Chapter 12 - Unleashing Capitalism

22

CHAPTER 12 by Daniel S. Sutter and Andres Bello CONSTITUTIONALLY CONSTRAIN GOVERNMENT TO UNLEASH CAPITALISM 225

Transcript of Chapter 12 - Unleashing Capitalism

16

REFERENCES

Autor, David H. and Mark G Duggan. 2002. The Rise in Disability Recipiency and the

Decline in Unemployment. Chestnut Hill: center for Retirement Research at Boston College.

Benitez-Silva, Hugo, Moshe Buchinsky, and John Rust. 2004. How Large are the Classification Errors in the Social Security Disability Award Process? NBER Working

Paper No. 10219. Cambridge: National Bureau of Economic Research. Bureau of Economic Analysis, U.S. Department of Commerce. 2009. Regional Economic

Information System [electronic file]. Washington, DC: U.S. Department of Commerce. Online: http://www.bea.gov/regional/index.htm (accessed: August 20, 2009).

Bureau of Labor Statistics, U.S. Department of Labor. 2009. Glossary [electronic file]. Washington, DC: U.S. Department of Labor. Online: http://www.bls.gove/bls/ glossary.htm (accessed: August 20, 2009).

Bureau of Labor Statistics, U.S. Department of Labor. 2009. Regional Data [electronic file]. Washington DC: U.S. Department of Labor. Online http://www.bea.gov/regional/ index.htm (accessed: August 20, 2009).

National Association of Child Care Resource and Referral Agencies. 2006. Breaking the Piggy Bank-Parents and the High Price of Child Care Report, Appendix A [electronic file] Arlington, VA. Online: http://www.naccrra.org/ (accessed: August 20, 2009).

Low Income Working Families Project. 2008. Net Income Calculator [electronic file]. Washington DC: Urban Institute. Online: http://www.urban.org/center/lwf/index.cfm (accessed: August 10, 2009)

Social Security Administration. 2009. Supplemental Security Income [electronic file]. Washington DC: U.S. Social Security Administration. Online: http://www.ssa.gov/ notices/supplemental-security-income/ (accessed: August 20, 2009).

South Carolina Department of Social Services. 2009. Family Independence [electronic file]. Columbia SC. Online: http://dss.sc.gov/content/customers/finance/fi.aspx (accessed August 20, 2009). U.S. Census Bureau. 2009. Historical Tables of Poverty: 1980-2007 [electronic file]. Washington, DC: U.S. Census Bureau, Current Population Survey, Annual Social and Economic Supplements. Online: http://www.census.gove/hhes/poverty/histpov/ hstpov21.html (accessed: August 20, 2009).

U.S. Department of Health and Human Services. 2009. Administration for Children & Families: Services [electronic file]. Washington, D.C: U.S. Department of Health and Human Services. Online: http://www.acf.hhs.gov/acf_services.html#walia (accessed: August 20, 2009).

U.S. Department of Health and Human Services. 2009. Administration for Children & Families: TANF Work Participation Rates [electronic file]. Washington, D.C: U.S. Department of Health and Human Services. Online: http://www.acf.hhs.gov/programs /ofa/particip/indexparticp.html (accessed: August 20, 2009).

C H A P T E R 1 2

by Daniel S. Sutter and Andres Bello

C O N S T I T U T I O N A L L Y C O N S T R A I N

G O V E R N M E N T T O

U N L E A S H C A P I T A L I S M

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

225CHAPTER 5: SPECIFIC TAX REFORMS

13

Presumably the original intent of imposing a tax rate schedule with graduated marginal tax rates was to make the income tax progressive. However, what progressivity exists in the state’s income tax structure is due to the zero tax on the first $2,630 of income, and because of the graduated marginal tax rates. However, since the marginal tax rate increases over such small steps in income, as shown in Figure 5.5, most of the progressivity occurs at lower income levels, not higher levels of income. At higher income levels, the average tax rate hardly increases at all. This nature of the current tax is directly contradictory to the goal of progressivity. So although on the surface it appears that the tax satisfies the vertical equity condition, it really does this only at the lower income levels reducing the wealth of these lowest income taxpayers, not the intended consequence.

Figure 5.5: South Carolina income tax: Current tax rates compared to inflation-indexed rates, 2009

Current Income Tax

Rates/Brackets

Income Tax Rates/Brackets if 1959 Tax Schedule was Inflation Adjusted to

2009

Taxable Income Tax

Amount Average Tax Rate

Tax Amount

Average Tax Rate

$5,000 $71 1.42% $125 2.5%

$10,000 $290 2.90% $250 2.5%

$15,000 $604 4.03% $377 2.51%

$20,000 $954 4.77% $527 2.63%

$30,000 $1,654 5.51% $834 2.78%

$50,000 $3,054 6.10% $1,695 3.39%

$75,000 $4,804 6.41% $3,127 4.17%

$100,000 $6,554 6.56% $4,877 4.88%

$150,000 $10,054 6.70% $8,377 5.58%

$200,000 $13,554 6.77% $11,877 5.94%

Figure 5.5 also shows what the average tax rates are for various incomes and taxes

under the current tax system in South Carolina. In the right columns it also shows what the taxes and average tax rates would be if the 1959 tax tables were indexed for inflation. The figure clearly shows that the 1959 indexed tax rate structure is more uniformly progressive, especially at higher levels of incomes. It keeps tax rates extremely low for the lowest income individuals in the state. Figure 5.5 also shows that the current tax system charges all income groups more in taxes than an indexed rate schedule. The only exception is the $5,000 income earner in the table. As South Carolina income taxes continue to climb while the tax brackets remain stagnant, the state becomes a relatively high-tax state. This has a negative impact on

3

12

CONSTITUTIONALLY CONSTRAIN

GOVERNMENT TO UNLEASH CAPITALISM

Daniel Sutter and Andres Bello

INTRODUCTION

Society can either rely on private or public sector decision-making to allocate

resources. The chapters of this book have described the benefits of capitalism, or private sector decision-making. This chapter addresses the most direct way government can direct resources, by taxing and spending. Economists have documented the benefits of limiting the size and scope of government, and we begin by reviewing the evidence on how large government slows growth. Despite the cost of large government, public choice analysis reveals that the interactions of self-interested politicians, bureaucrats, citizens, and interest groups result in excessive spending, or more spending than desired by the average citizen. We examine three ways to counter the spending bias of representative democracy and benefit South Carolina: fiscal decentralization and competition between local governments; separation of powers; and tax and expenditure limits. Along the way we specifically examine the performance of South Carolina. South Carolina scores about average overall on the economic freedom index of institutional quality, but South Carolina’s poor record on government spending substantially lowers its ranking. South Carolina ranks below the national average on several measures of entrepreneurship, the mechanism through which economic freedom translates into growth. Reducing the size of state and local government will be important in unleashing capitalism in South Carolina.

MARKET INSTITUTIONS AND ECONOMIC PROSPERITY Adam Smith, the founder of economics, was an early proponent of the role of institutions in generating wealth for nations. The last several decades have witnessed an explosion of research examining the link between institutions, and specifically the institutions of the market economy, to economic growth, both across nations and within nations. Humans

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

226 CHAPTER 5: SPECIFIC TAX REFORMS

13

Presumably the original intent of imposing a tax rate schedule with graduated marginal tax rates was to make the income tax progressive. However, what progressivity exists in the state’s income tax structure is due to the zero tax on the first $2,630 of income, and because of the graduated marginal tax rates. However, since the marginal tax rate increases over such small steps in income, as shown in Figure 5.5, most of the progressivity occurs at lower income levels, not higher levels of income. At higher income levels, the average tax rate hardly increases at all. This nature of the current tax is directly contradictory to the goal of progressivity. So although on the surface it appears that the tax satisfies the vertical equity condition, it really does this only at the lower income levels reducing the wealth of these lowest income taxpayers, not the intended consequence.

