Chapter 12 Long-Term Liabilities: Bonds and Notes … 12 Long-Term Liabilities: Bonds and Notes ......

22

Chapter 12 Long-Term Liabilities: Bonds and Notes Study Guide Solutions 1 ©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part. Fill-in-the-Blank Equations 1. A discount 2. Face amount 3. A premium 4. Interest expense Exercises 1. The Garden Supply has two options in financing: issue $3,000,000 of common stock with a $20 par value and $2,000,000 of 10% bonds or issue $2,500,000 of the same common stock and $2,500,000 of the same bonds. All bonds and stock are issued at their par or face amount. If the earnings before interest and income taxes are $750,000 with a 40% tax rate, what would the effect of the two financing options be on the earnings per share? Option 1 Option 2 Common stock, $20 par $3,000,000 $2,500,000 10% bonds 2,000,000 2,500,000 Total $5,000,000 $5,000,000 Earnings before interest & income tax 750,000 750,000 Deduct interest on bonds 200,000 250,000 Income before income tax 550,000 500,000 Deduct income tax 220,000 200,000 Net income 330,000 300,000 Shares of common stock outstanding 150,000 125,000 Earnings per share on common stock $2.20 $2.40

-

Upload

duongxuyen -

Category

Documents

-

view

251 -

download

2

Transcript of Chapter 12 Long-Term Liabilities: Bonds and Notes … 12 Long-Term Liabilities: Bonds and Notes ......

Chapter 12

Long-Term Liabilities: Bonds and Notes

Study Guide Solutions

1 ©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

Fill-in-the-Blank Equations

1. A discount

2. Face amount

3. A premium

4. Interest expense

Exercises

1. The Garden Supply has two options in financing: issue $3,000,000 of common stock with a $20 par value and $2,000,000 of 10% bonds or issue $2,500,000 of the same common stock and $2,500,000 of the same bonds. All bonds and stock are issued at their par or face amount. If the earnings before interest and income taxes are $750,000 with a 40% tax rate, what would the effect of the two financing options be on the earnings per share?

Option 1 Option 2 Common stock, $20 par $3,000,000 $2,500,000 10% bonds 2,000,000 2,500,000 Total $5,000,000 $5,000,000 Earnings before interest & income tax 750,000 750,000 Deduct interest on bonds 200,000 250,000 Income before income tax 550,000 500,000 Deduct income tax 220,000 200,000 Net income 330,000 300,000 Shares of common stock outstanding 150,000 125,000 Earnings per share on common stock $2.20 $2.40

2 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

2. Gifts For All has the financing options below. Assume all bonds and stock are issued at their par or face amount. The company’s earnings before interest and income taxes are $1,900,000 with a 35% tax rate. What would the effect of the financing options be on the earnings per share? Round EPS to two decimal places.

Option 1 Option 2 Option 3 Amount Percent Amount Percent Amount Percent

Issue 15% bonds — $ 5,000,000 50% $ 2,500,000 25%Issue preferred 6% stock, $25 par value —

2,500,000 25% 2,500,000 25%

Issue common stock, $15 par value $10,000,000 100% 2,500,000 25% 5,000,000 50%

$10,000,000 100% $10,000,000 100% $10,000,000 100%

Option 1 Option 2 Option 3 15% bonds — $5,000,000 $2,500,000 Common stock, $15 par $10,000,000 2,500,000 5,000,000 Preferred 6% stock, $25 par — 2,500,000 2,500,000 Total $10,000,000 $10,000,000 $10,000,000 Earnings before interest & income tax 1,900,000 1,900,000 1,900,000 Deduct interest on bonds — 750,000 375,000 Income before income tax 1,900,000 1,150,000 1,525,000 Deduct income tax 665,000 402,500 533,750 Net income 1,235,000 747,500 991,250 Dividends on preferred stock — 150,000 150,000Available for dividends on common stock 1,235,000 597,500 841,250Shares of common stock outstanding 666,667 166,667 333,333 Earnings per share on common stock $1.85 $3.58 $2.52

Option 2 would give the company the highest earnings per share. The option gives the highest tax savings for interest. Although Option 2 generates the lowest net income, less shares of common stock are outstanding to distribute the earnings.

Long-Term Liabilities: Bonds and Notes 3

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

3. AMC Corporation has the financing options below. Assume all bonds and stock are issued at their par or face amount. The company’s earnings before interest and income taxes for the year are $1,500,000 at a 40% tax rate. Which option would generate the highest earnings per share?

