Chapter 12lbacon/chap9.doc · Web view · 2002-03-28Chapter 9. Foreign currency ... Foreign...

52

CHAPTER 9 FOREIGN CURRENCY TRANSACTIONS AND HEDGING FOREIGN EXCHANGE RISK ANSWERS TO QUESTIONS 1. Under the two transaction perspective, an export sale (import purchase) and the subsequent collection (payment) of cash are treated as two separate transactions to be accounted for separately. The idea is that management has made two decisions: (1) to make the export sale, and (2) to extend credit in foreign currency to the foreign customer. The income effect from each of these decision should be reported separately. 2. Foreign currency receivables resulting from export sales are revalued at the end of accounting periods using the current spot rate. An increase in the value of a receivable will be offset by reporting a foreign exchange gain in income, and a decrease will be offset by a foreign exchange loss. Foreign exchange gains and losses are accrued even though they have not yet been realized. 3. Foreign exchange gains and losses are created by two factors: having foreign currency exposures (foreign currency receivables and payables) and changes in exchange rates. Appreciation of the foreign currency will generate foreign exchange gains on receivables and foreign exchange losses on payables. Depreciation of the foreign currency will generate foreign exchange losses on receivables and foreign exchange gains on payables. 4. Hedging is the process of eliminating exposure to foreign exchange risk so as to avoid potential losses from fluctuations in exchange rates. Hedging involves creating balanced positions (assets equal to liabilities) in individual foreign currencies. In addition to avoiding possible losses, companies hedge foreign currency transactions and commitments so as to introduce an element of certainty into the future cash flows resulting from foreign currency activities. 5. A forward exchange contract is an agreement between two parties to exchange at a future date currencies of different countries at an established rate (called the forward rate). Each party will Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-1

Transcript of Chapter 12lbacon/chap9.doc · Web view · 2002-03-28Chapter 9. Foreign currency ... Foreign...

CHAPTER 9FOREIGN CURRENCY TRANSACTIONS AND

HEDGING FOREIGN EXCHANGE RISK

ANSWERS TO QUESTIONS

1. Under the two transaction perspective, an export sale (import purchase) and the subsequent collection (payment) of cash are treated as two separate transactions to be accounted for separately. The idea is that management has made two decisions: (1) to make the export sale, and (2) to extend credit in foreign currency to the foreign customer. The income effect from each of these decision should be reported separately.

2. Foreign currency receivables resulting from export sales are revalued at the end of accounting periods using the current spot rate. An increase in the value of a receivable will be offset by reporting a foreign exchange gain in income, and a decrease will be offset by a foreign exchange loss. Foreign exchange gains and losses are accrued even though they have not yet been realized.

3. Foreign exchange gains and losses are created by two factors: having foreign currency exposures (foreign currency receivables and payables) and changes in exchange rates. Appreciation of the foreign currency will generate foreign exchange gains on receivables and foreign exchange losses on payables. Depreciation of the foreign currency will generate foreign exchange losses on receivables and foreign exchange gains on payables.

4. Hedging is the process of eliminating exposure to foreign exchange risk so as to avoid potential losses from fluctuations in exchange rates. Hedging involves creating balanced positions (assets equal to liabilities) in individual foreign currencies. In addition to avoiding possible losses, companies hedge foreign currency transactions and commitments so as to introduce an element of certainty into the future cash flows resulting from foreign currency activities.

5. A forward exchange contract is an agreement between two parties to exchange at a future date currencies of different countries at an established rate (called the forward rate). Each party will deliver a set amount of one currency as payment for a set amount of a different currency.

6. A forward contract may be established for one of several reasons:a. A company may want to eliminate exposure to the possible incurrence of a loss on a

foreign currency transaction that has already taken place. b. A company may want to eliminate exposure to the possible loss that can occur as a

result of the exchange rate changing between the time a purchase or sale commitment is made and the date that it is consummated.

c. A contract can be acquired as an investment for speculation purposes if the value of the currency is expected to change in an amount or direction different from what is anticipated by the forward rate.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-1

7. SFAS 133 requires an enterprise to recognize all derivative financial instruments as assets or liabilities on the balance sheet and measure them at fair value.

8. The fair value of a foreign currency forward contract generally is zero at the date it is entered into. After the inception date, the fair value of a forward contract is determined by reference to the new forward rate for a contract which extends to the maturity date of the forward contract actually entered into. The difference between the number of dollars that will be received (paid) under the actual forward contract and the number of dollars that could be received (paid) under a forward contract entered into currently is the current fair value of the actual forward contract. The fair value of a forward contract can be positive, in which case an asset and a gain are recognized, or negative, in which case a liability and a loss are recognized. A change in fair value which increases (decreases) the forward contract asset or decreases (increases) the forward contract liability is recognized as a gain (loss) on forward contract.

9. The economic benefit from a hedge is not accounted for separately. It is buried in the net gain or loss which measures the cash flow impact of giving or accepting foreign currency credit.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-2 Solutions Manual

10. In a hedge of a transaction, foreign exchange gains and losses related to the transaction and gains and losses on the forward contract are recognized independently from one another. In other words, hedge accounting is not applied. The net result is that the sale or purchase is recognized at the spot rate at the date of the transaction and the premium or discount on the forward contract is recognized as a net gain or loss.

In a hedge of a commitment, gains and losses on the forward contract are reported and offset by gains and losses on the firm commitment to receive or pay foreign currency, i.e., hedge accounting applies. The firm commitment account is closed as an adjustment to the transaction when it takes place. The net result is that the sale or purchase is measured at the forward rate, with zero net gain or loss.

11. The imported machinery will be carried on Casper’s books at the net cash outflow associated with its acquisition. This will be based upon the forward exchange rate.

12. Under SFAS 133, all foreign currency forward contracts are recognized as assets or liabilities and measured at their fair value. The major difference between a speculative forward contract and a hedge of commitment is that with a speculative forward contract, there is no gain or loss on firm commitment which offsets the gain or loss on forward contract.

13. The holder of a foreign currency put option has the right but not the obligation to sell foreign currency at a predetermined price (strike price) at a specified future date or period of time.

14. A party to a foreign currency forward contract is obligated to deliver one currency in exchange for another at a specified future date, whereas the owner of a foreign currency option can choose whether or not to deliver one currency in exchange for another.

15. Foreign currency options have an advantage over forward contracts in that the holder of the option can choose not to exercise if the future spot rate turns out to be more advantageous. Forward contracts, on the other hand, can lock a company into an unnecessary loss (or a reduced gain). The disadvantage associated with foreign currency options is that a premium must be paid up front even though the option might never be exercised.

16. The premium on a foreign currency option should be accounted for as an asset (deferred charge) and amortized to expense over the life of the option.

17. Hedge accounting is defined as recognition of gains and losses on the hedging instrument in the same period as the recognition of gains and losses on the underlying hedged asset or liability (or firm commitment). The objective of hedge accounting is to report a net foreign exchange gain or loss of zero.

18. In accounting for a fair value hedge, the change in the fair value of the foreign currency option is reported as a gain or loss in net income, offset by a loss or gain on the related firm commitment. The net gain or loss reported in income is zero.

In accounting for a cash flow hedge, changes in the fair value of the option are reported in

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-3

other comprehensive income. There is no gain or loss on a firm commitment to offset against it. The amount accumulated in other comprehensive income is then transferred to net income at the date when the transaction was originally expected to occur.

19. The accounting for a foreign currency borrowing involves keeping track of two foreign currency payables--the note payable and interest payable. As both the face value of the borrowing and accrued interest represent foreign currency liabilities, both are exposed to foreign exchange risk and can give rise to foreign currency gains and losses.

