Change is Hard. You go First. Five Healthcare Trends You Can’t Ignore. Mark L Fenlon MD, MBA,...

84

Change is Hard. You go First. Five Healthcare Trends You Can’t Ignore. Mark L Fenlon MD, MBA, FAAFP 29 May 2015

Transcript of Change is Hard. You go First. Five Healthcare Trends You Can’t Ignore. Mark L Fenlon MD, MBA,...

Change is Hard. You go First.Five Healthcare Trends You Can’t Ignore.

Mark L Fenlon MD, MBA, FAAFP29 May 2015

Disclosure All faculty/speakers participating in a sponsored activity are

expected to disclose to the audience any financial interests or other relationships, including those of a spouse/partner, that may have a bearing on the subject matter of education.

Mark L. Fenlon M.D. has no relevant financial relationships to disclose.

Change

Willem Einthoven

Objectives

1. Understand the concept and drivers of “moving from volume to value”.

2. Be able to address strategies/initiatives within your organization that address identified trends.

3. Improve you ability as physician leaders to engage in discussions about prevalent changes in healthcare.

Agenda

• Why change• Moving from volume to value• Transparency and results• Consumerism• Population Health• Cost and compensation

Why change?

Why Change?

• In 2013 U.S. health care spending increased 3.6 percent to reach $2.9 trillion.

• $9,255 per person.• The share of the economy devoted to health

spending has remained at 17.4 percent since 2009

Source: http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/downloads/highlights.pdf

Health Spending by Service or ProductType of Service or Product Cost in $Billions

Hospital Care $936.9

Physician & Clinical Services $586.7

Other Professional Services $80.2

Dental $111.0

Other Health, Residential and Personal Care Services

$148.2

SNF/CBRF $155.8

Prescription Drugs $271.1

Durable Medical Equipment $43.0

Other $55.9

Source: http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/downloads/highlights.pdf

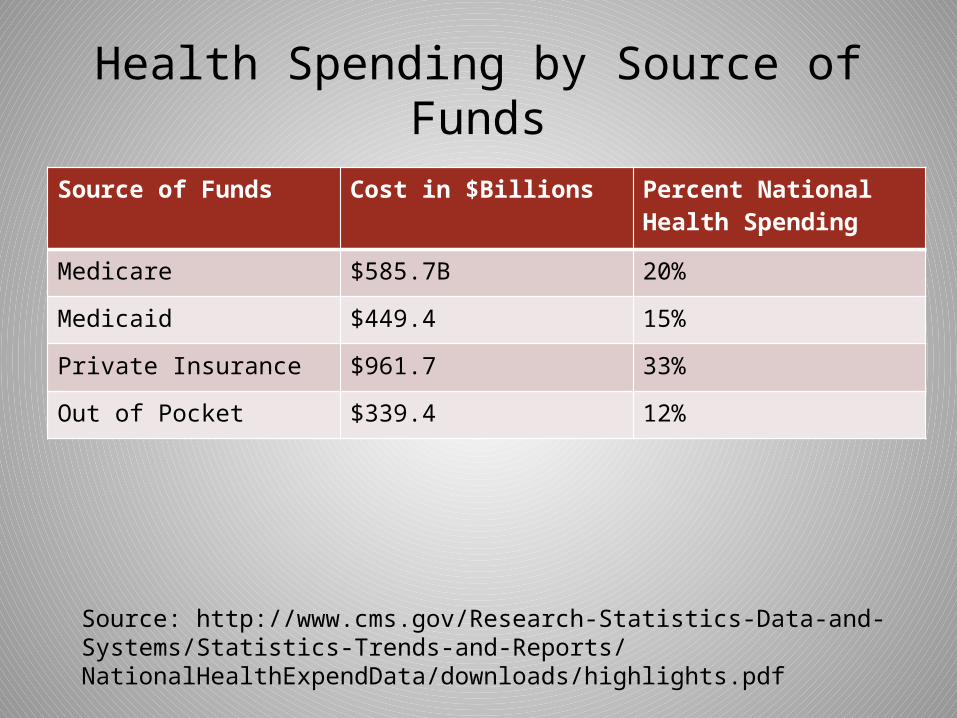

Health Spending by Source of Funds

Source of Funds Cost in $Billions Percent National Health Spending

Medicare $585.7B 20%

Medicaid $449.4 15%

Private Insurance $961.7 33%

Out of Pocket $339.4 12%

Source: http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/downloads/highlights.pdf

