CFO Forumwebserver.pwc.lu/StaticContent/ClientsSurveyDOC/CFO_Forum_170615... · • Stand-alone...

40

www.pwc.lu 17 June 2015 CFO Forum

Transcript of CFO Forumwebserver.pwc.lu/StaticContent/ClientsSurveyDOC/CFO_Forum_170615... · • Stand-alone...

www.pwc.lu

17 June 2015

CFO Forum

PwC

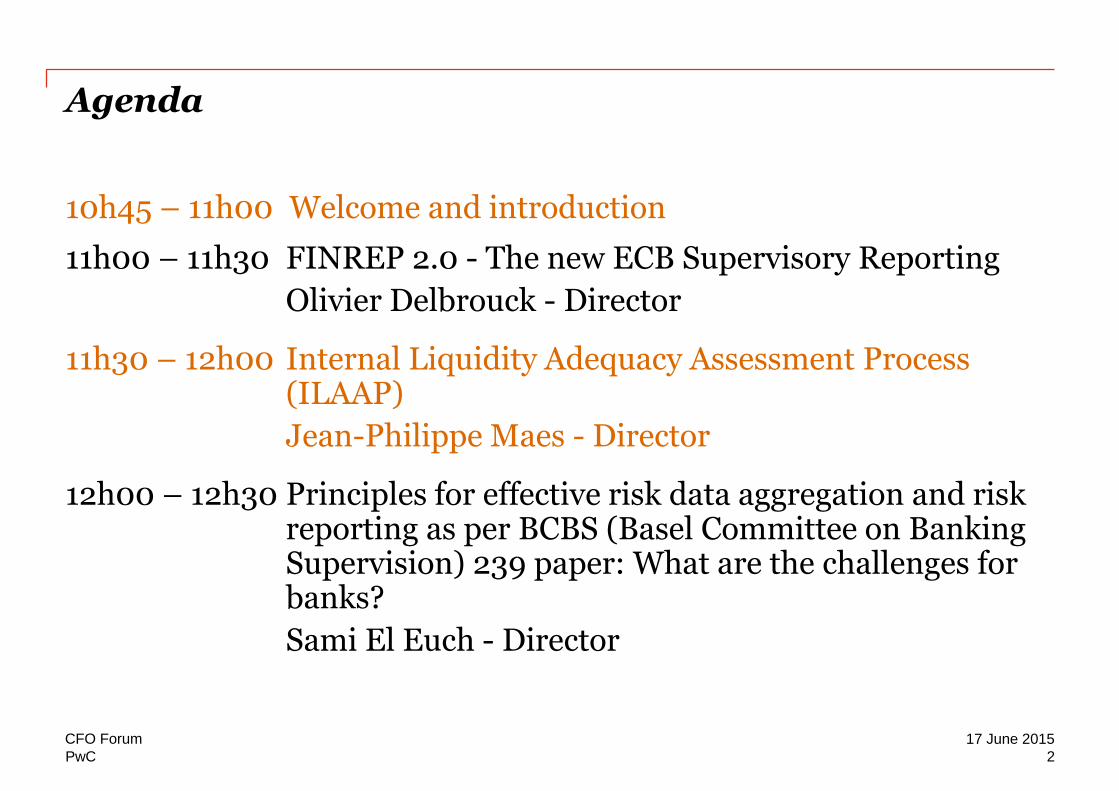

Agenda

10h45 – 11h00 Welcome and introduction

11h00 – 11h30 FINREP 2.0 - The new ECB Supervisory Reporting

Olivier Delbrouck - Director

11h30 – 12h00 Internal Liquidity Adequacy Assessment Process (ILAAP)

Jean-Philippe Maes - Director

12h00 – 12h30 Principles for effective risk data aggregation and risk reporting as per BCBS (Basel Committee on Banking Supervision) 239 paper: What are the challenges for banks?

Sami El Euch - Director

2

17 June 2015 CFO Forum

CFO Forum FINREP 2.0

www.pwc.lu

PwC

FINREP - Actual reporting requirements

CSSF Circular 14/593 as amended by the CSSF Circular 15/613

(published on 27 October 2014)

• Stand alone and consolidated reporting need to be distinguished.

Stand alone reporting Consolidated reporting

Partially in the scope of the CRR 575/2013

In scope of the CRR 575/2013

CSSF requirements still applicable*

* Tables B1.1, B1.6, B2.1 and B2.5 (including new reporting concerning “Forbearance and non-performing exposures” (CRR - Art. 199(4))

Requirements of the Regulation 680/2014 are applicable

4

17 June 2015 CFO Forum

PwC

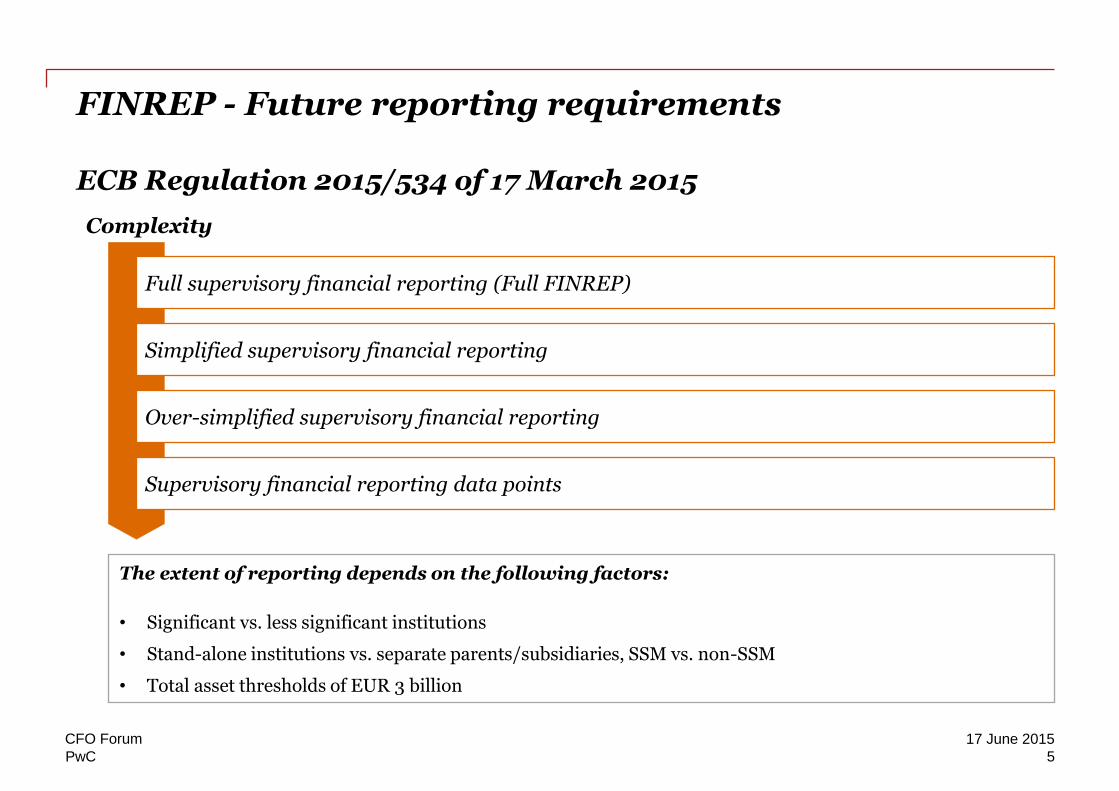

Complexity

Full supervisory financial reporting (Full FINREP)

Simplified supervisory financial reporting

Over-simplified supervisory financial reporting

Supervisory financial reporting data points

The extent of reporting depends on the following factors:

• Significant vs. less significant institutions

• Stand-alone institutions vs. separate parents/subsidiaries, SSM vs. non-SSM

• Total asset thresholds of EUR 3 billion

FINREP - Future reporting requirements ECB Regulation 2015/534 of 17 March 2015

CFO Forum

5

17 June 2015

PwC

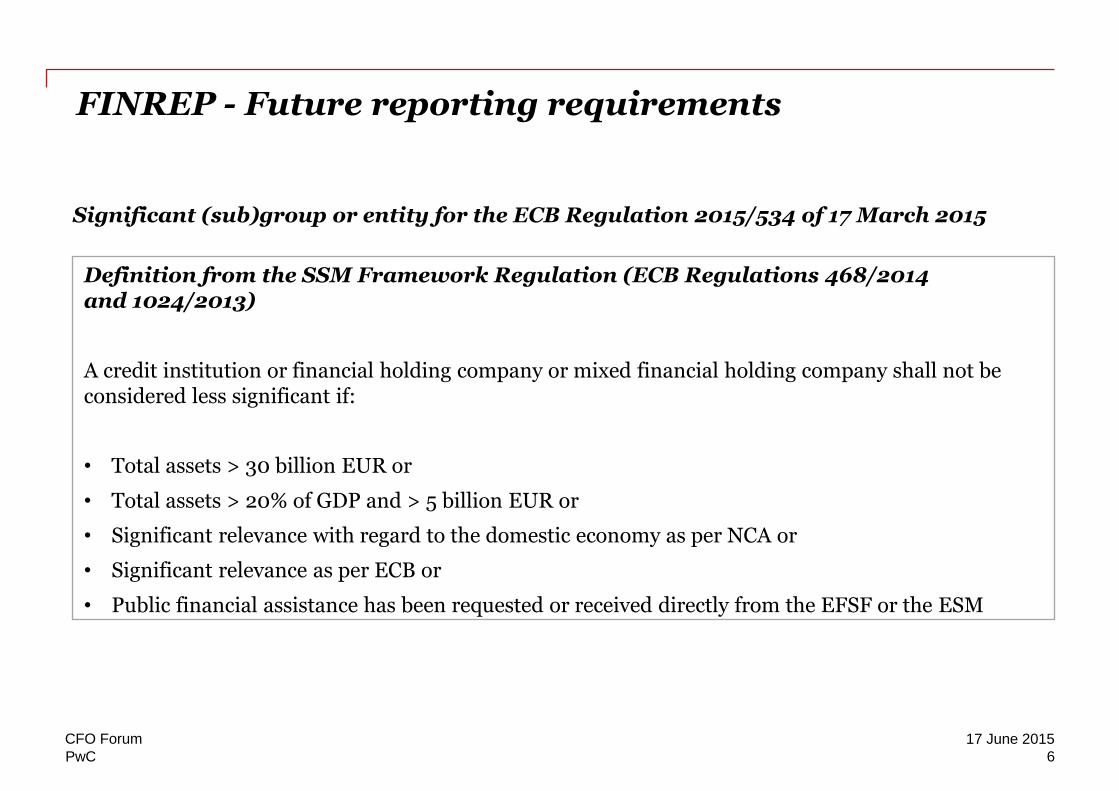

Significant (sub)group or entity for the ECB Regulation 2015/534 of 17 March 2015

Definition from the SSM Framework Regulation (ECB Regulations 468/2014 and 1024/2013)

A credit institution or financial holding company or mixed financial holding company shall not be considered less significant if:

• Total assets > 30 billion EUR or

• Total assets > 20% of GDP and > 5 billion EUR or

• Significant relevance with regard to the domestic economy as per NCA or

• Significant relevance as per ECB or

• Public financial assistance has been requested or received directly from the EFSF or the ESM

FINREP - Future reporting requirements

CFO Forum

6

17 June 2015

PwC

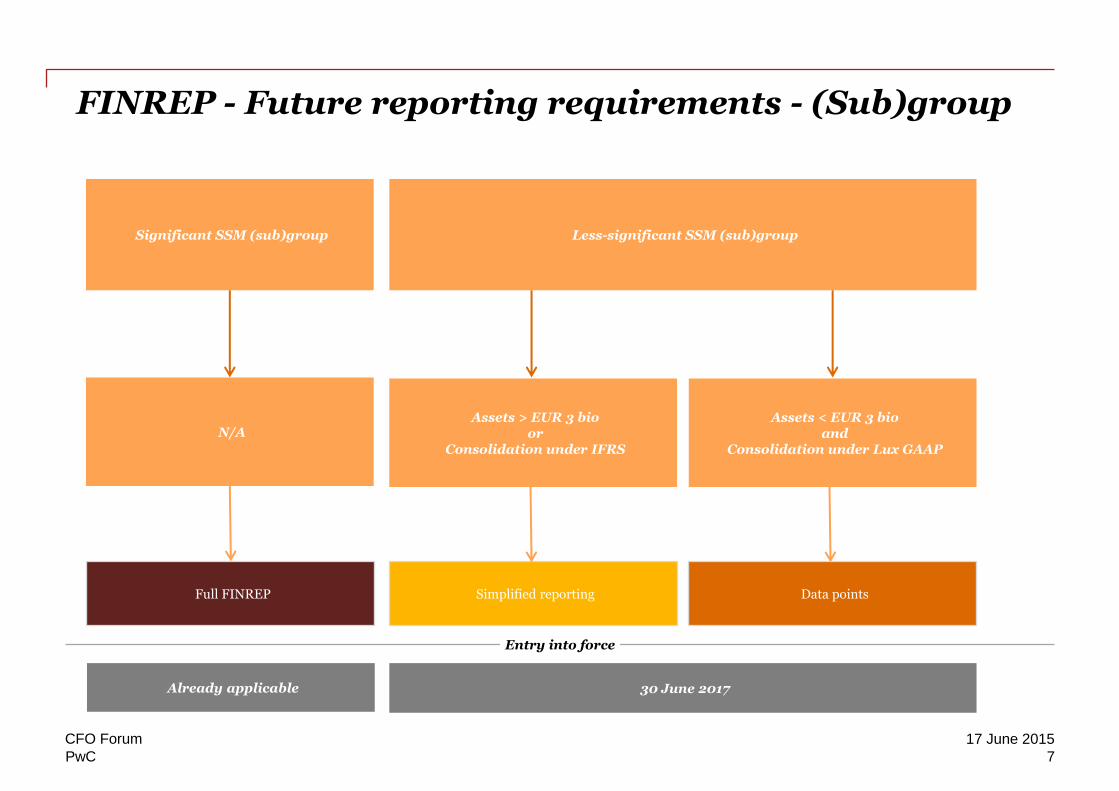

FINREP - Future reporting requirements - (Sub)group

Already applicable 30 June 2017

Full FINREP Data points

Significant SSM (sub)group

Simplified reporting

Entry into force

Less-significant SSM (sub)group

Assets > EUR 3 bio or

Consolidation under IFRS

Assets < EUR 3 bio and

Consolidation under Lux GAAP

N/A

CFO Forum

7

17 June 2015

PwC

FINREP - Future reporting requirements - Standalone

31 December 2015 30 June 2017 30 June 2016

Full FINREP Simplified reporting

Entry into force

Significant SSM entity

Not included in a SSM (sub)group

Over-simplified reporting

Not included in a significant

SSM (sub)group

Included in a significant SSM

(sub)group

Less-significant SSM entity

Assets > EUR 3 bio

Assets < EUR 3 bio

Data points

Assets > EUR 3 bio

Included in a less-significant SSM (sub)group

Assets < EUR 3 bio

Data points

CFO Forum

8

17 June 2015

PwC

31 December 2015 30 June 2016

Full FINREP None

Significant branch of non-SSM bank

Over-simplified reporting

Entry into force

Non-SSM subsidiaries of significant SSM (sub)group

N/A

Assets > EUR 3 bio Assets < EUR 3 bio Assets > EUR 3 bio Assets < EUR 3 bio

Less-significant branch of non-SSM bank

Simplified reporting None

N/A 30 June 2017

CFO Forum

9

17 June 2015

FINREP - Future reporting requirements -

Branch/Subsidiaries

PwC

FINREP - Reporting templates

Over-simplified + Simplified + Full FINREP

Full FINREP All reportings Simplified + Full FINREP

Part 2 Quarterly Reporting (if above thresholds)

Part 1 Quarterly Reporting

Breakdown of financial assets by instrument and by

counterparty sector (4)

Statement of comprehensive

income (3)

Assets (1.1 )

Liabilities (1.2)

Statement of profit or loss

(2)

Equity (1.3)

Breakdown of loans and advances by

product (5)

Breakdown of loans and advances to non-financial corporations

by NACE codes (6)

Financial assets subject to impairment

that are past due or impaired

(7)

Breakdown of financial liabilities

(8)

Loan commitments, financial guarantees

and other commitments given

(9.1)

Derivatives – Trading (10)

Derivatives – Hedge Accounting

(11)

Movements in allowances for credit

losses and impair-ment of equity

instruments (12)

Collateral and guarantees received

(13)

Fair value hierarchy: financial instruments

at fair value (14)

Derecognition and financial liabilities

associated with transferred financial

assets (15)

Some breakdown of selected statement of

profit or loss items (16.1 and 16.3)

Forborne exposures (19)

Reconciliation between accounting and CRR scope of

consolidation (17)

Performing and non-performing exposures

(18)

Tangible assets and intangible assets: assets subject to operating lease

(21)

Asset management, custody and other service functions

(22)

Some geographical Breakdown

(20.1 to 20.3 and 20.7)

Loan commitments, financial guarantees

and other commitments received

(9.2)

Some breakdown of selected statement of

profit or loss items (16.2 and 16.4 to 16.7)

Some geographical Breakdown

(20.4 to 20.6)

Part 3 Semi-annually Reporting

Part 4 Annually Reporting

Group structure by entity (40.1)

Off-balance sheet activities: interests in

unconsolidated structured entities

(30)

Related parties (31)

Group structure by entity (40.1)

Group structure by instrument (40.2)

Fair value (41)

Tangible and intangible assets:

carrying amount by measurement method

(42)

Provisions (43)

Defined benefit plans and employee benefits

(44)

