Changing incentives for better ecological quality of ... · • Reduce taxes and social security...

24

1 Changing incentives for better ecological quality of growth Asia-Pacific experiences (mainly related to Environmental Tax/Fiscal Reforms – ETR/EFR) From Dessau/Germany to Bangkok/Thailand, 14 th November 2012 via resource-efficient and enironmentally-friendly tele-conference Kai Schlegelmilch Vice-President GREEN BUDGET GERMANY (GBG) • GREEN BUDGET EUROPE (GBE)

-

Upload

truongngoc -

Category

Documents

-

view

213 -

download

0

Transcript of Changing incentives for better ecological quality of ... · • Reduce taxes and social security...

1

Changing incentives for better ecological quality of growth

Asia-Pacific experiences

(mainly related to Environmental Tax/Fiscal Reforms – ETR/EFR)

From Dessau/Germany to Bangkok/Thailand, 14th November 2012 via resource-efficient and enironmentally-friendly tele-conference

Kai Schlegelmilch

Vice-President

GREEN BUDGET GERMANY (GBG) • GREEN BUDGET EUROPE (GBE)

2

Globally the first single-issue-NGO on environmental tax/fiscal reform (ETR/EFR)

Conviction that in market-economies full-cost market-prices are THE driver of decisions, hence full internalisation of costs is crucial

Green Budget Germany (GBG) GBE Over-seas

1994 Eco-Tax Experts (ETR) in Germany

X

1996 Building up international network

X X

1999 All market-based instruments (EFR)

X

2005 International Country projects on ETR

2008 Foundation of GBE

X

X

2008 Changing German Name to Ecological Social Market Economy

X

2009 Green Keynes, green revenues

X

2010 Green growth vs. Post-Growth X X 2010 Initiative: Green Budget Asia (GBA) X X

Our aspiration • From German ETR

to ambitious EFR in Europe and beyond

• From an often tech-nocratic instrument debate to visions of a greener society

• From a network of experts to Think Tank and Advocacy

• From an amateur to professional organi-sation and lobbyism

3

Reasons for EFR • In market economies, prices are THE driver of decisions. Leaving

out this leverage means missing the likely most powerful incentive • Internalisation of external cost –

market-based instruments are most efficient • Reduce dependency of oil and gas imports (and of uranium) • Stimulating innovations • Reduce taxes and social security contributions imposed on labour • Create new jobs (double dividend) and thus increasing

competitiveness • Use part of revenues for environmental subsidies

(renovation of buildings, energy efficiency measures, renewables, public transport)

• Stern Review: Postponing action for climate protection will lead to much higher cost in the future

• And a very obvious one… see next slide!

4

Remaining Agenda: Selected Examples for Elements of Environmental Fiscal Reforms in:

• China

• Indonesia

• Thailand

• Vanuatu

• Viet Nam

Asia-Pacific experiences with Environmental Tax/Fiscal Reforms

5

On behalf of GTZ, Kai Schlegelmilch was the International Coordinator of the „Task Force on Economic Instruments for Energy Efficiency and the Environment“ of the „China Council for International Cooperation on Environement and Development“ (CCICED – an international advisory body for China). Operating from 4.2008-11.2009 Final report published at the Annual General Meeting (AGM) in 11/2009 Recommendations on tools like : - increasing energy productivity - bank products such as credits, guarantees - insurance premiums, liability schemes - environmental taxation (including reducing environmentally harmful subsidies and introducing an energy/carbon tax) Possible impact: Announcement that before 2015 China will introduce a carbon tax

China

6

• As 3rd largest democracy and as one of the largest oil exporters ID has a crucial role to play regarding EFR. • Climate policy is high on the national agenda given the push thanks to the international climate conference on Bali 2007.

• Is shifting between subsidising domestic use and benefiting from internationally relatively high world oil prices.

• GIZ/Danida are supporting the Government which is exploring possibilities to establish an ETR/EFR.

•Indonesia has already a very good basis of EFR-elements in its fiscal system.

