CEO Briefing 2014 The Business Agenda for Europe: Growth in a Digital …€¦ · CEO Briefing 2014...

24

CEO Briefing 2014 The Business Agenda for Europe: Growth in a Digital World Written by:

Transcript of CEO Briefing 2014 The Business Agenda for Europe: Growth in a Digital …€¦ · CEO Briefing 2014...

CEO Briefing 2014 The Business Agenda for Europe: Growth in a Digital World

Written by:

Business confidence is returning globally and many leaders are more optimistic about the outlook for their organisations, expressing bold ambitions for growth. While the European Union (EU) is slowly recovering from the recession, the impact of the euro zone crisis is still evident in the continually growing gap in competitiveness with other major global economies. Countries such as the United States and China have increased their investment in new digital technologies and innovation as a means to drive growth, while adoption in the major EU economies is lagging as these executives remain less convinced about digital and the impact it can have on their business.

With the impact of traditional levers such as fiscal and monetary policy currently limited, the EU finds itself in a unique set of circumstances in which digital presents itself as a powerful lever which can be effectively used to bridge the ever-widening competitiveness gap.

Digital technologies are enabling organisations to transform the way they do business, with opportunities to enhance their efficiency, create new ways of interacting with their customers and reduce the time from product design to market launch.

Accenture believes that enthusiastic adoption of digital technologies will make it possible for Europe to return to higher economic growth and reduce this widening global competitiveness gap. With its high penetration rates across Broadband, Mobile and smartphones as well as eGovernment services, the EU is in a good position to exploit its strong performance in the adoption of technology. In order to succeed in rebuilding competitiveness in both the short and long term however, Europe’s business and policy makers must take urgent steps to convert its strong digital potential into higher levels of productivity, innovation and growth.

The EU can become a leader in a new era of digital business. The time to act is now.

Foreword

2 Foreword

Jo DeblaereChief Operating Officer and Group Chief Executive – Accenture, Europe

3CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

While the economic outlook has been more positive in recent months, the European Union has yet to see a genuine, positive shift in the competitiveness of its economies. In order to stop the gap in European competitiveness growing and potentially gain ground, business leaders and policy makers will need to urgently address the two critical areas of productivity and innovation.

Europe is home to 14 of the world’s 50 largest companies. The region has a strong corporate base with significant capacity for innovation and advanced technology infrastructures. It also boasts a significant number of entrepreneurs and young businesses as well as a sophisticated consumer base, that tend to be experienced with and receptive to the use of a wide variety of technologies in their daily lives.

The potential impact of digital technologies on businesses and industries across the EU is hard to overstate. These disruptive technologies are breaking down industry boundaries and requiring organisations to reinvent themselves by developing or adapting to new business models. They are also fundamentally changing the behaviour of citizens and consumers, who exhibit a seemingly boundless appetite for all things digital. If embraced enthusiastically, digital technologies will enable new business outcomes, multi-channel customer experiences, digital customer interactions, digital sales, and digital channel distribution options.

EU companies also have ambitious overseas investment strategies for growth through the sale of new products and services to new customers – particularly in non-BRIC rapidly growing emerging markets. Despite this, the majority of EU executives confirm their digital investments are primarily focused on increasing productivity and internal efficiency to reduce costs. While cost is a necessary focus, executives may need to rebalance their investment to better support their ambitious growth plans. This will enable companies to generate new levels of innovation and growth to better serve customers and consumers that demand new products, services, and better experiences. Investment in people and organisational structure is also necessary in order to fully capitalise on implementation of new technologies.

The steps needed to close Europe’s competitiveness gap with their global counterparts will require a significant and concerted effort from business and government if Europe wants to replicate its historic success as the driving force of industrialisation and become a leader in the new era of the digital business. It’s time to seize the opportunity.

Introduction

Mauro Macchi Senior Managing Director – Accenture Strategy, Europe, Africa, Middle East and Latin America

The business landscape for Europe

4 The business landscape for Europe

As executives within the European Union (EU) evaluate the business landscape and shape their strategies regarding the year ahead, their optimism for the world’s economic prospects is more muted than that of their global peers according to a survey conducted by The Economist Intelligence Unit (EIU) for Accenture’s CEO Briefing 2014.

Furthermore, their enthusiasm for the capabilities of digital technologies is decidedly less pronounced than that of C-suite executives outside the EU. These two preoccupations may be interrelated as productivity growth in the EU languishes behind other major economies. The need to innovate and improve competitiveness is clear, but so far, this challenge has not been met with the urgency it deserves.

Within the five largest EU economies – Germany, UK, France, Italy and Spain – a wide diversity of views prevails. While 44 percent of executives globally are bullish on the world’s economic outlook, this rises to 48 percent among those from the UK but falls among those from Germany (30 percent), and France and Italy (both 31 percent), where optimism is decidedly weaker.1

For Italy, Luigi Ferraris, CFO at Enel Group, the European energy utility, sees improvement from the country’s poor GDP performance in 2013 and signs of a rise in the employment rate. However, for now he predicts continued challenges for the economy. “Poor competitiveness, labour market rigidity and tight credit conditions will continue to affect the economic outlook at least in the short term,” he says.

Meanwhile, 70 percent of executives based in Spain are optimistic about prospects in their home market in the next 12 months, compared with only just over half of those based in France (52 percent) and Italy (51 percent).2 This is perhaps surprising, given the continued impact of the economic crisis on the Spanish market. However, some leading executives see southern Europe’s prospects improving, as does Franck Cohen, President for Europe, the Middle East and Africa. “Last year, South Europe grew by double digits for SAP,” he says. “That’s a clear indication that people are investing.”

This is in line with analysis from the EIU, which sees subdued growth for Spain in the medium term, but signs of increased competitiveness as private consumption and gross fixed investment turn more positive.

