Ch 17 Hull Fundamentals 8 the d

32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull !"1# The Greek Letters Chapter 17 1

description

Hull Derivatives

Transcript of Ch 17 Hull Fundamentals 8 the d

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 1/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull !"1#

The Greek Letters

Chapter 17

1

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 2/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

Example (Page 365)

A bank has sold for $300,000 a European calloption on 100,000 shares of a non-dividend-paying stock

S 0 !", K #0, r #, σ %0,

T = %0 &eeks, µ 13 'he (lack-)choles-*erton value of the option

is $%!0,000 +o& does the bank hedge its risk

2

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 3/32

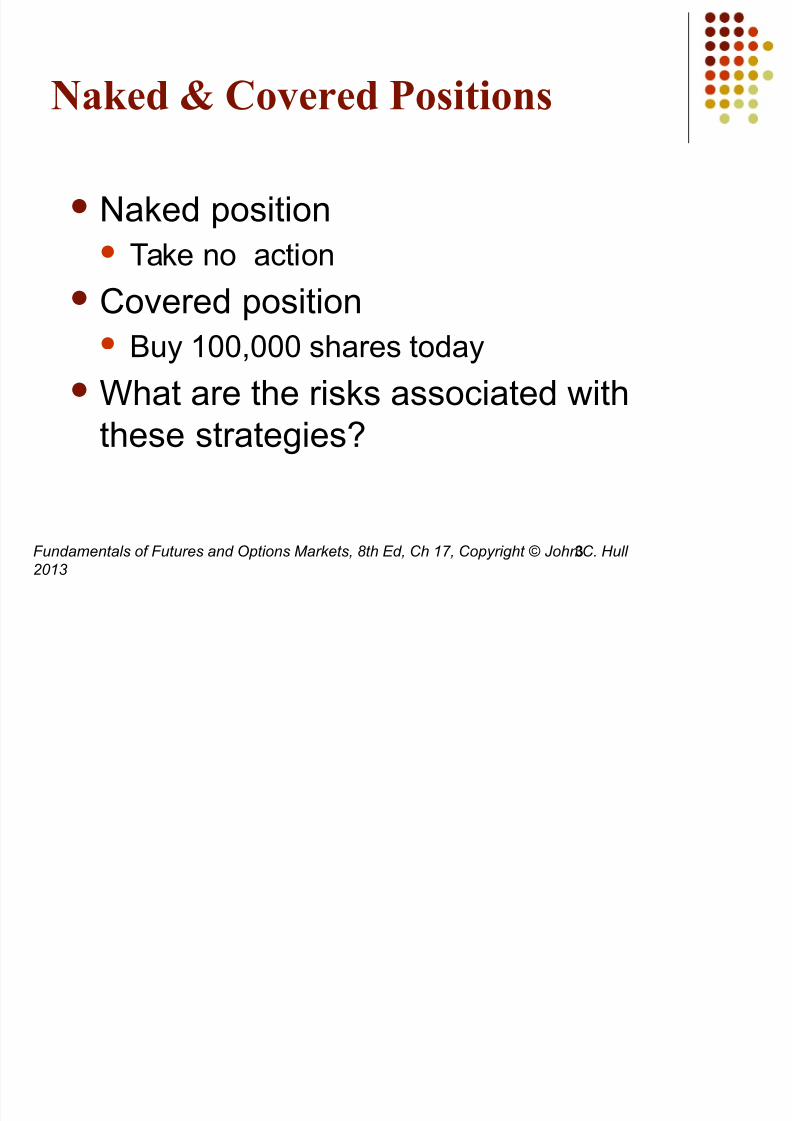

Naked & Covered Positions

aked position 'ake no action

Covered position (uy 100,000 shares today

.hat are the risks associated &iththese strategies

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

3

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 4/32

top!Loss trateg"

