Chandulal M Shah & Co.

16

GST Updates Chandulal M Shah & Co. Vol. 05/2020

Transcript of Chandulal M Shah & Co.

GST Updates

Chandulal M Shah & Co.

Vol. 05/2020

P a g e 1 | 15

Chandulal M Shah & Co.

Background of Refund under Inverted duty structure:

In GST, there are two types of scenario where Refunds is admissible:

1. Refund in case of Zero rate supplies (Exports or SEZ) 2. Refund on account of Inverted duty structure.

Inverted duty structure means the case where GST rate of input (Purchase/Expense) is higher than GST rate of output (Sale). Under such scenario there will be an accumulation of GST Credit due to higher rate of GST on inputs and hence input tax credit availed will remain unutilized which would be eligible for refund. The issue under the consideration was whether while claiming refund of unutilized input tax credit on account of inverted duty structure, refund eligible was restricted only to accumulated ITC of inputs (Goods) or whether refund of accumulated ITC of both Inputs and Input services (Goods as well as services) allowed? Rule 89(5) of CGST Rules, 2017 which deals with the calculation of refund of inverted tax amended in April-2018 retrospectively from 01st July 2017 with Notification No: 21/2018 central tax dated 18th April 2018 which remove the benefits of ITC refund on ‘Input services’ and allow refund only of ‘Inputs’. In other word, as per calculation of refund formula, one would be able to claim ITC refund of goods only and not ITC refund of services. Many petitions have been filed before various High Court challenging the validity of Rule 89(5) because there is no such restriction which has been imposed through GST Act that Input service will not be considered while claiming refund under this category but such restriction has been imposed by way of Rules that too with retrospective effect. Recently, Hon’ble Gujarat High Court has held in the case of VKC FOOTSTEPS INDIA PVT. LTD. V/S UNION OF INDIA & 2 Other(s) that the refund is admissible of both inputs (Goods) as well as input services (Services) both.

Facts of the case and argument by petitioner

Petitioner manufacture and supplies footwear which is taxable @ 5% and have inward supply of Job work (services) and Leather, PU etc. (Inputs/Goods) taxable @ 12%/18%.

Section 54(3) which gives refund of any unutilized input tax credit that means input tax credit of input service would also be eligible for refund.

Inverted rate duty structure Refund changes after Hon’ble Guj.

High court decision

P a g e 2 | 15

Chandulal M Shah & Co.

Rule 89(5) is ultra-virus to section 54 of the Act. Rule cannot override Act.

Rule 89(5) cannot be amended retrospectively

Once rate of input is higher than rate on output, then all refund of input tax credit of input and input services should be allowed.

There is no power under section 54(3) which enable authority to frame rules.

Argument of the petitioner in nutshell, request refund of input tax credit of input as well input service both that is refund of tax paid on Jobwork being input service as well as tax paid on leather, PU being input/goods.

Key points of Hon’ble High court decision

Rules which goes beyond the statues is ultra vires and hence its liable to struck down.

Rule 89(5) is contrary to provision of 54(3) to the extent it won’t include refund of input services.

Input and Input services both are part of “Input tax credit”

Hence, Hon’ble Gujarat High Court Pronounced the judgement in the favour of the taxpayer stating that while calculating refund of unutilized input tax credit, Input tax credit of Inputs that is Goods as well as Input tax credit of input services that is services both would be counted which remains unutilized and have higher GST rate.

Refund Comparison in pre and post judgement scenario

Let’s take an example to understand effect of this judgement. XYZ Ltd is a Solar panel manufacturer and the GST rate of solar panels is 5% (Output tax rate) Sale transaction of solar panel is as below. Particulars Quantity Rate Tax

Rate Taxable Value

CGST SGST

Solar Panel

1000 10.00 5% 10,000.00 250.00 250.00

Total Tax Payable 250.00 250.00

P a g e 3 | 15

Chandulal M Shah & Co.

