ACID PRECIPITATION CHAPTER 12 SESCTION 3 CHAPTER 12 SESCTION 3.

Upload

hashim-reedCategory

view

24download

0description

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Comprehensive Volume

1

Chapter 12

Tax Credits and Payments

2

The Big Picture

• Tom and Jennifer Snyder have two dependent children in college. – Lora is a freshman

• Her tuition and required fees in 2011 total $14,000. • She has a scholarship amounting to $6,500, and the Snyders paid the

balance of her tuition ($7,500), plus room and board of $8,500. – Sam is a junior, and the Snyders paid $8,100 for his tuition plus $7,200

for his room and board. • The Snyders have AGI of $158,000. • They would like to know what tax options are available to

them related to these educational expenses. – They have heard about education tax credits, but they believe that their

income is too high for them to get any benefit. – Are they correct?

• Read the chapter and formulate your response.

3

Tax Credit VS. Tax Deduction

• Tax benefit received from a tax deduction depends on the marginal tax rate of the taxpayer– Tax benefit received from a tax credit is not affected by the

taxpayer’s marginal tax rate

• Example: $1,000 expenditure: tax benefit of 25% credit compared to tax deduction at various marginal tax rates

MTR 0% 15% 35%

Tax benefit if a 25% credit is allowed $250 $250 $250

Tax benefit if tax deduction is allowed –0– $150 $350

4

Refundable vs Nonrefundable Credits (slide 1 of 2)

• Refundable credits– Paid even if the tax liability is less than amount of

credit

5

Refundable vs Nonrefundable Credits (slide 2 of 2)

• Nonrefundable credits– Credit can only be used to offset tax liability– If credit exceeds tax liability, excess is lost

• Exception: some nonrefundable credits have carryover provisions for excess

6

General Business Credit (slide 1 of 2)

• Comprised of a number of business credits combined into one amount

• Limited to net income tax reduced by greater of:– Tentative minimum tax– 25% of net regular tax liability that exceeds

$25,000

• Unused credit is carried back 1 year, then forward 20 years

7

General Business Credit (slide 2 of 2)

• Includes the following:– Tax credit for rehabilitation expenditures– Work opportunity tax credit– Research activities credit– Low-income housing credit– Disabled access credit– Credit for small employer pension plan startup

costs– Credit for employer-provided child care

8

Rehabilitation Expenditure Credit (slide 1 of 3)

• Credit is a percentage of expenditures made to substantially rehabilitate industrial and commercial buildings and certified historic structures

• Credit rate– 20% for nonresidential and residential certified

historic structures– 10% for other structures originally placed into

service before 1936

9

Rehabilitation Expenditure Credit (slide 2 of 3)

• To qualify for credit, building must be substantially rehabilitated meaning qualified rehab expenditures exceed the greater of:– The adjusted basis of the property before the rehab

expenditures, or– $5,000

• Qualified rehab expenditures do not include the cost of the building and related facilities or cost of enlarging existing building

10

Rehabilitation Expenditure Credit (slide 3 of 3)

• Basis in structure is reduced by the credit amount

• Subject to recapture if rehabilitated property held less than 5 years or ceases to be qualifying property

11

Jobs Credit

• A new $1,000 Jobs Credit is allowed for every unemployed individual hired from Feb. 4 through Dec. 31, 2010– Must work for employer for at least 52 consecutive

weeks – Wages during last 26 weeks of employment must

equal at least 80% of wages for first 26 weeks

• The credit applies to any tax year ending after the 2010 date of enactment.

12

Work Opportunity Tax Credit(slide 1 of 2)

• Applies to first 12 months of wages paid to individuals falling within target groups – Credit limited to a percentage of first $6,000

wages paid per eligible employee• 40% if employee has completed at least 400 hours of

service to employer

• 25% if at least 120 hours of service

– Deduction for wages is reduced by credit amount– The credit is available for qualifying employees

that start work by December 31, 2011

13

Work Opportunity Tax Credit(slide 2 of 2)

• Targeted individuals generally subject to high rates of unemployment, including– Qualified ex-felons, high-risk youths, food stamp

recipients, veterans, summer youth employees, and long-term family assistance recipients

• Summer youth employees: Only first $3,000 of wages paid for work during 90-day period between May 1 and September 15 qualify for credit

14

Work Opportunity Tax Credit: Long-Term Family Assistance Recipient (slide 1 of 2)

• Applies to first 24 months of wages paid to individuals who have been long-term recipients of family assistance welfare benefits– Long-term is at least an 18 month period ending on

hiring date

15

Work Opportunity Tax Credit: Long-Term Family Assistance Recipient (slide 2 of 2)

• Maximum credit is a percentage of first $10,000 qualified wages paid in first and second year of employment– 40% in first year– 50% in second year

• Maximum credit per qualified employee is $9,000– Deduction for wages is reduced by credit amount

16

Research Activities Credit (slide 1 of 5)

• Comprised of three parts– Incremental research activities credit– Basic research credit– Energy research credit

17

Research Activities Credit (slide 2 of 5)

• Incremental research activities credit– Credit amount = 20% × (qualified expenditures – base

amount)

• Expenditures qualify if research relates to discovery of technological info intended for use in developing a new or improved business component for taxpayer– Expenditures qualify fully if research done in-house

– Only 65% qualifies if research conducted by outside party (under contract)

18

Research Activities Credit (slide 3 of 5)

• Tax treatment of R&E expenditures– Full credit and reduce expense deduction by credit

amount– Full expense deduction and reduce credit by

(100% × credit × max. corp. tax rate)– Full credit and capitalize research expenses and

amortize over 60 months or more• Amount capitalized is reduced by full amount of credit

only if the credit exceeds the amount allowable as a deduction

19

Research Activities Credit (slide 4 of 5)