'his involves/

(uying 100,000 shares as soon as pricereaches $#0

)elling 100,000 shares as soon as pricefalls belo& $#0

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

4

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 5/32

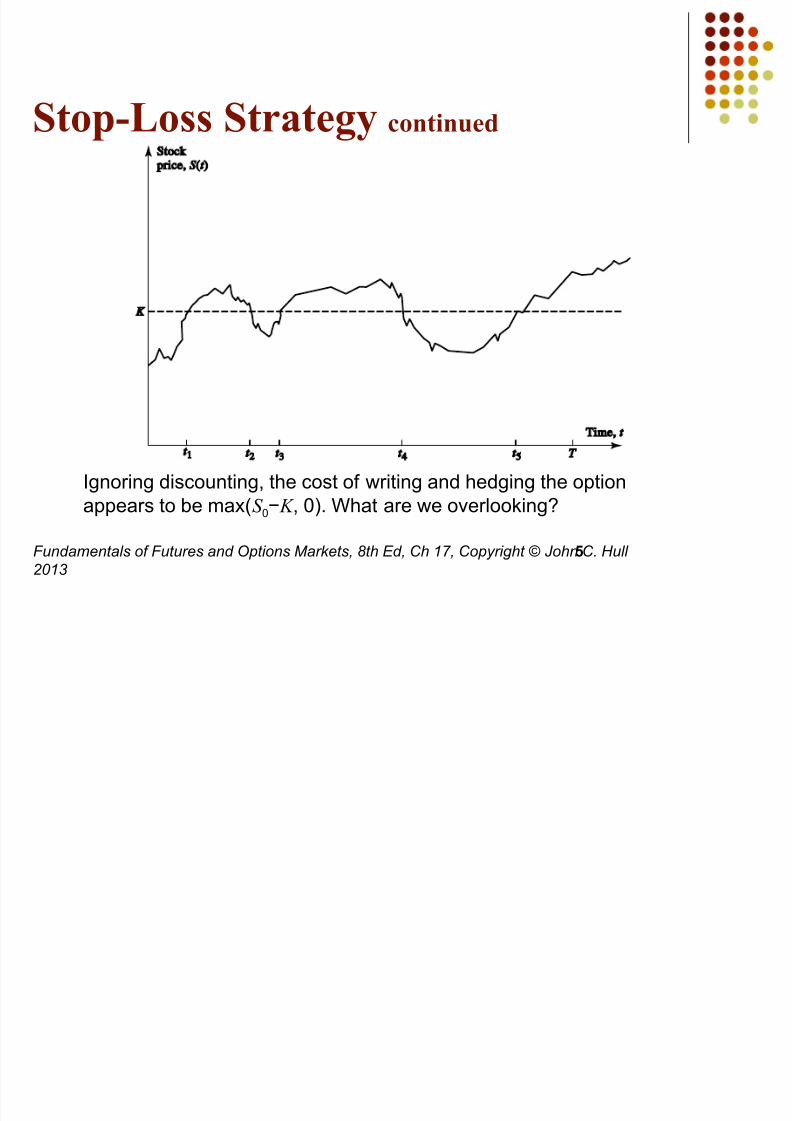

top!Loss trateg"#ontin$ed

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

5

gnoring discounting, the cost of &riting and hedging the optionappears to be a2S 04 K , 056 .hat are &e overlooking

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 6/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

%elta (ee ig$re '*+ page 36,)

elta ∆5 is the rate of change of theoption price &ith respect to the underlying

8ption

price

A

( )lope ∆ = 0.6

)tock price

6

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 7/32

-edge

'rader &ould be hedged &ith the position/ short 1000 options buy 900 shares

:ain;loss on the option position is offset byloss;gain on stock position

elta changes as stock price changes and tiepasses

+edge position ust therefore be rebalanced

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

7

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 8/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

%elta -edging

'his involves aintaining a delta neutralportfolio

'he delta of a European call on a non-dividend-paying stock is N (d 1)

'he delta of a European put on the stock is

[ N (d 1) – 1]