XYZ Ltd procures some Inputs and Inputs services both to manufacture this solar panel and details of purchases are follows:

Inputs/Input Services

CGST SGST Total

Inputs @ 18% 100.00 100.00 200.00

Inputs @ 28% 200.00 200.00 400.00

Input Services @ 18%

150.00 150.00 300.00

As the Output tax rate for the product is higher than the inputs and inputs services tax rate, this situation leads to accumulation of ITC eligible for refund which is governed by Section 54(3) of CGST Act, 2017. The provision for rule 89(5) of CGST Rules, 2017 prescribes a formula for determining the refund on account of inverted duty structure as follows:

Maximum Refund Amount = {(Turnover of inverted rated supply of goods and services) x Net ITC ÷ Adjusted Total Turnover} - tax payable on such inverted rated supply of goods and services. Net ITC =Net ITC shall mean input tax credit availed on inputs during the relevant period other than the input tax credit availed for which refund is claimed under sub-rules (4A) or (4B) or both. (Please note that Net ITC formulae prescribed here doesn’t include ITC on Input service)

Case-A Before Court’s Judgement Scenario:

Inputs/Input Services

CGST SGST Eligible for refund?

NET ITC as per Rule 89(5)

Inputs @ 18% 100 100 Yes 200

Inputs @ 28% 200 200 Yes 400

Input Services @ 18%

150 150 No -

Net ITC eligible for Refund: 600

Calculation of Refund amount:

Turnover of Inverted Rated supply of Goods or services. 10,000

Net ITC as calculated above 600

Adjusted total turnover 10,000

Tax payable on Inverted rate Supply 500

P a g e 4 | 15

Chandulal M Shah & Co.

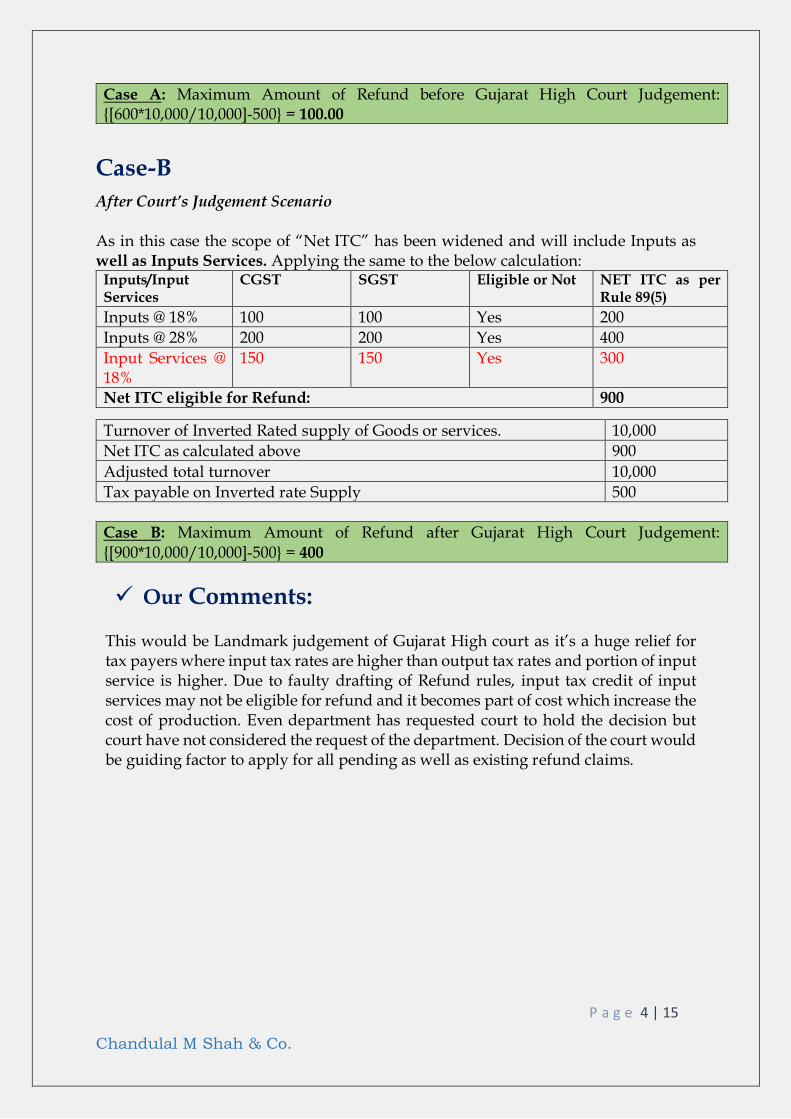

Case A: Maximum Amount of Refund before Gujarat High Court Judgement: {[600*10,000/10,000]-500} = 100.00