Figure 5.5: South Carolina income tax: Current tax rates compared to inflation-indexed rates, 2009

Current Income Tax

Rates/Brackets

Income Tax Rates/Brackets if 1959 Tax Schedule was Inflation Adjusted to

2009

Taxable Income Tax

Amount Average Tax Rate

Tax Amount

Average Tax Rate

$5,000 $71 1.42% $125 2.5%

$10,000 $290 2.90% $250 2.5%

$15,000 $604 4.03% $377 2.51%

$20,000 $954 4.77% $527 2.63%

$30,000 $1,654 5.51% $834 2.78%

$50,000 $3,054 6.10% $1,695 3.39%

$75,000 $4,804 6.41% $3,127 4.17%

$100,000 $6,554 6.56% $4,877 4.88%

$150,000 $10,054 6.70% $8,377 5.58%

$200,000 $13,554 6.77% $11,877 5.94%

Figure 5.5 also shows what the average tax rates are for various incomes and taxes

under the current tax system in South Carolina. In the right columns it also shows what the taxes and average tax rates would be if the 1959 tax tables were indexed for inflation. The figure clearly shows that the 1959 indexed tax rate structure is more uniformly progressive, especially at higher levels of incomes. It keeps tax rates extremely low for the lowest income individuals in the state. Figure 5.5 also shows that the current tax system charges all income groups more in taxes than an indexed rate schedule. The only exception is the $5,000 income earner in the table. As South Carolina income taxes continue to climb while the tax brackets remain stagnant, the state becomes a relatively high-tax state. This has a negative impact on

3

12

CONSTITUTIONALLY CONSTRAIN

GOVERNMENT TO UNLEASH CAPITALISM

Daniel Sutter and Andres Bello

INTRODUCTION

Society can either rely on private or public sector decision-making to allocate

resources. The chapters of this book have described the benefits of capitalism, or private sector decision-making. This chapter addresses the most direct way government can direct resources, by taxing and spending. Economists have documented the benefits of limiting the size and scope of government, and we begin by reviewing the evidence on how large government slows growth. Despite the cost of large government, public choice analysis reveals that the interactions of self-interested politicians, bureaucrats, citizens, and interest groups result in excessive spending, or more spending than desired by the average citizen. We examine three ways to counter the spending bias of representative democracy and benefit South Carolina: fiscal decentralization and competition between local governments; separation of powers; and tax and expenditure limits. Along the way we specifically examine the performance of South Carolina. South Carolina scores about average overall on the economic freedom index of institutional quality, but South Carolina’s poor record on government spending substantially lowers its ranking. South Carolina ranks below the national average on several measures of entrepreneurship, the mechanism through which economic freedom translates into growth. Reducing the size of state and local government will be important in unleashing capitalism in South Carolina.

MARKET INSTITUTIONS AND ECONOMIC PROSPERITY Adam Smith, the founder of economics, was an early proponent of the role of institutions in generating wealth for nations. The last several decades have witnessed an explosion of research examining the link between institutions, and specifically the institutions of the market economy, to economic growth, both across nations and within nations. Humans

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

227CHAPTER 5: SPECIFIC TAX REFORMS

13

Presumably the original intent of imposing a tax rate schedule with graduated marginal tax rates was to make the income tax progressive. However, what progressivity exists in the state’s income tax structure is due to the zero tax on the first $2,630 of income, and because of the graduated marginal tax rates. However, since the marginal tax rate increases over such small steps in income, as shown in Figure 5.5, most of the progressivity occurs at lower income levels, not higher levels of income. At higher income levels, the average tax rate hardly increases at all. This nature of the current tax is directly contradictory to the goal of progressivity. So although on the surface it appears that the tax satisfies the vertical equity condition, it really does this only at the lower income levels reducing the wealth of these lowest income taxpayers, not the intended consequence.

Figure 5.5: South Carolina income tax: Current tax rates compared to inflation-indexed rates, 2009

Current Income Tax

Rates/Brackets

Income Tax Rates/Brackets if 1959 Tax Schedule was Inflation Adjusted to

2009

Taxable Income Tax

Amount Average Tax Rate

Tax Amount

Average Tax Rate

$5,000 $71 1.42% $125 2.5%

$10,000 $290 2.90% $250 2.5%

$15,000 $604 4.03% $377 2.51%

$20,000 $954 4.77% $527 2.63%

$30,000 $1,654 5.51% $834 2.78%

$50,000 $3,054 6.10% $1,695 3.39%

$75,000 $4,804 6.41% $3,127 4.17%

$100,000 $6,554 6.56% $4,877 4.88%

$150,000 $10,054 6.70% $8,377 5.58%

$200,000 $13,554 6.77% $11,877 5.94%

Figure 5.5 also shows what the average tax rates are for various incomes and taxes

under the current tax system in South Carolina. In the right columns it also shows what the taxes and average tax rates would be if the 1959 tax tables were indexed for inflation. The figure clearly shows that the 1959 indexed tax rate structure is more uniformly progressive, especially at higher levels of incomes. It keeps tax rates extremely low for the lowest income individuals in the state. Figure 5.5 also shows that the current tax system charges all income groups more in taxes than an indexed rate schedule. The only exception is the $5,000 income earner in the table. As South Carolina income taxes continue to climb while the tax brackets remain stagnant, the state becomes a relatively high-tax state. This has a negative impact on

