CENTRAL BANK OF SEYCHELLES Report 2000.pdf8.11 Government of Seychelles Re -finance Scheme; 1995...

107

CENTRAL BANK OF SEYCHELLES ANNUAL REPORT 2000

Transcript of CENTRAL BANK OF SEYCHELLES Report 2000.pdf8.11 Government of Seychelles Re -finance Scheme; 1995...

CENTRAL BANK OF SEYCHELLES

ANNUAL REPORT 2000

CENTRAL BANK OF SEYCHELLES

ANNUAL REPORT

2000

CONTENTS

Letter of Transmittal

Board of Directors

List of Tables

Economic Review of 2000 1

Section One World Economic Conditions 4

Section Two Highlights of the Seychelles Economy 17

Section Three Financial Survey 20

Section Four Government Finance 32

Section Five The External Sector 43

Section Six The Real Sector: Production, Employment and Prices 57

Section Seven Investment and Offshore Developments 77

Section Eight Operations and Administration of the Central Bank 83

Letter of Transmittal

Central Bank of Seychelles

P.O. Box 701

Victoria

March 31, 2001.

President F. A. René

State House

Victoria

Dear Mr. President,

In accordance with section 43(3) of the Central Bank of Seychelles Act, 1982, as

amended, I have the honour to submit for your approval the Eighteenth Annual Report of

the Central Bank together with a copy of the Annual Accounts for 2000 certified by the

Auditors.

Yours faithfully,

CENTRAL BANK OF SEYCHELLES

Board of Directors

(as at 31 December 2000)

Norman Weber, Governor - Chairman Francis Chang Leng - Member

Errol Dias - Member

Francis Chang-Sam - Member

Secretary to the Board

Patrick Stravens

List of Charts and Tables Chart No. Title Page Financial Survey 3.1 Growth rates of the money supply aggregates; 1995-2000 23 3.2 Growth rates of credit of the banking system; 1995-2000 25 3.3 Growth rates of credit held by the economic agents; 1995-2000 27 3.4 The movement in credit/deposit ratio in 2000 30 3.5 The movement in commercial bank credit and deposit in 2000 30 3.6 Level of interest rates; 1995-2000 30 The Real Sector: Production, Employment and Prices 6.1 Real GDP growth; 1990-2000 57

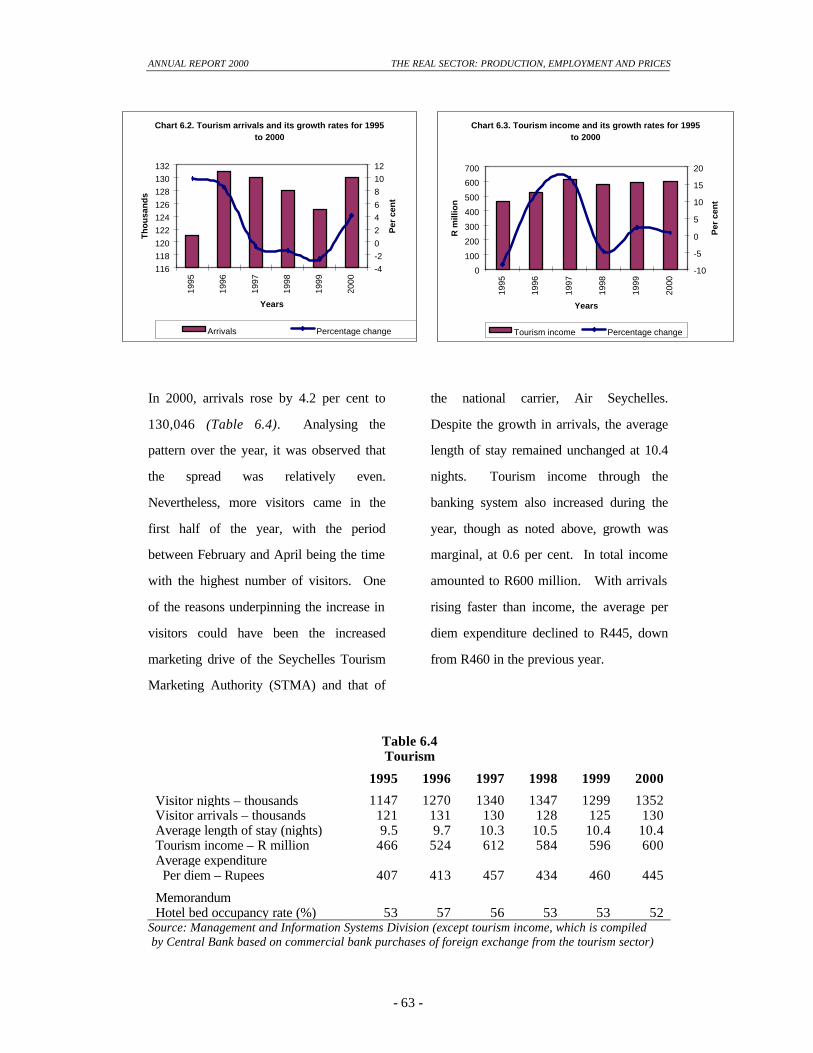

6.2 Tourism arrivals and its growth rates for 1995-2000 63

6.3 Tourism income and its growth rates for 1995-2000 63

6.4 Canned tuna produced and exported from 1995-2000 73

6.5 Revenue earned from export from 1995-2000 73

6.6 Inflation rate for 1995-2000 76

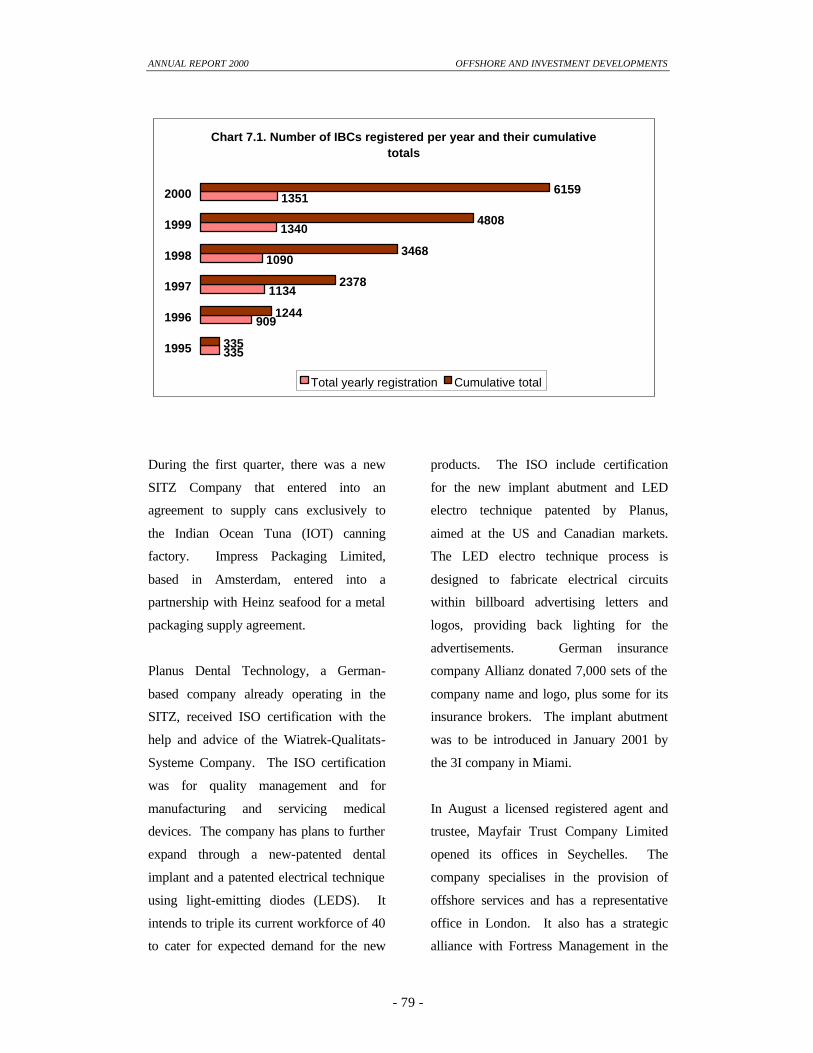

Investment and Offshore Developments 7.1 Number of IBCs registered per year and their

cumulative totals; 1995-2000 80

Operations and Administration of the Central Bank 8.1 Advances to Government; 1995-2000 85 8.2 Currency in circulation; 1995-2000 86 8.3 Stock of Public Debt Instruments; 1995-2000 89 8.4 Local Assets Ratio from 1995-2000 94

