CH17

70

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition Solutions Manual 17-1 Chapter 17 Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is strictly prohibited. CHAPTER 17 COMPLEX FINANCIAL INSTRUMENTS ASSIGNMENT CLASSIFICATION TABLE Topics Brief Exercises Exercises Problems Writing Assignments 1. Convertible debt and preferred shares. 1, 2 1, 2, 3, 4, 5, 6, 7, 8 2, 4 2. Warrants and debt. 3, 4 7, 8, 9 1, 3 1 3. Stock options. 5 10, 11, 12 1, 5 2 4. Derivative instruments for speculation 10, 11, 12, 13 15 6, 7, 8, 9, 5. Classification: debt vs. equity 6, 7, 8, 9 *6. Derivative instruments for hedging. 14 16, 17, 18 10, 11, 12 *7. Stock appreciation rights. 15 13, 14 *This material is dealt with in an Appendix to the chapter.

Transcript of CH17

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-1 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

CHAPTER 17

COMPLEX FINANCIAL INSTRUMENTS

ASSIGNMENT CLASSIFICATION TABLE

TopicsBrief

Exercises Exercises ProblemsWriting

Assignments

1. Convertible debt andpreferred shares.

1, 2 1, 2, 3, 4,5, 6, 7, 8

2, 4

2. Warrants and debt. 3, 4 7, 8, 9 1, 3 1

3. Stock options. 5 10, 11,12

1, 5 2

4. Derivative instrumentsfor speculation

10, 11,12, 13

15 6, 7, 8,9,

5. Classification: debt vs.equity

6, 7, 8, 9

*6. Derivative instrumentsfor hedging.

14 16, 17,18

10, 11,12

*7. Stock appreciationrights.

15 13, 14

*This material is dealt with in an Appendix to the chapter.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-2 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

ASSIGNMENT CHARACTERISTICS TABLE

Item DescriptionLevel ofDifficulty

Time(minutes)

E17-1 Issuance and conversion of bonds. Simple 15-20E17-2 Conversion of bonds. Moderate 20-25E17-3 Conversion of bonds. Simple 5-10E17-4 Conversion of bonds. Moderate 15-20E17-5 Conversion of bonds. Simple 10-20E17-6 Conversion of bonds. Moderate 25-35E17-7 Issuance of bonds with warrants. Simple 10-15E17-8 Issuance of bonds with detachable warrants. Simple 10-15E17-9 Issuance of bonds with warrants. Simple 10-15E17-10 Issuance and exercise of stock options. Moderate 15-25E17-11 Issuance, exercise, and termination of stock

options.Moderate 15-25

E17-12 Issuance, exercise, and termination of stockoptions.

Moderate 15-25

*E17-13 Stock appreciation rights. Moderate 15-25*E17-14 Stock appreciation rights. Moderate 15-25 E17-15 Derivative transaction. Simple 10-15*E17-16 Cash Flow Hedge. Moderate 15-20*E17-17 Cash Flow Hedge. Moderate 15-20*E17-18 Fair Value Hedge. Complex 20-25

P17-1 Entries for various financial instruments. Moderate 35-40P17-2 Entries for conversion, amortization, and

interest of bonds.Moderate 45-50

P17-3 Issuance of notes with warrants. Simple 10-15P17-4 Conversion of bonds: book value vs. market

value methods. Moderate 10-15P17-5 Stock option plan. Moderate 30-35P17-6 Call option contract – purchased. Moderate 30-40P17-7 Call option contract – written. Moderate 30-40P17-8 Put option contract – derivative instrument. Moderate 30-40P17-9 Put option contract – derivative instrument. Moderate 35-45

*P17-10 Fair value hedge interest rate swap. Complex 35-45*P17-11 Cash flow hedge – futures contract. Complex 40-50*P17-12 Fair value hedge – put option. Complex 40-50

W18-1 Stock warrants—various types. Moderate 15-20W18-2 Stock compensation plans. Moderate 25-30

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-3 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 17-1

Bonds Payable............................................... 500,000Discount on Bonds Payable ................. 30,000Common Shares .................................... 470,000

BRIEF EXERCISE 17-2

Preferred Shares ........................................... 65,000Common Shares .................................... 65,000

BRIEF EXERCISE 17-3

Cash (900 X $1,000 X 1.01)............................ 909,000Discount on Bonds Payable ......................... 22,039

Bonds Payable ....................................... 900,000Contributed Surplus—Stock Warrants 31,039

FMV of bonds (900 X $1,000 X .99) $ 891,000FMV of warrants (900 X $35) 31,500Aggregate FMV $ 922,500

Allocated to bonds (891/922.5 X $909,000) $ 877,961Allocated to warrants (31.5/922.5 X $909,000) 31,039

$ 909,000

BRIEF EXERCISE 17-4

Cash (1,000 X $1,000 X 1.03)......................... 1,030,000Discount on Bonds Payable ......................... 30,000

Bonds Payable ....................................... 1,000,000Contributed Surplus—Stock Warrants 60,000

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-4 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

BRIEF EXERCISE 17-5

1/1/05 No entry

12/31/05 Compensation Expense............. 70,000Contributed Surplus—Stock Options ............................ 70,000

12/31/06 Compensation Expense............. 70,000Contributed Surplus—Stock Options ............................ 70,000

[$70,000 = $140,000 X 1/2]

BRIEF EXERCISE 17-6

The bond is considered to be a perpetual debt obligation.Jamieson is obligated to provide to the holder, payments onaccount of interest at fixed dates extending into the indefinitefuture, and a principal payment for the face value of the bond veryfar into the future. The bond would be reported on Jamieson’sbalance sheet at the present value of the annuity of interestpayments over the term of the bond, calculated at the market rateof interest, ignoring the future value of the principal payment.Because the perpetual bond’s value is driven solely by thecontractual obligation to pay interest it would be classified as along-term debt on the balance sheet.

BRIEF EXERCISE 17-7

Under the terms of the agreement with the preferred shareholders,it is highly likely that Silky Limited will be redeeming the preferredshares before the dividend rate doubles after five years. Failing todo so would result in Silky paying an extremely high dividend tothe preferred shareholders. Silky has little or no discretion to avoidpaying out the cash and this obligation to deliver cash creates a

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-5 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

liability. Consequently, the preferred shares should be classifiedas long-term debt on the balance sheet.

BRIEF EXERCISE 17-8

Because the preferred shares are classified as long-term debt onthe balance sheet, the dividends declared and paid to preferredshareholders would be classified as interest expense on theincome statement. Depending on the degree of significancedistinguishing between interest and dividends on the incomestatement, it might be desirable to separate the amount ofdividends paid on the preferred shares with the interest paid onother debt.

BRIEF EXERCISE 17-9

When a preferred share provides for mandatory redemption by theissuer for a fixed or determinable amount at a fixed ordeterminable future date or gives the holder the right to require theissuer to redeem the share at or after a particular date for a fixedor determinable amount, the instrument meets the definition of afinancial liability. Consequently, the preferred shares should beclassified as long-term debt on the balance sheet.

BRIEF EXERCISE 17-10

Pseudo should account for the call option at the cost to acquire it$500 and record it as Investments – Trading. Pseudo is notobligated to exercise the option and buy the shares. Theinvestment would be measured at market value at year-end with again or loss recorded for the difference between the cost and themarket value.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-6 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

BRIEF EXERCISE 17-11

Unlike BE17-10 Pseudo has written a call option and is obligatedto deliver to Alter shares in Ego under the terms of the option.Because the call option creates an obligation for Pseudo, it isaccounted as a liability on the balance sheet of Pseudo.