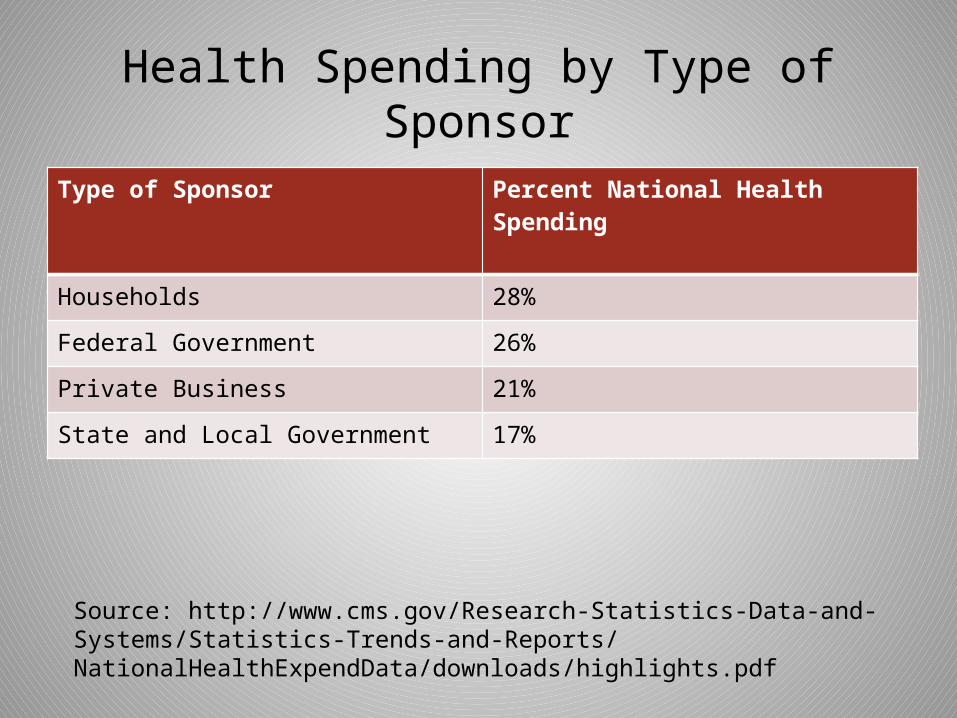

Health Spending by Type of SponsorType of Sponsor Percent National Health Spending

Households 28%

Federal Government 26%

Private Business 21%

State and Local Government 17%

Source: http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/downloads/highlights.pdf

#1 Moving from Volume to Value

Volume based reimbursement

• Current incentives favor volume over value in many markets

• “Do as much as you can to as many people as possible”

• Incentives reward substandard quality –services that do not benefit patients are financially rewarded

• Encourages cost shifting

VALUE = QUALITY / COST

What is value?

HEALTH OUTCOMES ACHIEVED PER DOLLAR SPENT.

What Is Value in Health Care?Michael E. Porter, Ph.D.N Engl J Med 2010; 363:2477-2481December 23, 2010DOI: 10.1056/NEJMp1011024

Value based reimbursement

• Multiple quality measures – who decides?• Measurement based on claims vs. clinical data• Cost to deliver care more difficult to measure• Value is intuitive concept - no mathematical