• Within the process of decentralisation, the law on provincial and local taxes (28/2009) was adopted and the tax bases determined therein have a direct or indirect relevance for the environment.

• Furthermore regions are prohibited from collecting taxes other than those types of taxes. This supports the conditions for further implementing EFR-elements.

Indonesia

7

The following types of taxes are already in place due to law on provincial

and local taxes (28/2009) which comprises many environmentally related taxes, but still offers ample room for increases and reducing exemptions in terms of tax basis:

1. provinces: • Motor Vehicle Taxes; • Excise/Taxes For Transfer of Ownership of

Motor Vehicle; • Taxes on Fuel for Motor Vehicles; • Surface Water Taxes; • Cigarette Taxes.

Indonesia

8

The following types of taxes are already in place due to law on provincial and local taxes (28/2009) which comprises many environmentally related taxes, but still offers ample room for increases and reducing exemptions in terms of tax basis: 2. districts/towns: • Hotel Taxes; • Restaurant Taxes; • Entertainment Taxes; • Advertising Taxes; • Street Lighting Taxes (is nothing else but an electricity tax as the local administrations try to receive back their expenditures for the lighting costs of streets. To this end they charge all electricity consumers according to their consumption. It could thus be renamed an electricity tax which would add to the transparency and clarity of fiscal laws)

• Taxes on Non-Metal and Non-Rock Minerals; • Parking Taxes; • Ground Water Taxes; • Taxes on Swallows’ Nests; • Rural and Urban Land and Building Taxes; • Excise/Taxes for Acquiring Right on Land and Building

Indonesia

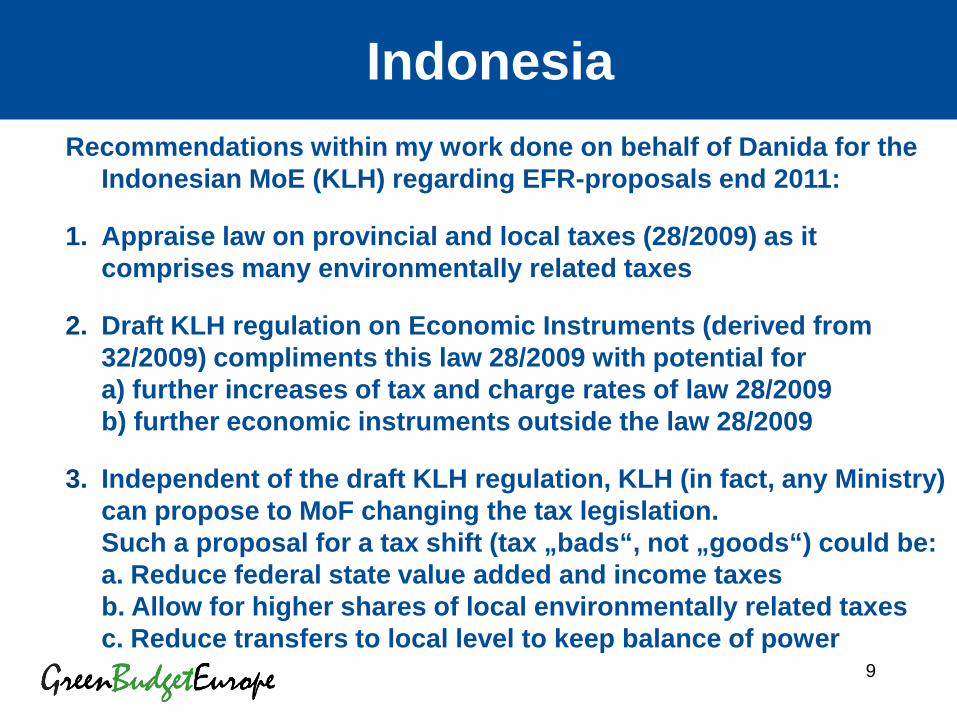

9

Recommendations within my work done on behalf of Danida for the Indonesian MoE (KLH) regarding EFR-proposals end 2011:

1. Appraise law on provincial and local taxes (28/2009) as it comprises many environmentally related taxes

2. Draft KLH regulation on Economic Instruments (derived from 32/2009) compliments this law 28/2009 with potential for a) further increases of tax and charge rates of law 28/2009 b) further economic instruments outside the law 28/2009

3. Independent of the draft KLH regulation, KLH (in fact, any Ministry) can propose to MoF changing the tax legislation. Such a proposal for a tax shift (tax „bads“, not „goods“) could be: a. Reduce federal state value added and income taxes b. Allow for higher shares of local environmentally related taxes c. Reduce transfers to local level to keep balance of power

Indonesia

10

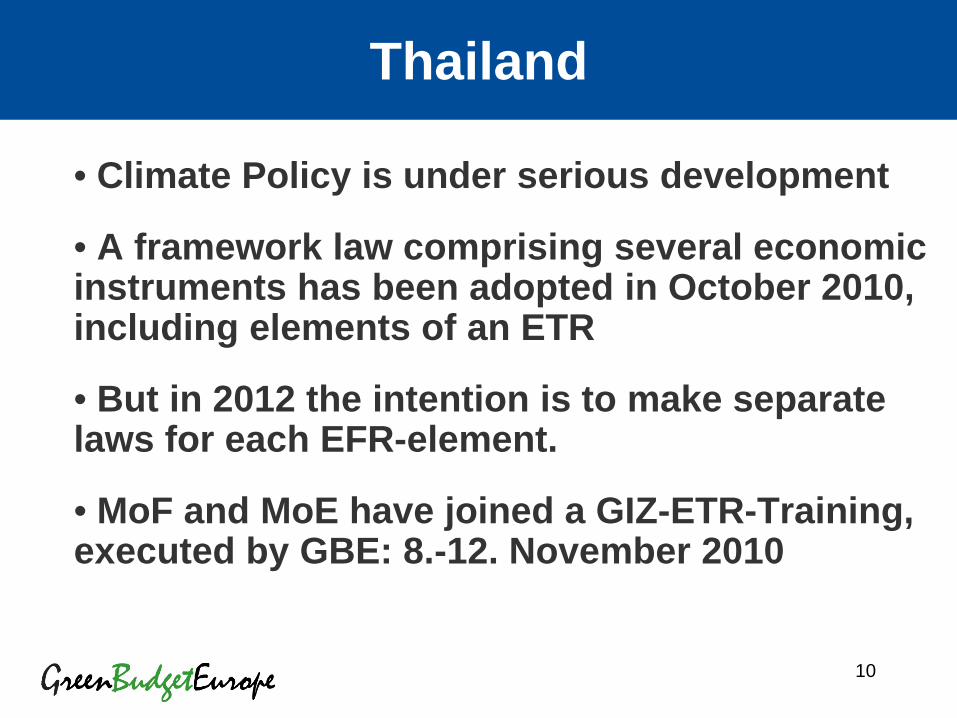

Thailand

• Climate Policy is under serious development

• A framework law comprising several economic instruments has been adopted in October 2010, including elements of an ETR

• But in 2012 the intention is to make separate laws for each EFR-element.

• MoF and MoE have joined a GIZ-ETR-Training, executed by GBE: 8.-12. November 2010

11

Experiences with economic instruments Is limited and usually confined to the levying of non-compliance fees or charges 1. Excise Tax Act: a) Taxes on petroleum products, automobiles, motorcycles,

electronic appliances, batteries b) differential tax measures for • batteries with recycled / non-recycled lead • different fuel types, such as diesel with high sulphur content has been

successfully ended i.a. through a higher tax rate in comparison to those on diesel with low-sulphur content.

