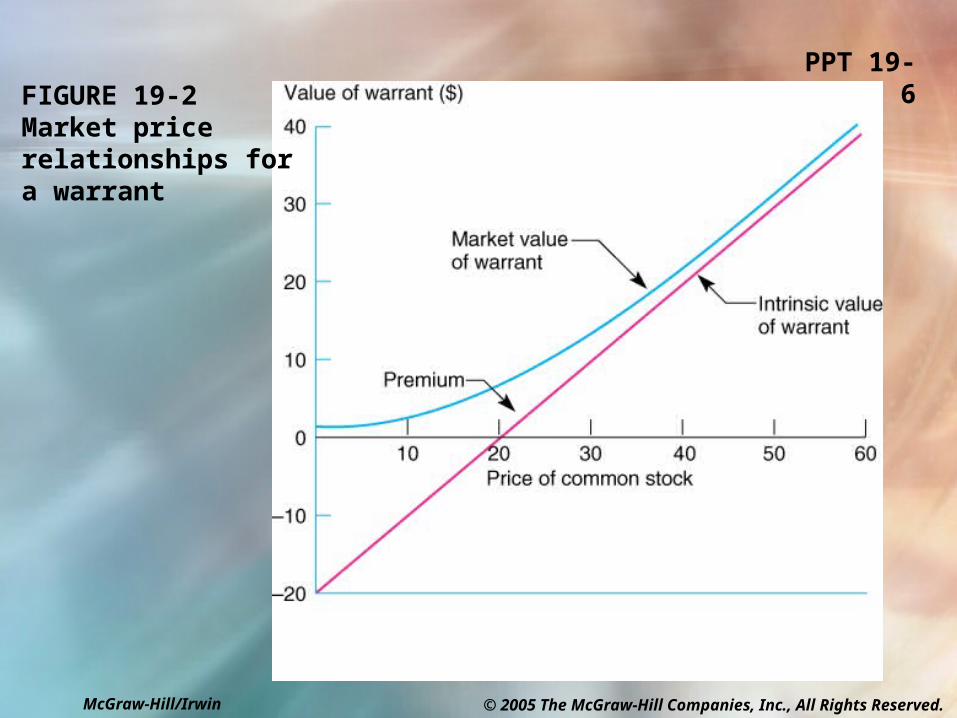

PPT 19-6FIGURE 19-2Market price relationships fora warrant

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

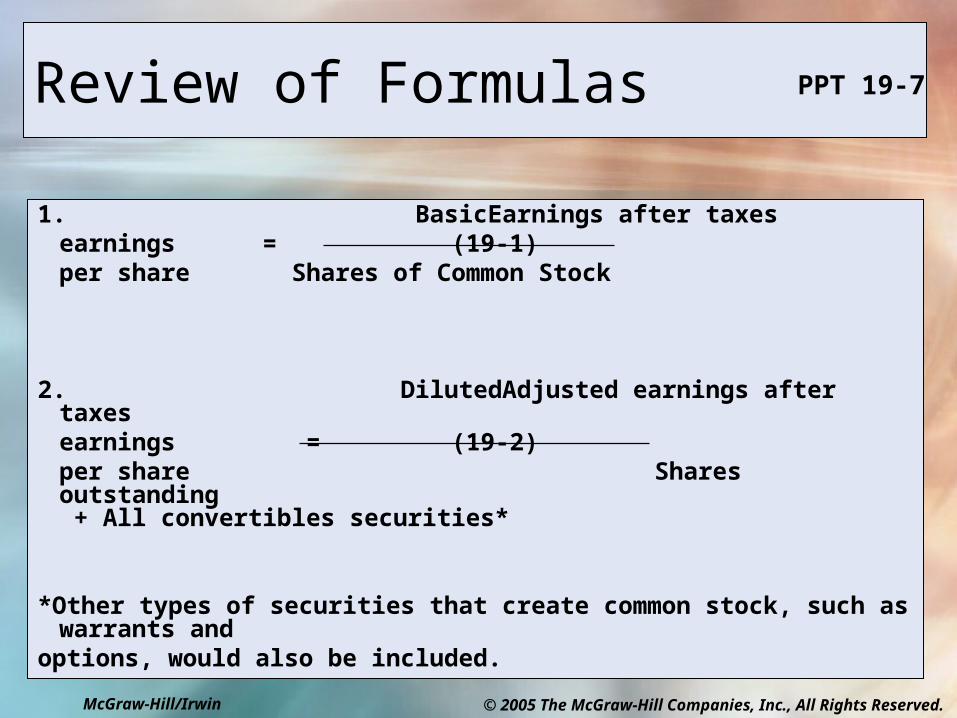

Review of Formulas PPT 19-7

1. Basic Earnings after taxesearnings = (19-1)per share Shares of Common Stock

2. Diluted Adjusted earnings after taxesearnings = (19-2)per share Shares outstanding

+ All convertibles securities*

*Other types of securities that create common stock, such as warrants and options, would also be included.

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