Option 1 Option 2 Option 3 Amount Percent Amount Percent Amount Percent

Issue 18% bonds 1,000,000 20% $3,000,000 60% $2,000,000 40%Issue preferred 4% stock, $15 par value 2,500,000 50% 1,000,000 20% 1,500,000 30%Issue common stock, $5 par value $1,500,000 30% 1,000,000 20% 1,500,000 30%

$5,000,000 100% $5,000,000 100% $5,000,000 100%

Option 1 Option 2 Option 3 18% bonds $1,000,000 $3,000,000 $2,000,000 Preferred 4% stock, $15 par 2,500,000 1,000,000 1,500,000 Common stock, $5 par 1,500,000 1,000,000 1,500,000 Total $5,000,000 $5,000,000 $5,000,000 Earnings before interest & income tax 1,500,000 1,500,000 1,500,000 Deduct interest on bonds 180,000 540,000 360,000 Income before income tax 1,320,000 960,000 1,140,000 Deduct income tax 528,000 384,000 456,000 Net income 792,000 576,000 684,000 Dividends on preferred stock 100,000 40,000 60,000 Available for dividends on common stock 692,000 536,000 624,000 Shares of common stock outstanding 300,000 200,000 300,000 Earnings per share on common stock $2.31 $2.68 $2.08

Option 2 would give the highest earnings per share.

Strategy: Earnings per share on common stock should be calculated using earnings after interest and income taxes. First, determine the amount of interest to be paid on any bonds outstanding and subtract this amount from earnings before interest and taxes. Subtract income tax from the income before tax to arrive at net income. If any preferred stock is outstanding, dividends will be first be paid to the preferred shareholders, so subtract the preferred dividends from net income to calculate net income allocable to common shareholders. Divide the net income allocable to common shareholders by the common stock outstanding to arrive at earnings per share on common stock.

4 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

4. Roses Corporation issued a bond with a contract interest rate of 10%. The current market rate of a bond is 9%. Is the bond being issued at a discount, premium, or face amount? Would the selling price be higher or lower than the face amount?

The bond is being issued at a premium, and the selling price would be higher than the face amount.

5. The Garden Supply issued a $1,000,000 bond for $975,000. Would the contract rate be higher or lower than the market rate? Is the bond being issued at a discount, premium, or face amount?

The bond is being issued at a discount, and the contract rate would be lower than the market rate.

6. If The Garden Supply issued a $5,000,000 bond with the same market rate as the contract rate, how much cash would the company receive for the bond? Is the bond being issued at a discount, premium, or face amount?

The company would receive $5,000,000 for the bond because it is being issued at face amount.

Strategy: A bond issued at face amount means that the contract rate is equal to the market rate, so the amount of cash received is equal to the bond payable. If a premium exists, the contract rate is higher than the market rate, so investors are willing to pay more for the bond. However, if the contract rate is lower than the market rate, investors will only want to invest if they have an incentive, such as a discount.

Long-Term Liabilities: Bonds and Notes 5

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

7. The Howling Moon issued $2,500,000 of 5-year, 10% bonds at par value on January 1, 2015. Interest is payable semiannually, on June 30 and December 31. Prepare the journal entries related to the following:

a. Issuance of the bonds

Jan. 1 Cash 2,500,000 Bonds Payable 2,500,000

b. Interest expense on June 30, 2015

June 30 Interest Expense 125,000 Cash 125,000

Interest expense: $2,500,000 × 10% × ½ year

c. Retirement of the bonds

Jan. 1 Bonds Payable 2,500,000 Cash 2,500,000

8. Burns’ Alley issued $1,000,000 of 10-year, 8% bonds at par value on June 30, 2015. The

interest is payable annually, beginning on January 1 of the following year. Prepare the journal entries related to the following:

a. Issuance of the bonds

June 30 Cash 1,000,000 Bonds Payable 1,000,000

b. Interest expense on January 1, 2016

Jan. 1 Interest Expense 80,000 Cash 80,000

Interest expense: $1,000,000 × 8%

c. Retirement of the bonds

June 30 Bonds Payable 1,000,000 Cash 1,000,000

6 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

9. RPC Corporation issued $4,000,000 of 2-year, 12% bonds at par value on September 30, 2015. The interest is payable every quarter, starting on December 31, 2015. Prepare the journal entries for the following:

a. Issuance of the bonds

Sept. 30 Cash 4,000,000 Bonds Payable 4,000,000

b. Interest expense on January 1, 2016

Jan. 1 Interest Expense 120,000 Cash 120,000

Interest expense: $4,000,000 × 12% × ¼ year

c. Retirement of the bonds

Sept. 30 Bonds Payable 4,000,000 Cash 4,000,000

Strategy: When bonds are issued at par, the cash received is equal to the face amount of the bond, so a premium or discount will not be recorded and amortized. The interest expense is equal to the contract rate multiplied by the face amount of the bond.

Long-Term Liabilities: Bonds and Notes 7

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

10. Shem Creek issued $200,000 of 5-year, 9% bonds for $192,298 on January 1, 2015. The interest is payable semiannually on June 30 and December 31, beginning on June 30, 2015. The market rate at the time of issuance is 10%. Calculate the amount of interest expense and amortization of the discount recorded for the first fiscal year ending December 31, 2015 using:

a. Straight-line method for amortization

Discount on bonds payable $7,702 Term of bonds 5 years Semiannual amortization ($7,702/10 periods) $770.20

Interest expense: ($9,000 + $770.20) × 2 periods = $19,540.40

Amortization of discount: $770.20 × 2 periods = $1,540.40

b. Effective interest method for amortization

Payment Date

Int. Paid (Face × 9% × ½)

Int. Exp. (Carrying value × 10% ×½)

Disc. Amortization (Int. Exp. – Int. Paid)

Unamortized Disc.

