Changing Regulatory Environment and the Prospect of ... · 11.09.2013 2 Agenda Regulatory...

23

Changing Regulatory Environment and the Prospect of Shariah Compliant Finance İbrahim M. TURHAN, Ph.D. Chairman & CEO September 11, 2013

Transcript of Changing Regulatory Environment and the Prospect of ... · 11.09.2013 2 Agenda Regulatory...

Changing Regulatory Environment and the Prospect of Shariah Compliant Finance

İbrahim M. TURHAN, Ph.D.

Chairman & CEO

September 11, 2013

11.09.2013 2

Agenda

Regulatory Implications of 2008 Financial Crisis

Issues related to Securitization: OTC vs Organized Markets

The Prospect of Shariah Compliant Finance

Borsa İstanbul’s Vision on Islamic Finance

11.09.2013 3

Agenda

Regulatory Implications of 2008 Financial Crisis

Issues related to Securitization: OTC vs Organized Markets

The Prospect of Shariah Compliant Finance

Borsa İstanbul’s Vision on Islamic Finance

11.09.2013 4

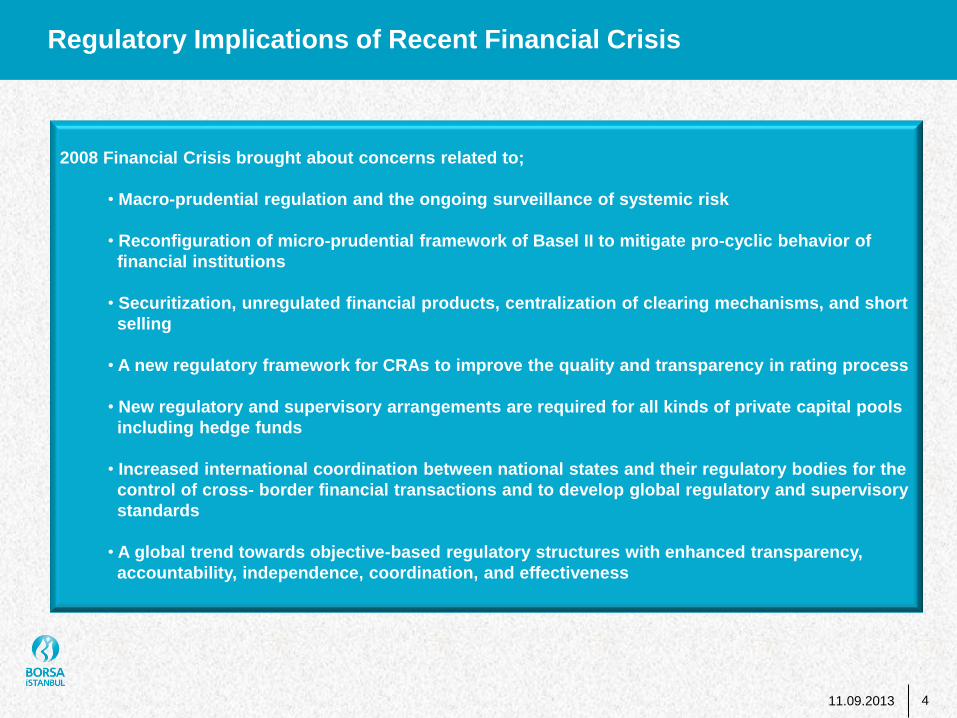

Regulatory Implications of Recent Financial Crisis

2008 Financial Crisis brought about concerns related to;

• Macro-prudential regulation and the ongoing surveillance of systemic risk

• Reconfiguration of micro-prudential framework of Basel II to mitigate pro-cyclic behavior of

financial institutions

• Securitization, unregulated financial products, centralization of clearing mechanisms, and short

selling

• A new regulatory framework for CRAs to improve the quality and transparency in rating process

• New regulatory and supervisory arrangements are required for all kinds of private capital pools

including hedge funds

• Increased international coordination between national states and their regulatory bodies for the

control of cross- border financial transactions and to develop global regulatory and supervisory

standards

• A global trend towards objective-based regulatory structures with enhanced transparency,

accountability, independence, coordination, and effectiveness

11.09.2013 5

Global Network of Regulation on Financial Markets

11.09.2013 6

Issues Related to Securitization: Organized Markets vs. OTC

“All standardized OTC derivative contracts should be traded on

exchanges or electronic trading platforms, where appropriate, and

cleared through central counterparties by end-2012 at the latest.”

