Ch10_Auditing Expenditure Cycle

21

Chapter 10: Auditing the Expenditure Cycle IT Auditing & Assurance, 2e, Hall & Singleton

-

Upload

rizka-furqorina -

Category

Documents

-

view

118 -

download

0

Transcript of Ch10_Auditing Expenditure Cycle

Chapter 10:Auditing the Expenditure

Cycle

IT Auditing & Assurance, 2e, Hall & Singleton

IT Auditing & Assurance, 2e, Hall & Singleton

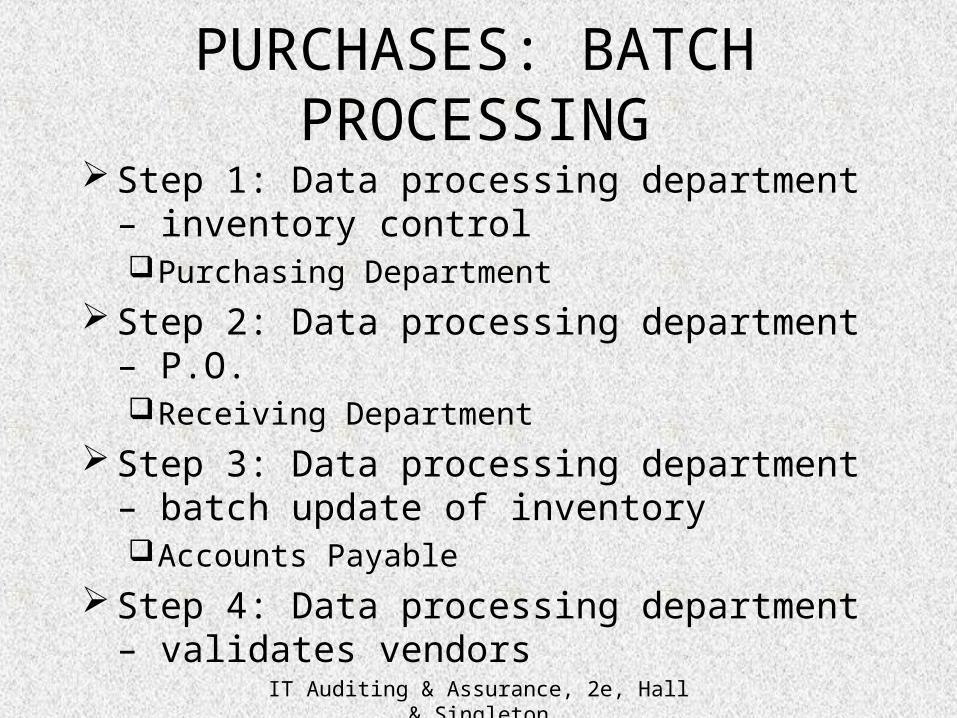

Step 1: Data processing department – inventory controlPurchasing Department

Step 2: Data processing department – P.O.Receiving Department

Step 3: Data processing department – batch update of inventoryAccounts Payable

Step 4: Data processing department – validates vendors

PURCHASES: BATCH PROCESSING

IT Auditing & Assurance, 2e, Hall & Singleton

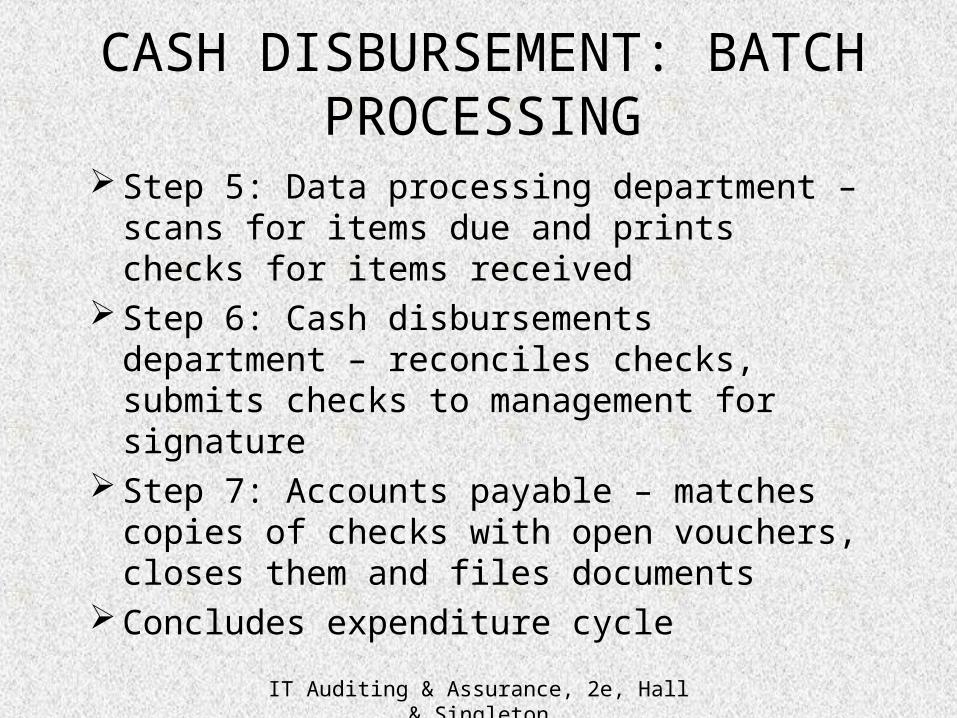

Step 5: Data processing department – scans for items due and prints checks for items received

