Chapter 12-1. Chapter 12-2 Accounting Information Systems, 1 st Edition Administrative Processes and...

31

Chapter 12-1

-

Upload

luke-conley -

Category

Documents

-

view

227 -

download

1

Transcript of Chapter 12-1. Chapter 12-2 Accounting Information Systems, 1 st Edition Administrative Processes and...

Chapter 12-1

Chapter 12-2 Accounting Information Systems, 1st Edition

Administrative Processes and Controls

Chapter 12-3

1. An introduction to administrative processes

2. Source of capital processes

3. Investment processes

4. Risks and controls in capital and investment processes

5. General ledger processes

6. Risks and controls and risks in general ledger processes

7. Reporting as an output of the general ledger processes

8. Ethical issues related to administrative processes and reporting

9. Corporate governance in administrative processes and reporting

Study ObjectivesStudy ObjectivesStudy ObjectivesStudy Objectives

Chapter 12-4

Three administrative processes described in this chapter:

1. Source of capital processes

2. Investment processes

3. General ledger processes

Administrative ProcessesAdministrative ProcessesAdministrative ProcessesAdministrative Processes

Chapter 12-5

Administrative processes are transactions and activities that either are specifically authorized by top managers or are used by managers to perform administrative functions.

First set of processes: Examples include sale of stocks or bonds, the initiation of loans, bonds or notes payable, and the investment of funds in marketable securities.

Second set of processes: financial information beingrecorded in general ledger accounts.

SO 1 An introduction to administrative processesSO 1 An introduction to administrative processes

Introduction to Administrative Introduction to Administrative ProcessesProcessesIntroduction to Administrative Introduction to Administrative ProcessesProcesses

Chapter 12-6

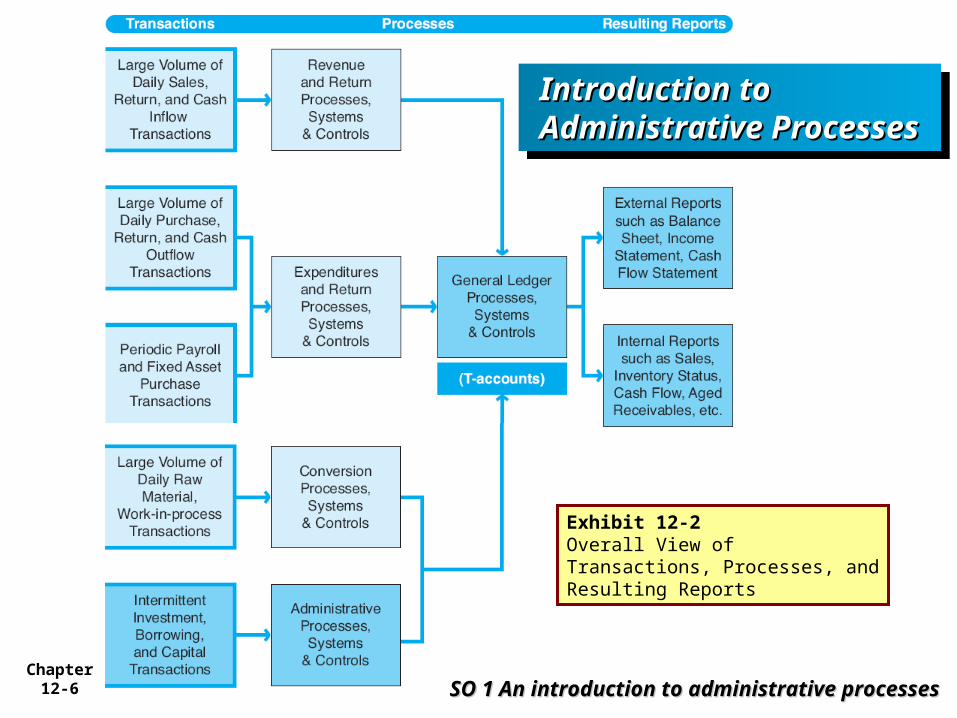

Exhibit 12-2Overall View ofTransactions, Processes, andResulting Reports

Introduction to Introduction to Administrative Administrative ProcessesProcesses

Introduction to Introduction to Administrative Administrative ProcessesProcesses

SO 1 An introduction to administrative SO 1 An introduction to administrative processesprocesses

Chapter 12-7

Which of the following is not part of an administrative process?

a. The sale of stock

b. The sale of bonds

c. The write-off of bad debts

d. The purchase of marketable securities

Quick ReviewQuick Review

SO 1 An introduction to administrative processesSO 1 An introduction to administrative processes

Introduction to Administrative Introduction to Administrative ProcessesProcessesIntroduction to Administrative Introduction to Administrative ProcessesProcesses

Chapter 12-8

Capital is the funds used to acquire long-term, capital assets of an organization.