• Basic research credit– Additional 20% credit is allowed on basic research

payments in excess of a base amount• Basic research payments - amounts paid in cash to a qualified basic

research organization, such as a college or university or a tax-exempt organization operated primarily to conduct scientific research

– Basic research is any original investigation for the advancement of scientific knowledge not having a specific commercial objective

• The definition excludes basic research conducted outside the United States and basic research in the social sciences, arts, or humanities

20

Research Activities Credit (slide 5 of 5)

• Energy Research Credit –– This credit is intended to stimulate additional

energy research– Credit amount = 20% of amounts paid or incurred

by a taxpayer to an energy research consortium for energy research

21

Low-income Housing Credit

• Credit is issued on a nationwide allocation program

• Credit amount– Based on qualified basis of the property which is

dependent on the number of units rented to low-income tenants

– Credit is allowed over a 10-year period– Subject to potential recapture

22

Disabled Access Credit

• Credit available for eligible access expenditures made by small businesses– Includes amounts paid to remove barriers that would

otherwise make a business inaccessible to disabled and handicapped individuals

– Facility qualifies if placed in service before November 6, 1990

• Credit amount– 50% × expenditures that exceed $250 but not in excess

of $10,250• Thus, max. credit is $5,000

– Basis in asset is reduced by credit amount

23

Credit For Pension Plan Startup Costs

• Small businesses can claim nonrefundable tax credit for admin costs of establishing and maintaining a qualified retirement plan– Small business has < 100 employees who have earned at

least $5,000 of compensation

• Credit amount = 50% of qualified startup costs limited to max credit of $500 per year for 3 years– Deduction for startup costs is reduced by amount of credit

24

Credit For Employer-Provided Child Care (slide 1 of 2)

• Employers can claim a credit for providing child care facilities to their employees during normal working hours– Limited to $150,000 per year

• Credit amount:– 25% of qualified child care expenses– 10% of qualified child care resource and referral

services

25

Credit For Employer-Provided Child Care (slide 2 of 2)

• Deductible qualifying expenses must be reduced by the credit amount

• Basis of qualifying property must be reduced by credit amount

• Credit may be subject to recapture if child care facility ceases to be used for qualifying purpose within 10 years of being placed in service

26

Earned Income Credit (slide 1 of 3)

• General qualifications for credit– Must have earned income from being an employee

or self-employed – For 2009 and 2010, ARRTA of 2009 increases

• Credit percentage for families with three or more children, and

• Phaseout threshold amounts for married taxpayers filing joint returns

– The Tax Relief Act of 2010 extends this treatment through 2012

27

Earned Income Credit (slide 2 of 3)

• Credit amount (2011 tax year)– Applicable percentage rate × earned income

• Rate and maximum amount of earned income determined by number of qualifying children

• Phase-out of credit begins when earned income (or AGI) exceeds $21,770 for MFJ with qualifying child ($16,690 for other taxpayers)

• Use IRS tables to calculate exact credit amount

28

Earned Income Credit (slide 3 of 3)

• Credit for taxpayers having no children– Available to taxpayers aged 25 through 64

• Credit amount for couple filing jointly with no qualifying children (2011 tax year)– 7.65% × earned income (up to $6,070)– Phase-out of credit begins when earned income (or

AGI) exceeds $12,670 for MFJ ($7,590 for others)

29

Credit for Elderly or Disabled Taxpayers (slide 1 of 2)

• General qualifications– Age 65 or older, or– Under age 65 and permanently and totally disabled

30

Credit for Elderly or Disabled Taxpayers (slide 2 of 2)

• Credit amount– Maximum credit = $1,125

• Amount reduced for taxpayers with Social Security benefits or AGI in excess of specified amounts

– IRS will calculate credit for taxpayer if necessary

31

Foreign Tax Credit(slide 1 of 2)

• The purpose of the foreign tax credit (FTC) is to mitigate double taxation since income earned in a foreign country is subject to both U.S. and foreign taxes– Credit applies to both individuals and corporations

that pay foreign income taxes– Instead of claiming a credit, a deduction may be

claimed for the taxes paid

32

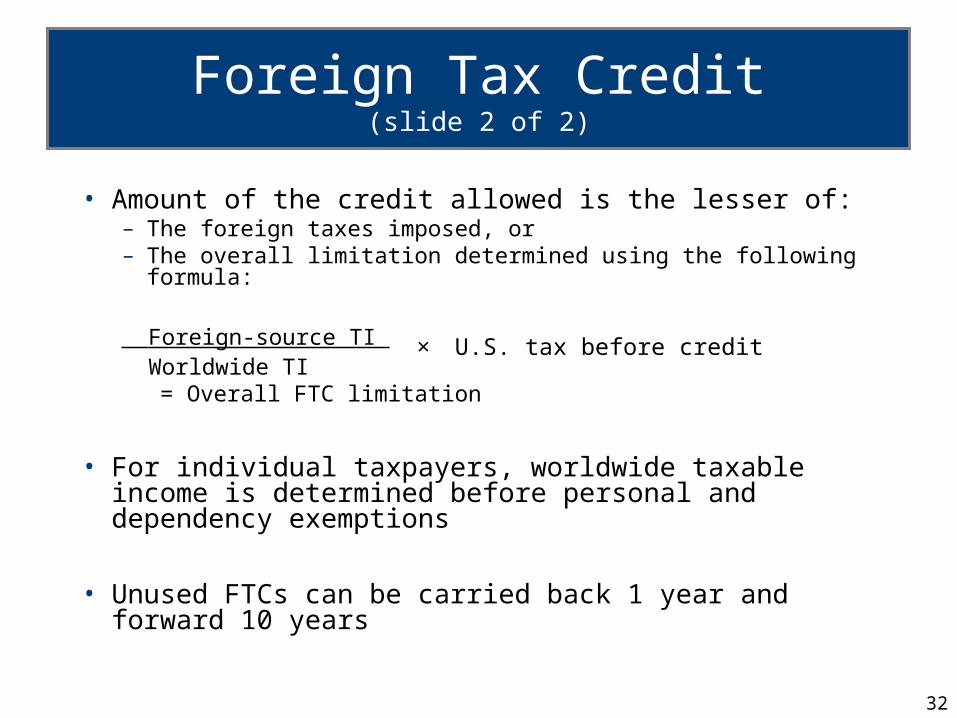

Foreign Tax Credit(slide 2 of 2)