Bond Carrying Value

$7,702.00 $192,298.00 June 30 $9,000 $9,614.90 $614.90 7,087.10 192,912.90 Dec. 31 9,000 9,645.60 645.60 6,441.50 193,558.50

Interest expense: $9,614.90 + $9,645.60 = $19,260.50

Amortization of discount: $614.90 + $645.60 = $1,260.50

11. Prepare the journal entries for the issuance, interest payments for the first year, and retirement of the bonds for Shem Creek using the information in Exercise 10. Assume the company uses the effective interest method to amortize the bond discount.

Issuance Jan. 1 Cash 192,298.00 Discount on Bonds Payable 7,702.00 Bonds Payable 200,000.00Int. Payment June 30 Interest Expense 9,614.90 Discount on Bonds Payable 614.90 Cash 9,000.00Int. Payment Dec. 31 Interest Expense 9,645.60 Discount on Bonds Payable 645.60 Cash 9,000.00Retirement Jan. 1 Bonds Payable 200,000.00 Cash 200,000.00

8 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

12. Cooper River Corporation issued $1,000,000 of 5-year, 8% bonds for $922,780 at the beginning of its fiscal year on July 1, 2015, when the market rate is 10%. The interest is payable semiannually, beginning December 31, 2015. Calculate the interest expense and discount amortization for the first fiscal year using:

a. Straight-line method for amortization

Discount on bonds payable $77,220 Term of bonds 5 years Semiannual amortization ($77,220 / 10 periods) $7,722

Interest expense: ($7,722 + $40,000) × 2 periods = $95,444

Amortization of discount: $7,722 × 2 periods = $15,444

b. Effective interest method for amortization (round answers to the nearest dollar)

Payment Date

Int. Paid (Face × 8% × ½)

Int. Exp. (Carrying value × 10% ×½)

Disc. Amortization (Int. Exp. – Int. Paid)

Unamortized Disc.

Bond Carrying Value

$77,220.00 $922,780.00 Dec. 31 $40,000 $46,139.00 $6,139.00 71,081.00 928,919.00 June 30 40,000 46,445.95 6,445.95 64,635.05 935,364.95

Interest expense: $46,139.00 + $46,445.95 = $92,584.95

Amortization of discount: $6,139.00 + $6,445.95 = $12,584.95

13. Prepare the journal entries required for the issuance, interest payments for the first year, and retirement of the bonds for Cooper River Corporation using the information in Exercise 12. Assume the company accounts for the bond discount using the straight-line method.

Issuance July 1 Cash 922,780 Discount on Bonds Payable 77,220 Bonds Payable 1,000,000Int. Payment Dec. 31 Interest Expense 47,722 Discount on Bonds Payable 7,722 Cash 40,000Int. Payment June 30 Interest Expense 47,722 Discount on Bonds Payable 7,722 Cash 40,000Retirement July 1 Bonds Payable 1,000,000 Cash 1,000,000

Long-Term Liabilities: Bonds and Notes 9

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

14. On January 1, 2015, Terese Corporation issued $2,000,000 of 3-year, 13% bonds for $1,952,334.20. Interest on the bonds is payable semiannually, on June 30 and December 31. On the date of issuance, the market rate of bonds was 14%. Calculate the interest expense and bond amortization for the first fiscal year using:

a. Straight-line method for amortization

Discount on bonds payable $47,665.80 Term of bonds 3 years Semiannual amortization ($47,665.80/6 periods) $7,944.30

Interest expense: ($7,944.30 + $130,000) × 2 periods = $275,888.60

Amortization of discount: $7,944.30 × 2 periods = $15,888.60

b. Effective interest method for amortization

Payment Date

Int. Paid (Face × 13% × ½)

Int. Exp. (Carrying value × 14% ×½)

Disc. Amortization (Int. Exp. – Int. Paid)

Unamortized Disc.

Bond Carrying Value

$47,665.80 $1,952,334.20 June 30 $130,000 $136,663.39 $6,663.39 41,002.41 1,958,997.59 Dec. 31 130,000 137,129.83 7,129.83 33,872.58 1,966,127.42

Interest expense: $136,663.39 + $137,129.83 = $273,793.22

Amortization of discount: $6,663.39 + $7,129.83 = $13,793.22

Strategy: If a bond is issued at a discount, the investors are essentially receiving interest for not paying the full amount of the bond, so the amortization of the discount should be added to the interest paid by the corporation to calculate the interest expense. The amount of interest expense and discount amortization depends upon the method used, with straight line giving the same interest expense every period, and the effective interest method varying over time.