ANSWERS TO INTERNET ASSIGNMENTS

Internet Assignment 1

This assignment asks students to determine whether the foreign currency hedging instruments discussed in the chapter are used by companies and see how the results of accounting for foreign currency activities are reflected in the financial statements. The answers to the questions might change over time as foreign currency exposures change, companies change the way in which they use foreign currency derivatives, or companies change the disclosures related to them. The following is based on the 1998 annual reports of these three companies and indicates in what parts of the annual report the answers to these questions might be found. (Note that some items of information might be repeated in more than one place in the annual report, e.g., MD&A and notes).

Federal Mogul1. Forward contracts--primarily British pounds and South African rand (Note 10).2. No; the Company does not hold or issue derivative financial instruments for trading (i.e.,

speculative) purposes (Note 10).3. Not specifically; however, page 24, “Foreign Currency Risk” describes forward contracts in

British pounds and South African rand (Management Discussion and Analysis).4. Yes; there are two items on the income statement--International currency exchange losses

and Net (gain) loss on British pound currency option and forward contract (Income Statement).

Ford Motor Company1. Forward contracts, options, and swaps (Note 1, Accounting Policies--Derivative Financial

Instruments).2. No; "company policy specifically prohibits the use of derivatives for speculative purposes"

(Note 1, Accounting Policies--Derivative Financial Instruments).3. Yes; British pound, Japanese yen, euro, Mexican peso, and Brazilian real (Note 1,

Accounting Policies--Derivative Financial Instruments). 4. Ford does not separately disclose the aggregate amount of foreign exchange gains/losses.

General Motors Corporation1. Forward contracts and options (Note 11, Derivative Financial Instruments and Risk

Management).2. GM does not discuss the speculative use of derivatives in its annual report; therefore, it

might be logical assume that the company does not speculate.3. Canada, Mexico, Western European countries, Australia, Japan, and Brazil (Note 11).

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-4 Solutions Manual

4. Note 11 discloses amounts of deferred foreign exchange gains and losses, but not the amount reported in income, and there is no separate line item related to foreign exchange gains/losses on the income statement.

Instructors might wish to add additional questions to this assignment. For example, questions could be asked regarding the relative importance of the various types of financial instruments used to hedge foreign exchange risk. Also, other companies could be added to or substituted for the three companies included in this assignment.

Internet Assignment 2 The major objectives of this assignment are to show students how exchange rates can fluctuate over a short period of time, and to force them to analyze the impact these fluctuations would have on the dollar value of a foreign currency account receivable. Answers to the questions will depend upon the period of time for which exchange rates are being tracked. Instructors using this assignment will need to tell the students what the starting and ending (one week later) dates are, and will need to solve the assignment along with the students. The following general rules (based on direct quotes, i.e., U.S. $ per unit of foreign currency) apply in solving the assignment:

second spot rate > first spot rate, currency has strengthened; second spot rate < first spot rate, currency has weakened; stronger currency + account receivable = foreign exchange gain; weaker currency + account receivable = foreign exchange loss.

If a currency does not change in value over the course of the week, this is probably due to the currency being pegged to the U.S. dollar. In the past, the value of the Argentinean peso and Panamanian dollar have been fixed against the U.S. dollar.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-5

ANSWERS TO PROBLEMS

1. B This is a hedge of a purchase commitment. In this situation, the purchased parts are recorded at the actual cash outflow--$21,000--as established by the forward contract.

2. C An import purchase causes a foreign currency payable to be carried on the books. If the foreign currency depreciates, the dollar value of the foreign currency payable decreases, yielding a foreign exchange gain.

3. D Since the forward rate exceeds the spot rate, a premium exists. Answers a. and c. can be eliminated. A foreign currency receivable is being hedged. Francs are being sold forward at a higher forward rate; hence, a net gain will be reported.

4. D Foreign exchange gains and losses are recorded in income in the period in which the exchange rate changes.

5. C The 10 million won receivable has changed in dollar value from $35,000 at 12/16/01 to $33,000 at 12/31/01. The won receivable will be written down by $2,000 and a foreign exchange loss will be reported in 2001 income.

6. A The fair value of the forward contract on December 31, 2001 is a positive $2,000, the difference between the amount to be received from the forward contract actually entered into, $34,000 ($.0034 x 10 million), and the amount that could be received by entering into a forward contract on December 31, 2001 that matures on January 15, 2002, $32,000 ($.0032 x 10 million). On December 31, 2001, MNC Corp. will recognize a $2,000 gain on the forward contract and a foreign exchange loss of $2,000 on the won receivable. The net impact on 1998 income is zero.

7. B Foreign exchange gains related to foreign currency import purchases are treated as a component of income before income taxes. If there is no foreign exchange gain in operating income, then the purchase must have been denominated in US dollars or there was no change in the value of the foreign currency from October 1 to December 31, 2001.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-6 Solutions Manual

8. A 10/31/01 Foreign currency option............................... $1,500 Cash............................................................. $1,500

12/31/01 Foreign currency option................................. $200 Gain on option [$1,700 - $1,500]............... $200

Loss on firm commitment............................... $200 Firm commitment....................................... $200

9. C 1/5/02 Foreign currency option................................. $1,300 Gain on option [$3,000* - $1,700].............. $1,300

Loss on firm commitment............................... $1,300 Firm commitment....................................... $1,300

Foreign currency (C$)..................................... $77,000 Sales revenue............................................. $77,000

Cash.................................................................. $80,000 Foreign currency (C$)................................ $77,000Foreign currency option............................ 3,000

Firm commitment............................................. $1,500 Sales revenue............................................. $1,500

* Fair value of option is the difference between amount received by exercising the option ($80,000) and the amount received if the C$ were converted at the 1/5/02 spot rate ($77,000).

10. B The company would have received $77,000 if the Canadian dollar receivable had not been hedged with a foreign currency option. With the option, the company receives $80,000 from the sale of Canadian dollars, but paid $1,500 to acquire the option. The net cash flow is $78,500, $1,500 more than if the option had not been acquired.

11. B The dollar value of the LCU receivable has increased from $110,000 at December 31, 2001 to $120,000 at February 15, 2002. This increase of $10,000 should be reported as a foreign exchange gain in 2002.

12. D The increase in the dollar value of the lire note payable represents a foreign exchange loss. In this case a $30,000 loss would have been accrued in 2001 and a $40,000 loss will be reported in 2002.

13. D A foreign currency receivable will generate a foreign exchange gain when the foreign currency increases in dollar value. A foreign currency payable will generate a foreign exchange gain when the foreign currency decreases in dollar value. Hence, the correct combination is yen (increase) and franc (decrease).

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-7

14. D The merchandise purchase results in a foreign exchange loss of $8,000, the difference between the U.S. dollar equivalent at the date of sale and at the date of settlement. The increase in the dollar equivalent of the note’s principal results in a foreign exchange loss of $20,000. The accrued interest on the original dollar value of the note is $10,000 [$300,000 x .10 x 4/12]. Since the U.S. dollar equivalent of the accrued interest at December 31, 2001 is $12,000, there is a $2,000 foreign exchange loss related to the interest. The total foreign exchange loss is $30,000. ($8,000 + $20,000 +$2,000)

15. C This is a hedge of a foreign currency commitment using a foreign currency option. With this type of hedge, gains and losses on the option and the firm commitment offset one another and the sale is reported at the actual amount of net cash inflow. This is comprised of two components:

Exercise of option at strike price: 1 mn krone x $.15 = $150,000less: Option premium (1 mn krone x $.005) = (5,000)

$145,000

16. C By entering into a forward contract to sell 200,000 ramda, Palmer will receive $31,000 at the end of six months. At the end of two months, Palmer could have entered into a forward contract to sell 200,000 ramda four months in the future for $34,400 ($.172 x 200,000). As a result, Palmer's forward contract has a value of negative $3,400. This will be recognized as a liability and a loss on forward contract. Because this is a hedge of a firm commitment, hedge accounting applies, and an offsetting $3,400 gain on the firm commitment must also be recorded.