• Amount of the credit allowed is the lesser of:– The foreign taxes imposed, or– The overall limitation determined using the following formula:

Foreign-source TI × U.S. tax before credit

Worldwide TI = Overall FTC limitation

• For individual taxpayers, worldwide taxable income is determined before personal and dependency exemptions

• Unused FTCs can be carried back 1 year and forward 10 years

33

Adoption Expenses Credit (slide 1 of 2)

• Credit for qualified adoption expenses incurred in adoption of eligible child– Examples of expenses: adoption fees, court costs,

attorney fees

• Maximum credit is $13,360 (in 2011) – Credit is phased-out ratably for modified AGI

between $185,210 and $225,210

34

Adoption Expenses Credit (slide 2 of 2)

• Eligible child is one that is – Less than 18 years of age, or– Physically or mentally incapable of taking care of

himself or herself

• Nonrefundable credit– Excess may be carried forward for five years

• Married taxpayers must file jointly to claim

35

Child Tax Credit (slide 1 of 2)

• Credit amount is $1,000 per child

• Eligible children are:– Under age 17,– US citizen, and– Claimed as dependent on taxpayer’s tax return

36

Child Tax Credit (slide 2 of 2)

• Credit is phased out by $50 for each $1,000 of AGI above specified levels– $110,000 for joint filers– $55,000 for married filing separately– $75,000 for single

37

Child and Dependent Care Credit (slide 1 of 4)

• General qualifications for credit– Must have employment related care costs for a

• Dependent under age 13, or

• Dependent or spouse who is physically or mentally incapacitated and who lives with the taxpayer for more than one-half of the year

38

Child and Dependent Care Credit (slide 2 of 4)

• Credit amount– Eligible care costs × applicable percentage– Applicable percentage ranges from 20% to 35%

depending on AGI

• Married taxpayers must file a joint return to obtain credit

39

Child and Dependent Care Credit (slide 3 of 4)

• Eligible care costs defined– Costs for care of qualified individual within

taxpayer’s home or outside home• If outside home, physically or mentally incapacitated

dependent or spouse must spend at least 8 hours a day within taxpayer’s home

– Amount of costs that qualify is the lesser of actual costs or $3,000 for one qualified individual, and $6,000 for two or more qualified individuals

40

Child and Dependent Care Credit (slide 4 of 4)

• Earned income limitation– Amount of eligible care costs cannot exceed lower

of taxpayer’s or spouse’s earned income– Full-time student or disabled taxpayer or spouse

are deemed to have earned income up to maximum per month limits

41

Education Tax Credits(slide 1 of 5)

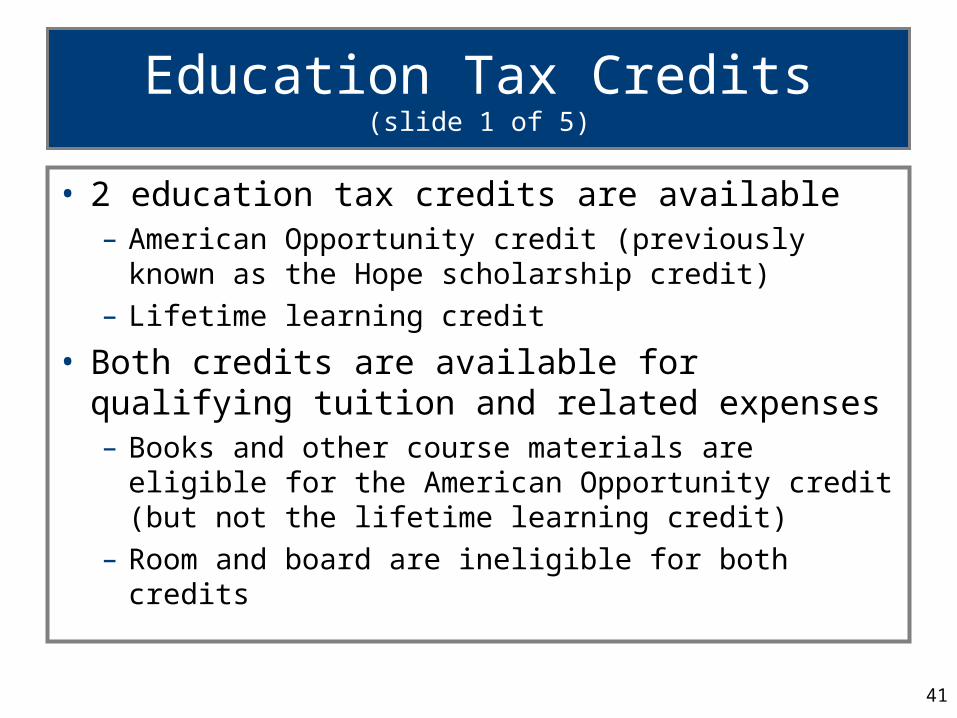

• 2 education tax credits are available– American Opportunity credit (previously known as the

Hope scholarship credit)

– Lifetime learning credit

• Both credits are available for qualifying tuition and related expenses– Books and other course materials are eligible for the

American Opportunity credit (but not the lifetime learning credit)

