CERTIFIED CLASS ACTION FEDERAL COURT … REPLY...Daniel Wallace MCINNES COOPER ... (retired) John G....

31

(Response Written submissions - Manuge Questions of Law3.DOC) Court File No.: T-463-07 CERTIFIED CLASS ACTION FEDERAL COURT BETWEEN: DENNIS MANUGE Plaintiff and HER MAJESTY THE QUEEN Defendant PLAINTIFF CLASS’ REPLY MEMORANDUM OF FACT AND LAW MOTION TO DETERMINE QUESTIONS OF LAW HEARING DATES: NOVEMBER 16 and 17, 2011 HEARING LOCATION: HALIFAX Peter J. Driscoll Daniel Wallace MCINNES COOPER 1300-1969 Upper Water Street Halifax, NS B3J 2V1 Tel: (902) 425-6500 Fax: (902) 425-6350 Ward K. Branch BRANCH MACMASTER 1210-777 Hornby Street Vancouver, BC V6Z 1S4 Tel: (604) 654-2999 Fax: (604) 684-3429 Myles J. Kirvan Deputy Attorney General of Canada Per: Lori Rasmussen James Gunvaldsen-Klaassen Susan Inglis DEPARTMENT OF JUSTICE 1400-5251 Duke Street Halifax, NS B3J 1P3 Tel: (902) 426-0020 Fax: (902) 426-2329 Solicitors for the Plaintiff Class Solicitors for the Defendant

Transcript of CERTIFIED CLASS ACTION FEDERAL COURT … REPLY...Daniel Wallace MCINNES COOPER ... (retired) John G....

(Response Written submissions - Manuge Questions of Law3.DOC)

Court File No.: T-463-07

CERTIFIED CLASS ACTION

FEDERAL COURT

BETWEEN:

DENNIS MANUGE Plaintiff

and

HER MAJESTY THE QUEEN Defendant

PLAINTIFF CLASS’ REPLY MEMORANDUM OF FACT AND LAW MOTION TO DETERMINE QUESTIONS OF LAW

HEARING DATES: NOVEMBER 16 and 17, 2011

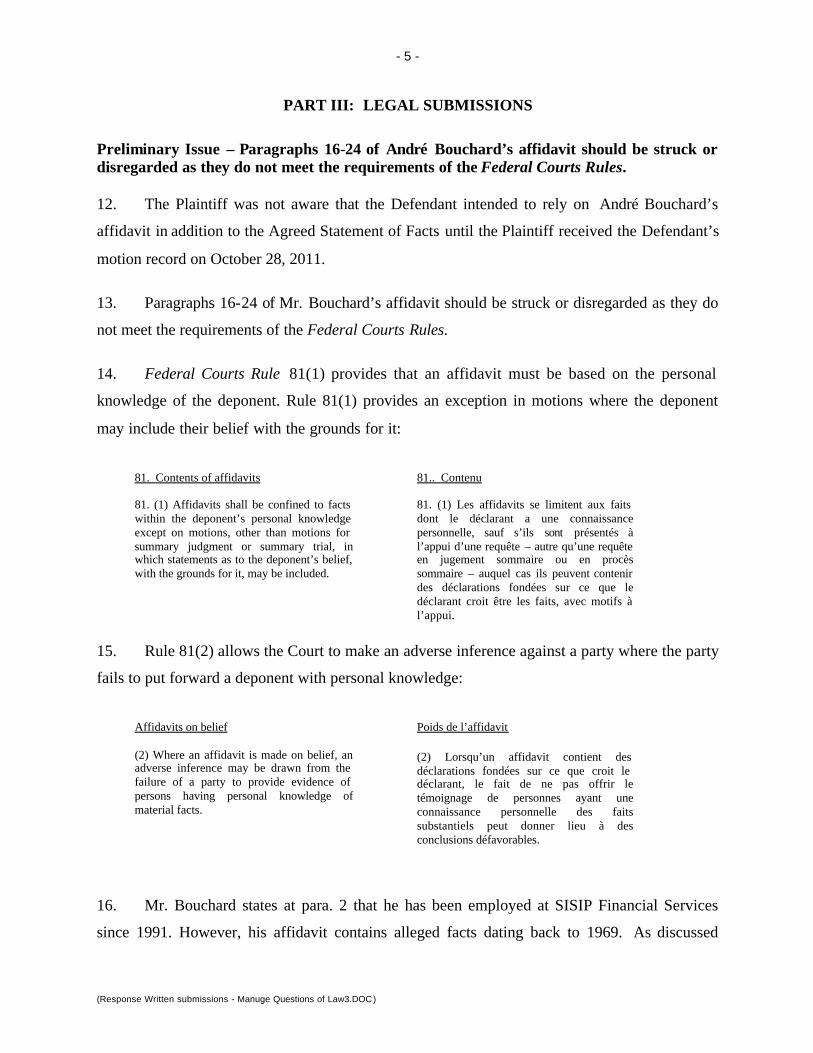

HEARING LOCATION: HALIFAX

Peter J. Driscoll Daniel Wallace MCINNES COOPER 1300-1969 Upper Water Street Halifax, NS B3J 2V1 Tel: (902) 425-6500 Fax: (902) 425-6350

Ward K. Branch BRANCH MACMASTER 1210-777 Hornby Street Vancouver, BC V6Z 1S4 Tel: (604) 654-2999 Fax: (604) 684-3429

Myles J. Kirvan Deputy Attorney General of Canada Per: Lori Rasmussen James Gunvaldsen-Klaassen Susan Inglis DEPARTMENT OF JUSTICE 1400-5251 Duke Street Halifax, NS B3J 1P3 Tel: (902) 426-0020 Fax: (902) 426-2329

Solicitors for the Plaintiff Class Solicitors for the Defendant

- 1 -

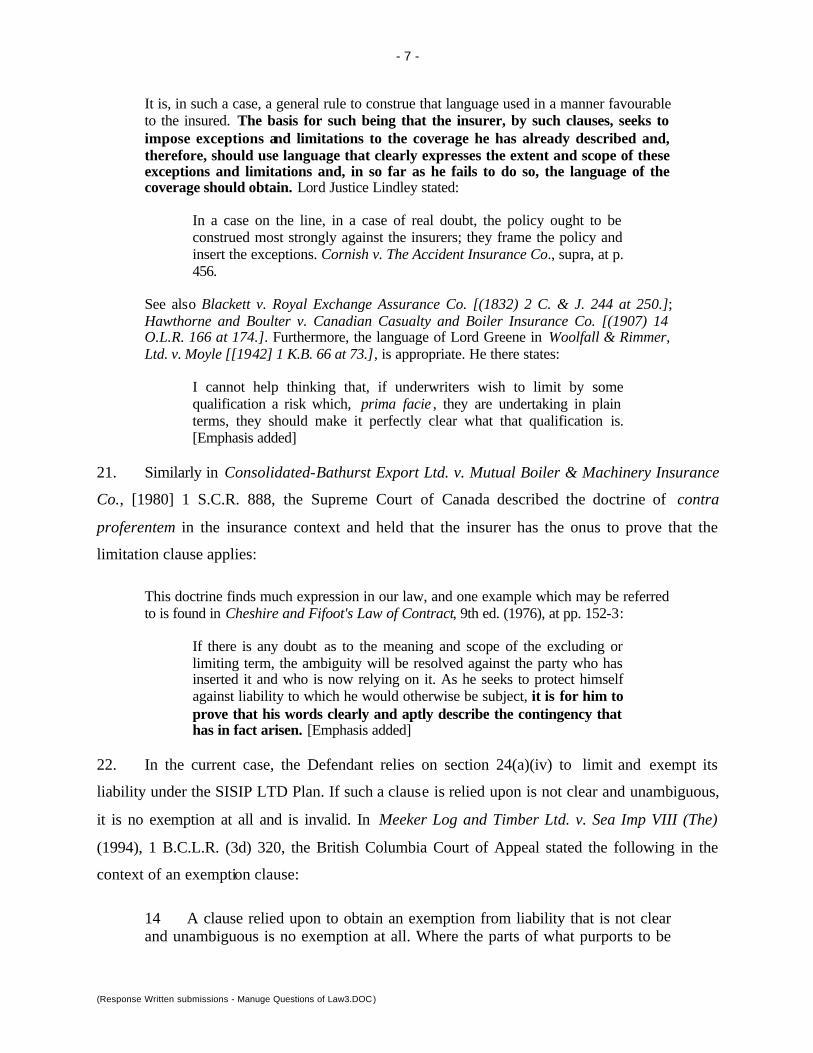

(Response Written submissions - Manuge Questions of Law3.DOC)

“SISIP LTD is an income replacement scheme...It is designed to operate in conjunction with other sources of income the employee may have, and other specified income replacement programs that they may be entitled to, rather than in addition to those sources.”1

“Many of these complaints were grounded in the common misbelief [sic] that [Pension Act] disability pensions are a form of income replacement, when in fact they are intended to provide compensation for reductions in the quality, and sometimes the quantity, of life experienced by the disabled.”2

“In light of the above, it is clear – and, indeed indisputable – that Pension Act disability pensions are not meant to be income replacement. As I indicated above, they must be characterized as amounts paid for pain, suffering and loss of enjoyment of life.”3

PART I: CONCISE STATEMENT OF FACT

1. The Plaintiff refers to its concise statement of facts in its written submissions.

2. The Plaintiff would like to specifically address two of the Defendant’s stated facts that

were presented in the Defendant’s factum. 4

3. The Defendant relies on André Bouchard’s January 3, 2008 affidavit to introduce

extrinsic evidence to support the Defendant’s interpretation of the SISIP LTD Plan.