When it comes to the outlook for profitability in their own companies, German executives are more confident than most – despite their caution on prospects for global economic growth – with 82 percent expecting increased profits over the next year, compared with 71 percent among their global peers.3

This is reflected in EIU forecasts, which recognise Germany’s economy as more resilient than those in the wider eurozone,

with a modest increase in GDP and a gradual firming of underlying demand after a weaker 2013. This upbeat view on profitability is also shared among executives from the UK (85 percent), who see increased profits in the coming 12 months.4 Steve Morriss, CEO of European operations at AECOM, a provider of professional technical and management support services to sectors ranging from energy to construction, is amongst those who see the UK’s outlook improving. “In our business, we see some of the earliest indicators for the return of confidence in private developments in building,” he says. “And there’s no doubt that’s really picking up in the UK.”

The consensus view among executives across these five countries is that manufacturing, energy and healthcare are likely to perform well in the coming year. However, there are some nuanced surprises with the automotive sector in France showing remarkable confidence. Consumer goods features prominently in the UK while the construction and real estate sector is frequently cited by executives based in Germany.5

5CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

1 Figure 1: Q1 3 Figure 2: Q4 5 Appendix: Q2

2 Figure 1: Q14 Figure 2: Q4

Figure 1: Q1 – In the next 12 months, to what extent are you optimistic or pessimistic about the prospects for the following. Percentage optimistic about the next 12 months:

Figure 2: Q4 – Thinking about your organisation in the next 12 months, do you expect the following to increase, decrease or stay the same? Expectations of profit growth in next 12 months:

Figure 2 source: Accenture, “CEO Briefing 2014 | The Global Agenda: Competing in a Digital World.” See: http://www.accenture.com/ceobriefing

Figure 1 source: Accenture, “CEO Briefing 2014 | The Global Agenda: Competing in a Digital World.” See: http://www.accenture.com/ceobriefing

0% 100%

Globalaverage

Germany

UK

France

Italy

Spain 64%

US 71%

China 93%

58%

63%

85%

82%

71%

0% 100%

Globalaverage

Germany

UK

France

Italy

Spain

US

China

44%

On their own organisation'sprospects

On the country wherethey are based

On the global economy

62%

30%69%

48%63%

31%52%

31%51%

42%70%

62%70%

59%76%

76%

80%

76%

69%

77%

72%

78%

89%

6 An ambitious push for growth

As EU companies emerge from the economic malaise of recent years, cost cutting remains on the agenda but the emphasis has changed.

An ambitious push for growth

Germany-based executives expect a year of increased reductions in costs but also see a period of workforce increases ahead - a difficult combination.6

But while cost reductions are still being implemented across major markets in the EU, the positioning is far more optimistic than in recent years. “Cost-cutting is not our focus,” says Mr Morriss. “A couple of years ago, we got our business into a position where it was able to make money in a depressed economy. But while you’re always looking for the odd efficiency here and there, we are absolutely in growth mode.”

Mr Cohen sees this approach being adopted broadly across the region. “My sense in western Europe is that people have been cutting costs for the past seven or eight years,” he says. “Now they are in a different mode – and they have to innovate to develop their business.”

Amongst the EU countries, the UK and Germany stand out for their more ambitious growth strategies. While globally 36 percent of respondents are aiming to sell new products or services to new customers, in their home markets with similar proportions in France, Italy and Spain, this rises to 50 percent amongst

UK-based executives and to 53 percent for those based in Germany.7 When it comes to export markets this difference becomes even more pronounced. For example, the proportion of executives aiming to grow by selling new products to new customers in overseas mature markets is 72 percent amongst German-based executives, and 63 percent among UK-based executives (compared with a 47 percent global average).8

Companies are also looking to invest where they see prospects for growth – and for many, that means focusing on emerging markets. “Emerging markets will continue their economic growth cycle, although some of them have been affected by a swift contraction in foreign funds and sharp currency depreciation,” says Mr Ferraris. He also sees the recovery in mature markets benefiting emerging economies.

Among EU respondents, Germany-based executives are more positive than their global peers 9 and (along with UK-based executives) have the most ambitious overseas investment strategies, particularly in non-BRIC (Brazil, Russia, India and China) rapidly growing emerging markets.

7CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

Figure 3: Q9c – Which of the following strategies will be most important to driving revenue growth in your company over the next three years? Outside your home market – Emerging markets growth strategy:

Fully 82 percent of Germany-based executives say they plan to shift their focus from BRIC countries towards other, more rapidly growing emerging markets, as do 74 percent of UK-based executives.10

Similarly, when it comes to their strategies in emerging markets, executives in Germany (82 percent) the UK (74 percent) emerge as the most ambitious in saying that selling new products and services to new customers is their strategy (versus 54 percent overall).11

For SAP, this strategy reflects demand from young companies that are developing rapidly. “Companies in emerging markets need the whole enchilada of the software we are selling because they have nothing today,” explains Mr Cohen. “European companies are equipped in basic functionality and are buying advanced products.”

For western European companies to compete in emerging markets, Mr Cohen argues that they need to be prepared to innovate. “They can’t outspend the guys in Asia,” he says. “So they have to outsmart them with innovation.”

More than most, Germany, the UK and Italy are responding to this need. Executives in these countries see research and development (R&D) investments as a critical part of their strategies. While overall, 80 percent of all executives surveyed are increasing their R&D investment in the coming year, this rises to 96 percent amongst Germany-based executives, 94 percent among Italy-based executives and 90 percent among UK-based executives.12

For Enel Group, investment strategies are shaped according to market demands and the pace of growth in each region. In mature markets, this means maximising cash flow, optimising the distribution network management, cutting costs and adding value through investments in smart grid technology.

By contrast, in emerging markets, the company plans to capitalise on population growth and urbanisation, as well as the expansion of access to electricity services and the development of traditional thermal generation as well as renewables. “The growth in emerging markets will be mainly seized through an increase in renewable capacity, in addition to conventional generation capacity in areas such as Latin America, to satisfy those countries’ fast-growing electricity needs,” says Mr Ferraris.