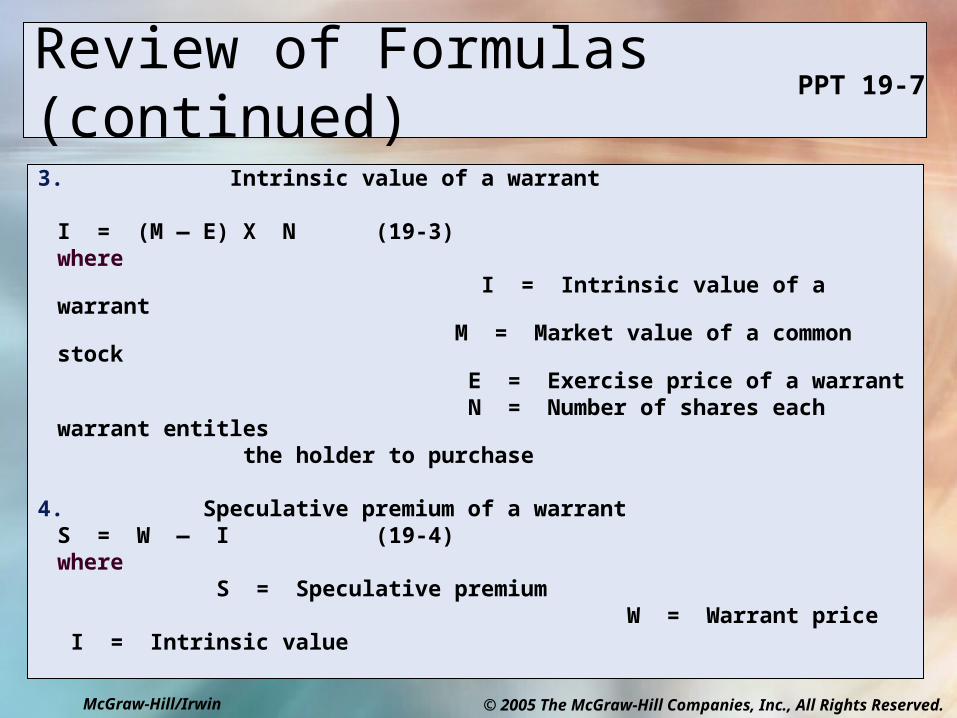

Review of Formulas (continued) PPT 19-7

3. Intrinsic value of a warrant

I = (M — E) X N (19-3)where I = Intrinsic value of a warrant M = Market value of a common stock E = Exercise price of a warrant N = Number of shares each warrant entitles

the holder to purchase

4. Speculative premium of a warrantS = W — I (19-4)

where S = Speculative premium

W = Warrant price I = Intrinsic value

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

Chapter 19 - Outline LT 19-1

Convertible Security Convertible Terminology Advantages and Disadvantages of Convertible