4. At paras. 5-14 of his affidavit, Mr. Bouchard selectively paraphrases two documents that

were appended to his affidavit: the Minister of National Defence’s June 1969 authorization to

create SISIP (Exhibit B) and an attached brief (Exhibit A). At paras. 3-4 of its factum, the

Defendant discusses these documents.

5. Mr. Bouchard’s affidavit and the Defendant’s factum both fail to mention the second

paragraph of the Minister’s two paragraph authorization:

1 André Bouchard Affidavit, paras. 32 and 34. 2 Veterans Affairs Canada’s Reference Paper: “The Origins and Evolution of Veterans Benefits in Canada 1914-2004”. Affidavit of Sergeant (retired) John G. Bartlett, Exhibit B, Page 8. 3 Department of National Defence and Canadian Forces Ombudsman Yves Côté, Q.C., Ombudsman Calls for Fair Treatment for Injured Canadian Forces Veterans (March 6, 2007). 4 Paras. 3-13 of the Defendant’s Factum.

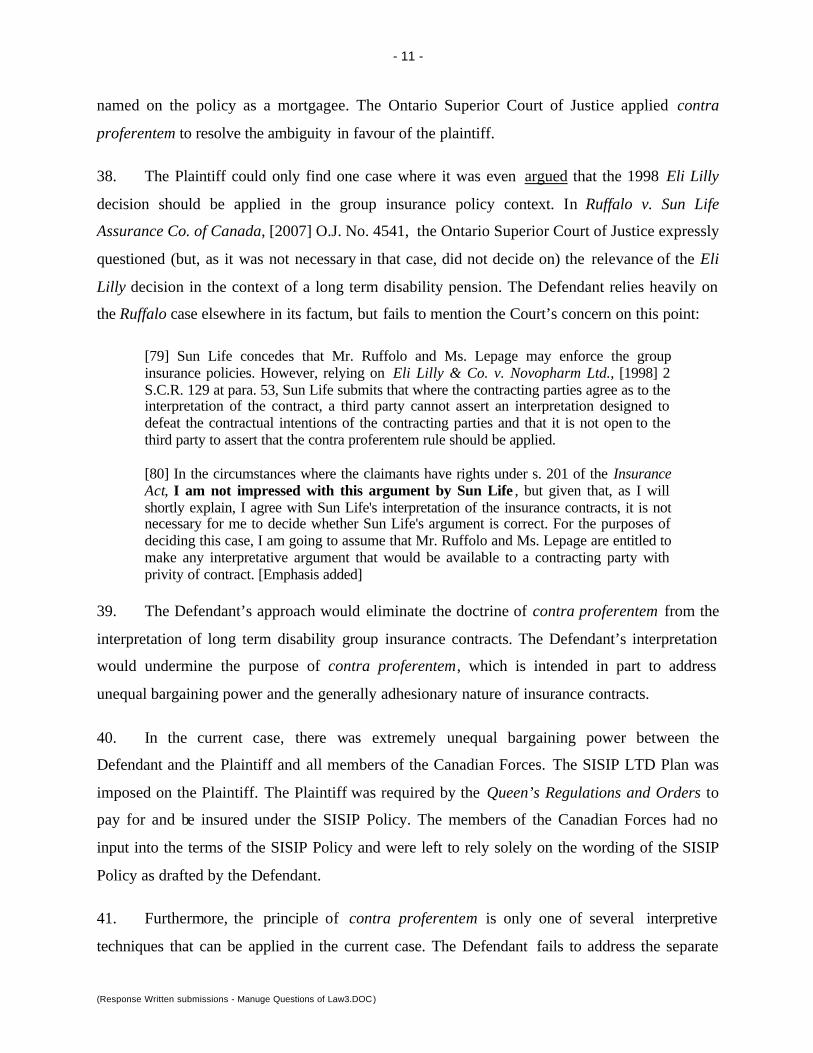

- 2 -

(Response Written submissions - Manuge Questions of Law3.DOC)

In this way participating service personnel will have the benefit of the co-operative savings of a group plan as a supplementary means of providing protection over and above entitlements under existing public plans.5

6. At para. 7 of its factum, the Defendant states that “[s]ince, as of 1976, a CF member

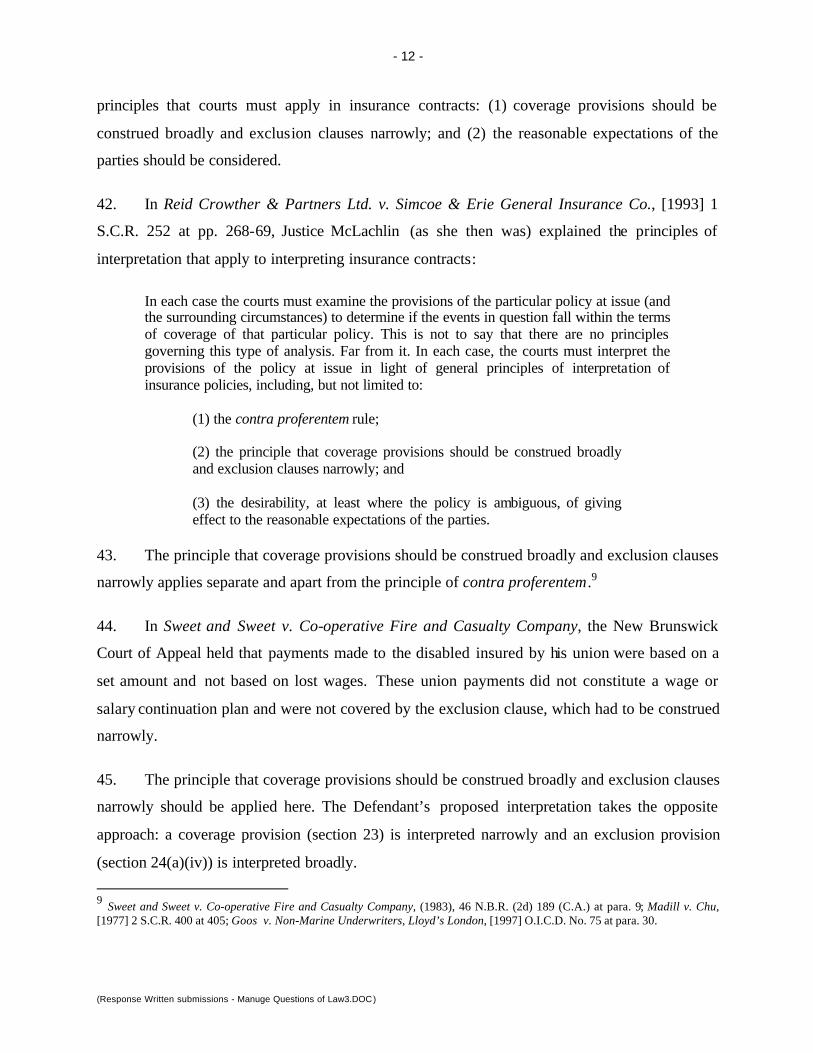

could receive both SISIP LTD and Pension Act benefits in respect of the same disability, Pension

Act benefits were added to the list of reductions now set out in s. 24(a) of the SISIP policy, to

prevent double recovery.”

7. First, the Defendant’s wording is incorrect: “monthly income benefits payable to the

member under the Pension Act” were added to s. 24(a) not “Pension Act benefits” as suggested

by the Defendant. As clear wording in an insurance contract’s reduction clause is necessary to

permit the insurer to make a reduction, it is crucial to accurately describe that wording.

8. Second, in respect to the Defendant’s statement regarding payments for the same

disability, it is significant to note that the Defendant reduces a Member’s SISIP LTD benefit by

all of the Member’s Pension Act disability pensions even if they are for wholly unrelated

medically conditions. In his October 30, 2003 special report Unfair Deductions from SISIP

Payments to Former CF Members, DND and CF Ombudsman André Marin provided an example

of the Defendant’s reduction of Pension Act disability pensions for unrelated medical conditions :

[16] Prior to suffering the stroke, the complainant had injured his leg and knee in a CF base-sanctioned hockey game. While he was still a member of the CF, the complainant applied to VAC for a disability pension under the Pension Act on the basis that the leg injury was attributable to his CF service. His claim was denied. After he applied for SISIP long term disability benefits because of his stroke, a SISIP representative advised him to re-apply to VAC for a disability pension under the Pension Act. The SISIP representative also suggested that the complainant might be more successful in obtaining a disability pension if he had legal representation. As a result, he engaged a lawyer at his own expense and was successful in obtaining a 10% disability pension for his leg injury.

[17] The complainant advised his SISIP representative of the amount awarded by VAC in disability pension for his leg injury. The SISIP representative then advised him that this amount would also reduce the amount of his monthly SISIP long term disability benefits. The complainant felt that because this disability pension was for his leg injury and was unrelated to the stroke that led to his release and his SISIP long term disability benefits, the amount of his Pension Act disability pension should not reduce the amount of his SISIP long term disability benefits.

5 André Bouchard Affidavit, exhibit B.

- 3 -

(Response Written submissions - Manuge Questions of Law3.DOC)

9. Further, the Defendant’s stated purpose that the reduction of Pension Act disability

pensions is to avoid double recovery does not withstand scrutiny. The Pension Act disability

pension and SISIP LTD plan have different purposes, characteristics and compensate for

different losses.6

6 Plaintiff’s Factum, para. 101-108.

- 4 -

(Response Written submissions - Manuge Questions of Law3.DOC)

PART II: QUESTIONS OF LAW

10. Preliminary issue – should portions of André Bouchard’s affidavit be struck or

disregarded due to their failure to meet the requirements of the Federal Courts Rules?