BRIEF EXERCISE 17-12

Investment – Held for Trading – Forward Contract ............................... 70

Gain on Forward Contract.............. 70($1,300 - $1,230)

BRIEF EXERCISE 17-13

January 15, 2005Investment – Held for Trading

– Forward Contract................................ 10Cash ................................................. 10

Investment – Held for in Trading – Forward Contract............................... 70

Gain on Forward Contract.............. 70

*BRIEF EXERCISE 17-14

A fair value hedge would protect Tinsdale against an existingexposure that results from an existing asset, in this case the NotesReceivable. A cash flow hedge would protect Tinsdale against afuture transaction that has not yet been realized on the balancesheet. The latter would be appropriate if Tinsdale was concernedwith the risk of a change in variable interest. There is no mentionof interest for the notes receivable. Tinsdale is concerned aboutthe exchange risk of an existing asset, and so should use a fairvalue hedge.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-7 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*BRIEF EXERCISE 17-15

2005: [5,000 X ($22 – $20)] X 50% = $5,000

2006: [5,000 X ($29 – $20)] – $5,000 = $40,000

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-8 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

SOLUTIONS TO EXERCISES

EXERCISE 17-1 (15-20 minutes)

(a) Cash ($10,000,000 X .98) ....................... 9,800,000Discount on Bonds Payable ................. 500,000

Bonds Payable ................................ 10,000,000Contributed Surplus— Conversion Rights ..................... 300,000

Bond Issue Costs .................................. 70,000Cash ................................................. 70,000

(b) Cash........................................................ 19,600,000Discount on Bonds Payable ................. 1,200,000

Bonds Payable ................................ 20,000,000Contributed Surplus—Stock Warrants 800,000

Value of bonds plus warrants ($20,000,000 X .98) $19,600,000Value of warrants (200,000 X $4) 800,000Value of bonds $18,800,000

(c) Bond Conversion Expense ................... 65,000Bonds Payable ....................................... 10,000,000Contributed Surplus—

Conversion Rights .................... 200,000Discount on Bonds Payable .......... 75,000Common Shares ............................. 10,125,000Cash ................................................. 65,000

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-9 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-2 (20-25 minutes)

The journal entry for the initial issuance follows:

Cash........................................................ 4,975,000*Discount on Bonds Payable ................. 150,000

Bond Payable ................................. 5,000,000Interest Payable.............................. 75,000Contributed Surplus - Conversion Rights .................... 50,000

*[($5,000,000 X .98) + $75,000]

(a) Interest Payable ($225,000 X 2/6) ......... 75,000Interest Expense .................................... 155,084

Discount on Bonds Payable .......... 5,084Cash ($5,000,000 X 9% ÷ 2) ............ 225,000

Calculations:Par value $5,000,000Issuance price @ .97 4,850,000Total discount $ 150,000

Months remaining 118Discount per month $1,271 ($150,000 ÷ 118)Discount amortized $5,084 (4 X $1,271)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-10 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-2 (Continued)

(b) Bonds Payable ....................................... 1,500,000Contributed Surplus—

Conversion Rights ..................... 15,000Discount on Bonds Payable ........... 41,186Common Shares .............................. 1,473,814

Calculations:

Discount related to 30% of the bonds ($150,000 X .3) $45,000Less discount amortized [($45,000 ÷ 118) X 10] 3,814Unamortized bond discount $41,186

Actual proceeds when bonds sold $4,900,000Value of bonds only 4,850,000Value of conversion rights 50,000Proportion converted _ _30%Value of rights converted $15,000

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-11 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-3 (5-10 minutes)

Bonds Payable ...................................... 1,500,000Premium on Bonds Payable ................ 20,500Contributed Surplus—

Conversion Rights ................... 14,000Preferred Shares ............................ 1,534,500

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-12 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-4 (15-20 minutes)

(a) Cash........................................................ 10,800,000Discount on Bond Payable ................... 1,500,000

Bonds Payable ............................... 10,000,000 Contributed Surplus— Conversion Rights ................... 2,300,000

(To record issuance of $10,000,000 of 8% convertible debentures for $10,800,000. The bonds mature in20 years, and each $1,000 bond is convertibleinto 5 common shares)

(b) Bonds Payable ....................................... 3,000,000Contributed Surplus—

Conversion Rights ................... 690,000Discount on Bonds Payable (Schedule 1)............................... 405,000Common Shares (Schedule 2) ..... 3,285,000

(To record conversion of 30% of the outstanding 8% convertible debentures after giving effect to the 2-for-1 stock split)

Schedule 1Computation of Unamortized Discount on Bonds Converted

Discount on bonds payable on January 1, 2004 $1,500,000Amortization for 2004 ($1,500,000 ÷ 20) $75,000Amortization for 2005 ($1,500,000 ÷ 20) 75,000

150,000Discount on bonds payable on January 1, 2006 1,350,000Bonds converted 30%Unamortized discount on bonds converted $405,000

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-13 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-4 (Continued)

Schedule 2Computation of Common Shares Resulting from Conversion

Number of shares convertible on January 1, 2004: Number of bonds ($10,000,000 ÷ $1,000) 10,000 Number of shares for each bond X 5

50,000Stock split on January 1, 2005 X 2Number of shares convertible after the stock split 100,000% of bonds converted X 30%Number of shares issued 30,000

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-14 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-5 (10-20 minutes)

Interest Expense............................................ 26,024Discount on Bonds Payable ................. 1,024 [$10,240 ÷ 40 = $256; $256 X 4]Cash (10% X $500,000 X 1/2)................. 25,000

(Assumed above that the interest accrual was reversed as of January 1, 2006 with only the

amount of the payable reversed to theinterest expense account and not the amortization of the discount; if the interest

accrual was not reversed, interest expense would be $17,691 and interest payable would be debited for $8,333)

Interest Expense............................................ 26,536Discount on Bonds Payable ................. 1,536 [$10,240 ÷ 40 = $256; $256 X 6]Cash (10% X $500,000 X 1/2)................. 25,000

(Alternately assumed that the entire interest accrual entry was reversed as of January 1, 2006)

Bonds Payable............................................... 500,000Contributed Surplus—

Conversion Rights .......................... 19,000Discount on Bonds Payable ................. 9,216*Common Shares .................................... 509,784

* ($10,240 – $1,024)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-15 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-6 (25-35 minutes)

(a) December 31, 2005Bond Interest Expense.......................... 204,000Premium on Bonds Payable ................. 6,000 ($120,000 X 1/20)

Cash ($6,000,000 X 7% X 6/12) ...... 210,000

(b) January 1, 2006Bonds Payable ....................................... 400,000Contributed Surplus—

Conversion Rights ................... 8,000*Premium on Bonds Payable ................. 6,400

Common Shares............................. 414,400*[1.04 less 1.02 = 2% X $6 million X 6.667%]

Total premium ($6,000,000 X .02) $120,000Premium amortized ($120,000 X 2/10) 24,000Balance $96,000

Bonds converted ($400,000 ÷ $6,000,000) 6.667%Related premium ($96,000 X 6.667%) 6,400

(c) March 31, 2006Bond Interest Expense.......................... 6,800Premium on Bonds Payable ................. 200 ($120,000 / 10 X 3/12 X 6.667%)

Bond Interest Payable ................... 7,000 ($400,000 X 7% X 3/12)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-16 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-6 (Continued)

March 31, 2006Bonds Payable ....................................... 400,000Contributed Surplus—

Conversion Rights ................... 8,000Premium on Bonds Payable ................. 6,200

Common Shares............................. 414,200

Premium as of January 1, 2006 for $400,000 of bonds $6,400$6,400 ÷ 8 years remaining X 3/12 (200)

Premium as of March 31, 2006 for $400,000 of bonds $6,200

(d) June 30, 2006Bond Interest Expense.......................... 176,800Premium on Bonds Payable ................. 5,200Bond Interest Payable ........................... 7,000 ($400,000 X 7% X 3/12)