2. Wastewater charges and solid waste collection fees. But not enforced particularly successfully Reasons: • Regional or local governments responsible for enforcement are concerned

that they will lose future elections, should they enforce these instruments. • Lack of capacity to monitor wastewater pollution and to enforce these

instruments

Thailand

12

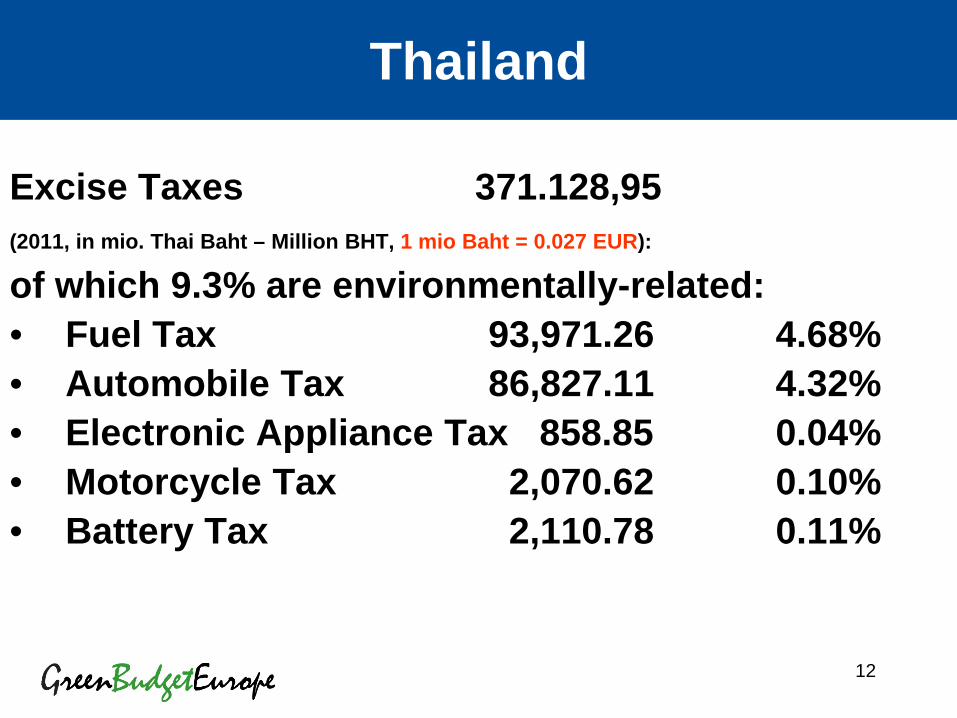

Excise Taxes 371.128,95 (2011, in mio. Thai Baht – Million BHT, 1 mio Baht = 0.027 EUR): of which 9.3% are environmentally-related: • Fuel Tax 93,971.26 4.68% • Automobile Tax 86,827.11 4.32% • Electronic Appliance Tax 858.85 0.04% • Motorcycle Tax 2,070.62 0.10% • Battery Tax 2,110.78 0.11%

Thailand

13

Perspectives for EFR-elements After several years of intensive policy dialogue: 1. Shift towards EFR is possible in the near future. Rationale: Thailand’s National Economic and Social Development

Board’s 11th Five-Year Plan (2011–2015) has put green growth and low-carbon society as one of the central themes, creating a demand for a solid economic framework to be achieved by means of a relatively wide-reaching EFR package.

2. EFR plans should/could include a realistic plan to phase out

subsidies to diesel, and possibly also CNG and LPG. Rationale: The Energy Ministry has estimated that subsidies were

worth 8% of the total fiscal budget in the 2010-2011 fiscal year.