4

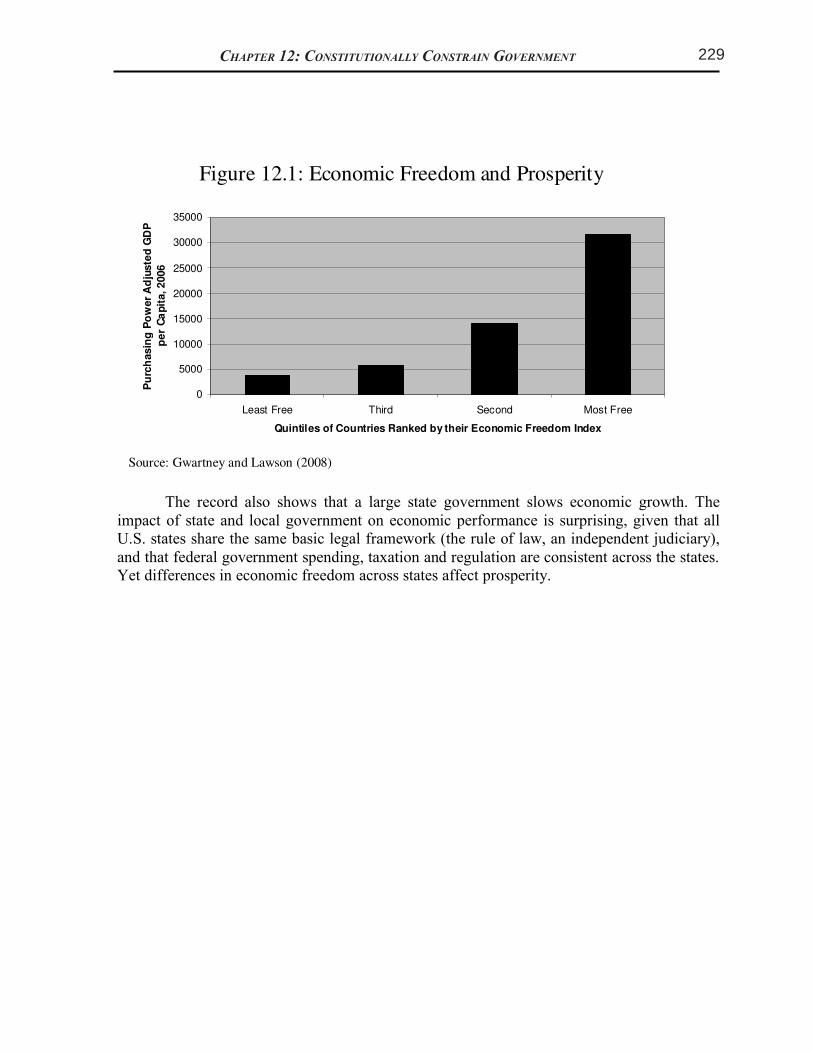

have an inherent tendency to improve the quality of their lives, and the institutions of a market economy harness this self-interest in service of others through the profit incentive. Much of the recent research on institutions and economic performance employs an index of economic freedom for more than 140 countries worldwide compiled by the Fraser Institute (Gwartney and Lawson 2008). The international economic freedom index measures the quality of institutions based on five component areas: the size of government, the legal system and protection of property rights, the quality of the money supply, freedom to engage in international trade, and economic regulation (e.g., of credit and labor markets). The index is a score from 0 to 10, with 10 representing a high level of economic freedom. The index allows comparisons between countries, or a way to classify countries as having more or less economic freedom. A market economy requires a legal infrastructure protecting property rights and the freedom to trade. Internationally, many weak or predatory governments fail to supply the basic framework for market exchange, with terrible consequences for human well-being, as illustrated by Figure 12.1. The figure reports Gross Domestic Product (GDP) per capita, a measure of the standard of living across nations, averaged across quintiles of countries as ranked by their economic freedom score, as reported by Gwartney and Lawson (2008). GDP per capita is nearly ten times higher in the top 25 percent of countries as ranked by economic freedom than in the bottom 25 percent of countries. These differences in standard of living did not occur over night, and can reflect the cumulative impact over decades of an environment hospitable to a market economy. The difference between the top and bottom quartiles of nations reflects the effect of the lack of protection of property and the rule of law. But GDP per capita is still more than double in the freest 25 percent of countries than in the second 25 percent, so even among nations where the rule of law is reasonably well established, limiting government spending and regulation is critical for growth and a high standard of living.1 Economic freedom does not merely lead to the pursuit of a narrow measure of the standard of living, or produce growth for some at the expense of poverty for others. Norton and Gwartney (2008) show that economic freedom reduces extreme poverty and improves a nation’s score on the United Nations’ Human Poverty Index.

1 Economists have extensively investigated the relationship between economic freedom and prosperity. For a

discussion of some of the findings of these studies, see Gwartney, Holcombe and Lawson (2004) and Lawson

(2007).

5

Figure 12.1: Economic Freedom and Prosperity

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

Least Free Third Second Most Free

Quintiles of Countries Ranked by their Economic Freedom Index

Purc

hasin

g

Pow

er

Adju

ste

d

GD

P

per

Capit

a,

20

06

Source: Gwartney and Lawson (2008)

The record also shows that a large state government slows economic growth. The impact of state and local government on economic performance is surprising, given that all U.S. states share the same basic legal framework (the rule of law, an independent judiciary), and that federal government spending, taxation and regulation are consistent across the states. Yet differences in economic freedom across states affect prosperity.

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

228 CHAPTER 5: SPECIFIC TAX REFORMS

13

Presumably the original intent of imposing a tax rate schedule with graduated marginal tax rates was to make the income tax progressive. However, what progressivity exists in the state’s income tax structure is due to the zero tax on the first $2,630 of income, and because of the graduated marginal tax rates. However, since the marginal tax rate increases over such small steps in income, as shown in Figure 5.5, most of the progressivity occurs at lower income levels, not higher levels of income. At higher income levels, the average tax rate hardly increases at all. This nature of the current tax is directly contradictory to the goal of progressivity. So although on the surface it appears that the tax satisfies the vertical equity condition, it really does this only at the lower income levels reducing the wealth of these lowest income taxpayers, not the intended consequence.

Figure 5.5: South Carolina income tax: Current tax rates compared to inflation-indexed rates, 2009

Current Income Tax

Rates/Brackets

Income Tax Rates/Brackets if 1959 Tax Schedule was Inflation Adjusted to

2009

Taxable Income Tax

Amount Average Tax Rate

Tax Amount

Average Tax Rate

$5,000 $71 1.42% $125 2.5%

$10,000 $290 2.90% $250 2.5%

$15,000 $604 4.03% $377 2.51%

$20,000 $954 4.77% $527 2.63%

$30,000 $1,654 5.51% $834 2.78%

$50,000 $3,054 6.10% $1,695 3.39%

$75,000 $4,804 6.41% $3,127 4.17%

$100,000 $6,554 6.56% $4,877 4.88%

$150,000 $10,054 6.70% $8,377 5.58%

$200,000 $13,554 6.77% $11,877 5.94%

Figure 5.5 also shows what the average tax rates are for various incomes and taxes

under the current tax system in South Carolina. In the right columns it also shows what the taxes and average tax rates would be if the 1959 tax tables were indexed for inflation. The figure clearly shows that the 1959 indexed tax rate structure is more uniformly progressive, especially at higher levels of incomes. It keeps tax rates extremely low for the lowest income individuals in the state. Figure 5.5 also shows that the current tax system charges all income groups more in taxes than an indexed rate schedule. The only exception is the $5,000 income earner in the table. As South Carolina income taxes continue to climb while the tax brackets remain stagnant, the state becomes a relatively high-tax state. This has a negative impact on

4

have an inherent tendency to improve the quality of their lives, and the institutions of a market economy harness this self-interest in service of others through the profit incentive. Much of the recent research on institutions and economic performance employs an index of economic freedom for more than 140 countries worldwide compiled by the Fraser Institute (Gwartney and Lawson 2008). The international economic freedom index measures the quality of institutions based on five component areas: the size of government, the legal system and protection of property rights, the quality of the money supply, freedom to engage in international trade, and economic regulation (e.g., of credit and labor markets). The index is a score from 0 to 10, with 10 representing a high level of economic freedom. The index allows comparisons between countries, or a way to classify countries as having more or less economic freedom. A market economy requires a legal infrastructure protecting property rights and the freedom to trade. Internationally, many weak or predatory governments fail to supply the basic framework for market exchange, with terrible consequences for human well-being, as illustrated by Figure 12.1. The figure reports Gross Domestic Product (GDP) per capita, a measure of the standard of living across nations, averaged across quintiles of countries as ranked by their economic freedom score, as reported by Gwartney and Lawson (2008). GDP per capita is nearly ten times higher in the top 25 percent of countries as ranked by economic freedom than in the bottom 25 percent of countries. These differences in standard of living did not occur over night, and can reflect the cumulative impact over decades of an environment hospitable to a market economy. The difference between the top and bottom quartiles of nations reflects the effect of the lack of protection of property and the rule of law. But GDP per capita is still more than double in the freest 25 percent of countries than in the second 25 percent, so even among nations where the rule of law is reasonably well established, limiting government spending and regulation is critical for growth and a high standard of living.1 Economic freedom does not merely lead to the pursuit of a narrow measure of the standard of living, or produce growth for some at the expense of poverty for others. Norton and Gwartney (2008) show that economic freedom reduces extreme poverty and improves a nation’s score on the United Nations’ Human Poverty Index.