8

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 9/32

The Costs in %elta -edging

#ontin$ed

elta hedging a &ritten option involves

a <buy high, sell lo&= trading rule

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

9

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 10/32

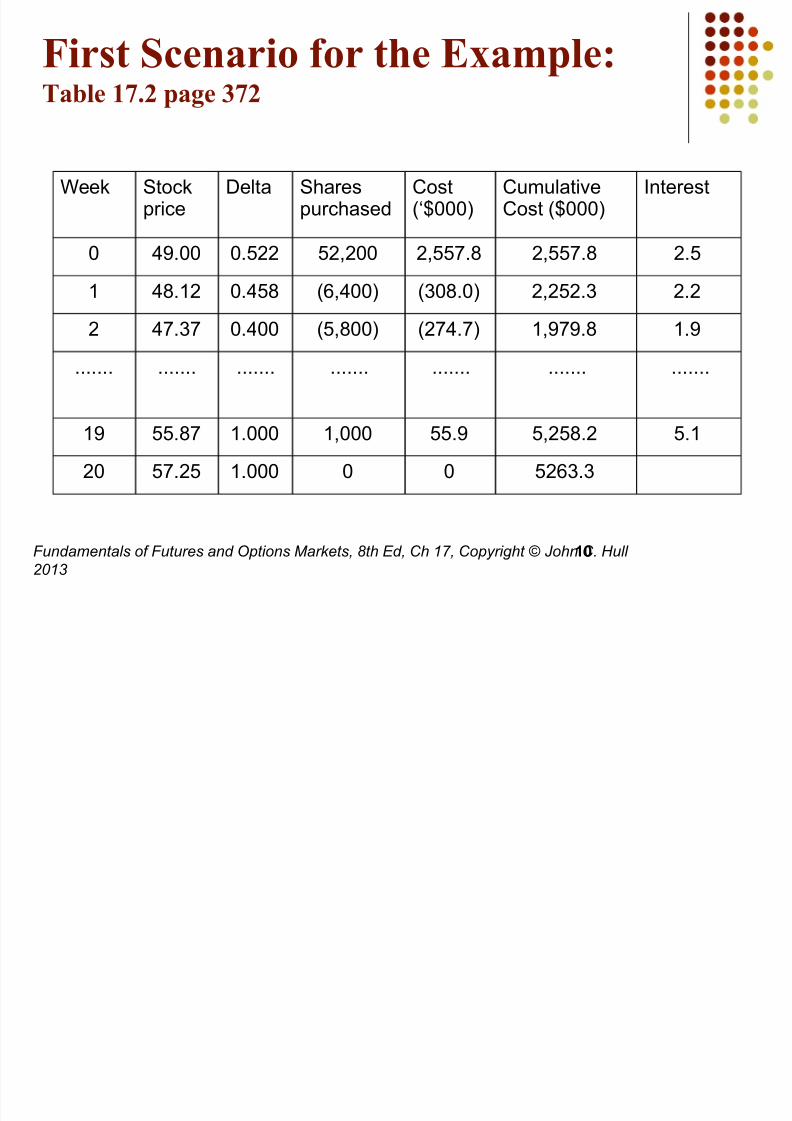

irst #enario .or the Example/Ta0le '* page 3*

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

.eek )tockprice

elta )harespurchased

Cost>$0005

CuulativeCost $0005

nterest

0 !"600 06#%% #%,%00 %,##76? %,##76? %6#

1 !?61% 06!#? 9,!005 30?605 %,%#%63 %6%

% !7637 06!00 #,?005 %7!675 1,"7"6? 16"

6666666 6666666 6666666 6666666 6666666 6666666 6666666

1" ##6?7 16000 1,000 ##6" #,%#?6% #61

%0 #76%# 16000 0 0 #%9363

10

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 11/32

e#ond #enario .or the Example

Ta0le '3 page 33

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

.eek )tockprice

elta )harespurchased

Cost>$0005

CuulativeCost $0005

nterest

0 !"600 06#%% #%,%00 %,##76? %,##76? %6#

1 !"67# 06#9? !,900 %%?6" %,7?"6% %67

% #%600 0670# 13,700 71%6! 3,#0!63 36!

6666666 6666666 6666666 6666666 6666666 6666666 6666666

1" !9693 06007 17,9005 ?%0675 %"060 063

%0 !?61% 06000 7005 33675 %#969

11

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 12/32

Theta

'heta Θ5 of a derivative or portfolio ofderivatives5 is the rate of change of thevalue &ith respect to the passage of tie

'he theta of a call or put is usuallynegative6 'his eans that, if tie passes&ith the price of the underlying asset andits volatility reaining the sae, the value

of a long call or put option declines

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

12

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 13/32

Theta .or Call 1ption/ S 2 K 52+

*54+ r 54+ T '