Figure 3 source: Accenture, “CEO Briefing 2014 | The Global Agenda: Competing in a Digital World.” See: http://www.accenture.com/ceobriefing

Globalaverage

Germany

UK

France

Italy

Spain

54% 15%17% 14%

82% 5%9%

74% 6%16%

61% 8%

18%25%47% 10%

18%51% 10% 21%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Selling new products/services to existing customers

Selling existing products/services to new customers

Selling new products/services to new customers

Selling existing products/services to existing customers

4%

4%

25% 6%

6 Figure 2: Q4 8 Appendix, Q9b 10 Appendix, Q7b 12 Appendix, Q7e

7 Appendix, Q9a, 9 Appendix, Q6a,11 Figure 3: Q9c,

8 Too hesitant to embrace technology change

Despite the need to innovate to avoid losing further competitiveness, responses from executives in the UK, Germany, Italy, France and Spain indicate that EU countries are lagging behind the global norm when it comes to the importance placed on digital technologies.

Too hesitant to embrace technology change

While most respondents see “significant change” as a result of advances in digital technologies (particularly in the UK, where 61 percent of executives agree), amongst the five largest EU markets, only France-based executives (and just 11 percent of them) see digital technologies as having a “transformational” effect on business.13

This is surprising, given that these executives are based in mature markets that need to compete on quality and innovation. It also contrasts with the emphasis executives in Germany, the UK and Italy place on R&D investments. Although R&D is clearly on the agenda, many companies are less likely to emphasise information technologies to improve their competitive position than their Asian or North American peers.

For Mr Cohen, however, technology is a powerful force for disruption. “It’s going to affect the vast majority of industries,” he says. “For some of them, the changes are dramatic, especially in the media, telecoms and music, but others, like more traditional consumer products companies, will also have to reinvent themselves.”

Even for industries that remain rooted in the physical – such as infrastructure, architecture and construction – digital technologies are bringing about dramatic operational changes.

“The design and construction phases are being transformed,” says Mr Morriss. “People are talking about building information modelling in terms of 3D, 4D, 5D, 6D as they start to describe overlay of cost and construction sequencing – and that will be a significant improvement.”

For the energy sector, technology is permitting an increased focus on the customer and a decentralisation of energy production. “These changes are expected to have on the energy sector the same disruptive consequences that the internet had on telecommunications,” says Mr Ferraris. “If this materialises, digital could represent one of the most important key success factors, and could lead to integration between digital systems and the power system.”

9CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

Figure 4: Q16 – Please select the statement that best describes your company’s approach to digital business investments (such as cloud computing, data analytics, machine-to-machine communications, social and mobile).

Not all companies appear to acknowledge these advances. In fact, both Germany- and France-based respondents lag behind the global averages in the importance they attach to digital technologies and their assessment of what they can do for their businesses.

This is in line with EIU data which highlight sluggish growth in the markets for information and communications technology (ICT) in France and Germany. In France, growth rates are forecast to decline from an already low 0.7 percent in 2013 to 0.6 percent in 2014. Germany experienced paltry growth of 0.1 percent in ICT in 2013, well below the overall economy’s growth. Compare that with the US or Canada, both of which experienced faster ICT growth than their (already stronger) overall GDP growth rates.

Although respondents from Germany, Italy, Spain and the UK agree with their global peers that digital technologies are important for the delivery of new goods and services, only 27 percent of France-based executives say this is the case (the global average is 46 percent).14

Meanwhile, rather than focusing on the power of technology to help grow their business, executives in Germany (70 percent) and Italy (69 percent) see its main purpose as increasing efficiency and cutting costs.15 This may be a failure of imagination as Europe’s companies are less likely consider the revenue growth potential of these technologies. While 45 percent of executives globally see digital technologies as a means of growing sales, this proportion falls to 33 percent in the EU5 and a mere 25 percent among Germany-based executives.16

In short, EU executives appear to be underrating what digital technologies can do for their businesses compared with their peers in other regions. Moreover, they are more likely to see these investments focus on the promotion of efficiency. This can overlook a more transformative approach to harnessing technology advances.

0% 100%

Globalaverage

Germany

UK

France

Italy

Spain

59%31%

70%

59%

48%33%

69%18%

47%23%

Primarily focused on growthopportunities and new waysof reaching customers

Primarily focused on processefficiencies and cost reduction

26%

30%

Figure 4 source: Accenture, “CEO Briefing 2014 | The Global Agenda: Competing in a Digital World.” See: http://www.accenture.com/ceobriefing

13 Appendix, Q1515 Figure 4: Q16

14 Figure 5: Q17 16 Figure 5: Q17

10 Missing the boat on digital competitiveness

Missing the boat on digital competitivenessIf many EU executives discount the potential for technology to help expand their businesses, some are also down playing its importance in cementing relationships with customers. While 61 percent of all respondents recognise the importance of digital technologies to improve the customer experience, in Germany the proportion is only 49 percent and Italy 51 percent.17 Their peers in the US and in Asia are far more likely to value these opportunities to deepen customer connections with 69 percent in the US and 89 percent in China citing this use of digital technologies.

However, UK-based respondents stand out for their recognition of the role digital technology can play to meet new consumer demands with a majority (70 percent) highlighting this as a route to improved customer experience.18 They are also more likely to recognise the importance of data analytics to their businesses (65 percent) than the global average (53 percent) or their EU5 peers (47 percent).

Mr Cohen believes this approach is critical if companies are to survive in an era where customers want to access goods and services at any time and from anywhere. “They have to reinvent the customer experience, and technology today allows that,” he says. Understanding the uses of data and connectivity is crucial for many businesses to maintain their edge.

For Mr Morriss, technology adoption is key to a company’s competitive advantage. “We see a real opportunity in our industry,” he says. “The ability to out compete smaller competitors by investing in technology and making the best use of it, is really important for us.”

Capitalising on new technologies takes more than financial investments, however it also investment in people and organisational structure.

For SAP, changes in technology demand investments in human resources. “It requires a lift-and-shift exercise within the company to move back office-type of processes into customer-oriented activities,” says Mr Cohen. “And that requires a different set of skills.”