1 Economists have extensively investigated the relationship between economic freedom and prosperity. For a

discussion of some of the findings of these studies, see Gwartney, Holcombe and Lawson (2004) and Lawson

(2007).

5

Figure 12.1: Economic Freedom and Prosperity

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

Least Free Third Second Most Free

Quintiles of Countries Ranked by their Economic Freedom Index

Purc

hasin

g

Pow

er

Adju

ste

d

GD

P

per

Capit

a,

20

06

Source: Gwartney and Lawson (2008)

The record also shows that a large state government slows economic growth. The impact of state and local government on economic performance is surprising, given that all U.S. states share the same basic legal framework (the rule of law, an independent judiciary), and that federal government spending, taxation and regulation are consistent across the states. Yet differences in economic freedom across states affect prosperity.

Chapter 12: Constitutionally Constrain government

Figure 12.1: Economic Freedom and Prosperity

0

5000

10000

15000

20000

25000

30000

35000

Least Free Third Second Most Free

Quintiles of Countries Ranked by their Economic Freedom Index

Pu

rch

asin

g P

ow

er

Ad

juste

d G

DP

pe

r C

ap

ita, 2

006

Source: Gwartney and Lawson (2008)

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

229CHAPTER 5: SPECIFIC TAX REFORMS

13

Presumably the original intent of imposing a tax rate schedule with graduated marginal tax rates was to make the income tax progressive. However, what progressivity exists in the state’s income tax structure is due to the zero tax on the first $2,630 of income, and because of the graduated marginal tax rates. However, since the marginal tax rate increases over such small steps in income, as shown in Figure 5.5, most of the progressivity occurs at lower income levels, not higher levels of income. At higher income levels, the average tax rate hardly increases at all. This nature of the current tax is directly contradictory to the goal of progressivity. So although on the surface it appears that the tax satisfies the vertical equity condition, it really does this only at the lower income levels reducing the wealth of these lowest income taxpayers, not the intended consequence.

Figure 5.5: South Carolina income tax: Current tax rates compared to inflation-indexed rates, 2009

Current Income Tax

Rates/Brackets

Income Tax Rates/Brackets if 1959 Tax Schedule was Inflation Adjusted to

2009

Taxable Income Tax

Amount Average Tax Rate

Tax Amount

Average Tax Rate

$5,000 $71 1.42% $125 2.5%

$10,000 $290 2.90% $250 2.5%

$15,000 $604 4.03% $377 2.51%

$20,000 $954 4.77% $527 2.63%

$30,000 $1,654 5.51% $834 2.78%

$50,000 $3,054 6.10% $1,695 3.39%

$75,000 $4,804 6.41% $3,127 4.17%

$100,000 $6,554 6.56% $4,877 4.88%

$150,000 $10,054 6.70% $8,377 5.58%

$200,000 $13,554 6.77% $11,877 5.94%

Figure 5.5 also shows what the average tax rates are for various incomes and taxes

under the current tax system in South Carolina. In the right columns it also shows what the taxes and average tax rates would be if the 1959 tax tables were indexed for inflation. The figure clearly shows that the 1959 indexed tax rate structure is more uniformly progressive, especially at higher levels of incomes. It keeps tax rates extremely low for the lowest income individuals in the state. Figure 5.5 also shows that the current tax system charges all income groups more in taxes than an indexed rate schedule. The only exception is the $5,000 income earner in the table. As South Carolina income taxes continue to climb while the tax brackets remain stagnant, the state becomes a relatively high-tax state. This has a negative impact on

6

Figure 12.2: Per Capita Income (2008) vs. Size of

State Government (1977)

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

4 6 8 10 12 14

State Spending as a Percent of Income (1977)

Per

Cap

tia P

erso

nal In

com

e (2

008)