Step 6: Cash disbursements department – reconciles checks, submits checks to management for signature

Step 7: Accounts payable – matches copies of checks with open vouchers, closes them and files documents

Concludes expenditure cycle

CASH DISBURSEMENT: BATCH PROCESSING

IT Auditing & Assurance, 2e, Hall & Singleton

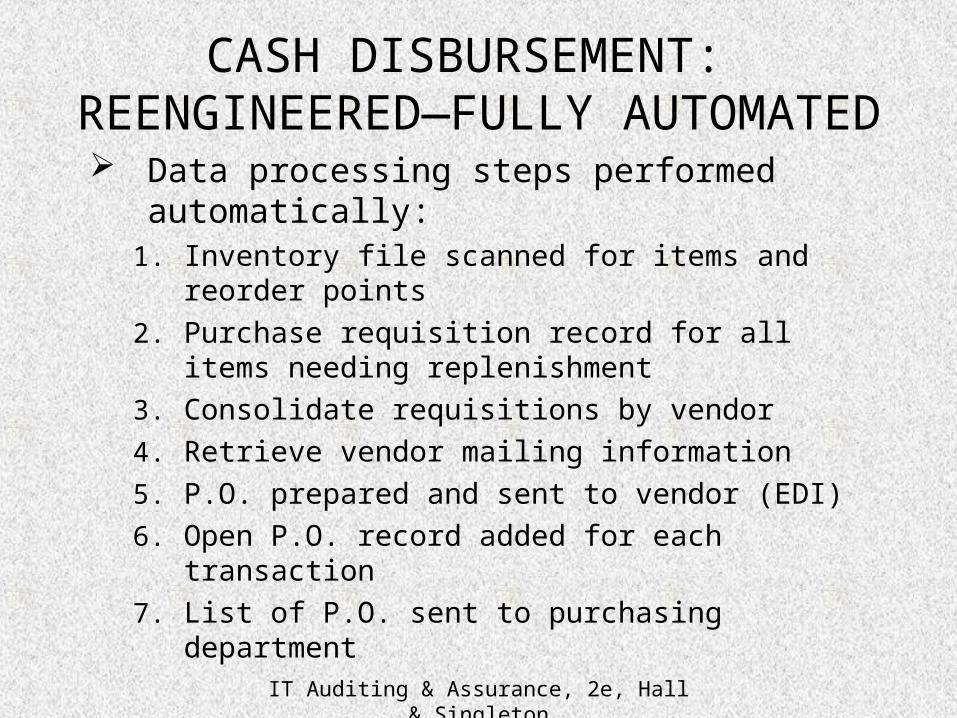

Data processing steps performed automatically:

1. Inventory file scanned for items and reorder points

2. Purchase requisition record for all items needing replenishment

3. Consolidate requisitions by vendor

4. Retrieve vendor mailing information

5. P.O. prepared and sent to vendor (EDI)

6. Open P.O. record added for each transaction

7. List of P.O. sent to purchasing department

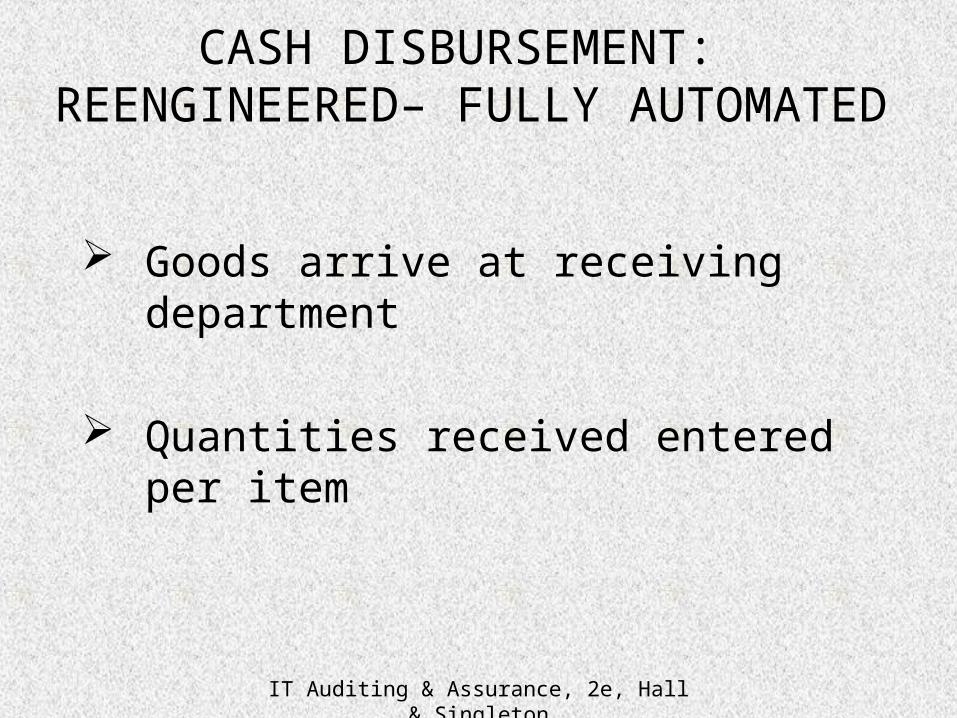

CASH DISBURSEMENT: REENGINEERED—FULLY AUTOMATED

IT Auditing & Assurance, 2e, Hall & Singleton

Goods arrive at receiving department

Quantities received entered per item

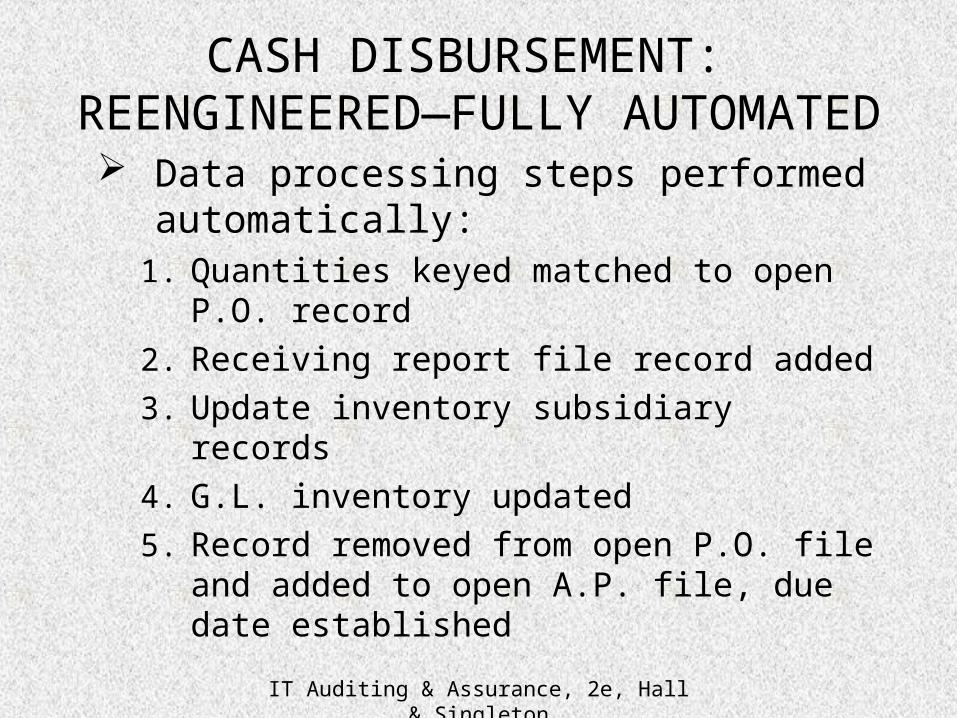

CASH DISBURSEMENT: REENGINEERED– FULLY AUTOMATED

IT Auditing & Assurance, 2e, Hall & Singleton

Data processing steps performed automatically:

1. Quantities keyed matched to open P.O. record

2. Receiving report file record added

3. Update inventory subsidiary records

4. G.L. inventory updated

5. Record removed from open P.O. file and added to open A.P. file, due date established

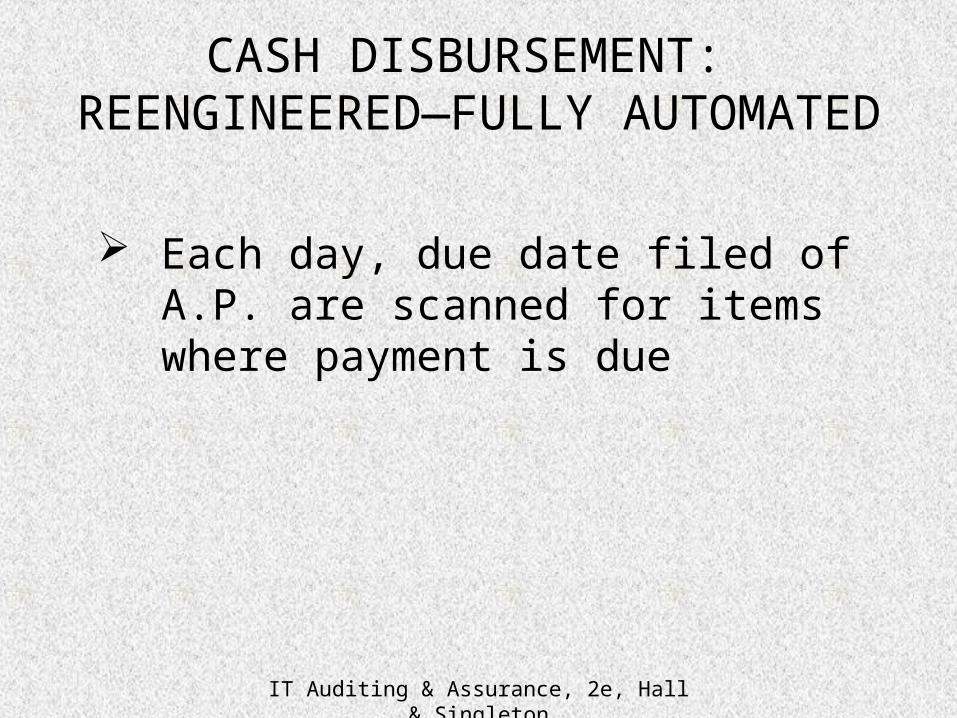

CASH DISBURSEMENT: REENGINEERED—FULLY AUTOMATED

IT Auditing & Assurance, 2e, Hall & Singleton

Each day, due date filed of A.P. are scanned for items where payment is due

CASH DISBURSEMENT: REENGINEERED—FULLY AUTOMATED

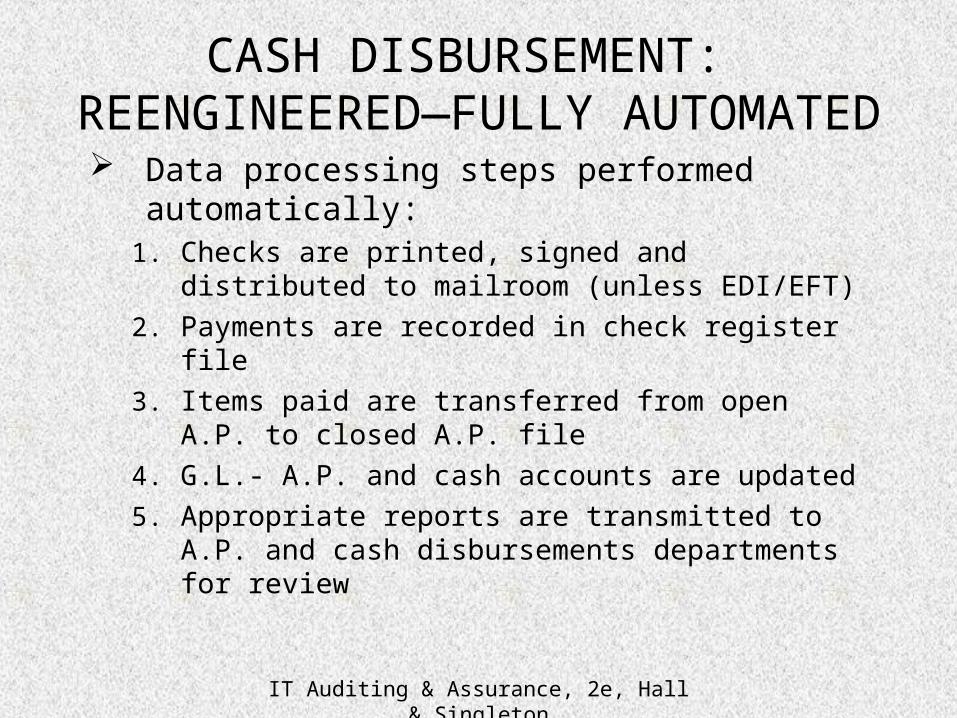

IT Auditing & Assurance, 2e, Hall & Singleton

Data processing steps performed automatically:

1. Checks are printed, signed and distributed to mailroom (unless EDI/EFT)

2. Payments are recorded in check register file

3. Items paid are transferred from open A.P. to closed A.P. file

4. G.L.- A.P. and cash accounts are updated

5. Appropriate reports are transmitted to A.P. and cash disbursements departments for review

CASH DISBURSEMENT: REENGINEERED—FULLY AUTOMATED

IT Auditing & Assurance, 2e, Hall & Singleton

Control implications

General in nature Similar to those of Chapter 9

CASH DISBURSEMENT: REENGINEERED—FULLY AUTOMATED

IT Auditing & Assurance, 2e, Hall & Singleton

Improved inventory control Better cash management Less time lag Better purchasing time management Reduction of paper documents

BATCH AUTOMATED SYSTEM VS. MANUAL BATCH

IT Auditing & Assurance, 2e, Hall & Singleton

Segregation of duties

Accounting records and access controls

REENGINEERED SYSTEM VS.

BATCH AUTOMATED SYSTEM

IT Auditing & Assurance, 2e, Hall & Singleton

Drawbacks to using regular A.P. and cash disbursements systems to do payroll

General expenditure procedures that apply to all vendors will not apply to employees

Writing checks to employees requires special controls

General expenditure procedures are designed to accommodate relatively smooth flow of transactions