In the survey, change management is seen as one of the biggest challenges to digital implementation among EU executives, with large proportions in each country citing this among their top three challenges to implementing digital technologies.19 Other important obstacles cited by EU executives include poor funding, silos between departments, low customer demand, skills shortages and a lack of senior executive support.

Figure 5: Q17 – How important are investments in digital technologies (such as cloud computing, E-commerce, data analytics, machine-to-machine communication, social and mobile) to the following areas of your business? Recognising digital’s importance for customer experience:

0% 100%

Globalaverage

Germany

UK

France

Italy

Spain

US 69%

China 89%

51%

54%

70%

49%

61%

60%

Figure 5 source: Accenture, “CEO Briefing 2014 | The Global Agenda: Competing in a Digital World.” See: http://www.accenture.com/ceobriefing

11CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

Figure 6: Q14 – How important will the following digital technologies be for your company in the next 12 months? Cloud computing, E-commerce, Machine-to-machine communications, Social media, Mobile and Data analytics.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Globalaverage

54%

53%

50%

47%

45%

43%

Germany

38%

40%

42%

29%

33%

27%

UK

43%

65%

39%

44%

43%

46%

France

54%

48%

37%

46%

29%

46%

Italy

40%

53%

47%

44%

39%

29%

Spain

52%

47%

47%

52%

40%

49%

Social media

Cloud computing

Mobile

Machine-to-machinecommunications

Data analytics

E-commerce

Figure 6 source: Accenture, “CEO Briefing 2014 | The Global Agenda: Competing in a Digital World.” See: http://www.accenture.com/ceobriefing

17 Figure 5: Q17 19 Appendix, Q19

18 Figure 5: Q17

12 Conclusion

13CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

After a difficult period, EU executives are looking forward to a year of gradually accelerating growth and the expansion of their businesses. As they map out their plans, they have established more ambitious overseas investment strategies than their global peers, particularly in non-BRIC emerging markets. They also recognise the importance of continuing to make investments in research and development. As advanced, service-based economies, this is vital for them.

Yet they may be underestimating the role of technology in meeting their goals. And crucially respondents in the EU5 are less likely than their global

peers to focus on digital technologies as key tools in delivering an improved customer experience or opening up new sales channels. Overlooking the revenue growth opportunities made possible by advances in digital technology may impede European companies from achieving their competitive potential. This may slow the EU’s overall growth prospects.

Given the battering Europe’s economies have taken in the wake of the global financial and subsequent euro crisis, many companies are more focused on rebuilding their businesses than on prioritising investments in cutting-edge technologies.

However, in a world where customers expect increasingly personalised engagement and in the face of intensifying competition in emerging markets, the pressure is on for companies to adopt a new approach – one that may lead them to embrace digital technology, or be left behind.

Conclusion

Appendix

14 Appendix

15CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

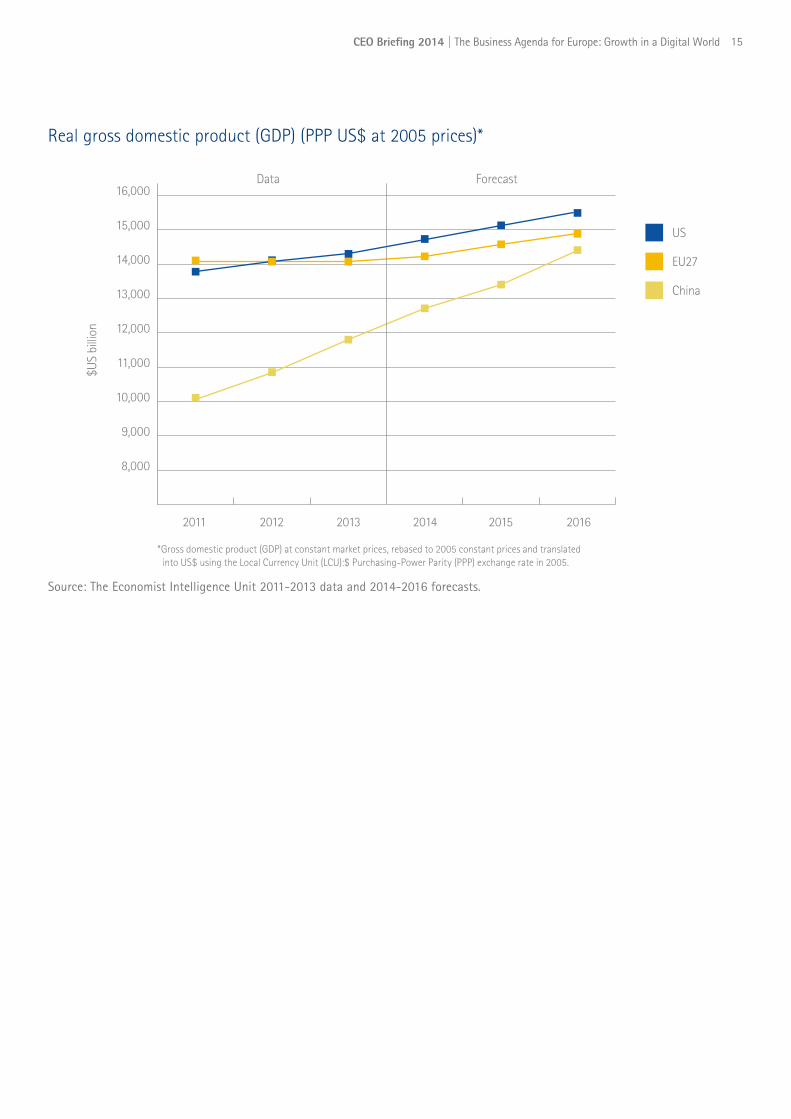

Real gross domestic product (GDP) (PPP US$ at 2005 prices)*

Source: The Economist Intelligence Unit 2011-2013 data and 2014-2016 forecasts.

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

2011 2012 2013 2014 2015 2016

*Gross domestic product (GDP) at constant market prices, rebased to 2005 constant prices and translated into US$ using the Local Currency Unit (LCU):$ Purchasing-Power Parity (PPP) exchange rate in 2005.