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

13

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 14/32

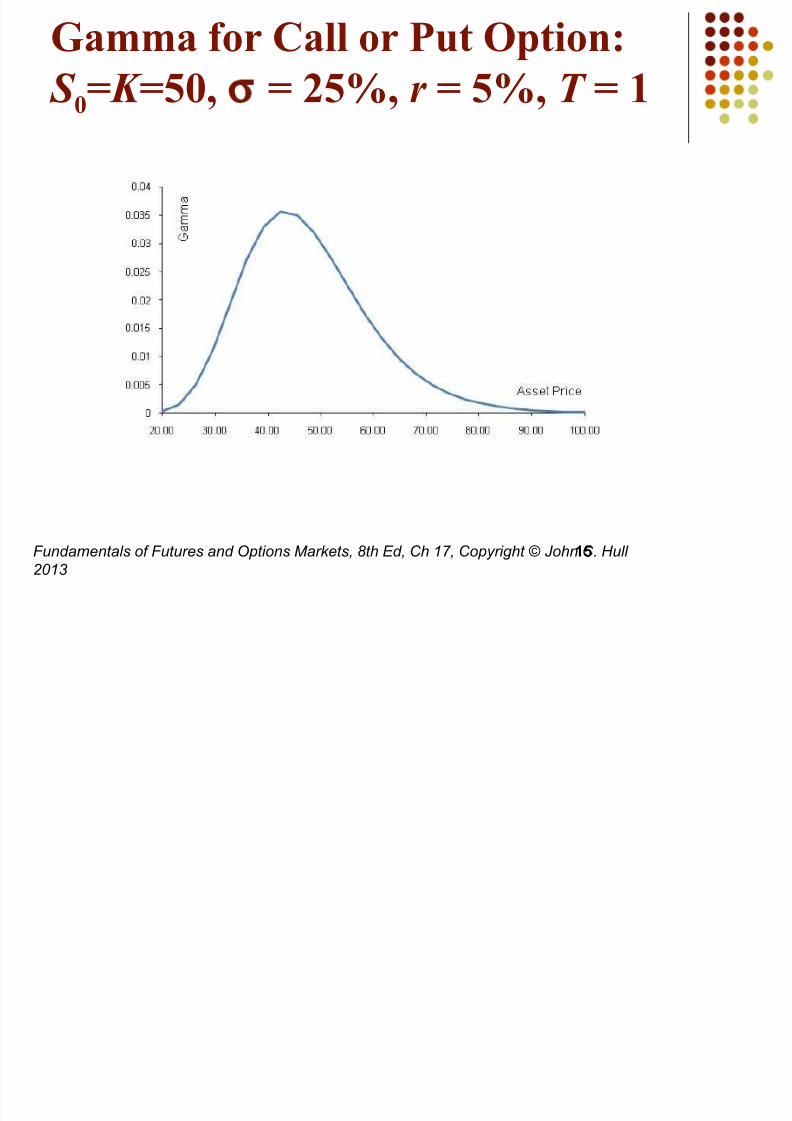

Gamma

:aa Γ 5 is the rate of change ofdelta ∆5 &ith respect to the price of

the underlying asset:aa is greatest for options that

are close to the oney

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

14

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 15/32

Gamma .or Call or P$t 1ption/

S 2 K 52+ *54+ r 54+ T '

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

15

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 16/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

Gamma ddresses %elta -edging

Errors Ca$sed " C$rvat$re(ig$re '+ page 3)

)

C)tock price

)@

Callprice

C@

C@@

16

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 17/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

