Champion Manufacturing Industries 2025manufacturing.chipsoftindia.in/Document/CS_242... ·...

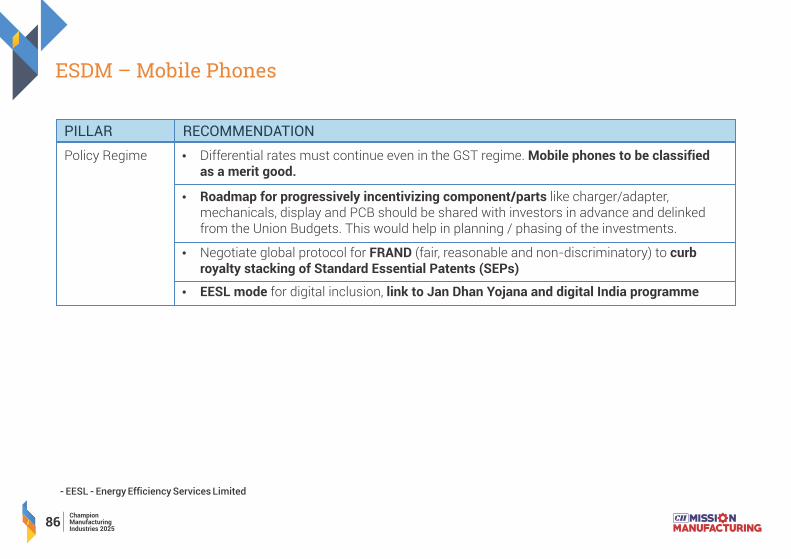

124

Champion Manufacturing Industries 2025

Transcript of Champion Manufacturing Industries 2025manufacturing.chipsoftindia.in/Document/CS_242... ·...

Champion Manufacturing

Industries 2025

Copyright © (2016) Confederation of Indian Industry (CII). All rights reserved.

No part of this publication may be reproduced, stored in, or introduced into a retrieval system, or transmitted in any form or by any means (electronic, mechanical, photocopying, recording or otherwise), in part or full in any manner whatsoever, or translated into any language, without the prior written permission of the copyright owner. CII has made every effort to ensure the accuracy of the information and material presented in this document. Nonetheless, all information, estimates and opinions contained in this publication are subject to change without notice, and do not constitute professional advice in any manner. Neither CII nor any of its office bearers or analysts or employees accept or assume any responsibility or liability in respect of the information provided herein. However, any discrepancy, error, etc. found in this publication may please be brought to the notice of CII for appropriate correction.

Published by Confederation of Indian Industry (CII), The Mantosh Sondhi Centre; 23, Institutional Area, Lodi Road, New Delhi 110003, India, Tel: +91-11-24629994-7, Fax: +91-11-24626149; Email: [email protected]; Web: www.cii.in

Champion Manufacturing

Industries 2025

Table of Contents

Background

Need for Make in India 2.0

03

11

Overall level recommendations

Annexure

Sector and Industry level recommendations

Building Firm Level Competitiveness

25

40

40

105

Executive Summary 01

01Champion Manufacturing Industries 2025

Executive Summary

India is one of the fastest growing emerging economy. Manufacturing is key and at the heart of economic security as it provides a significant multiplier to economy in terms of output and employment creation. As per National Manufacturing Policy 2011, GoI ‘Every job created in manufacturing has a multiplier effect of 2-3X additional jobs in related activities.Manufacturing is thus rightfully at the center-place of Hon’ble Prime Minister’s Vision for Make in India i.e. to increase contribution of manufacturing to GDP to 25%. The manufacturing sector will have to grow at at-least 12.7% year on year to power India’s economic growth story sustainably and to actualize the vision of Make in India. Achieving this high growth trajectory will entail an integral blend of policy interventions and firm-level actions targeted at maximizing local value add, creating scale, capturing global market share and fulfilling India’s job creation needs.

Make in India has brought about a significant shift towards local value addition, sustainable innovation and ease of doing business. It also aims at increasing federal and state alignment for coherent policy making and positions India centre-stage as a global manufacturing hub. In line with the above evolution, CII believes that it istime for the next phase of Make in India or Make in India 2.0 that will strategically identify specific Champion Industries which will drive growth in manufacturing.

With this background CII Manufacturing Council has been working on an initiative to identify Champion Manufacturing industries that have the potential to drive double digit growth in manufacturing and contribute to significant job creation and in which India could be number 1 or 2 in the next 10 years.

CII identified a list of manufacturing sectors that contribute to the majority of manufacturing GDP which include Aerospace and Defense, Auto and Auto Components, Cement, Chemicals, Engineering, ESDM, Pharmaceuticals, Steel and Textiles.

Within these 9 broad sectors CII identified 156 industries that comprise the universe of all major sub-sectors. For each of these 156 industries CII did an analysis on the Commercial and Strategic Attractiveness of the industry. Commercial attractiveness included factors such as Market Attractiveness, Competitive Landscape, Supply Chain Ecosystem, Ease of doing business, Favourable Infrastructure and Human resource capital and while Strategic Attractiveness included factors such as Industry Ecosystem Development, Economic Impact, Investment Favourability, Environment Sustainability.

Basis this criteria, a comparative analysis was done to identify 28 Champion Industries that were leading. These are Aircraft Components, Auto-Electricals & Electronics, Automotive batteries, HCV, Passenger Cars, Two and Three wheelers, Cement, Agro Intermediates, Agro Chemicals, Basic Polymers and Elastomers, Construction Chemicals, Other Performance Chemicals, Valves and Pumps, Construction Machinery, Machine Tools, Pressure Vessels, Solar PV, Lighting (Conv. + LED), Mobile phones, PCB and PCB A, Bulk drugs, Pharma APIs, Generic Pharmaceuticals, Flats, Forgings and Castings, Longs, Apparels and Made-ups.

‘Champion Manufacturing Industries 2025'

02Champion Manufacturing Industries 2025

For each of the industries sectoral committees from within CII identified key interventions that would help give a fillip to the industry. Wide industry consultations were done at each step to ensure accurate articulation of recommendations. Common themes were identified from sectors and across sectors to identify sector level and overall manufacturing level recommendations respectively. The recommendations at the overall and sector level have the potential to create significant positive impact on other industries in the overall manufacturing sector.

Championing Manufacturingin India will entail targeted interventions aimed at unleashing thebasic building blocks of manufacturing such as cost, technology, manpower and policy regime and establishing the drivers for championing manufacturing such as building scale and market share, platform innovation, brand and sustenance.

Using the above framework CII has identified key policy interventions at the overall manufacturing level, sector level and industry level. If pursued these interventions will trigger significant Industry actions translating to the creation of Champion Industries, significant growth in output (from the current average sales growth of 8-10% to 15-20%), employment generation (from the current levels of 0-5% to 5-10%) and increase in India’s share of global manufacturing exports (from 1.6% currently to 3-4%).

CII’s Recipe of Excellence, which is an online tool developed by analysing performance of 32,000 companies and that benchmarks competitiveness across 6 functions – marketing, operations, supply chain, human resources and leadership, research development and technology and environment sustainability and governance to help identify a company’s weakest link, will in tandem help companies become more competitive and enable them to transition from good to great.

CII has shared the study and its findings with senior Government officials including Mr P K Sinha, Cabinet Secretary; Mr Amitabh Kant, CEO, NITI Aayog; the PM-appointed Group of Secretaries on Commerce & Industry (multiple occasions), Mr Ramesh Abhishek, Secretary, DIPP; Mr Ashok Lavasa, Finance Secretary; Ms Rita Teaotia, Commerce Secretary; Dr Aruna Sharma, Secretary, Ministry of Steel; Ms Aruna Sundararajan, Secretary, MEITY; Mr Girish Shankar, Secretary, Department of Heavy Industry, Ms. Rashmi Verma, Secretary, Ministry of Textiles; Mr Anuj Kumar Bishnoi, Secretary, Department of Chemicals & Petrochemicals; Mr. K. K Jalan, Secretary, Ministry of MSME and Ms. M Sathiyavathy, Secretary, Ministry of Labour & Employment. All officials have been very supportive of the initiative.

Mr Abhishek at the inaugural session of the conference on Make in India, Karnataka in February 2017 announced that the CII study would form the basis for Make in India 2.0.

Background

Source : World Bank : 2015 figures

USA 2.4%

Brazil -3.8%

EU 1.9%

Russia -3.7%

China 6.9%

India 7.6%

Japan 0.5%

RSA 1.3%

India –fastest growing emerging economy… need to sustain….

Manufacturing key and at heart of our economic security

05Champion Manufacturing Industries 2025

06Champion Manufacturing Industries 2025

… and, thus, the core of the Hon’ble PM’s Vision for Make in India

- Excerpt from Hon'ble Prime Minister Shri Narendra Modi's speech on the Independence day of India, 15 August 2014, New Delhi

If we have to develop a balance between imports and exports, we will have to strengthen manufacturing sector. If we have to put in use the education, the capability of the youth, we will have to go for manufacturing sector and for this Hindustan also will have to lend its full strength, but we also invite world powers. Therefore I want to appeal [to] all the people world over… "Come, make in India", "Come, manufacture in India". Sell in any country of the world but manufacture here. We have got skill, talent, discipline, and determination to do something… "Come, Make in India.

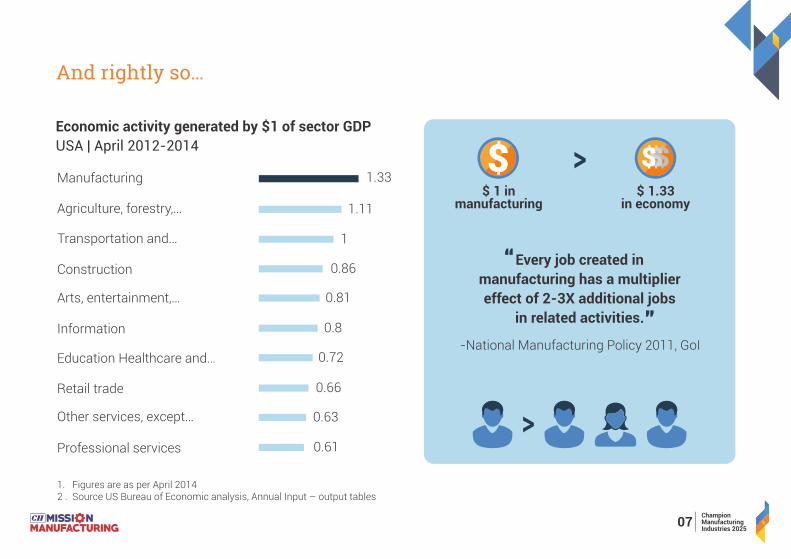

1. Figures are as per April 20142 . Source US Bureau of Economic analysis, Annual Input – output tables

0.61

0.63

0.66

0.72

0.8

0.81

0.86

1

1.11

1.33

Professional services

Other services, except…

Retail trade

Education Healthcare and…

Information

Arts, entertainment,…

Construction

Transportation and…

Agriculture, forestry,…

Manufacturing

And rightly so…

07Champion Manufacturing Industries 2025

-National Manufacturing Policy 2011, GoI

$ 1 in manufacturing

$ 1.33 in economy

Every job created in

manufacturing has a multiplier

effect of 2-3X additional jobs

in related activities.