Cash ................................................ 189,000*

[Premium to be amortized: ($120,000 X 86.667%) X 1/20 =$5,200, or $83,200** ÷ 16 (remaining interest andamortization periods) = $5,200]

**Total to be paid: ($5,200,000 X 7% ÷ 2) + $7,000 = $189,000

***Original premium $120,0002004 amortization (12,000)2005 amortization (12,000)Jan. 1, 2006 write-off (6,400)Mar. 31, 2006 amortization (200)Mar. 31, 2006 write-off (6,200)

$83,200

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-17 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-7 (10-15 minutes)

(a) Basic formulas:

warrantsof Valuearrants without wbonds of Valuearrants without wbonds of Value

+

X Issue price = Value assigned to bonds

warrantsof Valuearrants without wbonds of Value

warrantsof Value

+

X Issue price = Value assigned to warrants

$24,000 $136,000$136,000

+ X $152,000 = $129,200 Value assigned to bonds

$24,000 $136,000$24,000

+ X $152,000 = 22,800 Value assigned to warrants

Cash........................................................ 152,000Discount on Bonds Payable ................. 40,800 ($170,000 – $129,200)

Bonds Payable ............................... 170,000Contributed Surplus—Stock Warrants 22,800

(b) When the warrants are non-detachable, separate recognitionis given to the warrants. The accounting treatment parallelsthat given convertible debt because the debt and equityelement must be separated.

$152,000 Total

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-18 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-8 (10-15 minutes)

SANDS CORP.Journal Entry

September 1, 2005 Cash.................................................................. 5,192,500Bond Issue Costs ............................................ 20,000

Bonds Payable (5,000 X $1,000) ............. 5,000,000Premium on Bonds Payable—Schedule 1 70,000Contributed Surplus—Stock Warrants— Schedule 1............................................ 30,000Bond Interest Expense—Schedule 2 ..... 112,500 (To record the issuance of the bonds)

Schedule 1Premium on Bonds Payable and Value of Stock Warrants

Sales price (5,000 X $1,000 X 1.02) $5,100,000Face value of bonds 5,000,000

100,000Deduct value assigned to stock warrants (5,000 X 2 = 10,000 X $3) 30,000Premium on bonds payable $ 70,000

Schedule 2Accrued Bond Interest to Date of Sale

Face value of bonds $5,000,000Interest rate 9%Annual interest $ 450,000

Accrued interest for 3 months – ($450,000 X 3/12) $ 112,500

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-19 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-9 (10-15 minutes)

(a) Cash ($5,000,000 X 1.01) ....................... 5,050,000Discount on Bonds Payable ................. 100,000 [(1 – .98) X $5,000,000]

Bonds Payable ............................... 5,000,000Contributed Surplus—Stock Warrants 150,000*

*$5,050,000 – ($5,000,000 X .98)

(b) Market value of bonds without warrants $4,900,000 ($5,000,000 X .98)Market value of warrants (5,000 X $40) 200,000Total market value $5,100,000

$4,900,000$5,100,000 X $5,050,000 = $4,851,961 Value assigned to bonds

$200,000$5,100,000 X $5,050,000 = $198,039 Value assigned to warrants

Cash........................................................ 5,050,000Discount on Bonds Payable ................. 148,039

Bonds Payable ............................... 5,000,000Contributed Surplus—Stock Warrants 198,039

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-20 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-10 (15-25 minutes)

1/2/06 No entry (total compensation cost is $450,000)

12/31/06 Compensation Expense....................... 225,000Contributed Surplus—Stock Options 225,000 [To record compensation expense for 2006 (1/2 X $450,000)]

4/1/07 Contributed Surplus—Stock Options 28,125Compensation Expense.......... 28,125 ($450,000 X 2,000/32,000) (To record termination of stock options held by resigned employees)

12/31/07 Compensation Expense....................... 225,000Contributed Surplus—Stock Options 225,000 [To record compensation expense for 2007 (1/2 X $450,000)]

1/3/08 Cash (20,000 X $40).............................. 800,000Contributed Surplus—Stock Options. 281,250

($450,000 X 20,000/32,000)Common Shares ........................ 1,081,250

(To record issuance of 20,000 shares uponexercise of options at option price of $40)

(Note to instructor: The market price of the shares has norelevance in this entry and the following one.)

5/1/08 Cash (10,000 X $40) ................................ 400,000Contributed Surplus—Stock Options ... 140,625 ($450,000 X 10,000/32,000)

Common Shares .............................. 540,625

(To record issuance of 10,000 shares upon exercise of remaining options at option price of $40)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-21 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-11 (15-25 minutes)

1/1/06 No entry

12/31/06 Compensation Expense................ 275,000Contributed Surplus—Stock Options 275,000 ($550,000 X 1/2) (To recognize compensation expense for 2006)

12/31/07 Compensation Expense................ 275,000Contributed Surplus—Stock Options 275,000 ($550,000 X 1/2) (To recognize compensation expense for 2007)

3/31/08 Cash (12,000 X $20)...................... 240,000Contributed Surplus

—Stock Options .................... 165,000 ($550,000 X 12,000/40,000)

Common Shares.................... 405,000

(To record exercise of stock options)

12/31/08 Contributed Surplus—Stock Options .................... 385,000

($550,000 X 28,000/40,000)Contributed Surplus –

Expired Stock Options ..... 385,000

(To record expiration of stock options)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-22 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

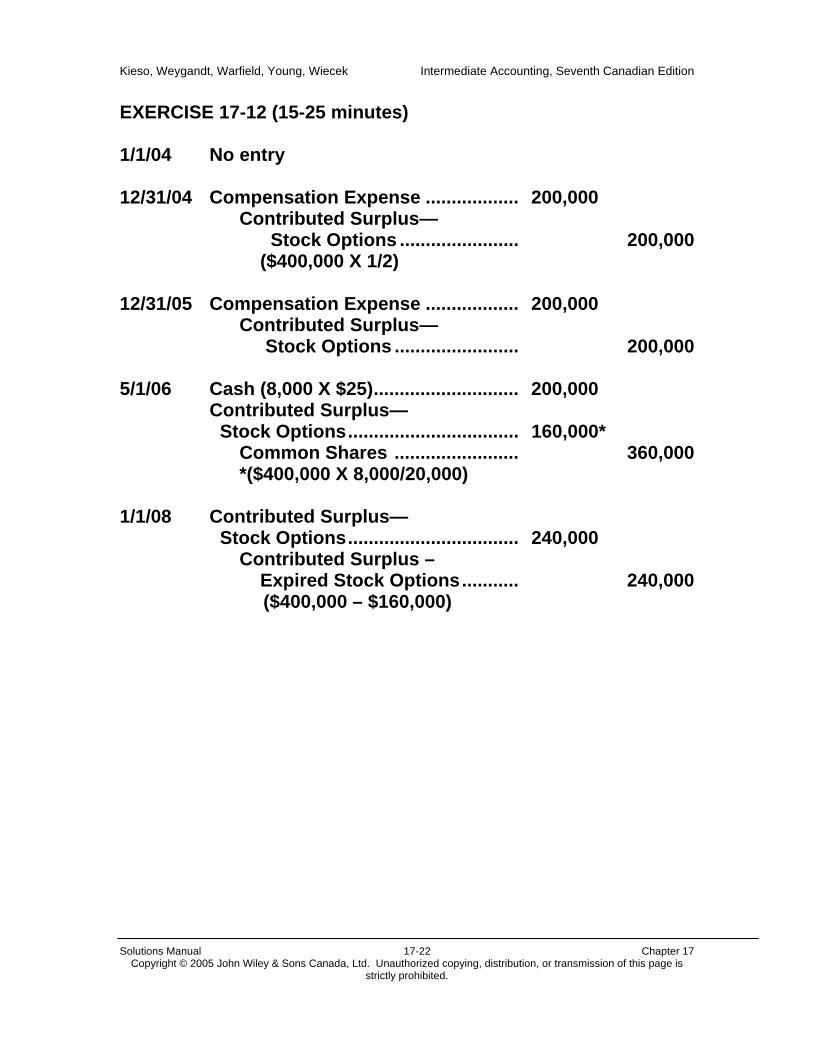

EXERCISE 17-12 (15-25 minutes)