11. The Plaintiff brings this motion for this Honourable Court to determine the following two

questions of law pursuant to Rule 220 of the Federal Courts Rules:

1. Are the pension payments made pursuant to s. 21 of the Pension Act, “total monthly income benefits” as that term is described in section 24(a)(iv) of Part III(B) of S.I.S.I.P. Policy 901102?

2. Are the pension payments made pursuant to s. 21 of the Pension Act,

“monthly pay in effect on the date of release from the Canadian Forces” as that term is described in section 23(a) of Part III(B) of S.I.S.I.P. Policy 901102?

- 5 -

(Response Written submissions - Manuge Questions of Law3.DOC)

PART III: LEGAL SUBMISSIONS

Preliminary Issue – Paragraphs 16-24 of André Bouchard’s affidavit should be struck or disregarded as they do not meet the requirements of the Federal Courts Rules. 12. The Plaintiff was not aware that the Defendant intended to rely on André Bouchard’s

affidavit in addition to the Agreed Statement of Facts until the Plaintiff received the Defendant’s

motion record on October 28, 2011.

13. Paragraphs 16-24 of Mr. Bouchard’s affidavit should be struck or disregarded as they do

not meet the requirements of the Federal Courts Rules.

14. Federal Courts Rule 81(1) provides that an affidavit must be based on the personal

knowledge of the deponent. Rule 81(1) provides an exception in motions where the deponent

may include their belief with the grounds for it:

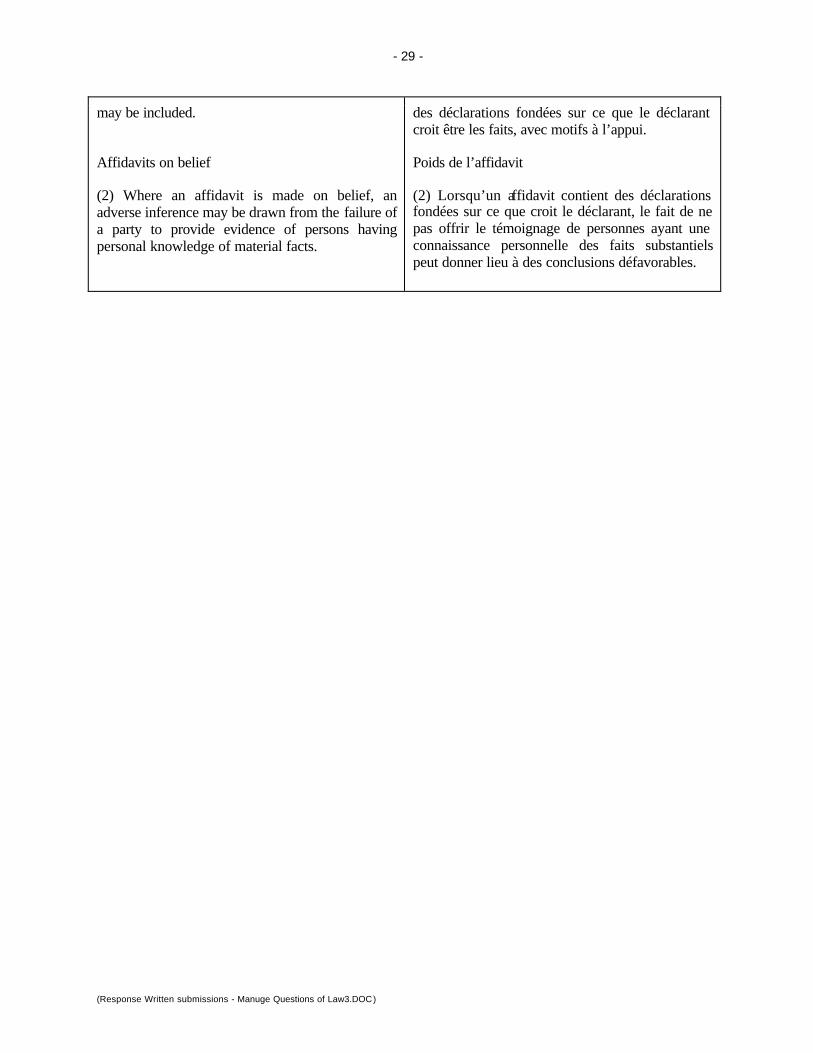

81. Contents of affidavits 81. (1) Affidavits shall be confined to facts within the deponent’s personal knowledge except on motions, other than motions for summary judgment or summary trial, in which statements as to the deponent’s belief, with the grounds for it, may be included.

81.. Contenu 81. (1) Les affidavits se limitent aux faits dont le déclarant a une connaissance personnelle, sauf s’ils sont présentés à l’appui d’une requête – autre qu’une requête en jugement sommaire ou en procès sommaire – auquel cas ils peuvent contenir des déclarations fondées sur ce que le déclarant croit être les faits, avec motifs à l’appui.

15. Rule 81(2) allows the Court to make an adverse inference against a party where the party

fails to put forward a deponent with personal knowledge:

Affidavits on belief (2) Where an affidavit is made on belief, an adverse inference may be drawn from the failure of a party to provide evidence of persons having personal knowledge of material facts.

Poids de l’affidavit

(2) Lorsqu’un affidavit contient des déclarations fondées sur ce que croit le déclarant, le fait de ne pas offrir le témoignage de personnes ayant une connaissance personnelle des faits substantiels peut donner lieu à des conclusions défavorables.

16. Mr. Bouchard states at para. 2 that he has been employed at SISIP Financial Services

since 1991. However, his affidavit contains alleged facts dating back to 1969. As discussed

- 6 -

(Response Written submissions - Manuge Questions of Law3.DOC)

above, at paras. 5 – 14, Mr. Bouchard selectively paraphrases two documents appended to his

affidavit as exhibits “A” and “B”.

17. Paras. 16 – 24 of Mr. Bouchard’s affidavit deal with facts that pre-date Mr. Bouchard’s

employment with SISIP by 15 years. He cannot have personal knowledge of these facts yet he

does not state the grounds upon which he believes them. Unlike paras. 5-14, there are no

supporting exhibits to provide grounds for Mr. Bouchard’s belief.

18. At para. 24 of his affidavit, Mr. Bouchard purports to give evidence regarding the 1976

introduction of section 24(a)(iv) to the SISIP LTD Plan. He does not state the grounds for his

belief. This is contrary to Rule 81(1). In the alternative that is evidence is admissible, it should be

given little weight in accordance with Rule 81(2). Furthermore, this extrinsic evidence is not

permissible unless the SISIP LTD Plan is ambiguous.

Question 1: The pension payments made pursuant to s. 21 of the Pension Act are not “total monthly income benefits” as that term is described in section 24 (a)(iv) of Part III(B) of S.I.S.I.P. Policy 901102. The principle of contra proferentem applies to the current case.

19. The principle of contra proferentem is particularly important in the insurance context.

Insurance contracts are essentially adhesionary and “one must always be alert to the unequal

bargaining power at work in insurance contracts, and interpret such contracts accordingly.”7

20. In Indemnity Insurance Co. of North America v. Excel Cleaning Service, [1954] S.C.R.

169, the Supreme Court of Canada discussed the importance of contra proferentem in insurance

contracts and stated that the insurer should use language that clearly expresses the extent and

scope of exceptions and limitations:

Such a construction would largely, if not completely, nullify the purpose for which the insurance was sold - a circumstance to be avoided, so far as the language used will permit. Cornish v. The Accident Insurance Co. [(1889) 23 Q.B.D. 453.], where at p. 456 Lindley L.J. stated:

The object of the contract is to insure against accidental death and injuries, and the contract must not be construed so as to defeat that object, nor so as to render it practically illusory.

7 Non-Marine Underwriters, Lloyd’s v. Scalera, [2000] 1 S.C.R. 551 at para. 70.

- 7 -

(Response Written submissions - Manuge Questions of Law3.DOC)

It is, in such a case, a general rule to construe that language used in a manner favourable to the insured. The basis for such being that the insurer, by such clauses, seeks to impose exceptions and limitations to the coverage he has already described and, therefore, should use language that clearly expresses the extent and scope of these exceptions and limitations and, in so far as he fails to do so, the language of the coverage should obtain. Lord Justice Lindley stated:

In a case on the line, in a case of real doubt, the policy ought to be construed most strongly against the insurers; they frame the policy and insert the exceptions. Cornish v. The Accident Insurance Co., supra, at p. 456.