US

China

EU27

$US

billi

on

Data Forecast

16 Appendix

-4.0 -2.0 0.0 2.0 4.0 6.0 8.0 10.0

France

Germany

Italy

Spain

UK

US

China

India

0.2%0.8%

0.5%1.4%

-1.9%0.5%

-0.2%0.7%

1.9%2.7%

1.9%3.0%

7.7%7.2%

4.9%6.0% 2014 forecast

2013 data

Russia1.5%

2.9%

Brazil2.3%

1.8%

% real change pa

Source: The Economist Intelligence Unit 2013 data and 2014 forecast.

Source: The Economist Intelligence Unit 2013 data and 2014 forecast.

GDP growth: Percentage change in real GDP, over previous year

Export growth of goods and services: Percentage change in real exports of goods and services, over previous year

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0

0.6%2.9%

0.6%3.3%

0.1%2.3%

5.6%3.6%

1.0%3.2%

2.8%2.8%

6.4%7.6%

11.6%13.0%

2.2%5.9%

2.5%3.2%

France

Germany

Italy

Spain

UK

US

China

India

Russia

Brazil

% real change pa

2014 forecast

2013 data

17CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

0.0-1.0 2.01.0 4.03.0 6.0 8.05.0 7.0

France

Germany

Italy

Spain

UK

US

China

India

0.4%0.8%

-0.1%0.8%

-0.4%0%

1.9%0.4%

0.5%1.5%

0.8%1.4%

7.4%6.8%

4.2%4.4%

Russia1.2%

2.6%

Brazil1.1%1.2%

GDP at PPP, per worker, % pa

2014 forecast

2013 data

0.0 5.0 10.0 15.0 20.0 25.0 30.0

10.4%10.3%

5.3%5.2%

12.4%12.5%

26.4%25.9%

7.5%6.8%

7.4%6.5%

6.6%6.3%

9.0%8.6%

4.8%4.5%

5.4%6.1%

France

Germany

Italy

Spain

UK

US

China

India 2014 forecast

2013 data

Russia

Brazil

%

Source: The Economist Intelligence Unit 2013 data and 2014 forecast.

Source: The Economist Intelligence Unit 2013 data and 2014 forecast.

Growth of overall productivity of labour: Growth of real GDP, at 2005 constant prices, per person employed

Recorded unemployment: Harmonized unemployment rate

18 Appendix

-4.0 -2.0 0.0 2.0 4.0 6.0 8.0 10.0

France

Germany

Italy

Spain

UK

US

China

India

0.8%0.5%

1.5%1.2%

0.2%0.3%

-2.8%0%

1.2%-0.1%

0.7%0.7%

7.7%8.0%

-1.7%-1.2%

Russia4.0%

4.5%

Brazil1.4%

1.9%

% change pa

2014 forecast

2013 data

0% 100%

EuropeanUnion

France

Germany

Italy

Spain

UK

55%

Online access to public services

Individuals ordering goodsor services online

Using online banking

47%

70%59%

56%68%

37%20%

46%32%

60%77%

41%

60%

49%

21%

44%

41%

Average real wages: Percentage change in hourly wages in local currency adjusted for inflation, over previous year.

Access to digital services

Source: The Economist Intelligence Unit

Source: The Economist Intelligence Unit 2013 data and 2014 forecast.

19CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

Access to digital infrastructure

Source: The Economist Intelligence Unit

0% 100%

EuropeanUnion

France

Germany

Italy

Spain

UK

95%

Take-up of mobile broadband(subscriptions per 100 people)

Households with Internetaccess (% of households)

Fixed Broadband Coverage(% of households)