PAYROLL PROCEDURES

IT Auditing & Assurance, 2e, Hall & Singleton

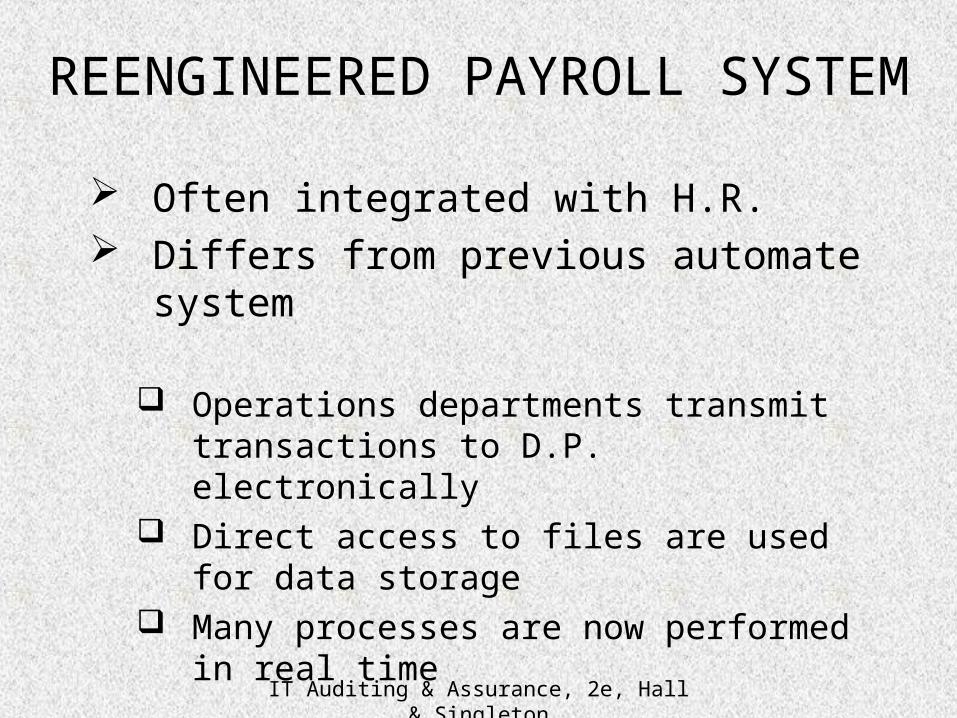

Often integrated with H.R. Differs from previous automate system

Operations departments transmit transactions to D.P. electronically

Direct access to files are used for data storage

Many processes are now performed in real time

REENGINEERED PAYROLL SYSTEM

IT Auditing & Assurance, 2e, Hall & Singleton

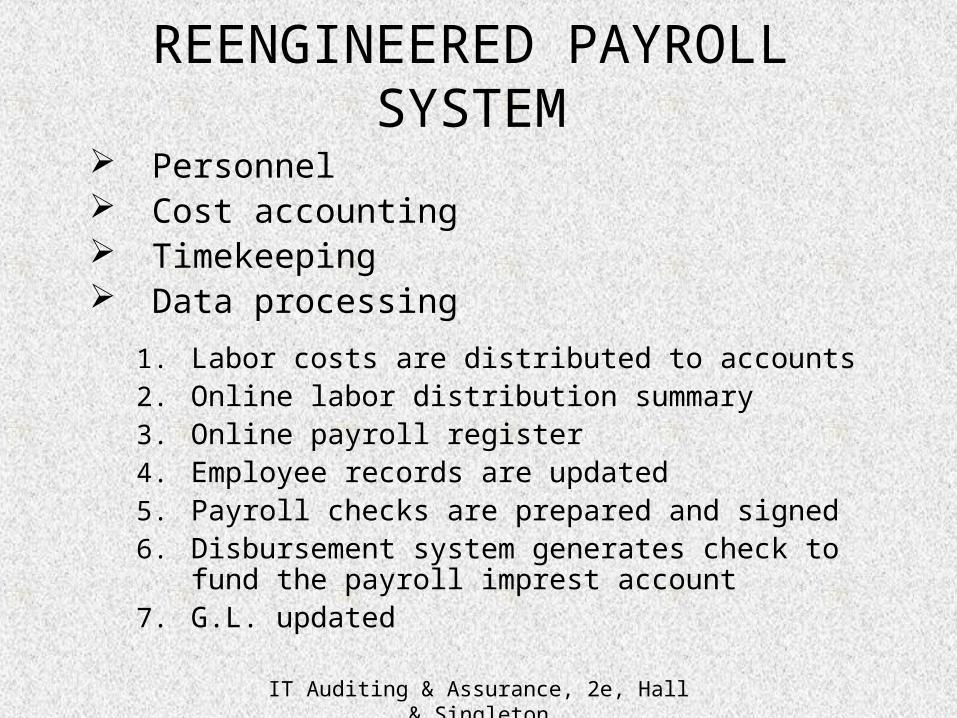

Personnel Cost accounting Timekeeping Data processing

1. Labor costs are distributed to accounts2. Online labor distribution summary 3. Online payroll register4. Employee records are updated5. Payroll checks are prepared and signed6. Disbursement system generates check to fund the