Economic activity generated by $1 of sector GDP

USA | April 2012-2014

1 At Current PricesUSD 1 = INR 65GDP basis GVA calculation methodology

2015: 1GDP ~USD 1.88 Trillion /

INR 122.79 Lakh Crore

2025: 1GDP ~USD 3.62 Trillion /

INR 235 Lakh Crore

Aspiration:

Manufacturing contribution to GDP

25% = ~ USD 905 Billion / INR 58.85 Lakh Crore

Current:

Manufacturing contribution to GDP 16.2% = ~ USD 306 Billion /INR 19.94

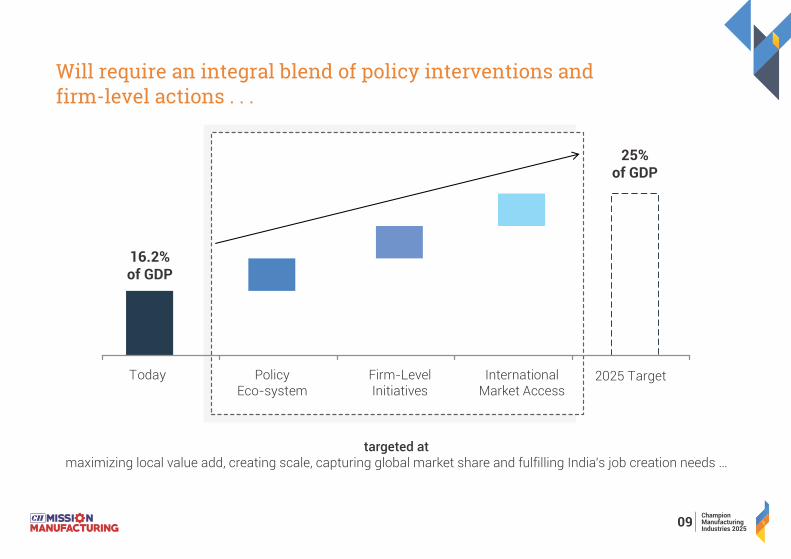

Lakh CroreManufacturing sector will need to grow at least 12.7% y-o-y to reach 25% of total

GDP by 2025

To power India's economic growth story sustainably…

Need to generate 100 million jobs and increase contribution of manufacturing sector to

GDP to 25% by 2025

08Champion Manufacturing Industries 2025

Assuming 7.5%

y-o-y GDP growth

Will require an integral blend of policy interventions and

firm-level actions . . .

Today Policy Eco-system

Firm-LevelInitiatives

InternationalMarket Access

2025 Target

25%of GDP

16.2% of GDP

targeted at maximizing local value add, creating scale, capturing global market share and fulfilling India’s job creation needs …

09Champion Manufacturing Industries 2025

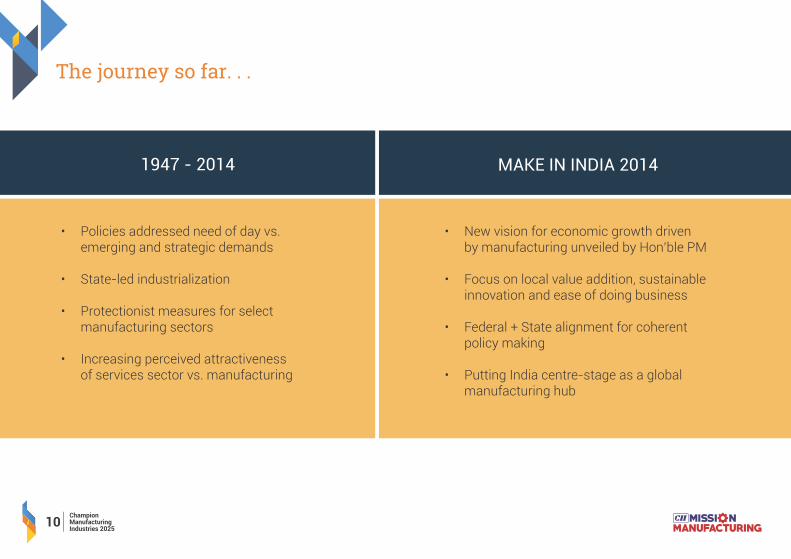

The journey so far. . .

• Policies addressed need of day vs. emerging and strategic demands

• State-led industrialization

• Protectionist measures for select manufacturing sectors

• Increasing perceived attractiveness of services sector vs. manufacturing

• New vision for economic growth driven by manufacturing unveiled by Hon’ble PM

• Focus on local value addition, sustainable innovation and ease of doing business

• Federal + State alignment for coherent policy making

• Putting India centre-stage as a global manufacturing hub

1947 - 2014 MAKE IN INDIA 2014

10Champion Manufacturing Industries 2025

Make in India 2.0

Identify manufacturing industries in which

- India could be number 1 or 2 in the next 10 years

- can drive double digit growth and significant job creation

Focus on

- Scale and market share

- Platform Innovation

- Brand

- Sustenance

STRATEGICALLY IDENTIFY SPECIFIC CHAMPION INDUSTRIES

STRENGTHEN ECO-SYSTEM

MAKE IT HAPPEN

Address issues related to

- Non-competitive costs

- Encouraging technology Investments

- Appropriately skilling manpower

- Empowering policies

MII 2.0 : The Concept

12Champion Manufacturing Industries 2025

Enhancing India’s soft power

The Concept in action . . .

IDENTIFICATION OF TOPMANUFACTURING SECTORS

1. Aerospace and Defense

2. Auto and Auto Components

3. Cement

4. Chemicals

5. Engineering

6. ESDM

7. Pharmaceuticals

8. Steel

9. Textiles

IDENTIFICATION OF UNIVERSE OF INDUSTRIES

Criteria for Filtration

• Local Manufacturing

• Dependence on Imports

• Ability to Manufacture

• Ability to Export

• Potential for Disruption

Current Driver

Future Indicator

~156 industries

13Champion Manufacturing Industries 2025

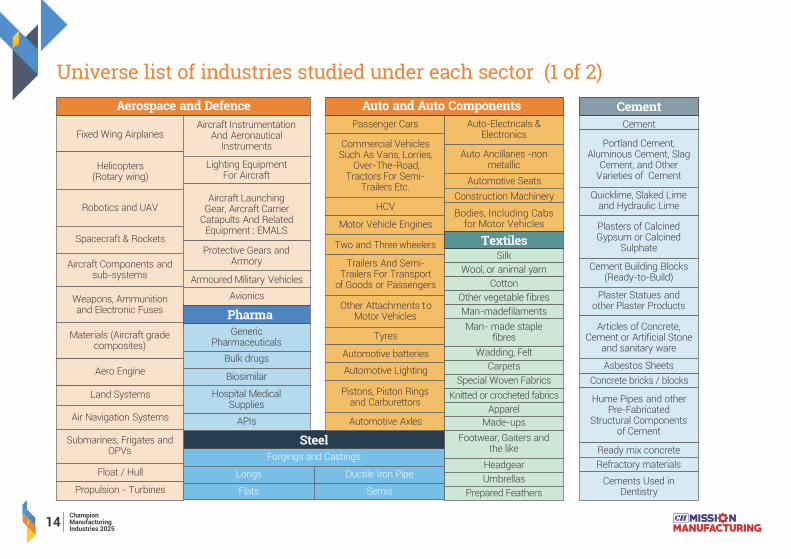

Universe list of industries studied under each sector (1 of 2)

Forgings and Castings

Longs

Flats

Ductile Iron Pipe

Semis

Steel

Fixed Wing Airplanes

Helicopters(Rotary wing)

Robotics and UAV

Spacecraft & Rockets

Aircraft Components and sub-systems

Weapons, Ammunition and Electronic Fuses

Materials (Aircraft grade composites)

Aero Engine

Land Systems

Air Navigation Systems

Submarines, Frigates and OPVs

Float / Hull

Aircraft Instrumentation And Aeronautical

Instruments

Lighting EquipmentFor Aircraft

Aircraft Launching Gear, Aircraft Carrier

Catapults And Related Equipment ; EMALS

Avionics

Protective Gears and Armory

Armoured Military Vehicles

Generic Pharmaceuticals

Bulk drugs

Hospital Medical Supplies

APIs

Biosimilar

Pharma

Propulsion - Turbines

Aerospace and Defence

Passenger Cars

Commercial Vehicles Such As Vans, Lorries,

Over-The-Road, Tractors For Semi-

Trailers Etc.

HCV

Motor Vehicle Engines

Two and Three wheelers

Trailers And Semi-Trailers For Transport

of Goods or Passengers

Other Attachments to Motor Vehicles

Tyres

Automotive batteries

Automotive Lighting

Pistons, Piston Rings and Carburettors

Automotive Axles

Auto-Electricals & Electronics

Auto Ancillaries -non metallic

Automotive Seats

Construction Machinery

Bodies, Including Cabs for Motor Vehicles

Knitted or crocheted fabrics

Wadding, Felt

Carpets

Special Woven Fabrics

Silk

Cotton

Other vegetable fibres

Man- made staple fibres

Man-madefilaments

Wool, or animal yarn

Apparel

Made-ups

Footwear, Gaiters and the like

Headgear

Umbrellas

Prepared Feathers

Textiles

Auto and Auto Components

Portland Cement, Aluminous Cement, Slag

Cement, and Other Varieties of Cement

Quicklime, Slaked Lime and Hydraulic Lime

Asbestos Sheets

Concrete bricks / blocks

Hume Pipes and other Pre-Fabricated

Structural Components of Cement

Ready mix concrete

Refractory materials

Cements Used in Dentistry

Plasters of Calcined Gypsum or Calcined

Sulphate

Cement Building Blocks (Ready-to-Build)

Plaster Statues and other Plaster Products

Articles of Concrete, Cement or Artificial Stone

and sanitary ware

Cement

Cement

14Champion Manufacturing Industries 2025

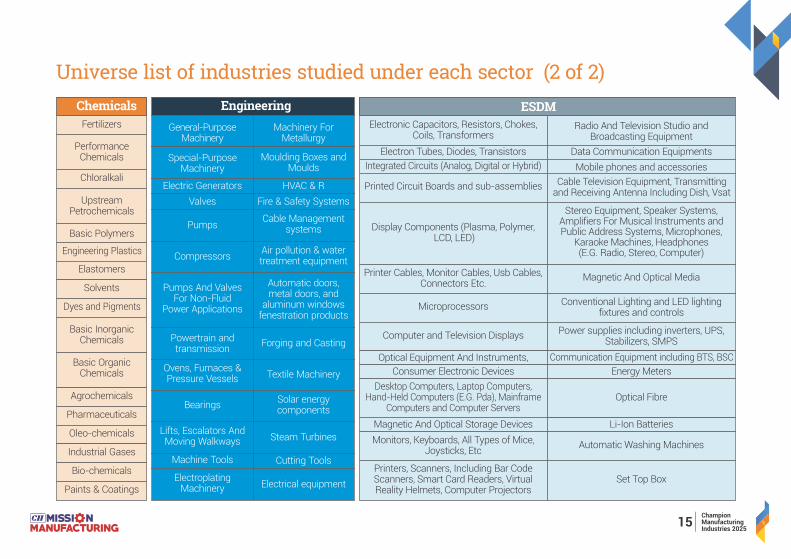

Universe list of industries studied under each sector (2 of 2)

Electroplating Machinery Electrical equipment

HVAC & R

Machinery For Metallurgy

Moulding Boxes and Moulds

Air pollution & water treatment equipment

Automatic doors, metal doors, and

aluminum windows fenestration products

General-Purpose Machinery

Special-Purpose Machinery

Electric Generators

Valves

Powertrain and transmission

Ovens, Furnaces & Pressure Vessels

Bearings

Lifts, Escalators And Moving Walkways

Machine Tools

Cable Management systemsPumps

Pumps And Valves For Non-Fluid

Power Applications

Compressors

Solar energy components

Steam Turbines

Fire & Safety Systems

Forging and Casting

Textile Machinery

Cutting Tools

Engineering

Basic Polymers

Chloralkali

Performance Chemicals

Upstream Petrochemicals

Fertilizers

Solvents

Dyes and Pigments

Elastomers

Basic Inorganic Chemicals

Basic Organic Chemicals

Agrochemicals

Pharmaceuticals

Bio-chemicals

Paints & Coatings

Industrial Gases

Oleo-chemicals

Chemicals ESDM

Data Communication Equipments

Mobile phones and accessories

Stereo Equipment, Speaker Systems, Amplifiers For Musical Instruments and Public Address Systems, Microphones,

Karaoke Machines, Headphones (E.G. Radio, Stereo, Computer)

Magnetic And Optical Media

Automatic Washing Machines

Radio And Television Studio andBroadcasting Equipment

Conventional Lighting and LED lighting fixtures and controls

Power supplies including inverters, UPS, Stabilizers, SMPS

Energy Meters

Electron Tubes, Diodes, Transistors

Printed Circuit Boards and sub-assemblies

Printer Cables, Monitor Cables, Usb Cables, Connectors Etc.