10 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

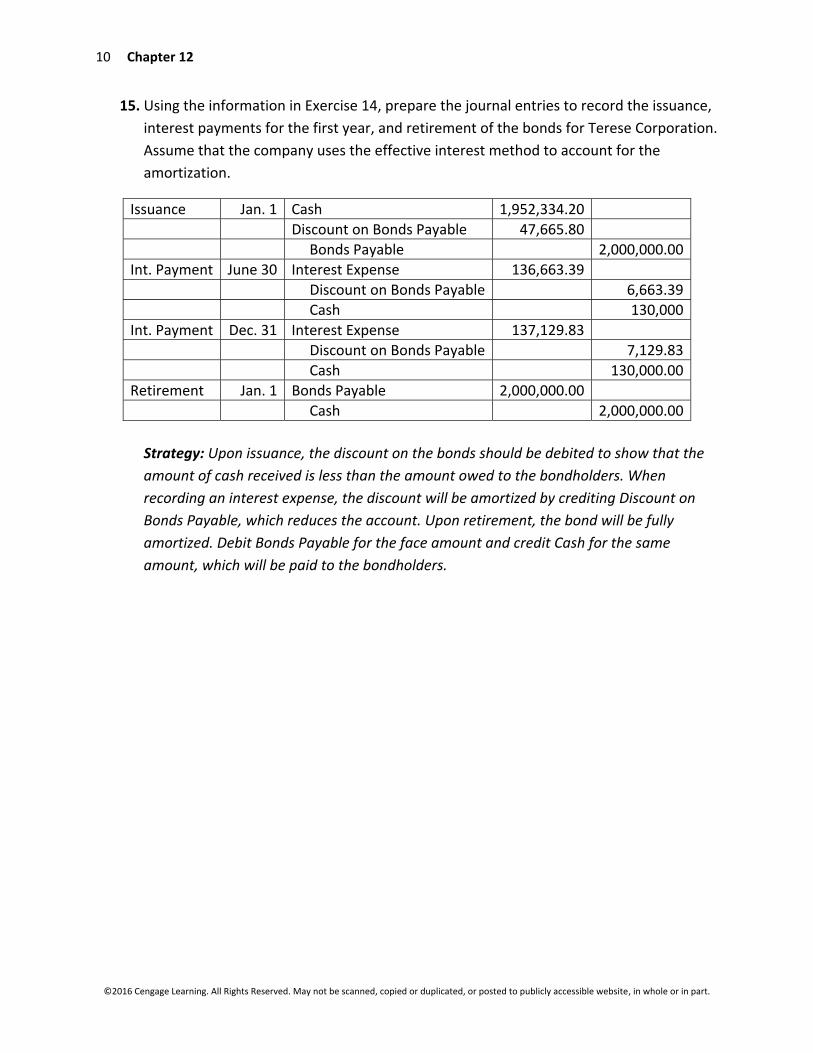

15. Using the information in Exercise 14, prepare the journal entries to record the issuance, interest payments for the first year, and retirement of the bonds for Terese Corporation. Assume that the company uses the effective interest method to account for the amortization.

Issuance Jan. 1 Cash 1,952,334.20 Discount on Bonds Payable 47,665.80 Bonds Payable 2,000,000.00Int. Payment June 30 Interest Expense 136,663.39 Discount on Bonds Payable 6,663.39 Cash 130,000Int. Payment Dec. 31 Interest Expense 137,129.83 Discount on Bonds Payable 7,129.83 Cash 130,000.00Retirement Jan. 1 Bonds Payable 2,000,000.00 Cash 2,000,000.00

Strategy: Upon issuance, the discount on the bonds should be debited to show that the amount of cash received is less than the amount owed to the bondholders. When recording an interest expense, the discount will be amortized by crediting Discount on Bonds Payable, which reduces the account. Upon retirement, the bond will be fully amortized. Debit Bonds Payable for the face amount and credit Cash for the same amount, which will be paid to the bondholders.

Long-Term Liabilities: Bonds and Notes 11

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

16. Trends Inc. issued $1,000,000 of 5-year, 9% bonds on January 1, 2015, for $1,041,000. The bonds will pay interest semiannually, beginning on June 30, 2015. The market rate at the date of issuance was 8%. Calculate the interest expense and bond amortization for the first fiscal year using:

a. Straight-line method for amortization

Premium on bonds payable $41,000 Term of bonds 5 years Semiannual amortization ($41,000/10 periods) $4,100

Interest expense: ($45,000 - $4,100) × 2 periods = $81,800

Amortization of premium: $4,100 × 2 periods = $8,200

b. Effective interest method for amortization

Payment Date

Int. Paid (Face × 9% × ½)

Int. Exp. (Carrying value × 8% ×½)

Prem. Amortization (Int. Paid – Int. Exp.)

Unamortized Prem.

Bond Carrying Value

$41,000.00 $1,041,000.00 June 30 $45,000 $41,640.00 $3,360.00 37,640.00 1,037,640.00 Dec. 31 45,000 41,505.60 3,494.40 34,145.60 1,034,145.60

Interest expense: $41,640 + $41,505.60 = $83,145.60

Amortization of premium: $3,360 + $3,494.40 = $6,854.40

17. Using the information in Exercise 16, prepare the journal entries to record the issuance, interest payments for the first year, and retirement of the bonds for Trends Inc. Assume that the company uses the effective interest method to account for the amortization.