payroll imprest account7. G.L. updated

REENGINEERED PAYROLL SYSTEM

IT Auditing & Assurance, 2e, Hall & Singleton

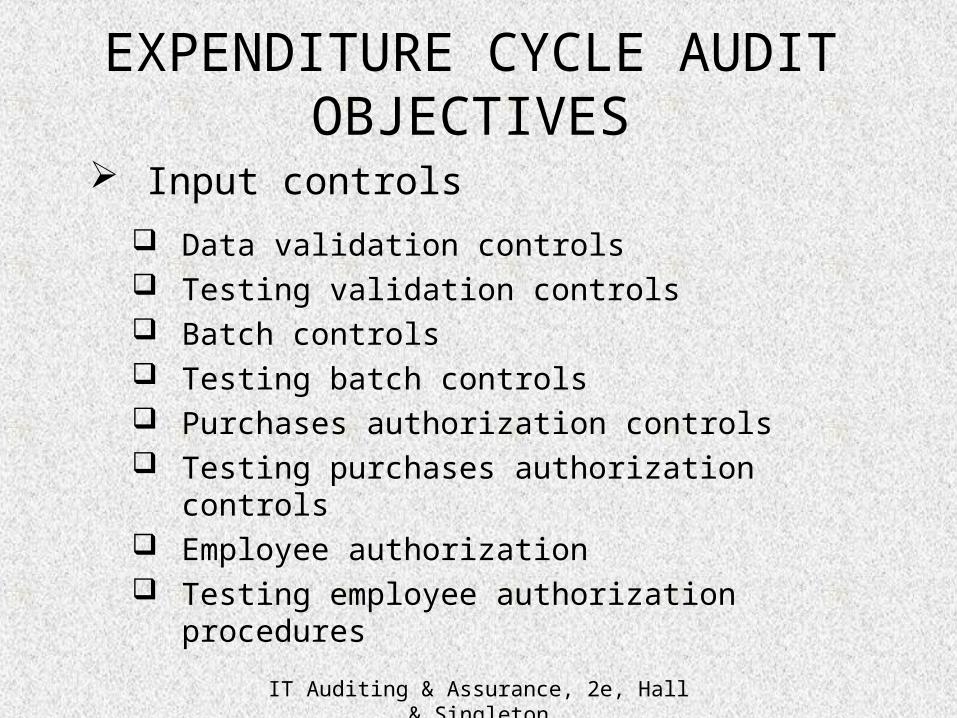

Input controls

Data validation controls Testing validation controls Batch controls Testing batch controls Purchases authorization controls Testing purchases authorization controls Employee authorization Testing employee authorization procedures

EXPENDITURE CYCLE AUDIT OBJECTIVES

IT Auditing & Assurance, 2e, Hall & Singleton

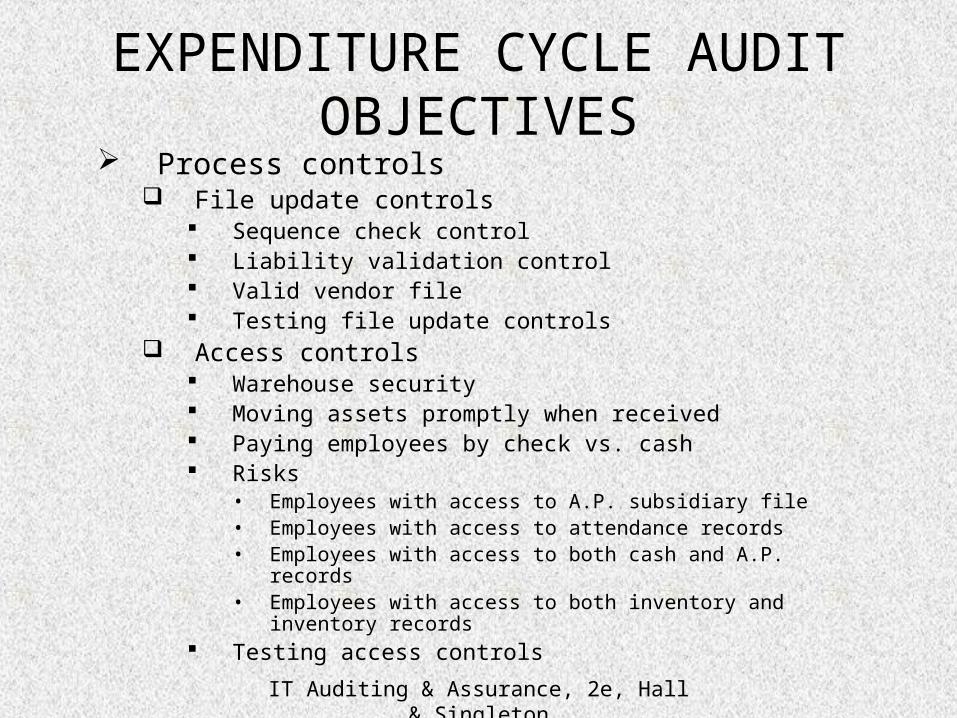

Process controls File update controls

Sequence check control Liability validation control Valid vendor file Testing file update controls

Access controls Warehouse security Moving assets promptly when received Paying employees by check vs. cash Risks

• Employees with access to A.P. subsidiary file• Employees with access to attendance records• Employees with access to both cash and A.P. records• Employees with access to both inventory and inventory records