Case-B

After Court’s Judgement Scenario

As in this case the scope of “Net ITC” has been widened and will include Inputs as well as Inputs Services. Applying the same to the below calculation:

Inputs/Input Services

CGST SGST Eligible or Not NET ITC as per Rule 89(5)

Inputs @ 18% 100 100 Yes 200

Inputs @ 28% 200 200 Yes 400

Input Services @ 18%

150 150 Yes 300

Net ITC eligible for Refund: 900

Turnover of Inverted Rated supply of Goods or services. 10,000

Net ITC as calculated above 900

Adjusted total turnover 10,000

Tax payable on Inverted rate Supply 500

Case B: Maximum Amount of Refund after Gujarat High Court Judgement: {[900*10,000/10,000]-500} = 400

Our Comments:

This would be Landmark judgement of Gujarat High court as it’s a huge relief for tax payers where input tax rates are higher than output tax rates and portion of input service is higher. Due to faulty drafting of Refund rules, input tax credit of input services may not be eligible for refund and it becomes part of cost which increase the cost of production. Even department has requested court to hold the decision but court have not considered the request of the department. Decision of the court would be guiding factor to apply for all pending as well as existing refund claims.

P a g e 5 | 15

Chandulal M Shah & Co.

E- Invoicing system will be effective from 01st October 2020. The same was

deferred earlier by government which was planned to be implemented in early

2020.

E-Invoicing system shall apply to those taxpayers with Annual turnover

exceeding Rs 500 Crore instead of Rs 100 Crore. Though yet not clarified by

government but it seems that turnover of FY 2019-20 is to be considered.

Exemption from E-invoicing has been granted to Insurance, banking, financial

institution, Non-Banking Financial Companies (NBFC’s), Goods

Transportation Agencies and recently added in exemption list, Special

Economic Zones (SEZ) makes exhaustive list of sectors exempted from E-

Invoicing.

Our Comments:

E-Invoicing would be one of the biggest digital change synchronizing E-Way bill and GST Returns. It would change many processes of business operation since Invoicing mechanism would change from stretch. We believe that business should start implementing E-invoice system in existing ERP/Accounting system and test the functionality, process and modus operandi in advance to avoid and detect error at early stage and developed robust system before October-2020 for smooth functioning.

E-Invoicing Updates

P a g e 6 | 15

Chandulal M Shah & Co.