17. (10 minutes) (Foreign Currency Purchase/Payable)

The decrease in the dollar value of the LCU payable from November 12 (60,000/.29 = $206,897) to December 31 (60,000/.33 = $181,818) is recorded as a $25,079 foreign exchange gain in 2001. The increase in the dollar value of the LCU payable from December 31 ($181,818) to January 19 (60,000/.28 = $214,286) is recorded as a $32,468 foreign exchange loss in 2002.

18. (10 minutes) (Foreign Currency Sale/Receivable)

The ostra receivable decreases in dollar value from (50,000 x $1.05) $52,500 at December 20 to $51,000 (50,000 x $1.02) at December 31, resulting in a foreign exchange loss of $1,500 in 2001. The further decrease in dollar value of the ostra receivable from $51,000 at December 31 to $49,000 (50,000 x $.98) at January 10 results in an additional $2,000 foreign exchange loss in 2002.

19. (10 minutes) (Foreign Currency Sale/Receivable)

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-8 Solutions Manual

9/15/01 Accounts receivable (FCU) [100,000 x $.40]........ $40,000

Sales................................................................... $40,000

9/30/01 Accounts receivable (FCU) [100,000 x ($.42-$.40)] $2,000 Foreign exchange gain..................................... $2,000

10/15/01 Foreign exchange loss......................................... $5,000 Accounts receivable (FCU) [100,000 x ($.37-$.42)] $5,000

Cash........................................................................ $37,000 Accounts receivable (FCU).............................. $37,000

20. (10 minutes) (Foreign Currency Purchase/Payable)

12/1/01 Inventory................................................................ $52,800 Accounts payable (LCU) [60,000 x $.88]......... $52,800

12/31/01 Accounts payable (LCU) [60,000 x ($.82-$.88)].... $3,600 Foreign exchange gain..................................... $3,600

1/28/02 Foreign exchange loss.......................................... $4,800 Accounts payable (LCU) [60,000 x ($.90-$.82)] $4,800

Accounts payable (LCU)........................................ $54,000 Cash................................................................... $54,000

21. (15 minutes) (Foreign Currency Purchase/Payable and Sale/Receivable)

6/1 Inventory................................................................. $10,400 Accounts payable (ertu) [20,000 x $.52]............... $10,400

8/1 Accounts receivable (ertu) [30,000 x $.55]........... $16,500 Sales........................................................................ $16,500

10/1 Accounts payable (ertu) [$10,400 x 1/2]............. $5,200 Foreign exchange loss [10,000 x ($.60-$.52)]................. 800

Cash [10,000 x $.60].......................................... $6,000

11/1 Cash [10,000 x $.64]............................................. $6,400 Accounts receivable [$16,500 x 1/3]............... $5,500Foreign exchange gain [10,000 x ($.64-$.55)] 900

21. (continued)

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-9

12/31 Foreign exchange loss........................................ $1,300 Accounts payable (ertu) [10,000 x ($.65-$.52)] $1,300

Accounts receivable (ertu) [20,000 x ($.65-$.55)] $2,000 Foreign exchange gain..................................... $2,000

22. (15 minutes) (Determine U.S. Dollar Balance For Foreign Currency Transactions)

Inventory and Cost of Goods Sold are reported at the spot rate at the date the inventory was purchased. Sales are reported at the spot rate at the date of sale. Accounts Receivable and Accounts Payable are reported at the spot rate at the balance sheet date. Cash is reported at the spot rate when collected and the spot rate when paid.

Inventory [50,000 pesos x 40% x $.17].........................................................$3,400COGS [50,000 pesos x 60% x $.17]...............................................................$5,100Sales [45,000 pesos x $.18]...........................................................................$8,100Accounts receivable [45,000 - 40,000 = 5,000 pesos x $.21]......................$1,050Accounts payable [50,000 - 30,000 = 20,000 pesos x $.21]........................$4,200Cash [(40,000 x $.19) - (30,000 x $.20)].........................................................$1,600

23. (15-20 minutes) (Forward Contract Hedge of Export Sale Transaction)

12/1/01 Accounts receivable (K) [20,000 x $2.00]........... $40,000 Sales................................................................. $40,000

No entry for the forward contract.

12/31/01 Accounts receivable (K) [20,000 x ($2.10-$2.00)] $2,000 Foreign exchange gain................................... $2,000

Loss on forward contract [20,000 x ($2.08-$2.20)] $2,400 Forward contract............................................. $2,400

Impact on 2001 income: Sales........................................... $40,000Foreign exchange gain ................. $2,000 Loss on forward contract.............. ( 2,400) Net gain (loss).................................. (400)Total.................................................. $39,600

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-10 Solutions Manual

23. (continued)

3/1/02 Accounts receivable (K) [20,000 x ($2.25-$2.10)] $3,000 Foreign exchange gain................................... $3,000

Loss on forward contract..................................... $1,000 Forward contract [20,000 x ($2.20-$2.25)]..... $1,000

Foreign currency (K) [20,000 x $2.25]................. $45,000

Accounts receivable (K).................................. $45,000

Cash [20,000 x $2.08]............................................ $41,600 Forward contract.................................................. 3,400

Foreign currency............................................. $45,000

Impact on 2002 income: Foreign exchange gain........... $3,000 Loss on forward contract............... (1,000) Net gain (loss).................................. 2,000Total.................................................. $2,000

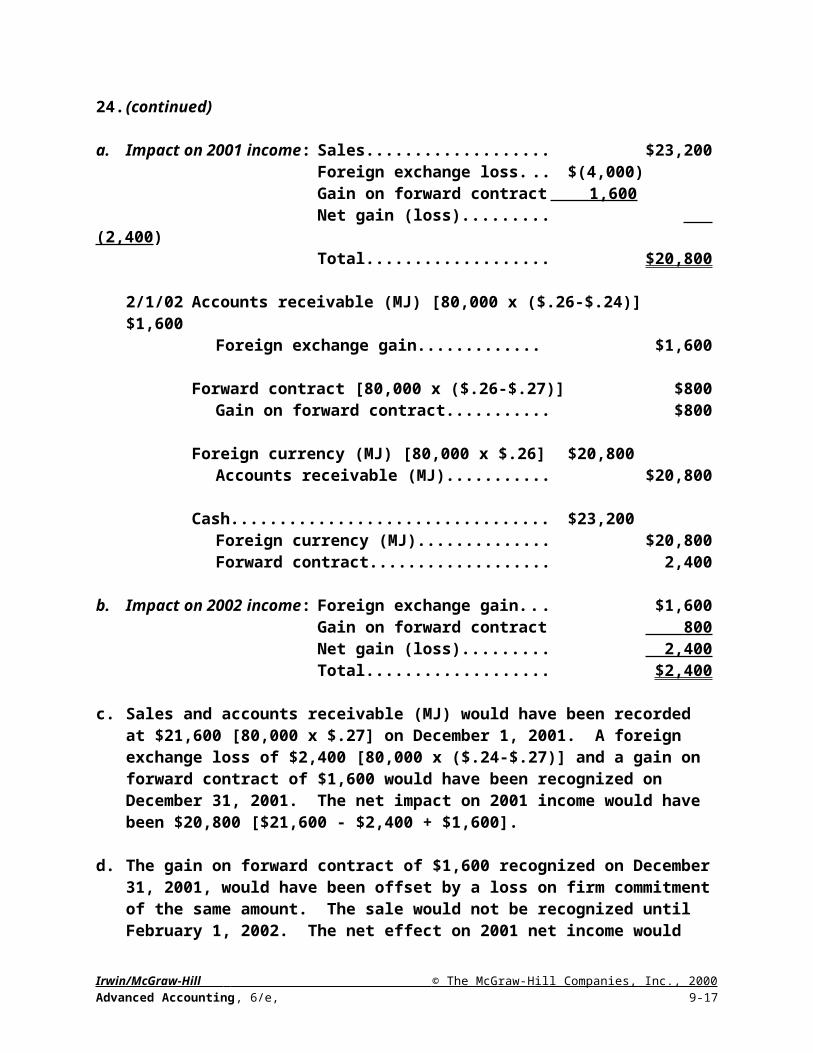

24. (20-25 minutes) (Delayed Forward Contract Hedge of Export Sale Transaction)

11/10/01 Accounts receivable (MJ) [80,000 x $.29]......... $23,200 Sales................................................................. $23,200

12/1/01 No entry to record the forward contract.