1/1/04 No entry

12/31/04 Compensation Expense .................. 200,000Contributed Surplus— Stock Options ....................... 200,000 ($400,000 X 1/2)

12/31/05 Compensation Expense .................. 200,000Contributed Surplus— Stock Options ........................ 200,000

5/1/06 Cash (8,000 X $25)............................ 200,000Contributed Surplus— Stock Options................................. 160,000*

Common Shares ........................ 360,000*($400,000 X 8,000/20,000)

1/1/08 Contributed Surplus— Stock Options................................. 240,000

Contributed Surplus – Expired Stock Options........... 240,000

($400,000 – $160,000)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-23 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*EXERCISE 17-13 (15-25 minutes)

(a)Schedule of Compensation Expense - Stock AppreciationRights (250,000)

DateMarketPrice

PreestablishedPrice

CumulativeCompensationRecognizable

PercentageAccrued

CompensationAccrued to Date

Expense2001

Expense2002

Expense2003

Expense2004

12/31/01

12/31/02

12/31/03

12/31/04

$15

9

21

19

$12

12

12

12

$ 750,000

0

2,250,000

1,750,000

25%

50%

75%

100%

$ 187,500( (187,500) 0

1,687,500 62,500$1,750,000

$187,500$(187,500)

$1,687,500$62,500

(b) Compensation Expense .......................................................... 62,500Liability Under Stock Appreciation Plan........................

(c) Liability Under Stock Appreciation Plan................................ 1,750,000Cash [250,000 X ($19 – $12)] ...........................................

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-24 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*EXERCISE 17-14 (15-25 minutes)

(a)Schedule of Compensation Expense - Stock AppreciationRights (50,000)

DateMarketPrice

PreestablishedPrice

CumulativeCompensationRecognizable

PercentageAccrued

Compen-sation

Accruedto Date

Expense2003

Expense2004

Expense2005

Exp20

12/31/03

12/31/04

12/31/05

12/31/06

12/31/07

$36

39

45

36

48

$32

32

32

32

32

$200,000

350,000

650,000

200,000

800,000

25%

50%

75%

100%

—

$50,000 125,000 175,000 312,500 487,500 (287,500) 200,000 600,000$800,000

$50,000$125,000

$312,500

$(28

(b)2003

Compensation Expense..................................................................... 50,000Liability Under Stock Appreciation Plan...................................

2006Liability Under Stock Appreciation Plan .......................................... 287,500

Compensation Expense .............................................................

2007Compensation Expense..................................................................... 600,000

Liability Under Stock Appreciation Plan...................................

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-25 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

EXERCISE 17-15 (10-15 minutes)

(a) January 2, 2004Investment – Trading - Call Option .............. 200

Cash .................................................... 200

(b) March 31, 2004Investment – Trading - Call Option .............. 13,000

Gain 13,000[1,000 X ($53-$40)]

(c) The gain increases net income for the period by $13,000.(d) Jones has used the option for speculative purposes. Jones

is not hedging to minimize the risk of a current or futuretransaction.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-26 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*EXERCISE 17-16 (15-20 minutes)

(a)June 30, 2005 Note Rate AmountInterest paid $ 100,000 3.35%* $ 3,350 Cash received on swap (350)Interest expense $ 100,000 3% $ 3,000 * (5.7% + 1%) X 6/12

December 31, 2005 Note Rate AmountInterest paid $ 100,000 3.85%** $ 3,850 Cash received on swap (850) Interest expense $ 100,000 3% $3,000

** (6.7% + 1%) X 6/12(b) December 31, 2005Interest Expense............................................ 7,200

Cash......................................................... 7,200

[(100,000 X 6.7% X 6/12) + ($100,000 X 7.7% x 6/12)] = $7,200

Cash ($850 + $350) ........................................ 1,200Interest Expense..................................... 1,200

(c) The interest rate swap is a cash flow hedge because thepurpose in using the hedge is to protect MacCloud againstvariations in future cash flows caused by the changes in theprime rate of interest. At the time of entering into thecontract, MacCloud had not yet incurred the interest chargesfor the note. The cash flows are therefore related to futureinterest payments. Consequently the hedge cannot be a fairvalue hedge.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-27 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*EXERCISE 17-17 (15-20 minutes)

(a)December 31, 2004 Note Rate Amount

Interest paid$ 10,000,000

5.8% $ 580,000

Cash paid on swap 20,000

Interest expense$ 10,000,000

6% $ 600,000

December 31, 2005 Note Rate Amount

Interest paid$ 10,000,000

6.6% $ 660,000

Cash received on swap (60,000)

Interest expense$ 10,000,000

6% $ 600,000

(b) December 31, 2004Interest Expense............................................ 580,000

Cash ...................................................... 580,000

Interest Expense............................................ 20,000Cash ...................................................... 20,000

December 31, 2005Interest Expense............................................ 660,000

Cash ...................................................... 660,000

Cash................................................................ 60,000Interest Expense..................................... 60,000

(d) The interest rate swap is a cash flow hedge because thepurpose in using the hedge is to protect Parton againstvariations in future cash flows caused by the changes in theLIBOR rate of interest. At the time of entering into thecontract, Parton had not yet incurred the interest charges forthe note. The cash flows are therefore related to future

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-28 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

interest payments. Consequently the hedge cannot be a fairvalue hedge.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-29 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*EXERCISE 17-18 (20-25 minutes)

(a) December 31, 2005Cash................................................................ 75,000

Interest Revenue..................................... 75,000(1,000,000 X 7.5%)

(b) December 31, 2005Cash................................................................ 13,000

Interest Revenue..................................... 13,000

(c) December 31, 2005Held for Trading – Swap Contract................ 48,000

Unrealized Holding Gain or Loss -Income .............................................. 48,000

(d) December 31, 2005Unrealized Holding Gain or Loss on

Available for Sale Investments………. 48,000Fair Value Allowance on Available for

Sale Investments - Bonds............... 48,000

Note: Had the investment in bonds not been hedged, theunrealized loss would have been recorded to OtherComprehensive Income.

(e) The interest rate swap is a fair value hedge in this situationbecause the interest rate exposure is from an existingasset, the bonds.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-30 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*EXERCISE 17-18 (Continued)

(f) The interest rate swap can act as a cash flow hedge becausethe hedge allows Sarazan to participate in the potential for ahigher return on its investment caused by an increase invariable interest rates in the future. At the time of entering intothe contract, Sarazan had not yet earned the interest incomefrom its investment in bonds. The cash flows are thereforerelated to future interest receipts. Consequently the hedge canbe a cash flow hedge. Sarazan decided to change from a fixedto variable rate of interest on its investment, using the hedge.Since the investment was already in place at the time ofentering into the hedge is considered a fair value hedge.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-31 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

TIME AND PURPOSE OF PROBLEMS

Problem 17-1 (Time 35-40 minutes)

Purpose—to provide the student with an opportunity to prepare entries to properlyaccount for a series of transactions involving the issuance and exercise of commonstock rights and detachable stock warrants, plus the granting and exercise of stockoptions. The student is required to prepare the necessary journal entries to recordthese transactions and the shareholders’ equity section of the balance sheet as ofthe end of the year.