G-20 Summit Statement, Pittsburgh – 2009

“The recent financial crisis exposed weaknesses in the structure of the

over-the-counter (OTC) derivatives markets that had contributed to the

build-up of systemic risk. While markets in certain OTC derivatives asset

classes continued to function well throughout the crisis, the crisis

demonstrated the potential for contagion arising from the

interconnectedness of OTC derivatives market participants and the

limited transparency of counterparty relationships. ”

Financial Stability Board, October 2010

“A series of reforms under way for OTC derivatives are affecting the way

derivatives are traded, reported, and cleared, as well as the capital

required for bilateral trading.”

IMF Global Financial Stability Report, October 2012

11.09.2013 7

Agenda

Regulatory Implications of 2008 Financial Crisis

Issues related to Securitization: OTC vs Organized Markets

The Prospect of Shariah Compliant Finance

Borsa İstanbul’s Vision on Islamic Finance

11.09.2013 8

OTC Market Information & ETFs

Notional Amounts Outstanding of OTC and Exchange Traded Derivatives (USD Trillions)

Breakdown of Contracts As of June 2012

0

100

200

300

400

500

600

700

800

Dec 2010 June 2011 Dec 2011 June 2012

601

707 648 639

68 57 56 53

OTC Traded Exchange Traded

77%

10%

4%

8%

Interest Rate Contracts Foreign exchange contracts

Credit default swaps Other Contracts

0

25

50

75

100

125

150

175 169

158

79 66

58 48

26 17 16 14 14 8 4

Global ETF Turnover* (USD Billions, 2012)

15th

(1) NYSE Euronext (US) 2,96 Tn USD

(2) NASDAQ OMX 2.89 Tn USD

BIST

11.09.2013 9

Alternative Trading Platforms

0

500

1,000

1,500 1,426 1,321

949

768

513

353 352 289 202

88

Equity Market Traded Value in Europe (USD Billions, as of December 31st, 2012 )

*Source: FESE

The “innovative business model” brought with ATSs/MTFs have led to structural changes in the