Table No. Title Page Financial Survey 3.1 Monetary Survey; 1995-2000 24

3.2 Credit; 1995-2000 26

3.3 Commercial Banks – Loans and Advances to Non-Government

Sector by Economic Sectors; 1996-2000 28

3.4 Loans by Development Bank by Economic Sectors; 1996-2000 29

3.5 Liquidity Indicators of Commercial Banks; 1995-2000 29

3.6 Interest Rates; 1995-2000 31

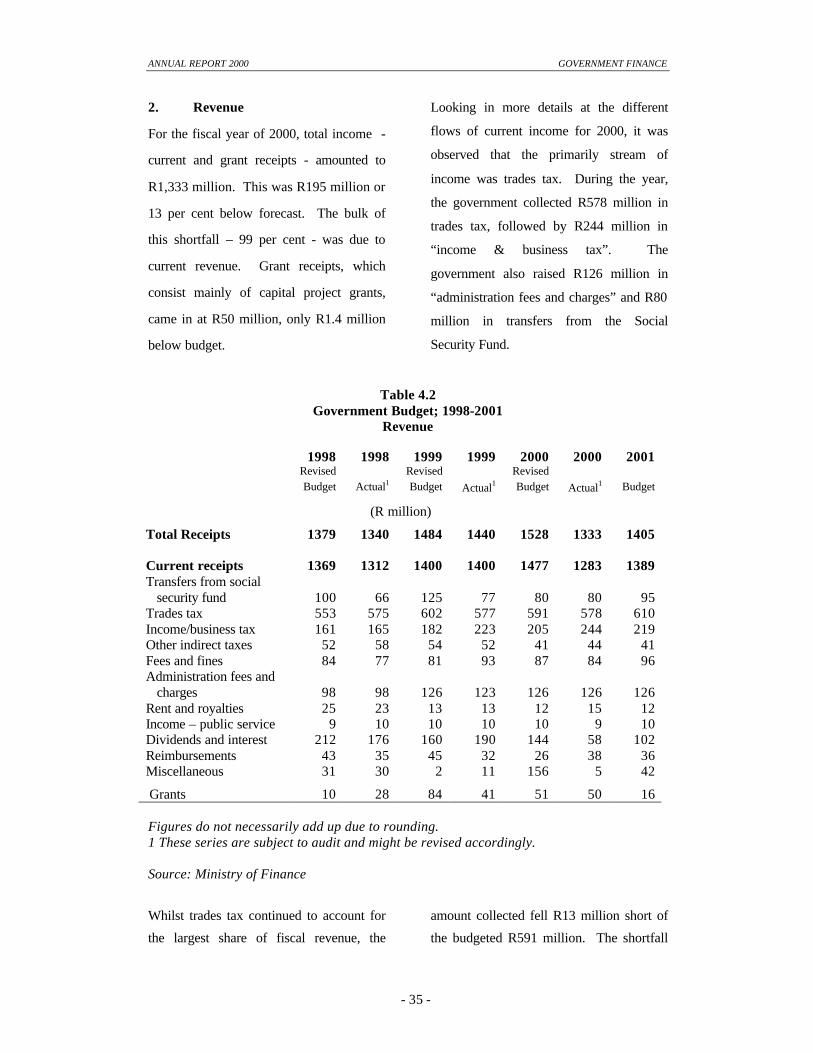

Government Finance 4.1 Government Budget; Summary 1998-2001 34

4.2 Government Budget; Revenue 1998-2001 35

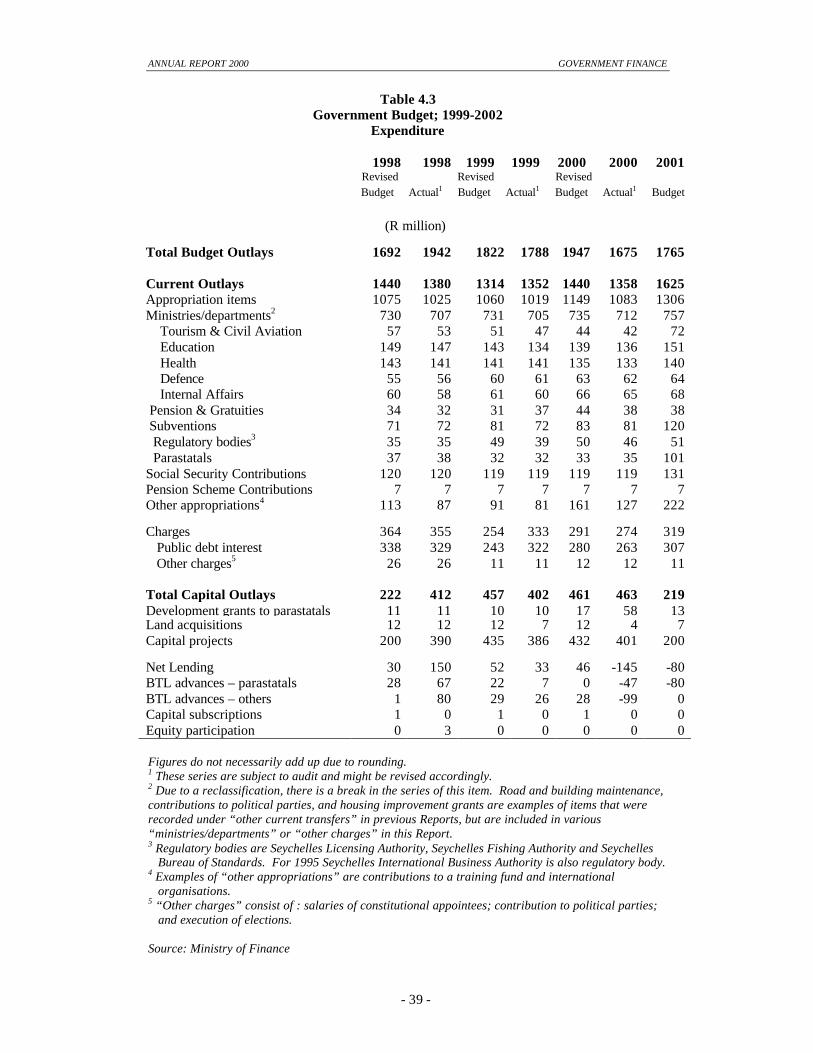

4.3 Government Budget; Expenditure 1998-2001

4.4 Public Sector Capital Project Expenditure 1995-2000 40

The External Sector 5.1 Balance of Payments; 1995-2000 44

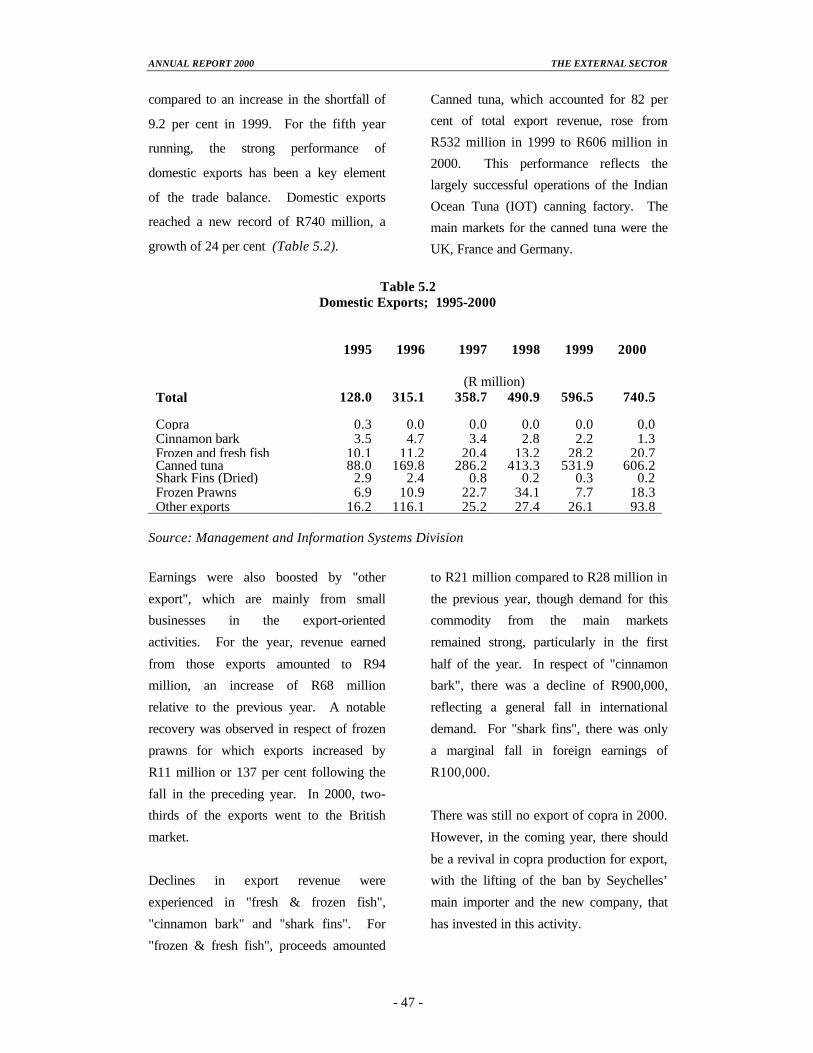

5.2 Domestic Exports; 1995-2000 47

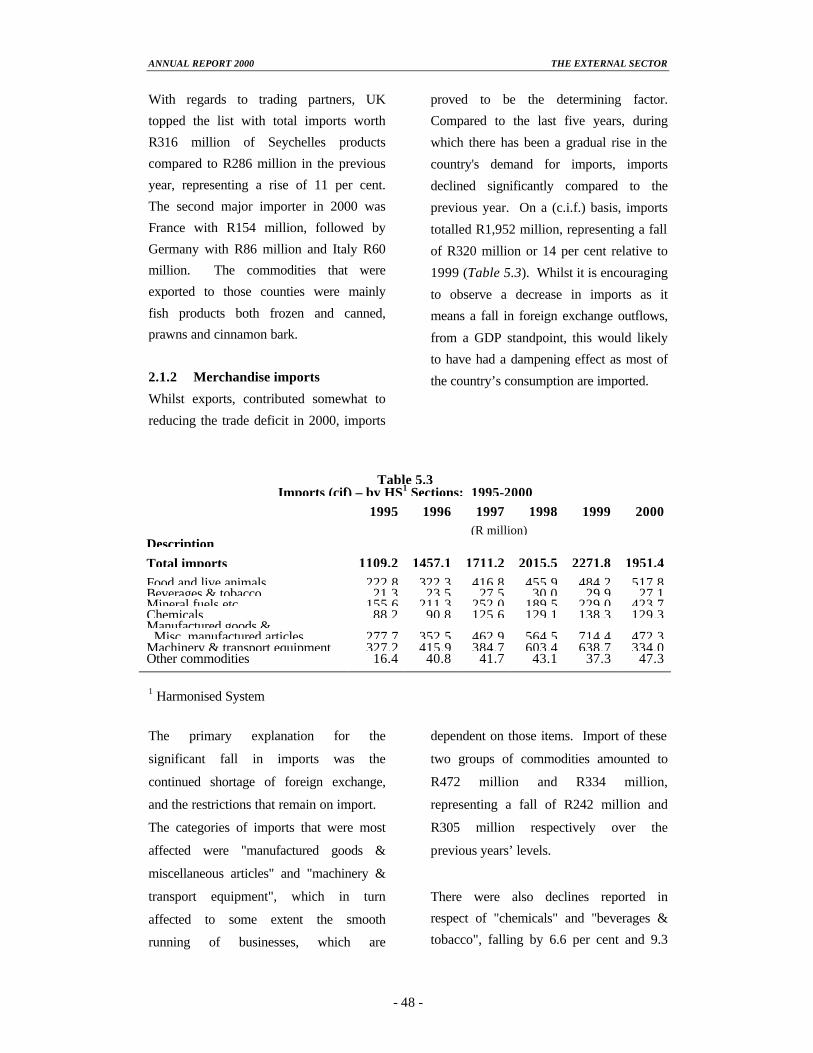

5.3 Imports (cif) – by SITC Sections; 1995-2000 48

5.4 Goods procured in ports; 1995-2000 50

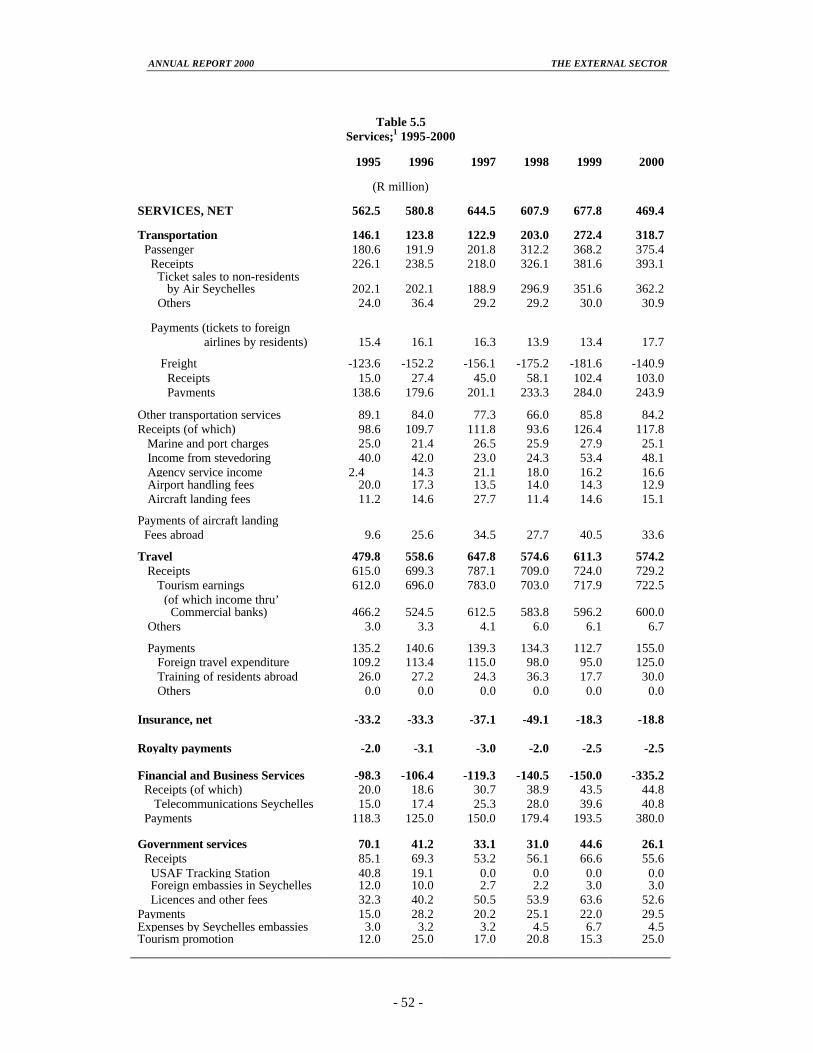

5.5 Services 1995-2000 52

5.6 External Reserves; 1995-2000 55

5.7 Exchange Rates; 1995-2000 56

The Real Sector: Production, Employment and Prices 6.1 Gross Domestic Product by Kind of Economic Activity at constant market prices 58 6.2 Gross Domestic Product by Kind of Economic Activity at current market prices 59 6.3 Gross Domestic Product by Broad Productive Sectors at current market prices 61 6.4 Tourism 64

Table No. Title Page

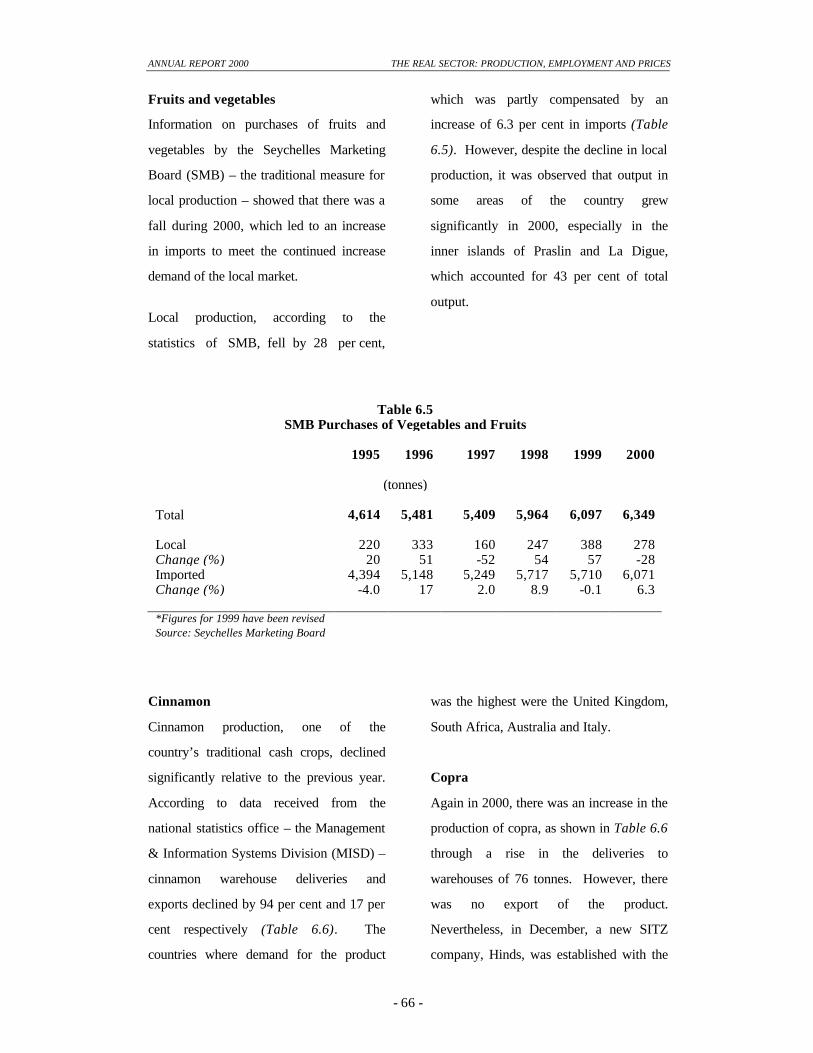

6.5 SMB Purchases of Vegetables and Fruits 66

6.6 Crops 68

6.7 Livestock (slaughters) 68

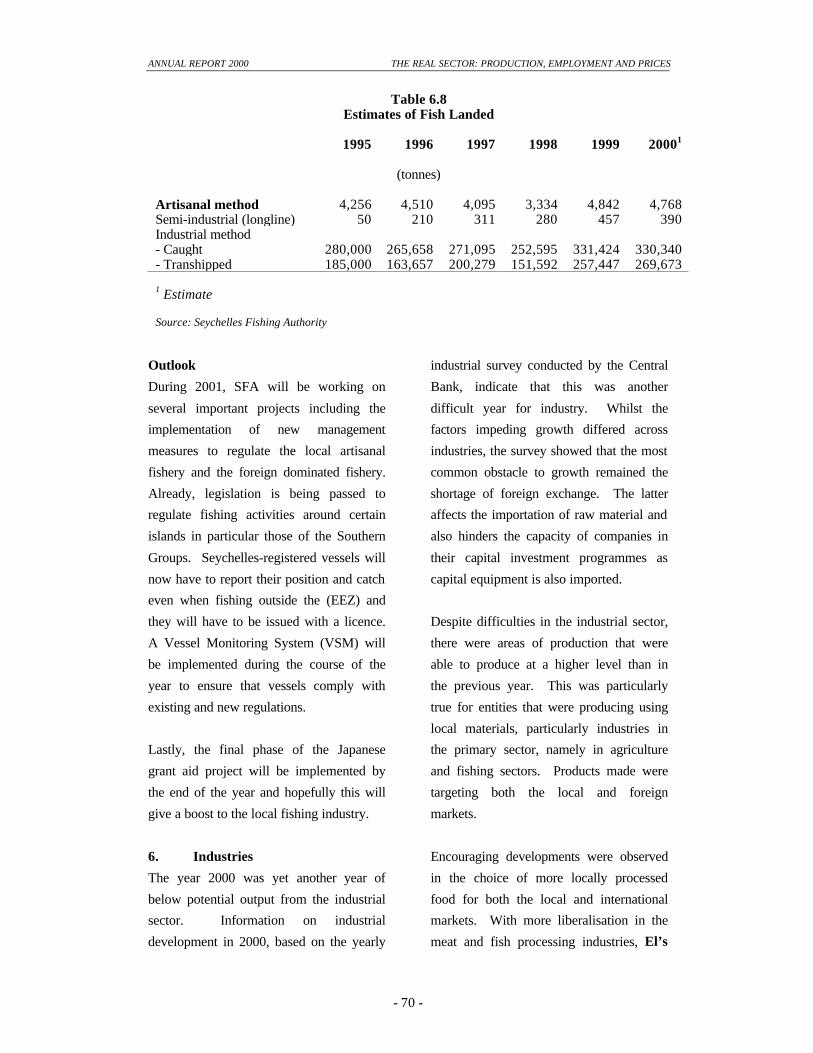

6.8 Estimates of Fish Landed 71

6.9 Employment 75

6.10 Composition of Retail Price Index 77

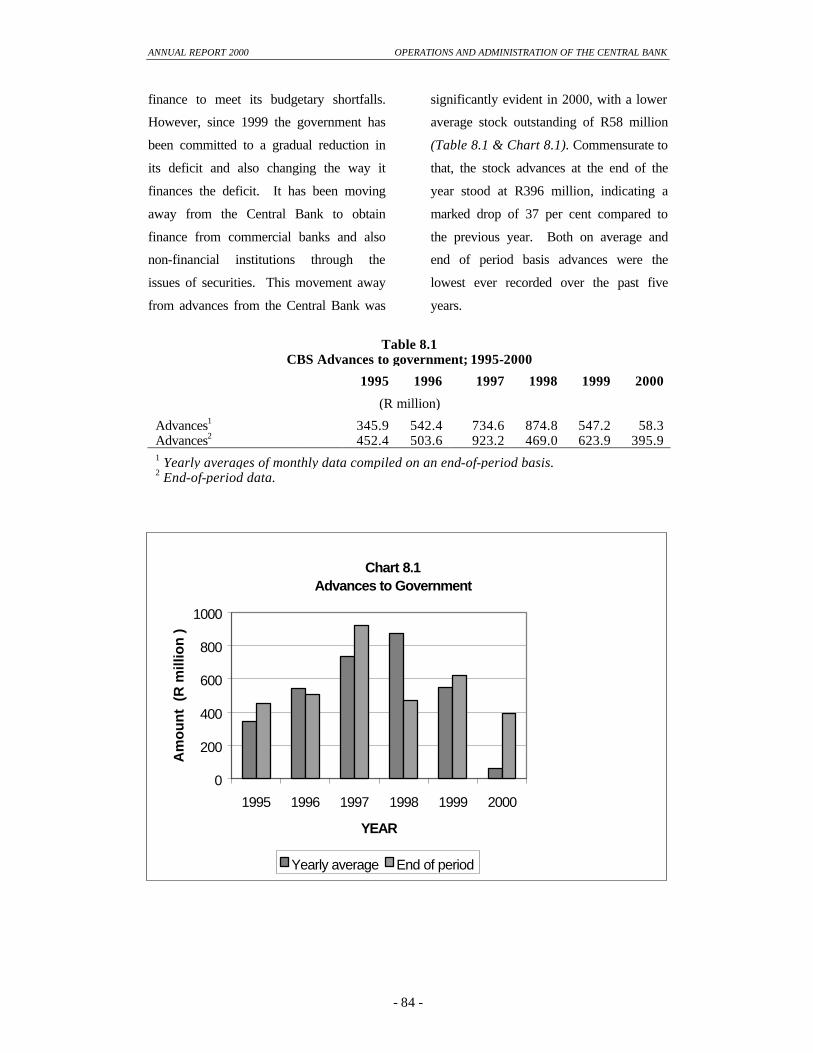

Operations and Administration of the Central Bank 8.1 CBS Advances to government; 1995-2000 85