Magnetic And Optical Storage Devices

Monitors, Keyboards, All Types of Mice, Joysticks, Etc

Printers, Scanners, Including Bar Code Scanners, Smart Card Readers, Virtual Reality Helmets, Computer Projectors

Electronic Capacitors, Resistors, Chokes, Coils, Transformers

Microprocessors

Computer and Television Displays

Consumer Electronic Devices

Optical Equipment And Instruments,

Display Components (Plasma, Polymer, LCD, LED)

Integrated Circuits (Analog, Digital or Hybrid)

Optical FibreDesktop Computers, Laptop Computers,

Hand-Held Computers (E.G. Pda), Mainframe Computers and Computer Servers

Li-Ion Batteries

Set Top Box

Communication Equipment including BTS, BSC

Cable Television Equipment, Transmitting and Receiving Antenna Including Dish, Vsat

Engineering Plastics

15Champion Manufacturing Industries 2025

The Concept in action . . .

CRITERIA FOR FILTRATION

• Market Attractiveness

• Competitive Landscape

• Supply Chain Ecosystem

• Ease of doing business

• Favourable Infrastructure

• Human resource capital

• Industry Ecosystem Development

• Economic Impact

• Investment Favourability

• Environment Sustainability

Strategic Attractiveness

Commercial Attractiveness

IDENTIFICATION OF TOPMANUFACTURING SECTORS

IDENTIFICATION OF UNIVERSE OF INDUSTRIES

1. Aerospace and Defense

2. Auto and Auto Components

3. Cement

4. Chemicals

5. Engineering

6. ESDM

7. Pharmaceuticals

8. Steel

9. Textiles

IDENTIFICATION OF CHAMPIONINDUSTRIES BASED ON

1CA AND SA

CRITERIA FOR FILTRATION

Current Driver

• Local Manufacturing

• Dependence on Imports

Future Indicator

• Ability to Manufacture

• Ability to Export

• Potential for Disruption

~156 industries

1 Commercial Attractiveness (CA) ; Strategic Attractiveness (SA)

16Champion Manufacturing Industries 2025

Detailing of criteria …

Industry Ecosystem

Development30%

Economic Impact

35%

Investment Favourability

20%

Environment Sustainability

15%

Availability/ Use of Industry Clusters

Information Availability/ Ease of Networking

Impact on Ancillary Industries/ Services

Contribution to GDP

Job Creation/ Potential

Ability to drive future investments

FDI inflow

Attractiveness for Local Capital Investment

Favourable FDI regulations/ rules

Impact on Environment

Environmental Regulations/ Framework

Reporting on Environment

40%

Factor Sub-Factor Weight

30%

30%

40%

25%

35%

45%

25%

30%

45%

35%

20%

Strategic Attractiveness

Factor Sub-Factor Weight

Market Attractiveness

20%

Competitive Landscape

15%

Supply Chain Ecosystem

20%

EODB15%

Infrastructure20%

Human Resource

Capital10%

Indian Market Contribution to the globe

Expected Indian Market Contribution to the globe

Growth rate (2014/5-2025) (India)

Export Potential

Import Substitution

Substitute global location (that could compete with India)

No. of domestic players

Market Concentration

Availability of local downstream suppliers

Maturity of existing supply chain ecosystem

Ease of establishment (registration, approvals, licenses etc.)

Infrastructure availability (land, equipment etc).

Technology availability

Cost Associated with the infrastructure

Frequency of labour disruption

Availability of skilled labour

Cost of labour

30%

30%

20%

10%

10%

30%

30%

40%

50%

50%

100%

35%

30%

35%

50%

35%

15%

Commercial Attractiveness

17Champion Manufacturing Industries 2025

CRITERIA FOR FILTRATION

• Market Attractiveness

• Competitive Landscape

• Supply Chain Ecosystem

• Ease of doing business

• Favourable Infrastructure

• Human resource capital

• Industry Ecosystem Development

• Economic Impact

• Investment Favourability

• Environment Sustainability

Strategic Attractiveness

Commercial Attractiveness

The Concept in action . . .

IDENTIFICATION OF TOPMANUFACTURING SECTORS

IDENTIFICATION OF UNIVERSE OF INDUSTRIES

1. Aerospace and Defense

2. Auto and Auto Components

3. Cement

4. Chemicals

5. Engineering

6. ESDM

7. Pharmaceuticals

8. Steel

9. Textiles

IDENTIFICATION OF CHAMPIONINDUSTRIES BASED ONCA AND SA1

CRITERIA FOR FILTRATION

• Local Manufacturing

• Dependence on Imports

• Ability to Manufacture

• Ability to Export

• Potential for Disruption

Current Driver

Future Indicator

~156 industries

~28industries identified

1 Commercial Attractiveness (CA) ; Strategic Attractiveness (SA)

18Champion Manufacturing Industries 2025

… Translating to

Strategically Attractive

Emerging Commercially Attractive

• Ready-Mix Concrete

• Performance Plastics

• Electronic Capacitors, Resistors, Chokes, Coils, Transformers

• Semis

• Armoured Military Vehicles

• Robotics and UAV

• Spacecraft & Rockets

• Refractory Materials

• Electronic Chemicals

• Excipients and Additives

• Solvents

• Air pollution & water

treatment equipment

• Automatic doors, metal doors,

and aluminium windows

fenestration products

• Fire & Safety Systems

• FiberOptics

• Set Top Box

• Biosimilar

• Ductile Iron Pipe

• Aircraft Components and sub-systems

• Auto-Electricals & Electronics

• Automotive batteries

• Construction Machinery

• HCV

• Passenger Cars

• Two and Three wheelers

• Cement

• Agro Intermediates

• Agro Chemicals

• Basic Polymers and Elastomers

• Construction Chemicals

• Other Performance Chemicals

• Auto Ancillaries -non metallic

• Automotive Lighting

• Automotive Seats

• Cable Management systems

• Compressors

• HVAC & R

• Industrial Bearings

• Powertrain and transmission

• Power supplies including

inverters, UPS, Stabilizers,

SMPS

• Valves and Pumps• Machine Tools• Pressure Vessels• Solar PV• Lighting (Conv. + LED)• Mobile phones• PCB and PCB A• Bulk drugs• Pharma APIs• Generic Pharmaceuticals• Flats• Forgings and Castings• Longs• Made-ups• Apparel

Moderate HighCommercially Attractive

Co

mm

erc

ially

Att

racti

ve

M

od

era

teH

igh

Source : Frost & Sullivan Analysis

19Champion Manufacturing Industries 2025

Most Attractive – Champion Industries

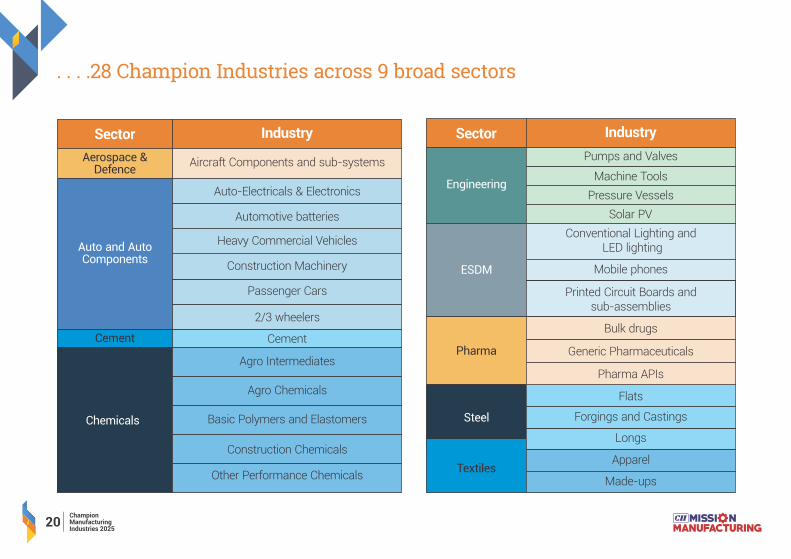

. . . .28 Champion Industries across 9 broad sectors

Aircraft Components and sub-systems

Sector Industry Sector Industry

Conventional Lighting and LED lighting

Mobile phones

Printed Circuit Boards and sub-assemblies

Aerospace & Defence

Cement

Engineering

ESDM

Pharma

Steel

Textiles

20Champion Manufacturing Industries 2025

Apparel

Flats

Forgings and Castings

Longs

Made-ups

Bulk drugs

Generic Pharmaceuticals

Pharma APIs

Auto-Electricals & Electronics

Automotive batteries

Heavy Commercial Vehicles

Construction Machinery

Passenger Cars

2/3 wheelers

Cement

Other Performance Chemicals

Construction Chemicals

Basic Polymers and Elastomers

Agro Chemicals

Agro Intermediates

Pumps and Valves

Machine Tools

Pressure Vessels

Solar PV

Chemicals

Auto and Auto Components

Mapping of Select GoI Schemes

Sanitation & Healthcare Urbanization

Competitiveness : Make in India, Skill India, Digital India

• Smart City Mission

• Housing for All

• AMRUT

• HRIDAY

• Deen Dayal e-Rickshaw Project

Roads / Highways

• Setu Bharatam Project

• Swadesh Darshan Yojana

• Pradhan Mantri Gram Sadak Yojana

Ports - SagarMala Project

Power

• Prakash Path (UJALA)

• National Solar Mission

• National Renewables Mission

• Deen Dayal Upadhaya Gram Jyoti Yojana

• Pradhan Mantri Awas Yojana (Rural)

• Pradhan Mantri Gram SinchaiYojana

• SPMRM or RURBAN India Mission

• Swachh Bharat

• Indradhanush

• Namami Gange Mission

• National Health Mission

Infrastructure Rural Transformation

Cement; Basic Polymers and Elastomers; Construction Chemicals; Other Performance Chemicals; Construction Machinery; Pumps and valves; Solar PV; Conventional Lighting and LED lighting; Mobile phones; Printed Circuit Boards and sub-assemblies; Bulk drugs ; Generic Pharmaceuticals; Pharma APIs; Flats; Forgings and Castings; Longs

Heavy Commercial Vehicles; Two and Three wheelers; Cement; Basic Polymers and Elastomers; Construction Chemicals; Other Performance Chemicals; Construction Machinery; Flats; Forgings and Castings; Longs

Heavy Commercial Vehicles; Basic Polymers and Elastomers; Construction Chemicals; Other Performance Chemicals; Construction Machinery; Pumps and valves; Machine Tools; Pressure Vessels; Solar PV; Conventional; Lighting and LED lighting; Printed Circuit Boards and sub-assemblies; Flats; Forgings and Castings; Longs; Made-ups; Apparel

Heavy Commercial Vehicles; Two and Three wheelers; Cement; Basic Polymers and Elastomers; Construction Chemicals; Other Performance Chemicals; Construction Machinery; Pumps and valves; Machine Tools; Solar PV; Conventional; Lighting and LED lighting; Mobile phones; Printed Circuit Boards and sub assemblies; Flats; Forgings and Castings; Longs