Source of capital processes are those processes to

authorize the raising of capital,

the execution of raising capital, and

the proper accounting of that capital.

SO 2 Source of capital processesSO 2 Source of capital processes

Sources of Capital ProcessesSources of Capital ProcessesSources of Capital ProcessesSources of Capital Processes

Chapter 12-9

SO 2 Source of capital SO 2 Source of capital processesprocesses

Sources of Sources of Capital Capital ProcessesProcesses

Sources of Sources of Capital Capital ProcessesProcesses

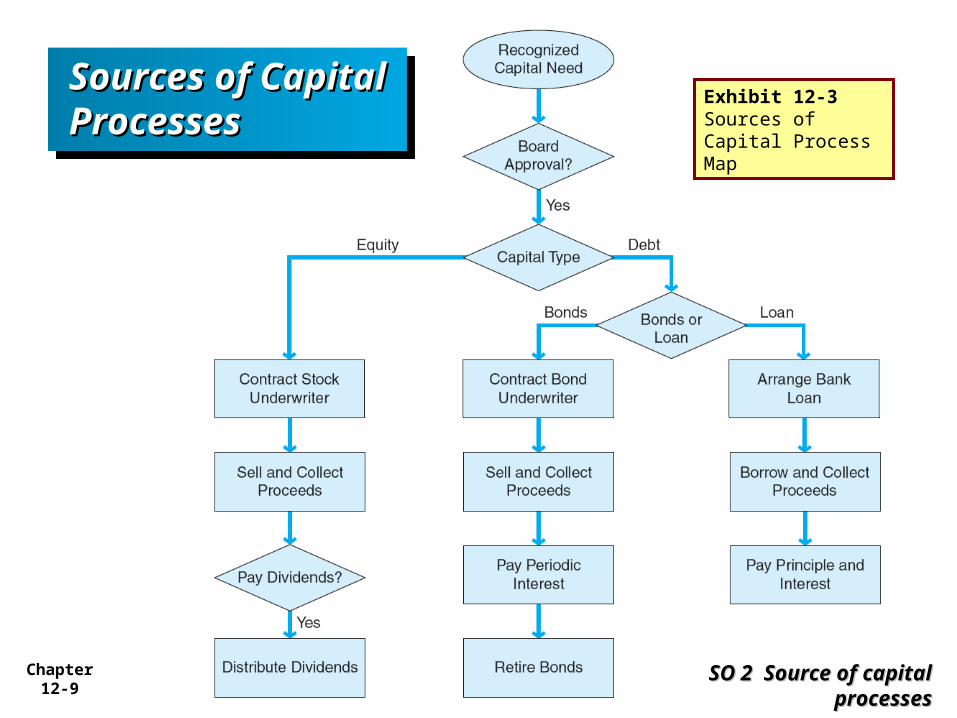

Exhibit 12-3Sources of Capital Process Map

Chapter 12-10

Which of the following statements is not true regarding source of capital transactions?

a. These processes should not be initiated unless there is specific authorization by management at a top level.

b. Source of capital processes will result in potential dividend or interest payments.

c. Retirement of debt is a source of capital process.

d. The fact that these transactions and processes cannot occur without oversight by top management means other controls are not necessary.