Issuance Jan. 1 Cash 1,041,000.00 Premium on Bonds Payable 41,000.00 Bonds Payable 1,000,000.00Int. Payment June 30 Interest Expense 41,640.00 Premium on Bonds Payable 3,360.00 Cash 45,000.00Int. Payment Dec. 31 Interest Expense 41,505.60 Premium on Bonds Payable 3,494.40 Cash 45,000.00Retirement Jan. 1 Bonds Payable 1,000,000.00 Cash 1,000,000.00

12 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

18. Fast Tires issued $5,000,000 of 5-year, 10% bonds on June 30, 2015, for $5,405,550. The bonds pay interest quarterly, beginning September 30, 2015. At the date of issuance, the market rate was 8%. Calculate the interest expense and bond amortization for the first fiscal year using:

a. Straight-line method for amortization

Premium on bonds payable $405,550 Term of bonds 5 years Quarterly amortization ($405,550/20 periods) $20,277.50

Interest expense: ($125,000 – $20,277.50) × 4 periods = $418,890

Amortization of premium: $20,277.50 × 4 periods = $81,110

b. Effective interest method for amortization

Payment Date

Int. Paid (Face × 10% × ¼)

Int. Exp. (Carrying value × 8% ×¼)

Prem. Amortization (Int. Paid – Int. Exp.)

Unamortized Prem.

Bond Carrying Value

$405,550.00 $5,405,550.00Sept. 30 $125,000 $108,111.00 $16,889.00 388,661.00 5,388,661.00

Dec. 31 125,000 107,773.22 17,226.78 371,434.22 5,371,434.22Mar. 31 125,000 107,428.68 17,571.32 353,862.90 5,353,862.90June 30 125,000 107,077.26 17,922.74 335,940.16 5,335,940.16

Interest expense: $108,111 + $107,773.22 + $107,428.68 + $107,077.26 = $430,390.16

Amortization of premium: $16,889.00 + $17,226.78 + $17,571.32 + $17,922.74 = $69,609.84

19. Use the information in Exercise 18 to prepare the journal entries to record the issuance, first interest payment, and retirement of the bonds for Fast Tires. Assume the company uses the straight-line method for amortization.

Issuance June 30 Cash 5,405,550 Premium on Bonds Payable 405,550 Bonds Payable 5,000,000Int. Payment Sept. 30 Interest Expense 104,722.50 Premium on Bonds Payable 20,277.50 Cash 125,000Retirement June 30 Bonds Payable 5,000,000 Cash 5,000,000

Long-Term Liabilities: Bonds and Notes 13

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

20. Tortoise Cleaning Corp. issued $250,000 of 5-year, 7% bonds payable for $271,880 on January 1, 2015. The bonds will pay interest semiannually, beginning on June 30, 2015. At the time of issuance, the market rate was 5%. Calculate the interest expense and bond amortization for the first year using:

a. Straight-line method for amortization

Premium on bonds payable $21,880 Term of bonds 5 years Semiannual amortization ($21,880/10 periods) $2,188

Interest expense: ($8,750 – $2,188) × 2 periods = $13,124

Amortization of premium: $2,188 × 2 periods = $4,376

b. Effective interest method for amortization

Payment Date

Int. Paid (Face × 7% × ½)

Int. Exp. (Carrying value × 5% ×½)

Prem. Amortization (Int. Paid – Int. Exp.)

Unamortized Prem.

Bond Carrying Value

$21,880.00 $271,880.00June 30 $8,750 $6,797.00 $1,953.00 19,927.00 269,927.00Dec. 31 8,750 6,748.18 2,001.82 17,925.18 267,925.18

Strategy: If a bond is issued at a premium, the corporation will have to pay more in interest than the market rate. The amortization of the premium should be subtracted from the interest paid to calculate interest expense for the period.

21. Use the information in Exercise 20 to prepare the journal entries to record the issuance, first interest payment, and retirement of the bonds for Tortoise Cleaning Corp., assuming the company uses the straight-line method for amortization.

Issuance Jan. 1 Cash 271,880 Premium on Bonds Payable 21,880 Bonds Payable 250,000 Int. Payment June 30 Interest Expense 6,562 Premium on Bonds Payable 2,188 Cash 8,750 Retirement Jan. 1 Bonds Payable 250,000 Cash 250,000

14 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

Strategy: When recording the issuance of a bond at a premium, credit Premium on Bonds Payable to show that the corporation received more cash than will be paid back at retirement. Over time the premium will be amortized, which should be recorded by debiting Premium on Bonds Payable. At the time of retirement, the premium will be fully amortized. Debit Bonds payable for the face amount and credit Cash for the same amount, which is also the amount paid to the investors.