See also Blackett v. Royal Exchange Assurance Co. [(1832) 2 C. & J. 244 at 250.]; Hawthorne and Boulter v. Canadian Casualty and Boiler Insurance Co. [(1907) 14 O.L.R. 166 at 174.]. Furthermore, the language of Lord Greene in Woolfall & Rimmer, Ltd. v. Moyle [[1942] 1 K.B. 66 at 73.], is appropriate. He there states:

I cannot help thinking that, if underwriters wish to limit by some qualification a risk which, prima facie , they are undertaking in plain terms, they should make it perfectly clear what that qualification is. [Emphasis added]

21. Similarly in Consolidated-Bathurst Export Ltd. v. Mutual Boiler & Machinery Insurance

Co., [1980] 1 S.C.R. 888, the Supreme Court of Canada described the doctrine of contra

proferentem in the insurance context and held that the insurer has the onus to prove that the

limitation clause applies:

This doctrine finds much expression in our law, and one example which may be referred to is found in Cheshire and Fifoot's Law of Contract, 9th ed. (1976), at pp. 152-3:

If there is any doubt as to the meaning and scope of the excluding or limiting term, the ambiguity will be resolved against the party who has inserted it and who is now relying on it. As he seeks to protect himself against liability to which he would otherwise be subject, it is for him to prove that his words clearly and aptly describe the contingency that has in fact arisen. [Emphasis added]

22. In the current case, the Defendant relies on section 24(a)(iv) to limit and exempt its

liability under the SISIP LTD Plan. If such a clause is relied upon is not clear and unambiguous,

it is no exemption at all and is invalid. In Meeker Log and Timber Ltd. v. Sea Imp VIII (The)

(1994), 1 B.C.L.R. (3d) 320, the British Columbia Court of Appeal stated the following in the

context of an exemption clause:

14 A clause relied upon to obtain an exemption from liability that is not clear and unambiguous is no exemption at all. Where the parts of what purports to be

- 8 -

(Response Written submissions - Manuge Questions of Law3.DOC)

an exempting clause are so inconsistent as to render unclear the actual exemption agreed, no part can be relied upon; as a whole the clause is invalid: Nelson Line (Liverpool), Limited. v. James Nelson & Sons, Limited., [1908] A.C. 16 (H.L.).

23. The Defendant submits that the principle of contra proferentem cannot be used in the

interpretation of the SISIP LTD Plan. In support of its submission, the Defendant relies solely

on one decision; a decision made in the context of pharmaceutical patent litigation: Eli Lilly &

Co. Novopharm Ltd., [1998] 2 S.C.R. 129.

24. As the Supreme Court of Canada dealt with a very different factual situation sur rounding

the interpretation of the contract in Eli Lilly, it is necessary to briefly set out the facts in Eli Lilly.

Novopharm received a compulsory license for a pharmaceutical patent owned by Eli Lilly. One

of the terms of the compulsory license prohibited Novopharm from granting “any sublicense”.

25. Novopharm and Apotex subsequently entered into a contract. Eli Lilly argued that

Novopharm granted a sublicense to Apotex in that contract and thereby breached the terms of the

compulsory license. Novopharm and Apotex both denied that their contract constituted a

sublicense. The issue before the Court was whether Novopharm and Apotex’s contract

constituted a sublicense.

26. Eli Lilly was not a party to Novopharm and Apotex’s contract. In fact, Eli Lilly had no

involvement whatsoever with the contract: it provided no consideration, received no benefits and

did not have any obligations under Novopharm and Apotex’s contract.

27. When interpreting the terms of Novopharm and Apotex’s contract, the Court held that Eli

Lilly could not argue the doctrine of contra proferentem because Eli Lilly was not a party to the

contract and both parties to the contract agreed on its interpretation.

28. The facts of the current case are clearly distinguishable from Eli Lilly. In the current case,

members of the Plaintiff Class paid for their SISIP LTD Plan coverage throughout their career

and are the insured beneficiaries under the SISIP LTD Plan.8 Further, there is no evidence before

the Court that the insurer has taken any position as to the correct interpretation of the SISIP LTD

Plan.

8 Agreed Statement of Facts, para. 3.

- 9 -

(Response Written submissions - Manuge Questions of Law3.DOC)

29. The Defendant cites only Eli Lilly to support its position that contra proferentem cannot

be applied in the current case. The Defendant does not cite any cases where a court has decided

that an insured is not permitted to argue contra proferentem because the policy being interpreted

was a group insurance policy. Similarly, the Defendant has not cited any cases where the Eli

Lilly decision was followed in the long term disability insurance context.

30. The Defendant does not address the decisions (decided post-Eli Lilly) contained in the

Plaintiff’s factum that apply the principle of contra proferentem to the benefit of the insured

under a group policy.

31. In Canada Life Assurance Co. v. Donohue (1999), 46 O.R. (3d) 82 aff’d [2000] O.J. 2217

(C.A.), the Ontario Superior Court of Justice interpreted a group insurance policy issued by

Canada Life to the insured’s employer. The Ontario Superior Court of Justice followed the

leading decision of Consolidated-Bathurst Export Ltd. v. Mutual Boiler and Machinery

Insurance Co., above.

32. In Canada Life Assurance Co., the Court found that the policy exclusion was not

“perfectly clear that they were qualifying a risk” and so it should be interpreted against the

insurer:

14 As the policy in its exclusions does not mention specifically severance pay, I find that Canada Life did not make it perfectly clear that they were qualifying a risk. The structure of the policy referred to by Canada Life at the hearing that consists of a clause stating a lump sum payment can be converted to payments on a monthly basis applies to the existing sources subject to integration level enumerated in paragraphs 1 to 9. That clause, therefore, does not help me to interpret the policy. 15 The policy is therefore ambiguous and I proceed to step 2 in resolving the ambiguity against Canada Life who has inserted it and who is now relying on it. Canada Life in the words of Mr. Justice Estey has not proven that "the words clearly and aptly describe the contingency that has in fact risen".

33. The Ontario Court of Appeal unanimously upheld the Superior Court of Justice’s

decision in Canada Life Assurance Co.

34. In Milner v. Manufacturer’s Life Insurance Company, 2006 BCSC 1571 at para. 7, the

British Columbia Supreme Court followed Canada Life Assurance Co. and applied the principle

of contra proferentem in the case of a group insurance policy in a “manner favourable to the

- 10 -

(Response Written submissions - Manuge Questions of Law3.DOC)

insured because it is within the insurer’s power to be as clear as it wants to be when trying to

limit the risk.”

35. In Milner, the Court even found that it was probably the insurer’s intention to include the

amount at issue in the reduction provision, but the Court found for the insured because the

insurer failed to clearly state that intention in the group policy:

[15] ...[Canada Life Assurance Co.] is instructive because, similarly to the case at bar, one could probably infer that it was Canada Life's intention to include severance pay as a lump sum settlement received in lieu of income from any employment. However, because it was not more clearly stated, the Court refused to accept it as fact.

III. CONCLUSION

[16] Given that I cannot resolve the ambiguity in Manulife's policy, I move to step two of the interpretative process, the application of the contra proferentem rule. Under this doctrine I interpret the policy in the manner which is favourable to Ms. Milner and, as a result, the payments to her from Athabasca University will not be deductible as "other income" under the policy.

36. In Abdulrahim v. Manufacturers Life Insurance Co. (2003), 65 O.R. (3d) 543, the Ontario

Superior Court of Justice considered a long term disability policy issued by an insurer to the

plaintiff’s employer. The Court thoroughly discussed the principles of insurance contract

interpretation and found that contra proferentem applied to resolve the matter in favour of the

plaintiff:

[60] In the case at bar, the insurer will be held responsible for the manner in which the exclusion clause has been worded and the exclusion clause will be interpreted narrowly: see Reid Crowther, supra, and Somersall, supra. [...] [64] In short, the principles of contractual interpretation with respect to insurance contracts and the substantive pr inciples of insurance law lead me to interpret this exclusion provision against the insurer. Contra proferentem applies in this case: the meaning of the expression "benefits the Employee receives or is entitled to receive" is interpreted in favour of the plaintiff.

37. In Healy v. Pilot Insurance Co. (2003),68 O.R. (3d) 741, the Ontario Superior Court of

Justice applied the principle of contra proferentem to the benefit of the plaintiff even though the

plaintiff was not a party to the insurance contract. The insurance contract was between the

insurer and the property owner, who mortgaged the property to the plaintiff. The plaintiff was

- 11 -

(Response Written submissions - Manuge Questions of Law3.DOC)

named on the policy as a mortgagee. The Ontario Superior Court of Justice applied contra

proferentem to resolve the ambiguity in favour of the plaintiff.

38. The Plaintiff could only find one case where it was even argued that the 1998 Eli Lilly

decision should be applied in the group insurance policy context. In Ruffalo v. Sun Life

Assurance Co. of Canada, [2007] O.J. No. 4541, the Ontario Superior Court of Justice expressly

questioned (but, as it was not necessary in that case, did not decide on) the relevance of the Eli

Lilly decision in the context of a long term disability pension. The Defendant relies heavily on

the Ruffalo case elsewhere in its factum, but fails to mention the Court’s concern on this point:

[79] Sun Life concedes that Mr. Ruffolo and Ms. Lepage may enforce the group insurance policies. However, relying on Eli Lilly & Co. v. Novopharm Ltd., [1998] 2 S.C.R. 129 at para. 53, Sun Life submits that where the contracting parties agree as to the interpretation of the contract, a third party cannot assert an interpretation designed to defeat the contractual intentions of the contracting parties and that it is not open to the third party to assert that the contra proferentem rule should be applied. [80] In the circumstances where the claimants have rights under s. 201 of the Insurance Act, I am not impressed with this argument by Sun Life , but given that, as I will shortly explain, I agree with Sun Life's interpretation of the insurance contracts, it is not necessary for me to decide whether Sun Life's argument is correct. For the purposes of deciding this case, I am going to assume that Mr. Ruffolo and Ms. Lepage are entitled to make any interpretative argument that would be available to a contracting party with privity of contract. [Emphasis added]

39. The Defendant’s approach would eliminate the doctrine of contra proferentem from the

interpretation of long term disability group insurance contracts. The Defendant’s interpretation

would undermine the purpose of contra proferentem, which is intended in part to address

unequal bargaining power and the generally adhesionary nature of insurance contracts.

40. In the current case, there was extremely unequal bargaining power between the

Defendant and the Plaintiff and all members of the Canadian Forces. The SISIP LTD Plan was

imposed on the Plaintiff. The Plaintiff was required by the Queen’s Regulations and Orders to

pay for and be insured under the SISIP Policy. The members of the Canadian Forces had no

input into the terms of the SISIP Policy and were left to rely solely on the wording of the SISIP

Policy as drafted by the Defendant.