construct to measure value

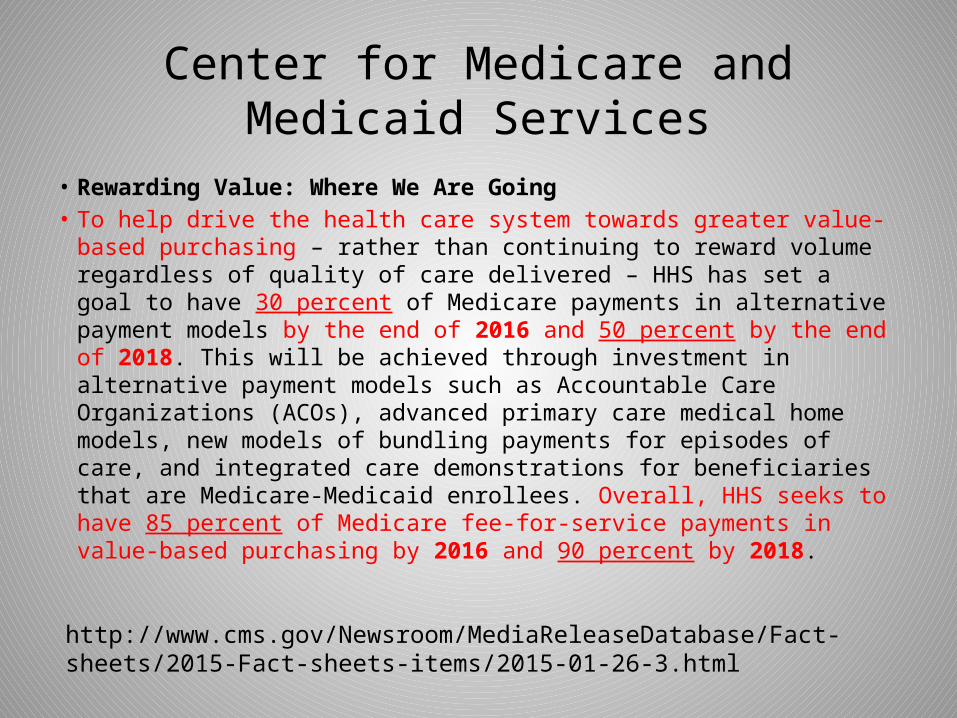

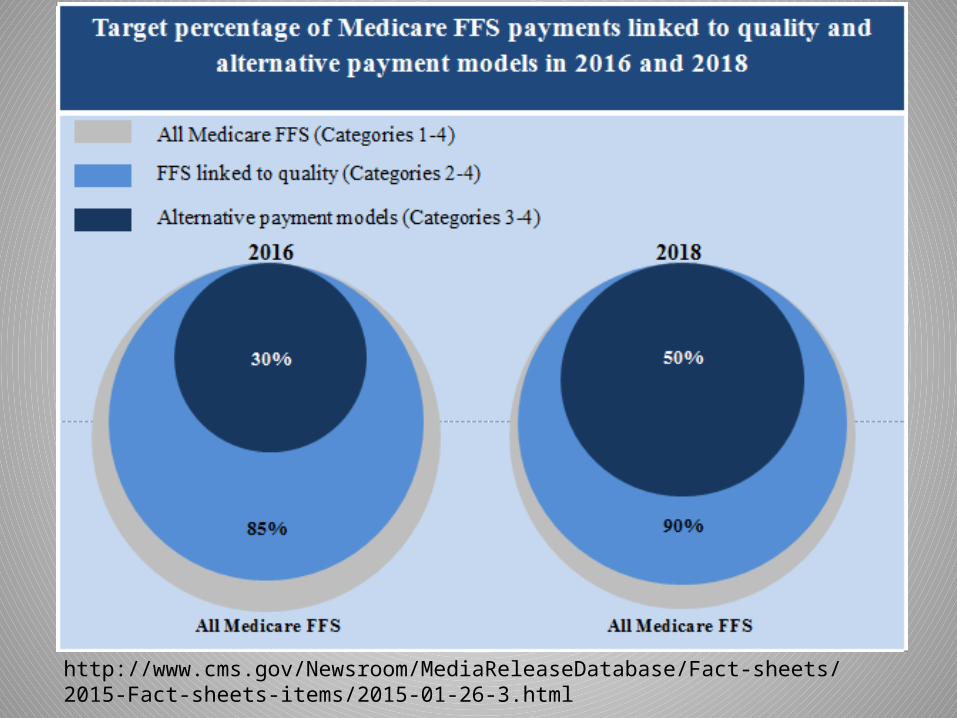

Center for Medicare and Medicaid Services

• Rewarding Value: Where We Are Going• To help drive the health care system towards greater value-based

purchasing – rather than continuing to reward volume regardless of quality of care delivered – HHS has set a goal to have 30 percent of Medicare payments in alternative payment models by the end of 2016 and 50 percent by the end of 2018. This will be achieved through investment in alternative payment models such as Accountable Care Organizations (ACOs), advanced primary care medical home models, new models of bundling payments for episodes of care, and integrated care demonstrations for beneficiaries that are Medicare-Medicaid enrollees. Overall, HHS seeks to have 85 percent of Medicare fee-for-service payments in value-based purchasing by 2016 and 90 percent by 2018.

http://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2015-Fact-sheets-items/2015-01-26-3.html

http://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2015-Fact-sheets-items/2015-01-26-3.html

http://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2015-Fact-sheets-items/2015-01-26-3.html

Emerging Threats to Hospital Pricing

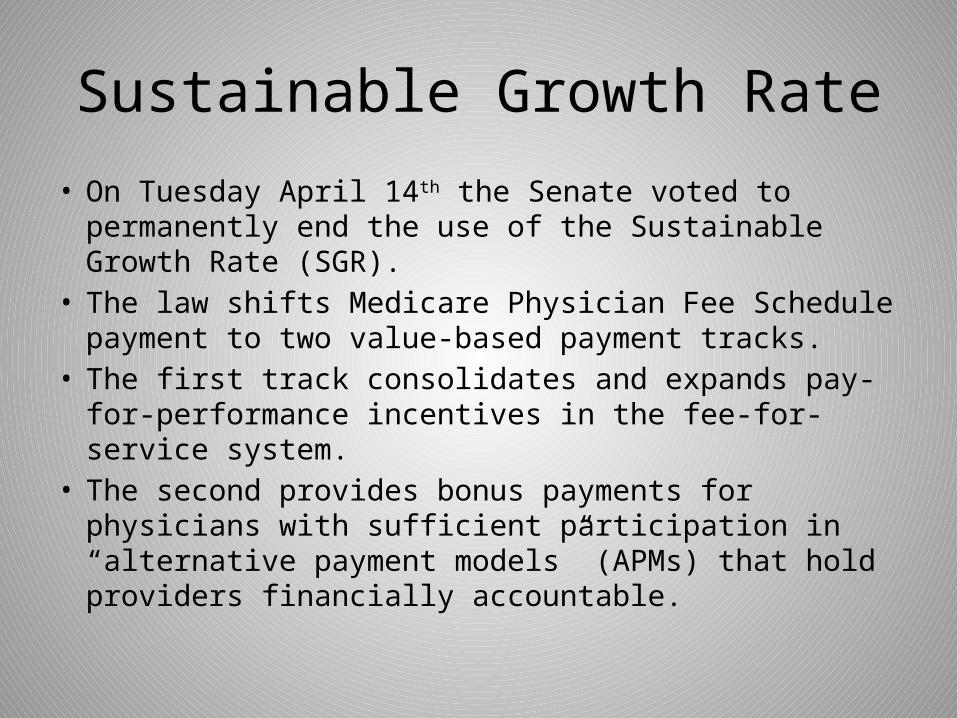

Sustainable Growth Rate

• On Tuesday April 14th the Senate voted to permanently end the use of the Sustainable Growth Rate (SGR).

• The law shifts Medicare Physician Fee Schedule payment to two value-based payment tracks.

• The first track consolidates and expands pay-for-performance incentives in the fee-for-service system.

• The second provides bonus payments for physicians with sufficient participation in “alternative payment models” (APMs) that hold providers financially accountable.

Sustainable Growth Rate

• Represents a significant step in the shift toward value-based payments

• Locks-in slow trajectory for payment rates - Over the next ten years, annual updates to Medicare Physician Fee Schedule payment rates will range from 0.0% to 0.75%

• Broadens the scope and elevates the importance of quality measurement

• Boosts the attractiveness of two-sided risk models• Furthers trend toward patient price sensitivity

Insurers take first steps to change how doctors, hospitals are paidBy Guy Boulton of the Journal Sentinel

April 26, 2015

• A nationwide initiative to make the fragmented and costly health care system more efficient could affect the more than 340,000 people in Wisconsin enrolled in Medicare Advantage plans.

• Humana and UnitedHealthcare — two of the largest health insurers that offer Medicare Advantage plans — are striking agreements with what are known as accountable care organizations.

Accountable Care Organizations

• An ACO can be defined as a set of health care providers—including primary care physicians, specialists, and hospitals—that work together collaboratively and accept collective accountability for the cost and quality of care delivered to a population of patients.