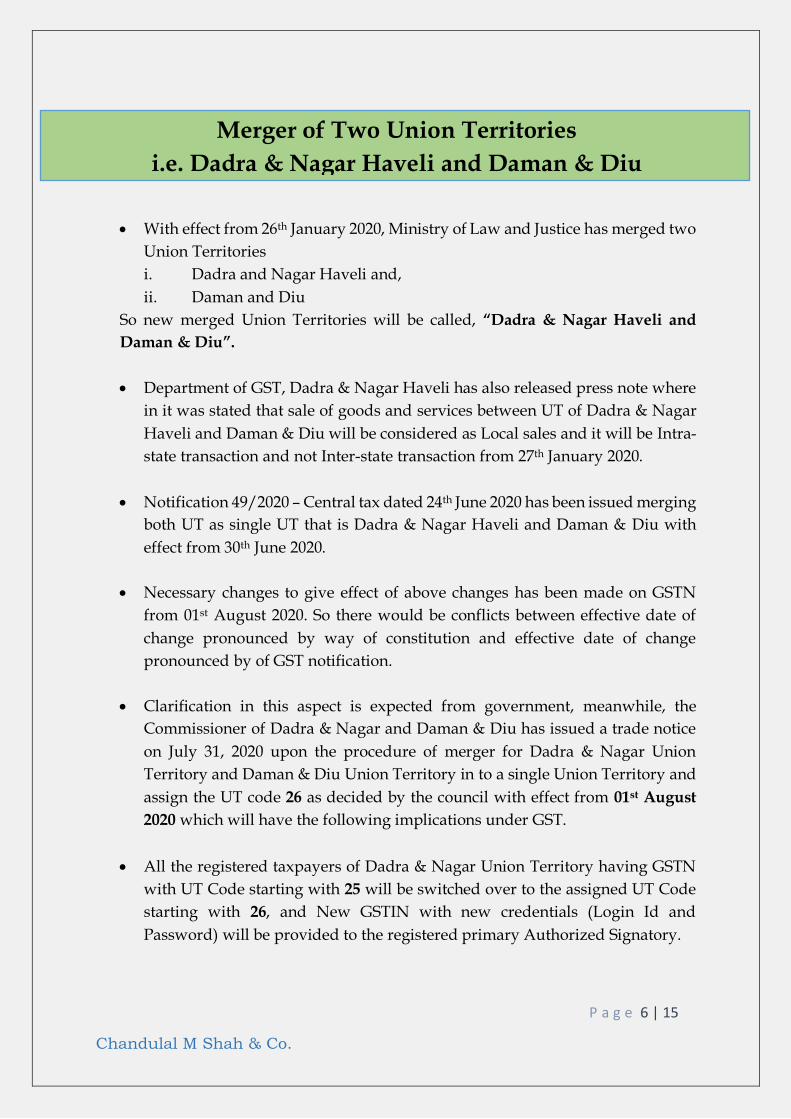

With effect from 26th January 2020, Ministry of Law and Justice has merged two

Union Territories

i. Dadra and Nagar Haveli and,

ii. Daman and Diu

So new merged Union Territories will be called, “Dadra & Nagar Haveli and

Daman & Diu”.

Department of GST, Dadra & Nagar Haveli has also released press note where

in it was stated that sale of goods and services between UT of Dadra & Nagar

Haveli and Daman & Diu will be considered as Local sales and it will be Intra-

state transaction and not Inter-state transaction from 27th January 2020.

Notification 49/2020 – Central tax dated 24th June 2020 has been issued merging

both UT as single UT that is Dadra & Nagar Haveli and Daman & Diu with

effect from 30th June 2020.

Necessary changes to give effect of above changes has been made on GSTN

from 01st August 2020. So there would be conflicts between effective date of

change pronounced by way of constitution and effective date of change

pronounced by of GST notification.

Clarification in this aspect is expected from government, meanwhile, the

Commissioner of Dadra & Nagar and Daman & Diu has issued a trade notice

on July 31, 2020 upon the procedure of merger for Dadra & Nagar Union

Territory and Daman & Diu Union Territory in to a single Union Territory and

assign the UT code 26 as decided by the council with effect from 01st August

2020 which will have the following implications under GST.

All the registered taxpayers of Dadra & Nagar Union Territory having GSTN

with UT Code starting with 25 will be switched over to the assigned UT Code

starting with 26, and New GSTIN with new credentials (Login Id and

Password) will be provided to the registered primary Authorized Signatory.

Merger of Two Union Territories

i.e. Dadra & Nagar Haveli and Daman & Diu

P a g e 7 | 15

Chandulal M Shah & Co.

On or after 01st August 2020, supplies made between Dadra & Nagar haveli

and Daman & Diu will be considered as Intra-state supplies and accordingly

CGST and UTGST shall be charged while supplies made outside the Union

Territory IGST shall be charged.

The Input Tax Credit lying electronic credit ledger UT Code 25 taxpayers shall

have to transfer Input Tax Credit to the New GSTN bearing UT Code 26 and

the same shall be done by debiting the Electronic credit ledger of Old GSTIN in

table 4(B) (2) of GSTR-3B form and crediting the same in table 4(A) (5) of GSTR-

3B form in the New GSTIN. In short, GST Credit will be reversed in GSTR-3B

of Old GSTN and the same GST Credit will be availed in GSTR-3B of New

GSTN.