Quick ReviewQuick Review

SO 2 Source of capital processesSO 2 Source of capital processes

Sources of Capital ProcessesSources of Capital ProcessesSources of Capital ProcessesSources of Capital Processes

Chapter 12-11

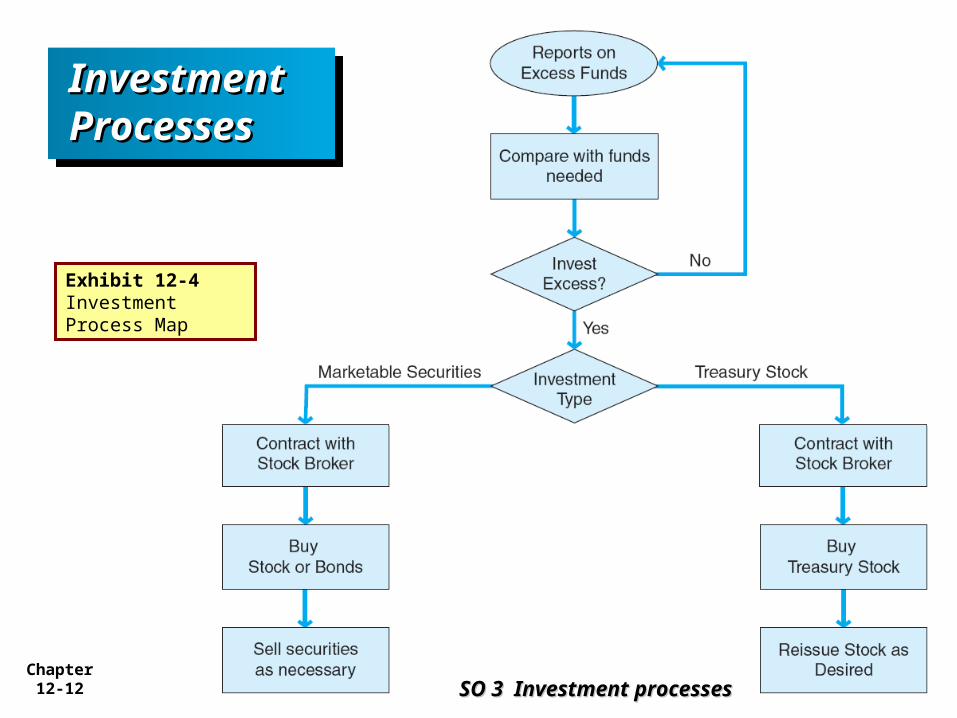

Management should properly manage, or administer, the investment of excess funds.

Investment processes are those processes which

authorize,

execute,

manage, and

properly account for

investments of excess funds.SO 3 Investment processesSO 3 Investment processes

Investment ProcessesInvestment ProcessesInvestment ProcessesInvestment Processes

Chapter 12-12 SO 3 Investment SO 3 Investment

processesprocesses

Investment Investment ProcessesProcessesInvestment Investment ProcessesProcesses

Exhibit 12-4Investment Process Map

Chapter 12-13

The officer within a corporation that usually has oversight responsibility for investment processes is the

a. controller.

b. treasurer.

c. chief executive officer (CEO).

d. chief accounting officer (CAO).

Quick ReviewQuick Review

SO 3 Investment processesSO 3 Investment processes

Investment ProcessesInvestment ProcessesInvestment ProcessesInvestment Processes

Chapter 12-14 SO 4 Risks and controls in capital and investment processesSO 4 Risks and controls in capital and investment processes

Risks and Controls in Capital and Risks and Controls in Capital and Investment ProcessesInvestment ProcessesRisks and Controls in Capital and Risks and Controls in Capital and Investment ProcessesInvestment Processes

For both source of capital processes and investment processes, the important control is the specific authorization and oversight by top management.

Generally, the risks are not related to employee fraud, but are instead related to management fraud.

Chapter 12-15

Which of the following statements is not true regarding internal controls of capital and investment processes?

a. Internal controls aimed at preventing and detecting employee fraud in capital and investment processes are not as effective.

b. Top management fraud, rather than employee fraud, is more likely to occur.

c. Any fraud is likely to involve manipulating capital and investment processes.

d. Because of top management oversight, the auditor need not review these processes.