77%

99%82%

97%87%

98%69%

98%70%

100%88%

58%

50%

42%

57%

58%

82%

20 Appendix

Strongly optimistic 12 4 6 4 8 7 20 22 11 26 10

Somewhat optimistic 32 27 24 28 34 41 42 37 38 20 39

Neither optimistic nor pessimistic 41 54 56 51 47 37 27 20 37 34 39

Somewhat Pessimistic 15 15 15 18 11 15 10 20 13 20 14

Strongly pessimistic 1 0 0 0 0 0 1 0 1 0 0

Healthcare, pharmaceuticals and biotechnology 29 31 40 31 28 33 31 22 39 20 14

Financial services 19 6 20 18 17 13 13 18 17 14 17

Telecoms 16 10 13 26 19 11 19 13 13 20 14

Software and IT 18 12 11 22 21 17 30 24 25 12 17

Professional services 12 10 16 10 15 9 8 7 11 14 14

Mining and extractive industries 15 19 18 10 17 17 14 11 17 10 15

Energy, oil and gas 30 39 35 29 30 41 38 16 41 28 21

Consumer goods 26 25 22 24 28 39 30 13 25 16 29

Construction and real estate 24 25 35 14 26 30 21 15 28 14 19

Aerospace and defence 5 10 2 6 8 7 10 0 3 0 4

Utilities 13 10 18 2 23 15 18 9 13 10 12

Agriculture 8 8 4 14 15 7 7 4 9 10 4

Manufacturing 30 29 29 22 25 44 26 31 29 36 37

Automotive 22 35 33 12 21 15 20 13 20 14 31

Significant increase 37 27 47 20 23 44 34 69 33 18 40

Moderate increase 34 37 35 38 40 41 36 24 37 42 35

No change 18 27 16 32 19 9 17 4 18 28 21

Moderate decrease 9 10 0 8 17 6 11 2 10 10 4

Significant decrease 2 0 2 2 0 0 1 2 1 2 0

Don't know 0 0 0 0 0 0 1 0 0 0 0

Strongly optimistic 16 6 11 10 25 11 16 35 13 8 23

Somewhat optimistic 46 46 57 41 45 52 54 42 49 48 44

Neither optimistic nor pessimistic 29 29 32 28 13 30 24 22 30 34 23

Somewhat Pessimistic 8 15 0 18 13 7 6 2 9 10 10

Strongly pessimistic 1 4 0 4 4 0 0 0 0 0 0

Significant increase 39 39 49 18 30 44 39 70 39 16 39

Moderate increase 37 39 38 50 53 46 43 20 36 32 42

No change 13 15 11 18 9 7 12 4 9 36 8

Moderate decrease 8 6 2 12 4 0 3 4 13 10 8

Significant decrease 3 2 0 2 4 2 2 2 4 2 2

Don't know 1 0 0 0 0 0 1 0 0 4 2

Strongly optimistic 17 19 9 8 11 11 16 44 13 22 29

Somewhat optimistic 52 50 56 57 60 65 45 47 55 48 41

Neither optimistic nor pessimistic 26 29 33 22 23 15 34 7 30 24 28

Somewhat Pessimistic 5 2 2 14 4 9 5 2 3 6 2

Strongly pessimistic 0 0 0 0 2 0 0 0 0 0 0

Strongly optimistic 24 14 19 20 15 15 22 57 19 28 33

Somewhat optimistic 52 56 61 57 57 61 56 32 58 42 55

Neither optimistic nor pessimistic 19 21 20 18 26 20 19 7 15 18 10

Somewhat Pessimistic 5 10 0 6 2 4 3 4 8 12 2

Strongly pessimistic 0 0 0 0 0 0 0 0 0 0 0

Question 1

1a. In the next 12 months, to what extent are you optimistic or pessimistic about the prospects for the global economy?

Question 2

Globally, which industries do you believe enjoy the best growth prospects in the next 12 months?

Question 4

4a. Thinking about your organisation in the next 12 months, do you expect the following to increase, decrease or stay the same? Profit:

1b. In the next 12 months, to what extent are you optimistic or pessimistic about the prospects for the economy of the country where you are based?

4b. Thinking about your organisation in the next 12 months, do you expect the following to increase, decrease or stay the same? Revenues:

1c. In the next 12 months, to what extent are you optimistic or pessimistic about the prospects for your industry?

1d. In the next 12 months, to what extent are you optimistic or pessimistic about the prospects for your own organisation?

Percentage of respondents (%)

Global Total

France

Germ

any

Italy

Spain

UK

US

China

India

Russia

Brazil

100 5 5 5 5 5 10 5 8 5 5 Percentage of respondents (%)

Global Total

France

Germ

any

Italy

Spain

UK

US

China

India

Russia

Brazil

100 5 5 5 5 5 10 5 8 5 5

21CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

Significant increase 14 6 13 6 15 13 13 28 14 16 10

Moderate increase 44 52 64 39 42 48 46 50 49 32 46

No change 32 37 22 45 34 33 28 19 33 28 33

Moderate decrease 8 4 2 6 8 6 12 2 3 16 8

Significant decrease 2 2 0 4 2 0 1 0 1 4 4

Don't know 1 0 0 0 0 0 1 2 0 4 0

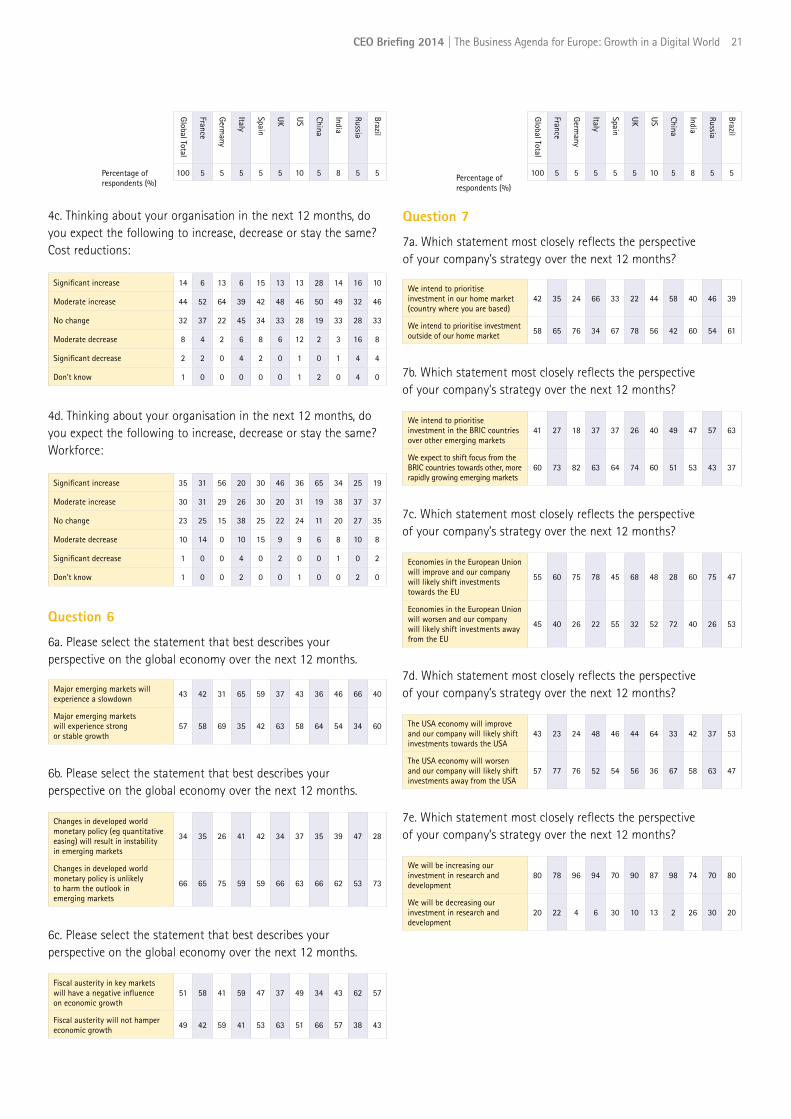

We intend to prioritise investment in our home market (country where you are based)

42 35 24 66 33 22 44 58 40 46 39

We intend to prioritise investment outside of our home market 58 65 76 34 67 78 56 42 60 54 61

Major emerging markets will experience a slowdown 43 42 31 65 59 37 43 36 46 66 40