8.2 Circulation of Notes and Coins; 1995-2000 86

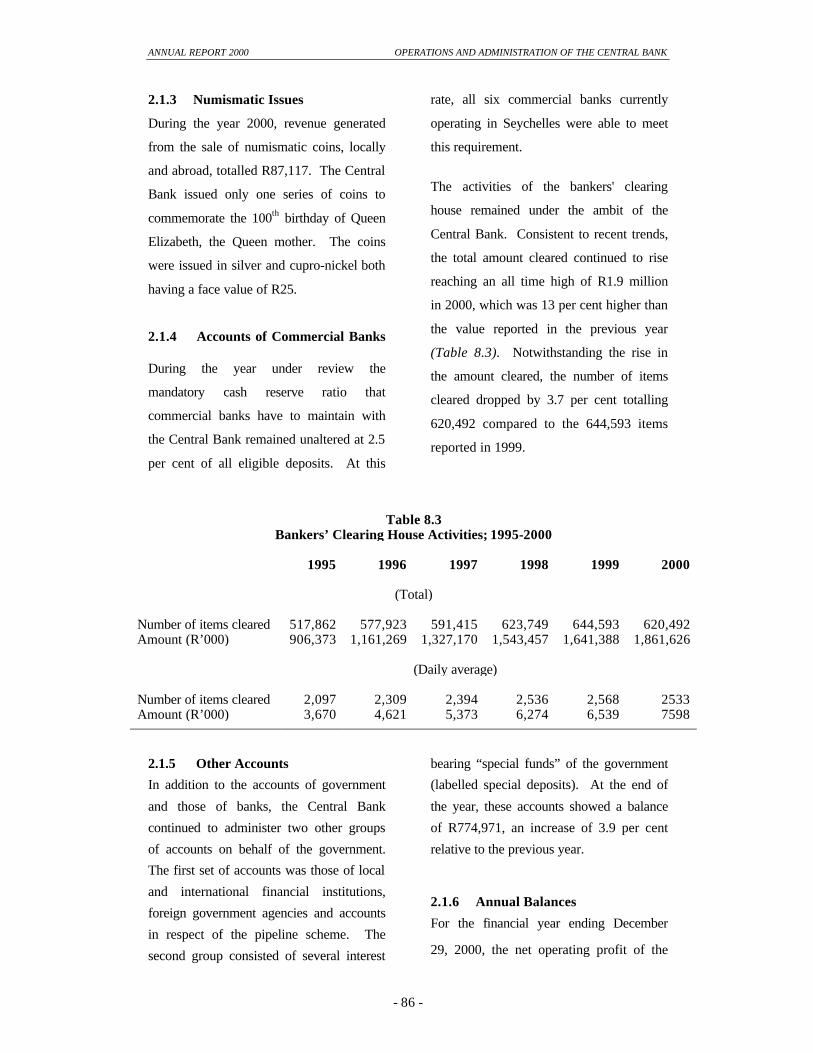

8.3 Bankers’Clearing House Activities; 1995-2000 87

8.4 Treasury Bill Yields; 1995-2000 89

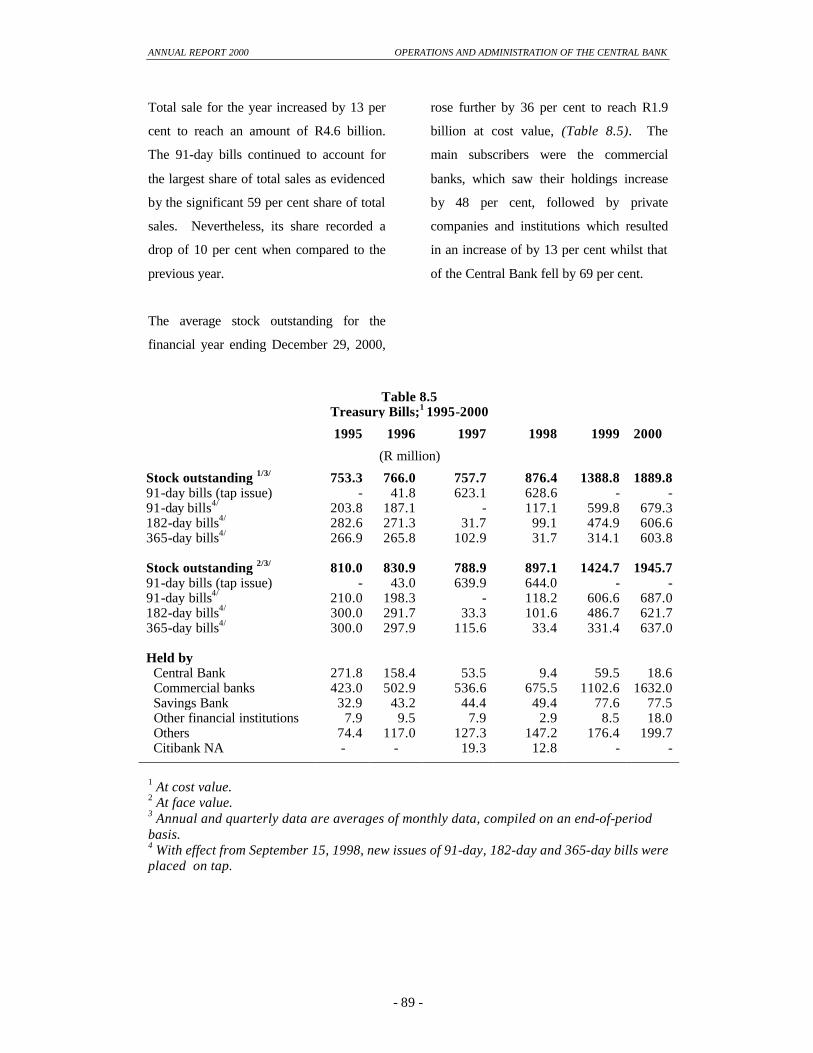

8.5 Treasury Bills; 1995-2000 90

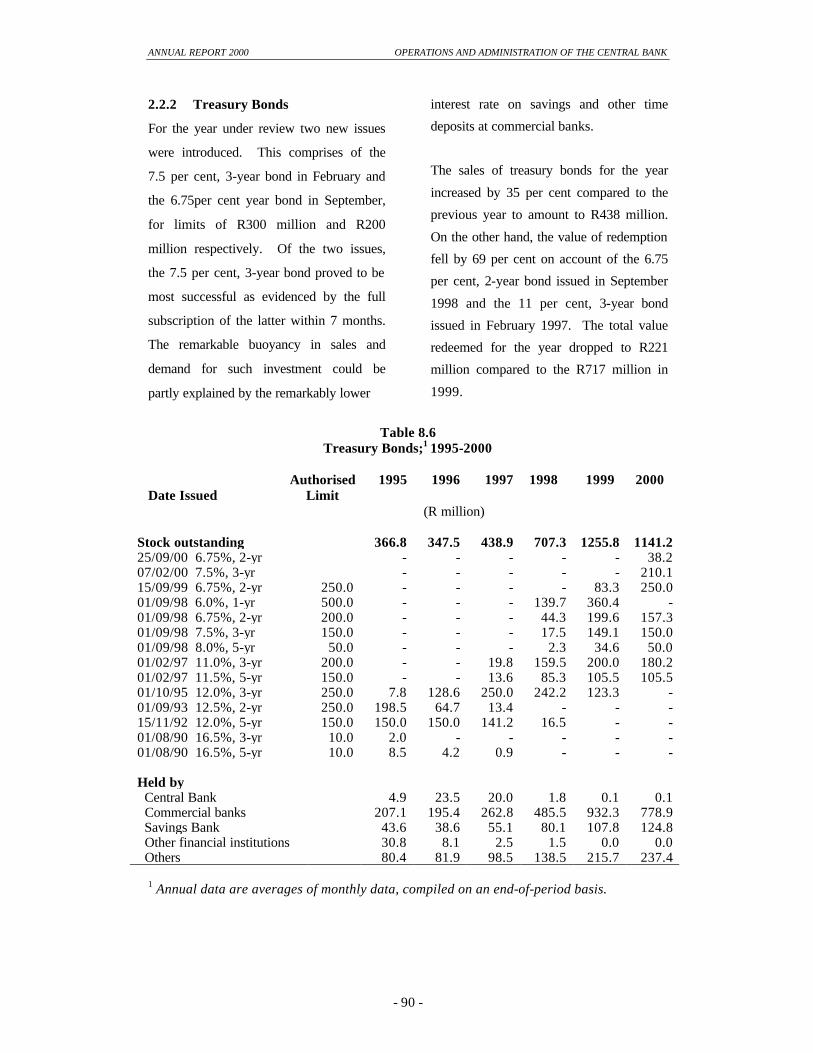

8.6 Treasury Bonds; 1995-2000 91

8.7 Government Stocks; 1995-2000 92

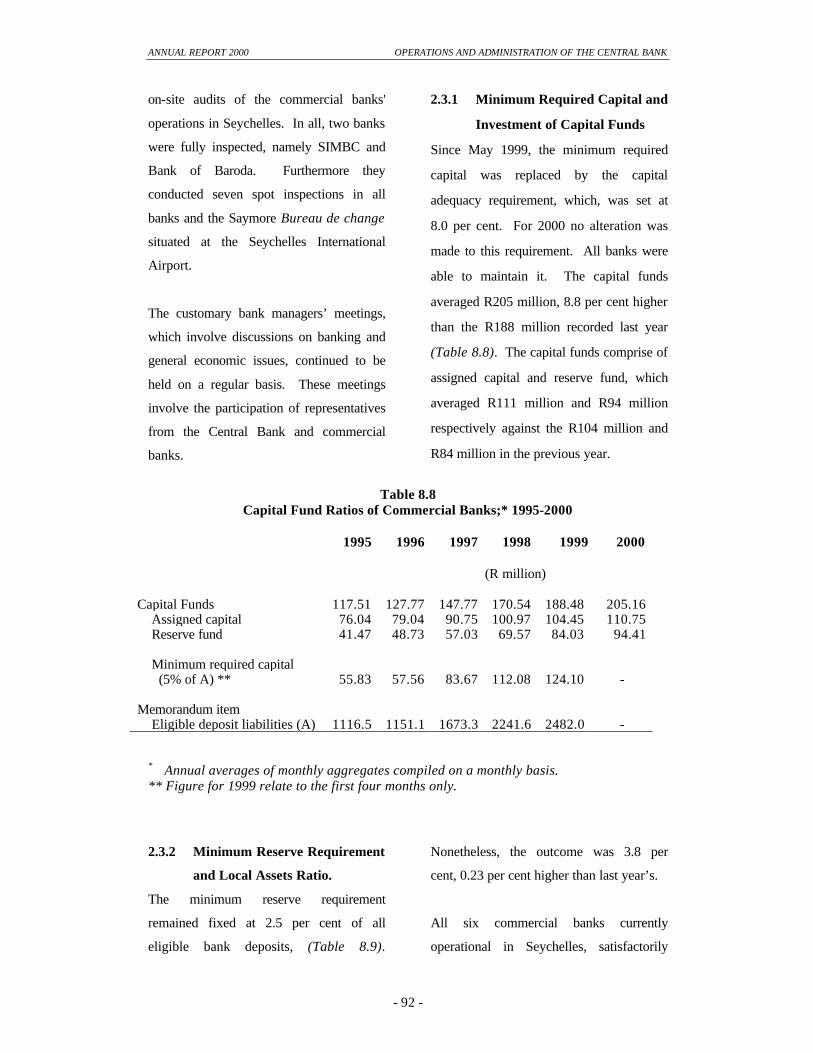

8.8 Capital Fund Ratios of Commercial Banks; 1995-2000 93

8.9 Minimum Reserves and Local Assets Ratio; 1995-2000 94

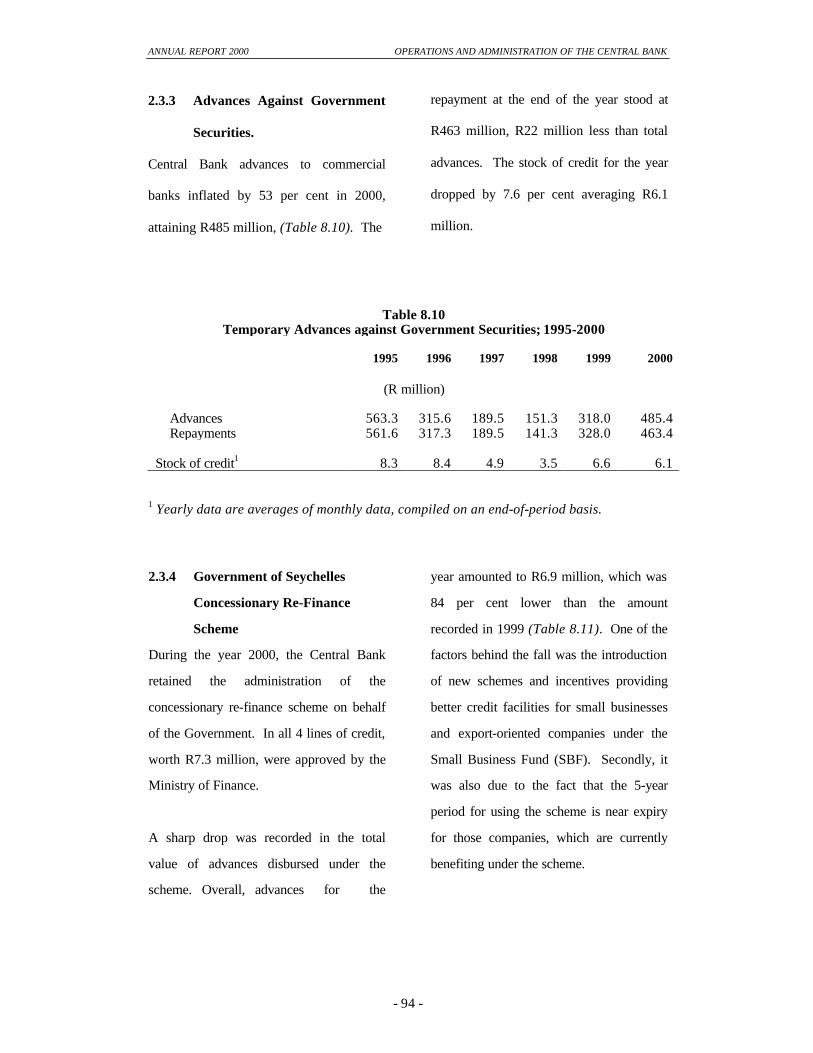

8.10 Temporary Advances against Government Securities; 1995-2000 95

8.11 Government of Seychelles Re-finance Scheme; 1995-2000 96

8.12 Commercial Bank Advances to Non-Seychellois; 1998-2000 96

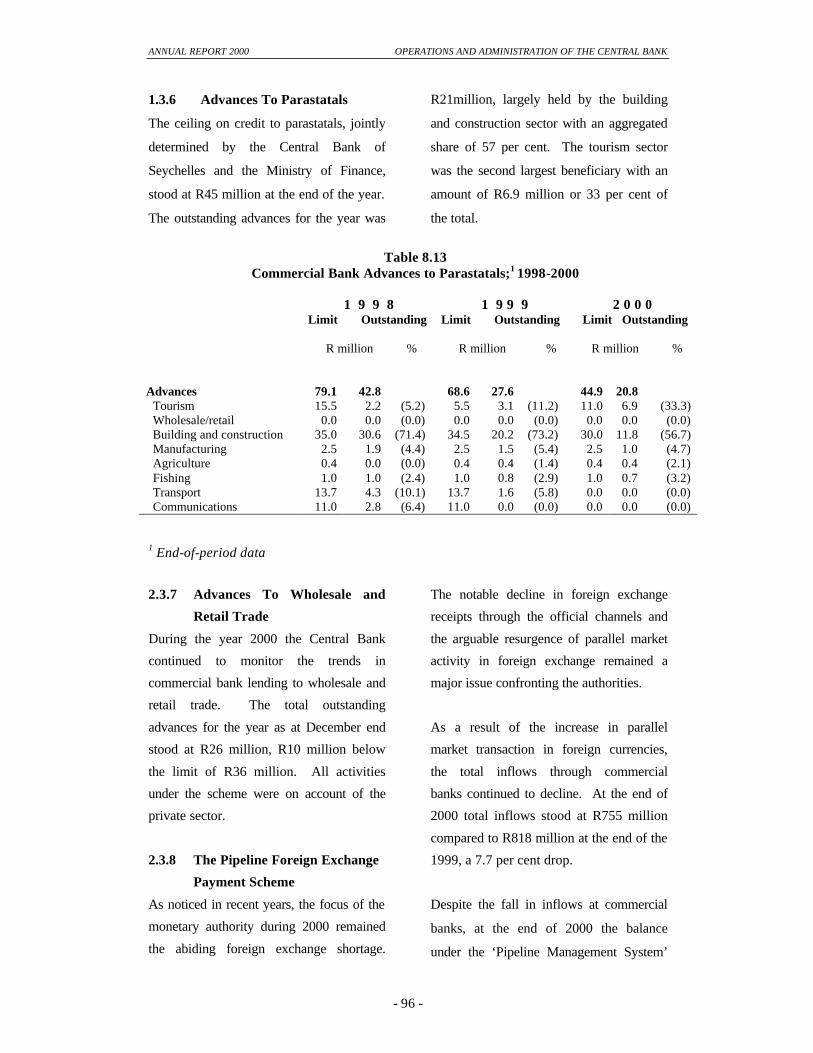

8.13 Commercial Bank Advances to Parastatals; 1998-2000 97

Technical Note

Owing to rounding of figures, the sum of separate items may not always add up to the total shown. Abbreviations used in this Report are: R = Seychelles Rupee CBS = Central Bank of Seychelles n.a = Figure not available .. = Negligible -/0 = Nil

ECONOMIC REVIEW OF 2000

Seychelles was formally accepted as a member of the Indian Ocean Rim

Association for Regional Co-operation (IOR-ARC) at an Extraordinary meeting

of the Association’s Council of Minister’s held in Muscat, Oman.

Seychelles benefit from a donation of R13 million from the French Government

following the signing of a treaty between the two Governments.

An agreement for the purchase of 34 new buses by the Seychelles Public transport

Corporation (SPTC) and TATA International of India under an Indian

Government US $2 million credit line was finalised on 11 February.

On March 7, the Executive Chairman of the Public Utilities Corporation (PUC),

Mr Mukesh Valabhji and Mr Johan Oelofse, the Senior Manager for Nedbank

South Africa, signed a financial agreement which will finance a sewage project.

The sewage treatment project would be for the districts of Beau Vallon and part of

Bel Ombre area and would cost around US$14 million (R75 million).

Seychelles Marketing Board (SMB) announced price reductions on 12 imported

commodities following the Vice President’s budget speech.

The Chief Executive Officer (CEO), Captain David Savy, announced that Air

Seychelles would acquire a third aircraft, a Boeing 737-700, to add to its

international fleet in 2001, while the present 767-200 would be replaced with a

B767-300 in April 2001.

January

March

April

New Boeing 737-700 for Air Seychelles

February

PUC to undertake R75m project

SPTC to receive 34 new buses

Paris gives out R13m

Seychelles joins IOR-ARC

Price reduction

- 1 -

- 2 -

SMB continued to lower prices of goods as part of ongoing efforts to combat

inflation. The price was reduced on the Liqui-Fruit juice, powdered milk as well

as women toiletries.

The US$50 million Victoria power station project was inaugurated by President

Mr. F. A Rene as part of events commemorating the National day celebrations.

The project has been financed partly by the PUC and partly by a US$44 million

loan from the ABN AMRO Bank of Netherlands.

In July a new set of incentives for small business, export-oriented, was announced

by the Vice President. The scheme would include a Small Business Finance

Fund; no trades tax on imported raw material and the right to operate foreign

exchange accounts for export and re-exports businesses.

The Barclays Bank PLC and the Central Bank announced plans to incorporate

Barclays’ existing branches in Seychelles. Barclays Bank (Seychelles) Limited,

effective as from October 1, 2000 would be a wholly owned subsidiary of

Barclays Bank PLC, although shares in the corporation would be offered for sale

to staff and the general public.

The Seychelles International Business authority (SIBA), conducted Seychelles

first ever offshore conference with the theme of ''Future of Offshore Centres in

the Cyber Age''. The two-day conference focussed on the growing influence of

commerce on the International Financial Services Industry.

The Vice-President announced, in the National Assembly in October during a

question time session, that the Government had secured a loan of Euro 50 million

(R245 million) from Citibank to complete the East Coast project.

October October

June

August

September

President inaugurate power station

SIBA Conference

East Coast project

Further price reductions

Bank to be locally incorporated

July

New incentives for small businesses

May

- 3 -

US$6.4 million loan was signed in Khartoum by the Minister of Foreign Affairs,

Mr Jeremie Bonnelame, and the Director General of the Arab Bank for

Development in Africa (BADEA), Mr Medhat Lofty. The loan would go towards

the construction of the new Seychelles Industrial Training Centre (ITC).

After much deliberation on the 2001 budget proposal, the National Assembly

approved the Appropriation Bill 2001. The Appropriation Bill 2001 caters for a

National Budget of R1,225,536,000 and has been the trend throughout the years,

that the Ministry of Education receives the largest share of the budget, R139

million. The Ministry of Health obtained the second largest allocation - R137

million - followed by the Department of Internal Affairs with R68 million and the

Ministry of Defence with R60 million.

December October

BADEA loan for ITC

Budget 2001 approved

SECTION ONE

World Economic Conditions

1. Overview

The global economic recovery that started in

1999 continued to gain strength in 2000 with

the IMF projecting a global output growth of

4.7 per cent for the year under review.

Growth increased in all major economies of

the world, led by the strong US economy;

the robust upswing in Europe; the

consolidation of the recovery in Asia; and a

rebound from 1999’s slowdowns in

emerging markets in Latin America and the

Middle East and Europe. Activity in Africa

rose further, and the countries in transition

saw a second year of solid growth,

underpinned by a much better than expected

performance in Russia. Nevertheless, a

number of countries continued to experience

serious economic problems, in some cases

due to natural disasters and adverse

movements in commodity prices.

With most advanced economies growing at

rates at or above potential, most central

banks continued to raise interest rates.

Although headline inflation rates increased

in response to higher energy prices,

underlying inflation in most advanced

countries remained relatively subdued. In

part, this reflected the continued margins of

slack in some regions of the world, notably

in Japan and to a lesser extent in continental

Europe. But other factors, including fiscal

consolidation and regulatory and

technological changes also played a role.

While the overall outlook was encouraging,

there were significant risks and

uncertainties, for which one of them was oil

prices. Oil prices have been significantly

higher than previously expected, due to both

supply constraints in producing countries

- 4 -

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 5 -

and the continued strength in global

demand. Following the announcement of

further supply increases at the OPEC

meeting in June, as well as indications that

some oil producers would be willing to

boost supply further, the oil price fell back

within in the OPEC target range of US$22-

US28 per barrel in July. However, since

early August prices have rebounded

significantly.

1.1. Developed economies

1.1.1 United States

According to the Monetary Policy Report

submitted to the Congress in February 2001,