Thailand

14

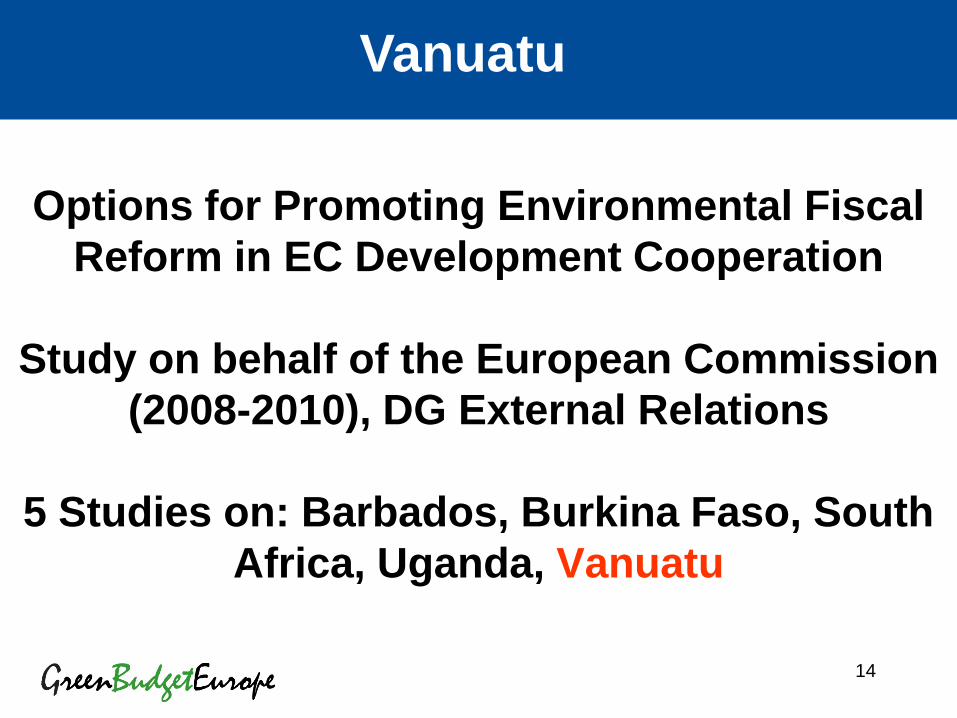

Options for Promoting Environmental Fiscal Reform in EC Development Cooperation

Study on behalf of the European Commission

(2008-2010), DG External Relations

5 Studies on: Barbados, Burkina Faso, South Africa, Uganda, Vanuatu

Vanuatu

15

Vanuatu

Vanuatu

Environmental taxes

No

Energy products Yes

Transport / vehicles

Yes

Other environ. taxes

Yes

User charges water sanitation waste

No

Feed-in-tariff (renewable electricity

No

No established system of environmental fees and charges, foregoing revenues Large potential for developing proposals for EFR-elements. Transport: Duty on diesel + gasoline is at 25 VUV/l (0.17 EUR/l) plus VAT at 12.5% = 35 VUV/litre (0.24 EUR/l = 40% of the price due to taxes). The fee for motor cars varies from VUV 11.200 to VUV 38.000 (80-260 EUR) according to their tonnage and cylinder capacity number. However Vanuatu aims at reducing costs for transportation and utilities as one of the priorities.