21Champion Manufacturing Industries 2025

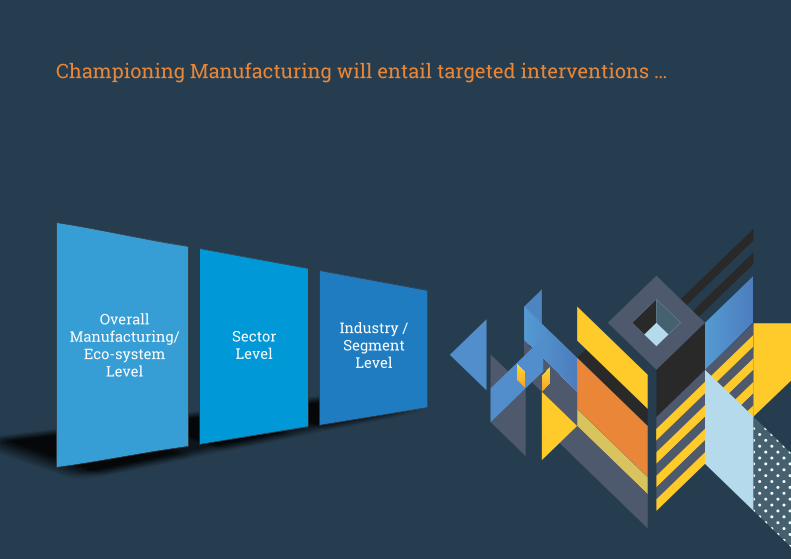

Championing Manufacturing will entail targeted interventions …

Overall Manufacturing/

Eco-system Level

Industry / Segment

Level

Sector Level

…aimed at…

23Champion Manufacturing Industries 2025

Establishing theDrivers for ChampioningManufacturing

Scale & Market Share

Brand

Sustenance

Unleashing theBasic Building Blocksof Manufacturing

Cost

Technology

Manpower

Policy Regime

Platform Innovation

• Zero Defect

• IP & Global Standards

• Skills Availability

• India Brand

• Plug and Play

• IP & Global Standards

• Institutional Eco-system

• Collaborations

• Testing

• Skills Availability

• Taxation

• Cluster Development

• Zero Defect

• IP & Global Standards

• Institutional Eco-system

• Skills Availability

• Labour Flexibility

• Regulatory

• Policy Certainty

• Environment

• Compliance

• Plug andPlay

• Finance

• Power

• Raw Material

• Logistics

• Zero Defect

• Automation

• IP & Global Standards

• Testing

• Skills Availability

• Labour Flexibility

• Regulatory

• Taxation

• Land

• Policy Certainty

• Environment

• Trade

• Cluster Development

Manpower

Policy Regime

• Plug and Play infra

• Finance

• Power

• Raw Material

• Logistics

• Zero Defect

• IP & Global Standards

• Institutional Eco-system

• Collaborations

• Automation

• Testing

• Skills Availability

• Labour Flexibility

• Regulatory

• Policy Certainty

• Taxation

• Land

• Environment

• Trade

• Cluster Development

• Compliance

• India Brand

Cost

Basic Building Blocks ofManufacturing

…instilling a holistic framework to create champion industries

Drivers for Championing Manufacturing

Scale and MarketShare

PlatformInnovation Brand Sustenance

Technology

24Champion Manufacturing Industries 2025

Overall Manufacturing Level Recommendations

Overall Manufacturing/

Eco-system Level

Industry / Segment

Level

Sector Level

Core strategies to champion manufacturing (1/4)

POLICY

Legend ImportantImperative

26Champion Manufacturing Industries 2025

Recognize Champion Industries through special and differential treatment for next 10 years

• Harmonize Indian standards with internationally accepted standards

• Provide stable and co-ordinated policy regime transitions with adequate lead times and certainty e.g.

environmental related regulations in Auto, Cement, Chemicals, Construction Equipment, Pharma, etc.

• Accelerate the announced policy to lower the corporate tax rate to an internationally competitive 18%

• Modify Government procurement approach

- Through domestic purchase preference

- Shift criteria from L1 to TCO1 (Life Cycle Cost of Ownership –Initial Price, Running Cost, Durability,

Sustainability)

- Remove prior track record clause for indigenously developed new products and establish clear mechanism

for validation

•

-

Resource Efficiency (energy, water, minerals)

Introduce Green Project Rating system for Government Projects (focus –Emissions, Waste recovery,

Core strategies to champion manufacturing (2/4)

POLICY

• Expedite setting-up of an umbrella USTR-cum-USITC type body to strengthen the trade negotiating capacity

and streamline review processes for speedy and time bound trade remedial actions

• Enhance Champion Industry Branding –integrate India’s commercial missions with brand building initiative

–structured engagement with diplomats for industry sensitisation and specific KRAs for growth of market

share of India product portfolio

• Speedy implementation of a simple and deflationary GST

• Encourage multilateral funding towards champion industries for lower costs of finance

• Incentivize manufacturers to develop products that have pre-defined targets for reduction in TCO and

emission footprint year on year

• Encourage FDI for setting up R&D labs with financial incentives

• Prioritize EODB for champion sectors

USITC: United States International Trade Commission ; USTR: United States Trade Representative

27Champion Manufacturing Industries 2025

Legend ImportantImperative

Core strategies to champion manufacturing (3/4)

COST

• Provide time-bound compensation of disabilities on account of finance, power, logistics costs through WTO-compatible production subsidy based on value addition

• Leverage Industrial Corridors network as spines for creating manufacturing centres / clusters

• Create Plug and Play parks (precursor) for manufacturing companies

• Set-up multi-modal logistics network

• Expedite implementation of inland waterways policy

• Expedite creation/expansion of dedicated railway freight corridors

• Expedite national roadways and ports plan

• Provide internationally competitive and easily accessible priority sector funding

•

• Power

• Allow net-metering to enable industries to set up solar plants in remote locations and electricity trading / offset of captive consumption

Implement electronic tolling through RFIDs

MANPOWER

• Create sector skill councils for all 28 Champion industries and have focussed programmes for each of the

industries

• Extend Fixed Term Employment to all manufacturing sectors

• PM Doctoral Fellowship Programme to prioritize champion industries

• Extend 2% CSR proviso for funding research chairs in recognized institutes

28Champion Manufacturing Industries 2025

Legend ImportantImperative

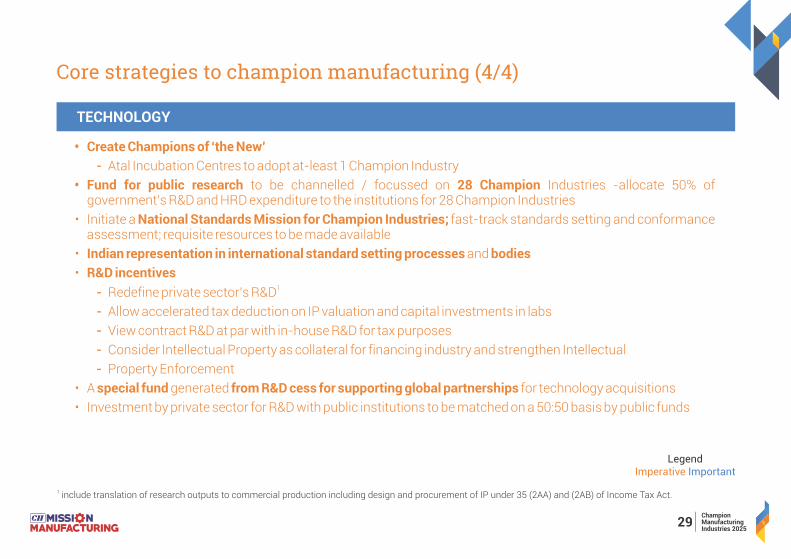

Core strategies to champion manufacturing (4/4)

1 include translation of research outputs to commercial production including design and procurement of IP under 35 (2AA) and (2AB) of Income Tax Act.

TECHNOLOGY

• Create Champions of ‘the New’

- Atal Incubation Centres to adopt at-least 1 Champion Industry

• Fund for public research to be channelled / focussed on 28 Champion Industries -allocate 50% of government’s R&D and HRD expenditure to the institutions for 28 Champion Industries

• Initiate a National Standards Mission for Champion Industries; fast-track standards setting and conformance assessment; requisite resources to be made available

• Indian representation in international standard setting processes and bodies

• R&D incentives

- Redefine private sector’s R&D

- Allow accelerated tax deduction on IP valuation and capital investments in labs

- View contract R&D at par with in-house R&D for tax purposes

- Consider Intellectual Property as collateral for financing industry and strengthen Intellectual

- Property Enforcement

• A special fund generated from R&D cess for supporting global partnerships for technology acquisitions

• Investment by private sector for R&D with public institutions to be matched on a 50:50 basis by public funds

1

29Champion Manufacturing Industries 2025

Legend ImportantImperative

… will trigger significant Industry actions

• Life-cycle cost of ownership oriented design and manufacturing processes addressing sustainability, safety,

running costs, durability, energy and water efficiency, corrosion resistance etc.

• Transition to ‘Green’ and ‘Clean’

• Convergence of attention to national programmes / priorities

- Partnering for development of Industrial Corridors

• Conformance to global standards and quality

• Greater acceptability to external trade opportunities

• Platform innovation and new product development through enhanced focus on research and development

• Greater value addition, particularly locally

• Increased inclination to hire formally

• Increased employability of workforce

30Champion Manufacturing Industries 2025

… translating to a Champion Industry Report Card

Sales growth 15-20%

ROCE > 20%Sales Growth ROCE

3-4%

India’s Share of GlobalManufacturing exports

5-10%

Employment generation

Future -Unleashed

31Champion Manufacturing Industries 2025

1.6%

India’s Share of GlobalManufacturing exports

Sales Growth 8-10%

ROCE < 20%Sales Growth ROCE

0-5%

Employment generation

Current -Business as Usual

*Current Market Size 2015

5

94.2

30

144

107.2

85

22

37.6

97

586

** Business as Usual2025

9.2

173.2

50.7

264.74

166.3

156.3

40.4

69.1

210

1140

Sector

1

Aerospace and Defense

2Auto and Auto Components

4Chemicals5Engineering

7Pharmaceuticals

3

Cement

6

ESDM

8

Steel9

Textiles

Total

IndicativeAll Figures are in USD Billion

**Accelerated Growth2025

21

261

70

444

297

349

90

154

287

1973

… and significant growth in output

* Current market sizes are basis estimates sourced from publically reported data and are not mutually exclusive.** Business as usual is ~7% growth y.o.y; whereas Accelerated Growth has been taken as 17% growth except for Cement, Chemicals, Engineering and Auto and Auto Components which have been assumed to grow at 10%, 13%, 12% and 12% respectively1 Aerospace and Defence –Considered only aircraft components market based on Frost & Sullivan Analysis2 Auto and Auto Component market size based on aggregation of size of industry from SIAM and ACMA3 Cement -Reversed the market size based 70 Billion market in 2025 at 540 tonne capacity; Using this estimated current market size at 290 capacity utilization4 Chemicals Ministry Annual Report 2015-165 Engineering market consists of Consists of Capitals Goods, Electrical Equipment Market, ER&D, Construction Equipment, Telecom Equipment and is sourced from IBEF6 ESDM market size as per report by Department of Electronics and Information Technology7 Pharma market size as reported by Government department –Department of Pharmaceuticals8 Market Size calculated from data point -Steel Industry contributes 2% to GDP (may not factor in imports)9 Basis CII-BCG study "Weaving the Way: Breakout Growth Agenda for the Indian Apparel, Made-ups & Textile industry

32Champion Manufacturing Industries 2025

… and employment generation

* All employment figures are direct employment except for Chemicals sector where both direct and indirect have been considered** Delta is between accelerated growth scenario 2025 and current employment as of 2015-161 Aerospace and Defence –Considered only aircraft components; Since the base is small growth rate has been taken as 10%; Assumed employment of HAL and

vendors. Business as usual (BAU) growth rate of 1%.2 Auto and Auto Component employment has been taken from NSDC skill gap report 2013 and figures for 2016 and BAU have been extrapolated this. 2025 figures

are based on AMP II targets using a assuming a 57% direct and 43% indirect ratio.3 Cement current employment is 1.5 Lakhs; BAU rate is 2% and accelerated rate is 5%4 Chemicals –Industry estimates ~50 lakh as employment base of Chemicals and Ancillary markets, BAU rate is 2% and acc. rate is3.8%.5 Engineering market size is 4 Million as taken from IBEF; BAU rates are 3% and Acc. Growth rate is 5%6 ESDM figures are sourced from NSDC skill gap reports and extrapolated for 2016 and 2025; BAU rates are 8.39% and accrate is 11%.7 Pharma figures are sourced from NSDC skill gap reports and extrapolated for 2016 and 2025; BAU rates are 7.55% and accrate is 10%;8 Steel employment as widely quoted sources is 6 lakhs; BAU rate is 3% and Accelerated growth is 6%9 Textiles –As per the CII-BCG study "Weaving the Way: Breakout Growth Agenda for the Indian Apparel, Made-ups & Textile industry