Quick ReviewQuick Review

Risks and ControlsRisks and ControlsRisks and ControlsRisks and Controls

Chapter 12-16 SO 5 General ledger processesSO 5 General ledger processes

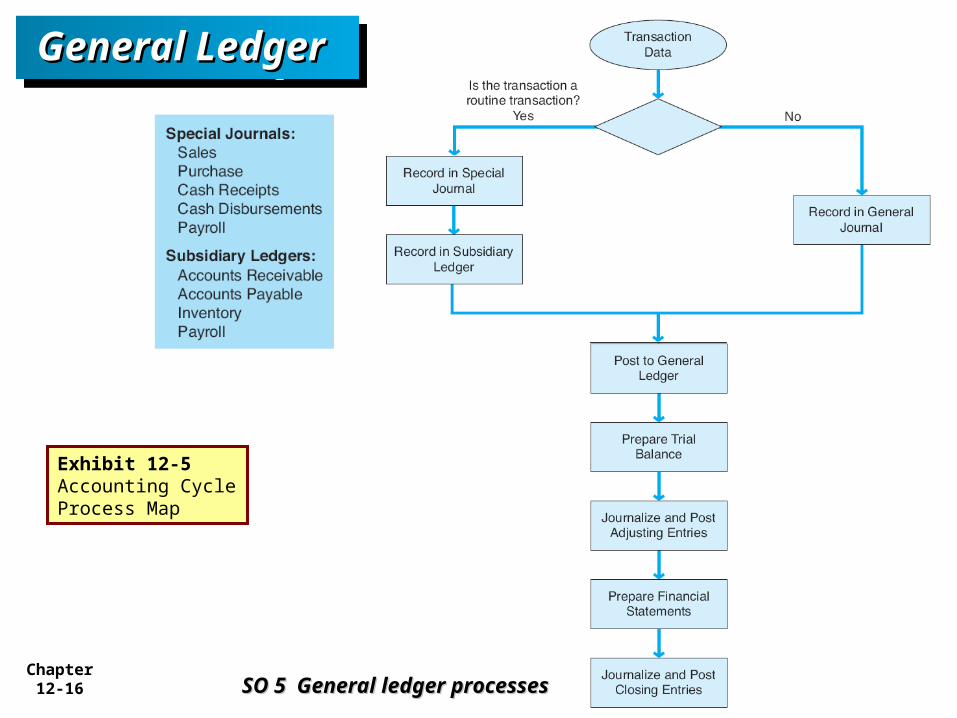

Exhibit 12-5Accounting Cycle Process Map

General General Ledger Ledger General General Ledger Ledger

Chapter 12-17

Which of the following statements is true?

a. Routine transactions are recorded in the general journal.

b. Nonroutine transactions are entered in the general journal.

c. Nonroutine transactions are recorded in a subsidiary ledger.

d. Nonroutine transactions are recorded in a special journal.

Quick ReviewQuick Review

SO 5 General ledger processesSO 5 General ledger processes

General Ledger ProcessGeneral Ledger ProcessGeneral Ledger ProcessGeneral Ledger Process

Chapter 12-18

Regarding subsidiary ledgers and general ledger control accounts, which of the following is not true?

a. Total balances in a subsidiary ledger should always equal the balance in the corresponding general ledger account.

b. The general ledger maintains details of subaccounts.

c. Control is enhanced by separating the subsidiary ledger from the general ledger.

d. Reconciling a subsidiary ledger to the general ledger can help to detect errors or fraud.

Quick ReviewQuick Review

SO 5 General ledger processesSO 5 General ledger processes

General Ledger ProcessGeneral Ledger ProcessGeneral Ledger ProcessGeneral Ledger Process

Chapter 12-19 SO 6 Risks and controls and risks in general ledger processesSO 6 Risks and controls and risks in general ledger processes

Risks and Controls in General Ledger Risks and Controls in General Ledger ProcessesProcessesRisks and Controls in General Ledger Risks and Controls in General Ledger ProcessesProcesses

Common procedures associated with the general ledger:

Authorization of transactions

Segregation of duties

Adequate records and documents

Security of the general ledger and documents

Independent checks and reconciliation

Cost-benefit considerations

Chapter 12-20

Which of the following statements regarding the authorization of general ledger posting is not true?

a. Posting to the general ledger always requires specific authorization.

b. User IDs and passwords can serve as authorization to post transactions to the general ledger.

c. A journal voucher serves as authorization for manual systems.

d. As IT systems become more automated, the authorization of general ledger posting is moved to lower levels of employees.