Securities Warrant Use of Warrants in Corporate Finance Options

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

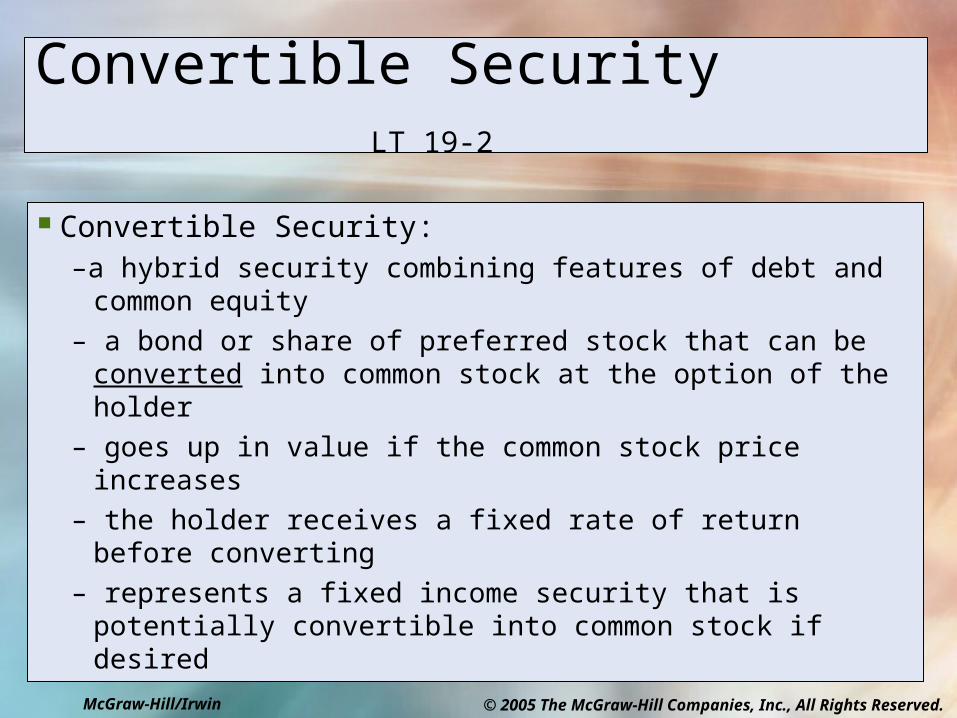

Convertible Security LT 19-2

Convertible Security: –a hybrid security combining features of debt and common

equity

– a bond or share of preferred stock that can be converted into common stock at the option of the holder

– goes up in value if the common stock price increases

– the holder receives a fixed rate of return before converting

– represents a fixed income security that is potentially convertible into common stock if desired