1

Aerospace and Defense

2Auto and Auto Components

4Chemicals

5Engineering

7Pharmaceuticals

3

Cement

6

ESDM

8

Steel9

Textiles

Total

70,000

12,150,735

150,000

5,000,000

4,000,000

5,513,632

2,313,678

600,000

49,000,000

76,558

16,466,569

179,264

6,000,000

5,219,093

11,383,804

4,453,209

782,864

68,000,000

165,056

37,050,000

232,699

7,000,000

6,205,313

14,104,074

5,455,532

1,013,687

103,000,000

95,056

24,899,265

82,699

2,000,000

2,205,313

8,590,442

3,141,854

413,687

54,000,000

95,428,317

Indicative

Employment* 2015-16

Business as Usual 2025

Accelerated Growth 2025

**DeltaSector

33Champion Manufacturing Industries 2025

…and increase in India’s share of global manufacturing exports

1.6%

India’s Share of GlobalManufacturing exports

USD 200 Billion(2015)

3-4%

India’s Share of GlobalManufacturing exports

USD 500 Billion

Target

India’s merchandise exports could grow 11% y-o-y toachieve target of INR 500 Billion by 2025

34Champion Manufacturing Industries 2025

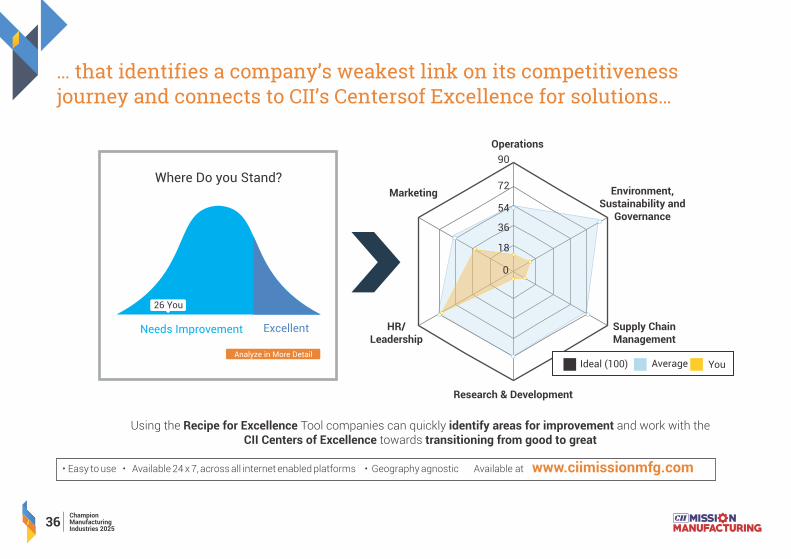

… supported by CII’s Recipe for Excellence (Rx) …

35Champion Manufacturing Industries 2025

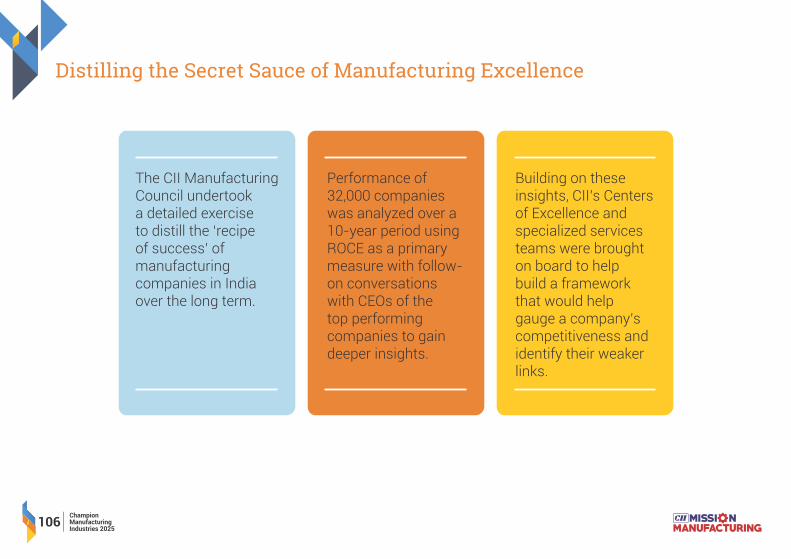

The CII Manufacturing

Council undertook

a detailed exercise

to distill the ‘recipe

of success’ of

manufacturing

companies in India

over the long term.

Performance of 32,000

companies was analyzed

over a 10-year period

using ROCE as a primary

measure with follow-on

conversations with CEOs

and CXOs of the top

performing companies

to gain deeper insights.

Building on these insights,

CII’s Centers of Excellence and

specialized services teams were

brought on board to help build a

framework that would help gauge

a company’s competitiveness

and identify their weaker links.

01 02 03

… that identifies a company’s weakest link on its competitiveness

journey and connects to CII’s Centersof Excellence for solutions…

www.ciimissionmfg.com

36Champion Manufacturing Industries 2025

Using the Recipe for Excellence Tool companies can quickly identify areas for improvement and work with the CII Centers of Excellence towards transitioning from good to great

Operations

Marketing Environment,Sustainability and

Governance

HR/Leadership

Supply ChainManagement

Research & Development

90

72

54

36

18

0

Average Ideal (100) You

Where Do you Stand?

Needs Improvement Excellent

26 You

Analyze in More Detail

• Easy to use • Available 24 x 7, across all internet enabled platforms • Geography agnostic Available at

The Champion Formula

FUTURE - UNLEASHED

IncreasedSales & ROCE

IncreasedExports

IncreasedEmployment

CHAMPION INDUSTRY

www.ciimissionmfg.com

Businessas usual

37Champion Manufacturing Industries 2025

Overall Manufacturing/

Eco-system Level

Industry / Segment

Level

Sector Level

…with a proposed review mechanism

38Champion Manufacturing Industries 2025

Through an Apex-levelGovernment-Industry

Joint Task Force

Inter-ministerialparticipation

Annual update

3-year review& changes

Mode Participation Frequency

1 2 3

Summary –Champions of Manufacturing Study

• Opportune time for India to rally around the 28 industries that have the potential to be #1 or #2 globally and create 100M jobs in the next decade

• Each sector has debated and identified specific recommendations that would maximize the probability of success:

- Across the manufacturing sector

- Across the champion sectors

- Across the specific champion industries

• The recommendations involve a close partnership between Government and Industry

• Need to embark on an urgent time bound implementation journey with regular reviews of progress on the key metrics of success

- Industry sales growth

- Industry global market share growth

- Industry profitability in terms of return on capital invested

-# of jobs created

39Champion Manufacturing Industries 2025

Annexure 1

Sector and Industry Level Recommendations

Overall Manufacturing/

Eco-system Level

Industry / Segment

Level

Sector Level

Index of Recommendations

Aerospace & Defence

Auto and Auto Components

Cement

Aircraft Components and Sub-systems

Auto-Electricals & Electronics

Automotive Batteries

Construction Machinery

Heavy Commercial Vehicles

Passenger Cars

Two and Three Wheelers

Cement

Agro Intermediates

Agro Chemicals

Basic Polymers and Elastomers

Construction Chemicals

Chemicals

Other Performance Chemicals

SECTOR INDUSTRY

Engineering

ESDM

Pharma

Steel

Textiles

SECTOR INDUSTRY

Pumps and Valves

Machine Tools

Pressure Vessels

Solar PV

Conventional Lighting and LED Lighting

Mobile Phones

Printed Circuit Boards and Sub-assemblies

Bulk Drugs

Generic Pharmaceuticals

Pharma APIs

Flats

Forgings and Castings

Longs

Made-ups

Apparel

41Champion Manufacturing Industries 2025

Aerospace & Defence

Aerospace and Defence –Sectoral Snapshot and Potential

200,000 employment generated by

sector

60%

Requirement met by imports

USD 38.322Billion Defence

Budget

rd3 Largest defence force in the world

2.25%

defence budget in

GDP

43Champion Manufacturing Industries 2025

Aircraft Components and sub-systems - SWOT

44Champion Manufacturing Industries 2025

• Significant budget allocation for defense -17.2 % of the total central government expenditure for the year 2016-17; 60%imports).

• Increasing air passenger traffic

• Potential to become a global MRO hub

• Strategic barriers for critical technologies

• Strong competition from other Asian markets

NADCAP - National Aerospace and Defense Contractors Accreditation Program ; FAA – Federal Aviation Administration, USA

• Large low cost engineering talent pool

• Cost competitive technology development capability

• Supportive policy framework

• IT competitiveness

• Vibrant and innovative MSMEs

• Low level of investment in technology, innovation and upgradation

• Lack of supporting infrastructure and robust supply chain including availability of raw materials.

• Complex policy environment

• Lack of experienced technical manpower

• Lack of process and product certification infrastructure, applicable for global standards (FAA, NADCAP) in the country

STRENGTHS WEAKNESSES

OPPORTUNITIES THREATS

Aircraft Components and sub-systems (1 of 3)

Policy Regime

Ÿ Create a national data base of process, product and test certification requirements of global OEMs and create a national certifications body, affiliated to NADCAP

Ÿ Offset Policy to be linked to a specific segment of defence and civil aviation as opposed to sector-agnostic counter-trade as at present.

PILLAR RECOMMENDATION

Ÿ India to be developed as a global MRO hub

Ÿ Development and production phases to be combined for procurement purpose; Alternately, development partner to have first right of refusal for participating in production phase

Ÿ Mandate indigenisation of spares by IAF / HAL to curb imports and encourage domestic industry, e.g. Keiretsu programme of Japan - development of ancillaries catalysed by Technology Development Fund set up explicitly for purpose for critical items

Ÿ Allow for long term contracting of spares and components to enable industry to plan and invest accordingly knowing what the 5 year outlook entails.

– Develop National Aerospace Industrial Parks alongside industrial corridors (near Bangalore, Hyderabad, Nagpur, Pune) with shared infrastructure, e.g. airfield, ATC, hangars and manufacturing units, MROs, training and educational institutes, warehouses, design and testing centres etc.

MRO: Maintenance, Repair and Operations

45Champion Manufacturing Industries 2025

Aircraft Components and sub-systems (2 of 3)

46Champion Manufacturing Industries 2025

Cost

Ÿ Create local manufacturing capacity for strategic raw materials through a capacity development programme (in PPP / match making / etc. mode)

Ÿ

Award of ContractMandate and enforce strict timelines from Acceptance of Necessity (AON) to

PILLAR RECOMMENDATION

Ÿ Create an Advanced Materials and Applications Programme (AMAP) to nurture and foster manufacturing capabilities of aerospace grade materials such as aluminium alloys, titanium alloys, composites.

– Creating awareness amongst potential users of benefit (e.g. life cycle cost) and applications

– Providing knowledge on best practices and advisory services on materials, manufacturing practices and standards.

– Development of requisite skilled workforce

Aircraft Components and sub-systems (3 of 3)

Technology

Ÿ Develop R&D infrastructure of global standards (design, development infrastructure including equipment and testing facilities) in Govt Labs /Institutes to be accessible to Industry (especially MSMEs), by way of pay-per-use model or strategic partnerships ; through PPP, Government Owned Contractor Operated (GOCO) or any other such model with technical collaboration with global agencies

Ÿ Establish an Aerospace Technology and Skill Development Centre (ATSDC) in partnership with global OEMs as part of their contracts with MoD

PILLAR RECOMMENDATION

Ÿ Channelize Technology Acquisition and Development Fund (TADF) for providing technology upgradation support / funding support for MSMEs

Ÿ Establish focussed ITIs in Aerospace Industrial parks in PPP mode, with curriculum developed with Industry

Manpower

47Champion Manufacturing Industries 2025

Auto and Auto Components

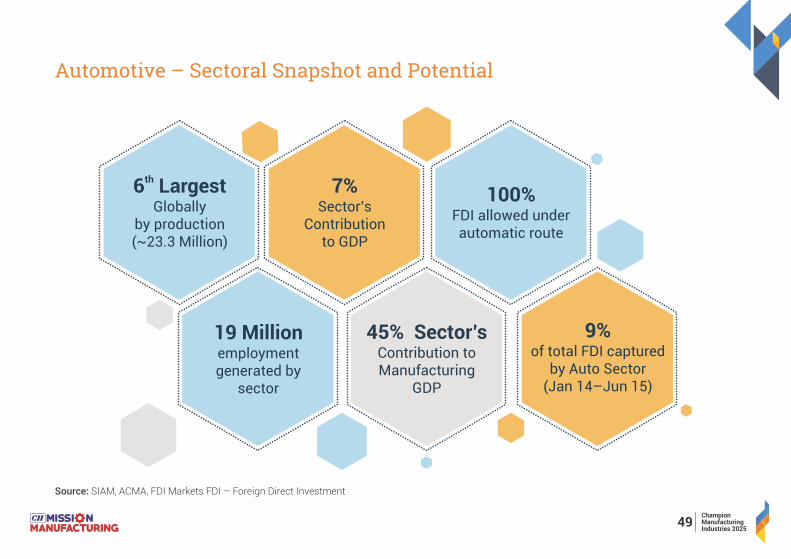

Source: SIAM, ACMA, FDI Markets FDI – Foreign Direct Investment

Automotive – Sectoral Snapshot and Potential

th6 Largest Globally

by production (~23.3 Million)