Source: U.S. Census and Bureau of Economic Analysis

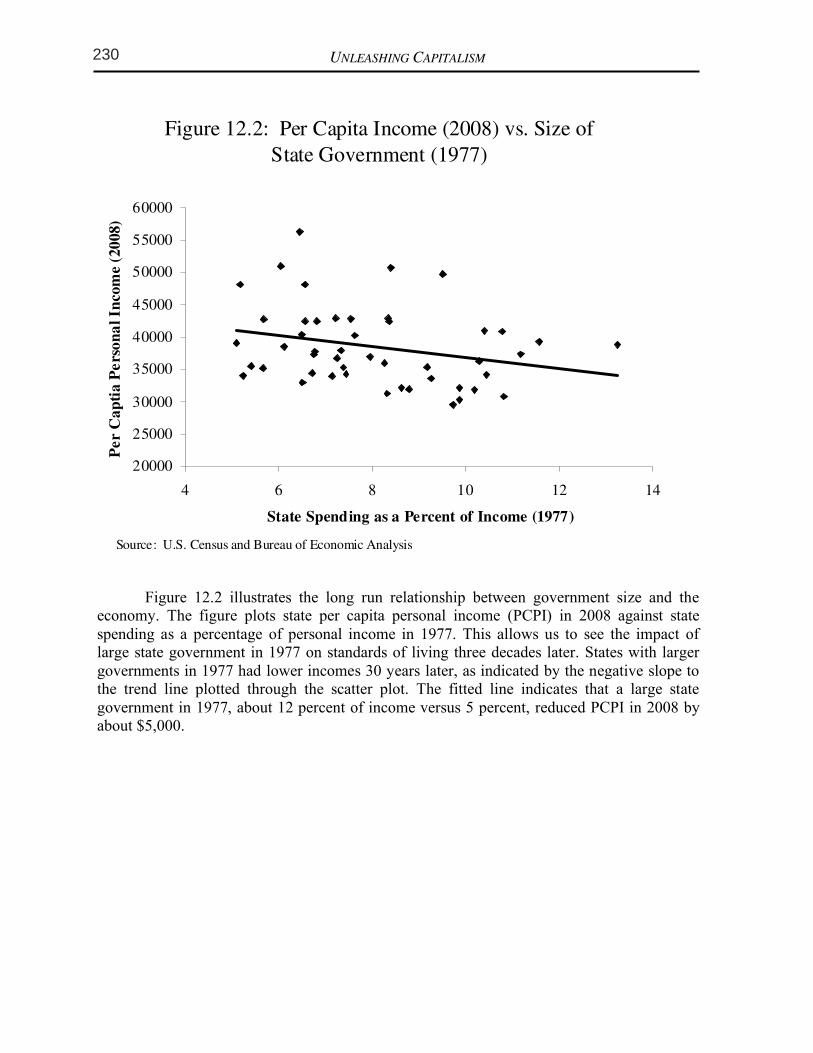

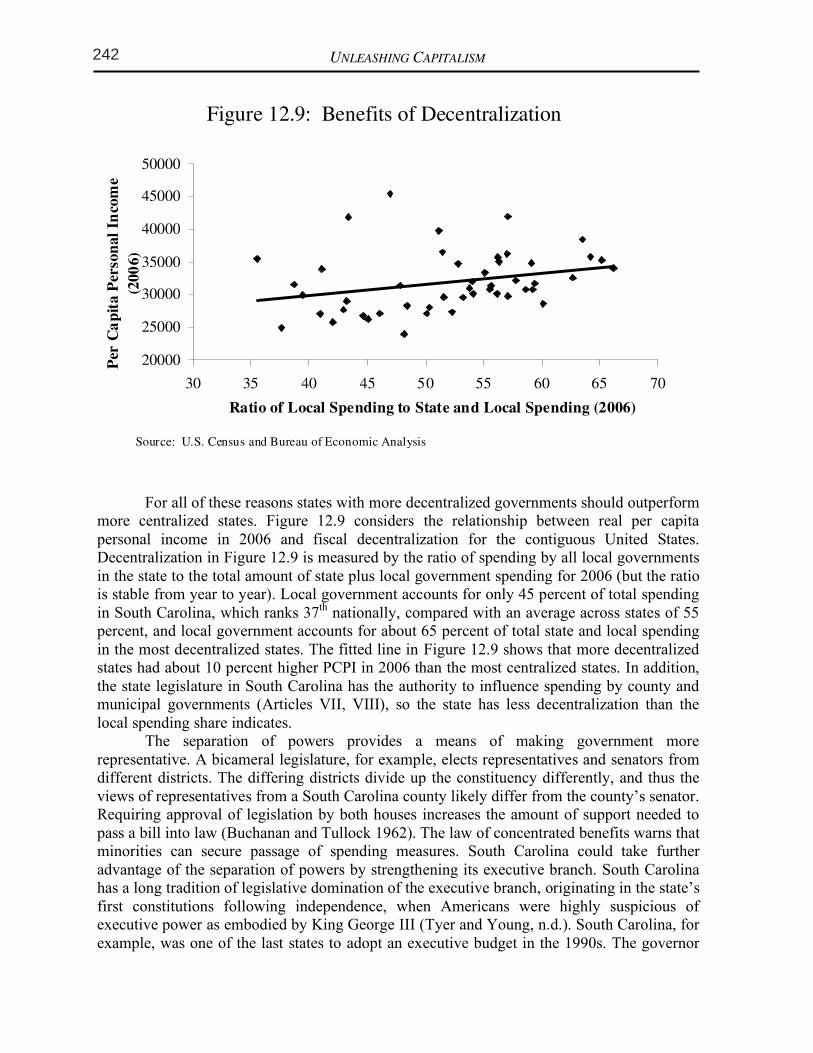

Figure 12.2 illustrates the long run relationship between government size and the economy. The figure plots state per capita personal income (PCPI) in 2008 against state spending as a percentage of personal income in 1977. This allows us to see the impact of large state government in 1977 on standards of living three decades later. States with larger governments in 1977 had lower incomes 30 years later, as indicated by the negative slope to the trend line plotted through the scatter plot. The fitted line indicates that a large state government in 1977, about 12 percent of income versus 5 percent, reduced PCPI in 2008 by about $5,000.

7

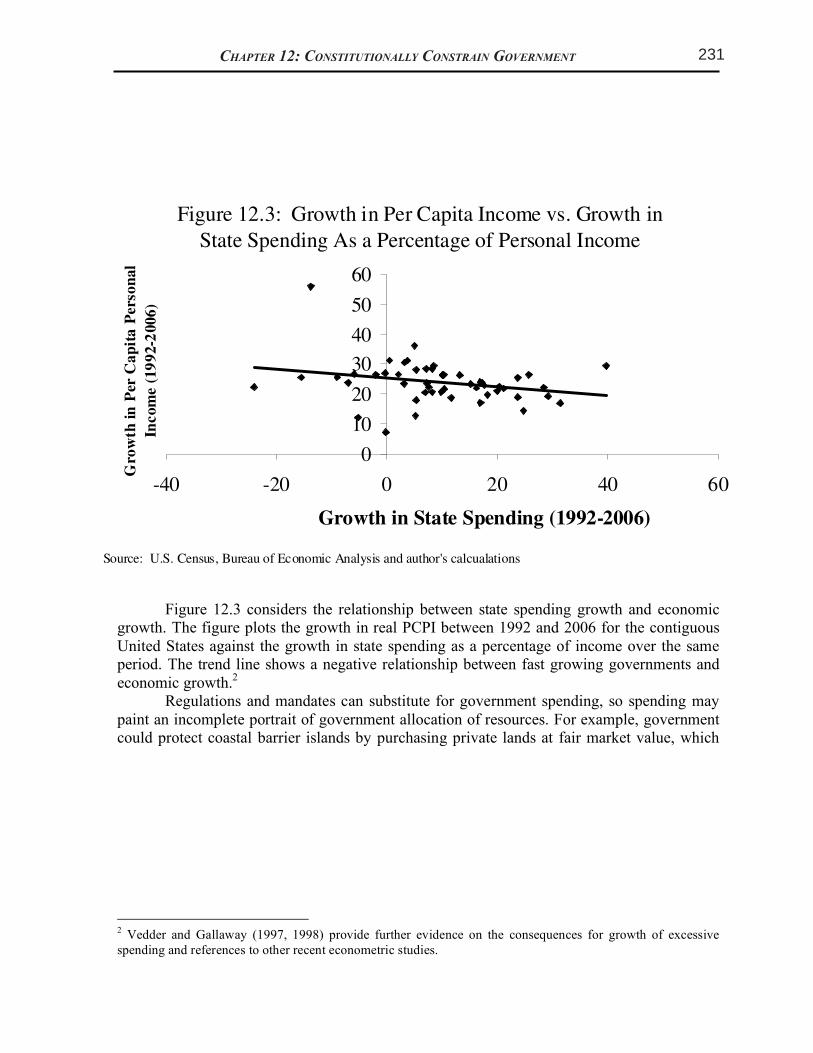

Figure 12.3 considers the relationship between state spending growth and economic

growth. The figure plots the growth in real PCPI between 1992 and 2006 for the contiguous United States against the growth in state spending as a percentage of income over the same period. The trend line shows a negative relationship between fast growing governments and economic growth.2 Regulations and mandates can substitute for government spending, so spending may paint an incomplete portrait of government allocation of resources. For example, government could protect coastal barrier islands by purchasing private lands at fair market value, which

2 Vedder and Gallaway (1997, 1998) provide further evidence on the consequences for growth of excessive

spending and references to other recent econometric studies.

7

Figure 12.3 considers the relationship between state spending growth and economic

growth. The figure plots the growth in real PCPI between 1992 and 2006 for the contiguous United States against the growth in state spending as a percentage of income over the same period. The trend line shows a negative relationship between fast growing governments and economic growth.2 Regulations and mandates can substitute for government spending, so spending may paint an incomplete portrait of government allocation of resources. For example, government could protect coastal barrier islands by purchasing private lands at fair market value, which

2 Vedder and Gallaway (1997, 1998) provide further evidence on the consequences for growth of excessive

spending and references to other recent econometric studies.

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

Figure 12.2: Per Capita Income (2008) vs. Size of

State Government (1977)

20000

25000

30000

35000

40000

45000

50000

55000

60000

4 6 8 10 12 14

State Spending as a Percent of Income (1977)

Per C

ap

tia

Pe

rso

na

l In

com

e (

20

08)

Source: U.S. Census and Bureau of Economic Analysis

7

Figure 12.3 considers the relationship between state spending growth and economic

growth. The figure plots the growth in real PCPI between 1992 and 2006 for the contiguous United States against the growth in state spending as a percentage of income over the same period. The trend line shows a negative relationship between fast growing governments and economic growth.2 Regulations and mandates can substitute for government spending, so spending may paint an incomplete portrait of government allocation of resources. For example, government could protect coastal barrier islands by purchasing private lands at fair market value, which

2 Vedder and Gallaway (1997, 1998) provide further evidence on the consequences for growth of excessive

spending and references to other recent econometric studies.