22. On March 31, 2015, RPC Corporation redeems ½ of the outstanding bonds payable for $62,500. The total bonds outstanding had a face amount of $120,000 and an unamortized premium of $7,500. Prepare the journal entry to record the redemption.

Mar. 31 Bonds Payable 60,000 Premium on Bonds Payable 3,750 Gain on Redemption of Bonds 1,250 Cash 62,500

23. Apple Tree Corp. redeemed ¼ of the outstanding bonds payable for $90,000 on May 5, 2015. The total bonds outstanding had a face amount of $400,000 and an unamortized bond discount of $16,000. Prepare the journal entry to record the redemption.

May 5 Bonds Payable 100,000 Gain on Redemption of Bonds 6,000 Discount on Bonds Payable 4,000 Cash 90,000

24. On July 15, 2015, a corporation redeems ½ of its outstanding bonds payable for $24,000. The total bonds outstanding had a face amount of $50,000 and an unamortized bond discount of $2,200. Prepare the journal entry to record the redemption.

July 15 Bonds Payable 25,000 Loss on Redemption of Bonds 100 Discount on Bonds Payable 1,100 Cash 24,000

Strategy: When a bond is redeemed prior to retirement, the unamortized discount or premium related to the bond redeemed also needs to be taken off the books. A discount will be removed with a credit, while a premium will be removed with a debit. Debit Bonds Payable to remove the liability from the books using a debit for the face amount. Credit Cash for the amount paid. Any difference in the cash paid and the bond’s carrying value creates a loss or gain on the redemption. Record losses using a debit and gains using a credit.

Long-Term Liabilities: Bonds and Notes 15

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

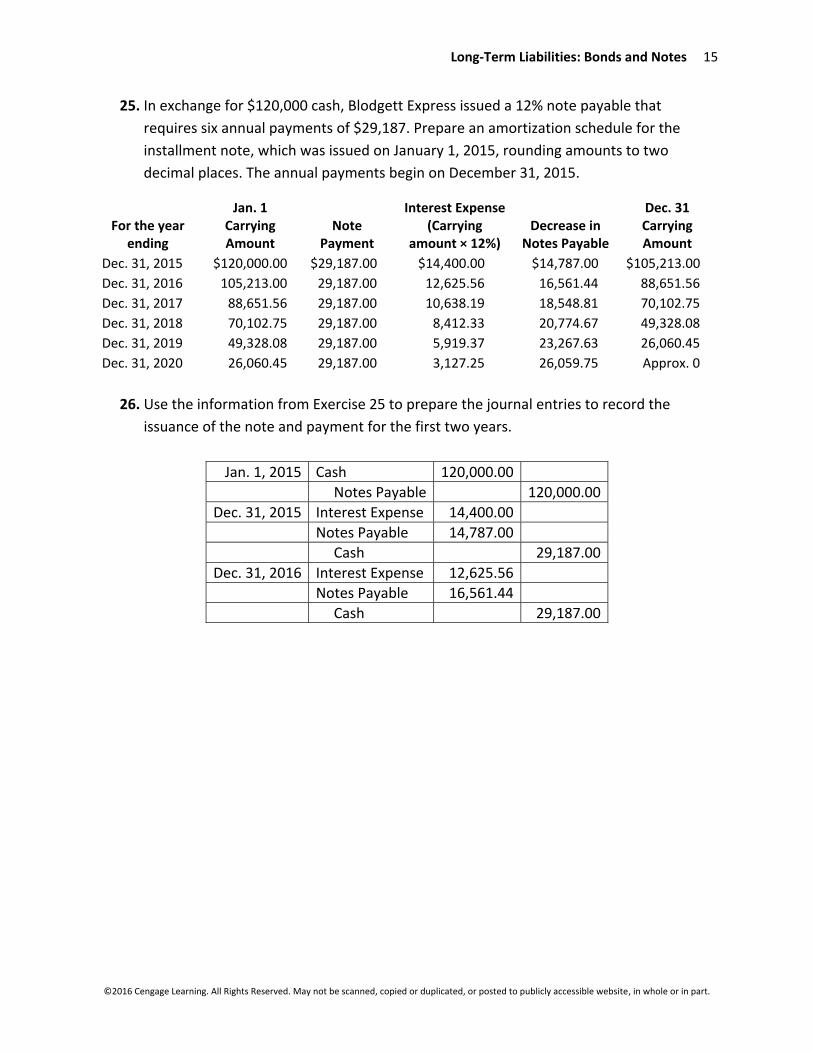

25. In exchange for $120,000 cash, Blodgett Express issued a 12% note payable that requires six annual payments of $29,187. Prepare an amortization schedule for the installment note, which was issued on January 1, 2015, rounding amounts to two decimal places. The annual payments begin on December 31, 2015.