16

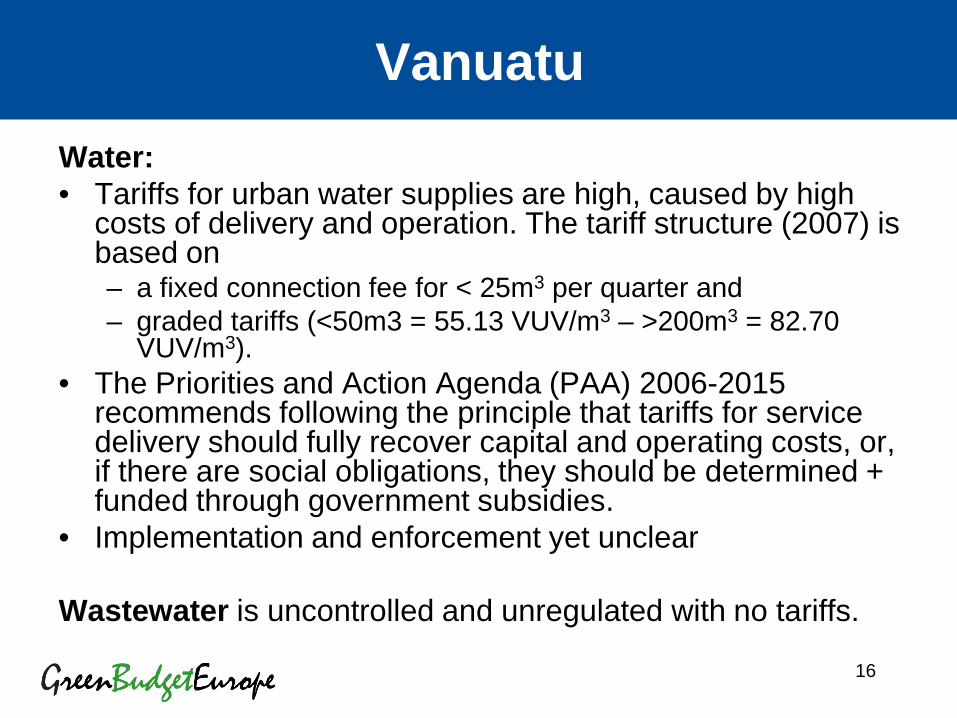

Vanuatu Water: • Tariffs for urban water supplies are high, caused by high

costs of delivery and operation. The tariff structure (2007) is based on – a fixed connection fee for < 25m3 per quarter and – graded tariffs (<50m3 = 55.13 VUV/m3 – >200m3 = 82.70

VUV/m3). • The Priorities and Action Agenda (PAA) 2006-2015

recommends following the principle that tariffs for service delivery should fully recover capital and operating costs, or, if there are social obligations, they should be determined + funded through government subsidies.

• Implementation and enforcement yet unclear

Wastewater is uncontrolled and unregulated with no tariffs.

17

In a nutshell:

• Viet Nam will be heavily affected by climate change

• Viet Nam realised that its past environmental policy instruments are not that effective

• Since 2012: Taxes enacted on energy/transport, but also covering CFCs, plastic bags, pesticides

• Viet Nam is now the first Asia-Pacific country with a relatively comprehensive legislation on environmental taxes.

Viet Nam

18

19.11.2012

MILESTONES ACHIEVED ALONG THE WAY

Vietnamese Prime Minister asked for an Ecological Tax to be introduced by 2011

GTZ Advisory starts Editorial Team (TPD, MoF)

Global Conference on Environ. Taxation 1. EU Study Tour

Dec. 2008

Nov. 2009

• Various missions with Kai, consultative workshops with different stakeholders (central, provincial) • Excellent national staff bridging the gap between international best practices (international expert) and the local needs (TPD)

July 2010

May 2010

Final Impact Assessment First reading in N.A.

2. EU Study Tour

15. Nov. 2010

Final reading and approval by National Assembly (98.7%)