45% Sector’s Contribution to Manufacturing

GDP

9% of total FDI captured

by Auto Sector (Jan 14–Jun 15)

19 Million employment generated by

sector

7% Sector’s

Contribution to GDP

100% FDI allowed under automatic route

49Champion Manufacturing Industries 2025

Automotive - SWOT

BNVSAP - Bharat New Vehicle Safety Assessment Program ; CAFÉ - Corporate Average Fuel Economy ; BS – Bharat Stage NEMMP - National Electric Mobility Mission Plan ; FAME – Faster Adoption and Manufacturing of (Hybrid &) Electric Vehicles India

• India recognized as a global manufacturing hub by global OEMs

• Extensive presence of entire value chain and strong business eco-system

• Global leader in small vehicle segment

• Import dependency for advanced automotive technologies

• Technology follower v/s leader

• Implementation of NEMMP / FAME behind pace and magnitude

• Inconsistencies in quality

• Implementation of global norms expected to bridge the gap between India and Americas /Europe / Japan

• BNVSAP

• CAFÉ / AFCS

• BS VI Norms

• AMP II envisions 3-4x growth in the auto and auto components

• Significant focus on roads and highway development

• Policy uncertainty, multiplicity of authorities

• Limited local hi technology innovation capabilities hampering component localization potential and growth

• May have missed the bus on electronics components; limited manufacturing in India

• Growing non-databased environmental concerns

• Proliferation of counterfeit goods

STRENGTHS

OPPORTUNITIES

WEAKNESSES

THREATS

50Champion Manufacturing Industries 2025

Automotive – Overall (1 of 2)

Policy Regime

Ÿ Single point authority for all regulations for all road transport with representatives from all relevant ministries / departments / institutions such as DHI, MoPNG, NATRIP etc.

Ÿ Announce roadmap for FAME scheme for the remaining 8 years to enable industry to plan investments and develop indigenous design and component manufacturing base; FAME needs to be applicable throughout the country.

PILLAR RECOMMENDATION

Ÿ Regulations / restrictions on vehicles should be performance-cum-emissions based and not specific technology or fuel-based

Ÿ Waive taxes such as registration taxes on electric vehicles to drive adoption

Ÿ Stronger IP enforcement to ensure control of counterfeit goods

Ÿ Mandate procedure for Type Approval and Establishing Conformity of Production for Safety Critical Components

FAME – Faster Adoption and Manufacturing of (Hybrid &) Electric Vehicles India; NATRIP - National Automotive Testing and R&D Infrastructure Project

51Champion Manufacturing Industries 2025

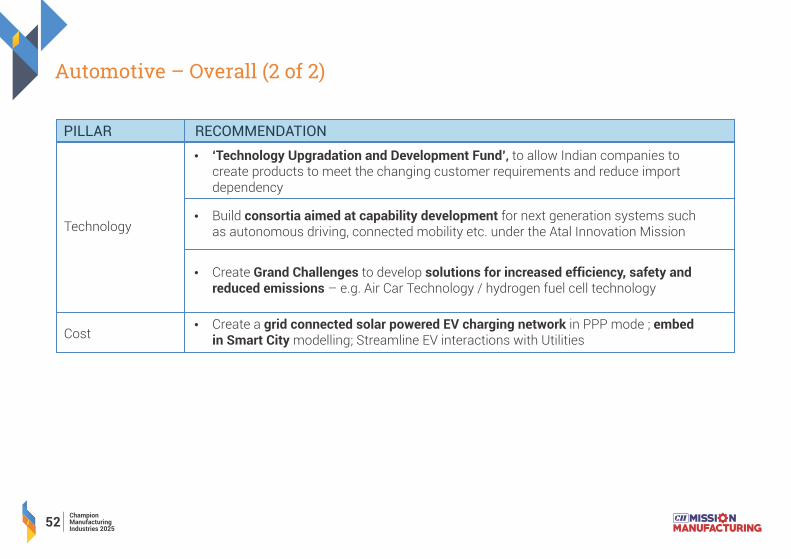

Automotive – Overall (2 of 2)

Technology

Ÿ ‘Technology Upgradation and Development Fund’, to allow Indian companies to create products to meet the changing customer requirements and reduce import dependency

Ÿ Create Grand Challenges to develop solutions for increased efficiency, safety and reduced emissions – e.g. Air Car Technology / hydrogen fuel cell technology

PILLAR RECOMMENDATION

Ÿ Build consortia aimed at capability development for next generation systems such as autonomous driving, connected mobility etc. under the Atal Innovation Mission

Cost

52Champion Manufacturing Industries 2025

Ÿ Create a grid connected solar powered EV charging network in PPP mode ; embed in Smart City modelling; Streamline EV interactions with Utilities

Automotive – Automotive Batteries

Policy RegimeŸ Announce a clear policy framework for manufacturing and recycling of batteries of all

types including lead-acid and Lithium-ion

PILLAR RECOMMENDATION

Ÿ Create research programmes in battery and storage technologies and focussed research on the following aspects

Ÿ Battery technology modellingŸ Battery capacity estimationŸ Energy management systems for electric carsŸ Battery charging

Ÿ Commercialization of new technologies to be supported via academia-industry partnerships.

Technology

53Champion Manufacturing Industries 2025

Automotive – Auto Electricals and Electronics (1 of 2)

Policy Regime

Ÿ Create a Phased Manufacturing Programme for the complete value chain of Auto Electricals and Electronics ensuring component eco-system is developed in tandem

Ÿ Ensure Domestic Tariff Area sales of Information Technology Agreement-1 (ITA-1)/Zero duty electronics products manufactured in the country are given the status of physical export as per para 2.1(b) of the National Policy on Electronics 2012; extending this status to all suppliers to domestic manufacturers of zero duty ESDM products would also eliminate the inverted duty structure at Tier-2 industries

PILLAR RECOMMENDATION

Ÿ Set up automotive EMC (Electronics Manufacturing Cluster) near auto hubs and incentivize manufacturing of sensors, LEDs, PCBs and LCDs etc.

Ÿ Incentivise vehicles with a certain minimum auto electronic content designed and manufactured in India

Ÿ Make budget provision for extending financial incentives as provided for under MSIPS to enable sufficient scale of projects to be supported

Ÿ Today, even for consolidation within the country, RBI rules prevent Indian companies to borrow money for acquisitions, foreign companies can borrow for acquisition putting Indian companies at a disadvantage. Allow companies to borrow for acquisitions

MSIPS - Modified Special Incentives Package Scheme

54Champion Manufacturing Industries 2025

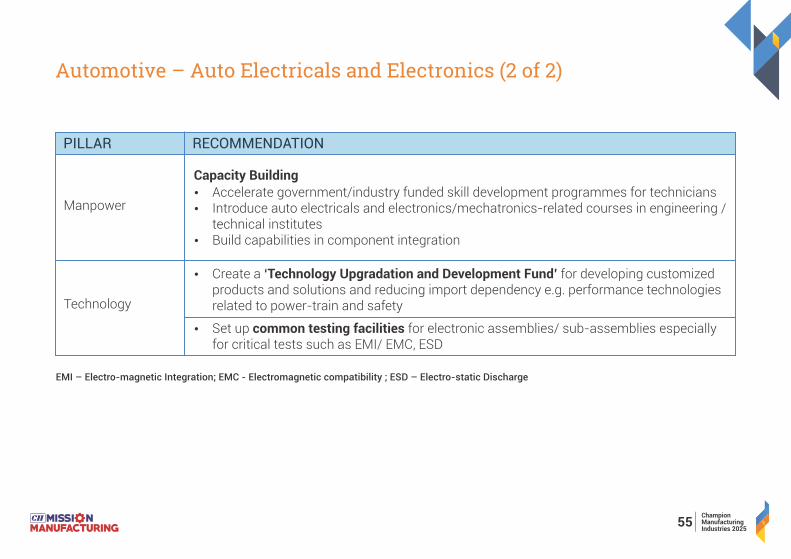

Automotive – Auto Electricals and Electronics (2 of 2)

Manpower

Capacity Building

Ÿ Accelerate government/industry funded skill development programmes for techniciansŸ Introduce auto electricals and electronics/mechatronics-related courses in engineering /

technical institutesŸ Build capabilities in component integration

PILLAR RECOMMENDATION

Ÿ Create a ‘Technology Upgradation and Development Fund’ for developing customized products and solutions and reducing import dependency e.g. performance technologies related to power-train and safetyTechnology

Ÿ Set up common testing facilities for electronic assemblies/ sub-assemblies especially for critical tests such as EMI/ EMC, ESD

EMI – Electro-magnetic Integration; EMC - Electromagnetic compatibility ; ESD – Electro-static Discharge

55Champion Manufacturing Industries 2025

Automotive – Construction Machinery

Cost

Ÿ Major Government infrastructure projects / initiatives such as Smart Cities, Housing for all etc. should have time bound implementation targets and accountability with name(s) of contractor and project start / end date specified

Ÿ Expedite passage and implementation of the National Mineral Exploration Policy

PILLAR RECOMMENDATION

Ÿ Priority sector funding for providing easy and globally competitive financing

Ÿ Create / allow for equipment banks which integrate physical equipment, finance, trained operators and spare capacities

Ÿ Skill development program to provide training, certifications, grants and scholarship to enable consistent pipeline supply of skilled resources.

Ÿ Uniform safety requirements across the country by using trained mechanics and operators

Policy Regime

Manpower

TechnologyŸ Create Technology Co-Development facilities in Technical Institutes for emerging

technologies, e.g. autonomous construction equipment

56Champion Manufacturing Industries 2025

Automotive – Passenger Vehicles, 2/3 Wheelers, HCVs (1 of 2)

* Argentina, Bangladesh, Colombia, Kenya, Mexico, Nigeria

Policy Regime

PILLAR RECOMMENDATION

57Champion Manufacturing Industries 2025

Ÿ Create a Green Vehicle Exchange incentive for Fleet upgradation / End of Life vehicles whilst upgrading to hybrid or electric vehicles; bias for higher local content

Ÿ Incentivize OEMs to introduce hybrid or electric vehicles across all segments (e.g. Most options in PVs exist in Luxury segments only)

Ÿ Introduce Safety Standards / Star rating for vehicles - Reduce tax incidence on OEMs with higher star rating (currently between 57 - 75%) to offset cost to consumer

Ÿ 6 X 6 Export Market Push (6 markets*, 6 year plan) – evolve an integrated export-oriented approach comprising

Ÿ participation in key trade shows,

Ÿ setting up of India Auto Showcase as Government –supported permanent display-cum-tech centre for demo, training and on-site tech development

Ÿ Commercial missions to be integrated with KPIs linked to exports growth

Ÿ Explore FTAs with Argentina, Bangladesh, Colombia, Kenya, Mexico, Nigeria

Ÿ MAT Credit should be extended till it is completely utilized. (MAT Credit lapses after 10 years)

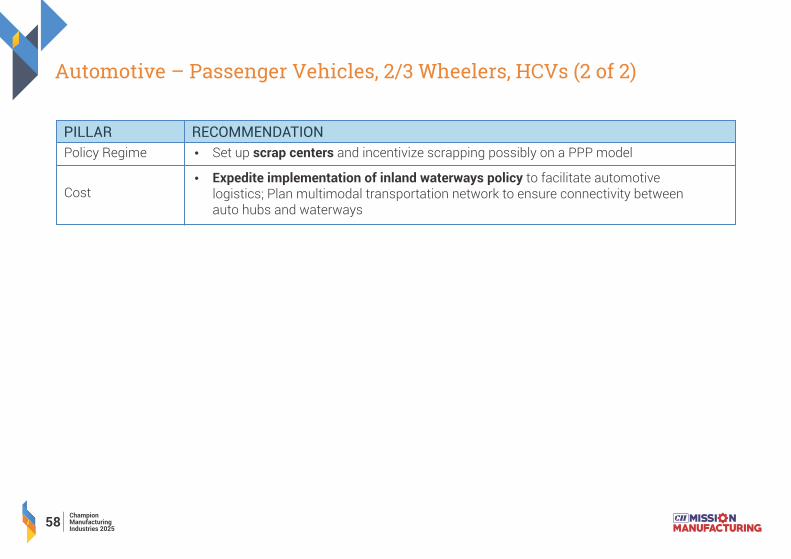

Automotive – Passenger Vehicles, 2/3 Wheelers, HCVs (2 of 2)

Cost

PILLAR RECOMMENDATION

Policy Regime

58Champion Manufacturing Industries 2025

Ÿ Set up scrap centers and incentivize scrapping possibly on a PPP model

Ÿ Expedite implementation of inland waterways policy to facilitate automotive logistics; Plan multimodal transportation network to ensure connectivity between auto hubs and waterways

Cement

Cement – Sectoral Snapshot and Potential

Source – India Brand Equity Foundation; International Journal of Emerging Research in Management &Technology

nd 2 Largest producer in the world

1.5%

Contribution to India’s GDP

Direct Employment to

150,000

& Indirect Employment to

500,000

people

7%Share in global

production

6.7%CAGR of

Production over FY07-15

USD 3 bnFDI inflow to

sector April 2000 – Dec 2015

60Champion Manufacturing Industries 2025

Cement - SWOT

• Rapid technological upgradation and vibrant growth during the last two decades

• Significant contribution towards clean environment (consumes 75% of the Fly Ash recycled in the country, and also several other hazardous wastes like blast furnace slag, used tyres, etc.)