the combination of exceptionally strong

growth in the first half of 2000 and subdued

growth in the second half resulted in a rise

in real GDP of about 3.5 per cent for the

year. Domestic demand started out the year

with incredible vigour but decelerated

thereafter and was sluggish by the year-end.

Exports surged for the three quarters and

then faltered. In the labour market, growth

in employment slowed over the year but was

sufficient to keep the unemployment rate

around the lowest sustained level in more

than thirty years.

Core inflation remained low during the year

in the face of sharp increases in energy

prices. Unit labour costs picked up

moderately, adding to the cost pressures

from energy. Nevertheless, the ability of

businesses to raise prices was restrained by

the slowing of the economy and the

persistence of competitive pricing

conditions.

Personal consumption expenditures

increased 4.5 per cent in real terms after

growths of 5.0 per cent and 5.5 per cent in

1998 and 1999 respectively. A large portion

of the gain was in the first quarter, when

consumption grew at a fast pace. For the

remainder of the year, growth was moderate,

averaging about 3.5 per cent. One of the

factors influencing consumption in the year

under review was the change in income and

wealth. Both provided less support to

consumption in 2000 than in other recent

years. Real disposable personal income rose

about 2.25 per cent after a gain of slightly

more than 3.0 per cent in 1999. Disposable

income did not rise quite as much in

nominal terms as it did in 1999, and rising

prices eroded a larger portion of the nominal

gain.

In the business sector, real business fixed

investment rose 10 per cent in 2000

according to an estimate from the

Commerce Department. Investment

spending shot ahead at an annual rate of 21

per cent in the first quarter of the year due to

the high-tech purchases that had been

delayed from 1999 by companies that did

not want their operating systems to be in a

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 6 -

state of change at the onset of the new

millennium. Expansion of investment was

slower but still relatively brisk in the second

and third quarters, at annual rate of about 15

per cent and 8.0 per cent respectively. In the

fourth quarter, however, capital spending

downshifted abruptly, falling at an annual

rate of 1.5 per cent in response to the

slowing economy, tightening financial

conditions, and rising concern about the

prospects for profits.

On the external front, the current account

deficit reached US$452 billion (annual rate)

in the third quarter or 4.5 per cent of GDP,

compared with US$331 billion for 1999.

Most of the expansion in the deficit occurred

in the balance of trade in goods and services.

The deficit on trade in goods and services

widened to US$383 billion (annual rate) in

the third quarter from US$347 billion in the

first half of the year. Data for October and

November suggest that the deficit may have

increased further in the fourth quarter.

Exports of goods and services rose an

estimated 7.0 per cent during the year under

review. Exports surged during the three

quarters, supported by a pickup in economic

activity abroad that began in 1999. By

market destination, US exports were

strongest in Mexico and countries of Asia.

About 45 per cent of goods exports were

capital equipment, 20 per cent were

industrial supplies, and roughly 10 per cent

each were agricultural, automotive,

consumer, and other goods. The quantity of

import of goods and services expanded

rapidly during the first three quarters, due to

the continuing strength of domestic

economy. The counterpart to the increased

US current account deficit was an increase

in net capital flows. As in the previous year,

US capital flows reflected the relatively

strong cyclical position of the economy for

most of the year and the global wave of

corporate mergers.

In the labour market, the non-farm payroll

employment increased about 1.5 per cent in

2000, measured on a December-to-

December basis. Over the first few months

of 2000, the expansion of jobs proceeded at

a faster pace than in 1999, boosted both by

the federal government’s hiring of the

decennial census and by a somewhat faster

rate of job creation in the private.

Indications of a moderation in private hiring

started to emerge towards mid-year. Over

the remainder of the year, monthly increases

in private employment stepped down further

due to a slowing economy.

In terms of changes in the price level, this

was mainly influenced by the surge in

energy prices. The chain-type price index

for real GDP, the broadest measure of goods

and services produced domestically, rose

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 7 -

2.25 per cent in 2000. In addition, the price

index for gross domestic purchases, the

broadest measure of prices for goods and

services purchased by domestic buyers,

posted a rise of 2.5 per cent. The prices of

energy products purchased directly by

consumers increased by 15 per cent in 2000.

In response to the rise in world oil prices,

consumer prices of motor fuels rose nearly

20 per cent. Prices also rose rapidly for

home heating oil.

Businesses had to cope with rising costs of

energy production, transportation, and

temperature control. In some industries that

depend particularly heavily on energy

inputs, the rise in costs had a large effect on

product prices. Despite the spillover of

energy effects into other markets, inflation

outside the energy sector remained overall

moderate.

1.1.2 European Union

1.1.2.1 Eurozone economies

The expansion in the Euro area, which

started in the second half of 1999 continued

to gather strength in the first half of 2000,

with GDP growth rising steadily at around

3.0 per cent. This increase in economic

momentum was aided by resurgent export

growth due to the strengthening of the

global recovery and a highly competitive

currency. During the remainder of the year,

high consumer and business confidence and

the favourable external environment

sustained the expansion. For the year as a

whole, GDP growth was projected at 3.5 per

cent, with all countries registering above-

potential growth rates. The pickup in

activity has been accompanied by a

substantial decline in unemployment.

However, with some slack still remaining in

area-wide labour and product markets,

underlying price pressures have been

restrained. The headline CPI increased to

2.4 per cent by midyear, due largely to rising

oil prices and exchange rate pass through.

Core inflation, at about 1.3 per cent, has

remained subdued, aided by moderate wage

settlements, falling utility prices as

deregulation and privatisation took effect,

and, in some countries, cuts in direct taxes.

Nevertheless, one of the preoccupations of

the European economies was the euro. The

Euro was quite volatile, hitting record lows

against the U.S dollar and most other major

currencies in mid-May, and again in early

September. By early September, the Euro

had depreciated over 15 per cent in nominal

effective terms since its inception in 1999,

and was below the level that could be

justified medium-term fundamentals. In

part, this has reflected the relative cyclical

position of the Euro area, with United

States. In addition, relative interest rate

differentials and market perceptions of

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 8 -

differences in the underlying climate for

investment across countries may have

played a role.