– Room and board are ineligible for both credits

42

Education Tax Credits(slide 2 of 5)

• Maximum credits– American Opportunity credit maximum per

eligible student is $2,500 per year for first 4 years of postsecondary education

• 100% of the first $2,000 of tuition expenses plus 25% of the next $2,000 of tuition expenses

– Lifetime learning credit maximum per taxpayer is 20% of qualifying expenses (up to $10,000 per year in 2011)

• Cannot be claimed in same year the American Opportunity credit is claimed

43

Education Tax Credits(slide 3 of 5)

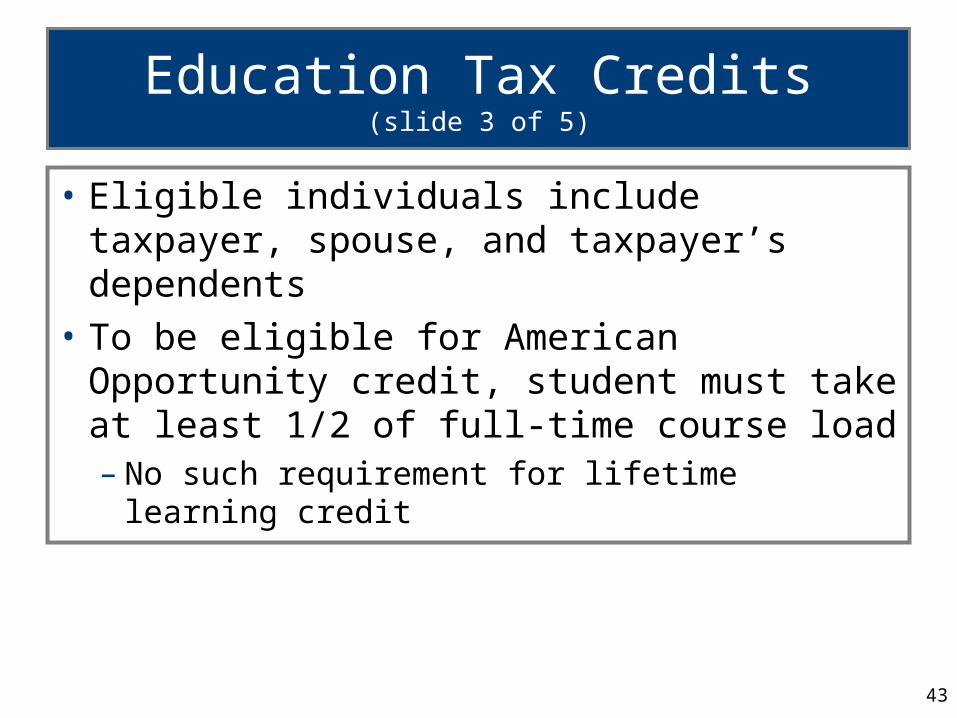

• Eligible individuals include taxpayer, spouse, and taxpayer’s dependents

• To be eligible for American Opportunity credit, student must take at least 1/2 of full-time course load– No such requirement for lifetime learning credit

44

Education Tax Credits(slide 4 of 5)

• Both education credits are subject to income limitations, which differ for 2009 through 2012– In addition, 40% of the American Opportunity credit is

refundable and the entire credit allowed may be used to offset a taxpayer’s AMT liability

• The lifetime learning credit is neither refundable nor an AMT liability offset

• The American Opportunity credit is phased out, beginning when the taxpayer’s modified AGI reaches $80,000 ($160,000 for MFJ)– The credit is completely eliminated when modified AGI

reaches $90,000 ($180,000 for MFJ)

45

Education Tax Credits(slide 5 of 5)

• The lifetime learning credit amount is phased out when modified AGI reaches $51,000 ($102,000 for MFJ)– The credit is completely eliminated when AGI reaches

$61,000($122,000 for MFJ)

• Taxpayers are prohibited from receiving a double tax benefit associated with qualifying educational expenses– Can’t claim education credit and deduct the same expenses– Can’t claim the credit for amounts that are excluded from income

• e.g., scholarships, employer-paid educational assistance

– May claim an education tax credit and exclude from gross income amounts distributed from a Coverdell Education Savings Account as long as the distribution is not used for the same expenses for which the credit is claimed

46

The Big Picture - Example 32

American Opportunity Credit• Return to the facts of The Big Picture on p. 12-2. • Recall that Tom and Jennifer Snyder are married, file a joint

tax return, have modified AGI of $158,000.– Both Lora (a freshman) and Sam (a junior) are full-time students and

are Tom and Jennifer’s dependents.• The Snyders paid the following education expenses.

– $7,500 of tuition and $8,500 for room and board for Lora, and – $8,100 of tuition plus $7,200 for room and board for Sam.

• Lora’s and Sam’s tuition are qualified expenses for the American Opportunity credit. – For 2011, Tom and Jennifer may claim a $2,500 American Opportunity

credit [(100% $2,000) + (25% $2,000)] for both Lora’s and Sam’s expenses.

– In total, a $5,000 American Opportunity credit.