• Easy availability of low cost skilled labor

• Fragmented regional players with weak economies of scale

• Relatively higher cost of capital in India.

• Poor raw material linkages (coal, limestone, etc.)and supporting infrastructure

• Demand-supply gap; overcapacity

• Continuous process industry vulnerable to unreliable grid supply

• Upcoming infrastructure projects by GoI (Housing For All scheme by 2022, Smart cities, National and State Highways, etc.)

• Liberalization of FDI caps in user sectors is expected to surge demand for cement in the coming years

• Entry of multinational companies, leading to new technologies, improved efficiency and access to global value chains

• Demand volatility

• Increasing pressures w.r.t. environmental issues and policies requiring speedy compliance with inadequate transition time

• Increasing imports from neighboring countries

OPPORTUNITIES THREATS

WEAKNESSESSTRENGTHS

61Champion Manufacturing Industries 2025

Cement – Recommendations ( 1 of 2)

Policy Regime

Ÿ Encourage use of AFR as co-processing in cement Kilns for sustainable solution for waste management

Ÿ Introduce “Polluter to Pay” concept.Ÿ Single Window permits should be given

PILLAR RECOMMENDATION

Ÿ Encourage mineral resource optimization and reduce CO2 emissions by incentivizing use of green cements - PPC (fly ash), PSC (slag), Composite Cement and use of recycled aggregates

Ÿ Monitoring Protocol - Day average to be consideredŸ Time for implementation – Relaxation till March 2019 (Current timeline is March 31,

2017) as India has no experience in required NOX emission control technologiesŸ e.g. risk associated with Ammonia transportation and handling

Ÿ Government procurementŸ Missions / programmes such as Housing for all, Smart Cities, Industrial Corridors,

Gram Sadak Yojana (PMGSY) etc. to be undertaken on basis of Life Cycle Cost of Ownership (TCO1)

Ÿ Incentivize manufacturers to develop products that have pre-defined targets for reduction in emissions

Ÿ Create WTO compatible norms to check dumping of cement into India

Alternative Fuels and Materials:

Government /Infra Projects (Roads, Buildings etc.):

Environment: Emission Norms: GSR No: 496 (E) dt.09.05.16 & GSR No: 497 (E) 10.05.16

62Champion Manufacturing Industries 2025

Cement – Recommendations (2 of 2)

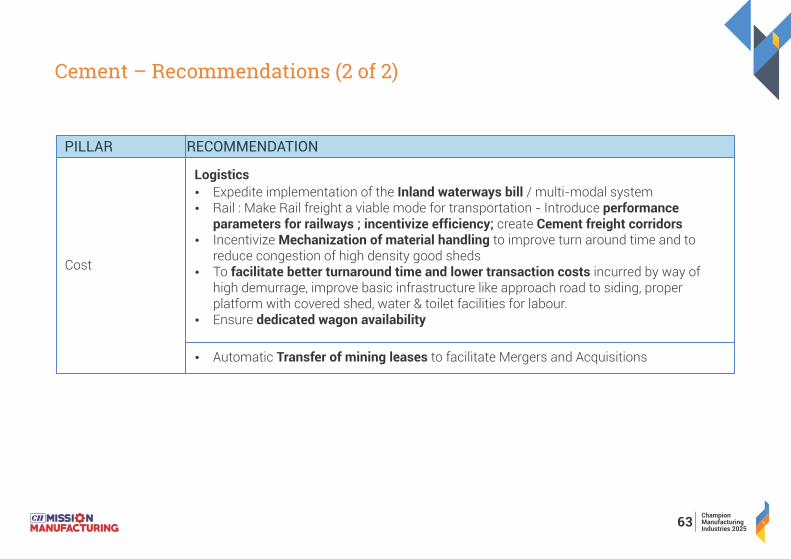

Cost

Logistics

PILLAR RECOMMENDATION

Ÿ Expedite implementation of the Inland waterways bill / multi-modal systemŸ Rail : Make Rail freight a viable mode for transportation - Introduce performance

parameters for railways ; incentivize efficiency; create Cement freight corridorsŸ Incentivize Mechanization of material handling to improve turn around time and to

reduce congestion of high density good shedsŸ To facilitate better turnaround time and lower transaction costs incurred by way of

high demurrage, improve basic infrastructure like approach road to siding, proper platform with covered shed, water & toilet facilities for labour.

Ÿ Ensure dedicated wagon availability

Ÿ Automatic Transfer of mining leases to facilitate Mergers and Acquisitions

63Champion Manufacturing Industries 2025

Chemicals

65Champion Manufacturing Industries 2025

Chemicals – Sectoral Snapshot and Potential

2% Sector’s

Contribution to GDP

100% FDI allowed

under automatic route

th6 Largest Globally

by production

15% Sector’s

Contribution to Manufacturing

GDP

6.57% of total FDI captured by the sector during

April-Dec 2015

5+ Million employment generated by

sector

66Champion Manufacturing Industries 2025

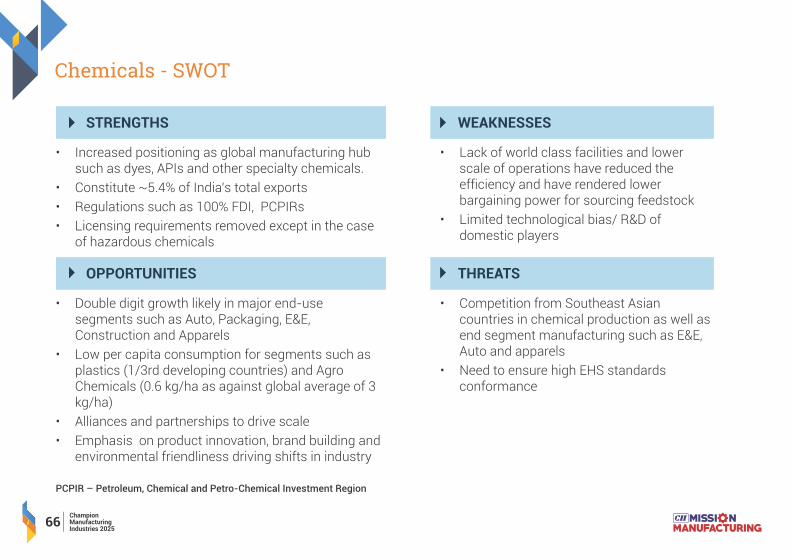

Chemicals - SWOT

• Increased positioning as global manufacturing hub such as dyes, APIs and other specialty chemicals.

• Constitute ~5.4% of India’s total exports

• Regulations such as 100% FDI, PCPIRs

• Licensing requirements removed except in the case of hazardous chemicals

• Lack of world class facilities and lower scale of operations have reduced the efficiency and have rendered lower bargaining power for sourcing feedstock

• Limited technological bias/ R&D of domestic players

• Double digit growth likely in major end-use segments such as Auto, Packaging, E&E, Construction and Apparels

• Low per capita consumption for segments such as plastics (1/3rd developing countries) and Agro Chemicals (0.6 kg/ha as against global average of 3 kg/ha)

• Alliances and partnerships to drive scale

• Emphasis on product innovation, brand building and environmental friendliness driving shifts in industry

• Competition from Southeast Asian countries in chemical production as well as end segment manufacturing such as E&E, Auto and apparels

• Need to ensure high EHS standards conformance

PCPIR – Petroleum, Chemical and Petro-Chemical Investment Region

STRENGTHS WEAKNESSES

THREATSOPPORTUNITIES

Chemicals – Overall (1 of 2)

Policy Regime

Ÿ Clear 3-5 year roadmap for regulatory regime especially for Environment, Health and Safety norms

PILLAR RECOMMENDATION

Ÿ Develop a national chemicals inventory to create a comprehensive database on the capabilities, properties, classification, regulatory status and safety aspects of chemicals being produced in India as a single point of reference

Ÿ Create single window mechanism for Chemicals Industry for dealing with all Chemical related issues / regulations with time bound and automated responses

Ÿ Lay down standards in conformance to global standards and ensure mutual recognition

Ÿ Commission a National Feedstock Research Mission Programme for identifying alternate sources of feedstock like coal, biomass etc.

Ÿ Promote co-development of end use applications and tax incentives for application R&D investments and increase industry linkages with academic institutions ; create National Chemicals Laboratories co-located in Chemical clusters

Technology

67Champion Manufacturing Industries 2025

Chemicals – Overall (2 of 2)

Cost / Infra

Ÿ Raw Material SecurityŸ To maximize potential of PCPIR, MoPNG to ensure that requirements of potential

downstream units committing to long term offtake are ascertained before project commissioning

Ÿ GoI to enter into bilateral strategic relationships for securing supply of feedstock with resource rich countries (Iran, Mozambique, Myanmar) e.g. setting up of reverse SEZs.

Ÿ Ethanol mission – Incentivize / Credits for green Ethanol production

PILLAR RECOMMENDATION

Ÿ Need for uninterrupted power supply as these are Continuous Process Industries (CPI); Reinstatement of power trading and facilities of net energy metering (NEM) services

Ÿ Fast-track implementation of the National Pipeline Grid

Ÿ Accelerated depreciation for renewable energy investment

68Champion Manufacturing Industries 2025

Chemicals – Construction Chemicals

Policy Regime

Ÿ Public infrastructure projects and Building Code should be based on TCO1 as opposed to L1; TCO 1 (performance parameters) to be inclusive of sustainability, safety, durability, energy efficiency and water efficiency, corrosion resistance etc.

PILLAR RECOMMENDATION

Ÿ Building scale through - Housing for all, Smart Cities, Gram Sadak Yojana, National Highway Programme, Industrial Corridors etc. Ensure GoI strategic initiatives such as Smart Cities operate based on world class standards

Ÿ Incentivise green buildings and other environmentally superior standards by offering rebates/incentives to encourage adoption.

Ÿ IRDA to mandate lower premium based on performance parameters - to be inclusive of sustainability, energy efficiency and water efficiency, corrosion resistance etc.

Ÿ Actively evaluate and mandate phase out of Alkylphenol Ethoxylates(APEO) based technologies and other polluting/ harmful chemicals banned in other emerging geographies to avoid adverse environmental impact

Manpower Ÿ Appropriate training of personnel to reduce TCO - Total Cost of Ownership

69Champion Manufacturing Industries 2025

Chemicals – Agro Chemicals and Intermediates

Policy Regime

Technology

Manpower

Ÿ Expedite implementation of a science-based regulatory framework for safe nutritional security in the country.