Problem 17-2 (Time 45-50 minutes)

Purpose—to provide the student with an understanding of the entries to properlyaccount for convertible debt. The student is required to prepare the journal entriesto record the conversion, amortization, and interest in connection with these bondson specified dates.

Problem 17-3 (Time 10-15 minutes)

Purpose—to provide a simple entry of the issuance of a note payable sold togetherwith a warrant. The incremental method applies in this case.

Problem 17-4 (Time 10-15 minutes)

Purpose—to provide the student with an opportunity to contrast the rationale ofrecording of the conversion of bonds payable into common shares using the bookvalue or market value methods.

Problem 17-5 (Time 30-35 minutes)

Purpose—to provide the student with an understanding of the entries to properlyaccount for a stock option plan over a period of years. The student is required toprepare the journal entries when the stock option plan was adopted, when theoptions were granted, when the options were exercised, and when the optionsexpired.

Problem 17-6 (Time 30-40 minutes)

Purpose—the student calculates and records the purchase and the transactionsconcerning a call option contract for shares over two accounting periods and alsorecord the ultimate settlement of the call option.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-32 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

TIME AND PURPOSE OF PROBLEMS (CONTINUED)

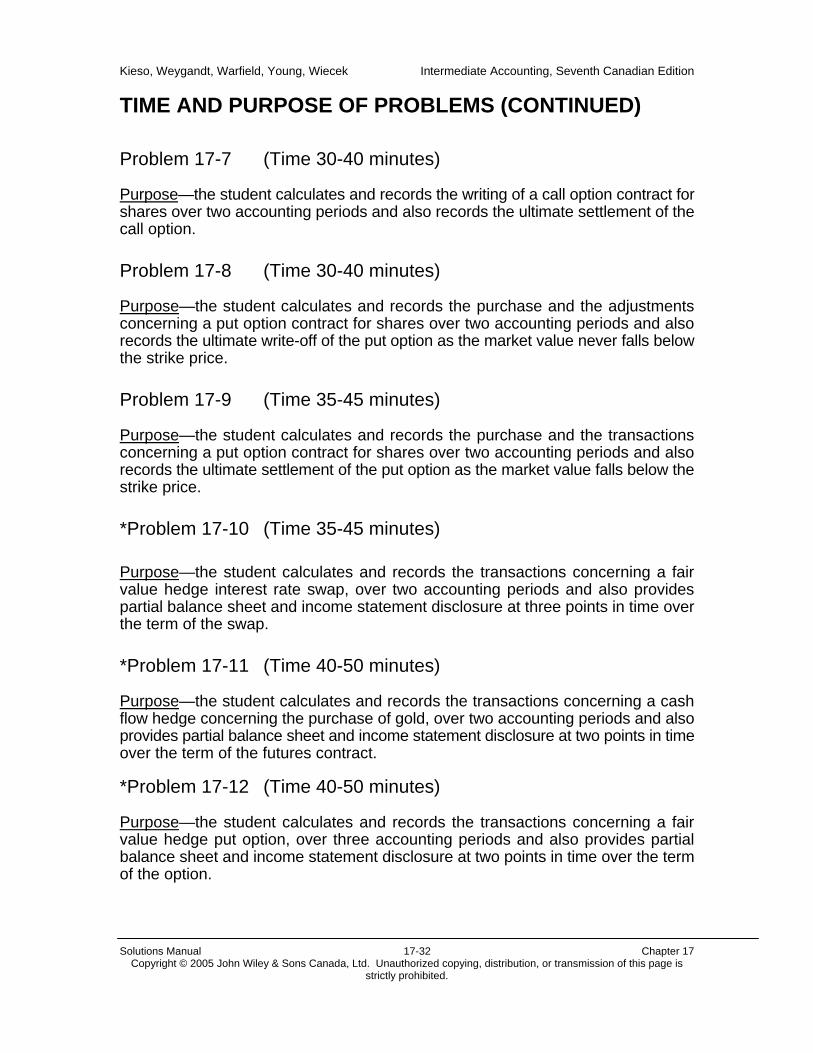

Problem 17-7 (Time 30-40 minutes)

Purpose—the student calculates and records the writing of a call option contract forshares over two accounting periods and also records the ultimate settlement of thecall option.

Problem 17-8 (Time 30-40 minutes)

Purpose—the student calculates and records the purchase and the adjustmentsconcerning a put option contract for shares over two accounting periods and alsorecords the ultimate write-off of the put option as the market value never falls belowthe strike price.

Problem 17-9 (Time 35-45 minutes)

Purpose—the student calculates and records the purchase and the transactionsconcerning a put option contract for shares over two accounting periods and alsorecords the ultimate settlement of the put option as the market value falls below thestrike price.

*Problem 17-10 (Time 35-45 minutes)

Purpose—the student calculates and records the transactions concerning a fairvalue hedge interest rate swap, over two accounting periods and also providespartial balance sheet and income statement disclosure at three points in time overthe term of the swap.

*Problem 17-11 (Time 40-50 minutes)

Purpose—the student calculates and records the transactions concerning a cashflow hedge concerning the purchase of gold, over two accounting periods and alsoprovides partial balance sheet and income statement disclosure at two points in timeover the term of the futures contract.

*Problem 17-12 (Time 40-50 minutes)

Purpose—the student calculates and records the transactions concerning a fairvalue hedge put option, over three accounting periods and also provides partialbalance sheet and income statement disclosure at two points in time over the termof the option.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-33 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

SOLUTIONS TO PROBLEMS

PROBLEM 17-1

(a) 1. Memorandum entry made to indicate the number of rightsissued.

2. Cash .................................................. 200,000Discount on Bonds Payable*........... 15,385

Bonds Payable ........................ 200,000Contributed Surplus—

Stock Warrants** ............. 15,385

**Allocated to Bonds:

$8 $96$96+

X $200,000 = $184,615;

Discount = $200,000 – $184,615 = $15,385

**Allocated to Warrants:

$8 $96$8+

X $200,000 = $15,385

3. Cash *................................................. 288,000Common Shares...................... 288,000

*[(100,000 – 10,000) rights exercised] ÷*[(10 rights/share) X $32 = $288,000

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-34 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-1 (Continued)

4. Contributed Surplus—Stock Warrants 12,308 (15,385 X 80%)Cash*....................................................... 48,000

Common Shares........................... 60,308

*.80 X $200,000/$100 per bond = 1,600*warrants exercised; 1,600 X $30 = $48,000

5. Compensation Expense*...................... 50,000Contributed Surplus – Stock Options......................... 50,000

*$10 X 5,000 options = $50,000

6. For options exercised:Cash (4,000 X $30) ................................. 120,000Contributed Surplus—Stock Options .. 40,000 (80% X $50,000)

Common Shares........................... 160,000

For options lapsed:Contributed Surplus—Stock Options .. 10,000

Compensation Expense* ............. 10,000

*(Note to instructor: This entry provides an opportunity toindicate that a credit to Compensation Expense occurs whenthe employee fails to fulfill an obligation, such as remainingin the employ of the company, performing certain jobfunctions, etc. Conversely, if a stock option lapses becausethe share price is lower than the exercise price, then a creditto Contributed Surplus—Expired Stock Options occurs.)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-35 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-1 (Continued)

(b)

Shareholders’ Equity:Share Capital:

Common Shares, authorized 1,000,000 shares, 314,600 shares issued and outstanding $4,108,308Contributed Surplus—Stock Warrants 3,077 $4,111,385

Retained Earnings 750,000Total Shareholders’ Equity $4,861,385

Calculations:Common Shares

Number AmountAt beginning of yearFrom stock rights (entry #3 above)From stock warrants (entry #4 above)From stock options (entry #6 above)

Total

300,000 9,000 1,600 4,000 314,600

$3,600,000 288,000 60,308

160,000$4,108,308

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-36 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-2