If any balance is lying is Electronic Cash Ledger the same shall be claimed as

refund by filing refund application.

Any audit/recovery/refund/payment/notice for the period prior to 01st

August 2020 shall be made of Old GSTIN only.

A fresh LUT application has to be filed for the New GSTIN Obtained for

supplying of Goods or Services or both without payment of tax by way of

exports or supply to SEZ.

New signup will be done on E-Waybill website for New GSTIN and the same

shall be complied w.e.f 01st August 2020 onwards.

P a g e 8 | 15

Chandulal M Shah & Co.

Background

The Hon’ble Gujarat High Court has pronounced a judgement where the issue

under consideration was the services provided by Intermediary under cross

border transaction can be treated as export of services hence GST would not be

payable on it.

The Hon’ble Gujarat High Court in the case of Material Recycling Association

of India Vs Union of India and two others held that the services provided by

intermediary or agent in India cannot be treated as “Export of services” and it

should be subject to Goods and Service Tax.

The petitioner that is, Material Recycling Association of India is an association

comprising the recycling industry engaged in the manufacture or metals and

casting etc. The petitioner also acts as an agents for scrape, recycling companies

based outside India engaged in providing intermediary services for the

principal located out of India. The petitioner only earn revenue by way of

commission upon the sale proceeds made by the foreign entity in convertible

foreign exchange.

Definition of Intermediary as given u/s 2(13) of IGST Act.

“Intermediary” means a broker, an agent or any other person, by whatever

name called, who arranges or facilitates the supply of goods or services or both,

or securities, between two or more persons, but does not include a person who

supplies such goods or services or both or securities on his own account”

Facts of the case and Argued by Petitioner

The petitioner earns revenue by way of commission acting as intermediary for

his foreign entity. (Eg: person A in Gujarat provides intermediary services to person B Based in USA to procure an order from person C in Gujarat. A earns commission on sale value of transaction being carried out between B and C )

Services provided by “Intermediary” under cross border transaction is not export of services and subject to GST.

P a g e 9 | 15

Chandulal M Shah & Co.

The services provided by the petitioner should be considered as Export of Services and should not be subject to GST since services are provided outside India.

The GST is a destination based consumption tax accordingly any transaction which terminates outside the territory of India should not be taxed.

The provision under section 13(8) (b) of IGST Act, 2017 is unconstitutional.

The same is violating the principles of Article 286 (No power to levy tax on cross border transaction except by parliament), Article 14 (Equality), Article 19 (Restricting the right to carry trade or profession), and Article 265 (No tax on export transaction) of the constitution of India.

The definition of “Intermediary” under the act is vague i.e. unclear.

Under section 13(8)(b) of the IGST Act, the place of supply of services of Intermediary or Agent service should be treated as location of recipient not the location of supplier.

There is no reason to treat intermediary services differently from the other advisory services as the form of services are substantially same except the performance functions.

The petitioner also claimed that there is a possibility that intermediaries would adopt unreasonable means to escape tax implication catching the grey areas.

Key points of Hon’ble High Court Decision

The Court held that for determining the place of supply for “Intermediary”

section 13(8) (b) of IGST Act, 2017 is to be referred and it says Place of supply

should be the location of supplier i.e. from the place where the

“Intermediaries” are providing the services.

As if the place of supply is the location of supplier and further for charging the

tax, location of supplier and place of supply is to be considered. Since location

of supplier itself becomes place of supply, consequently it will attract CGST

and SGST and would not qualify for Export of Service.

Under Article 246A of The Constitution of India Parliament has exclusive

power to frame laws in respect of interstate supply of goods or services or both.

However, the legislature has thought fit to consider the place of supply in case

P a g e 10 | 15

Chandulal M Shah & Co.

of intermediaries should be location of supplier i.e. the same would be intra-

state transaction and the same is not violating the principles of Article 286 of

The Constitution of India.