PILLAR RECOMMENDATION

Ÿ 5 X 5 ExportMarket Push (5 markets*, 5 year plan) –evolve an integrated export-oriented approach comprising

Ÿ Createa bilateral technical assistance programme for enhancing agricultural output

Ÿ Simplified registration norms for pesticides exports and increased scope of regulations to include all types of pesticides (including bio-pesticides)

Ÿ Create a digitized National Soil Map linked with the Soil Health Card Scheme

Ÿ Time-bound and e-enabled regulatory clearances for registration of agro-chemicals

Ÿ Stronger IP enforcement to curb counterfeiting

Ÿ Create vocational training programmes for Agronomy related disciplines

* Africa, South / SE Asia

70Champion Manufacturing Industries 2025

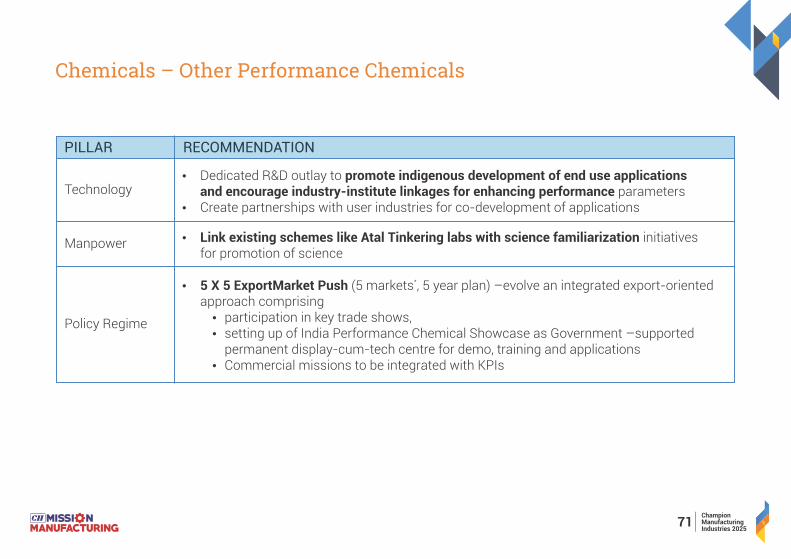

Chemicals – Other Performance Chemicals

TechnologyŸ Dedicated R&D outlay to promote indigenous development of end use applications

and encourage industry-institute linkages for enhancing performance parametersŸ Create partnerships with user industries for co-development of applications

PILLAR RECOMMENDATION

Ÿ Link existing schemes like Atal Tinkering labs with science familiarization initiatives for promotion of science

*Ÿ 5 X 5 ExportMarket Push (5 markets , 5 year plan) –evolve an integrated export-oriented

approach comprisingŸ participation in key trade shows,Ÿ setting up of India Performance Chemical Showcase as Government –supported

permanent display-cum-tech centre for demo, training and applicationsŸ Commercial missions to be integrated with KPIs

Policy Regime

Manpower

71Champion Manufacturing Industries 2025

Chemicals – Basic Elastomers and Polymers

Policy Regime

Ÿ Dedicated plastic processing parks as export hubs with shared infrastructure alongside PCPIRs

PILLAR RECOMMENDATION

Ÿ Green credit system linked to a tax credit for fully recyclable laminates, conforming to BIS standards

Ÿ Enforcement of existing mandates / legislations like “Edible Oil Packaging Order”

Ÿ Building Code should be based on TCO1 as opposed to L1; TCO 1(performance parameters) to be inclusive of sustainability, safety, durability, energy efficiency and water efficiency, corrosion resistance etc.

Ÿ Encourage resource-saving measures like energy-efficient building codes using plastic profiles in buildings, etc.

Ÿ Encourage plasticulture* applications for water / fertilizer-saving in agriculture, etc.

* Plasticulture refers to the practice of using plastic materials in agricultural applications

72Champion Manufacturing Industries 2025

Engineering

Engineering – Sectoral Snapshot and Potential

* w.r.t Capital Goods Sector ** Source: DIPP

*2 % Sector’s Contribution

to GDP

100% FDI

allowed under automatic

route

*12 % Sector’s

Contribution to Manufacturing

GDP

9 Million

employment generated by

sector

**6 %

of total FDI captured by the sector during April -

Dec 2015

74Champion Manufacturing Industries 2025

Engineering - SWOT

• Cost competitive technology development capability

• Pool of engineering talent

• Supportive / Conducive policy framework

• Component and raw material sourcing ecosystem in existence

• Vibrant and innovative MSMEs

STRENGTHS

• Export potential with Middle East, Africa, Latin America, South / SE Asia and CIS/Russia

• Govt thrust on infrastructure development, e.g. Industrial Corridors, Smart Cities, Housing for All, Make in India, PMGSY, NHDP etc.

• Demand shifting towards efficiency-enhancing parameters, automation

OPPORTUNITIES

• Low cost imports and lack of regulation to govern sub-standard imports

• Increasing dependence on US and Europe for exports and technology(without commitments on technology transfer)

THREATS

• Low productivity and quality consistency

• Lack of focused skill development

• Legacy / obsolete labor laws

• Lack of standards

• Limited investment by domestic manufacturers in innovation and R&D

WEAKNESSES

75Champion Manufacturing Industries 2025

Engineering – Overall

Policy Regime

Ÿ 5 X 5 ExportMarket Push (5 markets*, 5 year plan) –evolve an integrated export-oriented approach comprising

Ÿ participation in key trade shows,Ÿ setting up of India Engineering Showcase as Government –supported permanent

display-cum-tech centre for demo, training and on-site tech developmentŸ Commercial missions to be integrated with KPIsŸ Portal

PILLAR RECOMMENDATION

Ÿ Purchase equipment through indirect barter and/or Indian Rupee form while negotiating trade agreements with countries where mutually acceptable (e.g Iran, Myanmar) or with whom trade balance is negative.

Ÿ Provide financing at LIBOR rate to facilitate overseas acquisitions of distressed assets, thus enabling market access, leveraging of existing brand and access to technology

Ÿ Preference to firms manufacturing in India for projects funded by loans originating from India

*Africa/East Africa; South East Asia; CIS/Russia; Latin America; Middle East

76Champion Manufacturing Industries 2025

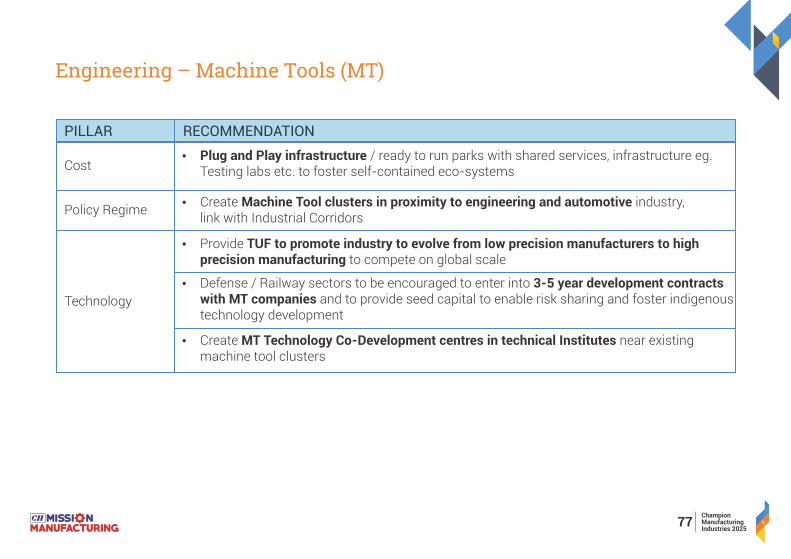

Engineering – Machine Tools (MT)

Cost

Policy Regime

Technology

Ÿ Plug and Play infrastructure / ready to run parks with shared services, infrastructure eg. Testing labs etc. to foster self-contained eco-systems

PILLAR RECOMMENDATION

Ÿ Create Machine Tool clusters in proximity to engineering and automotive industry, link with Industrial Corridors

Ÿ Provide TUF to promote industry to evolve from low precision manufacturers to high precision manufacturing to compete on global scale

Ÿ Defense / Railway sectors to be encouraged to enter into 3-5 year development contracts with MT companies and to provide seed capital to enable risk sharing and foster indigenous technology development

Ÿ Create MT Technology Co-Development centres in technical Institutes near existing machine tool clusters

77Champion Manufacturing Industries 2025

Engineering – Pumps and Valves

Policy Regime

Technology

Ÿ Introduce Energy Efficiency cum Emissions Star Rating (E3SR) for pumps

PILLAR RECOMMENDATION

Ÿ Aggregate procurement and distribution through– EESL type mechanism for proliferation of solar pumps

Ÿ Government to introduce TCO1 for procurement vs L1 at present especially for Smart Cities initiative

Ÿ Mutual recognition of international standards including for government contracts also

Ÿ Develop linkages with key user industries and promote co-development e.g. with oil and gas industry (Spec design that define product design, come from EPC players, need to be aligned with them for better access and products)

Ÿ Create Technology Co-Development facilities in Technical Institutes for R&D in Smart Control Systems

78Champion Manufacturing Industries 2025

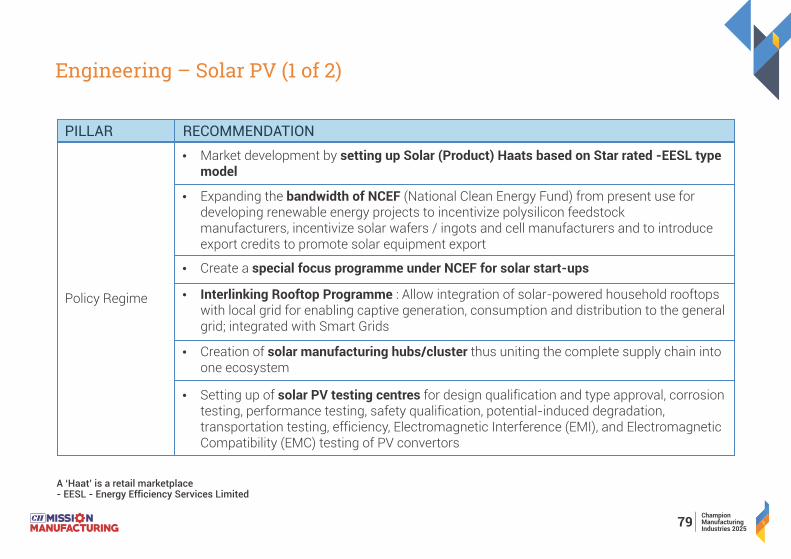

Engineering – Solar PV (1 of 2)

Policy Regime

Ÿ

modelMarket development by setting up Solar (Product) Haats based on Star rated -EESL type

PILLAR RECOMMENDATION

Ÿ Expanding the bandwidth of NCEF (National Clean Energy Fund) from present use for developing renewable energy projects to incentivize polysilicon feedstock manufacturers, incentivize solar wafers / ingots and cell manufacturers and to introduce export credits to promote solar equipment export

Ÿ Create a special focus programme under NCEF for solar start-ups

Ÿ Interlinking Rooftop Programme : Allow integration of solar-powered household rooftops with local grid for enabling captive generation, consumption and distribution to the general grid; integrated with Smart Grids

Ÿ Creation of solar manufacturing hubs/cluster thus uniting the complete supply chain into one ecosystem

Ÿ Setting up of solar PV testing centres for design qualification and type approval, corrosion testing, performance testing, safety qualification, potential-induced degradation, transportation testing, efficiency, Electromagnetic Interference (EMI), and Electromagnetic Compatibility (EMC) testing of PV convertors

A ‘Haat’ is a retail marketplace- EESL - Energy Efficiency Services Limited

79Champion Manufacturing Industries 2025

Engineering – Solar PV (2 of 2)

Policy Regime

Technology

Ÿ Propagate wasteland usage for setting up of solar power generating and storage systems

PILLAR RECOMMENDATION

Ÿ Establish sets of standards for different types of modules – rooftop and grid, covering all technologies, at par with international levels:

Ÿ Validate with kFW, IREDA, Fraunhofer who have experience in ratifying modulesŸ Consolidate standards from Germany, US, Japan, India, etc.Ÿ Standards for cells and modules for India