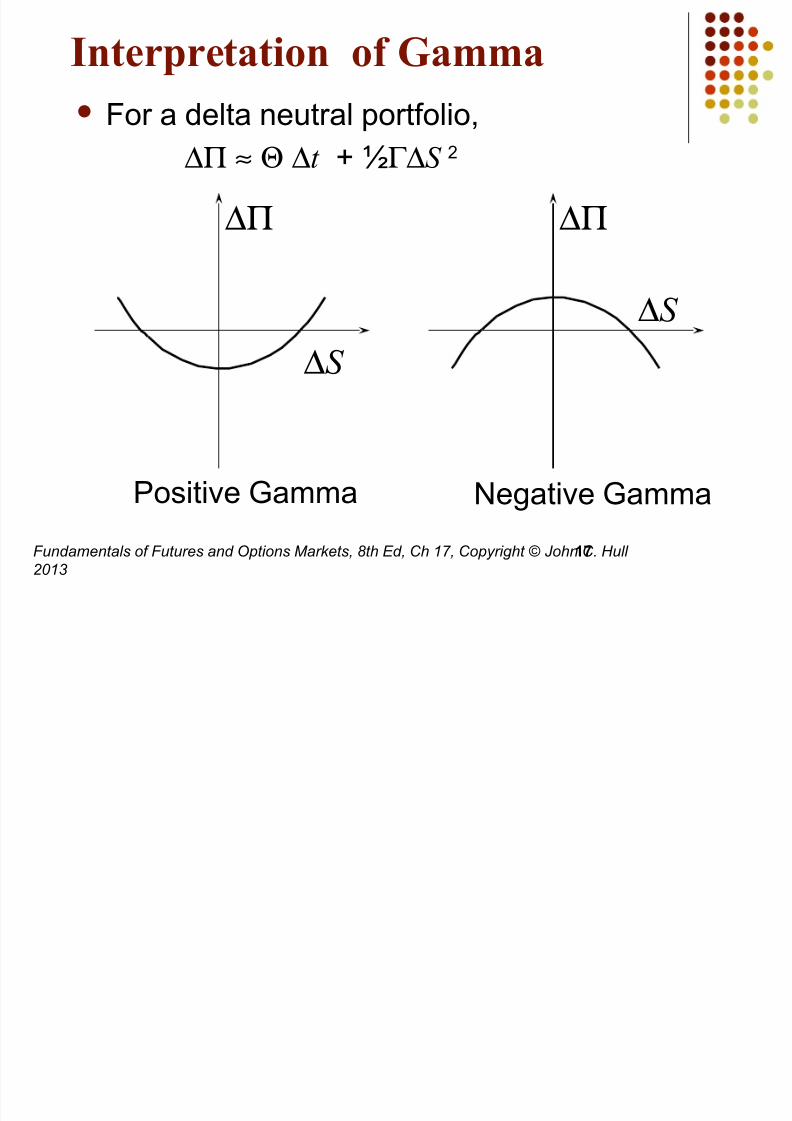

7nterpretation o. Gamma

or a delta neutral portfolio,

∆Π ≈ Θ ∆t B Γ∆S %

∆Π

∆S

egative :aa

∆Π

∆S

Dositive :aa

17

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 18/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