(a) Entries at August 1, 2006Bonds Payable.................................................. 150,000

Discount on Bonds Payable (Schedule 1) 5,707*Common Shares ....................................... 144,293 (To record the issuance of 750 common shares in exchange for $150,000 of bonds and the

write-off of the discount on bonds payable)

*($64,000 X 1/10) X (107/120)

Interest Payable.................................................... 1,500Cash ($150,000 X 12% X 1/12)...................... 1,500 (To record payment in cash of interest accrued on bonds converted as of August 1, 2006 – accrual and amortization was recorded July 31, 2006)

(b) Entries at August 31, 2006Bond Interest Expense......................................... 480*

Discount on Bonds Payable (Schedule 1) .. 480 (To record amortization of one month’s discount on $1,350,000 of bonds)

*($64,000 X 90%) X (1/120)

Bond Interest Expense......................................... 13,500Interest Payable ($1,350,000 X 12% X 1/12) 13,500 (To record accrual of interest for August on $1,350,000 of bonds at 12%)

(c) Entries at December 31, 2006(Same as August 31, 2006, and the following closing entry)

Income Summary........................................... 178,631Bond Interest Expense (Schedule 2) ... 178,631 (To close expense account)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-37 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-2 (Continued)

Schedule 1Monthly Amortization Schedule

Unamortized discount on bonds payable:Amount to be amortized over 120 months $64,000Amount of monthly amortization ($64,000 ÷ 120) $533Amort. for 13 months to July 31, 2006 ($533 X 13) $6,929Balance unamortized 7/31/06 ($64,000 – $6,929) $57,07110% applicable to debentures converted (5,707)Balance August 1, 2006 $51,364Remaining monthly amort. over remaining 107 months $480

Schedule 2Interest Expense Schedule

Amortization of bond discount charged to bond interest expensein 2006 would be as follows:

7 months X $533 $3,7315 months X $480 2,400

Total $6,131

Interest on Bonds:12% on $1,500,000 $180,000Amount per month ($180,000 ÷ 12) $15,00012% on $1,350,000 $162,000Amount per month ($162,000 ÷ 12) $13,500Interest for 2006 would be as follows:

7 months X $15,000 $105,0005 months X $13,500 67,500

Total $172,500

Total interestAmortization of discount $ 6,131Cash interest paid 172,500Bond interest expense $178,631

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-38 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-3

Cash................................................................ 20,040,000Discount on Notes Payable .......................... 3,960,000*

Notes Payable ......................................... 18,000,000Contributed Surplus—Stock Warrants.. 6,000,000

*($18,000,000 X 22%)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-39 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-4

When accounting for the conversion of bonds into commonshares, whether using the book value or the market value methods,certain accounts will need to be relieved of their proportionatecarrying value in order to properly record the conversion. Sincethe conversion took place immediately after an interest date, thereis no accrued interest nor amortization of bond discount to recordprior to the recording of the conversion.

Under the book value method, the pro-rata carrying value of theBonds Payable, Discount on Bonds Payable and ContributedSurplus – Stock Options would be removed and a correspondingnet entry to Common Shares would result. No gain or loss onredemption would result.

Under the market value method, the common shares would berecorded at market value (their market value or the market value ofthe bonds), the Contributed Surplus, Bonds Payable, and Discounton Bonds Payable amounts would be proportionately reduced, anda gain/credit or loss/debit would result. Since the CICA requiresshares to be recorded at their cash equivalent value, legalrequirements would tend to support this approach. The interestingquestion is whether the resulting gain/credit or loss/debit would betreated as an operating or capital transaction. If it was seen asarising from debt extinguishment, it would be an operating item(gain or loss) and recognized through the income statement. If itwas seen as part of the process of issuing shares, it should bebooked through equity.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-40 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-5

2006. No journal entry would be recorded at the time the stockoption plan was adopted. However, a memorandum entry in thejournal might be made on November 30, 2006, indicating that astock option plan had authorized the future granting to officers ofoptions to buy 70,000 common shares at $8 a share.

2007 January 2No entry

December 31Compensation Expense................................ 209,524

Contributed Surplus—Stock Options. 209,524 (To record compensation expense attributable to 2007—22,000 options)

Pro-rata calculation: 2007 2008 Total President 15,000 13,000 28,000 Vice- President 7,000 7,000 14,000 Total options 22,000 20,000 42,000 Compensation Expense $ 209,524* $ 190,476** $400,000 * 22,000 / 42,000 X $400,000 = $209,524** 20,000 / 42,000 X $400,000 = $190,476

2008 December 31Compensation Expense................................ 190,476

Contributed Surplus—Stock Options. 190,476 (To record compensation expense attributable to 2008—20,000 options)

Contributed Surplus—Stock Options.......... 209,524Contributed Surplus—Expired Stock Options................................... 209,524

(To record lapse of president’s and vice president’s options to buy 22,000 shares)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-41 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-5 (Continued)

2009 December 31Cash (20,000 X $8)......................................... 160,000Contributed Surplus—Stock Options.......... 190,476

Common Shares............................... 350,476 (To record issuance of 20,000 common shares

upon exercise of options at option price of $8)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-42 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-6

(a) July 7, 2004Investment – Trading - Call Option .............. 240

Cash......................................................... 240

(b) September 30, 2004Investment – Trading - Call Option .............. 1,400

Gain ......................................................... 1,400[200 X ($77-$70)]

Loss ................................................................ 60Investment – Trading – Call Option ...... 60

($240-$180)

(c) December 31, 2004Loss ................................................................ 400

Investment – Trading – Call Option ...... 400[200 X ($75-$77)]

Loss ................................................................ 115Investment - Trading – Call Option ....... 115

($180-$65)

(d) January 4, 2005Cash [200 x ($76 -$70)].................................. 1,200

Gain on Settlement of Call Option ........ 135Investment - Trading - Call Option........ 1,065

July 7, 2004 $ 240

Sept. 30, 2004 1,400

Sept. 30, 2004 (60)Dec. 31, 2004 (400)Dec. 31, 2004 (115)Balance $ 1,065

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-43 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-7

(a) July 7, 2004Cash................................................................ 240

Obligation – Call Option......................... 240

(b) September 30, 2004Loss - Call Option.......................................... 1,400

Obligation – Call Option......................... 1,400[200 X ($77-$70)]

Obligation – Call Option................................ 60Gain – Call Option .................................. 60

($240-$180)

(c) December 31, 2004Obligation – Call Option................................ 400

Gain – Call Option .................................. 400[200 X ($75-$77)]

Obligation – Call Option................................ 115Gain – Call Option .................................. 115

($180-$65)

(d) January 4, 2005Obligation – Call Option................................ 1,065Loss on Settlement of Call Option............... 135

Cash [200 x ($76 -$70)]........................... 1,200

July 7, 2004 $ (240)

Sept. 30, 2004 (1,400)

Sept. 30, 2004 60Dec. 31, 2004 400Dec. 31, 2004 115Balance $ (1,065)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-44 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-8

(a) July 7, 2004Investment – Trading – Put Option .............. 240

Cash......................................................... 240

(b) September 30, 2004No accrual of Unrealized Holding Gain since the market priceof Ewing shares increased beyond the $70 strike price.

Loss - Put Option........................................... 115Investment – Trading - Put Option........ 115

($240-$125)

(c) December 31, 2004No accrual of Unrealized Holding Gain since the market priceof Ewing shares still exceeds $70, the strike price.

Loss – Put Option.......................................... 75Investment – Trading – Put Option ...... 75

($125-$50)

(d) January 31, 2005Put option is not used as the market price of Ewing sharesexceeds $70, the strike price.