equity trading landscape

Dark pools-decreasing transparency and increasing market fragmentation

11.09.2013 10

Agenda

Regulatory Implications of 2008 Financial Crisis

Issues related to Securitization: OTC vs Organized Markets

The Prospect of Shariah Compliant Finance

Borsa İstanbul’s Vision on Islamic Finance

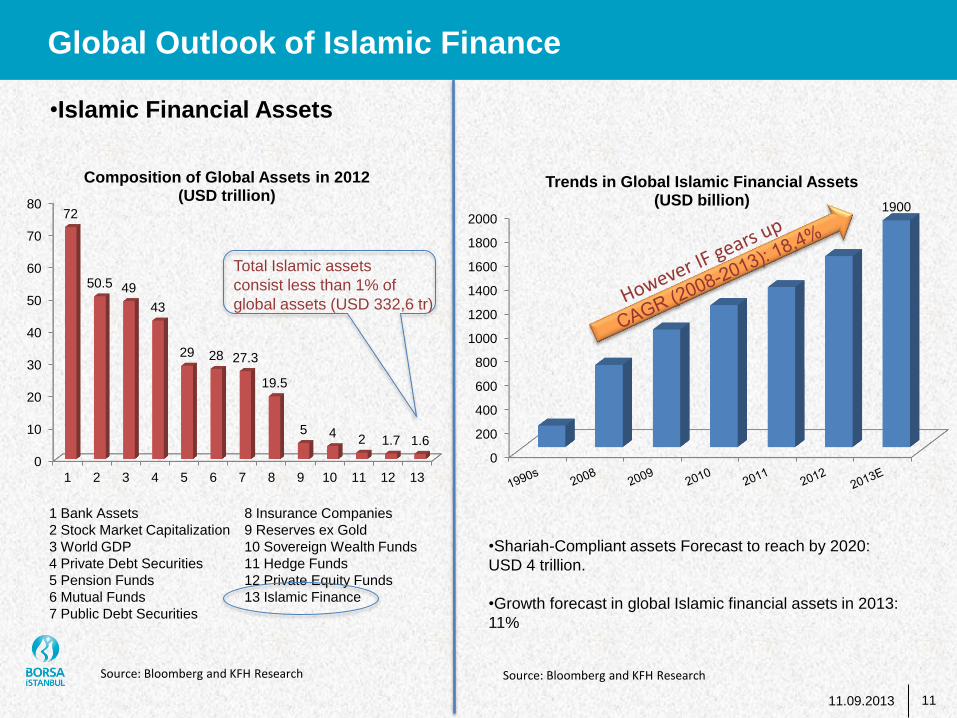

Global Outlook of Islamic Finance

Source: Bloomberg and KFH Research

0

10

20

30

40

50

60

70

80

1 2 3 4 5 6 7 8 9 10 11 12 13

72

50.5 49

43

29 28 27.3

19.5

5 4 2 1.7 1.6

Composition of Global Assets in 2012 (USD trillion)

1 Bank Assets

2 Stock Market Capitalization

3 World GDP

4 Private Debt Securities

5 Pension Funds

6 Mutual Funds

7 Public Debt Securities

8 Insurance Companies

9 Reserves ex Gold

10 Sovereign Wealth Funds

11 Hedge Funds

12 Private Equity Funds

13 Islamic Finance

Total Islamic assets

consist less than 1% of

global assets (USD 332,6 tr)

0

200

400

600

800

1000

1200

1400

1600

1800

2000 1900

Trends in Global Islamic Financial Assets (USD billion)

11

•Shariah-Compliant assets Forecast to reach by 2020:

USD 4 trillion.

•Growth forecast in global Islamic financial assets in 2013:

11%

Source: Bloomberg and KFH Research

•Islamic Financial Assets

11.09.2013

Global Outlook of Islamic Finance

Source: Bloomberg and KFH Research

12

Islamic Banking ;

80.3%

Takaful; 1.1%

Sukuk; 14.6%

Islamic Funds; 4.0%

Composition of Global Islamic Financial Assets in 2012

•Islamic Financial Assets

11.09.2013

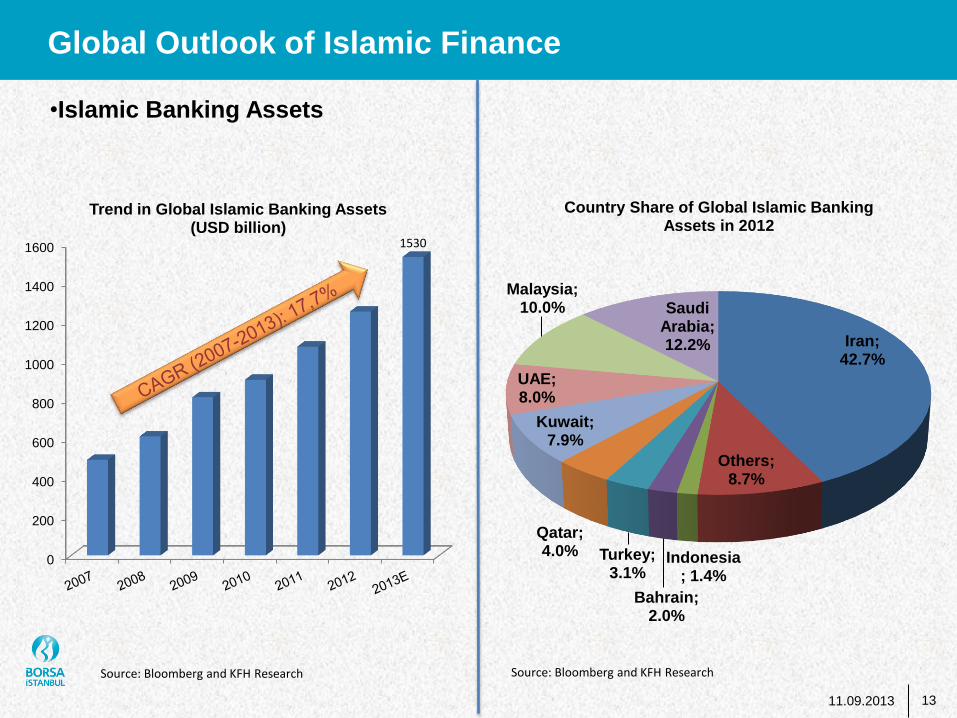

13

Global Outlook of Islamic Finance

Source: Bloomberg and KFH Research

0

200

400

600

800

1000

1200

1400

1600 1530

Trend in Global Islamic Banking Assets (USD billion)