Breakdown of selected items of statement of

profit or loss (45)

Statement of changes in equity

(46)

CFO Forum

10

17 June 2015

CFO Forum

11

17 June 2015

PwC

CFO Forum Key features of an ILAAP

www.pwc.lu

1. From SSM to ILAAP

CFO Forum

13

17 June 2015

PwC

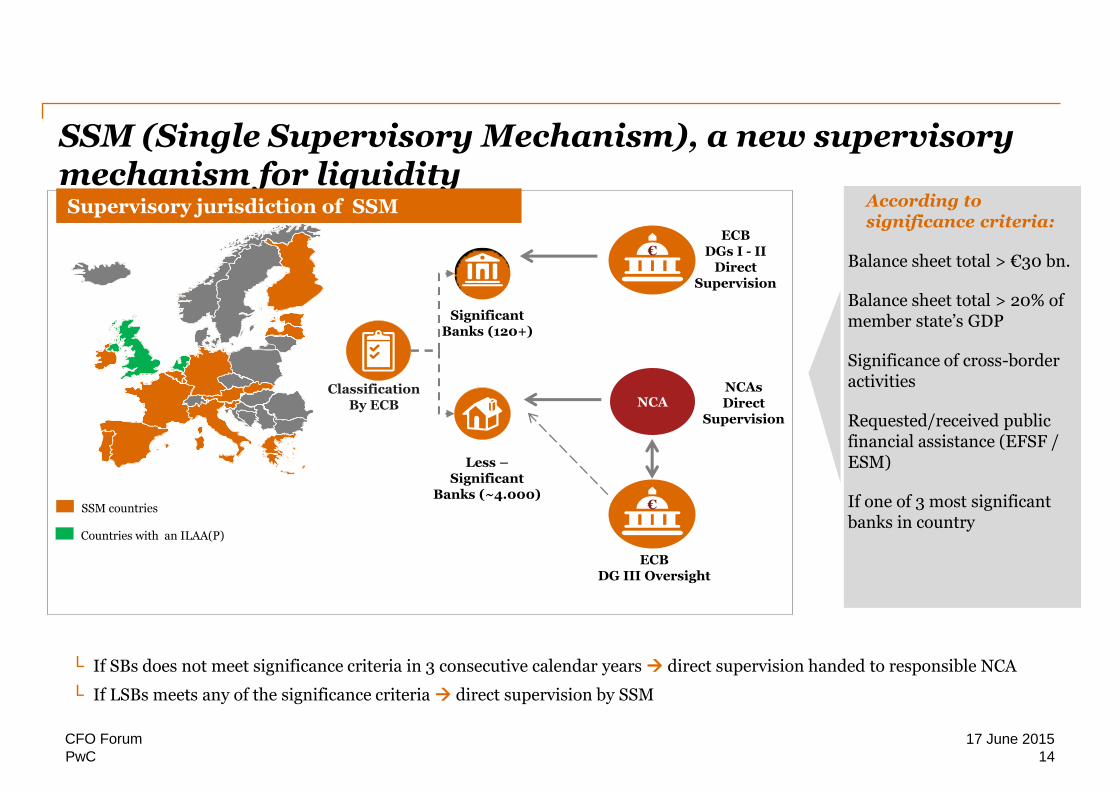

SSM (Single Supervisory Mechanism), a new supervisory mechanism for liquidity

SSM countries

According to significance criteria:

Balance sheet total > €30 bn.

Balance sheet total > 20% of member state’s GDP

Significance of cross-border activities

Requested/received public financial assistance (EFSF / ESM)

If one of 3 most significant banks in country

Supervisory jurisdiction of SSM

Significant Banks (120+)

Less –Significant

Banks (~4.000)

Classification By ECB

└ If SBs does not meet significance criteria in 3 consecutive calendar years direct supervision handed to responsible NCA

└ If LSBs meets any of the significance criteria direct supervision by SSM

€ ECB

DGs I - II Direct

Supervision

NCA

€

ECB DG III Oversight

NCAs Direct

Supervision

Countries with an ILAA(P)

CFO Forum

14

17 June 2015

PwC

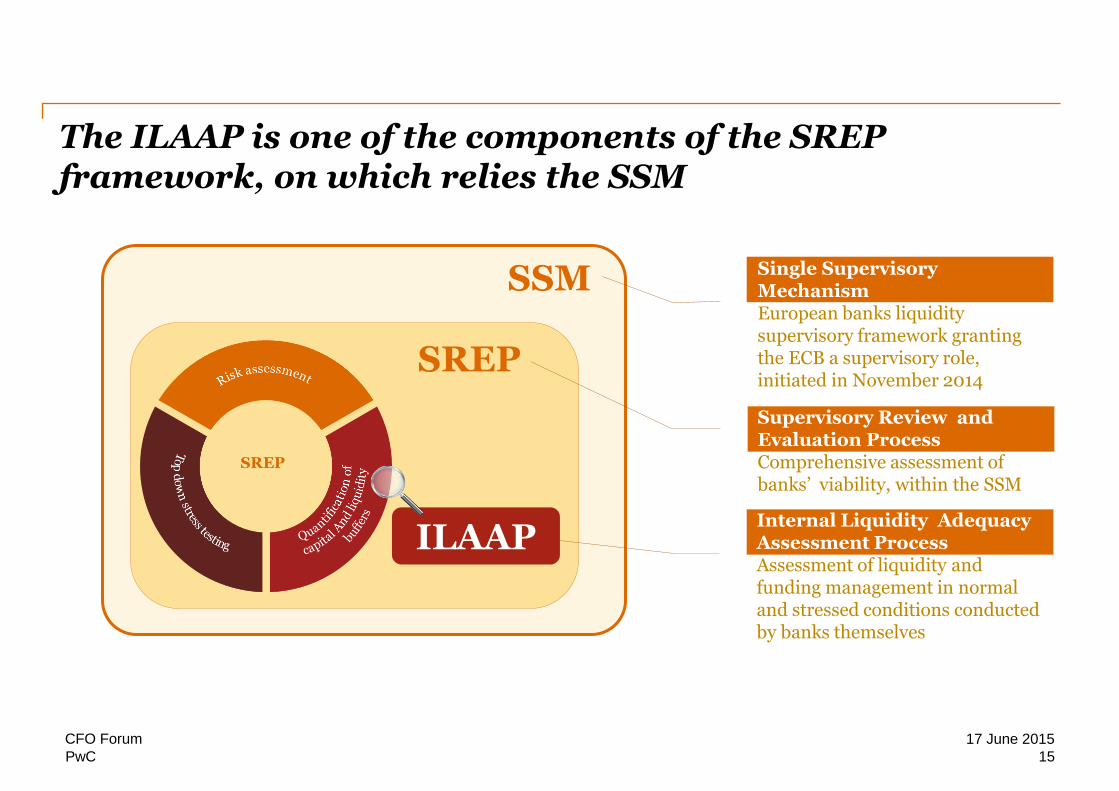

SSM

SREP

The ILAAP is one of the components of the SREP framework, on which relies the SSM

ILAAP

Single Supervisory Mechanism European banks liquidity supervisory framework granting the ECB a supervisory role, initiated in November 2014

Supervisory Review and Evaluation Process Comprehensive assessment of banks’ viability, within the SSM

Internal Liquidity Adequacy Assessment Process Assessment of liquidity and funding management in normal and stressed conditions conducted by banks themselves

PwC

CFO Forum 17 June 2015

15

PwC

The ILAAP, a key pillar of the SREP framework

The SREP aims to form a comprehensive, holistic view on the risk profile and viability of the institution in order to steer the SSM supervision scope, frequency and intensity and to define early intervention measures to address concerns if necessary.

Main SREP components

SREP outcomes

Categorisation of institutions

Monitoring of key indicators

Business Model AnalysisAssessment of internal

governance and institution-wide controls

Assessment of risk capital

Assessment of inherent risks and controls

Stress testing

Capital adequacy assessment

Assessment of risks to liquidity and funding

Supervisory Measures

Assessment of risks to liquidity and funding

Stress testing

Liquidity adequacy assessment

Quantitative capital measures Quantitative liquidity measures Other supervisory measures

Early intervention measures

Overall SREP assessment

Liquidity & funding risk within the

SREP

16

17 June 2015 CFO Forum

PwC

SREP liquidity assessment framework: Overview

ILAAP Process

Assessment of inherent liquidity Risk

Assessment of inherent funding risk

Assessment of risk management and controls

Assessment of liquidity adequacy

Quantitative and qualitative assessment of the short and medium term liquidity risk and the quality of assets that should be held by the institution to meet its liquidity needs under normal and stressed conditions

Deal with the assessment of the funding risk with a focus on the funding plan and funding instruments. Their ability to allow the institution to meet its obligations, as well as their diversity and stability under normal and stressed conditions will be assessed.

Assessment of the liquidity and funding risks management frameworks including related policies, procedures and their implementation and whether an appropriate level of liquid assets is provisioned to cover these risks in case of an adverse event.