41. Furthermore, the principle of contra proferentem is only one of several interpretive

techniques that can be applied in the current case. The Defendant fails to address the separate

- 12 -

(Response Written submissions - Manuge Questions of Law3.DOC)

principles that courts must apply in insurance contracts: (1) coverage provisions should be

construed broadly and exclusion clauses narrowly; and (2) the reasonable expectations of the

parties should be considered.

42. In Reid Crowther & Partners Ltd. v. Simcoe & Erie General Insurance Co., [1993] 1

S.C.R. 252 at pp. 268-69, Justice McLachlin (as she then was) explained the principles of

interpretation that apply to interpreting insurance contracts:

In each case the courts must examine the provisions of the particular policy at issue (and the surrounding circumstances) to determine if the events in question fall within the terms of coverage of that particular policy. This is not to say that there are no principles governing this type of analysis. Far from it. In each case, the courts must interpret the provisions of the policy at issue in light of general principles of interpretation of insurance policies, including, but not limited to:

(1) the contra proferentem rule; (2) the principle that coverage provisions should be construed broadly and exclusion clauses narrowly; and (3) the desirability, at least where the policy is ambiguous, of giving effect to the reasonable expectations of the parties.

43. The principle that coverage provisions should be construed broadly and exclusion clauses

narrowly applies separate and apart from the principle of contra proferentem.9

44. In Sweet and Sweet v. Co-operative Fire and Casualty Company, the New Brunswick

Court of Appeal held that payments made to the disabled insured by his union were based on a

set amount and not based on lost wages. These union payments did not constitute a wage or

salary continuation plan and were not covered by the exclusion clause, which had to be construed

narrowly.

45. The principle that coverage provisions should be construed broadly and exclusion clauses

narrowly should be applied here. The Defendant’s proposed interpretation takes the opposite

approach: a coverage provision (section 23) is interpreted narrowly and an exclusion provision

(section 24(a)(iv)) is interpreted broadly.

9 Sweet and Sweet v. Co-operative Fire and Casualty Company, (1983), 46 N.B.R. (2d) 189 (C.A.) at para. 9; Madill v. Chu, [1977] 2 S.C.R. 400 at 405; Goos v. Non-Marine Underwriters, Lloyd’s London, [1997] O.I.C.D. No. 75 at para. 30.

- 13 -

(Response Written submissions - Manuge Questions of Law3.DOC)

46. The Plaintiff refers to paras. 138-140 of its factum on the reasonable expectations of the

parties. The Members had a reasonable expectation that the SISIP LTD Plan, an income

replacement plan that they paid into their entire careers, would provide them with income

replacement. The Members also had a reasonable expectation that their income replacement plan

would be nullified if their disability was so severe that it merited a large Pension Act disability

pension.

The Defendant states that the SISIP LTD policy allows for the reduction of a Member’s income and income replacement. But the Pension Act disability pension is neither income nor income replacement. 47. Based on the purpose and wording of the SISIP LTD Plan, the Plaintiff submits that

“monthly income benefit” in section 24 should mean income or income replacement amounts. As

discussed below, the Defendant appears to support this interpretation.10

48. The Defendant asserts that “‘income’ can have many meanings”. 11 However, the

Defendant does not put forward any definition of either “income” or “monthly income benefit”

in its factum. The Defendant does not cite any dictionary or case law (outside of the Federal

Child Support Guidelines context) that informs us of its interpretation of “income” or “monthly

income benefit”.

49. When drafting the SISIP LTD Plan, the Defendant was entitled to define any term to

ascribe a particular meaning to it. In fact, the SISIP Policy General Provisions and the Part III –

Post-November 30, 1999 SISIP LTD Plan specifically define twenty and fourteen terms,

respectively. However, neither of the definition sections define either “income” or “monthly

income benefit”.12

50. The Defendant submits that the use of the phrase “monthly income benefits” elsewhere in

the SISIP LTD Plan indicates that the parties have “ascribed their own particular meaning to a

contractual term”. However, in its factum, the Defendant does not inform us of that alleged

particular ascribed meaning of “monthly income benefit”.

10 André Bouchard Affidavit, paras. 32-35. 11 Defendant’s Factum, para. 28. 12 Agreed Statement of Facts, pages 3-6 and 31-33.

- 14 -

(Response Written submissions - Manuge Questions of Law3.DOC)

51. As the Defendant does not define the term in the SISIP LTD Plan or provide the alleged

ascribed meaning of “monthly income benefit” in its factum, it is necessary to consider

admissions in André Bouchard’s January 3, 2008 affidavit to ascertain the Defendant’s position.

52. Mr. Bouchard explains that the SISIP LTD payment is solely for a Member’s income

replacement (and not compensation for the gravity of one’s injuries), and is to be reduced by the

amount of a Member’s “income or income replacement”:

32. SISIP LTD is an income replacement scheme ...It exists to ensure that, accounting for all specified sources of income or income replace ment, an eligible member will be guaranteed to receive 75% of salary at time of release. [...]

33. The SISIP LTD benefit is an insurance program; it is not a compensatory scheme. Disabled released members of the CF receive SISIP benefits in order to replace a portion of their lost income. [...]

34. The set-off provision was implemented as part of SISIP when it was first created because it is required for the proper functioning of a disability insurance scheme. It is designed to operate in conjunction with other sources of income the employee may have, and other specified income replacement programs that they may be entitled to, rather than in addition to those sources. This is because if an employee is entitled to multiple sources of income replacement operating independently of one another, that disabled employee could theoretically receive more funds in income replacement than he or she ever earned as an employee. For example, an employee who is able to receive benefits independently from many government benefit programs could effectively receive more than 100% of his or her former income.

53. The Plaintiff agrees with Mr. Bouchard that the SISIP LTD payment is an income

replacement benefit. The Plaintiff further agrees that the SISIP LTD payment is only to be

reduced by income or income replacement amounts as provided in the Plan.

54. As stated above, based on the purpose and wording of the SISIP LTD Plan and Mr.

Bouchard’s affidavit, the Plaintiff submits that “monthly income benefit” should mean income or

income replacement amounts.

55. The Pension Act disability pension is not income or income replacement and therefore is

not a “monthly income benefit” and does not meet the requirements of section 24(a)(iv). Rather

the Pension Act disability pension is a non-indemnity payment designed to provide compensation

- 15 -

(Response Written submissions - Manuge Questions of Law3.DOC)

for pain and suffering and to recognize the service and sacrifice of the members of the Canadian

Forces.13

56. In its factum, the Defendant does not dispute the Plaintiff’s submissions that the Pension

Act disability pension is not income replacement. Outside of this litigation, the Defendant has

repeatedly acknowledged that the Pension Act disability pension is not income replacement. The

Plaintiff provides three examples in its factum, including the Veterans Affairs Canada’s

Reference Paper The Origins and Evolution of Veterans Benefits in Canada 1914-2004:

Many of these complaints were grounded in the common misbelief [sic] that disability pensions are a form of income replacement, when in fact they are intended to provide compensation for reductions in the quality, and sometimes the quantity, of life experienced by the disabled.14

Unlike the Pension Act disability pension, other SISIP LTD reductions are income or income replacement benefits.

57. The Defendant notes that section 23 of the SISIP LTD Plan uses the term “monthly

income benefit”. The use of the term “monthly income benefit” in section 23 is consistent with

the Plaintiff’s above interpretation, as the sole nature and purpose of the section 23 payment is to

provide income replacement to former members of the Canadian Forces who are discharged due

to a disability.15

58. The Defendant asserts that the parties have ascribed a particular meaning to the term

“monthly income benefit” in the SISIP LTD Plan by using that term in the reduction provision

applicable to reservists. The Defendant does not inform us of that particular ascribed meaning.

59. The Defendant asserts that the SISIP LTD Plan “deems payments under Workers

Compensation plans, the Canadian Forces Superannuation Act and the Government Employees’

Compensation Act to be ‘monthly income benefits’”.16

60. The SISIP LTD Plan does not “deem” payments under these sources to be “monthly

income benefits”. Rather, the Plan states that “monthly income benefits” (i.e. income or income 13 The Plaintiff refers to paras. 49-76 of its Factum for its submissions on this point. 14 Affidavit of Sergeant (retired) John G. Bartlett, Exhibit B, Page 8.; see also November 24, 2005 letter written to Sgt. Bartlett, Vice Admiral, G.E. Jarvis, Assistant Deputy Minister (Human Resources – Military), Affidavit of Sergeant (retired) John G. Bartlett, Exhibit A, Page 2; Veterans Affairs Canada website, Affidavit of Sergeant (retired) John G. Bartlett, Exhibit C, Page 13. 15 André Bouchard Affidavit, paras. 32-35. 16 Defendant’s Factum, para. 30.

- 16 -

(Response Written submissions - Manuge Questions of Law3.DOC)

replacement) from these sources are to cause a reduction. If one or more of these sources do not

provide “monthly income benefits”, than the SISIP LTD Plan does not allow for a reduction.

61. Further, in contrast to the Pension Act disability pension, the sources listed by the

Defendant are all, wholly or partially, income replacement payments and are all included in

computing a taxpayer’s income under the Income Tax Act.

In order for the Court to consider whether or not the parties have ascribed their own particular meaning to a word, there must be an ambiguity in the wording of the contract. If the SISIP LTD Plan is ambiguous, contra proferentem applies and the ambiguity must be interpreted in favour of the Plaintiff.