Iran; 42.7%

Others; 8.7%

Indonesia; 1.4%

Bahrain; 2.0%

Turkey; 3.1%

Qatar; 4.0%

Kuwait; 7.9%

UAE; 8.0%

Malaysia; 10.0% Saudi

Arabia; 12.2%

Country Share of Global Islamic Banking Assets in 2012

Source: Bloomberg and KFH Research

•Islamic Banking Assets

11.09.2013

14

Global Outlook of Islamic Finance

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

1.2 1.4 7.1 9.5

13.7

33.8

50.0

24.3

37.9

53.0

92.4

137.5 Global Sukuk Issuance (USD billion)

Source: IIFM Database

• Based on current growth forecast, Islamic financial institutions will require at least US$ 400b of short term, credible,

liquid securities for liquidity and capital management purposes, by 2015.

•Islamic Capital Markets

11.09.2013

15

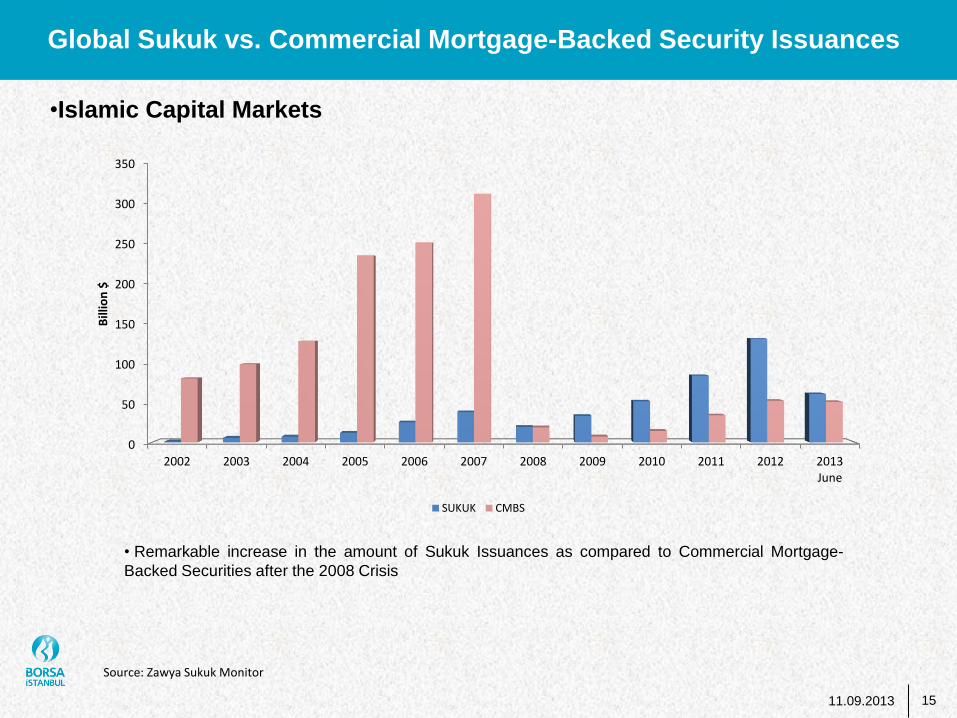

Global Sukuk vs. Commercial Mortgage-Backed Security Issuances

Source: Zawya Sukuk Monitor

•Islamic Capital Markets

11.09.2013

0

50

100

150

200

250

300

350

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 June

Bill

ion

$

SUKUK CMBS

• Remarkable increase in the amount of Sukuk Issuances as compared to Commercial Mortgage-

Backed Securities after the 2008 Crisis

16

Global Outlook of Islamic Finance

Structural Breakdown of Domestic Sukuk Issuance

(2001-2013)

Structural Breakdown of International Sukuk Issuance

(2001-2013)

Source: IIFM Database

Musharakah; 14%

Ijarah; 45%

Exchangable; 8%

Murabahah; 3%

Mudharabah; 6%

Hybrid; 8% Wakalah;