Definition whether the Bank retains a sufficient level of own funds to cover its risks, current or future, in normal and stressed conditions, or if corrective measures are required. This dimension assesses the reliability of methodologies used.

1

2

3

4

17

17 June 2015 CFO Forum

2. ILAAP insights

CFO Forum

18

17 June 2015

PwC

PwC

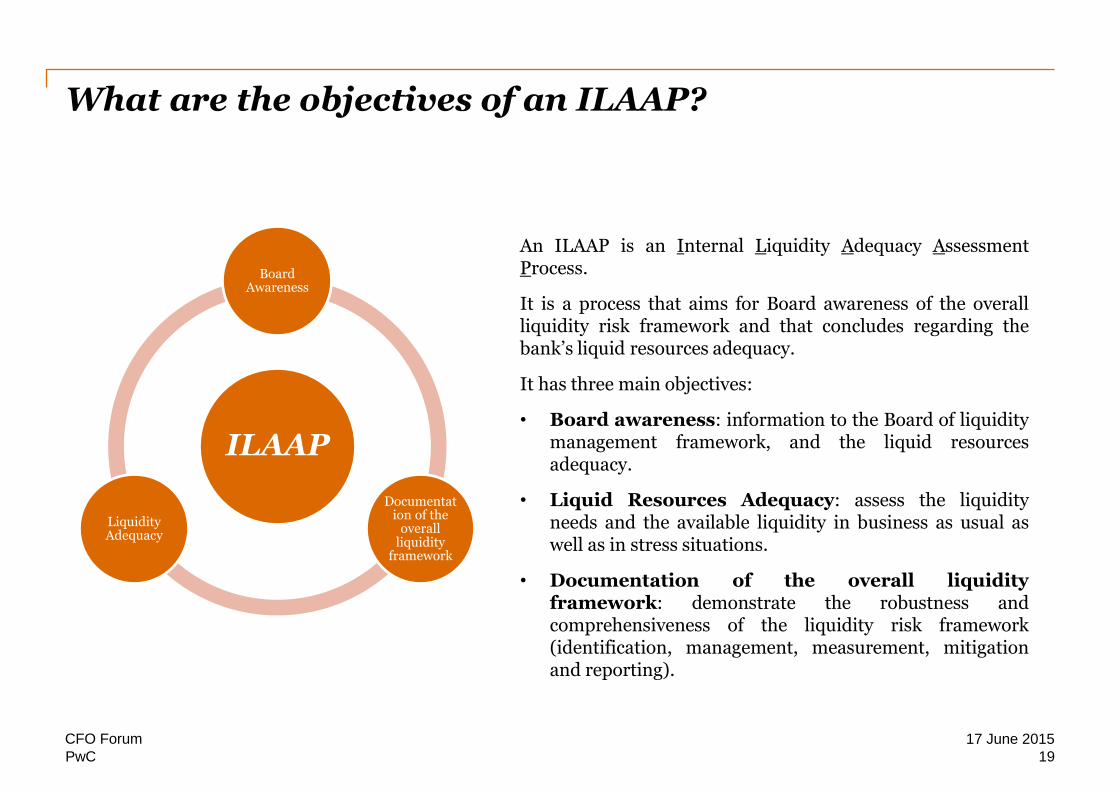

What are the objectives of an ILAAP?

ILAAP

Board Awareness

Documentation of the

overall liquidity

framework

Liquidity Adequacy

An ILAAP is an Internal Liquidity Adequacy Assessment Process.

It is a process that aims for Board awareness of the overall liquidity risk framework and that concludes regarding the bank’s liquid resources adequacy.

It has three main objectives:

• Board awareness: information to the Board of liquidity management framework, and the liquid resources adequacy.

• Liquid Resources Adequacy: assess the liquidity needs and the available liquidity in business as usual as well as in stress situations.

• Documentation of the overall liquidity framework: demonstrate the robustness and comprehensiveness of the liquidity risk framework (identification, management, measurement, mitigation and reporting).

19

17 June 2015 CFO Forum

PwC

SREP liquidity assessment framework: Overview A bank should establish a robust ILAAP process, supported by an adequate liquidity risk

management framework, that ensures it maintains sufficient liquidity, including a cushion of unencumbered, high quality liquid assets, to withstand a range of stress events, including those involving the loss or impairment of both unsecured and secured funding sources.

20

17 June 2015 CFO Forum

PwC

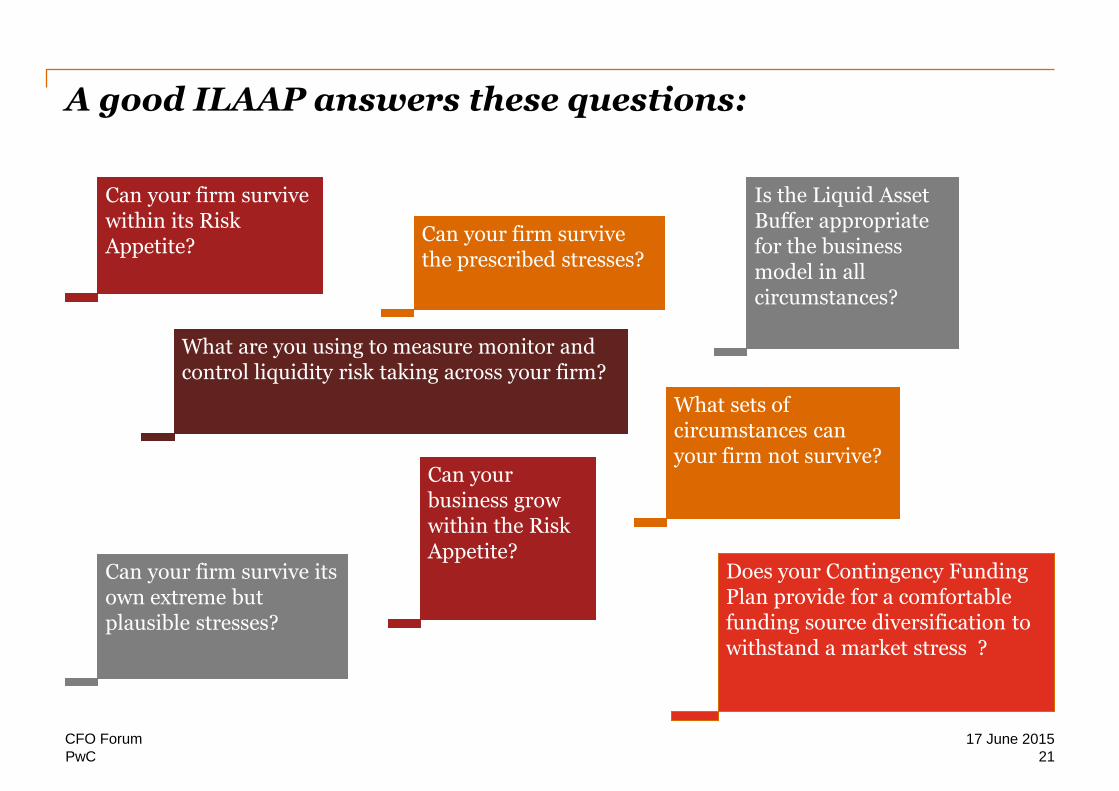

A good ILAAP answers these questions:

Can your firm survive within its Risk Appetite?

Can your firm survive the prescribed stresses?

Can your firm survive its own extreme but plausible stresses?

Is the Liquid Asset Buffer appropriate for the business model in all circumstances?

What are you using to measure monitor and control liquidity risk taking across your firm?

Can your business grow within the Risk Appetite?

What sets of circumstances can your firm not survive?

Does your Contingency Funding Plan provide for a comfortable funding source diversification to withstand a market stress ?

21

17 June 2015 CFO Forum

PwC

Illustration - ILAAP documentation Plan

• Executive summary

• Background: business model, current and future liquidity position

• Governance Structure

• Risk Tolerance

• Organisation

• Risk identification (intraday, FX, ST liquidity, MLT Funding…)

• Liquidity risk management framework:

o Overall approach to managing liquidity risk

o Measurement (regulatory and internal indicators) and Limits

o Mitigation techniques

• Contingency Funding Plan (‘CFP’) or ‘Liquidity Recovery Plans’:

o Roles and responsibilities

o Invocation procedures

o Management actions

• Stress testing:

o Regulatory stress test

o Internal / bespoke stress tests

• Conclusion regarding Adequacy

Expected ILAAP Documentation Plan

A key deliverable of an ILAAP is the report aimed at the Board, that presents the overall liquidity risk framework and concludes regarding the adequacy of the available liquid resources given the institution’s risk profile.