62. The Defendant does not indicate whether or not it considers section 24(a) to be

ambiguous. However, the Defendant argues two interpretive techniques that are only available if

there is an ambiguity. There is no ambiguity in the current case: the Pension Act disability

pension is not a monthly income benefit.

63. Although neither of the definition sections in the general SISIP Policy or Part III – Post-

November 30, 1999 SISIP LTD Plan defines “income” or “monthly income benefit”, the

Defendant asserts that the term “monthly income benefit” has nonetheless been given an ascribed

meaning in the SISIP LTD Plan. The Defendant fails to explain that particular ascribed meaning.

64. To support this proposition, the Defendant cites the 1837 English case of Lloyd v. Lloyd,

(1837) 2 My. & Cr. 192.17 In Lloyd, Lord Chancellor Cottenham states that the Court will

consider that “the parties have themselves furnished a key to the meaning of the words used”

only if two requirements are met: the provisions and expressions of the contract are

contradictory, and if the real intention of the parties appears upon the face of the instrument:

If the provisions are clearly expressed, and there is nothing to enable the Court to put upon them a construction different from that which the words import, no doubt the words must prevail; but if the provisions and expressions be contradictory, and if there be grounds, appearing upon the face of the instrument, affording proof of the real intention of the parties, then that intention will prevail against the obvious and ordinary meaning of the words. If the parties have themselves furnished a key to the meaning of the words used, it is not material by which expression they convey their intention. [Emphasis Added]

17 Defendant’s Factum, para. 31.

- 17 -

(Response Written submissions - Manuge Questions of Law3.DOC)

65. In Lloyd, Lord Chancellor Cottenham held that an ambiguity is required before

considering the ascribed meaning of a contractual term. It is unclear if the Defendant submits

that there are “contradictory provisions and expressions” in the SISIP LTD Plan, which are

necessary before the Court can consider “if there be grounds, appearing upon the face of the

instrument, affording proof of the real intention of the parties”. If so, the Defendant has not met

the onus of showing that section 24(a)(iv) clearly and aptly provides for the reduction of the

Pension Act disability pension. Also, the doctrine of contra proferentem would apply to resolve

the ambiguity in the Plaintiff’s favour.

66. Furthermore, “it is not enough for the defendant to make out a possible intention

favourable to his view; he must shew a reasonable certainty that the intention is such as he

suggests.”18 That standard is certainly not met.

Subsequent conduct of the parties is only admissible if there is an ambiguity. If the SISIP LTD Plan is ambiguous, contra proferentem applies and the ambiguity must be interpreted in favour of the Plaintiff.

67. The Defendant submits that the subsequent conduct of the parties is admissible when

interpreting the SISIP LTD Plan.19 The Defendant again fails to note that the court must find first

that there is an ambiguity before admitting evidence of subsequent conduct.

68. The Defendant cites Montreal Trust Co. of Canada v. Birmingham Lodge Ltd. (1995), 24

O.R. (3d) 97 at para. 23 for the proposition that subsequent conduct can be considered by the

Court. However, the Defendant fails to mention para. 24 of Montreal Trust Co. of Canada where

the Court quoted the following passage from the Supreme Court of Canada:

24 Lambert J.A. discussed the relevance of subsequent conduct in Canadian National Railways v. Canadian Pacific Ltd., [1979] 1 W.W.R. 358 at p. 372, 95 D.L.R. (3d) 242 (B.C.C.A.), affirmed (1979), 105 D.L.R. (3d) 170, [1979] 6 W.W.R. 96 (S.C.C.):

In Canada the rule with respect to subsequent conduct is that, if, after considering the agreement itself, including the particular words used in their immediate context and in the context of the agreement as a whole, there remain two reasonable alternative interpretations , then certain additional evidence may be both admitted and taken to have legal

18 Re Fischbach & Moore of Canada Ltd. and Noranda Mines Ltd. (1971), 19 D.L.R. (3d) 329 (Sask. C.A.) at para. 9 quoting Pannell v. Mill, (1846), 3 C.B. 625 at p. 638, 136 E.R. 250 at p. 255.

19 Defendant’s Factum, para. 32.

- 18 -

(Response Written submissions - Manuge Questions of Law3.DOC)

relevance if that additional evidence will he lp to determine which of the two reasonable alternative interpretations is the correct one. It certainly makes no difference to the law in this respect if the continuing existence of two reasonable alternative interpretations after an examination of the agreement as a whole is described as doubt or an ambiguity or as uncertainty or as difficulty of construction. [Emphasis Added]

See also Arthur Andersen Inc. v. Toronto-Dominion Bank (1994), 17 O.R. (3d) 363 at p. 372 (C.A.)

69. The Court in Montreal Trust at para. 24 also referred to Arthur Andersen Inc. v. Toronto-

Dominion Bank (1994), 17 O.R. (3d) 363 at p. 372 (C.A.) leave ref’d [1994] S.C.C.A. No. 189.

In Arthur Andersen, the Ontario Court of Appeal similarly held that an ambiguity is necessary to

admit evidence subsequent conduct:

First, the words of the contract must be analyzed “in its factual matrix”, and a conclusion arrived at that there are two possible interpretations of the contract. Then, and only then, may the trial judge look at other facts , including facts leading up to the making of the agreement, circumstances existing at the time the agreement was made, and evidence of subsequent conduct of the parties to the agreement. [Emphasis Added]

70. Again, it is unclear if the Defendant submits that there is an ambiguity in the wording of

the SISIP LTD Plan necessary for the admission of subsequent conduct. If so, the doctrine of

contra proferentem should apply to resolve the ambiguity in the Plaintiff’s favour.

71. Further, the only evidence of subsequent conduct is that the Plaintiff Class members’

SISIP LTD benefits have been reduced by the amount of their respective Pension Act disability

pension. In effect, the Defendant is defending the allegation that it is improperly reducing SISIP

LTD benefits by stating that it has similarly reduced SISIP LTD benefits in the past.

72. The Defendant also refers to a document signed by Mr. Manuge in June 30, 2003 in order

to receive any of his SISIP LTD payment.20 Again, this document is not admissible unless there

is an ambiguity in the SISIP LTD Plan.

73. Even if this document is admissible, it is unclear how it supports the Defendant’s

position. At the time that Mr. Manuge signed this document, he had been involuntarily

discharged from the Canadian Forces by the Defendant because he became disabled as a result of

his service. Mr. Manuge had no income following his discharge and needed to sign this

20 Defendant’s Factum, para. 57.

- 19 -

(Response Written submissions - Manuge Questions of Law3.DOC)

document to access the long term disability income replacement that he had paid for his entire

career. To suggest that this was conduct by Mr. Manuge affirming his view of the correctness of

the Defendant’s proposed legal interpretation of a particular section of the SISIP Plan is artificial

in the extreme.

The only cases cited by the Defendant are in the context of the Federal Child Support Guidelines, which has a different purpose and broad definition of “income” in order to maximize child support. 74. Even though it is the Defendant’s onus to prove that the wording in section 24 clearly and

aptly allows for a reduction based on the Pension Act disability pension21, the Defendant does

not make any submissions on the purpose and nature of the Pension Act disability pension. The

Defendant appears to acknowledge that the Pension Act disability pension is not considered

income in at least some contexts.

75. At para. 35, the Defendant submits that “whatever the basis on which the Pension Act

disability pension is paid, it is considered ‘income’ in some contexts.” [Emphasis added] In

support of its submission, the Defendant refers to only one context: the Federal Child Support

Guidelines SOR/97-175.

76. The Federal Child Support Guidelines are regulations made pursuant to the Divorce Act.

The Federal Child Support Guidelines expressly state that one of the objectives of the Guidelines

is to ensure that the children benefit from the financial means of both spouses after separation:

Objectives 1. The objectives of these Guidelines are:

(a) to establish a fair standard of support for children that ensures that they continue to benefit from the financial means of both spouses after separation; [...]

Objectifs 1. Les présentes lignes directrices visent à:

(a) établir des normes équitables en matière de soutien alimentaire des enfants afin de leur permettre de continuer de bénéficier des ressources financières des époux après leur séparation;

21 See Consolidated-Bathurst Export Ltd. v. Mutual Boiler & Machinery Insurance Co., above.

- 20 -

(Response Written submissions - Manuge Questions of Law3.DOC)

77. The Federal Child Support Guidelines define “income” in sections 15-20. Section 19

allows the Court to impute income where the parent ’s income is unreflective of their ability to

contribute to the maintenance of a child.22

78. In Dahlgren v. Hodgson, 1999 ABCA 23, the Court imputed the ex-husband’s workers’

compensation benefits as income for the purposes of the Federal Child Support Guidelines. In

Dahlgren, the Court relied on the very broad definition of income in the Federal Child Support

Guidelines. The Defendant excerpts a portion of a sentence from the Dahlgren decision, failing

to include the Court’s full sentence that clearly distinguishes it from the current case:

[4] The definition of “income” in the Child Support Guidelines is very broad and clearly encompasses these benefits. That definition reflects Parliament’s intention that in dealing with a parent’s obligation to support a child, it is fair and appropriate to take into account many forms of income, or benefits, or compensation, or attributed income, benefits or compensation, etc. that would not otherwise be treated as taxable income under the Income Tax Act. [Emphasis added to portion not included in the Defendant’s factum.]

79. In Marbach v. Marbach, 2008 ABQB 516, the Court followed Dahlgren and other cases

that considered the Federal Child Support Guidelines’ broad definition of “income”.

80. While the Federal Child Support Guidelines contain a very broad definition of income,

the SISIP LTD Plan does not define income. The SISIP LTD Plan certainly does not allow for

the imputation of income.