12/31/01 Foreign exchange loss......................................... $4,000 Accounts receivable (MJ) [80,000 x ($.24-$.29)] $4,000

Forward contract [80,000 x ($.27-$.29)].............. $1,600 Gain on forward contract................................ $1,600

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-11

24. (continued)

a. Impact on 2001 income: Sales........................................... $23,200 Foreign exchange loss............. $(4,000) Gain on forward contract......... 1,600 Net gain (loss)........................... (2,400)

Total........................................... $20,800

2/1/02 Accounts receivable (MJ) [80,000 x ($.26-$.24)] $1,600 Foreign exchange gain.................................. $1,600

Forward contract [80,000 x ($.26-$.27)].............. $800 Gain on forward contract................................ $800

Foreign currency (MJ) [80,000 x $.26]................. $20,800 Accounts receivable (MJ)............................... $20,800

Cash....................................................................... $23,200 Foreign currency (MJ)..................................... $20,800Forward contract............................................. 2,400

b. Impact on 2002 income: Foreign exchange gain............ $1,600Gain on forward contract......... 800Net gain (loss)........................... 2,400Total........................................... $2,400

c. Sales and accounts receivable (MJ) would have been recorded at $21,600 [80,000 x $.27] on December 1, 2001. A foreign exchange loss of $2,400 [80,000 x ($.24-$.27)] and a gain on forward contract of $1,600 would have been recognized on December 31, 2001. The net impact on 2001 income would have been $20,800 [$21,600 - $2,400 + $1,600].

d. The gain on forward contract of $1,600 recognized on December 31, 2001, would have been offset by a loss on firm commitment of the same amount. The sale would not be recognized until February 1, 2002. The net effect on 2001 net income would have been zero.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-12 Solutions Manual

25. (25 minutes) (Prepare Journal Entries for Foreign Currency Transactions)

2/1/01 Equipment............................................................ $17,600 Accounts payable (L) [40,000 x $.44]............. $17,600

4/1/01 Accounts payable (L)........................................... $17,600 Foreign exchange loss......................................... 400

Cash [40,000 x $.45]........................................ $18,000

6/1/01 Inventory................................................................ $14,100 Accounts payable (L) [30,000 x $.47]............. $14,100

8/1/01 Accounts receivable (L) [40,000 x $.48].............. $19,200 Sales................................................................ $19,200

Cost of goods sold.............................................. $9,870 Inventory [$14,100 x 70%]............................... $9,870

10/1/01 Cash [30,000 x $.49].............................................. $14,700 Accounts receivable (L) [$19,200 x 3/4]....... $14,400Foreign exchange gain................................... 300

11/1/01 Accounts payable (L) [$14,100 x 2/3]................. $9,400 Foreign exchange loss [20,000 x ($.50-$.47)]..... 600

Cash [20,000 x $.50]........................................ $10,000

12/31/01 Foreign exchange loss........................................ $500 Accounts payable (L) [10,000 x ($.52-$.47)]. $500

Accounts receivable (L) [10,000 x ($.52-$.48)]. . $400 Foreign exchange gain................................... $400

2/1/02 Cash [10,000 x $.54]............................................. $5,400 Accounts receivable (L) [10,000 x $.52]........ $5,200Foreign exchange gain................................... 200

3/1/02 Accounts payable (L) [10,000 x $.52]................. $5,200 Foreign exchange loss......................................... 300

Cash [10,000 x $.55]........................................ $5,500

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-13

26. (10 minutes) (Forward Contract Hedge of Export Sale Transaction—Determine Economic Benefit of Hedge)

a. Second quarter 2001.6/1/01 Accounts receivable (JG) [1 million x $.045]...... $45,000

Sales................................................................. $45,000No entry to record the forward contract.

6/30/01 Accounts receivable (JG) [1 million x ($.048-$.045)] $3,000 Foreign exchange gain................................... $3,000

Loss on forward contract..................................... $2,000 Forward contract [1 million x ($.51-$.49)]...... $2,000

Impact on second Sales...................................... $45,000quarter 2001 income: Foreign exchange gain........ $3,000

Loss on forward contract..... (2,000) Net gain (loss)....................... 1,000

Total....................................... $46,000The change in the value of the JG results in a net gain of $1,000 in the second quarter.

b. Third quarter 2001.9/1/01 Foreign exchange loss......................................... $4,000

Accounts receivable (JG) [1 million x ($.44-$.48)] $4,000

Forward contract [1 million x ($.44-$.51)].......... $7,000 Gain on forward contract................................ $7,000

Foreign currency (JG) [1 million x $.44]............. $44,000 Accounts receivable (JG)............................... $44,000

Cash....................................................................... $49,000 Foreign currency (MJ)..................................... $44,000Forward contract............................................. 5,000

Impact on third Foreign exchange loss.............. $(4,000) quarter 2001 income: Gain on forward contract............ 7,000

Net gain (loss).............................. 3,000Total.............................................. $3,000

The change in the value of the JG results in a net gain of $3,000 in the third quarter. Over the two quarters, the total gain recognized in income is $4,000 which is equal to the premium on the forward contract at June 1 [1 million x ($.049 forward - $.045 spot).

26. (continued)

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-14 Solutions Manual

c. The net economic benefit (or loss) is determined by comparing the amount of dollars received from selling JG 1,000,000 under the forward contract ($49,000) with the amount of dollars that would have been received if Alexander had not sold JG forward, but instead had sold JG at the September 1 spot rate ($44,000). The economic benefit is $5,000. The net gain on forward contract recognized over the two quarters of $5,000 ($2,000 loss in second quarter plus $7,000 gain in third quarter) accurately reflects this economic benefit.