Given buoyant activity, money and credit

development, rising oil prices, and later the

weakness of the Euro, the European Central

Bank (ECB) started raising interest rates

early in the year. Over the period between

February to October, the ECB increased

interest rates by 175 basis points with the

aim on the one hand of forestalling potential

pressures on wages and prices and on the

other to boost the value of the currency.

During 2000, growth rates among individual

countries in the Euro area have continued to

differ markedly, which – since monetary

policy must be set on the basis of conditions

in the Euro area as a whole – has posed

challenges for policymakers, particularly in

the small and faster growing economies.

Over the coming year, differences in growth

rates are projected to decline as the recovery

in Italy and Germany catches up with that in

France and some of the cyclically advanced

countries. Nevertheless, substantially

differences in underlying cyclical positions

are likely to persist for a period. Most of the

cyclically advanced countries continue to

experience higher than average inflation,

rapid growth in domestic credit, sharply

rising property prices, and, in Portugal, a

large current account deficit. In some cases,

particularly Ireland and possibly the

Netherlands, relatively clear signs of

overheating have emerged. While budgetary

positions in these countries are in most cases

in surplus, every effort appeared to have

been made to save the fiscal windfalls

arising from higher growth in order to avoid

fuelling demand pressures.

1.1.2.2 Non-eurozone economies

In the United Kingdom, GDP growth was

projected to pick up to 3.1 per cent in 2000

from 2.1 per cent in 1999, reflecting a

smaller deterioration of the trade balance

and continued strong domestic demand

growth, bolstered partly by the planned

expansion in government consumption.

Inflation has remained below the Bank of

England’s 2.5 per cent target, owing to

subdued wage pressure, falling price-cost

margin, and the strength of sterling.

Nevertheless, labour market conditions

remain tight with the unemployment rate (on

a claimant count basis) below 4.0 per cent.

During the year, the Bank of England

increased interest rates only twice, both at

the early stages of the year, by 50 basis

points taking the repo rate from 5.50 per

cent to 6.00 per cent, where it then remained

until the end of the year.

In Sweden, another country that has

remained outside the monetary union, GDP

growth was estimated at 4.5 per cent in

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 9 -

2000, driven by strengthening domestic

demand and a firming up of net exports.

Nevertheless, some slack still remained in

the economy; wage increases have been

moderate, and core inflation was well below

the 2 per cent midpoint of the target zone.

Activity has also remained strong in Greece,

which, aided by a stability-oriented

economic policy and also introduction of

administrative measures to reduce inflation,

has helped it to successfully meet the

European Monetary Union (EMU)

convergence requirements. From January

2001, Greece will become the 12th member

of the Monetary Union.

In the smaller states, namely Denmark,

Norway and Switzerland, solid recovery was

also underway. In Norway and Denmark,

where the slowdown partly reflected policy

measures to address overheating, the

ensuing rebound has been led by rising

exports (for Norway, aided by higher oil

prices). Domestic demand increased in both

countries during 2000, as fiscal policies

returned to a broadly neutral stance.

In Switzerland, both exports and domestic

demand, aided by an accommodative

monetary stance, drove the recovery. As the

strength of the recovery became apparent,

the Central Bank appropriately moved to

tighten monetary conditions, while allowing

the franc to appreciate against the Euro.

1.1.3 Japan

For the year as a whole, Japanese real GDP

is estimated to have increased about 2.0 per

cent, a substantial improvement from the

very small increase of the previous year and

the decline recorded in 1998. Growth,

which was concentrated in the first part of

the year, was led by private nonresidential

investment. In contrast, residential

investment weakened as the effect of tax

incentives waned. Consumption rebounded

early in the year from a sharp decline at the

end of the previous year but then stagnated,

depressed in part by record-high

unemployment and concerns that ongoing

corporate restructuring could lead to further

job losses. Public investment, which gave a

major boost to the economy in 1999,

remained strong through the first half of the

year but then fell off sharply. For the year

as a whole the fiscal stance is estimated to

have been somewhat contractionary.

Inflation was negative for the second

consecutive year, with the prices of both

consumer goods and real estate continuing

to move lower.

In terms of monetary policy, the Bank of

Japan, which had adopted a zero interest rate

policy since February 1999, changed its

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 10 -

stance in the second half of the year. More

precisely on August 11, the monetary policy

committee of the Bank decided by majority

vote to increase the key interest rate – the

uncollaterised overnight call rate – by 25

basis points to 0.25 per cent. According to

the Bank, the change was effected due to

substantial improvement in the economy.

At that time, the economy was showing

signs of recovery led mainly by business

fixed investment.

1.2 Developing economies

1.2.1 Asia

The rebound from the crisis of 1997-98

continued in Asia, with growth projected to

rise from 6.0 per cent in 1999 to more than

6.5 per cent in 2000 and 2001. The rapid

recovery of output in 1999 was fuelled by

continuing monetary and fiscal stimulus, as

well as external demand, supported by a

recovery in prices of electronics. Asia was

now the world’s largest supplier of such

equipment.

Continuing demand for information

technology goods helped underpin the

expansion, but private domestic demand

became a more important force propelling

regional growth in 2000, particularly in the

countries most advanced in recovery, where

fixed investment was increasing rapidly.

Activity also continued to be buttressed by

continuing robust growth in the region’s two

most populous economies, China and India.

Despite some concerns in financial markets

about the pace of structural reforms, and

political uncertainties, growth in Indonesia

was set to grow at about 4.0 per cent in 2000

and 5.0 per cent in 2001, supported by firm

oil prices, while activity in South Korea was

forecasted to moderate to 8.75 per cent in

2000 and 6.5 per cent in 2001. Fiscal

policies have been generally supportive of

activity, but were starting to move to a more

neutral stance. This process, which has

already started in Korea, was being initiated

in the Philippines, while elsewhere it is

planned to start in 2001. The export-led

nature of the recovery has led to strong

current account positions throughout the

regions, although surpluses were beginning

to fall in response to domestic recovery and

higher oil prices. External surpluses were

helping to insulate parts of the region from

some of the financial impact of tighter

global monetary conditions.

Economic data indicate that China, the

world’s most populous economy, continued

to grow at a robust pace. Stronger private

consumption and export supported real GDP

growth, set at 7.5 per cent in 2000, with

monetary policy remaining accommodative.

On the fiscal side, the authorities announced

a package of additional expenditures;

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 11 -

however, buoyant revenues caused by strong

activity were shifting policy to a more

neutral stance. In India, the second largest

economy, economic performance has been

remarkable in recent years, despite the

adverse effects of the regional crisis on

exports and the more recent hike in world oil

prices. Growth for 2000 forecasted at 6.75

per cent, reflected continued strength in the

information technology sector and a rebound

in agricultural production.

1.2.2 Latin America

Latin America and the Caribbean continued

to recover from the effects of the emerging

market crises of 1997-98. Growth was

fuelled by buoyant exports, particularly to

the United States, as well as a recovery in

consumer confidence and spending that was

occurring despite falls in stock prices. Real

GDP, which was basically flat in 1999, was

expected to expand by a healthy 4.25 per

cent in 2000, reflecting healthy export

volumes and some improvement in the terms

of trade coming from higher commodity

prices. These aggregate trends, however,

mask important differences across countries.

Several countries, such as Brazil, Mexico,

and Chile, were exhibiting more rapid

growth than other countries in the region,

particularly those where economic and

political uncertainties were most acute.

Growth in Brazil continued to recover, led

by exports, which surged as a result of the

depreciation in early 1999. As the year

progressed, rising consumer spending and

investment also contributed to the increased

economic momentum. Real GDP was

projected to rise by 4.0 per cent in 2000 and

4.5 per cent in 2001. Chile was also

experiencing a recovery, supported by

buoyant consumer spending. In both

countries, confidence has been maintained

by responsible macroeconomic policies,

including inflation-targeting regimes. In

Brazil, the government targeted for public

sector primary surplus of 3.25 per cent of

GDP, which was expected to be consistent

with a further decline in public debt relative

to GDP.

Mexico’s economy continued to expand at a

healthy pace, as it has been doing since

1995, backed by prudent monetary policy, as

well as higher oil prices, rapid growth in the

United states, buoyant consumer spending,

and healthy demand for investment goods.

Growth was forecasted to accelerate to

almost 6.5 per cent in 2000 before falling

back slightly in 2001, while inflation was

projected to continue to decline as monetary

policy was tightened. Higher oil prices were

supporting the external position and the

fiscal policy.

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 12 -

In Argentina, the economy was slowly

recuperating from the severe recession of

1999. This should continue in the coming

year in the absence of any external shocks.

Early in the year, the authorities introduced

a fiscal package that reduced planned

government outlays to minimise the

overshoot compared to the targeted deficit.

This helped moderate concerns in

international capital markets about fiscal

slippages, although on average financial

conditions remain tighter than in the latter

part of 1999. Against these headwinds real

GDP was set to grow at around 2 per cent in

2000 and the current account deficit was

anticipated to decline significantly.

Continued structural reform in the fiscal area

remain a high priority, including passing

laws tightening tax administration,

modifying revenue sharing arrangement

with provinces, and reforming the social

security system.

The Andean region, outside of Chile and

Peru, was particularly hard hit by 1998-99

recession. Activity was expanding again in

2000, but political uncertainties was slowing

progress on needed reforms and created

pressures to relax macroeconomic policies.

Business confidence remained weak in

Colombia, in part due to continuing internal

armed conflict, and the currency fell to

record lows against the U.S dollar. In

Venezuela the fiscal benefits of higher oil

prices were partially offset by increased

spending.

1.2.3 The Middle East and Africa

During the 1999-2000 period, the rebound in

world oil prices as well as the increases in

OPEC oil production quotas boosted

economic activity and prospects for most of

the oil-producing countries of the region.

The rise in oil prices and oil output led to

stronger fiscal and external balances in these

countries and also improved confidence and

greater domestic demand. Many of the non-

oil-producing countries of the region,

however, were faced with substantial terms-

of-trade losses as export prices of non-fuel

commodities and other primary goods

remained generally depressed, particularly

in real terms, while oil import prices rose

continuously.

Nonetheless, the upward trend in growth in a

number of these countries in 1999 and 2000

was due to the macroeconomic policies and

reforms that have made economic activity

more broad based and allowed these

countries to benefit from stronger export

market growth.

In the Middle East, economic growth among

the Gulf oil exporters was projected to turn

positive in 2000 and remain so in 2001.

Despite the improved growth prospects, as

well as external and fiscal balances, many of

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 13 -

these countries are pressing ahead, albeit

sometimes slowly, structural reforms to

boost the non-oil private sector that were

initiated when much slower oil prices

threatened macroeconomic stability. For

example, in Saudi Arabia, the government

has been restructuring and corporatising the

telecommunication and utility sectors to

make them more attractive to private

investment, as well as revising laws and

regulations to improve the business

environment and attract foreign investment

and expertise.

Annual output growth in Africa was

projected at 3 ½ percent in 2000, rising to 4

½ percent in 2001, spurred by rebounds in

South Africa and oil-exporting countries as

well as continued strength in some of the

smaller economies. In South Africa, the

continent’s largest economy, the economic

recovery, while still fragile, was gaining

momentum, with output on track to grow 3

to 4 percent in each of the next two years.

The rebound has been supported by a

strengthening of public finances,

improvements in external competitiveness,

and the expansion in world output. The rand

has come under some pressure since the

beginning of 2000 year largely as a result of

the fallout of the turbulence in Zimbabwe

and decreased relative bond yields, but

progress continued to be made in reducing

the net open forward position of the Reserve

Bank, which has helped reduce the risks

premium on South African investment and

boost economic activity. Improvements in

productivity growth have helped dampen the

potential inflationary impact of the

economic recovery. Nevertheless, some

cost-cut pressures have been evident as a

result of the depreciation of the rand, and

flood-related surge in food prices. The

Reserve Bank is being careful in ensuring

that these developments do not undermine

confidence in the inflationary-targeting

framework.

2. Currency movements

2.1 The euro

The dollar showed particular strength in

2000 against the euro, the common currency

of 11 member countries of Western Europe.

During the first three quarters of the year,

the euro continued to weaken, and by late

October had fallen to a low of just above 82

cents, nearly one-third below its value when

it was introduced in January 1999. The

euro’s decline against the dollar through

most of the year, according to market

analysts, appeared to be due mainly to the

vigorous growth of real GDP and

productivity in the US. In September, a

concerted intervention operation by the

monetary authorities of G-7 countries,

including the US, was undertaken at the

request of European authorities to provide

support for the euro. The European Central

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 14 -

Bank also made intervention purchases on

several occasions acting on its own. Late in

the year, the euro changed course and started

to move up strongly, reversing over half of

its decline witnessed earlier in the year.

This recovery of the euro against the dollar

appeared to reflect mainly a market

perception that, while growth was slowing

in both Europe and the US, the slowdown

was much sharper in the latter. For the year

as a whole, the dollar appreciated, on a net

basis about 7.0 per cent against the euro.

3. Trade and investment

3.1 The World Trade Organisation

According to an assessment by the director-

general of the World Trade Organisation

(WTO), the institution for trade and global

trade in general has been practically good in

2000. One year on from the protest and

anger of the Seattle summit, WTO was

starting to function effectively and fairly as

a forum where 140 governments get together

to negotiate rules, promote freer trade and

provide a transparent and predictable

framework for business. Freer trade means

faster economic growth, cheaper imports

and more choice for consumers. The

Organisation also help countries to settle

trade disputes.

In the first half of 2000, world trade rose by

14 per cent, four times faster than in 1999.

Asia’s exports rose by around a quarter.

Imports from the five Asian developing

countries most affected by the financial

crisis in 1997-98 rose above their pre-crisis

levels. Latin America’s exports rose by

about 20 per cent, the United States by 14

per cent. The WTO estimates that world

trade would rise by 10 per cent in 2000 as a

whole, as fast as in the best years of the

1990s.

At the WTO itself, progress has been made

on at least five issues. First, negotiations

have been launched on agriculture and

services, which together account for over

two-thirds of the world economy. The

world has seen a fall in food prices,

telephone calls and better financial services

and a spread of the internet. Liberalising

agriculture and manufacturing alone would

add over US$250 billion a year to the world

economy, according to the Centre for

Economic Policy Research in London. The

gains from services liberalisation, though

hard to quantify, could be even higher.

Secondly, the WTO has welcomed five new

members: Jordan, Georgia, Albania, Croatia

and Oman. Many more countries are about

to join. By far, the biggest is China, which

has concluded bilateral agreements with all

WTO members that requested one except

Mexico. The US Senate and House of

Representatives have both voted

convincingly for permanent normal trade

relations with China.

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 15 -

Third, WTO is doing its upmost to help

developing countries get a better deal from

the world trading system. It has set up a

mechanism for dealing with their difficulties

in implementing the organisation’s

commitments. It has also worked through

an important package to help the poorest

countries. Twenty-seven richer countries,

including the United States and the 15

members of the European Union, have

offered to open their markets more.

Fourthly, the institution is involving all its

140 members in its work. It operates by

consensus, so every country – however

small – has a veto. Furthermore, it is using

the internet to keep its smaller members

better informed.

Finally, WTO is doing more to reconnect

itself with ordinary people everywhere.