81. Further, the purpose and nature of the Federal Child Support Guidelines is completely

different than the purpose of a LTD income replacement plan. The express purpose of the

Federal Child Support Guidelines is “to establish a fair standard of support for children that

ensures that they continue to benefit from the financial means of both spouses after separation.”

The purpose of the SISIP LTD Plan is to provide income replacement to Members who are

medically released from the Canadian Forces due to a disability.23

82. To invoke a generous purposive approach created to protect children to support an ability

to pay less to Canada’s disabled veterans is highly dubious.

22 See Peterson v. Horan, 2006 SKCA 61. 23 André Bouchard Affidavit, paras. 32-35.

- 21 -

(Response Written submissions - Manuge Questions of Law3.DOC)

The Pension Act disability pension may be a “benefit”, but it is not an “income benefit”. 83. The Defendant submits that the Pension Act disability pension is a monthly “benefit” and

therefore should be considered a “total monthly income benefit”.

84. The Plaintiff agrees that the Pension Act disability pension is a “benefit”. The Defendant

agrees that the Pension Act disability pension is properly considered where the SISIP LTD Plan

reduces “any benefit amount payable to the beneficiary under the Pension Act” (section 7(a))24

and “any monthly benefits payable pursuant to the Pension Act” (section 64)25. The fact that the

SISIP Policy uses these phrases without the qualifier “income” requires that the use of the term

income in subsection 24(a)(iv) be given its intended, and distinct, effect.

85. The Defendant submits that the Court should ignore the word “income” in subsection

24(a)(iv) at the same time that it argues that no term should be rendered meaningless. The

Defendant is trying to have it both ways.

86. The Defendant states that “total”, “monthly” and “income” are merely descriptive and

“benefits” is the core of the phrase. Using that logic, a onetime lump sum benefit to compensate

for pain and suffering would meet the definition of “total monthly income benefit”. That is a

manifestly unfair result. That result is contrary to the principle that insurance contracts should be

interpreted in accordance with the language used and that the insurer must use words that clearly

and aptly provide for a limitation of risk.26

87. Further, the Defendant’s submission that “total”, “monthly” and “income” are merely

descriptive and “benefits” is the core of the phrase is also contrary to Mr. Bouchard’s

explanation in his affidavit why the New Veterans Charter disability pension (which replaced the

Pension Act disability pension) is not included:

27. In 2006, the CF Members and Veterans Re-establishment and Compensation Act (“New Veterans Charter”) came into force, which replaced the monthly payments made under the PA with a one-time, lump sum payment. Because these lump sum payments are not a “monthly income benefit” within the meaning of s. 24(a)(iv) of the Policy, they are not deducted from SISIP LTD benefits. [Emphasis Added]

24 Agree Statement of Facts, page 17. 25 Agreed Statement of Facts, page 26. 26 See Consolidated-Bathurst Export Ltd., above, and Canada Life Assurance Co., above.

- 22 -

(Response Written submissions - Manuge Questions of Law3.DOC)

88. There are several other benefits under the Pension Act : pensions for death, Prisoner of

War compensation, exceptional incapacity allowance, and wear and tear on an amputee’s

clothing. None of these payments cause a reduction under s. 24(a)(iv) and rightfully so, as none

of these payments are “monthly income benefits” either.

The Pension Act disability pension has been offset by the Defendant in other circumstances, but the Defendant has used clear, unambiguous language in those case. 89. The Plaintiff has submitted that the SISIP LTD reduction has an inequitable and unfair

result contrary to the reasonable commercial expectation of the members.27 Both the House of

Commons and Senate Subcommittee of Veterans Affairs have concurred that the SISIP LTD

reduction is “unfair”.28

90. However, contrary to the Defendant’s assertion29, the Plaintiff has not stated in this

motion that the Pension Act disability pension can never cause a reduction to another benefit.

Rather, the Plaintiff submits that there is no contractual basis to reduce the Plaintiff’s SISIP LTD

benefit based on the Pension Act disability pension in this case.

91. As noted in the Defendant’s factum30, the Pension Act disability pension is offset in

legislation, namely the War Veterans Allowance Act, and the earnings loss benefit and income

support benefit under the Canadian Force Members and Veterans Re-establishment and

Compensation Act.

92. It is instructive to look at the language used by Parliament and Governor in Council to

describe and offset the Pension Act disability pension under the Canadian Force Members and

Veterans Re-establishment and Compensation Regulations:

22. The following sources are prescribed for the purpose of the amount of variable B in subsection 19(1) of the Act:

(a) disability pension benefits payable

22. Dans la détermination de l’élément B de la formule figurant au paragraphe 19(1) de la Loi, les sommes exigibles d’une source réglementaire sont les suivantes :

(a) la pension d’invalidité à verser en

27 Plaintiff’s Factum, paras. 119-126. 28 Standing Senate Committee on National Security and Defence, “Report on Reductions of Service Income Security Insurance Plan Long Term Disability Benefits”, (18 June 2008); and House of Commons of Canada motion (7 November 2006). 29 Defendant’s Factum, para. 60 30 Para. 59-60, and Plaintiff’s Factum, para

- 23 -

(Response Written submissions - Manuge Questions of Law3.DOC)

under the Pension Act; vertu de la Loi sur les pensions;

37. For the purposes of section 37 of the Act, the prescribed sources of current monthly benefits are:

(c) disability pension benefits payable under the Pension Act, the Royal Canadian Mounted Police Pension Continuation Act or the Royal Canadian Mounted Police Superannuation Act other than amounts payable in respect of dependant children;

37. Pour l’application de l’article 37 de la Loi, les avantages mensuels réglementaires sont les suivants :

c) la pension pour invalidité versée en vertu de la Loi sur les pensions, de la Loi sur la continuation des pensions de la Gendarmerie royale du Canada ou de la Loi sur la pension de retraite de la Gendarmerie royale du Canada à l’exclusion de la fraction de la pension versée pour le compte d’un enfant à charge;

93. It is also instructive to look at the language used by the Defendant to describe and offset

the Pension Act disability pension under the War Veterans Allowance Act: “the current monthly

benefits, if any, payable under the Pension Act.”

94. By using this language to describe the Pension Act disability pension, the Defendant has

clearly indicated its view of the purpose and nature of the Pension Act disability pension. It also

indicates the clear language that the Defendant has used, and continues to use, to reduce the

amount of the Pension Act disability pension from another amount. The Defendant could have

used this clear language when limiting its coverage in the SISIP LTD Plan.

Question 2: In the alternative, if the Defendant’s interpretation of s. 24 is correct, then the pension payments must be treated as “monthly pay in effect on the date of release from the Canadian Forces” as that term is described in section 23(a) of Part III(B) of S.I.S.I.P. Policy 901102. 95. Unlike the term “monthly income benefit”, the term “monthly pay” has been defined in

the SISIP Policy. In fact, “monthly pay” has been defined twice: once in the General Provisions

and once specifically for Part III(B) – Post-November 30, 1999 Long Term Disability Insurance

Plan. This further demonstrates that if the Defendant intended to ascribe a particular meaning to

“monthly income benefit”, it could have easily done so.

- 24 -

(Response Written submissions - Manuge Questions of Law3.DOC)

96. Part III(B) – Post-November 30, 1999 Long Term Disability Insurance Plan defines

“monthly pay” for the purposes of that Part:

For the purposes of this Part III(B), the following terms shall have the meanings set forth below:

(g)(i) For members defined at Section 1.f(i) and Section 1.f.(v), “monthly pay” or “monthly salary” shall mean the rate of pay at date of release from the Canadian Forces. [Emphasis added]

97. It is instructive to note that Part III(A) - Pre-November 30, 1999 Long Term Disability

did not define “monthly pay”. The November 30, 1999 timing of this new definition is

instructive because it approximately corresponds with the 2000 enactment of Bill C-41 that

allowed all Canadian Forces members to receive the Pension Act disability pension while they

were still serving.

98. In contrast to Part III(A) - Pre-November 30, 1999 Long Term Disability, the SISIP

Policy’s General Provisions define “monthly pay” with specific reference to the Queen’s

Regulations and Orders Chapter 204 pay tables:

The following terms shall have the meanings set forth below: (i.) “Monthly pay” or “monthly salary” shall mean the member’s rate of pay specified in QR and O Chapter 204 pay tables for Regular Forces Personnel.

99. The Defendant submits that the Court should apply the SISIP Policy’s interpretation in its

General Provisions rather than the clause that is specifically applicable to Part III(B). At the

same time that the Defendant argues that every term should be given meaning, the Defendant

seeks to render the specific definition of “monthly pay” in Part III(B) – Post-November 30, 1999

Long Term Disability Insurance Plan meaningless.

100. In Morton et al. v. Rabito et al. (1998), 42 O.R. (3d) 161, the Ontario Court of Appeal

interpreted the Insurance Act, which had two different definitions of “automobile”: one definition

was in the general provisions of the Act and one definition was in the part of the Act specifically

applicable to automobile insurance:

But if it is legitimate to have recourse to the Insurance Act in order to inform the meaning of "automobile" in the Morton automobile insurance policy, the appropriate definition to

- 25 -

(Response Written submissions - Manuge Questions of Law3.DOC)

consider must surely be the definition found in that Part of the statute that deals specifically with automobile insurance, that is, Part VI. Regele holds that, in a case to which Part VI of the Insurance Act is applicable, the definition in s. 224(1) takes precedence over the definition in s. 1.

101. Similarly, in the current case, the definition of “monthly pay” specific to Part III(B)

should apply to the interpretation of “monthly pay” in that Part.