22

17 June 2015 CFO Forum

PwC

Contacts

Jean-Philippe Maes PwC Luxembourg Director

2, rue Gerhard Mercator B.P. 1443, L-1014 Luxembourg

Telephone: +352 49 48 48 2874 E-mail: [email protected]

Emmanuelle Henniaux PwC Luxembourg Partner

2, rue Gerhard Mercator B.P. 1443, L-1014 Luxembourg

Telephone: +352 49 48 48 2111 E-mail: [email protected]

23

17 June 2015 CFO Forum

PwC

CFO Forum

24

17 June 2015

BCBS 239 - Risk Data Aggregation and Reporting

What are the challenges?

www.pwc.lu

17 June 2015

Agenda

Introduction

What’s BCBS 239?

What are the challenges?

How to achieve compliance?

Project interdependencies – ex. AnaCredit

Conclusion

26 17 June 2015 CFO Forum

PwC

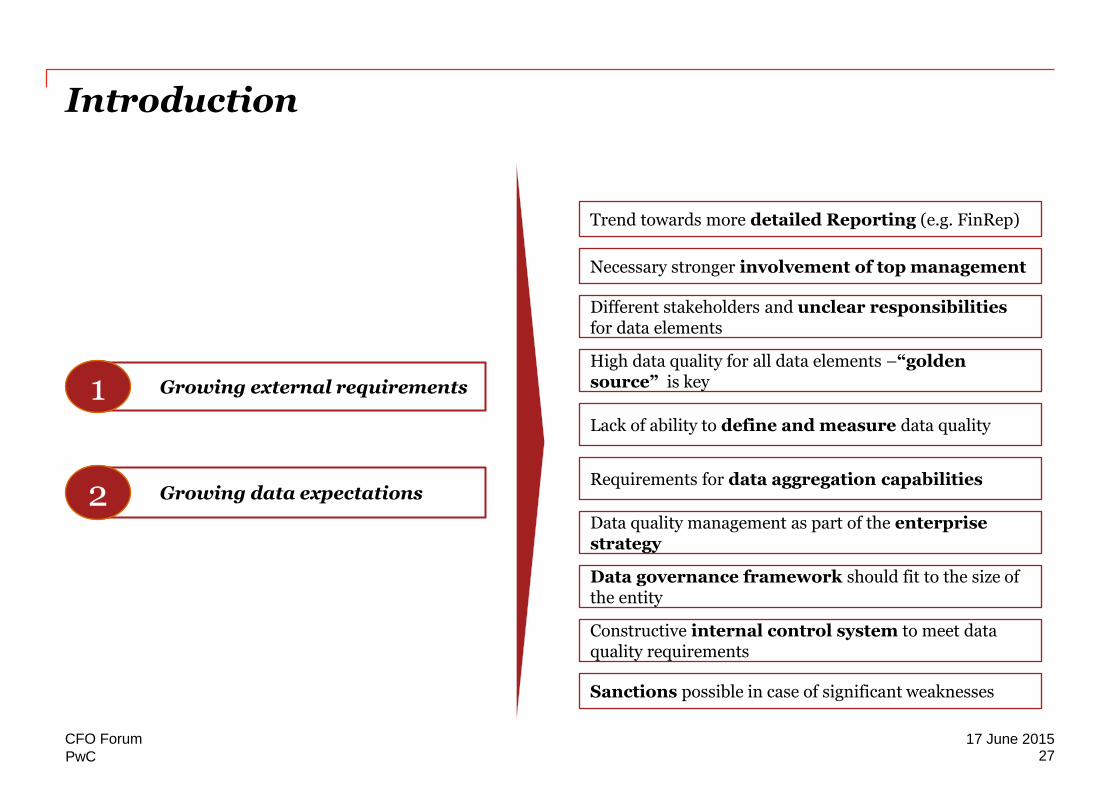

Introduction

Growing external requirements 1

Growing data expectations 2

Trend towards more detailed Reporting (e.g. FinRep)

Necessary stronger involvement of top management

Sanctions possible in case of significant weaknesses

High data quality for all data elements –“golden source” is key

Requirements for data aggregation capabilities

Data quality management as part of the enterprise strategy

Data governance framework should fit to the size of the entity

Constructive internal control system to meet data quality requirements

Different stakeholders and unclear responsibilities for data elements

Lack of ability to define and measure data quality

27 17 June 2015 CFO Forum

PwC

PwC

What is BCBS239?

BCBS 239 key objectives:

Enhance the infrastructure

Improve the speed

Facilitate a comprehensive assessment of risk exposures

Reduce the probability and severity of losses

Improve strategic planning

28

17 June 2015 CFO Forum

PwC

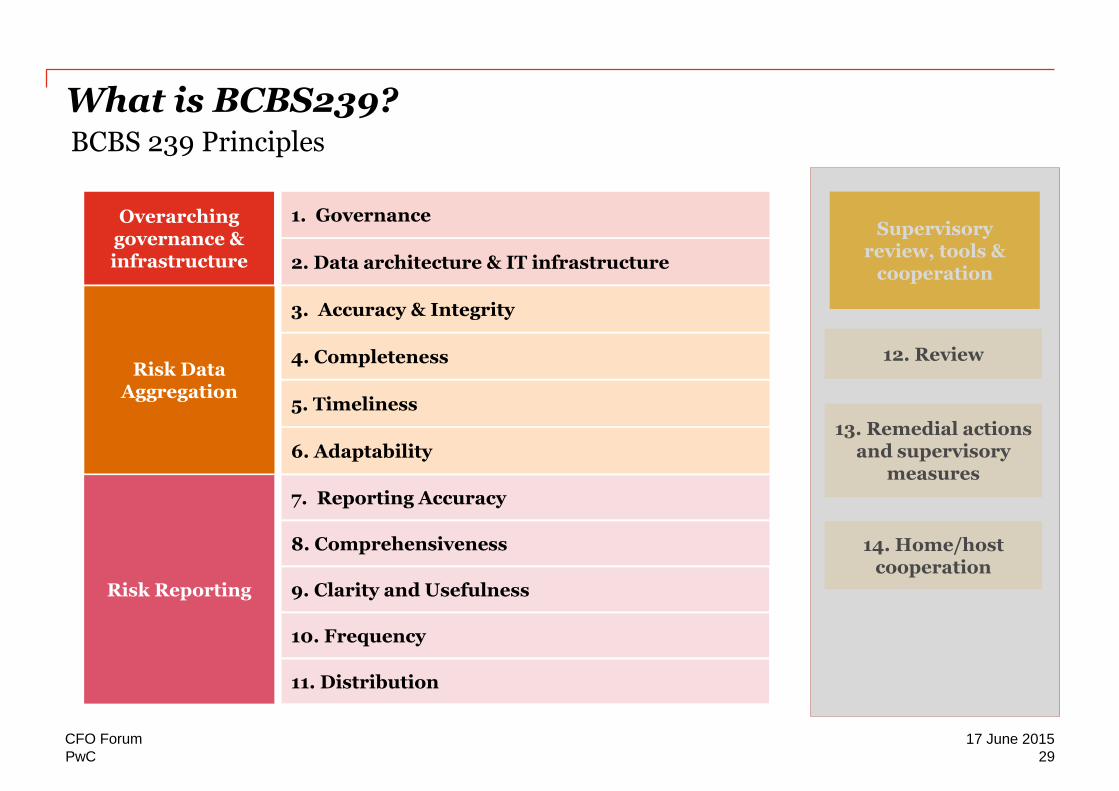

What is BCBS239?