47

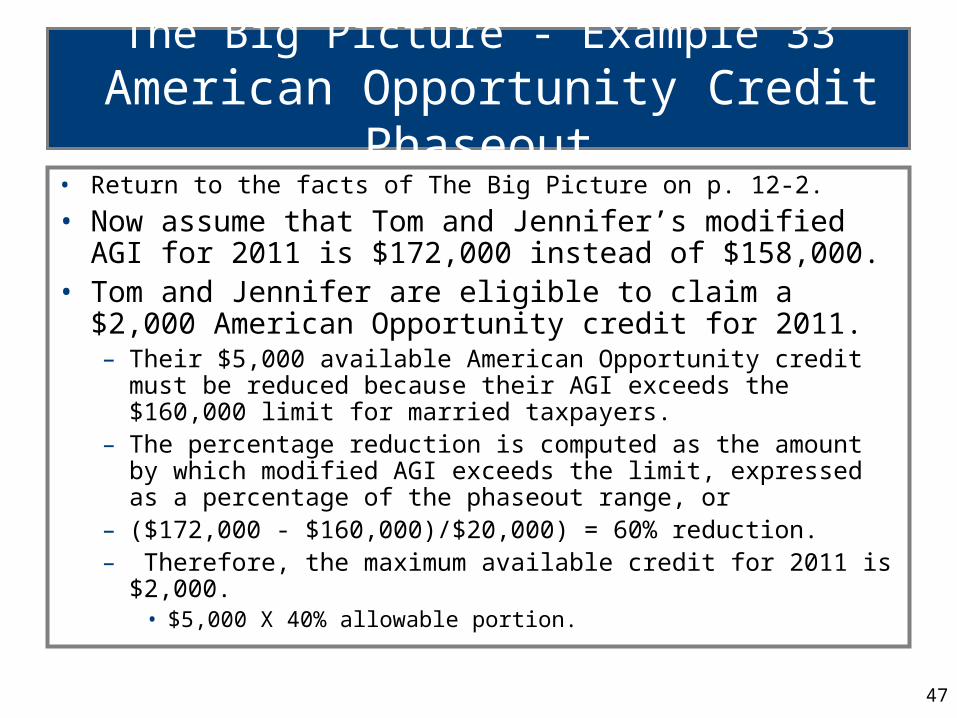

The Big Picture - Example 33 American Opportunity Credit Phaseout

• Return to the facts of The Big Picture on p. 12-2.

• Now assume that Tom and Jennifer’s modified AGI for 2011 is $172,000 instead of $158,000.

• Tom and Jennifer are eligible to claim a $2,000 American Opportunity credit for 2011. – Their $5,000 available American Opportunity credit must be reduced

because their AGI exceeds the $160,000 limit for married taxpayers. – The percentage reduction is computed as the amount by which

modified AGI exceeds the limit, expressed as a percentage of the phaseout range, or

– ($172,000 - $160,000)/$20,000) = 60% reduction.– Therefore, the maximum available credit for 2011 is $2,000.

• $5,000 X 40% allowable portion.

48

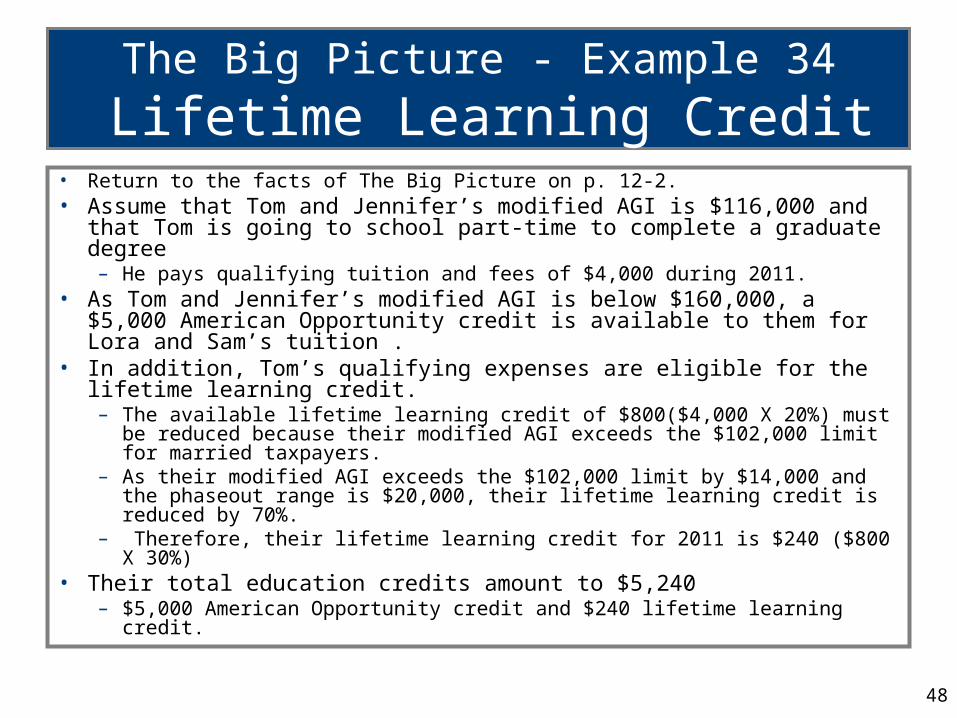

The Big Picture - Example 34

Lifetime Learning Credit• Return to the facts of The Big Picture on p. 12-2. • Assume that Tom and Jennifer’s modified AGI is $116,000 and that Tom is

going to school part-time to complete a graduate degree – He pays qualifying tuition and fees of $4,000 during 2011.

• As Tom and Jennifer’s modified AGI is below $160,000, a $5,000 American Opportunity credit is available to them for Lora and Sam’s tuition .

• In addition, Tom’s qualifying expenses are eligible for the lifetime learning credit. – The available lifetime learning credit of $800($4,000 X 20%) must be reduced

because their modified AGI exceeds the $102,000 limit for married taxpayers.– As their modified AGI exceeds the $102,000 limit by $14,000 and the phaseout

range is $20,000, their lifetime learning credit is reduced by 70%.– Therefore, their lifetime learning credit for 2011 is $240 ($800 X 30%)

• Their total education credits amount to $5,240 – $5,000 American Opportunity credit and $240 lifetime learning credit.