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

230 CHAPTER 5: SPECIFIC TAX REFORMS

13

Presumably the original intent of imposing a tax rate schedule with graduated marginal tax rates was to make the income tax progressive. However, what progressivity exists in the state’s income tax structure is due to the zero tax on the first $2,630 of income, and because of the graduated marginal tax rates. However, since the marginal tax rate increases over such small steps in income, as shown in Figure 5.5, most of the progressivity occurs at lower income levels, not higher levels of income. At higher income levels, the average tax rate hardly increases at all. This nature of the current tax is directly contradictory to the goal of progressivity. So although on the surface it appears that the tax satisfies the vertical equity condition, it really does this only at the lower income levels reducing the wealth of these lowest income taxpayers, not the intended consequence.

Figure 5.5: South Carolina income tax: Current tax rates compared to inflation-indexed rates, 2009

Current Income Tax

Rates/Brackets

Income Tax Rates/Brackets if 1959 Tax Schedule was Inflation Adjusted to

2009

Taxable Income Tax

Amount Average Tax Rate

Tax Amount

Average Tax Rate

$5,000 $71 1.42% $125 2.5%

$10,000 $290 2.90% $250 2.5%

$15,000 $604 4.03% $377 2.51%

$20,000 $954 4.77% $527 2.63%

$30,000 $1,654 5.51% $834 2.78%

$50,000 $3,054 6.10% $1,695 3.39%

$75,000 $4,804 6.41% $3,127 4.17%

$100,000 $6,554 6.56% $4,877 4.88%

$150,000 $10,054 6.70% $8,377 5.58%

$200,000 $13,554 6.77% $11,877 5.94%

Figure 5.5 also shows what the average tax rates are for various incomes and taxes

under the current tax system in South Carolina. In the right columns it also shows what the taxes and average tax rates would be if the 1959 tax tables were indexed for inflation. The figure clearly shows that the 1959 indexed tax rate structure is more uniformly progressive, especially at higher levels of incomes. It keeps tax rates extremely low for the lowest income individuals in the state. Figure 5.5 also shows that the current tax system charges all income groups more in taxes than an indexed rate schedule. The only exception is the $5,000 income earner in the table. As South Carolina income taxes continue to climb while the tax brackets remain stagnant, the state becomes a relatively high-tax state. This has a negative impact on

6

Figure 12.2: Per Capita Income (2008) vs. Size of

State Government (1977)

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

4 6 8 10 12 14

State Spending as a Percent of Income (1977)

Per

Cap

tia P

erso

nal In

com

e (2

008)

Source: U.S. Census and Bureau of Economic Analysis

Figure 12.2 illustrates the long run relationship between government size and the economy. The figure plots state per capita personal income (PCPI) in 2008 against state spending as a percentage of personal income in 1977. This allows us to see the impact of large state government in 1977 on standards of living three decades later. States with larger governments in 1977 had lower incomes 30 years later, as indicated by the negative slope to the trend line plotted through the scatter plot. The fitted line indicates that a large state government in 1977, about 12 percent of income versus 5 percent, reduced PCPI in 2008 by about $5,000.

7

Figure 12.3 considers the relationship between state spending growth and economic

growth. The figure plots the growth in real PCPI between 1992 and 2006 for the contiguous United States against the growth in state spending as a percentage of income over the same period. The trend line shows a negative relationship between fast growing governments and economic growth.2 Regulations and mandates can substitute for government spending, so spending may paint an incomplete portrait of government allocation of resources. For example, government could protect coastal barrier islands by purchasing private lands at fair market value, which

2 Vedder and Gallaway (1997, 1998) provide further evidence on the consequences for growth of excessive

spending and references to other recent econometric studies.

7

Figure 12.3 considers the relationship between state spending growth and economic

growth. The figure plots the growth in real PCPI between 1992 and 2006 for the contiguous United States against the growth in state spending as a percentage of income over the same period. The trend line shows a negative relationship between fast growing governments and economic growth.2 Regulations and mandates can substitute for government spending, so spending may paint an incomplete portrait of government allocation of resources. For example, government could protect coastal barrier islands by purchasing private lands at fair market value, which

2 Vedder and Gallaway (1997, 1998) provide further evidence on the consequences for growth of excessive

spending and references to other recent econometric studies.

Chapter 12: Constitutionally Constrain government

Figure 12.3: Growth in Per Capita Income vs. Growth in

State Spending As a Percentage of Personal Income

0

10

20

30

40

50

60

-40 -20 0 20 40 60

Growth in State Spending (1992-2006)

Gro

wth

in

Per

Ca

pit

a P

ers

on

al

Incom

e (

19

92-2

006

)

Source: U.S. Census, Bureau of Economic Analysis and author's calcualations

7

Figure 12.3 considers the relationship between state spending growth and economic

growth. The figure plots the growth in real PCPI between 1992 and 2006 for the contiguous United States against the growth in state spending as a percentage of income over the same period. The trend line shows a negative relationship between fast growing governments and economic growth.2 Regulations and mandates can substitute for government spending, so spending may paint an incomplete portrait of government allocation of resources. For example, government could protect coastal barrier islands by purchasing private lands at fair market value, which

2 Vedder and Gallaway (1997, 1998) provide further evidence on the consequences for growth of excessive

spending and references to other recent econometric studies.

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

231CHAPTER 5: SPECIFIC TAX REFORMS

13

Presumably the original intent of imposing a tax rate schedule with graduated marginal tax rates was to make the income tax progressive. However, what progressivity exists in the state’s income tax structure is due to the zero tax on the first $2,630 of income, and because of the graduated marginal tax rates. However, since the marginal tax rate increases over such small steps in income, as shown in Figure 5.5, most of the progressivity occurs at lower income levels, not higher levels of income. At higher income levels, the average tax rate hardly increases at all. This nature of the current tax is directly contradictory to the goal of progressivity. So although on the surface it appears that the tax satisfies the vertical equity condition, it really does this only at the lower income levels reducing the wealth of these lowest income taxpayers, not the intended consequence.