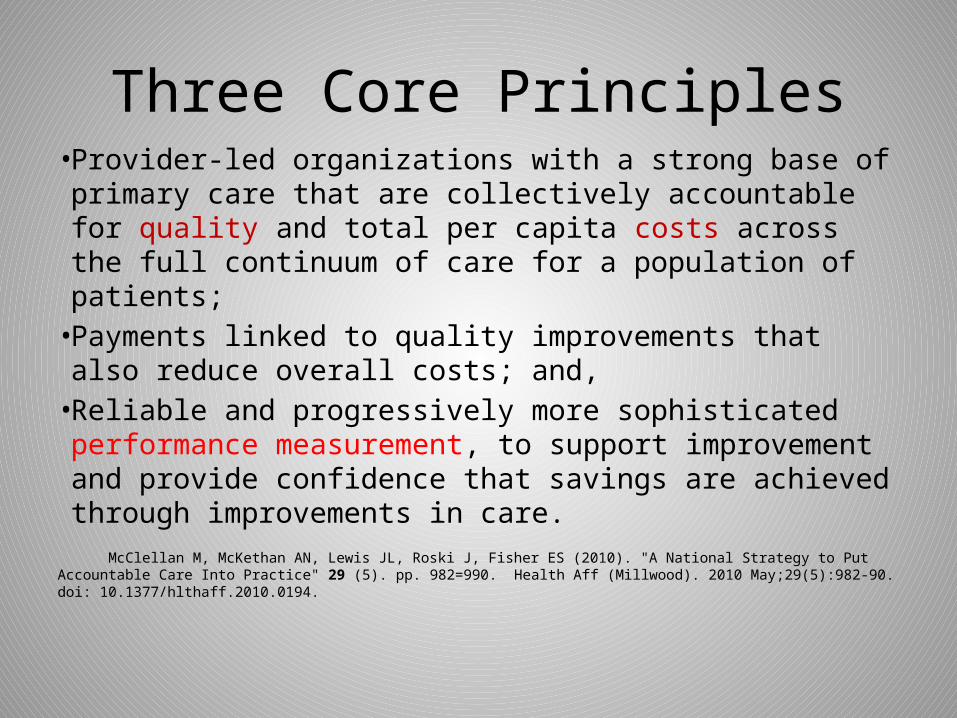

Three Core Principles• Provider-led organizations with a strong base of primary

care that are collectively accountable for quality and total per capita costs across the full continuum of care for a population of patients;

• Payments linked to quality improvements that also reduce overall costs; and,

• Reliable and progressively more sophisticated performance measurement, to support improvement and provide confidence that savings are achieved through improvements in care.

McClellan M, McKethan AN, Lewis JL, Roski J, Fisher ES (2010). "A National Strategy to Put Accountable Care Into Practice" 29 (5). pp. 982=990. Health Aff (Millwood). 2010 May;29(5):982-90. doi: 10.1377/hlthaff.2010.0194.

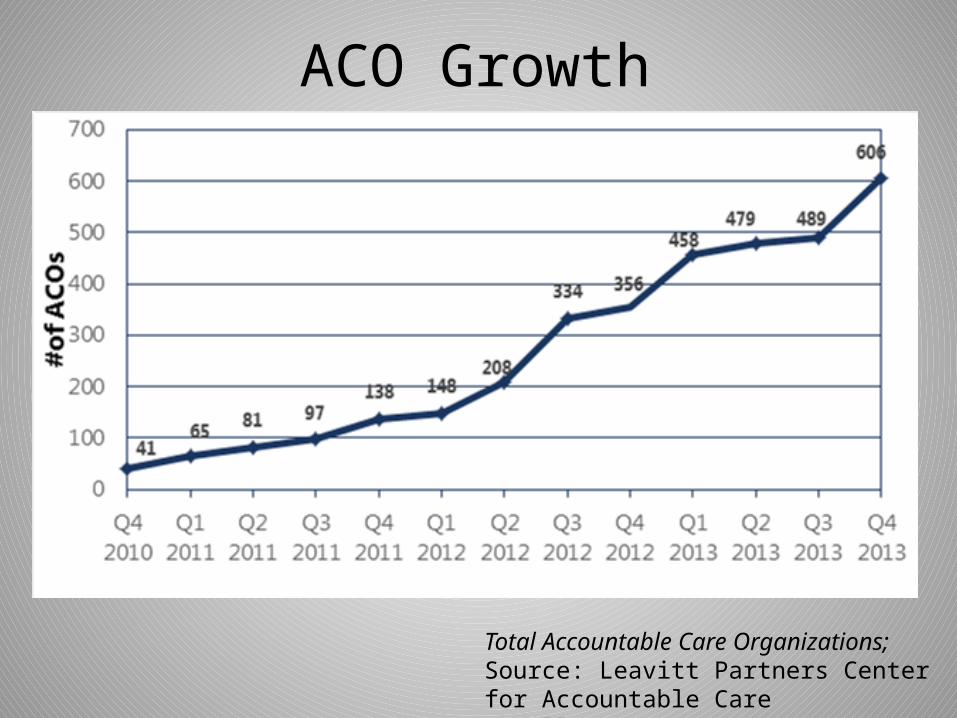

ACO Growth

Total Accountable Care Organizations; Source: Leavitt Partners Center for Accountable Care Intelligence

How we get there• This will be achieved through investment in

alternative payment models such as Accountable Care Organizations (ACOs), advanced primary care medical home models, new models of bundling payments for episodes of care, and integrated care demonstrations for beneficiaries that are Medicare-Medicaid enrollees.

http://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2015-Fact-sheets-items/2015-01-26-3.html

#2 Transparency and results• Insurers and employers are steering beneficiaries to low-

cost sites.– Employers and Insurers are investing in price comparison

tools and offering incentives to their beneficiaries if patients choose low-cost alternatives to traditional care

• Policy makers are passing transparency legislation– 39 states have some transparency requirement, and

most require hospitals to provide charge information. – Some states are moving to all-payer, statewide claims

databases to build a central transparency site, so transparency is no longer totally voluntary. • The number of consumers in High-Deductible Health

Plans (HDHP) is rising.