Enactment with guiding decrees

1. Jan 2012

1. draft

2004

Viet Nam

19 19.11.2012

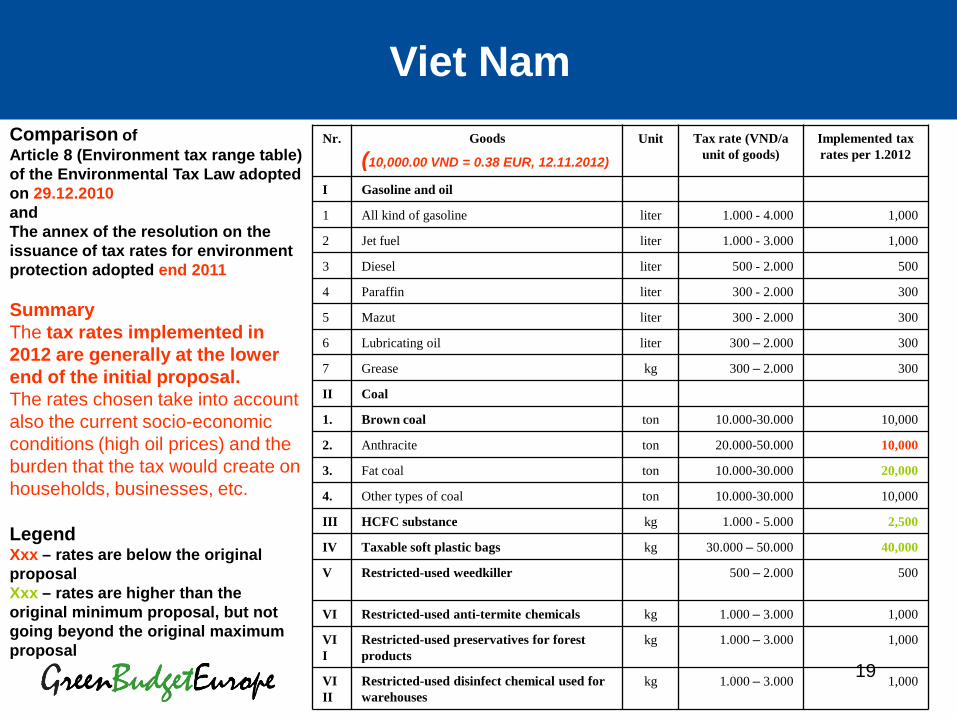

Viet Nam Nr. Goods

(10,000.00 VND = 0.38 EUR, 12.11.2012)

Unit Tax rate (VND/a unit of goods)

Implemented tax rates per 1.2012

I Gasoline and oil

1 All kind of gasoline liter 1.000 - 4.000 1,000

2 Jet fuel liter 1.000 - 3.000 1,000

3 Diesel liter 500 - 2.000 500

4 Paraffin liter 300 - 2.000 300

5 Mazut liter 300 - 2.000 300

6 Lubricating oil liter 300 – 2.000 300

7 Grease kg 300 – 2.000 300

II Coal

1. Brown coal ton 10.000-30.000 10,000

2. Anthracite ton 20.000-50.000 10,000

3. Fat coal ton 10.000-30.000 20,000

4. Other types of coal ton 10.000-30.000 10,000

III HCFC substance kg 1.000 - 5.000 2,500

IV Taxable soft plastic bags kg 30.000 – 50.000 40,000

V Restricted-used weedkiller 500 – 2.000 500

VI Restricted-used anti-termite chemicals kg 1.000 – 3.000 1,000

VII

Restricted-used preservatives for forest products

kg 1.000 – 3.000 1,000

VIII

Restricted-used disinfect chemical used for warehouses

kg 1.000 – 3.000 1,000

Comparison of Article 8 (Environment tax range table) of the Environmental Tax Law adopted on 29.12.2010 and The annex of the resolution on the issuance of tax rates for environment protection adopted end 2011 Summary The tax rates implemented in 2012 are generally at the lower end of the initial proposal. The rates chosen take into account also the current socio-economic conditions (high oil prices) and the burden that the tax would create on households, businesses, etc.

Legend Xxx – rates are below the original proposal Xxx – rates are higher than the original minimum proposal, but not going beyond the original maximum proposal

20

19.11.2012

IMPACT ASSESSMENT, RESULTS

Results: CO2 emissions drop by 2.3% under the low and by 7.5% under

the high scenario (up to 9.3 mill. t in 2012 alone)

Transport and fishery sector are strongly affected

Social effects: all income groups equally affected

Economic: considerable shift in purchasing power from households to government

Negligible GDP growth impact

Fiscal: increase in revenue by 7.3% in high scenario

Viet Nam

21

19.11.2012

SUCCESS FACTORS

• Trusted relationship to high level political decision makers in the Ministry of Finance

• Continuous Advisory by a short term consultant from a ministry (“consultations among equals”)

• Provision of access to international networks and knowledge through conferences and study tour

• Right mix of modalities (study tours, advisory, workshops, trainings)

• National staff instrumental for know how transfer including Vice-Minister himself

• Strong ownership and dynamic leadership on the partner side

• GIZ/consultant provided only comments on the law (MoF wrote it)

Viet Nam

22

Summary and Conclusions (I) • Many Asia-Pacific countries are about to introduce broad energy taxes, often in the context of an Environmental Tax/Fiscal Reform (ETR/EFR)

• Vanuatu has started considering fiscal instruments, but yet no systematic and strategic approach like in Thailand

• Thailand considers several fiscal instruments (i.a. water charge, fuel tax) • China announced introducting a carbon tax for 2015, based on some existing environmental charges and taxes • Indonesia started phasing out fossil fuel subsidies and it has a very comprehensive tax base already in place, but needs to enhance and exploit its potential.