Quick ReviewQuick Review

SO 6 Risks and controls and risks in general ledger processesSO 6 Risks and controls and risks in general ledger processes

Risks and Controls in General Ledger Risks and Controls in General Ledger ProcessesProcessesRisks and Controls in General Ledger Risks and Controls in General Ledger ProcessesProcesses

Chapter 12-21

In a manual system with proper segregation of duties, an employee in the general ledger department should only

a. authorize posting to the general ledger.

b. post transactions to the general ledger.

c. reconcile the subsidiary ledger to the general ledger.

d. post transactions to the subsidiary ledger.

Quick ReviewQuick Review

SO 6 Risks and controls and risks in general ledger processesSO 6 Risks and controls and risks in general ledger processes

Risks and Controls in General Ledger Risks and Controls in General Ledger ProcessesProcessesRisks and Controls in General Ledger Risks and Controls in General Ledger ProcessesProcesses

Chapter 12-22 SO 7 Reporting as an output of the general ledger processesSO 7 Reporting as an output of the general ledger processes

Reporting as an Output of the General Reporting as an Output of the General Ledger ProcessesLedger ProcessesReporting as an Output of the General Reporting as an Output of the General Ledger ProcessesLedger Processes

External ReportingFour general purpose financial statements

balance sheet,

income statement,

statement of cash flows, and

statement of retained earnings

are created from general ledger account balances.

Chapter 12-23 SO 7 Reporting as an output of the general ledger processesSO 7 Reporting as an output of the general ledger processes

Reporting as an Output of the General Reporting as an Output of the General Ledger ProcessesLedger ProcessesReporting as an Output of the General Reporting as an Output of the General Ledger ProcessesLedger Processes

Internal ReportingInternal reports are usually not financial

statements, but reports tailored to specific needs of each management level and function. Many factors affect the type of report provided

Type of organization

Function managed

Time horizon

Chapter 12-24

Which of the following statements about reporting is true?

a. External users need detailed, rather than summarized, information.

b. All reports, internal and external, are derived only from general ledger data.

c. All organizations need similar internal reports.

d. Internal reports are tailored to the specific needs of each management level and function.

Quick ReviewQuick Review

SO 7 Reporting as an output of the general ledger processesSO 7 Reporting as an output of the general ledger processes

Reporting as an Output of the General Reporting as an Output of the General Ledger Ledger Reporting as an Output of the General Reporting as an Output of the General Ledger Ledger

Chapter 12-25

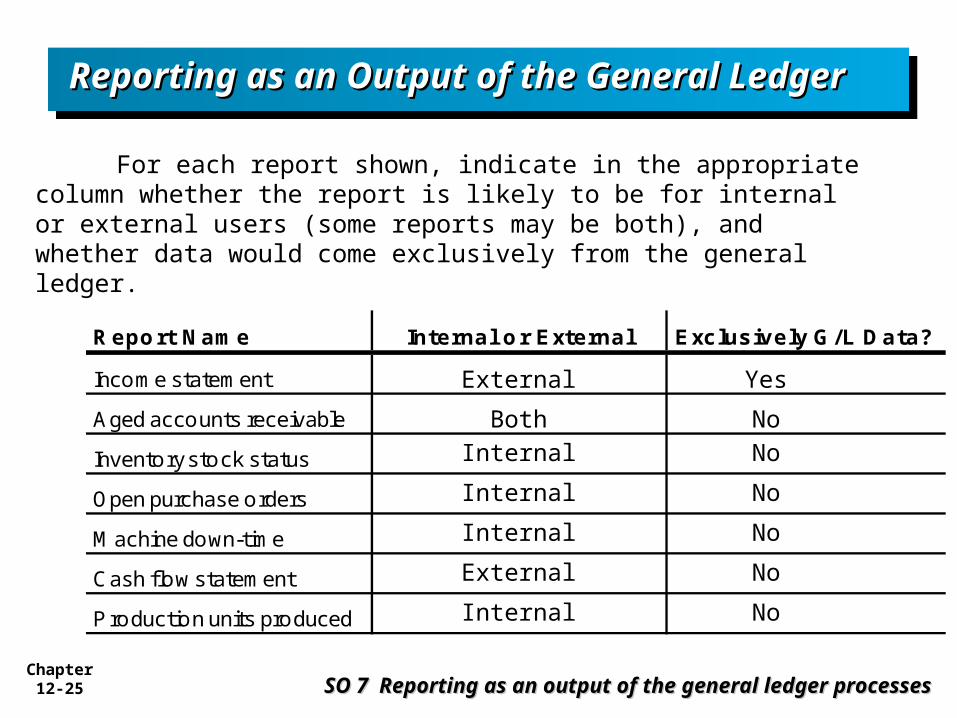

For each report shown, indicate in the appropriate column whether the report is likely to be for internal or external users (some reports may be both), and whether data would come exclusively from the general ledger.