Wisconsin Health Information Organization

• All payer claims database• Public website MyHealthWI.org • More that 4 million individuals (70% Wi pop)• More than 250 million claims• More than $70 billion billed charges –

commercial, Medicaid, Medicare Advantage and Medicare FFS in 2015

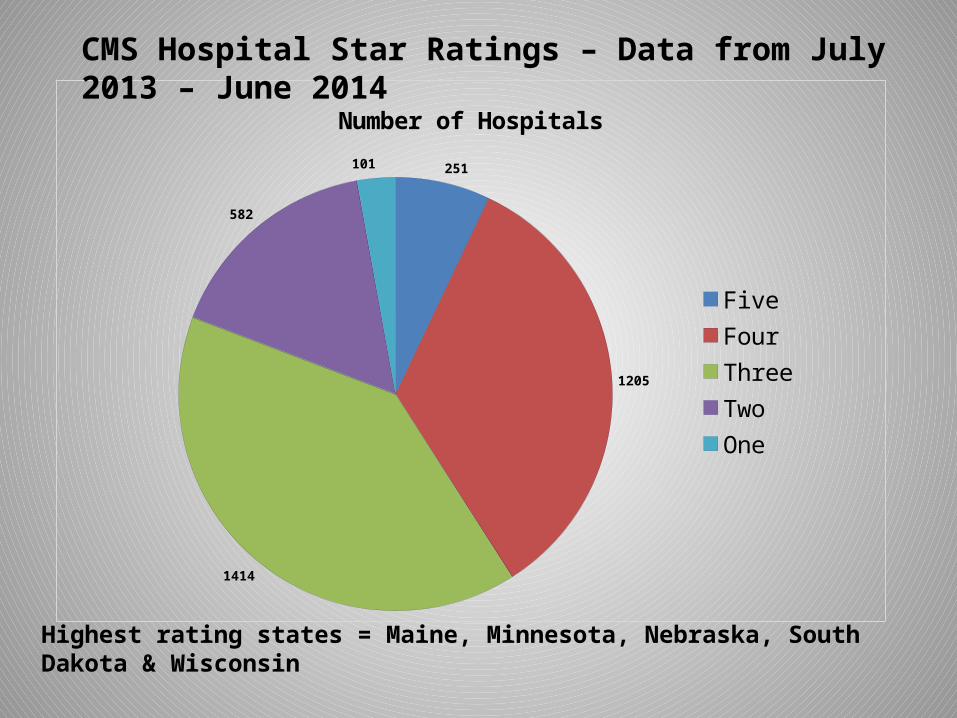

CMS Releases First Ever Hospital Compare Star RatingsComparison Ratings that Help Consumers Compare and

Choose Among Hospitals

Today, the Centers for Medicare & Medicaid Services (CMS) for the first time introduced star ratings on Hospital Compare, the agency’s public information website, to make it easier for consumers to choose a hospital and understand the quality of care they deliver. Today’s announcement builds on a larger effort across HHS to build a health care system that delivers better care, spends health care dollars more wisely, and results in healthier people

http://www.cms.gov/Newsroom/MediaReleaseDatabase/Press-releases/2015-Press-releases-items/2015-04-16.html

http://www.cms.gov/Newsroom/MediaReleaseDatabase/Press-releases/2015-Press-releases-items/2015-04-16.html

Summary of HCAHPS Measures Used to Determine HCAHPS Star Ratings

There is a star rating for each of the following HCAHPS measures:

•HCAHPS Composites Measures • Communication with Nurses (Q1, Q2, Q3) • Communication with Doctors (Q5, Q6, Q7) • Responsiveness of Hospital Staff (Q4, Q11) • Pain Management (Q13, Q14) • Communication about Medicines (Q16, Q17) • Discharge Information (Q19, Q20) • Care Transition (Q23, Q24, Q25)

•HCAHPS Individual Items • Cleanliness of Hospital Environment (Q8)• Quietness of Hospital Environment (Q9)

•HCAHPS Global Items • Overall Hospital Rating (Q21) • Recommend the Hospital (Q22)

251

1205

1414

582

101

Number of Hospitals

FiveFourThreeTwoOne

CMS Hospital Star Ratings – Data from July 2013 – June 2014

Highest rating states = Maine, Minnesota, Nebraska, South Dakota & Wisconsin

High Deductible Health Insurance

Wisconsin Percent Change

Average Annual Growth

Average Annual Growth

Commonwealthfund.org 2003 2010 2013 2003-2013 2003-2013 2010-2013

Single Premiums $3,749 $5,384 $5,730 53% 5.3% 2.1%

Family Premiums $9,562 $14,542 $16,665 74% 6.2% 4.6%

Premiums as % median income

15% 20% 29%

Employee premium contribution (single)

$830 $1,174 $1,220 47% 5.1% 1.3%

% employees with a deductible (single)

75% 87% 86%

Deductible (single) $490 $1,145 $1,335 172% 12.9% 5.3%

High Deductible Health Insurance

• Often paired with Health Savings Account• Average deductible = $2098• 18% have deductible of $3,000 or more• Average Family deductible = $4059• ~ 1/3 have deductible of $5,000