49

First-Time Homebuyer Credit (slide 1 of 5)

• For home purchases from January 1, 2009 through April 30, 2010, a credit of 10% of the purchase price is allowed for first-time buyers– Max credit is $8,000 ($4,000 for married filing separately)

• Single and married persons filing jointly are treated alike– Each is subject to the same $8,000 maximum

– Only available if purchase price of home is $800,000 or less

• The credit is phased out for modified AGI between $125,000 and $145,000 for single taxpayers ($225,000 and $245,000 for MFJ)

50

First-Time Homebuyer Credit (slide 2 of 5)

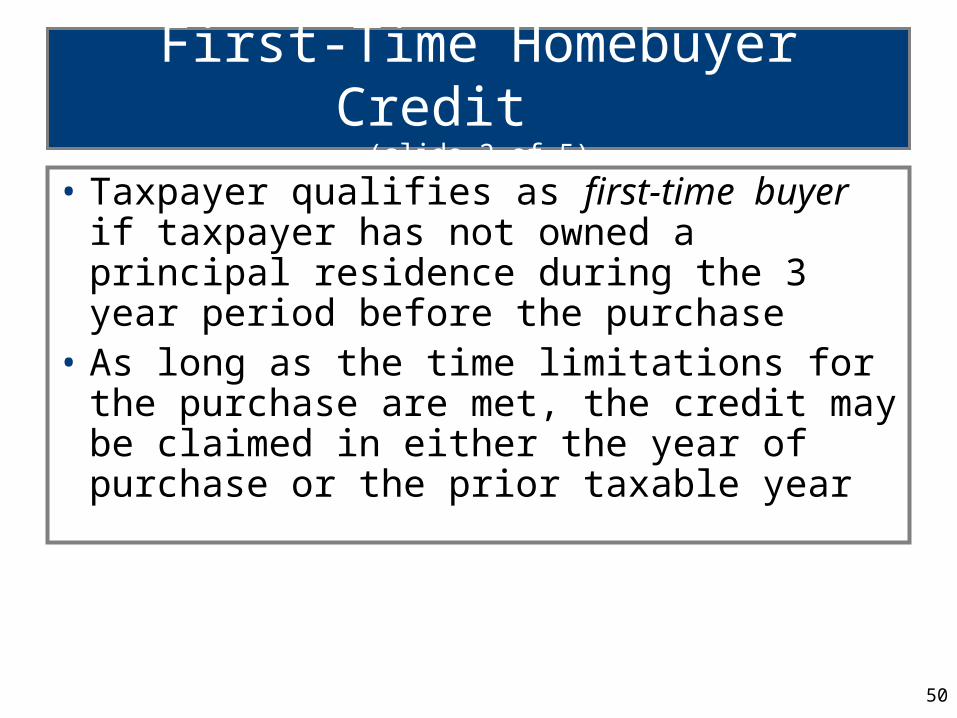

• Taxpayer qualifies as first-time buyer if taxpayer has not owned a principal residence during the 3 year period before the purchase

• As long as the time limitations for the purchase are met, the credit may be claimed in either the year of purchase or the prior taxable year

51

First-Time Homebuyer Credit (slide 3 of 5)

• For homes purchased after 11-06-09, credit is available to existing homeowners who are long-term residents– Must have maintained the same principal residence

for 5 of the last 8 years– Max credit is limited to $6,500 ($3,250 for married

individuals filing separately)

52

First-Time Homebuyer Credit (slide 4 of 5)

• The homebuyer credit contains a recapture provision– Provision is waived for homes purchased after December

31, 2008 (even if the credit is claimed in 2008)

• For homes purchased in 2008, credit must be repaid beginning 2 years after home is purchased– Repaid in equal installments over 15 years

– If disposed of before the 15-year period is up, recapture of the unpaid balance occurs

53

First-Time Homebuyer Credit (slide 5 of 5)

• Homes purchased after December 31, 2008 are also subject to an accelerated recapture rule– If disposed of within 36 months from the date of purchase

or if the property ceases to be taxpayer’s principal residence, the entire credit must be recaptured

• Recapture cannot exceed any gain from the sale

• No recapture upon the death of taxpayer, involuntary conversion, or transfer between spouses incident to a divorce

• The Homebuyer Credit is a refundable credit– Thus, in certain situations, it could generate a payment

from the IRS in excess of any tax liability

54

Credit For Certain Retirement Plan Contributions

• Credit was enacted to encourage low and middle income taxpayers to contribute to qualified retirement plans

• Eligible contributions of up to $2,000 qualify• Credit rate depends on level of AGI and filing status

– Maximum credit is $1,000 ($2,000 × 50%)

• To qualify, must be at least 18 years old and not a dependent of another taxpayer or a full-time student