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

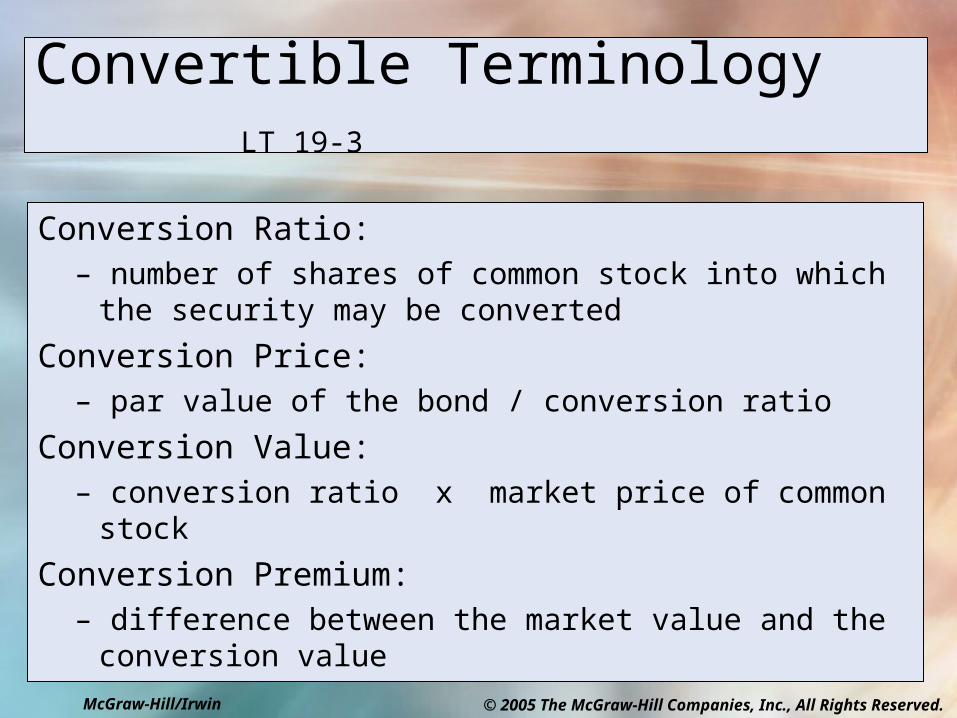

Convertible Terminology LT 19-3

Conversion Ratio:– number of shares of common stock into which the security

may be converted

Conversion Price:– par value of the bond / conversion ratio

Conversion Value:– conversion ratio x market price of common stock

Conversion Premium:– difference between the market value and the conversion

value

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

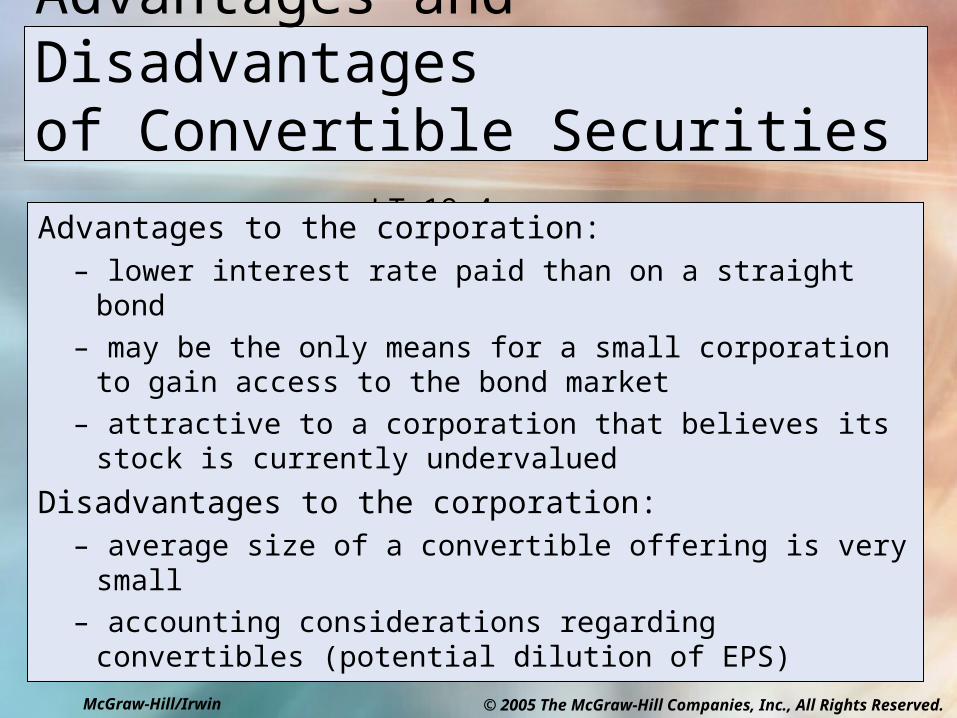

Advantages and Disadvantages of Convertible Securities LT 19-4

Advantages to the corporation:– lower interest rate paid than on a straight bond

– may be the only means for a small corporation to gain access to the bond market

– attractive to a corporation that believes its stock is currently undervalued

Disadvantages to the corporation:– average size of a convertible offering is very small

– accounting considerations regarding convertibles (potential dilution of EPS)