7. Reporting Accuracy

8. Comprehensiveness

9. Clarity and Usefulness

10. Frequency

11. Distribution

Risk Reporting

1. Governance

2. Data architecture & IT infrastructure

Overarching governance & infrastructure

3. Accuracy & Integrity

4. Completeness

5. Timeliness

6. Adaptability

Risk Data Aggregation

BCBS 239 Principles

Supervisory review, tools &

cooperation

12. Review

13. Remedial actions and supervisory

measures

14. Home/host cooperation

29

17 June 2015 CFO Forum

PwC

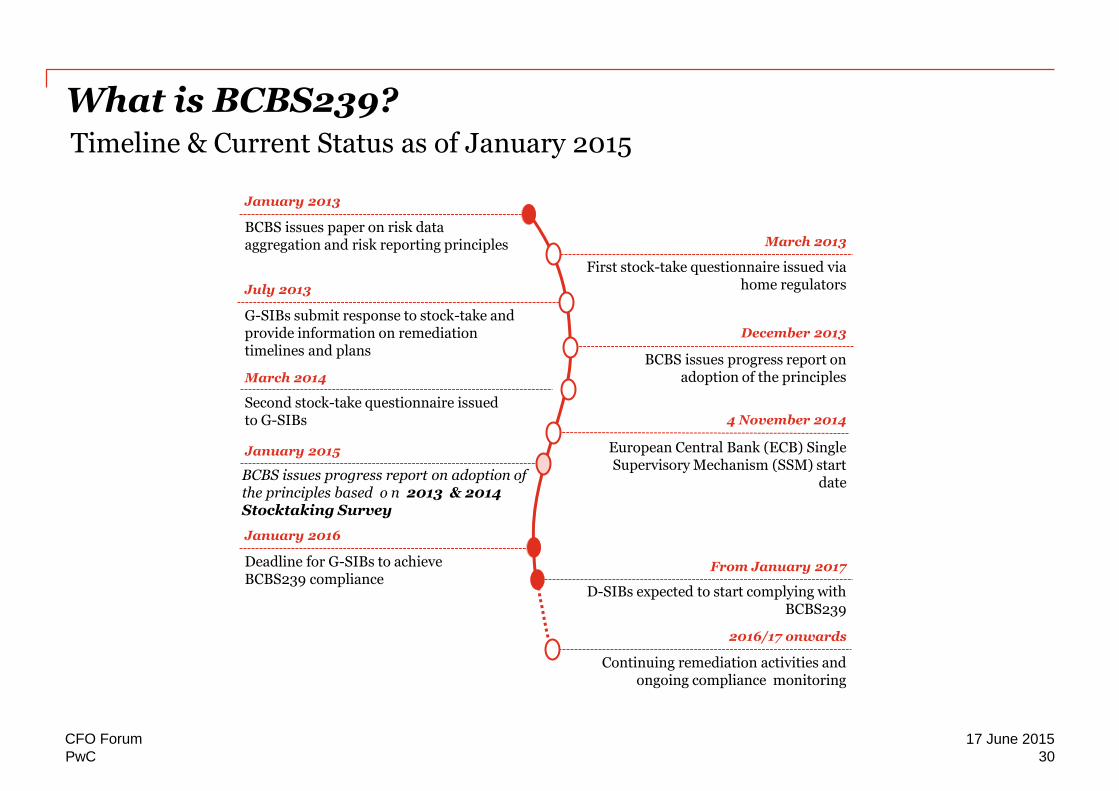

What is BCBS239?

Timeline & Current Status as of January 2015

First stock-take questionnaire issued via home regulators

March 2013 BCBS issues paper on risk data aggregation and risk reporting principles

January 2013

G-SIBs submit response to stock-take and provide information on remediation timelines and plans

July 2013

BCBS issues progress report on adoption of the principles

December 2013

Second stock-take questionnaire issued to G-SIBs

March 2014

D-SIBs expected to start complying with BCBS239

From January 2017 Deadline for G-SIBs to achieve BCBS239 compliance

January 2016

Continuing remediation activities and ongoing compliance monitoring

2016/17 onwards

4 November 2014

European Central Bank (ECB) Single Supervisory Mechanism (SSM) start

date

January 2015

BCBS issues progress report on adoption of the principles based o n 2013 & 2014 Stocktaking Survey

30

17 June 2015 CFO Forum

PwC

Planning and/or Monitoring

Assessment and/or Review

BCBS 239 - Compliance Planning Challenges

Deliverables A group-wide data governance organisation and set of frameworks and policies that define the overall data governance and management

standards to which all functions and business units must comply – examples:

• Group data vision and strategy

• Data Management policies, processes and tools including:

• Data ownership

• Critical data elements

• Golden sourcing

• Data publication and enrichment policies

• Data quality framework

• Metadata / Master Data Management

A bank-wide data architecture strategy and IT infrastructure to support:

• Global data models and metadata management

• Global Master Data Management

• Resilient infrastructure

Global standards, frameworks, policies and documentation hierarchy for risk data aggregation, including:

• Process documentation

• Critical Risk data elements, owners, and golden sources

• Control framework

• Data quality standards (metrics, materiality / tolerance, etc.)

And risk reporting, including:

• Risk reports inventory

• Standardised risk reporting practices and governance

• Explicit requirements (e.g. timeliness, accuracy) and consistent adoption of core risk metrics

• Appropriate balance of risk data, analysis and interpretation

• Ensure packs are meaningful and appropriately tailored to the needs of recipients

Specific remediation projects within risk areas and business units to improve the underlying technology infrastructure and architecture to support

data aggregation and reporting:

• Reduced reliance on manual aggregation processes

• Appropriate controls over timeliness, completeness, and accuracy

• Flexible risk data aggregation capability and customisable reporting tools

• Alignment between Risk and Finance

Principle 1 Governance

…

Principle 11. Distribution

Principles Question 1

Question 2

Question 3

…

…

Question i

…

…

Questions Requirement 1

Requirement 2

Requirement 3

…

…

…

…

…

…

Requirement j

…

Requirements

Data Governance and Management

Data Integration & Infrastructure

Specific remediation projects

Risk Standards and Processes

Programmes

From Principles to Planning

31

17 June 2015 CFO Forum

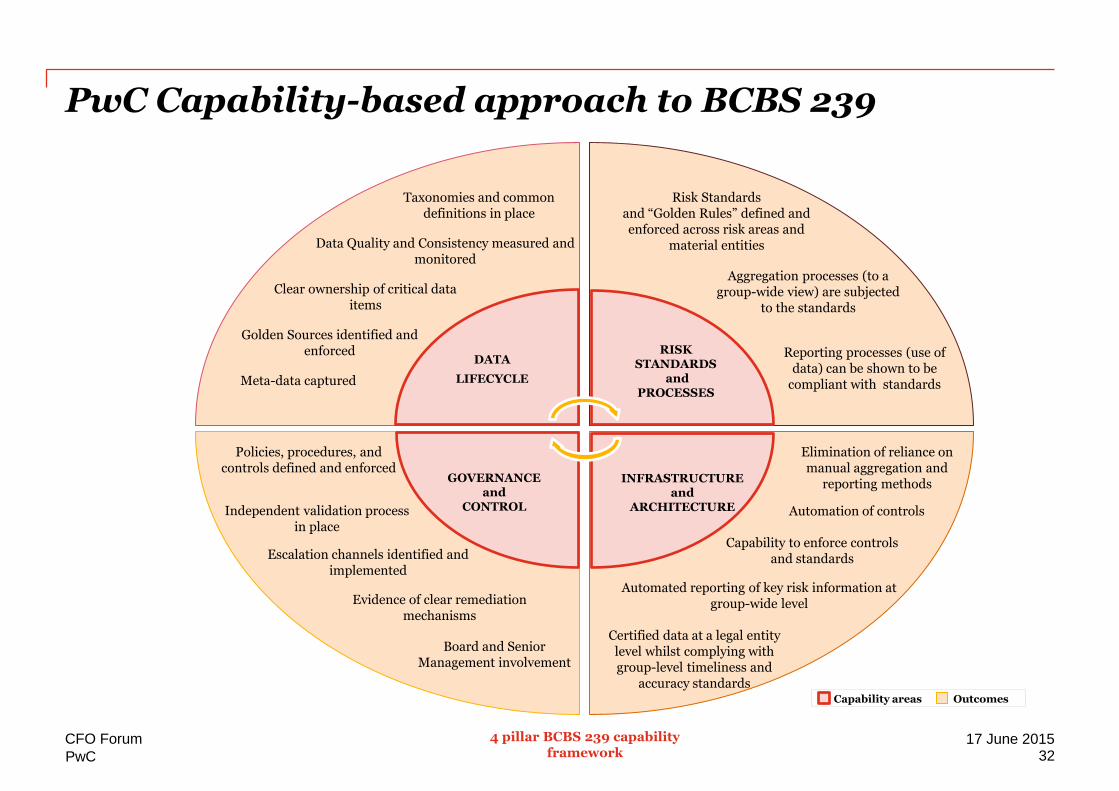

Taxonomies and common definitions in place

Data Quality and Consistency measured and monitored

Clear ownership of critical data items

Golden Sources identified and enforced

Meta-data captured

DATA

LIFECYCLE

Risk Standards and “Golden Rules” defined and enforced across risk areas and

material entities

Reporting processes (use of data) can be shown to be

compliant with standards

Aggregation processes (to a group-wide view) are subjected

to the standards

RISK STANDARDS

and PROCESSES

Policies, procedures, and controls defined and enforced

Independent validation process in place

Escalation channels identified and implemented

Evidence of clear remediation mechanisms

Board and Senior Management involvement

GOVERNANCE and

CONTROL

Elimination of reliance on manual aggregation and

reporting methods

Automation of controls

Capability to enforce controls and standards

Automated reporting of key risk information at

group-wide level

Certified data at a legal entity level whilst complying with group-level timeliness and