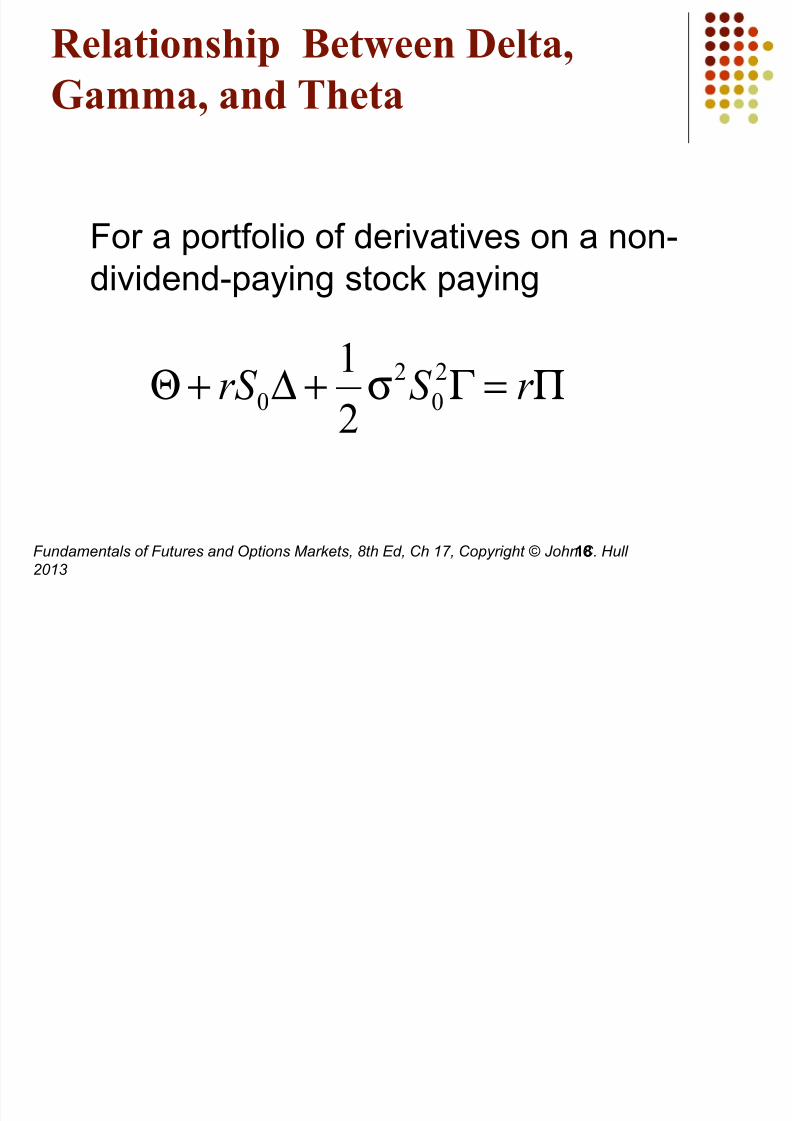

8elationship et9een %elta+

Gamma+ and Theta

or a portfolio of derivatives on a non-

dividend-paying stock paying

18

Π=Γ σ+∆+Θ r S rS 2

0

2

0

2

1

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 19/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

:ega

ega ν5 is the rate of change of the

value of a derivatives portfolio &ith

respect to volatility

19

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 20/32

:ega .or Call or P$t 1ption/

S 2 K 52+ *54+ r 54+ T '

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

20

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 21/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

;anaging %elta+ Gamma+ &

:ega

elta can be changed by taking aposition in the underlying asset

'o adFust gaa and vega it isnecessary to take a position in anoption or other derivative

21

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 22/32

Example

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

22

$elta %amma &ega

Dortfolio 0 4#000 4?000

8ption 1 069 06# %60

8ption % 06# 06? 16%

.hat position in option 1 and the underlying asset &illake the portfolio delta and gaa neutral Ans&er/Gong 10,000 options, short 9000 of the asset

.hat position in option 1 and the underlying asset &illake the portfolio delta and vega neutral Ans&er/ Gong!000 options, short %!00 of the asset

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 23/32

Example #ontin$ed

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

23

$elta %amma &ega

Dortfolio 0 4#000 4?000

8ption 1 069 06# %60

8ption % 06# 06? 16%

.hat position in option 1, option %, and the asset &ill ake theportfolio delta, gaa, and vega neutral.e solve

4#000B06#w1 B06?w2 04?000B%60w1 B16%w2 0

to get w1 !00 and w2 90006 .e reHuire long positions of !00 and

9000 in option 1 and option %6 A short position of 3%!0 in the asset isthen reHuired to ake the portfolio delta neutral

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 24/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

8ho

Iho is the rate of change of thevalue of a derivative &ith respectto the interest rate

24

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 25/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

-edging in Pra#ti#e

'raders usually ensure that their portfoliosare delta-neutral at least once a day

.henever the opportunity arises, theyiprove gaa and vega As portfolio becoes larger hedging

becoes less e2pensive

25

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 26/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

#enario nal"sis

A scenario analysis involves testing theeffect on the value of a portfolio ofdifferent assuptions concerning assetprices and their volatilities

26

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 27/32

Greek Letters .or E$ropean 1ptions on an sset that Provides a <ield at 8ate q (Ta0le '6+ page 3=6)

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1# 27

%reek 'etter Call Option (ut Option

elta:aa

'heta

ega

Iho

)( 1d N e qT −

T S

ed N qT

σ 0

1)( −′

T S

ed N qT

σ 0

1)( −′

[ ]1)( 1 −−

d N e qT

( ))()(

2)(

210

10

d N rKeed N qS

T ed N S

rT qT

qT

−−

−

−+

′− σ ( ))()(

2)(

210

10

d N rKeed N qS

T ed N S

rT qT

qT

−+−−

′−

−−

−σ

qT ed N T S −′ )( 10

qT ed N T S −′ )( 10

)( 2d N KTe rT −)( 2d N KTe rT −− −

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 28/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