Loss – Put Option.......................................... 50Investment – Trading - Put Option........ 50

July 7, 2004 $ 240 Sept. 30, 2004 (115)Dec. 31, 2004 (75)Balance $ 50

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-45 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

PROBLEM 17-9

(a) January 7, 2004Investment – Trading - Put Option............... 360

Cash......................................................... 360

(b) March 31, 2004Investment –Trading - Put Option................ 2,000

Gain – Put Option .................................. 2,000[400 X ($85-$80)]

Loss – Put Option.......................................... 160Investment – Trading - Put Option........ 160

($360-$200)

(c) June 30, 2004Loss – Put Option.......................................... 800

Investment – Trading - Put Option........ 800[400 X ($82-$80)]

Loss – Put Option.......................................... 110Investment –Trading - Put Option......... 110

($200-$90)

(d) July 6, 2004Cash [400 x ($85 -$77)].................................. 3,200

Gain on Settlement of Put Option ......... 1,910Investment – Trading - Put Option........ 1,290

Jan 7, 2004 $ 360

March 31,2004 2,000

March 31,2004 (160)June 30, 2004 (800)June 30, 2004 (110)Balance $ 1,290

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-46 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*PROBLEM 17-10

(a) (1) December 31, 2004No entry required

(2) June 30, 2005Interest Expense............................................ 350,000

Cash......................................................... 350,000($10,000,000 X 7% X 6/12)

(3) June 30, 2005Interest Expense............................................ 50,000

Cash......................................................... 50,000($10 million X 8% less 7% X 6/12)

(4) June 30, 2005Note Payable.................................................. 200,000

Unrealized Holding Gain or Loss -Income ................................................ 200,000

(5) June 30, 2005Unrealized Holding Gain or Loss - Income 200,000

Other Liabilities – Swap Contract ......... 200,000

(b) Mercantile Corp.

Balance sheet (partial)December 31, 2004

Long-term liabilitiesNote payable $10,000,000

Income Statement (partial)For the Year Ending December 31, 2004

No items to report

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-47 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*PROBLEM 17-10 (Continued)(c)

Mercantile Corp.Balance sheet (partial)

June 30, 2005Current liabilities

Swap contract $200,000

Long-term liabilitiesNote payable $9,800,000

Income Statement (partial)For the Six Months Period Ending June 30, 2005

Interest expense $400,000

Other revenues and gains:Unrealized holding gain – Note payable $200,000Unrealized holding loss- Swap contract (200,000) 0

(d)Mercantile Corp.

Balance sheet (partial)December 31, 2005

Current assetsSwap contract $60,000

Current liabilitiesNote payable $10,060,000

Income Statement (partial)For the Year Ending December 31, 2005

Interest expense* $800,000

Other revenues and gains:Unrealized holding loss – Note payable $(60,000)Unrealized holding gain – Swap contract 60,000 0

*($10 Million X 8 %)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-48 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*PROBLEM 17-11

(a) April 1, 2005No entry required

(b) June 30, 2005Futures Contract............................................ 5,000

Unrealized Holding Gain or Loss –Income (OCI) ...................................... 5,000($310-$300) X 500 ounces

(c) September 30, 2005Futures Contract............................................ 2,500

Unrealized Holding Gain or Loss –Income (OCI) ...................................... 2,500($315-$310) X 500 ounces

(d) October 31, 2005Raw Materials Inventory - Gold .................... 157,500

Cash (500 ounces X $315) ..................... 157,500

Cash................................................................ 7,500Other Assets – Futures Contract .......... 7,500

($157,500 - $150,000)

(e) December 20, 2005Accounts Receivable/Cash........................... 350,000

Sales ........................................................ 350,000

Cost of Goods Sold ....................................... 200,000Finished Goods Inventory ..................... 200,000

Unrealized Holding Gain or Loss –Income (OCI) ............................................ 7,500

Cost of Goods Sold ................................ 7,500

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-49 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*PROBLEM 17-11 (Continued)

(f)LEW Jewellery Corp.

Balance sheet (partial)June 30, 2005

Current assetsFutures Contract $5,000

EquityAccumulated Other Comprehensive Income $5,000

Income Statement (partial)For the Six Months Period Ending June 30, 2005

Other Comprehensive Income:Unrealized holding gain – Futures contract $5,000

(g)LEW Jewellery Corp.

Income Statement (partial)For the Year Ending December 31, 2005

Sales $350,000Cost of goods sold ($200,000 - $7,500) 192,500Gross profit $ 157,500

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-50 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*PROBLEM 17-12(a)(1) November 3, 2005Investments – Available-for-Sale -

Johnstone.................................................. 200,000Cash......................................................... 200,000

Investments – Available-for-Sale– PutOption ......................................................... 600

Cash......................................................... 600

(2) December 31, 2005Loss ............................................................... 225

Investments – Available-for-SaleInvestments – Put Option................... 225($600-$375)

(3) March 31, 2006Unrealized Holding Gain/Loss on

Available-for-Sale Investments (OCI)...... 20,000Fair Value Allowance on Available-

for-Sale Investments........................... 20,000[4,000 X ($50-$45)]

Loss ................................................................ 200Investments – Available for Sale

Investments – Put Option................... 200($375-$175)

(4) June 30, 2006Unrealized Holding Gain/Loss on

Available-for-Sale Investments (OCI)...... 8,000Fair Value Allowance on Available-

for-Sale Investments........................... 8,000[4,000 X ($45-$43)]

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-51 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*PROBLEM 17-12 (Continued)

June 30, 2006Loss ................................................................ 135

Investments – Available for SaleInvestments – Put Option .................. 135($175-$40)

(5) July 1, 2006Cash (4,000 X $43)......................................... 172,000Loss on Sale of Available-for-Sale

Securities 28,000Investments – Available-for- Sale-

Johnstone.......................................... 200,000

Cash [4,000 X ($50-$43)] ............................... 28,000Gain/Loss on Settlement of Put

Option ................................................ 28,000

Fair Value Allowance on Available-for-Sale Investments ...................................... 28,000

Unrealized Holding Gain/Loss onAvailable-for-Sale Investments (OCI) .

28,000

Loss ................................................................ 40Investments – Available for Sale

Investments – Put Option ................. 40

Nov. 3, 2005 $ 600 Dec. 31, 2005 (225)March 31, 2006 (200)June 30, 2006 (135)Balance $ 40

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-52 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*PROBLEM 17-12 (Continued)

(b)Spinkle Corp.

Balance sheet (partial)December 31, 2005

Current Assets:Investments – Available for Sale – Put option $375

Non-Current Assets:Investments – Available for Sale - Johnstone $200,000

Income Statement (partial)For the Year Ending December 31, 2005

Other expenses and losses:Loss on available-for-sale investments

– put option $225

(c)Sprinkle Corp.

Balance sheet (partial)June 30, 2006

Current Assets:Investments – Available for Sale – Put option $40Investments – Available for Sale - Johnstone $200,000Less: Fair Value Allowance on

Available-for-Sale Investments (28,000)$172,040

Equity:Accumulated Other Comprehensive Income $(28,000)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-53 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

*PROBLEM 17-12 (Continued)

Income Statement (partial)For the Six Months Period Ending June 30, 2006

Other expenses and losses:Loss on available-for-sale investments

– put option $335

Other Comprehensive Income:Unrealized Holding Gain/Loss on

Available-for-Sale Investments $(28,000)

*March 31,2006 loss (200)

June 30, 2006 loss (135)$ (335)

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-54 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

TIME AND PURPOSE OF WRITING ASSIGNMENTS

Assignment 17-1 (Time 15-20 minutes)

Purpose—to provide the student with an understanding of the proper accountingand conceptual merits for the issuance of stock warrants to three different groups:existing shareholders, key employees, and purchasers of the company’s bonds.This problem requires the student to explain and discuss the reasons for usingwarrants, the significance of the price at which the warrants are issued (or granted)in relation to the current market price of the company’s shares, and the necessaryinformation that should be disclosed in the financial statements when stock warrantsare outstanding for each of the groups.