Major emerging markets will experience strong or stable growth

57 58 69 35 42 63 58 64 54 34 60

Significant increase 35 31 56 20 30 46 36 65 34 25 19

Moderate increase 30 31 29 26 30 20 31 19 38 37 37

No change 23 25 15 38 25 22 24 11 20 27 35

Moderate decrease 10 14 0 10 15 9 9 6 8 10 8

Significant decrease 1 0 0 4 0 2 0 0 1 0 2

Don't know 1 0 0 2 0 0 1 0 0 2 0

We intend to prioritise investment in the BRIC countries over other emerging markets

41 27 18 37 37 26 40 49 47 57 63

We expect to shift focus from the BRIC countries towards other, more rapidly growing emerging markets

60 73 82 63 64 74 60 51 53 43 37

Economies in the European Union will improve and our company will likely shift investments towards the EU

55 60 75 78 45 68 48 28 60 75 47

Economies in the European Union will worsen and our company will likely shift investments away from the EU

45 40 26 22 55 32 52 72 40 26 53

The USA economy will improve and our company will likely shift investments towards the USA

43 23 24 48 46 44 64 33 42 37 53

The USA economy will worsen and our company will likely shift investments away from the USA

57 77 76 52 54 56 36 67 58 63 47

We will be increasing our investment in research and development

80 78 96 94 70 90 87 98 74 70 80

We will be decreasing our investment in research and development

20 22 4 6 30 10 13 2 26 30 20

Changes in developed world monetary policy (eg quantitative easing) will result in instability in emerging markets

34 35 26 41 42 34 37 35 39 47 28

Changes in developed world monetary policy is unlikely to harm the outlook in emerging markets

66 65 75 59 59 66 63 66 62 53 73

Fiscal austerity in key markets will have a negative influence on economic growth

51 58 41 59 47 37 49 34 43 62 57

Fiscal austerity will not hamper economic growth 49 42 59 41 53 63 51 66 57 38 43

4c. Thinking about your organisation in the next 12 months, do you expect the following to increase, decrease or stay the same? Cost reductions:

Question 7

7a. Which statement most closely reflects the perspective of your company’s strategy over the next 12 months?

Question 6

6a. Please select the statement that best describes your perspective on the global economy over the next 12 months.

4d. Thinking about your organisation in the next 12 months, do you expect the following to increase, decrease or stay the same? Workforce:

7b. Which statement most closely reflects the perspective of your company’s strategy over the next 12 months?

7c. Which statement most closely reflects the perspective of your company’s strategy over the next 12 months?

7d. Which statement most closely reflects the perspective of your company’s strategy over the next 12 months?

7e. Which statement most closely reflects the perspective of your company’s strategy over the next 12 months?

6b. Please select the statement that best describes your perspective on the global economy over the next 12 months.

6c. Please select the statement that best describes your perspective on the global economy over the next 12 months.

Percentage of respondents (%)

Global Total

France

Germ

any

Italy

Spain

UK

US

China

India

Russia

Brazil

100 5 5 5 5 5 10 5 8 5 5 Percentage of respondents (%)

Global Total

France

Germ

any

Italy

Spain

UK

US

China

India

Russia

Brazil

100 5 5 5 5 5 10 5 8 5 5

22 Appendix

Selling new products/ services to existing customers 32 37 27 33 28 17 37 49 24 22 37

Selling existing products / services to new customers 19 14 18 28 23 17 22 11 20 22 14

Selling new products / services to new customers 36 39 53 31 36 50 32 31 47 44 33

Selling existing products / services to existing customers 13 12 2 8 13 17 9 9 9 12 16

Extremely important 20 8 6 12 19 11 26 46 18 10 29

Moderately important 25 31 20 31 15 22 25 24 25 30 16

Somewhat important 31 35 33 35 43 35 31 9 33 16 37

Slightly important 20 25 35 10 19 24 17 22 22 28 16

Not at all important 4 2 6 12 4 7 2 0 3 6 2

Don’t know 1 0 2 0 0 0 0 0 0 10 0

Complete Transformation 12 12 0 0 0 0 5 15 17 24 10

Significant change 40 35 48 37 36 61 47 62 37 28 41

Moderate change 31 39 37 43 47 33 35 21 32 30 24

Incremental change 14 14 15 14 17 4 10 0 13 10 14

No change 2 0 0 6 0 2 1 0 0 0 6

Don't know 2 0 0 0 0 0 2 2 1 8 6

Selling new products/ services to existing customers 23 15 15 16 34 7 27 51 18 16 22

Selling existing products / services to new customers 23 33 11 22 13 19 20 18 18 24 18

Selling new products / services to new customers 47 46 72 48 45 63 41 31 58 52 53

Selling existing products / services to existing customers 7 6 2 14 8 11 12 0 6 8 8

Selling new products/ services to existing customers 15 6 6 10 10 6 15 28 9 13 20

Selling existing products / services to new customers 17 25 9 25 18 16 20 20 15 23 18

Selling new products / services to new customers 54 62 82 47 51 75 47 46 63 48 50

Selling existing products / services to existing customers 14 8 4 18 22 4 17 6 13 17 12

Extremely important 24 25 11 12 11 26 32 51 18 8 24

Moderately important 37 29 38 39 49 44 36 38 49 39 37

Somewhat important 24 27 38 33 21 20 20 11 18 31 18

Slightly important 13 17 11 12 17 6 10 0 15 18 16

Not at all important 2 2 0 4 2 4 2 0 0 2 6

Don’t know 0 0 2 0 0 0 0 0 0 2 0

Question 9

9a. Which of the following strategies will be most important to driving revenue growth in your company over the next three years? In home market Country where you are based:

Question 17

17a. How important are investments in digital technologies (such as cloud computing, E-commerce, data analytics, machine-to-machine communication, social and mobile) to the following areas of your business? Grow sales:

Question 15

To what extent do you expect the continued evolution of digital technologies (such as cloud computing, E-commerce, data analytics, machine-to-machine communication, social and mobile) to change your industry over the next 12 months?