accuracy standards

INFRASTRUCTURE and

ARCHITECTURE

PwC Capability-based approach to BCBS 239

Capability areas Outcomes

4 pillar BCBS 239 capability framework 32

17 June 2015 CFO Forum

PwC

PwC

Overall BCBS 239 compliance journey for banks

2016 onwards

2015 2014 2013

GSIBs Compliance deadline

Assess and plan 1

1. Assess and plan Build

foundation 2

2. Foundation

Implement solutions 3

3. Solution implementation

Review and monitor compliance programme 4

4. Compliance programme review

Certification framework

5

5. Certification framework

Certify compliance 6

6. Ongoing certification

33

17 June 2015 CFO Forum

Data is the key for several requirements

Data Quality as a

cross-sectional topic

Principles from BCBS 239

transferable to other

regulations and vice versa

Lessons learnt Asset Quality Review

Data

Collection

Aggregation

Reporting

Ownership

BCBS 239

COREP/ FINREP

CRD IV/ CRR

IFRS 9

MiFIR/ MiFID II

EMIR

FATCA LEI

HFT

MaSan

SREP

AnaCredit

34 17 June 2015 CFO Forum

PwC

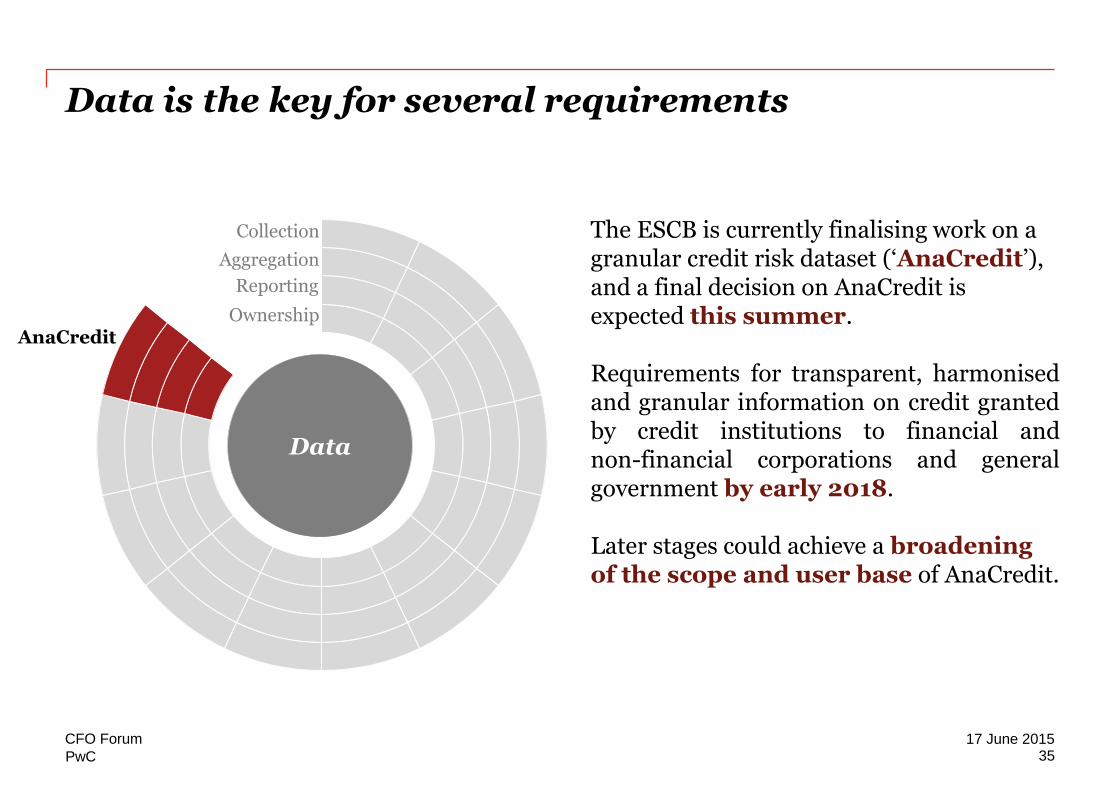

Data is the key for several requirements

Data

Collection

Aggregation

Reporting

Ownership AnaCredit

The ESCB is currently finalising work on a granular credit risk dataset (‘AnaCredit’), and a final decision on AnaCredit is expected this summer. Requirements for transparent, harmonised and granular information on credit granted by credit institutions to financial and non-financial corporations and general government by early 2018. Later stages could achieve a broadening of the scope and user base of AnaCredit.

35 17 June 2015 CFO Forum

PwC

PwC

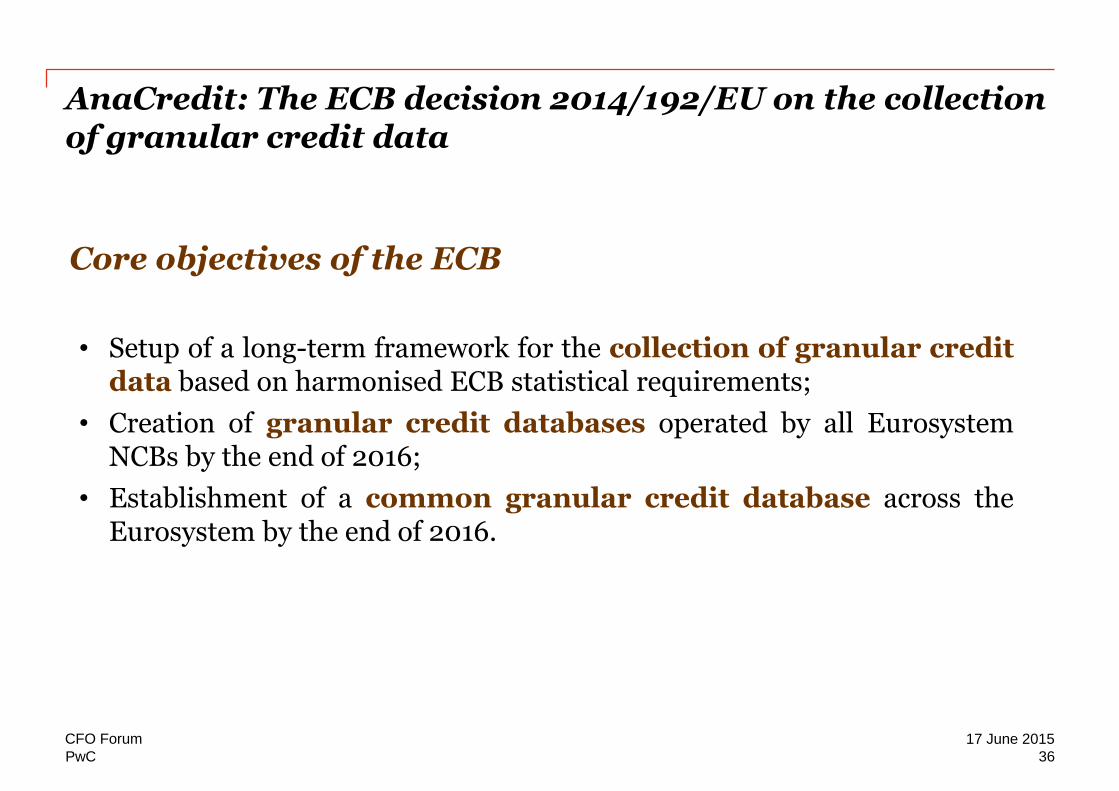

AnaCredit: The ECB decision 2014/192/EU on the collection of granular credit data

• Setup of a long-term framework for the collection of granular credit data based on harmonised ECB statistical requirements;

• Creation of granular credit databases operated by all Eurosystem NCBs by the end of 2016;

• Establishment of a common granular credit database across the Eurosystem by the end of 2016.

Core objectives of the ECB

36

17 June 2015 CFO Forum

PwC

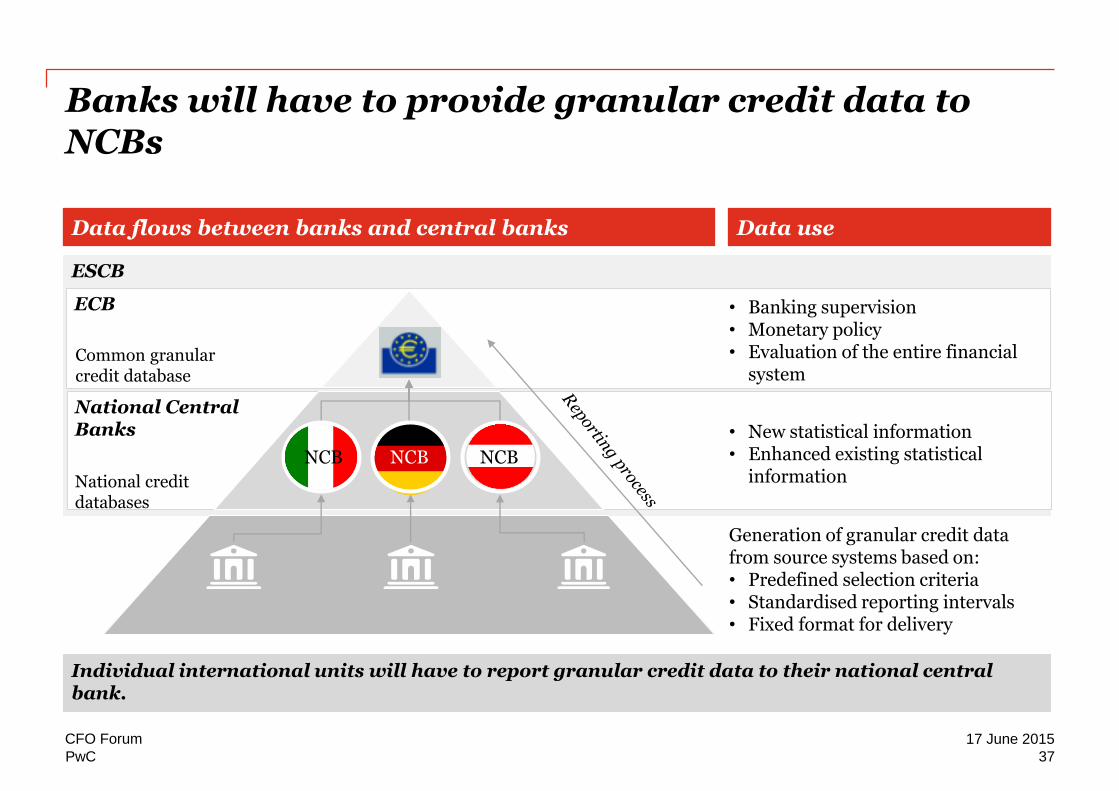

Banks will have to provide granular credit data to NCBs Data flows between banks and central banks Data use