Source: Kaiser Family Foundation/Health Research & Educational Trust 2014 Employer Benefit Survey

#3 Consumerism

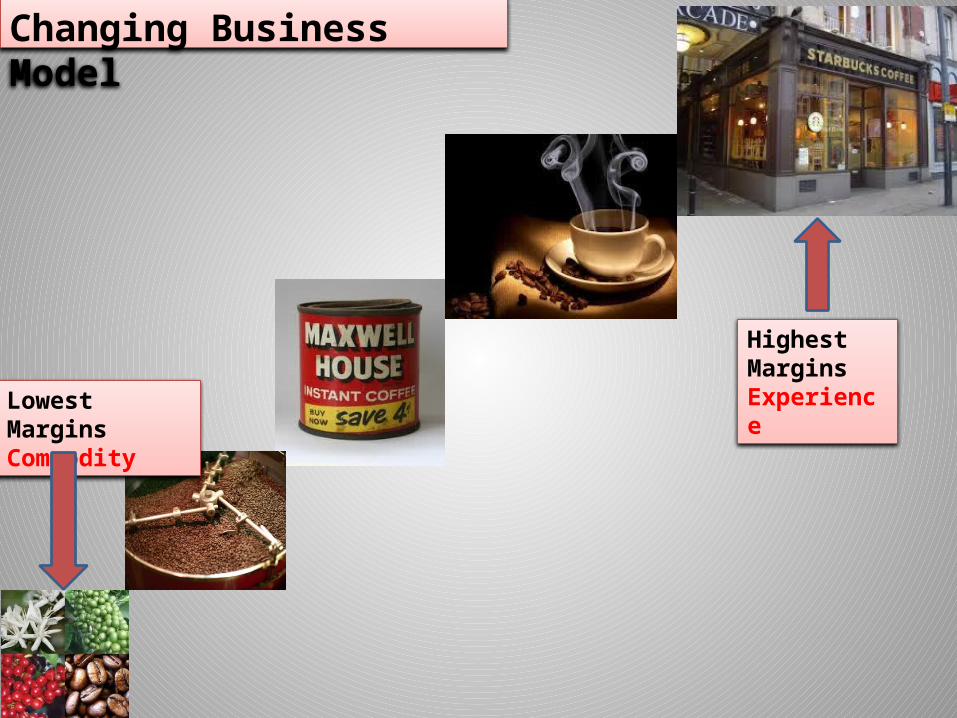

• Convenience, cost and access trump loyalty• Retail – Walmart, CVS, Walgreens• Changing business model• You can’t be average – Lake Wobegon

Have you used Yelp?

April 20, 2015

Shopping tools help patients find cash prices for medical procedures• When Vicki Burns was told she needed total hip replacement surgery

in 2012 she asked her local hospital for a cash price. She got a $79,000 estimate for the surgery.

• MediBid - or $4.95 a month or $25 for a year of unlimited requests, patients can post the medical services they need, and doctors bid for their business.

• "Within two days, I had two quotes."• The prices included her hospital stay, the anesthesiologist, pre-operative

tests and post-surgical visits.• She settled on a surgeon in Glendale who offered to operate for $13,400.

Including the cost of traveling to California, she figures she spent $18,000 for the surgery she got in 2012.

Your Smartphone Will See You Now

By Eric J. Topol Jan. 9, 2015 1:37 p.m. ET The Wall Street Journal

The Creative Destruction of Medicine: How the Digital Revolution Will Create Better Health Care

AliveCor AC-009-I5-A Heart Monitor with Case for Iphone 5

The Future of Medicine Is in Your SmartphoneNew tools are tilting health-care control from doctors to patients

Over the past decade, smartphones have radically changed many aspects of our everyday lives, from banking to shopping to entertainment. Medicine is next. With innovative digital technologies, cloud computing and machine learning, the medicalized smartphone is going to upend every aspect of health care. And the end result will be that you, the patient, are about to take center stage for the first time.