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

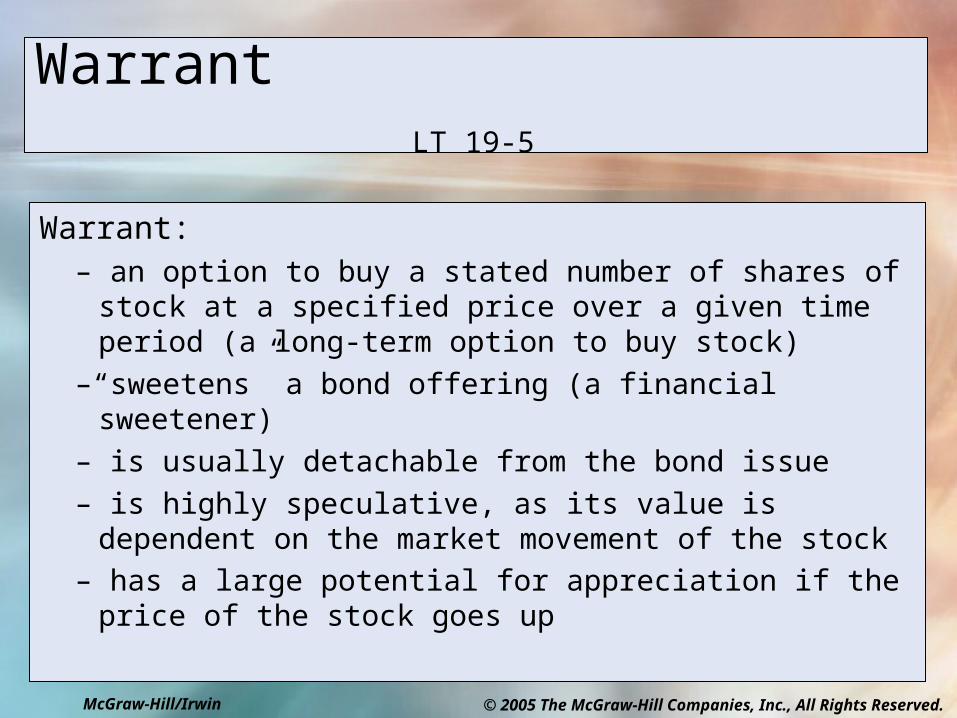

Warrant LT 19-5

Warrant:– an option to buy a stated number of shares of stock at a

specified price over a given time period (a long-term option to buy stock)

–“sweetens” a bond offering (a financial sweetener)

– is usually detachable from the bond issue

– is highly speculative, as its value is dependent on the market movement of the stock

