Chapter 11 Corporate Income Tax - Accountax Individuals Lecture XI Presentation.pdfChapter 11...

31

Chapter 11 Corporate Income Tax 2012 Cengage Learning Income Tax Fundamentals 2012 Gerald E. Whittenburg Martha Altus-Buller

-

Upload

hoangtuong -

Category

Documents

-

view

215 -

download

2

Transcript of Chapter 11 Corporate Income Tax - Accountax Individuals Lecture XI Presentation.pdfChapter 11...

Chapter 11Corporate Income Tax

2012 Cengage Learning

Income Tax Fundamentals 2012

Gerald E. Whittenburg

Martha Altus-Buller

Learning Objectives

This chapter pertains to corporations�Calculate tax liability using tax rates

�Compute basic capital gains/losses

�Ascertain how special deduction may affect taxable income

� Identify components of Schedule M-1

�Outline corporate tax return filing and estimated tax payment requirements

�Understand how S-Corporations operate and are taxed

�Understand basic tax rules when forming entity

�Describe accumulated earnings and personal holding company taxes

�Define elements of alternative minimum tax calculation

2012 Cengage Learning

Corporate Tax Rates

�Corporate rates are progressive ° Marginal rates are from 15% to 39%, depending on taxable income

° There are eight brackets

° There are a number of ‘tax bubbles’ – these occur when tax rate schedules recapture savings from prior brackets

�For corporations with large income (more than $18.33 million) the rate is a flat 35%

�Qualified personal service corps taxed at flat 35%◦ Architects, CPAs, consultants, etc.

2012 Cengage Learning

Example Corporate Tax Rates

Example

Johnson & Kelby Inc. (a dental products wholesaler) has taxable income of $300,000 for the current year. What is the corporation’s tax liability? How would the answer change if it was an architectural firm, and Johnson & Kelby were principals who provided personal services to their clients?

2012 Cengage Learning

Solution

Example

Johnson & Kelby Inc. (a dental products wholesaler) has taxable

income of $300,000 for the current year. What is the

corporation’s tax liability? How would the answer change if it

was an architectural firm, and Johnson & Kelby were

principals who provided personal services to their clients?

Solution

Corporate tax = $100,250

$22,250 + (39%)($300,000 – 100,000)

If Johnson & Kelby is a qualified personal service corporation,

corporate tax = $105,000 ($300,000 x 35%)

2012 Cengage Learning

Corporate Capital Gains

�A corporation can choose from two alternative tax treatments on capital gains◦ Taxed at ordinary rates

or

◦ Elect to pay an alternative tax (35%) on net long-term capital gain (LTCG)

�Essentially equivalent to maximum regular corporate tax (no tax benefit to LTCG)

�Bottom line: there is no difference in tax on ordinary vs. capital income

2012 Cengage Learning

Dividends Received Deduction

�Corporations are allowed a deduction for a percentage of the dividends received from other corporations ◦ Attempt to alleviate triple taxation

�Dividends received deduction is allowed based upon ownership

2012 Cengage Learning

Percentage Ownership Dividends Received % Deduction

< 20% 70%

20% or more, less than 80% 80%

> 80% 100%

Dividends received deduction is limited by %

of corporate taxable income shown above

(calculated before certain deductions)

Organizational Expenditures & Start Up Costs

� Organizational expenditures pertain to LLCs, corporations and partnerships

� Start up costs can be incurred by any organization, including a sole proprietorship and entities mentioned above

◦ Examples of these type of costs include◦ Investigatory costs to look at a business before deciding whether or not to pursue it

◦ Legal/accounting services incidental to organization, costs of a temporary board of directors and state incorporation fees

◦ Preopening costs such as advertising expenses, employee training costs, etc.

2012 Cengage Learning

Amortization of Organizational Expenditures &

Start Up Costs

�Organizational expenditures and start up costs are capitalized and then amortized over 180 months

� However, can make election to deduct up to $5,000 of organization costs in the year corporation begins business◦ $5,000 amount is reduced $1 for each $1 that organizational expenses exceed $50,000

2012 Cengage Learning

Charitable Contributions

�Corporations are allowed a deduction for charitable contributions◦ Cash basis taxpayers can deduct when paid◦ Accrual basis taxpayers have until the 15th day of the third month following year-end to contribute, as long as pledge is made by year-end

�Charitable contributions limited to 10% of taxable income*◦ Carry forward unused deduction for five years

*Calculated before any loss carry backs, net operating

losses (NOLs) or the dividend received deduction

2012 Cengage Learning

Example Charitable Contributions

Example

Ferndale Corp. had net operating income of $400,000 for the current year and made charitable contributions of $60,000. A dividends received deduction of $80,000 is included in the net operating income calculation. What is Ferndale’s charitable contribution deduction; what is the charitable contribution carry forward?

2012 Cengage Learning

Solution

Example

Ferndale Corp. had net operating income of $400,000 for the current year and made charitable contributions of $60,000. A dividends received deduction (DRD) of $80,000 is included in the net operating income calculation. What is Ferndale’s charitable contribution deduction; what is the carry forward?