Testing access controls

EXPENDITURE CYCLE AUDIT OBJECTIVES

IT Auditing & Assurance, 2e, Hall & Singleton

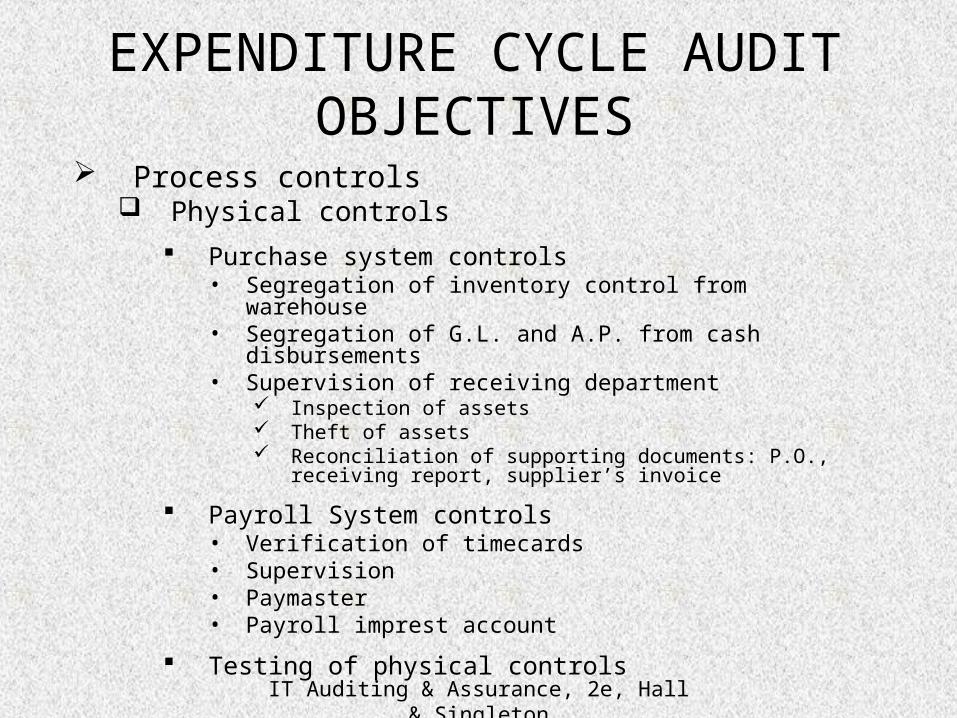

Process controls Physical controls

Purchase system controls• Segregation of inventory control from warehouse• Segregation of G.L. and A.P. from cash disbursements• Supervision of receiving department

Inspection of assets Theft of assets Reconciliation of supporting documents: P.O., receiving

report, supplier’s invoice

Payroll System controls• Verification of timecards• Supervision• Paymaster• Payroll imprest account

Testing of physical controls

EXPENDITURE CYCLE AUDIT OBJECTIVES

IT Auditing & Assurance, 2e, Hall & Singleton

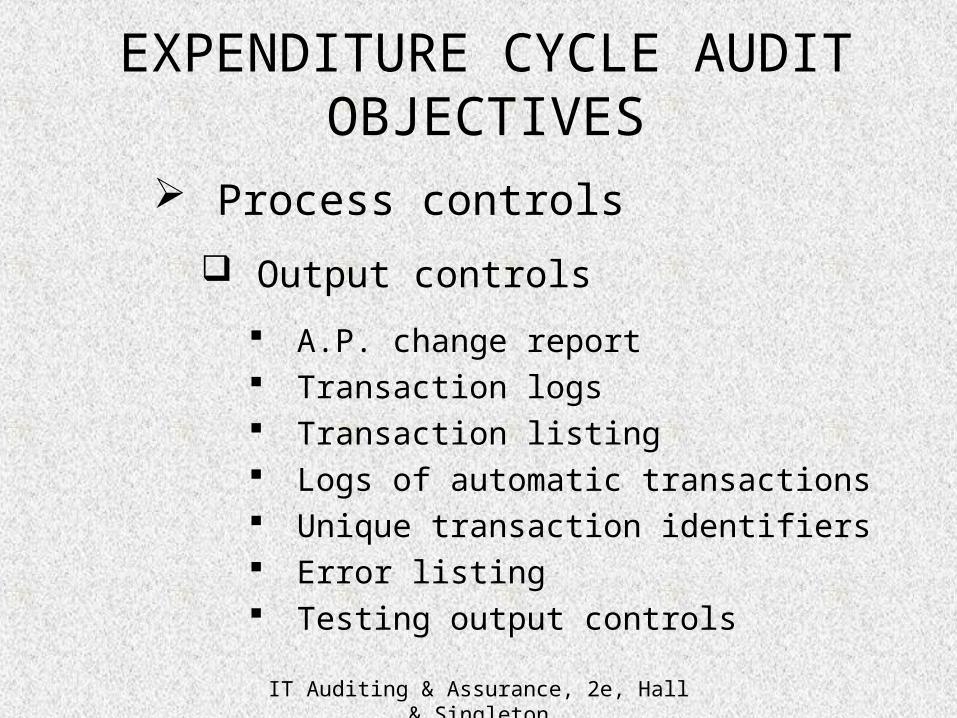

Process controls

Output controls

A.P. change report Transaction logs Transaction listing Logs of automatic transactions Unique transaction identifiers Error listing Testing output controls