– has a large potential for appreciation if the price of the stock goes up

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

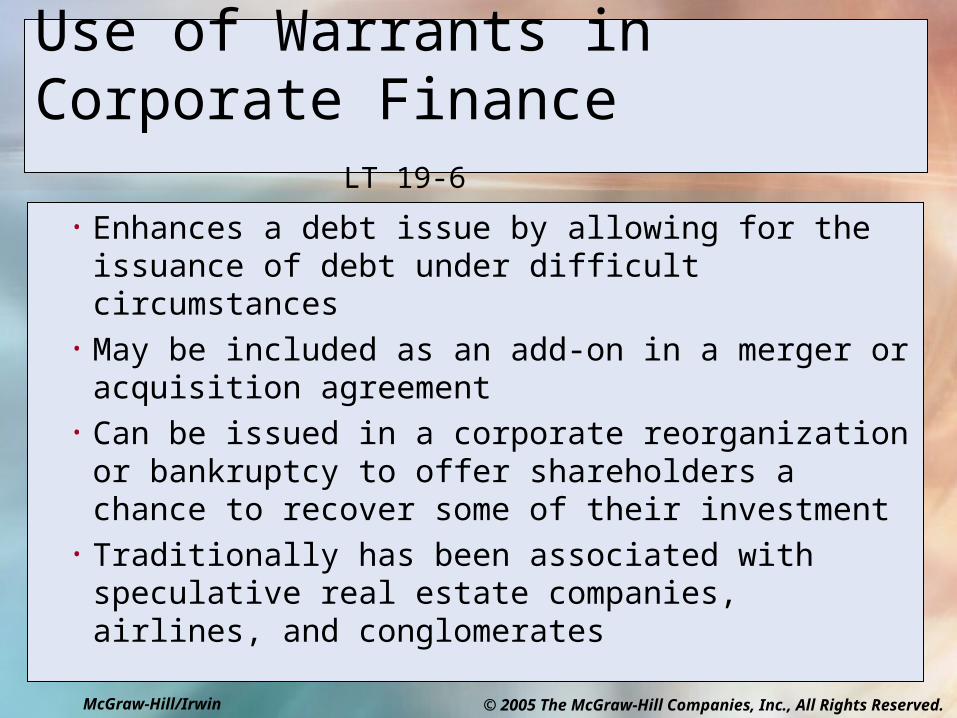

Use of Warrants in Corporate Finance LT 19-6

• Enhances a debt issue by allowing for the issuance of debt under difficult circumstances

• May be included as an add-on in a merger or acquisition agreement

• Can be issued in a corporate reorganization or bankruptcy to offer shareholders a chance to recover some of their investment

• Traditionally has been associated with speculative real estate companies, airlines, and conglomerates

McGraw-Hill/Irwin © 2005 The McGraw-Hill Companies, Inc., All Rights Reserved.

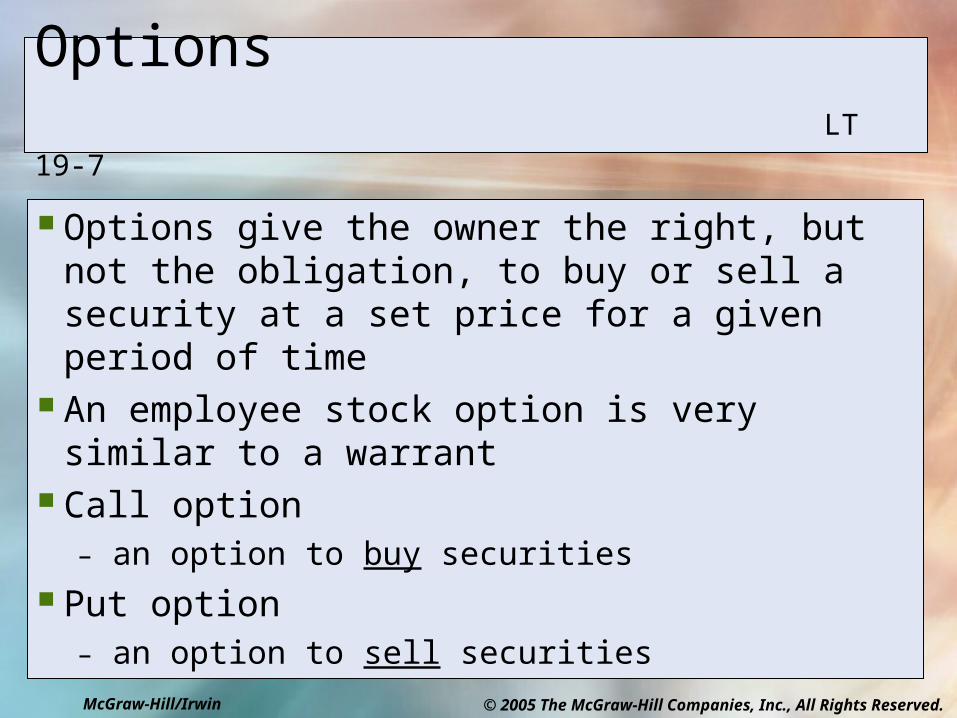

Options LT 19-7

Options give the owner the right, but not the obligation, to buy or sell a security at a set price for a given period of time

An employee stock option is very similar to a warrant Call option

– an option to buy securities Put option

– an option to sell securities