ESCB

National Central Banks

ECB • Banking supervision • Monetary policy • Evaluation of the entire financial

system

• New statistical information • Enhanced existing statistical

information

Generation of granular credit data from source systems based on: • Predefined selection criteria • Standardised reporting intervals • Fixed format for delivery

Individual international units will have to report granular credit data to their national central bank.

Common granular credit database

National credit databases

NCB NCB NCB

37

17 June 2015 CFO Forum

PwC

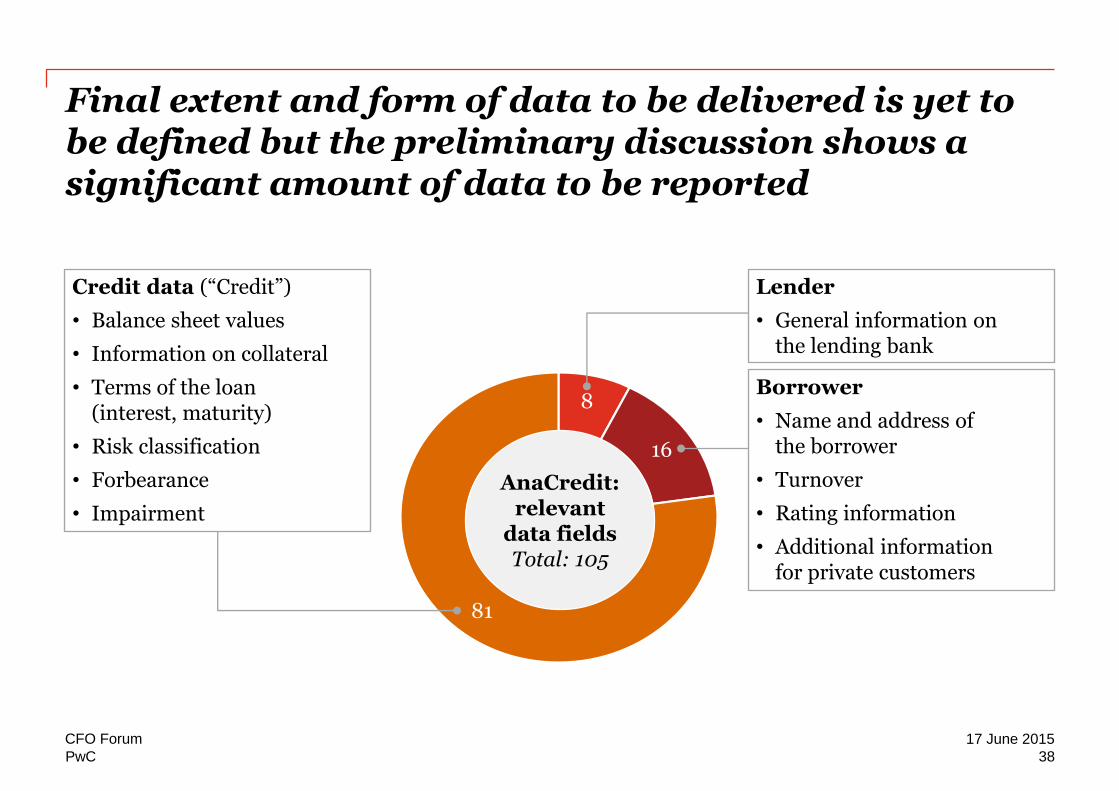

Final extent and form of data to be delivered is yet to be defined but the preliminary discussion shows a significant amount of data to be reported

81

8

16

AnaCredit: relevant

data fields Total: 105

Lender

• General information on the lending bank

Borrower

• Name and address of the borrower

• Turnover

• Rating information

• Additional information for private customers

Credit data (“Credit”)

• Balance sheet values

• Information on collateral

• Terms of the loan (interest, maturity)

• Risk classification

• Forbearance

• Impairment

38

17 June 2015 CFO Forum

PwC

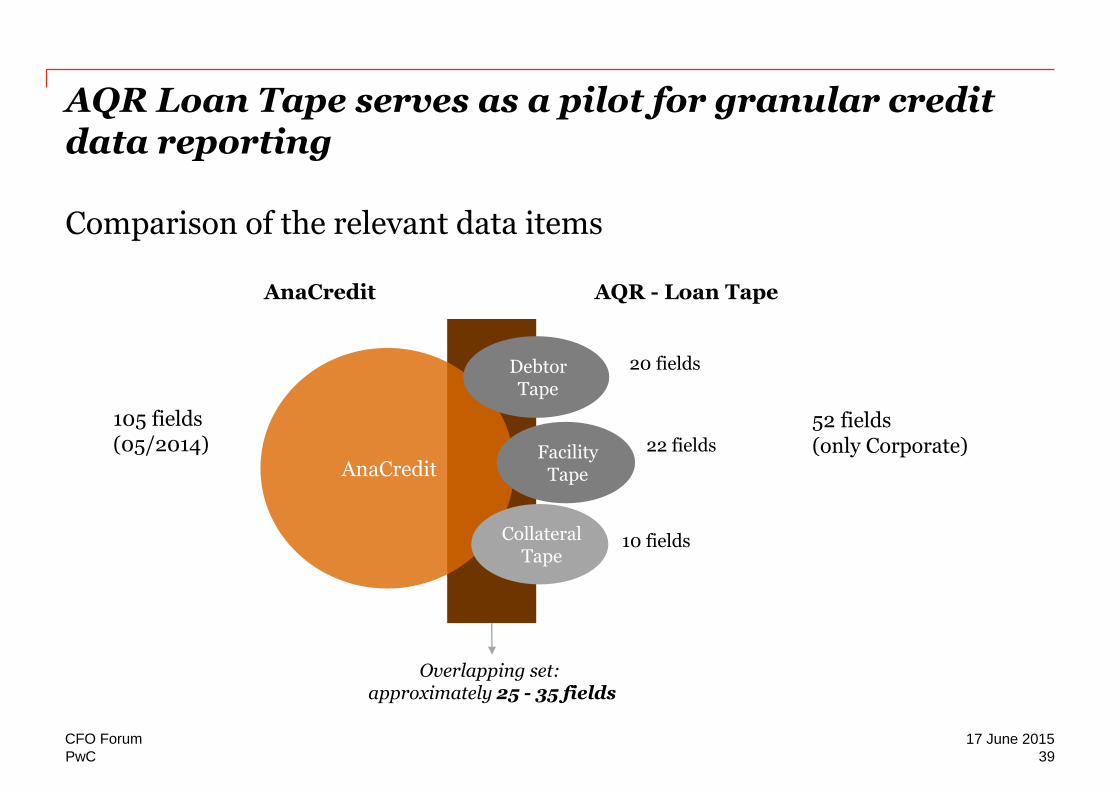

Overlapping set: approximately 25 - 35 fields

AQR Loan Tape serves as a pilot for granular credit data reporting Comparison of the relevant data items

AnaCredit AQR - Loan Tape

AnaCredit

105 fields (05/2014)

Debtor Tape

20 fields

Facility Tape

22 fields

Collateral Tape

10 fields

52 fields (only Corporate)

39

17 June 2015 CFO Forum

Thank You

This publication has been prepared for general guidance on matters of interest only, and does

not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained

in this publication, and, to the extent permitted by law, PricewaterhouseCoopers, Société

coopérative, its members, employees and agents do not accept or assume any liability,

responsibility or duty of care for any consequences of you or anyone else acting, or refraining

to act, in reliance on the information contained in this publication or for any decision based on

it.

© 2015 PricewaterhouseCoopers, Société coopérative. All rights reserved. In this document,

“PwC” refers to PricewaterhouseCoopers, Société coopérative Luxembourg, which is a

member firm of PricewaterhouseCoopers International Limited, each member firm of which is a

separate legal entity.