55

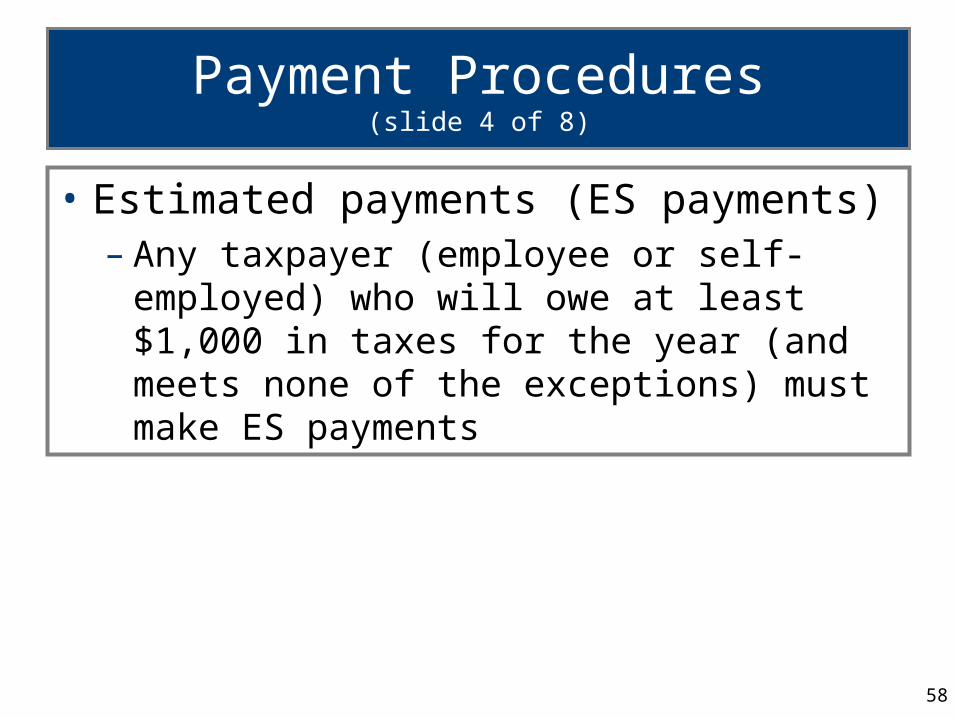

Payment Procedures(slide 1 of 8)

• Employer is responsible for withholding income taxes and employees’ share of FICA employment taxes (Social Security and Medicare)

• Also, employer must match FICA and pay full cost of FUTA (unemployment taxes)

56

Payment Procedures(slide 2 of 8)

• Social Security & Medicare– 2011 rates

• Social Security: 4.2% of first $106,800 wages– The Tax Relief Act of 2010 reduced the employee’s (but not the

employer’s) Social Security tax rate from 6.2% to 4.2% for 2011

• Medicare: 1.45% of all wages

– If employee is overwithheld for Social Security, excess is refundable credit

57

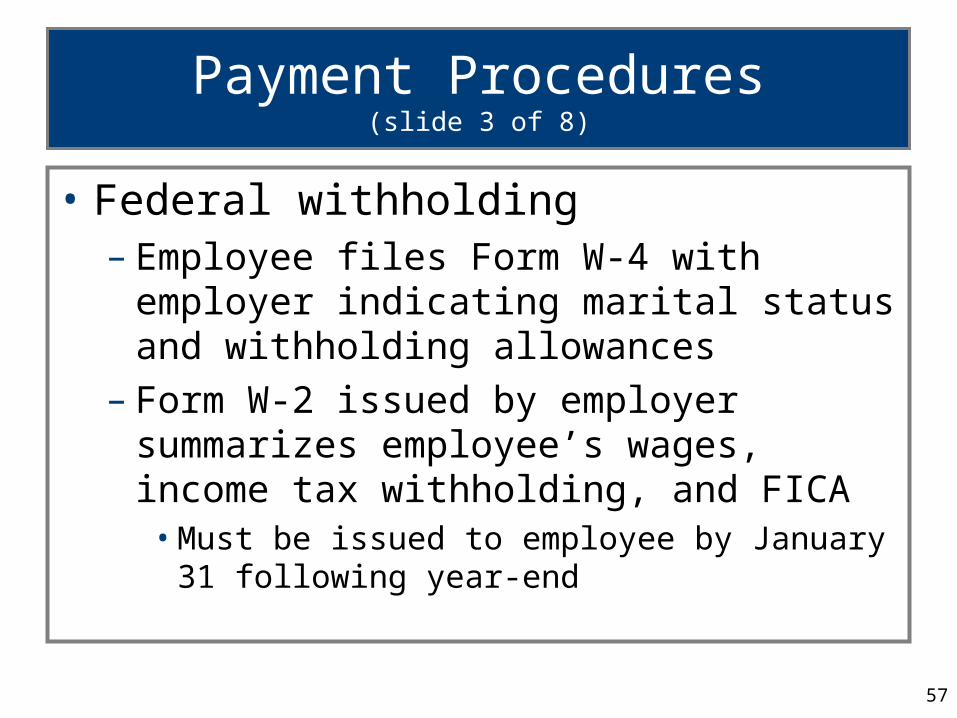

Payment Procedures(slide 3 of 8)

• Federal withholding– Employee files Form W-4 with employer

indicating marital status and withholding allowances

– Form W-2 issued by employer summarizes employee’s wages, income tax withholding, and FICA

• Must be issued to employee by January 31 following year-end

58

Payment Procedures(slide 4 of 8)

• Estimated payments (ES payments)– Any taxpayer (employee or self-employed) who

will owe at least $1,000 in taxes for the year (and meets none of the exceptions) must make ES payments