Similar situation was also existing in the service tax regime with effect from

October 1st, 2020 and the same has been continued in Goods and Service Tax

also.

Thus it can be said that the provision of section 138(8) (b) are not ultra vires or

unconstitutional in any manner.

Impact of the judgement on some sectors.

Let us analyse the impact of the judgement on various sectors, which are having

cross border transactions, by analysing with provision in details.

In order to classify the services as export of services we need to refer the

definition of Export of services given under 2(6) of IGST Act, 2017 which says: “Export of service” means the supply of any service when,

(a) The supplier of service is located in India. (b) The recipient of service is located outside India. (c) The place of supply of service is located outside India. (d) The payment of such service should be received in convertible foreign

currency. (e) The supplier and recipient are not merely an establishment of distinct

person.

The place of supply provision under section 13 deals where location of one of

the party be it supplier or recipient should be outside India and the relevant

extract is as follows;

i. Section 13(1) the provisions of this section shall apply to determine the

place of supply of services where the location of the supplier of services or

the location of the recipient of services is outside India.

ii. Section 13(2) The place of supply of services except the services provided

under from section 13 sub section (3) to (13) shall be the “location of

recipient” of the services.

P a g e 11 | 15

Chandulal M Shah & Co.

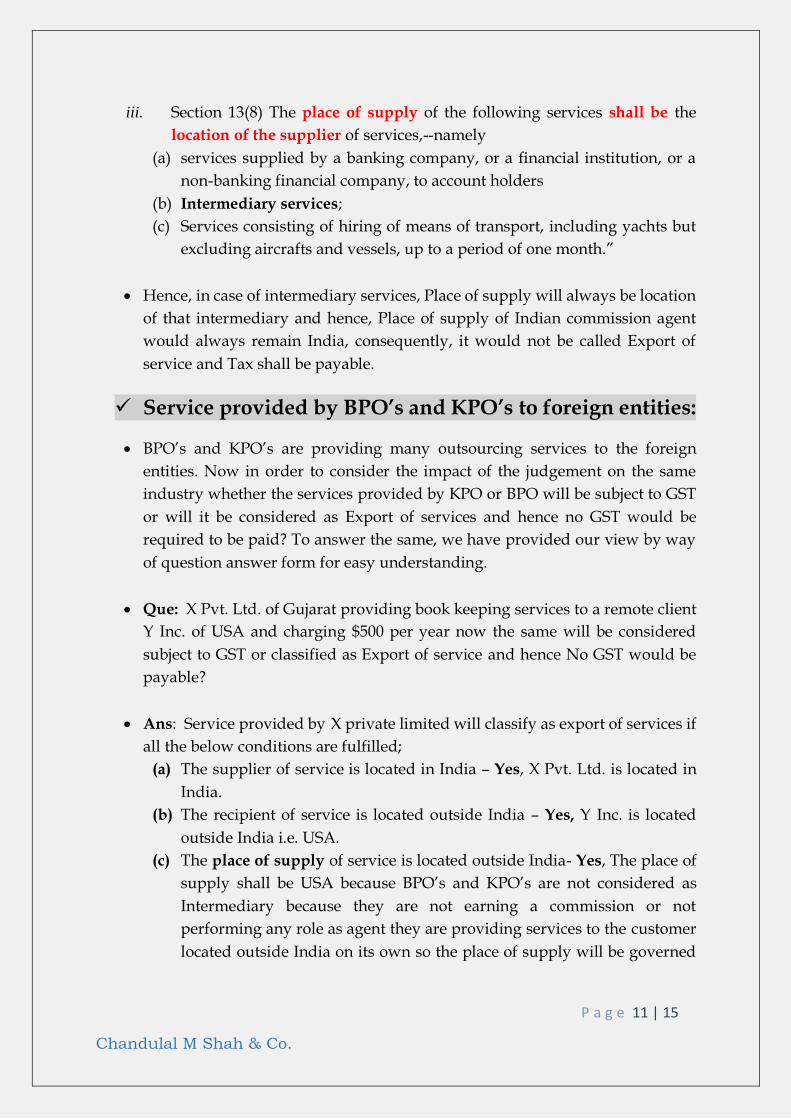

iii. Section 13(8) The place of supply of the following services shall be the

location of the supplier of services,--namely

(a) services supplied by a banking company, or a financial institution, or a

non-banking financial company, to account holders

(b) Intermediary services;

(c) Services consisting of hiring of means of transport, including yachts but

excluding aircrafts and vessels, up to a period of one month.”