Changing incentives for better ecological quality of growth Asia-Pacific experiences:

Environmental Tax/Fiscal Reforms

23

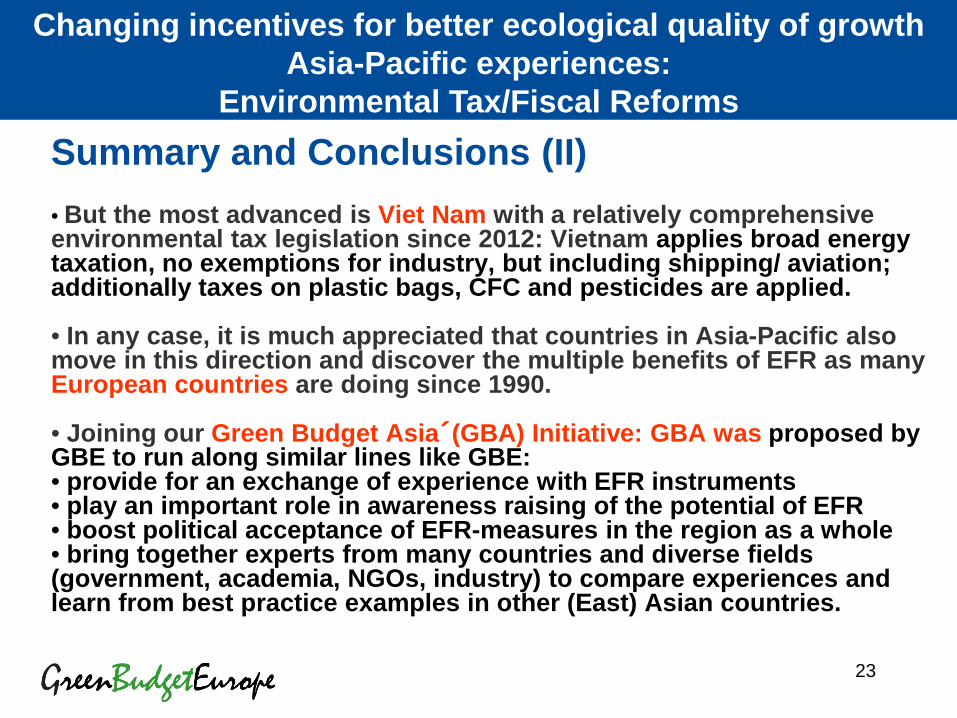

Summary and Conclusions (II) • But the most advanced is Viet Nam with a relatively comprehensive environmental tax legislation since 2012: Vietnam applies broad energy taxation, no exemptions for industry, but including shipping/ aviation; additionally taxes on plastic bags, CFC and pesticides are applied.

• In any case, it is much appreciated that countries in Asia-Pacific also move in this direction and discover the multiple benefits of EFR as many European countries are doing since 1990.

• Joining our Green Budget Asia´(GBA) Initiative: GBA was proposed by GBE to run along similar lines like GBE: • provide for an exchange of experience with EFR instruments • play an important role in awareness raising of the potential of EFR • boost political acceptance of EFR-measures in the region as a whole • bring together experts from many countries and diverse fields (government, academia, NGOs, industry) to compare experiences and learn from best practice examples in other (East) Asian countries.

Changing incentives for better ecological quality of growth Asia-Pacific experiences:

Environmental Tax/Fiscal Reforms

24

Thank you for your attention! Kai Schlegelmilch Vice President of Green Budget Europe (GBE) www.green-budget.eu [email protected]

• International studies: http://www.foes.de/publikationen/studien/?lang=en/#franz3

• Green Budget Asia (GBA) Initiative: http://www.foes.de/pdf/2011-11-GBE_Asia_Initiative.pdf

• EFR-Training (developed by GBE on behalf of GIZ): http://www.foes.de/internationales/oefr-in-entwicklungslaendern/

Changing incentives for better ecological quality of growth Asia-Pacific experiences:

Environmental Tax/Fiscal Reform