For the year ending

Jan. 1 Carrying Amount

Note Payment

Interest Expense (Carrying

amount × 12%) Decrease in

Notes Payable

Dec. 31 Carrying Amount

Dec. 31, 2015 $120,000.00 $29,187.00 $14,400.00 $14,787.00 $105,213.00 Dec. 31, 2016 105,213.00 29,187.00 12,625.56 16,561.44 88,651.56 Dec. 31, 2017 88,651.56 29,187.00 10,638.19 18,548.81 70,102.75 Dec. 31, 2018 70,102.75 29,187.00 8,412.33 20,774.67 49,328.08 Dec. 31, 2019 49,328.08 29,187.00 5,919.37 23,267.63 26,060.45 Dec. 31, 2020 26,060.45 29,187.00 3,127.25 26,059.75 Approx. 0

26. Use the information from Exercise 25 to prepare the journal entries to record the

issuance of the note and payment for the first two years.

Jan. 1, 2015 Cash 120,000.00 Notes Payable 120,000.00

Dec. 31, 2015 Interest Expense 14,400.00 Notes Payable 14,787.00 Cash 29,187.00

Dec. 31, 2016 Interest Expense 12,625.56 Notes Payable 16,561.44 Cash 29,187.00

16 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

27. A corporation issues a 12% installment note for $500,000 cash on the beginning of its fiscal year, April 1, 2015. The note requires 10 semiannual payments of $67,934 every September 30 and March 31, which begin the same year. Prepare an amortization schedule for the installment note. Round amounts to two decimal places.

For the period ending

April 1 Carrying Amount

Note Payment

Interest Expense (Carrying amount

× 12% × ½) Decrease in

Notes Payable

Mar. 31 Carrying Amount

Sept. 30, 2015 $500,000.00 67,934.00 $30,000.00 $37,934.00 $462,066.00 Mar. 31, 2016 462,066.00 67,934.00 $27,723.96 40,210.04 421,855.96 Sept. 30, 2016 421,855.96 67,934.00 25,311.36 42,622.64 379,233.32 Mar. 31, 2017 379,233.32 67,934.00 22,754.00 45,180.00 334,053.32 Sept. 30, 2017 334,053.32 67,934.00 20,043.20 47,890.80 286,162.52 Mar. 31, 2018 286,162.52 67,934.00 17,169.75 50,764.25 235,398.27 Sept. 30, 2018 235,398.27 67,934.00 14,123.90 53,810.10 181,588.16 Mar. 31, 2019 181,588.16 67,934.00 10,895.29 57,038.71 124,549.45 Sept. 30, 2019 124,549.45 67,934.00 7,472.97 60,461.03 64,088.42 Mar. 31, 2020 64,088.42 67,934.00 3,845.31 64,088.69 Approx. 0

28. Use the information from Exercise 27 to prepare the journal entries required for the

installment note over the first fiscal year.

April 1, 2015 Cash 500,000.00 Notes Payable 500,000.00

Sept. 30, 2015 Interest Expense 30,000.00 Notes Payable 37,934.00 Cash 67,934.00

Mar. 31, 2016 Interest Expense 27,723.96 Notes Payable 40,210.04 Cash 67,934.00

Long-Term Liabilities: Bonds and Notes 17

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

29. On January 1, 2015, Allen Ales issued a 6% installment note for $100,000 in cash. The note requires five annual payments of $23,739.64, which are due beginning December 31, 2015. Prepare an amortization schedule for the installment note. Round amounts to two decimal places.

For the year ending

Jan. 1 Carrying Amount Note Payment

Interest Expense (Carrying amount

× 6%)

Decrease in Notes

Payable

Dec. 31 Carrying Amount

Dec. 31, 2015 $100,000.00 $23,739.64 $6,000.00 $17,739.64 $82,260.36 Dec. 31, 2016 82,260.36 23,739.64 4,935.62 18,804.02 63,456.34 Dec. 31, 2017 63,456.34 23,739.64 3,807.38 19,932.26 43,524.08 Dec. 31, 2018 43,524.08 23,739.64 2,611.44 21,128.20 22,395.89 Dec. 31, 2019 22,395.89 23,739.64 1,343.75 22,395.89 0

Strategy: An amortization schedule shows in detail the amount of interest expense and decrease in principal of the note that should be recorded each period. The note payment remains constant over the life of the note, but interest expense changes, which also changes the amount of principal paid each period. Interest Expense is calculated by multiplying the contract rate by the carrying amount at the beginning of the period. The difference between the note payment and payment of interest is the amount of principal paid.

30. Using the information from Exercise 29, prepare the journal entries required for the installment note during the 2015 fiscal year.

Jan. 1 Cash 100,000.00 Notes Payable 100,000.00

Dec. 31 Interest Expense 6,000.00 Notes Payable 17,739.64 Cash 23,739.64

Strategy: When issuing an installment note, debit Cash for the amount received, which is also the same amount of the note payable to record (credit to increase the account). An annual payment includes payment of the principal and interest, so Interest Expense and Notes Payable should both be debited to record the payment of interest and reduction in the liability.

18 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

31. A corporation currently has $1,500,000 of 5% bonds outstanding and $5,000,000 of installment notes payable. The company makes semiannual payments of $129,000 on the note ($24,000 of which will be related to interest in the upcoming year). Ignoring any other liabilities, how much of current and long-term liabilities will the corporation’s balance sheet present?