Nearly all WTO documents are posted on its

website immediately.

The organisation is now ready to build on

2000’s achievements. The task as seen by

the director-general for the new year is to

broaden support for further multilateral

liberalisation.

3.2 China-US trade relations

Since the beginning of the year, with the

concern of top leaders and joint efforts from

both countries, China-US bilateral relations

have maintained a trend of stable

development. Bilateral economic and trade

relations have developed very fast with rapid

increase of China’s export to and import

from the United States. The two countries

reached a bilateral agreement in 1999 on

China’s joining the World Trade

Organisation (WTO).

According to statistics of the Chinese

customs, during the period from January to

October 2000, Sino-US bilateral trade

amount reached US$61.323 billion,

increasing by 23.4 per cent over the 1999

level. The toal amount of China’s export to

the US during the 10-month period was

US$43.367 billion, increasing by 27.2 per

cent whilst the total amount of China’s

import during the same period was

US$17.955 billion, rising by 15.1 per cent.

It is estimated that the total amount of

bilateral trade will set an all-time record and

reach about US$73.5 billion, accounting for

about 16 per cent of China’s total trade in

the whole year. The United States is

China’s second largest trading partner, and

China is the fourth largest trading partner of

the US.

Moreover, with the constant deepening of

reform and opening up and sustained

economic growth, the scale of US direct

investment in China has been growing year

after year. From January to November

ANNUAL REPORT 2000 WORLD ECONOMIC CONDITIONS

- 16 -

2000, China has approved 2,301 US

investment projects with a total contract

amount of US$7.326 billion. China has also

increased the establishment of companies in

the US. During the same period, 37 Chinese

funded enterprises have been approved with

a total amount of investment reaching

US$70.62 million.

Experts of foreign economic relations in

China are convinced that economic and

trade cooperation between China and the US

has great development potential and is of

complementary nature and mutually

beneficial.

SECTION TWO

Highlights of the Seychelles Economy

Overview

Despite yet another tough year, the

Seychelles economy continued to weather

the storm in 2000. Most indicators of real

GDP growth point to a slowdown as

industries once again struggled to cope with

the foreign exchange shortage. The

situation was not helped as inflows through

the commercial banks declined. Overall,

however, the signs were that there was a

notable degree of consolidation as the

budget deficit was reduced further and

liquidity growth slowed down.

No firm real GDP figures was yet available

at the time of publication, however, Central

Bank estimates based on a survey of

industries and that of the Management &

Information Systems Division (MISD)

suggest that growth in real output stood at

around 1.4 per cent.

Despite the fall in foreign exchange inflows,

as measured by commercial bank receipts,

the balance of payments position improved

significantly compared to the previous year,

mostly on account of a sharp improvement

in the current account.

Whilst growth in GDP output far from

achieved its full potential there were signs of

growth in some areas of economic activity

as reflected by an increase in sectoral output

growth.

For the year 2000, GDP is estimated at

R3450.4 million (nominal terms). A major

boost to income growth has been the tourism

industry, as both tourism arrivals and

income increased relative to the previous

year. Other sectors that achieved important

growth were in ‘electricity & water’,

‘building and construction’ and

‘telecommunications’.

- 17 -

ANNUAL REPORT 2000 HIGHLIGHTS OF THE SEYCHELLES ECONOMY

-18 -

Whilst a drop would have been preferable, it

was nonetheless encouraging to note that

though it remained on the high side at 6.3

per cent, the inflation rate remained

unchanged in 2000. There were however,

some marked changes in how the prices

moved during the year. There was a

slowdown in import prices compared to the

previous year, down from 10 per cent to

only 4.4 per cent. However, in respect of

local prices there was an increase in the rate

of change from 4.4 per cent to 7.2 per cent,

showing a movement from import prices

into local prices.

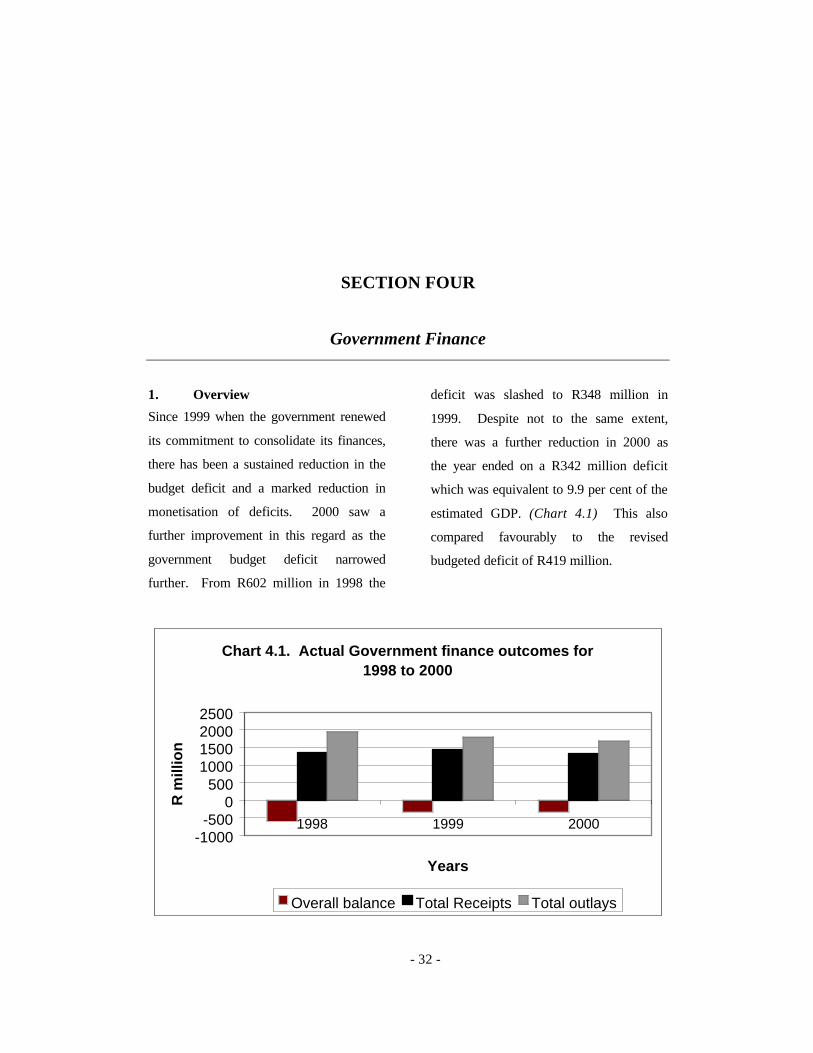

The budget deficit was estimated at 9.9 per

cent of the estimated nominal GDP for the

year, down from 11 per cent in 1999. In

monetary terms, the deficit narrowed by

R5.7 million to R342 million. The

improvement in the fiscal position compared

to 1999 resulted mostly from a decline in its

expenditure, with all major headings of

expenditure – current and capital outlays;

and net lending, recording reduced

expenditure relative to their budgeted levels.

The improved fiscal performance had a

positive spin-off effect on the monetary

sector as the lower demand for financing

translated into an abatement of liquidity

growth. Furthermore, the positive outcome

on the monetary side also reflected the

manner in which the government financed

its requirements in 2000 compared to the

previous years. It would be noted that at the

end of 1999, the government introduced a

limit on how much it borrows from the

Central Bank as advances, thus reducing the

monetisation process of the deficit. This

commitment to limit monetisation of

government deficit was announced by the

Finance Minister - Vice-President James

Michel in his budget address for 2000. In

2000, the government switched to the

commercial banks and the non-financial

sector for the bulk of its financing

requirements through the issues of

government paper (treasury bills, treasury

bonds & government stocks). This had a

direct impact on the growth of money

supply, which slowed down from 19 per

cent in 1999 to only 8.2 per cent in 2000.

There were no major changes in interest

rates during 2000. The two rates that are

under the ambit of the Central Bank, the

minimum savings rate and that of the

maximum lending rate remained at 3.0 per

cent and 10.0 per cent respectively. In terms

of the interest on time deposits, most

instruments registered declines in their

respective rates. Interest on treasury bills

remained on the tap system and the yields

stood at 4.502 per cent, 4.995 per cent, and

5.496 per cent for the 91-day, 182-day and

365-day bills respectively.

ANNUAL REPORT 2000 HIGHLIGHTS OF THE SEYCHELLES ECONOMY

-19 -

As already noted above, the year under

review saw an improvement in the external

position of Seychelles as indicated by the

balance of payments (BOP) estimates for the

year. Balance of payments figures (recorded

on a commitment basis) for 2000 show an

overall balance surplus of R109 million.

This represented an increase of R130 million

or 596 per cent relative to last year. This

significant improvement in the external

position of the economy was attributable

mainly to the current account, as the deficit

was reduced to R295 million, down from

R645 million in 1999.

In terms of the rate of exchange between the

Seychelles rupee and that of other

currencies, the rupee remained pegged to the

Seychelles Trade and Tourism Weighted

Basket, the peg introduced in May 1996. As

regards the movement of the local currency

vis-à-vis the major currencies, there was

somewhat a volatile fluctuation, which

ranged between negative 7.9 per cent and

plus 12 per cent.

Activity in the offshore sector managed by

the Seychelles International Business

Authority (SIBA) was significantly more

positive during the year under review. The

year was highlighted by the incorporation of

1.351 IBCs and one new trust, which

brought the total since the operations started

to 6, 159 IBCs and 21 trusts. SIBA also

issued three new SITZ licences.

SECTION THREE

Financial Survey

1. Overview

There were significant improvements in

the movements in the key monetary

indicators. The authorities would have

been encouraged to observe a marked

slowdown in liquidity and credit growth.

For the year as a whole, liquidity growth,

as measured by the movements in M2(p),

was only 8.2 per cent, down from 19 per

cent in 1999. As for credit, it grew by 10

per cent compared to 16 per cent over the

year earlier. This notable slowdown in the

pace of both these aggregates during the

year was helped by the strong government

commitment towards budget

consolidation.

During 2000, the government managed to

curb its fiscal deficit further and at the

same time financing that deficit in a less

expansionary manner, through the sale of

government paper rather than have

recourse to Central Bank advances.

Therefore, the switch from Central Bank

borrowing in favour of commercial bank

funding was a key factor in to curbing

monetary growth. During the year, the

government issued two new bonds with

authorised limits of R200 million and

R300 million respectively. As commercial

banks are the main investors in those

instruments, their lending to the

government increased during the course of

the year, albeit at a much slower pace, as

the lower fiscal deficit reduced

Government’s demand for financing.

However, despite these encouraging

developments outlined above, the foreign

exchange difficulties continued to be a

major concern for the authorities. Despite

- 20 -

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 21 -

not putting new measures in place in the

year under review, the government has

indicated that it would be more vigorous in

its approach in the coming year towards

this problem.

As regards interest rates, there were no

changes to the level of interest rates.

Whilst the two interest rates set by the

Central Bank, namely the savings rate and

the maximum lending rate remained

unchanged, there was a general decline in

the market-determined rates, which are

mostly time deposits.

2. Monetary Policy Instruments1

Central banks use monetary policy

instruments to meet certain objectives and

in most cases, aiming to attain an

environment of stable and low inflation.

However, in Seychelles, the Central Bank

uses such instruments mostly to achieve a

manageable level of liquidity; to manage

foreign currency flows; and to fine-tune

interest rates.

2.1 Interest rate floor

As already noted, there was no change in

the minimum statutory interest rate floor

and the maximum lending rate during

2000. The saving rate remained at 3.0 per

cent per annum, and the maximum lending

rate was at 10.0 per cent per annum

throughout the year.

2.2 Minimum reserve requirement

The minimum reserve ratio, which is the

percentage of its liabilities that a

commercial bank is required to hold with

the Central Bank, remained unchanged at

2.5 per cent during the year. All banks

were able to maintain the ratio.

2.3 Local assets ratio2

The local asset ratio is the instrument that

is used by the Central Bank to influence

liquidity at commercial banks. All banks

operating in Seychelles were able to meet

this requirement, which since September

1998 was set at a minimum of 70 per cent.

__________________________________ 1 The minimum reserve requirement is a minimum ratio of cash reserves to eligible deposits that commercial banks are required to hold at the Central Bank. The higher is this ratio, the lower is the money multiplier, and thus the monetary impact of new injections of liquidity. The minimum reserve requirement was set at 20 per cent on 16 November 1992. As from 15 September 1998, this ratio was lowered to 2.5 per cent (see Section Eight in this report for further details). 2 With effect from 15 September 1998, the local assets ratio was raised from 50 per cent to 70 per cent.

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 22 -

2.4 Central Bank advances to

banks3

Central Bank advances are available to

commercial banks to allow them to meet

shortfalls in liquidity. During 2000, total

advances to the commercial banks

increased further, rising by R167 million

or 53 per cent relative to the previous year.

Out of the R485 million disbursed, R463

million was repaid during the period,

leaving an average outstanding stock of

R6.1 million. The high level of advances

during the year reflected the tight liquidity

positions that banks experienced at times,

particularly towards the end of the year,

when the level of transactions by

economic agents tended to rise faster

(transactions demand for money).

2.5 Open market operations4

Open-market operations is one of the

instruments that a Central Bank can use to

regulate the degree of liquidity in the

economy. Though it has been used in a

limited way in Seychelles in the past, since

last year, this strategy has become more

prominent to control the high level of

liquidity in the Seychelles economy. With

the commitment of the government to

reduce the monetisation of its deficit, by

on one hand, limiting the amount it

borrows from the Central Bank, and on the

other, by issuing securities through the

Bank, it has help to reduce the monetary

growth significantly in 2000. During the

year, the government issued two new

treasury bonds with limits of R200 million

and R300 million.

3. Money Supply

Also in 2000, liquidity growth, as

measured by the broad money aggregate

M2(p) increased by only 8.2 per cent,

which represented a decline of 11 per cent

relative to last year, when it grew by 19

per cent (Chart 3.1). This significant

slowdown in money growth in the

economy could be reviewed as a

welcoming development as it set the stage

for further stabilisation, not only in

liquidity, but also in other main economic

indicators. It is also the first time since

1987 that money growth has been below

the 10 per cent mark.

________________________________________

3 This is the sole standing facility offered by the Central Bank of Seychelles. Since September 1993 the rate on advances has been set at 50 basis points above the average of the last tender rate, rounded to 1/8 of 1 per cent. 4 Open market operations are purchases/sales of financial securities by Central Bank in the open market to regulate the money supply. Such instruments frequently used to mop up excess liquidity. The securities involved can be both short and long term.

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 23 -

Chart 3.1. Growth rates of the money supply aggregates for 1995 to 2000

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

1995 1996 1997 1998 1999 2000

Years

Per

cen

t

M2(p) M2 M1 Pipeline deposits

A more detailed analysis of the

deceleration in the pace of the money

growth showed that it stemmed from both

domestic and external factors, with the

latter being influenced by a decline of

R126 million in net foreign assets. From

the domestic side, the pace of money

supply growth declined due to the

moderate growths in bank deposits and in

currency with the public.

This was reflected in the slower growth

rate of M2, which consist of M1 (currency

with public plus demand deposits) and

quasi-money (time deposits plus savings

deposits), compared to the previous year.

M2 grew by 9.1 per cent compared to 22

per cent in the preceding year, influenced

by a 6.2 per cent increase in M1 and an 11

per rise in quasi-money. Last year, these

aggregates grew by 37 per cent and 14 per

cent respectively.