SO 7 Reporting as an output of the general ledger processesSO 7 Reporting as an output of the general ledger processes

Reporting as an Output of the General Reporting as an Output of the General Ledger Ledger Reporting as an Output of the General Reporting as an Output of the General Ledger Ledger

Report Name Internal or External Exclusively G/L Data?

Income statement

Aged accounts receivable

Inventory stock status

Open purchase orders

Machine down-time

Cash flow statement

P roduction units produced

External

BothInternal

Internal

Internal

External

Internal

Yes

NoNo

No

No

No

No

Chapter 12-26 SO 8 Ethical issues related to administrative processes and SO 8 Ethical issues related to administrative processes and

reportingreporting

Ethical Issues Related to Administrative Ethical Issues Related to Administrative Processes and ReportingProcesses and ReportingEthical Issues Related to Administrative Ethical Issues Related to Administrative Processes and ReportingProcesses and Reporting

Reasons that unethical and fraudulent behavior would tend to be management-initiated.

First, in a properly controlled system, employees do not have access to related assets or source documents.

Second, administrative processes are tightly controlled and supervised by top management.

Finally, routine nature of processes such as sales, purchasing, payroll, and conversion generates a huge volume of transactions.

Chapter 12-27 SO 8 Ethical issues related to administrative processes and SO 8 Ethical issues related to administrative processes and

reportingreporting

Ethical Issues Related to Administrative Ethical Issues Related to Administrative Processes and ReportingProcesses and ReportingEthical Issues Related to Administrative Ethical Issues Related to Administrative Processes and ReportingProcesses and Reporting

Unethical Management Behavior in Capital Sources and Investing

Management should

be honest in the financial statements presented, footnote disclosures, and any related disclosures.

not try to mislead creditors about

the financial status of the company or

its ability to repay any borrowing.

Chapter 12-28 SO 8 Ethical issues related to administrative processes and SO 8 Ethical issues related to administrative processes and

reportingreporting

Ethical Issues Related to Administrative Ethical Issues Related to Administrative Processes and ReportingProcesses and ReportingEthical Issues Related to Administrative Ethical Issues Related to Administrative Processes and ReportingProcesses and Reporting

Internal Reporting ethical Issues

Top management has an ethical obligation to use financial and other reports to encourage beneficial and ethical behavior. Reports to lower level managers are usually used for two purposes.

1. Feedback to lower level managers.

2. Used by upper management to evaluate and reward the performance of lower level managers.

Chapter 12-29

Which of the following is not an area of measure in a balanced scorecard?

a. Vendor

b. Customer

c. Financial

d. Learning and growth

Quick ReviewQuick Review

SO 8 Ethical issues related to administrative processes and SO 8 Ethical issues related to administrative processes and reportingreporting

Ethical Issues Related to Administrative Ethical Issues Related to Administrative Processes and ReportingProcesses and ReportingEthical Issues Related to Administrative Ethical Issues Related to Administrative Processes and ReportingProcesses and Reporting

Chapter 12-30 SO 9 Corporate governance in administrative processes and SO 9 Corporate governance in administrative processes and

reportingreporting

Corporate Governance in Administrative Corporate Governance in Administrative Processes and ReportingProcesses and ReportingCorporate Governance in Administrative Corporate Governance in Administrative Processes and ReportingProcesses and Reporting

Setting and monitoring financial goals, and establishing and maintaining reliable accounting journals and ledgers so that performance can be properly reported, are important to effective corporate governance.

In addition, internal controls and ethical practices within the administrative processes help ensure proper financial stewardship of a company’s administrative resources.

Chapter 12-31

Copyright © 2008 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

CopyrightCopyrightCopyrightCopyright