Assignment 17-2 (Time 25-30 minutes)

Purpose—to provide the student with an opportunity to respond to a contrary viewof the FASB’s standard on “Accounting for Stock-Based Compensation,” and todefend the concept of neutrality in financial accounting and reporting.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-55 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

SOLUTIONS TO WRITING ASSIGNMENTS

ASSIGNMENT 17-1

(a) 1. The objective of issuing warrants to existing shareholders on a pro-ratabasis is to raise new equity capital. This method of raising equity capitalmay be used because of pre-emptive rights on the part of a company’sshareholders and also because it is likely to be less expensive than apublic offering.

2. The purpose of issuing stock warrants to certain key employees, usuallyin the form of a nonqualified stock option plan, is to increase their interestin the long-term growth and income of the company and to attract newmanagement talent. Also, this issuance of stock warrantsto key employees under a stock option plan frequently constitutes animportant element in a company’s executive compensation program.Though such plans result in some dilution of the shareholders’ equitywhen shares are issued, the plans provide an additional incentive to thekey employees to operate the company efficiently.

3. Warrants to purchase common shares may be issued to purchasers ofa company’s bonds in order to stimulate the sale of the bonds byincreasing their speculative appeal and aiding in overcoming theobjection that rising price levels cause money invested for long periodsin bonds to lose purchasing power. The use of warrants in thisconnection may also permit the sale of the bonds at a lower interest cost.

(b) 1. Because the purpose of issuing warrants to existing shareholders is toraise new equity capital, the price specified in the warrants must besufficiently below the current market price to reasonably assure that theywill be exercised. Because the success of the offering depends entirelyon the current market price of the company’s shares in relation to theexercise price of the warrants, and because the objective is to raisecapital, the length of time over which the warrants can be exercised isvery short, frequently 60 days.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-56 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

ASSIGNMENT 17-1 (Continued)

2. Warrants may be offered to key employees below, at, or above themarket price of the shares on the day the rights are granted except forincentive stock option plans. If a stock option plan is to provide a strongincentive, warrants that can be exercised shortly after they are grantedand expire, say, within two or three years, usually must be exercisableat or near the market price at the date of the grant. Warrants that cannotbe exercised for a number of years after they are granted or those thatdo not lapse for a number of years after they become exercisable may,however, be priced somewhat above the market price of the shares atthe date of the grant without eliminating the incentive feature. This doesnot upset the principal objective of stock option plans, heightening theinterest of key employees in the long-term success of the company.Income tax laws penalize the issuance of warrants and stock options atprices below market price on the day the rights are granted, by taxingthem as part of employment income.

3. Income tax laws impose no restrictions on the exercise price of warrantsissued to purchasers of a company’s bonds. The exercise price may beabove, equal to, or below the current market price of the company’sshares. The longer the period of time during which the warrant can beexercised, however, the higher the exercise price can be and stillstimulate the sale of the bonds because of the increased speculationappeal. Thus, the significance of the length of time over which thewarrants can be exercised depends largely on the exercise price (orprices). A low exercise price in combination with a short exercise periodcan be just as successful as a high exercise price in combination with along exercise period.

(c) 1. Financial statement information concerning outstanding stock warrantsissued to a company’s shareholders should include a description of theshares being offered for sale, the option price, the time period duringwhich the rights may be exercised, and the number of rights needed topurchase a new share.

2. Financial statement information concerning stock warrants issued to keyemployees should include the following: status of these plans at end ofperiods presented, including the number of shares under option, theprices at which the warrants may be exercised, the time periods andconditions under which they may be exercised, and the number ofwarrants exercised and forfeited during the year.

3. Financial statement disclosure of outstanding stock warrants that havebeen issued to purchasers of a company’s bonds should include theprices at which they can be exercised, the length of time they can beexercised, and the total number of shares that can be purchased by thebondholders.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-57 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

ASSIGNMENT 17-2

The following is an excerpt from a presentation given by Dennis Beresford onthe concept of neutrality.

The Board often hears that we should take a broader view, that we mustconsider the economic consequences of a new accounting standard. TheFASB should not act, critics maintain, if a new accounting standard wouldhave undesirable economic consequences. We have been told thatthe effects of accounting standards could cause lasting damage to Americancompanies and their employees. Some have suggested, for example, thatrecording the liability for retiree health care or the costs for stock-basedcompensation will place U.S. companies at a competitive disadvantage. Thesecritics suggest that because of accounting standards, companies may reducebenefits or move operations overseas to areas where workers do not demandthe same benefits. These assertions are usually combined with statementsabout desirable goals, like providing retiree health care or creating employeeincentives.

There is a common element in those assertions. The goals are desirable butthe means require that the Board abandon neutrality and establish reportingstandards that conceal the financial impact of certain transactions from thosewho use financial statements. Costs of transactions exist whetheror not the FASB mandates their recognition in financial statements. Forexample, not requiring the recognition of the cost of stock options or ignoringthe liabilities for retiree health care benefits does not alter the economics ofthe transactions. It only withholds information from investors, creditors, policymakers, and others who need to make informed decisions and, eventually,impairs the credibility of financial reports.

One need only look to the collapse of the thrift industry to demonstrate theconsequences of abandoning neutrality. During the 1970s and 1980s,regulatory accounting principles (RAP) were altered to obscure problems introubled institutions. Preserving the industry was considered a greater good.Many observers believe that the effect was to delay action and hide the truedimensions of the problem. The public interest is best served by neutralaccounting standards that inform policy rather than promote it. Stated simply,truth in accounting is always good policy.

Neutrality does not mean that accounting should not influence humanbehaviour. We expect that changes in financial reporting will have economicconsequences, just as economic consequences are inherent in existingfinancial reporting practices. Changes in behaviour naturally follow from morecomplete and representationally faithful financial statements. The fundamentalquestion, however, is whether those who measure and report on economicevents should somehow screen the information before reporting it to achievesome objective. In FASB Concepts Statement No. 2, Qualitative

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-58 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

ASSIGNMENT 17-2 (Continued)

Characteristics of Accounting Information (paragraph 102), the Boardobserved:

Indeed, most people are repelled by the notion that some “bigbrother,” whether government or private, would tamper with scalesor speedometers surreptitiously to induce people to lose weight orobey speed limits or would slant the scoring of athletic events orexaminations to enhance or decrease someone’s chances ofwinning or graduating. There is no more reason to abandonneutrality in accounting measurement.

The Board continues to hold that view. The Board does not set out to achieveparticular economic results through accounting pronouncements. We could notif we tried. Beyond that, it is seldom clear which result we should seekbecause our constituents often have opposing viewpoints. Governments, andthe policy goals they adopt, frequently change.

Kieso, Weygandt, Warfield, Young, Wiecek Intermediate Accounting, Seventh Canadian Edition

Solutions Manual 17-59 Chapter 17Copyright © 2005 John Wiley & Sons Canada, Ltd. Unauthorized copying, distribution, or transmission of this page is

strictly prohibited.

Chapter 17 Suggested Case SolutionsSee the Case Primer on the Digital Tool – also the Suggested outline for case solutions.Note that the first few chapters lay the foundation for financial reporting decision making.

CA 17-1 Sanford Corp.

Overview:

- the company is in the business of selling fire extinguishers- it is using shares as incentive to sell its products- closely held company and therefore GAAP may not be a constraint unless

users e.g. shareholders request as more relevant and reliable –assume so- note that as an analyst, would start with these statements (GAAP or not)

and adjust the numbers to get the most meaningful information about thecompany