The significant abatement in the growth

rate of M1 was caused by both its

components - "demand deposits" and

"currency with public". They grew at a

considerably slower pace than was

observed in the preceding year. During

2000, "demand deposits" grew by R50

million or 6.1 per cent whilst "currency

with public" rose by R16 million or 6.6

per cent. Of the increase of "demand

deposits", the private sector accounted for

82 per cent, as demand deposits of the

parastatal sector rose by R8.0 million only.

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 24 -

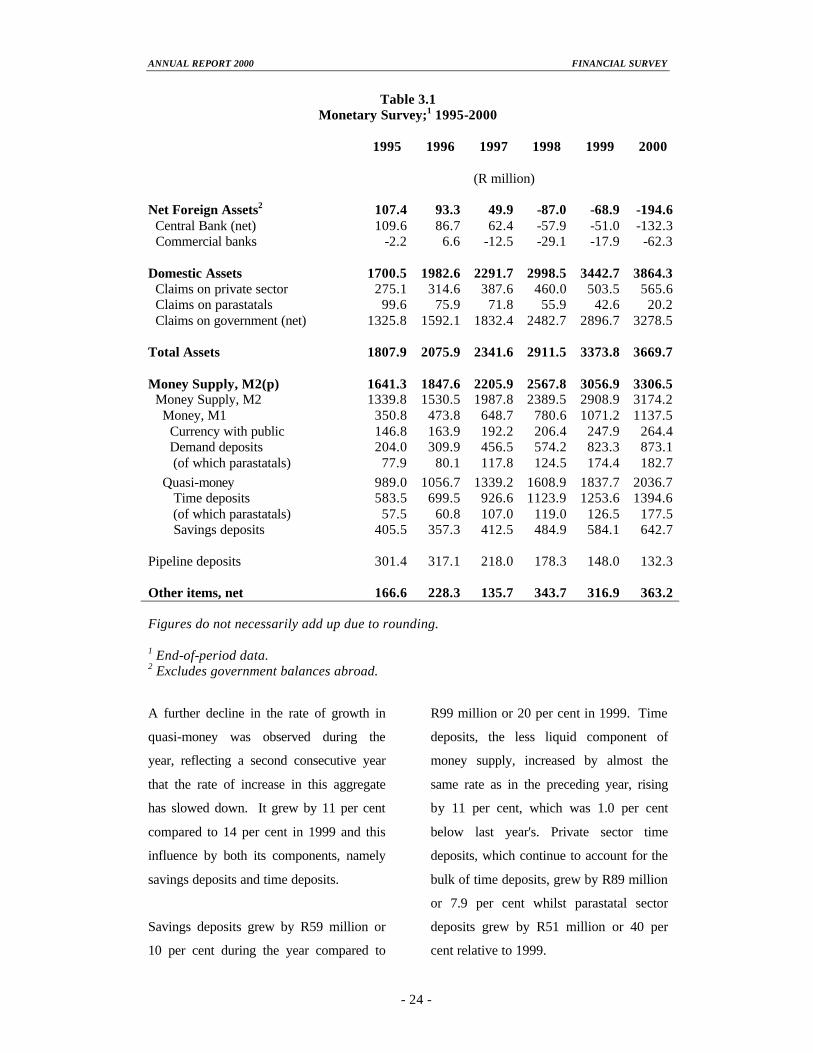

Table 3.1 Monetary Survey;1 1995-2000

1995 1996 1997 1998 1999 2000

(R million) Net Foreign Assets2 107.4 93.3 49.9 -87.0 -68.9 -194.6 Central Bank (net) 109.6 86.7 62.4 -57.9 -51.0 -132.3 Commercial banks -2.2 6.6 -12.5 -29.1 -17.9 -62.3 Domestic Assets 1700.5 1982.6 2291.7 2998.5 3442.7 3864.3 Claims on private sector 275.1 314.6 387.6 460.0 503.5 565.6 Claims on parastatals 99.6 75.9 71.8 55.9 42.6 20.2 Claims on government (net) 1325.8 1592.1 1832.4 2482.7 2896.7 3278.5 Total Assets 1807.9 2075.9 2341.6 2911.5 3373.8 3669.7 Money Supply, M2(p) 1641.3 1847.6 2205.9 2567.8 3056.9 3306.5 Money Supply, M2 1339.8 1530.5 1987.8 2389.5 2908.9 3174.2 Money, M1 350.8 473.8 648.7 780.6 1071.2 1137.5 Currency with public 146.8 163.9 192.2 206.4 247.9 264.4 Demand deposits 204.0 309.9 456.5 574.2 823.3 873.1 (of which parastatals) 77.9 80.1 117.8 124.5 174.4 182.7

Quasi-money 989.0 1056.7 1339.2 1608.9 1837.7 2036.7 Time deposits 583.5 699.5 926.6 1123.9 1253.6 1394.6 (of which parastatals) 57.5 60.8 107.0 119.0 126.5 177.5 Savings deposits 405.5 357.3 412.5 484.9 584.1 642.7 Pipeline deposits 301.4 317.1 218.0 178.3 148.0 132.3 Other items, net 166.6 228.3 135.7 343.7 316.9 363.2 Figures do not necessarily add up due to rounding. 1 End-of-period data. 2 Excludes government balances abroad.

A further decline in the rate of growth in

quasi-money was observed during the

year, reflecting a second consecutive year

that the rate of increase in this aggregate

has slowed down. It grew by 11 per cent

compared to 14 per cent in 1999 and this

influence by both its components, namely

savings deposits and time deposits.

Savings deposits grew by R59 million or

10 per cent during the year compared to

R99 million or 20 per cent in 1999. Time

deposits, the less liquid component of

money supply, increased by almost the

same rate as in the preceding year, rising

by 11 per cent, which was 1.0 per cent

below last year's. Private sector time

deposits, which continue to account for the

bulk of time deposits, grew by R89 million

or 7.9 per cent whilst parastatal sector

deposits grew by R51 million or 40 per

cent relative to 1999.

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 25 -

The other principal component of broad

money M2(p) is pipeline deposits. During

2000, clearing of pipeline deposits

continued with a reduction of R16 million

or 11 per cent. This decline however, was

significantly less than the R30 million

cleared in 1999. This year's outcome

reflects the further decline in the amount

of foreign exchange through entered the

banking system, from R818 million in

1999 to R755 million in 2000.

4. Net Foreign Assets

Seychelles’ net foreign asset position

deteriorated significantly during 2000,

falling by 183 per cent relative to the

previous year. In aggregate, the country's

net foreign assets at the end of the year,

which comprises Central Bank and

commercial bank reserves, stood at

negative R195 million, compared to

negative R69 million at the end of 1999.

This unfavourable outcome in 2000 was

attributed to declines in both the Central

Bank and commercial banks’ reserves.

The central bank’s reserves fell by R81

million whilst the net foreign reserve

position of the banking sector declined

from negative R18 million to negative R62

million.

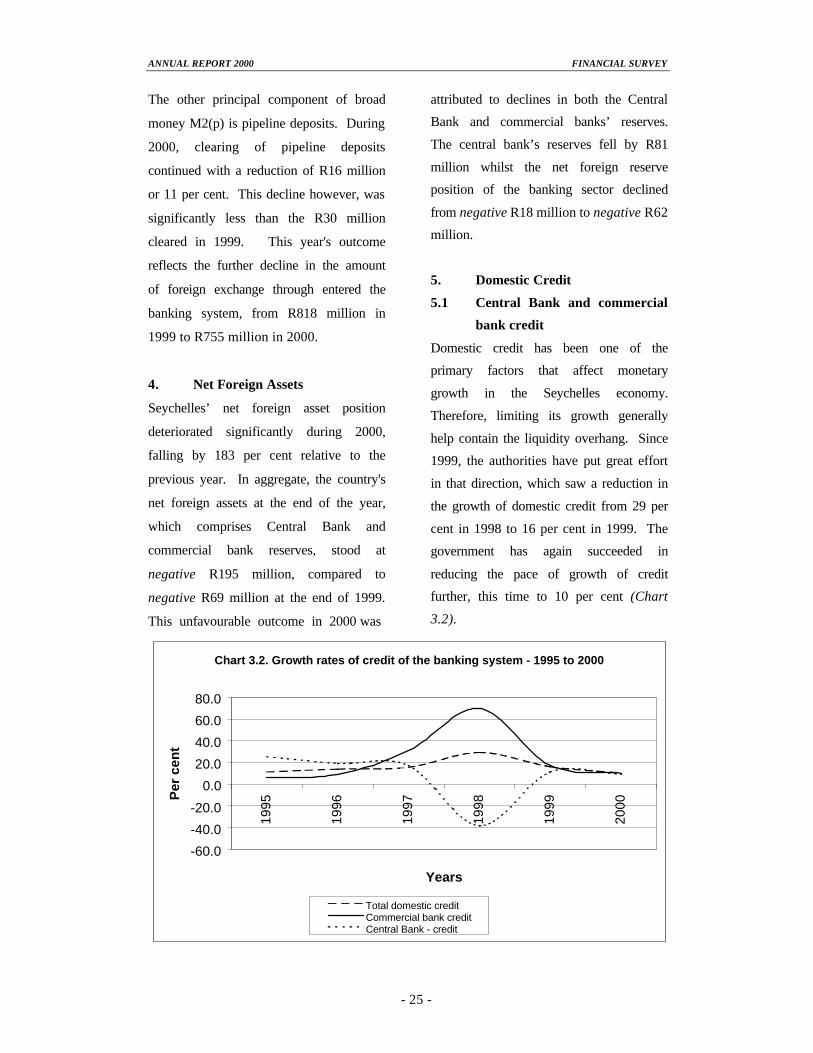

5. Domestic Credit

5.1 Central Bank and commercial

bank credit

Domestic credit has been one of the

primary factors that affect monetary

growth in the Seychelles economy.

Therefore, limiting its growth generally

help contain the liquidity overhang. Since

1999, the authorities have put great effort

in that direction, which saw a reduction in

the growth of domestic credit from 29 per

cent in 1998 to 16 per cent in 1999. The

government has again succeeded in

reducing the pace of growth of credit

further, this time to 10 per cent (Chart

3.2).

Chart 3.2. Growth rates of credit of the banking system - 1995 to 2000

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

1995

1996

1997

1998

1999

2000

Years

Per

cen

t

Total domestic creditCommercial bank creditCentral Bank - credit

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 26 -

The two principal lenders in the economy,

namely the commercial banks and Central

Bank, influenced the decline in the rate of

growth in 2000. Total commercial banks’

credit expanded by R319 million or 10 per

cent compared to R450 million or 17 per

cent in 1999. Credit of the Central Bank

grew by R58 million or 9.2 per cent during

the year, compared to a rise of 11 per cent

in 1999.

Table 3.2

Credit;1/2 1995-2000 1995 1996 1997 1998 1999 2000 (R million) Total Credit 1879.1 2139.8 2473.0 3197.6 3712.8 4090.3 Commercial banks 1215.7 1349.4 1546.2 2622.6 3072.7 3391.5 Claims on private sector 275.1 314.6 387.6 460.0 503.5 565.6 Claims on parastatals 99.6 75.9 71.8 55.9 42.6 20.2 Claims on government 841.0 958.9 1086.9 2106.7 2526.6 2805.7 Of which: Dev. Fund Stocks (64.6) (68.6) (82.0) (89.1) (96.2) (100.7) Treasury bonds (205.4) (308.0) (326.1) (1130.7) (770.6) (903.6) Treasury bills (484.1) (471.9) (608.8) (832.2) (1621.6) (1777.1) Central Bank 663.3 790.5 926.8 575.0 640.1 698.8 Claims on government 663.3 790.5 926.8 575.0 640.1 698.8 Of which: Advances (452.4) (503.6) (923.2) (469.0) (623.9) (395.8) Treasury bonds (23.3) (23.4) (3.2) (0.05) (0.05) (300.7) Treasury bills (184.0) (259.9) (0.4) (106.0) (16.2) (2.3) Figures do not necessarily add up due to rounding. 1 End-of period data. 2 All figures for stocks, bonds and bills are at cost value. Unlike the Central Bank, which lends only

to the Government, commercial banks also

lend to the private sector and parastatals.

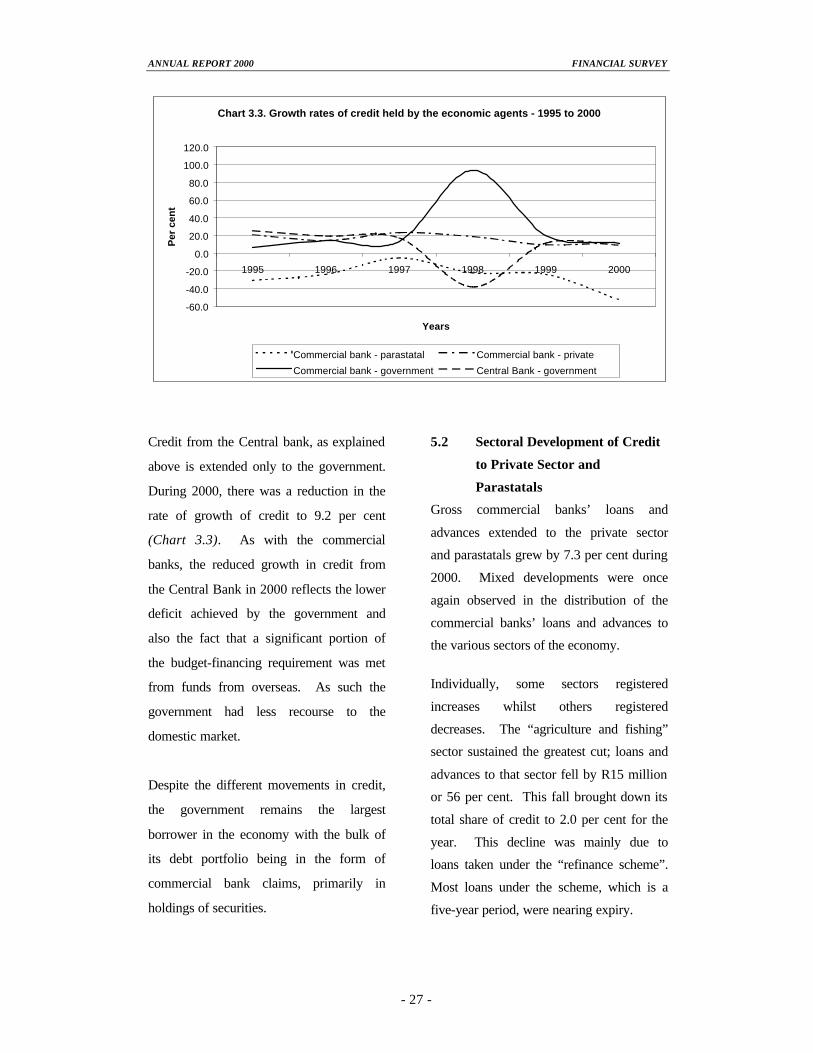

Analysing the different movements in

these portfolios of debt Chart 3.3, it was

observed that there was an increase in

credit extended to the private sector, rising

from 9.5 per cent in 1999 to 12 per cent in

the current year under review. For the

government, there continued to be a

further slowdown in its growth, falling to

11 per cent compared to a 20 per cent rise

in the previous year. This slowdown in

the growth of government claims from the

commercials reflected the lower than

forecasted deficit during the year, which

thus reduced the need to borrow. The

lower demand for funds by the

government has also released funds to

other sectors, namely to the private sector,

which has seen an increase in its growth as

described above. In terms of the

parastatals, there was a further decline,

this time by 53 per cent relative to 1999.