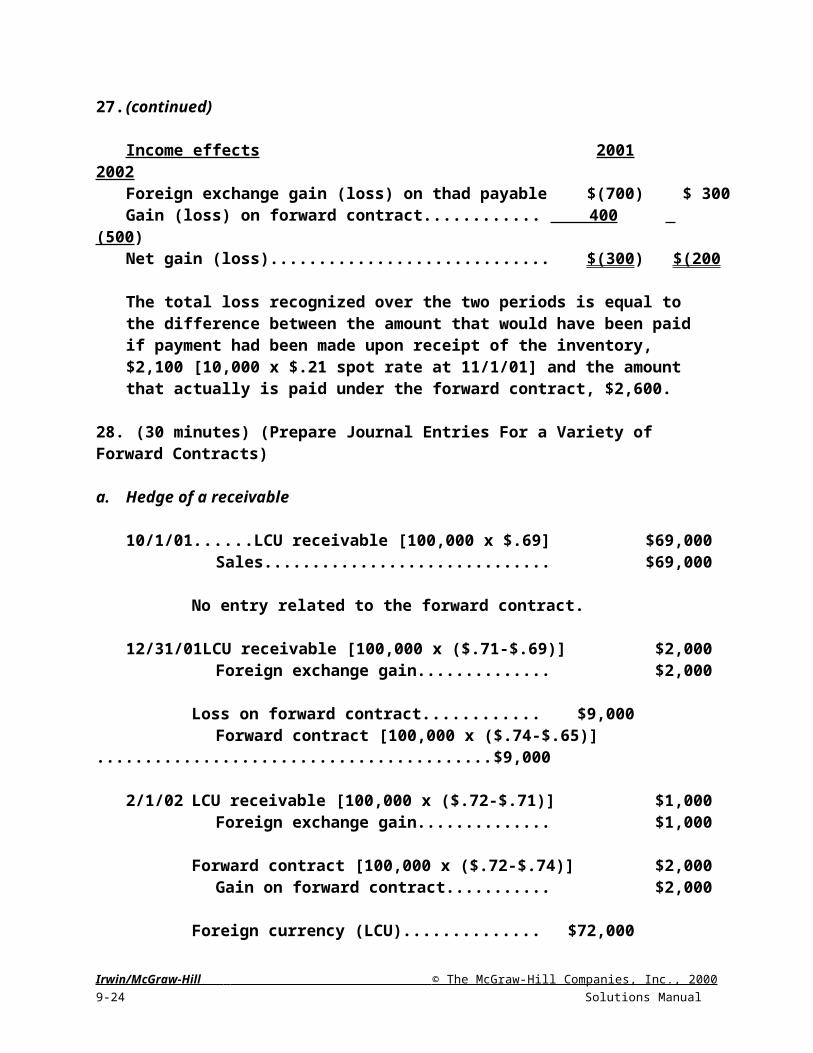

27. (20 minutes) (Foreign Currency Purchase/Payable and Forward Contract

Hedge)

a. The thad payable has a dollar value of $2,100 on November 1, 2001 [10,000 x $.21] and a dollar value of $2,800 on December 31, 2001 [10,000 x $.28]. The $700 increase in dollar value of the thad payable is reported as a foreign exchange loss in 2001.By February 1, 2002, the thad payable has decreased in dollar value to $2,500 [10,000 x $.25]. The $300 decrease in the dollar value of the thad payable since December 31, 2002 is reported as a foreign exchange gain in 2002.

b. The company still has a $700 foreign exchange loss related to the thad payable in 2001. The forward contract has a fair value of zero at December 1, 2001. At December 31, 2001, the forward contract has a fair value of positive $400 determined as follows. By entering into the forward contract, the company has locked-in to purchase 10,000 thads for $2,600 on February 1, 2002. If the company had not entered into the forward contract on December 1, but instead had waited until December 31 to purchase 10,000 thads forward, it would have to pay $3,000 [10,000 x $.30 forward rate to 2/1/02]. The forward contract actually entered into has therefore saved the company $400. This is the fair value of the forward contract on December 31, 2001. The change in the fair value since December 1 [$400 - $0] is recognized as a $400 gain on forward contract in 2001.

In 2002, the company reports a $300 foreign exchange gain related to the thad payable. The fair value of the forward contract is negative $100 at February 1, 2002. This is determined as the difference between the amount the company will pay for 10,000 thads under the forward contract ($2,600) and the amount the company would have paid if it had not entered into the forward contract ($2,500 = 10,000 x $.25 spot rate on 2/1/02). The change in the fair value of the forward contract is negative $500 [from positive $400 to negative $100], and this is recognized as a $500 loss on forward contract in 2002.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-15

27. (continued)

Income effects 2001 2002 Foreign exchange gain (loss) on thad payable............... $(700) $ 300 Gain (loss) on forward contract........................................ 400 (500)Net gain (loss)...................................................................... $(300) $(200)

The total loss recognized over the two periods is equal to the difference between the amount that would have been paid if payment had been made upon receipt of the inventory, $2,100 [10,000 x $.21 spot rate at 11/1/01] and the amount that actually is paid under the forward contract, $2,600.

28. (30 minutes) (Prepare Journal Entries For a Variety of Forward Contracts)

a. Hedge of a receivable

10/1/01 LCU receivable [100,000 x $.69].......................... $69,000 Sales................................................................. $69,000

No entry related to the forward contract.

12/31/01 LCU receivable [100,000 x ($.71-$.69)]................ $2,000 Foreign exchange gain................................... $2,000

Loss on forward contract.................................... $9,000 Forward contract [100,000 x ($.74-$.65)]....... $9,000

2/1/02 LCU receivable [100,000 x ($.72-$.71)]............... $1,000 Foreign exchange gain................................... $1,000

Forward contract [100,000 x ($.72-$.74)]............ $2,000 Gain on forward contract................................ $2,000

Foreign currency (LCU)....................................... $72,000 LCU receivable................................................. $72,000

Cash...................................................................... $65,000 Forward contract................................................... 7,000

Foreign currency (LCU).................................. $72,000

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-16 Solutions Manual

28. (continued)

Note that the net effect on income is $65,000 which is equal to the amount of Cash received: Sales—2001 ........................................................................................... $69,000 Foreign exchange gain--2001................................................................ 2,000 Loss on forward contract--2001........................................................... (9,000)Foreign exchange gain--2002................................................................ 1,000 Gain on forward contract--2002............................................................ 2,000 Net effect on income.............................................................................. $65,000

b. Hedge of commitment

10/1/01 No entries related to the forward contract or firm commitment.

12/31/01 Loss on forward contract..................................... $9,000 Forward contract [100,000 x ($.74-$.65)]....... $9,000

Firm commitment.................................................. $9,000 Gain on firm commitment.............................. $9,000

2/1/02 Forward contract [100,000 x ($.72-$.74)]............ $2,000 Gain on forward contract................................ $2,000

Loss on firm commitment.................................... $2,000 Firm commitment............................................. $2,000

Foreign currency (LCU)........................................ $72,000 Sales................................................................. $72,000

Cash....................................................................... $65,000 Forward contract................................................... 7,000

Foreign currency (LCU).................................. $72,000

Sales...................................................................... $7,000 Firm commitment............................................. $7,000

Note that as a result of these entries, gains and losses offset; Sales revenue is recognized at $65,000 which is equal to the amount of Cash received.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-17

29. (25 minutes) (Determine Income Effect of a Variety of Forward Contracts)

a. Hedge of a transactionFor 2001, Tompson recognizes a foreign exchange loss of $400 [($.64 - $.62) x 20,000 LCUs] on the LCU liability and a gain on forward contract of $800 [($.72 - $.68) x 20,000 LCUs], for a net gain of $400.

For 2002, Tompson recognizes a foreign exchange loss of $1,000 [($.69 - $.64) x 20,000 LCUs] on the LCU liability and a loss on forward contract of $600 [($.69 - $.72) x 20,000 LCUs], for a net loss $1,600.

Over the two years, the net effect on income is a negative $1,200, which is the difference between the amount paid for the LCUs under the forward contract--$13,600 [$.68 x 20,000 LCUs], and the amount that would have been paid if the LCUs had been purchased at the spot rate on November 1, 2001--$12,400 [$.62 x 20,000 LCUs].

b. Hedge of a commitmentFor 2001, Tompson recognizes a gain on forward contract of $800 [($.72 - $.68) x 20,000 LCUs] and an offsetting loss on firm commitment--net impact on income is zero.

For 2002, Tompson recognizes a loss on forward contract of $600 [($.69 - $.72) x 20,000 LCUs] and an offsetting gain on firm commitment--net impact on income is zero.

The inventory will be recorded at cost which is equal to the amount of U.S. dollars spent under the forward contract to acquire it--$13,600.

c. Speculative forward contractFor 2001, Tompson recognizes a gain on forward contract of $800 [($.72 - $.68) x 20,000 LCUs].