By Eric J. Topol Jan. 9, 2015 1:37 p.m. ET

The Wall Street Journal

Commodity

Changing Business Model

Changing Business Model

Commodity

Product

Changing Business Model

Commodity

Product

Service

Changing Business Model

Commodity

Experience

Product

Service

Changing Business Model

Business Model Has to be consistent with optimal resource utilization

Business Model can tolerate inefficiencies

Changing Business Model

Lowest Margins Commodity

Highest Margins Experience

Changing Business Model

Care Now

Care Decade Ago

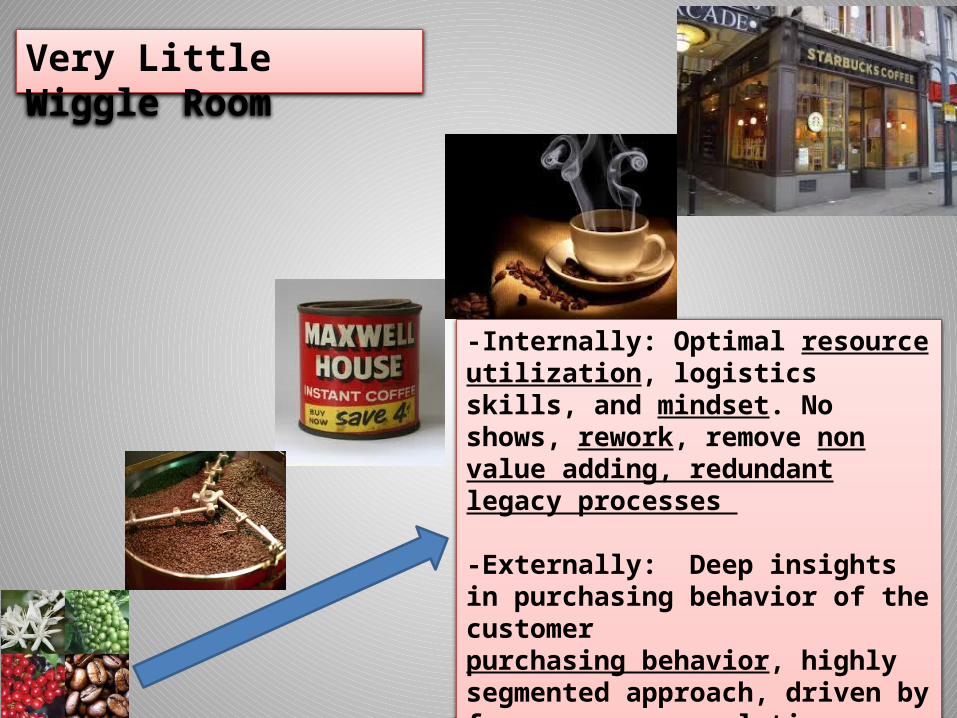

Very Little Wiggle Room

-Internally: Optimal resource utilization, logistics skills, and mindset. No shows, rework, remove non value adding, redundant legacy processes

-Externally: Deep insights in purchasing behavior of the customer purchasing behavior, highly segmented approach, driven by focus groups, analytics, testing pilots

IHI Triple Aim#4 Population Health

Population Health

• Population Health Management: ACOs have strong incentives to improve population health to meet quality goals and reduce costs. To do that, they must stress non-visit care and disease management, build care teams, and work with patients to improve their health behavior.

Population Health

• Population health is defined as the health outcomes of a group of individuals, including the distribution of such outcomes within the group. These groups are often geographic populations such as nations or communities, but can also be other groups such as employees, ethnic groups, disabled persons, prisoners, or any other defined group.

Population Health• The IHI Triple Aim team operationally defines the

term “population health” by the measures used, including measures such as life expectancy; mortality rates; health and functional status; disease burden (the incidence and/or prevalence of chronic disease); and behavioral and physiological factors such as smoking, physical activity, diet, blood pressure, BMI, and cholesterol (as measured via a Health Risk Appraisal).

http://www.ihi.org/communities/blogs/_layouts/ihi/community/blog/itemview.aspx?List=81ca4a47-4ccd-4e9e-89d9-14d88ec59e8d&ID=50

Population Management

• Population Management and the Evolution of Population Medicine

The rapid changes of the last five to seven years in policy-level decision making, payment structures, and provider alignment have shifted the focus from care provided and paid for at an individual level, to managing and paying for health care services for a discrete or defined population – an approach known as population management.

http://www.ihi.org/communities/blogs/_layouts/ihi/community/blog/itemview.aspx?List=81ca4a47-4ccd-4e9e-89d9-14d88ec59e8d&ID=50

Population Medicine

Population medicine is the design, delivery, coordination, and payment of high-quality health care services to manage the Triple Aim for a population using the best resources we have available to us within the health care system. Much of the efforts today such as the Accountable Care Organization, risk stratification methods, patient registries, Patient Centered Medical Home, and other models of team-based care are all part of a comprehensive approach to population medicine.

http://www.ihi.org/communities/blogs/_layouts/ihi/community/blog/itemview.aspx?List=81ca4a47-4ccd-4e9e-89d9-14d88ec59e8d&ID=50

“The core structure of medicine—how health care is organized and practiced—emerged in an era when doctors could hold all the key information patients needed in their heads and manage everything required themselves. One needed only an ethic of hard work, a prescription pad, a secretary, and a hospital willing to serve as one’s workshop, loaning a bed and nurses for a patient’s convalescence, maybe an operating room with a few basic tools. We were craftsmen. We could set the fracture, spin the blood, plate the cultures, administer the antiserum. The nature of the knowledge lent itself to prizing autonomy, independence, and self-sufficiency among our highest values, and to designing medicine accordingly. But you can’t hold all the information in your head any longer, and you can’t master all the skills. No one person can work up a patient’s back pain, run the immunoassay, do the physical therapy, protocol the MRI, and direct the treatment of the unexpected cancer found growing in the spine.”

May 26, 2011 Cowboys and Pit CrewsBy Atul Gawande

#5 Cost and Compensation

• Shift risk to providers and consumers• Rise of ACOs and alternative payment• Medical tourism• Cost apps• Understanding cost of care• You can’t be average• Physicians can not longer just focus on clinical