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 27 -

Chart 3.3. Growth rates of credit held by the economic agents - 1995 to 2000

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

1995 1996 1997 1998 1999 2000

Years

Per

cen

t

Commercial bank - parastatal Commercial bank - private

Commercial bank - government Central Bank - government

Credit from the Central bank, as explained

above is extended only to the government.

During 2000, there was a reduction in the

rate of growth of credit to 9.2 per cent

(Chart 3.3). As with the commercial

banks, the reduced growth in credit from

the Central Bank in 2000 reflects the lower

deficit achieved by the government and

also the fact that a significant portion of

the budget-financing requirement was met

from funds from overseas. As such the

government had less recourse to the

domestic market.

Despite the different movements in credit,

the government remains the largest

borrower in the economy with the bulk of

its debt portfolio being in the form of

commercial bank claims, primarily in

holdings of securities.

5.2 Sectoral Development of Credit

to Private Sector and

Parastatals

Gross commercial banks’ loans and

advances extended to the private sector

and parastatals grew by 7.3 per cent during

2000. Mixed developments were once

again observed in the distribution of the

commercial banks’ loans and advances to

the various sectors of the economy.

Individually, some sectors registered

increases whilst others registered

decreases. The “agriculture and fishing”

sector sustained the greatest cut; loans and

advances to that sector fell by R15 million

or 56 per cent. This fall brought down its

total share of credit to 2.0 per cent for the

year. This decline was mainly due to

loans taken under the “refinance scheme”.

Most loans under the scheme, which is a

five-year period, were nearing expiry.

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 28 -

Table 3.3

Commercial Banks – Loans and Advances To Non-Government Sector by Economic Sectors;1 1996-2000

1996 1997 1998 1999 2000 1996 1997 1998 1999 2000 (R million) (per cent) Total Advances 338.3 459.3 515.8 546.0 585.8 100.0 100.0 100.0 100.0 100.0 Agriculture & fishing 29.8 26.7 26.6 26.6 11.6 8.8 5.8 5.2 4.9 2.0 of which: Refinance scheme 18.0 18.8 18.3 18.8 3.1 5.3 4.1 3.5 3.4 0.5 Manufacturing 10.4 9.0 33.8 3.4 4.8 3.1 2.0 6.6 0.6 0.8 of which: Refinance scheme 8.0 7.0 29.0 0.0 0.0 2.4 1.5 5.6 0.0 0.0 Construction 13.1 15.8 22.9 20.6 29.8 3.4 3.3 3.4 4.4 3.8 Transportation 21.0 14.6 8.6 4.8 4.7 6.2 3.2 1.7 0.9 0.8 Tourist facilities 80.5 82.2 75.1 87.4 107.7 23.8 17.9 14.6 16.0 18.4 Wholesale & Retail trade 55.3 64.0 58.8 51.3 38.7 16.3 13.9 11.4 9.4 6.6 Other businesses 50.3 69.8 81.9 104.6 99.5 14.9 15.2 15.9 19.2 17.0 Private households & Non-profit organisations 77.8 177.3 208.2 247.3 288.9 23.0 38.6 40.4 45.3 49.3 of which: Mortgage loans 29.3 93.0 80.5 114.2 156.6 8.7 20.2 15.6 20.9 26.7 Figures do not necessarily add up due to rounding. 1 End-of-period data.

The most notable increase was observed in

credit granted to the construction sector.

Loans and advances made to that sector

rose by R9 million or 45 per cent during

the year to bring its share of total loans to

5.1 per cent. Loans and advances to the

transport sector fell further despite only by

1.6 per cent whilst the most significant

change occurred in respect of loans and

advances to the other business sector.

During the year, loans and advances to

other businesses fell by 4.9 per cent

compared to an increase of 28 per cent in

1999. This decline brought down its

percentage share of total credit by 2.2

percentage points to 17 per cent, in

relation to 1999. The other significant fall

was registered in respect of credit to the

trade sector; that sector lost 2.8 per cent of

its share of total credit by being granted 25

per cent less credit than the preceding

year.

However, the “manufacturing” and

“private household” sectors benefited from

42 per cent and 17 per cent increases in

credit allocated to them. During the year

2000, the tourism sector was granted 23

per cent or R18 million more credit than in

the preceding year. This growth brought

its percentage share of total to 18 per cent.

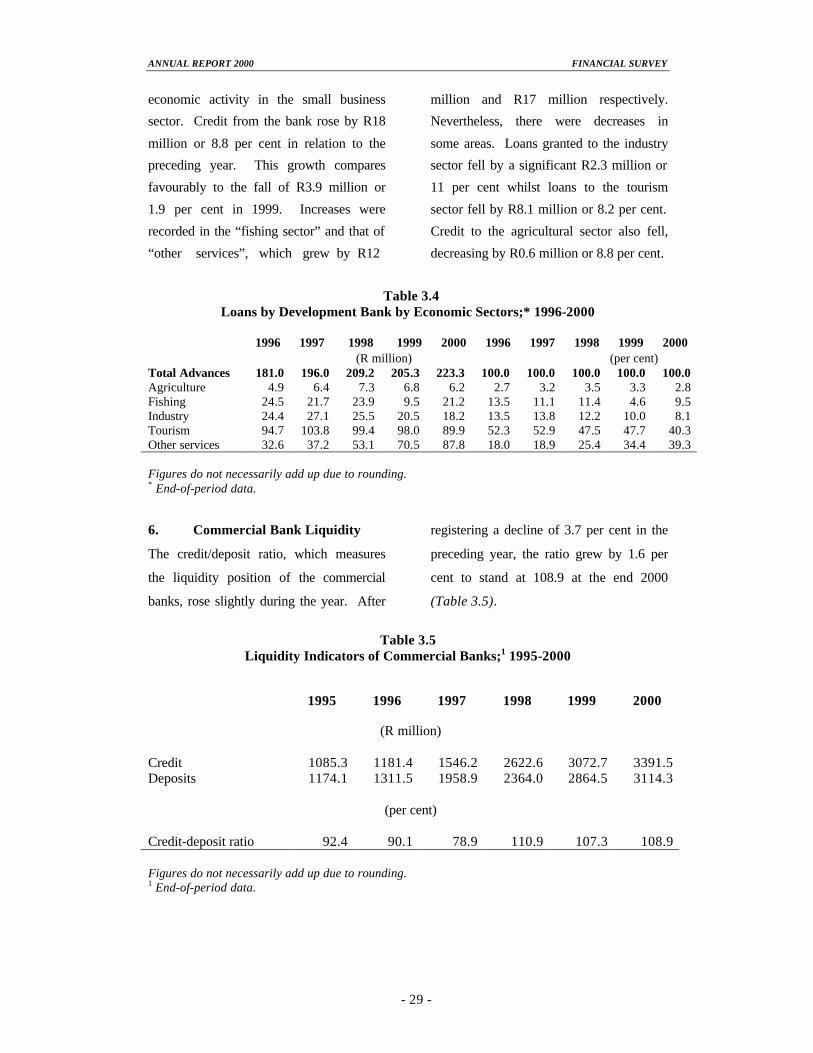

5.3 Development Bank Credit5

The Development Bank of Seychelles

(DBS) provides credit to mostly small to

medium sized enterprises, which generally

cannot obtain advances from commercial

banks. Data provided to the Central Bank

by DBS showed that total advances grew

during 2000, depicting an increase in

______________________________ 5 From 17 January 1994, the Development Bank of Seychelles provided credit to Seychellois investors at a concessionary rate of 12 per cent per annum. To qualify as ‘Seychellois’, Seychellois nationals must own at least 50 per cent of the investment. The minimum contribution for the investor was raised to 25 per cent from 15 per cent at the same occasion. The Development Bank does not provide credit for purposes of working capital. Previously it had lent at 12 per cent per annum for loans in excess of R50,000, rates varied between 9 per cent and 11 per cent depending on economic sector. This rule had been implemented on 17 July 1991.

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 29 -

economic activity in the small business

sector. Credit from the bank rose by R18

million or 8.8 per cent in relation to the

preceding year. This growth compares

favourably to the fall of R3.9 million or

1.9 per cent in 1999. Increases were

recorded in the “fishing sector” and that of

“other services”, which grew by R12

million and R17 million respectively.

Nevertheless, there were decreases in

some areas. Loans granted to the industry

sector fell by a significant R2.3 million or

11 per cent whilst loans to the tourism

sector fell by R8.1 million or 8.2 per cent.

Credit to the agricultural sector also fell,

decreasing by R0.6 million or 8.8 per cent.

Table 3.4 Loans by Development Bank by Economic Sectors;* 1996-2000

1996 1997 1998 1999 2000 1996 1997 1998 1999 2000 (R million) (per cent) Total Advances 181.0 196.0 209.2 205.3 223.3 100.0 100.0 100.0 100.0 100.0 Agriculture 4.9 6.4 7.3 6.8 6.2 2.7 3.2 3.5 3.3 2.8 Fishing 24.5 21.7 23.9 9.5 21.2 13.5 11.1 11.4 4.6 9.5 Industry 24.4 27.1 25.5 20.5 18.2 13.5 13.8 12.2 10.0 8.1 Tourism 94.7 103.8 99.4 98.0 89.9 52.3 52.9 47.5 47.7 40.3 Other services 32.6 37.2 53.1 70.5 87.8 18.0 18.9 25.4 34.4 39.3 Figures do not necessarily add up due to rounding. * End-of-period data.

6. Commercial Bank Liquidity

The credit/deposit ratio, which measures

the liquidity position of the commercial

banks, rose slightly during the year. After

registering a decline of 3.7 per cent in the

preceding year, the ratio grew by 1.6 per

cent to stand at 108.9 at the end 2000

(Table 3.5).

Table 3.5

Liquidity Indicators of Commercial Banks;1 1995-2000 1995 1996 1997 1998 1999 2000

(R million) Credit 1085.3 1181.4 1546.2 2622.6 3072.7 3391.5 Deposits 1174.1 1311.5 1958.9 2364.0 2864.5 3114.3

(per cent) Credit-deposit ratio 92.4 90.1 78.9 110.9 107.3 108.9 Figures do not necessarily add up due to rounding. 1 End-of-period data.

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 30 -

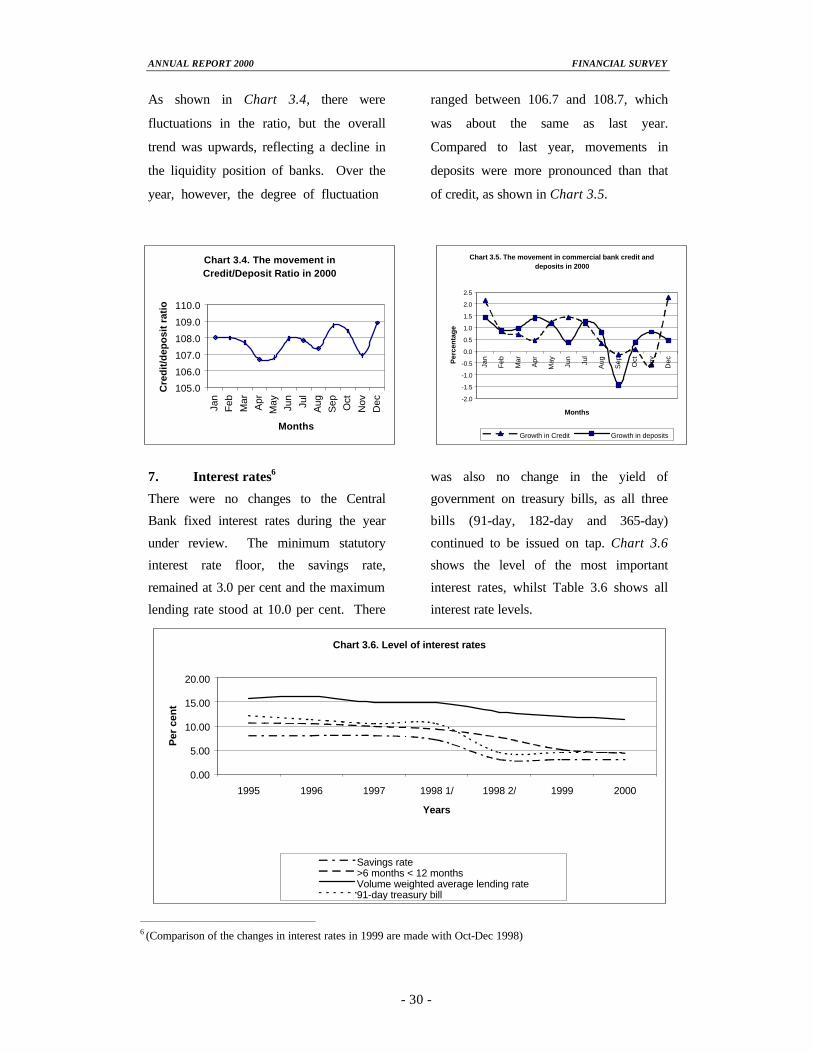

As shown in Chart 3.4, there were

fluctuations in the ratio, but the overall

trend was upwards, reflecting a decline in

the liquidity position of banks. Over the

year, however, the degree of fluctuation

ranged between 106.7 and 108.7, which

was about the same as last year.

Compared to last year, movements in

deposits were more pronounced than that

of credit, as shown in Chart 3.5.

7. Interest rates6

There were no changes to the Central

Bank fixed interest rates during the year

under review. The minimum statutory

interest rate floor, the savings rate,

remained at 3.0 per cent and the maximum

lending rate stood at 10.0 per cent. There

was also no change in the yield of

government on treasury bills, as all three

bills (91-day, 182-day and 365-day)

continued to be issued on tap. Chart 3.6

shows the level of the most important

interest rates, whilst Table 3.6 shows all

interest rate levels.

Chart 3.6. Level of interest rates

0.00

5.00

10.00

15.00

20.00

1995 1996 1997 1998 1/ 1998 2/ 1999 2000

Years

Per

cen

t

Savings rate>6 months < 12 monthsVolume weighted average lending rate91-day treasury bill

Chart 3.4. The movement in Credit/Deposit Ratio in 2000

105.0

106.0

107.0

108.0

109.0

110.0

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep Oct

Nov

Dec

Months

Cre

dit

/dep

osi

t ra

tio

Chart 3.5. The movement in commercial bank credit and deposits in 2000

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep Oct

Nov

Dec

Months

Per

cen

tag

e

Growth in Credit Growth in deposits

_____________________________________________

6 (Comparison of the changes in interest rates in 1999 are made with Oct-Dec 1998)

ANNUAL REPORT 2000 FINANCIAL SURVEY

- 31 -

As regards the market-determined interest

rates, there was again a general decline

during 2000. Nevertheless, the

movements in these rates were less

pronounced than they were in 1999. All

the rates on time deposits, except for the

rate on deposits with maturity between 3

months and 6 months and the deposits

with maturity above twelve months, fell on

average relative to 1999.

The rate on deposits maturing within 7

days fell by 14 basis points to reach 2.79

per cent at the end of the year, this after

registering a rise of 18 basis points in

1999. Interest on deposits with maturity

between 7 days and 3 months fell by 36

basis points to average 4.77 per cent. The

most significant decline was recorded in

respect of the rate on deposits with