59

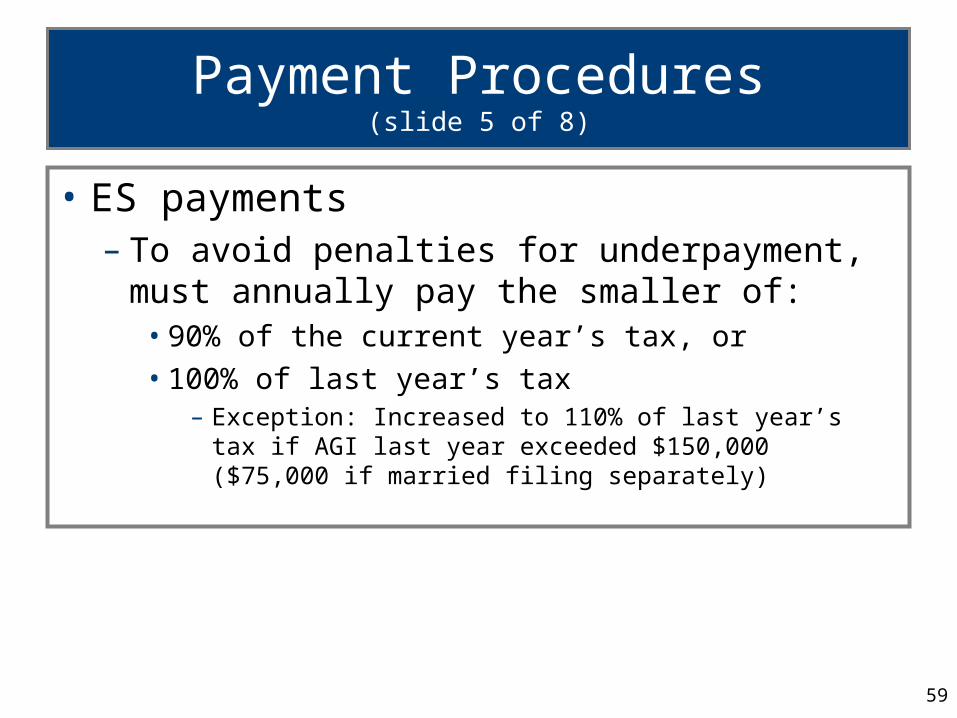

Payment Procedures(slide 5 of 8)

• ES payments– To avoid penalties for underpayment, must

annually pay the smaller of:• 90% of the current year’s tax, or

• 100% of last year’s tax– Exception: Increased to 110% of last year’s tax if AGI last

year exceeded $150,000 ($75,000 if married filing separately)

60

Payment Procedures(slide 6 of 8)

• ES payments– For calendar year individual taxpayer, ES

payments of 1/4 of annual amount are due• April 15, June 15, and September 15 of the tax year, and

January 15 of the following year

61

Payment Procedures(slide 7 of 8)

• Self-employment tax– Taxpayers with net self-employment earnings of at

least $400 must pay self-employment tax• 2011 rates

– Social Security: 10.4% of first $106,800 net self-employment income

» Normally the rate is 12.4%– Medicare: 2.9% of all net self-employment income

• These rates are twice what an employee pays on wages

62

Payment Procedures(slide 8 of 8)

• Self-employment tax– Taxpayer receives a deduction from net self-employment

income of 7.65% for purposes of calculating the actual self-employment tax

– Normally, the taxpayer receives a for AGI deduction for 50% of the self-employment tax paid

• Due to the 2% Social Security rate reduction in 2011, the income tax deduction is computed at the rate of 59.6% of the Social Security tax paid plus one-half of the Medicare tax paid

63

Refocus On The Big Picture (slide 1 of 2)

• Recent tax legislation made significant changes in education tax credits.

• The American Opportunity tax credit provides some relief for Tom and Jennifer Snyder.– Both Lora and Sam qualify for a $2,500 American Opportunity credit

in 2011. • 100% of the first $2,000 and 25% of the next $2,000 of qualified expenses.

– These credits are phased out for married taxpayers’ as AGI exceeds $160,000.

• The total education credits available to the Snyders on their 2011 income tax return is $5,240.– Further, this credit may be used to offset any AMT liability.– A portion of the credits is refundable to the Snyders.

64

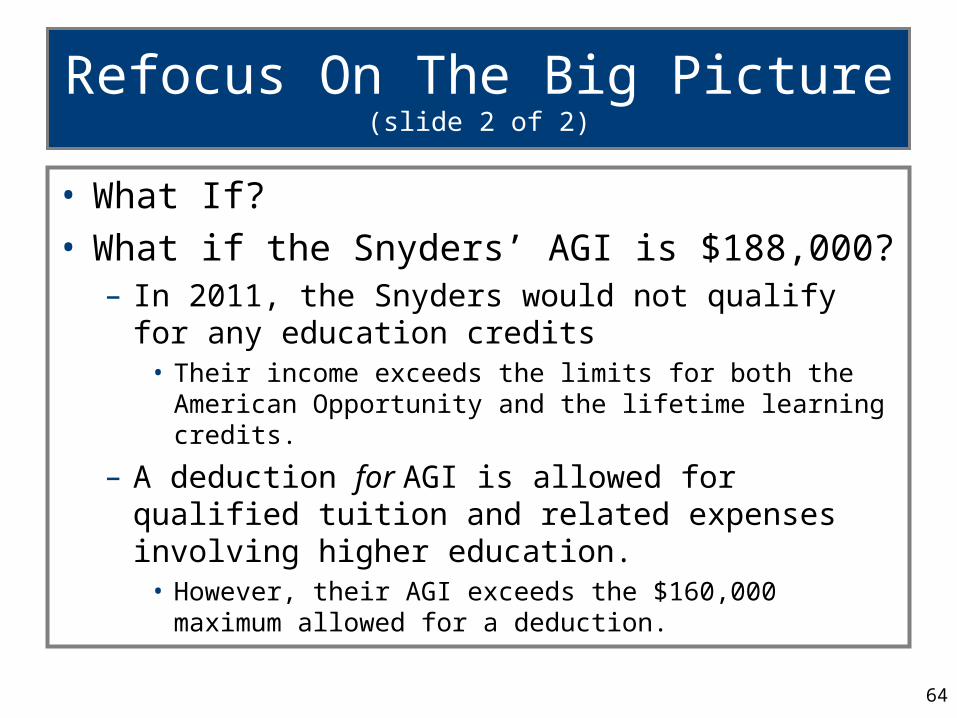

Refocus On The Big Picture (slide 2 of 2)

• What If?• What if the Snyders’ AGI is $188,000?

– In 2011, the Snyders would not qualify for any education credits

• Their income exceeds the limits for both the American Opportunity and the lifetime learning credits.

– A deduction for AGI is allowed for qualified tuition and related expenses involving higher education.

• However, their AGI exceeds the $160,000 maximum allowed for a deduction.

© 2012 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. 65

If you have any comments or suggestions concerning this PowerPoint Presentation for South-Western Federal Taxation, please contact:

Dr. Donald R. Trippeer, CPA [email protected]

SUNY Oneonta