Figure 5.5: South Carolina income tax: Current tax rates compared to inflation-indexed rates, 2009

Current Income Tax

Rates/Brackets

Income Tax Rates/Brackets if 1959 Tax Schedule was Inflation Adjusted to

2009

Taxable Income Tax

Amount Average Tax Rate

Tax Amount

Average Tax Rate

$5,000 $71 1.42% $125 2.5%

$10,000 $290 2.90% $250 2.5%

$15,000 $604 4.03% $377 2.51%

$20,000 $954 4.77% $527 2.63%

$30,000 $1,654 5.51% $834 2.78%

$50,000 $3,054 6.10% $1,695 3.39%

$75,000 $4,804 6.41% $3,127 4.17%

$100,000 $6,554 6.56% $4,877 4.88%

$150,000 $10,054 6.70% $8,377 5.58%

$200,000 $13,554 6.77% $11,877 5.94%

Figure 5.5 also shows what the average tax rates are for various incomes and taxes

under the current tax system in South Carolina. In the right columns it also shows what the taxes and average tax rates would be if the 1959 tax tables were indexed for inflation. The figure clearly shows that the 1959 indexed tax rate structure is more uniformly progressive, especially at higher levels of incomes. It keeps tax rates extremely low for the lowest income individuals in the state. Figure 5.5 also shows that the current tax system charges all income groups more in taxes than an indexed rate schedule. The only exception is the $5,000 income earner in the table. As South Carolina income taxes continue to climb while the tax brackets remain stagnant, the state becomes a relatively high-tax state. This has a negative impact on

8

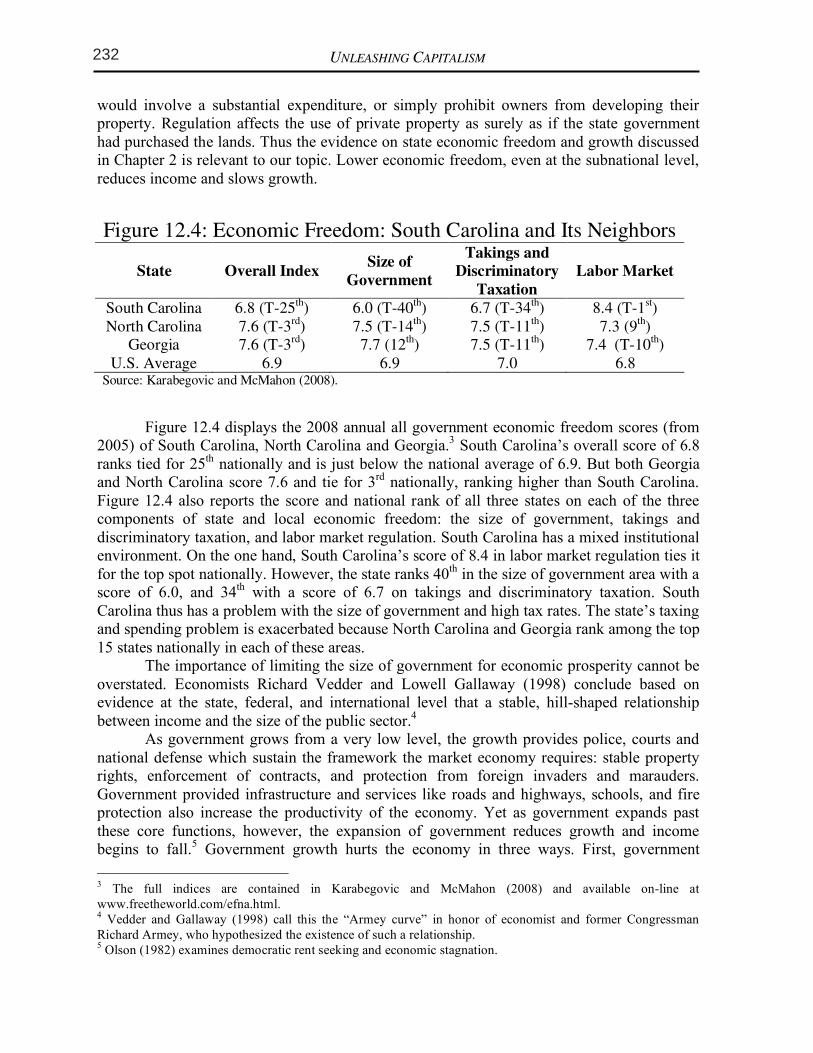

would involve a substantial expenditure, or simply prohibit owners from developing their property. Regulation affects the use of private property as surely as if the state government had purchased the lands. Thus the evidence on state economic freedom and growth discussed in Chapter 2 is relevant to our topic. Lower economic freedom, even at the subnational level, reduces income and slows growth.

Figure 12.4: Economic Freedom: South Carolina and Its Neighbors

State Overall Index Size of Government

Takings and Discriminatory Taxation

Labor Market

South Carolina 6.8 (T-25th) 6.0 (T-40th) 6.7 (T-34th) 8.4 (T-1st)

North Carolina 7.6 (T-3rd) 7.5 (T-14th) 7.5 (T-11th) 7.3 (9th)

Georgia 7.6 (T-3rd) 7.7 (12th) 7.5 (T-11th) 7.4 (T-10th)

U.S. Average 6.9 6.9 7.0 6.8 Source: Karabegovic and McMahon (2008).

Figure 12.4 displays the 2008 annual all government economic freedom scores (from

2005) of South Carolina, North Carolina and Georgia.3 South Carolina’s overall score of 6.8 ranks tied for 25th nationally and is just below the national average of 6.9. But both Georgia and North Carolina score 7.6 and tie for 3rd nationally, ranking higher than South Carolina. Figure 12.4 also reports the score and national rank of all three states on each of the three components of state and local economic freedom: the size of government, takings and discriminatory taxation, and labor market regulation. South Carolina has a mixed institutional environment. On the one hand, South Carolina’s score of 8.4 in labor market regulation ties it for the top spot nationally. However, the state ranks 40th in the size of government area with a score of 6.0, and 34th with a score of 6.7 on takings and discriminatory taxation. South Carolina thus has a problem with the size of government and high tax rates. The state’s taxing and spending problem is exacerbated because North Carolina and Georgia rank among the top 15 states nationally in each of these areas. The importance of limiting the size of government for economic prosperity cannot be overstated. Economists Richard Vedder and Lowell Gallaway (1998) conclude based on evidence at the state, federal, and international level that a stable, hill-shaped relationship between income and the size of the public sector.4

As government grows from a very low level, the growth provides police, courts and national defense which sustain the framework the market economy requires: stable property rights, enforcement of contracts, and protection from foreign invaders and marauders. Government provided infrastructure and services like roads and highways, schools, and fire protection also increase the productivity of the economy. Yet as government expands past these core functions, however, the expansion of government reduces growth and income begins to fall.5 Government growth hurts the economy in three ways. First, government

3 The full indices are contained in Karabegovic and McMahon (2008) and available on-line at

www.freetheworld.com/efna.html. 4 Vedder and Gallaway (1998) call this the “Armey curve” in honor of economist and former Congressman

Richard Armey, who hypothesized the existence of such a relationship. 5 Olson (1982) examines democratic rent seeking and economic stagnation.

9

increasingly makes resource allocation decisions, and these decisions are made for political reasons, not profit or loss considerations. Second, government must tax to fund spending. Taxes distort choices in the market, and the cost to the economy of this distortion exceeds the dollars collected for government to spend. Higher taxes reduce economic freedom, entrepreneurship (Garrett and Wall 2006), and growth (Poulson and Kaplan 2008). Marginal tax rates, the tax people pay if they earn an extra $1,000 or if a business earns an extra $1 million in profit, determine how much taxes reduce economic activity. The disruptive effect of taxes increases more than proportionally with the tax rate, so that the distortion from a 20 percent income tax rate is more than double that from a 10 percent. Vedder and Gallaway (1999) contend based on the available evidence that the cost of taxes may be 40 cents or more per dollar of revenue raised. Third, interest groups use resources to lobby politicians for increased spending, what Gordon Tullock (1967) labeled ‘rent seeking.’ Resources spent trying to secure favors from government cannot be used to produce things of value like cars, clothes, homes, and computers, making society poorer.