Primarily focused on growth opportunities and new ways of reaching customers

31 33 26 18 23 30 26 23 27 33 33

Primarily focused on process efficiencies and cost reduction 59 48 70 69 47 59 68 77 63 41 55

Not applicable 10 19 4 14 30 11 7 0 10 27 12

Question 16

Please select the statement that best describes your company’s approach to digital business investments (such as cloud computing, data analytics, machine to machine communications, social and mobile). Our company’s digital technology investments are:

9b. Which of the following strategies will be most important to driving revenue growth in your company over the next three years? Outside your home market – Developed markets:

9c. Which of the following strategies will be most important to driving revenue growth in your company over the next three years? Outside your home market – Emerging markets: 17b. How important are investments in digital technologies

(such as cloud computing, E-commerce, data analytics, machine-to-machine communication, social and mobile) to the following areas of your business? Improve the customer experience:

Percentage of respondents (%)

Global Total

France

Germ

any

Italy

Spain

UK

US

China

India

Russia

Brazil

100 5 5 5 5 5 10 5 8 5 5 Percentage of respondents (%)

Global Total

France

Germ

any

Italy

Spain

UK

US

China

India

Russia

Brazil

100 5 5 5 5 5 10 5 8 5 5

23CEO Briefing 2014 | The Business Agenda for Europe: Growth in a Digital World

Insufficient funding 35 40 35 22 47 28 36 26 37 28 37

Skills shortage 35 35 31 29 43 41 40 36 39 34 33

Lack of senior executive support 31 31 36 6 30 32 28 18 27 38 31

Insufficient customer demand for digital solutions 33 25 31 20 36 35 29 13 37 26 25

Poor cross-functional collaboration 35 48 38 18 34 33 44 15 38 38 33

Difficulties managing change 42 39 47 43 43 43 42 66 44 44 25

Other, please specify 1 0 0 0 2 0 2 0 0 0 2

None 3 0 2 24 0 0 1 2 3 4 8

Question 19

What are the most significant challenges you face when implementing investments into digital business initiatives (such as cloud computing, data analytics, machine to machine communications, social and mobile)?

Extremely important 19 6 9 10 12 19 23 42 12 16 26

Moderately important 25 39 16 28 26 15 28 29 26 34 30

Somewhat important 30 29 44 34 35 46 31 15 44 28 14

Slightly important 21 21 27 12 26 17 15 13 17 16 24

Not at all important 5 6 2 16 2 4 4 2 3 4 6

Don’t know 0 0 2 0 0 0 0 0 0 2 0

Extremely important 18 12 7 6 19 11 16 52 12 24 18

Moderately important 28 15 35 34 23 30 31 20 45 14 20

Somewhat important 31 48 36 24 38 35 39 15 27 26 35

Slightly important 17 23 16 26 13 20 12 11 14 22 18

Not at all important 5 2 4 10 8 4 2 2 3 10 10

Don’t know 0 0 2 0 0 0 0 0 0 4 0

Extremely important 35 29 16 20 30 28 31 69 33 34 37

Moderately important 35 44 35 35 32 52 41 22 34 26 31

Somewhat important 22 21 38 33 26 19 23 9 22 22 18

Slightly important 7 4 9 8 9 2 5 0 9 16 10

Not at all important 1 2 0 4 2 0 0 0 3 0 4

Don’t know 1 0 2 0 0 0 1 0 0 2 0

Extremely important 17 10 4 16 15 4 22 47 11 10 16

Moderately important 27 27 14 29 36 23 31 20 23 38 33

Somewhat important 28 25 35 29 26 49 27 18 25 24 28

Slightly important 22 31 37 22 17 21 17 11 32 20 20

Not at all important 5 8 10 4 6 4 2 2 9 8 4

Don’t know 1 0 2 0 0 0 1 2 0 0 0

17c. How important are investments in digital technologies (such as cloud computing, E-commerce, data analytics, machine-to-machine communication, social and mobile) to the following areas of your business? Open new sales channels:

17d. How important are investments in digital technologies (such as cloud computing, E-commerce, data analytics, machine-to-machine communication, social and mobile) to the following areas of your business? Create new products and services:

17g. How important are investments in digital technologies (such as cloud computing, E-commerce, data analytics, machine-to-machine communication, social and mobile) to the following areas of your business? Improve the efficiency of our operations:

17e. How important are investments in digital technologies (such as cloud computing, E-commerce, data analytics, machine-to-machine communication, social and mobile) to the following areas of your business? Improve management control, oversight & governance:

Percentage of respondents (%)

Global Total

France

Germ

any

Italy

Spain

UK

US

China

India

Russia

Brazil

100 5 5 5 5 5 10 5 8 5 5Percentage of respondents (%)

Global Total

France

Germ

any

Italy

Spain

UK

US

China

India

Russia

Brazil

100 5 5 5 5 5 10 5 8 5 5

Extremely important 21 14 11 10 19 17 18 56 15 24 27

Moderately important 39 54 46 39 42 44 43 29 51 24 41

Somewhat important 26 23 35 43 19 26 26 7 20 26 18

Slightly important 11 10 7 4 12 11 11 6 9 24 8

Not at all important 3 0 0 4 8 2 2 2 5 0 6

Don’t know 0 0 2 0 0 0 0 0 0 2 0

17f. How important are investments in digital technologies (such as cloud computing, E-commerce, data analytics, machine-to-machine communication, social and mobile) to the following areas of your business? Attract and retain the best talent:

About AccentureAccenture is a global management consulting, technology services and outsourcing company, with approximately 289,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’s most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$28.6 billion for the fiscal year ended Aug. 31, 2013. Its home page is www.accenture.com

Copyright © 2014 Accenture All rights reserved.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture.

Visit our sites to learn more: www.accenture.com/ceobriefing www.accenture.com/EuropeEconomicGrowth

or join the conversation via:

@AccentureStrat

www.facebook.com/accenturestrategy

www.linkedin.com/company/accenture-strategy

For more information about Accenture Strategy visit: www.accenture.com/strategy