Hence, in case of intermediary services, Place of supply will always be location

of that intermediary and hence, Place of supply of Indian commission agent

would always remain India, consequently, it would not be called Export of

service and Tax shall be payable.

Service provided by BPO’s and KPO’s to foreign entities:

BPO’s and KPO’s are providing many outsourcing services to the foreign

entities. Now in order to consider the impact of the judgement on the same

industry whether the services provided by KPO or BPO will be subject to GST

or will it be considered as Export of services and hence no GST would be

required to be paid? To answer the same, we have provided our view by way

of question answer form for easy understanding.

Que: X Pvt. Ltd. of Gujarat providing book keeping services to a remote client

Y Inc. of USA and charging $500 per year now the same will be considered

subject to GST or classified as Export of service and hence No GST would be

payable?

Ans: Service provided by X private limited will classify as export of services if

all the below conditions are fulfilled;

(a) The supplier of service is located in India – Yes, X Pvt. Ltd. is located in

India. (b) The recipient of service is located outside India – Yes, Y Inc. is located

outside India i.e. USA. (c) The place of supply of service is located outside India- Yes, The place of

supply shall be USA because BPO’s and KPO’s are not considered as

Intermediary because they are not earning a commission or not

performing any role as agent they are providing services to the customer

located outside India on its own so the place of supply will be governed

P a g e 12 | 15

Chandulal M Shah & Co.

by general clause which is section 13(2) of IGST Act and hence location of

recipient of services would be place of supply.

If you read the definition of Intermediary, it covers the suppliers of service

such as broker, agent whose primary work is to arrange supplies between

two or more other persons and also those who supplies goods or services

on its own, are not to be considered as intermediary. However, BPO, KPO

are not arranging supplies between two or more other person rather they

are performing on their own. (d) The payment of such service should be received in convertible foreign

currency- Yes, The payment will be received in convertible foreign

exchange. (e) The supplier and recipient are not merely an establishment of distinct

person- Yes, They are not distinct or related persons or establishment of

such person.

Conclusion: All the conditions of export of services are fulfilled so the same

will be considered as Export of services and hence BPO’s and KPO’s Services

will not be subject to GST.

Medical Research Institution for Pharmaceutical sector

One would refer section 13(13) of IGST Act where in it is stated that in order to

prevent double taxation or non-taxation the supply of a service, or for the

uniform application of the rules, the government shall have the power to notify

any description of services or circumstances in which the place of supply shall

be the place of effective use and enjoyment of a service.

Many medical research institution for pharmaceutical sector has been

established in India for the purpose of carrying out the medical and clinical

research in India on behalf of its parent entity situated outside India.

Now, in order to analyse the impact of this judgement on this industry, the test

taken above for export or services will be analysed to check whether such

Research and development carried out in India for foreign entity will be treated

as export of services or will it be subject to GST, we refer below example to

easily understand the impact.

P a g e 13 | 15

Chandulal M Shah & Co.

Que: X Limited a company based in Telangana providing medical research

services to its parent entity X Inc. based in USA. X Ltd charge $5000 for such

services to X Inc. Now the same will be considered as Export of Services or will

it be subject to GST?

Ans: X limited carrying research and development on behalf of X Inc. and

charging $5000. The same will be classified as Export of services if it fulfils all

the conditions for export of services mentioned below;

(a) The supplier of service is located in India – Yes, X Ltd. Is located in India.

(b) The recipient of service is located outside India – Yes, X Inc. is located

outside India i.e. USA.

(c) The place of supply of service is located outside India-

Depending on nature of service provided, Place of supply shall be

decided.