102. The question is then whether or not the Pension Act disability pension is part of the

member’s “rate of pay”. The Defendant’s interpretation is that the Pension Act disability pension

is a “monthly income benefit”, but not part of the member’s “rate of pay” is contradictory.

Further, it is contrary to the principle that coverage provisions in insurance policies should be

interpreted broadly and exclusion clauses should be interpreted narrowly. The Plaintiff Class

refers to paragraphs 141-151 of its factum for its complete submissions on this issue.

- 26 -

(Response Written submissions - Manuge Questions of Law3.DOC)

PART IV: ORDER SOUGHT

103. The Plaintiff Class respectfully submits that the questions of law raised in this motion

should be answered by this Honourable Court as follows:

1. Are the pension payments made pursuant to s. 21 of the Pension Act, “total monthly income benefits” as that term is described in section 24(a)(iv) of Part III(B) of S.I.S.I.P. Policy 901102?

No.

2. Are the pension payments made pursuant to s. 21 of the Pension Act, “monthly pay in effect on the date of release from the Canadian Forces” as that term is described in section 23(a) of Part III(B) of S.I.S.I.P. Policy 901102?

In the alternative, if the answer to the first question is yes, the Plaintiff Class respectfully submits that the answer to this question should also be yes.

104. The Plaintiff Class respectfully submits that no costs should be awarded on this motion.

The Plaintiff Class refers to Rule 334.39 of the Federal Court Rules, which deals with costs in a

class proceeding.

ALL OF WHICH IS RESPECTFULLY SUBMITTED.

DATED this 10th day of November, 2011.

________________________________________ Peter J. Driscoll, Ward K. Branch, Daniel F. Wallace Counsel for the Plaintiff Class

- 27 -

(Response Written submissions - Manuge Questions of Law3.DOC)

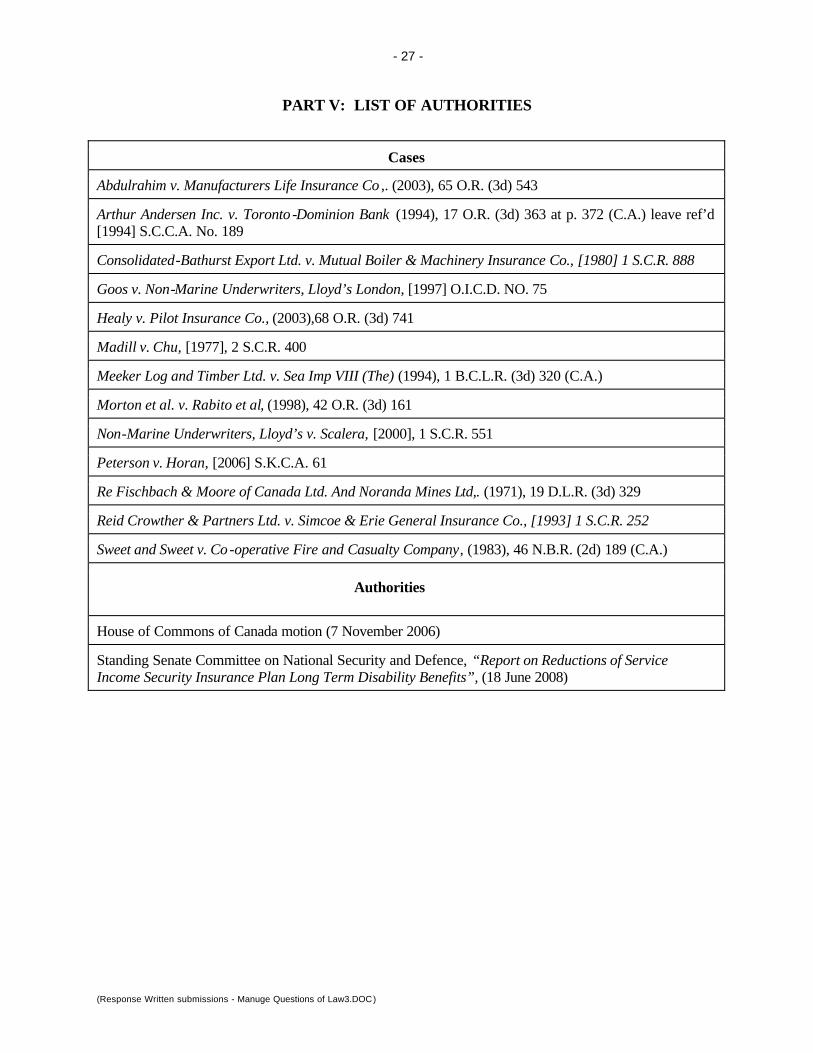

PART V: LIST OF AUTHORITIES

Cases

Abdulrahim v. Manufacturers Life Insurance Co ,. (2003), 65 O.R. (3d) 543

Arthur Andersen Inc. v. Toronto -Dominion Bank (1994), 17 O.R. (3d) 363 at p. 372 (C.A.) leave ref’d [1994] S.C.C.A. No. 189

Consolidated-Bathurst Export Ltd. v. Mutual Boiler & Machinery Insurance Co., [1980] 1 S.C.R. 888

Goos v. Non-Marine Underwriters, Lloyd’s London, [1997] O.I.C.D. NO. 75

Healy v. Pilot Insurance Co., (2003),68 O.R. (3d) 741

Madill v. Chu, [1977], 2 S.C.R. 400

Meeker Log and Timber Ltd. v. Sea Imp VIII (The) (1994), 1 B.C.L.R. (3d) 320 (C.A.)

Morton et al. v. Rabito et al, (1998), 42 O.R. (3d) 161

Non-Marine Underwriters, Lloyd’s v. Scalera, [2000], 1 S.C.R. 551

Peterson v. Horan, [2006] S.K.C.A. 61

Re Fischbach & Moore of Canada Ltd. And Noranda Mines Ltd,. (1971), 19 D.L.R. (3d) 329

Reid Crowther & Partners Ltd. v. Simcoe & Erie General Insurance Co., [1993] 1 S.C.R. 252

Sweet and Sweet v. Co-operative Fire and Casualty Company, (1983), 46 N.B.R. (2d) 189 (C.A.)

Authorities

House of Commons of Canada motion (7 November 2006)

Standing Senate Committee on National Security and Defence, “Report on Reductions of Service Income Security Insurance Plan Long Term Disability Benefits”, (18 June 2008)

- 28 -

(Response Written submissions - Manuge Questions of Law3.DOC)

Appendix A - Statutory Provisions

Canadian Forces Members and Veterans Re-establishment and Compensation Regulations, SOR/2006-50

22. The following sources are prescribed for the purpose of the amount of variable B in subsection 19(1) of the Act:

(a) disability pension benefits payable under the Pension Act; 37. For the purposes of section 37 of the Act, the prescribed sources of current monthly benefits are:

(c) disability pension benefits payable under the Pension Act, the Royal Canadian Mounted Police Pension Continuation Act or the Royal Canadian Mounted Police Superannuation Act other than amounts payable in respect of dependant children;

Règlement sur les mesures de réinsertion et d’indemnisation des militaires et vétérans des Forces canadiennes, DORS/2006-50

22. Dans la détermination de l’élément B de la formule figurant au paragraphe 19(1) de la Loi, les sommes exigibles d’une source réglementaire sont les suivantes :

a) la pension d’invalidité à verser en vertu de la Loi sur les pensions;

37. Pour l’application de l’article 37 de la Loi, les avantages mensuels réglementaires sont les suivants :

c) la pension pour invalidité versée en vertu de la Loi sur les pensions, de la Loi sur la continuation des pensions de la Gendarmerie royale du Canada ou de la Loi sur la pension de retraite de la Gendarmerie royale du Canada à l’exclusion de la fraction de la pension versée pour le compte d’un enfant à

Federal Child Support Guidelines SOR/97-175

Objectives 1. The objectives of these Guidelines are:

(a) to establish a fair standard of support for children that ensures that they continue to benefit from the financial means of both spouses after separation; [...]

Lignes directrices fédérales sur les pensions alimentaires pour enfants DORS/97-175

Objectifs 1. Les présentes lignes directrices visent à:

(a) établir des normes équitables en matière de soutien alimentaire des enfants afin de leur permettre de continuer de bénéficier des ressources financières des époux après leur séparation;

Federal Courts Rules

81. Contents of affidavits 81. (1) Affidavits shall be confined to facts within the deponent’s personal knowledge except on motions, other than motions for summary judgment or summary trial, in which statements as to the deponent’s belief, with the grounds for it,

Règles des Cours Fédérales

81. Contenu 81. (1) Les affidavits se limitent aux faits dont le déclarant a une connaissance personnelle, sauf s’ils sont présentés à l’appui d’une requête – autre qu’une requête en jugement sommaire ou en procès sommaire – auquel cas ils peuvent contenir

- 29 -

(Response Written submissions - Manuge Questions of Law3.DOC)

may be included.

Affidavits on belief (2) Where an affidavit is made on belief, an adverse inference may be drawn from the failure of a party to provide evidence of persons having personal knowledge of material facts.

des déclarations fondées sur ce que le déclarant croit être les faits, avec motifs à l’appui.

Poids de l’affidavit

(2) Lorsqu’un affidavit contient des déclarations fondées sur ce que croit le déclarant, le fait de ne pas offrir le témoignage de personnes ayant une connaissance personnelle des faits substantiels peut donner lieu à des conclusions défavorables.

- 30 -

(Response Written submissions - Manuge Questions of Law3.DOC)

Appendix B - Book of Authorities

Please see separately bound Supplementary Book of Authorities.