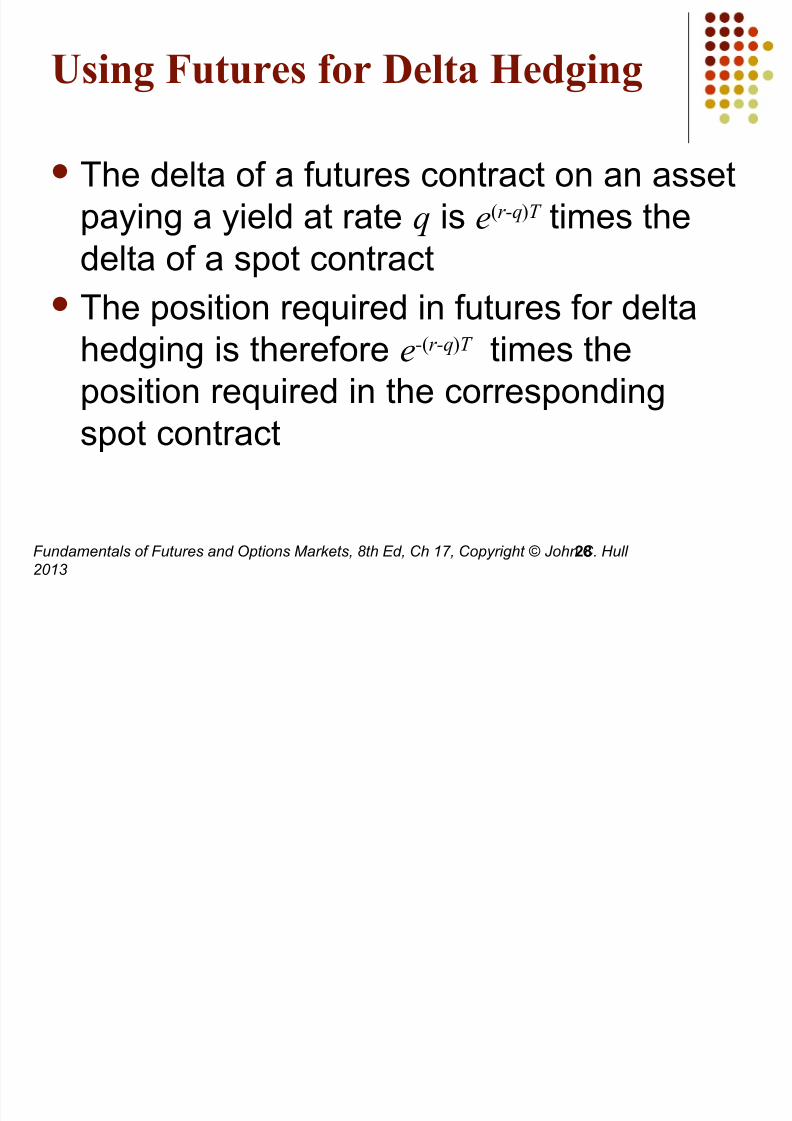

>sing $t$res .or %elta -edging

'he delta of a futures contract on an assetpaying a yield at rate q is e(r-q)T ties thedelta of a spot contract

'he position reHuired in futures for deltahedging is therefore e-(r-q)T ties theposition reHuired in the correspondingspot contract

28

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 29/32

-edging vs Creation o. an 1ption

"ntheti#all"

.hen &e are hedging &e takepositions that offset delta,

gaa, vega, etc.hen &e create an option

synthetically &e take positions

that atch delta, gaa, vega,etc

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

29

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 30/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

Port.olio 7ns$ran#e

n 8ctober of 1"?7 any portfolioanagers attepted to create a putoption on a portfolio synthetically

'his involves initially selling enough ofthe portfolio or of inde2 futures5 toatch the ∆ of the put option

30

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 31/32

Fundamentals of Futures and Options Markets, 8th Ed, Ch 17, Copyright © John C. ull!"1#

Port.olio 7ns$ran#e

#ontin$ed

As the value of the portfolio increases, the∆ of the put becoes less negative andsoe of the original portfolio isrepurchased

As the value of the portfolio decreases,the ∆ of the put becoes ore negativeand ore of the portfolio ust be sold

31

7/21/2019 Ch 17 Hull Fundamentals 8 the d

http://slidepdf.com/reader/full/ch-17-hull-fundamentals-8-the-d 32/32

Fundamentals of Futures and Options Markets 8th Ed Ch 17 Copyright © John C ull!"1#

Port.olio 7ns$ran#e

#ontin$ed

'he strategy did not &ork &ell on 8ctober

1", 1"?7666

32