14%

Salam; 2%

Musharakah; 16%

Ijarah; 17%

Murabahah; 50%

Mudharabah; 3%

Hybrid; 4%

Salam; 1%

Istisna; 1%

Bai Bithaman Ajil; 8%

•Islamic Capital Markets

Source: IIFM Database 11.09.2013

11.09.2013 17

Agenda

Regulatory Implications of 2008 Financial Crisis

Issues related to Securitization: OTC vs Organized Markets

The Prospect of Shariah Compliant Finance

Borsa İstanbul’s Vision on Islamic Finance

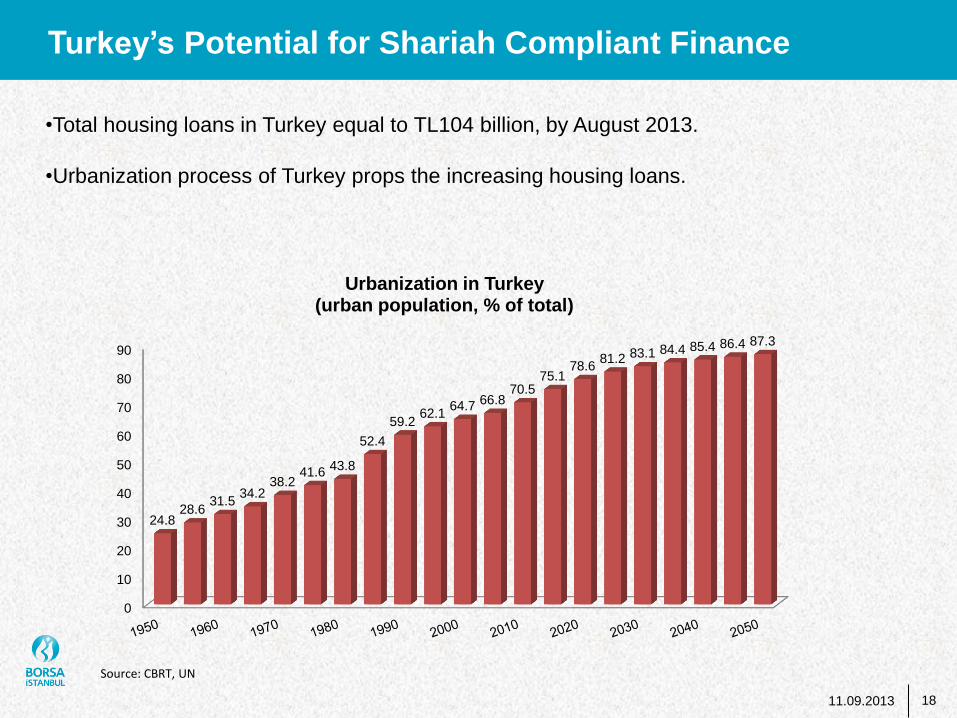

Turkey’s Potential for Shariah Compliant Finance

•Total housing loans in Turkey equal to TL104 billion, by August 2013.

•Urbanization process of Turkey props the increasing housing loans.

0

10

20

30

40

50

60

70

80

90

24.8 28.6

31.5 34.2

38.2 41.6

43.8

52.4

59.2 62.1

64.7 66.8 70.5

75.1 78.6

81.2 83.1 84.4 85.4 86.4 87.3

Urbanization in Turkey (urban population, % of total)

Source: CBRT, UN

18 11.09.2013

Turkey’s Potential for Shariah Compliant Finance

• For the plan of urban transformation, necessary to rebuild 8 million

dwellings in next 20 years.

• Urban transformation requires USD 800 billion.

• For liquidity, Turkey needs secondary loan market for housing sector.

• Islamic Finance tools such as Sukuk Issuance would be a solution.

19

Source: Yildirim, Y. (2012). Urban Transformation. Sabahattin Zaim Islam and Economy Symposium.

11.09.2013

Sukuk Issuances in Turkey

0

1

2

3

4

5

6

0

500

1000

1500

2000

2500

3000

3500

2010 2011 2012 2013 Aug

Turkey's Sukuk Market

Amount USD m.

No. of Issues

Source: IFIS

20 11.09.2013

Recent Developments on Islamic Finance

Source: IFIS

21 11.09.2013

Introduction of Sukuk and Equity Repo Market

World Bank Islamic Finance Research Center

Organization of Islamic Cooperation Member States’ Stock Exchanges Forum

S&P/OIC COMCEC 50 Shariah Index

S&P/OIC COMCEC 50 Shariah vs. DJIM Index

Source: Bloomberg

22 11.09.2013

90

95

100

105

110

115

120

DJIM Index SPOIC50P Index