EXPENDITURE CYCLE AUDIT OBJECTIVES

IT Auditing & Assurance, 2e, Hall & Singleton

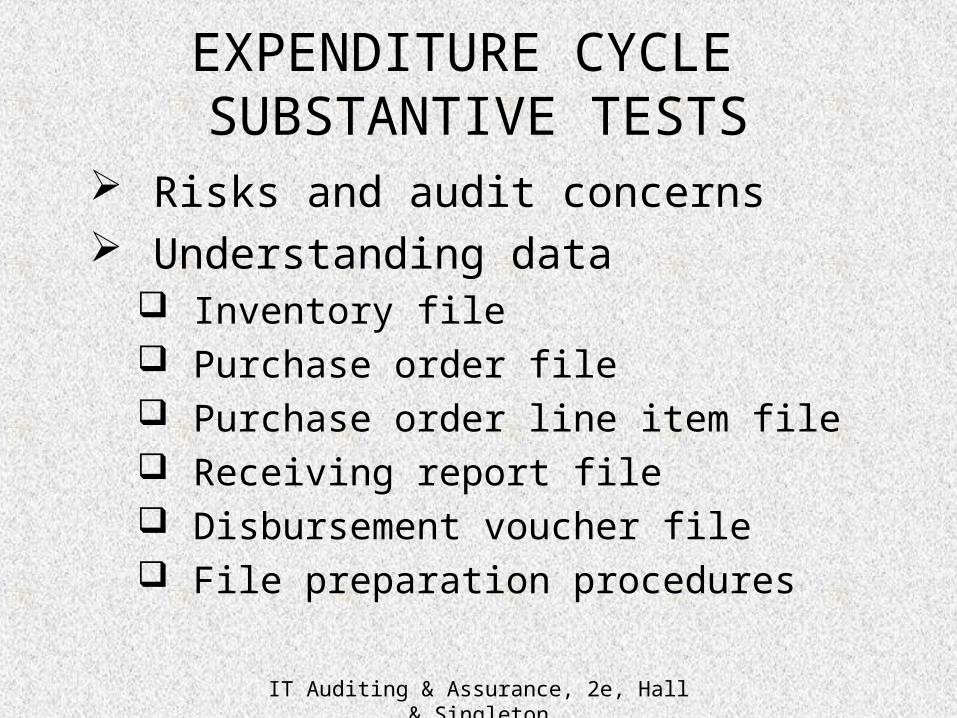

Risks and audit concerns Understanding data

Inventory file Purchase order file Purchase order line item file Receiving report file Disbursement voucher file File preparation procedures

EXPENDITURE CYCLE SUBSTANTIVE TESTS

IT Auditing & Assurance, 2e, Hall & Singleton

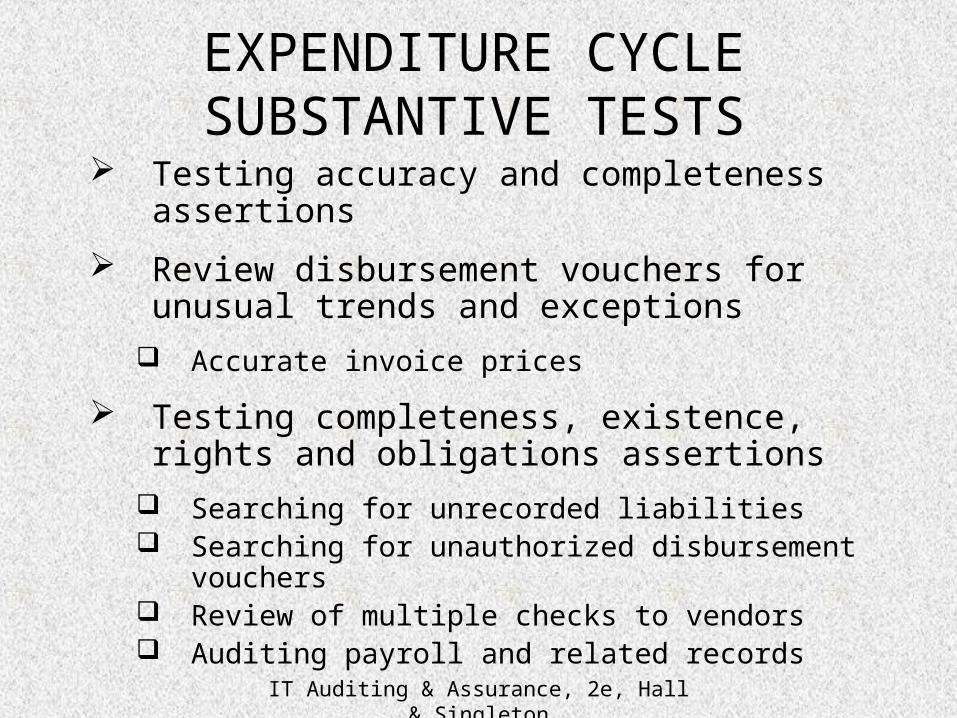

Testing accuracy and completeness assertions

Review disbursement vouchers for unusual trends and exceptions

Accurate invoice prices

Testing completeness, existence, rights and obligations assertions

Searching for unrecorded liabilities Searching for unauthorized disbursement vouchers Review of multiple checks to vendors Auditing payroll and related records

EXPENDITURE CYCLE SUBSTANTIVE TESTS

Chapter 10:Auditing the Expenditure

Cycle

IT Auditing & Assurance, 2e, Hall & Singleton