expertise

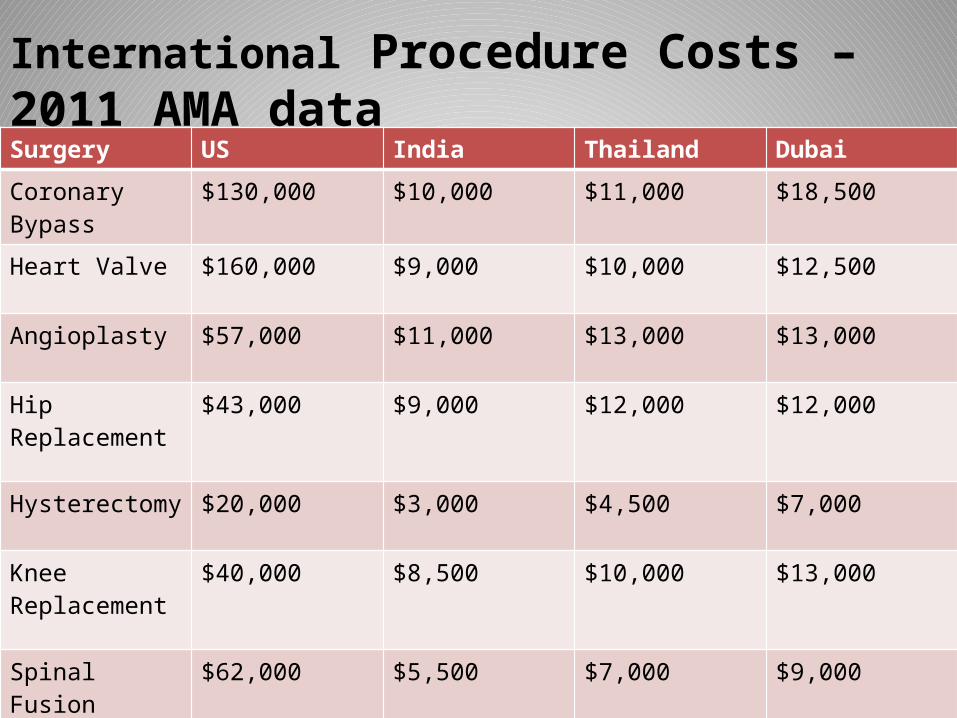

Surgery US India Thailand Dubai

Coronary Bypass $130,000 $10,000 $11,000 $18,500

Heart Valve $160,000 $9,000 $10,000 $12,500

Angioplasty $57,000 $11,000 $13,000 $13,000

Hip Replacement $43,000 $9,000 $12,000 $12,000

Hysterectomy $20,000 $3,000 $4,500 $7,000

Knee Replacement

$40,000 $8,500 $10,000 $13,000

Spinal Fusion $62,000 $5,500 $7,000 $9,000

International Procedure Costs – 2011 AMA data

But what about Quality?

UnitedHealthcare Health4Me ™ Mobile Application

myHealthcare Cost EstimatormyHealthcare Cost Estimator is changing the way you access personalized information, for the better. Using your benefit information, myHealthcare Cost Estimator shows you the estimated cost for a treatment or procedure, and how that cost is impacted by your deductible, co-insurance and out-of-pocket maximum. This means that you’ll get an estimate of what you’ll be responsible for paying out of your pocket, providing you with useful information for planning and budgeting

Physician Compensation trends 2014 – www.medscape.com

Physician Compensation trends 2014 – www.medscape.com

Cost Questions

• Who’s cost are you talking about?• How much does it cost to produce a service

like a cholecystectomy?• How much does it cost to care for a typical

diabetic for one year?• Do you have reliable, believable data to make

data driven decisions?

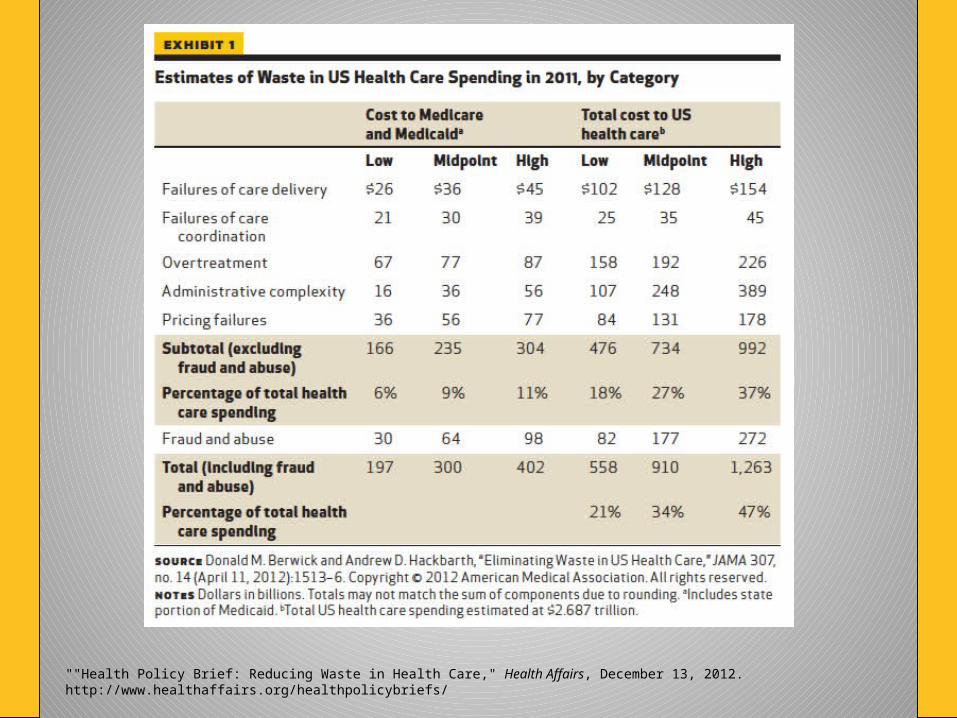

""Health Policy Brief: Reducing Waste in Health Care," Health Affairs, December 13, 2012.http://www.healthaffairs.org/healthpolicybriefs/

Change is Hard

• In the final analysis this is a big time cultural change. We’re looking for opportunities to lead that change. The losers will be organizations who cannot change, who are unable to redesign in ways that allows us to move forward and meet the needs of our society, in improving quality and safety and lowering costs…..You don’t need to be champion, but you cannot be an impediment to moving forward.”

Dr Gary Kaplan, CEO Virginia Mason Medical Center - Seattle

“In an ideal world, all physicians would be leaders with a clear commitment to patients in their journey through the healthcare system – caring about access, affordability, safety, everything. In this ideal state, physicians would eagerly take on broader responsibility, recognizing that with the unique influence doctors possess comes a responsibility for everything concerning a patient’s healthcare experience.”

Change is Hard