Solution

The charitable contribution deduction is $48,000

($400,000 + 80,000) x 10% = $48,000 limit*

Therefore, carry forward is $32,000 ($80,000 – 48,000)

*Note: had to add back DRD first!!

2012 Cengage Learning

Reconciliation of Income (Loss) per Books with Income Per Return

� Schedule M-1 of Form 1120 reconciles accounting (book) income to taxable income

� Amounts added to book income (left column)◦ Federal tax expense

◦ Capital losses

◦ Income recorded on tax return but not on books

◦ Expenses recorded on books but not on tax return

� Amounts deducted from book income (right column) ◦ Income recorded on books but not on tax return

◦ Expenses recorded on tax return but not on books

See chapter for other items included on Schedule M-1

2012 Cengage Learning

Schedule UTP Now Required

�Schedule UTP (Uncertain Tax Position) is required

beginning in 2010 for large corporations

� It requires that the corporation disclose any tax

positions taken on prior year’s returns that are

uncertain

o Allows the IRS to engage in more pointed and directed

audit

o Intended to generate additional revenue

2012 Cengage Learning

Filing Requirements & Estimated Tax

�Form 1120 filed for regular corporation

�Form 1120S filed for S Corporation◦ Returns are due by the 15th day of the third month after year-end

◦ Can file Form 7004 and receive automatic 6-month extension

�Corporations must make estimated tax payments in similar manner as self-employed taxpayers, in four installments

2012 Cengage Learning

S Corporations

�Certain qualified small business corporations may elect to be taxed in a manner similar to partnerships

�Qualified small business corporation may elect S Corporation status if several criteria apply◦ Operates as a domestic corporation

◦ Has 100 or fewer shareholders

� Shareholders may not be corporations or partnerships

◦ Has only one class of stock

◦ Has only shareholders that are U.S. citizens or resident aliens

2012 Cengage Learning

S Corporations

� Corporation must make election of S status in a prior

year ◦ Or within 2-1/2 months of the current tax year

� S Corp status stays in effect until revocation*◦ Status can be voluntarily revoked by consent of shareholders

or

◦ Involuntarily revoked� If corporation ceases to be a small business corporation

or

� If corporate passive income is 25% or more for three consecutive

years and corporation has accumulated earnings and profits at the

end of each of those years

*Election is terminated on the date status is revoked

2012 Cengage Learning

Example S Corporation Election

Example

Swannak Thermography Corporation is a calendar year corporation that makes an S Corporation election on May 25, 2011. In which year may the corporation first be treated as an S Corporation?

2012 Cengage Learning

Solution

Example

Swannak Thermography Corporation is a calendar year corporation that makes an S Corporation election on May 25, 2011. In which year may the corporation first be treated as an S Corporation?

Solution

Since Swannak did not make the S Corporation election within the first 2-1/2 months of the tax year, it will be treated as a regular corporation for 2011. It will become an S Corporation for tax year 2012.

2012 Cengage Learning

Income Reporting

�Must report all elements of income and expense separately on Form 1120S

�Then each shareholder reports his/her share of these items of corporate income/expense on personal return◦ K-1 takes total shareholder income/expenses and

allocates each item to each shareholder based upon

his/her ownership percentage

If shareholder dies, his/her portion of S Corp items

will be included in shareholder’s final return

2012 Cengage Learning

Loss Reporting

�Each shareholder of an S Corp may also report his/her respective share of loss◦ Individual taxpayer cannot take a loss in excess of adjusted basis in stock

◦ If loss exceeds adjusted basis in stock plus loans, shareholder can carry it forward

� If shareholder entered/departed S Corp mid-year, must allocate losses on a daily basis

2012 Cengage Learning

S Corporation Pass Through Items

�Many items retain tax character when passing through to the S Corporation’s shareholders on individual K-1

�Examples of such items include◦ Capital gains/losses

◦ §1231 gains/losses

◦ Dividend Income

◦ Charitable contributions

◦ Tax-exempt interest

◦ Most credits

2012 Cengage Learning

Special Taxes

�S Corporations, in general, do not pay corporate taxes on their taxable income

�Certain exceptions exist such as:◦ Built-in gains tax (paid on appreciated assets that were held by corporation prior to S Corp election)

◦ Certain tax imposed if corporation has large amount of passive income, such as dividends and income

These rules are complex and will not be covered in this text

2012 Cengage Learning

Corporate Formation

� Shareholders often transfer high-value low-basis assets

to a corporation in exchange for stock in company

�No tax is due on gain from transfer of appreciated

assets if following conditions met

◦ Shareholder transferred cash or property

and

◦ Shareholder made transfer solely in exchange for stock*

� Shareholder is not providing a service and all taxpayers together

own at least 80% of stock after transaction

*If shareholder receives boot in addition to stock,

transaction may qualify for partial nonrecognition of gain

2012 Cengage Learning

Shareholder Basis in Stock

� A shareholder’s initial basis in his/her stock is calculated as follows

Basis of property transferred

Less Boot received*

Plus Gain recognized

Less Liabilities transferred

Equals Basis in stock

� The corporation has a carry-over basis in the property contributed equal to the basis in the hands of the shareholder, increased by any gain recognized by shareholder on the transfer