If Research and development service is being carried out on certain goods

which are provided by its customer based outside India and Indian R&D

company needs to work on such goods then the same may fall u/s 13(3)(a)

which is reproduced as below.

13(3) the place of supply of the following services shall be the location

where the services are actually performed, namely:-

Services supplied in respect of goods which are required to be made

physically available by the recipient of services to the supplier of services,

or to a person acting on behalf of the supplier of services in order to

provide the services:

If we go by this provision, then Place of supply would remain where

services are actually performed and hence the same would be in India and

that would not be considered as export of service.

To mitigate this hardship faced by many R&D units, Government has

issued Notification No: 04/2019 IGST on 30th September, 2019 where it

was stated that in case where services are supplied by Indian entity to

recipient based outside India however, due to nature of service provided,

place of supply falls in India so condition of being the same as export of

service is not getting fulfilled.

P a g e 14 | 15

Chandulal M Shah & Co.

In such case, Notification 04/2019- IGST dated 30th Sep 2019 has been

issued which says that in above case, Place of supply shall be location of

recipient and not place of actual performance of service. Result of this

notification is that now it would be considered as export of service

provided other condition simultaneously getting fulfilled.

Relevant extract of notification is as below.

Sr.

No

Description of

services

Place of supply

1 Supply of research and

development services

related to

pharmaceutical sector

as specified in Column

(2) and (3) from Sl. No. 1

to 10 in the Table B by a

person located in

taxable territory to a

person located in the

non-taxable territory

The place of supply of services shall be the

“location of the recipient” of services subject to

fulfillment of the following conditions:-

(i) Supply of services from the taxable territory are

provided as per a contract between the service

provider located in taxable territory and service

recipient located in non-taxable territory.

(ii) Such supply of services fulfills all other

conditions in the definition of export of services,

except sub- clause (iii) provided at clause (6) of

Section 2 of Integrated Goods and Services Tax

Act, 2017 (13 of 2017)

Now to answer the question cited, as per Notification 04/2019-

Integrated tax dated 30th Sep 2019, the place of supply of research

institution will be the “location of Recipient” that is location of X Inc.

which is in USA and hence POS falls outside India in given case.

(d) The payment of such service should be received in convertible foreign

currency- Yes, The payment will be received in convertible foreign exch.

(e) The supplier and recipient are not merely an establishment of distinct

person- Yes, X Limited and X Inc. can be called separate establishment

provided both are separate legal entity and X Inc. should not be merely

branch of X Limited. We premise that both X Limited and X Inc. are

separate legal entity registered in individual country and hence this

condition also gets fulfilled.

Conclusion: All the conditions of export of services are fulfilled so the

services provided by Research and development company will be considered

as Export of services and it will not be subject to GST.

P a g e 15 | 15

Chandulal M Shah & Co.

CONTACT US:

MR. HIREN PATHAK

(M): +91-9033655245

Mail:[email protected]

Disclaimer:

GST Updates in this article are

reproduction of legal provision in

simplified language for better

understanding and it’s for information

purpose only. Our comments and views

are not termed as Legal opinion or

advise. Kindly contact us before taking

any action based on this presentation

for accurate compliances to GST Laws.

CHANDULAL M SHAH & CO. CHARTERED ACCOUNTANTS

OFFICE:

A-6, WING-A, 6TH FLOOR,

SAFAL PROFITAIRE, OPP. AUDA GARDEN,

CORPORATE ROAD, PRAHLADNAGAR,

AHMEDABAD-380052

CONTACT NO: 079- 29601085

www.cmshah.com

![mm. ANTOPHILL Ru]. SHAH & co. LTD. UMMHWHCMM · 2019. 9. 6. · m 2‘"one: am W719‘W.m mmcommum, Ru]. mm.ANTOPHILL SHAH & co. LTD. WWW» 0.4% UMMHWHCMM as“: flmlfl WACW q Ref:](https://static.fdocuments.us/doc/165x107/60d6ee6e239a6976d241b73e/mm-antophill-ru-shah-co-ltd-ummhwhcmm-2019-9-6-m-2aone.jpg)