Current liabilities: Interest payable $ 99,000 Notes payable, current portion 105,000 Total current liabilities $ 204,000 Long-term liabilities: Bonds payable $1,500,000 Notes payable 4,895,000 Total long-term liabilities $6,395,000

Interest payable: $24,000 + (5% × $1,500,000)

Notes payable, current portion: $129,000 – $24,000

Notes payable: $5,000,000 – $105,000

Long-Term Liabilities: Bonds and Notes 19

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

32. In addition to the Accounts Payable of $125,000, RPC Corporation has the following liabilities as of December 31, 2015: Notes Payable, $750,000 and 10% Bonds Payable, $2,000,000. The company’s bonds have an unamortized discount of $134,000 and the notes payable has a payment of $100,000 due in the upcoming January, $21,000 of which will be for interest in the upcoming year. Ignoring any other liabilities the company may have, prepare the liabilities portion of the balance sheet.

RPC Corporation Balance Sheet

As of December 31, 2015 Current liabilities: Accounts payable $ 125,000 Interest payable 221,000 Notes payable, current portion 79,000 Total current liabilities $425,000 Long-term liabilities: Bonds payable, 10% $2,000,000 Less unamortized discount 134,000 $1,866,000 Notes payable 671,000 Total long-term liabilities $2,537,000 Total liabilities $2,962,000

Interest payable: $21,000 + (10% × $2,000,000)

Notes payable, current portion: $100,000 – $21,000

Notes payable: $750,000 – $79,000

20 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

33. Shem Creek has the following liabilities outstanding: Notes Payable, $6,700,000; 7.5% Bonds Payable, $3,100,000; and Accounts Payable, $150,000. The installment note requires quarterly payments of $41,000 every year, $36,000 of which will be for interest payments for the upcoming year. The bond also has an unamortized premium of $400,000. Ignoring any other liabilities Shem Creek may have, prepare the liabilities portion of the balance sheet for the 2015 calendar year-end.

Shem Creek Balance Sheet

As of December 31, 2015 Current liabilities: Accounts payable $ 150,000 Interest payable 268,500 Notes payable, current portion 128,000 Total current liabilities $ 546,500 Long-term liabilities: Bonds payable, 10% $3,100,000 Plus unamortized premium 400,000 $ 3,500,000 Notes payable 6,572,000 Total long-term liabilities $10,072,000 Total liabilities $10,618,500

Interest payable: $36,000 + (7.5% × $3,100,000)

Notes payable, current portion: ($41,000 × 4 periods) - $36,000

Notes payable: $6,700,000 – $128,000

Strategy: Current liabilities include liabilities that will be paid within the upcoming business cycle. Any current portion of installment notes, interest on the installment notes, and interest on bonds payable should be recorded as a current liability. Bonds should be recorded as long-term liabilities, unless due within the upcoming business cycle, at their carrying amount.

Long-Term Liabilities: Bonds and Notes 21

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

34. Use the information below to determine a corporation’s number of times interest charges are earned for 2015 and 2016. Determine if the change is favorable or unfavorable. Round answers to two decimal places.

2016 2015 Interest expense $38,750 $35,450 Income before income tax expense 326,900 320,875 Number of times interest charges are earned 9.44 10.05

The decrease in number of times interest charges are earned is unfavorable because the debt holders are less confident they will receive interest payments

35. Assume the interest on the bonds listed below will be Cooper River’s only interest expense for 2015 and 2016. Calculate the company’s number of times interest charges are earned ratio for the two years and determine if the change is favorable or unfavorable. Round answers to two decimal places.

2016 2015 10% Bonds $1,300,000 $1,200,000 Income before income tax expense 1,025,000 920,000 Interest expense (Bonds outstanding × 10%) 130,000 120,000 Number of times interest charges are earned 8.88 8.67

The increase in number of times interest charges are earned is a favorable trend.

22 Chapter 12

©2016 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to publicly accessible website, in whole or in part.

36. Using the information below, calculate the number of times interest charges are earned in 2015 and 2016 for Tortoise Cleaning Corporation. Assume the interest paid on the bond will be the only interest expense for both years and the company is subject to a 40% tax rate. How many times in each year will the corporation be able to cover its interest payments? Round answers to two decimal places.

2016 2015 8% Bonds $5,270,000 $5,000,000 Net income 525,000 450,000 Interest expense (Bonds outstanding × 8%) 421,600 400,000 Income before income tax expense [Net income/(1 – 40%)] 875,000 750,000 Number of times interest charges are earned 3.08 2.88 In 2015, the corporation earned enough income to pay its interest expense 2.88 times. The number of times it could pay interest increased to 3.08 in 2016.

Strategy: To find the number of times interest charges are earned, first determine the income before tax expense and interest expense. Add the two and divide the sum by the interest expense. Investors prefer a higher ratio because it indicates the company has a higher ability to pay its interest.