Since the forward contract is sold for $610 without any offsetting costs, the net gain from speculation is $610. As a gain of $800 was already reported in 2001, a loss of $190 must be reported in 2002 income to generate a net gain of $610.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-18 Solutions Manual

30. (20 minutes) (Determine Income Effect of Foreign Currency Purchase/Payable)

a. Benjamin, Inc. has a liability of AL160,000. On the date that this liability was created (December 1, 2001), the liability had a dollar value of $70,400 (AL 160,000 x $.44). On December 31, 2001, the dollar value has risen to $76,800 (AL 160,000 x $.48). The increase in the dollar value of the liability creates a foreign exchange loss of $6,400 ($76,800 - $70,400) in 2001.

By March 1, 2002, when the liability is paid, the dollar value has dropped to $72,000 (AL 160,000 x $.45) creating a foreign exchange gain of $4,800 ($72,000 - $76,800) to be reported in 2002.

b. Benjamin, Inc. has a liability of AL160,000. On the date that this liability was created (September 1, 2001), the liability had a dollar value of $73,600 (AL 160,000 x $.46). On December 1, 2001, when the liability is paid, the dollar value has decreased to $70,400 (AL 160,000 x $.44). The drop in the dollar value of the liability creates a foreign exchange gain of $3,200 ($70,400 - $73,600) in 2001.

c. Benjamin, Inc. has a liability of AL160,000. On the date that this liability was created (September 1, 2001), the liability had a dollar value of $73,600 (AL 160,000 x $.46). On December 31, 2001, the dollar value has risen to $76,800 (AL 160,000 x $.48). The increase in the dollar value of the liability creates a foreign exchange loss of $3,200 ($76,800 - $73,600) in 2001.

By March 1, 2002, when the liability is paid, the dollar value has dropped to $72,000 (AL 160,000 x $.45) creating a foreign exchange gain of $4,800 ($72,000 - $76,800) to be reported in 2002.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-19

31. (40 minutes) (Prepare Journal Entries For a Variety of Forward Contracts)

a. Speculative Forward Contract11/1/01 No journal entries12/31/01 Loss on forward contract [20,000 x ($.40 - $.42)] $400

Forward contract (MZ)..................................... $4005/1/02 Forward contract (MZ).......................................... $2,000

Gain on forward contract [20,000 x ($.50 - $.40)] $2,000Investment in MZ.................................................. $10,000

Cash.................................................................. $8,400Forward contract............................................. 1,600

Cash....................................................................... $10,000 Investment in MZ............................................. $10,000

The net increase in cash is $1,600 ($10,000 - $8,400). A loss of $400 is recognized in 2001 and a gain of $2,000 is reported in 2002.

b. Hedge of a Commitment11/1/01 No journal entries12/31/01 Loss on forward contract[20,000 x ($.40 - $.42)] $400

Forward contract (MZ)..................................... $400Firm commitment.................................................. $400

Gain on firm commitment............................... $4005/1/02 Forward contract (MZ)........................................ $2,000

Gain on forward contract [20,000 x ($.50 - $.40)] $2,000Loss on firm commitment.................................... $2,000

Firm commitment............................................. $2,000Foreign currency (MZ).......................................... $10,000

Cash.................................................................. $8,400Forward contract............................................. 1,600

Equipment........................................................... $8,400 Firm commitment.................................................. 1,600

Foreign currency (MZ)..................................... $10,000There is no impact on income from the hedge of a firm commitment. Equipment is carried at a cost of $8,400, the exact amount of Cash paid to acquire MZ 20,000.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-20 Solutions Manual

31. (continued)

c. Hedge of a Transaction

11/1/01 Land...................................................................... $9,600 Accounts payable (MZ) [20,000 x $.48].......... $9,600

No entry related to the forward contract.

12/31/01 Accounts payable (MZ) [20,000 x ($.45-$.48)].... $600 Foreign exchange gain................................... $600

Loss on forward contract [20,000 x ($.40 - $.42)] $400 Forward contract (MZ)..................................... $400

5/1/02 Foreign exchange loss......................................... $1,000 Accounts payable (MZ) [20,000 x ($.50-$.45)] $1,000

Forward contract (MZ).......................................... $2,000 Gain on forward contract [20,000 x ($.50 - $.40)] $2,000

Foreign Currency (MZ)......................................... $10,000 Cash.................................................................. $8,400Forward contract............................................. 1,600

Accounts payable (MZ)....................................... $10,000 Foreign currency (MZ)..................................... $10,000

The net result is that Land is carried at a cost of $9,600, the actual decrease in Cash is only $8,400, the difference being a net gain of $1,200. A net gain of $200 is reported in 2001 and a net gain of $1,000 is reported in 2002.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-21

32. (30 minutes) (Forward Contract Hedge of a Net Foreign Currency Receivable Exposure) 11/15/01 Accounts receivable (mong) [500,000 x $.53].... $265,000

Sales................................................................. $265,000(To record the sale of equipment and a mong account receivable.)Inventory................................................................ $159,000

Accounts payable (mong) [300,000 x $.53]... $159,000(To record the purchase of inventory and a mong account payable.)No entry related to the forward contract.

12/31/01 Foreign exchange loss......................................... $15,000 Accounts receivable (mong) [500,000 x ($.50-$.53)] $15,000(To record a loss on the mong account receivable.)Accounts payable (mong) [300,000 x ($.50-$.53)] $9,000

Foreign exchange gain................................... $9,000 (To record a gain on the mong account payable.)

Forward contract [200,000 x ($.48-$.52)]............ $8,000 Gain on forward contract................................ $8,000

(To record a gain on the forward contract.)Impact on 2001 income: Sales........................................... $265,000

Foreign exchange loss............. $(15,000) Foreign exchange gain............ 9,000 Gain on forward contract......... 8,000 Net gain (loss)........................... 2,000Net impact on income............ $267,000

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-22 Solutions Manual

32. (continued)

1/15/02 Foreign exchange loss......................................... $5,000 Accounts receivable (mong) [500,000 x ($.49-$.50)] $5,000

(To record a loss on the mong account receivable.)Accounts payable (mong) [300,000 x ($.49-$.50)] $3,000

Foreign exchange gain.................................. $3,000(To record a gain on the mong account payable.) Loss on forward contract..................................... $2,000

Forward contract [200,000 x ($.49-$.48)]...... $2,000Foreign currency (mong) [500,000 x $.49].......... $245,000

Accounts receivable (mong).......................... $245,000(To record the collection of the mong account receivable.)Accounts payable (mong).................................... $147,000

Foreign currency (mong) [300,000 x $.49]..... $147,000(To record the payment of the mong account payable.)Cash....................................................................... $104,000

Foreign currency (mong) [200,000 x $.49]..... $98,000Forward contract............................................. 6,000

(To record the delivery of 200,000 mongs to the foreign currency broker in exchange for $104,000.)

Impact on 2002 income: Foreign exchange loss............. $(5,000)Foreign exchange gain............ 3,000 Loss on forward contract......... (2,000)Net gain (loss)........................... $(4,000)

Over the two years, Eximco recognizes a total net loss of $2,000 related to changes in the value of the mong. This is equal to the discount of $2,000 [200,000 x ($.53 spot - $.52 forward)] on the forward contract to sell 200,000 mongs two months forward.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-23

33. (30 minutes) (Foreign Currency Borrowing) 9/30/01 Cash....................................................................... $100,000

Note payable (dudek) [1,000,000 x $.10]........ $100,000(To record the note and conversion of 1 million dudeks into $ at the spot rate.)

12/31/01 Interest expense.................................................... $525 Interest payable (dudek) ................................ $525[1,000,000 x 2% x 3/12 = 5,000 dudeks x $.105 spot rate]

(To accrue interest for the period 9/30 - 12/31/01.)Foreign exchange loss......................................... $5,000

Note payable (dudek) [1 mn x ($.105-$.10)]... $5,000(To revalue the note payable at the spot rate of $.105 and record a foreign exchange loss.)