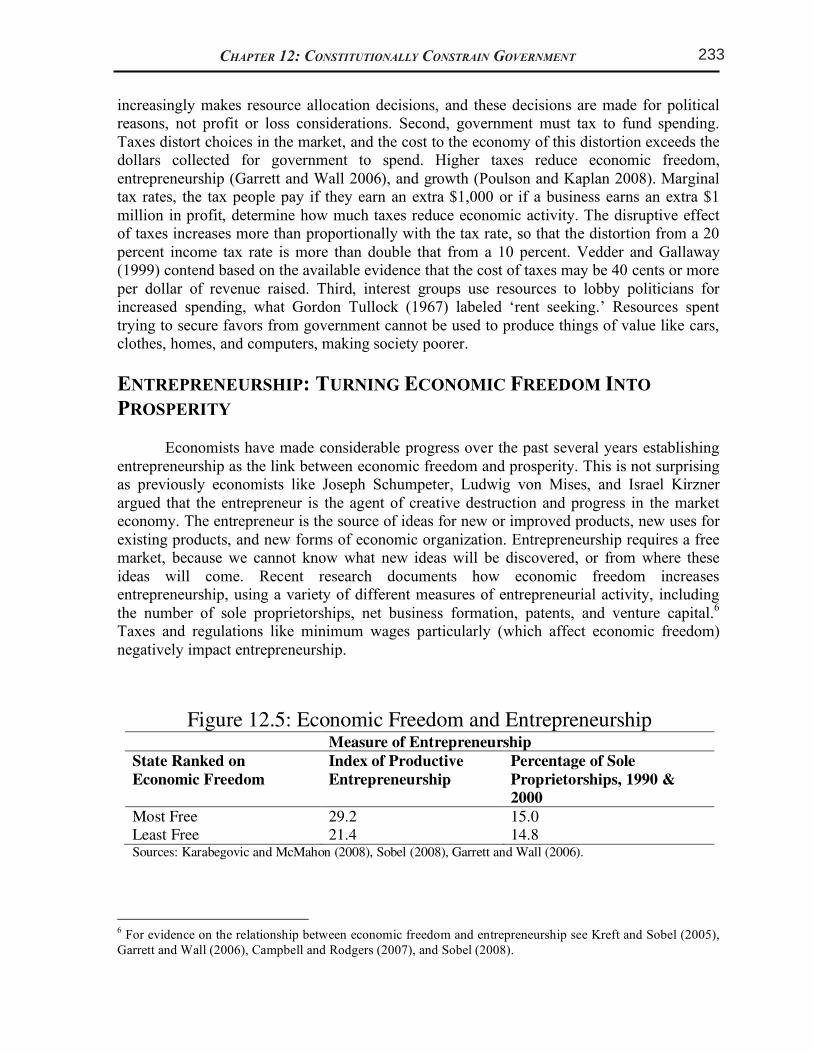

ENTREPRENEURSHIP: TURNING ECONOMIC FREEDOM INTO

PROSPERITY

Economists have made considerable progress over the past several years establishing entrepreneurship as the link between economic freedom and prosperity. This is not surprising as previously economists like Joseph Schumpeter, Ludwig von Mises, and Israel Kirzner argued that the entrepreneur is the agent of creative destruction and progress in the market economy. The entrepreneur is the source of ideas for new or improved products, new uses for existing products, and new forms of economic organization. Entrepreneurship requires a free market, because we cannot know what new ideas will be discovered, or from where these ideas will come. Recent research documents how economic freedom increases entrepreneurship, using a variety of different measures of entrepreneurial activity, including the number of sole proprietorships, net business formation, patents, and venture capital.6 Taxes and regulations like minimum wages particularly (which affect economic freedom) negatively impact entrepreneurship.

Figure 12.5: Economic Freedom and Entrepreneurship

Measure of Entrepreneurship

State Ranked on Economic Freedom

Index of Productive Entrepreneurship

Percentage of Sole Proprietorships, 1990 & 2000

Most Free 29.2 15.0

Least Free 21.4 14.8 Sources: Karabegovic and McMahon (2008), Sobel (2008), Garrett and Wall (2006).

6 For evidence on the relationship between economic freedom and entrepreneurship see Kreft and Sobel (2005),

Garrett and Wall (2006), Campbell and Rodgers (2007), and Sobel (2008).

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

Figure 12.4: Economic Freedom: South Carolina and Its Neighbors

State Overall Index Size of

Government

Takings and

Discriminatory

Taxation

Labor Market

South Carolina 6.8 (T-25th) 6.0 (T-40

th) 6.7 (T-34

th) 8.4 (T-1

st)

North Carolina 7.6 (T-3rd

) 7.5 (T-14th) 7.5 (T-11

th) 7.3 (9

th)

Georgia 7.6 (T-3rd

) 7.7 (12th) 7.5 (T-11

th) 7.4 (T-10

th)

U.S. Average 6.9 6.9 7.0 6.8 Source: Karabegovic and McMahon (2008).

Figure 12.5: Economic Freedom and Entrepreneurship Measure of Entrepreneurship

State Ranked on

Economic Freedom

Index of Productive

Entrepreneurship

Percentage of Sole

Proprietorships, 1990 &

2000

Most Free 29.2 15.0

Least Free 21.4 14.8 Sources: Karabegovic and McMahon (2008), Sobel (2008), Garrett and Wall (2006).

UNLEASHING CAPITALISM 18

manufacturing property tax in the country. In Figure 5.8 we present the effective property tax rates data for Southeastern states, for comparison. The ranks given for the states are out of all 50 states. The ‘net tax’ and ‘effective tax rate’ are calculated based on property valued at $25 million ($12.5 million in machinery and equipment, $12.5 million in inventories, and $2.5 million in fixtures). Notice that South Carolina’s effective tax rate on industrial property is over 7.8 times higher than the most industry-friendly state, Delaware. (Delaware is listed in the figure because it is the lowest-tax state.)

Figure 5.8: Industrial Property Taxes in Southeastern states*, 2007 State Rank (of 50) Net Tax Effective Tax Rate

South Carolina 1 $1,864,900 3.73%

Mississippi 4 $1,291,050 2.58%

Texas 6 $1,264,358 2.53%

Tennessee 10 $1,033,544 2.07%

West Virginia 14 $833,234 1.67%

Louisiana 17 $783,407 1.57%

Georgia 20 $760,381 1.52%

Florida 24 $677,683 1.36%

Alabama 35 $533,776 1.11%

North Carolina 37 $491,071 0.98%

Kentucky 47 $327,100 0.65%

Virginia 49 $241,498 0.48%

Delaware 50 $238,840 0.48%

Source: National Association of Manufacturers (2009) * Taxes measured in the states’ largest city only.

Importantly, South Carolina’s effective tax rate is almost 2.5 times greater than Georgia’s tax, and almost 4 times greater than North Carolina’s. This puts South Carolina at a serious disadvantage, in terms of its ability to attract and keep industry. Since South Carolina has the highest tax in the country on industrial property, it should be no surprise that it has one of the lowest per capita incomes and economic growth rates in the country. Although it is probably not critical that South Carolina set its tax rate to the lowest in the country, it should definitely make it at least competitive for the Southeast. Since Georgia’s rate is effectively 1.52 percent and North Carolina’s is just under 1 percent, a rate at around 1 percent might be sufficient to attract more industry. Working to reduce the various taxes applied to industry would seriously improve the state’s competitiveness. Such a significant reduction in taxes on industrial property would obviously lead to a reduction in tax revenues on industrial property, at least initially. However, the overall revenue may in fact increase once the growth rate in the state begins to pick up and more industry moves into the state. Furthermore, if the official tax rates are lowered, then the state

232 CHAPTER 5: SPECIFIC TAX REFORMS

13