*Boot is any property other than stock

2012 Cengage Learning

Note: generally, corporate assumption of shareholder liabilities that are attached to property are not

considered boot received

Accumulated Earnings Tax (AET)

�Penalty tax designed to prevent a corporation from avoiding tax by retaining earnings

� 15% AET imposed on “unreasonable” accumulation of earnings; this is in addition to corporate income taxo Corporation may accumulate up to $250,000 a year that is exempt from AET tax or $150,000 for a service corporation

o May accumulate more if can prove a valid business purpose

2012 Cengage Learning

Example Accumulated Earnings Tax

Example

Xinix Corporation (a medical device manufacturing firm) has accumulated earnings of $800,000. The corporation can establish reasonable needs for $500,000 of the accumulation. What would Xinix’ accumulated earnings tax be?

2012 Cengage Learning

Solution

ExampleXinix Corporation (a medical device manufacturing firm) has accumulated earnings of $800,000. The corporation can establish reasonable needs for $500,000 of the accumulation. What would Xinix’ accumulated earnings tax be?

SolutionXinix’ AET = $45,000($800,000 – 500,000) x 15%Note: this is paid in addition to regular tax

2012 Cengage Learning

Personal Holding Company Tax

�Penalty tax designed to encourage Personal Holding Companies to distribute earnings to shareholders◦ Tax is 15% on undistributed earnings

�Corporation is not liable for both the personal holding company tax and the AET in the same year

2012 Cengage Learning

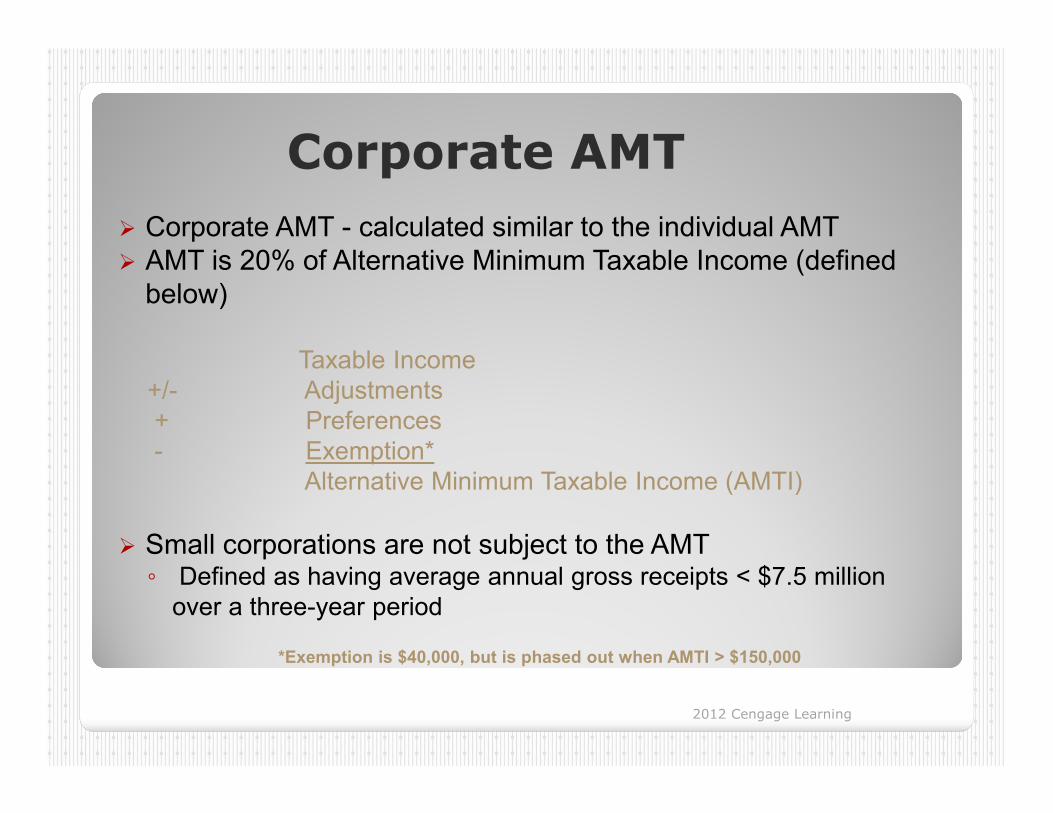

Corporate AMT

� Corporate AMT - calculated similar to the individual AMT� AMT is 20% of Alternative Minimum Taxable Income (defined below)

Taxable Income +/- Adjustments + Preferences - Exemption*

Alternative Minimum Taxable Income (AMTI)

� Small corporations are not subject to the AMT◦ Defined as having average annual gross receipts < $7.5 million over a three-year period

*Exemption is $40,000, but is phased out when AMTI > $150,000

2012 Cengage Learning

You’re Done with Chapter 112012 Cengage Learning