9/30/02 Interest expense [15,000 dudeks x $.12]............ $1,800 Interest payable (dudek)...................................... 525 Foreign exchange loss [5,000 dudeks x ($.12-$.105)] 75

Cash [20,000 dudeks x $.12] .......................... $2,400(To record the first annual interest payment, record interest expense for the period 1/1 - 9/30/02, and record a foreign exchange loss on the interest payable accrued at 12/31/01.)

12/31/02 Interest expense.................................................... $625 Interest payable (dudek) [5,000 dudeks x $.125] $625

(To accrue interest for the period 9/30 - 12/31/02.)Foreign exchange loss........................................ $20,000

Note payable (dudek) [1 mn x ($.125-$.105)] $20,000(To revalue the note payable at the spot rate of $.125 and record a foreign exchange loss.)

9/30/03 Interest expense [15,000 dudeks x $.15]....... $2,250 Interest payable (dudek)...................................... 625 Foreign exchange loss [5,000 dudeks x ($.15-$.125)] 125

Cash [20,000 dudeks x $.15]........................... $3,000(To record the second annual interest payment, record interest expense for the period 1/1 - 9/30/03, and record a foreign exchange loss on the interest payable accrued at 12/31/02.)Note payable (dudek)........................................... $125,000 Foreign exchange loss......................................... 25,000

Cash [1 mn dudeks x $.15]............................. $150,000(To record payment of the 1 million dudek note.)

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-24 Solutions Manual

33. (continued)

The effective cost of borrowing can be determined by considering the total interest expense and foreign exchange losses related to the loan and comparing this with the amount borrowed:

2001 Interest expense.................. $ 525 Foreign exchange loss....... 5,000 Total...................................... $5,525 / $100,000 = 5.525% for 3 months

= 22.1% for 12 months2002 Interest expense.................. $ 2,425

Foreign exchange losses. . . 20,075 Total...................................... $22,500 / $100,000 = 22.5% for 12 months

2003 Interest expense.................. $ 2,250 Foreign exchange losses. . . 25,125 Total...................................... $27,375 / $100,000 = 27.38% for 9 months

= 36.5% for 12 monthsBecause of appreciation in the value of the dudek, effective annual borrowing costs range from 22% - 36%.The net cash flow from this borrowing is:Cash ouflows: Interest ($2,400 + $3,000)........................ $ 5,400

Principal................................................... 150,000 $154,500Cash inflow: Borrowing................................................. 100,000Net cash outflow................................................................. $ 54,500Ignoring compounding, this results in an effective borrowing cost of approximately 27.25% per year [$54,500 / $100,000 = 54.5% over two years / 2 years = 27.25% per year].

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-25

34. (20 minutes) (Option Hedge of a Foreign Currency Commitment) Because this is a hedge of a commitment, the parts will be recorded at the net cash outflow expended to acquire them (a one-transaction perspective).

a. The option strike price ($.19) is less than the spot rate ($.21) on June 25, the date the parts are to be paid for. Therefore, Big Arber will exercise its option. The parts will be recorded at:Strike price [50,000 pijios x $.19].............................................................. $9,500plus: Option premium [50,000 pijios x $.008]......................................... 400Total............................................................................................................ $9,900Journal entries would be:5/25/01 Foreign currency options..................................... $400

Cash.................................................................. $4006/25/01 Parts inventory...................................................... $9,900

Cash.................................................................. $9,500Foreign currency options............................... 400

b. The option strike price ($.19) is greater than the spot rate ($.18) on June 25, the date the parts are to be paid for. Therefore, Big Arber will allow the option to expire unexercised. Foreign currency will be acquired at the spot rate on June 25. The parts will be recorded at:

Spot price [50,000 pijios x $.18]............................................................... $9,000plus: option premium [50,000 pijios x $.008].......................................... 400Total............................................................................................................. $9,400

Journal entries would be:

5/25/01 Foreign currency options..................................... $400 Cash.................................................................. $400

6/25/01 Parts inventory...................................................... $9,400 Cash.................................................................. $9,000Foreign currency options............................... 400

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-26 Solutions Manual

35. (20 minutes) (Option Hedge of a Foreign Currency Transaction)a. spot rate at January 15, 2002 is $1.103.

11/15/01 Accounts receivable (LCU).................................. $110,000 Sales................................................................. $110,000

Foreign currency options..................................... $2,500 Cash [100,000 LCU x $.025] .......................... $2,500

12/31/01 Foreign exchange loss......................................... $500 Accounts receivable (LCU)............................. $500

(To adjust the carrying value of the LCU receivable to the spot rate of $1.095.)Foreign currency options..................................... $250

Gain on foreign currency options.................. $250(To adjust the fair value of the foreign currency option from $2,500 to $2,750.)

Impact on 2001 income: Sales........................................................... $110,000Foreign exchange loss........................ (500)Gain on options......................................... 250Total............................................................ $109,750

At January 15, 2002, the LCU receivable has increased in value to $110,300, a gain of $800 [$110,300 - ($110,000 - $500) = $800]. The option has decreased in value to $1,700, a loss of $1,050. The journal entries required in 2002 are as follows:1/15/02 Accounts receivable (LCU).................................. $800

Foreign exchange gain................................... $800(To adjust the carrying value of the LCU receivable to the spot rate of $1.103.) Loss on foreign currency options....................... $1,050

Foreign currency options.............................. $1,050(To adjust the fair value of the foreign currency option from $2,750 to $1,700.)Foreign currency (LCU)........................................ $110,300

Accounts receivable (LCU)............................. $110,300(To record collection of 100,000 LCU from the customer.)Cash....................................................................... $112,000

Foreign currency (LCU).................................. $110,300Foreign currency options............................... 1,700

(To record exercise of the foreign currency option at the strike price of $1.12.)

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-27

35. (continued)

Impact on 2002 income: Foreign exchange gain................................ $ 800 Loss on options.......................................... (1,050 )

Total............................................................... $ (250 ) The net impact on income over the two years is $109,500 ($109,750 - $250), equal to the net cash inflow ($112,000 - $2,500 option premium).

b. spot rate at January 15, 2002 is $1.123.The entries at November 15, 2001 and December 31, 2001 would be the same as above.At January 15, 2002, the LCU receivable has increased in value to $112,300, a gain of $2,800 [$112,300 - ($110,000 - $500) = $2,800]. The option has decreased in value to zero, a loss of $2,750. The journal entries required in 2002 are as follows:1/15/02 Accounts receivable (LCU).................................. $2,800

Foreign exchange gain................................... $2,800(To adjust the carrying value of the LCU receivable to the spot rate of $1.123.) Loss on foreign currency options....................... $2,750

Foreign currency options............................... $2,750(To adjust the fair value of the foreign currency option from $2,750 to $0.)Foreign currency (LCU)........................................ $112,300

Accounts receivable (LCU)............................. $112,300(To record collection of 100,000 LCU from the customer.)Cash....................................................................... $112,300

Foreign currency (LCU)................................. $112,300(To record sale of 100,000 LCU at the spot rate of $1.123.)

Impact on 2002 income: Foreign exchange gain.............................. $2,800Loss on options.......................................... (2,750 ) Total............................................................. $ 50

The net impact on income over the two years is $109,800 ($109,750 + $50), equal to the net cash inflow ($112,300 - $2,500 option premium).

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-28 Solutions Manual

36. (20 minutes) (Option Hedge of a Forecasted Transaction--Cash Flow Hedge)12/15/01 No journal entries related to the forecasted transaction.

Foreign currency options..................................... $5,000 Cash.................................................................. $5,000

[1 million marks x $.005]12/31/01 Dr. Foreign currency options.............................. $3,000

Cr. Other comprehensive income--foreign currency options................................ $3,000

(To recognize the increase in the value of the foreign currency option in other comprehensive income.)

No impact on 2001 net income. 3/15/02 Dr. Foreign currency options............................... $2,000

Cr. Other comprehensive income-- foreign currency options.......................... $2,000

(To recognize the increase in the value of the foreign currency option in other comprehensive income.)

Dr. Foreign currency (marks)............................... $590,000 Cr. Cash............................................................ $580,000 Foreign currency options......................... 10,000

(To record exercise of the foreign currency option at the strike price of $.58 and close out the foreign currency options account.) Dr. Parts inventory................................................ $590,000

Cr. Foreign currency (marks)......................... $590,000(To record the purchase of parts and payment of 1 million marks to the supplier.)

Dr. Other comprehensive income – foreign currency options................................... $5,000

Cr. Parts inventory........................................... $5,000(To transfer the cumulative gain recognized in other comprehensive income to parts inventory.)

No impact on 2002 net income. The net “gain” on the foreign currency option that had been deferred in Other Comprehensive Income is closed out to Parts Inventory when the parts are received. The net effect is:

Carrying value of parts inventory: ($590,000 - $5,000)..................... $585,000

Net cash outflow for component parts: ($580,000 + $5,000)......... $585,000

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-29

37. (60 minutes) (Foreign Currency Transaction, Forward Contract and Option Hedge of Foreign Currency Transaction, Forward Contract and Option Hedge of Foreign Currency Firm Commitment)

a. Unhedged Foreign Currency Transaction9/15/02 Inventory................................................................ $169,500

Accounts payable (FF).................................... $169,500[FF 1 million x $.1695]

9/30/02 Foreign exchange loss......................................... $500 Accounts payable (FF).................................... $500

[FF 1 million x ($.1700 - $.1695)]10/15/02 Foreign exchange loss......................................... $300

Accounts payable (FF).................................... $300[FF 1 million x ($.1703 - $.1700)]Foreign currency (FF)........................................... $170,300

Cash [FF 1 million x $.1703 spot]................... $170,300Accounts payable (FF)......................................... $170,300

Foreign currency (FF)..................................... $170,300Summary—Inventory is carried at the spot rate on the date it is received,

$169,500. The difference between this amount and the $170,300 of cash paid, $800, is reflected as a foreign exchange loss in income--$500 in the 3rd quarter and $300 in the 4th quarter.

b. Forward Contract Hedge of Foreign Currency Transaction9/15/02 Inventory................................................................ $169,500

Accounts payable (FF).................................... $169,500[FF 1 million x $.1695]No entry related to the forward contract.

9/30/02 Foreign exchange loss......................................... $500 Accounts payable (FF).................................... $500

[FF 1 million x ($.1700 - $.1695)]Forward contract................................................... $700

Gain on forward contract................................ $700[FF 1 million x ($.1705 - $.1698)]

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-30 Solutions Manual

37. (continued)

10/15/02 Foreign exchange loss......................................... $300 Accounts payable (FF).................................... $300

[FF 1 million x ($.1703 - $.1700)]Loss on forward contract..................................... $200

Forward contract............................................. $200[FF 1 million x ($.1703 - $.1705)]Foreign currency (FF)........................................... $170,300

Cash [FF 1 million x $1.698 forward rate]...... $169,800Forward contract............................................. 500

Accounts payable (FF)......................................... $170,300 Foreign currency (FF)..................................... $170,300

Summary—Inventory is carried at the spot rate on the date it is received, $169,500. The difference between this amount and the $169,800 of cash paid, $300, is reflected as a net loss in income--$200 net gain in the 3rd quarter and $500 net loss in the 4th quarter. The net gain on forward contact of $500 recorded over the two periods reflects the fact that the company pays $500 less in acquiring the inventory through the forward contract hedge.

c. Forward Contract Hedge of Foreign Currency Firm Commitment9/15/02 No journal entries; both the purchase order and the forward contract

are executory in nature.9/30/02 Forward contract................................................... $700

Gain on forward contract................................ $700[FF 1 million x ($.1705 - $.1698)]Loss on firm commitment.................................... $700

Firm commitment ............................................ $700

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-31

37. (continued)

10/15/02 Loss on forward contract..................................... $200 Forward contract............................................. $200

[FF 1 million x ($.1703 - $.1705)]Firm commitment.................................................. $200

Gain on firm commitment .............................. $200Foreign currency (FF)........................................... $170,300

Cash [FF 1 million x $1.698 forward rate]...... $169,800Forward contract............................................. 500

Inventory................................................................ $170,300 Foreign currency (FF)..................................... $170,300

Firm commitment.................................................. $500 Inventory.......................................................... $500

Summary—Consistent with the one-transaction perspective, Inventory is carried at a cost of $169,800 which is the exact amount of cash paid. There is no impact on income. The net gain on forward contact of $500 recorded over the two periods reflects the fact that the company pays $500 less in acquiring the inventory through the forward contract hedge.

d. Option Hedge of Foreign Currency Transaction9/15/02 Inventory................................................................ $169,500

Accounts payable (FF).................................... $169,500[FF 1 million x $.1695]Foreign currency options..................................... $1,000

Cash [FF 1 million x $.001]............................. $1,0009/30/02 Foreign exchange loss......................................... $500

Accounts payable (FF).................................... $500[FF 1 million x ($.1700 - $.1695)]Foreign currency options..................................... $100

Gain on foreign currency options.................. $100[$1,100 - $1,000]

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-32 Solutions Manual

37. (continued)

10/15/02 Foreign exchange loss......................................... $300 Accounts payable (FF).................................... $300

[FF 1 million x ($.1703 - $.1700)]

Loss on foreign currency options....................... $300 Foreign currency options............................... $300

[$800 - $1,100]Foreign currency (FF)........................................... $170,300

Cash [FF 1 million x $.1695 strike]................ $169,500Foreign currency options............................... 800

Accounts payable (FF)......................................... $170,300 Foreign currency (FF)..................................... $170,300

Summary—Inventory is carried at the spot rate on the date it is received, $169,500. The difference between this amount and the $170,500 of cash paid, $1,000, is reflected as a net loss in income--$400 net loss in the 3rd quarter and $600 net loss in the 4th quarter. The net loss on foreign currency options of $200 recorded over the two periods reflects the fact that the company pays $200 more in acquiring the inventory with the option than if it had not purchased the option.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 Advanced Accounting, 6/e, 9-33

e. Option Hedge of Foreign Currency Firm Commitment 9/15/02 Foreign currency options..................................... $1,000

Cash [FF 1 million x $.001]............................. $1,0009/30/02 Foreign currency options..................................... $100

Gain on foreign currency options................. $100[$1,100 - $1,000]Loss on firm commitment.................................... $100

Firm commitment............................................. $10010/15/02 Loss on foreign currency options....................... $300

Foreign currency options............................... $300[$800 - $1,100]Firm commitment.................................................. $300

Gain on firm commitment............................... $300Foreign currency (FF)........................................... $170,300

Cash [FF 1 million x $.1695 strike]................. $169,500Foreign currency options............................... 800

Inventory................................................................ $170,300 Foreign currency (FF)..................................... $170,300

Inventory................................................................ $200 Firm commitment............................................. $200

Summary—Consistent with the one-transaction perspective, Inventory is carried at a cost of $170,500 which is the exact amount of cash paid ($169,5000 + $1,000 option premium). There is no net impact on income. The net loss on foreign currency options of $200 recorded over the two periods reflects the fact that the company pays $200 more in acquiring the inventory with the option than if it had not purchased the option.

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 2000 9-34 Solutions Manual